Q-1 The Main Reason why Satyam Fraud came into limelight was- Discuss the circumstances under which the Satyam scam was exposed. Why he confessed ? The gap in the balance sheet reached unmanageable proportions and could not be filled anyhow in future. The whistle blower whose email to a Satyam board members triggered a chain of events . Ramalinga Raju’s Confession Failure to complete MAYTAS (Infra & Property) deal which could have helped R.Raju to cover inflated balance sheets. World Bank’s 8 year ban on Satyam for data theft & bribery allegations (Dec 23, 2008) 4 board members resign in the wake of MAYTAS controversy (Dec 28, 2008) Sale of pledged shares of promoters resulted into promoters’ stack coming down (from 25 % in 2001 to around 5 % in 2009) . Share Price of Satyam got affected because of negativity spread in market.

Transcript

Q-1

The Main Reason why Satyam Fraud came into limelight was-

Discuss the circumstances under which the Satyam scam was exposed.

Why he confessed ? The gap in the balance sheet reached

unmanageable proportions and could not be filled anyhow in future.

The whistle blower whose email to a Satyam board members triggered a chain of events .

Ramalinga Raju’s Confession

Failure to complete MAYTAS (Infra & Property) deal which could have helped R.Raju

to cover inflated balance sheets.

World Bank’s 8 year ban on Satyam for data theft & bribery allegations (Dec 23, 2008)

4 board members resign in the wake of MAYTAS controversy (Dec 28, 2008)

Sale of pledged shares of promoters resulted into promoters’ stack coming down

(from 25 % in 2001 to around 5 % in 2009) .

Share Price of Satyam got affected because of negativity spread in market.

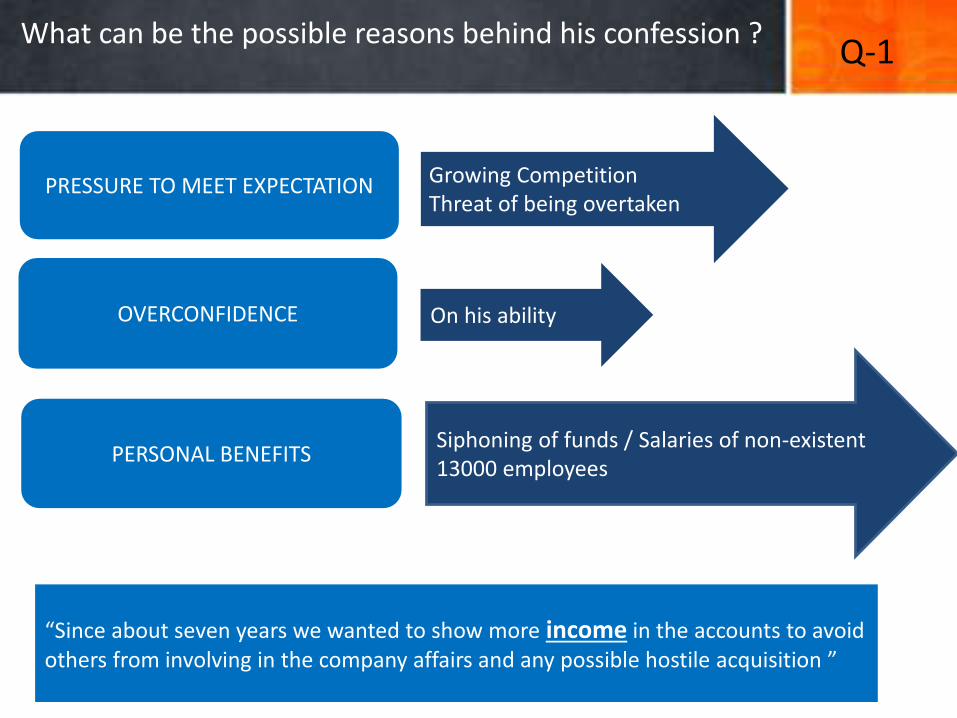

PRESSURE TO MEET EXPECTATION Growing CompetitionThreat of being overtaken

OVERCONFIDENCE On his ability

PERSONAL BENEFITSSiphoning of funds / Salaries of non-existent 13000 employees

“Since about seven years we wanted to show more income in the accounts to avoid others from involving in the company affairs and any possible hostile acquisition ”

