Australian Financial Markets Association ABN 69 793 968 987 Level 3, Plaza Building, 95 Pitt Street GPO Box 3655 Sydney NSW 2001 Tel: +612 9776 7955 Fax: +61 2 9776 4488 Email: [email protected]Web: www.afma.com.au 9 November 2012 Ms Prashanti Ravindra Senior Lawyer, Strategic Policy Australian Securities and Investments Commission Level 5, 100 Market Street SYDNEY NSW 2000 By email: [email protected]Dear Ms Ravindra ASIC Consultation Paper 189 – Future of Financial Advice: Conflicted remuneration Thank you for the opportunity to provide submissions in response to Consultation Paper 189 – Future of Financial Advice: Conflicted remuneration (CP 189). We have provided comments on some of the specific questions in the consultation paper in the accompanying comments table. Our overarching comments on ASIC’s approach to the conflicted remuneration ban, as set out in the draft guidance, are as follows. 1. Timing and transition to full compliance ASIC’s guidance on conflicted remuneration is one of the core components of our members’ preparations to become fully compliant with the Future of Financial Advice (FOFA) reforms. In hindsight, it would have been preferable for CP 189 to have been released earlier, given that ASIC expects to finalise the guidance in February 2013. A preliminary observation by our members is that there is not much time between finalisation of the guidance and the cut-off date of 1 July 2013 by which all licensees must be fully compliant with FOFA. To the extent there is still any uncertainty about ASIC’s policy position before 1 July 2013, licensees will have to form their own views about whether their remuneration structures comply with the FOFA requirements. This is appropriate given that the statutory obligations rest on the licensee and the advice provider. In addition, there are several regulations yet to be made that are central to deciding how remuneration arrangements should be structured going forward so that they are compliant with FOFA. In the absence of these finalised regulations, it is very difficult for our members to make decisions that take account of how the FOFA regime will apply across their whole business.

Transcript

Australian Financial Markets Association ABN 69 793 968 987

Level 3, Plaza Building, 95 Pitt Street GPO Box 3655 Sydney NSW 2001 Tel: +612 9776 7955 Fax: +61 2 9776 4488

9 November 2012 Ms Prashanti Ravindra Senior Lawyer, Strategic Policy Australian Securities and Investments Commission Level 5, 100 Market Street SYDNEY NSW 2000 By email: [email protected] Dear Ms Ravindra

ASIC Consultation Paper 189 – Future of Financial Advice: Conflicted remuneration

Thank you for the opportunity to provide submissions in response to Consultation Paper 189 – Future of Financial Advice: Conflicted remuneration (CP 189). We have provided comments on some of the specific questions in the consultation paper in the accompanying comments table. Our overarching comments on ASIC’s approach to the conflicted remuneration ban, as set out in the draft guidance, are as follows. 1. Timing and transition to full compliance ASIC’s guidance on conflicted remuneration is one of the core components of our members’ preparations to become fully compliant with the Future of Financial Advice (FOFA) reforms. In hindsight, it would have been preferable for CP 189 to have been released earlier, given that ASIC expects to finalise the guidance in February 2013. A preliminary observation by our members is that there is not much time between finalisation of the guidance and the cut-off date of 1 July 2013 by which all licensees must be fully compliant with FOFA. To the extent there is still any uncertainty about ASIC’s policy position before 1 July 2013, licensees will have to form their own views about whether their remuneration structures comply with the FOFA requirements. This is appropriate given that the statutory obligations rest on the licensee and the advice provider. In addition, there are several regulations yet to be made that are central to deciding how remuneration arrangements should be structured going forward so that they are compliant with FOFA. In the absence of these finalised regulations, it is very difficult for our members to make decisions that take account of how the FOFA regime will apply across their whole business.

In our view, a further transitional period (similar to the Financial Services Reform Act and other reforms in relation to superannuation) should be put in place to allow sufficient time to change processes, procedures, business models, remuneration structures, and associated training and communication systems. We will pursue this issue with the Government, but we encourage ASIC to consider what practical steps it might be able to take to assist the industry as it moves towards full compliance. 2. Performance benefits While AFMA encourages ASIC to provide clear guidance as to how the legislation will be interpreted, the guidance indicating that performance benefits, for example, in excess of 5% or 7% are more likely to be scrutinised is not a realistic benchmark for our members and is therefore unhelpful. While this kind of measure may be realistic for a very limited segment of the industry (the example of an ADI teller given in the guidance) this is not the case for the majority of the industry - particularly the majority that is the most influential in the formulation and provision of advice to retail clients. For instance, the remuneration structure for financial advisers usually includes a salary which is a lower percentage of the employee’s total reward. In fact, the economics of the industry is built around this structure. Therefore we suggest that ASIC removes the guidance that imposes numerical thresholds on different performance benefits, and instead takes a principles based approach that allows each licensee to make an assessment of what is likely to be, and not likely to be, conflicted remuneration based on their particular business model. 3. Asset based fees on borrowed amounts 3.1 Scope of the ban on asset based fees While AFMA acknowledges a key factor behind the FOFA reforms were losses suffered as a result of poor financial advice that recommended gearing into financial products, the draft guidance provides a strong disincentive for an asset based fee where a client has any form of debt. Australians, particularly the younger generations, regularly and reasonably undertake investment activities while having some form of debt at the same time. It is also common for Australians to utilise a line of credit facility to manage their day to day cash flows. In these situations, funds used for investment purposes may have a link back to borrowed monies and this will act as a deterrent for financial advisers to use an asset based fee structure. This appears contrary to the objectives of FOFA in that asset based fees are less likely to influence advice than transactional fees, for example. AFMA therefore suggests that the scope of the ban on asset based fees is limited in practice to situations where the financial product is used to collateralise a borrowed amount or to situations where the client received financial advice to enter into a gearing strategy. 3.2 Instalment warrants AFMA made the following submissions to Treasury in October 2011 as part of the consultation process for the development of the legislation. We did not receive a response to this particular issue and are still of the view that it would be useful to clarify the treatment of instalment warrants. We suggest that ASIC could deal with this in the guidance. The rationale for the ban on asset based fees for geared investments is to remove the incentive for advisers to gear up a client’s investments for the purpose of increasing the value of funds under management and thereby maximise the fees chargeable.

Page 3 of 6

This policy rationale does not hold in relation to internally geared/leveraged products, as compared to externally geared products where the client’s increased equity in the assets can affect the adviser’s remuneration.

Section 964G(1) of the Corporations Act says that, for the purposes of the subdivision, “borrowed” means borrowed in any form, whether secured or unsecured, including through:

(a) a credit facility within the meaning of the regulations; and (b) a margin lending facility.

Subsection (2) says, for the avoidance of doubt, an amount is no longer borrowed to the extent that it has been repaid.

In the case of an internally geared managed fund, the fund borrows money and pays for the loan from dividends and income received from the fund’s investment. On this basis, AFMA understands that internally geared products are not be captured under the ban because the client does not borrow any funds in relation to their investments.

