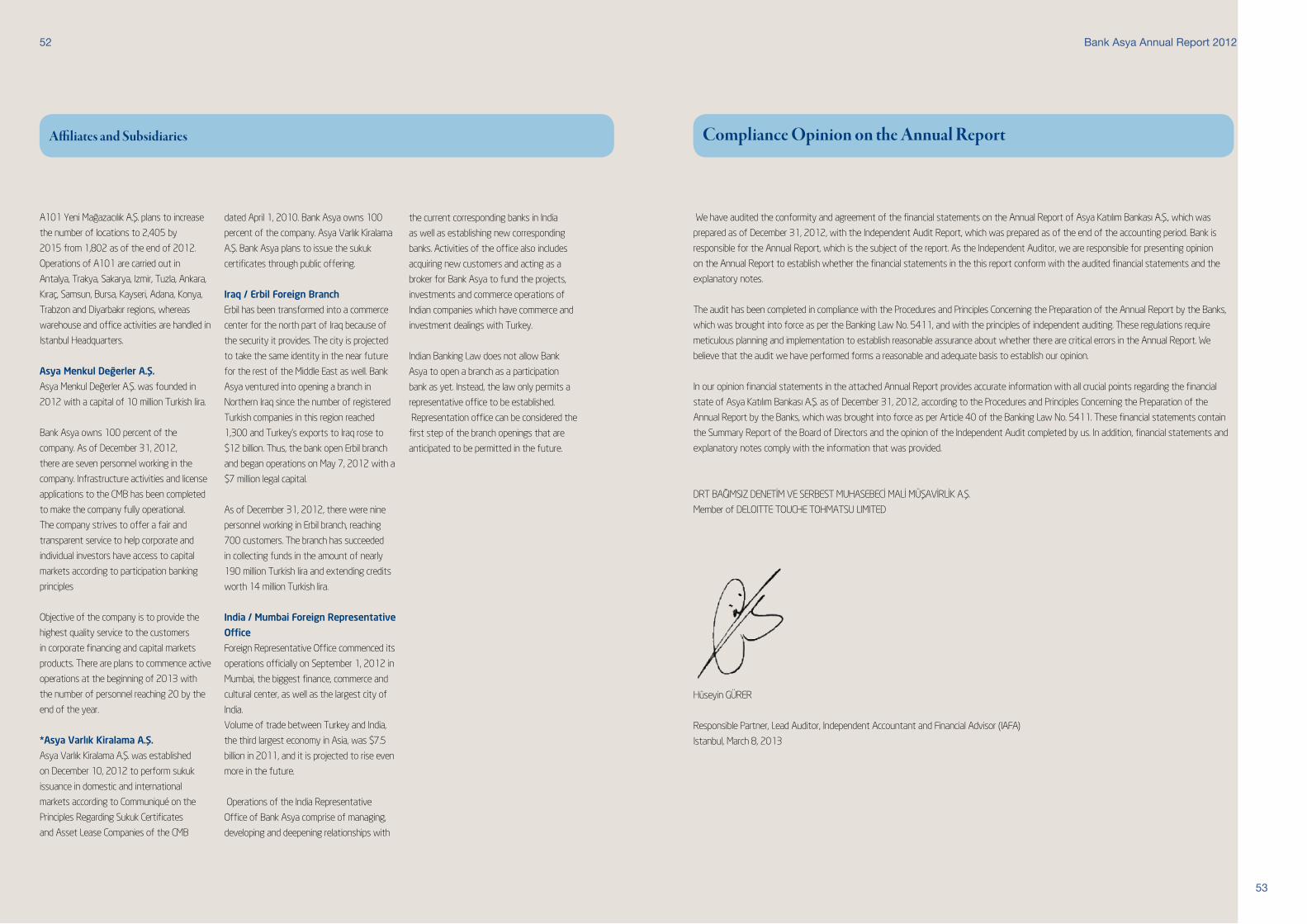

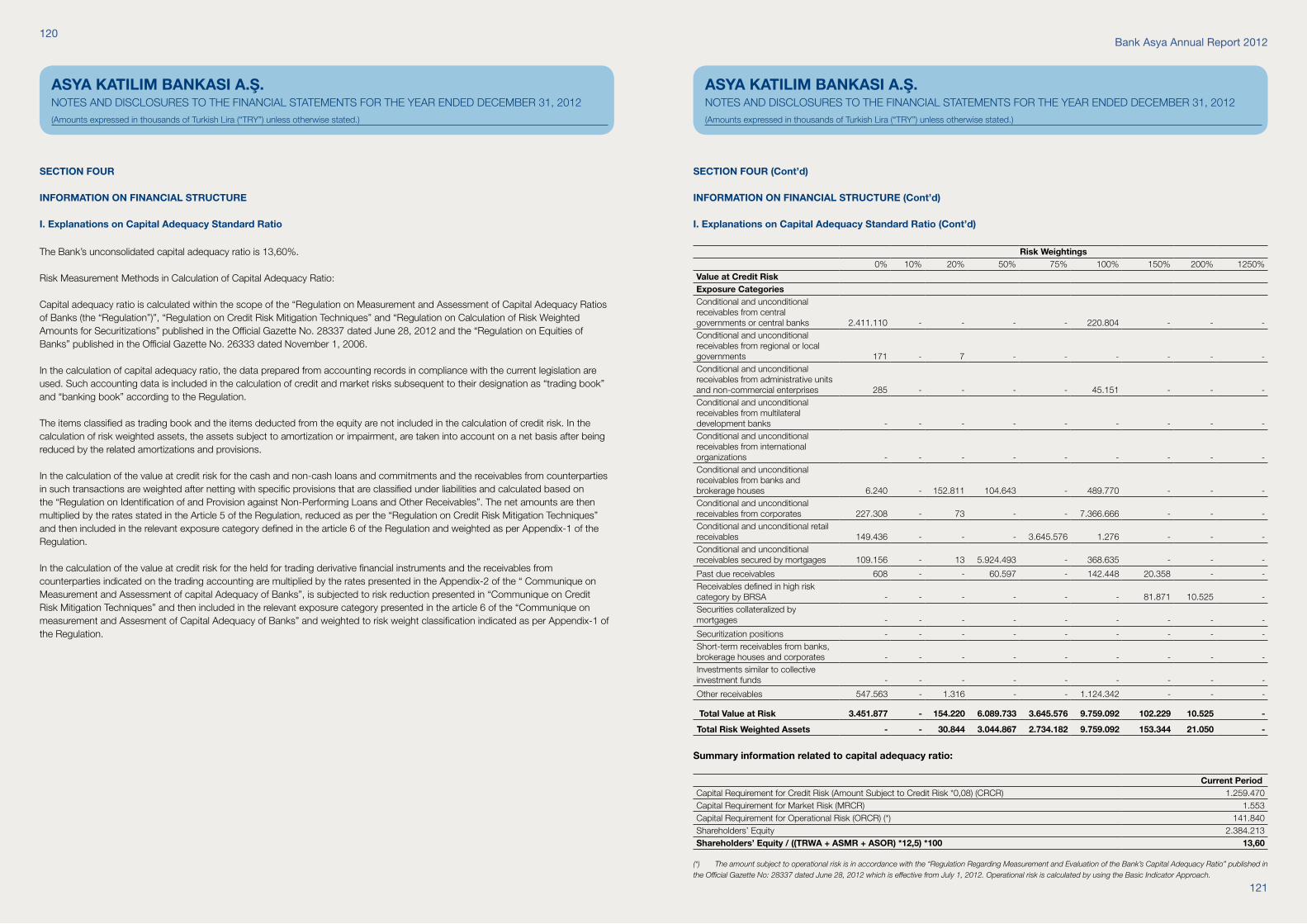

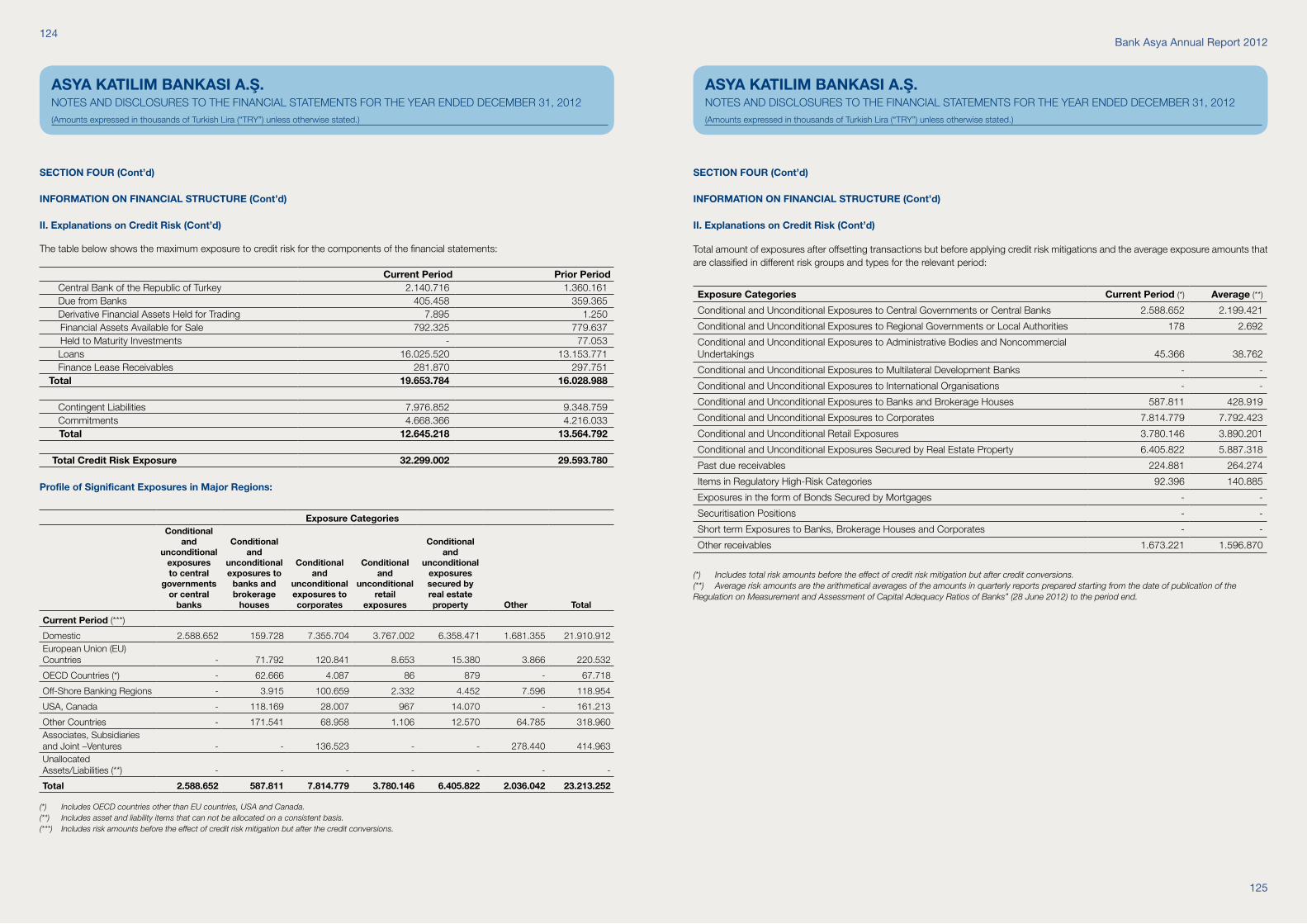

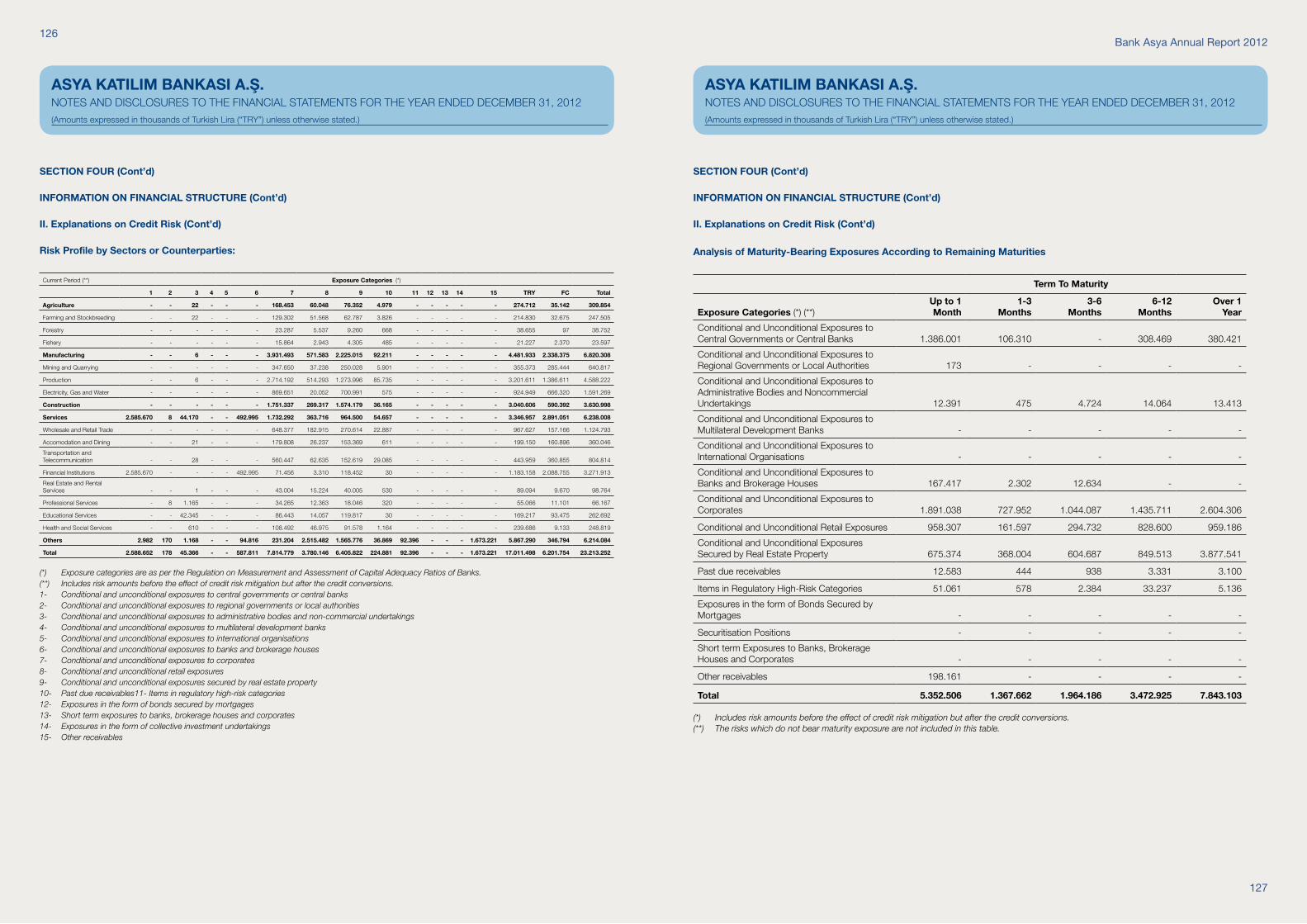

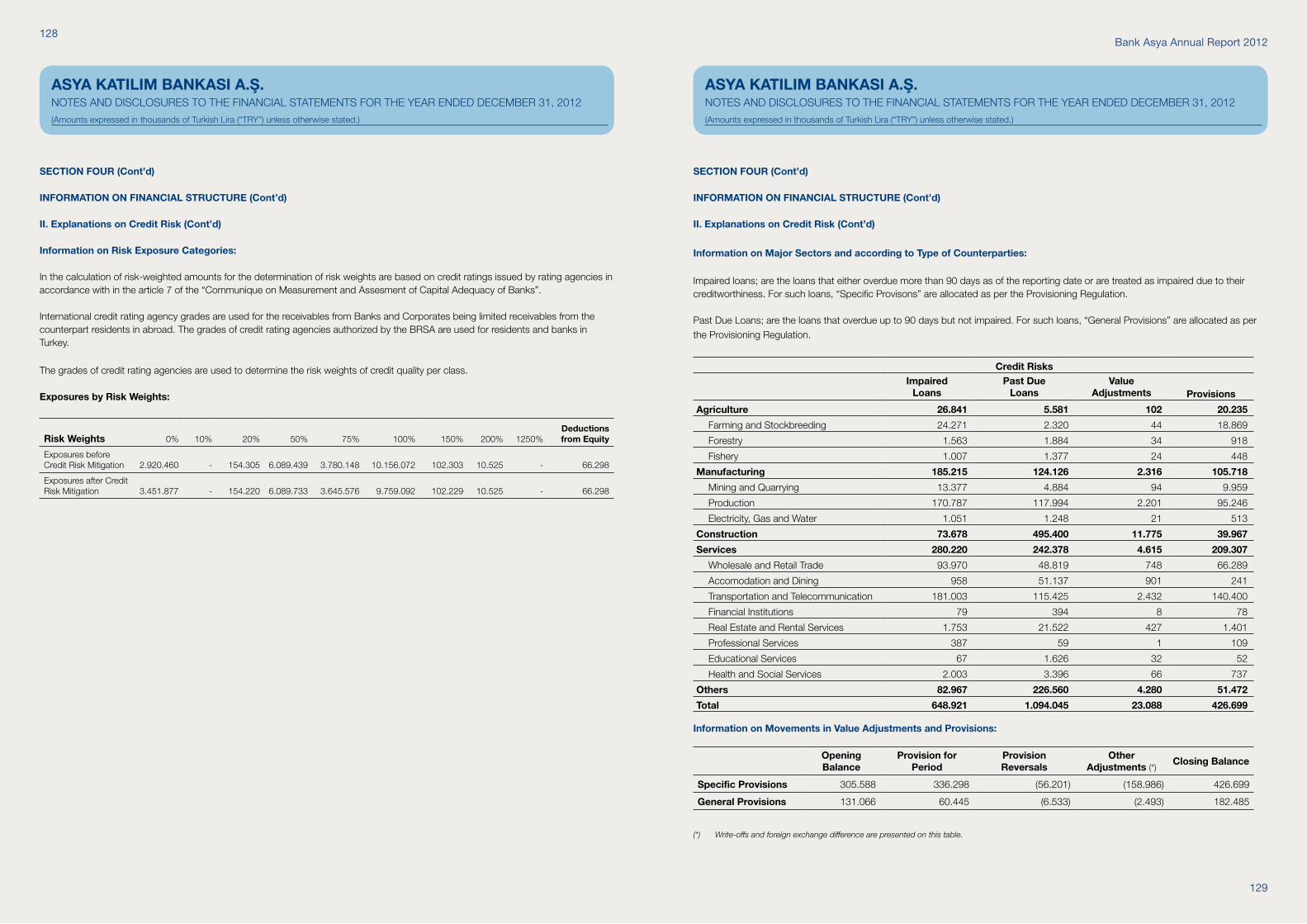

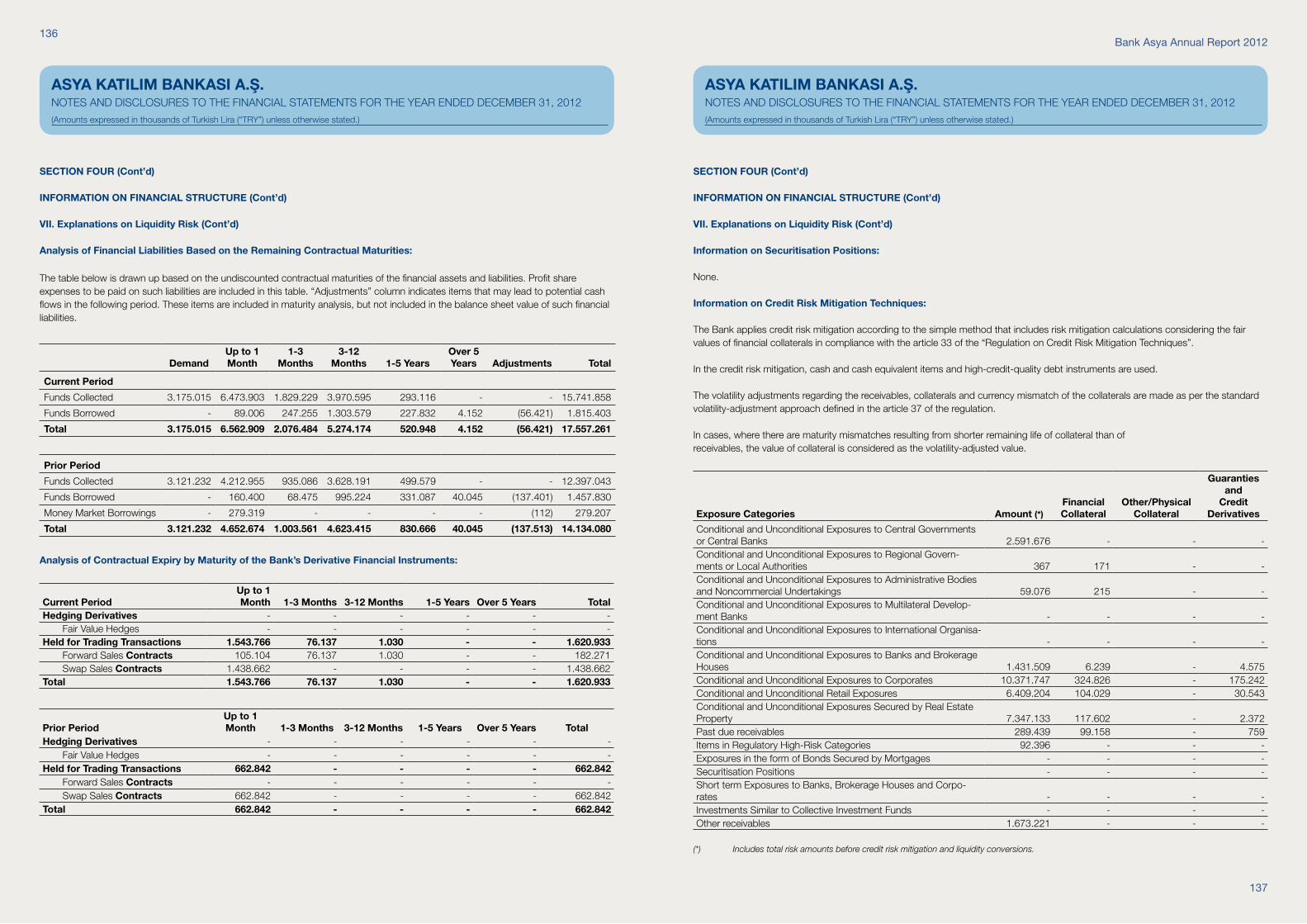

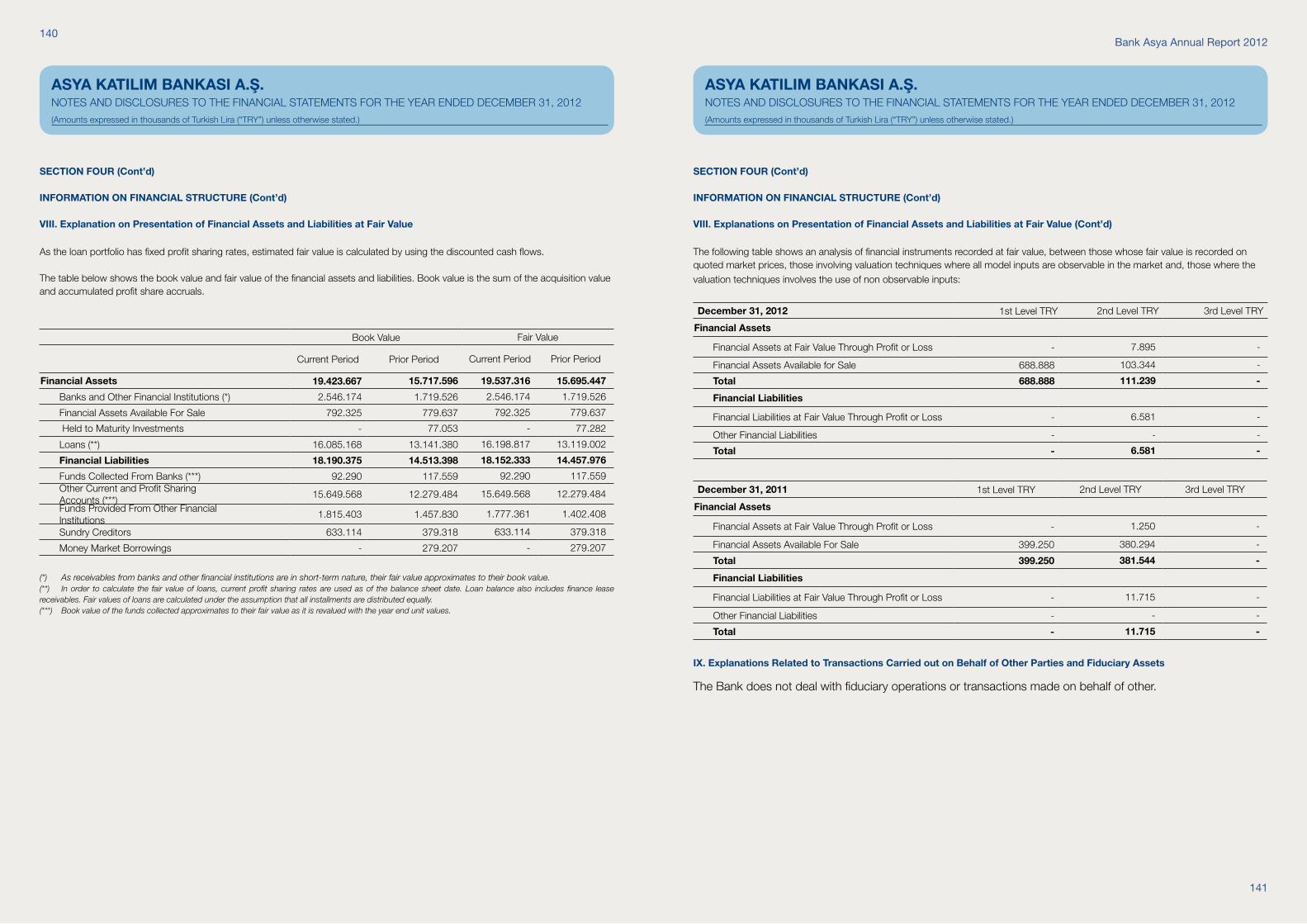

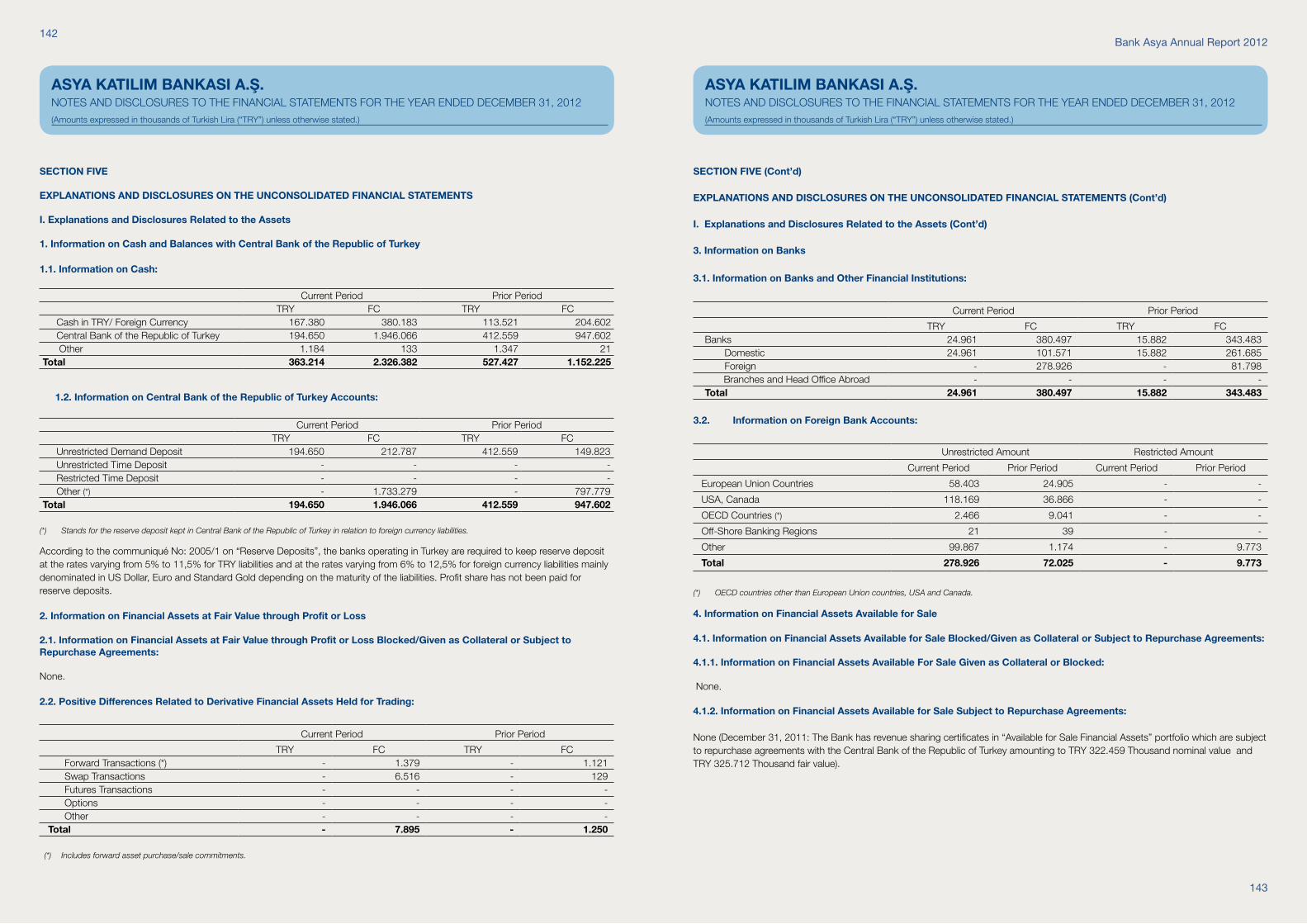

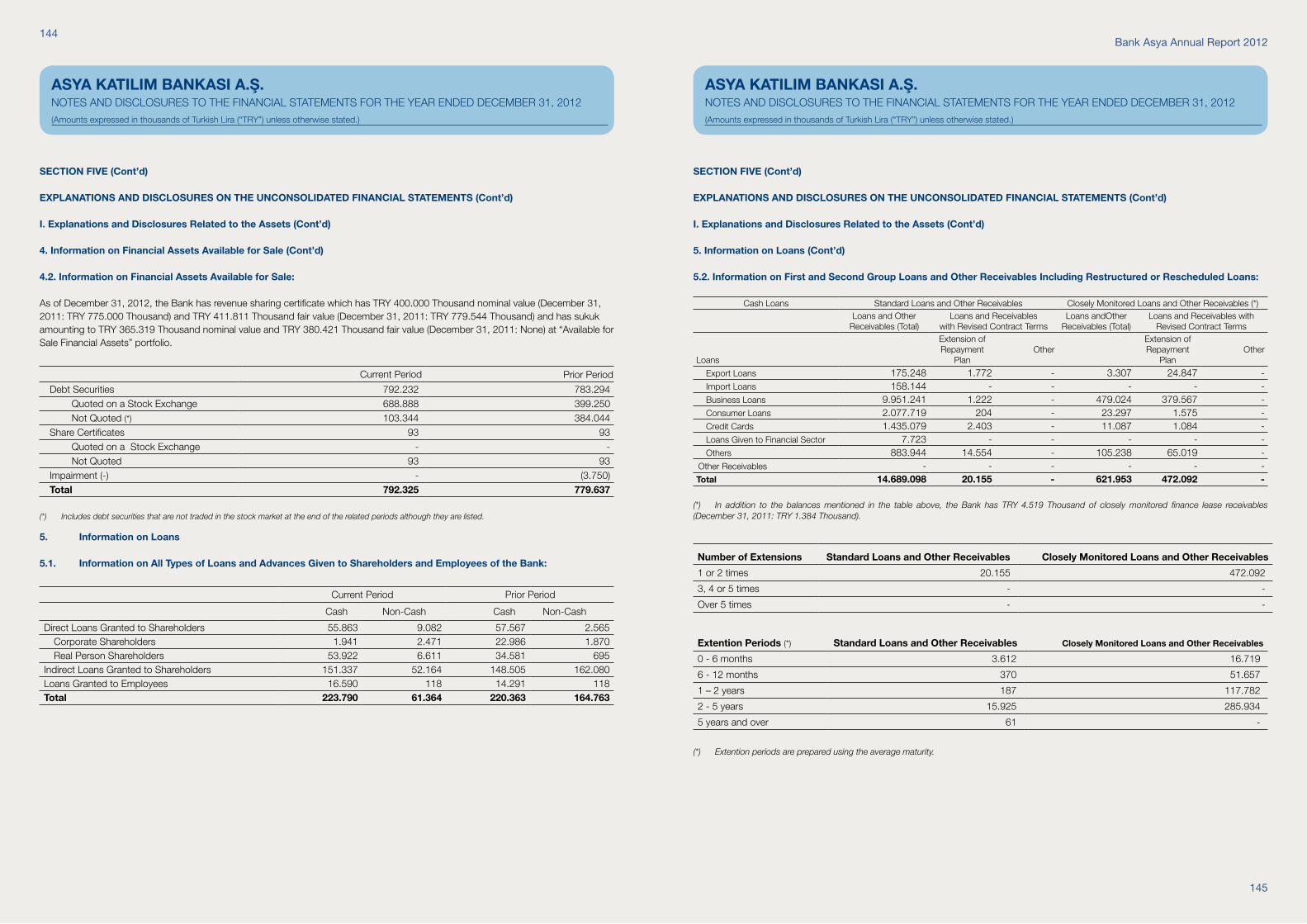

95

Annual Report 2012 ASYA KATILIM BANKASI A.Ş.

Annual Report 2012ASYA KATILIM BANKASI A.Ş.

01

Section 1/Presentation

Section 2/Management Information and Corporate Governance Principles

Section 3/Financials and Assessments Regarding Risk Management

02 Bank Asya in Brief 05 Vision, Mission, Strategic Objectives 06 Main Indicators 08 Position of Bank Asya in the Industry 010 Comparison of Bank Asya with the Other Participation Banks 014 Growth Strategy of Bank Asya 016Milestones for Bank Asya 018 Capital and Partnership Structure of Bank Asya, and Changes that have taken place during the Operating Cycle 022 Message from the Chairman of the Board of Directors 024 Message from the Chief Executive Officer 030 Macroeconomic Outlook and the Banking Industry 034 Development of the Banking Industry 036 2012 Operating Activities of Bank Asya 048 Corporate Social responsibility Projects 049 Affiliates and and Subsidiaries 053 Conformity Opinion for the Annual Activity Report

056 Board of Directors 058 Audit Committee 060 Executive Management 062 Organization Chart 064 Committees 069Summary Report of the Board of Directors 070 Human Resources (HR) 072 Education 073 Business Volume of the Risk Group the Bank Belongs to, Unresolved Credits and Funds Collected at the end of the Operating Cycle, Operating Income and Expenses 074 Corporate Governance Principles Compliance Report 080 Activities with Support Services 081 Dividend Policy 081 Dividend Proposal for 2012 082 Matters Regarding the General Assembly 084 Briefing Regarding the Agenda

088 Summary Audit Report 089 Financials for the Operating Cycle Including the Reporting Period 090 Assessment of the Financial Standing, Profitability and Solvency 091 Assessment from the Audit Committee Regarding the Operation of Internal Systems 092 Information on Risk Management Policies that are Applied According to Risk Types 094 International Rating Scores

Section 4/Unconsolidated Financial Statements and Footnotes Regarding Financial Statements097 Independent Audit Report

Section 5/Contact Information

190 Bank Asya Branches

02

03

Bank Asya Annual Report 2012

Bank Asya is the youngest and fastest growing participation bank in Turkey. It was established as the sixth private

financing institution in Turkey with the name Asya Finance. Bank Asya has earned an influential, solid and highly regarded position in the banking industry in a short span of time with its dynamic and innovative organization.

Turkey’s first participation bank to go public. Bank Asya implements strategies with determination and places high emphasis on corporate structuring. Bank Asya was formed as the first participation bank with aspirations to establish a sound and extensive capital base.

