DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, LEGAL ENTITY DISCLOSURE AND ANALYST CERTIFICATIONS. Asia in 2017 Trump, trade and rates March 2017 Fixed Income Analyst, + 65 6212 3412, [email protected]Ray Farris, Head of Fixed Income Research and Economics, Asia Pacific

Transcript

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, LEGAL ENTITY DISCLOSURE AND ANALYST CERTIFICATIONS.

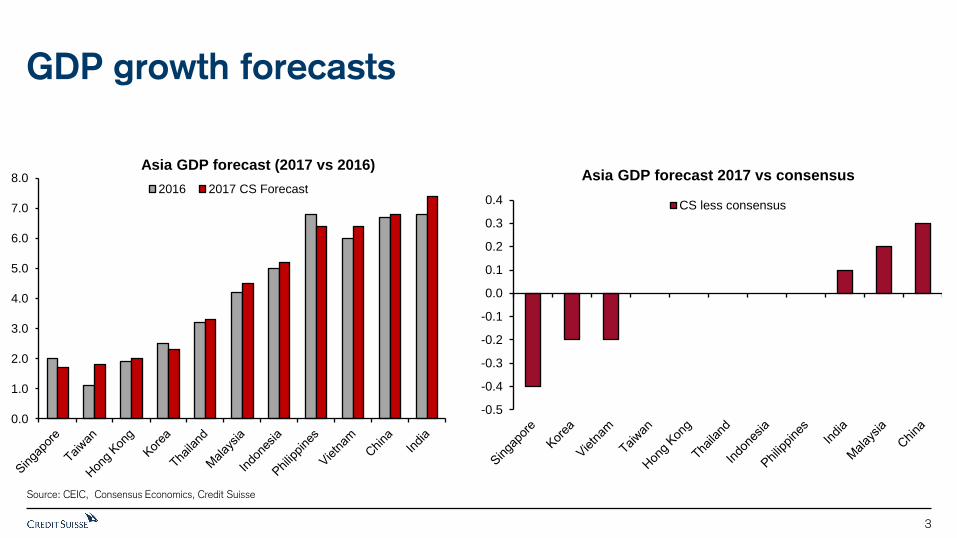

Inflation higher but not high so central banks likely steady

We expect only the Philippines to hike rates in 2017, and China to continue tightening liquidity

8

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Asia Inflation yoy 2016 vs 2017F

2016 2017F

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

VN TW ID MY IN PH KR SG CH TH HK

CPI expected deviation from target/forecasts 2017*

*We use central bank forecasts and targets for 2017 where available. We have used long-term average CPI for China and Hong Kong Source: CEIC, Credit Suisse

Theme 2: ASEAN’s pivot to China

Month Day, Year LEGAL ENTITY, department or author (Click Insert | Header & Footer)

