152

1 MIG Investor Day 22 May 2009 London 1

11

MIG Investor Day

22 May 2009London

1

22

Section 1Marfin Investment GroupGroup overviewFinancial highlights

MIG CompaniesVivartiaAtticaHygeiaSingularLogicOlympicMarfin Popular BankMIG Private EquityIntra-group synergies

Contents

2

33Group overview

Leading companies across key sectors

Food & Dairy

Healthcare

Transportation

IT & TelecomsFinancial Institutions

Private Equity

ATHEX listed with a market capitalisation of c.€2.5bn

Net Asset Value stands at a total of €4.075bn

Portfolio of leading companies in mainly defensivesectors across the SEE region

Diversified group with global presence

37% sales outside GreecePresence in 40 countriesMore than 22 business segments

Total workforce in excess of 50 thousand employees and associates

MIG Group Operating Performance

2008 Consolidated Revenues: €1,773m2008 EBITDA: €326.8m2008 Net Profit: €112.6m

MIG Parent:

€1,078m cash87% of investment portfolio in quoted instrumentsConstructive dividend proposed for 2009 of €0.20 per share

Highlights

3

44

4

U.S.A.

Egypt

ATLANTIC OCEAN

Malta

Guernsey

Cyprus

Mexico

SaudiArabia

Vivartia Hygeia MPB Singular HiltonKorasidisRKB Sunce FAI Attica

Nigeria

Australia

A group with a global footprint

NORTH SEA

MEDITERRANEAN SEA

PolandGermany

Italy

Turkey

Ukraine

Romania

Bulgaria

Russia

Montenegro

Croatia BLACK SEA

Estonia

Serbia

Albania

Greece

4

55

MIG continuously enhances its sectoral and geographical diversification

A diversified group

Portfolio companies by sector

Production sector: Dairy & Beverages, Bakery & confections andFrozen Foods activities.Real Estate sector: investment property activities in Serbia andGreece.Service Sector: Food services, Transportation, Hotel & Leisure,Healthcare, Financial Inst, IT & TelBreakdown as per Group’s Gross Asset Value

Group sales by geography

Group Sales include only fully consolidated companies:Vivartia, Attica, Hilton and RKB (during 2008 RKB portfolioassets were under refurbishment, therefore no material incomehas been generated)

Rest of the world 11%

€ 3,348.8m € 1,773.0m

5

66A diversified group (cont’d)

MIG’s current portfolio consists of leading companies in their sectors across SEE

Portfolio companies by industry (a),(b)

(a) MIG’s gross asset value, amounted to €3,348.8m

(b) MIG portfolio is classified in 5 core businesses & private equity

(c) Vivartia breakdown in 4 business lines according to averageEBITDA of years 2009 to 2013 (as per the latest business plan)

Private equity by industry (d),(e)

€ 3,348.8m € 386.2m

(d) Breakdown as per Group’s Gross Asset Value

(e) The Private equity Sector includes : MIG Leisure, RKB Serbia,MIG Leisure & Real Estate Croatia, MIG Real Estate &Anakon/Theros

Entertainment 15%

6

7MIG group structure

Main controlling interest in subsidiaries & associates

Sector Cons. Method Current stake

Vivartia Food and Dairy Full 90.3%

Attica Transportation Full 86.8%

Hilton Private Equity: Hospitality Full 75.1%

MIG Real Estate Private Equity: Real Estate Equity 50.0%

JSC Robne Kuce Beograd Private Equity: Real Estate Full 66.7%

Sunce Bluesun Private Equity: Hospitality Equity 49.9%

Singular Logic IT & Telecom Equity 31.2%

FAI Flight Ambulance Private Equity: Flight Ambulance Equity 49.9%

Minority Interests - Non consolidated companies

MPB Financial Institutions None 9.7%

Hygeia Healthcare None 33.3%

7

88

Section 1Financial highlights

Section 2

8

99Key financials - Profit & Loss

20082007

pro forma2007

reported

Sales 1,773 1,444 604

EBITDA 327 191 34

Profit after tax from continuing operations 184 182 69

Profits after tax from discontinued operations 0 268 268

Net profit for the period 184 450 337

Net profit after minorities from continuing operations 113 126 62

Basic EPS from continuing operations (in €) 0.15 - 0.16

Group income statement (€m)

20082007

reported

Operating income 173 394

Net operating income 116 348

Net profit for the period 77 278

Basic EPS (in €) 0.10 0.70

Group income statement (after minorities)Contribution by unit (€m)

20082007

pro forma

Net income from Holding & consolidation adjustments 76 43

Net income from Operational units (production & services sectors) 57 69

Net income from Real estate units 87

Gains (losses) from revaluation of investment portfolio (107) 14

Net profit after minorities from continuing operations 113 126

Consolidated sales presented a robust increase of 23% vs pro forma sales of 2007

Consolidated EBITDA posted a substantial uplift of 71% compared to pro forma respective figures of 2007, whereas EBITDA margin soared by 520 bps from 13.2% in 2007 pro forma to 18.4% in 2008

Basic EPS stood at €0.15 at a consolidated basis compared to €0.16 in 2007 as reported

Company income statement (€m)

2007 company’s net profit includes €242m extraordinary income from the disposal of banking assets

9

1010Key financials – Balance sheet

2008 2007

Goodwill 1,383 1,086

Fixed & intangible assets 2,660 2,345

Investment & trading portfolio 1,328 3,718

Other assets 741 973

Cash & Cash Equivalents 1,509 1,508

Total Assets 7,621 9,631

Long term debt 1,509 1,013

Short term debt 755 2,358

Other liabilities 832 758

Shareholder’s funds 4,155 4,945

Minority interests 369 556

Total Equity & Liabilities 7,621 9,631

Group balance sheet (€m)

Net debt 755 1,864

Net debt / equity 17% 34%

Net debt / total assets 10% 19%

Equity / total assets 59% 57%

2008 2007

Total investments (Gross Asset Value) 3,349 5,916

Other assets 229 170

Cash & Cash Equivalents 1,078 1,189

Total Assets 4,656 7,275

Long term debt 0 0

Short term debt 516 2,148

Other liabilities 66 186

Shareholder’s funds 4,074 4,941

Total Equity & Liabilities 4,656 7,275

Company balance sheet (€m)

Net debt/(cash) (563) 960

Net debt / equity (14%) 19%

Net debt / total Investments (17%) 16%

Equity / total investments 122% 84%

The €2bn decrease in total assets relates to thedisposal of the stake in OTE

Debt has been reduced by €1,633m to €516m due to the reimbursement of loans for the financing of the investment in OTE.A highly liquid balance sheet with Net Cash of €563m

10

1111Strong liquidity at group level

Net debt evolution at group level

Cash breakdown Debt breakdown

Amidst adverse market conditions, MIG has significantly reduced its net debt position at a group level while all portfolio companies maintain healthy balance sheet structures and strong cash positions

€1,509m

€2,264m

11

1212Net asset value

NAV composition 31 December 2008

€ 4,074m

Portfolio companies

82%

Net Cash14%

Working capital

4%

NAV bridge between Dec-07 & Dec-08

Strong Balance Sheet: Cash rich and healthy net debt levels

The company has maintained a very strong cash position of €1,078m and a healthy net cash that accounts for 14% of the NAV

As of 31 Dec 2008 the NAV per share stands at €5.45 compared to €6.59 the year before

(1,885)

(691)

12

1313

Section 1MIG companies

Marfin Investment Group

13

1414

Section 1

Vivartia

Section 3

14

1515Vivartia

The largest food company in the SEE region, operating under four divisions:

Dairy, Bakery, Food Services & Frozen Foods

Date of Investment: July 2007MIG Ownership: 90.3%Vivartia is the largest food company in South-East Europe, with #1 market positions in each of its core business lines, and #1 or #2 market shares in key products under each division, selling 3,5 billion units of product every yearDairy & Beverages: #1 Milk in Greece, Cyprus and Bulgaria; #1 Yoghurt in Cyprus; #2 Yoghurt in Greece and Bulgaria; #1 Fresh Juice in GreeceBakery: #1 Pastry in Greece, Bulgaria, Romania, Poland and Hungary; #1 Biscotti, #1 Bagel Chip, #1 Melba Toast and #2 Pita Chip in the USAFoodservice & Entertainment: #1 QSR, #1 Branded Coffee Shops and #1 Catering in GreeceFrozen Foods: #1 Frozen Vegetable and #1 Frozen Pastry in GreeceVivartia distributes to over 35 countries worldwide, and has joint ventures with leading players in several key growth markets outside of Greece, including PepsiCo in Mexico, Leventis Group (Coca Cola) in Nigeria, Almarai in Saudi Arabia and the Berzi Family in Egypt Vivartia is headquartered in Athens, operates 35 factories worldwide (30 fully-owned and 5 through joint venture agreements), with over 450,000m2 of owned buildings and over 1,300,000m2 of owned land

Company profile

Financial highlights (€m)

Net profit +21%28.1EBITDA +21%126.6Sales +28%1,118.7

Total equityNet Debt 390.5 +85%

2007 2008 Growth

1,437.2153.5

34.2692.4 683.4 -1%

722.0

15

1616Vivartia – At a glance

Strategic & operational highlights of the yearKey Events of 2008

Completion of the operational and legal merger of the two subsidiaries in Cyprus (Charalambides Dairies & Christis Dairies)Acquisition of Nonni’s (US) in April 2008 (Bakery Division)Acquisition of Everest & Olympic Catering completed in June 2008 (Food Services & Entertainment Division)UMC (Bulgarian subsidiary) was fully consolidated in 2008 (partial consolidation as of July 1st , 2007) – Dairy Division

Year 2008 PerformanceGroup sales increased by 28.5% over last year. The increase was driven by healthy organic growth of 7.2%, first time partial consolidation of Nonni’s, Everest and Olympic Catering, and first-time full year consolidation of the subsidiary in Cyprus, Christis DairiesThe third and fourth quarters of 2008 presented significant improvement in profitability versus the corresponding quarters of 2007, and the first two quarters of 2008EBITDA increased by 21.2% over last year mainly enhanced by the increase of Bakery & Entertainment divisions EBITDA and consolidation of the recent acquisitions The Group’s EBITDA margin decreased by 64 bps to 10.7% amidst an unprecedented rise in commodity prices in 2008 and a significant slowdown in the second half of 2008 in the US and CEEDespite the adverse environment, FY2008 results were less than 2% below the 5-year business plan targets in terms of revenues and less than 1% below in terms of EBITDA while net earnings were 93% higher than those projected