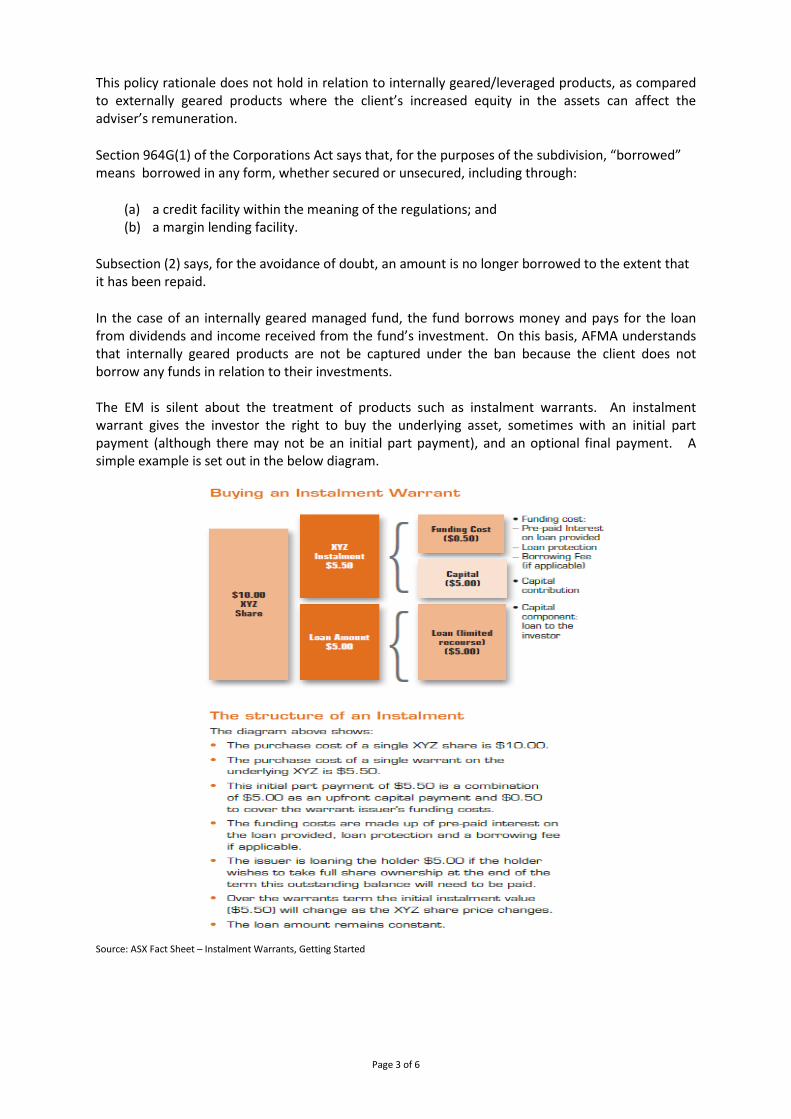

The EM is silent about the treatment of products such as instalment warrants. An instalment warrant gives the investor the right to buy the underlying asset, sometimes with an initial part payment (although there may not be an initial part payment), and an optional final payment. A simple example is set out in the below diagram.

Source: ASX Fact Sheet – Instalment Warrants, Getting Started

Page 4 of 6

Unlike other products that can be used to leverage an investment exposure, an instalment warrant does involve lending and the investor pays interest on the underlying loan. In the above simple example, there is a limited recourse loan for the second instalment, which is not drawn down until the investor makes the decision that they want to own the share at the end of the warrant term. The investor’s liability is limited to the underlying asset and in the event of a default on the loan, the borrower can extinguish their liability by handing back the asset. For instalment warrants that are internally geared, the internal gearing is limited recourse and the client will only lose, at most, the initial instalment payment (if any) and it is not a product feature for that initial instalment to be loaned by the issuer.

The instalment warrant is itself the investment, and arguably the investor would need to borrow to purchase the instalment warrant for it to be considered a geared investment. In the above example, the investor has not borrowed the initial instalment payment of $5.50. There are also instalment warrant products that have a loan to value ratio (LVR) of 100% that do not have an initial instalment payment at all, but in any case the internal gearing is limited recourse so that the client may walk away without any further liability if they choose not to pay any final instalment or interest payment during the life of the product.

Some instalment warrants have a loan reset, where the loan amount may increase or decrease. Even if the loan amount decreases so that if the client is asked to repay part of the loan amount, it remains limited recourse and the investor can simply walk away. Where it increases during the term of the product, the client will receive further funds or can apply the funds against another liability and the limited recourse nature of the product is unchanged.

Furthermore, in practical terms, an asset based fee charged on an instalment warrant would be based on the equity component of the warrant – that is, the market value of the warrant – and not on the value of the underlying shares/units. Difficulties in distinguishing between the geared and ungeared component would not arise in this case.

In Class Order 10/1034, ASIC has declared that an instalment warrant:

(a) that is in a class of financial products that are admitted to quotation on the licensed market

operated by ASX Limited; (b) that is issued by a financial services licensee; and (c) that is a standard margin lending facility

is not a margin lending facility. The class order should put it beyond doubt that instalment warrants are not captured by the reference to a margin lending facility in section 964G(1)(b).

On this basis, AFMA is of the view that instalment warrants are not captured under Subdivision B of Division 5 of the exposure draft. Clarification on this point in the guidance would be useful. 4. Proximity/nexus between payments and advice to retail customers ASIC’s proposed approach to conflicted remuneration as set out in the consultation paper is quite restrictive in some respects given that, as noted above, it is up to licensees to determine whether their remuneration arrangements comply with FOFA. AFMA’s understanding, having been an active participant in the peak consultation group process and the development of the legislation, is that the Government’s intention is to move the financial services industry away from remuneration and incentive structures that create potential conflicts of interest and may result in investors receiving inappropriate advice. However, ASIC’s policy position as described in the consultation paper indicates that many forms of reward for effort are likely to be

Page 5 of 6

treated as conflicted remuneration whether or not they actually have the capacity to create a conflict of interest. 5. Opportunity to articulate what “influence” means There is a real opportunity to articulate what “influence” means in the context of section 963A of the Corporations Act. The guidance would be extremely helpful to industry in implementing the reforms. In re-setting remuneration arrangements to comply with FOFA, a preferred approach (although not the only option) for industry is to move to a balanced scorecard model which has elements of a base salary plus other discretionary components based on things like customer satisfaction with the adviser, the adviser’s contribution to the profitability and success of the business, the adviser’s compliance record, and the results of the advice provided. It is helpful to think of this approach as an incentive model that encourages appropriate behaviour and rewards good advice.

ASIC recognises this approach in section D of the consultation paper, but then goes on to say that ASIC will be “more likely” to scrutinise performance benefits that are more than 5% or 7% (inclusive) of an employee’s base salary, depending on whether the benefit is wholly or partly volume based. It is far from clear that a benefit that is above this threshold will cause a conflict of interest, particularly when it is part of a balanced scorecard approach. Moreover, this statement suggests that ASIC intends to adopt an excessively restrictive approach to determining if an arrangement is not conflicted remuneration for the purposes of the Act.

Section D of the consultation paper refers to a number of performance benefits for employees including bonuses, pay rises, attendance at networking events, promotion or other forms of recognition, attendance at reward-focused conferences and other events, and shares or options in their employer. At paragraph 69, there is an explicit statement that these benefits will be conflicted remuneration if they influence the financial product advice given by an employee that is an AFS licensee or representative.

The distinction that has not been made in the consultation paper is that the “influence” of those performance benefits can be a very positive influence that encourages an adviser to perform to the absolute best of their ability in providing high quality advice.

The best interests duty (BID) will operate alongside the conflicted remuneration ban to ensure that the adviser provides advice that is in the best interests of the client, without particular regard to the different components that make up the adviser’s overall remuneration. Any attempt to massage or inflate particular components of that remuneration are (a) likely to be picked up under compliance controls implemented by licensees; and (b) may result in an adviser breaching the best interests obligation, for which there is a very significant penalty. The operation of the duty and the conflicted remuneration ban together create a strong disincentive to inappropriate behaviour.

Our concern about the draft guidance is that ASIC appears to be taking the view that certain forms of reward for effort are likely to be considered conflicted remuneration even though they could not (from an overall perspective and taking into account the comments about the operation of the BID and the conflicted remuneration ban above) be reasonably expected to cause an adviser to recommend inappropriate financial products, or give advice to a retail client that is motivated by the adviser’s self-interests before the client’s interests. Few advisers and licensees will be willing to take this kind of risk.

***

Page 6 of 6

AFMA would like to note its support for the submissions of the Australian Bankers’ Association and the Financial Services Council in response to CP 189. If you would like to discuss any aspect of this submission and the accompanying table of responses to the consultation questions, please contact me on 02 9776 7997 or [email protected] Yours sincerely

AFMA submission to ASIC Consultation Paper 189 – Future of Financial Advice: conflicted remuneration

Section B – Conflicted remuneration Reference Issue Comment/question B1Q1 Do AFS licensees and representatives need ASIC

guidance to assist in identifying whether a benefit is conflicted remuneration?

• The provision of guidance is helpful given that the law is so high level. • ASIC guidance is also important for areas that have not been adequately

clarified in the law eg. white label arrangements. • The guidance should avoid being too prescriptive (eg. scrutinising performance

benefits that are 5% or 7% of salary) and should be principles based instead. B1Q2 Do you agree with our proposed guidance? There are some significant issues that need to be addressed, in particular:

• It is the licensee’s (and in some cases, the advice provider’s) obligation to

determine what is likely to be considered conflicted remuneration in the context of the particular business and having regard to the type of clients and the type of products on which advice may be given. An incentive that may have the capacity to influence the behaviour of an adviser in a particular sector of the financial services industry, may be of no consequence to and have little or no capacity to influence behaviour of an adviser in another sector. The guidance should be less prescriptive in relation to performance benefits, or alternatively, recognise that performance benefits will have different effects in different sectors.

• More prominence should be given to the proximity of a payment flow to the advice given to a retail investor. Payments that are remote from an individual customer and are product neutral are highly unlikely to influence advice given to a retail customer.

• The guidance should distinguish between incentives that have the capacity to influence an adviser to act in their own interest/act in an undesirable way, and may result in a negative outcome for investors (which is clearly the focus of the FOFA reforms), as opposed to incentives that are likely to influence good behaviour, good advice and good performance.

