122

Assessing Fraud Risks: Understanding Common Fraud Schemes Course # 3044, 8 CPE Credits

| Date post: | 21-Oct-2015 |

| Category: |

Documents |

| Upload: | saccontala |

| View: | 148 times |

| Download: | 1 times |

Assessing Fraud Risks: Understanding Common Fraud Schemes

Course # 3044, 8 CPE Credits

Course CPE Information

i

Course CPE Information Course Expiration Date AICPA and NASBA Standards require all Self-Study courses to be completed and the final exam submitted within 1 year from the date of purchase as shown on your invoice. No extensions are allowed under AICPA/NASBA rules. On rare occasion, in response to customer feedback, Western CPE deems it necessary to change one or more of the final exam questions. Thank you for choosing Western CPE for your continuing professional education needs. Field of Study Auditing. Some state boards may count credits under different categories—check with your state board for more information. Course Level Basic. Prerequisites There are no prerequisites. Advanced Preparation None. Course Description Business fraud causes losses of billions of dollars annually. This course takes a dual approach to fraud, explaining how it can be detected as well as prevented. It shows how to identify common fraud schemes and how to proceed in an audit based on the guidance and requirements of SAS No. 99. To make topics easier to understand and apply, author Marshall Romney breaks the material down and includes many helpful examples. Publication/Revision Date This course was last updated February 2009.

Instructional Design

ii

Instructional Design Western CPE Self-Study courses are organized so as to lead you through a learning process using instructional methods that will help you achieve the stated learning objectives. You will be informed of the knowledge, skills, or abilities you will learn within each chapter of the course (clearly defined learning objectives); you will learn the material (course content and instructional methods); your learning will be reinforced (review questions); and your completion of meeting the learning objectives will be measured (final exam questions). These and additional instructional elements are listed and explained below. Please review this information completely to familiarize yourself with all instructional features and to help ensure you will achieve all course learning objectives. Course CPE Information The preceding section, “Course CPE Information,” details important information regarding CPE. If you skipped over that section, please go back and review the information now to ensure you are prepared to complete this course successfully. Table of Contents The table of contents allows you to quickly navigate to specific sections of the course. Outline The outline displays the organizational and instructional hierarchy of the course as well as the detailed contents of each chapter. Chapter Learning Objectives and Content Chapter learning objectives clearly define the knowledge, skills, or abilities you will gain by completing each section of the course. Throughout the course content, you will find various instructional methods to help you achieve the learning objectives, such as examples, case studies, charts, diagrams, and explanations. Please pay special attention to these instructional methods as they will help you achieve the stated learning objectives. Review Questions The review questions accompanying each chapter are designed to assist you in achieving the learning objectives stated at the beginning of each chapter. The review section is not graded; do not submit it in place of your final exam. While completing the review questions, it may be helpful to study any unfamiliar terms in the glossary in addition to chapter course content. After completing the review questions for each chapter, proceed to the review question answers and rationales. Review Question Answers and Rationales Review question answer choices are accompanied by unique, logical reasoning (rationales) as to why an answer is correct or incorrect. Evaluative feedback to incorrect responses and reinforcement feedback to correct responses are both provided. Glossary The glossary defines key terms. Please review the definition of any words of which you are not familiar. Index The index allows you to quickly locate key terms or concepts as you progress through the instructional material. Final Exam Final exams measure (1) the extent to which the learning objectives have been met and (2) that you have gained the knowledge, skills, or abilities clearly defined by the learning objectives for each section of the course. Unless otherwise noted, you are required to earn a minimum score of 70% to pass a course. You are allowed up to three attempts to pass the final exam. If you do not pass on your first attempt, please review the learning objectives, instructional materials, and review questions and answers before attempting to retake the final exam to ensure all learning objectives have been successfully completed.

Instructional Design

iii

Evaluation Upon successful completion of your online exam, we ask that you complete an online course evaluation. Your feedback is a vital component in our future course development. Thank you.

Western CPE Self-Study 243 Pegasus Drive

Bozeman, MT 59718 Phone: (800) 243-7395

Fax: (206) 774-1285 E-mail: [email protected]

Web site: www.westerncpe.com Notice: This publication is designed to provide accurate information in regard to the subject matter covered. It is sold with the understanding that neither the author, the publisher, nor any other individual involved in its distribution is engaged in rendering legal, accounting, or other professional advice and assumes no liability in connection with its use. Because regulations, laws, and other professional guidance are constantly changing, a professional should be consulted should you require legal or other expert advice. Information is current at the time of printing.

Table of Contents

iv

Table of Contents

Course CPE Information.............................................................................................................................. i

Instructional Design.................................................................................................................................... ii

Table of Contents....................................................................................................................................... iv

Outline.......................................................................................................................................................viii

Chapter 1: Introduction to Fraud...............................................................................................................1

Learning Objectives...................................................................................................................................1

Who commits fraud and why .....................................................................................................................3 A situational pressure ............................................................................................................................3 A perceived opportunity .........................................................................................................................4 A rationalization .....................................................................................................................................4

Introduction to SAS No. 99........................................................................................................................4 SAS N0. 82 ............................................................................................................................................5 Types of material misstatements ...........................................................................................................8 Fraudulent financial reporting ................................................................................................................8 Misappropriation of assets.....................................................................................................................9

Fraud risk factors.......................................................................................................................................9

Chapter 1 Review Questions...................................................................................................................11

Chapter 1 Review Question Answers and Rationales ............................................................................12

Chapter 2: Fraudulent Financial Reporting Risk Factors .....................................................................14

Learning Objectives.................................................................................................................................14

Pressures/incentives risk factors.............................................................................................................14 Threats to stability or profitability are present......................................................................................14 Pressure to meet expectations ............................................................................................................15 Threats to personal net worth ..............................................................................................................16 Excessive pressure to meet financial targets ......................................................................................16

Opportunity risk factors............................................................................................................................16 The nature of the industry or the entity’s operations ...........................................................................16 Complex or unstable organizational structure .....................................................................................17 Weak internal controls .........................................................................................................................18 Ineffective monitoring of management.................................................................................................19

Attitude/rationalization risk factors...........................................................................................................20

Chapter 2 Review Questions...................................................................................................................22

Chapter 2 Review Question Answers and Rationales ............................................................................23

Chapter 3: Misappropriation of Assets Risk Factors ............................................................................25

Learning Objectives.................................................................................................................................25

Pressure/incentive risk factors ................................................................................................................26 Personal financial obligations ..............................................................................................................26 Adverse relationships between the entity and employees...................................................................28

Opportunity risk factors............................................................................................................................29 Susceptibility of assets to misappropriation.........................................................................................29 Internal-control weaknesses ................................................................................................................30

Attitude/rationalization .............................................................................................................................32

Table of Contents

v

Common rationalizations .....................................................................................................................33 Attitude/rationalization risk factors .......................................................................................................33

Other asset-misappropriation risk factors................................................................................................34 Discrepancies in accounting records ...................................................................................................34 Conflicting or missing evidential matter ...............................................................................................35 Problematic or unusual relationships between the auditor and the client ...........................................35

Chapter 3 Review Questions...................................................................................................................37

Chapter 3 Review Question Answers and Rationales ............................................................................38

Chapter 4: Audit-Team Discussions, Obtaining Information, and Identifying and Assessing Risks....................................................................................................................................................................40

Learning Objectives.................................................................................................................................40

Discussion among engagement personnel regarding the risks of material misstatement due to fraud .40

Topics to be discussed............................................................................................................................40 The client being audited and its industry .............................................................................................40 Management override of internal controls ...........................................................................................41 Susceptibility of financial statements to fraud......................................................................................41 Professional skepticism .......................................................................................................................41

Obtaining information to identify fraud risks: Making inquiries and other information.............................41