Recent DevelopmentsOn 26 March 2009, Vivartia announced the reorganization of the Company into four subsidiaries through the separation of divisions. This separation will enhance the management of activities by division due to the increased volume of operations and significant international expansion while, on the other hand, it provides each new company with greater flexibility in formulating its strategy and pursuing strategic initiatives and co-operations

16

1717Vivartia – Key financials & guidance

Recent actual financials and five-year guidance

€m2007

Actual

2008(5 yr

Guidance)2008

Actual2009

Guidance2010

Guidance2011

Guidance2012

Guidance2013

GuidanceCAGR’08-’13

Sales 1,119 1,458 1,437 1,731 1,909 2,136 2,403 2,672 13%

EBITDA 127 155 154 186 208 256 303 332 17%

EAT 28 27 34 46 58 91 119 139 32%

EPS 0.13 0.08 0.15 0.26 0.40 0.85 1.16 1.36 55%

17

Despite the adverse environment, FY2008 results were less than 2% below the 5-year business plan targets in terms of revenues and less than 1% below in terms of EBITDA while net earnings were 93% higher than those projected

1818Vivartia – Current economic climate

Vivartia is well-prepared for any conditions arising from the current economic climate

It is our expectation that on an average basis, volumes will lag 2008 levels by around 5% - 7%

However, we do not expect any material adverse effects on profitability due to the following circumstances:

Extraordinary increases in the prices of raw materials in late 2007 & 2008 forced us to correspondingly increase consumer prices in 2008; in 2009 we are taking advantage of these adjusted consumer prices and the dramatically lower raw material pricesTimely and prudent internal cost cutting initiatives

18

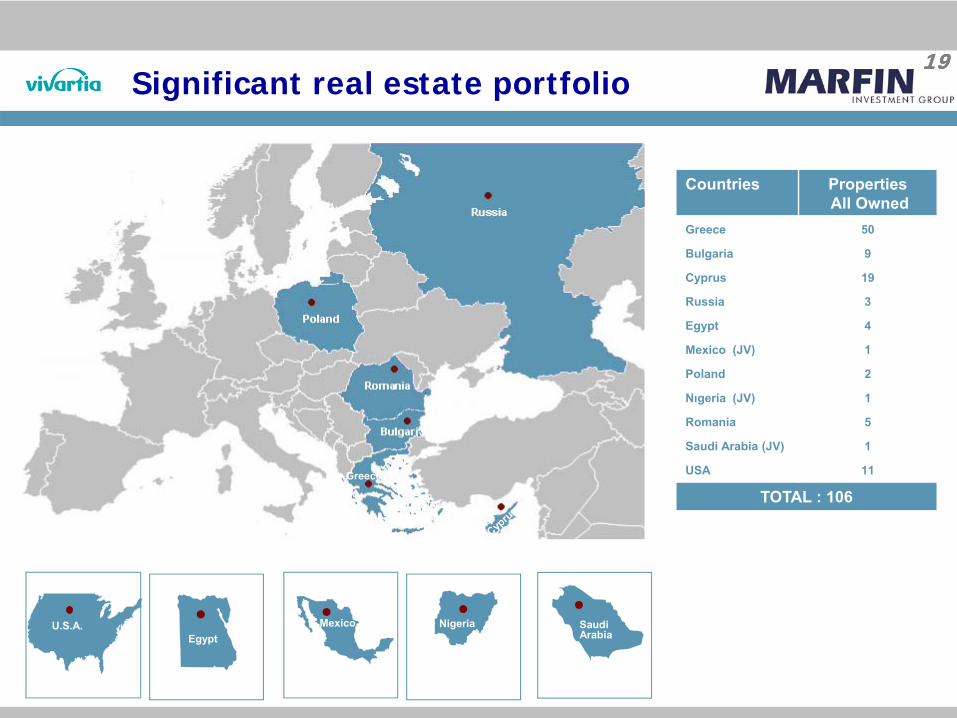

1919

U.S.A.Egypt

Mexico SaudiArabia

Nigeria

Countries PropertiesAll Owned

Greece 50

Bulgaria 9

Cyprus 19

Russia 3

Egypt 4

Mexico (JV) 1

Poland 2

Νιgeria (JV) 1

Romania 5

Saudi Arabia (JV) 1

USA 11

TOTAL : 106

Significant real estate portfolio

GreeceGreeceGreeceGreece

19

2020Production sites excluding Bakery & Confectionary

Bulgaria Cyprus

Imathias

Thessaloniki

Larissas

ViotiasAttikis

Factory locations Ownership Production activity Food & Beverages Division

Food Services & Entertainment

Frozen Foods

20

2121Dairy - Introduction

The Dairy Division has a market-leadership strategy which is based on:

Strong umbrella & individual brandsEffective commercial distributionEfficient industrial setup

Strong umbrella brand: the Delta brand, with its daily exposure to a large number of consumers through milk consumption, is an umbrella brand complemented by successful sub-brands to create a product portfolio with both high-volume commodity products and high margin value-added productsExtensive distribution network: the division has a very strong position in the trade due to its leadership position in many product lines. It has the largest chilled distribution network in Greece, with daily visits to most of the stores which sell dairy productsCompetitive R&D and industrial operations: the division has a strong R&D department to support product innovation and manufacturing operations that follow the strictest quality standards and are conveniently located close to the end-market

Competitive advantages and strategy Dairy & Beverages strategy

Market Leadership

Competitive R&D / Industrial Operations

21

2222Dairy – Main product categories

The main product categories are milk, fresh dairy products, chilled fresh juices and cheeses

In Milk, a wide range of products is offered, covering all types of white (fresh, HP, UHT, evapore) and chocolate milk

In Fresh Dairy Products, Vivartia offers not only white and flavored yogurts, but also products catering to specific consumer needs (i.e. functional and children’s yoghurts)

In Beverages/Chilled Juices, Vivartia offers a diverse range of flavors

In Cheeses, Vivartia offers branded and non-branded feta, halloumi, and cream cheeses

The Dairy business includes 4 main categories

• Fresh milk• HP• UHT• Chocolate

flavored• Condensed• Children’s

milk

Dairy & Beverages products

Milk

Fresh dairy products Beverages

Milk

Beverages

Fresh Dairy Products• White yogurt• Fruits &

cereals yogurt• Children’s

yogurt• Functional• Desserts

• Chilled juices

Cheeses• Cheese (feta,

halloumi, cream)

Cheeses

22

2323Dairy – Leading market positions

Vivartia enjoys leading market shares across all its dairy product-lines

Country Category Market shares(rank)

Greece White milk 26.7% (#1)

Greece Choco milk 55.6% (#1)

Greece Yogurt 19.2% (#2)

Greece Chilled Juices 60.2% (#1)

Cyprus White milk 62.3% (#1)

Cyprus Choco milk 81.8% (#1)

Cyprus Yoghurt 33.0% (#1)

Bulgaria Yoghurt 10.5% (#2)

Bulgaria Choco milk 82.0% (#1)

Bulgaria White milk 46.7% (#1)

Dairy & Beverages brands and sub-brands

Greece

BulgariaCyprus

23

Source: Nielsen

2424Dairy – Production network

Vivartia has an extensive production network of 8 Dairy factories across SEE

The Dairy division has operations in Greece (Delta)Cyprus (Vivartia Cyprus) and Bulgaria (United Milk Company)

The production footprint network is located close to densely populated areas, which ensures low cost and timely service of the market

Location Ownership Production activity

Ag Stefanos, Greece Owned Yogurt

Tavros, Greece Owned Milk & Juices

Sindos, Greece Owned Milk

Imathia Platy, Greece Owned Evapore

Ellasona, Greece Owned Feta cheese

Eurofeed, Greece Owned Animal feed

Limassol, Cyprus Owned All Dairy products

Plovdiv, Bulgaria Owned All Dairy products

Map of production plants

Ag.Stefanos(Athens)

Delta, fresh, HP & chocolate milk

Eurofeed, animal feed

Delta, yoghurt , desserts

Delta, fresh & chocolate milk, chilled juices

Sindos

Delta,condensed milk

Tavros(Athens)

Imathia

Vigla

UMC, fresh, UHT, flavored milk,

yoghurt, cheeseGreece

Bulgaria

Cyprus

LimasolChristis, fresh & UHT milk yoghurt , cheese

Delta,feta cheese

Plovdiv

24

2525Bakery – Introduction

Competitive advantages & strategy

Bakery’s market leadership strategy is based on Uniqueness of productsSize of operations Continued successful geographical expansion

Uniqueness of products: Unique long shelf life croissant products in a continuously expanding portfolio, supported by unparalleled brand equity in most of the countries of presence

Size of operations: 35 production lines all over the world, providing unique advantage to retailers

Continued successful geographical expansion:after the initial successful expansion into Central/Eastern Europe, Bakery expanded into broader geographies, such as the US, Nigeria and Saudi Arabia through acquisitions and joint ventures

Bakery & Confectionary strategy

Size of operations

Uniqueness of products

Continued successful geographical expansion

#1

25

2626Bakery – Main product categories

The Soft Dough products portfolio consists of: Croissants (single & mini)Cakes (Swiss rolls, cake bars, madalenas), and Other niche products (strudel, mini strudel, tsoureki & treccina)

The Savory products portfolio includes:Bake rolls, and Pita bakes (based on Arabic pita)

From the recent acquisition of Nonni’s, these product categories are further enriched with biscotti and other specialty baked goods

The Bakery business includes 2 main product categories

Bakery products

Soft dough products Savory products

Nonni’s sweet and savory products

26

2727Bakery – Leading market positions

Vivartia enjoys #1 market shares across all its bakery product-lines

Country Category Market shares(rank)

Greece Pastry 80.0% (#1)

Romania Croissant 77.1% (#1)

Romania Bread snacks 70.8% (#1)

Bulgaria Croissant 88.1% (#1)

Bulgaria Bake rolls 91.7% (#1)

Poland Croissant 94.7% (#1)

Russia Croissant 78.5% (#1)

Egypt Cakes 81.0% (#1)

USA Biscotti 68.0% (#1)

Bakery & Confectionary brands

27

Source: Nielsen

2828Bakery – Production network

Vivartia has an extensive production network of 17 Bakery factories across SEE

The Bakery divsion has 17 manufacturing plants in Greece and abroad (Bulgaria, Romania, Poland, Russia, Egypt, USA, Mexico, Nigeria, Saudi Arabia)12 of the 17 plants are company owned while the other 5 are joint ventures in Egypt, Saudi Arabia, Mexico & Nigeria

Production & DistributionBulgaria EgyptGreeceMexico (*)Nigeria(*) (**)Poland RomaniaRussiaSaudi Arabia (*) (**)U.S.A.

