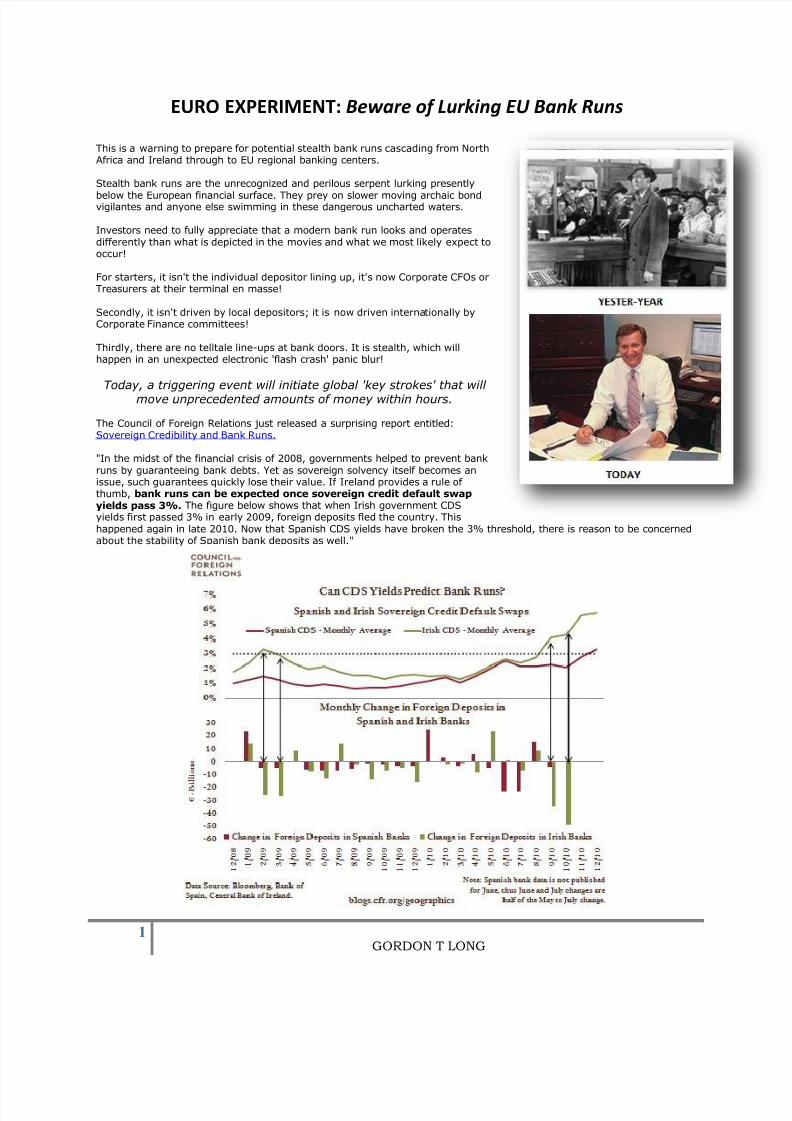

1 GORDON T LONG EURO EXPERIMENT: Beware of Lurking EU Bank Runs This is a warning to prepare for potential stealth bank runs cascading from North Africa and Ireland through to EU regional banking centers. Stealth bank runs are the unrecognized and perilous serpent lurking presently below the European financial surface. They prey on slower moving archaic bond vigilantes and anyone else swimming in these dangerous uncharted waters. Investors need to fully appreciate that a modern bank run looks and operates differently than what is depicted in the movies and what we most likely expect to occur! For starters, it isn't the individual depositor lining up, it's now Corporate CFOs or Treasurers at their terminal en masse! Secondly, it isn't driven by local depositors; it is now driven interna tionally by Corporate Finance committees! Thirdly, there are no telltale line-ups at bank doors. It is stealth, which will happen in an unexpected electronic 'flash crash' panic blur! Today, a triggering event will initiate global 'key strokes' that willmove unprecedented amounts of money within hours. The Council of Foreign Relations just released a surprising report entitled: Sovereign Credibility and Bank Runs. "In the midst of the financial crisis of 2008, governments helped to prevent bank runs by guaranteeing bank debts. Yet as sovereign solvency itself becomes an issue, such guarantees quickly lose their value. If Ireland provides a rule ofthumb, bank runs can be expected once sovereign credit default swap yields pass 3%. The figure below shows that when Irish government CDS yields first passed 3% in early 2009, foreign deposits fled the country. This happened again in late 2010. Now that Spanish CDS yields have broken the 3% threshold, there is reason to be concerned about the stability of Spanish bank deposits as well."

This is a warning to prepare for potential stealth bank runs cascading from NorthAfrica and Ireland through to EU regional banking centers.

Stealth bank runs are the unrecognized and perilous serpent lurking presently

below the European financial surface. They prey on slower moving archaic bondvigilantes and anyone else swimming in these dangerous uncharted waters.

Investors need to fully appreciate that a modern bank run looks and operatesdifferently than what is depicted in the movies and what we most likely expect tooccur!

For starters, it isn't the individual depositor lining up, it's now Corporate CFOs orTreasurers at their terminal en masse!

Secondly, it isn't driven by local depositors; it is now driven internationally byCorporate Finance committees!

Thirdly, there are no telltale line-ups at bank doors. It is stealth, which willhappen in an unexpected electronic 'flash crash' panic blur!

Today, a triggering event will initiate global 'key strokes' that will move unprecedented amounts of money within hours.

The Council of Foreign Relations just released a surprising report entitled:Sovereign Credibility and Bank Runs.

"In the midst of the financial crisis of 2008, governments helped to prevent bankruns by guaranteeing bank debts. Yet as sovereign solvency itself becomes anissue, such guarantees quickly lose their value. If Ireland provides a rule of thumb, bank runs can be expected once sovereign credit default swapyields pass 3%. The figure below shows that when Irish government CDSyields first passed 3% in early 2009, foreign deposits fled the country. Thishappened again in late 2010. Now that Spanish CDS yields have broken the 3% threshold, there is reason to be concernedabout the stability of Spanish bank deposits as well."

