Residential Refresher Course Issues & Controversies in Income Tax Assessment By Mulesh Savla FCA, DISA (ICAI), [email protected]Tax Practitioners’ Association - Aurangabad The Misty, Igatpuri TPA-Aurangabad-RRC - Igatpuri 1 03/16/22

System. Regular Scrutiny cases. DC / CIT monitored cases. Search – Survey cases. Re-opened / re assessment cases.

TPA-Aurangabad-RRC - Igatpuri

3

04/19/23

Scrutiny Assessments

CASS Annual Information Returns filed by the specified persons (AIR) – Specified financial

transactions. Central Information Branch (CIB). TDS returns filed by the tax deductors. Online Tax Accounting System (OLTAS).

TPA-Aurangabad-RRC - Igatpuri

4

04/19/23

CASS

AIR filed by Specified Persons

Specified Financial Transactions Case deposits in savings account Credit card payments Investments in MF / Shares / Debentures /

Bonds etc. Purchase & sale of Immovable Property

TPA-Aurangabad-RRC - Igatpuri

5

04/19/23

CIB

Central Information Branch (CIB)

Registration of Vehicles Cash deposit at one time of Rs. 2,00,000 or

more High school fees Higher spending at hotels etc. Immigration details Stock exchange transactions Information from other government

departments. TPA-Aurangabad-RRC - Igatpuri

6

04/19/23

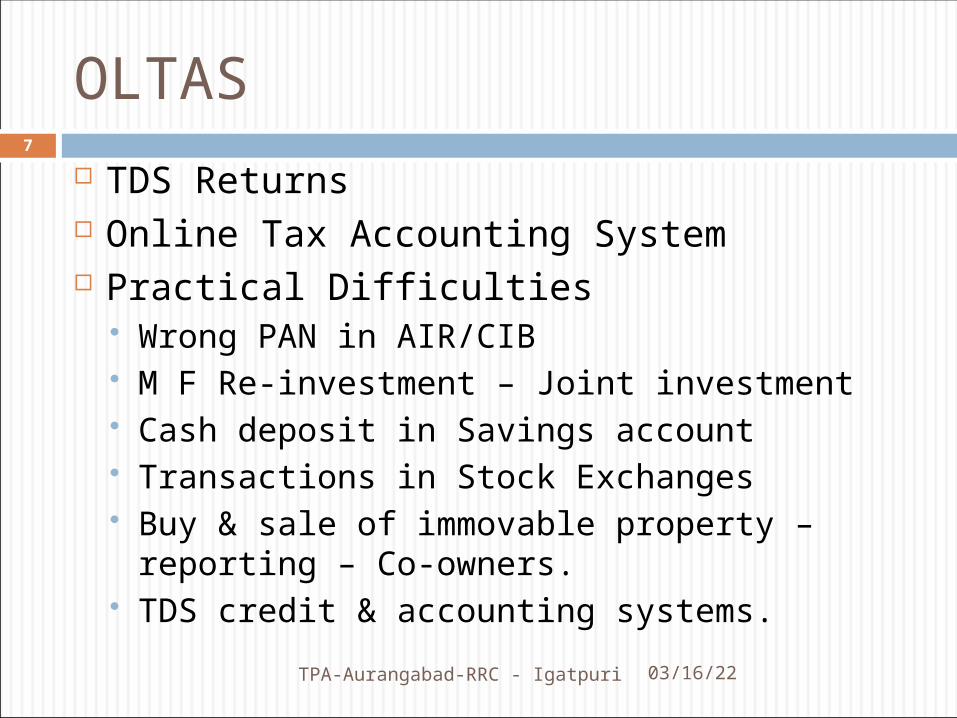

OLTAS

TDS Returns Online Tax Accounting System Practical Difficulties

Wrong PAN in AIR/CIB M F Re-investment – Joint investment Cash deposit in Savings account Transactions in Stock Exchanges Buy & sale of immovable property –