2

B1Q3 Do you have any comments on the examples in this section?

B1Q4 Are there other examples you would like us to provide on benefits that are or are not conflicted remuneration? Please provide as much specific information as possible, as this will assist us in providing further examples, if needed.

In addition to the examples of what might be considered conflicted remuneration, ASIC should provide more meaningful examples of remuneration that is not conflicted, including examples of where a licensee can rebut the presumption that a volume based payment is conflicted. One suggested example for inclusion is as follows. Scenario: A product issuer issues financial products to retail clients through 3rd party licensed financial advisers ("Advisory group(s)") whose representatives provide personal or general financial product advice to retail clients. The application form for the product provides space for the client to indicate what, if any, upfront fee (a percentage of the total amount invested by the investor) they have agreed that the Advisory Group will receive for the advice provided in relation to the acquisition of the relevant product. For example, the application form may provide a list of options including 0%, 1% , 2% or 3%. The application form and product terms will stipulate that the fee paid by the client to their Advisory group will be collected by the product issuer (as agent of the 3rd party Advisory group, along with their funds applied to purchase the product) and the fee will then be transmitted from the product issuer to the 3rd party Advisory group whose representatives provided the financial product advice. The form may also include a section for the adviser to sign confirming its acknowledgement of the fee arrangement. Commentary: Based on ASIC's commentary in Table 4 of the Appendix to CP 189, such fees for advice would fall within the exemption to the ban on conflicted remuneration in s963B(1)(d)and the arrangement described in the above scenario would be permissible on the basis that the benefit is being provided by the retail client, via the product issuer, at its direction and having been authorised by both the client and the adviser (supported by s52 of the Corporations ct 2001 (Cth) which states that a reference to doing an act, such as giving a benefit to an AFS licensee or representative, includes authorising the act to be done). The interposing

3

of the product issuer between the retail client and Advisory group in the payment of the fee for advice is simply a means of ensuring a more efficient payment process with the product issuer receiving both the investment funds and adviser fees and applying both in accordance with the retail client's direction. Also, by ensuring the application form for the product provides the option for the client to elect for no upfront fee (ie 0%) to be paid, this may provoke discussion between the client and their adviser as to what the appropriate fee arrangement should be for the particular client and allows advisers and their clients to come to other fee arrangements between themselves (if they so wish). It is also consistent with the EM to the Corporations Amendment (Further Future of Financial Advice Measures) Bill 2011 at para 2.26 which states that: "Where the monetary benefit is given by the client in relation to the issue or sale of a product or in relation to financial product advice provided to the client, this is not conflicted remuneration. This ensures that ‘fee for service’ arrangements — where the client is the person paying the adviser — are not conflicted remuneration (even where the client pays a volume-based fee). The provision is intended to exclude from the definition of conflicted remuneration any fee for service paid by the retail client, whether the benefit is given directly by the retail client or is given by another party at the direction, or with the clear consent, of the retail client."

We submit that the scenario described above fits within the terms of the exemption to the ban on conflicted remuneration and is consistent with the policy objectives behind the ban. It would be helpful to the industry for ASIC to include this example, and similar examples, in its guidance as a number of product issuers within our membership have raised this particular issue.

B1Q5 Is there any further guidance we should give on whether a benefit is conflicted remuneration? Please provide as much specific information as possible, as this will assist us to provide further guidance, if needed.

Examples of conflicted remuneration in paragraph 34 - it would be useful if ASIC could expand on what consider would be reasonably expected to influence the advice or recommendation, and to distinguish between positive and negative influence. There are some examples in the guidance, but there is no explanation as to how those examples might actually influence the advice or recommendations.

4

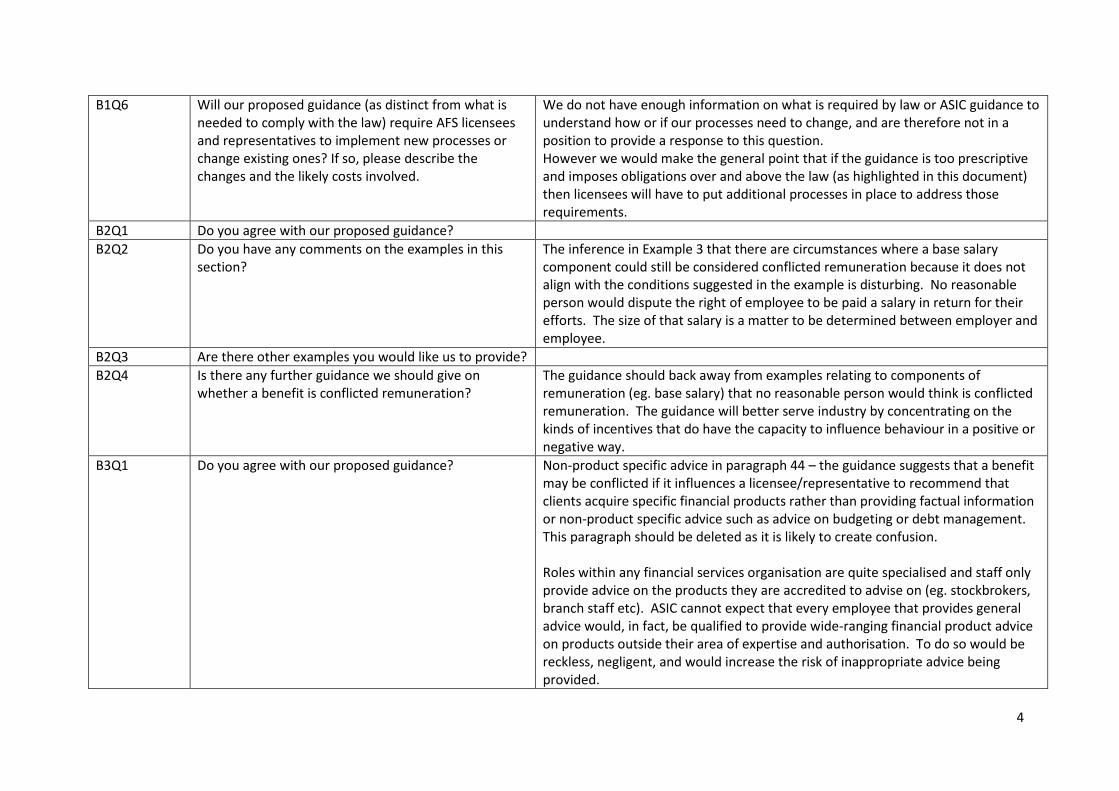

B1Q6 Will our proposed guidance (as distinct from what is needed to comply with the law) require AFS licensees and representatives to implement new processes or change existing ones? If so, please describe the changes and the likely costs involved.

We do not have enough information on what is required by law or ASIC guidance to understand how or if our processes need to change, and are therefore not in a position to provide a response to this question. However we would make the general point that if the guidance is too prescriptive and imposes obligations over and above the law (as highlighted in this document) then licensees will have to put additional processes in place to address those requirements.

B2Q1 Do you agree with our proposed guidance? B2Q2 Do you have any comments on the examples in this

section? The inference in Example 3 that there are circumstances where a base salary component could still be considered conflicted remuneration because it does not align with the conditions suggested in the example is disturbing. No reasonable person would dispute the right of employee to be paid a salary in return for their efforts. The size of that salary is a matter to be determined between employer and employee.

B2Q3 Are there other examples you would like us to provide? B2Q4 Is there any further guidance we should give on

whether a benefit is conflicted remuneration? The guidance should back away from examples relating to components of remuneration (eg. base salary) that no reasonable person would think is conflicted remuneration. The guidance will better serve industry by concentrating on the kinds of incentives that do have the capacity to influence behaviour in a positive or negative way.

B3Q1 Do you agree with our proposed guidance? Non-product specific advice in paragraph 44 – the guidance suggests that a benefit may be conflicted if it influences a licensee/representative to recommend that clients acquire specific financial products rather than providing factual information or non-product specific advice such as advice on budgeting or debt management. This paragraph should be deleted as it is likely to create confusion. Roles within any financial services organisation are quite specialised and staff only provide advice on the products they are accredited to advise on (eg. stockbrokers, branch staff etc). ASIC cannot expect that every employee that provides general advice would, in fact, be qualified to provide wide-ranging financial product advice on products outside their area of expertise and authorisation. To do so would be reckless, negligent, and would increase the risk of inappropriate advice being provided.

