76

C ONSOLIDATED F INANCIAL S TATEMENTS AND S UPPLEMENTARY I NFORMATION Ascension Health Alliance d/b/a Ascension Years Ended June 30, 2014 and 2013 With Reports of Independent Auditors

C O N S O L I D A T E D F I N A N C I A L

S T A T E M E N T S A N D S U P P L E M E N T A R Y

I N F O R M A T I O N

Ascension Health Alliance d/b/a Ascension Years Ended June 30, 2014 and 2013 With Reports of Independent Auditors

1403-1210450

Ascension

Consolidated Financial Statements and Supplementary Information

Years Ended June 30, 2014 and 2013

Contents

Report of Independent Auditors.......................................................................................................1

Consolidated Financial Statements

Consolidated Balance Sheets ...........................................................................................................3 Consolidated Statements of Operations and Changes in Net Assets ...............................................5 Consolidated Statements of Cash Flows ..........................................................................................7 Notes to Consolidated Financial Statements ....................................................................................9

Supplementary Information

Report of Independent Auditors on Supplementary Information ..................................................66 Schedule of Net Cost of Providing Care of Persons

Living in Poverty and Other Community Benefit Programs ......................................................67 Credit Group Consolidated Balance Sheets as of June 30, 2014 and 2013 ...................................68 Credit Group Consolidated Statements of Operations and Changes in Net Assets for the Years Ended June 30, 2014 .............................................................................................70 Schedule of Credit Group Cash and Investments ..........................................................................72 Schedule of Credit Group Statistical Information .........................................................................73

1403-1210450 1

Report of Independent Auditors

The Board of Directors Ascension Health Alliance d/b/a Ascension

We have audited the accompanying consolidated financial statements of Ascension Health Alliance d/b/a Ascension, which comprise the consolidated balance sheets as of June 30, 2014 and 2013, and the related consolidated statements of operations and changes in net assets and cash flows for the years then ended, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in conformity with U.S. generally accepted accounting principles; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free of material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

A member firm of Ernst & Young Global Limited

Ernst & Young LLP The Plaza in Clayton Suite 1300 190 Carondelet Plaza St. Louis, MO 63105-3434

Tel: +1 314 290 1000 Fax: +1 314 290 1882 ey.com

1403-1210450 2

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the consolidated financial position of Ascension Health d/b/a Ascension at June 30, 2014 and 2013, and the consolidated results of their operations and their cash flows for the years then ended in conformity with U.S. generally accepted accounting principles.

ey September 11, 2014

A member firm of Ernst & Young Global Limited

3 1403-1210450

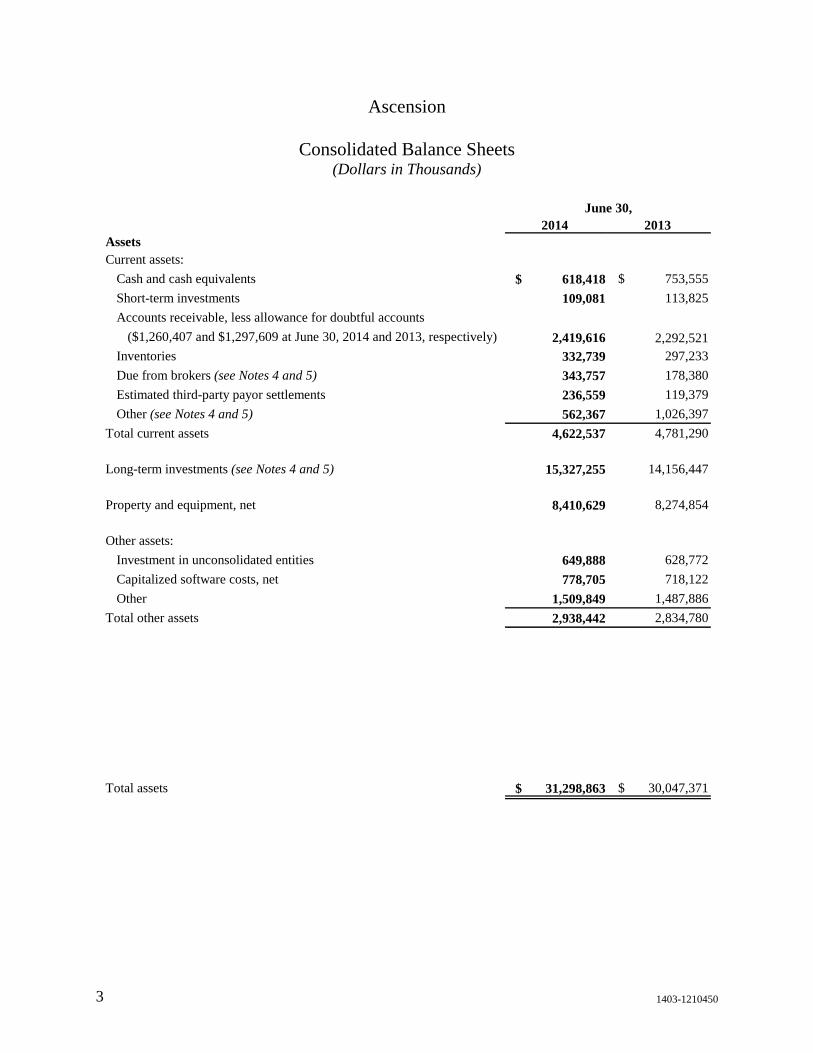

Ascension

Consolidated Balance Sheets (Dollars in Thousands)

2014 2013AssetsCurrent assets:

Cash and cash equivalents $ 618,418 $ 753,555

Short-term investments 109,081 113,825

Accounts receivable, less allowance for doubtful accounts

($1,260,407 and $1,297,609 at June 30, 2014 and 2013, respectively) 2,419,616 2,292,521 Inventories 332,739 297,233

Due from brokers (see Notes 4 and 5) 343,757 178,380

Estimated third-party payor settlements 236,559 119,379

Other (see Notes 4 and 5) 562,367 1,026,397

Total current assets 4,622,537 4,781,290

Long-term investments (see Notes 4 and 5) 15,327,255 14,156,447

Property and equipment, net 8,410,629 8,274,854

Other assets:

Investment in unconsolidated entities 649,888 628,772

Capitalized software costs, net 778,705 718,122

Other 1,509,849 1,487,886

Total other assets 2,938,442 2,834,780

Total assets $ 31,298,863 $ 30,047,371

June 30,

1403-1210450 4

2014 2013

Liabilities and net assets

Current liabilities:

Current portion of long-term debt $ 91,532 $ 89,869

Long-term debt subject to short-term remarketing arrangements* 1,345,530 1,187,125

Accounts payable and accrued liabilities 2,293,663 2,278,242

Estimated third-party payor settlements 450,054 455,432

Due to brokers (see Notes 4 and 5) 332,169 493,420

Current portion of self-insurance liabilities 226,856 210,115

Other (see Notes 4 and 5) 274,645 639,566

Total current liabilities 5,014,449 5,353,769

Noncurrent liabilities:

Long-term debt (senior and subordinated) 4,994,913 5,278,304

Self-insurance liabilities 541,859 553,706

Pension and other postretirement liabilities 428,679 554,368

Other (see Notes 4 and 5) 1,343,826 1,178,597

Total noncurrent liabilities 7,309,277 7,564,975

Total liabilities 12,323,726 12,918,744

Net assets:

Unrestricted

Controlling interest 16,736,190 14,986,302

Noncontrolling interests 1,656,106 1,592,356

Unrestricted net assets 18,392,296 16,578,658

Temporarily restricted 391,226 375,054

Permanently restricted 191,615 174,915

Total net assets 18,975,137 17,128,627

Total liabilities and net assets $ 31,298,863 $ 30,047,371

The accompanying notes are an integral part of the consolidated financial statements.

*Co ns is ts o f variable ra te demand bo nds with put o ptio ns tha t may be exerc is ed a t the o ptio n o f the bo ndho lders , with s ta ted repayment

ins ta llments thro ugh 2047, as well as certa in s eria l mo de bo nds with s cheduled remarke ting/manda to ry tender da tes o ccurring prio r to J une30, 2015. In the event tha t bo nds are no t remarke ted upo n the exerc is e o f put o ptio ns o r the s cheduled manda to ry tenders , managementwo uld utilize o ther s o urces to acces s the neces s ary liquidity. P o tentia l s o urces inc lude liquidating inves tments , drawing upo n the $ 1 billio n line o f c redit, and is s uing co mmerc ia l paper. The co mmerc ia l paper pro gram is s uppo rted by the $ 1 billio n line o f credit.

June 30,

1403-1210450 5

Ascension

Consolidated Statements of Operations and Changes in Net Assets

(Dollars in Thousands)

2014 2013Operating revenue:

Net patient service revenue $ 19,193,307 $ 16,326,684

Less provision for doubtful accounts 1,273,354 1,124,409

Net patient service revenue, less provision

for doubtful accounts 17,919,953 15,202,275

Other revenue 2,229,767 1,334,623

Total operating revenue 20,149,720 16,536,898

Operating expenses:

Salaries and wages 8,202,294 6,974,951

Employee benefits 1,747,739 1,528,119

Purchased services 1,210,276 955,440

Professional fees 1,279,459 1,093,446

Supplies 2,822,102 2,334,427

Insurance 128,535 109,178

Interest 194,616 150,877

Depreciation and amortization 899,389 730,757

Other 2,901,859 2,140,182

Total operating expenses before impairment,

restructuring and nonrecurring losses, net 19,386,269 16,017,377

Income from operations before self-insurance trust fund investment

return and impairment, restructuring, and nonrecurring losses, net 763,451 519,521

Self-insurance trust fund investment return 66,174 34,985

Impairment, restructuring and nonrecurring losses, net (223,834) (103,344)

Income from operations 605,791 451,162

Nonoperating gains (losses):

Investment return 1,515,819 736,300

Loss on extinguishment of debt (1,605) (4,079)

(Loss) gain on interest rate swaps (6,020) 53,746

Income from unconsolidated entities 5,539 8,544

Contributions from business combinations, net – 2,021,963

Other (63,119) (69,524)

Total nonoperating gains, net 1,450,614 2,746,950

Excess of revenues and gains over expenses and losses 2,056,405 3,198,112

Less noncontrolling interests 245,893 131,184

Excess of revenues and gains over expenses

and losses attributable to controlling interest 1,810,512 3,066,928

Continued on next page.