DistributionCzech Republic (***)Germany Hungary (***)ItalySlovakia (***)Ukraine (***)

ExportsAlbania (***)AustraliaAustria Belarus (***)Bosnia (***)CanadaCroatia (***)FYROM (***)KazakhstanLebanon (***)Malta (***)Moldova (***)Serbia (***)Montenegro (***)Slovenia (***)

(*) Joint Ventures / Companies with Vivartia minority stakes (**) Start-ups, 1st quarter 2009(***) Countries with advertising support and high brand awareness

Vivartia factories

Owned plants

Joint ventures plants

Joint ventures

• The plants in Egypt (Cairo) and Saudi Arabia (Jeddah) produce croissants and cakes

• The plants in Mexico (Mexico City) and Nigeria (Abuja) produce croissants

Owned plants

• The manufacturing plant in Greece is located in Lamia and makes croissants, bake rolls, pita bakes, rusks, tsoureki, potato chips and extruded snacks

• The plant in Bulgaria is located in Sofia and produces croissants and bake rolls

• The plant in Romania is located in Bucharest and produces croissants, cakes, Swiss rolls and Creamlineproducts

• The plant in Poland is located in Tomasov (100km from Warsaw) and produces exclusively croissants

• The plant in Russia is located in St. Petersburg Producing croissants, cakes, Swiss rolls, mini rolls, magdalena and flan cakes

• There are 6 plants in the US. Biscotti products are made in Tulsa (OK) and Ferndale (NY), bagel chips in Bronx (NY) and South Dayton (NJ) and crackers are made in Knoxville (TN) and Willingboro (NJ)

28

2929Product categories – Bakery & Confectionary

* Production to start by the end of the first quarter 2009

USA facilities: - Owned: Ferndale NY, Willingboro NJ, Knoxville TN - Leased: Bronx NY, Dayton NJ, Tulsa OK

1. CroissantsSingleMini

2. Cakes

COUNTRIES GREECE BULGARIA ROMANIA POLAND RUSSIA USA (6 facilities) MEXICO(JV) EGYPT (JV) NIGERIA (JV)* SAUDI ARABIA (JV)*

BAKERY & CONFECTIONARY DIVISION

PRODUCT CATEGORIES PRODUCED PER COUNTRY

CA

TEGO

RIES

1. CroissantsSingleMiniStrudelSingleSingle chocolate enrobed

2. Bake RollsBake RollsMini Bake Rolls

3. Pita Bakes

4. Rusks

5. Tsoureki

6. Potato Chips

7. Extruded Snacks

1. CroissantsSingleMiniStrudel

2. Bake RollsBake Rolls

1. CroissantsSingleMiniSingle chocolateTreccinaMini Strudel

2. CakesCake Bars

3. Swiss Rolls

4. Cream LineHazelnut PralineWaffers

1. CroissantsSingleMini

1. CroissantsSingleMiniMini Strudel

2. CakesCake Bars

3. Swiss RollsChocolate enrobed Swiss Rolls

4. Mini RollsChocolate enrobed Mini Rolls

5. Magdalena

6. Flan Cakes

1. Biscotti

2. Bagel Chips

3. Crackers

4. Bread Crumbs

1. CroissantsMini

1. CroissantsSingleMini

2. Cakes

1. CroissantsSingle

29

3030Food Services & Entertainment – Introduction

Competitive advantages & strategy

Goody’s has built its success both in casual restaurants and coffee shops through employment of a fully integrated approach that allows a strict quality control and flexibility in the design of the menu

This has trained the Greek consumers to value and be extremely loyal to a consistent and higher standard than the one offered by the international chains

The recent acquisition of Everest has reinforced the leadership position and the overall potential of the division, as it has added to the Group both a leading brand in snack bars, as well as other successful concepts (La Pasteria) that have potential for further growth

Food and Entertainment strategy

(2001)

Integrated approach, quality control and flexibility in menu design

Has set a high standard for “casual dining” in the Greek market

Good and healthy foodSuperior service

(2008)

Leader in snack bars and the “on the go” market

30

3131Food Services & Entertainment – Main brands

The FS&E division has brands that satisfy a wide range of consumer dining needs

Goody’s, for fast casual dining both for lunch and dinner both on premises and recently available through delivery Flocafé, for good quality coffee and gourmet dishes in a nice ambiance from mid-morning on, for on-premises consumption Everest, for quick snacks and coffee on the go, throughout the day, for consumption both on and off premises

La Pasteria, for casual Italian diningFS&E is also active in the B2B food service through four subsidiaries:

Hellenic Catering supplies the Goody’s & Flocafe outlets and the HoReCa channel Select is a producer of bakery goods available to Goody’s, Flocafé and the HoReCa channelGreenfood produces the salads sold at the Group’s retail stores, and also sold to the organised tradeOlympic Catering offers products to the airlines for their in-flight catering and operates canteens in the airports

The FS&E business includes 8 brands FS&E service categories

31

3232Food Services & Ent – Leading market positions

Goody’s, Flocafé, and Everest are strong, recognised market leaders

Food service market

Coffee service market

Stores & System sales

2008

Goody’s # of stores 181

Flocafe # of stores 84

Everest # of stores 226

La Pasteria # of stores 21

Papagalino # of stores 19

Kuzina # of stores 2

TOTAL 533

€m 2008

Goody’s System Sales 220

Flocafe System Sales 60

Everest System Sales 125

La Pasteria System Sales 20

Other System Sales 8

TOTAL 433

32

Total Vivartia market share22.3%

Total Vivartia market share16.5%

11.1%

5.4%

5.6%

11.4%

66.5%

Flocafe Everest Starbucks Other Branded Unbranded Café

16.3%

6.0%

1.5%

5.5%

70.7%

Goody'S Everest Mc Donalds Other Branded Unbranded

3333Frozen Foods – Introduction

Competitive advantages & strategy

The Frozen Foods division has a strong competitive advantage as a result of effective brand management as well as a high quality product offering that have yielded a leadership market position that is difficult for new entrants to compete against

The division also holds a leadership position in the fragmented frozen dough market

Market leadership and scale have resulted in a cost competitive advantage

Frozen Food strategy

High brand equityStrong commercial

push in a fragmented market

Market leadership and scale

Cost advantage

Competitive advantage

Vegetables Dough

33

3434Frozen Foods – Main product categories

Basic frozen vegetables, and frozen meals sold under the Barba Stathis brand; holds a 65% market share

Frozen dough products, sold under Chrysi Zymi to retail stores (25% market share), and Elliniki Zymiproducts sold to the HoReCa channel

Fresh salads, sold under the Barba Stathis brand

The Frozen Foods business includes of 4 main product categories

Frozen Foods products

Dough products

Frozen vegetables Frozen meals

Fresh salads

34

3535Frozen Foods – Production network

Vivartia has an extensive production network of 4 Frozen Foods factories across SEE

Location Ownership Production activity

Sindos, Greece Owned Frozen vegetables

Sindos, Greece Owned Frozen dough

Plovdiv, Bulgaria Owned Frozen vegetables

Larissa, Greece Owned Marmalades

Frozen Foods factories

Sindos• Barba Stathis,

frozen vegetables• Arabatzis,

frozen doughLarissa

• Viomar,marmalades

Greece

Bulgaria

Plovdiv

• Barba Stathis,frozen vegetables

35

3636

Section 1

Attica Group

Section 4

36

3737Transportation sector - Attica

No 1 passenger ferry operator in the Eastern Mediterranean

Date of Investment : October 2007 MIG Ownership : 86.8%No 1 passenger ferry operator in the Eastern Mediterranean, owner of 100% of Superfast Ferries (the leading ferry operator in the Adriatic sea) and 100% of Blue Star (the leading ferry operator in Aegean sea)The Group’s vessels (13 in total) operate in domestic and international waters, offering connections between Greece and Italy in the Adriatic Sea (5 vessels), and between mainland Greece, the Cycladic and Dodecanese islands, and Crete (8 vessels). The Piraeus - Crete route started on 12th

March 2009The current market value of the fleet, net of all debt obligations stands at €442.1m while the average age of vessels is 11 years (7.2 year excluding the 3 older vessels of the group)

Youngest fleet in the domestic market

Attica Volumes for year 2008:

During the year the company carried 4m passengers, 275k freight units and 583k private vehicles

Company profile

Financial highlights (€m)

Fuel cost adjustment (a) n/m-EBITDA -31%69.6Sales +3%316.3

EBITDA (like-for-like) (b)

Reported net profit 61.7 -64%

2007 2008 Growth325.9

47.728.6

69.6 76.3 +10%22.3

Recurring net profit 21.7 -42%12.6Recurring net profit (like-for-like) (b) 21.7 +90%41.2Total equity 506.1 -1%502.8Net Debt 250.9 +10%276.4(a) Assuming fuel costs at the 2007 levels(b) Adding the fuel cost adjustment

37

3838Attica Group

Through its subsidiaries Superfast Ferries and Blue Star Ferries, Attica Group owns and operates modern and fast cruise-class and car-passenger ferriesAttica provides year-round transportation services to passengers, private vehicles and freight in the Adriatic Sea as well as in the Greek domestic market

38

3939Group corporate structure

As a result of a Mandatory Public Offer completed on 2nd January 2008, MIG and its subsidiaries own 86.8% of Attica GroupFollowing a triple merger completed in December 2008, Superfast Ferries and Blue Star Ferries are 100% owned by Attica Holdings S.A.As a result of the merger by absorption, Blue Star Maritime S.A. was delisted from the Athens Exchange in December 2008

