64

HEADING I Q3 2012 Issue 3 | Volume 1 The Electronic Trading Resource for Asia Asia E trader ASEAN Link Explained e Truth About HFT in Asia

| Date post: | 11-Mar-2016 |

| Category: |

Documents |

| Upload: | the-magazine-production-company |

| View: | 227 times |

| Download: | 2 times |

heading iQ3 2012Issue 3 | Volume 1

The Electronic Trading Resource for Asia

Asia Etrader

ASEAN Link Explained The Truth About HFT in Asia

*Standard data rates apply.

“Bank of America Merrill Lynch” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities

are performed globally by banking af� liates of Bank of America Corporation, including Bank of America, N.A., member FDIC. Securities, strategic advisory, and other investment banking activities are

performed globally by investment banking af� liates of Bank of America Corporation (“Investment Banking Af� liates”), including, in the United States, Merrill Lynch, Pierce, Fenner & Smith Incorporated

and Merrill Lynch Professional Clearing Corp., both of which are registered broker-dealers and members of FINRA and SIPC, and, in other jurisdictions, by locally registered entities. Investment products

offered by Investment Banking Af� liates: Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed. TAKING YOUR OPPORTUNITY FURTHER is a trademark of Bank of America Corporation,

registered in the U.S. Patent and Trademark Of� ce. ©2012 Bank of America Corporation

Asia +852.2161.7550 | Japan +813.6225.8398 | Europe +44.20.799.64521 | New York +1.212.449.6090

View the Instinct® videos.*ba.ml.com/instinct

A good trader spots all the right signals at just the right time.All on Instinct.

The new Instinct® Algo.

Combining the strengths of our widely used algorithms, the new Instinct® Algo

recognizes and adapts to more signals and more conditions more quickly than ever.

Yet for all its innate sophistication, it’s incredibly easy to use. When you want to

perform at the highest levels, go with our Instinct.

Taking your opportunity further. That’s return on relationship.

Email: [email protected] Bloomberg: MSG MLAPDSA<GO>

1

www.asiaetrading.com z Q3 2012 z asia etrader

HEADING IQ3 2012Issue 3 | Volume 1

The Electronic Trading Resource for Asia

Asia Etrader

ASEAN Link Explained � e Truth About HFT in Asia

leader

The Summer of Change

CREDITS

Chief EditorStephen [email protected]

Contributing WritersDan [email protected]

Roger [email protected]

Keiren [email protected]

Frederic [email protected]

Cover DesignNadia [email protected]

Graphic DesignMariel [email protected]

Magazine DesignThe Magazine Production Company,Adur Business Centre, Little High Street,Shoreham-by-Sea, West Sussex, BN43 5EG

PrinterCentury View Printing Limited Units B3, B4 & A1; 10/F Ko Fai Industrial Building7 Ko Fai Road Yau TongKowloon Hong Kong

Advertising [email protected]

Subscription [email protected]

Scan the Quick Response Codewith your iPhone or Android Phoneto take you to the Subscription page

Wild Wild Web Ltd.GPO Box 11108Hong Kong

www.asiaetrading.com

©2012

The summer issue of the Asia Etrader

brings with it the demise of Chi-east and

the birth of the ASEAN Trading Link. It

was a very busy quarter with a number

of new developments across the region

– short sale reporting in Hong Kong, new

listed futures contracts, new exchange

trading members, growing connectivity

options and of course the HKEx’s bid

for the LME. Despite the slowdown in

China and the Euro zone problems Asia

keeps moving forward developing its

own distinct market structure among

the global trading community.

Competition is growing in Japan, Australia and India (yes India). India,

while still restricted, has to be the largest arena for exchange competition

in Asia. We can see BSE’s market share in equities being eaten into and

new entrants like the MCX-SX and the exchange in Delhi will make the sub-

continent a battleground for liquidity. The Mainland government is pushing

reforms through now at a faster rate to prop up the flagging economy and

there could be a few surprises in the coming months. Not to forget Japan

whose regulators are trying to rewrite commodity trading policy and deal

with the TSE and OSE merger to ensure that country remains a viable and

competitive trading destination. Then we have Hong Kong and the LME

acquisition. Did they offer too much? How will an exchange known for its

IPOs and its weak secondary market absorb an asset class it knows little

about? Could this be the White Knight that Hong Kong needs to keep it a

viable market after the mainland opens up? And let us not forget Singapore.

A blow to exchange competition and best execution in Asia with the closing

of Chi-east. But the ASEAN Link is a development we can look forward

to. Perhaps this is the first steps to a pan-regional regulatory framework.

Whatever it and all the rest are, Asia sure is an exciting and dynamic place

and we are honoured to bring you the latest issue of our humble publication.

Have a safe and relaxing holiday this summer. The Fall season is going

to be hectic.

Stephen J. Edge

Editor

*Standard data rates apply.

“Bank of America Merrill Lynch” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities

are performed globally by banking af� liates of Bank of America Corporation, including Bank of America, N.A., member FDIC. Securities, strategic advisory, and other investment banking activities are

performed globally by investment banking af� liates of Bank of America Corporation (“Investment Banking Af� liates”), including, in the United States, Merrill Lynch, Pierce, Fenner & Smith Incorporated

and Merrill Lynch Professional Clearing Corp., both of which are registered broker-dealers and members of FINRA and SIPC, and, in other jurisdictions, by locally registered entities. Investment products

offered by Investment Banking Af� liates: Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed. TAKING YOUR OPPORTUNITY FURTHER is a trademark of Bank of America Corporation,

registered in the U.S. Patent and Trademark Of� ce. ©2012 Bank of America Corporation

Asia +852.2161.7550 | Japan +813.6225.8398 | Europe +44.20.799.64521 | New York +1.212.449.6090

View the Instinct® videos.*ba.ml.com/instinct

A good trader spots all the right signals at just the right time.All on Instinct.

The new Instinct® Algo.

Combining the strengths of our widely used algorithms, the new Instinct® Algo

recognizes and adapts to more signals and more conditions more quickly than ever.

Yet for all its innate sophistication, it’s incredibly easy to use. When you want to

perform at the highest levels, go with our Instinct.

Taking your opportunity further. That’s return on relationship.

Email: [email protected] Bloomberg: MSG MLAPDSA<GO>

asia etrader z Q3 2012 z www.asiaetrading.com

ConTenTS2

Contents

IN THE ZONE

our quarterly round-up of industry news and developments across asia last quarter.

Page 4

COvEr STOrIES

ASEAN Trading Link Explained – a significant development for exchange cooperation

and regional harmonisation as the aSean Trading link is about to go live. how does it

work? Who are the players, and who stands to benefit? Page 6

The Truth About HFT in Asia – high Frequency Trading is a global buzzword for a poorly

understood group of buy-side. This article looks at how prevalent hFT is in asia, who is

doing it and why they aren’t. Page 14

OPINION & ANALySIS

Market Data With Asian Characteristics – Keiren harris, a renowned market data

expert in asia, gives us his views on the regional market data playing field. Page 12

DErIvATIvES

Asia’s Increasing Appetite for Futures Trading. exchanges across asia are adding

more derivatives products to a growing community of sophisticated buyside. Find out

where on Page 20

Asia Futures Trading Q2 2012 recap. See our quarterly update on which

exchanges are trading the most futures around asia. Page 22

volatility in Asia Q2 2012. read our report on the how asia’s markets are reacting to

macro and local events. Page 24

BUy SIDE

Who’s Got the Biggest Blocks in Australia? Finding liquidity is becoming increasingly

challenging in a fragmenting australia so where can you find the biggest block?

Page 26

The Broker Panel. Three of asia’s leading buy-sides sat with asia etrader in a Q&a

discussion on how they are choosing the right broker for their execution needs.

Page 28

EXCHANGE SPOTLIGHT vultures Swoop Over Bombay Stock Exchange. This article that looks at the

competitive pressures the BSe is under from the nSe and new exchanges in india.

Page 31

www.asiaetrading.com z Q3 2012 z asia etrader

ConTenTS 3

rISK

Market Surveillance Technology Spearheads Integrity Drive Across Asia

Exchanges. The industry is focusing on weeding out rogue traders and

protecting participants. Page 34

WHO’S WHO emily Yu, head of the iT Strategy and Planning department at the Shenzhen Stock

exchange (SZSe), sat down with asia etrader and gave us her views and insights.

Page 36

EQUITIES The Autopsy of Chi-east. We held a roundtable discussion on the demise of Chi-east

and our panelists had some interesting insights on the reasons. Page 40

Asia’s Fragmentation Footprint Q2 2012. Fragmentation and the regulations supporting

it are gaining momentum. See just where liquidity in asia equities markets is going.

Page 42

Asia Equity Trading Q2 2012 recap. our quarterly review of turnover, average trade

