Assurance on XBRL Instance Documents: The Case of United Technologies Corporation University of Waterloo Efrim Boritz Won Gyun No UWCISA - 5th Symposium on Information Systems Assurance October 12, 2007

Transcript

Assurance on XBRL Instance Documents:

Assurance on XBRL Instance Documents:

The Case of United Technologies CorporationThe Case of United Technologies Corporation

University of Waterloo

Efrim BoritzWon Gyun No

UWCISA - 5th Symposium on Information Systems AssuranceOctober 12, 2007

IntroductionIntroduction

XBRL and Assurance

SEC’s Voluntary XBRL Filling

Reporting Framework for Electronic Filings

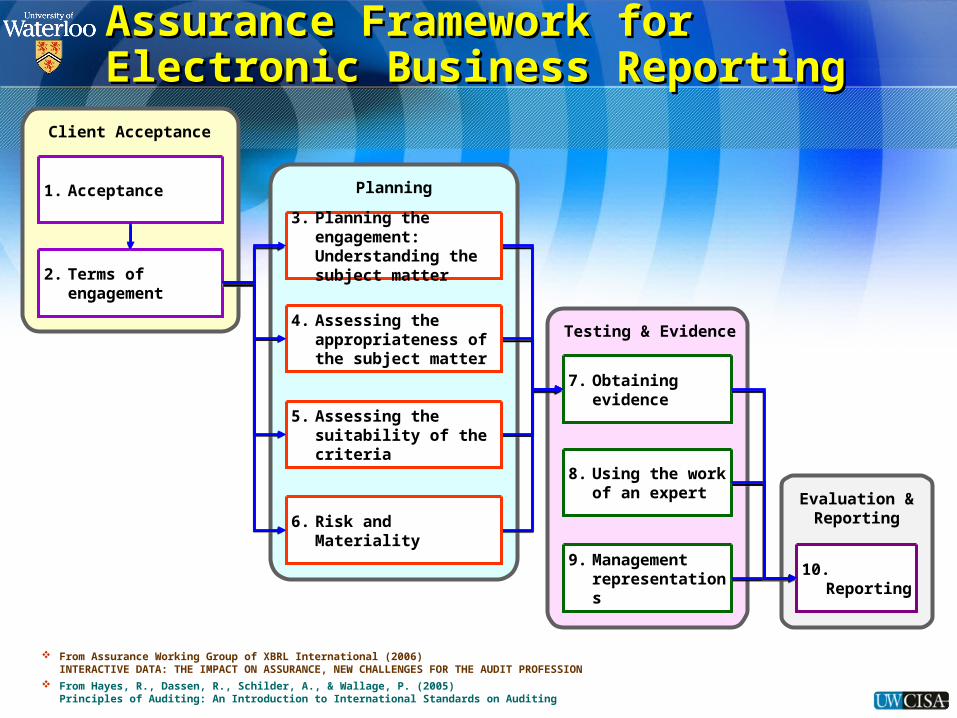

Assurance Framework for Electronic

Business Reporting

Findings

Recommendations

AgendaAgenda

Increased XBRL implementation for regulatory filings across the world.Increased XBRL implementation for regulatory filings across the world. U.S.: SEC U.S.: SEC XBRL voluntary program on EDGAR XBRL voluntary program on EDGAR and $5.5M to XBRL-US to develop and $5.5M to XBRL-US to develop

taxonomies.taxonomies.

U.K.: Plans to make XBRL mandatory for company tax filings from 2010.U.K.: Plans to make XBRL mandatory for company tax filings from 2010.

Canada: CSA XBRL voluntary filing program on January 19, 2007.Canada: CSA XBRL voluntary filing program on January 19, 2007.

Japan: Japan: TSE XBRL reporting system in 2006.TSE XBRL reporting system in 2006.

XBRL 3rd in FEI’s top 10 financial reporting challenges for 2007(Heffes, 2007).

Most companies currently providing their information using XBRL are doing so

without assurance.

