140

UNIVERSITY OF SARGODHA

| Date post: | 20-Nov-2014 |

| Category: |

Documents |

| Upload: | atif-aslam |

| View: | 107 times |

| Download: | 0 times |

UNIVERSITY OF SARGODHA

Internship Report

Page 2

Internship Report

Internship Letter

Page 3

Internship Report

Preface

In order to be able to crumble with the altering environment it is necessary to

have some practical experience. As the students of Commerce we have to pass

through a series of various managerial techniques. During this practical course

we are provided with an opportunity to learn that how the theoretical knowledge

can be implemented in practical grounds. I was selected to do my internship in

NIB Bank of Pakistan Mian Khan Road Branch Sargodha. I worked there for six

weeks & it gave me a greater practical knowledge about the operations of a

bank.

Page 4

Internship Report

Dedicated To

Hazrat

Muhammad

(P.B.U.H) and

my beloved parents

and teachers who

inspired us to

higher ideas of life.

Page 5

“O mankind if you have a doubt about yhe resurrection (consider)that we created you out of dust, then out of sprem, then out of a beach like cloth, the out of morsel of flesh, partly formed and partly unformed, in order that We may manifest (foster you) that you may reach your age of full strength; and some of you are called to die, and some are sent back to the feeblest old age, so that they know nothing after having known much,”. “Holy Quran”

Internship Report

THE HOLY QURAN SAYS,

Page 6

Internship Report

AcknowledgementBy the Grace of Almighty Allah, the most Merciful, the most Beneficial, I'm today

submitting my internship report; I have the pearls of my eyes to admire the

blessings of the compassionate, omnipotent, the Merciful and the beneficent

Allah who is the entire source of knowledge and wisdom.

Due to his bounteous blessings, I become able to contribute this comprehensive

assignment toward the deep ocean of knowledge already exists. Heart is warm

with love and thoughts have turned to the city of knowledge – The Holy Profit

(P.B.U.H) His saying “Learn from to Cradle to Grave” inspired the strong desire in

me to under take this course of valuable studies.

It would obviously be injustice not to mention the name of the people involved to

make this assignment possible and helped their utmost to make me understand

the overall operation of the company as of their best knowledge.

Despite of the most hectic schedule, Madam “javeria Islam” helped me so much

and also branch Manager “Raja Qaiser”. I'm really grateful to ma’am for

clarifying my concepts and making me learn from her experience. Whatever I

learnt from you will definitely help me in my upcoming study and the professional

life ahead. Thank you so much for being so co- operative and so helpful every

time. I hope ma’am I have been up to your expectations.

Date: Sep20, 2010

Supervisor:_______________________

Observer:________________________

Head of Department: _______________

Page 7

Internship Report

Executive SummaryNIB Bank Limited provides various financial products and services in Pakistan.

Its Corporate Banking segment engages in underwriting and initial public offer

related activities. The company’s Trading and Sales segment provides fixed

income, equity, foreign exchanges, commodities, credit, funding, securities,

brokerage debt, and prime brokerage services. NIB Bank’s Retail and Consumer

Banking segment offers lending and deposits, banking services, private lending

and deposits, and banking services to retail customers, and small and medium

enterprises. The company's Commercial Banking segment provides finance,

export finance, trade finance, leasing, lending, guarantees etc.

I have done 6 weeks internship starting from 7 th July to 19th August 2010 from NIB Bank branch from Sargodha region.It is the main part of my internship report. It consist on the detail of the work that I have done there as an internee. In NIB Bank I worked in Account opening, Credit, Foreign Trade and Accounts Department. The detail of my work in each department is described in this part with all possible details.

The mostly I worked under the head of Current Account and work for opening of Basic Banking Account .It helped me a lot under stand the criteria for opening of Basic Banking Account. This includes the following points.

The initial minimum deposit to open the account will be Rs. 1,000; however, there

will be no minimum balance charges, if the balance falls below the above

threshold.

If the balance in the account remains ‘Nil' for a continuous six month's period, the

account will be closed. However, exemption to this effect may be solicited from

business head.

Page 8

Internship Report

During the course of internship I learned about different functions performed by

Remittances, Advances, Foreign Exchange and Customer Service Office

department and bank as a whole. I also learned bank’s correspondence with their

customers and within branches. I learned about documentation requirements and

record keeping for different activities and processes, especially the

documentation requirement for different kinds of financing facilities.

Page 9

Internship Report

1. Industry Introduction………………………………………………..12

2. An Overview of Organization……………………………………...19

2 .1 - History of Organization…………….….……19

2.2 - Nature of Organization…………….………...25

a. Vision Statement………………25

b. Mission Statement…………….25

2.3 - Main Features…………………………...…….28

2.4 – Competitors……………………………..…….55

3. Organizational Structure…………………………………….……..56

3.1 - Hierarchy Chart....................................…...56

3.2 - Number of Employees……………………….57

3.3 - Main Offices…………………….……………..57

3.4 - Introduction of all Departments………...….59

3.5 - Comments on Organizational Structure….69

4. Work done by Internee………………………………………….…..70

5. Financial Analysis of Organization……………………………….73

5.1 - Financial data of last 5 years……………….73

a. Horizontal Analysis

b. Vertical Analysis

Page 10

Internship Report

5.2 - Significance of Ratio………………………..78

5.3 - Components of Ratios (formulae used)…79

5.4 - Horizontal Analysis of Ratios

5.5 - Interpretation of Ratios

6. SWOT Analysis……………………………..………………………..91

7. Conclusion……………………………………………………………94

8. Recommendations.………………………………………………….96

9. Limitations…………………………………………………………..100

10. Bibliography`………………………………………………………101

11. Annexes…………………….………………………………………102

12. Glossary…………………………………………………..………..103

1.Industry Introduction:-

Page 11

Internship Report

History of Banking:

What is BANK?

It has not so far been decided as to how the word ‘Bank’ originated. Some

authors opine that this word is derived from the words ‘Bancus’ or Banque’ which

mean a bench. Other authorities hold the opinion that the word ‘Bank’ is derived

from the German word ‘Back’, which means ‘joint stock fund’. It is therefore, not

possible to decide as to which of the opinion is correct, for no record is available

to ascertain the validity of any of the opinions

The term bank is being used for a long time yet it has no precise definition. The

basic reason is that the banks perform not just one but many types of functions

originally the banks were supposed to make short term loans to the traders only.

The banks now not only make short term loans to the formers, traders,

industrialist etc. But also invest in a wide variety of long term earning assets.

The commercial banks also undertake and execute trust, deal in stock, shares

and debentures, issue guaranties and indemnities underwrite and sell new

securities, and deal in foreign exchange etc.

Banking industry acts as life-blood of modern trade and commerce acting as a

bridge to provide a major source of financial intermediation.

However some of the definitions of bank from different authors are as follows.

Depository financial institution: a financial institution that accepts deposits and

channels the money into lending activities; "he cashed a check at the bank"; "that

bank holds the mortgage on my home"

According to Dr. Hart

Page 12

Internship Report

“Banker or bank is a person

or company carrying on business of

Receiving money and collecting drafts for the

Customers subject to the obligation of honouring cheques

Drawn upon them from time to time by

Customers to the extends of

The amounts available

On their currents

Accounts”

In the words of G W Gilbert

“A banker is a dealer in capital

Or more properly a dealer in money.

He is an intermediate party between the borrower and lender.

He borrows one party and

Lends to the

Another”

Types of Banks

Commercial bank.

Page 13

Internship Report

Exchange bank.

Central bank or state bank.

Industrial bank.

Agriculture bank.

Investment bank.

Saving bank.

Central Bank

Every country has its central bank or state bank. Its major function is to carry out

a country’s monetary policy with an aim to safeguard its financial and economic

stability. It has the monopoly of note issue. It is also the custodian of money

market. State bank is the Banks bank and lender to the government.

Commercial Bank

Commercial banks are profit earning concerns. They receive deposits and

advance loans to the borrows. They greatly help in financing for internal and

external trade of the country.

Exchange Bank

The main function of the exchange bank is to finance the foreign trade by the

purchase and sale of foreign currencies in the form of drafts, bills of exchange,

telegraphic transfers. They also perform the function of commercial bank.