The bank has embraced a sustainable corporate governance concept. Bank Asya was listed on the Istanbul Stock Exchange (ISE) in 2006 with an initial free float rate of 23 percent. The bank extended its capital base even more by increasing this rate to 53.36 percent in 2012. Paid capital of the bank was 900 million Turkish lira as of the end of 2012.

Groundbreaking products and services in participation banking. Bank Asya continuously and expeditiously develops new range of products and services in all facets of banking so as to fulfill varying customer demands and expectations. It is the first participation bank to have earned the ISO 9001 - Quality System Management Certificate. Bank Asya incessantly pioneers new interest free participation banking products. The bank also toils to ensure that all of its banking products and services are efficaciously attuned to the participation banking system. Accordingly, Bank Asya continues to strengthen its progressive position in the market.

The biggest investment is the one that is made in people. Bank Asya is aware of the fact that a qualified workforce is the main consideration when investing in the future. Bank Asya is the home to young and dynamic employees who welcome development and who are well adjusted to their corporate identity. Thus, the bank entertains high hopes for the future and consistently achieves a growing trend with the strength it gets from its workforce.

Participation bank that sets precedents in technology. What distinguishes Bank Asya from the rest of the participation banks is its valuable workforce and cutting edge technological infrastructure. Investments in technological infrastructure and alternative delivery channels allow Bank Asya to offer improved products and services in 250 branches throughout Turkey and one branch abroad as well as in other delivery channels. The bank especially stands out with the leading-edge payment system products offered for the customers. The best examples of these products are AsyaCard DIT, the most advanced non-touch credit card in Europe, and AsyaPratic DIT, the first prepaid non-touch bank card in Turkey. The bank has remained as a leader in the industry with DIT Mobile and Mobile Wallet KGS products which allow non-touch transactions through mobile telephones.

Introducing more sustainable values. Bank Asya performs banking activities with the responsibility of a true corporate citizen. The bank establishes its strategic objectives in this in direction with the principle of introduction more sustainable values for the stakeholders in its operations as well as in social responsibility projects.