Tighter immigration control – policy has tightened and more is in the

pipeline; Vietnam and the Philippines will be hit the most via remittances

US border adjustment tax would be highly disruptive for Asian

economies via trade and/or USD surge

Higher US inflation and more hawkish Fed. Asian economies are much

better positioned to withstand the shocks now vs 2013

14

Immigration policy change: Philippines and Vietnam at risk

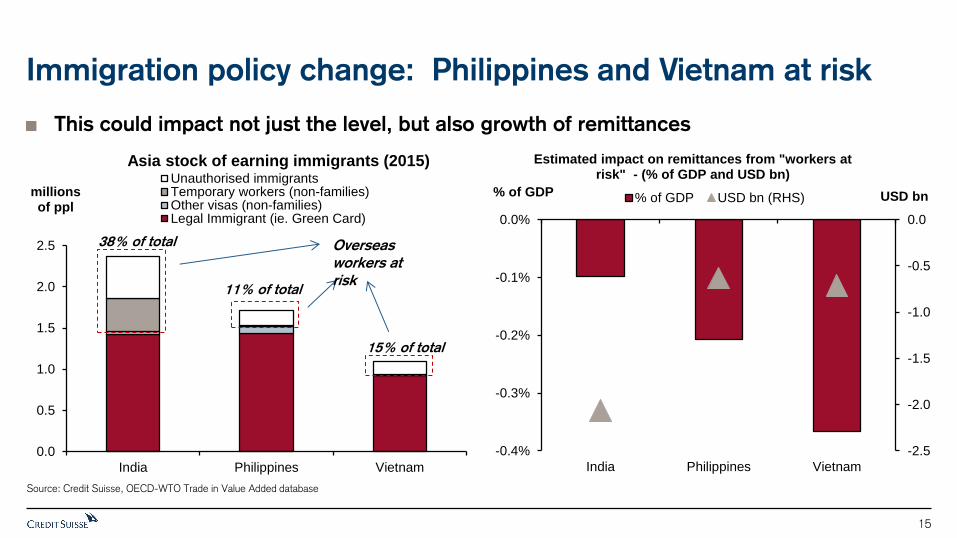

This could impact not just the level, but also growth of remittances

15

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

-0.4%

-0.3%

-0.2%

-0.1%

0.0%

India Philippines Vietnam

USD bn % of GDP

Estimated impact on remittances from "workers at risk" - (% of GDP and USD bn)

% of GDP USD bn (RHS)

0.0

0.5

1.0

1.5

2.0

2.5

India Philippines Vietnam

millions of ppl

Asia stock of earning immigrants (2015) Unauthorised immigrantsTemporary workers (non-families)Other visas (non-families)Legal Immigrant (ie. Green Card)

Overseas

workers at

risk

38% of total

11% of total

15% of total

Source: Credit Suisse, OECD-WTO Trade in Value Added database

US Border Adjusted Tax could prove highly disruptive for Asia

Import price in the US could surge 25%, causing sharp downturns in Asian exports

VN, TW, KR, and MY most at risk from US Border Adjusted Tax implementation

16

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

PH CH TW KR VN SG IN TH MY ID ASIA

% share Negative impact to value added goods exports from

US border adjustment tax (% of exports)

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

VN TW KR MY TH PH SG CH ID IN ASIA

% of GDP Negative impact to value added goods exports from US border adjustment tax (% of GDP)

Source: Credit Suisse, OECD-WTO Trade in Value Added database

Asia is better placed to weather higher US rates now vs 2013

17

-5%

0%

5%

10%

15%

20%

25%

CN HK IN ID KR MY PH SG TW TH VN

Asia Current Account (% of GDP)

2013 Latest

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Asia 2y real bond yields

2013 Latest

Source: CEIC, Credit Suisse

Indonesia: More boon for the banks

Month Day, Year LEGAL ENTITY, department or author (Click Insert | Header & Footer)

Indonesia

GDP growth to accelerate to 5.2% in 2017 from 5.0%, reflecting higher commodity prices,

and the lagged impact of rate cuts

Headline inflation to rise to 4.5% in 2017 from 3.5%, but mainly due to subsidy reforms

Bank Indonesia likely to keep policy rates unchanged, but we still see a chance of a 50bps

RRR cut

Current account deficit should narrow to 1.5% of GDP from 1.8%, much better than market

and BI expectations of over 2%

We see good chance of a credit rating upgrade by S&P this year

19

Private consumption should recover further

Lagged impact of lower inflation, interest rates, and stronger commodity prices should

propel private consumption in 2017

20

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0-40

-30

-20

-10

0

10

20

30

40

50

60

2011 2012 2013 2014 2015 2016

Motor Vehicle Sales (% YoY)

Change in lending rates (YoY, inverted, RHS)

-40

-30

-20

-10

0

10

20

30

40

50

60

-60

-40

-20

0

20

40

60

80

2011 2012 2013 2014 2015 2016 2017

Average of palm and rubber prices in IDR (%YoY)

Motor vehicle sales (% yoy, RHS)

Source: Credit Suisse estimates, CEIC

Credit growth should also improve further

Our preferred lead indicators suggest credit growth should improve further

Rebound in commodity prices and lower lending rates suggest NPLs should gradually improve

21

-5

0

5

10

15

20

25

30

35

40

-80

-60

-40

-20

0

20

40

60

80

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Banking survey (change in demand for new loans), 3-qtr lead

Credit growth (% yoy, RHS)-30

-20

-10

0

10

20

30

40-40

-30

-20

-10

0

10

20

30

40

50

60

70

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Palm and rubber in IDR (%yoy)

Total banking system NPL (RHS, inverted scale)

Source: Credit Suisse estimates, CEIC

BI is likely to keep policy rates unchanged

Headline inflation is likely to rise to 4.5% in 2017 from 4.3% in 2016 but due to electricity

subsidy cuts; core to remain stable around its current rate of 3.5%.