100% owned 100% owned

Listed on the Athens Exchange Market capitalisation: €325m

39

4040Leading operator in the domestic market

Market shares 2008(a)

Passengers Freight units Private vehicles

(a) The market shares are derived from statistical data of the Greek Port Authorities

40

4141The fleet

Superfast Ferries 5 ships, all built after 20014 operate between Greece – Italy1 operates in the Piraeus – Heraklion, Crete route since 12th March, 2009

The newly built Superfast I, acquired in October 2008, operates in the Patras – Igoumenitsa - Bari routeSuperfast II will be delivered Autumn 2009 and will operate in the same route as Superfast I

Blue Star Ferries8 ships, of which 5 built after 20007 operate in the Greek Islands 1 operates between Greece – ItalyA successful turnaround story of an acquired and rebranded competitor

41

4242

* This figure was limited to 804 by the Greek law

Fleet specifications

Vessel Built Rebuilt Length overall (meters)

Speed (knots)

Passengers Berths / Air seats

Private vehicles

Freight units / Lane meters

Superfast I 2008 - 199.14 24.0 950* 374 / 118 100 140 / 2,505

Superfast V 2001 - 203.9 28.3 1,595 842 / 90 90 110 / 1,920

Superfast VI 2001 - 203.9 28.3 1,595 842 / 90 90 110 / 1,920

Superfast XI 2002 - 199.9 29.1 1,639 710 / 46 90 110 / 1,915

Superfast XII 2002 - 199.9 29.1 1,639 710 / 46 90 110 / 1,915

Blue Star Paros 2002 - 124.2 24.4 1,475 104 / 378 48 21 / 360

Blue Star Naxos 2002 - 124.2 24.4 1,473 104 / 378 48 21 / 360

Blue Star 1 2000 - 176.1 28.0 1,802 458 / 179 100 100 / 1,718

Blue Star 2 2000 - 176.1 28.0 1,890 430 / 349 100 100 / 1,718

Blue Star Ithaki 2000 - 123.8 24.1 1,313 22/275 126 21 / 360

Diagoras 1990 2001 141.5 21.0 1,468 424 / 236 75 50 / 625

Blue Horizon 1987 1999 187.1 22.5 1,510 582 / 119 67 110 / 1,850

Superferry II 1974 1992 121.7 19.5 1,530 70 / 330 130 24(12m)+ 4(10m) / 346

Superfast Ferries: Average fleet age 6 years - Blue Star Ferries: Average fleet age 15 years

The most modern fleet in the domestic market42

4343The routes

Greece - Italy

Superfast I (since October 08)

Superfast V

Superfast VI

Superfast XI

Blue Horizon

Scotland-Belgium

Blue Star 1 (discontinued Sept 08)

Cyclades

Blue Star Ithaki

Blue Star Paros

Blue Star Naxos

Superferry II

Dodecanese

Blue Star 2

Diagoras

Blue Star 1 (since October 08)

Crete

Superfast XII (since March 09)

International routes Greek Island routes

43

4444Recent corporate activity

Strategic & operational highlights of the year

In February of 2008, Attica’s shares were converted from bearer to nominalFour RoRo vessels were sold at a profit of €9.7m, resulting in a cash surplus of €24m for the 1st quarter 2008Triple merger of Attica Group with Superfast Ferries Maritime and Blue Star Maritime (now delisted) completedAcquisition of two new RoPax vessels (Superfast I and Superfast II), for €156m in June 2008, deliveries in October 2008 and Autumn 2009Discontinuation of the North Sea route, with rerouting of Blue Star 1 to the Piraeus-Dodekanese route from September 2008Financing arranged for Superfast I (€48m at 135bp spread, 40% equity) – September 2008Delivery of Superfast I and deployment in the Bari route – October 2008Decision to reroute Superfast XII to Piraeus-Heraklion route – December 2008; service commenced on 12th March 2009

44

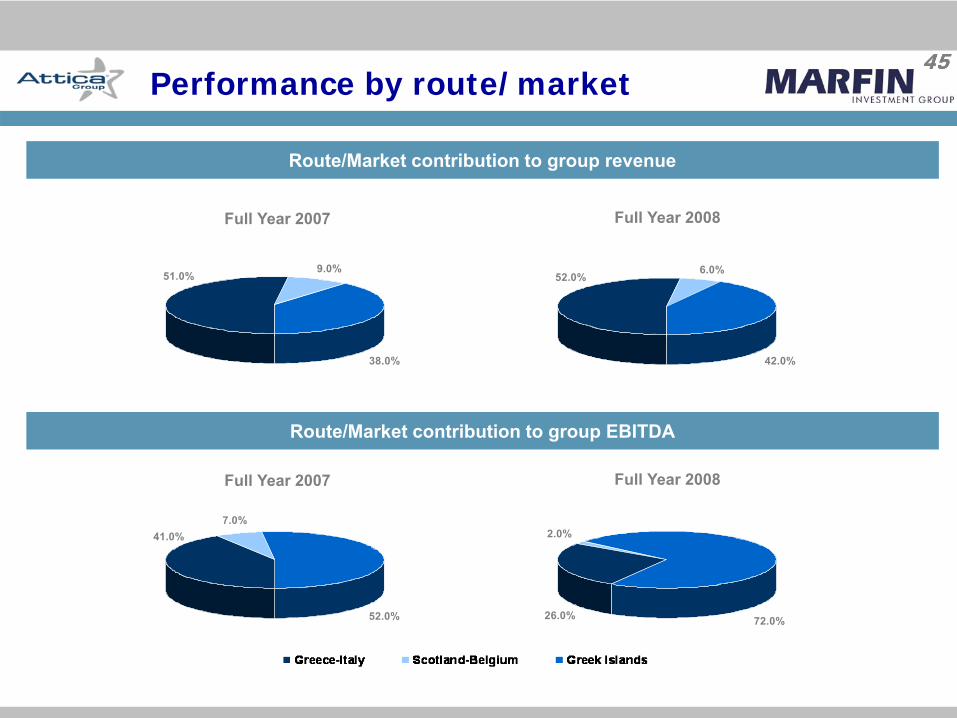

4545Performance by route/market

Route/Market contribution to group revenue

Route/Market contribution to group EBITDA

38.0%

9.0%51.0%

Full Year 2007 Full Year 2008

42.0%

6.0%52.0%

52.0%

7.0%41.0%

72.0%

2.0%

26.0%

Full Year 2007 Full Year 2008

45

4646Revenue/Cost breakdown

Attica Group revenue breakdown per traffic segment – FY 2007

Attica Group revenue breakdown per traffic segment – FY 2008

51.0%14.0%

35.0%

International Routes

22.0%8.0%

70.0%

Greek Islands Routes

36.0%

13.0%51.0%

71.0%

7.0%

22.0%

International Routes Greek Islands Routes

46

4747Revenue/Cost breakdown (cont’d)

Attica Group cost structure, as a share of operating expenses

Attica Group cost structure, as a share of revenue

12.0%

6.0%2.0%

12.0%

8.0%

24.0%

48.0%

Full Year 2007 Full Year 2008

9.0%

6.0%2.0%

10.0%

7.0%

18.0%

50.0%

7.0%

3.0%

1.0%8.0%

6.0%

14.0%

31.0%

6.0%

3.0%

1.0%8.0%

5.0%

14.0%

30.0%

47

4848Market: Greece – Italy

Full year 2008 traffic data

Passengers: 717,09333.2% Market Share - Rank: 1st

FY07: 727,742 passengers33.6% market share, rank: 1st

Freight units: 148,93030.2% Market Share - Rank: 1st

FY07: 141,339 freight units 30.9% market share, rank: 1st

Private vehicles: 137,310 27.2% Market Share - Rank: 2nd

FY07: 141,404 private vehicles 27.9% market share, rank: 2nd

Volumes and corresponding market shares for Attica are Superfast and Blue Star Ferries aggregates

Market shares data as per Greek Port Authorities and Attica data

13.1%

9.1%

21.3%23.3%

33.2%

22.2%

12.5%

17.6%17.4%

30.2%

10.2%8.1%

25.5%

29.0%

27.2%

Passengers

Freight Units

Private Vehicles

48

4949Market: Greece – Italy (cont’d)

Monthly load and revenue figures

Full Year 2007 Monthly average passengers and freight units

Monthly passenger/car and freight revenue4 Superfast and 1 Blue Star ferries

Monthly passenger/car and freight revenue4 Superfast and 1 Blue Star ferries

0

20

40

60

80

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec01002003004005006007008009001,000

Freight Units Passengers

0

20

40

60

80

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec01002003004005006007008009001,000

Freight Units Passengers

02,0004,0006,0008,000

10,00012,00014,00016,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Freight Revenue Passenger / Car Revenue

02,0004,0006,0008,000

10,00012,00014,00016,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Freight Revenue Passenger / Car Revenue

49

Full Year 2008 Monthly average passengers and freight units

5050Market: Greek Islands

Full year 2008 traffic data – Cycladic Islands (Santorini, Mykonos, Paros)

Attica operates 4 ships (avg. age 13 yrs) and serves 12 islands, daily and year-round, while the competition operates 17 ships (avg. age 18 yrs)

With 34.7% of total sailings in this market, Blue Star Ferries had:

49.3% in passenger traffic Rank: 1st

53.4% in freight unit traffic Rank: 1st

46.4% in private vehicle traffic Rank: 1st

Market shares data as per Greek Port Authorities and Attica data

30.7%

20.0%

49.3%

42.1%

4.6%

53.4%

34.7%

18.9%

46.4%

Passengers

Freight Units

Private Vehicles

50

5151Market: Greek Islands (cont’d)

Full year 2008 traffic data – Dodecanese Islands (Kos, Rhodes)

Attica operates 3 ships (aged 8 and 18 yrs) year-round, while the competition operates 2 ships (avg. age 35 yrs)

With 54% of total sailings in this market, Blue Star Ferries had:

78.0% in passenger traffic Rank: 1st

71.4% in freight unit traffic Rank: 1st

76.0% in private vehicle traffic Rank: 1st

*Following the discontinuation of the North Sea route, Blue Star 1 was rerouted to this market at end 2008

Market shares data as per Greek Port Authorities and Attica data

22.0%

78.0%

28.6%

71.4%

24.0%

76.0%

Passengers

Freight Units

Private Vehicles

51

525252Indicative 5-year potential

Projected potential traffic data 2013 and actual data 2008

52

2008A 2013F

Sailings 5,568 6,613

Freight units 276,055 351,508

Passengers 4,083,875 5,084,005

Private vehicles (all) 583,192 703,206

There are many factors influencing performance of a shipping group such as Attica; these factors include fuel costs, demand for tourism, acquisition or building of new vessels and new route deployment/utilisation

While we cannot disclose any details, based on the projected data above it is estimated that by 2013, it may be possible to achieve:

Approximately €90m in EBITDA, andApproximately €45m in net income

0

20

40

60

80

100

2008 2013

0

10

20

30

40

50

60

2008 2013

EBITDA

Net income

CAGR 14%

CAGR 15%

5353Outlook for the future

Attica is a holding companyOur expertise lies in quality shipping, transportation and leisureThrough strong and lasting growth, we are committed to adding value for the benefit of all our shareholdersWe plan to expand our business by adapting our presence according to market demandWe aim to play a bigger role in our home marketWe focus on constantly improving operational and bottom line profitability and generating positive cash flows to support our policy for higher dividend pay-out in the years to comeAlthough our route in Crete started just two months ago, we have already achieved:

27% of passenger traffic24% of private vehicle traffic13% of freight traffic

53

Market shares data as per Greek Port Authorities and Attica data

5454

Section 1

Hygeia

Section 5

54

55Hygeia – Healthcare sector

55

Leading private provider of integrated healthcare services in SEE Date of investment: January 2006

MIG Ownership: 33.3%Hygeia is a market leader in private hospital units in GreeceHygeia Group consists of 3 main divisions

Secondary Care: Hygeia General Hospital, Mitera S.A, Leto S.A, Achillion Hospital (Cyprus), Hygeia Hospital Tirana, Evangelismos Hospital (Cyprus), SAFAK Group (Turkey)Primary Care: Magnetic Health diagnostic S.A, Alpha LabCommercial Activities: Y-Pharma S.A, Y-Logimed S.A (procurement companies for pharmaceuticals and supply consumables & impantable devices respectively), Stem Health S.A, Stem Health Hellas S.A, Stem Health Unirea S.A Romania (Stem Cell banks)

9 hospitals are in full operation while 1 is under construction (Hygeia Hospital in Tirana). The total licensed bed capacity of the group as of Dec 31, 2008 was 1,548 beds, expected to be increased to 1,768 beds after the beginning of Hygeia Tirana Hospital’s operation (Jan 2010)

Company Profile

Financial Highlights (€m)

Net profit +75%11.9EBITDA +107%24.0Sales +116%130.3

Total equityNet Debt 78.0 +108%

2007 2008 Growth281.8

49.820.8

358.5 379.1 +6%162.3

55

56Hygeia – Group structure (a)

56

(a) Direct and indirect stakes as at 30 April 2009

56

Hygeia operates through three main divisions; Domestic, International, and Commercial Services

57Hygeia Group – History and key events

57

Key Dates Event1970 Establishment of Hygeia Hospital

June 2002 Listing in the ATHEX

January 2006 Marfin acquires 49% stake of Hygeia S.A.

April 2006 Hygeia acquires 24.8% of Mitera S.A.

December 2006 Mitera S.A. increases its stake to Leto S.A. from 34% to 72.4%

April 2007 Establishment of Y-Pharma S.A.

April 2007 Establishment of Stem Health S.A.

July 2007 Establishment of Hygeia Hospital Tirana Sha

November 2007 Hygeia increases its stake to Mitera S.A. to 98.6%

December 2007 Establishment of Stem Health Hellas S.A.

January 2008 Acquisition of Achillion Hospital Ltd. (Cyprus) 56.7% stake

July 2008 Acquisition of Evangelismos Hospital Ltd. (Cyprus) 60% stake

July 2008 Hygeia increases its stake to Achillion to 65.75%

September 2008 Establishment of Stem Health Unirea S.A. (Romania)

December 2008 Acquisition of Safak Group (Turkey) 50% stake

March 2009 Mitera S.A. increases its stake to Leto S.A. from 72.4% to 88.8%

57

58Hygeia – Healthcare sector

58

Key Events of 2008In January 2008 Hygeia concluded the acquisition of a 65.7% stake of Achillion Hospital in Limassol for €15.6mIn July 2008 Hygeia concluded the acquisition of a 60% stake of Evangelismos Hospital in Paphos for €7.1mIn July 2008 Stem-Health, a cell bank, commenced operationsIn September 2008 Stem-Health Unirea was established in Romania; it will commence operations in H109In December 2008 Hygeia concluded the acquisition of a 50% stake of Safak Group in Turkey. Safak Group controls 4 hospitals with 470 beds capacity in the metropolitan area of IstanbulIn view of the challenging macroeconomic environment Hygeia Group decided to realign its investment plan, proceeding only with committed investments that support sustainable organic growthIn this context Hygeia Group decided in December 2008 and Implemented in January 2009, the following initiatives:

Full redemption of the existing Convertible Bond of €306.0m on its first call (Jan 13, 2009). A share capital Increase of circa €83m, in favor of old Shareholders (to be completed in H2 09), followed by a new debt bridge financing

Year 2008 PerformanceFY2008 consolidated revenues increased by 116% y-o-y to €281.8m (Consolidated P&L is not directly comparable, due to the full-consolidation of Mitera-Leto Group, Achillion, Evangelismos and Safak Group)FY2008 EBITDA soared by 107.4% y-o-y to €49.8mEBITDA margin stood at 17.7% versus 18.4% in 2007 impacted by the integration costs of the newly acquired hospitals in Cyprus

58

Strategic & Operational Highlights of the year

59Hygeia – Mission, values, vision

59

Provide high quality services at the leading edge of medical science and technologyDevelop an integrated health services network in Greece, and in SEEPromote corporate integrity and social responsibilityServe as the recognised reference point for patients and medical staffContinue to be a reliable and responsible employerCreate value for our shareholders

Our ValuesCommitment toward patient safetyFocus on healthcare services delivery with dignity & respectProactive respect for the environmentHolistic approach toward patient carePromote medical ethics and the advancement of medical science

Our VisionTo become the largest private sector provider of integrated Healthcare services in SEE, the Mediterranean & theMiddle East

59

Our Mission

60Hygeia – Regional strengths

6060

Hygeia has taken steps to become the largest private sector provider of integrated healthcare services in SEE, the Mediterranean and the Middle East

61Hygeia – Long term strategy

61

Increased efficiency, reduction of length-of-stay (LOS)Cost containment, efficient internal controlOperating leverageExtract synergies from mergers and acquisitions, centralize suppliesSkew of revenue mix towards value added servicesModernise & upgrade key medical technologyIncrease emphasis on medical researchSupplement voids in the public health system

Greenfield expansion in SEE & the Middle EastMergers and acquisitions in Greece, SEE & the Middle EastFurther utilise relationship with Marfin Investment Group

Comprehensive hospital infrastructureOne-stop diagnostic servicesContinuation of best-in-class medical servicesBroaden outpatient servicesPioneer scientific advancementsDevelop new medical capabilities

OrganicGrowth

Geographicalexpansion in Greece and SEE

Business development

61

Hygeia has adopted the following strategies for long-term growth…

62Hygeia – Short term strategy

62

In light of the challenging macroeconomic environment, both globally and in particular in SEE,Hygeia Group has decided to realign its investment plans and implement a less aggressivestrategy in the short-term, by:

proceeding only with committed investments,and pursuing only selective acquisitions in the region that support sustainable organic growth,focusing on operating consolidation of the newly acquired companies,Fully extracting synergies that arise amongst the Hygeia Group of companies and the larger MIGfamily of companies

62

…while focusing on effectively managing its short term strategy

63Hygeia – Management views on strengths and initiatives

63

Experienced & proven management team; clearly recognised in the regionHigh brand awareness as a health organisation of high reputationDedicated and professional staffSuperior, leading customer serviceReliability - continuity of careContinuing education programsNew technologies and treatment protocolsScientific research contributions acknowledged domestically and internationally

Hygeia Group initiatives

Expand in SEE and replicate Hygeia’s successful business model, transferring know-how and technologyTake advantage of the fragmented domestic private sectorFocus on de-regulation of the domestic primary healthcare sectorFocus on de-regulation of the domestic pharmaceutical and pharmacy sectorsBenefit from increase in out-of-pocket healthcare spending of Greek & SEE citizens

63

Hygeia Group strengths

64Hygeia – The Greek healthcare market

64

Greek healthcare spending as a % of GDP stands at 9.1%The OECD countries average stands at 8.9%

Source: OECD 2008

64

10% 10% 10% 10% 10% 9% 9% 9% 9% 9% 9% 9% 9% 9% 8% 8% 8% 8% 8%8% 7% 7% 7% 7% 6% 6% 6%

11%11%

15%

11%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

U.S.

A.Sw

itzer

land

Fran

ceGe

rman

yBe

lgium

Portu

gal

Austr

iaCa

nada

Denm

ark

The

Neth

erlan

dsN.

Zea

land

Swed

enGr

eece

Icela

nd

Italy

OECD

Ave

rage

Austr

alia

Norw

aySp

ain U.K

.Hu

ngar

yFi

nlan

dJa

pan

Irelan

dLu

xem

burg

Slov

akia

Czec

hM

exico

Kore

aPo

land

Turk

ey

Healthcare spending per GDP in OECD countries

65Hygeia – The Greek healthcare market (cont’d)

65

Greek private sector spending represents 38.4% of total spendingThe OECD countries average private sector spending stands at 27%USA private sector accounts for 54.2% of total healthcare spending

Source: OECD 2008

65

38% 38%

33%30% 30% 29% 29% 29% 29% 28% 27% 26% 24% 24% 23% 23% 22% 22% 20%

18% 18% 18% 16% 16%13% 12%

9%

40%

54%56%

45%

0%

10%

20%

30%

40%

50%

60%

Mex

icoU.