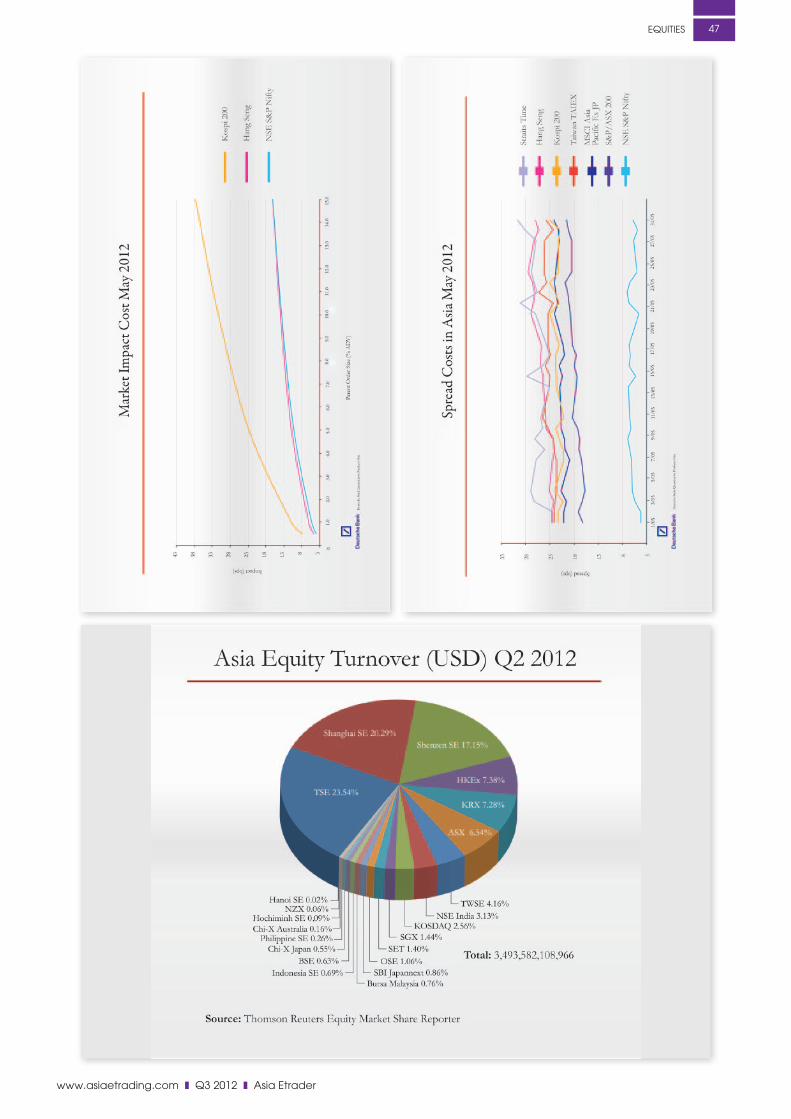

sizes, spread and market impact costs on asia’s exchanges. Page 46

Short report Q2 2012 recap. hong Kong updated its short selling reporting

requirements and we expanded our coverage to australia. Page 48

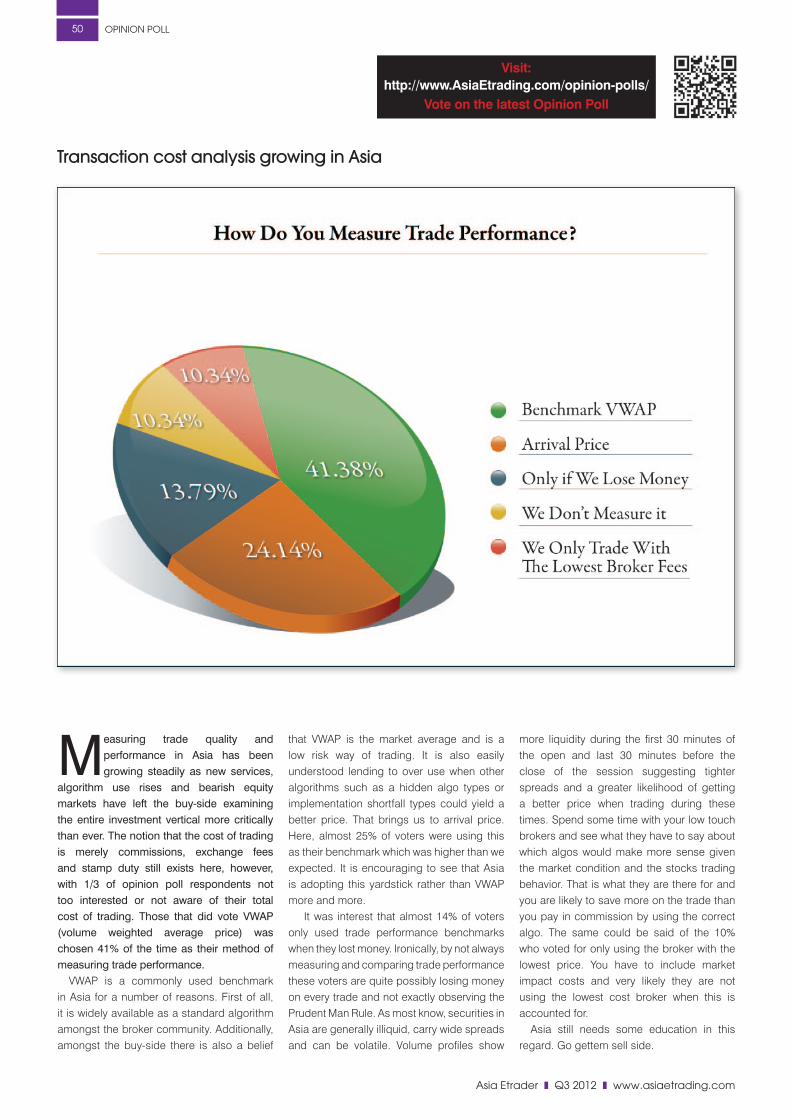

OPINION POLLS How Do you Measure Trade Performance? Measuring the cost of trading goes

beyond commission and exchange fees. hear what our expert says on the matter.

Page 50

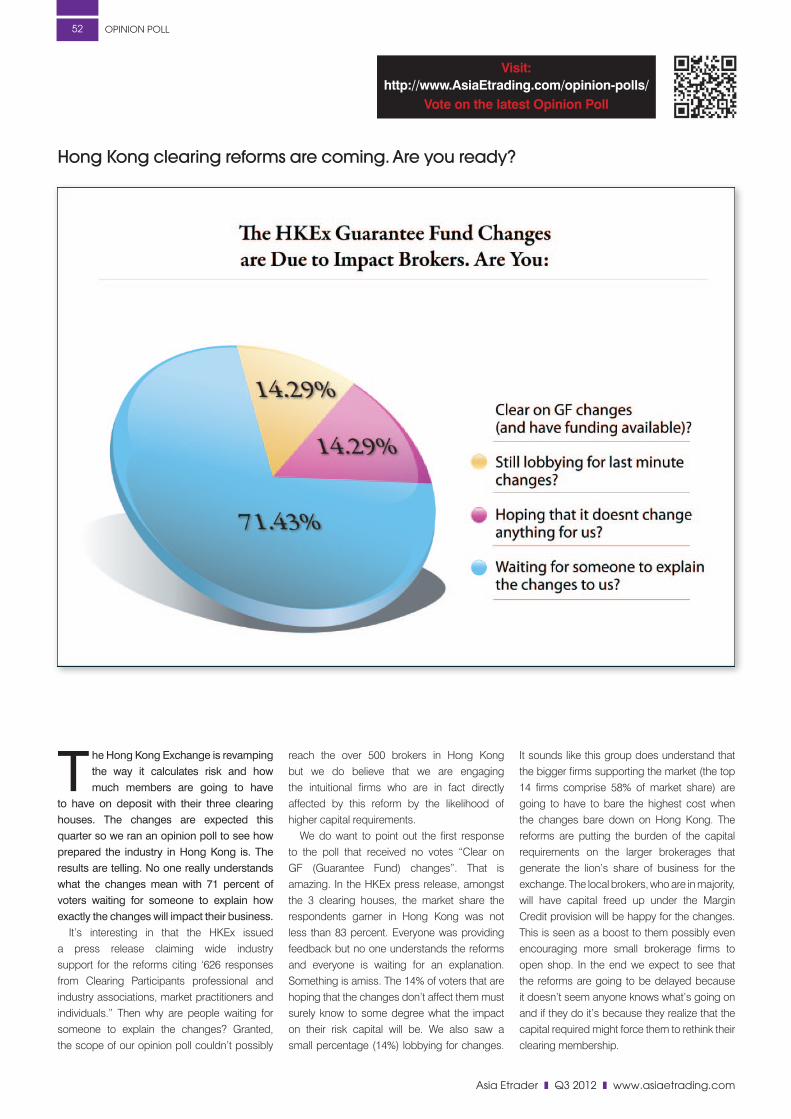

Are you ready for The HKEx Clearing House reforms? hong Kong is modernizing

its risk requirements for its members but are they ready? our expert shares his views.

Page 52

TECHNOLOGy Competitive Advantage in the Cloud. The added flexibility of leveraging The Cloud

can make all the difference to retain and win new business. Page 54

BACK PAGE 56 Careers – The latest career opportunities and job market insights

Dates – exchange holidays and important industry events

Directory – a listing of asia’s electronic trading industry participants

Social Media – news and information on the trends in Social Media of asia’s

financial industry

asia etrader z Q3 2012 z www.asiaetrading.com

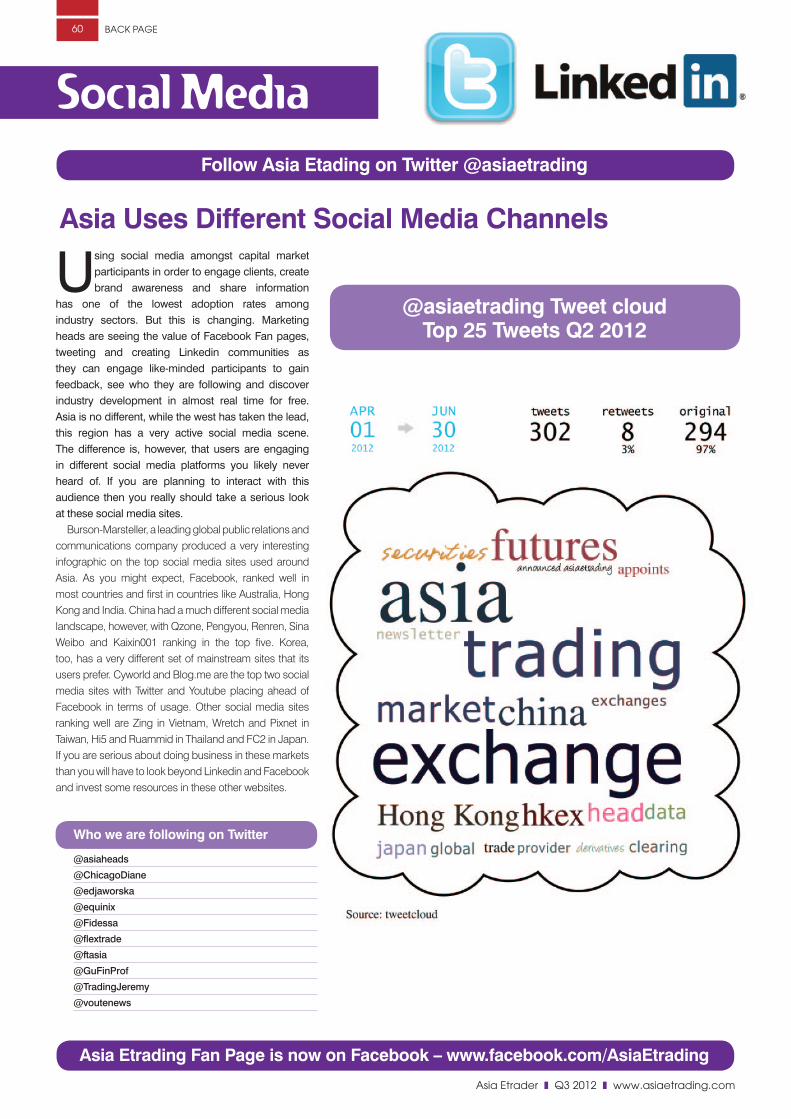

in The Zone4

Depending on how you’re placed within the electronic trading vertical there were three events that topped the list

of developments and they are the closure of Chi-east, the HKEx offer for the London Metal Exchange (LME) and the long awaited start of the ASEAN Trading Link.

Chi-east, the first pan-Asia broker-to-broker darkpool, closed its doors May 31 in a tough equity market that has seen volumes deteriorate in stagnant markets (See page 38 The Autopsy of Chi-east). The independent venue faced other daunting challenges including cost of connectivity to the broker community, special clearing requirements in different domiciles and the acceptance of this kind of service across the industry. We hope that this doesn’t put in a negative light on the viability of exchange competition in Asia. On the subject of competition, it was finally announced after months of speculation that the HKEx came out as the front runner to buy the LME for a whopping HKD 16.67 billion. The offer raises a lot of questions like did they pay too much? Will the marriage work? What will this mean for global metals trading? How involved is the Chinese government? We recognize the HKEx has to do something to sustain its longevity and will be watching this development very closely. Lastly, the ASEAN Trading Link has just gone live after 5 years of discussions and planning. This is a particularly exciting development as the so-called Asian Tigers band together to develop a trading bloc in a region that is generally hard to access, not fully developed in terms of market structure and has over 500 million consumers with a growing standard of living. (See page 4 ASEAN Trading Link Explained).