A brand value that rises as a result of unmatched growth dynamics. Bank Asya was founded to provide support for the non-financial sector and for production. As such, it promotes a business model according to the main principles of interest free banking. The bank has transformed this business model into a sound and successful participation banking example through funding, risk and quality policies that is applies by utilizing administrative competence as well as through the ingenuity and unparalleled growth dynamics it displays. Bank Asya is determined to enhance its brand value that it has earned in the domestic and international markets due to a groundbreaking business model which welcomes development. Bank Asya succeeded in maintaining profitability and growth in 2012 according to its projections, thanks to its sound capital structure, extensive customer base and robust finances. The bank continued to protect the leadership position in 2012 with its asset size and collected funds, in addition to cash and non-cash credits it has granted.

Bank Asya aims to spread to a wide community the advantages of the interest free banking system and practices

while performing its duties to support the non-financial sector and production. Bank Asya meets customer demands through innovative retail banking products and services as

well as providing support through solution oriented corporate products and services for the growth of businesses, which help

Turkey prosper. Bank Asya affirms sustainable growth as a trustworthy,

respected and strong participation bank with international banking standards it provides through customer satisfaction

focused banking approach, value of its personnel and technology investments as well as through long-term finance

and non-financial sector investments at home and abroad.

Bank Asya in Brief

Bank Asya carries out its operations

with a focus on strategic targets to ensure sustainable

profitability and to create added value for all of its stakeholders.

05

04 Bank Asya Annual Report 2012

Vision

To be a respected, trustworthy and influential bank that provides services in global standards with the

products it develops.

Mission

To make a contribution to stakeholders as well as to Turkish economy by fulfilling customer demands

and expectations with “Different demands, different solutions” approach and by improving banking

services according to interest free banking principles.

Strategic Objectives

• To emerge as one of the leading participation banks in the world,

• To continue being the participation bank with the highest brand value in Turkey,

• To be in the front lines among the companies that qualified people would want to work in,

• To improve its market share in the industry,

• To spearhead the industry with the innovations it introduces,

• To establish itself as the customer’s first bank,

• To maintain its support to social responsibility projects like community activities or sports events,Visio

n, M

issio

n an

d St

rate

gic

07

06

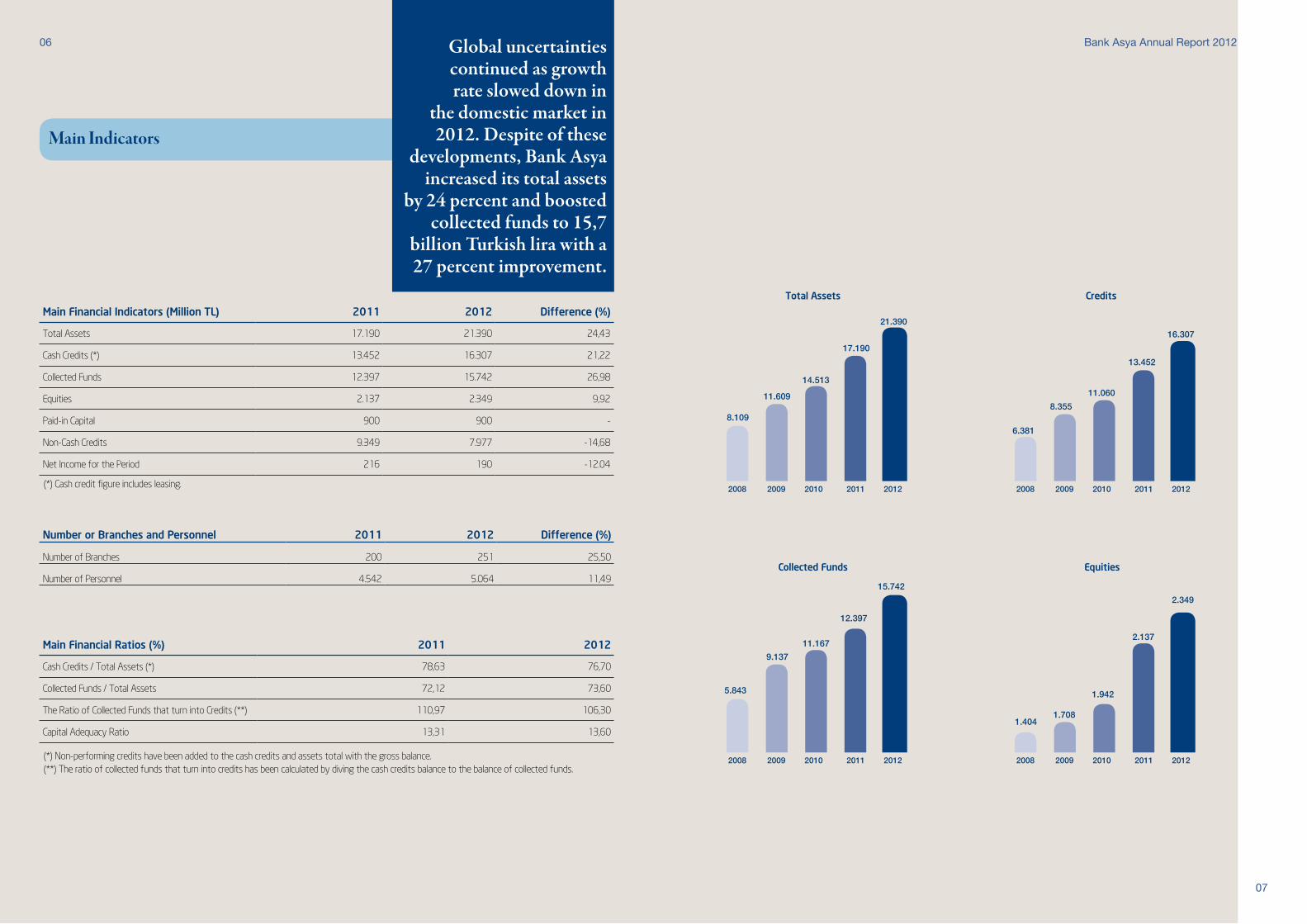

Main Indicators

Global uncertainties continued as growth rate slowed down in

the domestic market in 2012. Despite of these

developments, Bank Asya increased its total assets

by 24 percent and boosted collected funds to 15,7

billion Turkish lira with a 27 percent improvement.