What can be the possible reasons behind his confession ?Q-1

Who could have prevented this fraud ? Q-2

Investors

Board Members

Government Intervention

Accounting Standards

Ethics &

Code of Conduct

Board Composition(Aug 2008, Form 20-F, No individual as Audit Committee Financial Expert, Out of 6 non management directors- 4 were academicians. )

Board Independence (Non management directors didn’t meet without management directors)

Board Committee(Lack of nominating & corporate governance body)

Corporate Governance Mechanisms Adopted By Satyam Q-3

Roles of External Auditors:

Auditor didn’t confirm & re-verify the bank balances independently.

Violation in cross checking of financial data: No sample checking of invoices.

They took audit fees ( 430 mn INR ) which were way above than Industry average. (Wipro- 280 mn , Infosys- 153 mn, TCS- 277 mn INR)

At the end of financial year 2007-08, Satyam showcased a debt of 2.36 Billion INR , even after having unused cash asset of 44.62 Billion INR – Surprisingly none of the auditors checked this discrepancy.

Assessing Responsibilities of Internal & External Auditors Q-4

Roles of Internal Auditors:

Fake invoices of total 327 companies (registered in names of Raju & his family) went unverified over the years.

Cash and Bank Balances / fictitious assets were not cross checked.

Audit Plans were prepared on the basis of the approval of the promoters.

Internal auditors didn’t raise their concern regarding assigning PWC as an external auditor for the long time, and high audit fees got approved without any issues.

Serious findings of the auditing team were ignored by the audit team leader at the time of signing the audit report.

In actual nobody did their job properly right starting with committee headed by CFO and team

Chairman used all his brains just to save himand make money by taking a step ofacquiring his sons’ companies MYTAS (Infra& Property) but as deal did not happen anddue to other factors company downfallstarted.

Even after confessing he tried to portrayhimself as sympathetically innocent andtook the overall responsibility about thewrong doings.

Somehow, He was sure that by doing this hewill get the sympathy and also surrenderingmay lead to less jail terms andconsequences. He admitted all the frauds insuch a way that it may look genuine, and heremains ‘GOOD’ in the eyes of hisshareholders.

“ It was like riding a tiger,not knowing how to get off

without being eaten.. “

Evaluating statement made by R.Raju in his resignation letter Q-5

Roles of Board of Directors in Preventing a Financial Fraud

Board of directors should be inquisitive enough to check this kind of irregularitiesand raise doubts if something appears fishy.

Independent director is responsible for final audit hence he must have abackground of CA, ICWA or Accounts as is evident from post-crisis board ofSatyam- 3 of the 5 independent board of directors do have B.Com andChartered Accountant background, This feature of independent directorshailing from Accountant was strictly absent in pre-crisis board of Satyam.

Other general characteristics of board that can play a role in preventing financialstatement frauds are -

Periodically Monitor - financial activity on a regular basis, comparing actual tobudgeted revenues and expenses

Avoid or discourage related party transactions - useful in preventing subsidiaryrelated frauds.

Q-6

Statistics have shown time and time again that a lot of employees will do just that in order to meet budgetary goals, secure bank loans, earn bonuses and salary increases, and obtain donor funding.

Reduce the pressures that encourage financial statement fraud– Don’t give your employees unachievable financial goals such as unreasonable fundraising quotas or unrealistic budgets.– Set firm accounting policies, and don’t allow exceptions.

Reduce the opportunities employees see to commit fraud– Maintain accurate accounting records – including monthly reconciliations of all accounts and constant management overview.– Physically secure company assets, check stock, signature stamps, etc.– Always have segregation of duties in the accounting department.– Run background checks on all potential employees before hiring.

Reduce the rationalization of fraudulent actions– Set the tone at the top and lead by example. Employees can easily rationalize dishonest behavior if they see unethical behavior in management as well.– Establish strong company policies that define what is and is not tolerated within the organization.

