ASEAN and Asian Emerging Markets: From Exporting to Innovating The 2nd Seminar on Board of Trade of Thailand’ Strategy Innovating Business Reform to Move Forward George Abonyi Visiting Professor Department of Public Administration and Executive Education Program Maxwell School, Syracuse University 30 September 2015 1

Transcript

ASEAN and Asian Emerging Markets: From Exporting to Innovating

The 2nd Seminar on Board of Trade of Thailand’ Strategy Innovating Business Reform to Move Forward

George Abonyi Visiting Professor

Department of Public Administration and Executive Education ProgramMaxwell School, Syracuse University

30 September 2015

1

Overview of “the story”

2

Thailand: sustained development success

Thailand has achieved a remarkable combination of sustained rapid growth, macroeconomic stability, economic diversification, declining poverty, until the Asian Crisis of 1997-98

Asian Crisis eroded but did not erase gains from growth and development; and the economy generally recovered

Since the Asian Crisis, economic performance has been moderate; and there are concerns that Thailand has fallen into the “middle-income trap”

Source: Pasuk (2014)

3

From sustained development sustained development success success to Middle Income TrapMiddle Income TrapSource: Ohno (2011)

4

Income growth stalled• Manufactured exports stalled

Trap: between low-wage

manufacturers and

high-wage innovators

MACRO CONTEXT

Key role of manufactured exports

5

Export-driven growth Source: NESDB, 2015

Key role of exports in driving growth to date

• Import intensity of exports, e.g. hard disk drive (HDD) Note: Significant drop in investment since Asian Crisis (1997/8);

particularly private investment

• Key reason for infrastructure investment need, e.g. logistics

6

Manufactures dominate exports (% share of exports) Source: Ministry of Commerce, NESDB 2015

Electronics and Electrical: 30% of exports (2014)• Automotive (parts, assembly): around to 10%

Compare with rubber products: under 3% of exports• Yet Thailand is the world’s largest producer/exporter of natural rubber

• But close to 90% of rubber exports is not manufactures – little value added

7

CHALLENGE

Manufactured exports, key driver of growth, have stalled•Product/production challenge•Market challengeMarket challenge

Manufactured exports diversified and increased in sophistication, e.g. hard disk drive (HDD)

Thailand is losing comparative advantage in low-wage sectors (+ demography, e.g. migrant workers)

Most Thai firms, unlike in Korea or Taiwan, have not used low-cost labour advantage for knowledge-based capabilities to compete: upgrade (innovate), e.g. HDD

9

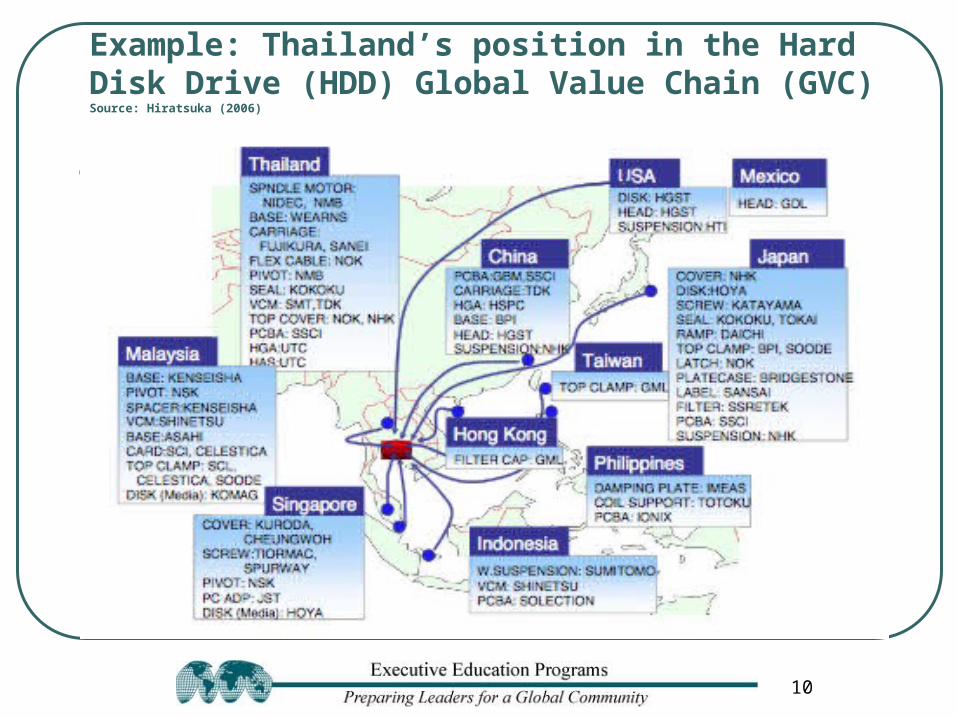

Example: Thailand’s position in the Hard Disk Drive (HDD) Global Value Chain (GVC)Source: Hiratsuka (2006)