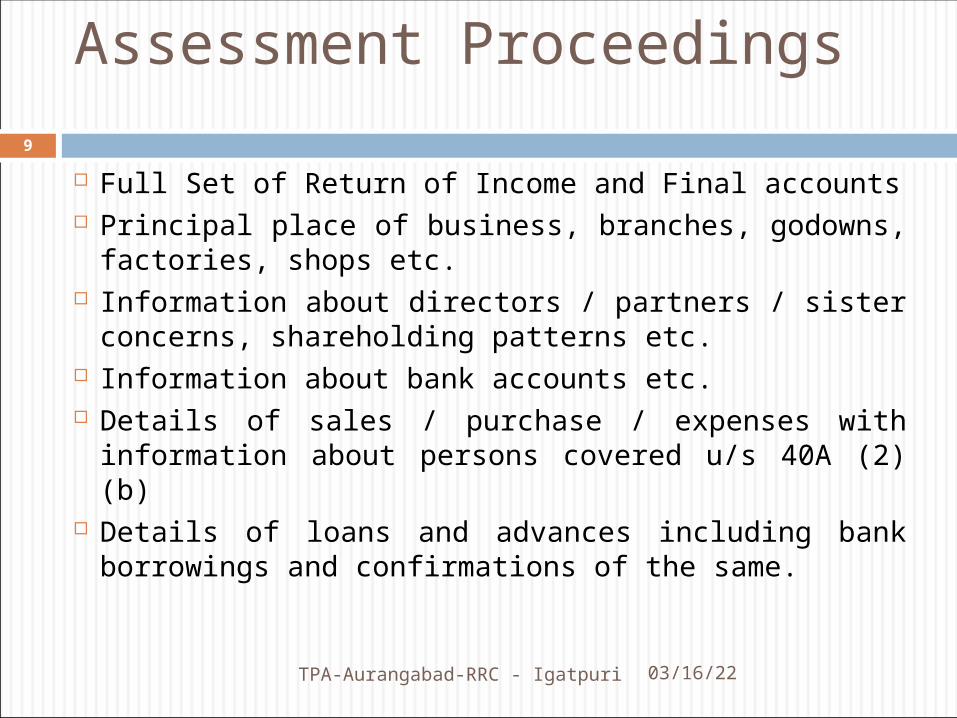

Full Set of Return of Income and Final accounts Principal place of business, branches, godowns,

factories, shops etc. Information about directors / partners / sister

concerns, shareholding patterns etc. Information about bank accounts etc. Details of sales / purchase / expenses with

information about persons covered u/s 40A (2)(b) Details of loans and advances including bank

borrowings and confirmations of the same.

TPA-Aurangabad-RRC - Igatpuri

9

04/19/23

Assessment Proceedings

Details about deductions / exemptions claimed. Details about investments made during the year. G P / N P comparison Information on book profit u/s 115JB etc. Information related to international transactions

and transfer pricing norms including domestic T P Regulations.

Details about past losses set offs/arrears/ refunds. Any other specific information as may be sought

by the A O.