Still within target of 3-5% so we don’t expect rate hikes

22

2

3

4

5

6

7

8

9

2010

2011

2012

2013

2014

2015

2016

2017

CPI (% yoy)

Inflation target range 3-5%

2

3

4

5

6

7

8

9

2013

2014

2015

2016

2017

CPI (% yoy) 7-day reverse repo rate (RHS)

Source: BI, Credit Suisse estimates, CEIC

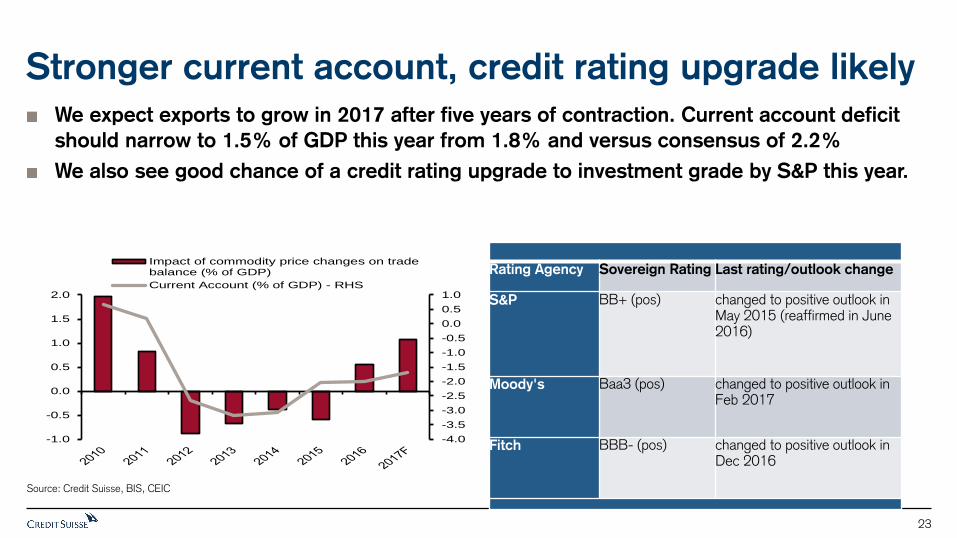

Stronger current account, credit rating upgrade likely

We expect exports to grow in 2017 after five years of contraction. Current account deficit

should narrow to 1.5% of GDP this year from 1.8% and versus consensus of 2.2%

We also see good chance of a credit rating upgrade to investment grade by S&P this year.

23

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Impact of commodity price changes on tradebalance (% of GDP)

Current Account (% of GDP) - RHS

Rating Agency Sovereign Rating Last rating/outlook change

S&P BB+ (pos) changed to positive outlook in May 2015 (reaffirmed in June 2016)

Moody's Baa3 (pos) changed to positive outlook in Feb 2017

Fitch BBB- (pos) changed to positive outlook in Dec 2016

Currency in circulation has been moving higher since January 2017 and the pace of

increase accelerated somewhat recently. We estimate that re-monetisation should

complete by April

46

-7

-6

-5

-4

-3

-2

-1

0

1

2

Nov-16 Dec-16 Jan-17 Feb-17

Monthly change in currency in circulation (INR bn)

2

3

4

5

6

7

8

9

10

11

12

0

5

10

15

20

25

30

Dec-05 Dec-07 Dec-09 Dec-11 Dec-13

M1 (t+1, %yoy)

Quarterly GDP (% yoy, rhs)

Source: Credit Suisse estimates, CEIC

Easy monetary conditions should support credit growth

Higher banking system liquidity has allowed lending rates to fall; this could add 30-40bps

to GDP in 2H' FY2017-18

47

64

66

68

70

72

74

76

78

80

Feb-14 Feb-15 Feb-16 Feb-17

Loan to deposit ratio

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

Feb-14 Feb-15 Feb-16 Feb-17

Deposit rate (1-year, %, average of major banks)

Repo rate (%)

Lending rate (1-year MCLR of ICICI Bank, %)