10

Stuck in the middle of the GVC “smile curve”with lagging productivity: challenge of process and product innovationinnovation

Stuck in the middle? Value Added per Worker in 1990,

2000, 2010: USA figure = 100Source: Suehiro (2015)

11

Market challenge: “New normal” and “greater divergence” in the global economySource: IMF WEO, July 2015; October 2008

Slow-growth global economy esp. developed economies; slowing but relatively faster growth in Asian emerging economies

• Especially ASEAN, China, India (ACI) And political uncertainty of economic management (e.g. EU, China)

Source: IMF WEO, July 2015, October 2008

Note: IMF has continually overestimated growth since 2009

12

Thailand’s changing export markets (%) and the role of China Source: Suehiro (2015), NESDB

China is now the largest single market for Thai exports – but misleading

13

Developed economies and China as markets: slowing

Developed economies (particularly US) driving region’s growth as final markets• Intra-ASEAN trade is less than 25% of its total trade

Developed economies’ anemic growthSource: Lim and Lim (2012)

• China has imported 50% of all intra-regional intermediate exports (parts, components); but for final export to developed economies economies, e.g. iPhones to US and EU (source: ADB, 2011)

• China: rebalancing and extended slow growth• From high (national) savings and related

investment- and export-driven model;

to domestic consumption driven growth• Challenge of “political economy”

14

China’s investment-driven growth: increasing debt, declining efficiency,most new debt is to service old debt

China’s increasing debt and composition – mostly SOEs and local government

• Nearly 50% related to real estate

Source: MGI (2015)

Growing non-productive overinvestment: i.e. declining efficiency of investment

(Marginal Product of Capital)Source: Ha Jiming, Goldman Sachs China (2015)

S

15

Key Chinese activity indicators Nearly every industry is at 30% or more overcapacity

• Average accounts receivable for consumer electronics retailers/manufacturers:123 days

• Average days of inventory for clothing companies: 174 days (Bloomberg 2015)

Source: Haver Analytics, in Financial Times, 19 Aug. 2015

China’s import growth has declined significantly

Source: OECD, 16 Sept. 2015

16

China market challenge

China’s rebalancing from investment to consumption-driven growth even if smoothly successful, will mean extended slow growth; AND does not automatically translate into increased imports of final manufactures

China as market for final goods is shaped not by size or growth of GDP, but capacity to generate net demand for import of final manufactures • China has been major importer of Thailand’s/region’s exports of parts and components; but for its

final exports to developed economies, e.g. iPhones to US and EU

To become a growth locomotive for manufactures of Thailand and region China would need to raise not only its domestic consumption as a share of GDP, but also its imports of final goods from the region

17

OPPORTUNITY

Over the longer term, Asian emerging markets – particularly ASEAN, China, and India (ACI); but different from developed economies, Thailand’s traditional final markets.

18

Future of Asia is bright By 2030 40% of global consumer spending from Asia, especially ACISource for figures: Australian Government White Paper (2013)Note: assumes China will grow on average by 7% p.a. 2012 - 2025

Asia’s rising share of global GDP Asia’s rising incomes (Bubble area reflects size of GDP; income per person in PPP)

19

Future of ASEAN is brightSource: Euromonitor International (2015)