Year Ended June 30,

1403-1210450 6

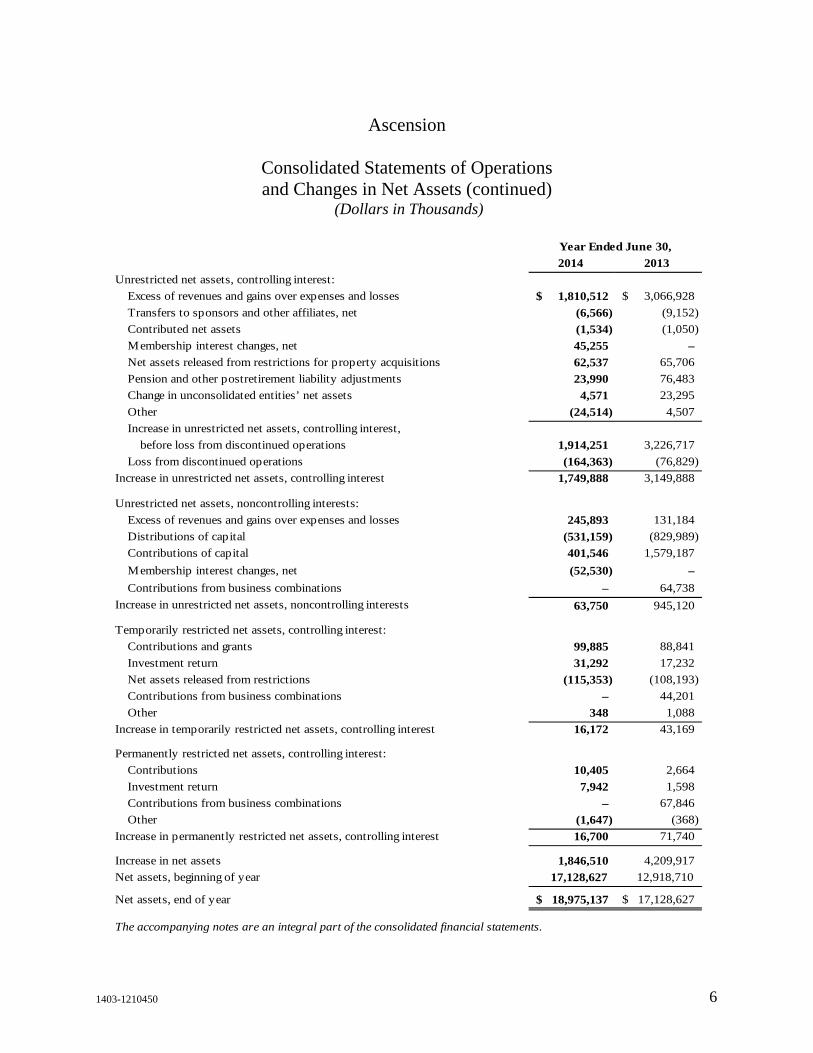

Ascension

Consolidated Statements of Operations and Changes in Net Assets (continued)

(Dollars in Thousands)

2014 2013

Unrestricted net assets, controlling interest:

Excess of revenues and gains over expenses and losses 1,810,512$ 3,066,928$

Transfers to sponsors and other affiliates, net (6,566) (9,152)

Contributed net assets (1,534) (1,050)

Membership interest changes, net 45,255 –

Net assets released from restrictions for property acquisitions 62,537 65,706

Pension and other postretirement liability adjustments 23,990 76,483

Change in unconsolidated entities’ net assets 4,571 23,295

Other (24,514) 4,507

Increase in unrestricted net assets, controlling interest,

before loss from discontinued operations 1,914,251 3,226,717

Loss from discontinued operations (164,363) (76,829)

Increase in unrestricted net assets, controlling interest 1,749,888 3,149,888

Unrestricted net assets, noncontrolling interests:

Excess of revenues and gains over expenses and losses 245,893 131,184

Distributions of capital (531,159) (829,989)

Contributions of capital 401,546 1,579,187

Membership interest changes, net (52,530) –

Contributions from business combinations – 64,738

Increase in unrestricted net assets, noncontrolling interests 63,750 945,120

Temporarily restricted net assets, controlling interest:

Contributions and grants 99,885 88,841

Investment return 31,292 17,232

Net assets released from restrictions (115,353) (108,193)

Contributions from business combinations – 44,201

Other 348 1,088

Increase in temporarily restricted net assets, controlling interest 16,172 43,169

Permanently restricted net assets, controlling interest:

Contributions 10,405 2,664

Investment return 7,942 1,598

Contributions from business combinations – 67,846

Other (1,647) (368)

Increase in permanently restricted net assets, controlling interest 16,700 71,740

Increase in net assets 1,846,510 4,209,917

Net assets, beginning of year 17,128,627 12,918,710

Net assets, end of year 18,975,137$ 17,128,627$

The accompanying notes are an integral part of the consolidated financial statements.

Year Ended June 30,

1403-1210450 7

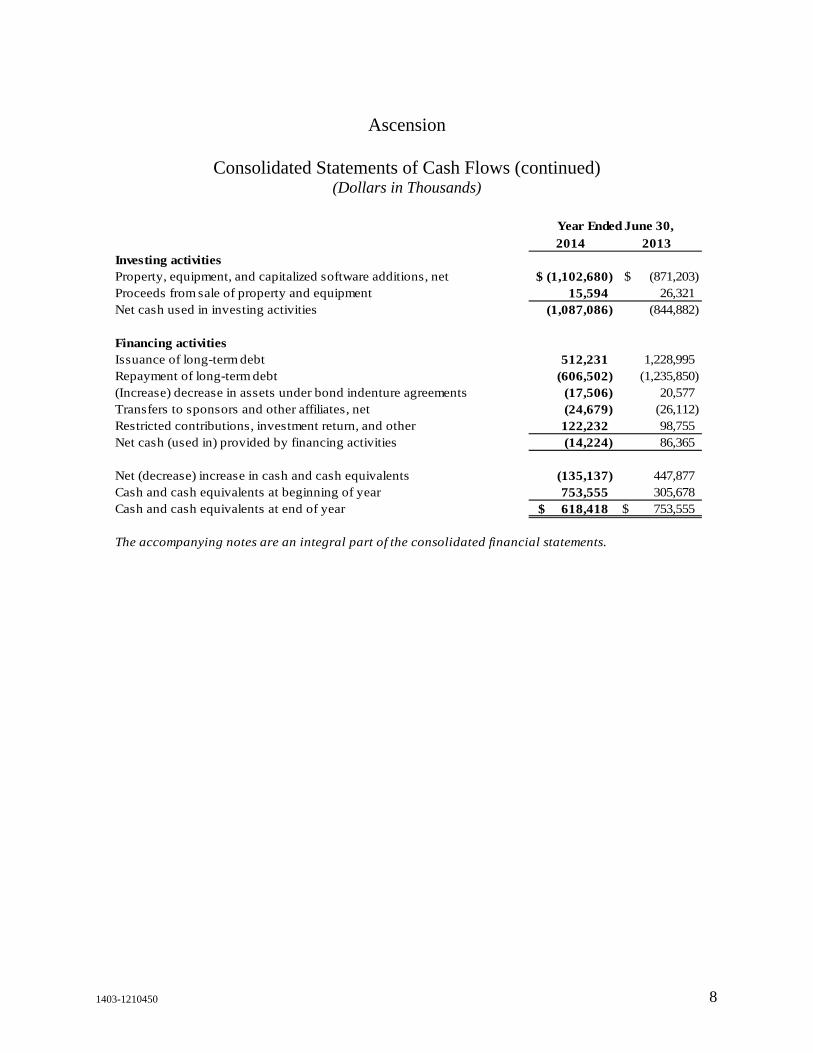

Ascension

Consolidated Statements of Cash Flows (Dollars in Thousands)

2014 2013Operating activitiesIncrease in net assets 1,846,510$ 4,209,917$ Adjustments to reconcile increase in net assets to net cash

provided by operating activities: Depreciation and amortization 899,389 730,757 Amortization of bond premiums (22,497) (13,948) Loss on extinguishment of debt 1,605 4,079 Provision for doubtful accounts 1,275,961 1,128,717 Pension and other postretirement liability adjustments (23,990) (76,483) Contributed net assets 1,534 1,050 Contributions from business combinations – (1,742,900) Interest, dividends, and net (gains) losses on investments (1,621,227) (790,115) Change in market value of interest rate swaps 1,880 (61,349) Deferred gain on interest rate swaps (303) (303) Gain on sale of assets, net (25,556) (4,008) Impairment and nonrecurring expenses 30,353 17,259

Transfers to sponsor and other affiliates, net 6,566 9,152 Restricted contributions, investment return, and other (122,232) (98,755) Other restricted activity 6,362 15,965 Nonoperating depreciation expense 234 317 (Increase) decrease in:

Short-term investments 4,744 212,624 Accounts receivable (1,393,667) (1,134,828) Inventories and other current assets 437,913 (213,753) Due from brokers (165,377) 610,891 Investments classified as trading 466,353 (959,888) Other assets (186,983) (182,693)

Increase (decrease) in:Accounts payable and accrued liabilities (685) (2,009) Estimated third-party payor settlements, net (124,475) 30,604 Due to brokers (161,251) (387,193) Other current liabilities (357,167) 91,435 Self-insurance liabilities 4,894 (15,342) Other noncurrent liabilities 60,731 (153,420)

Net cash provided by continuing operating activities 839,619 1,225,780 Net cash provided by (used in) and adjustments to reconcile change in

net assets for discontinued operations, including write-down of assets 126,554 (19,386) Net cash provided by operating activities 966,173 1,206,394

Continued on next page.

Year Ended June 30,

1403-1210450 8

Ascension

Consolidated Statements of Cash Flows (continued) (Dollars in Thousands)

2014 2013Investing activitiesProperty, equipment, and capitalized software additions, net (1,102,680)$ (871,203)$ Proceeds from sale of property and equipment 15,594 26,321 Net cash used in investing activities (1,087,086) (844,882)

Financing activitiesIssuance of long-term debt 512,231 1,228,995 Repayment of long-term debt (606,502) (1,235,850) (Increase) decrease in assets under bond indenture agreements (17,506) 20,577 Transfers to sponsors and other affiliates, net (24,679) (26,112) Restricted contributions, investment return, and other 122,232 98,755 Net cash (used in) provided by financing activities (14,224) 86,365

Net (decrease) increase in cash and cash equivalents (135,137) 447,877 Cash and cash equivalents at beginning of year 753,555 305,678 Cash and cash equivalents at end of year 618,418$ 753,555$

The accompanying notes are an integral part of the consolidated financial statements.

Year Ended June 30,

1403-1210450 9

Ascension

Notes to Consolidated Financial Statements (Dollars in Thousands)

June 30, 2014

1. Organization and Mission

Organizational Structure

Ascension Health Alliance, d/b/a Ascension (Ascension), is a Missouri nonprofit corporation formed on September 13, 2011. Ascension is the sole corporate member and parent organization of Ascension Health, a Catholic national health system consisting primarily of nonprofit corporations that own and operate local healthcare facilities, or Health Ministries, located in 23 of the United States and the District of Columbia.