Different groups auditors need to speak with about fraud.......................................................................43 Management ........................................................................................................................................43 Audit committee ...................................................................................................................................44 Internal audit ........................................................................................................................................44 Others in the organization....................................................................................................................44

Obtaining information to identify fraud risks: Analytical procedures .......................................................45

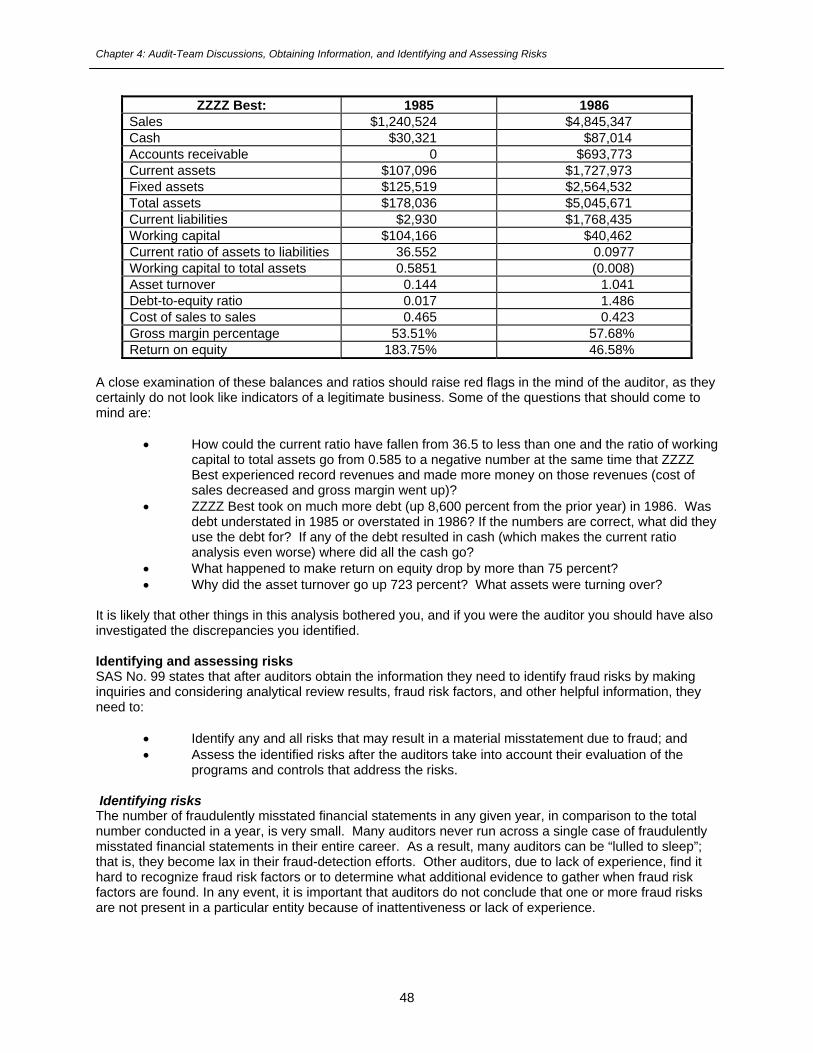

Identifying and assessing risks................................................................................................................48 Identifying risks ....................................................................................................................................48 Assessing the identified risks after evaluating the entity’s programs and controls..............................49

Chapter 4 Review Questions...................................................................................................................51

Chapter 4 Review Question Answers and Rationales ............................................................................52

Chapter 5: Assessment Results Response............................................................................................54

Learning Objectives.................................................................................................................................54

Overall responses to identified risks........................................................................................................54 Professional skepticism and audit evidence........................................................................................54 Assignment of personnel and supervision...........................................................................................55 Accounting principles ...........................................................................................................................55 Predictability of auditing procedures....................................................................................................55

Responses: The nature, timing, and extent of audit procedures ............................................................56 The nature of auditing procedures.......................................................................................................56 The timing of substantive tests ............................................................................................................56 The extent procedures are applied ......................................................................................................57

Responses: Misappropriation-of-assets and fraudulent-financial-statement fraud risks ........................57

Inventory fraud and responses to inventory-fraud risk ............................................................................58 Audit procedures when inventory fraud risks are identified .................................................................60

Inventory fraud case study: Phar-Mor .....................................................................................................62

Chapter 5 Review Questions...................................................................................................................63

Table of Contents

vi

Chapter 5 Review Question Answers and Rationales ............................................................................64

Chapter 6: Revenue-Recognition Fraud .................................................................................................66

Learning Objectives.................................................................................................................................66