S.A.

Kore

aSw

itzer

land

Gree

ceTh

e Ne

ther

lands

Austr

alia

Polan

dCa

nada

Portu

gal

Hung

ary

Spain

Turk

eyBe

lgium

OECD

Ave

rage

Slov

akia

Finl

and

Austr

iaGe

rman

yIta

lyN.

Zea

land

Irelan

dFr

ance

Japa

nSw

eden

Islan

dNo

rway

Denm

ark

U.K.

Czec

hLu

xem

burg

Percentage of private healthcare spending in OECD countries

6666Hygeia – The Greek healthcare market (cont’d)

Private hospital and diagnostic center revenues reached €1.79bn, increasing 19% y-o-y, while the CAGR for the period 1997-2007 was 13.4%

Source: ICAP 2008, OECD 2008, NSS Revised Data July 2008

Growth trends in Greek hospitals

It is estimated that in the following 2 years, the CAGR of private general hospitals will be 16-18% y-o-y, while maternity hospitals will grow by 9-11% y-o-y and primary care by 10% y-o-y due to the following catalysts:

Ageing population: population over age 65 is 18.6% versus 13.8% in 1991; according to NSS, by 2030, 24% of population will be above 65-years oldIncreasing life expectancy: life expectancy stands at 79.3 years from 77.2 years in 1991Under-insured population: circa 10% of the population have private insuranceHighest proportion of smokers in the OECD: 38.6% of the population vs 24.3% OECD averageAround 22% of adults are classified as obeseHigh impact of immigration: approximately 1m immigrants live in Greece, overwhelming public sector hospital capabilitiesThe chronic inefficiency of the public healthcare systemleaves ample room for private sector; only 18% of population is satisfied with public sector care versus 56% E.U. averageTwo-tier private sector with very few players offering high-end services and a large number low-end players that substitute the public sectorPoor quality health care services outside the main Greek cities (Athens & Thessaloniki)Highly fragmented private sector

53.6% 52.9% 52.1% 51.6%

15.8% 16.1% 16.5% 15.5%

8.2% 8.7% 9.3% 9.5%

9.5% 10.0% 10.2% 10.7%

12.7%11.9%12.2%12.9%

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007

Other IATRIKO IASO EUROMEDICA HYGEIA GROUP

More than 200 players none of them above 5% market share

66

Market share of private healthcare institutions

67Hygeia – Group hospitals

67

Hygeia Group has a portfolio of 9 hospitals in SEE, with a total licensed bed capacity of 1,548; of these, 3 hospitals are in Greece, 4 are in Turkey and 2 are in Cyprus With the conclusion of build of the new hospital in Albania by the end of 2009, the Group will have 10 hospitals with a total licensed bed capacity of 1,768 beds

Hygeia Group will have 71 operating theatersHygeia Group will have 42 delivery roomsHygeia Group will have 22 Intensive Care Units (148 beds)

During 2008, over 65,000 operations were performed and more than 21,500 babies were born in Hygeia Group hospitalsHygeia Group is the largest obstetrics and gynecology group in Greece with more than 17,500 Greek deliveries, implying a 16% market share Inpatient admissions c. 108,000 per annumOutpatient visits c. 840,000 per annum

67

The Hygeia Group has an impressive portfolio of leading state-of-the-art hospitals

68Hygeia – Group hospitals (cont’d)

68

D.T.C.A. Hygeia General Hospital is a state-of-the-art general acute care hospital of 40k m2, in the northern suburbs of Athens, in close proximity to AIA and the ports of Lavrio & Rafina. The hospital is licensed for 369 beds, has 17 operating theaters and 4 Intensive Care UnitsMitera Maternity Hospital is a state of the art Maternity, Gynaecology and General Hospital of 35k m2, adjacent to HYGEIA. The hospital is licensed for 442 beds, has 19 operating theaters, 22 delivery rooms and 3 Intensive Care Units Leto Maternity Hospital is a state of the art Maternity and Gynecology Hospital of 6.5k m2, close to Athens’ center. The hospital is licensed for 110 beds, has 7 operating theaters, 7 delivery rooms and an Intensive Care UnitAchillion Hospital was built in 2004 and is a 7k m2 facility with a licensed capacity of 86 beds in Limassol, Cyprus. The hospital has 8 operating theaters, 5 delivery rooms and an Intensive Care UnitEvangelismos Hospital was built in 2003 and is a 6.2k m2 facility with 71 licensed beds, in Paphos, Cyprus. The hospital has 3 operating theaters, 2 delivery rooms and an Intensive Care Unit

68

Hygeia Group hospitals: in detail

69Hygeia – Group hospitals (cont’d)

69

Avrupa Safak General Hospital is a state-of-the-art general acute care Hospital of 8.5k m2 that was established in 1998 in Gaziosmanpasa, Istanbul. The hospital is licensed for 180 beds, has 5 operating theaters, 2 delivery rooms and 4 Intensive Care UnitsJFK Hospital commenced operations in December 1999 and is a 9k m2

facility with licensed capacity of 126 beds in Besyuz Evler, Istanbul. The hospital has 5 operating theaters, 2 delivery rooms and 3 Intensive Care UnitsGoztepe Safak Hospital commenced operations in April 2004 and is a 6.8k m2 facility with licensed capacity for 87 beds in Goztepe, Istanbul. The hospital has 4 operating theaters, 2 delivery rooms and 3 Intensive Care UnitsIstanbul Safak commenced operations in January 2005 and is a 2.5k m2

facility with licensed capacity for 77 beds in Gaziosmanpasa, Istanbul. The hospital has 3 operating theaters, 2 delivery rooms and 2 Intensive Care UnitsHygeia Hospital Tirana will be the 1st integrated private hospital in Albania and is expected to commence operation in 2010. The 220-bed hospital will be a circa 25k m2 state-of-the-art facility on a main traffic artery of Tirana

69

Hygeia Group hospitals: in detail

70The sector leader in cutting-edge technology

70

Linear Accelerator ELEKTA AXESSETM

Hygeia is the 1st hospital in Europe to install the Elekta Axesse linear accelerator, and among the first globally. Hygeia’s Radiation Oncology Department will use the Elekta Axesse to offer the latest treatment modalities

da Vinci® S Robotic Surgery System, (Intuitive Surgical – da Vinci)This is the latest generation da Vinci S Robotic Surgery System and the 1st and only one to be installed in Greece. This device allows surgeons to perform a variety of surgical procedures using the most modern and precise techniques. The 1st

coronary artery bypass graft operation using the da Vinci S Robotic Surgery System was successfully performed at Hygeia in 2008

Open Magnetic Resonance Imaging Device with high field uniformity 1.0T (Philips Ambient Experience)

The Mitera General, Obstetrics & Gynecology and Pediatrics Clinic possesses the most advanced medical imaging technology with this new Magnetic Resonance Imaging (MRI) system. This MRI allows high definition images to be captured very quickly in a totally patient-friendly, open ambient environment

70

71The sector leader in cutting-edge technology (cont’d)

71

Hemodynamic-Angiographic and Electrophysical LaboratoryThis laboratory provides the capability for complex diagnostic examinations and invasive procedures and operates in the Mitera Pediatric Cardiac Surgery Clinic. The laboratory is in an ideal location near both the pediatric cardiac surgery intensive care unit and the pediatric cardiology & cardiac surgery unit. This laboratory is the only one of its kind in Greece treating pediatric arrhythmias

Gamma Knife (Elekta-Leksell Gamma-Knife C)This represents the most sophisticated device for treating life-threatening cancer tumors of the brain. The Leksell Gamma Knife allows these extremely complex neurosurgical procedures achieve a precision of 0,3mm. Hygeia has performed over 500 of these therapies with a success rate exceeding 95%

PET/CT (Siemens-Biograph PET-CT)Hygeia’s PET-CT Department was the first to be established in 2004 and to achieve ISO 9001:2000 certification. The PET-CT is an imaging device for patients diagnosed with cancer. In such, the PET-CT Department works very closely with Hygeia’s Radiation Therapy and Oncology Center to ensure the patient receives the best care possible. The Department has successfully conducted over 2,400 PET-CT examinations

71

72Hygeia – Group personnel and KPIs

72

The Hygeia Group has over 8,000 physicians and staff encompassing nearly 50 different specialties, of which:

3,659 nurses, administrative and other402 salaried physicians4,019 cooperating physicians

In the last year, we have dedicated over 40,000 training hours to our personnel; staff turnover has dropped from 24% in 2007 to 6.5% in 2008 The vast majority of our physicians have received all or part of their medical education & training in the United States and the UKOur objective is to continue our strategy of attracting the highest caliber physicians from abroadThe Hygeia Group will be the first healthcare group to receive the JCI Accreditation in Greece, forthcoming this year

Hygeia Group 2004 2005 2006 2007 2008Inpatients 14,536 14,893 15,144 49,501 108,257change y-o-y 2.5% 1.7% 226.9% 118.7%Outpatient Visits 66,221 69,581 77,398 321,271 839,609change y-o-y 5.1% 11.2% 315.1% 161.3%# of Deliveries 0 0 0 16,043 21,546change y-o-y 34.3%Length of Stay (Days) 4.54 4.48 4.47 3.50 3.04Occupancy Rate 71.0% 71.9% 73.0% 66.0% 71.1%

72

The Hygeia Group has over 8,000 physicians and staff contributing their skills and services to its patients

73Hygeia – Group revenue analysis

73

The Hospital Services business unit accounts for 91.4% of group salesHygeia, Mitera & Leto Hospitals account for circa 87% of salesRevenues from third countries accounts for 5% of group sales, since Achillion & Evangelismos were consolidated in 1Q08 & 3Q08 and Safak Group since Dec. 08 for the first timeWith the consolidation of Safak Group, SEE participation in 2009 will increase substantially

91.4%8.6%

Hospital ServicesPrimary Care & Commercial Services

Business units

2.6%

1.8%

7.0%0.6%

8.6%

30.8%

47.1%

Hygeia Mitera LetoAchillion Evangelismos Y-PharmaSafak

Companies

95.0%

5.0%

Greece Abroad

Geographical

73

74Hygeia – Group financials (a)