5

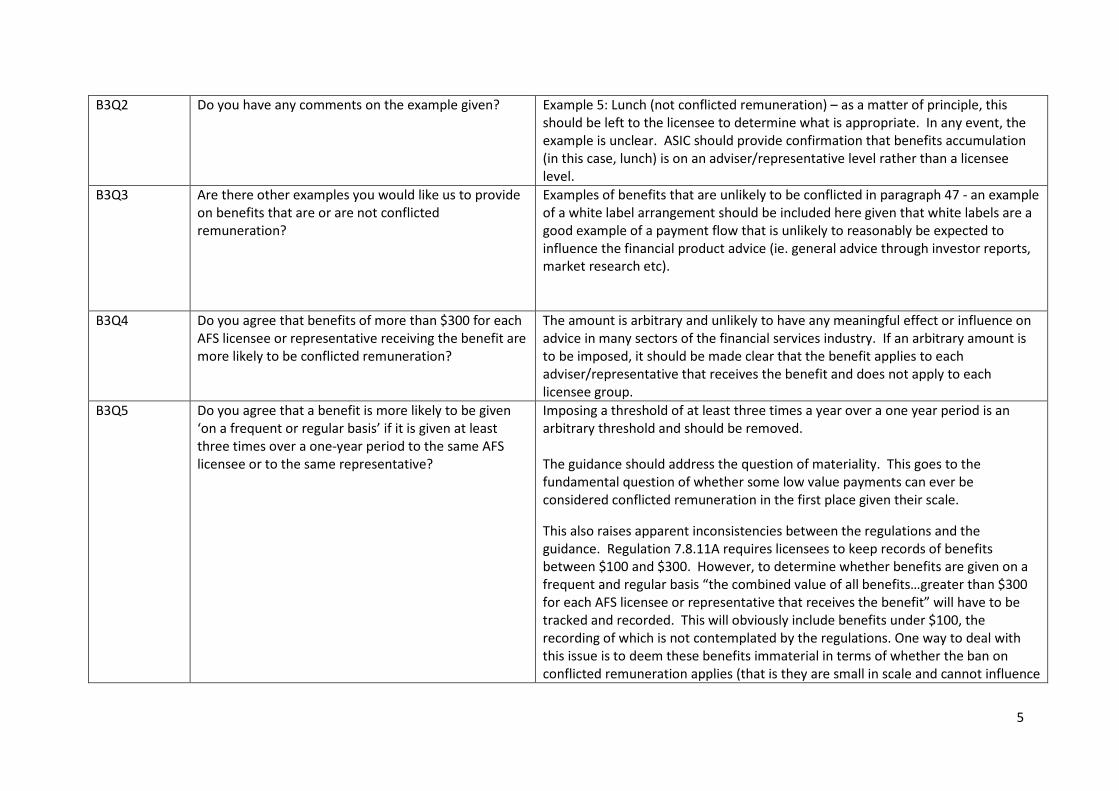

B3Q2 Do you have any comments on the example given? Example 5: Lunch (not conflicted remuneration) – as a matter of principle, this should be left to the licensee to determine what is appropriate. In any event, the example is unclear. ASIC should provide confirmation that benefits accumulation (in this case, lunch) is on an adviser/representative level rather than a licensee level.

B3Q3 Are there other examples you would like us to provide on benefits that are or are not conflicted remuneration?

Examples of benefits that are unlikely to be conflicted in paragraph 47 - an example of a white label arrangement should be included here given that white labels are a good example of a payment flow that is unlikely to reasonably be expected to influence the financial product advice (ie. general advice through investor reports, market research etc).

B3Q4 Do you agree that benefits of more than $300 for each AFS licensee or representative receiving the benefit are more likely to be conflicted remuneration?

The amount is arbitrary and unlikely to have any meaningful effect or influence on advice in many sectors of the financial services industry. If an arbitrary amount is to be imposed, it should be made clear that the benefit applies to each adviser/representative that receives the benefit and does not apply to each licensee group.

B3Q5 Do you agree that a benefit is more likely to be given ‘on a frequent or regular basis’ if it is given at least three times over a one-year period to the same AFS licensee or to the same representative?

Imposing a threshold of at least three times a year over a one year period is an arbitrary threshold and should be removed. The guidance should address the question of materiality. This goes to the fundamental question of whether some low value payments can ever be considered conflicted remuneration in the first place given their scale.

This also raises apparent inconsistencies between the regulations and the guidance. Regulation 7.8.11A requires licensees to keep records of benefits between $100 and $300. However, to determine whether benefits are given on a frequent and regular basis “the combined value of all benefits…greater than $300 for each AFS licensee or representative that receives the benefit” will have to be tracked and recorded. This will obviously include benefits under $100, the recording of which is not contemplated by the regulations. One way to deal with this issue is to deem these benefits immaterial in terms of whether the ban on conflicted remuneration applies (that is they are small in scale and cannot influence

6

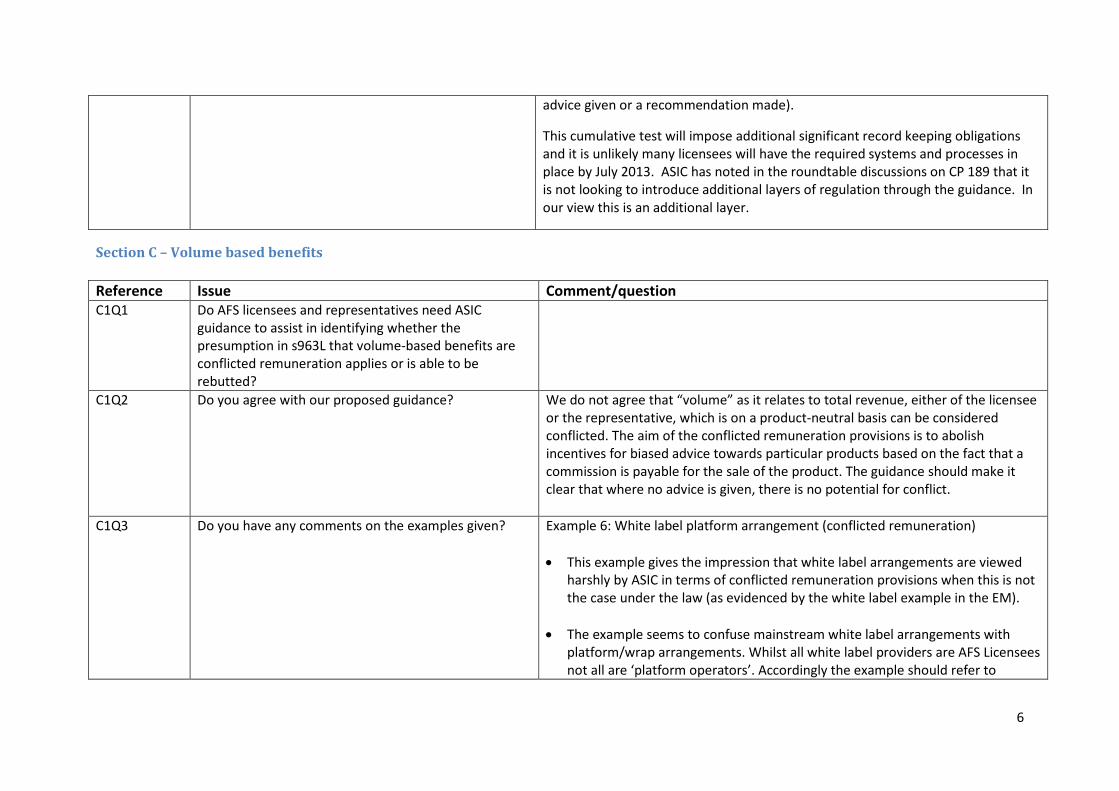

advice given or a recommendation made).

This cumulative test will impose additional significant record keeping obligations and it is unlikely many licensees will have the required systems and processes in place by July 2013. ASIC has noted in the roundtable discussions on CP 189 that it is not looking to introduce additional layers of regulation through the guidance. In our view this is an additional layer.

Section C – Volume based benefits Reference Issue Comment/question C1Q1 Do AFS licensees and representatives need ASIC

guidance to assist in identifying whether the presumption in s963L that volume-based benefits are conflicted remuneration applies or is able to be rebutted?

C1Q2 Do you agree with our proposed guidance? We do not agree that “volume” as it relates to total revenue, either of the licensee or the representative, which is on a product-neutral basis can be considered conflicted. The aim of the conflicted remuneration provisions is to abolish incentives for biased advice towards particular products based on the fact that a commission is payable for the sale of the product. The guidance should make it clear that where no advice is given, there is no potential for conflict.

C1Q3 Do you have any comments on the examples given? Example 6: White label platform arrangement (conflicted remuneration) • This example gives the impression that white label arrangements are viewed

harshly by ASIC in terms of conflicted remuneration provisions when this is not the case under the law (as evidenced by the white label example in the EM).