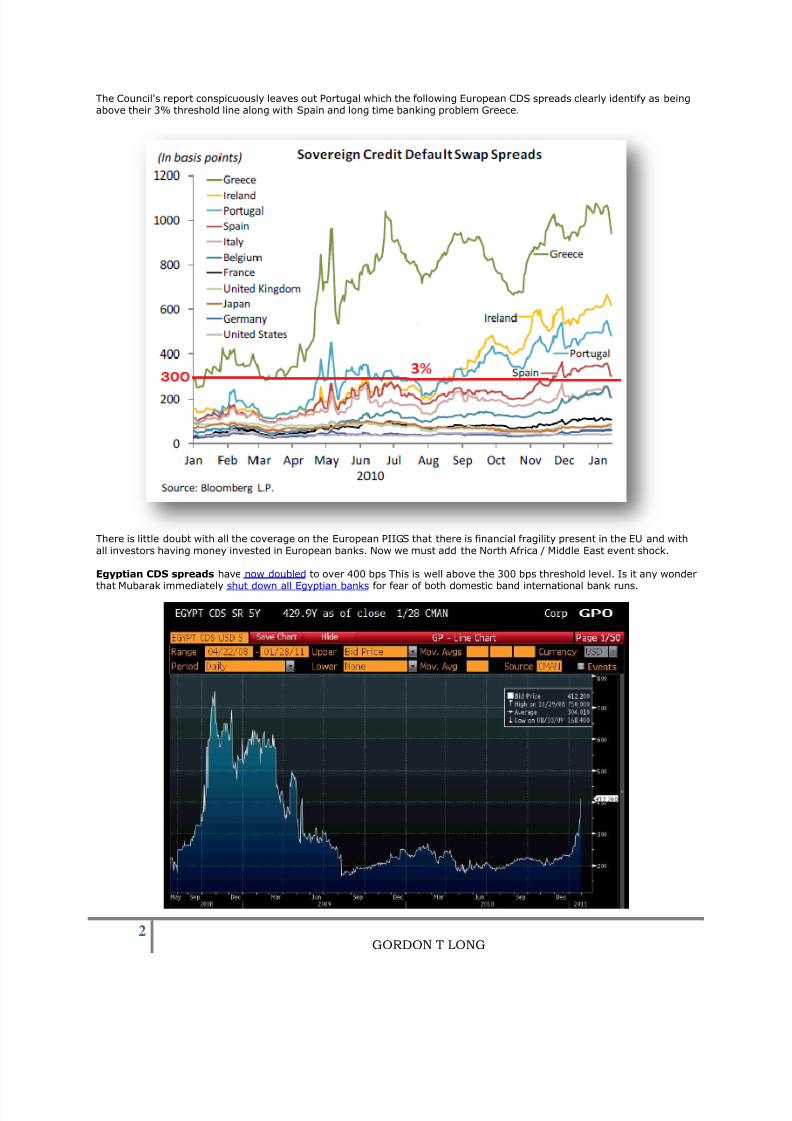

The Council's report conspicuously leaves out Portugal which the following European CDS spreads clearly identify as beingabove their 3% threshold line along with Spain and long time banking problem Greece.

There is little doubt with all the coverage on the European PIIGS that there is financial fragility present in the EU and withall investors having money invested in European banks. Now we must add the North Africa / Middle East event shock.

Egyptian CDS spreads have now doubled to over 400 bps This is well above the 300 bps threshold level. Is it any wonder

that Mubarak immediately shut down all Egyptian banks for fear of both domestic band international bank runs.

cash funds from money market funds to short term treasury bills. Literally trillions of money moved within one afternoonthat prompted the Fed to immediately react with money market guarantees above the FDIC $100,000 limit. Almostimmediately, Hank Paulson, the US Treasury Secretary and Ben Bernanke were forced onto Capitol Hill and into closeddoor sessions to discuss the gravity of the situation. The outcome was an avalanche of Fed programs and thegovernment's TARP program.

The point we need to remember is that when we have financial anxieties we have financial fragility. Any event, or rumor,or financial report, can act as a crystallizing catalyst to push the financial markets into immediate and panic action.

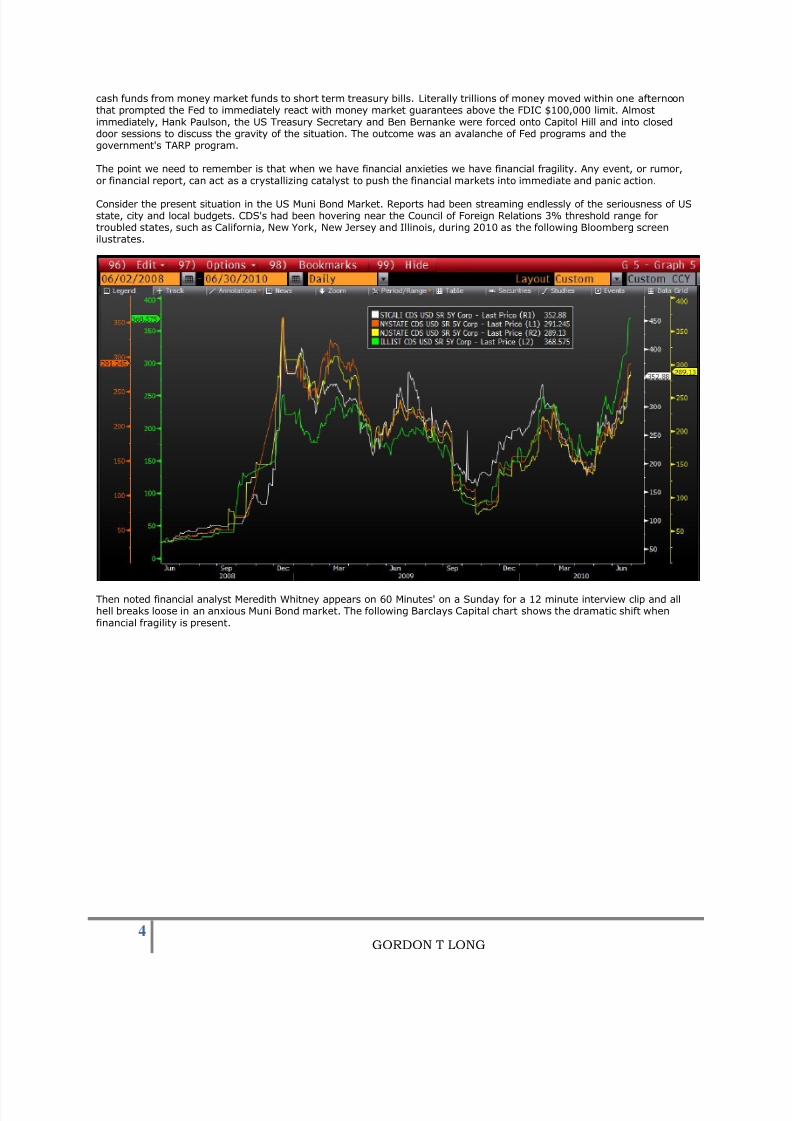

Consider the present situation in the US Muni Bond Market. Reports had been streaming endlessly of the seriousness of USstate, city and local budgets. CDS's had been hovering near the Council of Foreign Relations 3% threshold range fortroubled states, such as California, New York, New Jersey and Illinois, during 2010 as the following Bloomberg screenilustrates.