Receiving deposits and advancing loans.

Industrial Banks

Page 14

Internship Report

Commercial bank cannot afford to block their funds in long term investments. The

industrial banks receive long term deposits and finance the industries by

providing them long term credits. In Pakistan the Industrial bank named as

Industrial Development Bank of Pakistan (I.D.B.P) was established in 1961 for

this purpose.

Agricultural Bank

Agricultural bank provides short and long period loans for financing agriculture. The

agriculturists need short and long term loans for meeting their day to day and long term

requirements for making permanent improvement in the land. In Pakistan Agricultural

Bank is named as Agricultural Development bank of Pakistan (A.D.B.P) and it was

established in 1961

Investment Bank

The main function of investment bank the merchandising of shares and other

securities, managing and distributing the issue of shares and other securities.

Saving Banks

These are the institutions which are sponsored by the government for having

facilities to the people and small means. These banks collect small saving of

people and allow them to withdraw in small amounts. Also another institution i.e.

National Savings is working in the same capacity.

List of Banks in Pakistan

Page 15

Internship Report

The market for banks is diverse in Pakistan comprising nationalized commercial

banks (NCBs), Private Banks and foreign banks. In 1993, there were 33

commercial banks in

Pakistan 14 being local and 19 foreign. By the end of 2001, the number of banks

has increased to 43, 24 being local and 19 as foreign.

History Of Banking In Pakistan

Banking in fact is primitive as human society, for ever since man came to realize

the importance of money as a medium of exchange; the necessity of a controlling

or regulating agency or institution was naturally felt. Perhaps it was the

Babylonians who developed banking system as early as 2000 BC. IT is evident

that the temples of Babylon were used as ‘Banks’ because of the prevalent

respect and confidence in the clergy.

The partition plan was announced on June 3, 1947 and August 15, 1949 was

fixed as the date on which independence was to take effect. It was decided that

the Reserve bank of India should continue to function in the dominion of Pakistan

until September 30, 1948 due to administrative and technical difficulties involved

in immediately establishing and operating a Central Bank.

At the time of partition, total number of banks in Pakistan were 38 out of these

the commercial banks in Pakistan were 2, which were Habib Bank Limited and

Australia Bank of India. The total deposits in Pakistani banks stood at Rs.880

million whereas the advances were Rs.198 million. The Governor General of

Pakistan, Muhammad Ali Jinnah issued the order for the establishment of State

Bank of Pakistan on 1st of July 1948.

Page 16

Internship Report

In 1949, National Bank of Pakistan was established. It started with six offices in

former East Pakistan. There were 14 Pakistani scheduled commercial banks

operating in the country on December 1973, the name of these were:

National Bank of Pakistan

Habib Bank Limited

Habib Bank (Overseas) Limited

United Bank Limited

Muslim Commercial Bank Limited

Commerce Bank Limited

Australia Bank Limited

Standard Bank Limited

Bank of Bahawalpur Limited

Premier Bank Limited

Pak Bank Limited

Lahore Commercial Bank Limited

Sarhad Bank Limited

Punjab Provincial Co-operative Bank Limited

The Pakistan Banking Council prepared banks amalgamation schemes in 1974

for amalgamation of smaller banks with the five bigger banks of the country.

These five banks are as under:

National Bank of Pakistan

Habib Bank Limited

United Bank Limited

Muslim Commercial Bank Limited

Allied Bank Limited

Page 17

Internship Report

So, through the Nationalization of Bank Act 1974, the State Bank of Pakistan, all

the commercial banks incorporated in Pakistan and carrying on business in or

outside the country were brought under the government ownership with effect

from Jan. 1, 1974. The ownership, management, and control of all banks in

Pakistan stood transferred to and vested in the Federal Government. The

Finance Minister announced plans to start Islamic Banking system in Pakistan in

the budget speech on June 26, 1980, but it could not be possible till August,

2003.

State BANK Of Pakistan

The State Bank of Pakistan is the central bank of the country. Usually the starting

point for a central bank is a banking system that is already in place - the banking

system necessitates the presence of a central bank. But the State Bank of

Pakistan (SBP) is unique in the sense that it started its function in a newly born

country, where it also had to shoulder responsibilities of developing and

rehabilitating a banking system and the economy, in addition to the traditional

central banking functions. Performance of the Bank since its inception in 1948,

as reviewed in subsequent pages, shows that it has faced all the challenges with

a great zeal and commitment. The founders of the Bank set a multi-dimensional

target before it that included not only regulation of the monetary and credit

system but also the growth of this system. The vision of its founders was a stable

monetary system in Pakistan with fuller utilization of the country’s productive

resources (SBP Act, 1956).

2.An Overview of Organization

Page 18

Internship Report

2.1 History of NIB BANK

NIB Bank Limited started as NDLC-IFIC Bank Ltd.

which was incorporated in March 2003 as a public limited company. It started

operations in October 2003 when all assets, liabilities, rights and obligations of

the former National Development Leasing Corporation (NDLC) and Pakistan

operations of IFIC Bank were amalgamated with and into the Bank with a paid up

capital of Rs.1.2bn. In April 2004 the Pakistan operations of Credit Agricole

Indosuez were also amalgamated with and into NIB. In March 2005 Temasek

Holdings of Singapore acquired 25% shareholding in NIB Bank, through Bugis

Investments. This shareholding was further enhanced to over 70% in June '05

following an increase in NIB's paid up capital to Rs 3.4 bn. NIB Bank has since

grown rapidly from a base of 2 branches in 2003 to 45 in the 4th quarter of

2007, with a corresponding increase in its assets and deposits base.

NIB Bank's vision is to rank amongst the top 5 banks in the country. Therefore

towards the end of June 2007 it acquired majority shares of PICIC with the aim of

merging PICIC and its commercial banking subsidiary PICIC Commercial Bank

Limited (PCBL) into NIB. The acquisition was financed through the country's

largest private sector rights issue, with resultant increase in NIB's paid up capital

to Rs.22.0 bn. The PICIC acquisition bought with it another subsidiary "PICIC

AMC" and an affiliate "PICIC Insurance".

NIB already has a shareholding in NAFA, an Asset Management Company

(AMC) whose shareholders also include National Bank of Pakistan and Fullerton

Fund Management Company; thus NIB Group’s asset management business

has also increased, while it has diversified into the insurance business as well.

Page 19

Internship Report

The legal merger of PICIC & PCBL into NIB took place on December 31, 2007,

once all regulatory approvals were in place. NIB Bank continues to be led by

Khawaja Iqbal Hassan, supported by four business heads and ten business

enabling function heads.

The merger resulted in a vastly expanded network of 240 branches and total

assets of Rs 176.6 bn on merger date. NIB has the second highest paid up

capital of Rs. 28.4 bn amongst banks and ranks number 7 in terms of distribution

network. Merger synergies include lower cost deposits, enhanced customer

service delivery channels and overall improved efficiencies. These help provide a

competitive edge in the face of increasing competition in the banking sector.

Temasek Holdings continues to be the largest single investor in NIB Bank with

approximately 63% shareholding.

The powerful franchise of the three merged entities has been brought together to

form a much larger and stronger bank to complete in the market place. Going

forward management is confident that the combined bank will be a top performer

delivering a wide range of financial services through an extensive branch

network. The asset management arms and insurance affiliate are also expected

to perform well and provide an attractive dividend stream for NIB.

Temasek Shareholding

Temasek Holdings is an Asia investment house headquartered in Singapore.

With a multinational staff of 380 people, Temasek Holdings manages a portfolio

of over S$172 billion, or more than US$120 billion, focused primarily in Asia and

Singapore.

Guided by an independent board, Temasek Holdings operates autonomously on

commercial principles to maximize long-terms returns. Its total shareholder

return since inception 35 years ago is more than 16% compounded annually.

Temasek Holdings has a corporate credit rating of AAA/Aaa by Standard &

Page 20

Internship Report

Poor's and Moody's respectively.