74

(a)2004-2008 under IFRS

Income Statement (€m) 2002 2003 2004 2005 2006 2007 2008Revenues 74.0 68.9 79.2 83.6 94.6 130.3 281.8change y-o-y -6.8% 14.9% 5.5% 13.2% 37.8% 116.2%EBITDA 14.7 8.9 6.3 6.8 11.6 24.0 49.8change y-o-y -39.6% -28.8% 7.5% 70.6% 106.6% 107.5%margin 19.9% 12.9% 8.0% 8.1% 12.3% 18.4% 17.7%EBIT 9.2 4.3 -1.0 -0.3 5.1 16.6 33.9change y-o-y -53.0% n.m. n.m. n.m. 223.9% 104.4%margin 12.4% 6.2% -1.3% -0.3% 5.4% 12.7% 12.0%EBT 7.9 2.9 -3.0 -2.2 3.0 16.4 15.6change y-o-y -63.6% n.m. n.m. n.m. 450.6% -5.0%margin 10.7% 4.2% -3.8% -2.7% 3.2% 12.6% 5.5%Net Income 5.0 0.9 -1.5 -2.3 1.0 12.1 21.1change y-o-y -82.9% n.m. n.m. n.m. 1053.8% 74.5%margin 6.8% 1.2% -1.9% -2.8% 1.1% 9.3% 7.5%

Balance SheetNet Fixed Assets 64.6 76.3 103.3 98.9 94.3 316.0 373.1Working Capital 3.8 3.1 -1.5 -1.9 0.4 6.5 -0.2LT Assets 0.2 0.2 2.3 2.2 73.4 198.4 241.7Total Assets 68.7 79.6 104.0 99.3 168.1 520.9 614.6Net Debt 24.0 35.4 41.6 44.7 38.5 78.0 162.3LT & Other Liabilities 0.3 0.3 12.8 14.6 28.8 111.2 112.1Equity 44.4 44.0 49.6 40.0 100.8 331.6 340.1Capital Employed 68.7 79.6 104.0 99.3 168.1 520.9 614.6

Financial RatiosWC/Sales 5.2% 4.6% -1.9% -2.2% 0.5% 5.0% -0.1%Net Debt / EBITDA 1.6 x 4.0 x 6.6 x 6.6 x 3.3 x 3.3 x 3.3 x

Current Assets / Current Liabilities 0.9 x 0.7 x 0.5 x 0.5 x 0.7 x 0.6 x 0.7 xInterest Coverage (EBITDA/Interest Expenses) 11.2 x 6.2 x 3.2 x 3.3 x 2.5 x 7.4 x 1.7 x

74

75Hygeia – the future

75

The Hygeia Group has focused its efforts to creating the highest quality private healthcaregroup in SEE, the greater Mediterranean, and the Middle East

Clearly defined long-term strategyStrong shareholder structureStrong and stable financialsHigh brand awareness, excellent reputation in both the public as well as within the medical fieldManagement team with international background & training and significant experience in the sectorHighest-caliber physicians and high quality support personnel

The Hygeia Group is well equipped to be the leading healthcare provider in the region

75

7676

Section 1

SingularLogic

Section 6

76

7777

The leader in the highly fragmented local IT market with a diverse base of more

than 40,000 SME clients, 500 Large Enterprises and more than 100

Multinational Clients

Date of Investment: December 2006MIG Ownership: 31.2%Singular Logic is a leading player in the Greek BusinessSoftware market providing integrated solutions for the privateand public sectors, in Greece and abroad through threedynamic business divisions

Singular Logic has a large and reputable customer base ofGreek and international companies serviced on the back offocused and competent offerings developed alongsidepowerful partners

Company Profile

IT Sector

EnterpriseDIS (Corporate)

SingularLogicSoftware (SMEs)

SingularLogicIntegrator

(Public Sector)

Enterprise solution provider for the private sector using both own brand and third party

software

Leading software vendor for small and medium enterprises

Service provider for system and software

integration projects for the public sector

“Oracle EE & CIS Partner of the Year 2008 - Enterprise Application Partner Award”

“ΙΒΜ Business Partner Sales Leadership Achievement Award, IBM Retail Store Solutions 2007 – Europe”

Financial highlights (€m)

Net profit +370%2.0EBITDA +69%10.1Sales +31%81.9

Total equityNet Debt/(Cash) -6.0 +61%

2007 2008 Growth107.0

17.09.5

54.2 62.8 +16%-9.6

77

7878

Strategic & Operational highlights of the year

During the last year, SingularLogic has performed a successful financial turnaround which is demonstrated in all 2008 financial metrics:

FY2008 consolidated sales soared to €107.0m presenting a substantial increase of 31% compared to FY2007 (€81.9m)Consolidated FY2008 EBITDA reached €17.0m versus €10.1m in FY2007 representing a robust uplift of 69% The EBITDA Margin of the year increased by 361 bps to 15.9% vs 12.3% in 2007Consolidated FY2008 EBT posted an impressive increase reaching €11.5m compared to €3.5m in FY2007FY2008 Net Profits after Tax presented a substantial growth of 370% versus FY2007 amounting to €9.5m FY2008 Net Profits after Tax and Minorities amounted to €8.7m, 510% higher than FY2007In FY2008 SingularLogic preserved a strong financial structure with a highly liquid balance sheet which is illustrated through its strong net cash position of €9.6m (€36.9m cash vs €27.3m debt)

SingularLogic is continuously working towards the realisation of synergies with other MIG group companies. During 2008, Hygeia Group’s IT requirements were fully outsourced to SingularLogic. Similarly, the company has been working closely with MPB, Attica and Vivartia and it will be providing valuable IT solutions support to the newest company of the group, Olympic

IT Sector78

7979

SingularLogic has outperformed its competitors in all profitability figures(1), accounting for more than 1/3 of thesector’s Net Income and possessing the healthiest cash position(2) in the industry

The undisputed leader in the Greek IT sector

1. SingularLogic achieved the highest EBITDA in terms of absolute number (€17m) and a significant EBITDA growth ratio of 69.2%, unsurpassed in the sector, together with the highest Net Income after minority rights of €8.7m, which grew by +510% vs. 2007, the highest growth of all listed companies

2. As of 31.12.2008, the company held the highest cash reserves in the sector, at €36.9m

3. Figures in blue or red refer to Net Income figures for 2008

EBITDA Growth ‘08

Sales growth ’08/’07 Size of circle = latest available revenues, €m

797979

€9.5m

€0.9m

€1.1m

€1.7m€1.7m

(€27.0m)

(€7.0m)(€151.5m)

€1.2m

€2.3m

€1.0m

Negative band not drawn to scaleSource: FactSet, Company accounts

79

8080

SingularLogic has a clear focus on software services and is ranked No 1 in the Greek market

Focus on software

Business Software LicensingBusiness Software Maintenance and Services

31%

8% 7% 7% 6%3%

38%

Sing

ular

Logi

c

SAP

Alte

c

Rea

l C

onsu

lting

Prof

ile

Q&

R

Oth

er

27%

20%

13%9% 8%

5%

17%

Sing

ular

Logi

c

SAP

Alte

c

Rea

l C

onsu

lting

Prof

ile

Q&

R

Oth

er

80

8181

SingularLogic operates through three divisions, structured around a customer-centric approach

Main operating divisions

Finance HR Strategy & Corporate Marketing IT R & D

e-government

Transportation

Defence

Health

Regional government

ERP

Commercial Packages

Accounting Packages

Payroll / HR

CRM

Hotel

BI

Retail

Consumer Industrial Services

Account management

Strat. ProductDevelopment

Services

Project mgmt

Development

Marketing

Financial

Retail Enterprises

Business Outsourcing

Services

Account management

Strat. ProductDevelopment

Network support

Training

Development

Marketing

Account management

Strat. ProductDevelopment

Services

Project mgmt

Development

Marketing

TelecomsNational Elections

81

8282

SingularLogic operates through three divisions, structured around a customer-centric approach

Main operating divisions (cont’d)

Strategic technological partner & business integrator for large enterprises & organizations in the private sector in Greece and abroad

25 years of expertise in offering integrated own developed or internationally represented IT solutions500 large and 100 international companies from all business domains (Consumer/Industrial/Services, Retail, Financial, Telco Institutions, Healthcare)Customisation & system integration to support every business need (ERP, CRM, BI, EAI, etc)

Powerful national network behind the most reliable and complete product offering for small to medium enterprises

The largest installed base with more than 80,000 active installationsThe largest distribution network with more than 500 business partnersComplete product portfolio covering more than 10 business areas

Long standing, successful track record behind large scale IT projects for the Public Sector

Elections for the last 27 yearsIntegrated Information System for GDDIA, €5mAir battle control system for Lockheed Martin, €12.5m The largest public sector project in Greece for 2008 (heating petrol chain –IFESTOS, MoE)More than 300 local authorities customers and more than €15m projects in Regional Public AdministrationElectronic Urban Planning I-II-III

82

8383

SingularLogic attracts a diverse base of more than 80,000 SME clients, 500 large enterprises and more than 100 multinational clients

Large and diverse client base83

8484

SingularLogic utilises unique salesforce models

Large and diverse client base (cont’d)

4,000

15,000

140,000

650,000

Breakdown of businesses in Greece

Corporate and public sector

Large SMEs (average revenue €2.5m)

Small SMEs (average revenue €0.7m)

Professionals

Source: SingularLogic

• Over 50 expertly trained account managers dedicated to each major corporate segment (telco, retail, financial, consumer) and major public sector organisations

• Largest and most geographically extensive sales network of over 500 dealers, managed and expertly trained and coordinated by Singular Logic

84

8585

SingularLogic offers its clients a strong portfolio of 3rd party products developed by major international vendors

Large and diverse client base (cont’d)

IP Office Compact Contact CenterApplication Enablement ServiceIP Office Professional EditionIP Office Standard EditionDistributor of the Year Excellence 2008