Source: Credit Suisse estimates, CEIC

Demonetisation gains could boost fiscal spending

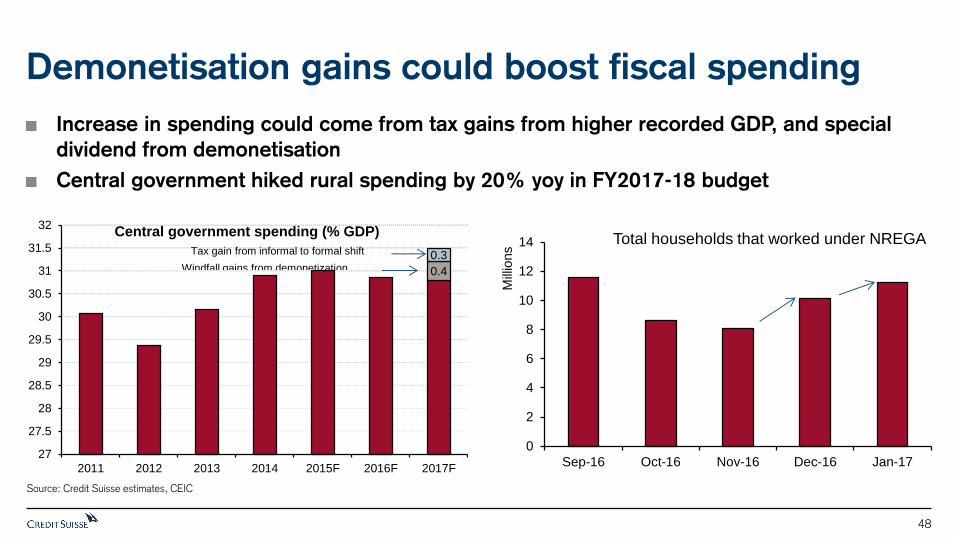

Increase in spending could come from tax gains from higher recorded GDP, and special

dividend from demonetisation

Central government hiked rural spending by 20% yoy in FY2017-18 budget

48

0

2

4

6

8

10

12

14

Sep-16 Oct-16 Nov-16 Dec-16 Jan-17

Mill

ions Total households that worked under NREGA

0.4

0.3

27

27.5

28

28.5

29

29.5

30

30.5

31

31.5

32

2011 2012 2013 2014 2015F 2016F 2017F

Central government spending (% GDP)

Windfall gains from demonetization

Tax gain from informal to formal shift

Source: Credit Suisse estimates, CEIC

RBI is likely to keep policy rates unchanged

Headline inflation is likely to rise slightly over 5.0% in FY2017-18 from 4.6% in FY2016-17

due to pay commission and GST impact

Still within target of 2-6% so we don’t expect rate hikes

49

-1

1

3

5

7

9

11

13

0

5

10

15

20

25

1997 2001 2005 2009 2013 2017

Personal disposable income (%yoy)

Private consumption (%yoy, rhs)

Consumption rise around previous pay commission hikes

6

6.5

7

7.5

8

8.5

9

0

2

4

6

8

10

12

14

Sep-12 Sep-13 Sep-14 Sep-15 Sep-16 Sep-17

CPI (%yoy) Repo rate (%, rhs)

CPI inflation target range 2-

6%

Source: Credit Suisse estimates, CEIC

Current account and macro supportive of INR

We expect current account deficit to widen slightly to 1.4% of GDP next year due to weaker services

trade and remittances . But decline in import intensity should mean CAD is manageable

Better growth-inflation trade off should continue to support the currency

50

8

10

12

14

16

18

20

22

Sep-04 Sep-06 Sep-08 Sep-10 Sep-12 Sep-14 Sep-16

Non-oil import/GDP

-6

-4

-2

0

2

4

6

8

10

12

14

-25

-20

-15

-10

-5

0

5

10

15

20

Sep-2005 Sep-2008 Sep-2011 Sep-2014 Sep-2017

INR/USD (%yoy)

Source: Credit Suisse, CEIC

Disclosure Appendix

51

Analyst Certification The analysts identified in this report each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

Important Global Disclosures Credit Suisse’s research reports are made available to clients through our proprietary research portal on CS PLUS. Credit Suisse research products may also be made available through third-party vendors or alternate electronic means as a convenience. Certain research products are only made available through CS PLUS. The services provided by Credit Suisse’s analysts to clients may depend on a specific client’s preferences regarding the frequency and manner of receiving communications, the client’s risk profile and investment, the size and scope of the overall client relationship with the Firm, as well as legal and regulatory constraints. To access all of Credit Suisse’s research that you are entitled to receive in the most timely manner, please contact your sales representative or go to.https://plus.credit-suisse.com.

Investment principal on bonds can be eroded depending on sale price or market price. In addition, there are bonds on which investment principal can be eroded due to changes in redemption amounts. Care is required when investing in such instruments. When you purchase non-listed Japanese fixed income securities (Japanese government bonds, Japanese municipal bonds, Japanese government guaranteed bonds, Japanese corporate bonds) from CS as a seller, you will be requested to pay the purchase price only.