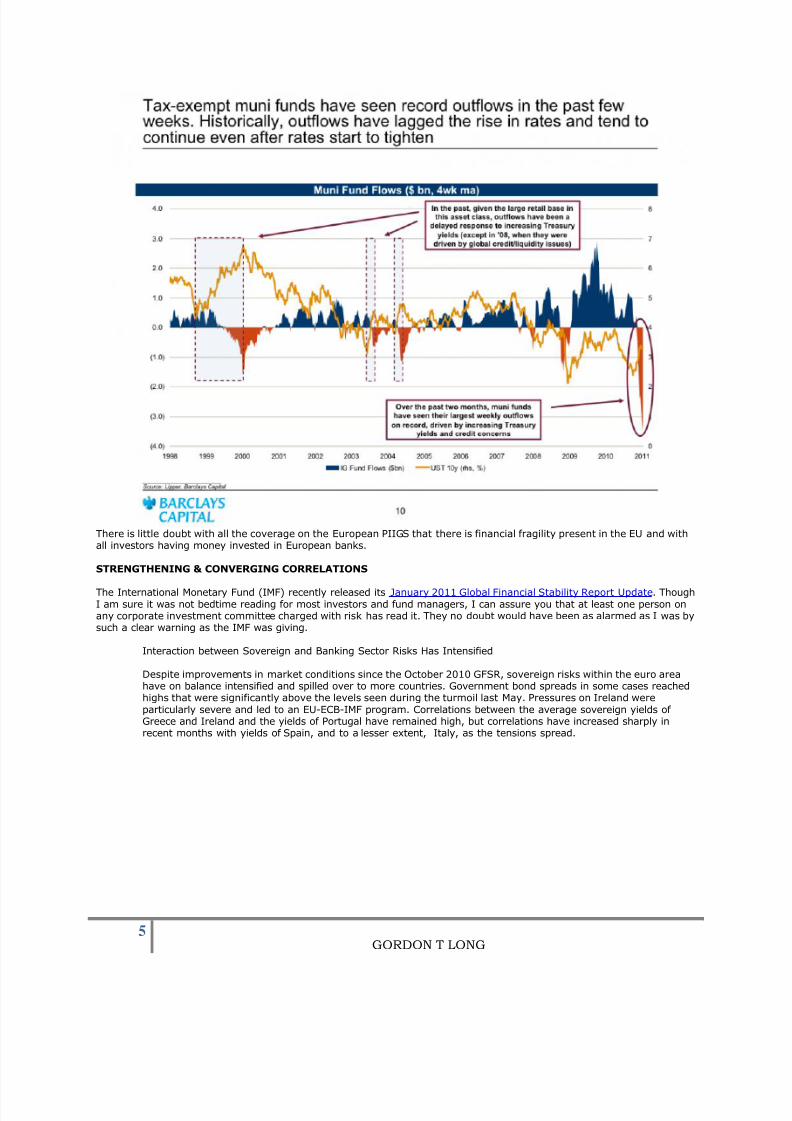

Then noted financial analyst Meredith Whitney appears on 60 Minutes' on a Sunday for a 12 minute interview clip and allhell breaks loose in an anxious Muni Bond market. The following Barclays Capital chart shows the dramatic shift whenfinancial fragility is present.

There is little doubt with all the coverage on the European PIIGS that there is financial fragility present in the EU and withall investors having money invested in European banks.

STRENGTHENING & CONVERGING CORRELATIONS

The International Monetary Fund (IMF) recently released its January 2011 Global Financial Stability Report Update. ThoughI am sure it was not bedtime reading for most investors and fund managers, I can assure you that at least one person onany corporate investment committee charged with risk has read it. They no doubt would have been as alarmed as I was bysuch a clear warning as the IMF was giving.

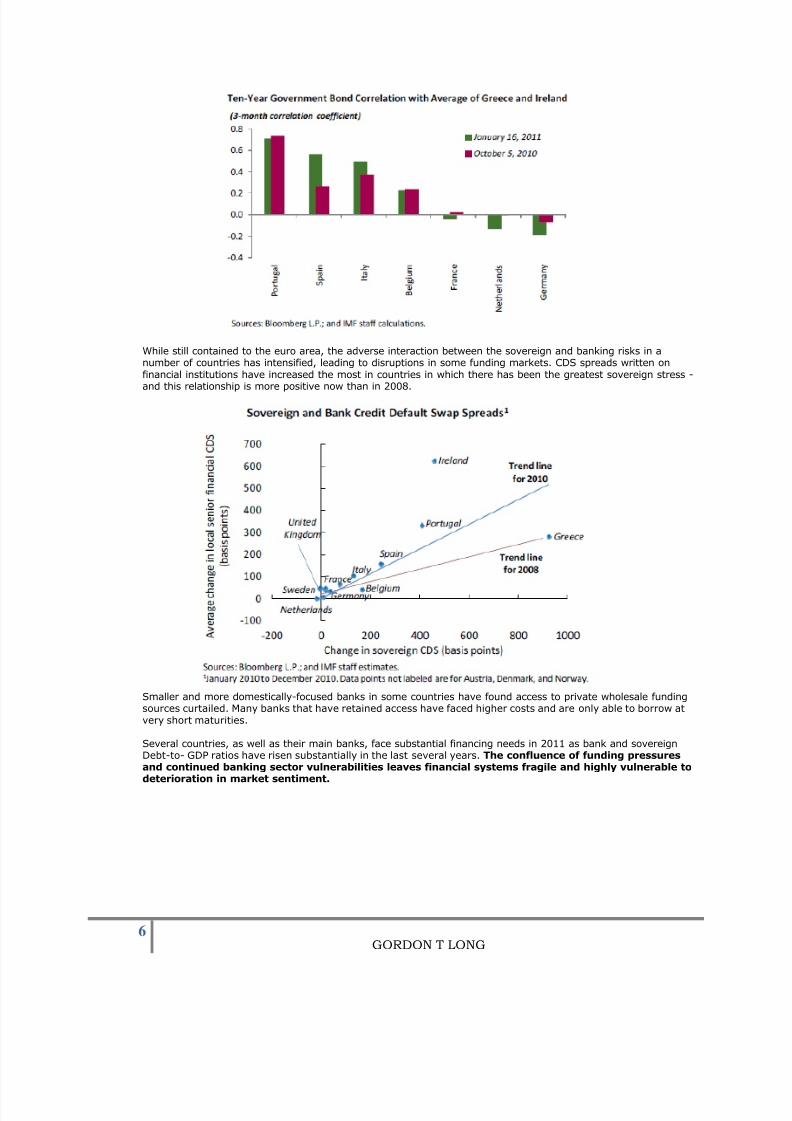

Interaction between Sovereign and Banking Sector Risks Has Intensified

Despite improvements in market conditions since the October 2010 GFSR, sovereign risks within the euro areahave on balance intensified and spilled over to more countries. Government bond spreads in some cases reachedhighs that were significantly above the levels seen during the turmoil last May. Pressures on Ireland wereparticularly severe and led to an EU-ECB-IMF program. Correlations between the average sovereign yields of Greece and Ireland and the yields of Portugal have remained high, but correlations have increased sharply inrecent months with yields of Spain, and to a lesser extent, Italy, as the tensions spread.