Very limited guidance and experience on XBRL instance document

preparation

SEC’s voluntary XBRL filing program Some errors in SEC filings

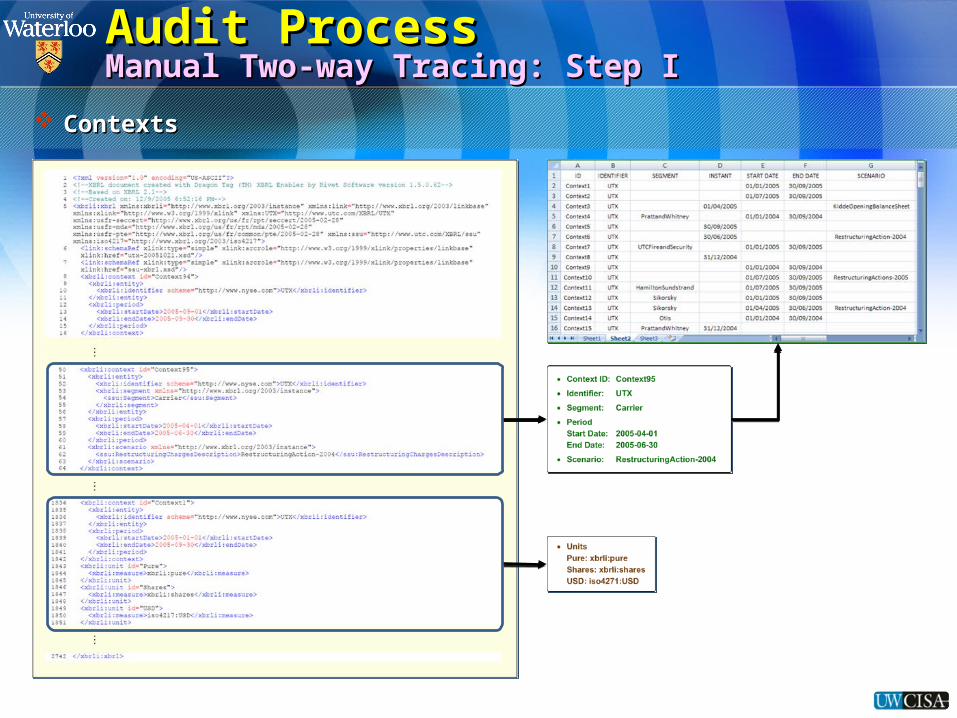

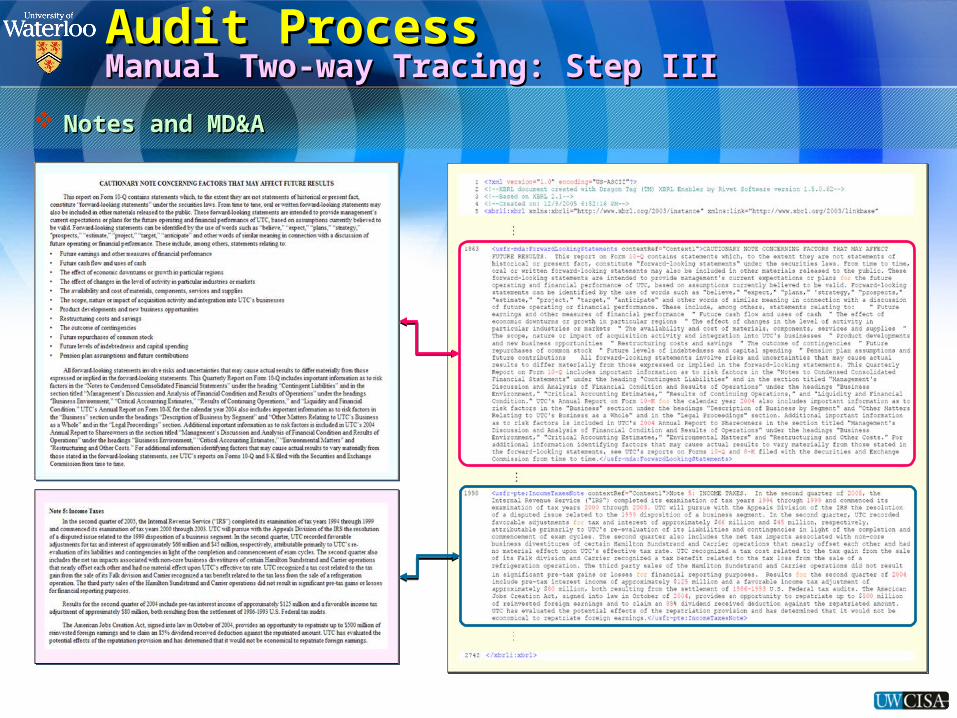

Case study of the EDGAR filing of United Technologies Corporation

Perform mock audit procedures

Interview preparers and auditors

Address a number of issues that an auditor might confront if/when provides assurance on