TPA-Aurangabad-RRC - Igatpuri

10

04/19/23

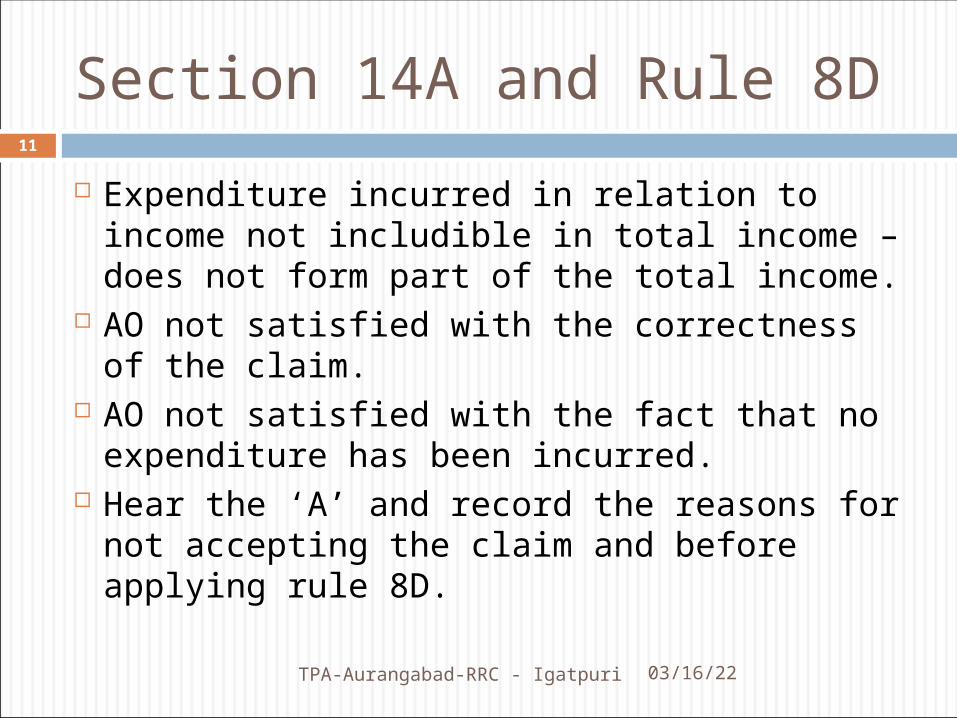

Section 14A and Rule 8D

Expenditure incurred in relation to income not includible in total income – does not form part of the total income.

AO not satisfied with the correctness of the claim.

AO not satisfied with the fact that no expenditure has been incurred.

Hear the ‘A’ and record the reasons for not accepting the claim and before applying rule 8D.

TPA-Aurangabad-RRC - Igatpuri

11

04/19/23

Issues under 14A

Expenditure with respect to dividend on shares held as stock in trade.

Disallowance be more than expenditure claimed.

Disallowance be made even if no exempt income.

Disallowance be more than exempt income.

04/19/23TPA-Aurangabad-RRC - Igatpuri

12

Section 2 (22) (e) of the Act. Advances or loan to

A shareholder, being beneficial owner of shareholding not less than 10% of voting power

Any concern in which such shareholder is a member or a partner having substantial interest

Any payment by such co on behalf or for the benefit of any such shareholder.

To be dividend if co has accumulated profits.

TPA-Aurangabad-RRC - Igatpuri

13

04/19/23

Section 2 (22) (e) of the Act.

Shareholder be registered shareholder or beneficial shareholder or both ???

Taxed in the hands of shareholder only or in the concern in which such shareholder has substantial interest ???

04/19/23TPA-Aurangabad-RRC - Igatpuri

14

Section 50 C of the Act.

Transfer of capital asset, being land or building or both,

Consideration is less than the stamp duty valuation,

Stamp duty valuation be deemed to be the consideration

Reference to the D V O Value as per DVO – more or less than

stamp duty valuation

TPA-Aurangabad-RRC - Igatpuri

15

04/19/23

Section 54 EC of the Act.

Capital gain from transfer of a long term capital asset

Investment of whole or part of capital gain in specified asset within six months of the date of transfer

Subject to maximum up to Rs. 50 lacs only. Qua long term asset or qua a financial year ? Rs. 50 lacs each in two financial year qua the

same long term capital asset ?

04/19/23TPA-Aurangabad-RRC - Igatpuri

16

Section 68 of the Act.

Any sum found credited in the books No explanation or explanation is not satisfactory. Sec 115BBE read with section 68

Application of Section 115 BBE is automatic ? In case of closely held company assessee Share application money, share capital, share

premium or any such amount by whatever name called – source of source to be explained

Venture capital fund or venture capital company will not be hit by this provisions.

TPA-Aurangabad-RRC - Igatpuri

17

04/19/23

Section 56 of the Act.