President

Khawaja Iqbal Hassan: President and CEO

Khawaja Iqbal Hassan is the President and Chief Executive Officer of NIB Bank. NIB Bank is the fastest growing commercial bank in Pakistan and has recently acquired controlling shares in Pakistan Industrial Credit and Investment Corporation (PICIC) and PICIC Commercial Bank. Mr. Iqbal Hassan is the founder of NIB Bank, which he created in 2003 through the merger of Pakistan’s then largest leasing company, NDLC, and the domestic branches of IFIC Bank. This was followed by an acquisition of the domestic branches of the French bank, Credit Agricole Indosuez.

Mr. Iqbal Hassan was the driving force behind the creation of National Fullerton Asset Management Company (NAFA) which is Pakistan’s fastest growing and best performing asset management company. NAFA is a joint venture between NIB, National Bank of Pakistan and Fullerton Fund Management, a subsidiary of TemasekHoldings.

Prior to starting NIB, Mr. Iqbal Hassan conceptualized and founded Global Securities in 1994. Global is one of the largest and most active corporate finance and securities houses in Pakistan. In 1996 Global became a joint venture partner of UBS AG, one of the largest banks in the world and continues to work with UBS AG in Pakistan. Global holds an unmatched s uccess record of having completed over 55% of all privatizations in Pakistan.

Landmark transactions managed by Global include the largest IPO in terms of number of investors (KAPCO); the largest IPO in terms of rupee value (Habib Bank); the largest domestic bond offerings (KESC and PIA); the first sub-debt issue by a commercial bank in Pakistan (MCB); buy-side advisories for the privatization of Habib Bank and United Bank, and domestic advisory on the only exchangeable bond offering for the Government of Pakistan. Global was also domestic advisor for the US$ 2.6 billion privatization of Pakistan Telecom. Global has also served as the adviser for the restructuring of PIA on two occasions.

Page 21

Internship Report

Before starting Global Securities Mr. Iqbal Hassan was the Regional Business Group Head and Vice President for Citibank in Pakistan. He was responsible for managing Citibank’s Local Corporate Group, Financial Institutions Group, Product Development and Securities Services Groups. Mr. Iqbal Hassan also served internationally as the Corporate Bank Head and Vice President, in Istanbul, Turkey on secondment to Saudi American Bank, a managed-affiliate of Citibank. Mr. Iqbal Hassan was the founder of the bank in Turkey where he envisioned and implemented the bank’s business plan focused on fee-based merchant banking and commercial banking businesses, fixed income and foreign exchange arbitrage. Prior to that Mr. Iqbal Hassan served as the Unit Head of the Construction Division of Saudi American Bank in Riyadh. He started his banking career at the Special Projects Team in Citibank New York where he was deployed on the task forces that re-scheduled foreign debt and conducted the de-freezing of assets of developing countries.

Mr. Iqbal Hassan obtained his Bachelor of Science degree in Business Administration from the University of San Francisco in 1980 from where he graduated with academic honors and majored in Finance and Marketing. He also holds a degree in Accountancy from the City of London Polytechnic.

In addition to his contributions to the development of the financial and banking sectors in Pakistan Mr. Iqbal Hassan serves/has served as a Board member of the following companies:

NIB Bank Limited.

PICIC.

PICIC Commercial Bank.

PICIC Insurance.

National Fullerton Asset Management Company Limited.

Civil Aviation Authority of Pakistan.

Pakistan Steel Mills Limited.

Habib Bank Limited.

Page 22

Internship Report

Global Securities Pakistan Limited.

Citicorp Investment Bank Pakistan Limited.

The Pakistan Fund.

The Central Depository Company of Pakistan Limited.

In view of his contributions to the field of banking and finance, Mr. Iqbal Hassan was conferred the Sitara-i-Imtiaz, Pakistan’s highest civilian award in 2007.

Ownership Profile

NIB BANK LIMITED Stockholders' Information as at March 31, 2010

Page 23

Particulars/> Shareholding Percentage

606Associated Companies / Undertakings, Related Parties, Directors, Chief Executive Officer, and their spouse and minor children

3,011,828,360 74.4815

NIT & ICP 34,301,653 0.8483Banks, Development Financial Institutions, Non Banking Financial Institutions

124,895,108 3.0886

Insurance Companies 7,247,594 0.1792Modarabas and Mutual Funds 7,606,338 0.1881

Public Sector companies & Corporations 250,618,626 6.1977General Public (including local & foreign individual) 459,058,320 11.6524Foreign Companies 14,045,558 0.3473Others 134,125,519 3.3169Shares held by 29,429 Shareholders 4,043,727,076 100.0000

Internship Report

Page 24

Board Of Directors

Francis Andrew Rozario Chairman

Syed Aamir Zahidi DirectorTejpal Singh Hora DirectorAsif Jooma DirectorMr. Muhammad Abdullah Yusuf DirectorTeo Cheng San, Roland DirectorMr. Najmus Saquib Hameed DirectorKhawaja Iqbal Hassan Director and President / CEO

Internship Report

2.2 Nature of NIB Bank:

Vision and Mission

Our Mission:

To improve the quality of life for millions

Our Core Purpose: Enabling success; Realizing dreams

Our Vision: To be the most admired Financial Institution in Pakistan

Our Values:

PASSION

RESPECT

INTEGRITY

EXCELLENCE

FAIRNESS

Passion

I am driven

I am committed

I am determined

I believe in what I do

I embrace life

Respect

Page 25

Internship Report

I appreciate different viewpoints

I am receptive to the diversity of ideas

I treat others as I would want to be treated

I look after the community in which we live and work

I contribute to the care and comfort of those around me

Behaviors: Integrity

I do what I say

I am honest and forthright

I never compromise my values

I am open and honest in all my dealings

I have the courage to stand up for what I believe to be true

Excellence

I strive for better

I exceed expectations

I am constantly improving

I always try to get it right the first time

I produce error free, superior quality work

Fairness

I am impartial

Page 26

Internship Report

I judge on merit

I don’t expect favours

I listen to both sides

I reward what you do not who you are

2.3 Features of NIB Bank

Page 27

Internship Report

Product Lines:

Salaam Banking

Salaam is an everyday salutation, a special tribute, a mark of admiration,

an expression of respect that is communicated through a gesture, a nod, a

salute or a

handshake.

By saying Salaam we mean to pay homage to the people belonging to self

employed mass market which includes small enterprises as well (retailers,

traders & services). We commit to serve these hard working people with a strong

belief that we are “privileged” to be their banking partner. We will assist them in

their business financial needs by providing them basic and advanced banking

services at their door step and we will do it with dedication and respect because

they value respect more than any thing. Our unique proposition provides our

customers with:

Basic and modern banking facilities.

Account opening with no minimum balance requirement.

Dedicated relationship officers to assist and consult for financial matters.

Branch presence close to customers.

Business loans, insurance and other value added services provided

through one stop shop.

Products Of Salaam Banking

Salaam Business Account

Page 28

Internship Report

The Salaam Business Account is a Pak Rupee current account with value

added transactional services designed specifically for the Salaam segment.

Features:

The savers can subscribe to other services including: ATM, Salaam

DirectPay, Salaam Cash Guard, Salaam Committee and Salaam Sahulat

(Cash Collection Services).

Fully dedicated relationship officer for the customer.

No minimum balance requirement.

No limitations on the number of withdrawals and deposits through any

channel.

Benefits:

No online transaction charges through a growing network of Salaam

and NIB Bank Limited branches.

ATMs of all other banks can also be used by paying a nominal charge.

Highlights:

Convenience of monthly bill payments through one-off or standing payment

instructions acceptable at branch and call center as well as all front end

Page 29

Internship Report

channels to be added in the future (e.g. mobile banking).

The customer will also be able to make the regular payments for other Salaam

products availed (such as loans and insurance) through direct debits to the

same Salaam Business Account.

Salaam Bachat Account

The Salaam Bachat Account is meant for customers who wish to accumulate and consolidate their disposable income to meet future financial needs.

Features:

A saving account that offers attractive returns without imposing minimum balance requirements.

Benefits:

Will encourage saving habit for customer’s financial security.

Highlights:

The savers can subscribe to other services including, ATM, Salaam Direct pay, Salaam Cash Guard, Salaam Committee and Salaam Sahulat (Cash Collection Services).