Engage the Auditor

An annual audit and a strong relationship with an auditor can add tremendous value to an organization, in terms of accounting expertise, advice on internal controls, and knowledge about industry issues.

There are many loop holes in government regulations, which companies use intentionally for their own profit.

But, to a large extent changes in the laws / regulations will help preventing companies doing all such kind of frauds. Some of the changes could be:

Proper auditing of publicly listed firms from more than 1 auditing agencies. Keeping in-check of assets and invoice related data of non-listed companies, so

that highly inflated B/L sheets can be traced down right from the beginning. Stricter Punishments and Faster decisions in such fraud cases, special trial / fast-

track courts should be made.

Corporate Governance is not something which can be enforced by mere legislation;it is a way of life and has to imbibe itself into the very business culture the companyoperates in. Ultimately, following practices of good governance leads to all roundbenefits for all the parties concerned. The company’s reputation is boosted, theshareholders and creditors are empowered due to the transparency CorporateGovernance brings in, the employees enjoy the improved systems of managementand the community at large enjoys the fruits of better economic growth in aresponsible way.

Making regulatory changes would help in preventing the fraud? Q-7

“Independent directors should also (in addition to the management) be held accountable for board decisions and audit-related compliance practices.”

— Andrew Holland, CEO, equities, Ambit Capital

“The concept of CEO and Board chair separation is well accepted in Europe, and American companies are steadily moving in that direction. This would bring a better

balance in the boardroom.” — Neville Dumasia, head, Governance, Risk and Compliance, KPMG

“Accountability and action against fraud/negligence are major concerns. Professionals (auditors) should be made accountable and consequences (punishment) should follow

if there are any deficiencies and slip-ups.” — N K Jain, secretary and CEO, Institute of Company Secretaries of India

Lessons learned from this case

Investigate All Inaccuracies Stricter Punishment / Rules, Faster

Decisions Corporate Governance Needs to be

Stronger

Q-8

Regulatory Changes in India After Satyam Scam Q-9

Satyam Scam increased risks stemming from being an independent director in Indian firms.

(i) IDs exited in large numbers from other Indian firms resulting in an overall decrease in the percentage of IDs in corporate boards.

(ii) The quality of IDs, as measured by their educational qualifications and professional experience, declined.

(iii) Director compensation, in particular fixed compensation, increased.

Consistent with the market interpreting ID exits as a negative signal about the firm, we find that negative stock price reactions to ID exits. This reaction is disproportionately more when the ID sat on the audit committee of the board and possessed business expertise.

The failure also highlighted the ineffectiveness of monitoring by IDs.

Regulatory Changes in India After Satyam Scam Q-9

The Satyam scandal also served as a catalyst for the Indian government to rethink the corporate governance, disclosure, accountability and enforcement mechanisms in place.

Corporate Governance provisions of the companies bill (2009)

Audit process, Auditors & Eligibility Independent Directors- Appointment, Qualification Meetings of the Board and its powers

MCA Guidelines

Issuance of a formal appointment letter to directors. Separation of the office of chairman and the CEO. Institution of a nomination committee for selection of directors. Limiting the number of companies in which an individual can become a director. Tenure and remuneration of directors, Training of directors. Performance evaluation of directors. Additional provisions for statutory auditors.

SEBI Committee on Disclosure & Accounting Standards (September,2009)

Appointment of the chief financial officer (CFO) by the audit committee after assessing the qualifications, experience and background of the candidate;

Rotation of audit partners every Five years (Now Ten) Voluntary adoption of International Financial Reporting Standards (IFRS); Interim disclosure of balance sheets (audited figures of major heads) on a half-yearly

basis Streamlining of timelines for submission of various financial statements by listed entities

as required under the Listing Agreement.46 In early 2010, SEBI amended the Listing Agreement to add provisions related to the

appointment of the CFO by the audit committee and other matters related to financial disclosures.