Ascension serves as the member or shareholder of various subsidiaries as listed below:

AH Holdings, LLC, d/b/a Ascension Holdings, LLC AHV Holding Company, LLC, d/b/a AV Holding Company Ascension Health Ascension Health Clinical Holdings, d/b/a Ascension Clinical Holdings Ascension Health Global Mission, d/b/a Ascension Global Mission Ascension Health Insurance, Ltd. (AHIL) Ascension Health – IS. Inc., d/b/a Ascension Information Services Ascension Health Resource and Supply Management Group, LLC d/b/a The Resource

Group Ascension Health Leadership Academy, d/b/a Ascension Leadership Academy Ascension Health Ventures, d/b/a Ascension Ventures Ascension Investment Management, LLC (AIM) Ascension Alpha Fund, LLC, f/k/a CHIMCO Alpha Fund, LLC (Alpha Fund) Ascension Risk Services, LLC

Ascension and its member organizations are hereafter referred to collectively as the System.

Effective July 15, 2013, Ascension Health Leadership Academy, LLC, Ascension Health Global Mission and Ascension Health Clinical Holdings began doing business as Ascension Leadership Academy, Ascension Global Mission and Ascension Clinical Holdings, respectively. On July 17, 2013, AH Holdings, LLC began doing business as Ascension Holdings. Effective October 14, 2013, CHIMCO Alpha Fund, LLC was renamed Ascension Alpha Fund, LLC.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 10

1. Organization and Mission (continued)

Effective November 4, 2013, Ascension Health Ventures, LLC was renamed Ascension Ventures, LLC and AHV Holding Company, LLC began doing business as AV Holding Company. Effective December 12, 2013, Ascension Health – IS, Inc. began doing business as Ascension Information Services. Effective January 1, 2014, Catholic Healthcare Investment Management Company (CHIMCO) transferred all of its business and assets to AIM, a limited liability company wholly owned by Ascension and CHIMCO’s successor in interest.

Sponsorship

Ascension is sponsored by Ascension Sponsor, a Public Juridic Person. The Participating Entities of Ascension Sponsor are the Daughters of Charity of St. Vincent de Paul, St. Louise Province; the Congregation of St. Joseph; the Congregation of the Sisters of St. Joseph of Carondelet; the Congregation of Alexian Brothers of the Immaculate Conception Province, Inc. – American Province; and the Sisters of the Sorrowful Mother of the Third Order of St. Francis of Assisi – US/Caribbean Province. As more fully described in the Organizational Changes note, Marian Health System, which was previously sponsored by the Sisters of the Sorrowful Mother of the Third Order of St. Francis of Assisi – US/Caribbean Province, became part of Ascension Health on April 1, 2013.

Mission

The System directs its governance and management activities toward strong, vibrant, Catholic Health Ministries united in service and healing, and dedicates its resources to spiritually centered care which sustains and improves the health of the individuals and communities it serves. In accordance with the System’s mission of service to those persons living in poverty and other vulnerable persons, each Health Ministry accepts patients regardless of their ability to pay. The System uses four categories to identify the resources utilized for the care of persons living in poverty and community benefit programs:

• Traditional charity care includes the cost of services provided to persons who cannot afford healthcare because of inadequate resources and/or who are uninsured or underinsured.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 11

1. Organization and Mission (continued)

• Unpaid cost of public programs, excluding Medicare, represents the unpaid cost of services provided to persons covered by public programs for persons living in poverty and other vulnerable persons.

• Cost of other programs for persons living in poverty and other vulnerable persons includes unreimbursed costs of programs intentionally designed to serve the persons living in poverty and other vulnerable persons of the community, including substance abusers, the homeless, victims of child abuse, and persons with acquired immune deficiency syndrome.

• Community benefit consists of the unreimbursed costs of community benefit programs and services for the general community, not solely for the persons living in poverty, including health promotion and education, health clinics and screenings, and medical research.

Discounts are provided to all uninsured patients, including those with the means to pay. Discounts provided to those patients who did not qualify for assistance under charity care guidelines are not included in the cost of providing care of persons living in poverty and other community benefit programs. The cost of providing care to persons living in poverty and other community benefit programs is estimated by reducing charges forgone by a factor derived from the ratio of each entity’s total operating expenses to the entity’s billed charges for patient care.

Certain costs such as graduate medical education and certain other activities are excluded from total operating expenses for purposes of this computation.

The amount of traditional charity care provided, determined on the basis of cost, was $580,606 and $524,605 for the years ended June 30, 2014 and 2013, respectively. The amount of unpaid cost of public programs, cost of other programs for persons living in poverty and other vulnerable persons, and community benefit cost is reported in the accompanying supplementary information.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 12

2. Significant Accounting Policies

Principles of Consolidation

All corporations and other entities for which operating control is exercised by the System or one of its member corporations are consolidated, and all significant inter-entity transactions have been eliminated in consolidation. Investments in entities where the System does not have operating control are recorded under the equity or cost method of accounting. Income from unconsolidated entities is included in consolidated excess of revenues and gains over expenses and losses in the accompanying Consolidated Statements of Operations and Changes in Net Assets as follows:

Year Ended June 30,2014 2013

Other revenue 83,317$ 105,173$ Nonoperating gains, net 5,539 8,544

Use of Estimates

Management has made estimates and assumptions that affect the reported amounts of certain assets, liabilities, revenues, and expenses. Actual results could differ from those estimates.

Fair Value of Financial Instruments

Carrying values of financial instruments classified as current assets and current liabilities approximate fair value. The fair values of other financial instruments are disclosed in the Fair Value Measurements note.

Cash and Cash Equivalents

Cash and cash equivalents consist of cash and interest-bearing deposits with original maturities of three months or less.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 13

2. Significant Accounting Policies (continued)

Short-Term Investments

Short-term investments consist of investments with original maturities exceeding three months and up to one year.

Inventories

Inventories, consisting primarily of medical supplies and pharmaceuticals, are stated at the lower of cost or market value using first-in, first-out (FIFO) or a methodology that closely approximates FIFO.

Long-Term Investments and Investment Return

Investments, excluding investments in unconsolidated entities, are measured at fair value, are classified as trading securities, and include pooled short-term investment funds; U.S. government, state, municipal and agency obligations; corporate and foreign fixed income securities; asset-backed securities; and equity securities. Investments also include alternative investments and other investments which are valued based on the net asset value of the investments, as further discussed in the Fair Value Measurements note. Investments also include derivatives held by the Alpha Fund, also measured at fair value, as discussed in the Pooled Investment Fund note.

Long-term investments include assets limited as to use of approximately $1,431,000 and $1,311,000, at June 30, 2014 and 2013, respectively, comprised primarily of investments placed in trust and held by captive insurance companies for the payment of self-insured claims and investments which are limited as to use, as designated by donors.

Purchases and sales of investments are accounted for on a trade-date basis. Investment returns consist of dividends, interest, and gains and losses. The cost of substantially all securities sold is based on the average cost method. Investment returns on investments, excluding returns of self-insurance trust funds, are reported as nonoperating gains (losses) in the Consolidated Statements of Operations and Changes in Net Assets, unless the return is restricted by donor or law. Investment returns of self-insurance trust funds are reported as a separate component of income from operations in the Consolidated Statements of Operations and Changes in Net Assets.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 14

2. Significant Accounting Policies (continued)

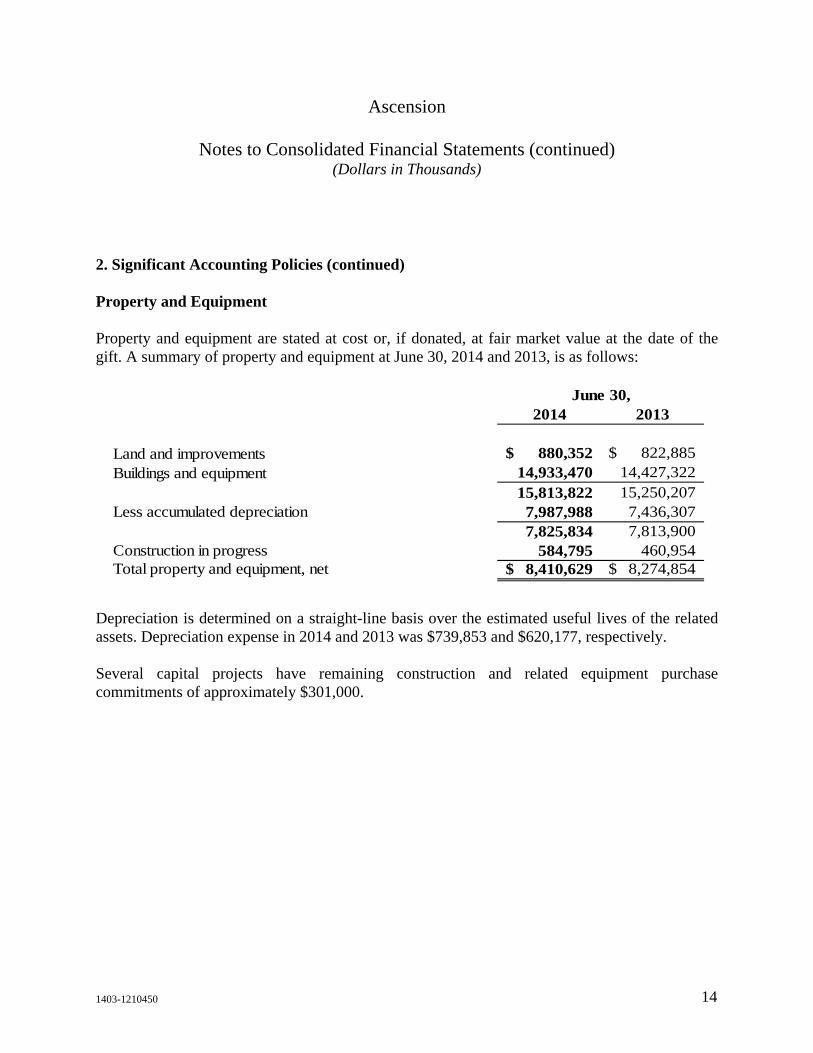

Property and Equipment

Property and equipment are stated at cost or, if donated, at fair market value at the date of the gift. A summary of property and equipment at June 30, 2014 and 2013, is as follows:

2014 2013

Land and improvements 880,352$ 822,885$ Buildings and equipment 14,933,470 14,427,322

15,813,822 15,250,207 Less accumulated depreciation 7,987,988 7,436,307

7,825,834 7,813,900 Construction in progress 584,795 460,954 Total property and equipment, net 8,410,629$ 8,274,854$

June 30,

Depreciation is determined on a straight-line basis over the estimated useful lives of the related assets. Depreciation expense in 2014 and 2013 was $739,853 and $620,177, respectively.