While still contained to the euro area, the adverse interaction between the sovereign and banking risks in anumber of countries has intensified, leading to disruptions in some funding markets. CDS spreads written onfinancial institutions have increased the most in countries in which there has been the greatest sovereign stress -and this relationship is more positive now than in 2008.

Smaller and more domestically-focused banks in some countries have found access to private wholesale fundingsources curtailed. Many banks that have retained access have faced higher costs and are only able to borrow atvery short maturities.

Several countries, as well as their main banks, face substantial financing needs in 2011 as bank and sovereignDebt-to- GDP ratios have risen substantially in the last several years. The confluence of funding pressuresand continued banking sector vulnerabilities leaves financial systems fragile and highly vulnerable todeterioration in market sentiment.

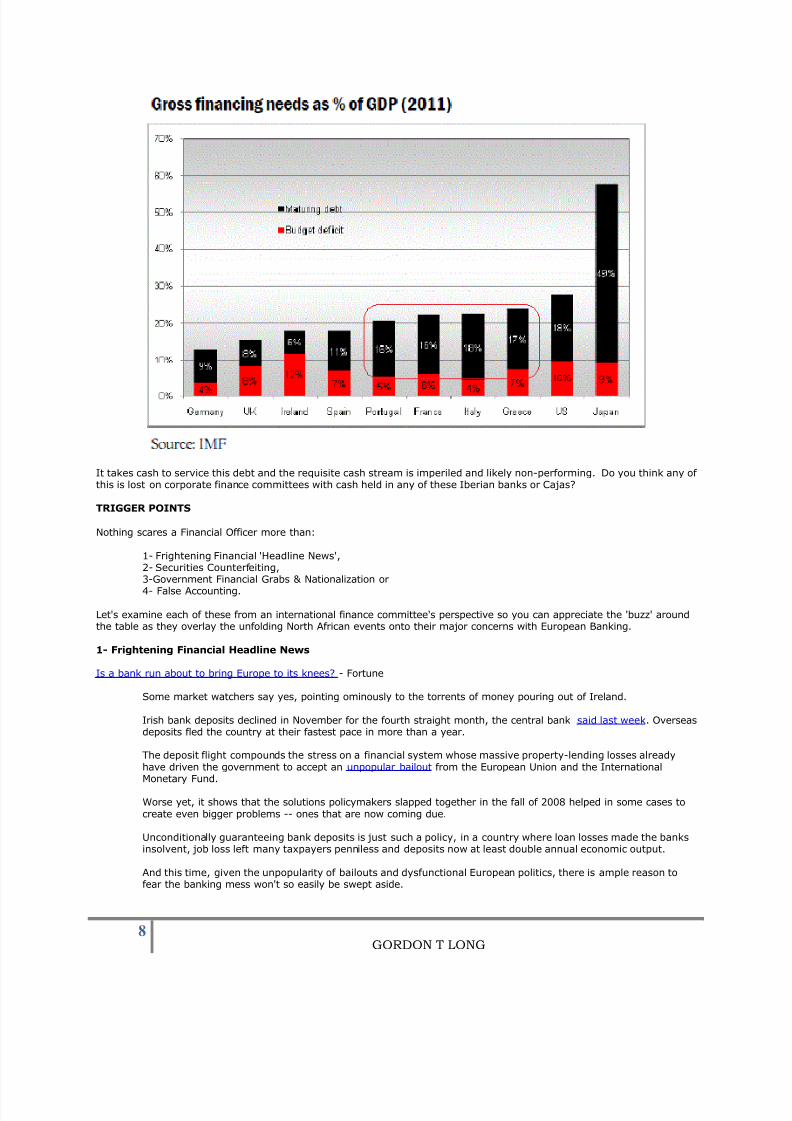

What clearly stands out in the European debt charts below is the relative size of private debt in the Iberian peninsula andthe short term maturity duration. A significant part of this is no doubt commercial real estate as a result of thepronounced real estate bubble experienced in both countries.

It takes cash to service this debt and the requisite cash stream is imperiled and likely non-performing. Do you think any of this is lost on corporate finance committees with cash held in any of these Iberian banks or Cajas?

Let's examine each of these from an international finance committee's perspective so you can appreciate the 'buzz' aroundthe table as they overlay the unfolding North African events onto their major concerns with European Banking.

1- Frightening Financial Headline News

Is a bank run about to bring Europe to its knees? - Fortune

Some market watchers say yes, pointing ominously to the torrents of money pouring out of Ireland.

Irish bank deposits declined in November for the fourth straight month, the central bank said last week. Overseasdeposits fled the country at their fastest pace in more than a year.

The deposit flight compounds the stress on a financial system whose massive property-lending losses alreadyhave driven the government to accept an unpopular bailout from the European Union and the InternationalMonetary Fund.

Worse yet, it shows that the solutions policymakers slapped together in the fall of 2008 helped in some cases tocreate even bigger problems -- ones that are now coming due.

Unconditionally guaranteeing bank deposits is just such a policy, in a country where loan losses made the banksinsolvent, job loss left many taxpayers penniless and deposits now at least double annual economic output.

And this time, given the unpopularity of bailouts and dysfunctional European politics, there is ample reason tofear the banking mess won't so easily be swept aside.

"Facing facts like these, each morning when I wake up I have to wonder, 'Why is today not a goodday for a wholesale run on the Irish banking system?' And if there is a wholesale run on the Irish

banking system, then what stops the same scenario from cascading into Portugal, Greece, Italy, andmost importantly, Spain?"

asks Scott Minerd, chief investment officer at Guggenheim Partners.

That is very much the question being asked in bond markets, where the cost of borrowing surged in all the so-called peripheral European countries in the second half of 2010. The yield on Irish 10-year government bonds, for

instance, surged to 9% at year-end from around 5% in August.

The high cost of market borrowing ties the hands of government officials who have promised to ride to the rescueof the bubble-ridden banks. Ireland has already ponied up outlandish sums to keep the banks afloat. Officialshave said at every turn they believed they had the ability to stabilize the system, but stability has remainedbeyond their reach.

Now, with the state locked out of the bond market and the banks losing depositors, who is going to lend in aneconomy that already has shrunk drastically from its bubbly size of just a few years ago?

Bank runs "will seriously undermine the prosperity of this country for a generation. The first steps to stemmingthe run would include "a big external aid package and steps by the Irish government."