Salaam Committee Salaam Committee is a unique product that combines the benefits of a saving

plan with an insurance cover.

It enables households to regularly put aside a portion of their income for savings

to achieve their desired amount while also availing the financial security of an

insurance plan. Salaam Committee enables our valued customers a highly

accessible, convenient and attractive avenue for regular savings by providing

increasing incentives over time.

Features:

Page 30

Internship Report

Minimum monthly deposit amount starts from as low as Rs.1000. Save at your convenience and become entitled for bigger bonus (es) as

you continue to save. *

Insurance coverage option available equal to 65 times of the monthly contribution amount.**

Free Current or Savings checking account with all applicable features.

No partial encashment allowed.

In case of encashment the entire scheme would terminate, including the insurance cover. **

No early encashment charges applicable from 7th monthly contribution onwards.

Benefits:

Get additional bonus installments after every 12 payments (first bonus payment

to start after completion of 24 payments. The longer you continue, the higher the

bonus contributions you earn.

The customer can opt for Depositor’s Insurance Option for no extra charges.

This represents coverage for Life and Permanent Total Disability up to 65 times

his monthly contribution or a maximum or Rs. 2 million whichever is lower.

NIB Committee is a unique product that combines the benefits of a savings plan

with an insurance cover.

It enables savers to regularly put aside a portion of their income across their

savings horizon to achieve their desired amount while also availing the financial

Page 31

Internship Report

security of an insurance plan.

Pricing

Annualized rate of expected return ranges from 3.90% to 5.15% depending upon

the number of contributions and tenor.

Contribution Deduction Date *

The Monthly Contribution amount will be deducted on the Deduction Date which

is the tenth (10th) of every month from the customer’s specified account or in the

event of insufficient balance being available in the customer’s specified account

on such date, such other two (2) dates as may be determined by the Bank, at

which time the account will be deducted directly to make the Monthly

Contribution payment. Such deduction of the Monthly Contribution amount shall

continue to be valid until the termination of the NIB Committee Plan.

*Revised deduction dates applicable to all existing Customers of NIB Committee

Plan.

Is there any limit to my insurance coverage amount?

Yes, your insurance coverage entitlement based on your age is given below:

Maximum Age

Limit

Maximum Coverage

Amount

Maximum Contribution

Amount

(65 times of monthly contribution amount)

Up to 40 years Rs. 2,000,000/- Rs. 30,500/-

41 to 50 years Rs.1,500,000/- Rs. 23,000/-

51 to 60 years Rs.1,000,000/- Rs. 15,000/-

Page 32

Internship Report

3% penalty applicable if encashed any time prior to the completion of 7

monthly contributions.

The scheme automatically terminates on 3 consecutive missed monthly

payments.

WHT applicable on profit on a monthly basis.

Zakat payable as per applicable laws unless exempted.

Annualized rate of expected return ranges from 3.90% to 5.15%

depending upon number of contributions & tenor.

Salaam Fixed Deposit

The Salaam Fixed Deposit will cater to customers who already have

accumulated savings and wish to preserve and increase their value.

Features:

The product will offer a monthly payout option as well as long term

Pay outs at maturity.

Minimum balance requirement is Rs. 5,000.

Benefits:

High rates of return.

Highlights:

The customer will be able to obtain overdrafts against these fixed deposits in

Page 33

Internship Report

order to meet short term liquidity needs.

Page 34

Internship Report

Mortgage Loan Insurance

NIB is also working towards allowing the customers to fulfill their long term business

needs by offering Cash Against Property, where the customers can avail financial

services and improve upon their business by simply applying for a mortgage loan

along with which you will be able to insure your homes in assistance with the bank.

Page 35

Internship Report

Features:

Higher loan amounts.

Longer tenure.

Benefits:

Lower interest rates.

Floating rates will be available in future.

Highlights:

Customized mortgage loan according to customer requirement.

Financing available against residential as well as commercial property.

Salaam CashGuard

Salaam CashGuard safeguards your cash withdrawn through ATMs and Over-the-

Counter against the risks of forced snatching through armed hold-ups or burglaries.

We offer a pre-underwritten insurance coverage in two different packages to our

customers in collaboration with New Jubilee Insurance Company Limited.

Features:

The two plan options available for CashGuard are as follows:

Option/

Coverage

Maximum Cover (ATM & OTC)* Monthly Service

ChargesPer Event Per Year

Plan A Rs. 20,000/- Rs. 40,000/- Rs. 190/-

Page 36

Internship Report

Plan B Rs. 50,000/- Rs. 100,000/- Rs. 230/-

*The insurance cover would be applicable for a period of one month (from the date of

enrollment to the same date of the next month), provided that the service charges are

paid for that month

Benefits:

Payments are made automatically by debiting your account.

Convenience at your doorstep.

Quick turnaround time for claim reimbursement.

Coverage for all ATM transactions from any bank in Pakistan.

Coverage for all cash transactions from any NIB branch in Pakistan.

Easy to subscribe and unsubscribe.

Highlights:

Convenience for the customer.

Offers 24/7 coverage for all your cash transactions.

ATM

Features:

Page 37

Internship Report

Make Cash Withdrawals

Get access to your accounts and make cash withdrawals 24x7.

Per Transaction Limit: Rs. 20,000.

Daily Limit: Rs. 50,000.

Pay Bills

Add, View and Pay your Utility & Mobile Bills, Reload / Top-up your Prepaid Mobile

connections.

Utility Companies – SSGC, SNGPL, KESC, PTCL, IESCO, HESCO and GEPCO

Mobile Companies – Ufone, Mobilink.

Prepaid Vouchers

Buy Prepaid Electronic Vouchers of ISPs, Calling Cards and Mobile Phones.

ISPs (Gerrysnet, Cybernet, Onspeed).

Calling Cards (PTCL & VPTCL)

Mobile Vouchers (Mobilink, Ufone, Zong, Telenor, Warid).

Funds Transfer from NIB to Other Banks

Through Inter Bank Funds Transfer from NIB to any 1-Link member Bank.

Per Transaction Limit: Rs. 50,000.

Per Day Transaction Limit: Rs. 250,000.

Transfer Funds within NIB

Instant funds transfer from NIB-to-NIB Accounts.

Per Transaction Limit: Rs. 50,000.

Page 38

Internship Report

Per Day Transaction Limit: Rs. 250,000.

Balance Inquiry

Keep an eye on your accounts and balances with the Balance Inquiry facility available

at NIB ATMs.

Mini Statement

Print last 10 Transactions of your account anytime.

PIN Change

Change your ATM PIN at your convenience.

Salaam CashGuard

An optional Cash withdrawal ATM Insurance service that allows the customer to be

covered for any unfortunate event of having their money snatched after an ATM

transaction.

Salaam DirectPay

A hassle free bill payments and transfers facility whereby customers can pay their utility

and mobile bills and transfer funds at their own convenience. Life

DirectPay offers the following services:

Electronic fund transfers.

Prepaid vouchers.

Utility bill payments.

Mobile bill payments and top-up

Page 39

Internship Report

Phone Banking

Bank at your convenience

NIB Phone Banking is a distinctive and efficient 24/7 Non-Stop Banking service available

for NIB customers. It is a virtual medium for existing and prospect customers to fulfill

their day to day financial needs through the telephone.

SCall our phone banking at 0800-00039 and make use of our phone banking for the

following:

Product Information

Loan Account Information Product Information

Application Status

Installment Repayment Inquiry

Branch Banking Information

Deposit Account Services Account Inquiry

Balance Inquiry

ATM Card Services ATM Card Activation

ATM Card Blocking

ATM PIN and TPIN Generations

ATM Card status and inquiry

ATM cash disputes

Updating customer personal information

Value Added Services

DirectPay - Bill Payments Funds Transfers

Bill Payments

Page 40

Internship Report

Mobile top up and other payments

CashGaurd – ATM insurance Inquiry

Complaints

Activations

Deactivations

IVR Services TPIN and ATM PIN Change

Loan Installment Details

Last 5 transactions

Balance Inquiry

Salaam DirectPay

Salaam DirectPay is a convenient bill payment and funds transfer facility whereby you can

instruct instant payment of your bills and transfer funds from your NIB bank account at

your own convenience and luxury.

