16

ATIS Market Roundup: Issue 9 (22/03/15)

| Date post: | 06-Aug-2015 |

| Category: |

Documents |

| Upload: | oliver-ward |

| View: | 48 times |

| Download: | 3 times |

ATIS Market Roundup: Issue 9 (22/03/15)

@FactSetCareers www.FactSet.com/careers

www.facebook.com/FactSet

@FactSetCareers www.FactSet.com/careers

www.facebook.com/FactSet

FactSet is a leading provider of financial data and analytic applications for investment management and investment banking professionals around the globe.

We hire Graduate Consultants every year. Combining knowledge of the industry and the technical expertise, Consultants work closely with our clients to ensure they are seamlessly integrating our software into their investment process.

Joining FactSet gives you an unequalled view into the investment world, working closely with high profile clients, helping then utilise the FactSet product suite effectively.

Find out more at www.FactSet.com/careers

Welcome to the ninth issue of the ATIS Market Roundup Newsletter.

I’m going to skip my usual introduction of familiarising ourselves with what we’ve held in the past fortnight because something very important is upon us. We are hiring for our next year’s committee.

We shall be letting the general public know about this soon, however if you wish to gain a one-up amongst other applicants please email [email protected] with your interest and with role(s) you wish to apply for by Wednesday midnight (25th). A full description of each role is given on the final page of the Roundup.

The only requirements we have are: - Must be an Aston student in the 2015/2016 academic year. - Must be on campus in the 2015/16 academic year (i.e. not on placement and not studying part-time at the University). - Must demonstrate interest in the financial industry.

Desirable traits: - Good social skills. You can know everything about the financial industry, but we need to like you as a person. - Commercial awareness skills. Depending on the role will depend on how much we will test this.

Roles available are: - Chairman - President - VP - Operations - Trading Officer x2 - Marketing - Market Roundup Editor

We look forward to your applications. Best of luck!

Oliver Ward

Contents3,6 The AIIB Pressure comes from US to stay clear

7,8 The Driverless Car Industry Next big thing or science fiction?

9,14 Morgan Stanley’s Investment Banking Outlook Their Annual Publication reveals debatable opinions

15,18 George Osborne’s Tax Levy Huge backlash from the City of London

19,20 Help to Buy ISA Our second article stemming from Osborne’s budget

21,22 Interest Rates Remain at Record Lows

23,24 2015/16 Committee Roles Available

Oliver Ward President and Senior Editor, is a second year BSc Business & Management student, focusing on Economics & Analytics for year 2. Along with being President of ATIS, he is a Director of the World’s largest University based consultancy, and the General Secretary of the Aston University Badminton Team, along with being a very keen badminton player himself. His strengths lie very much in sales, strategy, and growth, and he wishes to pursue this as a career path.

Joel Ntamirira Trading Officer and Senior Editor, is a second year student studying BSc Honours Finance. As well as being Trading Officer with the Aston Trading and Investment Society, Joel is Utilities and Healthcare Portfolio Manager with Aston Capital. His equity investment philosophy is concentrated, research driven, focused on value and growth ideas. He wishes to pursue a career in equity research & investment management.

Sharandas Thampi Contributing Writer, is an MSc Business and Management student at Aston Business School, with a keen interest in the Investment Management and Strategy Consulting industries. He holds an undergraduate first class honours degree in engineering and has 2 years of part-time and full time entrepreneurial leadership and management experience, leading a start-up team of engineers in the internet industry in India. His interests include financial markets/trading, business analysis and technology.

1 2

The AIIB The Americans have accused the Brits of a “constant accommodation” of China after Britain decided to join a new $50bn China-led financial institution. This new institution is called the Asian Infrastructure Investment Bank, (AIIB), with the purpose being to provide finance to infrastructure projects in the Asia-Pacific region. Roads, trains, whatever, the East wants to get more physically connected, which according to pretty much everyone is a good thing as infrastructure requirements in the Far East are vast.

The AIIB - What is it? The AIIB is regarded by some as a rival for the IMF, the World Bank and the Asian Development Bank, (ADB), which are somewhat dominated by developed countries like the United States. As a result, the Chinese Government are a little annoyed, want to show they are a powerhouse, and have decided to make, essentially, a leviathan of a bank with serious capital and resources available to them, where they are top dog. They are frustrated with what it regards as the slow pace of reforms and governance, and wants greater input in the IMF, World Bank and ADB which it claims are dominated by American, European and Japanese interests. The ADB published a report in 2010 which said that the region requires $8 trillion to be invested from 2010 to 2020 in infrastructure for the region to continue economic development.

The AIIB is one of four institutions created or proposed by Beijing in what some see as an attempt to create a Sino-centric financial system to rival western dominated institutions set up after WWII. The other institutions are 1) the New Development Bank, (better known as the BRIC’s bank), 2) a contingent reserve arrangement, (seen as alternatives to the World Bank and IMF), and 3) a proposed Development Bank of the Shanghai Co-operation Organisation, a six-country Eurasian political, economic and military grouping dominated by the Chinese and Russian.