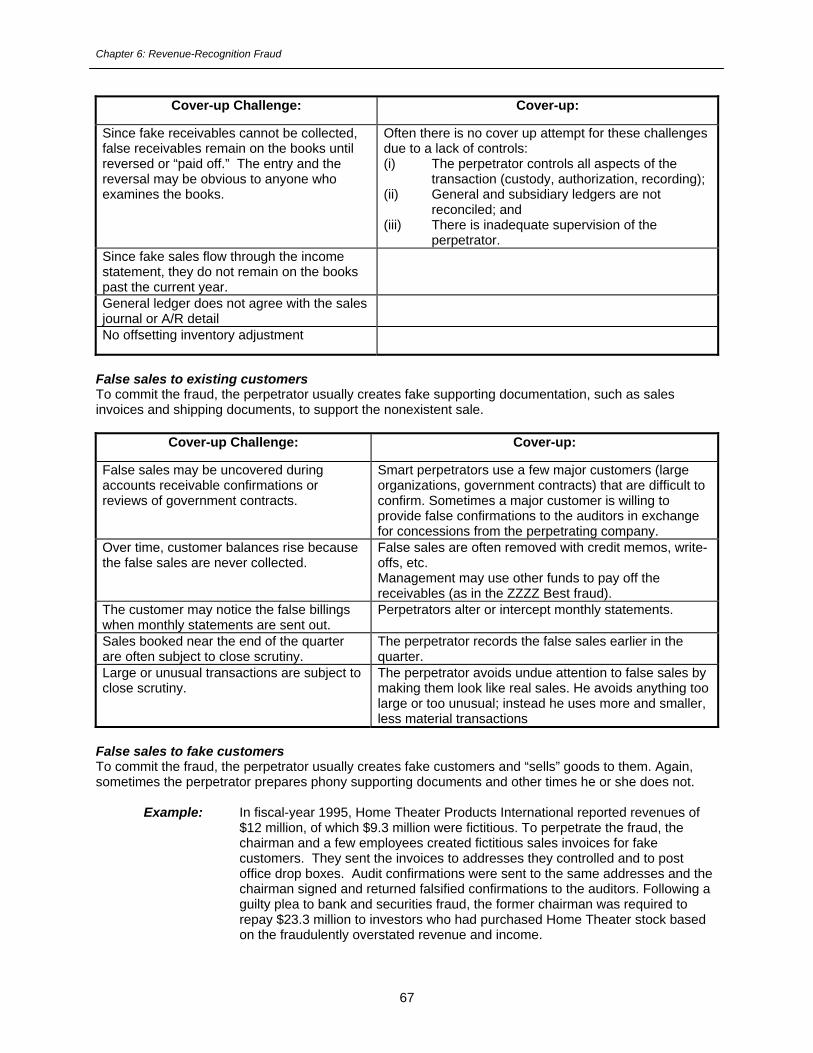

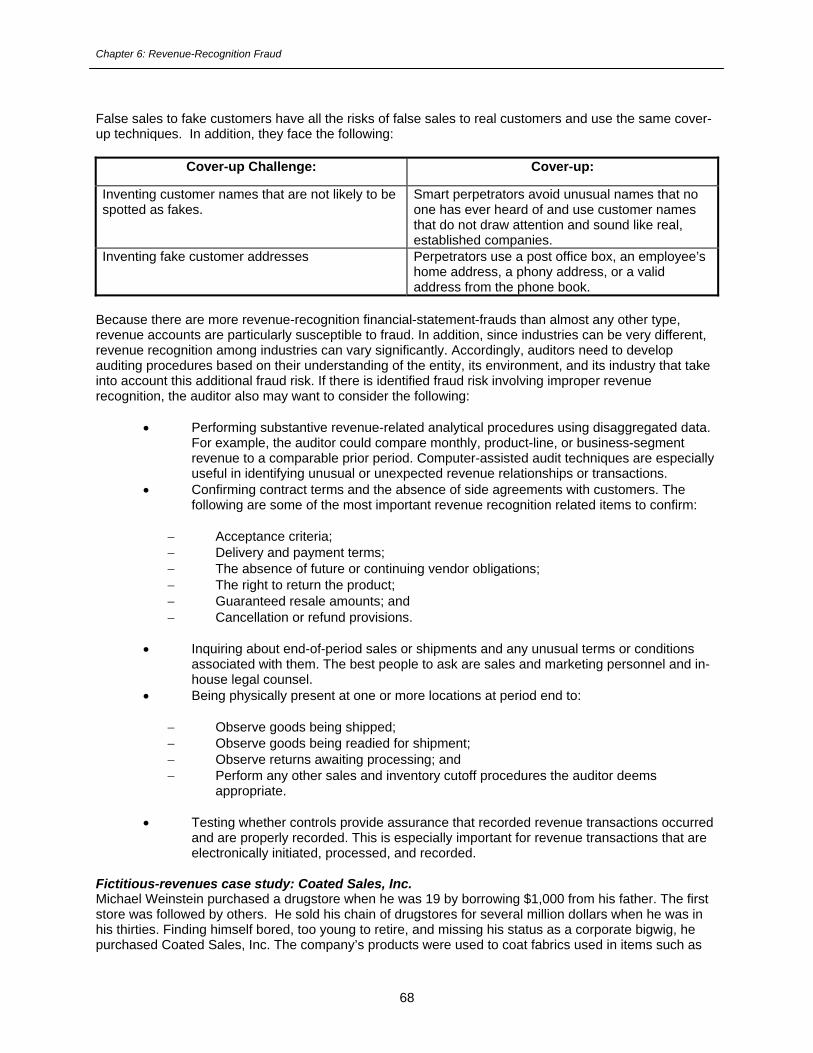

Booking fictitious revenues......................................................................................................................66 False journal entries.............................................................................................................................66 False sales to existing customers........................................................................................................67 False sales to fake customers .............................................................................................................67 Fictitious-revenues case study: Coated Sales, Inc..............................................................................68 Fictitious-revenues case study: ZZZZ Best .........................................................................................69

Cut-off frauds...........................................................................................................................................71 Hold the books open............................................................................................................................71 Close the books early ..........................................................................................................................71 Ship merchandise before the sale is final ............................................................................................72 Record revenue when services are still due........................................................................................72 Recognize revenue before sales contracts are finalized .....................................................................72 Stuff the channel ..................................................................................................................................72

Detecting fictitious revenues and timing differences ...............................................................................73

Timing differences case study: Regina Vacuum Cleaner Co..................................................................74

Bill-and-hold schemes .............................................................................................................................75 SEC enforcement case example .........................................................................................................76 Detecting bill-and-hold frauds ..............................................................................................................77

Chapter 6 Review Questions...................................................................................................................78

Chapter 6 Review Question Answers and Rationales ............................................................................79

Chapter 7: Disclosure Failures, Concealed Information, Management Override of Controls, and Management Estimates ............................................................................................................................81

Learning Objectives.................................................................................................................................81

Disclosure failures and concealed liabilities and losses..........................................................................81 Disclosure failures................................................................................................................................81 Audit procedures to detect undisclosed items .....................................................................................82 Fraudulent-disclosures case study: Midland State Bank.....................................................................84 Concealed liabilities and losses...........................................................................................................84

Responses...............................................................................................................................................86 Responses to the risk of management overriding controls..................................................................86 Examining journal entries and other adjustments................................................................................87 Evaluating the business rationale for significant unusual transactions ...............................................88 Management estimates........................................................................................................................88

Chapter 7 Review Questions...................................................................................................................92

Chapter 7 Review Question Answers and Rationales ............................................................................93

Chapter 8: Evaluating Audit Tests, Communicating Results, Documenting Audit Work, and Studying Fraud Schemes.........................................................................................................................95

Learning Objectives.................................................................................................................................95 Evaluating audit-test results.................................................................................................................95 Communicating fraud findings and documenting the auditor's consideration of fraud........................98 Documenting the auditor's consideration of fraud ...............................................................................99 To understand fraud, study fraud schemes .......................................................................................100 Avoiding legal liability during audits ...................................................................................................103

Table of Contents

vii

Chapter 8 Review Questions.................................................................................................................105

Chapter 8 Review Question Answers and Rationales ..........................................................................106

Glossary...................................................................................................................................................108

Index.........................................................................................................................................................110

Outline

viii

Outline

1) Chapter 1: Introduction to Fraud a. Who commits fraud and why

i. A situational pressure ii. A perceived opportunity iii. A rationalization

b. Introduction to SAS No. 99 i. SAS No. 82 ii. Types of material misstatements iii. Fraudulent financial reporting iv. Misappropriation of assets

c. Fraud risk factors 2) Chapter 2: Fraudulent Financial Reporting Risk Factors

a. Pressures/incentives risk factors i. Threats to stability or profitability are present ii. Pressure to meet expectations iii. Threats to personal net worth iv. Excessive pressure to meet financial targets

b. Opportunity risk factors i. The nature of the industry or the entity’s operations ii. Complex or unstable organizational structure iii. Weak internal controls iv. Ineffective monitoring of management

c. Attitude/rationalization risk factors 3) Chapter 3: Misappropriation of Assets Risk Factors

a. Pressure/incentive risk factors i. Personal financial obligations ii. Adverse relationships between the entity and employees

b. Opportunity risk factors i. Susceptibility of assets to misappropriation ii. Internal-control weaknesses

c. Attitude/rationalization i. Common rationalizations ii. Attitude/rationalization risk factors

d. Other asset-misappropriation risk factors i. Discrepancies in accounting records ii. Conflicting or missing evidential matter iii. Problematic or unusual relationships between the auditor and the client

4) Chapter 4: Audit-Team Discussions, Obtaining Information, and Identifying and Assessing Risks a. Discussion among engagement personnel regarding the risks of material misstatement

due to fraud b. Topics to be discussed

i. The client being audited and its industry ii. Management override of internal controls iii. Susceptibility of financial statements to fraud iv. Professional skepticism

c. Obtaining information to identify fraud risks: Making inquiries and other information d. Different groups auditors need to speak with about fraud

i. Management ii. Audit committee iii. Internal audit iv. Others in the organization

e. Obtaining information to identify fraud risks: Analytical procedures f. Indentifying and assessing risks

i. Indentifying risks

Outline

ix

ii. Assessing the identified risks after evaluating the entity’s programs and controls 5) Chapter 5: Assessment Results Response

a. Overall responses to identified risks i. Professional skepticism and audit evidence ii. Assignment of personnel and supervision iii. Accounting principles iv. Predictability of auditing procedures

b. Responses: The nature, timing, and extend of audit procedures i. The nature of auditing procedures ii. The timing of substantive tests iii. The extent procedures are applied

c. Responses: Misappropriation-of-assets and fraudulent-financial-statement fraud risks d. Inventory fraud and responses to inventory-fraud risk

i. Audit procedures when inventory fraud risks are identified e. Inventory fraud case study: Phar-Mor