Compliance & Enforcement : To Clause 49

Regulatory Changes in India After Satyam Scam

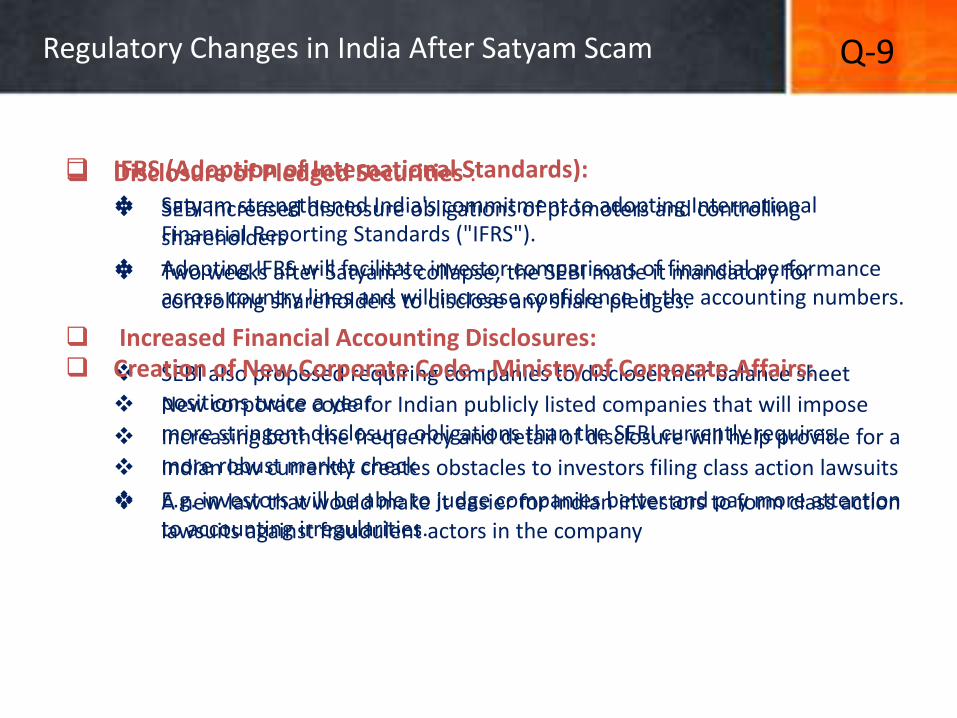

Disclosure of Pledged Securities :

SEBI increased disclosure obligations of promoters and controlling shareholders

Two weeks after Satyam's collapse, the SEBI made it mandatory for controlling shareholders to disclose any share pledges.

Increased Financial Accounting Disclosures:

SEBI also proposed requiring companies to disclose their balance sheet positions twice a year.

Increasing both the frequency and detail of disclosure will help provide for a more robust market check

E.g. investors will be able to judge companies better and pay more attention to accounting irregularities.

Q-9

IFRS (Adoption of International Standards):

Satyam strengthened India's commitment to adopting International Financial Reporting Standards ("IFRS").

Adopting IFRS will facilitate investor comparisons of financial performance across country lines and will increase confidence in the accounting numbers.

Creation of New Corporate Code - Ministry of Corporate Affairs:

New corporate code for Indian publicly listed companies that will impose more stringent disclosure obligations than the SEBI currently requires.

Indian law currently creates obstacles to investors filing class action lawsuits

A new law that would make it easier for Indian investors to form class action lawsuits against fraudulent actors in the company