XBRL instance document

IntroductionIntroduction

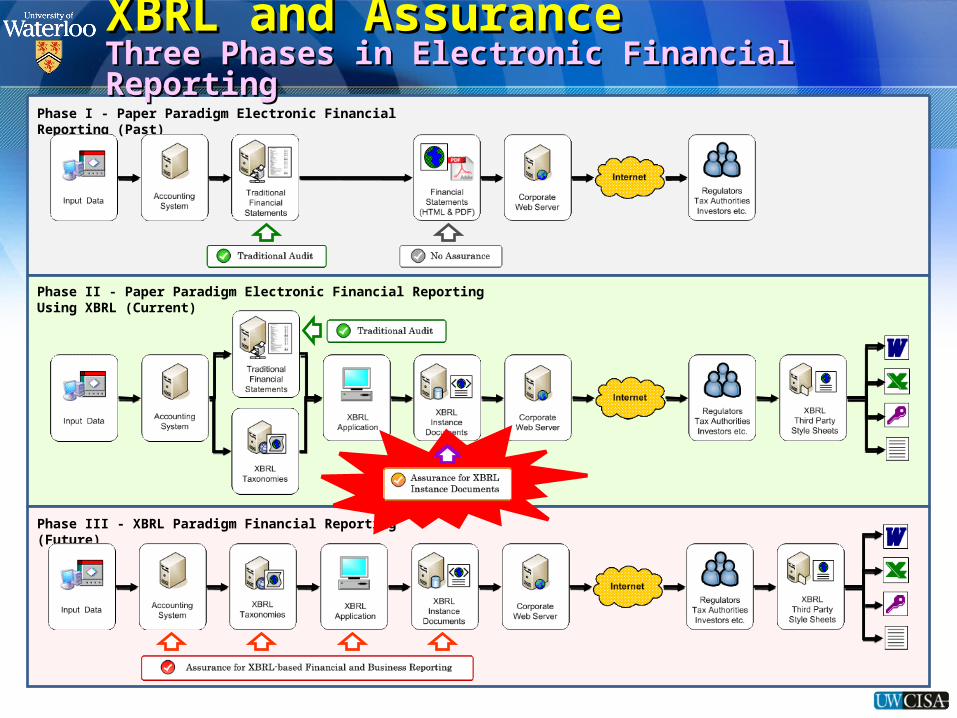

Phase I - Paper Paradigm Electronic Financial Reporting (Past)

Phase II - Paper Paradigm Electronic Financial Reporting Using XBRL (Current)

Phase III - XBRL Paradigm Financial Reporting (Future)

XBRL and AssuranceXBRL and AssuranceThree Phases in Electronic Financial ReportingThree Phases in Electronic Financial Reporting

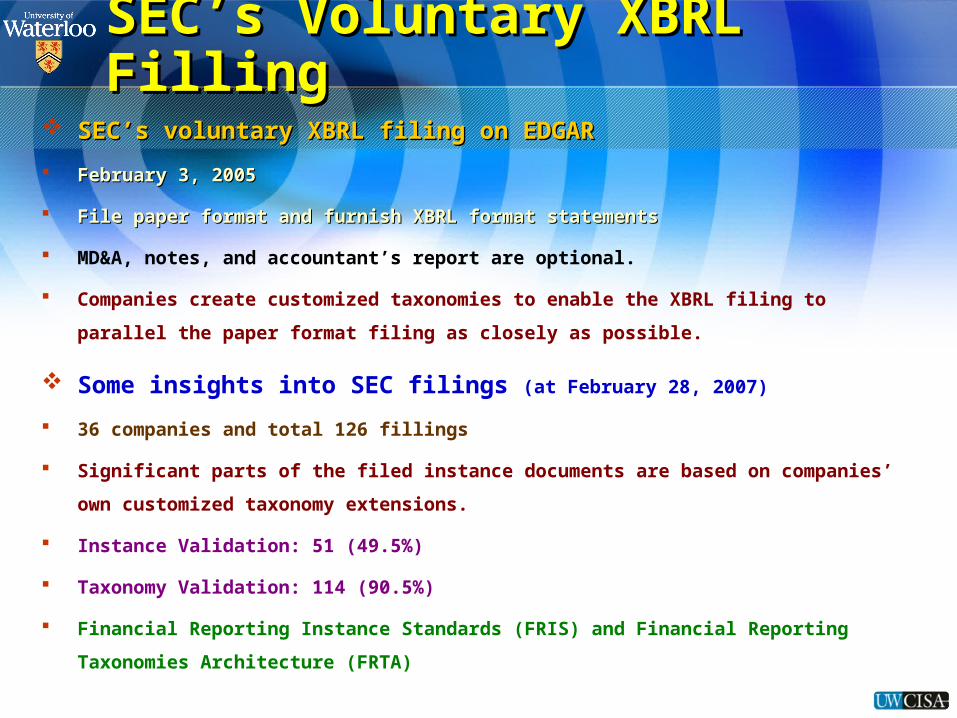

SEC’s voluntary XBRL filing on EDGARSEC’s voluntary XBRL filing on EDGAR

February 3, 2005February 3, 2005

File paper format and furnish XBRL format statementsFile paper format and furnish XBRL format statements

MD&A, notes, and accountant’s report are optional.