Pimco's Mohammed El-Erian said in November.

The IMF, the EU and the Irish government committed to those steps this fall. But there is still no sign people inIreland or elsewhere believe the $113 billion bailout package will keep their money safe. Among many otherthings, there has been a rush out of the euro for the Swiss franc, not to mention the ever-present embrace of

gold.

The flight from Irish banks has been most pronounced among foreigners, who presumably are less attached totheir bailed-out bankers and can easily find other banks that, at least for the moment, appear less apt to go outof business.

Some 20 billion euros ($27 billion) of overseas deposits fled the country in November alone, according to theCentral Bank of Ireland. The level of foreign deposits has plunged 28% in the past year and is down 42% from itsbubbly peak.

But don't blame just the foreigners. Domestic deposits tumbled by 6.3 billion euros in November, in theirsteepest decline since August 2009.

All told, the Irish banking system's deposit base has contracted by 15% over the past year -- which isn't makingit any easier for taxpayers to keep the deeply troubled banking sector afloat.

Meanwhile, the aid the Irish banks took from the eurosystem more than doubled over the past year, to 97 billion

euros from 45 billion in November 2009.

The flight of deposits from troubledIrish banks is an unhappy ironybecause Ireland was lauded in somequarters in 2008 when it became thefirst state to guarantee bankdeposits. That decision led to ashort-lived surge of funds into theIrish banks -- not that the moneystuck around for long. Since the late2008 peak, more than 100 billioneuros of overseas deposits have leftthe Irish banking system.

When you consider that similartrends could easily play out in theother euro countries, you have therecipe for a hangover-inducing NewYear that is likely, in the view of Minerd, to see the euro plunge anewagainst the dollar. He expects theeuro to test its decadelong lowagainst the dollar of 85 cents beforeall is said and done, compared witha recent $1.33.

continue to flow in and deposits in Europe's weakened banking system flow out, a broader crisis in Europeappears to be imminent in 2011," says Minerd.

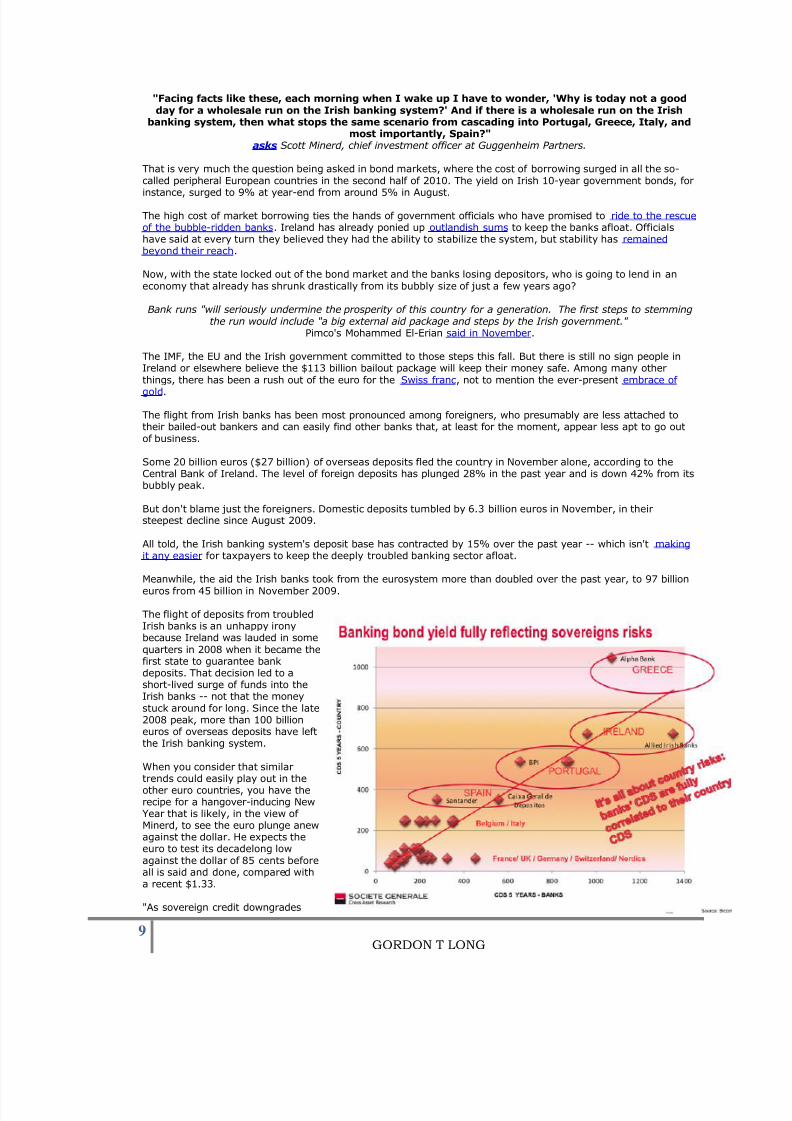

This chart from SocGen makes very clear that in Europe, the perceived credit risk of various banks is tightly linked to thecredit risks of the countries in which they preside. That magnifies the risk significantly, and truly creates a notion of systemic risk. In the US it's conceivable to have lots of defaults without a follow-on systemic crisis.