6) Chapter 6: Revenue-Recognition Fraud a. Booking fictitious revenues

i. False journal entries ii. False sales to existing customers iii. False sales to fake customers

b. Cut-off frauds i. Hold the books open ii. Close the books early iii. Ship merchandise before the sale is final iv. Record revenue when services are still due v. Recognize revenue before sales contracts are finalized vi. Stuff the channel

c. Detecting fictitious revenues and timing differences d. Bill-and-hold schemes

i. SEC enforcement case example ii. Detecting bill-and-hold frauds

7) Chapter 7: Disclosure Failures, Concealed Information, Management Override of Controls, and Management Estimates

a. Disclosure failures and concealed liabilities and losses i. Disclosure failures ii. Audit procedures to detect undisclosed items iii. Concealed liabilities and losses

b. Responses i. Responses to the risk of management overriding controls ii. Examining journal entries and other adjustments iii. Evaluating the business rationale for significant unusual transactions iv. Management estimates

8) Chapter 8: Evaluating Audit Tests, Communicating Results, Documenting Audit Work, and Studying Fraud Schemes

a. Evaluating audit-test results b. Communicating fraud findings and documenting the auditor’s consideration of fraud c. Documenting the auditor’s consideration of fraud d. To understand fraud, study fraud schemes e. Avoiding legal liability during audits

Chapter 1: Introduction to Fraud

1

Chapter 1: Introduction to Fraud Learning Objectives After completing this section of the course, you should be able to:

1. Define fraud 2. List the conditions necessary to commit fraud 3. Identify the types of misstatements that occur when fraud is committed 4. List the fraud risk factors 5. Recognize the requirements outlined in SAS No. 99

Fraud is a growing problem in businesses throughout the world. The Association of Certified Fraud Examiners conducted a comprehensive study of 663 cases of fraud and released a Report to the Nation on Occupational Fraud and Abuse. In it they state the following statistics:

• Six percent of revenues in the United States are lost to fraud. • Fraud costs organizations in the United States over $600 billion dollars a year. To put it

on a more personal level, fraud costs employers an average of $4500 per employee per year.

• Men committed more fraud (53.5 percent) than women. • Small businesses, with fewer and less effective internal controls, were more vulnerable to

fraud (average loss of $127,000) than were large businesses (average loss of $97,000). • Over 16 percent of frauds have losses greater than $1 million dollars. • Managers and executives perpetrated 42 percent of the frauds and employees

perpetrated 64 percent. • Eighty-six percent of the frauds involved asset misappropriations and five percent

involved fraudulent financial statements. Fraud is an intentional act of deceit that results in the perpetrator gaining an unfair advantage over another person. It also usually results in an injury to the rights or interests of the other person. Fraud can be perpetrated using things such as presentation of false or misleading information, suppressions of the truth, lies, tricks, cunning, and theft or misappropriation of assets. Fraud perpetrators are often referred to as white-collar criminals to distinguish them from criminals who commit violent crimes. To commit most frauds, a perpetrator must take three different steps: the theft itself; converting the asset to personal use; and concealing the fraud. This is a theft of something of value such as cash, inventory, tools, supplies, equipment, or data. In some cases, there must be an intentional reporting of misleading financial information. The perpetrator converts the assets into a form that can be used personally. This conversion is usually required for all stolen assets except cash.

Χ Stolen checks must be deposited to an account from which the perpetrator can withdraw funds. Information (such as trade secrets or confidential company data) is often sold to someone such as a competitor.

Χ Industry experts estimate computer companies annually lose up to $200 billion in computer chips due to armed robbery and employee theft. In some circles computer chips are better than gold. Their theft is being referred to as the crime of the electronic age. Employees who steal these chips must convert them to cash. A sophisticated black market exists for the chips and they often change hands ten times in three days. When some companies run short of chips they often end up buying their stolen chips back.

Example: The following example illustrates how conversion practices can be carried out.

On the advice of its trusted manager, a brand-name carpet manufacturer approved purchase orders replacing looms described by a subsidiary as

Chapter 1: Introduction to Fraud

2

deteriorated past reconditioning. But instead of being discarded or sold to a dealer, the used looms, which were in perfectly sound condition, found their way to another building in a town close by, along with skilled workers to man them. In a short time, a new low-priced carpet maker was bidding against the original brand.

The perpetrator must conceal the crime in order to avoid detection and to continue the fraud. Where there are checks and balances in the system, the perpetrator often must "cook the books" to avoid detection. For example, the theft of cash may require the employee to doctor the bank reconciliation or to make false accounting entries to avoid detection. Concealing a fraud often takes more effort and time and leaves behind more evidence than the actual theft does. For example, taking cash takes only a few seconds, but altering records to hide the theft can be more challenging and time consuming. Perpetrators go to a great deal of effort to conceal their frauds. The concealment often involves falsified documents, including ones that are forged. For example:

• Management might conceal fraudulent financial reporting by creating fictitious invoices. • Employees who misappropriate cash might try to conceal their thefts by forging

signatures or creating invalid electronic approvals on disbursement authorizations. These concealment efforts make detecting fraud difficult, because a GAAP audit rarely involves document authentication. Furthermore, auditors are not trained to authenticate documents and are not expected to do so. Collusion among employees, management, and outsiders is another way frauds are concealed. This collusion often causes the auditor to believe that evidence is persuasive when it is, in fact, not persuasive. Some examples of collusion include the following:

• Management and employees can collude to present the auditors with evidence that control activities have been performed effectively when they were, in fact, not performed.

• A company employee may collude with an outsider to send a false confirmation. Even though fraud perpetrators do their best to hide their activities, they usually leave clues or tracks that give them away. Perpetrators are typically vulnerable at these same three specific points: when they commit the fraud, when they conceal it, and when they try and convert the stolen asset to spendable funds or turn the misstatement into personal gain. A typical fraud has a number of important elements or characteristics.

Χ To commit and conceal the fraud, the perpetrator has to gain the trust of the party being defrauded. Perpetrators use false or misleading information to get someone to give them money or take assets that have been entrusted to them. They hide their tracks by falsifying records.

Χ Few frauds are terminated voluntarily. Some fraud schemes are self-perpetrating in that if the perpetrator stops the fraud, he will be discovered. In addition, once perpetrators start a fraud it is very hard for them to stop because they begin to depend on the "extra" income.

Χ Perpetrators spend what they take; they rarely save or invest it. Χ The longer they go undetected, the more confidence perpetrators have in their schemes.

Many get greedy and take ever-larger amounts of money at more frequent intervals. These larger amounts are more prone to be scrutinized carefully and a scheme that might go undetected for some time is uncovered because the amounts taken rise to unacceptable levels.

Chapter 1: Introduction to Fraud

3

Χ As time passes, many perpetrators grow careless or overconfident and do not take sufficient care to effectively hide their fraud. Those that do usually make a mistake that leads to their apprehension.

Χ In time, the sheer magnitude of the amount of the fraud leads to its detection. Χ The most significant contributing factor in most frauds is the failure to enforce existing

internal controls. Who commits fraud and why Several studies have attempted to produce a profile of the typical fraud perpetrator. Fraud perpetrators seem to fall into one of two groups. The first group is people who, prior to committing the fraud, do not have a criminal record. In other words, they are not "career criminals.” Studies conclude that it is relatively difficult to profile these fraud perpetrators or to predict who will move from being an otherwise honest, upright citizen to becoming a fraud perpetrator. Recently more career criminals have found fraud to be a lucrative occupation. For example, FBI director Louis Freeh has testified before the Senate Special Committee on Aging that cocaine distributors in Florida and California are switching to less risky but equally profitable health-care scams. Their chances for detection are much lower than with trafficking drugs and the profits are staggering. The bureau has some, 1500 cases backlogged and would need to double the size of its 249-agent investigative team to be taken seriously by scam artists who trade in bogus medical cards and phony insurance claims. When a new fraud is discovered, one of the most frequently asked questions is "Why in the world did he or she do it?" The question is asked so frequently because the perpetrator is often a well-respected employee who seemingly has everything to lose and not much to gain by committing the fraud. Research shows that three conditions are usually necessary for fraud to occur: (i) a situational pressure; (ii) a perceived opportunity to commit the fraud; and (iii) a rationalization. A situational pressure A situational pressure is the problem that motivates them to act dishonestly. These pressures can be financial, such as high personal debts; lifestyle, such as gambling or drug addiction; and work-related, such as peer pressures or the fear of losing one’s job. Often the pressure is on the company, not on the individual. For example, an urgent need for working capital or higher earnings may motivate an individual to fraudulently misstate financial statements.