• The example seems to confuse mainstream white label arrangements with platform/wrap arrangements. Whilst all white label providers are AFS Licensees not all are ‘platform operators’. Accordingly the example should refer to

7

‘licensees’ rather than platform providers. • In Example 6 ASIC advises that the fee split between the platform operator and

dealer group is conflicted remuneration “unless the dealer group or platform operator can show that this is not the case”. The example is said to be based on the example on page 29 of the revised AM. However, the EM example concludes that the fee split is not conflicted remuneration “as the scope of influence is remote”.

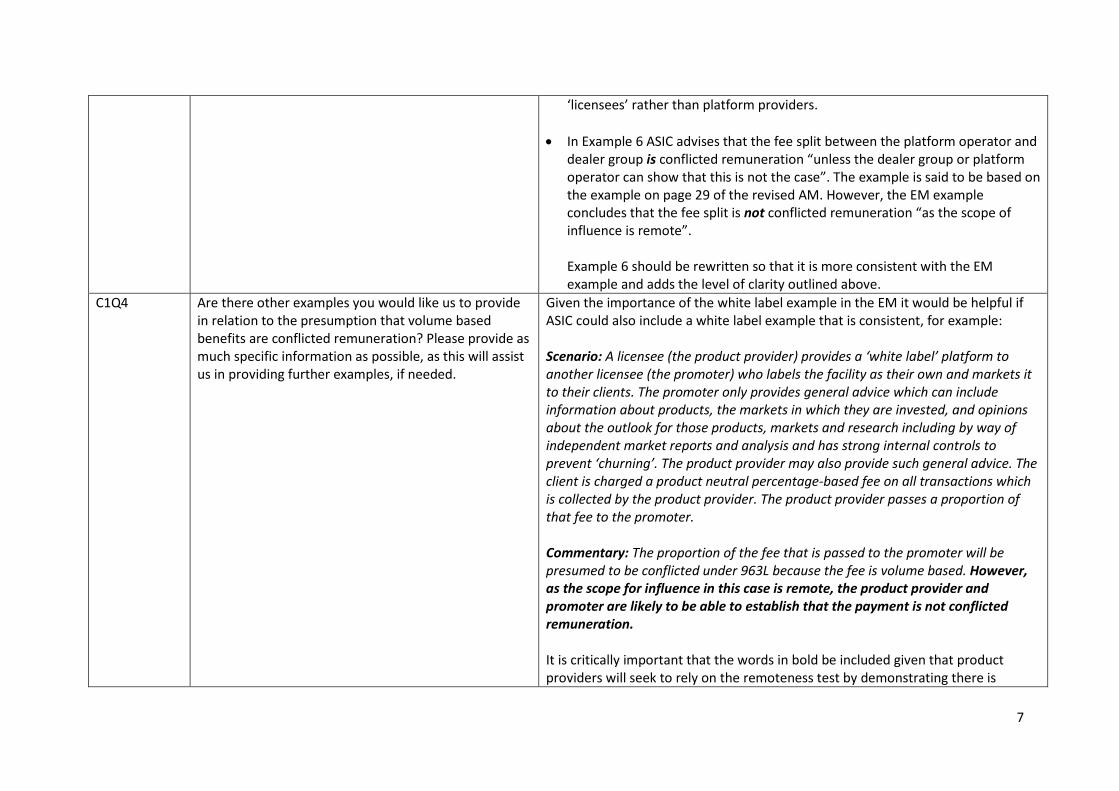

Example 6 should be rewritten so that it is more consistent with the EM example and adds the level of clarity outlined above.

C1Q4 Are there other examples you would like us to provide in relation to the presumption that volume based benefits are conflicted remuneration? Please provide as much specific information as possible, as this will assist us in providing further examples, if needed.

Given the importance of the white label example in the EM it would be helpful if ASIC could also include a white label example that is consistent, for example: Scenario: A licensee (the product provider) provides a ‘white label’ platform to another licensee (the promoter) who labels the facility as their own and markets it to their clients. The promoter only provides general advice which can include information about products, the markets in which they are invested, and opinions about the outlook for those products, markets and research including by way of independent market reports and analysis and has strong internal controls to prevent ‘churning’. The product provider may also provide such general advice. The client is charged a product neutral percentage-based fee on all transactions which is collected by the product provider. The product provider passes a proportion of that fee to the promoter. Commentary: The proportion of the fee that is passed to the promoter will be presumed to be conflicted under 963L because the fee is volume based. However, as the scope for influence in this case is remote, the product provider and promoter are likely to be able to establish that the payment is not conflicted remuneration. It is critically important that the words in bold be included given that product providers will seek to rely on the remoteness test by demonstrating there is

8

little/no connection between the payment made and the general advice given. C1Q5 A possible consequence of the conflicted remuneration

provisions is that they may prevent product issuers—such as trustees of superannuation funds, responsible entities, and platform operators—from giving financial product advice to retail clients to increase or maintain their investment or other interest in the issuer’s products. This is because this may result in an increase in, or the maintenance of, management or other fees payable out of the fund. These fees might reasonably be expected to influence the advice. Do you see this as a concern or unintended consequence?

Yes this is a concern and an unintended consequence because it can imply that product issuers are unable to promote their products by providing general advice. However, it is not clear when a platform operator or a product issuer is also a licensed dealer, how this would become conflicted remuneration as the payments are direct from the client and there would fall within the s963B(1)(d) and s963C(e) “benefits given by the client” exclusion.

C1Q6 If you are concerned, does your concern or view apply to all such situations or only to some situations—for example: (a) when intra-fund advice is provided by a trustee of a superannuation fund to a member; and (b) when general advice is provided by responsible entities in investor newsletters?

White label products are a good example of the difficulties with extending the conflicted remuneration provisions to general advice provided by way of investor newsletters. In a white label arrangement general advice may be provided which can include information about products, the markets in which they are invested, and opinions about outlook for those products, markets and research.

In a typical arrangement, when a client lodges a request online to buy or sell shares, brokerage is debited by the product provider directly from the customer’s bank account. Brokerage rates and all fees and charges are disclosed in the Financial Services Guide. A portion is then paid to the partner on a monthly basis calculated on a revenue share or fees for discrete service basis. This arrangement remunerates both parties as both contribute to the overall service to the end client

If the conflicted remuneration provisions do apply to white label arrangements the viability of these products will have to be re-assessed and the payment flows re-structured. Alternatively, general advice will be removed from websites (in which case the investor will have to make a less informed decision – contrary to the

9

principles of FOFA), or re-word the investor information so only factual information is provided.

C1Q7 Is there any further guidance we should give? Please provide as much specific information as possible, as this will assist us to provide further guidance, if needed.

It is not entirely clear whether sections C and D (volume based benefits and performance benefits for employees) are linked in any way and so whether the presumption of a conflict applies and can be rebutted through demonstration that the value is not significant. Paragraph 70 seems to indicate that this may not be the case, in that it states if any part of the performance payment is based on volume then the whole will be considered conflicted. However, paragraph 71 contradicts this view. There is a second category of white label or co-operation arrangements where guidance would also be helpful. These arrangement can involve an introducer issuing disclosure documents and entering into client agreements with their clients, who in turn transact in products such as margin FX contracts or CFDs with the introducer, who is licensed or may be an authorised representative. That introducer then enters into a client agreement with another licensee and undertakes offsetting or hedging transactions with that licensee. This is a common transaction in this segment of the industry. The introducer derives income in one of two ways:

• Through a difference in the spread offered by the introducer to their client, and that offered by the other licensee to the introducer;

• Where spreads are the same, by sharing profits – losses are borne by both parties.

In both cases the introducer is contractually liable to the client. The alignment if income derived by the introducer and any advice given is remote and arguably does not fall with the restrictions on conflicted remuneration.

C1Q8 Will our proposed guidance (as distinct from what is needed to comply with the law) require AFS licensees and representatives to implement new processes or change existing ones? If so, please describe the changes

If the volume ban is taken to include revenue (even product neutral revenue), then remuneration incentives and career progression roadmaps will need to be extensively reviewed. Our members are concerned about their continued ability to incentivise and reward productivity and good performance.

10

and the likely costs involved. C2Q1 Do you agree with our proposed guidance? Paragraph 54 states “the presumption in s963L can be rebutted by showing that

the value of the benefit is not significant enough that it could reasonably be expected to influence the financial product advice given to a client.” This seems to imply that this is the only basis upon which the presumption can be rebutted. However the (arguably) more important test that the presumption can be rebutted on is the remoteness test and ASIC should acknowledge this alongside the value of benefit test in C2.

C2Q2 Do you have any comments on the example given? C2Q3 Are there other examples you would like us to provide

in relation to rebutting the presumption that volume-based benefits are conflicted remuneration?