56 (2) (vii) any sum of money – any immovable property – any property other than immovable property – limit of Rs. 50,000.

Immovable property being land or building or both;

56 (2) (viia) firm or co receiving any security other than shares of a company.

56 (2) (viib) co receiving consideration for issue of shares in excess of its face value – and the aggregate consideration is in excess of the fair market value of the shares.

TPA-Aurangabad-RRC - Igatpuri

18

04/19/23

Hawala dealers

48(5) of MVAT Act Reject the claim of set off if purchasing dealer does

not pay VAT – Suspicious dealers – not bogus Cancel registration Identity is established Affidavit with VAT Department While registration Personally visited premises Dealer has signed in the presence of reg. authority Genuineness of the parties also satisfied Hertz & Waves Engineers P. Ltd. 45 TTJ 290 (Hyd.)

TPA-Aurangabad-RRC - Igatpuri

19

04/19/23

Hawala dealers

Whether party has filed MVAT Returns Bought under a tax invoice

- Name- Address-VAT Registration Number(TIN)-Details of goods sold, transportation if any etc.

-Amount of VAT etc. ITO v. Surana Traders, 93 TTJ 875 (Mum.)

TPA-Aurangabad-RRC - Igatpuri

20

04/19/23

Hawala dealers

Purchases recorded in books

Ledger copy/ Confirmation from party

Baishnab Charan Mohanty 212 ITR 199 (Orissa)

Stock register

Material Inward and Outward memos

ITO v. Surana Traders, 93 TTJ 875 (Mum.)

Job work

TPA-Aurangabad-RRC - Igatpuri

21

04/19/23

Hawala dealers

Payment by cheque Payment details like Party name , Cheque

Number, Date, Amount. Our bank Pass Book/ Statement Parties Bank Pass Book/ Statement

ITO v. Surana Traders, 93 TTJ 875 (Mum.)

Money flown back CIT v. M K Brothers (Guj) 30 Taxmann 547

TPA-Aurangabad-RRC - Igatpuri

22

04/19/23

Hawala dealers

Goods Sold

Copy of sales invoice

Date wise, Qty wise details – linkage of goods

sold from goods purchased

Details of subsequent payment received

Sale without purchase Balaji Textile Industries Pvt. Ltd. v. ITO, 49 ITD 177

TPA-Aurangabad-RRC - Igatpuri

23

04/19/23

Hawala dealers

A.O should allow cross verification

If not – can he proceed on presumption

without bringing material on record

CIT v. Grij Pal Sharma, 333 ITR 229 (P & H)

Counter Affidavit to testify our transactions

URD Purchase allowed – in past.

TPA-Aurangabad-RRC - Igatpuri

24

04/19/23

Hawala dealers

Books are audited

No adverse observation by auditors

A.O has not rejected the books

(1)- Trader (2)- Construction of Factory- Chartered

Architect (3)- Fabrication of Machine- Chartered

EngineerTPA-Aurangabad-RRC - Igatpuri

25

04/19/23

Section 44AD of the Act.

Turnover Rs 80,00,000/- F.Y 2012-13.

Rough accounts in vernacular language

Rough calculations – profit of Rs 16 Lacs

Should we offer Rs 16 Lacs or 6.4 Lacs for taxation ?

Provisions of Sec 44AD

TPA-Aurangabad-RRC - Igatpuri

26

04/19/23

Section 44 AD of the Act.

Sec 44AD (1)

Notwithstanding anything to the contrary contained in sections 28 to 43C, in the case of an eligible assessee engaged in an eligible business, a sum equal to eight per cent of the total turnover or gross receipts of the assessee in the previous year on account of such business or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the eligible assessee, shall be deemed to be the profits and gains of such business chargeable to tax under the head “Profits and gains of business or profession”.

Disclaimer: The contents of this presentation should not be construed an opinion. It provides general information existing at the time of preparation. It is recommended that professional advice be taken based on the specific facts and circumstances.