Example: When federal investigators raided an illegal gambling establishment, they found that Roswell Steffen, who earned $11,000 dollars a year, was betting up to $30,000 a day at the racetrack. Investigators at Union Dime Savings Bank discovered he had embezzled and gambled away $1.5 million dollars of their money over a three-year period. Steffen, a compulsive gambler, started out by borrowing $5,000 to place a bet on a "sure thing" that did not pan out. He embezzled ever-increasing amounts trying to win back the original money he had "borrowed." Steffen committed his fraud by transferring money from inactive accounts to his own account. If the owner of an inactive account complained, Steffen, who was the chief teller and had the power to resolve these types of problems, replaced the money by taking it from some other inactive account. After he was caught, he was asked how the fraud could have been prevented. He said the bank could have coupled a two-week vacation period with several weeks of rotation to another job function. That would have made his embezzlement, which required his physical presence at the bank and his constant attention, almost impossible to cover up.

Often people believe these pressures are nonsharable and not solvable in a socially sanctioned manner. These pressures can become so intense that a person feels that they have to act and he or she decides that fraud is the only (or the most satisfactory) solution. One inmate serving time in prison for fraud described his pressure this way: "I'm as honest as the next fellow, but I was backed up against the wall. I did not have any other alternative."

Chapter 1: Introduction to Fraud

4

A perceived opportunity The perpetrator perceives an opportunity to commit and conceal the dishonest act (viewed as a way to secretly resolve the nonsharable pressure). Opportunities may be created by individuals or permitted by the company. Individuals can create opportunities by increasing their knowledge of company operations, advancing to a position of trust where they can override internal controls, or being the only person who performs a particular procedure. A company increases opportunities for fraud by allowing related-party transactions, having an unnecessarily complex business structure, and failing to create or enforce an adequate system of internal controls. A rationalization There are acceptable ways for people to meet many of the situational pressures they face. For example, they can take out loans to buy a home or car or finance big Christmas spending with credit-card financing. However, there are many situational pressures that cannot be meet in a socially acceptable manner. For example, it is hard to get a loan to repay speculative losses, gambling debts, or to feed a drug addiction. It is also hard for some people to deal in a positive way with their feelings of resentment. When a person decides to solve the problem in an illegal or socially unacceptable manner they must, in their minds, either consciously "cross the line" from being an honest person to a dishonest person, or somehow justify their actions or rationalize them as not really being dishonest. A rationalization is what a perpetrator uses to justify or reconcile his or her dishonest action with his or her personal views of integrity. The decision to commit fraud is determined by the interaction of the three forces. A person with personal integrity and little opportunity or pressure to commit fraud will most likely behave honestly. However, the conditions for fraud become more enticing as individuals with less personal integrity are placed in situations with increasing pressures and greater opportunities to commit the crime. Individuals placed in difficult circumstances may feel that the only way out is to choose between their integrity and one or more of the following: their businesses, positions in the community, their reputations, or prestige. When they choose to sacrifice their integrity, fraud is often the result. Individuals with a great deal of personal integrity may be able to withstand tremendous pressures and a great opportunity. However, some will argue that everyone has their price. It is reported that Abraham Lincoln once angrily kicked a man out of his office. When Lincoln was asked about his actions, he stated that he had just turned down a substantial bribe. Then he said "Every man has his price and he was getting close to mine." Introduction to SAS No. 99 Over the years the auditing profession has provided its members with guidance on their responsibility to detect fraud. Despite the direction, the auditing profession has been the target of litigation and criticism regarding this guidance and the failure of auditors to detect material frauds. Many members of the investing public believe that auditors should be able to detect almost all cases of fraud. In fact, one survey a number of years ago revealed that 66 percent of the respondents thought that the primary purpose of an audit is to detect fraud. Auditors, on the other hand, have maintained that it is virtually impossible for auditors to detect all cases of fraud. The result has been what some people refer to as the “expectation gap.” The following important events took place in the early 1990s and motivated the Auditing Standards Board (ASB) to develop and issue SAS No. 99, Consideration of Fraud in a Financial Statement Audit.

• In 1992, the AICPA’s Expectation Gap Roundtable raised concerns that SAS No. 53 was not sufficiently successful in narrowing the expectation gap in the area of fraud.

• In 1993, the Public Oversight Board issued a report recommending that the ASB develop guidelines to help auditors assess the likelihood that management fraud may be occurring.

Chapter 1: Introduction to Fraud

5

• In 1993, the AICPA Board of Directors endorsed the recommendations of others that something be done about the “fraud problem.”

SAS N0. 82 In 1997, SAS No. 82, Consideration of Fraud in a Financial-Statement Audit, was issued by the Auditing Standards Board (ASB). Its purpose was to provide operational guidance to auditors on how to better consider material fraud while conducting a financial-statement audit. SAS No. 99 replaces SAS No. 82. The ASB felt that just as companies have a responsibility to continuously focus on fraud prevention and detection, the CPA profession has a responsibility to seek to continuously improve its ability to detect fraud in connection with external audits. The ASB perceived that the public expected auditors to detect fraud when they conduct financial-statement audits. They decided to do something to try and close the expectation gap between the profession and the users of financial statements. The result of their efforts is SAS No. 99, which establishes standards and provides guidance to auditors in fulfilling their responsibility as it relates to fraud in an audit of financial statements conducted in accordance with generally accepted auditing standards (GAAS). SAS No. 82 clarified, but did not increase, the auditor’s responsibility to detect fraud when conducting a financial-statement audit. It provided auditors with procedural and operational guidance to help them detect material misstatements in financial statements caused by fraud. It also clarified the responsibility auditors have to plan and perform an audit so that they can obtain reasonable assurance that the financial statements they audit are free from material misstatement caused by either error or by fraud. In addition, SAS No. 82 provided additional guidance on the standard of due professional care, including the need to exercise professional skepticism. SAS No. 82 was one of the auditing profession’s most highly publicized SAS’s. Many people feel it was written to re-sensitize auditors to the possibility of fraud. Auditors have always had the responsibility to detect material misstatements caused by fraud. These responsibilities have not changed. What has changed is the auditor’s performance, that is, what is required of auditors to fulfill those responsibilities. Sometime after SAS No. 82 was issued, several panels and committees were organized and several studies of fraud were funded. The purpose of both was to determine how to improve audit procedures and guidance with respect to fraud. In response to their findings, a Fraud Task Force was formed to revise SAS No. 82. The result is SAS No. 99, also titled Consideration of Fraud in a Financial Statement Audit. SAS No. 99 does not change an auditor’s responsibility to both plan and conduct audits so that reasonable assurance can be obtained about whether the financial statements are free of material misstatement, whether caused by error or fraud. However, SAS No. 99 does the following:

• It establishes standards and provides guidance with respect to fraud while conducting a financial-statement audit in accordance with generally accepted auditing standards (GAAS);

• It provides guidance on the discussions among engagement personnel that should take place regarding the risks of material misstatement due to fraud;

• It states that the audit team should design tests that are unpredictable and unexpected by the client, including testing areas, locations, and accounts that otherwise might not be tested; and

• It states that procedures should be developed to test for management override of controls on every audit.