C2Q4 Is there any further guidance we should give? C3Q1 Do you agree with our proposed guidance? Refer to C1Q6 and Q7 comments regarding white label arrangements. In particular

paragraph 56 may be interpreted as ASIC viewing all remuneration from white label arrangements as conflicted. It is not clear when a platform operator or a product issuer is also a licensed dealer, how this would become conflicted remuneration as the payments are direct from the client and therefore would fall within the s963B(1)(d) and s963C(e) “benefits given by the client” exclusion.

C3Q2 Do you have any comments on the examples given? One example in which a licensed dealer (broker) is also an ‘other-product issuer’ occurs when the broker makes available to clients a private-label (internal), managed discretionary portfolio. Such a portfolio enables clients who are time-poor to efficiently access the investment views of the broker. It is also conducive to better portfolio design outcomes than those which emanate from a transaction-by-transaction brokerage arrangement. For example, the client agrees that a sum of funds be invested in a portfolio of securities to be managed by the dealer on a structured, discretionary basis for an agreed (often rolling) period. Such arrangements are often subject to an asset-based (percentage of funds-under-

11

management) fee comprising a disclosed administration fee, a management fee and an advice fee with individual dealers receiving a proportion of the latter. This may be considered conflicted remuneration under paragraph 57 (the presumption being that the dealer is incentivised to sell additional internal product because of the fees they would personally receive), and the onus is placed upon the licensee to rebut the assumption of conflict. Such an arrangement is highly proximate to the client and, provided the fee structure and flow of fees (to the licensee and to the dealer) are adequately disclosed, the client’s ability to withdraw the funds from discretionary management would form part of their relationship with the dealer (there is no third-party relationship). Any incentive to sell additional product without regard for the client’s circumstances would likely fall under the dealer’s best interests obligations, and the penalties for breaching this are material.

C3Q3 Are there other examples you would like us to provide? C3Q4 Is there any further guidance we should give? C4Q1 Do you agree with our proposed guidance? It would be preferable for the guidance to back away from discussion about equity

arrangements, or be more specific about the concern that is being addressed. The suggestion that components like payment of dividends on equity might be conflicted remuneration contradicts the desire of licensees as employers to more closely tie the interests of their employees to the ongoing success of the business, which in turn is directly linked to ongoing good outcomes (in the broad sense, not just financial) for clients. There is also a tension between the ordinary right of a shareholders to receive dividend payments where a dividend is declared, and the inference by ASIC that dividends cannot be paid to a shareholder who is also a representative or employee because this might result in a conflict of interest. If ASIC’s goal is to deter equity arrangements that are clearly in the realm of avoidance, then this should be clearly stated and the guidance should address that particular concern. The guidance does acknowledge that equity arrangements do not always

12

constitute conflicted remuneration ie. paragraph 59 states that equity arrangements “..may be conflicted remuneration.” Paragraph 68 states that performance benefits (including shares or options) will be conflicted if they influence the financial product advice given. For the avoidance of doubt, it would be helpful if ASIC would include a paragraph or an example of equity arrangements that would not be conflicted because they have an insufficient nexus to advice given or recommendations made – for example, employee annual share allocation based on the overall performance of the organisation.

C4Q2 Do you have any comments on the example given? C4Q3 Are there other examples you would like us to provide? C4Q4 Is there any further guidance we should give?

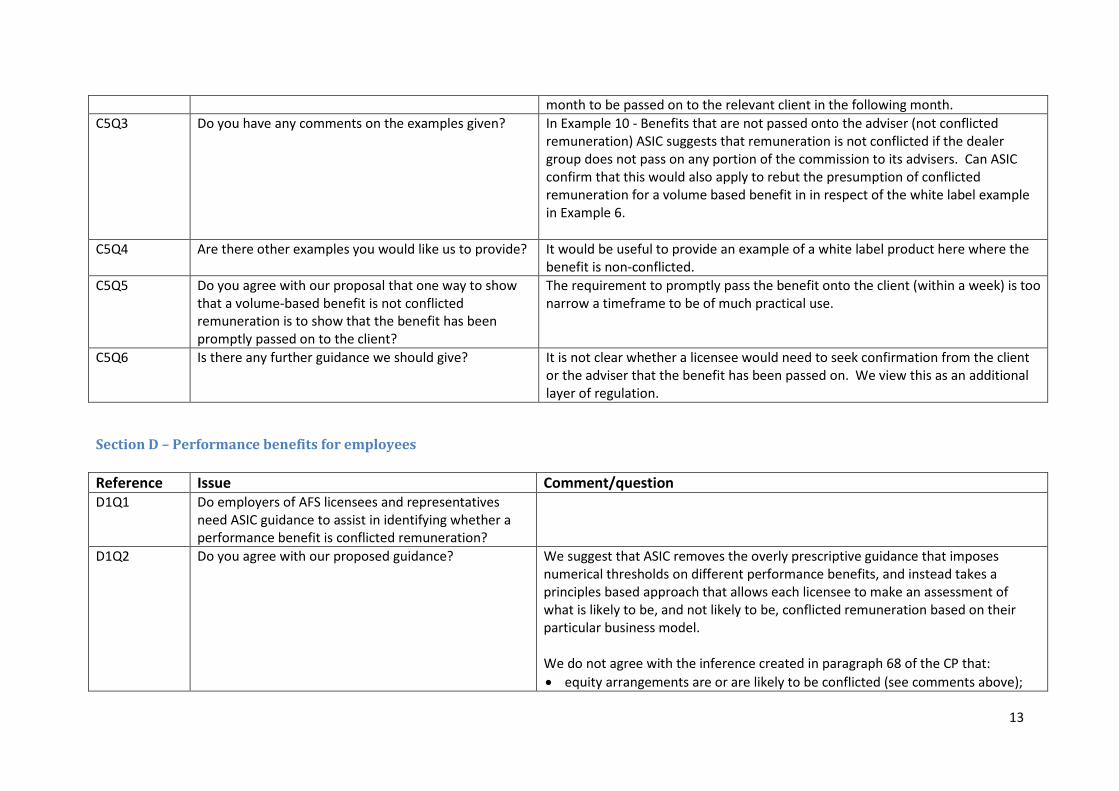

C5Q1 Do you agree with our proposed guidance? Yes, we agree. Fees passed on to a client, or not passed on to a financial adviser, are less likely to influence advice and therefore should generally not be treated as conflicted remuneration.

C5Q2 Do you think that there are other circumstances when a volume-based benefit is not conflicted remuneration?

It would be useful to include some text or an example of non-conflicted remuneration consisting of performance benefits based on the overall profitability (which includes a variety of factors such as managing costs, generating income etc.) of a division/organisation. Such a benefit is product neutral and does not influence the financial product advice given by an employee. ASIC should make it clear in the guide that any benefit paid or received that is wholly unrelated to the provision of financial product advice is exempt from the conflicted remuneration provisions. ASIC should also provide examples of the application of this approach. Paragraph 60(a) of the CP refers to a benefit needing to be passed on to a client within one week of receiving the benefit. One week is unreasonable from an administrative perspective and should be changed to 2 months to enable payments received from a product issuer or platform provider during one calendar

13

month to be passed on to the relevant client in the following month. C5Q3 Do you have any comments on the examples given? In Example 10 - Benefits that are not passed onto the adviser (not conflicted

remuneration) ASIC suggests that remuneration is not conflicted if the dealer group does not pass on any portion of the commission to its advisers. Can ASIC confirm that this would also apply to rebut the presumption of conflicted remuneration for a volume based benefit in in respect of the white label example in Example 6.

C5Q4 Are there other examples you would like us to provide? It would be useful to provide an example of a white label product here where the benefit is non-conflicted.

C5Q5 Do you agree with our proposal that one way to show that a volume-based benefit is not conflicted remuneration is to show that the benefit has been promptly passed on to the client?

The requirement to promptly pass the benefit onto the client (within a week) is too narrow a timeframe to be of much practical use.

C5Q6 Is there any further guidance we should give? It is not clear whether a licensee would need to seek confirmation from the client or the adviser that the benefit has been passed on. We view this as an additional layer of regulation.

Section D – Performance benefits for employees Reference Issue Comment/question D1Q1 Do employers of AFS licensees and representatives

need ASIC guidance to assist in identifying whether a performance benefit is conflicted remuneration?

D1Q2 Do you agree with our proposed guidance? We suggest that ASIC removes the overly prescriptive guidance that imposes numerical thresholds on different performance benefits, and instead takes a principles based approach that allows each licensee to make an assessment of what is likely to be, and not likely to be, conflicted remuneration based on their particular business model. We do not agree with the inference created in paragraph 68 of the CP that: • equity arrangements are or are likely to be conflicted (see comments above);

14

and • promotion, networking events and conferences can be conflicted. These are

generally educational in nature and help drive positive behaviours and improve the quality of advice provided.