Of course, much more happened here in Asia last quarter.

AustraliaThe Australian Securities Exchange began OTC clearing services for equity options. The regulator, the Australian Securities and Investments Commission (ASIC) updated its crossing reporting requirements under its Market Integrity Rules (MIR) and they also announced an upgrade to its market surveillance system which currently supports a single market system. The upgrade will provide for a multi-market system where volumes are expected to increase as algorithmic trading grows.

CambodiaThe Cambodia Securities Exchange began operation on April 18 listing the Phnom Penh Water Supply Authority.

DubaiThe Dubai Mercantile Exchange appointed a new CEO the former BNP Paribas head of marketing for commodity futures in Asia, Christopher Fix. The Dubai Gold and Commodities Exchange signed with Cinnober

for its clearing and surveillance technology due to go live Q4 2012.

ChinaGlobal exchange operators Deutsche Börse and NYSE Euronext signed agreements with the China Financial Futures Exchange as they attempt to woo future business and inter-listing to their western customers. The Dalian Commodity Exchange (DCE) began simulation of option trading as Liu Xingqiang the exchange president pushes for continued development of their product offering. The DCE also announced a revision to its exchange fees. The Shanghai Stock Exchange (SSE) began taking ETF positions as eligible collateral for margin trading and securities lending. The People’s Bank of

In the Zone... The first half of 2012 is already behind us and this quarter had a number of noteworthy industry developments right around Asia across all segments of the electronic trading ecosystem. Let’s take a very brief look at what happened In The Zone.

www.asiaetrading.com z Q3 2012 z asia etrader

in The Zone 5

China, the central bank, announced April 14 that it would the yuan’s daily trading limit against US dollar currency to 1 percent from 0.5%

Hong KongBesides the LME announcement the exchange made known it had received regulatory approval for the launch of the first listed RMB currency future. The HKEx also appointed Chow Chung Kong as Chairman, Stephen Marzo as Chief Financial Officer and Henry Ingrouille as its Chief Administrative Officer. The Ministry of Finance of China signed a MOU with the HKEx to begin listing and trading of RMB-denominated sovereign bonds in Hong Kong. The Hong Kong regulator rolled out new short selling regulations requiring positions to be reported. The Hong Kong Mercantile exchange was busy signing BOCOM International Securities and China Everbright as new members and their flagship gold future surpassed 10,000 traded contracts in one day. Goldman Sachs was censured by the exchange back in April. It was related to derivative warrants they had issued that incorrectly calculated the settlement conditions for the product by multiply rather than dividing the exchange rate. GS bought the warrants back at $1.10 on the dollar.

IndiaSEBI, India’s regulator, issued guidelines on algorithmic trading including a definition, exchange requirements and minimum risk checks. Lambertus Rutten would not renew his contract as CEO of MCX but would remain on the board.

IndonesiaIndonesia’s commodity exchange, the ICDX, has adopted Bloomberg’s Open Symbology and launched 27 currency pair futures contracts as this country continues its rise within the region.

JapanThe Tokyo Commodity Exchange added a new member in Phillip Securities and the announcement that the Tokyo Grain Exchange

would consolidate to TOCOM was made in June. It was announced that Masamichi Kono of the Japan FSA would lead IOSCOs new board and the Tokyo Stock Exchange signed an MOU with the central bank of Myanmar for establishing a securities exchange. SBI Japannext began the launch of X-Market, a service for retail brokers to trade on the PTS without the need to adapt to the smaller tick size.

KoreaThe Korea Exchange was also busy developing relationships where it signed an MoU with the Bolsa de Valores de Lima. MSCI passed over the country for an upgrade from emerging to developed.

MalaysiaBursa Malaysia began a consultation to amend rules for exchange traded bonds and its derivatives arm revamped its options on Malaysia’s composite index future the FKLI.

New ZealandCaroline Leckie resigned as Head of Market Supervision at the NZX. Tim Bennett the CEO

announced that two new positions would be created at the exchange, CFO and a Head of Cash Markets and the dairy future contract broker 20,000 contracts after 18 months of trading.

Singapore

The Singapore exchange was busy as usual extending its REACH program to Chicago and London via BT. They also began to offer cash settled MSCI Indonesia futures, brought some enhancements to OTC clearing for commodities and reported US$67 million in third quarter profits. Concord Futures became a new member and GFI Group executed the first iron ore swap cleared via STP with the exchange. Lastly, Project Mars, their surveillance system went live based on the Delta Stream CEP of First Derivatives. The Monetary Authority of Singapore issued a response to feedback on its proposed regulation of the derivatives market and issued a response to the regulator being accused of regulatory arbitrage. Equinix spent US$28.5 million on the expansion of their Singapore 2 data center.

TaiwanThe GreTai Securities Market, Taiwans SME exchange, was busy forging relationships in its push to raise its profile. They signed agreements with NASDAQ OMX, the Tokyo Stock Exchange and Deutsche Börse of Germany

ThailandThe Thai Futures Exchange began trading in its USD currency futures and its parent company launched the Thai Depository Portal on May 1. The local derivatives market continues to expand with KT ZMICO Securities offering Sungard’s Valdi trader front end.

TO SUBSCRIBE:

http://www.asiaetrading.com/asia-etrader-magazine/

Email:[email protected]

asia etrader z Q3 2012 z www.asiaetrading.com

Cover STorY6

The collaboration is something of a milestone and is widely viewed as the first steps of a pan-Asia trading

community to mirror that of Europe under MIFID. The compact comprises 7 exchanges in 6 countries boasting more than 3,600 companies. The BMB, SET and SGX represent approximately two-thirds of the US2.0 trillion market capitalisation of the seven members of the ASEAN Exchanges. The remaining four bourses are the Hanoi Stock Exchange (HSE), Hochiminh Stock Exchange (HOSE), the Indonesia Stock Exchange (IDX) and the Philippine Stock Exchange (PSE). The seeds for the initiative were sown during the 12th ASEAN Summit held January 2007 where members had agreed to accelerate integration and trade into and amongst the community by 2015. The goals of the ASEAN Economic Community are threefold:

• Promoting ASEAN as an asset class to global investors

• Lower the funding cost for listed companies• Improving trading efficiency and lower

trading cost locally and abroad

The long road has inevitably encountered some bumps along the way. Initially, NYSE Technologies was contracted to provide the network infrastructure as an extension of its Secure Financial Transaction Infrastructure (SFTI) network and also to provide connectivity to the respective exchanges within the Link. After 30 months of requests for proposals and three new CEO’s arriving to some of the ASEAN exchanges a business case for the Link couldn’t be justified. By this point, after much time and energy, NYSE Tech dropped the project. Not long after, however, SunGard stepped in to offer a solution that both provided support for the network and gateways but also the trading, post trade and risk software as well. After many hours of development, testing and more testing the ASEAN Trading Link is almost a reality.

How Does It Work?The ASEAN link is comprised of a fibre network, known as the Intra-ASEAN Network (IAN) connecting each of the exchanges at a hub through a gateway. Each segment of the network has been built by local providers in each of the respective countries but owned by the ASEAN members and managed entirely by SunGard. The connection to the hub is referred to as the ASEAN Common Exchange (ACE) interface. The ACE is the point at which the local broker and the local exchange will be connected. You might be asking isn’t the local broker already connected to the exchanges own API? Yes, they would be but in order for the local broker to send and receive trades to the Link partners they must be connected via the ACE. Each ACE is housed in a data center either collocated with the exchange as in the case of SGX or within close proximity to the exchange at a telco.

Broker A, the Originating Broker (OB) is in Kuala Lumpur and has just received an order to buy 100,000 shares of Capitaland in Singapore. The order can be received over the phone or electronically as long as the broker routes the order to the ACE at Bursa Malaysia which could be by a dedicated connection or over the internet. Once the order is received at the ACE it is then sent through the IAN where

it is then received at the SGX ACE and then continues to the exchanges matching engine. Each acknowledgement, change, cancel or fill report is sent back along the SGX ACE over the IAN back to the BMB ACE then back to the OB where the client can then report the trades to her client. Orders are not sent via the Sponsoring Brokers (SB) infrastructure, rather order messages are tagged with the SBs ID when the OB sends the order.

There is one other means of connecting to the Link referred to as the Neutral Access Point (NAP). Located in Singapore, this gateway will serve international clients seeking to connect directly into the Link. Like the ASEAN participants these firms will also need to have an account with a custodian and or an executing broker in each of the respective countries they plan to trade in. Access to the NAP can be by dedicated connectivity or via the web.

The messaging standard throughout the link is SunGard’s but there is a FIX 5.0 adapter available allowing for some measure of vendor neutrality. Because of the availability of FIX, sell side algorithms can be offered to clients. Additionally, SunGard’s Valdi Trader front end can offer a suite of algos via their Tactics server providing for clients the ability to slice up large orders too. Market making is also possible via SunGard Rubyx but given the latency constraints of a network versus colocating at the exchange we’re not likely to see much

The aSean Trading link explainedThe ASEAN Trading Link is expected to go live this month after 5 years of planning with Bursa Malaysia (BMB) and the Singapore Exchange (SGX) initiating the first tie. The Stock Exchange of Thailand (SET) is scheduled to comprise the next link in the third quarter after they upgrade their matching engine and infrastructure.

“The compact comprises

7 exchanges in 6

countries boasting more

than 3,600 companies.”

www.asiaetrading.com z Q3 2012 z asia etrader

Cover STorY 7

TO SUBSCRIBE:

http://www.asiaetrading.com/asia-etrader-magazine/

Email:[email protected]

cross-border market making over the Link.Risk is affected by SunGard’s Selector

product. Here, the SB assigns firm level restrictions to the OB such as equity limits, position limits and fat finger limits. The sponsor will also be allowed to view and cancel trades. The OB, under the firm level limits, will then provide risk limits to each of their clients applying the same limit types found at the firm level. The OB will also be allowed to view positions and cancel trades but only those under the firm ID as provided by the SB. The key point is that the broker in the home country where the securities are executed bares the risk of the trade and sets the risk limits of the originating broker in aggregate. Of course, each firm will have their own risk policy as required by local regulations and best practices.

Clearing and Settlement falls under the inter-broker model meaning that payment and transfer of securities will be the responsibility of the Sponsoring Broker (or Custodian) as designated by the Originating Broker. Trades are settled in the local currency, that is to say, in the example above the broker in Kuala Lumpur will need to convert Ringgit to Singapore Dollars when purchasing Capitaland. Under the FIX set up drop copies of the trades are available and under the SunGard structure end of day reporting will be available.

Market data is distributed by the local exchange to each of the respective exchange ACE gateways in real-time. This provides for a single point of access for the data of every exchange. Order flow goes from the client to the OB then on to the exchange via the executing ACE but the market data travels in the opposite direction over the same network.