Main Financial Ratios (%) 2011 2012

Cash Credits / Total Assets (*) 78,63 76,70

Collected Funds / Total Assets 72,12 73,60

The Ratio of Collected Funds that turn into Credits (**) 110,97 106,30

Capital Adequacy Ratio 13,31 13,60

Main Financial Indicators (Million TL) 2011 2012 Difference (%)

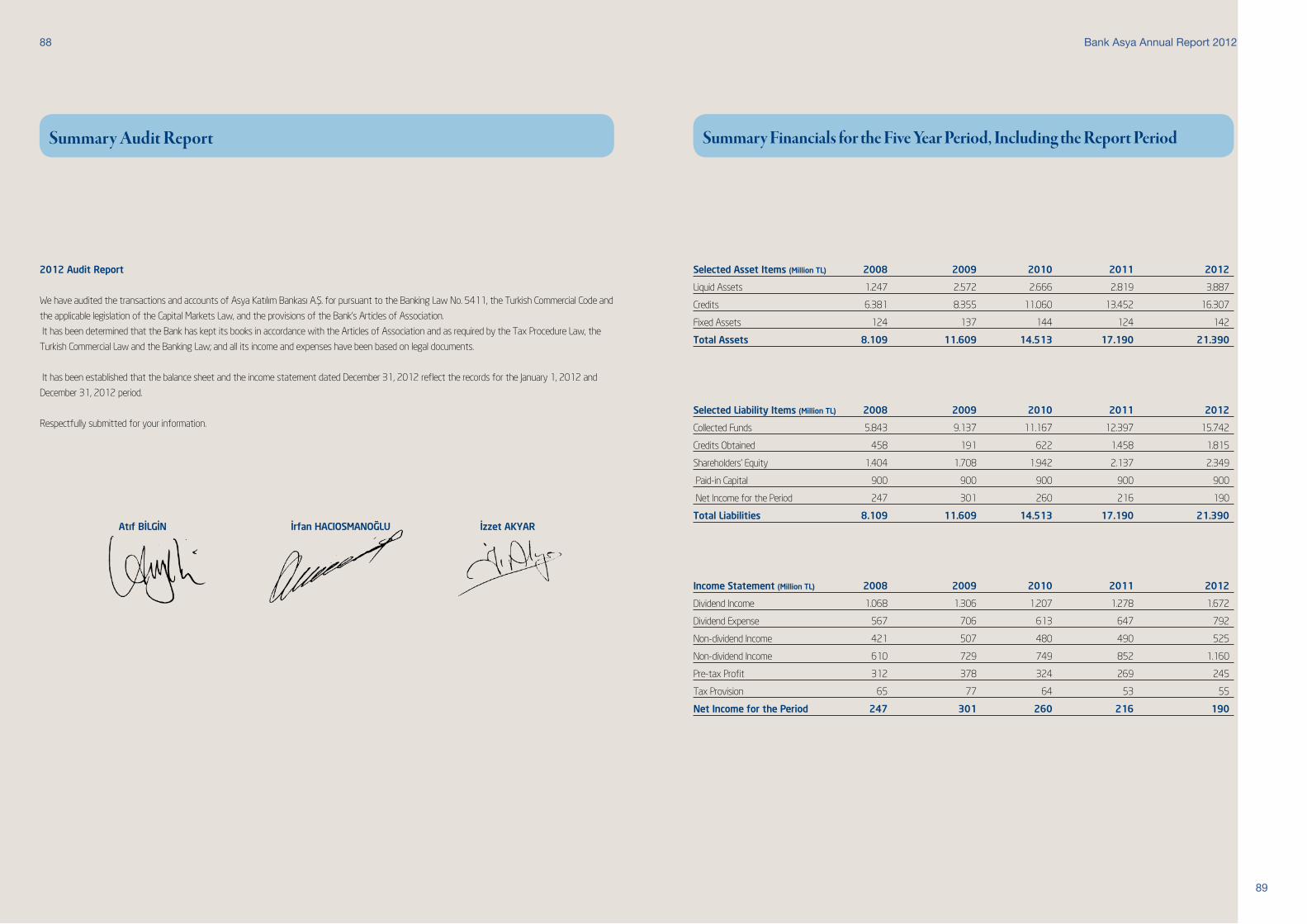

Total Assets 17.190 21.390 24,43

Cash Credits (*) 13.452 16.307 21,22

Collected Funds 12.397 15.742 26,98

Equities 2.137 2.349 9,92

Paid-in Capital 900 900 -

Non-Cash Credits 9.349 7.977 -14,68

Net Income for the Period 216 190 -12.04

Number or Branches and Personnel 2011 2012 Difference (%)

Number of Branches 200 251 25,50

Number of Personnel 4.542 5.064 11,49

(*) Cash credit figure includes leasing.

(*) Non-performing credits have been added to the cash credits and assets total with the gross balance.(**) The ratio of collected funds that turn into credits has been calculated by diving the cash credits balance to the balance of collected funds.

Bank Asya Annual Report 2012

8.109

Total Assets

20092008 2010 2011 2012

11.609

14.513

17.190

21.390

Collected Funds

20092008 2010 2011 2012

5.843

9.137

11.167

12.397

15.742

Credits

20092008 2010 2011 2012

6.381

8.355

11.060

13.452

16.307

Equities

20092008 2010 2011 2012

1.4041.708

1.942

2.137

2.349

09

Bank Asya Annual Report 2012

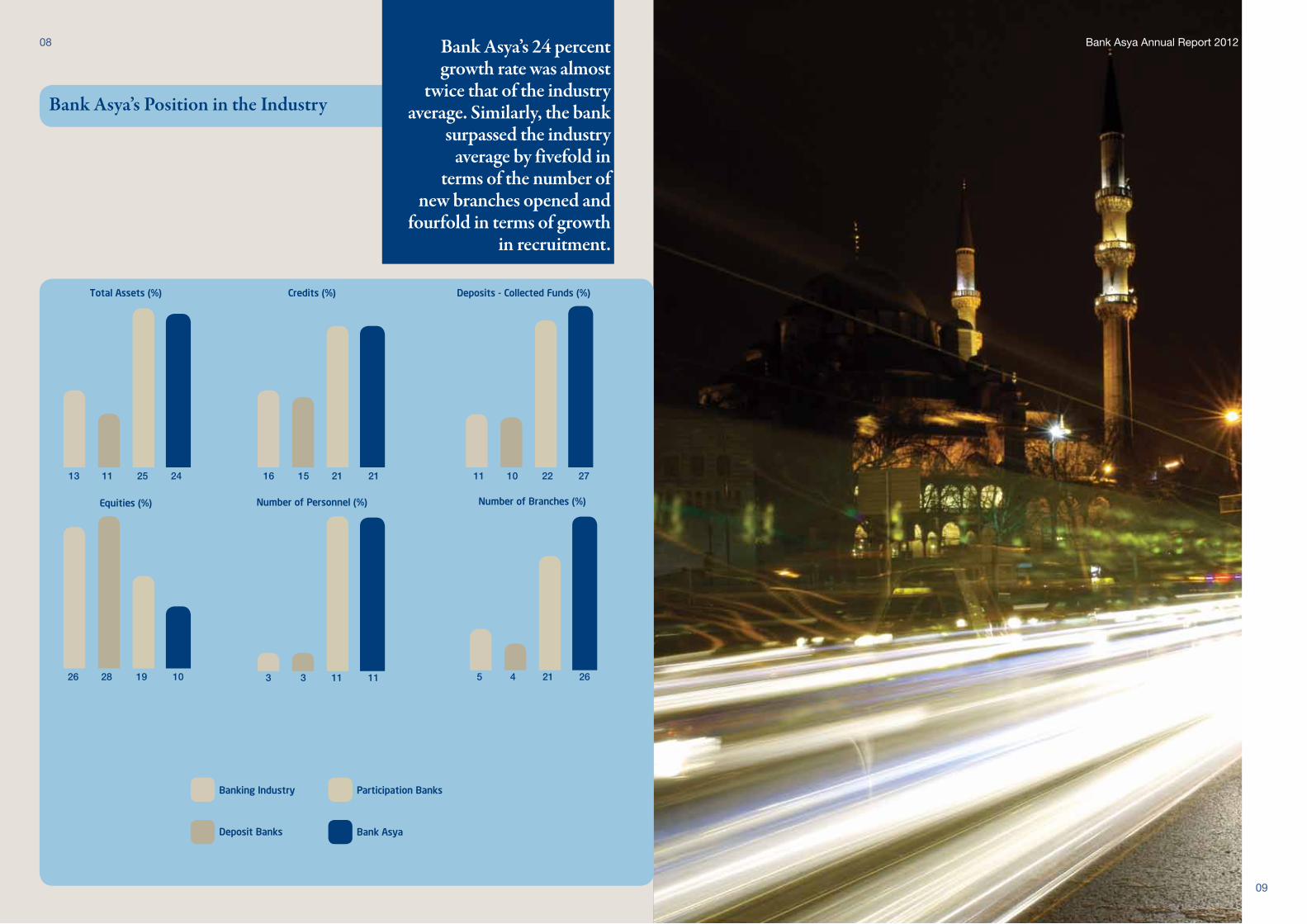

Bank Asya’s Position in the Industry

Credits (%)

Banking Industry

Deposit Banks

Participation Banks

Bank Asya

Total Assets (%)

13 11 25 24 16 15 21 21

Deposits - Collected Funds (%)

11 10 22 27

Number of Personnel (%)

3 3 11 11

Equities (%)

26 28 19 10

Number of Branches (%)

5 4 21 26

08 Bank Asya’s 24 percent growth rate was almost

twice that of the industry average. Similarly, the bank

surpassed the industry average by fivefold in

terms of the number of new branches opened and

fourfold in terms of growth in recruitment.

11

Bank Asya Annual Report 201210

Comparison of Bank Asya with other Participation Banks

70

Total Assets (%)

30

68

Equities (%)

32

67

Number of Personnel (%)

33

67

Collected Funds (%)

33

79

Net Profit and Loss for

the Period (%)

21

70

Number of Branches (%)

30

Bank Asya distinguished itself as the participation

bank recording the highest fund increase with a 27

percent improvement on collected funds in 2012.

The bank performed single-handedly in the industry;

30 percent of the asset totals, 33 percent of the

funds and 32 percent of the credits.

68

Credits (%)

32AWARDSBank Asya crowned the outstanding success of the 2012 operating

cycle with numerous awards and certifications received throughout

the year.

• Bank Asya took the third place in Emea’s “Top Ranking Performers

in the Contact Center World“ organization.

• Bank Asya’s call center was awarded the first place in the “Call

Centers are Competing” category of the Call Center Awards 2012

organization.

• Bank Asya Mobile Branch was elected as the best website in the

Middle East and Africa.

• ŞikayetEndex listed Bank Asya as the fourth most successful bank

according to the complaints and satisfactions points which were

sent by 650,000 “I have a complaint” members.

• Bank Asya took the “Pega Financial Services Customer Experience

Award” with its “CRM Project in 180 Days” feat in the PegaWORLD

2012 event which was held in Dallas on June 2012.

The same project was also rewarded for its technical and infrastructure

works in the “Information Technology Awards” organized by the CIO

Magazine on December 2012.

• Bank Asya’s technological prowess and service competency is

proven each year with the “Straight Through Processing” excellence

awards given by the leading banks of the world. Bank Asya was

deemed worthy of the STP Award by Standard Chartered Bank and

excellence award by Citibank.

• Awards were presented in the “Mixx Awards Turkey 2012” in the

Rahmi Koç Museum on February 13.

The event acknowledges the best establishments in the digital

marketing communication industry as well as the added value they

provide to the business and to the brands they offer services to.

Bank Asya received the Bronze Award in the Mobile Advertising

category with its “Bank Asya Text Message for Ladies’ Gold Party

Days” project in the third Mixx Awards event which was hosted by

IAB Turkey.

Other Participation Banks

Bank Asya

13

12

Bank Asya recorded 24 percent asset growth in 2012.

Bank Asya Annual Report 2012

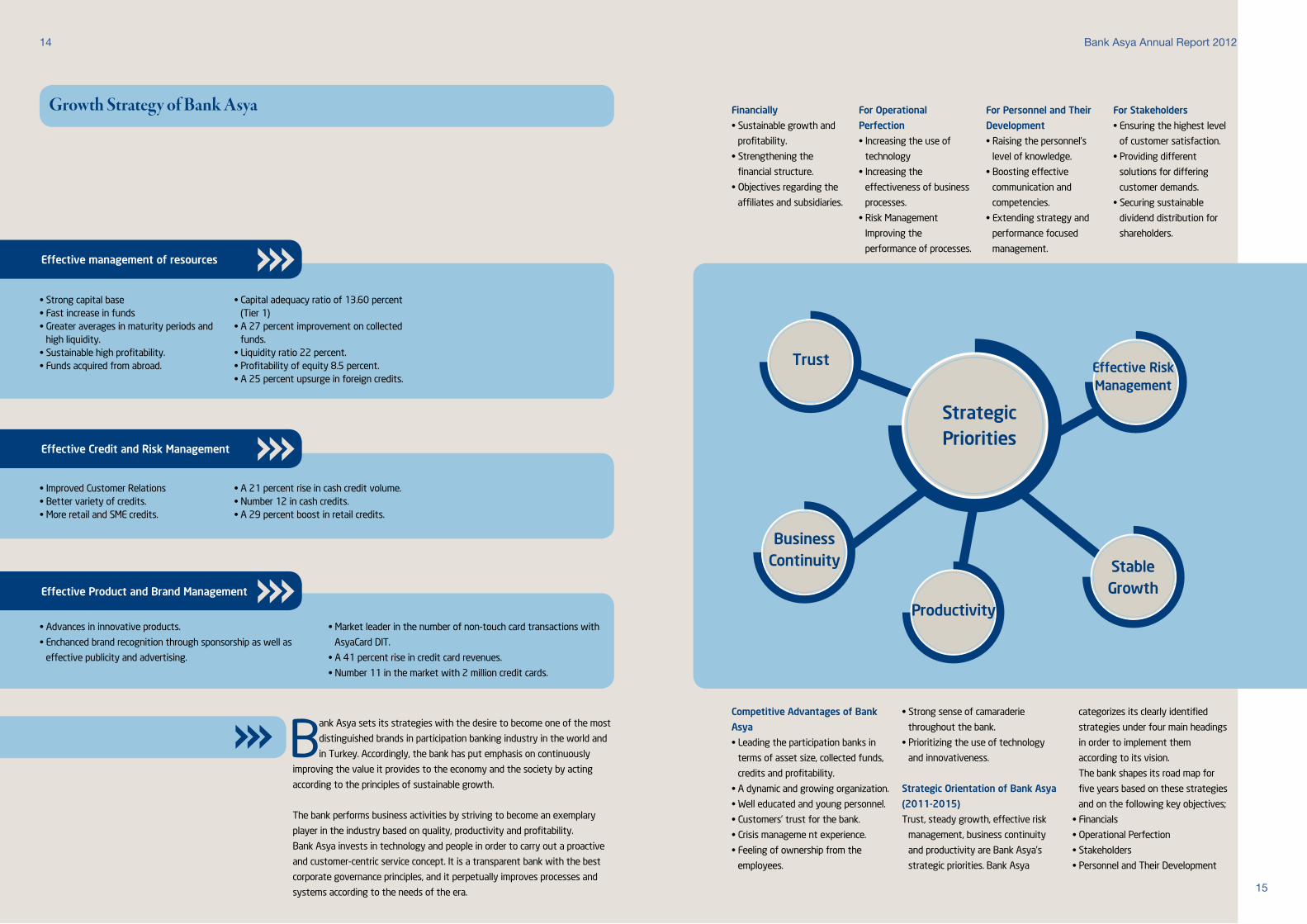

Growth Strategy of Bank Asya

15

14

Effective Credit and Risk Management

Effective Product and Brand Management

Effective management of resources

• Strong capital base• Fast increase in funds • Greater averages in maturity periods and

high liquidity.• Sustainable high profitability.• Funds acquired from abroad.