Chapter 1: Introduction to Fraud

6

It is the opinion of the ASB that the requirements and guidance in SAS No. 99 will substantially improve audit performance and increase the likelihood that auditors will detect material fraudulent financial statements. Much of the improved performance will come from an increased focus on professional skepticism as well as the requirement to ask management and other employees about the existence of fraud in the company. Unfortunately, it is not possible for an auditor to be absolutely sure that the financial statements are free of material misstatement resulting from fraud. According to SAS No. 99, a “material misstatement may not be detected because of the nature of audit evidence or because the characteristics of fraud may cause the auditor to rely unknowingly on audit evidence that appears to be valid, but is, in fact, false and fraudulent.” SAS No. 99 then explains that characteristics of fraud include concealment through:

• Collusion by both internal and third parties; • Withheld, misrepresented, or falsified documentation; and • The ability of management to override or instruct others to override what otherwise

appear to be effective controls. Although auditors have a responsibility to detect material fraud, management has the responsibility of designing and implementing controls and programs to prevent and detect fraud. SAS No. 1 (AU sec. 110.03) states "Management is responsible for adopting sound accounting policies and for establishing and maintaining internal control that will, among other things, record, process, summarize, and report transactions (as well as events and conditions) consistent with management's assertions embodied in the financial statements." However, members of the management team are not the only ones who are responsible for overseeing the financial-reporting process. For example, the board of directors and the audit committee help establish appropriate controls to prevent and detect fraud. They also have a responsibility to help set a proper organizational tone and create and maintain an organizational culture of honesty, integrity, and high ethical standards. Brief overview of SAS No. 99 The main components of SAS No. 99 are discussed in this section. Description and characteristics of fraud: Fraud is an intentional act of deceit by management, employees, or third parties, accompanied by a concealment of the true facts. According to SAS No. 99, auditors are not lawyers and “do not make legal determinations of whether fraud has occurred. Rather, the auditor's interest specifically relates to acts that result in a material misstatement of the financial statements.” Auditors are concerned about two types of misstatements: Fraudulent financial reporting and Misappropriation of assets (theft, defalcation, etc.).1 Discussion among engagement personnel regarding the risks of material misstatement due to fraud: While planning the audit, audit-team members should discuss among themselves how and where the company’s financial statements might be susceptible to material misstatement due to fraud. This will help team members remember how important it is to adopt an appropriate mind-set of professional skepticism, especially with respect to the potential for material misstatement due to fraud.2 Obtaining the information needed to identify the risks of material misstatement due to fraud: To assess the risks of material misstatement due to fraud, SAS No. 99 requires auditors to gather more information than simply considering the risk factors, as was required in SAS No. 82. The audit team now must expand their inquiries of management, the audit committee, the internal audit function, and others in the organization (such as operating management and employees in positions of authority). They must

1 SAS No. 99, Paragraphs 5-12. 2 SAS No. 99, Paragraphs 13-16.

Chapter 1: Introduction to Fraud

7

also consider the results of the analytical procedures performed in planning the audit and consider fraud risk factors and other information.3 Identifying risks that may result in a material misstatement due to fraud: Auditors should use the information they gather to identify the risks that may result in a material misstatement due to fraud.4 Assessing risks after evaluation: Another important component of SAS No. 99 is assessing the identified risks after taking into account an evaluation of the entity’s programs and controls that address the risks. Auditors must evaluate an entity's programs and controls that address the identified risks of material misstatement due to fraud. They should then assess these risks based on their evaluation.5 Responding to the results of the assessment: The auditor must respond to risks that have an overall effect on how the audit is conducted, that relate to the nature, timing, and extent of the auditing procedures to be performed, and are related to material misstatements due to management override of controls.6 Evaluating audit test results: Auditors are required to assess the risk of material fraudulent misstatements throughout the audit. When the audit is completed, the auditor must evaluate whether this preliminary assessment is affected by the evidence gathered during the audit. In addition, the auditor must determine whether any identified misstatements may indicate the presence of fraud. If they do, the auditor must determine the impact of this on the financial statements and the audit.7 Communicating with management, the audit committee, and others about possible fraud: Guidance is provided on if, how, and when auditors must communicate their findings about fraud to management, the audit committee, and others.8 Documenting the auditor's consideration of fraud: SAS No. 99 significantly extends the auditor’s documentation requirements with respect to fraud. Auditors are now required to document their compliance with virtually all the major requirements of SAS No. 99 in order to help ensure that they comply with its new requirements. The items that auditors must document are listed.9 Appendices and other information: The following additional information is also provided in SAS No. 99: Appendix A: Examples of Fraud Risk Factors; Appendix B: Proposed Amendment to Statement on Auditing Standards No. 1, Codification of Auditing Standards and Procedures; and The affect of SAS No. 82 on auditing standards. What does SAS No. 99 do? SAS No. 99: Supersedes Statement on Auditing Standards No. 82, Consideration of Fraud in a Financial Statement Audit; Supersedes AU sec. 316; and Amends SAS No. 1, Codification of Auditing Standards and Procedures, vol. 1, AU sec. 230, “Due Professional Care in the Performance of Work.” Effective date: SAS No. 99 is effective for financial-statement audits beginning on or after December 15, 2002. It applies to all financial-statement audits performed in accordance with generally accepted accounting principles (GAAP).

3 SAS No. 99, Paragraphs 17-31. 4 SAS No. 99, Paragraphs 32-38. 5 SAS No. 99, Paragraphs 39-42. 6 SAS No. 99, Paragraphs 43-66. 7 SAS No. 99, paragraphs 67-77. 8 SAS No. 99, Paragraphs 78-81. 9 SAS No. 99, Paragraph 82.

Chapter 1: Introduction to Fraud

8

Financial-statement audits versus fraud audits: It is important that financial-statement audits are not confused with fraud audits. These two types of audits differ in several material aspects. A financial-statement audit is conducted in accordance with generally accepted auditing standards (GAAS). Its purpose is to express an opinion on how fairly financial statements represent, in all material respects, the financial position, results of operations, and cash flows of a company, in conformity with GAAP. An auditor cannot obtain absolute assurance that material misstatements in the financial statements will be detected. There are at least two reasons why even a properly planned and performed audit may not detect a material misstatement resulting from fraud. First, there are the concealment aspects of fraud, including the fact that fraud often involves collusion or falsified documentation. Second, there is the need to apply professional judgment in the identification and evaluation of fraud risk factors and other conditions. In a fraud audit, the auditor does not express an opinion regarding the fair presentation of the financial statements. Instead, the auditor is called in as a consultant because fraud is suspected or has been discovered. In a fraud audit, the auditor may be asked to do a number of things, such as determine how the fraud occurred, who committed it, how much was taken, or the nature and amount of the misrepresentation. In the event of a lawsuit, the auditor might also be asked to serve as an expert witness or to support the litigation in some other way. Types of material misstatements Although there are many different types of fraud, auditors are most concerned with fraudulent acts that result in financial statements being materially misstated. These misstatements can result from either intentional or unintentional actions. The unintentional actions are usually referred to as errors or omissions. The intentional actions usually constitute a fraud. With respect to fraud, SAS No. 99 states that there are two different types of material misstatements that are important when auditing financial statements: (i) fraudulent financial reporting; and (ii) misappropriation of assets. These two types of material misstatements are discussed below. Fraudulent financial reporting Fraudulent financial reporting is intentional misstatements or omissions of amounts or disclosures in financial statements that are intended to deceive financial-statement users. They are usually perpetrated by management and are almost always material in amount or else they would not achieve their intended purpose. Those harmed by the fraud are usually the third-party users of the financial statements. Those who benefit directly from the fraud are the entity whose statements are misrepresented. Perpetrators benefit indirectly by such things as obtaining a raise, having the value of their stock rise, not losing their jobs, or gaining more status, power, or prestige in the company or among their peer groups. SAS No. 99 provides the following fraudulent-financial-reporting examples:

• Manipulation, falsification, or alteration of accounting records or documents from which financial statements are prepared;

• Misrepresentation or intentional omission of events, transactions, or other significant information; and

• Intentional misapplication of accounting principles relating to amounts, classification, manner of presentation, or disclosure.