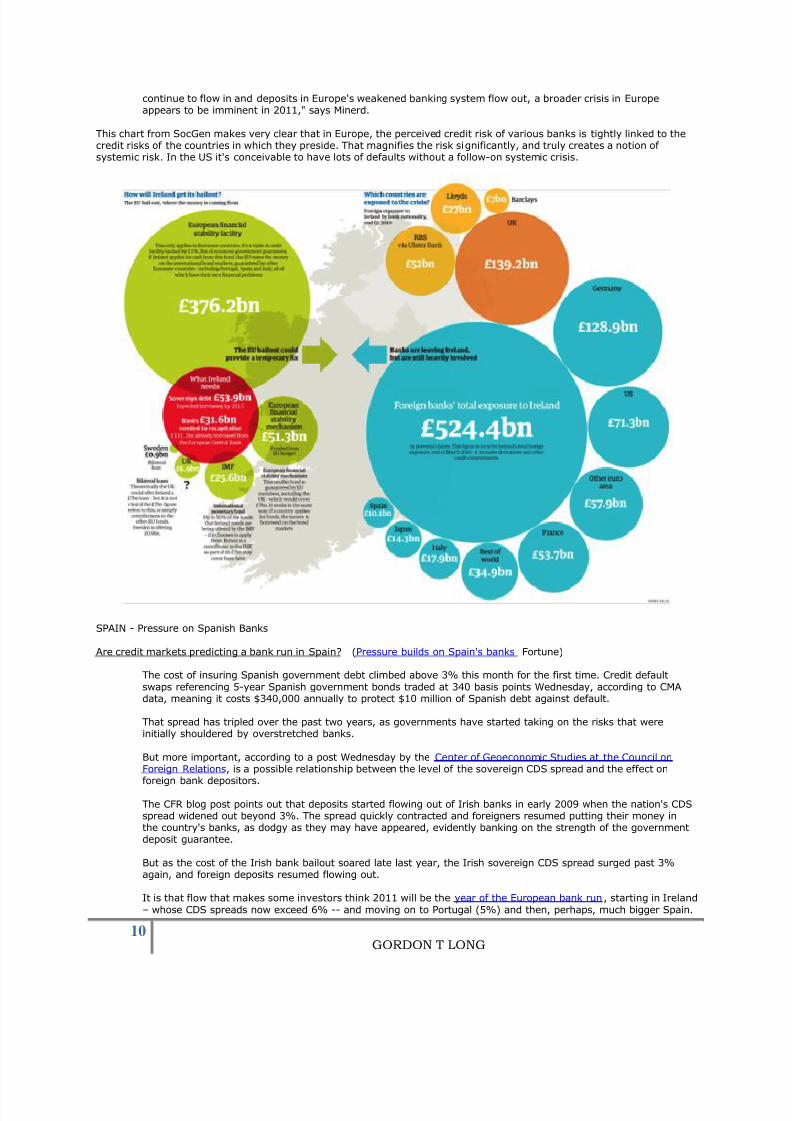

SPAIN - Pressure on Spanish Banks

Are credit markets predicting a bank run in Spain? (Pressure builds on Spain's banks Fortune)

The cost of insuring Spanish government debt climbed above 3% this month for the first time. Credit defaultswaps referencing 5-year Spanish government bonds traded at 340 basis points Wednesday, according to CMAdata, meaning it costs $340,000 annually to protect $10 million of Spanish debt against default.

That spread has tripled over the past two years, as governments have started taking on the risks that wereinitially shouldered by overstretched banks.

But more important, according to a post Wednesday by the Center of Geoeconomic Studies at the Council onForeign Relations, is a possible relationship between the level of the sovereign CDS spread and the effect on

foreign bank depositors.

The CFR blog post points out that deposits started flowing out of Irish banks in early 2009 when the nation's CDSspread widened out beyond 3%. The spread quickly contracted and foreigners resumed putting their money inthe country's banks, as dodgy as they may have appeared, evidently banking on the strength of the governmentdeposit guarantee.

But as the cost of the Irish bank bailout soared late last year, the Irish sovereign CDS spread surged past 3%again, and foreign deposits resumed flowing out.

It is that flow that makes some investors think 2011 will be the year of the European bank run, starting in Ireland– whose CDS spreads now exceed 6% -- and moving on to Portugal (5%) and then, perhaps, much bigger Spain.

Of course, it is early yet to say there will be a run on Spain's banks. While Spain and Ireland both had hugeproperty bubbles, Spain's biggest banks, Santander (STD) and Banco Bilbao (BBVA), have substantialinternational businesses and thus appear to be in much better shape than their Irish counterparts, such as thefraud-ridden Anglo Irish or the simply deflated Allied Irish (AIB).

The bad news is that there have been signs of a deposit pricing war that could add to the stress on the smallerregional banks, which are seen as the weak link in the system. There are few indications the government ismoving aggressively to clean up the bad loans everyone knows are out there.

Even if all goes well, the Spanish banking system is going to need time to earn its way out of years of property-lending misery. But if deposits start fleeing the country in earnest, the government will need to step in withcostly actions, such as mergers and recapitalizations and takeovers.

And as the Irish experience shows, a rising tab for taxpayer support of the banks isn't a recipe for making anyonehappy -- let alone for keeping money from heading for the exits.

2- Securities Counterfeiting

The international corporate finance committees and every CFO / Treasurer are reading that for the first time in the globalfiat currency system we have a European government printing money 'un-backed' in any way including the issue of government debt instruments (even if those instruments are a worthless shame). This is nothing short of outright financialcounterfeiting.

Ireland Prints 25% of its GDP in German Euro‟s Barnes

The Irish Central Bank has crossed the Rubicon in European Union currency terms. They have printed up about25% of their GDP in electronic credits, and stuffed those credits into their banks. These deposits, if you will, donot have new debt issued behind them.

This is a form of hyperinflation if you will, at least in context that a Central Bank, with no actual printing press, ora functioning bond market, has now electronically printed up new currency units for their banks without issuingdebt behind these actions.

While this has happened before in history, it has not happened in the Euro currency project officially beforetoday. This act is going to move the monetary policy of the union, to the individual capitals. The capacity to printelectronic credits, with out the creation of cash currency or debt, is a new wrinkle in the economic landscape.The implications and ramifications will take a while to appear, but “Mark” my words, Germany both as a people,and as a political organization will notice this event. The German people now find themselves captured in acurrency where neighbors who are in political and financial stress, have the capacity to print up German Euros ondemand. This is Germany‟s worse nightmare as both a nation and a people. I dare say, you could not design amore frightening prospect for the “United German States”, than to find their currency diluted on demand byreckless neighbors.

In the coming weeks, and I say that because thing rarely happen quickly in life, Europe is going to have aSovereign crisis of epic size. They will have to decide what happens next, and do so rather quickly.

EU politicians have known about Ireland‟s decision to print currency for weeks now. They have had time toconsider their response to Ireland‟s dilution of the Euro. I do not expect an initial reaction in the currencymarkets, as this kind of event takes time to be absorbed by all stakeholders in the Euro.

The Celtic Tiger has made their move and resorted to naked currency printing, to support its banks. The nextmove belongs to Europe and it‟s going to be interesting to see how this plays out in the public arena‟s. We knowwho is first, what CB will be second?

Irish lenders besiege central bank for emergency loans Pritchard

The latest data shows that Anglo Irish Bank and other lenders had borrowed €51bn (£43bn) from the Irishcentral bank by the end of December, under an obscure progamme listed in the balance sheet as "other assets".

This comes on top of €132bn in loans from the ECB itself, the figure normally tracked by analysts and itself 24pcof all ECB lending.

"This is a horror story: it shows the cataclysmic condition of the Irish banking system," said Tim Congdon fromInternational Monetary Research. "The banks have borrowed €183bn in total, or 110pc of Irish GDP. They haveburned through all their capital and a lot of their deposits as well. This is going to end up on the national debt".

The actions of the Irish central bank are authorized by Frankfurt, but fall into a grey area of monetary policysince they appear to involve creation of money outside the normal control of the ECB's governing council.

The use of Ireland's emergency liquidity assistance program (ELA) raises further questions since the quality of collateral is unacceptable for normal ECB operations. The volume of borrowing has begun to level off after asurge in November.