Your payments are made quickly and conveniently, and you no longer have to track

payment due dates, wait in long queues or suffer late payment charges. You can easily

pay your bills or transfer your funds through ATMs and/or Phone Banking 24 hours a day,

7 days a week. You can also ensure automatic payment of your bills and transfer of funds

from your NIB bank account by setting up direct debit

instructions and specifying your payment schedule.

Page 41

Internship Report

Features:

Salaam DirectPay offers the following services:

1. Utility Bill Payments

This service is available at NIB ATMs, Phone Banking and Branches. It is

available for both one-off and DirectDebit and only for the following companies:

KESC.

SSGC.

SNGPL.

PTCL.

IESCO.

HESCO.

GEPCO.

2. Mobile Bill Payments and Prepaid Mobile Top-up

This service is available at ATM, Phone Banking and Branches. It is available for

both one-off and DirectDebit and only for the following companies:

Ufone.

Mobilink

3. Fund Transfers

Within NIB This service enables customers to transfer funds from their NIB

account to any other NIB account. This service is available at ATMs, Phone

Banking and Direct Debit.

Page 42

Internship Report

Inter-Bank Funds Transfer

This service is only available at ATMs and only for transfers to accounts of the

following banks:

Royal Bank of Scotland (formerly ABN Amro)

Askari Commercial Bank

Allied Bank

Bank AL Habib

Bank Alfalah

Bank Islami Pakistan Limited

Habib Bank Limited

Soneri Bank Limited

Tameer Micro finance Bank Limited

Union Bank Limited / Standard Chartered

United Bank Limited

ATMs MobileMobile Prepaid vouchers for the following companies are available through Life

DirectPay.

Warid.

Mobilink.

Page 43

Internship Report

Zong.

Ufone.

Telenor.

Internet

Internet Prepaid vouchers for the following companies are available through Life

DirectPay.

Cybernet.

Gerrysnet.

On Speed.

Si3.

Calling Cards

Calling Card vouchers for the following companies are available through Life

DirectPay.

PTCL.

VPTCL.

Lifebanking

Page 44

Internship Report

Lifebanking will assist you in managing all your banking needs at

your office, you no longer have to stand in long queues or get stuck in traffic

jams. With your busy working schedule, Lifebanking would take care of all your

financial matters giving you more time to spend with your dear ones.

We aim at becoming your sole banking partner so you can enjoy every moment..

Lifebanking offers solutions for cash flow requirements, saving & investment

needs and for day to day financial transactions.

If you are a salaried individual, Lifebanking offers you:

Life Salary Account: One account from where you can manage your entire

monthly expenses.

Services at your office.

Assistance in saving for future.

Wide range of financing available to cater to all your needs.

Automatic payments for utility bills & monthly installments.

More than 100 ATMs across Pakistan

Products Of Life Banking

Page 45

Internship Report

Life Salary Account

Life Salary Account is a PKR current account that will provide the convenience of

managing the cash outflows for the month. Every month the companies would

either disburse your salary in these accounts or you can directly deposit it in your

Life Account.

Payment of utility bills, fees, loans etc, would be tagged to this account. If you

want us to save for you, we will maintain a certain amount each month. Products

and services availed by the employee would be tagged to this account and

individual can manage all

bill/fee payment, savings and investment and repayments via this account.

Features:

A current account with zero minimum balance requirement.

Free of charge ATM card for your usage.

Automatic payments of bills and fees.

Benefits:

Hassle free payments for your dues directly through your account.

All products and services tagged to your salary account.

NIB Tajir

Page 46

Internship Report

A Current Account for businessmen on the go!!

NIB Taajir Account is a business transaction management tool; a current account

that provides convenience to you to facilitate your business by managing the

cash outflows and inflows.

This account offers various features and benefits that enable a business to fulfill

all banking requirements ranging from payments to receipts; which include

payments to suppliers, vendors, utilities, service providers and salary

disbursement to employees. On the receipts side it includes collection and

management of receivables.

Tagged Products and Services

NIB Connect – Interbank Funds Transfer Facility

NIB Protect – Cheque Bounce Protection Facility

NIB Direct – Bills Payment and Funds Transfer Facility

NIB Sahulat – Cash Collection from customer premises

NIB Alerts – SMS & e-statements

NIB PaySys – Automated Salary disbursement Solution

Product Offering

Free Online Banking

Taajir account can be accessed from all NIB branches for the purpose of account

information, deposits, withdrawals, funds transfer, etc.

Page 47

Internship Report

Free Cheque Book (First)

First cheque book will be issued free of cost consisting of 25 leaves, all

subsequent cheque book issuance will be charged as per respective segment

SOC.

Free Pay Order Issuanc

Making payments via payorder is easy and cost effective for NIB Taajir account

holders.

Free Demand Draft (Drawn on NIB Branches)

Demand Draft issuance will be charged as per the respective branch segment.

Prepaid Vouchers and Other Payments)

ATM or call center. Through direct pay you can pay utility bills, mobile bills, get

prepaid vouchers and make payments to other NIB accounts. The facility is

available free of costto all Taajir account holders.

NIB Sahulat* (Cash Collection Facility from Customer Premises)

NIB Saluhat offers the convenience of cash collection from your business

premises upto a maximum amount of Rs.500,000/- per visit, automated deposit

slip is issued to the customer through a POS machine at the customer premises.

*Charges applicable as per SOC

Page 48

Internship Report

Life Profit Account

Life Profit Account is a PKR saving account providing saving avenues for the

salaried individual.

With minimal balance requirement and ease of opening this account the

customer can start depositing the monthly small contributions to this account and

earn profit based on daily balance on these savings.

Features:

Profit account opened with a balance of Rs. 5000.

Saving amount can be transferred to Life Profit Account simply through

Payroll Accounts.

o Inter Bank Funds Transfer – Banks on One link and IBFT certified.

o Cheque.

o Cash

Life Committee

It enables households to regularly put aside a portion of their income for savings

to achieve their desired amount while also availing the financial security of an

insurance plan. Life Committee enables our valued customers a highly

accessible, convenient and attractive avenue for regular savings by providing

increasing incentives over time.

Features:

Minimum monthly deposit amount starts from as low as Rs.1000.

Page 49

Internship Report

Save at your convenience and become entitled for bigger bonus(es) as you

continue to save. *

Insurance coverage option available equal to 65 times of the monthly

contribution amount. **

Free Current or Savings checking account with all applicable features.

No partial encashment allowed.

In case of encashment the entire scheme would terminate, including the

insurance cover.

No early encashment charges applicable from 7th monthly contribution onwards.

The contribution will be deducted on the tenth (10th) of every month or in the

event of insufficient balance being available on the 10th , on any such other two

(2) dates of that month as may be determined by the Bank.*

Applicable after completion of 24 payments, bonus increases after every 12

contributions.

Benefits:

Get additional bonus installments after every 12 payments (first bonus payment

to start after completion of 24 payments. The longer you continue, the higher the

bonus contributions you earn.

The customer can opt for Depositor’s Insurance Option for no extra charge. This

represents coverage for Life and Permanent Total Disability up to 65 times his

monthly contribution or a maximum or Rs. 2 million whichever is lower.

Life Committee is a unique product that combines the benefits of a savings plan

with an insurance cover.

Page 50

Internship Report

It enables savers to regularly put aside a portion of their income across their

savings horizon to achieve their desired amount while also availing the financial

security of an insurance plan.

Highlights:

Life Committee provides for a Forced Savings Avenue for the customers.

It also allows the customers the Convenience to contribute to their

growing savings.

It provides Safety and Security of your money with a reputable

organization.

It provides Free insurance coverage incase of an unforeseen event.

It provides for Growth in savings with bigger bonuses over time.

It provides Free checking account facility without minimum balance

requirement.

Pricing:

Annualized rate of expected return ranges from 3.90% to 5.15% depending upon

the number of contributions and tenor.

Life Personal Installment Loan

Life Personal Installment Loan provides personalized financing so you can

quickly pay off your liabilities, meet marriage expenses, make vital investment in

your child’s education or simply refurnish your house.