The key piece in the entire architecture is the ASEAN Common Exchange. This gateway routes orders to the respective ACE of the executing country, sends orders directly to the exchange, disseminates and receives the market data from each of the respective exchanges, holds the risk and client set up module and translates FIX messages into the proprietary protocol of the network.

The Link will expand to include a depository element offering custodian services helping to push down costs further. The depository is expected to come on line by the end of 2012 or early 2013. Then in 2013, a pan-regional clearing entity will be formed to bolster the region as one large exchange and to better manage risk. Additionally, Cambodia, Laos and Burma are likely to be folded into the mix at some point in the future.

Who Will Benefit?There are many beneficiaries of the ASEAN link. First of all the sponsoring broker in the

local market through just the connection to the ACE will be able to offer all its clients access to all the ASEAN markets that are part of the IAN (provided that broker has accounts setup with the respective sponsoring broker). Before, brokers would have had to establish point to point connections with brokers in the markets that they wished to trade in. They would have borne the cost of the network, hardware for routing orders, failover provisions and the staff needed to support it. By connecting into the link the broker will realize significant savings and offer trading in the region focusing on broking rather than providing technology.

An improved user experience for clients through the stability and lower latency within the network where before traders might have been subject to web based trading through ISPs or incongruent service level agreements (SLA) among network providers. The network managed by SunGard will offer central support, a standard level of service and experts who are managing the technology effectively.

Singapore and its exchange will stand to benefit from the trading link for a number of reasons. Firstly, Singapore has placed itself as a hub for trading between the ASEAN members and the markets it serves through its REACH program that it launched 15 August, 2011. Under REACH, SGX unveiled its latest matching engine and erected a new data center for colocation services. The other element of REACH is that in London, New York, Chicago and Tokyo the

exchange setup access points so that local participants in those international markets could access SGX by simply connecting to the local access point. With its position in the ASEAN Link, member participants can access, via Singapore, international financial centers and conversely international investors can now access the ASEAN link with Singapore right in the middle. This could prove to be a critical and important development for Singapore and its brokerage community if the Link proves successful standing at the gateway of more than 500 million people.

SunGard as the key technology provider stands to gain enormously. As part of the support agreement for the ASEAN link, Sungard is to provide several Valdi Trader screens to each exchange for 18 months giving them a stronger foothold into the region. Their risk software, Selector, is housed within each exchange ACE giving them a permanent home within crucial points of the infrastructure. Additionally, the trading community within the ASEAN is small and developing. Some of these markets have only begun to offer DMA, and algorithmic trading is just concentrated in Singapore, Malaysia and Thailand. As the national wealth of ASEAN grows, pension systems evolve and electronic trading expands SunGard will have a leg in as a technology provider across the trading vertical from Valdi in the front end, Selector providing risk and Clearvision in the post trade among others.

SunGard, too, has its own global network (SGN) where it will now extend its reach to the Link. SunGard has a large data center in Singapore providing easy access to both the SGX and the Neutral Access Point. Much like SGX REACH, SunGard will be able to provide connectivity for any customer connected to the SGN into ASEAN and also ASEAN members will be able to send trades to SunGard clients anywhere in the network. They are weaving themselves in to the fabric of the South East Asia’s electronic trading industry.

FIX protocol as a standard will be given a boost with the help of the ASEAN Link. FIX is widely used in Asia largely amongst the institutional brokerage community who are offering algorithms such as VWAP, Iceberg and Implementation Shortfall to clients. Having a FIX API at the ACE will offer vendor neutrality to the Link and also kick start the local and regional firms to look more closely at solutions that employ utilizing FIX. As a global standard, firms in the Link will be able to accept order with a wider trading community outside their market.

ASEAN investors are also going to benefit with the onset of the Link with access to a broader and more diverse portfolio of stocks to invest in and at a lower cost than what they might

Cover STorY8

asia etrader z Q3 2012 z www.asiaetrading.com

“The sponsoring broker in

the local market through

just the connection to

the ACE will be able to

offer all its clients access

to all the ASEAN markets.”

www.asiaetrading.com z Q3 2012 z asia etrader

Cover STorY 9

HANOI ACB DABACO HABUBANK KLS TIFOPLAST OCH.JSC PV GAS SOUTHERN PLC PVI PTSC PVC SACOMREAL SHB VINACONEX.,JSC VICOSTONE

HO CHI MINH

BAOVIET HOLDINGS BECAMEX IJC EXIMBANK FPT CORP HAGL KINH DO CORP MASAN GROUP CORP OGC PVFCCO REE JS COMPANY SACOMBANK SSI VIETCOMBANK VINAMILK VINCOM JSC

INDONESIAASTRA AGRO LESTA ADARO ENERGY TBK ANEKA TAMBANG ASTRA INTL TBK BNK CENTRAL ASIA BANK BNI TBK BANK RAKYAT INDO BANK DANAMON TBK BANK MANDIRI TBK BUMI RESOURCES CHAROEN POKPHAN XL AXIATA GUDANG GARAM TBK HARUM ENERGY

INDOFOOD CBP VALE INDONESIA INDOFOOD S M TBK INDOCEMENT T P INDO TAMBANGRAYA JASA MARGA KALBE FARMA TBK LIPPO KARAWACI LONDON SUMATRA P GAS NEGARA TBK TB BUKIT ASAM SALIM IVOMAS PRA SEMEN GRESIK TBK TELKOM INDONESIA UNITED TRACTORS UNILEVER INDONES

MALAYSIAAIRASIA BHD AMMB HLDGS BHD AXIATA GROUP BHD BRITISH AME TOBA BUMI ARMADA CIMB GRP BHD DIGI.COM GENTING MYS BHD GENTING BHD HONG LEONG BANK HONG LEONG FINAN IOI CORP BHD K.LUMPUR KEPONG MAYBANK BHD MALAYSIA MARINE MMC CORPORATION MAXIS BERHAD PETRONAS CHEML PPB GROUP BHD PETRONAS DAGANG PETRONAS GAS PUBLIC BANK BHD RHB CAPITAL SIME DARBY BHD TENAGA NASIONAL TELEKOM MALAYSIA UEM LAND HLDGS UMW HOLDINGS YTL POWER YTL CORPORATION

PHILIPPINES

AYALA CORP ABOITIZ EQUITY ALLIANCE GLOBAL AYALA LAND ABOITIZ POWER BDO UNIBANK BELLE CORP BK OF PHI ISLAND CEBU AIR INC DMCI HOLDINGS ENERGY DEVELOP FIRST GEN GLOBE TELECOM INTL CONTAINER JOLLIBEE FOODS JG SUMMIT METROPOLITAN BK MEGAWORLD CORP MANILA ELECTRIC METRO PACIFI INV MANILA WATER CO PHILEX MINING-A ROBINSONS LAND SEMIRARA MINING SM INVESTMENT SAN MIGUEL CORP SM DEVT CORP SM PRIME HLDGS PHI LONG DIS TEL UNIVERSAL ROBINA

SINGAPORECAPITALAND CAPITAMALLS ASIA COMFORTDELGRO CAPMALL TRUST CITY DEVT LTD DBS GRP HLDGS FRASER & NEAVE GOLDEN AGRI GENTING SPORE GLOBAL LOG PROP HONGKONG LAND JARDINE MATH 400 JARDINE C&C JARDINE STR 500 KEPPEL CORP NEPTUNE OL LTD

NOBLE GROUP

OCBC

OLAM INTER

SEMBCORP INDUST

SEMBCORP MARINE

SGX

SIA ENGR

SIA LTD

SPORE PRESS HLDG

STARHUB

ST ENGRG

SINGTEL

UOB LTD

WILMAR INTL

THAILANDADVANCED INFO SV

AIRPORTS OF TH

BANPU50

BANK OF AYUDHYA

BANGKOK BANK

BEC WORLD

BKK DUSIT MED

BIG C SUPER

CP ALL

CHAROEN

CENTRAL PAT

TOTAL ACCESS

ELECTRIC GEN

GLOW ENERGY

IRPC

INDORAMA VENT

KASIKORNBANK

KRUNG THAI BANK

LAND & HOUSE

PTT

PTT EXP & PROD

PTT GLOBAL CHE

RATCHABURI

SIAM COM BANK

SIAM CEMENT

SIAM CITY

THAI AIRWAYS

TMB BANK

THAI OIL

THAI UNION FRO

ASEAN STARS

The ASEAN Stars index will comprise the 30 largest and most liquid companies (total 180) from each of the member countries with banking and real estate representing the two largest sectors of the benchmark. With the advent of the ASEAN Stars investors will be able to allocate assets in the regional Blue Chips and provide for an identifiable reference for fund managers and exchange traded funds (ETF).

asia etrader z Q3 2012 z www.asiaetrading.com

Cover STorY10

otherwise have to pay. ASEAN as a whole will have a larger voice within the global economic community where they have lived in the shadow of China and India . Cooperation amongst the ASEAN Exchanges will increase its visibility and capability to the global investor. According to data from the World Federation of Exchanges the sum of the exchanges market capitalization from the ASEAN members would rank them ahead of BM&F Bovespa in Brazil and just behind the TMX group in Canada.

With the creation of the ASEAN link will come the STARS index. The Index while not finalized will comprise the 30 largest and most liquid companies (total 180) from each of the member countries with banking and real estate representing the two largest sectors of the benchmark. With the advent of the ASEAN Stars investors will be able to allocate assets in the regional Blue Chips and provide for an identifiable reference for fund managers and exchange traded funds (ETF)

The Link members are currently formalising an agreement with an index provider. At the time of this writing the talks were ongoing with an unnamed company to provide a range of ASEAN market data and analytics. There is currently an ASEAN 40 index provided by FTSE but the final details about the Stars Index such as whether it will be tradable or a reference index are still under negotiation.

The Challenges AheadWith such an ambitious regional cross border initiative the viability of the Link has come under scrutiny. The Philippine Stock Exchange disclosed last November that it would postpone its plans to join the link claiming that the local brokerage industry and investing public hadn’t been as supportive of entering the arrangement as initially expected. The announcement went on to say that the PSE would join the link at a future date but felt the more technically advanced bourses should be the first to see if they can bring the project to market. The PSE upgraded their matching engine in 2010 using NYSE Technologies products. The Indonesia Stock Exchange has also pulled back on their commitment to the Link as they too wait and see how successful the initial development becomes. There is also a belief that the potential for the economy and financial industry will outstrip the rest of the ASEAN members and that connecting to the Link may not be necessary. That could very well be true. Moody’s recently upgraded Indonesia to investment grade and the economy is expected to grow by 7% this year in that nation of 240 million people despite the global economic travails.

Regulations also pose a challenge to the development of the linkage. Each country has its own rules and policies to police and preserve the integrity of their respective capital markets. There are different rules for foreign investors accessing each county, ownership rules, qualified institutions and retail investors are subject to differing guidelines. What would be ideal would be a supra-regulator to govern the bloc and this notion, some believe, is that the Link could be the catalyst for a common set of rules. Of course there are no guarantees that a regional policy would work as we see how the Europe story is unfolding.