• Capital adequacy ratio of 13.60 percent (Tier 1)

• A 27 percent improvement on collected funds.

• Liquidity ratio 22 percent.• Profitability of equity 8.5 percent.• A 25 percent upsurge in foreign credits.

• Improved Customer Relations • Better variety of credits. • More retail and SME credits.

• A 21 percent rise in cash credit volume. • Number 12 in cash credits. • A 29 percent boost in retail credits.

• Advances in innovative products.

• Enchanced brand recognition through sponsorship as well as

effective publicity and advertising.

• Market leader in the number of non-touch card transactions with

AsyaCard DIT.

• A 41 percent rise in credit card revenues.

• Number 11 in the market with 2 million credit cards.

Bank Asya sets its strategies with the desire to become one of the most

distinguished brands in participation banking industry in the world and

in Turkey. Accordingly, the bank has put emphasis on continuously

improving the value it provides to the economy and the society by acting

according to the principles of sustainable growth.

The bank performs business activities by striving to become an exemplary

player in the industry based on quality, productivity and profitability.

Bank Asya invests in technology and people in order to carry out a proactive

and customer-centric service concept. It is a transparent bank with the best

corporate governance principles, and it perpetually improves processes and

systems according to the needs of the era.

Financially

• Sustainable growth and

profitability.

• Strengthening the

financial structure.

• Objectives regarding the

affiliates and subsidiaries.

For Operational

Perfection

• Increasing the use of

technology

• Increasing the

effectiveness of business

processes.

• Risk Management

Improving the

performance of processes.

For Personnel and Their

Development

• Raising the personnel’s

level of knowledge.

• Boosting effective

communication and

competencies.

• Extending strategy and

performance focused

management.

For Stakeholders

• Ensuring the highest level

of customer satisfaction.

• Providing different

solutions for differing

customer demands.

• Securing sustainable

dividend distribution for

shareholders.

Business Continuity

Trust

Strategic Priorities

Productivity

Stable Growth

Effective Risk Management

Competitive Advantages of Bank

Asya

• Leading the participation banks in

terms of asset size, collected funds,

credits and profitability.

• A dynamic and growing organization.

• Well educated and young personnel.

• Customers’ trust for the bank.

• Crisis manageme nt experience.

• Feeling of ownership from the

employees.

• Strong sense of camaraderie

throughout the bank.

• Prioritizing the use of technology

and innovativeness.

Strategic Orientation of Bank Asya

(2011-2015)

Trust, steady growth, effective risk

management, business continuity

and productivity are Bank Asya’s

strategic priorities. Bank Asya

categorizes its clearly identified

strategies under four main headings

in order to implement them

according to its vision.

The bank shapes its road map for

five years based on these strategies

and on the following key objectives;

• Financials

• Operational Perfection

• Stakeholders

• Personnel and Their Development

Bank Asya Annual Report 2012

17

Milestones

Bank Asya was founded as Asya Finans in 1996.

It became the first participation bank to be listed in 2006. In 2011, it succeeded as the first

Turkish institution to receive the “Business

Continuity Management Certification” from the

BSI.

1996It began operations under the title of Asya Finans Kurumu A.Ş. in Altunizade headquarters with 2 million Turkish lira original capital.

1999Become subject to the Banking Law. Increased paid capital to 10 million Turkish lira.

2000Increased the number of branches to 25. Launched Asya Finans Internet Branch.

2004Increased the number of branches to 62. Launched Alo Asya Telephone Banking. Increased paid capital to 120 million Turkish lira.

2008Increased the number of branches to 149. Bank Asya became a name sponsor to the TFF 1. League. Increased paid capital to 900 million Turkish lira. Launched non-touch technology products AsyaCard DIT and AsyaPratic DIT.

2005Increased the number of branches to 72. Increased paid capital to 240 million Turkish lira. Changed Asya Finans Kurumu A.Ş. name to Asya Katılım Bankası A.Ş.

2009Increased the number of branches to 158. Became a partner with Senegal based Tamweel Africa Holding SA. AsyaCard DIT received both the “Best Cash Displacement Initiative” award and the “Best New Credit Card Product Launch” award.Bank Asya founded Tuna GYO A.Ş.

2006Increased the number of branches to 92. Increased paid capital to 300 million Turkish lira. Bank Asya shares started the be traded in the ISE with ASYAB code after offering 23 percent of the shares to the public.

2010Increased the number of branches to 175. AsyaPratic DIT was named the “Best Prepaid MasterCard Product in Turkey.” Bank Asya was included in the MoneyGram service network. Introduced AsyaAssist, Lodestar and DIT Mobile.

2002Increased the number of branches to 28. Increased paid capital to 40 million Turkish lira. Launched ASYA24 ATMs and installment credit cards.

2003Increased the number of branches to 43. Asya Finans became a member of VISA. Increased paid capital to 60 million Turkish lira. Bank Asya became a partner to Işık Sigorta A.Ş.

2007Increased the number of branches to 118. Bank Asya shares included in the ISE 30 Index as of 2007.

2011Increased the number of branches to 200. Bank Asya became the first Turkish institution to receive the “Business Continuity Management Certification” from the BSI. Launched mobile branch operations.Introduced PAKSIT and DIT Mobile. Bank Asya succeeded in becoming the first ever organization in Europe to receive the ISO 10002 Customer Satisfaction Management and the EN 15838 Contact Center quality certificates at the same time. Bank Asya fouded Asya Emeklilik A.Ş World Finance named Bank Asya as the Best Commercial Bank in Turkey.

2012Increased the number of branches to 251, the number of ATMs to 671. Bank Asya Call Center launched operations in its second location in Trabzon. Opened its first branch abroad in Erbil and the first overseas office in India. Took the third place in Emea’s “Top Ranking Performers in the Contact Center World“ organization. Bank Asya’s call center was awarded the first place in the “Call Centers are Competing” category of the Call Center Awards 2012 organization. Bank Asya Mobile Branch was elected as the best website in the Middle East and Africa. ŞikayetEndex listed Bank Asya as the fourth most successful bank according to the complaints and satisfactions points which were sent by 650,000 “I have a complaint” members.Bank Asya took the “Pega Financial Services Customer Experience Award” with its “CRM Project in 180 Days” feat in the PegaWORLD 2012 event which was held in Dallas on June 2012. This year, the same project was also rewarded for the technical and infrastructure works in the “Information Technology Awards” organized by the CIO Magazine.

2001Increased paid capital to 20 million Turkish lira.

1997Increased the number of branches to 15.

1998Increased the number of branches to 16. Launched Asya Finans Credit Card.

16 Bank Asya Annual Report 2012

Capital and Partnership Structure of Bank Asya and the Changes that Took Place in the Operating Cycle

19

18

Following table provides information regarding the share distribution of the bank as of the end of 2011 and 2012.

Bank Asya 2011 and 2012 Year-End Share Distributions

2011 Year-End % 2012 Year-End %

Group A (Privileged) 360.000.000 40,00 360.000.000 40,00

Group B (Not traded on the ISE) 64.068.038 7,12 59.759.288 6,64

Group B (Traded on the ISE) 475.931.962 52,88 480.240.712 53,36

Total 900.000.000 100 900.000.000 100

Bank Asya is a multi-partner organization with a widespread domestic capital. With the exclusion of the publicly held portion, it has 216 partners with

privileged shares as of the end of 2012.

Shares owned by the Chairman of the Board of Directors, Board Members, Chief Executive Officer and Assistant Chief Executive Officers

Below is information about the shares owned by the Chairman of the Board of Directors, Board Members, Chief Executive Officer and Assistant Chief Executive Officers according to the stock ledger as of December 31, 2012.

Title Name and Last Name Areas of Responsibility

Chairman of the Board of Directors Professor Erhan BİRGİLİ Chairman of the Board of Directors

Board Members Mustafa Talat KATIRCIOĞLU Acting Chairman of the Board of Directors

Ali ÇELİK Board Member

Recep KOÇAK Board Member

Zafer ERTAN Board Member

Mehmet GÖZÜTOK Board Member

Ercüment GÜLER (Ph. D.) Member of the Board and the Audit Committee

Mehmet URUÇ Att. Member of the Board and the Audit Committee

Chief Executive Officer Ahmet BEYAZ Board Member and Chief Executive Officer

Vice Chief Executive Officers Murat DEMİR Commercial Banking Groups

Ahmet AKAR Credit Appropriation Group

Dr. Feyzullah EĞRİBOYUN Treasury Group

Fahrettin SOYLU Banking Operations Group

Mahmut YALÇIN Financial Affairs Group

Talha Salih YAYLA Risk Monitoring Legal Affairs Group

Hakan Fatih BÜYÜKADALI HR Group

Ali TUĞLU Information Technologies Group

Coordinator Abdurrahman KÖSE Retail Banking Group

Group Director Murat AYDOĞAN Support Services Group

Statutory Auditors Atıf BİLGİN Auditor

İrfan HACIOSMANOĞLU Auditor

İzzet AKYAR Auditor

(*) Shares owned by the Chairman of the Board of Directors, Board Members, Chief Executive Officer and Assistant Chief Executive Officers

are at a very insignificant level.

Bank Asya Annual Report 2012

Bank Asya Annual Report 2012

21

20

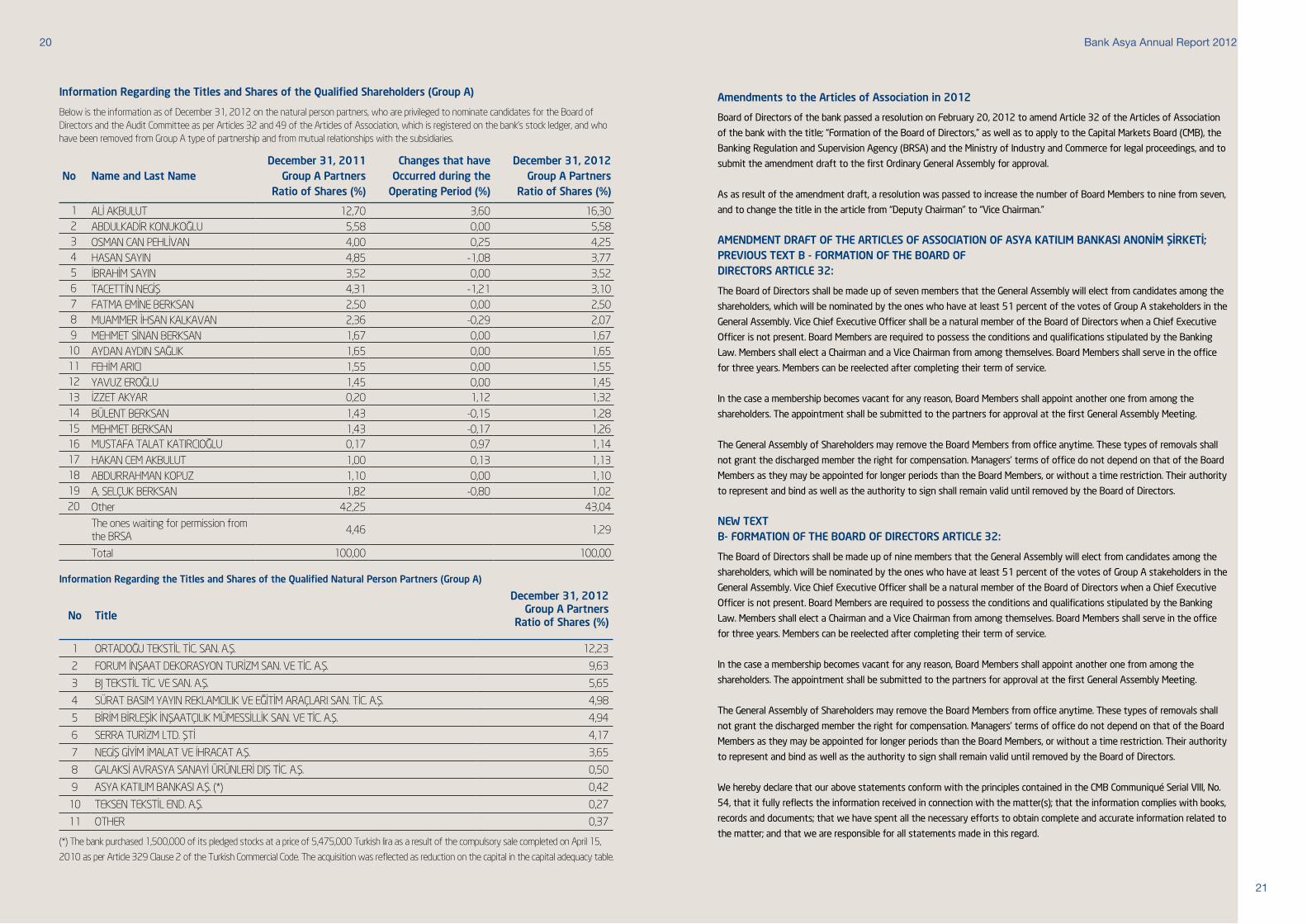

Information Regarding the Titles and Shares of the Qualified Shareholders (Group A)

Below is the information as of December 31, 2012 on the natural person partners, who are privileged to nominate candidates for the Board of Directors and the Audit Committee as per Articles 32 and 49 of the Articles of Association, which is registered on the bank’s stock ledger, and who have been removed from Group A type of partnership and from mutual relationships with the subsidiaries.