The guidance should make it clear that performance benefits based on the overall profitability (which includes a variety of factors such as managing costs, generating income etc) of a division/organisation is not conflicted. This is because it is product neutral and does not influence the financial product advice given by an employee. ASIC should make it clear that any benefit paid or received that is wholly unrelated to the provision of financial product advice is exempt from the conflicted remuneration provisions. ASIC should also provide examples of the application of this approach.

D1Q3 Do you have any comments on the examples given? D1Q4 Are there other examples you would like us to provide

on performance benefits for employees? Please provide as much specific information as possible, as this will assist us in providing further examples, if needed.

D1Q5 Is there any further guidance we should give? Please provide as much specific information as possible, as this will assist us to provide further guidance, if needed.

D1Q6 Will our proposed guidance (as distinct from what is needed to comply with the law) require employers to implement new performance arrangements or change existing arrangements? If so, please describe the changes and the likely costs involved.

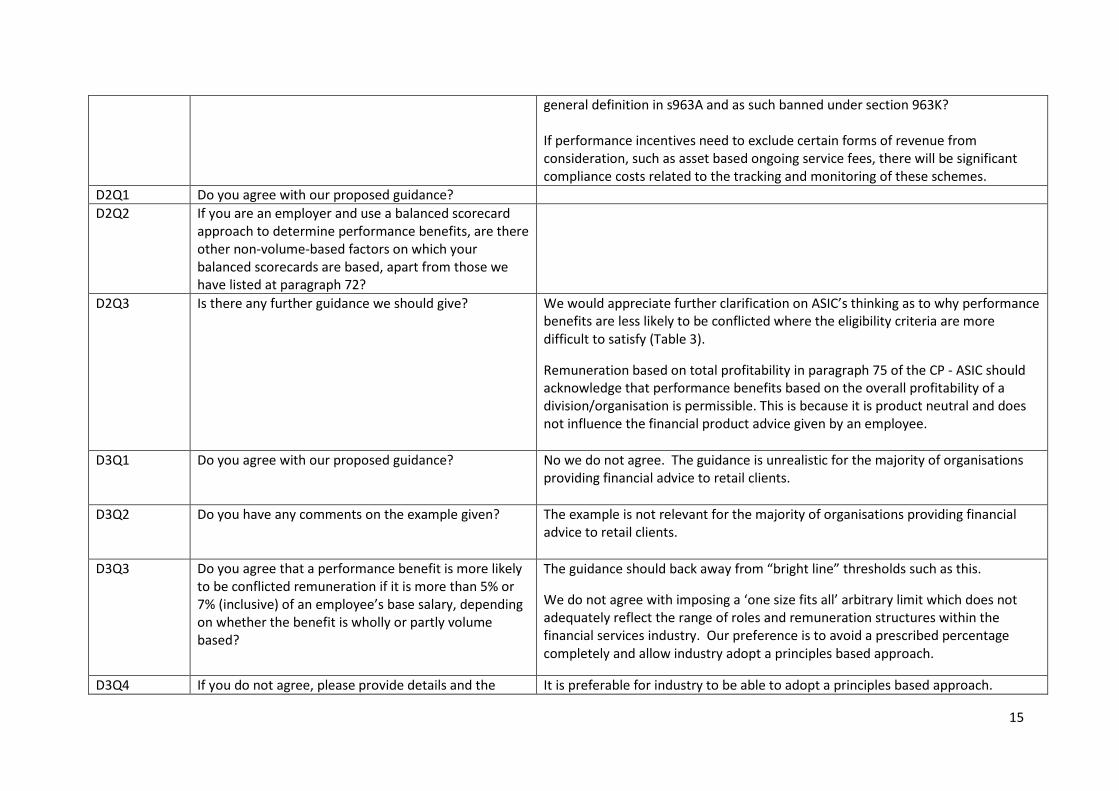

If the volume ban is taken to include revenue (even product-neutral revenue), then remuneration incentives and career progression roadmaps will need to be extensively reviewed. Our members are concerned about their continued ability to incentivise and reward productivity and good performance. It would be helpful if ASIC could clarify the interaction as between conflicted remuneration exempt under section 963B and the operation of section 963K. For example, if an asset based fee under section 963B(d)(i) or (ii) is paid to a licensee by a retail client, can these payments be shared with the representatives of that licensee under the terms of these exemptions or is such revenue presumed to be volume based under section 963L (in respect of s963(d)Ii) payments) or otherwise conflicted under the

15

general definition in s963A and as such banned under section 963K? If performance incentives need to exclude certain forms of revenue from consideration, such as asset based ongoing service fees, there will be significant compliance costs related to the tracking and monitoring of these schemes.

D2Q1 Do you agree with our proposed guidance? D2Q2 If you are an employer and use a balanced scorecard

approach to determine performance benefits, are there other non-volume-based factors on which your balanced scorecards are based, apart from those we have listed at paragraph 72?

D2Q3 Is there any further guidance we should give?

We would appreciate further clarification on ASIC’s thinking as to why performance benefits are less likely to be conflicted where the eligibility criteria are more difficult to satisfy (Table 3).

Remuneration based on total profitability in paragraph 75 of the CP - ASIC should acknowledge that performance benefits based on the overall profitability of a division/organisation is permissible. This is because it is product neutral and does not influence the financial product advice given by an employee.

D3Q1 Do you agree with our proposed guidance? No we do not agree. The guidance is unrealistic for the majority of organisations providing financial advice to retail clients.

D3Q2 Do you have any comments on the example given? The example is not relevant for the majority of organisations providing financial advice to retail clients.

D3Q3 Do you agree that a performance benefit is more likely to be conflicted remuneration if it is more than 5% or 7% (inclusive) of an employee’s base salary, depending on whether the benefit is wholly or partly volume based?

The guidance should back away from “bright line” thresholds such as this.

We do not agree with imposing a ‘one size fits all’ arbitrary limit which does not adequately reflect the range of roles and remuneration structures within the financial services industry. Our preference is to avoid a prescribed percentage completely and allow industry adopt a principles based approach.

D3Q4 If you do not agree, please provide details and the It is preferable for industry to be able to adopt a principles based approach.

16

percentages that you think are appropriate. D3Q5 Do you think that our guidance should explicitly state

when a performance benefit will or will not be conflicted remuneration? For example, should we state that a performance benefit is conflicted remuneration if it is 5% or more of an employee’s base salary, where the benefit is wholly volume based, or 7% or more, where the benefit is partly volume based? If so, do you agree with these percentages? If not, please provide details.

Arrangements vary across the industry and should be assessed on a case by case basis. The guidance should be principles based not make reference to specific percentages or limits.

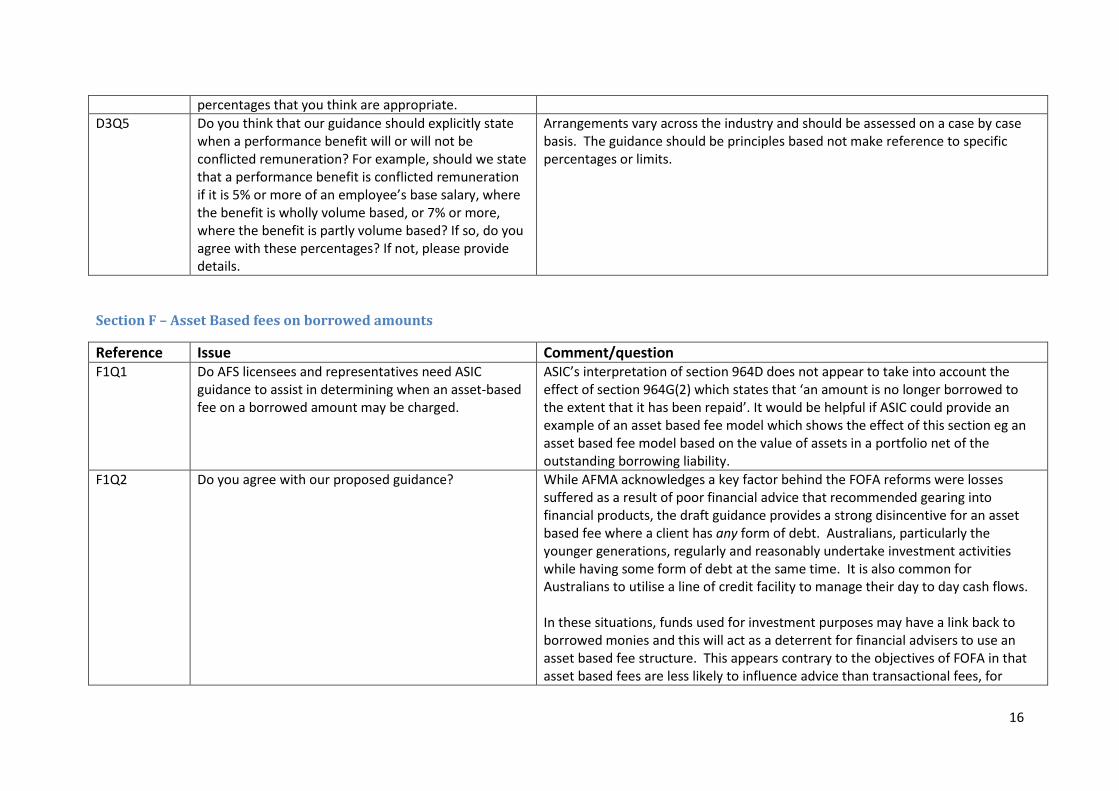

Section F – Asset Based fees on borrowed amounts

Reference Issue Comment/question F1Q1 Do AFS licensees and representatives need ASIC

guidance to assist in determining when an asset-based fee on a borrowed amount may be charged.