Example: A real estate company that was going public purchased and resold several

nursing homes. The company recognized $2 million in current and deferred profits, even though it only paid a $30,000 down payment when it bought the properties and only received $25,000 in cash when it sold them. The transaction boosted sales to $22 million from $6.7 million and converted its net income from a large loss to a gain.

Chapter 1: Introduction to Fraud

9

Misappropriation of assets Misappropriation of assets is the theft of an entity’s assets, whether by a lower-level employee or by someone in management. Misappropriation of assets often involves creating or using false or misleading documents or records. It can be perpetrated by a single person, or by collusion among employees, management, outsiders, and others. The entity is the one harmed and the employee benefits directly and immediately. Although there are many more immaterial misappropriations of assets than there are material ones, the auditor is primarily concerned with material misappropriations of assets. As a result of the theft, the company’s financial statements are not presented in accordance with generally accepted accounting principles. SAS No. 99 provides the following misappropriation-of-assets examples:

• Embezzling receipts; • Stealing assets; and • Causing a company to pay for goods or services that the company did not receive.

Example: The man in charge of shipping at a large manufacturer of gas appliances and

related equipment had a wife and nine children to support on a small salary. The pressures of family expenses finally became so great that he began stealing small appliances and fixtures from the warehouse. He sold the items and used the money to help make ends meet.

As explained earlier, both types of fraud usually involve a pressure or an incentive to commit fraud, a perceived opportunity to do so, and some form of rationalization. These three conditions usually are present for both types of fraud, although the nature of the pressure, opportunity, and rationalization can be quite different. For example, top management might perpetrate fraudulent financial reporting because they are under pressure to achieve an unrealistic earnings target. On the other hand, individual employees might misappropriate assets because they are living beyond their means. Fraud risk factors Most crimes leave unmistakable evidence. For example, when a bank is robbed there are often witnesses and even videotapes of the theft. When a restaurant is robbed after hours there are broken cash registers and signs of forced entry. There are often fingerprints, hair or fiber samples, or some other evidence that might identify the unknown perpetrator. In most cases, the investigator knows that a crime has been committed but does not know who perpetrated it. In contrast, in a fraud the difficult thing to prove is that a crime actually took place. When a fraud has taken place, the perpetrator is usually known to the company; in fact it is usually one of the company’s employees. Fraud is hard to detect because it is almost never observed directly. There are no videotapes, witnesses, broken doors or locks, smoking guns, or dead bodies. Furthermore, the person committing the fraud is usually a company employee with the power and authority to process company transactions. They are supposed to have access to company records and documents, as well as the company’s information system. In most frauds the perpetrator takes great pains to conceal his or her tracks and to make everything appear normal. The perpetrator usually hides or disguises the fraudulent transactions, intermingles them with valid transactions, and processes them through the company’s accounting information system. Because the fraudulent transactions are processed as if they were legitimate business transactions, it is often difficult to spot them. If a company does stumble over one of these fraudulent transactions, it is often not clear whether it is an intentional or unintentional error. Therefore, the first step in most investigations is to determine whether or not a crime has actually been committed. Often there is no direct evidence that a fraud is taking place. Therefore, those who want to detect fraud must learn to identify the indicators, or red flags, that are present in most frauds. These clues, which are often referred to as fraud symptoms, can point to the existence of fraud.

Chapter 1: Introduction to Fraud

10

A perpetrator is left exposed and leaves fraud symptoms at three key points:

• When the item of value, such as cash, is stolen or some part of the financial statement is materially misrepresented.

• When the perpetrator conceals his or her actions so that the fraud scheme is not detected. Concealment often requires documents or records to be created or altered, journal entries to be made, or some other effort made to ensure that the books balance.

• When the perpetrator converts noncash assets into a form that he or she can use or spend.

As each of these three steps is undertaken the perpetrator is vulnerable. For example, the perpetrator could be spotted taking the physical asset or misstating the information. The created or altered documents that hide the fraud can be spotted by some one else. The perpetrator could be caught trying to cash stolen checks. The vulnerability is not limited to the point in time when each of these three steps is taken. It extends for some time, often almost indefinitely. For example, it could be days or weeks later that the stolen item is missed. The auditor could note the altered document during the year-end audit. The stolen check that is cashed could be spotted by the company when it reconciles its checking account. Whenever a fraud takes places there are a number of signs or manifestations that a fraud has taken place, for example, missing assets, fraudulent documents, and forged checks. These signs or manifestations are referred to as fraud symptoms or fraud risk factors. There are symptoms at each point of the fraud: the theft, the concealment, and the conversion. Being aware of these symptoms and actively searching for them is one of the best ways to detect fraud. The fact that fraud symptoms are present is not a guarantee that fraud actually exists. At that point there are merely suspicions that a fraud might have taken place. However, every time there is a fraud one or more of these symptoms is present. Fraud symptoms should be thoroughly investigated to determine whether they are present due to fraud or due to other conditions. An active approach to searching for symptoms and investigating fraud also serves as a deterrent to further fraud taking place. Unfortunately, most people are unaware of what constitutes a fraud symptom. As a result, most fraud symptoms are never recognized. Oftentimes those that are familiar with fraud symptoms are so busy that they do not notice them. Many of those fraud symptoms that are noticed are never properly investigated. As a result, many frauds are never detected or are not uncovered as soon as they could be. The result is an ever-increasing amount lost to fraud.

Chapter 1 Review Questions

11

Chapter 1 Review Questions The review questions accompanying each chapter are designed to assist you in achieving the learning objectives stated at the beginning of each chapter. The review section is not graded; do not submit it in place of your final exam. While completing the review questions, it may be helpful to study any unfamiliar terms in the glossary in addition to chapter course content. After completing the review questions for each chapter, proceed to the review question answers and rationales. 1. Which of the following is the best definition of fraud?

A. An act that unintentionally deviates from what is correct, right, or true. B. An excessive and wrongful misuse of assets. C. An intentional act of deceit. D. The act of succumbing to temptation and beginning questionable practices.

2. Which of the following is an element or characteristic of fraud?

A. Perpetrators often save or invest the money they take. B. The longer the fraud is undetected, the more confidence the perpetrator has. C. Frauds are usually terminated voluntarily. D. As time goes on, perpetrators hide their fraud more cautiously.

3. Having an unnecessarily complex business structure is an example of which of the three

conditions necessary for fraud to occur?

A. Perceived opportunity. B. Situational pressure. C. Rationalization. D. Conversion.

4. Which employee committed fraudulent financial reporting?

A. Larry stole a laptop. B. Kathryn embezzled accounts receivable. C. Mike capitalized research and development costs. D. Anna created fictitious invoices in the name of her bogus company.

5. Which of the following is true regarding fraud risk factors or symptoms?

A. Frauds are usually caught while they are taking place. B. When there are fraud symptoms, fraud exists. C. There is often direct evidence that fraud is taking place. D. It is difficult to prove that an actual crime has taken place.

Chapter 1 Review Question Answers and Rationales

12

Chapter 1 Review Question Answers and Rationales Review question answer choices are accompanied by unique, logical reasoning (rationales) as to why an answer is correct or incorrect. Evaluative feedback to incorrect responses and reinforcement feedback to correct responses are both provided. 1. Which of the following is the best definition of fraud?