No Name and Last NameDecember 31, 2011

Group A Partners Ratio of Shares (%)

Changes that have Occurred during the

Operating Period (%)

December 31, 2012Group A Partners

Ratio of Shares (%)

1 ALİ AKBULUT 12,70 3,60 16,30 2 ABDULKADİR KONUKOĞLU 5,58 0,00 5,58 3 OSMAN CAN PEHLİVAN 4,00 0,25 4,25 4 HASAN SAYIN 4,85 -1,08 3,77 5 İBRAHİM SAYIN 3,52 0,00 3,52 6 TACETTİN NEGİŞ 4,31 -1,21 3,10 7 FATMA EMİNE BERKSAN 2,50 0,00 2,50 8 MUAMMER İHSAN KALKAVAN 2,36 -0,29 2,07 9 MEHMET SİNAN BERKSAN 1,67 0,00 1,67

10 AYDAN AYDIN SAĞLIK 1,65 0,00 1,65 11 FEHİM ARICI 1,55 0,00 1,55 12 YAVUZ EROĞLU 1,45 0,00 1,45 13 İZZET AKYAR 0,20 1,12 1,32 14 BÜLENT BERKSAN 1,43 -0,15 1,28 15 MEHMET BERKSAN 1,43 -0,17 1,26 16 MUSTAFA TALAT KATIRCIOĞLU 0,17 0,97 1,14 17 HAKAN CEM AKBULUT 1,00 0,13 1,13 18 ABDURRAHMAN KOPUZ 1,10 0,00 1,10 19 A, SELÇUK BERKSAN 1,82 -0,80 1,02 20 Other 42,25 43,04

The ones waiting for permission from the BRSA

4,46 1,29

Total 100,00 100,00

Amendments to the Articles of Association in 2012

Board of Directors of the bank passed a resolution on February 20, 2012 to amend Article 32 of the Articles of Association

of the bank with the title; “Formation of the Board of Directors,” as well as to apply to the Capital Markets Board (CMB), the

Banking Regulation and Supervision Agency (BRSA) and the Ministry of Industry and Commerce for legal proceedings, and to

submit the amendment draft to the first Ordinary General Assembly for approval.

As as result of the amendment draft, a resolution was passed to increase the number of Board Members to nine from seven,

and to change the title in the article from “Deputy Chairman” to “Vice Chairman.”

AMENDMENT DRAFT OF THE ARTICLES OF ASSOCIATION OF ASYA KATILIM BANKASI ANONİM ŞİRKETİ; PREVIOUS TEXT B - FORMATION OF THE BOARD OF DIRECTORS ARTICLE 32:

The Board of Directors shall be made up of seven members that the General Assembly will elect from candidates among the

shareholders, which will be nominated by the ones who have at least 51 percent of the votes of Group A stakeholders in the

General Assembly. Vice Chief Executive Officer shall be a natural member of the Board of Directors when a Chief Executive

Officer is not present. Board Members are required to possess the conditions and qualifications stipulated by the Banking

Law. Members shall elect a Chairman and a Vice Chairman from among themselves. Board Members shall serve in the office

for three years. Members can be reelected after completing their term of service.

In the case a membership becomes vacant for any reason, Board Members shall appoint another one from among the

shareholders. The appointment shall be submitted to the partners for approval at the first General Assembly Meeting.

The General Assembly of Shareholders may remove the Board Members from office anytime. These types of removals shall

not grant the discharged member the right for compensation. Managers’ terms of office do not depend on that of the Board

Members as they may be appointed for longer periods than the Board Members, or without a time restriction. Their authority

to represent and bind as well as the authority to sign shall remain valid until removed by the Board of Directors.

NEW TEXTB- FORMATION OF THE BOARD OF DIRECTORS ARTICLE 32:

The Board of Directors shall be made up of nine members that the General Assembly will elect from candidates among the

shareholders, which will be nominated by the ones who have at least 51 percent of the votes of Group A stakeholders in the

General Assembly. Vice Chief Executive Officer shall be a natural member of the Board of Directors when a Chief Executive

Officer is not present. Board Members are required to possess the conditions and qualifications stipulated by the Banking

Law. Members shall elect a Chairman and a Vice Chairman from among themselves. Board Members shall serve in the office

for three years. Members can be reelected after completing their term of service.

In the case a membership becomes vacant for any reason, Board Members shall appoint another one from among the

shareholders. The appointment shall be submitted to the partners for approval at the first General Assembly Meeting.

The General Assembly of Shareholders may remove the Board Members from office anytime. These types of removals shall

not grant the discharged member the right for compensation. Managers’ terms of office do not depend on that of the Board

Members as they may be appointed for longer periods than the Board Members, or without a time restriction. Their authority

to represent and bind as well as the authority to sign shall remain valid until removed by the Board of Directors.

We hereby declare that our above statements conform with the principles contained in the CMB Communiqué Serial VIII, No.

54, that it fully reflects the information received in connection with the matter(s); that the information complies with books,

records and documents; that we have spent all the necessary efforts to obtain complete and accurate information related to

the matter; and that we are responsible for all statements made in this regard.

Information Regarding the Titles and Shares of the Qualified Natural Person Partners (Group A)

No Title

December 31, 2012 Group A Partners

Ratio of Shares (%)

1 ORTADOĞU TEKSTİL TİC. SAN. A.Ş. 12,23

2 FORUM İNŞAAT DEKORASYON TURİZM SAN. VE TİC. A.Ş. 9,63

3 BJ TEKSTİL TİC. VE SAN. A.Ş. 5,65

4 SÜRAT BASIM YAYIN REKLAMCILIK VE EĞİTİM ARAÇLARI SAN. TİC. A.Ş. 4,98

5 BİRİM BİRLEŞİK İNŞAATÇILIK MÜMESSİLLİK SAN. VE TİC. A.Ş. 4,94

6 SERRA TURİZM LTD. ŞTİ 4,17

7 NEGİŞ GİYİM İMALAT VE İHRACAT A.Ş. 3,65

8 GALAKSİ AVRASYA SANAYİ ÜRÜNLERİ DIŞ TİC. A.Ş. 0,50

9 ASYA KATILIM BANKASI A.Ş. (*) 0,42

10 TEKSEN TEKSTİL END. A.Ş. 0,27

11 OTHER 0,37

(*) The bank purchased 1,500,000 of its pledged stocks at a price of 5,475,000 Turkish lira as a result of the compulsory sale completed on April 15,

2010 as per Article 329 Clause 2 of the Turkish Commercial Code. The acquisition was reflected as reduction on the capital in the capital adequacy table.

23

22

Esteemed Shareholders,

Even though it has been five years since the global crisis, it was a year with many countries, especially developed economies and the Euro zone countries, failing to resolve their main macroeconomic and financial problems, debt crisis stifling the Euro zone and the US tackling uncertainties. In particular, global economic performance continued falling due to rising oil prices because of geopolitical risks.

On contrary to the negative outlook in developed countries, financial markets of the emerging countries achieved relatively positive performances. Financial markets in Turkey, too, had a successful year due to shrinking current deficit in particular and also as a result of the positive macro indicators, the atmosphere of trust in the economy and the credit rating agencies increasing Turkey’s score to investable.

Turkey continues to be a safe harbor for investors in the region. As a matter of fact, the ISE 100 Index soared by 52 percent in 2012 to the content of investors.

In 2012, global uncertainties lingered, Euro zone was marred by a deepened crisis and many European countries technically went into recession, in addition, debt and unemployment ratios climbed in developed countries, whereas, Turkey steer through a year with balanced domestic and foreign demand.

Nevertheless, following a strong and domestic market driven growth at a rate of eight percent that was led by the private sector, Turkey took measures to cool down the economy and the growth rate slowed down in 2012 as foreign demand withered because of the stalling global economy and expanding crisis in the Euro zone.

Turkish economy is projected to grow at a rate of 3 to 3.2 percent in 2012 as the country successfully goes through

the soft landing process, ensuing a well-adjusted slowing down period that was brought on with the measures taken to cool down the economy.

Banking sector in Turkey kept thriving with its strong and sound structure despite uncertainties in the global economy and the recession in Europe.

On the other hand, participation banks improved their share in asset size and collected funds by displaying a higher performance than the industry.

Bank Asya continued to grow and remain profitable with the industry also flourishing in 2012. The bank marched on confidently to carry out the strategy of using its capital more efficiently and establishing an expanded a credit portfolio. Bank Asya has focused on its main business areas of fund allocations and participation fund collection, achieving a growth rate over the industry average in credits and in fund collection.

Bank Asya strives to provide fast and high quality service in all corners of Turkey with a burgeoning service network within the scope of interest free banking principles. As such, the bank increased the number of its branches to 251, including an overseas branch, in 2012.

I would like to take this opportunity to thank devoted employees of Bank Asya as they have transformed the bank into a pioneering force in the industry. I would also like to say thanks to our stakeholders for playing a great role in the bank’s accomplishments as well as strengthening it with their presence and support. Let me also offer my gratitude to our esteemed customers who have embraced Bank Asya as their own for the whole world to see.

With my warmest regards,

Professor Erhan BİRGİLİ

Chairman of the Board of Directors

Message from the Chairman of the Board of Directors

The industry maintained growth in 2012. Accordingly, Bank Asya also succeeded in sustaining its profitability and growth with the objectives of increasing return on equity and extending its credit portfolio.

Bank Asya Annual Report 2012

24

25

Esteemed Shareholders,

Banking sector in Turkey preserved its sound and strong structure in 2012 during a year of persistent global uncertainties. The country maintained a positive outlook in liquidity, asset quality, capital adequacy and profitability indicators. Thus, the industry enjoys an unfaltering system compared to those of developed and emerging countries. Banking Industry has remained adamant in sustaining its growth despite a relative slow down due to a gentle down trend in the first half of 2012.

Funding cost for the banks rose and credit volume performed sluggishly in 2012 as a result of the Central Bank and the BRSA policies that increased credit costs and tightened monetary policies as well as shrinking the domestic demand.With faltering increase rates in deposits, which is the most significant financing source for the banks, the industry had to resort to alternative non-deposit resources in order to reduce the cost of financing, to diversify means of acquiring funds and to diminish the discordance in the balance sheets by extending maturity dates.

In spite of the aforementioned measures and the slow down in the economy, the banking industry succeeded in maintaining its growth. In 2012, the industry recorded a 15 percent rise in total credits and 11 percent in collected funds. The banking industry provided credits in the amount of 813.4 billion Turkish lira with an expansion of 112.8 billion Turkish lira in the same year. Return on equity surged to 14.4 percent with the capital adequacy rate swelling to 17.88 percent from 16.55 percent.

An analysis of the chart in terms of participation banking shows that credits climbed by 24 percent and collected funds by 22 percent, performing better than the industry. Participation banks pressed on, increasing their market share in the industry.They managed to take a six percents share in the industry by racking a 25 percent jump in total assets.

Bank Asya had another accomplished year in 2012 as pioneer among other participation banks. The bank strives to offer the best service to its customers within the scope of interest free banking principles. After setting targets to perform a healthy growth for 2012, Bank Asya fulfilled its objectives in allocating resources and granting funds. Bank Asya protected its leadership in participation banks in asset size, proving itself as major player once again by advancing the bank’s asset totals to 21.4 billion Turkish lira with a 24 percent improvement and collected funds to 15.7 billion Turkish lira with a 27 percent rise.

Reaching more customers with a concept of fast and quality service...

In the past two years, Bank Asya has shifted its focus from larger corporate clients to SMEs and retail customers to provide services to them. In an effort to expand its reach, the bank opened 51 new branches, increasing the total number of branches to 251, including an overseas branch, and the number of ATMs to 671.

These efforts bore fruit as credit amount provided to SME customers burst by 80 percent and credits granted to retail customers went up by 29 percent year-on-year.

Message from the Chief Executive Officer

Bank Asya Annual Report 2012

Bank Asya accomplished another year of growth in 2012, improving its asset total to 21.4 billion Turkish lira with a 24 percent rise.As the biggest participation bank in Turkey, Bank Asya made an impact on real economy in the amount of 24.3 billion Turkish lira through the credits it granted in 2012.

27

Bank Asya Annual Report 2012

As such, we have provided services to an even larger customer base by extending our credit portfolio. Furthermore, the bank secured a place at the top ranks of the industry with 2 million credit cards.

Bank Asya set its sights to perform a 22 percent improvement on credits and 21 percent in collected funds in 2013. The bank plans to extend the number of branches to 281 by initially launching 30 new ones in 2013 in order to reach more customers.Bank Asya is determined to repeat the success of 2012 by maintaining its growth in Retail Banking as well as in SME Banking in 2013. The bank takes pains to open branches in hinterland areas where SMEs and other customers can get easy access. For the next operating period, Bank Asya especially aims to reach export companies and to flourish in cities with export activities .

In addition to extending network of branches, the bank also maintained its organic growth in 2012. Bank Asya surged the number of district offices to 11 and personnel to 5,064.We intend to boost the productivity in using our labor force with the addition of new branches in 2013.

In 2012, Bank Asya also completed major affiliate investments as well as taking significant steps to fill a critical void in the industry in keeping with its mission of providing contemporary banking services according to interest free banking principles. Asya Emeklilik began its operations as

the first interest free pension company in Turkey.The company has already proven that it is on the way to becoming a dominant force in the industry with over 30,000 customers it has acquired in a short period of time.We founded Asya Menkul Değerler A.Ş. to extend our investments to the securities market. We will offer consulting services to our customers to help them put their investments to good use in diverse areas while providing intermediation for public offerings.

Bank Asya also kept its momentum with overseas investments by introducing its first branch abroad in Erbil and the first overseas office in India We are the first participation bank to open a foreign representative office in India. Moreover, we operate banks in Mauritania, Guinea, Senegal and Niger with Tamweel Holding. The bank has set its goals to focus more on the east when investing in foreign countries in 2013.

Asia is the rising star of the day. Accordingly, we plan to concentrate our investments in this region, of which the bank is named after in part. The bank takes into consideration certain criteria when carrying out foreign investment initiatives. These considerations are high growth potential, young population, income level, income distribution, the right environment in the country for participation banking and banking activities.We know that in order to provide better services to our customers, we have to

possess a sound technical infrastructure. Therefore, we never cease to invest in new technology as one of our priorities for 2013 is to expand the use of technology in the bank. Bank Asya’s own 270 strong employees are currently revamping our main banking software so as to enable it to be used by all banking systems in the world.

We offered a variety of gold related products and established a rich product diversity for our customers in 2012. Especially, gold-based checking accounts and participation accounts, as well as the initiation of physical gold purchase and sale transactions become a hit with the customers. These developments in gold-based products drove Bank Asya to the top ranks among other banks in terms product awareness.

Efforts by Bank Asya bore fruit as the bank become industry’s best performer in improvement of gold volume with reserves reaching 13.7 tons in 2012. In particular, ”Reception Day for Gold” drives that were carried out by Bank Asya branches brought in nearly 4 tons of gold to Turkish economy.

Awareness for social responsibility...The bank crowned its accomplishments with a myriad of awards received in 2012. Bank Asya took the number 476 spot among the “Most Valuable Banks in the World” in 2012 according to the Banker magazine.

Bank Asya’s call center was awarded the first place in the “Call Centers are Competing” category of the Call Center

Awards 2012 organization. Bank Asya Mobile Branch was elected as the best website in the Middle East and Africa. The bank took the “Pega Financial Services Customer Experience Award” with its “CRM Project in 180 Days” feat in the PegaWORLD 2012 event which was held in Dallas on June 2012.The same project was also rewarded for its technical and infrastructure works in the “Information Technology Awards” organized by the CIO Magazine on December 2012. Bank Asya came third in Emea’s “Top Ranking Performers in the Contact Center World“ organization.