Companies create customized taxonomies to enable the XBRL filing to

parallel the paper format filing as closely as possible.

Some insights into SEC filings (at February 28, 2007)

36 companies and total 126 fillings

Significant parts of the filed instance documents are based on companies’

own customized taxonomy extensions.

Instance Validation: 51 (49.5%)

Taxonomy Validation: 114 (90.5%)

Financial Reporting Instance Standards (FRIS) and Financial Reporting

Took an XBRL expert about Took an XBRL expert about 63 hours 63 hours to complete (not to complete (not

counting other steps that would be required)counting other steps that would be required)

Had high assurance high assurance that the instance document was a

complete and accurate reflection of UTX’s 10-Q paper format

filing

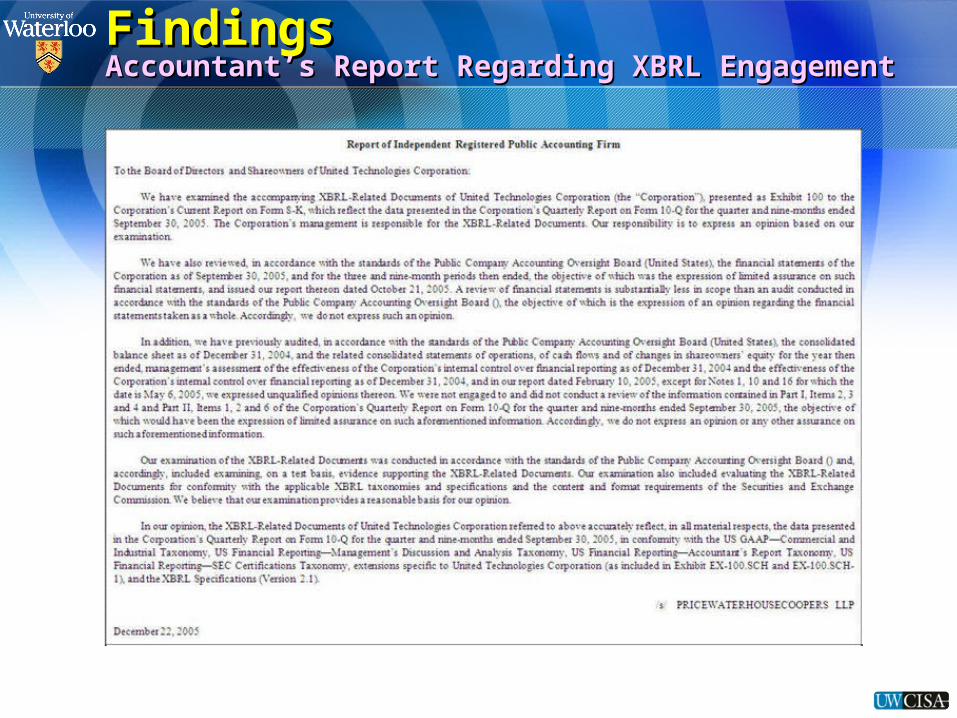

Cannot form a conclusion on the fairness ...in accordance

with GAAP of the instance document

No assurance standards or guidelines for making such an

assessment

Limited knowledge for evaluating the MD&A, regulatory

information, and the appropriateness of the company’s own

extensions to the XBRL taxonomies