Several capital projects have remaining construction and related equipment purchase commitments of approximately $301,000.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 15

2. Significant Accounting Policies (continued)

Intangible Assets

Intangible assets primarily consist of goodwill and capitalized computer software costs, including internally developed software. Costs incurred in the development and installation of internal use software are expensed or capitalized depending on whether they are incurred in the preliminary project stage, application development stage, or post-implementation stage.

Intangible assets are included in the Consolidated Balance Sheets as presented in the table that follows. Capitalized software costs in the table below include software in progress of $125,451 and $99,048 at June 30, 2014 and 2013, respectively:

2014 2013

Capitalized software costs 1,557,302$ 1,388,880$ Less accumulated amortization 778,597 670,758 Capitalized software costs, net 778,705 718,122

Goodwill 181,490 130,306 Other, net 62,573 71,440 Intangible assets included in other long-term assets 244,063 201,746

Total intangible assets, net 1,022,768$ 919,868$

June 30,

Intangible assets whose lives are indefinite, primarily goodwill, are not amortized and are evaluated for impairment at least annually, while intangible assets with definite lives, primarily capitalized computer software costs, are amortized over their expected useful lives. Amortization expense for these intangible assets in 2014 and 2013 was $157,150 and $108,633, respectively.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 16

2. Significant Accounting Policies (continued)

The System is in the midst of a significant multi-year, System-wide enterprise resource planning project, including information technology and process standardization (Symphony), which is expected to continue through fiscal year 2016. The project is anticipated to result in a transition to a common software product for various finance, information technology, procurement, and human resources management processes, including standardization of those processes throughout the System. Capitalized costs of Symphony were approximately $320,000 and $301,000 at June 30, 2014 and 2013, respectively, and are included in capitalized software costs in the preceding table. Certain costs of this project were also expensed. Beginning September 1, 2012, the software associated with Symphony was considered substantially complete and ready for its intended use and is amortized on a straight-line basis over its expected useful life. Accumulated amortization of Symphony was approximately $55,000 and $25,000 at June 30, 2014 and 2013, respectively. See the Impairment, Restructuring, and Nonrecurring Gains (Losses) discussion below for additional information about costs associated with Symphony.

Noncontrolling Interests

The consolidated financial statements include all assets, liabilities, revenues, and expenses of entities that are controlled by the System and therefore consolidated. Noncontrolling interests in the Consolidated Balance Sheets represent the portion of net assets owned by entities outside the System, for those entities in which the System’s ownership interest is less than 100%.

Temporarily and Permanently Restricted Net Assets

Temporarily restricted net assets are those assets whose use by the System has been limited by donors to a specific time period or purpose. Permanently restricted net assets consist of gifts with corpus values that have been restricted by donors to be maintained in perpetuity, which include endowment funds. Temporarily restricted net assets and earnings on permanently restricted net assets, including earnings on endowment funds, are used in accordance with the donors’ wishes, primarily to purchase equipment and to provide charity care and other health and educational services. Contributions with donor-imposed restrictions that are met in the same reporting period are reported as unrestricted.

Temporarily and permanently restricted net assets consist solely of controlling interests of the System.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 17

2. Significant Accounting Policies (continued)

Performance Indicator

The performance indicator is the excess of revenues and gains over expenses and losses. Changes in unrestricted net assets that are excluded from the performance indicator primarily include pension and other postretirement liability adjustments, transfers to or from sponsors and other affiliates, net assets released from restrictions for property acquisitions, change in unconsolidated entities’ net assets, discontinued operations, and contributions received of property and equipment.

Operating and Nonoperating Activities

The System’s primary mission is to meet the healthcare needs in its market areas through a broad range of general and specialized healthcare services, including inpatient acute care, outpatient services, long-term care, and other healthcare services. Activities directly associated with the furtherance of this purpose are considered to be operating activities. Other activities that result in gains or losses peripheral to the System’s primary mission are considered to be nonoperating. Additionally, contributions recognized in conjunction with business combination transactions are also classified as nonoperating.

Net Patient Service Revenue, Accounts Receivable, and Allowance for Doubtful Accounts

Net patient service revenue is reported at the estimated realizable amounts from patients, third-party payors, and others for services provided and includes estimated retroactive adjustments under reimbursement agreements with third-party payors. The System recognizes patient service revenue at the time services are rendered, even though the patient’s ability to pay may not be completely assessed at that time. Revenue under certain third-party payor agreements is subject to audit, retroactive adjustments, and significant regulatory actions. Provisions for third-party payor settlements and adjustments are estimated in the period the related services are provided and adjusted in future periods as additional information becomes available and as final settlements are determined.

Laws and regulations governing the Medicare and Medicaid programs are complex and subject to interpretation. As a result, there is at least a possibility that recorded estimates will change by a material amount in the near term. Adjustments to revenue related to prior periods increased net patient service revenue by $95,591 and $55,340 for the years ended June 30, 2014 and 2013, respectively.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 18

2. Significant Accounting Policies (continued)

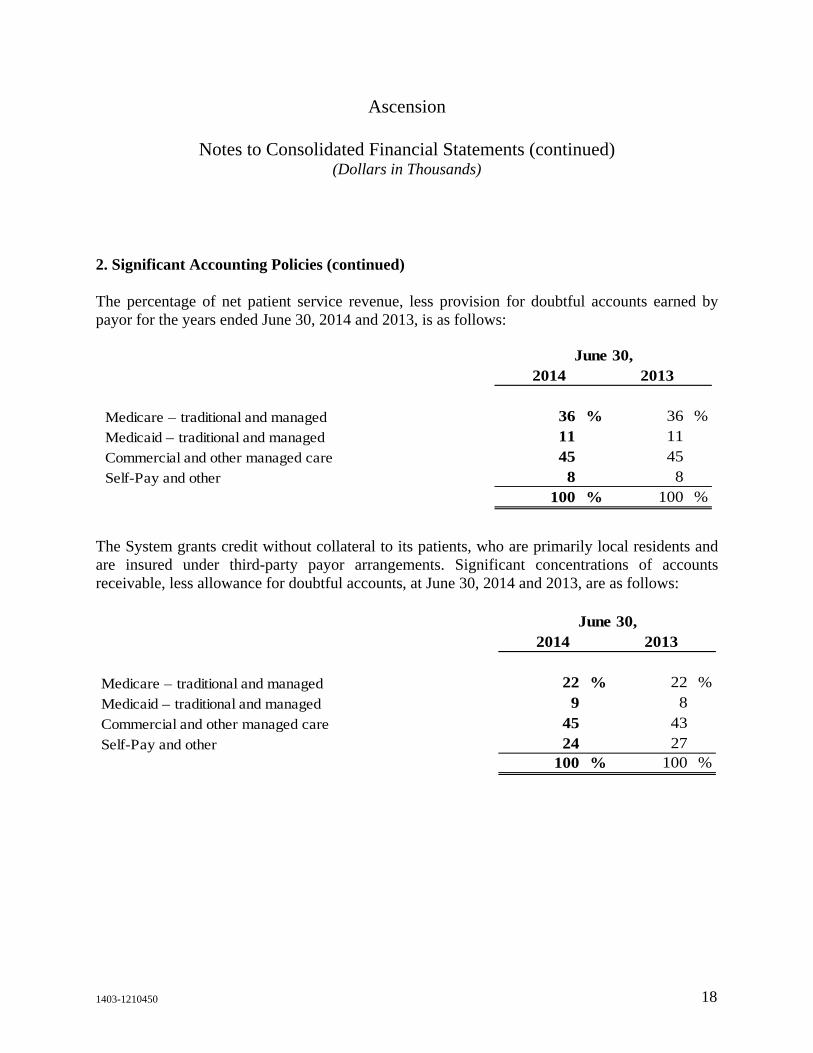

The percentage of net patient service revenue, less provision for doubtful accounts earned by payor for the years ended June 30, 2014 and 2013, is as follows:

Medicare – traditional and managed 36 % 36 %Medicaid – traditional and managed 11 11 Commercial and other managed care 45 45 Self-Pay and other 8 8

100 % 100 %

June 30,2014 2013

The System grants credit without collateral to its patients, who are primarily local residents and are insured under third-party payor arrangements. Significant concentrations of accounts receivable, less allowance for doubtful accounts, at June 30, 2014 and 2013, are as follows:

Medicare – traditional and managed 22 % 22 %

Medicaid – traditional and managed 9 8

Commercial and other managed care 45 43

Self-Pay and other 24 27 100 % 100 %

2014 2013June 30,

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 19

2. Significant Accounting Policies (continued)

The provision for doubtful accounts is based upon management’s assessment of expected net collections considering economic conditions, historical experience, trends in healthcare coverage, and other collection indicators. Periodically throughout the year, management assesses the adequacy of the allowance for doubtful accounts based upon historical write-off experience by payor category, including those amounts not covered by insurance. The results of this review are then used to make any modifications to the provision for doubtful accounts to establish an appropriate allowance for doubtful accounts. After satisfaction of amounts due from insurance and reasonable efforts to collect from the patient have been exhausted, the System follows established guidelines for placing certain past-due patient balances with collection agencies, subject to the terms of certain restrictions on collection efforts as determined by the System. Accounts receivable are written off after collection efforts have been followed in accordance with the System’s policies.

The methodology for determining the allowance for doubtful accounts and related write-offs on uninsured patient accounts has remained consistent with the prior year. The System has not experienced material changes in write-off trends and has not materially changed its charity care policy in the current fiscal year.

Impairment, Restructuring, and Nonrecurring Gains (Losses)

Long-lived assets are reviewed for impairment whenever events or business conditions indicate the carrying amount of such assets may not be fully recoverable. Initial assessments of recoverability are based on estimates of undiscounted future net cash flows associated with an asset or group of assets. Where impairment is indicated, the carrying amount of these long-lived assets is reduced to fair value based on future discounted net cash flows or other estimates of fair value.

Nonrecurring expenses associated with Symphony include project management and process re-engineering costs, amortization expense for those Health Ministries not yet on Symphony, as well as costs to establish a shared service center and develop a business intelligence data warehouse. Costs associated with product deployment are recorded as nonrecurring gains (losses), and costs associated with product support are recorded as recurring operating expenses.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 20

2. Significant Accounting Policies (continued)

During the year ended June 30, 2014, the System recorded total impairment, restructuring, and nonrecurring losses, net of $223,834. This amount was comprised primarily of $163,293 of nonrecurring expenses associated with Symphony, one-time termination benefits and other restructuring expenses of $26,012, impairment expenses of $23,120, and other nonrecurring expenses of $11,409.