Bank Asya operates with an awareness for social responsibility as it endeavors more and more each passing day to provide interest free banking products to its customers as well as making the highest contribution to the economy and increasing the share that participation banks have in the industry. In 2012, the bank maintained its support for global organizations like the international summits organized by the Turkish Confederation of Businessmen and Industrialists (TUSKON) and also the Turkish Olympics, in addition to launching the “I am Sending a Child to School” campaign by providing 350,000 Turkish lira for the initiative within the scope of the social responsibility project. We also made other alternatives available for our customers to pitch in to the campaign if they wish to do so by authorizing automatic payment order from their credit cards

or by donating the loose change amount after the dot on their current participation account. Through this project, we aimed to provide scholarship to orphans, to the children of martyrs or veterans, as well as to poor or accomplished children.

Bank Asya strives to offer good quality and fast services in every corners of Turkey with a service network that is expanding according to the principles of interest free banking. The bank is determined to stay on course for growth as a respected, trustworthy and active organization, providing services in international standards with the variety of products it develops.

I would like thank our devout employees for their commitment as a team in the success of Bank Asya as it has become as a pioneering force in participation banking, always offing new products and cutting-edge technological innovations to its customers. I would also like to offer my gratitude and thanks to our esteemed customers who incessantly supported Bank Asya and embraced it as their own. Let me also praise and express my gratitude to our stakeholders as we could count on their continuously support during our operations.

With my warmest regards,

Ahmet BEYAZBoard Member and Chief Executive Officer

Message from the Chief Executive Officer

26

29

28 Bank Asya Annual Report 2012

Bank Asya succeeded as the best performer in fund increases with a 27 percent improvement in 2012.

31

Bank Asya Annual Report 201230

Macroeconomic Outlook and the Banking Industry

Economic policies of 2012 shifted Turkish economy towards a more balanced growth model with stronger exports in 2012.

Despite starting the year with a positive outlook resulting from the monetary expansion, the markets had to follow

a generally uncertain course throughout the year in 2012 due to European countries failure to draw up a road map, amplifying risks in the Middle East and concerns about growth in emerging countries.

Developments in the International Arena Marco economic weaknesses and risks in developed countries caused the growth rate in emerging countries to go into a falling trend.

Risk perception of the markets has changed a result of the debt crisis in the Euro zone and the problems revolving around the banking industry. Government bond yields of risky countries like Spain and Portugal jumped to record high levels during the period.

Whereas, revenues from government debt securities of countries like Germany and France took the sharpest dive of the history with a desire to avoid risks. Central banks in developed countries were forced into taking additional expansionist measures as the debt crisis curtailed growth in the Euro zone and significantly increased the risks in the market, and the job market in the US recovered slower than expected.

Consequently, the European Central Bank (ECB) cut the policy rates by 0.25 points to 0.75 points and announced that it would acquire bonds from troubled countries in secondary markets only under certain conditions so as to reduce the effects of the debt crisis. The markets were also relieved with the news that the newly elected government of Greece in the June elections would continue with the austerity measures.

The Federal Reserve (FED) took similar measures as well, carrying out the third monetary expansion in order to spark the real estate market and to speed up recovery in the employment. In addition, it announced it would to purchase mortgage bonds from the market each month in the amount of $40 billion.

The FED displayed its determination to continue with the expansionist monetary policies by stating

Gross Domestic Product (GDP) grew by 3.4 percent in the first quarter of 2012, 3 percent in the second quarter, 1.6 percent in the third quarter and 2.6 percent in the first nine months of the year.

Domestic demand shrunk in 2012 as a result of the measures taken by the Central Bank of Turkey (CBT) and other authorities as well as due to policies in effect. The ratio of foreign demand in the GDP rose despite of the problems surrounding Europe which holds a significant share in our exports. This, in return, allowed growth to take a more balanced form.

Foreign demand increased partly due to rising exports to Africa and the Middle East, and also because gold exports were on a relatively higher trend for the period. Medium Term Plan (MTP) announced on October 2012 projects that contribution of exports to the growth will slow down and the growth rate for 2012 will be 3.2 percent with the domestic demand becoming more effective in the results.

Despite of slackening economic activities in the first half of 2012, initial indicators for the last month of the year show that there is a mild

that it was going to keep the interest rates close to zero percent until the middle of 2015.

Global risk appetite rallied in the second half of the year as central banks provided support to the economies of emerging countries and uncertainties surrounding the debt crisis in the Euro zone diminished. Emerging countries drew capital inflow at a fast rate during this period. Control measures resulted in the countries’ bond yields going into a downtrend and gains from the stock markets rising as of the last quarter of the year.

Markets in the US were uneasy with the controversy over the “Fiscal Cliff” on the last month of 2012. However, concerns surrounding the issue were dispelled when the US Senate speedily passed a bill that prevented the fiscal cliff.

Developments in the Domestic ArenaMeasures and economic policies that were implemented in 2012 heralded the first steps of a more sustainable growth model. Economic activity slowed down in Turkey with the fragility of global economy becoming more visible in 2012.

8

66

2,8

0,5

-3,4

3

1,6 1,31,5

-0,5

5,1

3,83,3 3,62,7

7,4

6,25,3

5,6

4

2

0

-2

-4

2008

Developed Countries Emerging Countries The World

2009 2010 2011 2012 (T) 2013 (T)

46,9

77,2 77,0 75,3 72,1

69,2 66,9 63,3 62,0 59,3

55,6 52,3 50,8 48,9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2010

2011

January

12

February

12

Marc

h 12

April 12

May 12

June 12

July 12

August 12

Septem

ber 12

October 1

2

November 1

2

Decem

ber 12

Global Growth Current Accounts Deficit (Billion US Dollar)

0,7

9.2

8.5

3.01.6

3.4

-4.8

2008 2010 2011 2012/1 2012/2 2012/3

Difference on (GDP) % (Based on Fixed Prices)

2009

33

Bank Asya Annual Report 201232

recovery. Industrial index reached its highest values in September and October without the seasonal and date related effects, while the rate of capacity utilization standing at 74.2 percent.

Even though the economy stalled and imports decreased, foreign trade and current accounts deficit also took a better shape in 2012. As a result of rising exports and declining imports, foreign trade deficit fell down to $105.9 billion at the end of 2011 and to $83.3 billion at the end of 2012. Ratio of exports to imports rose to 64.5 percent in 2012 from 56 percent in 2011. Exports surged to $152.4 billion and imports were $237.3 billion in 2012.

In parallel with the improvement in the balance of foreign trade, current accounts deficit shrunk significantly, dropping to $48.9 billion at the end of 2012 from $77.2 billion at the end of 2011. Risk premiums of emerging countries fell with the increasing global risk appetite in 2012. In particular, expansionary monetary policies that were implemented by many countries in the second half of the year helped strengthen the capital inflow into emerging countries.

Subsequently, Turkish lira had similar performance to those of the currencies of emerging countries. Currency basket sloped as the US Dollar lost value against Turkish lira during this period. Despite of the increase it displayed, real effective exchange rate remained at a relatively narrow margin. Real effective exchange rate (REER) rose due to the fact that risk appetite in global markets went up, macroeconomic indicators regarding Turkey improved and, international ratings agency, Fitch

Ratings increased Turkey’s long-term credit rating. REER advanced to 118.32 percent on December 2012 from 112.42 on January 2012. In the case that REER reaches 120 or 130 percent levels, the CBT warned that it would take measure at different levels to prevent Turkish lira gaining too much value.

A slow down in economic activities caused deceleration in the speed of tax revenues. When increases in primary expenditures were added to this fact, the budget balance was slightly disrupted compared to the year before. During this period, revenues from income and corporate tax weakened, and VAT revenues dropped with shrinking domestic demand. In 2012, Central Government Budget Deficit reached 28.8 billion Turkish lira with primary surplus hitting 19.6 billion Turkish lira. MTP that covers the period between 2013 and 2015 aims to preserve the down trend in the ratio of budget deficit to national income to keep it at around 1.8 percent.

Recent positive outlook on the public net debt stock continued in 2012. It rose to 532 billion Turkish lira by the end of 2012 with a 9.5 percent jump from 518.4 billion Turkish lira at the end of 2010 In the 2013-2015 MTP, the ratio of debt stock to national income is projected to fall down to 36.5 percent in 2012 from 39.9 percent in 2011.

Benchmark bond hit the lowest level of all times at 5.73 percent following the interest that was created for Turkey’s assets after Fitch Ratings increased the country’s credit note. In the mean time, the Undersecretariat of Treasury issued two sukuk certificates; one in US dollar and one

in Turkish lira, for the first time in its history in 2012. High demand for both of the sukuk certificates was a positive first step for the initiative. Sukuk certificate issuance is projected to provide help in increasing domestic savings, expanding the investor base and diversifying financing instruments.

Consumer Price Index (CPI) was 6.16 percent and Producer Price Index (PPI) was 2.45 annually in 2012. Even tough these results meant missing the year-end inflation target of 5 percent, it was still lower than the 7.4 percent rate projected in the last inflation report of the Central Bank. In its October 24 report, the CMB projected inflation to stand between 3.5 and 6.8 percent with the middle range being at 5.3 percent. The same report stipulates the inflation to remain stable at 5 percent in the mid-term.

In its Monetary Policy Meeting on December 2012, the CMB lowered the policy rate by 25 base points to 5.50 with an effort to support the financial stability. The Central Bank chose to narrow the interest rate corridor from the 5 to 12.5 percent margin at the beginning of 2012 by implementing cuts throughout the year. Interest rate for overnight borrowing was lowered to 4.75 percent and debt interest to 8.75 percent in the Monetary Policy Committee meeting on January 2013.

The CBT maintained its policy of keeping interest rates low in times of fast capital inflow so as to balance risks surrounding financial stability. Instead, it continued with macro precautionary measures by using the required reserves channel. The idea behind

In 2012, two large sukuk certificate issuance took place with great interest

for the both of them. These types of certificates

are extremely critical in terms of diversifying

participation banking products and also in

increasing savings in the domestic market.

using this channel is to strengthen the currency and gold reserves as well as relieving the banking system in terms of liquidity management. The CBT announced that it will implement a new structural policy instrument aimed at establishing financial stability. Starting from 2014, the new practice proposes the banks

to gradually allocate additional required reserves according to the leverage ratios on their balance sheets in the last quarter of 2013. The Central Bank stated that as well as the new instrument, in 2013, it will also continue using the policy rate, interest rate corridor, Turkish lira and foreign currency liquidity management as cyclical

instruments, in addition to using term based required reserves and reserve option mechanism as structural instruments. It declared that it would resort to currency purchasing and selling on foreign currency liquidity management instruments only it becomes truly necessary.

135

13121110

9876543

Real Effective Exchange Rate (2003=100)

Consumer Price Index (Percentage Difference in 12 Months)

130

125

120

115

110

105

100

Jan.

08

Apr

.08

July

.08

Oct

.08

Jan.

09

Apr

.09

July

.09

Oct

.09

Jan.

10

Apr

.10

July

.10

Oct

.10

Jan.

11

Apr

.11

July

.11

Oct

.11

Jan.

12

Apr

.12

July

.12

Oct

.12

Jan.

08

Apr

.08

July

.08

Oct

.08

Jan.

09

Apr

.09

July

.09

Oct

.09

Jan.

10

Apr

.10

July

.10

Oct

.10

Jan.

11

Apr

.11

July

.11

Oct

.11

Jan.

12

Apr

.12

July

.12

Oct

.12

35

Bank Asya Annual Report 201234

Asset Growth (Million TL)

Participation Banks Industry Participation Banks / Industry (%)2008 25.770 732.536 3,52

2009 33.628 834.014 4,03

2010 43.339 1.006.667 4,31

2011 56.148 1.217.695 4,61

2012 70.279 1.370.736 5,13

Growth on Collected Fund - Deposit

Participation Banks Industry Participation Banks / Industry (%)2008 19.045 454.599 4,19

2009 26.711 514.620 5,19

2010 33.089 617.037 5,36

2011 39.220 695.496 5,64

2012 47.921 771.884 6,21

Growth on Granted Funds (Million TL)

Participation Banks Industry Participation Banks / Industry (%)2008 20.190 397.460 5,08

2009 25.372 422.270 6,01

2010 32.412 537.492 6,03

2011 41.526 700.705 5,93

2012 50.323 813.444 6,19

Development of the Banking Industry

Assets of the banking industry grew by 13 percent to reach 1.4 trillion Turkish lira while collected funds in the industry improved by 11 percent to arrive at 772 billion Turkish lira year-on-year in 2012.

December 2012 data puts asset size of the banking industry at 1.4 trillion Turkish lira and collected funds at 773 billion Turkish lira.

The amount of credits is 813 billion Turkish lira.

Asses size of participation banks grew to 70.3 billion Turkish lira in 2012.

Their collected fund reached 47.9 billion Turkish lira with the credit volume standing at 50.3 billion Turkish lira. Participation banks outperformed the industry in active size and collected funds by improving its share. Ratio of the participation banks’ total assets to that of the banking industry rose to 5.13

percent by the end of December 2012 from 4.61 percent in 2011. Share of participation banks in collected funds increased to 6.21 percent in 2012 from 5.64 percent in 2011 with its share in credits climbing to 6.19 percent in 2012 from 5.93 percent year-on-year.

37

Bank Asya Annual Report 201236

Activities of Bank Asya in 2012

The bank performed a 27 percent growth rate in collected funds in 2012.Bank Asya succeeded in reaching 15.7 billion

Turkish lira in collected funds with a 27 percent

improvement year-on-year in 2012 at a year

when persistent uncertainty marred global

markets and growth rate in domestic market

bogged down

Fast growth on annual average current account Bank Asya advanced its annual average current

account to 2.9 billion Turkish lira with a 29

percent improvement in 2012 from 2.2 billion

Turkish lira in 2011.

Growth rate twice that of the industryBank Asya accomplished a 27 percent rise in

collected funds in 2012, attaining a growth rate

higher than those of the industry and the group

it belongs to. Collected fund increase was 11

percent the industry in general and 22 percent

in participation banks in the same year.

High fund target Following the momentum it achieved in collected

funds in 2012, Bank Asya is determined to

preserve this drive with a target of 21 percent

in 2013.

CORPORATE BANKINGBank Asya operates in the financial markets which is one of the industries that experience changes in the swiftest manner. The bank offers fast and effective solutions to answer customer need by utilizing its competitive advantage in corporate banking activities. Bank Asya performs corporate banking activities with a customer-centric, project based and multifaceted service concept as part of its permanent business partnership model with the customers.

Bank Asya provides services in six corporate branches with three in Istanbul and one each in Izmir and Antalya. Highly qualified corporate branch personnel offer strong financing opportunities to 711 companies in 302 different groups through the sound marketing and communication network they have established in corporate branches.

There are a myriad of corporate products and services Bank Asya extends to corporate banking customers as the bank expanded its product portfolio even more in 2012 by adding the Gold Participation Account, Forward Transactions and Private Pension System.

Products offered to corporate costumers • Personal Current Accounts• Participation Accounts• Cash Management• Cash Credits• Non-Cash Credits• Foreign Trade finance• Insurance Services• AsyaCard Business• Gold Participation Accounts• Forward Transactions• Corporate Pension Plans

Developing and changing economic conditions call for particular requirements as well. Bank Asya performs accurate analyses of these requirements and carries out effective marketing activities as a proponent of pioneering initiatives in the interest free banking system and by operating with the principle of constant improvement.