The Back Office issues faced by the compact will need to be addressed. The post trade is the most expensive and least automated segment of the trading business in every part of the world so how is this less developed region going to cope with multi-market, multi-currency settlement instructions? How will foreign holding tax be managed or, as in Singapore, will the members have to charge GST on its trades and if so, how do they pay that bill? How will Treasury cope with the currency demands? Will the post trade be overwhelmed by the onset of algorithmic trading and each and every confirmation that has to be created? Each country will also have different settlement calendars and oversight on

failed trades too. It is a daunting task and will be an eye opener to the most sophisticated back office.

ConclusionThe ASEAN members are expected to yield 6% growth in GDP between 2011-2015 amongst its 568 million inhabitants. The population are young, educated and will need somewhere to put their growing savings. Economic, political and regulatory union are by no means easy but this attempt to bring about a common market in this part of the world has to be commended. The worst case scenario is that the union will fail but the local exchanges will have had a taste of international interest and an improved trading infrastructure. The upside is a successful partnership that could form a key market for anyone’s portfolio. Regardless of the outcome it is a win-win for the region. Our hope is that the ASEAN Trading Link succeeds and will bring the world one step closer to an international electronic trading venue.

“How will foreign holding tax be

managed or, as in Singapore,

will the members have to charge

GST on its trades.”

TO SUBSCRIBE:

http://www.asiaetrading.com/asia-etrader-magazine/

Email:[email protected]

www.asiaetrading.com z Q3 2012 z asia etrader

Cover STorY 11

asia etrader z Q3 2012 z www.asiaetrading.com

oPinion & analYSiS12

Strong organic growth, and increasing overseas investment have transformed Asian Financial markets since

2000. Unsurprisingly the regional market data industry mirrors these developments. However the transition from vanilla based investing in Equities, Fixed Income, and FX/Money Markets to more sophisticated electronic trading, a wider range of financial instruments and greater overseas participation has not changed the simple fact each market remains domestically oriented and fragmented with the exception of regional hubs Hong Kong and Singapore.

The reasons for this fragmentation are well known, open and closed barriers to entry, cultural issues, and the underlying cost of operating across a very large percentage of the Earth’s surface.

The Asian market data industry naturally reflects both these trends, and arguably, the future could well see greater levels of fragmentation as new entrants seek a slice of a growing pie. However, especially in Asia, to be successful they need to differentiate their offerings to leverage unique product strengths rather than taking on the two Tier 1 universal aggregators, Bloomberg and Thomson Reuters. To a degree the Tier 2s, such as IDC, Morningstar, and SIX Telekurs, and specialist vendors have followed global clients into Asian markets as penetrating local institutions unwilling to invest in market data is often unprofitable.

This fragmentation is increasing on two levels geographically where there are 5 keymarket areas, China, Japan, Korea, Hong Kong Singapore, and the parochial domestic markets of the rest, though Indonesia is developing rapidly.

The result is that global vendors can offer pan-regional services with near universal content coverage with an entrenched institutional client base. Unfortunately for Tier 2 vendors their weaker OTC and contributed data coverage has until now limited their Asian aspirations. In contrast domestic vendors focus primarily on their local equity markets offering low cost, low margin, market depth coverage for a domestic and retail audience.

Demand DriversSadly, there is limited and unreliable information on market data revenues in Asia. However,

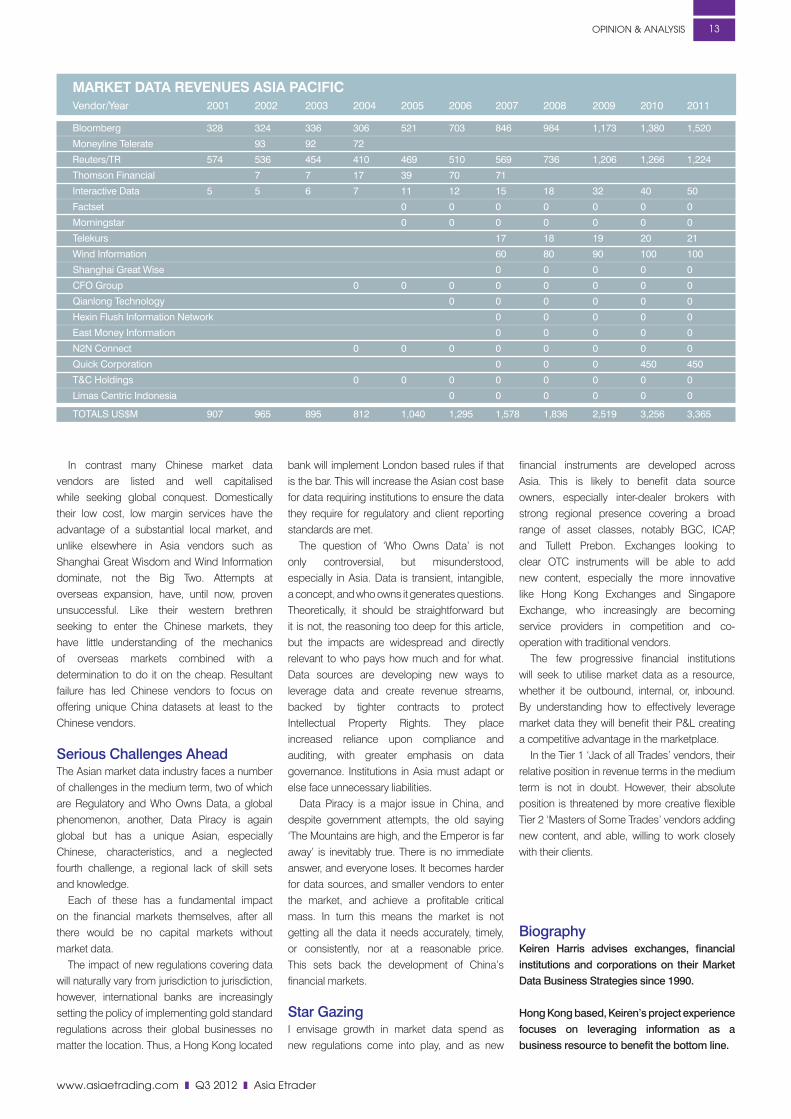

reliable estimates indicate growth for 16 leading vendors from US$2.241 Billion in 2007 to US$3.742 Billion in 2011. This excludes the many privately held vendors, exchanges and brokers, as well as other sources.

As terminal based services and applications revenue in Asia has apparently remained static, where does the market growth come from? Naturally we must look to developments in the financial markets themselves. Since 2007 increased electronic trading in liquid and open markets where global institutions have access has driven the data boom.

Increasingly liquidity not only drives data demand in the front office it fuels enterprise wide requirements from trade to post trade. The expansion of Asian electronic trading and Direct Market Access (DMA) generates an increased need for feeds, with the corollary requirement for reference data and evaluated pricing services. One feeding the other, so the same data can be put to multiple uses, and often charged multiple times as well.

Like in other global financial centres data usage has expanded from the Front Office throughout the business, and with increased use comes higher costs meaning for many institutions Market Data is now the third largest cost line item. This has meant institutions view Market Data as a cost to be managed, not a resource to be leveraged to benefit the business, as many institutions generate their own data, rarely seeking to exploit it, nor appreciating what is happening to their own data internally or externally.

Regional AspirationsBloomberg and Thomson Reuters overwhelmingly have dominated increasing their market share from 66.3% to 73.3%. The reason for this success? Comprehensive data coverage globally especially for OTC markets, via B-Pipe and Datascope products able to meet existing institutional client demand for expanding electronic trading and enterprise data usage. Arguably this is the fastest and strongest growing regional market segment, where competition, especially from Tier 2 global vendors has been weak, and exacerbated by poorer Asian OTC coverage.

Fortunately for Tier 2 vendors, they have prospered where Bloomberg and Thomson Reuters are traditionally weak, especially for

reference data and evaluated pricing. This is aided by institutions wary of the overwhelming dominance of the Big Two as well as an increasing amount of customer dissatisfaction with these vendors. This is generated by a perception of arrogance and high costs for Bloomberg, and the eternal internal collision of the Thomson/Reuters merger combined with a bewilderingly poorly supported product line up.

While Bloomberg’s and Thomson Reuters’ terminal services are not likely to be seriously challenged in the medium term, despite the efforts of the likes of Sungard’s ‘MarketMap’, their overall dominance is not sustainable as the market reaches saturation point.

Tier 2 vendors are increasing content coverage, while leveraging lower cost bases with more flexible market approaches to transition from the reference data space into offering competitive data feeds, where institutions require a second feed to back up Bloomberg and/or Thomson Reuters. The latter has left itself in a weaker position. Bloomberg’s move to open source instrument codes while Thomson Reuters labours in a somewhat dinosaur attempt to keep its RICS proprietary means the likes of IDC, already mapping to Bloomberg codes, can make displacing Thomson Reuters a less painful process than removing Bloomberg in the key datafeed market.

Local ExpectationsAcross Asia, there are many small privately held local vendors focusing on domestic equity markets with a retail oriented client bases, offering low cost, low margin, yet relatively sophisticated terminal based applications with market depth not distributed by global vendors. However, with few exceptions they are blighted by business blindness, unwilling to invest in new content or datafeeds with limited development strategies. Unattractive to potential buyers, and owner egos discouraging consolidation make it difficult to predict these vendors’ long term potential.

As usual Japan is an exception, despite stagnant domestic markets, it supports an almost universal vendor, Nikkei owned Quick Corporation with its loyal Japanese client base. Past failed attempts at overseas expansion has limited Quick to Japan placing a cap on growth, but not aggressive competition from global vendors attracted by the high fee environment.

Market data With asian Characteristics By Keiren Harris

TO SUBSCRIBE:

http://www.asiaetrading.com/asia-etrader-magazine/

Email:[email protected]

www.asiaetrading.com z Q3 2012 z asia etrader

oPinion & analYSiS 13

In contrast many Chinese market data vendors are listed and well capitalised while seeking global conquest. Domestically their low cost, low margin services have the advantage of a substantial local market, and unlike elsewhere in Asia vendors such as Shanghai Great Wisdom and Wind Information dominate, not the Big Two. Attempts at overseas expansion, have, until now, proven unsuccessful. Like their western brethren seeking to enter the Chinese markets, they have little understanding of the mechanics of overseas markets combined with a determination to do it on the cheap. Resultant failure has led Chinese vendors to focus on offering unique China datasets at least to the Chinese vendors.

Serious Challenges AheadThe Asian market data industry faces a number of challenges in the medium term, two of which are Regulatory and Who Owns Data, a global phenomenon, another, Data Piracy is again global but has a unique Asian, especially Chinese, characteristics, and a neglected fourth challenge, a regional lack of skill sets and knowledge.

Each of these has a fundamental impact on the financial markets themselves, after all there would be no capital markets without market data.

The impact of new regulations covering data will naturally vary from jurisdiction to jurisdiction, however, international banks are increasingly setting the policy of implementing gold standard regulations across their global businesses no matter the location. Thus, a Hong Kong located

bank will implement London based rules if that is the bar. This will increase the Asian cost base for data requiring institutions to ensure the data they require for regulatory and client reporting standards are met.