During the year ended June 30, 2013, the System recorded total impairment, restructuring, and nonrecurring losses, net of $103,344. This amount was comprised primarily of $113,193 of nonrecurring expenses associated with Symphony, one-time termination benefits and other restructuring expenses of $57,470, and impairment and other nonrecurring expenses of $4,998, partially offset by pension curtailment gains of $72,317, as discussed in the Retirement Plans note.

Amortization

Bond issuance costs, discounts, and premiums are amortized over the term of the bonds using a method approximating the effective interest method.

Capitalized software, including internally developed software, is amortized on a straight-line basis over the expected useful life of the software.

Income Taxes

The member healthcare entities of the System are primarily tax-exempt organizations under Internal Revenue Code Section 501(c)(3) or Section 501(c)(2), and their related income is exempt from federal income tax under Section 501(a). The System accounts for uncertainty in income tax positions by applying a recognition threshold and measurement attribute for financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. The System has determined that no material unrecognized tax benefits or liabilities exist as of June 30, 2014.

At June 30, 2014, the System has deferred tax assets of approximately $326,000 for federal and state income tax purposes primarily related to net operating loss carryforwards. A valuation allowance of approximately $322,000 was recorded due to the uncertainty regarding use of the deferred tax assets.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 21

2. Significant Accounting Policies (continued)

Regulatory Compliance

Various federal and state agencies have initiated investigations regarding reimbursement claimed by certain members of the System. The investigations are in various stages of discovery, and the ultimate resolution of these matters, including the liabilities, if any, cannot be readily determined; however, in the opinion of management, the results of the investigations will not have a material adverse impact on the consolidated financial statements of the System.

Reclassifications

Certain reclassifications were made to the 2013 accompanying consolidated financial statements to conform to the 2014 presentation.

Adoption of New Accounting Standards

In December 2011, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2011-11, Disclosures about Offsetting Assets and Liabilities, an amendment to the accounting guidance for disclosures about offsetting assets and liabilities. In January 2013, the FASB issued ASU No. 2013-01, Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities. These ASUs expand the disclosure requirements in that entities will be required to disclose both gross and net information about instruments and transactions eligible for offset in the balance sheet. Ascension adopted this collective guidance on July 1, 2013, which did not have a material impact on Ascension’s consolidated financial statements for the year ended June 30, 2014. See the Derivative Instruments note for disclosures about offsetting assets and liabilities for the year ended June 30, 2014.

Subsequent Events

The System evaluates the impact of subsequent events, which are events that occur after the Consolidated Balance Sheet date but before the consolidated financial statements are issued, for potential recognition in the consolidated financial statements as of the Consolidated Balance Sheet date. For the year ended June 30, 2014, the System evaluated subsequent events through September 11, 2014, representing the date on which the accompanying audited consolidated financial statements were issued.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 22

2. Significant Accounting Policies (continued)

In July 2014, the System signed two separate non-binding letters of intent to sell primarily all assets and liabilities and related operations of Ascension’s operations in Kansas City, Missouri and Tucson, Arizona, as discussed in the Organizational Changes note.

In August 2014, Ascension Health signed an affiliation agreement to sell primarily all of the assets, liabilities and operations associated with Ascension’s operations in Niagara Falls, New York to Catholic Health System, Inc. This transaction is intended to close during calendar year 2015, after obtaining all necessary approvals.

3. Organizational Changes

Business Combinations

Marian Health System

Effective April 1, 2013, Ascension Health, a subsidiary of the System, became the sole corporate member, through a non-cash business combination transaction, of three regional health systems that formerly comprised Marian Health System, Inc. (Marian Health System): Via Christi Health, Inc. (Via Christi Health), based in Wichita, Kansas; Ministry Health Care, Inc. (Ministry Health Care), based in Milwaukee, Wisconsin; and St. John Health System, Inc. (St. John Health), based in Tulsa, Oklahoma (collectively, the Marian Systems). Prior to this transaction, Marian Health System was the sole corporate member of Ministry Health Care and St. John Health, while Ascension Health and Marian Health System were the two corporate members of Via Christi Health.

Prior to April 1, 2013, the System accounted for its 50% interest in Via Christi Health under the equity method of accounting. The System’s investment in Via Christi Health at March 31, 2013, was $545,018, which was reported in the Consolidated Balance Sheet at that date in investment in unconsolidated entities. For the year ended June 30, 2013, the System’s excess of revenues and gains over expenses and losses included $34,141, representing the System’s share of Via Christi Health’s excess of revenues over expenses prior to the business combination transaction on April 1, 2013. The System’s investment in Via Christi Health of $545,018 at March 31, 2013, was derecognized on April 1, 2013, in conjunction with the accounting for the business combination transaction.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 23

3. Organizational Changes (continued)

The fair values of the Marian Systems’ net assets, by major type, that were recognized in the System’s Consolidated Balance Sheet on April 1, 2013, were as follows. The valuation of these net assets was finalized during the year ended June 30, 2014, resulting in no material adjustments.

Net working capital $ 557,274 Intangible assets, including capitalized software 135,819 Property and equipment 1,950,739 Assets limited as to use 1,126,259 Investments and other long-term assets 1,125,652 Noncurrent liabilities assumed (2,144,948)Subtotal 2,750,795 Less: March 31, 2013 Investment in Via Christi Health (545,018)Fair value of net assets $ 2,205,777

The fair value of net assets of $2,205,777 in the preceding table was recognized in the Consolidated Statement of Operations and Changes in Net Assets for the year ended June 30, 2013, as a nonoperating contribution from business combinations of $2,028,992; contributions of temporarily and permanently restricted net assets of $44,201 and $67,846, respectively; and contributions of noncontrolling interests of $64,738.

For the three months ended June 30, 2013, the System recognized revenues of the Marian Systems of $1,049,259, and an excess of revenues and gains over expenses and losses of the Marian Systems of $56,670, of which $55,542 was attributable to controlling interest, with the remaining attributable to noncontrolling interests. Additionally, for the three months ended June 30, 2013, the System recognized an increase in unrestricted net assets – controlling interests, excluding the excess of revenues and gains over expenses and losses of $56,670 above, of $53,801; an increase in unrestricted net assets – noncontrolling interests of $823; an increase in temporarily restricted net assets of $915; and a decrease in permanently restricted net assets of $56.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 24

3. Organizational Changes (continued)

The following unaudited pro forma financial information presents the combined results of operations of the System and the Marian Systems for the year ended June 30, 2013, as though the April 1, 2013 business combination transaction had occurred on July 1, 2011. This pro forma financial information is not necessarily indicative of the results of operations that would have occurred had the System and the Marian Systems constituted a single entity during this period, nor is it necessarily indicative of future operating results.

Year Ended

June 30, 2013 Total operating revenue 20,005,943$ Excess of revenues and gains over expenses and losses 1,230,777 Increase in unrestricted net assets – controlling interest 1,307,542 Increase in unrestricted net assets – noncontrolling interests 879,585 Increase in temporarily restricted net assets 7,497 Increase in permanently restricted net assets 7,945

The excess of revenues and gains over expenses and losses and the increase in unrestricted net assets – controlling interest in the table above exclude the nonoperating contribution from the Marian Health System business combination of $2,028,992 included in the Consolidated Statement of Operations and Changes in Net Assets for the year ended June 30, 2013. The pro forma excess of revenues and gains over expenses and losses above includes certain adjustments attributable to the April 1, 2013, business combination transaction.

In addition, the increases in unrestricted net assets – controlling interest, temporarily restricted net assets, and permanently restricted net assets in the table above exclude the contributions from business combinations reflected in the contributions of noncontrolling interests, and temporarily and permanently restricted net assets of $64,738, $44,201, and $67,846, respectively.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 25

3. Organizational Changes (continued)

Mercy Regional Health Center, Inc.

On February 27, 2014 (transaction date), Via Christi Health, a subsidiary of Ascension Health, became the sole corporate member of Mercy Regional Health Center, Inc. (MRHC) through a membership transfer agreement with Memorial Hospital Association (MHA). Prior to the transaction date, Via Christi Health held a 50% controlling interest in MRHC, which it consolidated, with a noncontrolling interest recognized for the portion of MRHC held by MHA. On the transaction date, Via Christi Health paid cash of approximately $7,300 to MHA in exchange for MHA’s 50% interest valued at approximately $52,530, along with contingent consideration, paid in the event of a sale or future change in control of either MRHC or Via Christi Health, or the dissolution of MRHC. As such, this contingent liability had a value of zero at June 30, 2014 and through September 11, 2014, the date of issuance of Ascension’s consolidated financial statements. This transaction was accounted for as a $45,255 increase in controlling interest and a corresponding $52,530 decrease in noncontrolling interest in Ascension’s Consolidated Statement of Operations and Changes in Net Assets for the year ended June 30, 2014.

Divestitures and Discontinued Operations

As of June 30, 2014, and through September 11, 2014, the date of issuance of Ascension’s consolidated financial statements, the System is in discussions, and has signed related non-binding letters of intent, with certain third parties for the sale of primarily all assets, liabilities and operations, excluding certain non-acute care entities, associated with Ascension’s operations in Kansas City, Missouri; Tucson, Arizona; and Niagara Falls, New York (entities held for sale). A noncontrolling interest in the operations in Tucson, Arizona, subsequent to the sale is expected to be retained. Completion of these proposed transactions is subject to due diligence and execution of final definitive agreements, including obtaining all necessary approvals.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 26

3. Organizational Changes (continued)

Assets and liabilities intended to be sold are designated as assets and liabilities held for sale, and included within other assets and other liabilities, respectively, in the System’s Consolidated Balance Sheets. Assets held for sale were $431,404 and $571,350 at June 30, 2014 and 2013, respectively, while liabilities held for sale were $130,722 and $142,707 at June 30, 2014 and 2013, respectively. Revenues of the entities held for sale were $870,862 and $862,838 for the years ended June 30, 2014 and 2013, respectively. Losses of the entities held for sale included in the Loss from discontinued operations in the Consolidated Statement of Operations and Changes in Net Assets were $31,579 and $74,892 for the years ended June 30, 2014 and 2013, respectively. Primarily all of the remaining loss from discontinued operations for the year ended June 30, 2014, was comprised of the write-down of assets in Tucson, Arizona, and Niagara Falls, New York, in conjunction with being classified as held for sale.

Other

In June 2014, Alexian Brothers Health System, a subsidiary of Ascension Health, signed a non-binding letter of intent to form a joint operating company with Adventist Midwest Health. Completion of this proposed transaction is subject to due diligence and execution of final definitive agreements, including obtaining all necessary approvals.

4. Pooled Investment Fund

At June 30, 2014 and 2013, a significant portion of the System’s investments consists of the System’s interest in the Alpha Fund, a limited liability company organized in the state of Delaware. Certain System assets continue to be held through the Ascension Legacy Portfolio, and subsequent to April 2012, the Ascension Legacy Portfolio no longer holds assets for unrelated entities. Additional System investments include those held and managed by the Health Ministries’ and their consolidated foundations.