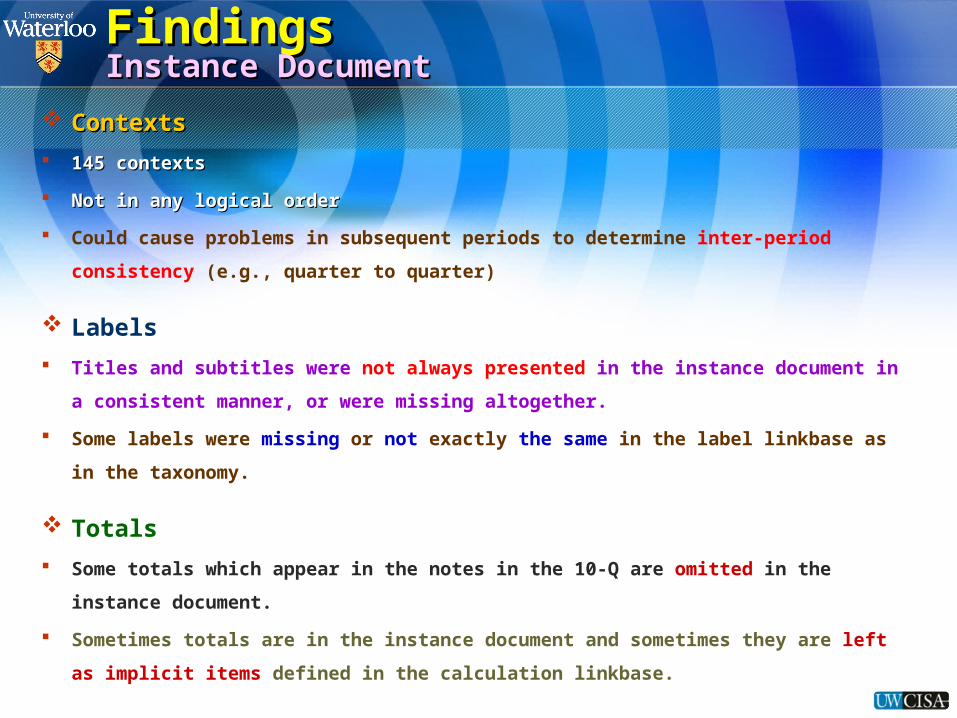

FindingsFindingsSummarySummary

Auditors’ effort, time, and cost could be reduced.Auditors’ effort, time, and cost could be reduced.

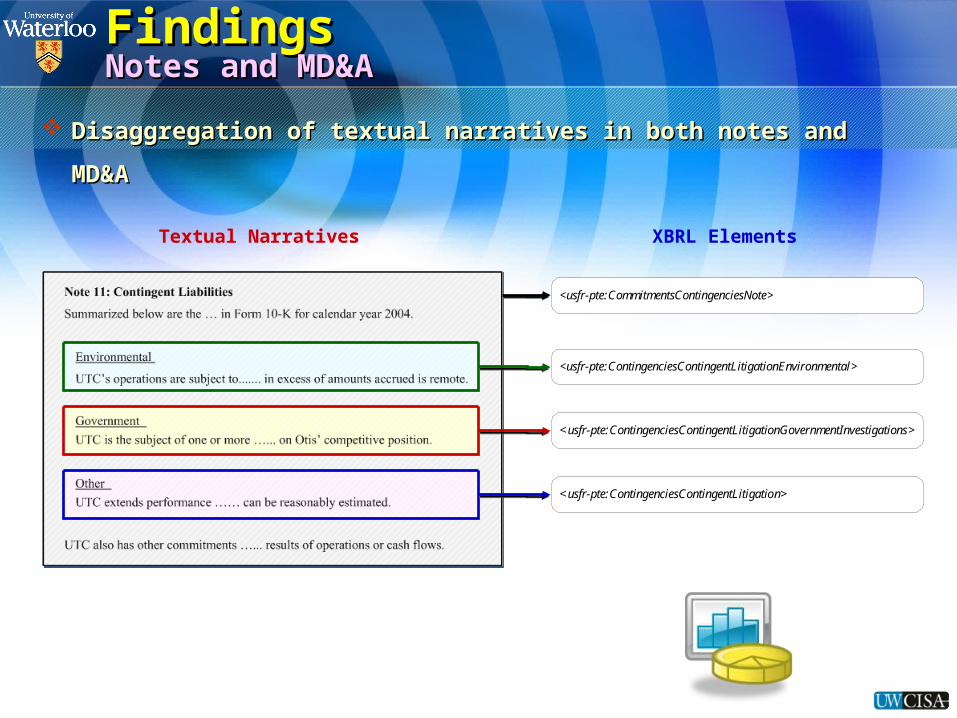

A deliberate A deliberate structuringstructuring of an XBRL instance document of an XBRL instance document

A A logical ordering logical ordering of elements in the XBRL instance document (e.g., by financial of elements in the XBRL instance document (e.g., by financial

statement, notes, and MD&A)statement, notes, and MD&A)

An embedded description of the structure

Explanation of why custom taxonomies are required or are preferred to approved

taxonomies.

Create rules for naming attributes (Sgt_Ottis_2004 vs. Context11)

Organize contexts systematically and document rules used to create them

Need Computer-Assisted Audit Techniques

Assurance on XBRL instance documents.

Some form of comfort/assurance will be necessary.

Need guidance for both preparers and auditors

If an external report is provided, then it should be provided as an XBRL instance

document to utilize the advantage of XBRL

Need a taxonomy for an auditor's assurance report on XBRL instance