The question of ‘Who Owns Data’ is not only controversial, but misunderstood, especially in Asia. Data is transient, intangible, a concept, and who owns it generates questions. Theoretically, it should be straightforward but it is not, the reasoning too deep for this article, but the impacts are widespread and directly relevant to who pays how much and for what. Data sources are developing new ways to leverage data and create revenue streams, backed by tighter contracts to protect Intellectual Property Rights. They place increased reliance upon compliance and auditing, with greater emphasis on data governance. Institutions in Asia must adapt or else face unnecessary liabilities.

Data Piracy is a major issue in China, and despite government attempts, the old saying ‘The Mountains are high, and the Emperor is far away’ is inevitably true. There is no immediate answer, and everyone loses. It becomes harder for data sources, and smaller vendors to enter the market, and achieve a profitable critical mass. In turn this means the market is not getting all the data it needs accurately, timely, or consistently, nor at a reasonable price. This sets back the development of China’s financial markets.

Star GazingI envisage growth in market data spend as new regulations come into play, and as new

financial instruments are developed across Asia. This is likely to benefit data source owners, especially inter-dealer brokers with strong regional presence covering a broad range of asset classes, notably BGC, ICAP, and Tullett Prebon. Exchanges looking to clear OTC instruments will be able to add new content, especially the more innovative like Hong Kong Exchanges and Singapore Exchange, who increasingly are becoming service providers in competition and co-operation with traditional vendors.

The few progressive financial institutions will seek to utilise market data as a resource, whether it be outbound, internal, or, inbound. By understanding how to effectively leverage market data they will benefit their P&L creating a competitive advantage in the marketplace.

In the Tier 1 ‘Jack of all Trades’ vendors, their relative position in revenue terms in the medium term is not in doubt. However, their absolute position is threatened by more creative flexible Tier 2 ‘Masters of Some Trades’ vendors adding new content, and able, willing to work closely with their clients.

BiographyKeiren Harris advises exchanges, financial institutions and corporations on their Market Data Business Strategies since 1990. Hong Kong based, Keiren’s project experience focuses on leveraging information as a business resource to benefit the bottom line.

MARKET DATA REVENUES ASIA PACIFIC Vendor/Year 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Bloomberg 328 324 336 306 521 703 846 984 1,173 1,380 1,520

Moneyline Telerate 93 92 72

Reuters/TR 574 536 454 410 469 510 569 736 1,206 1,266 1,224

Thomson Financial 7 7 17 39 70 71

Interactive Data 5 5 6 7 11 12 15 18 32 40 50

Factset 0 0 0 0 0 0 0

Morningstar 0 0 0 0 0 0 0

Telekurs 17 18 19 20 21

Wind Information 60 80 90 100 100

Shanghai Great Wise 0 0 0 0 0

CFO Group 0 0 0 0 0 0 0 0

Qianlong Technology 0 0 0 0 0 0

Hexin Flush Information Network 0 0 0 0 0

East Money Information 0 0 0 0 0

N2N Connect 0 0 0 0 0 0 0 0

Quick Corporation 0 0 0 450 450

T&C Holdings 0 0 0 0 0 0 0 0

Limas Centric Indonesia 0 0 0 0 0 0

TOTALS US$M 907 965 895 812 1,040 1,295 1,578 1,836 2,519 3,256 3,365

asia etrader z Q3 2012 z www.asiaetrading.com

Cover STorY 214

High Frequency Traders are drawn to a market under certain specific conditions generally comprising of low cost execution fees (sometimes rebated), low market impact

costs (liquidity), low clearing fees and tax. Other sunk costs include connectivity, rack space at a colocation or proximity facility, hardware, software for trading, for risk, developers to build the algorithms and real time streaming tick data captured in a large database. The exchange’s trading platform must be able to process thousands of order per second capable of matching trades within 100 microseconds or less. When taking all of these elements into account does HFT really take place in Asia?

The short answer is that High Frequency Trading does go on in Asia. There is a misconception that, largely rendered by an uninformed media, HFT is the domain of equity trading alone brought on by exchange competition and fueling fragmentation. The reality is that it is a multi-asset class pursuit attracting those that can afford to be the fastest.

One of the oldest HFT strategies is market making. The dealer markets like Nasdaq before RegNMS was a hive of computer driven trading where the market maker earns her money by capturing the spread; buying at the bid and selling at the offer all day. Another long time HFT strategy found in options market making are what are called reversals and conversions. These strategies are borne from a concept known as put-call parity where the value of a call option, at one strike price, implies a certain fair value for the put at the same strike price. Any deviation from this relationship would generate an arbitrage opportunity. There is plenty of finance literature that can explain this concept in detail. More recently, because of exchange competition, arbitrage between two or more venues has presented an opportunity for HFT strategies where buying in one venue and selling in another venue at a profit can be achieved. HFT within the derivatives space is all over Asia – Korea’s KOSPI, India’s NIFTY, Osaka’s Nikkei and Australia’s SPI to name just a few but what of HFT in the equity markets?

The Truth about hFT in asiaHigh Frequency Trading (HFT) is a difficult to define trading method but is universally accepted as requiring huge amounts of real-time tick data, hardware to process the data which feeds the algorithms affecting a trading decision sending an order over as short as possible length of fibre to a central order book. Positions are typically held for seconds or minutes and the trader goes home at the end of the day with no exposure to the market.

TO SUBSCRIBE:

http://www.asiaetrading.com/asia-etrader-magazine/

Email:[email protected]

www.asiaetrading.com z Q3 2012 z asia etrader

Cover STorY 2 15

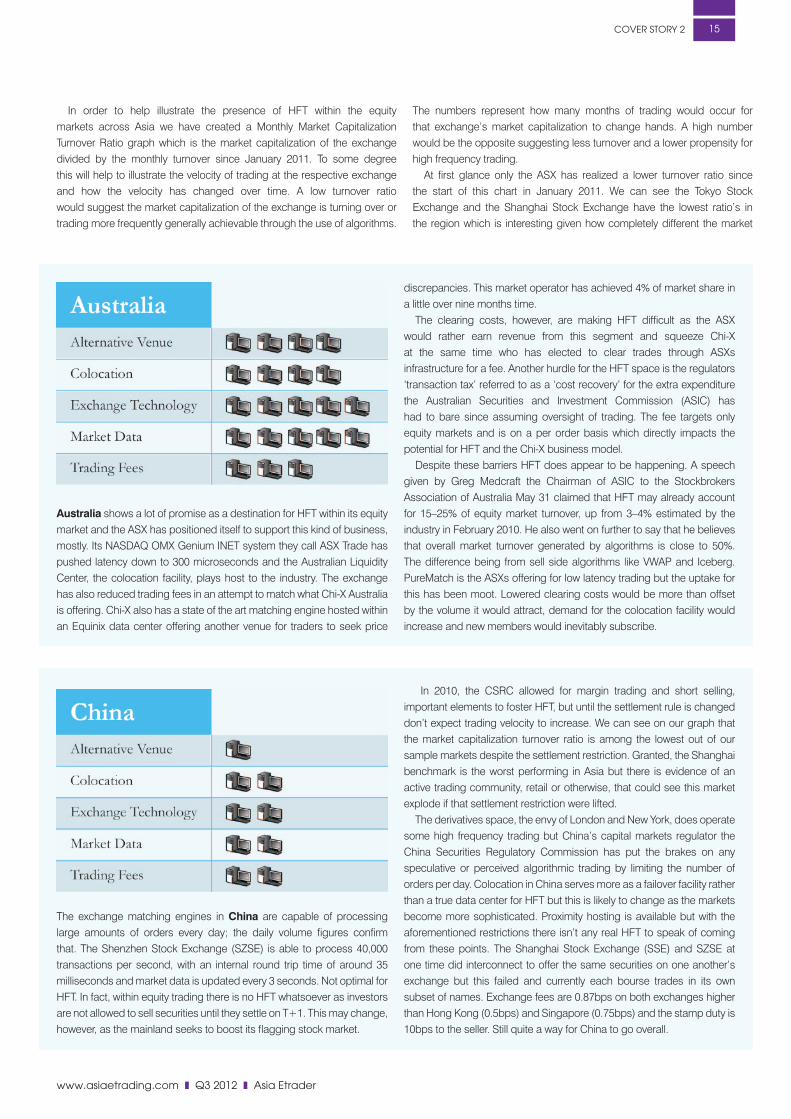

Australia shows a lot of promise as a destination for HFT within its equity market and the ASX has positioned itself to support this kind of business, mostly. Its NASDAQ OMX Genium INET system they call ASX Trade has pushed latency down to 300 microseconds and the Australian Liquidity Center, the colocation facility, plays host to the industry. The exchange has also reduced trading fees in an attempt to match what Chi-X Australia is offering. Chi-X also has a state of the art matching engine hosted within an Equinix data center offering another venue for traders to seek price

discrepancies. This market operator has achieved 4% of market share in a little over nine months time.

The clearing costs, however, are making HFT difficult as the ASX would rather earn revenue from this segment and squeeze Chi-X at the same time who has elected to clear trades through ASXs infrastructure for a fee. Another hurdle for the HFT space is the regulators ‘transaction tax’ referred to as a ‘cost recovery’ for the extra expenditure the Australian Securities and Investment Commission (ASIC) has had to bare since assuming oversight of trading. The fee targets only equity markets and is on a per order basis which directly impacts the potential for HFT and the Chi-X business model.

Despite these barriers HFT does appear to be happening. A speech given by Greg Medcraft the Chairman of ASIC to the Stockbrokers Association of Australia May 31 claimed that HFT may already account for 15–25% of equity market turnover, up from 3–4% estimated by the industry in February 2010. He also went on further to say that he believes that overall market turnover generated by algorithms is close to 50%. The difference being from sell side algorithms like VWAP and Iceberg. PureMatch is the ASXs offering for low latency trading but the uptake for this has been moot. Lowered clearing costs would be more than offset by the volume it would attract, demand for the colocation facility would increase and new members would inevitably subscribe.

The exchange matching engines in China are capable of processing large amounts of orders every day; the daily volume figures confirm that. The Shenzhen Stock Exchange (SZSE) is able to process 40,000 transactions per second, with an internal round trip time of around 35 milliseconds and market data is updated every 3 seconds. Not optimal for HFT. In fact, within equity trading there is no HFT whatsoever as investors are not allowed to sell securities until they settle on T+1. This may change, however, as the mainland seeks to boost its flagging stock market.

In 2010, the CSRC allowed for margin trading and short selling, important elements to foster HFT, but until the settlement rule is changed don’t expect trading velocity to increase. We can see on our graph that the market capitalization turnover ratio is among the lowest out of our sample markets despite the settlement restriction. Granted, the Shanghai benchmark is the worst performing in Asia but there is evidence of an active trading community, retail or otherwise, that could see this market explode if that settlement restriction were lifted.