A. An act that unintentionally deviates from what is correct, right, or true. Incorrect, because this is describes an error.

B. An excessive and wrongful misuse of assets. Incorrect, because this describes abuse. C. An intentional act of deceit. Correct, because fraud is an intentional act of deceit

that results in the perpetrator gaining an unfair advantage over another person. D. The act of succumbing to temptation and beginning questionable practices. Incorrect,

because this describes corruption. 2. Which of the following is an element or characteristic of fraud?

A. Perpetrators often save or invest the money they take. Incorrect, because perpetrators spend what they take; they rarely save or invest it.

B. The longer the fraud is undetected, the more confidence the perpetrator has. Correct, because perpetrators gain more confidence as their scheme goes undetected. Many will start taking larger amounts of money at more frequent intervals.

C. Frauds are usually terminated voluntarily. Incorrect, because few frauds are terminated voluntarily. Some schemes are self-perpetrating, meaning that if the fraud is to stop, the perpetrator will be discovered.

D. As time goes on, perpetrators hide their fraud more cautiously. Incorrect, because as time passes, many perpetrators grow careless or overconfident and do not take sufficient care to effectively hide their fraud.

3. Having an unnecessarily complex business structure is an example of which of the three

conditions necessary for fraud to occur?

A. Perceived opportunity. Correct, because a perceived opportunity occurs when a perpetrator is aware that the company is weak in certain areas that may allow fraud to occur. A company increases these opportunities by allowing related-party transactions, having an unnecessarily complex business structure, and failing to create or enforce adequate internal controls.

B. Situational pressure. Incorrect, because a situational pressure is a problem that motivates dishonest actions, such as high personal debt.

C. Rationalization. Incorrect, because rationalization is the justification for the dishonest action, such as the perpetrator believing he will pay the company back once he has won the stolen money back.

D. Conversion. Incorrect, because a conversion takes place when the asset stolen needs to be converted to a form that can be used personally. This is one of the steps a perpetrator usually needs to take to commit the fraud.

4. Which employee committed fraudulent financial reporting?

A. Larry stole a laptop. Incorrect, because stealing a laptop is a misappropriation of assets. Although the company will not be pleased with Larry’s actions, the auditors are primarily concerned with material misappropriation of assets.

B. Kathryn embezzled accounts receivable. Incorrect, because SAS No. 99 provides examples of misappropriation of assets which includes embezzling receipts.

Chapter 1 Review Question Answers and Rationales

13

C. Mike capitalized research and development costs. Correct, because fraudulent financial reporting includes intentional misapplication of accounting principles relating to amounts, classification, manner of presentation, or disclosure. GAAP requires research and development costs to be expensed in the period occurred. If Mike was aware of this, fraud has occurred.

D. Anna created fictitious invoices in the name of her bogus company. Incorrect, because this is an example of a misappropriation of assets. Misappropriation of assets can involve creating or using false or misleading documents or records.

5. Which of the following is true regarding fraud risk factors or symptoms?

A. Frauds are usually caught while they are taking place. Incorrect, because the time it takes to discover the fraud can extend for some time, often almost indefinitely.

B. When there are fraud symptoms, fraud exists. Incorrect, because the fact that fraud symptoms are present is not a guarantee that fraud actually exists.

C. There is often direct evidence that fraud is taking place. Incorrect, because often there is no direct evidence that fraud is taking place. Those who want to detect fraud must learn to identify the red flags that are present in most frauds.

D. It is difficult to prove that an actual crime has taken place. Correct, because fraud is difficult to prove because it is almost never observed directly.

Chapter 2: Fraudulent Financial Reporting Risk Factors

14

Chapter 2: Fraudulent Financial Reporting Risk Factors Learning Objectives After completing this section of the course, you should be able to:

1. Identify the fraudulent financial reporting risk factors identified in SAS No. 99, which include pressure/incentive risk factors, opportunity risk factors, and attitude/rationalization risk factors

SAS No. 99 has as its basis a “where there is smoke, there is fire” concept. The smoke is the clues, or conditions, that might alert auditors to the possible existence of fraud. The fire is fraud. In essence, SAS No. 99 states that one should learn to identify the smoke (what it calls “risk factors”) in order to be able to find the fire. SAS No. 99 identifies three different categories of risk factors related to fraudulent financial reporting (pressures/incentives, opportunities, and attitudes/rationalizations) and the same three categories of risk factors that relate to misstatements arising from misappropriation of assets. All six of these categories should be considered during the planning phase of an audit engagement as well as during field-work. The three fraudulent-financial-reporting categories are the topic of this chapter. In SAS No. 99 the fraud risk factors are presented in Appendix A, which is titled “Examples of Fraud Risk Factors.” Although the fraud risk factors described in Appendix A of SAS No. 99 cover a broad range of situations typically faced by auditors, they are only examples. The example risk factors in SAS No. 99 were compiled from research conducted by the author and many other researchers, as well as many practicing CPAs. Some may be of greater or lesser significance depending on the company’s size, ownership characteristics, industry, etc. In practice, the auditor should use any of the listed risk factors that are applicable to his or her client and should add additional risk factors as the situation merits. In this book, the order in which the example risk factors appear is not reflective of their frequency of occurrence or relative importance. The auditor should use professional judgment to evaluate the evidence gathered to:

• Determine if the evidence indicates that one or more fraud risk factors are present; • Assess the significance and relevance of fraud risk factors; • Identify and assess the risks of material fraud if risk factors are present; and • Determining the appropriate audit response.

Pressures/incentives risk factors The first fraudulent-financial-reporting category that SAS No. 99 identifies deals with the pressures, incentives, or motives management has for perpetrating fraud. For all practical purposes, there are scores of reasons why management is motivated to perpetrate fraud. The four most frequent are discussed below. Included among the different fraud risk factors are brief descriptions of past frauds that help to illustrate why a particular risk factor is important or how it was a factor or indicator of fraud. Threats to stability or profitability are present Management may be motivated to perpetrate fraud if it is believed that financial stability or profitability is threatened by economic, industry, or entity operating conditions. Such conditions are discussed below.

• There may be very significant competition or a high degree of market saturation, especially when accompanied by declining margins.

• The company may be highly vulnerable to rapid changes in the industry, such as changing technology or product obsolescence, or to changes in interest rates.

• The industry or overall economy may be declining with increasing business failures and significant declines in customer demand.

• Operating losses that make the threat of bankruptcy, foreclosure, hostile takeover, or

Chapter 2: Fraudulent Financial Reporting Risk Factors

15

other threats to ownership may be imminent. There is a significant relationship between impending business failures and fraud. When faced with the choice of losing their business and everything they have worked for over the years or "fudging" (in their eyes) the numbers a little bit in order to keep the business going, owners and employees may choose the latter course.

• There may be an inability to generate cash flows from operations while reporting earnings and earnings growth, or there may be recurring negative cash flows from operations.

• Management wants to achieve, maintain, or increase a level of growth or profitability that is significantly greater than that of other organizations in the same industry or at least wants to be perceived as doing so.

Example: The Equity Funding Fraud was one of the largest computer-assisted frauds in

history. In 1969, Equity Funding's stock sold for over $80, but because of difficult times in the insurance industry the stock fell to $12 by late 1970. Company management held vast holdings of the stock and were intent on boosting its price. They felt that the only way to do that was through higher and higher earnings. Unfortunately, new sales were down for the industry and existing policyholders were not renewing their insurance. To pump up earnings, Equity Funding began reinsuring fictitious policies. Sales skyrocketed and the reported insurance in force tripled. The industry was amazed at Equity Funding's ability to turn its program around and show surprising gains while everyone else was experiencing a severe decline.