Post Satyam : On-going Case & Current Justice System for white-collar crimes

On-going Case

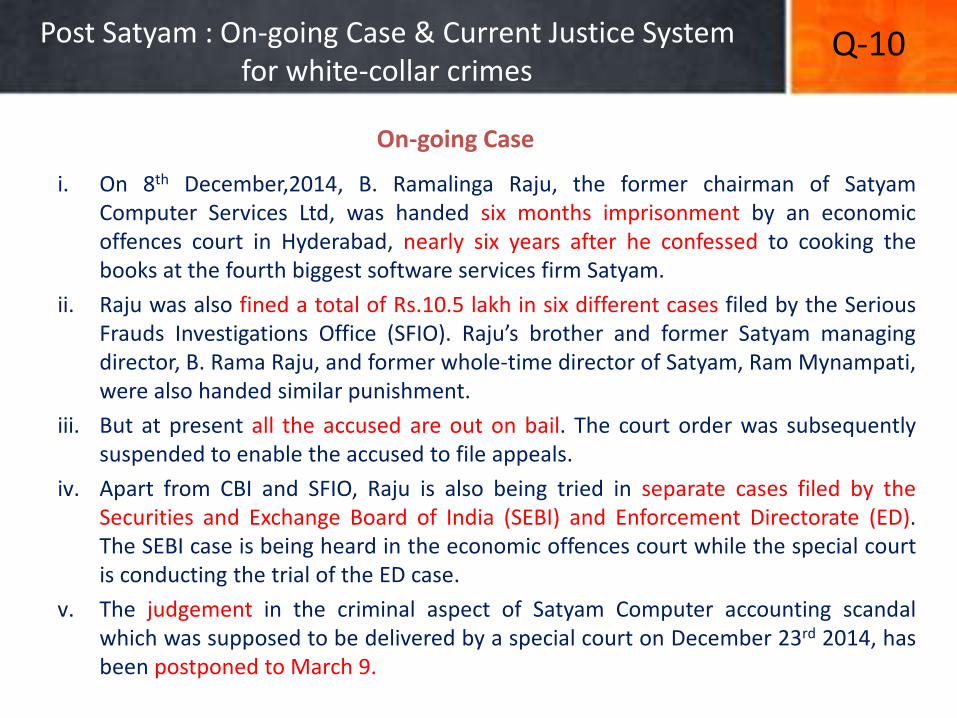

i. On 8th December,2014, B. Ramalinga Raju, the former chairman of SatyamComputer Services Ltd, was handed six months imprisonment by an economicoffences court in Hyderabad, nearly six years after he confessed to cooking thebooks at the fourth biggest software services firm Satyam.

ii. Raju was also fined a total of Rs.10.5 lakh in six different cases filed by the SeriousFrauds Investigations Office (SFIO). Raju’s brother and former Satyam managingdirector, B. Rama Raju, and former whole-time director of Satyam, Ram Mynampati,were also handed similar punishment.

iii. But at present all the accused are out on bail. The court order was subsequentlysuspended to enable the accused to file appeals.

iv. Apart from CBI and SFIO, Raju is also being tried in separate cases filed by theSecurities and Exchange Board of India (SEBI) and Enforcement Directorate (ED).The SEBI case is being heard in the economic offences court while the special courtis conducting the trial of the ED case.

v. The judgement in the criminal aspect of Satyam Computer accounting scandalwhich was supposed to be delivered by a special court on December 23rd 2014, hasbeen postponed to March 9.

Q-10

Post Satyam : Ongoing Case & Current Justice System for white-collar crimes

White-collar crime is a broad term that covers a variety of nonviolent crimes that arealleged to involve cheating in one form or another.committed by business andgovernment professionals.

Typical white-collar crimes (India) includes Health care fraud, bribery, Ponzi schemes,insider trading, embezzlement, cybercrime, copyright infringement, money laundering,identity theft, forgery, extortion, credit card frauds, Fake Employment placementrackets, Tax Evasion, Telemarketing fraud etc.

SEBI, CBI, Serious Fraud Investigation Office (Ministry of Corporate Affairs), CentralEconomic Intelligence Bureau, Directorate of Enforcement , Directorate general ofAnti-Evasion.

In USA : It has been made mandatory for the Chief Executive Officer (CEO) and the Chief Finance Officer (CFO) of a company to certify that: (a) the periodic reports filed with the SEC are materially correct; (b) the financial disclosures ‘fairly represent' the

company's operations financial conditions, and (c); they are responsible for evaluating and maintaining adequate internal controls. The penalty in case of false or improper

certification ranges from US$ 1 million to US$ 5 million or imprisonment up to ten years or both