The derivatives space, the envy of London and New York, does operate some high frequency trading but China’s capital markets regulator the China Securities Regulatory Commission has put the brakes on any speculative or perceived algorithmic trading by limiting the number of orders per day. Colocation in China serves more as a failover facility rather than a true data center for HFT but this is likely to change as the markets become more sophisticated. Proximity hosting is available but with the aforementioned restrictions there isn’t any real HFT to speak of coming from these points. The Shanghai Stock Exchange (SSE) and SZSE at one time did interconnect to offer the same securities on one another’s exchange but this failed and currently each bourse trades in its own subset of names. Exchange fees are 0.87bps on both exchanges higher than Hong Kong (0.5bps) and Singapore (0.75bps) and the stamp duty is 10bps to the seller. Still quite a way for China to go overall.

In order to help illustrate the presence of HFT within the equity markets across Asia we have created a Monthly Market Capitalization Turnover Ratio graph which is the market capitalization of the exchange divided by the monthly turnover since January 2011. To some degree this will help to illustrate the velocity of trading at the respective exchange and how the velocity has changed over time. A low turnover ratio would suggest the market capitalization of the exchange is turning over or trading more frequently generally achievable through the use of algorithms.

The numbers represent how many months of trading would occur for that exchange’s market capitalization to change hands. A high number would be the opposite suggesting less turnover and a lower propensity for high frequency trading.

At first glance only the ASX has realized a lower turnover ratio since the start of this chart in January 2011. We can see the Tokyo Stock Exchange and the Shanghai Stock Exchange have the lowest ratio’s in the region which is interesting given how completely different the market

asia etrader z Q3 2012 z www.asiaetrading.com

“Xxxxxxxx”

Cover STorY 216

Hong Kong is not a suitable HFT environment for the most part. The cost of trading, clearing and the government stamp duty makes trading the spread a loss making venture. The matching engine is the slowest in developed Asia (Thailand is faster) and there isn’t a colocation facility to speak of yet though proximity services are plentiful. The latter two points are to be rectified by the HKEx in Q3 with the new Tsuen Kwan O data centre but this will do little to fan the HFT flames given the hefty relative cost of trading. There are bright spots in the derivatives space

– the warrant market which are bank issued and the Hang Seng index options – but within equities it’s a difficult proposition. The government’s 10bps stamp duty is a real drag on trading but generates a significant proportion of the city’s income. In order for Hong Kong to eliminate this tax they would have to seek revenue in other places such as income tax which could hurt the SARs standing as a low tax business centre.

There is a line of thinking that if the stamp duty were cut then more trading would arise offsetting the revenue deficit. It could also attract highly skilled workers in the trading space who could then be taxed and spend their incomes locally. In recent days there has been an exodus of highly skilled traders and their highly paid jobs from Hong Kong. IMC, the Amsterdam-based trading firm, all but closed down their office in Hong Kong retaining a skeleton staff as a regulatory requirement, relocating key personal to Australia and their Netherlands headquarters. All Options, headed by Ralph Van Put, another Dutch trader shut its doors last year and Optiver, another algo-centric trading firm also has its regional headquarters in Australia.

On the subject of exchange competition there isn’t much to say. Unless the Hong Kong government lifts the monopoly the HKEx enjoys we won’t see much of any professional trading outside the warrants market or long-only fund managers putting in to question the validity that Hong Kong is an international financial center.

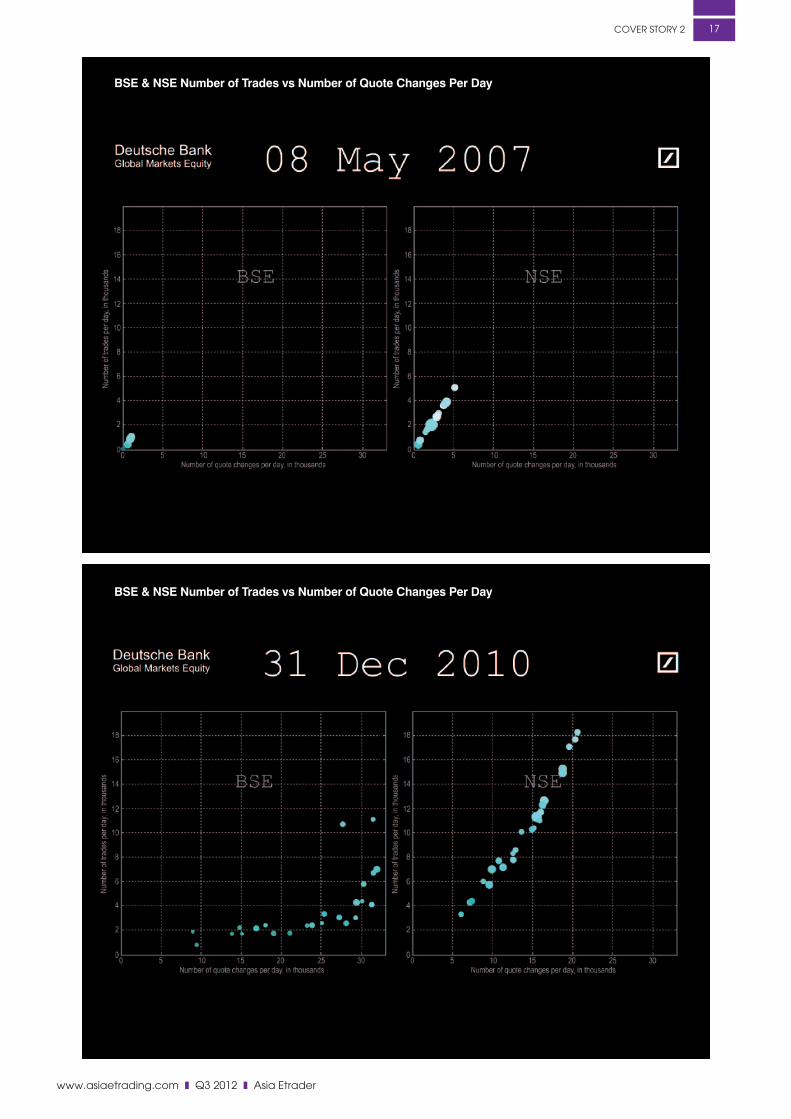

Since the Securities and Exchange Board of India (SEBI) permitted DMA in April 2008 there has been a large uptake of algorithmic trading on the sub-continent. We can illustrate the market structure changes that have occurred pre- and post-DMA. Graph A and B show a time series of quotes vs trades with the BSE on the left and the NSE on the right. The X-axis shows the number of quote changes per day and the Y-axis shows the number of trades per day. In May 2007, almost one year before DMA was introduced we can see that the ratio of trades to quotes is 5 to 1 in favour of the NSE. Graph B skips ahead to December 31, 2010 more than 18 months after the introduction of DMA revealing a resounding change in the India market.

While both of the exchanges liquidity profiles have changed dramatically the BSEs has been more extensive as the number of

quotes have increased substantially clearly indicative of automated market making and other algorithmic trading strategies. The BSE has no restriction on how many times quotes can be updated each day but the NSE does when the order to trade ratio exceeds 500 to 1 generating a denial of service fee when breeched.

At the heart of the NSE is its matching engine which has been benchmarked at 250 microseconds serving 100,000 messages per second. Five years ago the exchange was handling about 30 million messages per day and today that figure has jumped 10 fold to 300 million messages per day.

It is estimated that algo trading on the BSE is about 8-10 percent of all volume and the NSE is higher at around 15-20% in the equities segment.

There are some structural problems in India that do make it difficult to trade across exchanges and one of them is the clearing. Each exchange has their own clearing house where trades must settle through and no netting occurs between clearing houses forcing participants to carry two margins. Another factor preventing cross exchange arbitrage is that the cost of connecting to both the exchanges and building a Smart Order Router is too high so brokers prefer to connect to the former where most of the liquidity resides. This is expected to be further burdensome to the industry as the MCX-SX is lobbying SEBI for its equities market license which it was denied last year and the arrival of the Delhi Exchange, a platform for HFT, is expected very soon.

Each exchange does have a collocation facility and offers streaming tick data. Once the clearing issue is resolved and trading costs are reduced this will be a very exciting market.

“The reality is that HFT is a multi-asset class pursuit attracting

those that can afford to be the fastest.”

TO SUBSCRIBE:

http://www.asiaetrading.com/asia-etrader-magazine/

Email:[email protected]

www.asiaetrading.com z Q3 2012 z asia etrader

Cover STorY 2 17

BSE & NSE Number of Trades vs Number of Quote Changes Per Day

BSE & NSE Number of Trades vs Number of Quote Changes Per Day

asia etrader z Q3 2012 z www.asiaetrading.com

Cover STorY 218

Since the Arrowhead launch in January 2010 HFT, at least in equities, has been growing. Inter-venue arbitrage which drives fragmentation has seen the largest portion of HFT strategies. Volumes have been moving from the primary TSE to Chi-X and SBI Japannext with the PTSs achieving a record 6 percent of market share last January. There are obvious reasons for the onset of HFT in that market, new exchange technology, equally cutting edge hardware at the PTSs, the JSCC now clearing PTS trades lowering costs and eliminating counterparty risk and colocation facilities available at each venue. If we look to the Percentage of TSE Colo Orders graph the percentage of orders originating in the colo site for cash equities continues to trend upward. This does support the idea

the HFT is indeed growing in Japan. We have heard that 30%-40% of turnover on the TSE is HFT but this has not been confirmed or supported with any data. The monthly turnover ratio is difficult to determine if HFT trading is supported as the data is skewed by the Tsunami shock in March 2011 and the US credit rating downgrade also last year in August.

Market share on the PTSs is expected to continue to grow as the Japan FSA has recently removed one of the key barriers for the PTS and that is the Takeover Bid Rule. (See Fragmentation Footprint article for more on that). Another factor that will push fragmentation and HFT further is that the TSE offers a 1 yen tick size on its securities but the PTSs a 1/10 of 1 yen tick size which has favoured the alternative venues. The TSE could lower its tick size but isn’t likely to as Japan’s financial industry’s technology would need to upgrade their systems in order to cope with the fractional tick sizes. For the time being the PTSs have a tick size advantage and will attract more inter-venue HFT arbitrage.

The Osaka exchange’s flagship Nikkei 225 futures have been the focus of a great deal of HFT for quite some time. Newedge is the largest member on the OSE and services the most market makers trading that future. Trading strategies range from reversals and conversions, index basket trading and arbitrage between the SGX listed Nikkei and the CME listed Nikkei futures. Given the long geographical distances between matching engines – 67 milliseconds between Tokyo and Singapore and 128 milliseconds to Chicago – relatively speaking this would not necessarily be fast but high in frequency.