ASIC’s interpretation of section 964D does not appear to take into account the effect of section 964G(2) which states that ‘an amount is no longer borrowed to the extent that it has been repaid’. It would be helpful if ASIC could provide an example of an asset based fee model which shows the effect of this section eg an asset based fee model based on the value of assets in a portfolio net of the outstanding borrowing liability.

F1Q2 Do you agree with our proposed guidance? While AFMA acknowledges a key factor behind the FOFA reforms were losses suffered as a result of poor financial advice that recommended gearing into financial products, the draft guidance provides a strong disincentive for an asset based fee where a client has any form of debt. Australians, particularly the younger generations, regularly and reasonably undertake investment activities while having some form of debt at the same time. It is also common for Australians to utilise a line of credit facility to manage their day to day cash flows. In these situations, funds used for investment purposes may have a link back to borrowed monies and this will act as a deterrent for financial advisers to use an asset based fee structure. This appears contrary to the objectives of FOFA in that asset based fees are less likely to influence advice than transactional fees, for

17

example. AFMA therefore suggests that the scope of the ban on asset based fees for limited in practice to situations where the financial product is used to collateralise a borrowed amount or to situations where the client received financial advice to enter into a gearing strategy.

F1Q3 Do you have any comments on the examples given? F1Q4 Are there other examples you would like us to provide?

Please provide as much specific information as possible, as this will assist us in providing further guidance, if needed.

It may be the case that, as part of a funds-under-management arrangement incorporating an asset-based fee, an amount is borrowed in a foreign currency to fund a security transaction in that currency. Such a transaction would be considered conflicted remuneration under paragraph 102. However, in this case, the gearing would be entered into only in the interests of legitimately benefiting the client (in this case, reduced exposure to currency fluctuations), rather than “artificially increas[ing] the size of [the dealer’s] advice fees” (paragraph 105).

F1Q5 Is there any further guidance we should give? Please provide as much specific information as possible, as this will assist us to provide further guidance if needed.

F1Q6 Will our proposed guidance (as distinct from what is needed to comply with the law) require AFS licensees and representatives to implement new processes or change existing ones? If so, please describe the changes and the likely costs involved.

F2Q1 Do you agree with our proposed guidance? F2Q2 Is there any further guidance we should give? F3Q1 Do you agree with our proposed guidance?

If the asset based fee restriction is extended to circumstances outside of where the financial products recommended collateralise the loan, or where the client is provided with specific financial advice to enter into a gearing strategy, it will be extremely difficult to monitor borrowed and non-borrowed amounts for asset-based billing purposes.

F3Q2 Is there any further guidance we should give?

18

Section G – Transitional provisions Reference Issue Comment/question G1Q1 Do you have any comments on our proposed guidance? The loss of grandfathering on a transfer to a different product as referred to in

paragraph 121 does not appear to be consistent with the breadth of the terms of the grandfathering provision (s1528).

G1Q2 Is there any further guidance we should give? Please provide as much specific information as possible, as this will assist us to provide further guidance, if needed.

There is little meaningful guidance on grandfathering. Guidance is required about the extent to which existing arrangements can be grandfathered that cover all financial products issued by a product issuer, which could cover product issued after the Application Day. Further, with the withdrawal of draft regulation 7.7A.4.16, guidance is also required in relation to the extent that there may be grandfathering of arrangements which are not limited to investments existing in product before the Application Day – ie arrangements covering pre-Application Day product but continue in respect of new client investments following the Application Day.

G2Q1 Do AFS licensees and representatives need ASIC guidance to assist in determining when the conflicted remuneration transitional provisions apply?

It is becoming unlikely that the transition period to 1 July 2013 will be sufficient for industry to implement the required changes, given that ASIC guidance will not be finalised until February 2013. A further transitional period (similar to the Financial Services Reform Act and other reforms in relation to superannuation) should be put in place to allow sufficient time to change processes, procedures, business models, remuneration structures, systems and associated training and communications. AFMA is taking up this issue with Government.

G2Q2 Do you agree with our proposed guidance? Can ASIC provide some guidance on how staff on existing contracts (at 1 July 2013) will be treated versus staff on new contracts after that date.

19

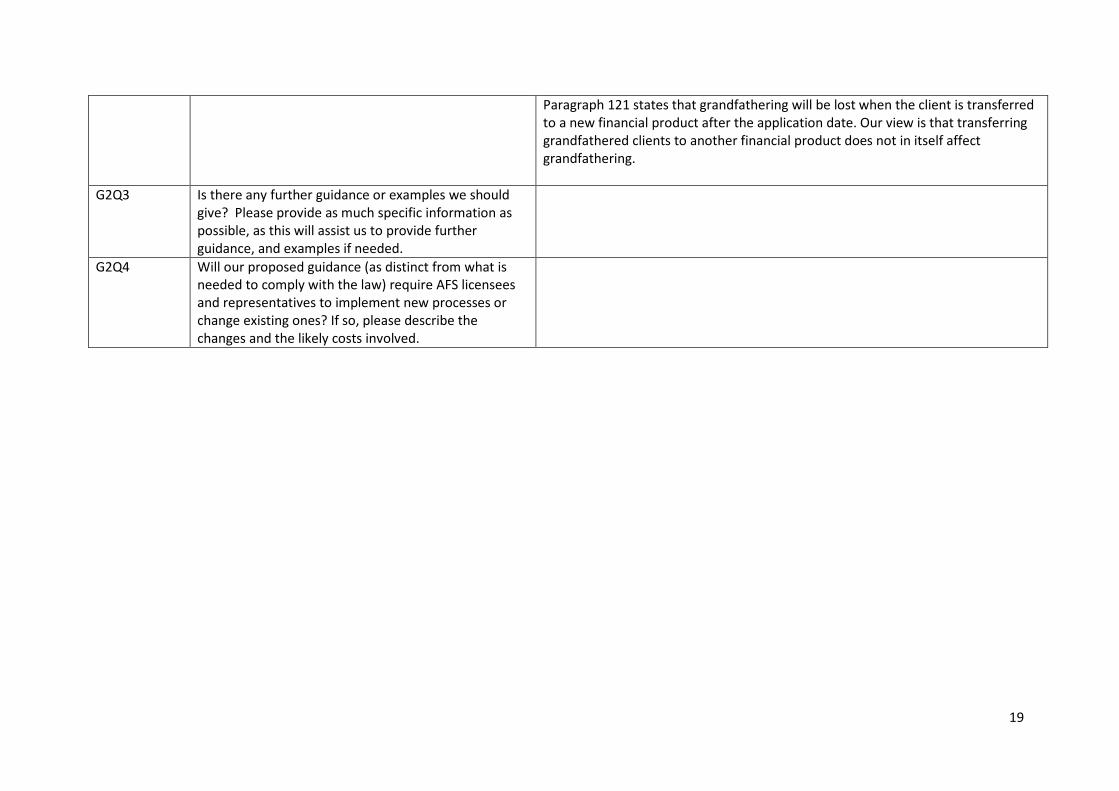

Paragraph 121 states that grandfathering will be lost when the client is transferred to a new financial product after the application date. Our view is that transferring grandfathered clients to another financial product does not in itself affect grandfathering.

G2Q3 Is there any further guidance or examples we should give? Please provide as much specific information as possible, as this will assist us to provide further guidance, and examples if needed.

G2Q4 Will our proposed guidance (as distinct from what is needed to comply with the law) require AFS licensees and representatives to implement new processes or change existing ones? If so, please describe the changes and the likely costs involved.