3- Government Financial Grabs and Nationalization

Hungary, Poland, and three other nations take over citizens' pension money to make up government budget shortfalls.

The Adam Smith Institute Blog European nations begin seizing private pensions Hungary, Poland, and three othernations take over citizens' pension money to make up government budget shortfalls. Old women eat lunch in aretirement home in Budapest Dec. 13, 2010. Hungarian lawmakers rolled back a 1997 pension reform, allowingthe government to effectively seize up to $14 billion in private pension assets to reduce the budget gap whileavoiding painful austerity measures. People‟s retirement savings are a convenient source of revenue forgovernments that don‟t want to reduce spending or make privatizations. As most pension schemes in Europe areorganized by the state, European ministers of finance have a facilitated access to the savings accumulated there,and it is only logical that they try to get a hold of this money for their own ends. In recent weeks I have notedfive such attempts: Three situations concern private personal savings; two others refer to national funds.

The most striking example is Hungary, where last month the government made the citizens an offer they couldnot refuse. They could either remit their individual retirement savings to the state, or lose the right to the basicstate pension (but still have an obligation to pay contributions for it). In this extortionate way, the governmentwants to gain control over $14bn of individual retirement savings.

The Bulgarian government has come up with a similar idea. $300m of private early retirement savings wassupposed to be transferred to the state pension scheme. The government gave way after trade unions protested

and finally only about 20% of the original plans were implemented.

A slightly less drastic situation is developing in Poland. The government wants to transfer of 1/3 of futurecontributions from individual retirement accounts to the state-run social security system. Since this system doesnot back its liabilities with stocks or even bonds, the money taken away from the savers will go directly to thestate treasury and savers will lose about $2.3bn a year. The Polish government is more generous than theHungarian one, but only because it wants to seize just 1/3 of the future savings and also allows the citizens tokeep the money accumulated so far.

The fourth example is Ireland. In 2001, the National Pension Reserve Fund was brought into existence for thepurpose of supporting pensions of the Irish people in the years 2025-2050. The scheme was also supposed toprovide for the pensions of some public sector employees (mainly university staff). However, in March 2009, theIrish government earmarked €4bn from this fund for rescuing banks. In November 2010, the remaining savingsof €2.5bn was seized to support the bailout of the rest of the country.

The final example is France. In November, the French parliament decided to earmark €33bn from the nationalreserve pension fund FRR to reduce the short-term pension scheme deficit. In this way, the retirement savings

intended for the years 2020-2040 will be used earlier, that is in the years 2011-2024, and the government willspend the saved up resources on other purposes.

It looks like although the governments are able to enforce general participation in pension schemes, they do notseem to be the best guardians of the money accumulated there.The table below is a summary of the discussed fiscal-retirement situations (source):*These figures do not include the costs of higher taxes, price inflation and low interest rates, which additionallydevaluate retirement savings.

Partial Nationalization of Cajas Savings Banks (Spain plans partial nationalization of savings banks)

Estimates of the cost to recapitalize the banks range from 17 billion to 120 billion euros with consensus falling in the 25 billion to 50 billion area, though Economy Minister Elena Salgado says it will be much lower.

- Spain plans a partial state takeover of its weakest savings banks as it seeks to reassure investors a rescue willnot weigh on its deficit.

- The government would force debt-laden regional savings banks to become conventional banks and seek stockmarket listings to persuade skittish investors that they are good investments.

- The state-backed bank restructuring fund (FROB) would then take stakes in the banks -- known as cajas -- thatfail to attract private investment, the source said. Up to now the FROB has functioned as a lender of last resort tothe cajas.

- Deputy Prime Minister Alfredo Perez Rubalcaba told reporters a new savings bank plan was coming soon andcould include new laws, implying a reform of the FROB.

- High levels of bad property loans at the cajas are seen as a major risk for Spain.

- The Bank of Spain forced the cajas last year into a round of mergers, reducing their number to 17 from 45. Fiveof them failed Europe-wide stress tests on banks last year.

- They must reveal by January 31 more details about their bad loans and property holdings. Only two cajas havereported so far, but once all the reports are in, the Bank of Spain will be able to give a clear idea of the totalrecapitalization needs.

- A bank recapitalization worth 50 billion euros would amount to about 5 percent of Spanish grossdomestic product, which could endanger the government's goal of cutting the budget deficit to 6 percent of GDP this year.

- The FROB would have to raise debt on the market to purchase the bank stakes. In theory, the books would bebalanced by the stakes in the savings banks to avoid a deficit impact, although the risk is those stakes dwindle invalue.Taking stakes in the banks will increase the government's debt needs, said Josep Soler, general director of Financial Studies Institute. "We still don't know ... how much the cajas are going to need," he said. The FROBwould invest in the cajas at market rates subject to EU anti-trust approval, a government source told Reuters.

- While some of the biggest cajas are seen as attractive, investors have shied away from smaller ones, notoriousfor being used by local politicians to fund pet projects from casinos to airports.

- The cajas plan a March trip to Asia, including China, following similar road shows in Europe and the UnitedStates.

4- False Accounting

What is obvious to any CFO / Treasurer following the banking situation in Europe is that the European Bank Stress testswere at best a sham and possibly even bordering on outright market manipulation by the powers to be. They are notconvinced.

The EU 'Extend & Pretend' program of hiding massive toxic debts, the avoidance of 'market-to market' real estateaccounting valuations to reflect (even approximate) acceptable LTV ratios, extensive off balance sheet StructuredInvestment Vehicle (SIV) bank debt obligations still in place and extreme bank leverage ratios relative to the rest of theworld, leaves most financial professionals nervous. Very nervous.