Life Corporate Loan

Life Corporate Loan is an installment based loan for salaried individuals, secured

Page 51

Internship Report

by the employer guarantee.

This facility is only available to employees of companies having secured loan

agreement with NIB Bank Limited. This loan would assist in meeting short-term

and long-term needs of a salaried individual without having any impact on the

provident fund balance accumulated and the returns on the provident fund.

Features:

Financing facility up to Rs. 500,000.

Credit Life Insurance option can provide security to you and your family in

times unfortunate events.

Free Life Current account with no minimum balance.

Peace of mind provided to you by managing your payments through Life

Current Account.

Loans at lower interest rates.

Life Auto Financing

NIB Auto Finance is an installment based financing and provides you with the

facility of buying a new or a used car with a minimum 10% down payment with

other product benefits.

Life Salary Advance

Overview

Life Salary Advance allows eligible customers to withdraw up to 25% of their net

monthly salary or a limit of PKR 100,000 whichever is lower by paying a minimal

upfront fee. This facility is valid for the entire month and the limit is refreshed

Page 52

Internship Report

when the customer’s salary is disbursed.

Features & Benefits:

Only for customers whose company payroll is with NIB Bank

Customers are pre-approved

Facility valid for 1 month; refreshed when salary is disbursed

Facility valid for 1 month; refreshed when salary is disbursed

Limit is up to 25% of net salary or PKR. 100,000 whichever is lower

Utilized amount is recovered through subsequent salary disbursal

Fee is deducted upfront from desired amount

Available only on NIB ATMs

Life Mortgage

Overview

Finding a competitive home loan which serves all of your needs is hard to come

by. Life Mortgage Loan is the answer to all your troubles. Just choose your ideal

home and we will do the rest! From initial documentation to the final

disbursement, you will experience seamless customer service. Read on for all

your queries.

Page 53

Internship Report

The following branches provide Life Mortgage facilities:

Landhi Branch,Karachi Clifton Branch,Karachi

Khalid Bin Walid Br.,Karachi Rashid Minhas Road,Karachi

SITE Branch,Karachi Korangi Industrial Area Branch,Karachi

West Wharf Road

Branch,KarachiNorth Karachi Industrial Area Branch,Karachi

Feature & Benefits

Types of Facilities offered:

Buy a Home:

A Mortgage loan specifically devised for customers who want to buy or build

their ideal home.

Balance Transfer Facility

By availing the BTF, customers can transfer their mortgage home loan to NIB

Bank.

Financing Limits and Security:

The loan granted under Life Mortgage will be secured against residential

property only. The financing limits will be based on the type of collateral ranging

from Rs. 500,000 to Rs. 20 Million*

(Limits are subject to type of collateral)

Tenure:

Minimum: 3 years Maximum: 20 years

Page 54

Internship Report

Moral Values of Employees:

Moral values of employees are very high and these moral values include.

PASSION

RESPECT

INTEGRITY

EXCELLENCE

FAIRNESS

2.4 Competitors:

The main competitors of the bank are:

Askari Commercial Bank.

Union Bank

Prime Commercial Bank.

Muslim Commercial Bank

Allied Bank

Al falah Bank

Soneri Bank

Page 55

Internship Report

3.Organizational StructureHierarchy Chart

Page 56

President / CEO

Group Leader

Cluster Manager

Manager

Relationship Manager

Operation Manager

Counter Service Supervisor

Counter Service Officer

Branch Service Officer

Personal Banking Consultant

Date Center Incharge

Internship Report

3.2 Number of Employees:

The overall Staff at NIB Bank branches are detailed below.

Page 57

Internship Report

(Numbers)

STAFF STRENGTH 2009 2008

Permanent 4,925 5,131

Temporary / on contractual basis 72 142

Group's own staff strength at the end of the year 4,997 5,273

Outsourced 1,430 1,656

Total staff strength 6,427 6,929

Trer are 34 employees in the branch where I did my internship.

3.3 Main Offices:

To cater to the diverse financial needs of the businesses spread across the

country, NIB has established five corporate centers in major Business and

Industrial hubs as follows:

Karachi:

Address: Muhammadi House, I.I.Chundrigar Road, Karachi.

UAN: 021-111-333-111

Direct: 021-32469413 / 32427413

Fax: 021-32415582

Lahore:

Address: NIB House, 2nd Floor, 14-A, Old Race Course Road, Shahrah-e-Awan-

e-Tijarat, Lahore.

PABX: 042-99200522

Direct: 042-36282731-4

Fax: 042-99201993

Islamabad:

Address: 1st Floor, Post Mall, F-7 Markaz, Islamabad.

Page 58

Internship Report

UAN: 051-111-333-111

Direct: 051-2608001-4

Fax: 051-2653448

Faisalabad:

Address: NIB Liaquat Road Branch, Faisalabad.

UDirect: 041-2610406 / 2620268

Multan:

Address: 66 Abdali Road Branch, Multan.

UAN: 061-111-333-111

Direct: 061-4781454

Fax: 061-4583041

3.4 Introduction of all departments

There are 3 main departments at the branch:

Page 59

Internship Report

1. ACCOUNT OPENING DEPARTMENT.

2. OPERATIONS DEPARTMENT.

3. TRADE FINANCE DEPARTMENT.

ACCOUNTS OPENING DEPARTMENT

Account opening Department is considered a blood-pumping instrument (heart)

in the banking sector. This department is considered very important in consumer

banking because it serves as a liaison between the customers and the bank.

During my training in this department I have learned a lot of things a few of which

are following.

The prospective customers who approach the bank for the purpose of account

opening are of several categories. For example, individual account holders and

corporate account holders. Corporate account holders are subdivided into

several categories such as

There are different requirements for different categories. Individual accounts are

on the name of persons while corporate accounts are on the name of business.

For the account opening of corporate customers several documents are required

like the certificate of incorporation etc. The higher the level of business the

complex is the requirements of account opening. In addition to account opening

this department is also responsible for issuance of chequebook, issuance of

loose cheques and issuance of account statements.

RULES FOR OPENING & OPERATION OF PLS ACCOUNTS

The procedure of opening the current and saving accounts is same, which

is as follows:

Page 60

Internship Report

1) The Accounts may be opened on an application made on the bank’s

prescribed account opening form.

2) The accounts may be opened in the name of an individual, jointly in the

names of two or more persons. These accounts may also be opened by the

charitable institutions or for provident fund & other funds of benevolent

nature by local bodies, autonomous corporations, companies, associations,

societies and education institutions.

3) The account should be opened after obtaining a proper introduction.

4) Not more than one account may be opened in any one name except in

cases where such accounts are opened in the name of parent or guardian

for more than one child.

5) A verified copy of National Identity Card should be obtained while opening

the account.

6) A distinctive number will be allotted to each account.

7) The signatures of account holder should be admitted on the AOF and SS

cards.

8) The signatures of the introducer should be verified on the AOF.

OPERATIONS DEPARTMENT

FUNCTIONS PERFOMED:

CLEARING

Page 61

Internship Report

REMITTANCE

Clearing

Inward clearing

Outward clearing

Inward clearing

In the morning, the bank receives its own cheques, which have been presented

by the customers in some other bank to be deposited in their account. NIFT

provides the facility of bringing cheque for inward and also takes the cheques of

outward clearing to other banks. The cheques received in inward clearing are the

cheques drawn on bank and the bank has to pay for them. For this purpose the

bank makes clearing in computer by checking the balances of the respective

customer, if their balances are up to the mark then that cheque is cleared and the

respective customer account is debited with the respective amount. If the

balances are short then that cheque is bounced back to the related bank.

Outward clearing:

Brighter Future All the cheques of other banks which are deposited to FBL are

presented in outward clearing. This is said as outward clearing because they

are presented on the very next day after depositing a cheque.

In outward clearing, the entry is made like:

Customer Account Cr.

State Bank of Pakistan Dr.

Page 62

Internship Report

This entry is made when we come to know about the clearing of all cheques,

which are sent to other banks.

Services provided

I. TRANSFER OF AMOUNT

II. TELLING ACCOUNT BALANCES

III. ISSUING CHEQUES BOOKS

I. TRANSFER OF AMOUNT

If a customer holds two accounts in the bank and he/she wants to transfer money

from one account to other account, customer writes a cheque and fills deposit

slip in which he/she writes account number to which amount is to be transferred.