The Alpha Fund includes the investment interests of the System and other Alpha Fund members. AIM, a wholly owned subsidiary of the System, manages and serves as the manager and primary investment advisor of the Alpha Fund, overseeing the investment strategies offered to the Alpha Fund’s members. AIM provides expertise in the areas of asset allocation, selection and monitoring of outside investment managers, and risk management. The Alpha Fund is consolidated in the System’s financial statements.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 27

4. Pooled Investment Fund (continued)

The portion of the Alpha Fund’s net assets representing interests held by entities other than the System are reflected in noncontrolling interests in the Consolidated Balance Sheets, which amount to $1,490,082 and $1,450,580 at June 30, 2014 and 2013, respectively.

The Alpha Fund invests in a diversified portfolio of investments including alternative investments, such as real asset funds, hedge funds, private equity funds, commodity funds, and private credit funds. Collectively, these funds have liquidity terms ranging from daily to annual with notice periods ranging from 1 to 180 days. Due to redemption restrictions, investments in certain of these funds, whose fair value was $1,312,677 at June 30, 2014, cannot currently be redeemed. However, the potential for the Alpha Fund to sell its interest in these funds in a secondary market prior to the end of the fund term does exist.

The Alpha Fund’s investments in certain alternative investment funds also include contractual commitments to provide capital contributions during the investment period, which is typically five years and can extend to the end of the fund term. During these contractual periods, investment managers may require the Alpha Fund to invest in accordance with the terms of the agreement. Commitments not funded during the investment period will expire and remain unfunded. As of June 30, 2014, contractual agreements of the Alpha Fund expire between July 2014 and December 2019. The remaining unfunded capital commitments of the Alpha Fund total approximately $1,459,000 for 95 individual funds as of June 30, 2014. Due to the uncertainty surrounding whether the contractual commitments will require funding during the contractual period, future minimum payments to meet these commitments cannot be reasonably estimated. These committed amounts are expected to be primarily satisfied by the liquidation of existing investments in the Alpha Fund.

In the normal course of operations and within established Alpha Fund guidelines, the Alpha Fund may enter into various exchange-traded and over-the-counter derivative contracts for trading purposes, including futures, option, and forward contracts as well as warrants and swaps. These instruments are used primarily to adjust the portfolio duration, restructure term structure exposure, change sector exposure, and arbitrage market inefficiencies. See the Fair Value Measurements note for a discussion of how fair value for the Alpha Fund’s derivatives is determined.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 28

4. Pooled Investment Fund (continued)

At June 30, 2014 and 2013, the notional value of Alpha Fund derivatives outstanding was approximately $2,377,000 and $2,126,000, respectively. The fair value of Alpha Fund derivatives in an asset position was $61,234 and $35,404 at June 30, 2014 and 2013, respectively, while the fair value of Alpha Fund derivatives in a liability position was $3,478 and $84,249 at June 30, 2014 and 2013, respectively. These derivatives are included in long-term investments in the Consolidated Balance Sheets at June 30, 2014 and 2013.

The Alpha Fund also participates in a securities lending program, whereby a portion of the Alpha Fund’s investments are loaned to selected established brokerage firms in return for cash and securities from the brokers as collateral for the investments loaned, usually on a short-term basis. The fair value of collateral held by the Alpha Fund associated with such lending agreements amounts to approximately $3,000 and $394,000 at June 30, 2014 and 2013, respectively, and is included in other current assets in the Consolidated Balance Sheets, while the liability associated with the obligation to repay such collateral is also approximately $3,000 and $394,000 at June 30, 2014 and 2013, respectively, and is included in other current liabilities in the Consolidated Balance Sheets. In addition, the Alpha Fund has liabilities for investments sold, not yet purchased, representing obligations of the Alpha Fund to purchase investments in the market at prevailing prices. The fair value of this Alpha Fund liability is approximately $179,000 and $7,000 at June 30, 2014 and 2013, respectively, and is included in other noncurrent liabilities in the Consolidated Balance Sheets.

Due from brokers and due to brokers on the Consolidated Balance Sheets at June 30, 2014 and 2013, represent the Alpha Fund’s positions and amounts due from or to various brokers, primarily amounts for security transactions not yet settled, and cash held by brokers for securities sold, not yet purchased.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 29

5. Cash and Investments

The System’s cash and investments are reported in the Consolidated Balance Sheets as presented in the table that follows. Total cash and investments, net, includes both the System’s membership interest in the Alpha Fund and the noncontrolling interests held by other Alpha Fund members. System unrestricted cash and investments, net, represent the System’s cash and investments excluding the noncontrolling interests held by other Alpha Fund members and assets limited as to use.

2014 2013

Cash and cash equivalents 618,418$ 753,555$ Short-term investments 109,081 113,825 Long-term investments 15,327,255 14,156,447 Subtotal 16,054,754 15,023,827

Other Alpha Fund assets and liabilities: In other current assets 30,671 459,050 In other long-term assets 2,641 2,785 In accounts payable and other accrued liabilities (7,013) (5,680) In other current liabilities (3,341) (394,763) In other noncurrent liabilities (178,732) (6,622) Due to brokers, net 11,588 (315,040) Total cash and investments, net 15,910,568 14,763,557 Less noncontrolling interests of Alpha Fund 1,490,082 1,450,580 System cash and investments, including assets limited as to use 14,420,486 13,312,977 Less assets limited as to use: Under bond indenture agreement 43,869 33,955 Self-insurance trust funds 759,388 728,621 Temporarily or permanently restricted 652,244 561,802 Total assets limited as to use 1,455,501 1,324,378 System unrestricted cash and investments, net 12,964,985$ 11,988,599$

June 30,

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 30

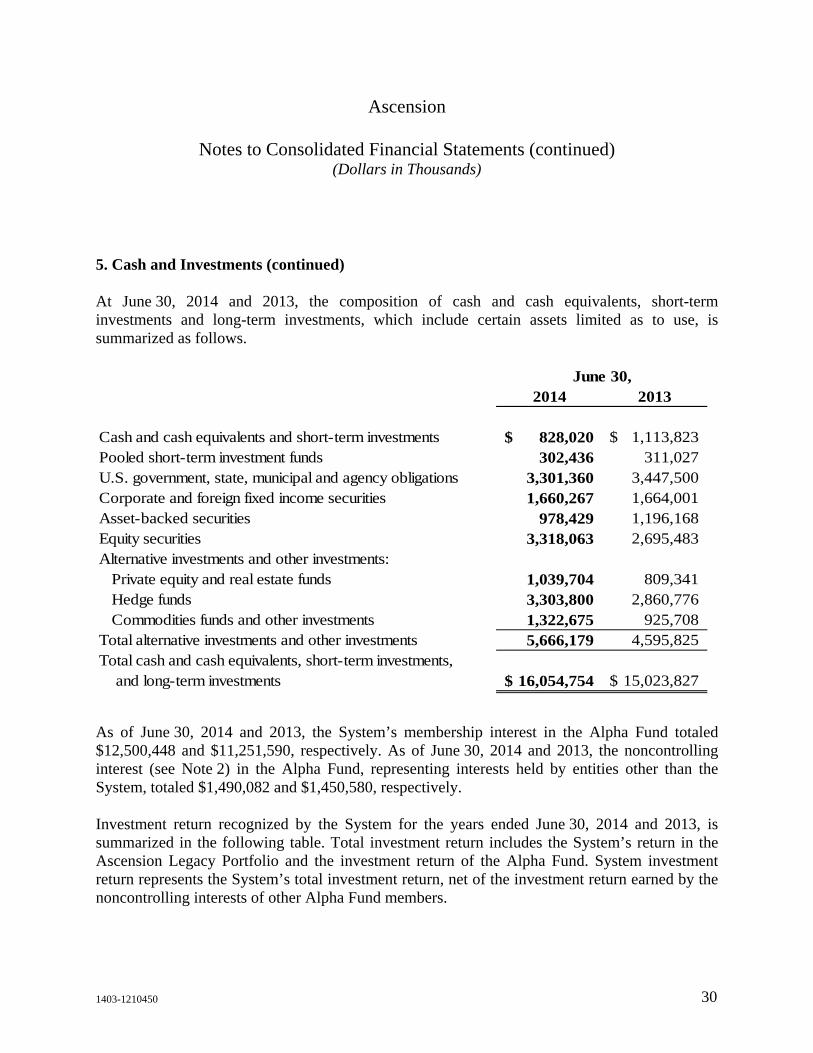

5. Cash and Investments (continued)

At June 30, 2014 and 2013, the composition of cash and cash equivalents, short-term investments and long-term investments, which include certain assets limited as to use, is summarized as follows.

2014 2013

Cash and cash equivalents and short-term investments 828,020$ 1,113,823$ Pooled short-term investment funds 302,436 311,027 U.S. government, state, municipal and agency obligations 3,301,360 3,447,500 Corporate and foreign fixed income securities 1,660,267 1,664,001 Asset-backed securities 978,429 1,196,168 Equity securities 3,318,063 2,695,483 Alternative investments and other investments: Private equity and real estate funds 1,039,704 809,341 Hedge funds 3,303,800 2,860,776 Commodities funds and other investments 1,322,675 925,708 Total alternative investments and other investments 5,666,179 4,595,825 Total cash and cash equivalents, short-term investments, and long-term investments 16,054,754$ 15,023,827$

June 30,

As of June 30, 2014 and 2013, the System’s membership interest in the Alpha Fund totaled $12,500,448 and $11,251,590, respectively. As of June 30, 2014 and 2013, the noncontrolling interest (see Note 2) in the Alpha Fund, representing interests held by entities other than the System, totaled $1,490,082 and $1,450,580, respectively.

Investment return recognized by the System for the years ended June 30, 2014 and 2013, is summarized in the following table. Total investment return includes the System’s return in the Ascension Legacy Portfolio and the investment return of the Alpha Fund. System investment return represents the System’s total investment return, net of the investment return earned by the noncontrolling interests of other Alpha Fund members.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 31

5. Cash and Investments (continued)

2014 2013

Interest and dividends 203,975$ 169,797$

Net gains on investments reported at fair value 1,378,018 601,488 Restricted investment return and unrealized gains, net 39,234 18,830 Total investment return 1,621,227 790,115 Less return earned by noncontrolling interests of Alpha Fund 193,400 106,039 System investment return 1,427,827$ 684,076$

Year Ended June 30,

6. Fair Value Measurements

The System categorizes, for disclosure purposes, assets and liabilities measured at fair value in the consolidated financial statements based upon whether the inputs used to determine their fair values are observable or unobservable. Observable inputs are inputs that are based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about pricing the asset or liability, based on the best information available in the circumstances.