Platinum Partner

85

8686

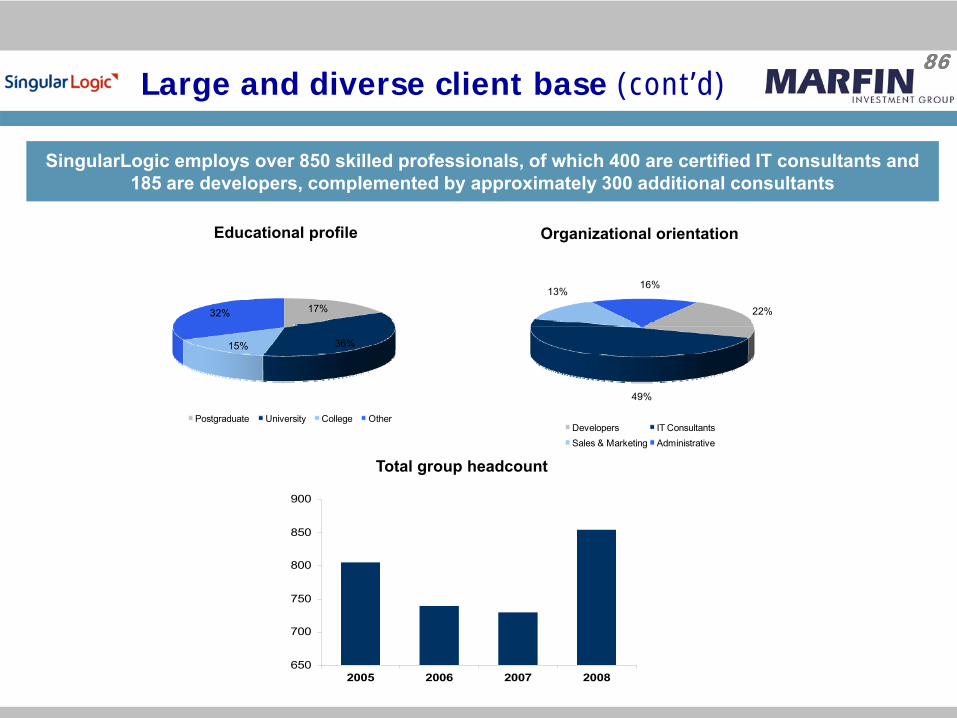

SingularLogic employs over 850 skilled professionals, of which 400 are certified IT consultants and 185 are developers, complemented by approximately 300 additional consultants

Large and diverse client base (cont’d)

Educational profile Organizational orientation

650

700

750

800

850

900

2005 2006 2007 2008

Total group headcount

86

17%

36%15%

32%

Postgraduate University College Other

22%

49%

13%16%

Developers IT ConsultantsSales & Marketing Administrative

8787

Three years ago two historical leaders with underperforming operations, and the late partial control of MIG joined forces to create a new IT leader – significantly improving profitability

SingularLogic – Result of a merger

Revenues (€m) EBITDA (€m)

Net income (€m)EBIT (€m)

(4.7)

1.0

10.1

17.0

-10

-5

0

5

10

15

20

2005 2006 2007 2008

(13.3)

(7.7)

2.0

9.5

-15

-10

-5

0

5

10

15

2005 2006 2007 2008

68.5

45.6

81.9

107.0

0

20

40

60

80

100

120

2005 2006 2007 2008

(10.0)

(2.5)

4.7

13.2

-15

-10

-5

0

5

10

15

2005 2006 2007 2008

87

8888

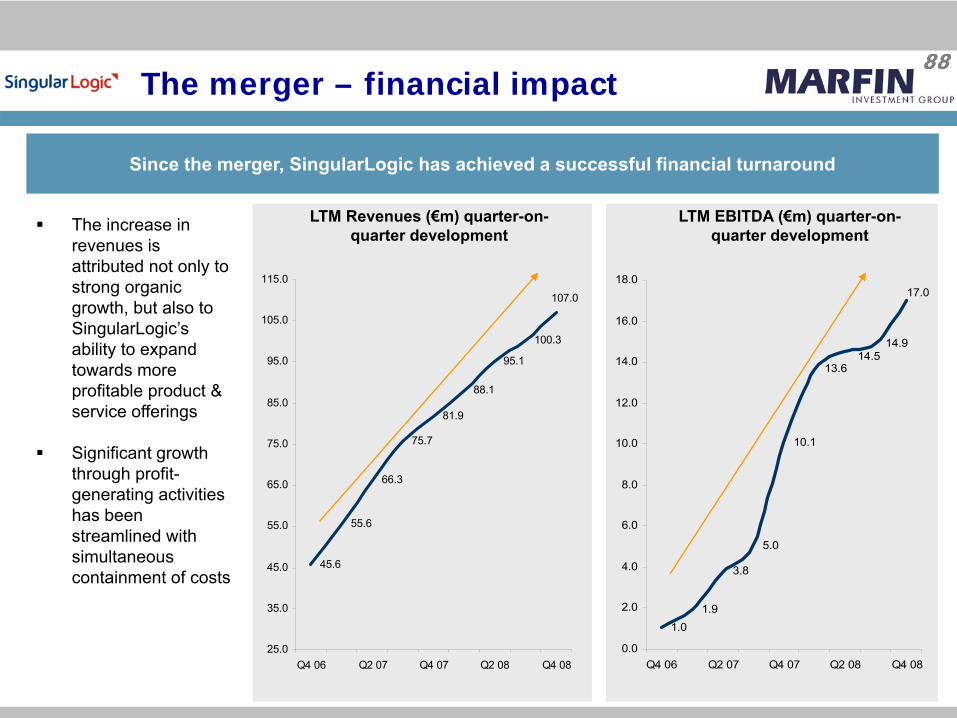

Since the merger, SingularLogic has achieved a successful financial turnaround

The merger – financial impact

LTM EBITDA (€m) quarter-on-quarter development

LTM Revenues (€m) quarter-on-quarter developmentThe increase in

revenues is attributed not only to strong organic growth, but also to SingularLogic’s ability to expand towards more profitable product & service offerings

Significant growth through profit-generating activities has been streamlined with simultaneous containment of costs

45.6

55.6

66.3

75.7

81.9

88.1

95.1

100.3

107.0

25.0

35.0

45.0

55.0

65.0

75.0

85.0

95.0

105.0

115.0

Q4 06 Q2 07 Q4 07 Q2 08 Q4 08

1.01.9

3.8

5.0

10.1

13.6

14.9

17.0

14.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Q4 06 Q2 07 Q4 07 Q2 08 Q4 08

88

8989

SingularLogic has experienced strong growth across all divisions

Revenue analysis

Turnover divisional breakdown, 2008 (€m)Turnover (€m)

39.5

20.122.0

51.5

29.725.7

0

10

20

30

40

50

60

Enterprise Integrator Software

2007 2008

30%

48%17% 51.5

25.7

29.7

Enterprise Integrator Software

89

9090

SingularLogic has had high growth across high-margin targeted product categories

Revenue analysis (cont’d)

Turnover breakdown by product, 2008 (€m)Turnover (€m)

12.9

20.9

31.8

16.116.1

22.4

53.9

14.4

0

10

20

30

40

50

60

Licenses Maintenance Services Hardware &System Software

2007 2008

25%

7%

69%

(11%)

14.4 16.1

53.9

22.4

Licenses Maintenance

Services Hardware &System Software

90

9191

Focused strategy of innovation, increased customer utilisation and cost consciousness

Strategic plans

Capitalising on internal group

clients

SingularLogic

Market share gains and increased

penetration Through new

product development efforts

International distribution of new products

Through agreements with major

international vendors

Further selective consolidation in

sector Profitable high-growth potential

targets

Strong pipeline in place

Momentum in both private and public

sectors

Initiation of 4th CSFP

Through significantly reduced competitive

pressure

91

Capitalising on internal group

clients

Market share gains and increased

penetration Through new product development efforts

Strong pipeline in place

Momentum in both private and public

sectors

9292

SingularLogic will focus on development of outsourcing and other value-added services

Areas of interest:Disaster recovery and business continuity servicesOutsourced customer support servicesApplication service provisionValue added services (mobile applications & communication enabled solutions)Business process outsourcing

Advanced software solutions and servicesProduct innovation through Galaxy, the latest state-of-the-art technology platformNew offerings

Retail, RestaurantCRM/Payroll: SaaS, IP telephony: Avaya CEBP offeringsICTM offerings: Alert Server, Voice & Web Shop, Digital Signage Easy Pack, Credit Assist, etc.E-securityJoint ICT offerings with WIND

Expanded Revenue streamsSOA service initiatives (Stock online, Data exchange, alerting)Opportunities from large customer base (upgrades, cross sell, up sell)Business Benefit program to attract the competition’s clientsInternational expansion in SEE through network developmentDistribution agreements with large international vendors (global market reach)

Strategic plans (cont’d)92

9393

Public sector modernisation projects are expected to provide further opportunities to the IT sector

Strategic plans (cont’d)

SingularLogic will target opportunities in the following major business categories:

National Elections, Efaistos, FosOffsets / Defense – surveillanceExpansion of the Forest Fire Detection SystemFurther business opportunities in CyprusPreparation for Espa bids/projects – H2 ’09PPP expected projects – Army supplies warehouse, Port Security, Health cardGovernment issues / needs – 3% rebate medicines, Payroll for public sector, consolidation of socialsecurity agencies, tourism, Ministry of Health, local registriesInnovative solutions – FOS, surveillance, IVR/SMS, simulators

93

9494

Section 1

Olympic

Section 7

94

95The transaction perimeter

Pantheon MRO

Brand name and logoSlots in Heathrow, Gatwick, JFK, Fiumicino, Frankfurt, Charles de Gaulle, Linate, Bucharest, Brussels

Long-term leases for 2 MRO hangars located at Athens Intl Airport (‘AIA’), expiring in 2026 Selected MRO equipment

Minimum Assets

€ 45.7m € 16.7mMIG’s offer

Additional slots, certain aircraft, IT systemsOther flight-related assets from OAS, prior to its liquidation

Additional MRO equipmentIT systemsAdditional

Assets

Ground Handling

Rights for the provision of handling services at 5 main liberalised Greek airportsLeases for AIA cargo and other facilities

€ 44.8m

Additional ground handling equipmentAdditional cargo equipment

MIG has acquired a number of commercially significant assets, free of any obligations, at a very attractive price of €107m

95

96The transaction