After making transfer entry in the computer, affix transfer stamp in the middle of

the cheque, crossing on the upper left and bank’s endorsement stamp on the

backside of the cheque.

Ii. Telling account balances

Whenever clearing officer receives phone call from the customer inquiring about

his/her account balance after confirming the name, address and other

information he tells the balance through computer.

Iii. Issuing cheque books

It is also the duty of department to issue a chequebook when an officer receives

request from the customer.

Remittance

Following are the functions of remittance department

Recovery of various charges as per schedule of charges

Page 63

Internship Report

Issuance of Demand drafts, Pay orders and Telegraphic Transfer:

Lodgment of outward bills and follow up for recovery

Telegraphic transfer

TT is prepared against cash or cheques. The Telegraphic Transfer is the

quickest and the most rapid mode of remitting money from one place to another.

Under T.T. the remittance takes place through telegram, telex, cable and in some

instances, on telephone. The applicant fills the application form specifying the

name of the payee, place of transfer and the amount.

The T.T. is issued in a particular tested message and under a test number.

The drawee branch makes payment only after the verification of the test

number.

Demand drafts

A bank draft is an order instrument issued for payment of a certain sum of money

to or order of a certain person and draws on one office of the bank by another

office usually. Unlike a cheque DD is bank’s liability and the bank has the

responsibility concerning payment. A customer prepares a DD from the bank

in case the payment is certainly to be made. Unlike a cheque there is no

problem of refusal of payment, due to various reasons such as insufficiency

of funds etc. In this case both the payer and the payee are the account

holders of the same bank but in different cities.

The drafts may be drawn on offices of other banks under the agency

arrangements. There are three parties to the draft:

DRAWER: Issuing bank

DRAWEE: The bank on which the draft is drawn.

PAYEE: The named person to whom the payment is to be made.

Bank issued a Demand Draft when it received a written request either on

the bank’s standard application form or on a separate paper signed by the

applicant enclosed with cash or cheque covering the amount of the draft

and other charges of the bank.

Page 64

Internship Report

Pay order

A “Payment Order” is an instrument drawn by a Bank on itself. It is issued

when the funds are intended to be remitted within the city. The payment

orders are generally issued for anyone of the following practical purposes:

a. To facilitate all locally payable expenses on account of a bank for the

reason that such payments are not executed through cheques,

b. For the sake of inland and foreign remittances in cases where the

beneficiaries do not maintain account with the bank.

c. For all local payments under instructions of the customers for sundry

purposes like payment of insurance premium, payments to third parties,

club bills, rent and taxes, etc.

Pay order is the account payees only mean it is only pay to the person who’s

name is written on the pay order. It is issued by the bank after filling a specific

form by the customers.

Foreign telegraphic transfer (ftt)

As per instructions of the account holder in foreign currency, the bank arranges

the transfer of the stated currency to the desired bank in the respective country.

Depending upon the particular type of currency the telex is sent to a bank in

the country, to which the currency belongs and in that country the bank has

the account with number of banks, which act as its correspondents.

Foreign Telegraphic Transfer is also known as FTT. The customers, who want to

transfer the funds from Pakistan to other country, have to inform the bank.

Because this department has to inform to Treasury department in Head Office to

arrange the transfer of funds, which is directly involved in the respective

transaction, as the function of the treasury department is to monitor the local

and foreign currency accounts of all the branches of the bank. Moreover it

also monitors the details pertaining to these accounts such as availability of

funds etc. In other words we can say, this department informs the treasury

Page 65

Trade Finance Department

Import Department

Export Department

Internship Report

department that this much amount of foreign currency should be arranged in

desired country where the funds are to be transferred. Moreover the customer

who wants to transfer the funds should have a foreign currency account in the

bank. Because State Bank made the restriction that foreign transaction is only

done through the foreign currency account.

Foreign demand draft (fdd)

Foreign demand drafts are issued when bank received an application on a

specific form and a letter printed on a letter pad of the company with authorized

signatures. FDD issued to only those customers who have a foreign currency

account in the bank. For the issuance of FDD customers have to inform the bank

before 11:30 am, because this department has to inform to treasury that we will

issued that numbers of FDD drawn on these banks. After receiving this

information the treasury department arranged the funds in the related

correspondence banks out side the country.

TRADE FINANCE DEPARTMENT

This trade finance department is divided in two sub departments

Import department

This import department consists on two persons. They both are the officer’s

imports and Mr. Khursheed Alam who is Operations Manager supervises them.

Page 66

Internship Report

PROCESSING OF DOCUMENTS AGAINST L/CS:

SBP may consider applications for advance remittance up to USD 10,000 against

imports where the goods are of a specialized or capital nature. In the event of

total or partial loss of goods it is the importers responsibility to recover claim from

insurance/shipping/ Supplier Company as the case may be.

Each of the four functions of the Import Department are discussed with reference

to

Import Policy

SBP regulations

UCP 500 regulations

Nib Bank internal requirements and procedures

Procedure

Issuance of the import limit

Establishment of LC

Opening of LC

Issuance of shipping guarantees

Retirement of LC

L/C Opening: Import Policy

No L/C can be established for goods which have either been shipped or

have arrived in Pakistan except with special permission.

All importers while applying for establishment of L/C shall produce a valid

certificate of membership of at least one of the trade organizations

licensed and recognized by the Federal Government

If shipment is made before the date of the opening of the L/C the importer

must deposit surcharge equivalent to 1% of the C&F value of goods

Valid original/copy of category pass book is required

All imports shall be made at the most competitive prices

Page 67

Internship Report

Import of items valued up to USD 10,000 or equivalent amount shall be

allowed against Fcy demand draft instead of L/C

For import of machinery against cash by commercial importers all banks

shall open direct L/C as per provisions of import policy

The designated pre-shipment inspection agencies are:

i. COTECNA for European and

ii. Middle Eastern countries

iii. SGS for Asian, Australasian and American countries

Pre-shipment inspection is not required for imported goods that are less

than $3,000 or equivalent amount in total value

SBP H.S. code provided to make sure that the goods are not on banned

list

Performa invoice reference and date match L/C application

EXPORT DEPARTMENT

Requirements for Export of Goods

The exporter is not eligible to export the commodity until and unless he

has an export license and is duly registered as an exporter with the “Chief

Controller of Imports and Exports”.

One should have a registered firm on basis of sole proprietorship,

Partnership or corporation.

A partnership deed has to be signed with the registrar of firms under the

partnership act (1935) and as a result a form-c is issued. According to

which the exporter can export.

Page 68

Internship Report

National Tax Number (NTN) is issued after the registration from the

income tax office.

Opening of foreign currency account in the bank is necessary. It is must

that the bank gives a “financial Credibility certificate” to the exporter so

that he can carry out its operations smoothly.

Exporter must also have an “Certificate of Association” in accordance with

the type of the industrial commodity to be exported.

REALIZATION OF EXPORT PROCEEDS

1. State Bank requires that full export value of goods exported from Pakistan should

be received within a period of four months from the date of shipment.

2. If the tenor of document is 120 days from shipment date then repatriation of

funds can be extended to 135 days.

3. Prior approval must be obtained from State Bank if the tenor of document is more

than 120 days from shipment date.

4. If payment is not realized within the prescribed time or short payment is realized,

then Authorized Dealer has to obtain an explanation letter of exporter and furnish

this to the State Bank.

Procedure for exporting of goods

The exporter sends the pro-forma invoice to the importer on the basis of which

the importer processes all the related documents through its bank. After the

process of the documents at the end of the issuing bank the “advisory Bank”

sends the documents to the exporter.

The exporter after receiving documents from the “Advisory Bank” presents them

to its bank that is named as “Negotiating Bank”. The negotiating bank claims the

payment from the reimbursing bank and after getting the payment pays back to

Page 69

Internship Report

the exporter. The negotiating bank after negotiating the documents and charging

the negotiation commission sends these documents to the issuing bank. The

negotiation includes the checking of all the documents and to make certain that

those are not in negation. In case any sort of discrepancy exists the bank sends

those documents on collection or approval basis to the issuing bank. If the

negotiating bank sends the discrepant documents then it is the responsibility of

that bank in case of any sort of major problem. The shipment is affected through

the Vessel, Plane or Railway.