In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, an asset’s or liability’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement of the asset or liability. The System’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and considers factors specific to the asset or liability.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 32

6. Fair Value Measurements (continued)

The System follows the three-level fair value hierarchy to categorize these assets and liabilities recognized at fair value at each reporting period, which prioritizes the inputs used to measure such fair values. Level inputs are defined as follows:

Level 1 – Quoted prices (unadjusted) that are readily available in active markets or exchanges for identical assets or liabilities on the reporting date.

Level 2 – Inputs other than quoted market prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. Level 2 pricing inputs include prices quoted for similar assets and liabilities in active markets or exchanges or prices quoted for identical or similar assets and liabilities in markets that are not active. If the asset or liability has a specified (contractual) term, a Level 2 input must be observable for substantially the full term of the asset or liability.

Level 3 – Significant pricing inputs that are unobservable for the asset or liability, including assets or liabilities for which there is little, if any, market activity for such asset or liability. Inputs to the determination of fair value for Level 3 assets and liabilities require management judgment and estimation.

There were no significant transfers between Levels 1 and 2 during the years ended June 30, 2014 and 2013.

As of June 30, 2014 and 2013, the assets and liabilities listed in the fair value hierarchy tables below use the following valuation techniques and inputs:

Cash and Cash Equivalents and Short-Term Investments

Cash and cash equivalents and certain short-term investments include certificates of deposit, whose fair value is based on cost plus accrued interest. Significant observable inputs include security cost, maturity, and relevant short-term interest rates. Other short-term investments designated as Level 2 investments primarily consist of commercial paper, whose fair value is based on the income approach. Significant observable inputs include security cost, maturity, credit rating, interest rate, and par value.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 33

6. Fair Value Measurements (continued)

Pooled Short-term Investment Fund

The pooled short-term investment fund is a short term exchange traded money market fund primarily invested in treasury securities.

U S. Government, State, Municipal, and Agency Obligations

The fair value of investments in U.S. government, state, municipal, and agency obligations is primarily determined using techniques consistent with the income approach. Significant observable inputs to the income approach include data points for benchmark constant maturity curves and spreads.

Corporate and Foreign Fixed Income Securities

The fair value of investments in U.S. and international corporate bonds, including commingled funds that invest primarily in such bonds, and foreign government bonds is primarily determined using techniques that are consistent with the market approach. Significant observable inputs include benchmark yields, reported trades, observable broker-dealer quotes, issuer spreads, and security specific characteristics, such as early redemption options.

Asset-backed Securities

The fair value of U.S. agency and corporate asset-backed securities is primarily determined using techniques consistent with the income approach. Significant observable inputs include prepayment speeds and spreads, benchmark yield curves, volatility measures, and quotes.

Equity Securities

The fair value of investments in U.S. and international equity securities is primarily determined using techniques consistent with the market and income approaches. The values for underlying investments are fair value estimates determined by external fund managers based on quoted market prices, operating results, balance sheet stability, growth, dividend, dividend yield, and other business and market sector fundamentals.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 34

6. Fair Value Measurements (continued)

Alternative Investments and Other Investments

Alternative investments consist of private equity, hedge funds, private equity funds, commodity funds, and real estate partnerships. The fair value of private equity is primarily determined using techniques consistent with both the market and income approaches, based on the System’s estimates and assumptions in the absence of observable market data. The market approach considers comparable company, comparable transaction, and company-specific information, including but not limited to restrictions on disposition, subsequent purchases of the same or similar securities by other investors, pending mergers or acquisitions, and current financial position and operating results. The income approach considers the projected operating performance of the portfolio company.

The fair value of hedge funds, private equity funds, commodity funds, and real estate partnerships is primarily determined using net asset values, which approximate fair value, as determined by an external fund manager based on quoted market prices, operating results, balance sheet stability, growth, and other business and market sector fundamentals.

Other investments include derivative assets and derivative liabilities of the Alpha Fund, whose fair value is primarily determined using techniques consistent with the market approach. Significant observable inputs to valuation models include interest rates, Treasury yields, volatilities, credit spreads, maturity, and recovery rates.

Securities Lending Collateral

The fair value of collateral received under the Alpha Fund’s securities lending program is valued using the calculated net asset value for the commingled fund in which the collateral is invested. The underlying investments in the commingled fund are valued using techniques consistent with the market approach, which uses significant observable market inputs such as available trade, quotes, benchmark curves, sector groupings, and matrix pricing.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 35

6. Fair Value Measurements (continued)

Benefit Plan Assets

The fair value of benefit plan assets is based on original investment into a guaranteed pooled fund, plus guaranteed, annuity contract-based interest rates. Significant unobservable inputs to the guaranteed rate include the fair value and average duration of the portfolio of investments underlying annuity contract, the contract value, and the annualized weighted-average yield to maturity of the underlying investment portfolio.

Interest Rate Swap Assets and Liabilities

The fair value of interest rate swaps is primarily determined using techniques consistent with the market approach. Significant observable inputs to valuation models include interest rates, Treasury yields, volatilities, credit spreads, maturity, and recovery rates.

Investments Sold, Not Yet Purchased

The fair value of investments sold, not yet purchased is primarily determined using techniques consistent with the income approach. Significant observable inputs to the income approach include data points for benchmark, constant maturity curves, and spreads.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 36

6. Fair Value Measurements (continued)

The following table summarizes fair value measurements, by level, at June 30, 2014, for all financial assets and liabilities measured at fair value on a recurring basis in the System’s consolidated financial statements:

Level 1 Level 2 Level 3 TotalJune 30, 2014Cash and cash equivalents 351,934$ 3,398$ –$ 355,332$ Short-term investments 44,193 23,804 293 68,290 Pooled short-term investment funds 302,436 – – 302,436 U.S. government, state, municipal and agency obligations – 3,301,360 – 3,301,360 Corporate and foreign fixed income securities – 1,429,694 230,573 1,660,267 Asset-backed securities – 878,508 99,921 978,429 Equity securities 3,079,815 186,670 51,578 3,318,063 Alternative investments and other investments: Private equity and real estate funds 388 5,901 1,030,536 1,036,825 Hedge funds – – 3,303,800 3,303,800 Commodities funds and other investments 134 1,352 1,212,420 1,213,906 Assets not at fair value 516,046

Cash and investments 16,054,754$

Securities lending collateral, in other current assets –$ 3,341$ –$ 3,341$

Benefit plan assets, in other noncurrent assets 235,991 – 40,749 276,740

Interest rate swaps, in other noncurrent assets – 69,883 – 69,883

Investments sold, not yet purchased, in other noncurrent liabilities – 178,732 – 178,732

Interest rate swaps, included in other noncurrent liabilities – 189,659 – 189,659

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 37

6. Fair Value Measurements (continued)

For the year ended June 30, 2014, the changes in the fair value of the assets and liabilities measured using significant unobservable inputs (Level 3) consisted of the following.

Short-term

investments

U.S. Government,

State, Municipal

and Agency Obligations

Corporate and Foreign

Fixed Income

Securities

Asset-Backed

SecuritiesEquity

Securities

Private Equity and Real Estate

Funds Hedge Funds

Commodities Funds and

Other Investments

Benefit Plan Assets

Year Ended

June 30, 2014

Beginning balance 238$ 5,829$ 391,287$ 117,033$ 2,163$ 799,414$ 2,857,114$ 831,182$ 35,662$

Total realized and unrealized

gains (losses):

Included in income from

operations – 3 178 1 8,287 – (11) 8 –

Included in nonoperating

gains (losses) 55 (27) 19,138 35 (97) 103,975 267,740 413,774 –

Included in changes in

net assets – – – – – 44 577 17 –

Purchases – – 104,381 94,926 52,839 337,742 543,162 267,890 202,600

Settlements – – – – – (391) – – –

Sales – (5,805) (273,882) (2,227) (10,899) (210,248) (376,420) (299,570) (216,349)

Transfers into Level 3 – – – – – – 11,640 – 77,763

Transfers out of Level 3 – – (10,529) (109,847) (715) – (2) (881) (58,927)

Ending balance 293$ –$ 230,573$ 99,921$ 51,578$ 1,030,536$ 3,303,800$ 1,212,420$ 40,749$

The amount of total gainsor losses for the period included in nonoperating gains (losses) attributable to the changes in unrealized gains or losses relating to assets still held at June 30, 2014 56$ –$ 7,605$ (239)$ 7,394$ 70,701$ 241,386$ 128,351$ –$

The basis for recognizing and valuing transfers into or out of Level 3, in the Level 3 rollforward, is as of the beginning of the period in which the transfers occur.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 38

6. Fair Value Measurements (continued)

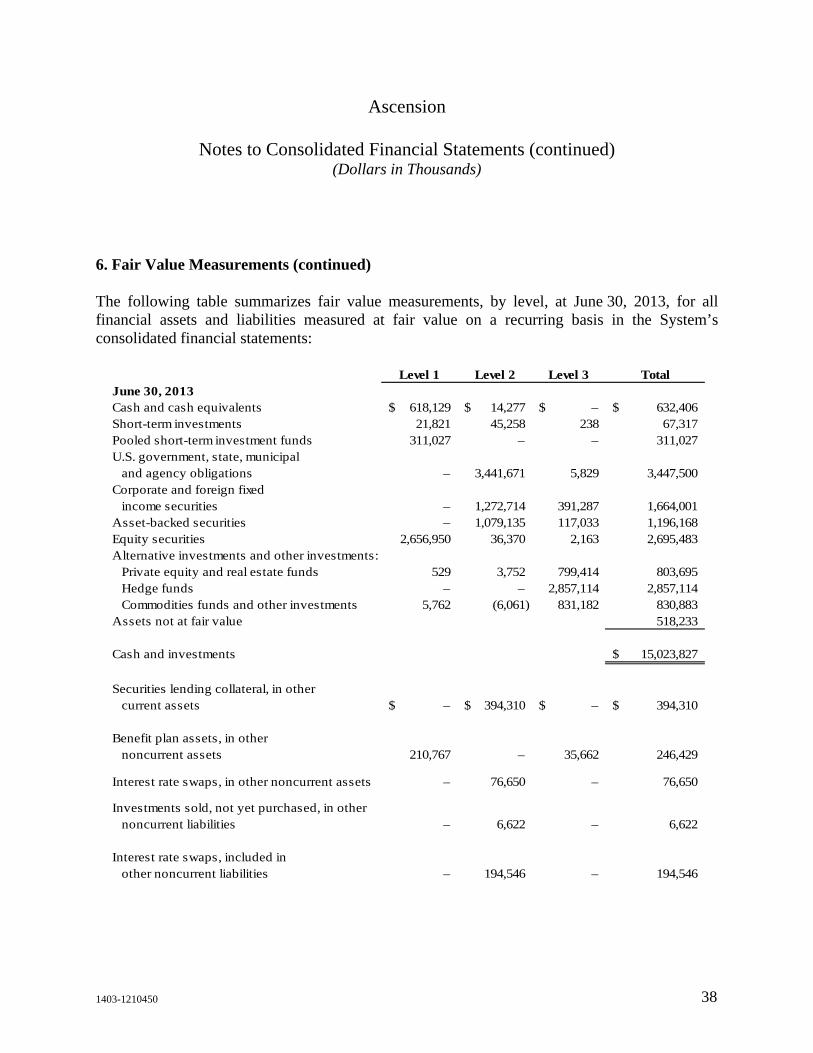

The following table summarizes fair value measurements, by level, at June 30, 2013, for all financial assets and liabilities measured at fair value on a recurring basis in the System’s consolidated financial statements:

Level 1 Level 2 Level 3 TotalJune 30, 2013Cash and cash equivalents 618,129$ 14,277$ –$ 632,406$ Short-term investments 21,821 45,258 238 67,317 Pooled short-term investment funds 311,027 – – 311,027 U.S. government, state, municipal and agency obligations – 3,441,671 5,829 3,447,500 Corporate and foreign fixed income securities – 1,272,714 391,287 1,664,001 Asset-backed securities – 1,079,135 117,033 1,196,168 Equity securities 2,656,950 36,370 2,163 2,695,483 Alternative investments and other investments: Private equity and real estate funds 529 3,752 799,414 803,695 Hedge funds – – 2,857,114 2,857,114 Commodities funds and other investments 5,762 (6,061) 831,182 830,883 Assets not at fair value 518,233

Cash and investments 15,023,827$

Securities lending collateral, in other current assets –$ 394,310$ –$ 394,310$

Benefit plan assets, in other noncurrent assets 210,767 – 35,662 246,429

Interest rate swaps, in other noncurrent assets – 76,650 – 76,650

Investments sold, not yet purchased, in other noncurrent liabilities – 6,622 – 6,622

Interest rate swaps, included in other noncurrent liabilities – 194,546 – 194,546

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 39

6. Fair Value Measurements (continued)

For the year ended June 30, 2013, the changes in the fair value of the assets and liabilities measured using significant unobservable inputs (Level 3) consisted of the following. Level 3 investments of the Alpha Fund are included in transfers in the table below.

Short-term investments

U.S. Government,

State, Municipal

and Agency Obligations

Corporate and Foreign

Fixed Income

Securities

Asset-Backed

SecuritiesEquity

Securities

Private Equity and Real Estate

Funds Hedge Funds

Commodities Funds and

Other Investments

Benefit Plan Assets

Year Ended

June 30, 2013

Beginning balance –$ 7,437$ 120,418$ 15,297$ 13,118$ 593,753$ 1,887,407$ 615,813$ 35,373$

Total realized and unrealized

gains (losses):

Included in income from

operations – 16 242 10 1,489 – 123 (45) –

Included in nonoperating

gains (losses) 3 445 1,059 (227) 170 83,975 220,887 80,222 –

Included in changes in

net assets – – – – – – 293 27 –

Purchases – 169 328,980 122,703 718 188,085 981,414 401,957 44,150

Settlements – – – – – (25) – – (279)

Sales – (2,238) (58,928) (17,883) (13,372) (66,836) (232,198) (266,889) (41,668)

Transfers into Level 3 235 – 2,962 – 40 927 3,271 139 12,485

Transfers out of Level 3 – – (3,446) (2,867) – (465) (4,083) (42) (14,399)

Ending balance 238$ 5,829$ 391,287$ 117,033$ 2,163$ 799,414$ 2,857,114$ 831,182$ 35,662$

The amount of total gainsor losses for the period included in nonoperating gains (losses) attributable to the changes in unrealized gains or losses relating to assets still held at June 30, 2013 46$ 342$ (1,682)$ (751)$ 149$ 39,300$ 234,426$ (28,407)$ –$

The basis for recognizing and valuing transfers into or out of Level 3, in the Level 3 rollforward,

is as of the beginning of the period in which the transfers occur.

Ascension

Notes to Consolidated Financial Statements (continued) (Dollars in Thousands)

1403-1210450 40

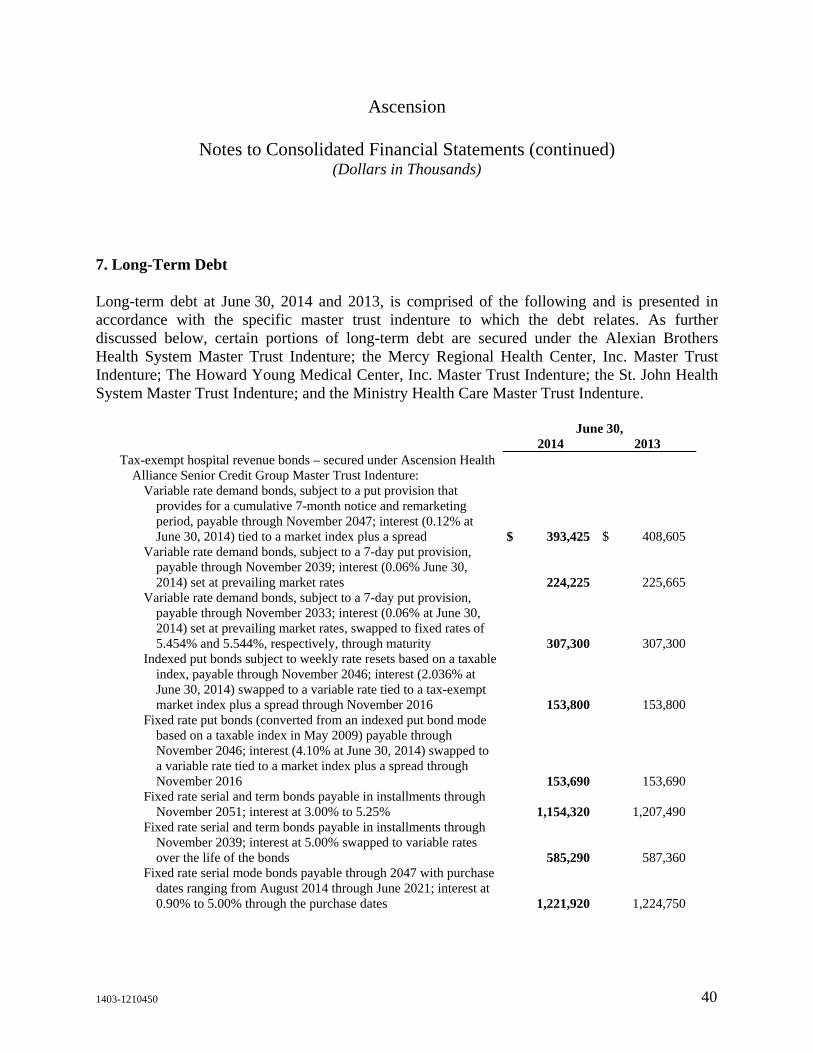

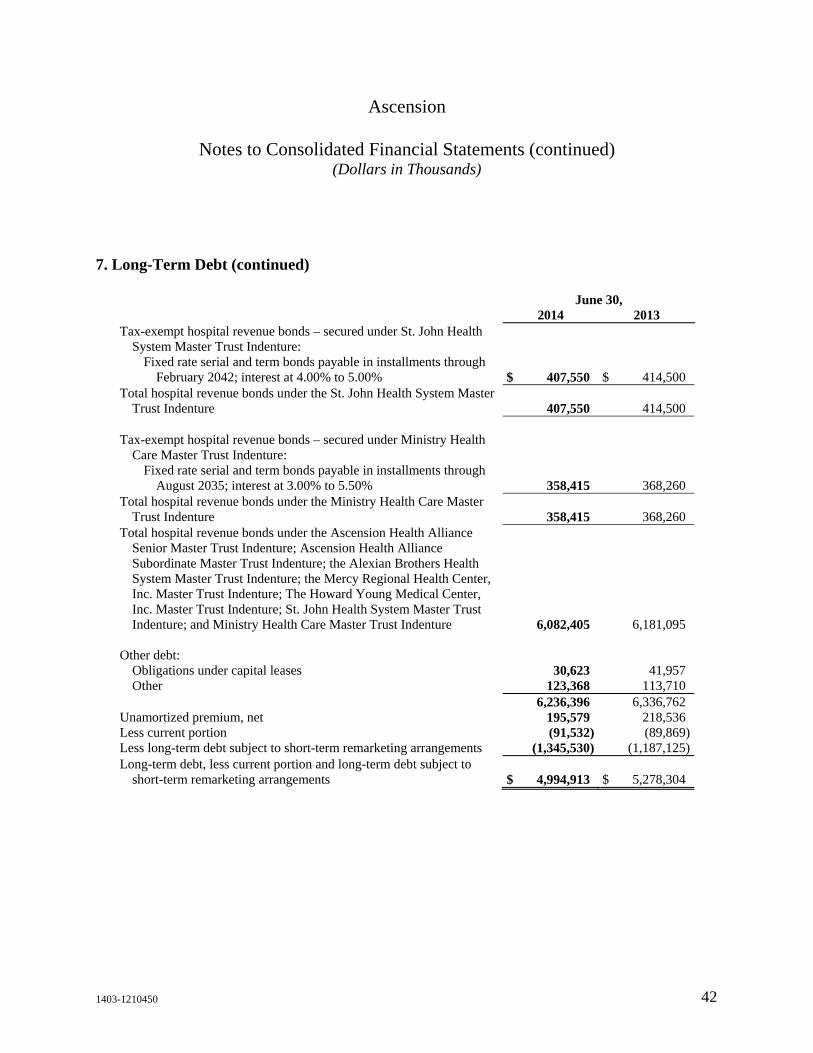

7. Long-Term Debt

Long-term debt at June 30, 2014 and 2013, is comprised of the following and is presented in accordance with the specific master trust indenture to which the debt relates. As further discussed below, certain portions of long-term debt are secured under the Alexian Brothers Health System Master Trust Indenture; the Mercy Regional Health Center, Inc. Master Trust Indenture; The Howard Young Medical Center, Inc. Master Trust Indenture; the St. John Health System Master Trust Indenture; and the Ministry Health Care Master Trust Indenture.

June 30, 2014 2013 Tax-exempt hospital revenue bonds – secured under Ascension Health

Alliance Senior Credit Group Master Trust Indenture: Variable rate demand bonds, subject to a put provision that

provides for a cumulative 7-month notice and remarketing period, payable through November 2047; interest (0.12% at June 30, 2014) tied to a market index plus a spread $ 393,425 $ 408,605

Variable rate demand bonds, subject to a 7-day put provision, payable through November 2039; interest (0.06% June 30, 2014) set at prevailing market rates 224,225 225,665