The bank takes into consideration the safety, liquidity and productivity aspects when assessing credit requests from customers.

Corporate MarketingThe size of the risk that Corporate Marketing Office of Bank Asya managed was in line with the bank’s targets and the market conditions in 2012.

Corporate customers opted to make us of their deposits in participation accounts of the Bank Asya after receiving services from the bank in 2012. The volume of the fund from customers in the corporate segment grew more than double compared to the year before.

Bank Asya makes future decisions regarding the corporate banking field by conforming to the principles that have guided the bank in the previous years as well.

Corporate Banking Principles• To call on regularly and stay in constant contact with the customers in order to meet their needs accurately. • To use time fastidiously and get back to customers swiftly when answering their requests.• To establish trust by providing clear answers to customer questions for continuity of business relationships.• To provide a wide variety of services to customers; from credits and cash management to foreign trade brokerage and project financing.• To develop new products and services tailored to customer expectations. • To be open to customers suggestions and to revamping the business processes according to their recommendations.•To increase its weight in the market by improving relationships with current customers and by adding new ones to its portfolio at the same time. • To offer products and services at productive, profitable and competitive prices.• To become organized and come up with results according to corporate objectives. Bank Asya performs Corporate Banking operations in a manner to meet customer demands in every area; from credits and cash management to foreign trade and investment products by utilizing a multifarious product range, professional portfolio teams, technology-based systems and other diverse service channels. As it has done in the past 16 years of its operations, Bank Asya is driven to make an impact on the county’s economy in 2013 by staying true to the company motto of “supporting the producers” and by continuing operations according to the customer-centric marketing concept of the bank and without compromising from corporate values as well as risk focused policies.

After advancing its collected funds by 27 percent in 2012, Bank Asya is determined to maintain this strong momentum in 2013 to rally fund growth by 21 percent and protect its position as the participation bank with the largest asset expansion.

11% 27%

Growth Rate in the Industry in 2012

Growth Rate of Participation Banks in 2012

Growth Rate of Bank Asya in 2012

22%

5.843

9.137

11.167

12.397

15.742

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

14.000.000

16.000.000

18.000.000

2008 2009 2010 2011 2012

Annual Trend on Collected Funds (Million TL)

39

Bank Asya Annual Report 201238

COMMERCIAL BANKINGBank Asya embraces quality and customer-

centric service concept in commercial banking. As

such, it provides fast, effective and innovative

solutions for customer needs.

Bank Asya’s main objective in regards to

commercial banking is to fulfill all banking

requirements of customers by making available

more rewarding financing choices and versatile

solution options in fluctuating and competitive

financial markets. Bank Asya develops long-term

and sustainable relationships with its customers

according to these objectives.

The bank takes into consideration the safety,

liquidity and productivity aspects when

assessing credit requests from corporate

customers. Banka Asya aims to spread the risk

and increase total productivity through customer

and industry segmentation.

Export focused growthBank Asya’s commercial banking practices

provides support to export operations, one of

the main driving forces of growth for Turkish

economy. Developing and emerging markets

will no doubt continue to increase export

opportunities in the coming days.

Bank Asya evolves its operations according

to this fact to remain as a dominant force in

the industry with expert technical personnel,

providing brokerage services for all foreign trade

transactions as well as offering technical service

and innovative foreign trade products.

Bank Asya will continue to offer the most

suitable banking product solutions to export

customers according to its concept of

supporting the producers through a wide variety

of products and professional portfolio teams as

well as effective and cutting-edge information

technology systems.

Profit and loss partnership projectsBank Asya pursues to offer project financing

to its customers by way of profit and loss

partnership projects which are one of the most

important instruments of participation banking.

The bank is currently working on various profit

and loss partnership projects which the Project

Financing Department is assessing and holding

meetings about. Bank Asya is planning to

venture into more projects in the construction,

energy, health, tourism and food industries in

the coming days.

Stable financial leasingFinancial lease transactions are available in

Bank Asya as the bank has previously provided

financing and leasing solutions to some of the

significant investments in Turkey.

Expert technical personnel in financial leasing

finalize customer request expeditiously and

smoothly. Bank Asya will continue to grow in

financial leasing transactions in 2013.

SME BANKINGBank Asya maintained its services for SMEs in

2012. The weight that SME customers hold

in the whole portfolio remained the same

in the 2012 operation period as the bank

provided support to these customers with

credits, cash management and consultancy

services.

Bank Asya completed organizational

structuring for SME Banking in its

Headquarters as well as in Districts and

Branches. Marketing organization was

changed by creating new Sales Coordination

Marketing and SME Product Development

Portfolio departments. SME Banking

operations are being carried out in three

District Offices in Istanbul as well as in the

ones located in Ankara, Izmir Bursa, Konya,

Gaziantep and Trabzon.

In 2012, Bank Asya once again stood

behind SME customers for all of their credit

requirements in their investments, projects,

capacity increase efforts and technological

innovation integrations, in addition to

business development projects to gain

a competitive edge and foreign trade

transactions. Direct Debiting System(DBS)

DBS continued catering to customers’ cash

management needs through Company Card,

Commercial Card, AsyaAssist Card, Checkbook,

POS, Tax, SSI, Bill Payments, Salary Payments,

Insurance and Internet Banking services.

This system allows main companies to

automatically collect the costs of goods

and products from their dealers or regular

customers. It was successfully implemented

in 2012 as well with conclusion of

agreements with 46 main customers and the

integration of 328 dealers with the system.

Bank Asya also provided a collection and

payment service through the Commercial

Card as an alternative to the DBS. The

card is another cash management product

that works through a close circuit system

between the wholesaler/main company and

retailer/dealer. As of 2012, the bank made

Commercial Card agreements with 57 main

companies and integrated 615 dealers to the

system.

In 2012, AsyaAssist Incentive Monitoring

module was launched by the AsyaAssist Card

which provides special assistance services to

business.

Incentive Monitoring system allows SMEs

to find out which incentive program they

can take advantage of according to the city,

district and industry.

They can also get updated information

regarding the programs and get answers to

their questions on the “www. cobanyildizim.

com” website. Incentive Monitoring system

gives quick access for SME costumers about

cost saving opportunities.

AsyaAssist Card extends assistance to

businesses for their medical, legal and

financial consultancy requirements as well

as for needs in emergency situations. The

number of customers taking advantage of

the card rose to 57,900 with a 35 percent

surge in 2012.

Bank Asya pressed on being a robust

participant of public supported projects aimed

for SMEs in 2012.

One of these was the Bank Asya and the

Credit Guarantee Fund (CGF) partner project

of providing credits to businesses which

lacked the guarantee. As of 2012, Bank Asya

extended CGF to 300 SMEs in the amount of

85 million Turkish lira, putting the bank in the

top four banks in the industry in this field.

Bank Asya will persistently make these types

of projects available to SMEs in 2013 as well.

The bank aims for completion and launch

of the SME & Commercial Segmentation

and SME Commercial CRM projects in 2013.

Bank Asya set its sight on displaying a

performance over the industry in SME

Banking. Similarly, it aspires to reach more

SMEs as their solution partner and to become

one the preferred banks by them in the

industry.

Bank Asya succeeded in ranking among the top four banks that extended the most Credit Guarantee Fund (CGF) in the whole banking industry by providing funding to 300 SMEs in the amount of 85 million Turkish lira in 2012.

41

Bank Asya Annual Report 201240

Retail Banking

Bank Asya is growing even more

through retail banking.

As of the end of 2012, there are 251 branches

offering retail banking services with 693

expert personnel. In addition to increases in

the number of branches and personnel, there

have been other significant developments

regarding retail customers. The number of Bank

Asya customers reached 3.9 million with an 18

percent rise.

Bank Asya completed three major retail

banking projects in 2012.

• CRM-Customer Focused Transformation

Project

• Personal Performance Management

• Real Customer Portfolio Management

CRM-Customer Focused Transformation

Project

Bank Asya transformed a product and process

focused organization into a customer-focused

one through the CRM project it initiated in 2010

and launched in January 2012. The project

has allowed the bank to develop a system of

grouping customers according to certain criteria

and enabling it to reach the right customers

through appropriate channels at advantageous

times to offer suitable products and services.

Bank Asya intended to establish a better

understanding of its customers through the

CRM Project. As such, the bank has made great

progress in the direction of developing the right

solutions for its customers by analyzing their

demands and needs.

The “CRM Project in 180 Days” is the last phase

of the great transformation initiative and it

earned Bank Asya the “Pega Financial Services

Customer Experience Award” in the PegaWORLD

2012 event which was held in Dallas on June

2012. The same project was also rewarded

for its technical and infrastructure works in the

“Information Technology Awards” organized by

the CIO Magazine on December 2012.

Retail financing products

Bank Asya strengthened its competitiveness

through housing finance and other financing

products it started offering in parallel with the

strategy of expanding the credit volume in

2012. The result was 29 percent growth in

retail credits compared to 2011.

The bank continued financing housing projects

throughout the year to drive housing credits up

by 32 percent year-on-year.

Private Pension and insurance

activities

Bank Asya remains adamant about providing

a high quality and fast service with a diverse

product range in the banking insurance

segment by closely studying customer needs

and industry trends, and also by taking into

consideration the bank’s risk approach.

The bank has complete infrastructure efforts

on its systems in 2012 so as to speed

up transaction time for insurance product

customers. Revenues from commissions

swelled by 40 percent as a result of the

system integration carried out by Işık Sigorta,

Bank Asya affiliate. With these endeavors,

Bank Asya elevated commission revenues

from insurance products and services over

the industry average.

Bank Asya entered into the Private Pension

System with its affiliate Asya Emeklilik

ve Hayat A.Ş. in May 2012. As the first

participation bank to offer interest free

pension services to customers, Bank Asya

was quickly rewarded for this effort with

the addition of 45,000 participants into

the Private Pension System through Asya

Emeklilik ve Hayat A.Ş.

Gold Banking

Bank Asya began physically acquiring gold in

2012. The bank physically collected four tons

of gold as of the end of the year, developing

into one of the major banks in the industry in

terms of gold accounts.

“Reception Day for Gold” activities held in

branches encouraged acquisition of scrap

gold and made a contribution the Turkish

economy.

Gold participation accounts with varying

maturity dates gave another opportunity

for customers to utilize their gold current

account savings as of May 2012.

Bank Asya began purchase and sale

transactions of physical gram gold bullion

bearing the bank’s logo in 2012.

Retail Customer Growth Trend (Pieces) Growth of Retail Financing Support (Million TL)

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

2008 2009 2010 2011 2012

2,000,000

2,420,000

3,307,000

3,725,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

2008 2009 2010 2011 2012

2,860,000

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

2008 2009 2010 2011 2012

2,000,000

2,420,000

3,307,000

3,725,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

2008 2009 2010 2011 2012

2,860,000

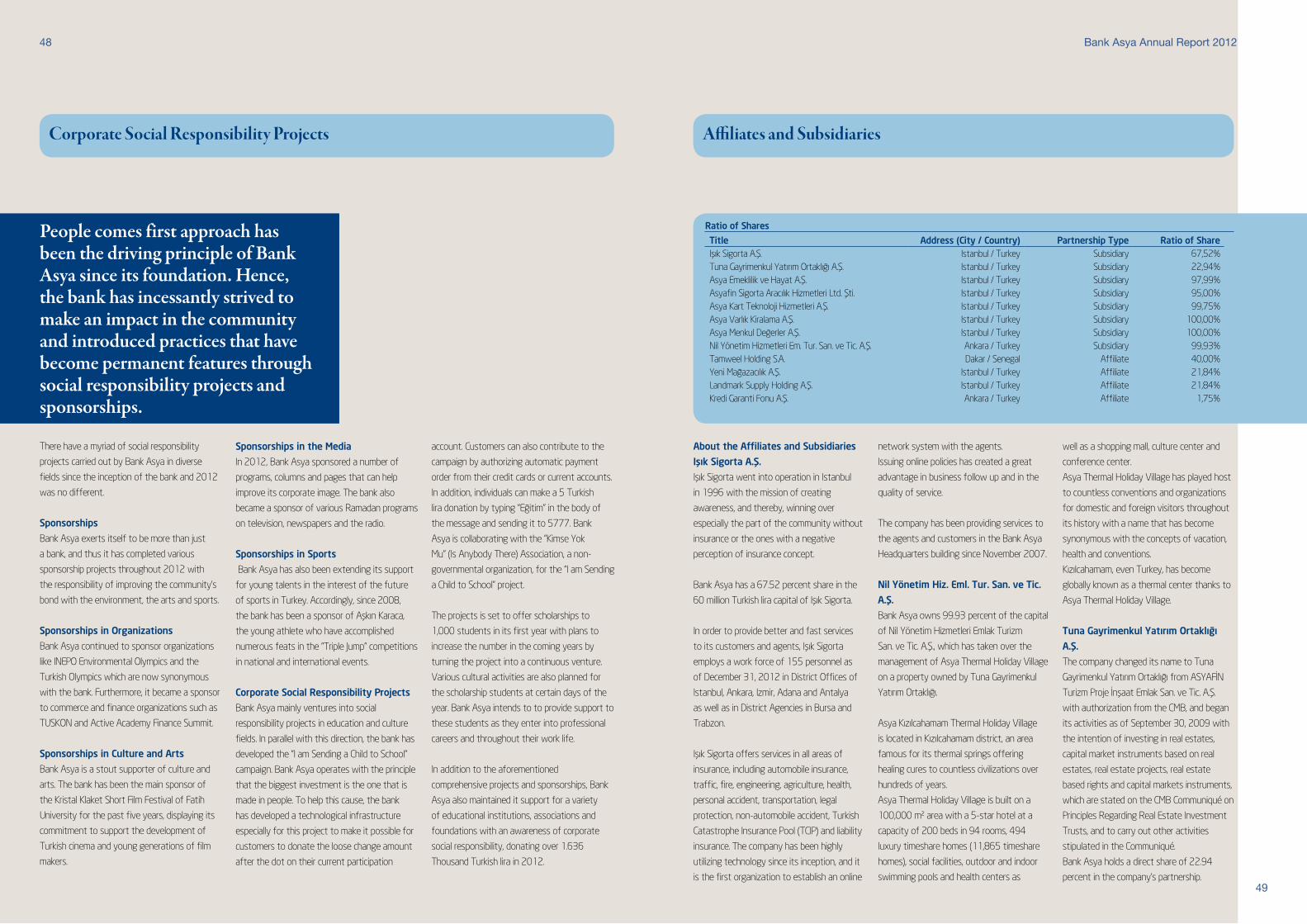

398 477

930

1.63

2.103

43

Bank Asya Annual Report 201242

Alternative Delivery Channels

Bank Asya grew even more effective in alternative

delivery channels in 2012. There were a number of

noteworthy projects completed in 2012 like the

launching of the second call center in Trabzon, call

center backup operation, CRM channel integration,