20

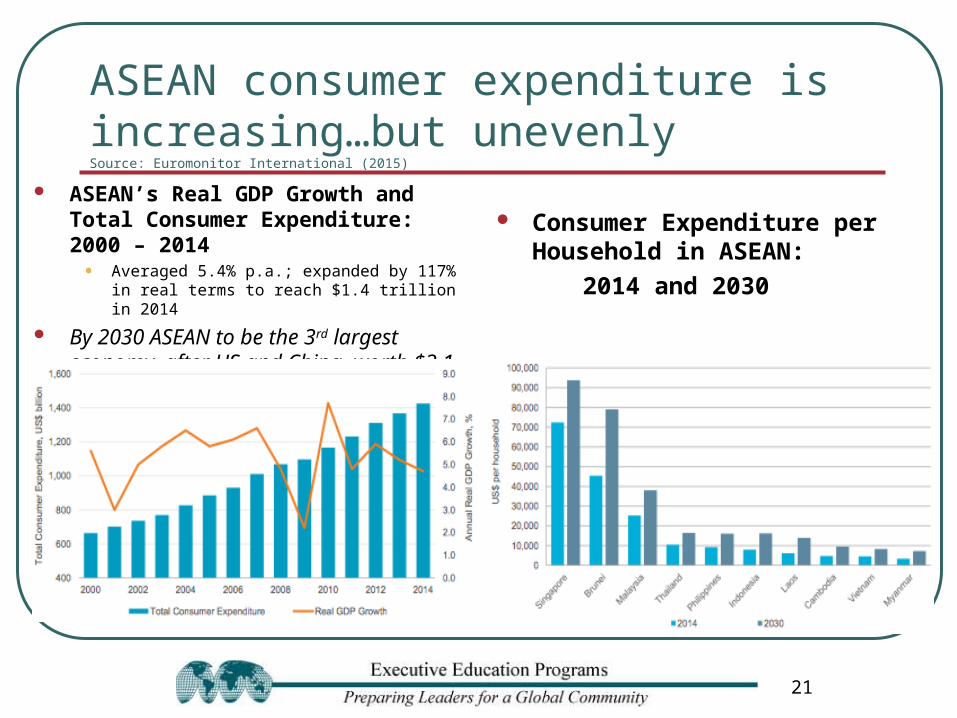

ASEAN consumer expenditure is increasing…but unevenlySource: Euromonitor International (2015)

ASEAN’s Real GDP Growth and Total Consumer Expenditure: 2000 – 2014• Averaged 5.4% p.a.; expanded by 117% in real

terms to reach $1.4 trillion in 2014

By 2030 ASEAN to be the 3rd largest economy, after US and China, worth $3.1 trillion in constant 2014 dollars

Consumer Expenditure per Household in ASEAN:

2014 and 2030

21

Asian emerging markets and consumers are different

But significantly lower disposable incomes in AEC in coming years as compared with developed

economies, region’s traditional final markets (source: Lawrence, ADBI (2013))

Fragmented markets,

growing income inequality,

and high proportion of

rural population will condition

consumer spending

Per Capita Real Annual Gross Income

in China and USA (1990–2030)Reflects consumers’ purchasing powerIn 2030: narrower, but US still 4.6 x China

Source: Euromonitor International (2014)

22

Consumer is at the centre of understanding market potential Source: Euromonitor International (2015)

Household Income Distribution in ASEAN: 2014

Households by Annual Disposable Income Band in ASEAN: 2014 and 2030

23

RESPONSE

From exporting to innovating for Asian emerging market consumers – but with a difference

24

The not-so-good news: Thailand is lagging on traditional measures of innovation such as R&DSource: NESDB, ADB

R&D as % share of GDP

Thai private sector's share of investment in total R&D is around 35-45%, vs. 77% for Korea, 76% for Taiwan, 66% for Singapore

25

Other constraints on innovatione.g. UNCTAD (2015); Abonyi/ADB (2014)

Narrow concept of innovation Narrow concept of innovation driving policies, programs, driving policies, programs, corporate strategiescorporate strategies Innovation-related policies and programs typically focus on supply-side

interventions for “mainstream markets”

• Firm-level innovation geared generally for “advanced consumers” either in developed markets or higher income consumers in emerging markets

• Focus on links between formal science and innovation – i.e. science, technology, innovation or STI -- in particular, R&D-intensive higher technology activities

• Inputs, e.g. PhDs, outputs: e.g. scientific publications (e.g. UNCTAD 2015)

Traditional STI policies and programs inadequately support innovation that is not high-level ST-intensive, e.g. incremental or adaptive innovation; for lower-income groups (e.g. lower middle-income; upper end of lower income)

• STI policy and corporate strategy generally fail to appreciate the potential contribution of such innovation to competitive export performance

AND increasingly:AND increasingly: New ecosystem of innovation: e.g. cheaper, faster, smaller, widespread ICT

devices, stakeholder collaboration, allow for easier low-cost market experiments in product/service/business model innovation (“Big Bang Disruption”) New innovations can enter market cheaper, more customizable, than existing productsNew innovations can enter market cheaper, more customizable, than existing products

27

The good newsThe good news: wider concept of innovation for Asian emerging markets

Consumers in Asian emerging markets have high aspirations, relatively low incomes, and a variety of constraints

Innovation for these consumers/markets can come not only from investment in high-level R&D and science and technology (STI): many entry points exist for Thai firms to “add value” along the value chain

Challenge to is to strengthen innovation suited to consumers and conditions of Asian emerging markets: requires also a focus on the DEMAND SIDE of innovation

• Investments in marketing, and product-related interactions with consumers may be as or more important to a firm in commercializing new ideas

• Interaction with consumers at early stages of product development is especially important in shaping innovation for emerging markets: innovation as (low cost) experimentation

“Breakthrough customer insights vs. breakthrough technology”

• Disposable income distribution: from “value for money” to (also) “value for many”

28

WHAT IS THE WORLD’S BEST SELLING CELL PHONE

29

Nokia 1100

Specifically for emerging markets, e.g.