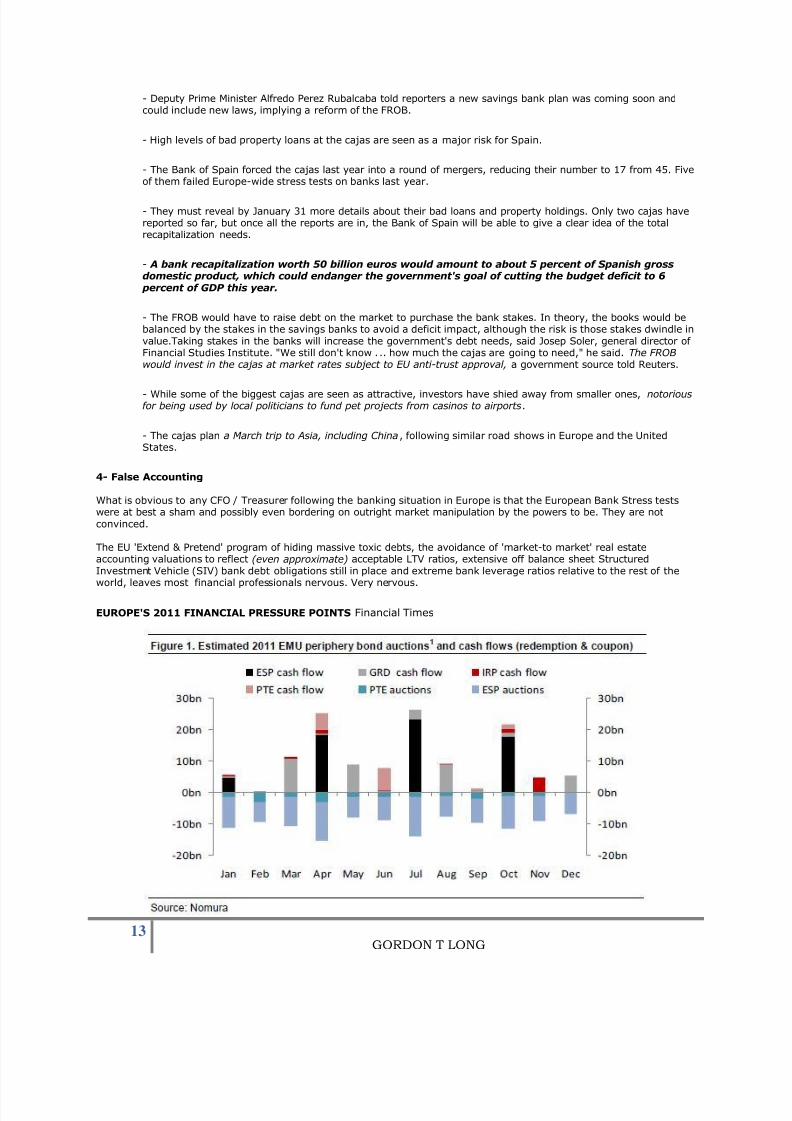

EUROPE'S 2011 FINANCIAL PRESSURE POINTS Financial Times

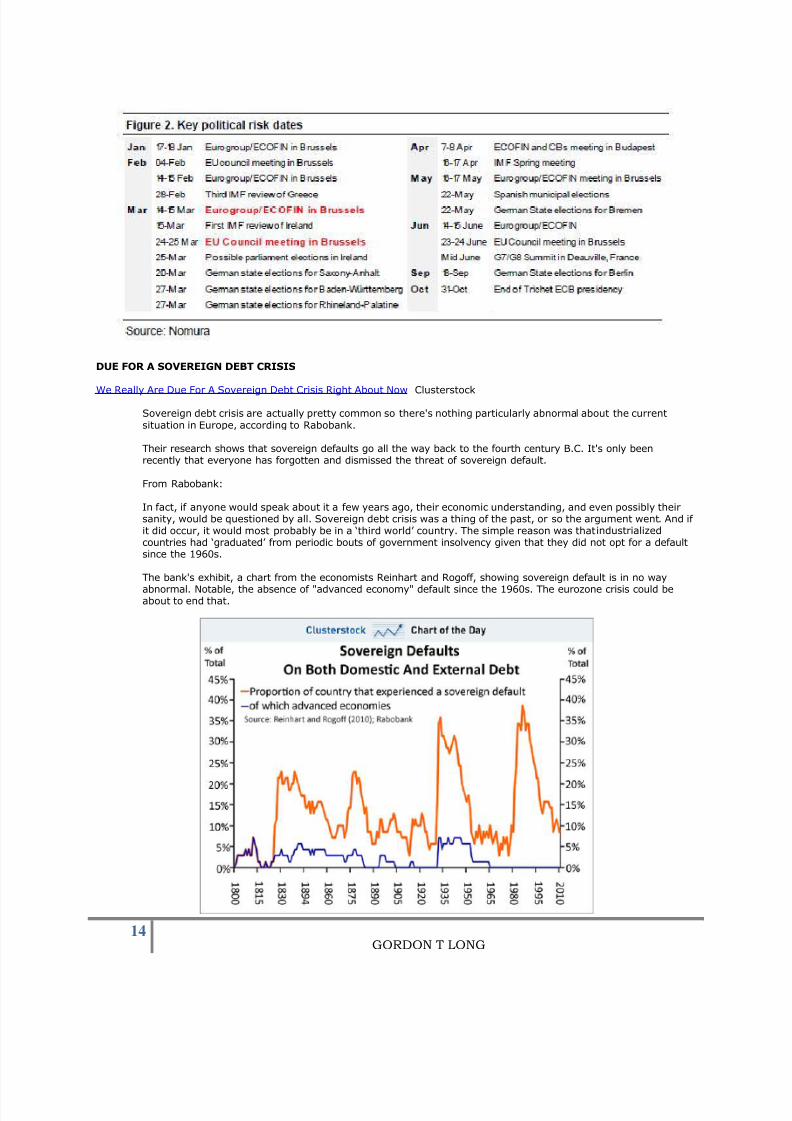

We Really Are Due For A Sovereign Debt Crisis Right About Now Clusterstock

Sovereign debt crisis are actually pretty common so there's nothing particularly abnormal about the currentsituation in Europe, according to Rabobank.

Their research shows that sovereign defaults go all the way back to the fourth century B.C. It's only beenrecently that everyone has forgotten and dismissed the threat of sovereign default.

From Rabobank:

In fact, if anyone would speak about it a few years ago, their economic understanding, and even possibly theirsanity, would be questioned by all. Sovereign debt crisis was a thing of the past, or so the argument went. And if it did occur, it would most probably be in a „third world‟ country. The simple reason was that industrializedcountries had „graduated‟ from periodic bouts of government insolvency given that they did not opt for a defaultsince the 1960s.

The bank's exhibit, a chart from the economists Reinhart and Rogoff, showing sovereign default is in no way

abnormal. Notable, the absence of "advanced economy" default since the 1960s. The eurozone crisis could beabout to end that.

“You will not know about, nor see these stealth bank runs until it is far too late to react ” The movement of money is hidden electronically and reported long after the fact.

Sign Up for the next FREE release in any of our research article themes at TIPPING POINTS E-mail: [email protected]

Type in the Subject Line: Research Themes

THEMES: Extend & Pretend, Sultans of Swap, Euro Experiment, Currency Wars, Preserve &

Protect. Go to COMMENTARY for a complete index.

Gordon T Long

Tipping Points Mr. Long is a former senior group executive with IBM & Motorola, a principle in a high tech public start-up and founder of aprivate venture capital fund. He is presently involved in private equity placements internationally along with proprietarytrading involving the development & application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and shouldnot be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any o therfinancial instrument at any time. While he believes his statements to be true, they always depend on the reliability of his own crediblesources. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies inyour legal jurisdiction, before making any investment decisions, and barring that, you are encouraged to confirm the facts on your own beforemaking important investment commitments.