TO SUBSCRIBE:

http://www.asiaetrading.com/asia-etrader-magazine/

Email:[email protected]

www.asiaetrading.com z Q3 2012 z asia etrader

Cover STorY 2 19

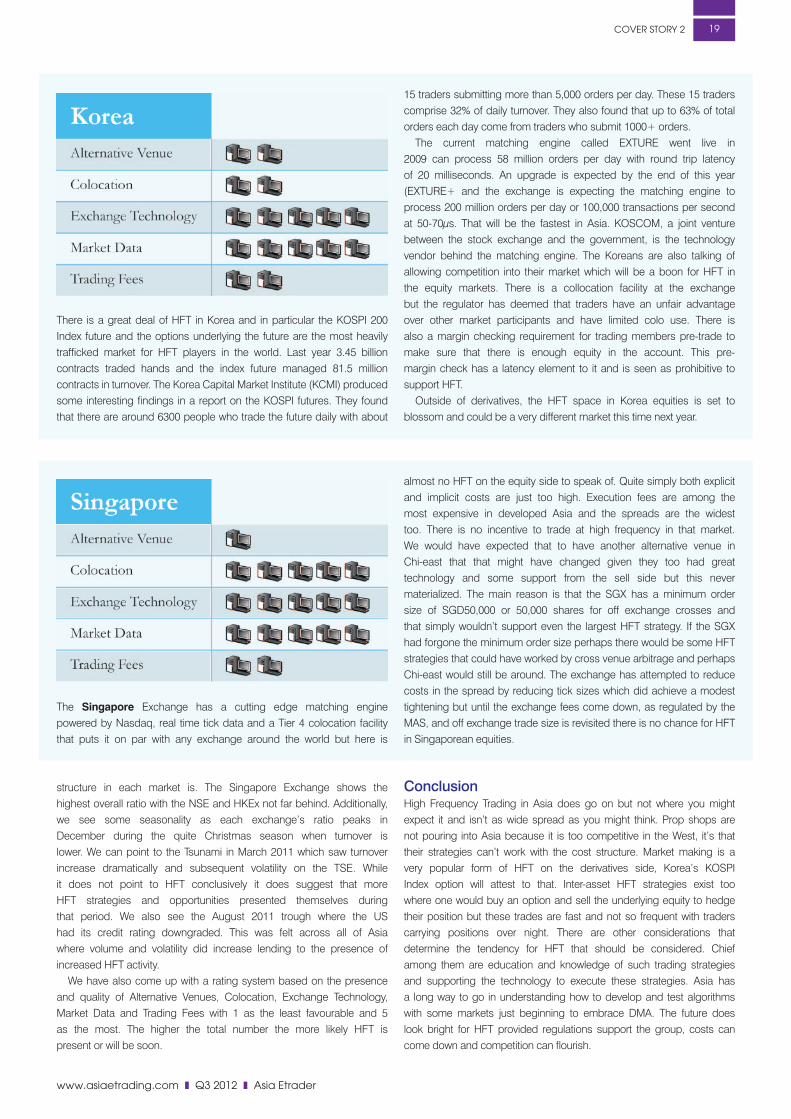

There is a great deal of HFT in Korea and in particular the KOSPI 200 Index future and the options underlying the future are the most heavily trafficked market for HFT players in the world. Last year 3.45 billion contracts traded hands and the index future managed 81.5 million contracts in turnover. The Korea Capital Market Institute (KCMI) produced some interesting findings in a report on the KOSPI futures. They found that there are around 6300 people who trade the future daily with about

15 traders submitting more than 5,000 orders per day. These 15 traders comprise 32% of daily turnover. They also found that up to 63% of total orders each day come from traders who submit 1000+ orders.

The current matching engine called EXTURE went live in 2009 can process 58 million orders per day with round trip latency of 20 milliseconds. An upgrade is expected by the end of this year (EXTURE+ and the exchange is expecting the matching engine to process 200 million orders per day or 100,000 transactions per second at 50-70μs. That will be the fastest in Asia. KOSCOM, a joint venture between the stock exchange and the government, is the technology vendor behind the matching engine. The Koreans are also talking of allowing competition into their market which will be a boon for HFT in the equity markets. There is a collocation facility at the exchange but the regulator has deemed that traders have an unfair advantage over other market participants and have limited colo use. There is also a margin checking requirement for trading members pre-trade to make sure that there is enough equity in the account. This pre-margin check has a latency element to it and is seen as prohibitive to support HFT.

Outside of derivatives, the HFT space in Korea equities is set to blossom and could be a very different market this time next year.

The Singapore Exchange has a cutting edge matching engine powered by Nasdaq, real time tick data and a Tier 4 colocation facility that puts it on par with any exchange around the world but here is

almost no HFT on the equity side to speak of. Quite simply both explicit and implicit costs are just too high. Execution fees are among the most expensive in developed Asia and the spreads are the widest too. There is no incentive to trade at high frequency in that market. We would have expected that to have another alternative venue in Chi-east that that might have changed given they too had great technology and some support from the sell side but this never materialized. The main reason is that the SGX has a minimum order size of SGD50,000 or 50,000 shares for off exchange crosses and that simply wouldn’t support even the largest HFT strategy. If the SGX had forgone the minimum order size perhaps there would be some HFT strategies that could have worked by cross venue arbitrage and perhaps Chi-east would still be around. The exchange has attempted to reduce costs in the spread by reducing tick sizes which did achieve a modest tightening but until the exchange fees come down, as regulated by the MAS, and off exchange trade size is revisited there is no chance for HFT in Singaporean equities.

structure in each market is. The Singapore Exchange shows the highest overall ratio with the NSE and HKEx not far behind. Additionally, we see some seasonality as each exchange’s ratio peaks in December during the quite Christmas season when turnover is lower. We can point to the Tsunami in March 2011 which saw turnover increase dramatically and subsequent volatility on the TSE. While it does not point to HFT conclusively it does suggest that more HFT strategies and opportunities presented themselves during that period. We also see the August 2011 trough where the US had its credit rating downgraded. This was felt across all of Asia where volume and volatility did increase lending to the presence of increased HFT activity.

We have also come up with a rating system based on the presence and quality of Alternative Venues, Colocation, Exchange Technology, Market Data and Trading Fees with 1 as the least favourable and 5 as the most. The higher the total number the more likely HFT is present or will be soon.

ConclusionHigh Frequency Trading in Asia does go on but not where you might expect it and isn’t as wide spread as you might think. Prop shops are not pouring into Asia because it is too competitive in the West, it’s that their strategies can’t work with the cost structure. Market making is a very popular form of HFT on the derivatives side, Korea’s KOSPI Index option will attest to that. Inter-asset HFT strategies exist too where one would buy an option and sell the underlying equity to hedge their position but these trades are fast and not so frequent with traders carrying positions over night. There are other considerations that determine the tendency for HFT that should be considered. Chief among them are education and knowledge of such trading strategies and supporting the technology to execute these strategies. Asia has a long way to go in understanding how to develop and test algorithms with some markets just beginning to embrace DMA. The future does look bright for HFT provided regulations support the group, costs can come down and competition can flourish.

asia etrader z Q3 2012 z www.asiaetrading.com

Derivatives trading in China and India have seen huge growth over the years and is the envy of the West

and the Japanese who have missed out on the global commodities boom entirely. Rising affluence and global trade are seen as the primary causes for fueling Asia’s commodity bread basket. Though notional volumes are small and reflect individual purchasing power, appetite for futures trading continues to evolve along with the sophistication of players who seek new ways to hedge risk, speculate and access other time zones and markets. The first half of 2012 saw the addition of no less than ten new listed futures products across Asia in currency, precious metals, interest rate, index and volatility derivatives. And that’s not all, more contracts have been announced for the second half building on the momentum in one of the few bright spots in the trading business.

Trading Volumes Incite ChangeIncreasing and sometimes record-setting trading volume at exchanges have precipitated bourse’s to update and add new products. Uncertainty and volatility in financial markets around the globe have been the drivers for increased hedging activity and the resulting higher trading volume. Bursa Malaysia’s derivatives (BMD) segment and the Tokyo Stock Exchange (TSE) have each seen new records in terms of turnover. On 16 May, BMD reported that 77,703 contracts changed hands that day with their crude palm oil (FCPO) contract comprising 63,019 units of that total. Also, five days later on 21 May the exchange re-introduced options underlying the KLCI future in an attempt to broaden trading strategies amongst local participants. The options are also listed on CME’s Globex platform as well to tap into international players.

The OSE made some modifications too by improving its strategy trading allowing these order types to be placed during the opening auction in addition to the regular session. They also plan to reduce the tick size for the Nikkei 225 future from 5 yen to 1 yen with both of these changes set to take effect 26 November.

In an effort to reduce retail participation the Korea Exchange increased the multiplier of the KOSPI index option, the world’s largest

traded derivative, from 100,000 to 500,000. The regulator believes that retail participants are at risk of losing too much money and they have stepped in to curb these players. Conversely, Eurex’s night session KOSPI option hit a volume record this quarter as well.

The Tokyo Stock Price Index (TOPIX) at the TSE has also reported record volumes early this year and on the 7 June the Japan Government Bond (JGB) saw a new one-day high with more than 102,000 contracts turning over.

Currency FuturesEveryone, now it seems, wants to access the currency market with Thailand, the HKEx and Indonesia joining the club now offering their own futures. The Thailand Futures Exchange (TFEX) last month launched its US dollar futures. The new product, underlying US1,000, will provide Thai investors the ability to hedge Thai baht through derivatives and access to the multi-trillion dollar currency market. For now, investors must be of Thai nationality or a resident of Thailand.

In its effort to position itself as the center for offshore RMB trading the HKEx announced the arrival of the Renminbi currency future. Scheduled for the third quarter of this year, the product will be the first exchange-traded currency futures settled in RMB. At expiration, the seller will be required to deliver US dollars

to the buyer who makes payment of the final settlement value in RMB to the seller. Contracts will be quoted in RMB per USD and margined in RMB where the final settlement price will be based on the spot USD/RMB fixing published by the Treasury Market Association at 11:15 am on the last trading day (two business days before the third Wednesday of the month).

Indonesia’s Commodity and Derivatives Exchange will launch 27 new currency pairs this quarter to facilitate a growing need by industry to hedge. These will be the first financial contracts ever listed on the bourse as this nation raises the bar and begins its ascent to becoming a regional financial center.

Volatility Index FuturesBoth the Osaka Securities Exchange (OSE) and the HKEx introduced volatility index futures this year.

The Nikkei 225 VI is based on the Nikkei Stock Average Volatility Index and is calculated by using prices from the Nikkei 225 futures and its underlying options. This cash-settled contract trades out for eight months, has a multiplier of 10,000 Yen and is available to trade as a spread. As of March 10, 2012 the US under CFTC Rule 30.13 allowed this product to be sold to US investors.

The HSI Volatility Index (VHSI) future began trading in February and has a tick size about six times larger than the OSE’s version. Subscribing to the CBOE’s VIX methodology this contract will help in pricing options, hedge risk and manage volatility in a market that tends to have higher volatility than most in Asia. Hong Kong index option volume is quite low and this product should help turnover in that market.

Stock Index FuturesIn addition to the volatility future, the OSE introduced a Dow Jones Industrial Average (DJIA) index future. OSE DJIA futures underly the same index as the DJIA futures traded on the Chicago Board of Trade (CBOT) but have a different trading currency which means the contracts do not necessarily trade at the same price. This allows for arbitrage of both these products much like the US- and Yen-based Nikkei 225 also on the CME. Furthermore, it allows the local Japanese market access to the US market in their local currency.

asia’s increasing appetite for Futures Trading

derivaTiveS20

“Volatility in financial

markets around the

globe have been the

drivers for increased

hedging activity and

the resulting higher