• Dustproof keyboard;

• Front face built-in flashlight;

• Non-slip slides;

• Battery life (stand by) up to 400 hours! Over 250 million sold since late 2003 (to 2015) World's best selling handset and electronics device Example of “frugal innovation”

• And of the nature of the frugal innovation process

30

Wider concept of innovation:frugalfrugal and reversereverse innovationSources: e.g. Zechsky et al (2014); Radjou and Prabhu (2014); The Economist (2014)

Frugal innovation Cost Innovation: Same Functionality at a Lower Cost

• Responds to constraints such as income, e.g. purchase price, servicing costs• Example: Huawei (China) smart phone; Hindustan Unilever (India) detergent powder

Good-Enough Innovation: Tailored Functionality at a Lower Cost • Responds to specific customer needs and constraints

Frugal Innovation: New Functionality at a Lower Cost• Responds to specific needs of emerging markets/consumers

• Example: MittiCool clay refrigerator (India); GE ECG (electrocardiogram) MAC 400/800; M-Pesa

Reverse innovation• Innovation for emerging market consumers finds market in developed economies,

where there is increasing demand for lower price/higher value

• Example Haier refrigerator; Logitec M215 wireless mouse; GE ECG MAC 600

31

Constraints on frugal innovation

Limited firm knowledge and therefore focus on the needs of lower income populations: not aware of market and revenue potential

Infrastructure (hard/soft) – e.g. roads and distribution channels – is inadequate/constrained, making it costly and difficult for companies to serve lower income (e.g. rural) customers. • E.g. 79% of roads were paved in OECD countries in 2011, but only 53% were

paved in middle-income economies and 21% in low-income economies (World Bank Development Indicators, 2014)

Challenges of scaling up to viable business proposition• Implications: “business model innovation”

32

Examples ofFrugal and Reverse Innovation

33

Source: adapted from Stassopoulos (2013)

34

Conventional vs. Frugal and Reverse Innovation: Different paths to emerging regional and global opportunities (e.g. GE Healthymagination)

Conventional Innovation

Frugal and Reverse Innovation

35

Products modified (“stripped down”) for emerging market consumers

R&D/innovation and commercialization for developed market consumers & conditions

Needs and conditions in developed markets

Applications in developed markets(Reverse innovationReverse innovation)

Innovation for emerging market consumers and conditions: translate “voice” of consumer into products/services (Frugal Frugal innovationinnovation)

Aspirations and needs in emerging markets

Thailand: Toward innovation-led growth

Thailand has enormous potential for innovation, reflected in the inherent

capacity for design, and globally admired crafts, products and services

Moving from potential to performance requires strengthening “national innovation

system”: government + business + education + NGOs

• Starts from broad concept of innovation, not just high level R&D/S&T

• Includes investments in early stage product-related interactions with consumers on the

“why” and “what” of a product or service; production process improvements; technology

adaptation; and new types of business systems -- including key services (e.g. product

design, marketing, distribution)

• For SMEs: adapting existing technology to local (regional) user needs is a practical way

to commercially viable products and services

Widens greatly scope for innovation and exports for Asian emerging markets

36

General agenda for action:Toward innovation-led growth

Policy commitment Coordination/collaboration Focus on key value chains, clusters Integrate demand and supply side factors

• Particular focus on Asian emerging markets Innovative financing mechanisms (SMEs) Cross-border production linkages to upgrade

37

Facilitating frugal innovation Incentivize research institutions (public, private) to focus on frugal innovations Develop innovative financing mechanisms for frugal innovation initiatives by SMEs

• E.g. India’s Inclusive Innovation Fund is a for-profit investment fund created to support enterprises (SMEs) and innovators India’s lower income groups

Support intermediary institutions and means of knowledge exchange to provide technical and market/consumer-related expertise and information to frugal innovators

• E.g. Honey Bee Network (e.g. India, China) helps frugal innovators by providing support needed to develop these innovators’ inventions including related to protection of intellectual property, and commercialization of marketable innovations, including connecting SME innovators with formal institutions such as universities and public research institutions

Support partnerships between SMEs and large firms, which have scale but often limited insight into lower income consumers’ needs and constraints; and with NGOs that often have significant insight into and access to lower income (e.g. rural) consumers

• E.g. Oorja Stove (NGOs; large firms) Support early and sustained market/consumer engagement by firms as the key to

facilitating the frugal innovation process (e.g. information, financing, role of ICTrole of ICT)

• E.g. Nokia 1100, Rapoo mouse, GE Mac 400/800

38

FRUGAL FRUGAL INNOVATION INNOVATION

AS COLLABORATIONAS COLLABORATIONALONG THE VALUE CHAINALONG THE VALUE CHAIN