III.5 Comments on Organizational Structure

Efficient staff.

Bank Alfalah offers its respective clients calendars, New Year table calendar

and key chains etc free of cost.

A very high level of secrecy is maintained.

A verified statement requisition is required to obtain statement of account

from the customers each time.

Branch Manager regularly informs the employees about positive and

negative points.

4.work done by Internee

Page 70

Internship Report

In terms of policy and instruction of Commmerce, I have undergone for 6 weeks

internship with NIB Bank Mian khan road Branch Distt. Sargodha.

I reported at the Branch on 7 july 2010. I was really astonished to see the

building of this Branch outward and inward at a first look and its location at a

prominent place on Mian khan Road. A part from cleanliness and tidiness of the

Branch the atmosphere and dealing of the staff with their clients was a surprising

factor for me and it has given

me a good understanding that how the commercial institutions are extending

services to the people.

On the very first day of my joining, the Manager of the Branch Mr. Raja Qaiser

depicted brief introduction of

NIB Bank Limited

The definition of the Bank

The Departments of the Bank

And different types of services being rendered by NIB Bank to the people.

My participation in the bank

The first day in the bank branch manager introduce me about the bank

employees and their work. I have done various types of assignments regarding

the bank work which have assigned me the different officers of the bank. The

details of my work is as under:

1) Debit credit rules of the bank

There are two types of deposit registers in the bank one is called daily

transaction register and other is called ledger because there is two way entry

process in the bank. Cashier of the bank post the entries on daily transaction

register. The register is divided into two parts receipts and payments

Page 71

Internship Report

respectively. When the bank receive some deposit the casher made the entry on

receipts side means the cash is debited while when the bank made some

payments the entry is passed on the payments side the cash is credited. The

difference between the receipts and payments is the cash balance and that

balance is carried forward and the opening balance of the next day. Actually the

daily transaction register is the book of bank transactions records while the

ledger is the book of customer’s record and their entry process is totally reversed

to the daily transaction record register. When some one deposits the cash, his

account is credited with the particular (by cash) and when some withdraw the

cash his account is debited with the particular (to check).

2) Learning about account opening process.

3) Learning about deposit management system (DMS).

4) Information and learning about the bank registers records which are

given below:

Daily transaction register, Deposit ledger, Interest ledger, OBL(Old Balances of

Loan) register, Save File register (after sanctioning of loan the file is called save

file), Loan Application register, Computerization Number of Loan Case (LC.no)

register, Delivery document register, account opening register (current, MM.PLS

and RBA), Issuance of Check Book register, Utility Billing register, Crop

Insurance register, Dispatch register.

5) Learning about the formula and calculation of interest rate. The

formula is given below.

Days multiply by amount multiply by mark up (in percentage) divided by umber of

days in a year. For example the amount is Rs. 45000/- and we want to find out

the interest (mark up) of 120 days while the interest rate is 9%. Then arcading to

formula the equation is:

R (mark up) = 120*45000*9 / 365*100 = Rs.1331.50/-

6) Scanning of account opening forms for the entry process in DMS.

Page 72

Internship Report

7) Posting of interest in all the development and production loans

ledgers (14 ledgers and each contain about 1000 pages).

8) DMS Balance matching with all deposit ledgers. There are about 34

running ledgers in the bank.

9) Learning about filling of deposit slip. There are following

requirement to fill the slip:

Account number, name, address, date, branch name, ledger folio (L/F), amount.

Page 73

Internship Report

5.Financial AnalysisINVESTMENTS

Investments are made by the banks in order to secure themselves and earn

some profit from it. Generally these investments are done in government

securities and shares. NIB bank invested its money in the following types of

securities;

1. Market treasury bills

2. Preference shares

3. Ordinary shares of listed companies

4. Pakistan Investment bonds

5. Term finance certificates and

6. Investments in Associates

The Market Treasury Bills and Pakistan Investment Bonds are held by the State

Bank Of Pakistan which are eligible for rediscounting. The market treasury bills

matures within 3 to 12 months yielding 8% to 9% markup while the Pakistan

Investment Bonds matures in 7 to 8 years carrying 8% of markup per annum.

2004 2005 2006 2007 2008

1,187,529

5,129,285

6,594,036

40,439,935 35,176,8

23

Page 74

Internship Report

RUPEES IN --- 000 ---

YEAR 2004 2005 2006 2007 2008

INVESTMENTS 1,187,529 5,129,285 6,594,036 40,439,935 35,176,823

Interpretation

As we can see from the above graph that the investments especially in the government

papers were round about 1 billion in 2004 it is just because that at that time it was a new

bank just starting off its business however in the next year 2005 the NIB bank rose its

investments to 5 billion and kept on rising it in 2006 as it were 6.5 billion approximately.

Similarly we can see that there is a huge fluctuation in 2007 and 2008 it’s just because of

the fact that the NIB bank acquired the PICIC commercial bank. But however these

investments were declined from 2007 to 2008 from 40 billion approx to 35 billion

approx. it is because of the economic melt down and recession originating from the west

which affected the whole world so as Pakistanis banks as well.

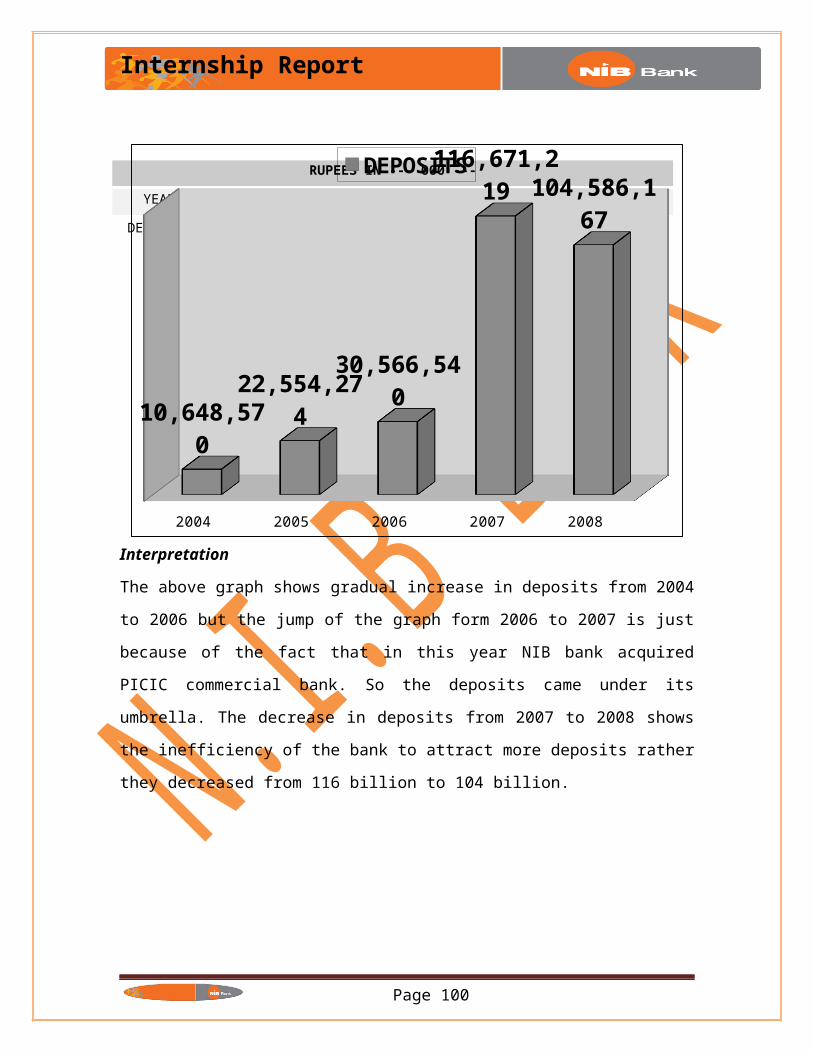

DEPOSITS

Deposits are the liabilities of a bank which is the main source of raising the funds.