What’s wrong with it? On the face of it, nothing. The perception, however, is that the AIIB isn’t complementary to what’s already been in existence. They are seen as a new football club treading on IMF’s turf. The ADB was established in 1966 and now has 67 members including 48 from Asia and the Pacific. But it is seen by many in the region as overly dominated by Japan and the US, which are by far its biggest shareholders with holdings of 15.7 and 15.6% respectively, compared with China’s 5.5%. The AIIB was founded last year with 21 members. Notably absent were the US, Japan, Australia and South Korea. The US, it is said, lobbied countries not to join, while China worked hard to get them in. One of the countries the Chinese did manage to get in was Britain: we’ve said we would be a founding member of the bank ahead of a deadline at the end of this month, and will be the first member of the G7 to join this institution.

Does this matter? Why are the US unhappy? To part one of that, both sides clearly think it does matter. Advocates of the AIIB criticise the ADB for being overly bureaucratic. The AIIB’s critics say the new lender will play fast and loose with conditionality and other restrictions on the behaviour of borrowers, allowing corruption to flourish. More significant, however, are strategic considerations. The US and China are increasingly engaged in a struggle for regional influence, played out through institutions such as these.

To part two of that, relations between Washington and David Cameron’s government have become a little tense as a result, with senior US officials criticising Britain over falling defence spending, which could soon go below the Nato target of 2% of GDP. A senior US administration official told the Financial Times that the British decision was taken after “virtually no consultation with the US” and at a time when the G7 had been discussing how to approach the new bank. “We are wary about a trend toward constant accommodation of China, which is not the best way to engage a rising power,” the US official said.

There are also 2 institutions available already, so the big question is “why create a third?” Well the demand for Asian demand for infrastructure is absolutely enormous, and an extra $50bn available made by this institution will go a decent way to that $8 trillion figure mentioned earlier. The argument of creating a third will create competition can be easily cut out by mentioning the ADB was created after the World Bank, overlapping some of the interests of the World Bank, and it appears to have been working rather well. Some people argue some competition between public states can be a good thing.

Britain’s Stance George Osborne was unapologetic, arguing that Britain should be in at the start of the new bank, ensuring that it operates in a transparent way. He believes it fills an important gap in providing finance for infrastructure for Asia. “Joining the AIIB at the founding stage will create an unrivalled opportunity for the UK and Asia to invest and grow together,” Mr Osborne said. He expects other western countries, which have been making positive noises privately about the new bank, to become involved. This stance by Mr Osbourne, who by the way has the most interesting Twitter account in the history of ever, (yawn), highlights his desire to pursue commercial relations with China aggressively, even at the expense of rattling Washington’s cage.

Britain appears to be showing signs of independence to the West, and highlight very clearly that as the East has been rising up in terms of power that the existing institutions, (IMF, World Bank, etc), simply haven't been accommodating of these new countries to reflect the say they now have in this world. The Chinese argument for this AIIB appears to be well justified, however that may be an opinion argued a lot if you're from Washington. Britain has cemented, if the UK does officially become a member by the end of this month, a first-mover advantage with Beijing.

3 4

Britain may come in for criticism from some other European countries, several of which were poised to join the AIIB in October but decided not to because of the American pressure. However, there is an expectation in London that other European countries will soon announce their intention to join up, along with Australia. British officials are also sceptical about why the US is making a fuss about the issue now, noting that it was not raised during recent telephone calls or face-to-face meetings between Mr Cameron and Barack Obama, US president. One said: “Of course it has nothing to do with the fact that the US couldn’t get this through Congress even if they wanted to.”

[Update] Europeans follow suit Things aren’t looking great for the Obama Administration, as France, Germany, and Italy have now all agreed to follow Britain’s lead. Australia has also said it will now ‘rethink’ their position. Momentum appears to be growing very rapidly for the AIIB.

5 6

The Driverless Car Industry A driverless car, as the name suggests, is an autonomous vehicle that can navigate roads without human control. UK Chancellor George Osborne, in a pre-budget speech, outlined the possibilities of unveiling a GBP 100 million pound investment in the driverless car industry. By 2020, General Motors, Audi, BMW, Tesla and Google are all expected to sell cars that can drive themselves at least a part of the time.

Is the driverless car industry the next big thing globally or is all of this just exaggerated science fiction?

Pros:The calculated benefits of driverless technology is in terms of lesser crash costs due to increased precision, lesser traffic jams due to lower gaps and spaces between vehicles and more efficient fuel utilisation. Another massive forecasted benefit is the removal of parking issues in major metropolitan cities because cars can pick up passengers without having to be parked adjacent to the drop-off point. Speed limits may also go up, which mean lesser transportation time.

Cons:The primary hurdle for the industry is that driverless cars will be held up to a higher standard by the general public, when compared to human driven vehicles. In initial stages, a few fatal accidents can potentially bring a massive cloud over the industry. Additionally, all of the benefits documented above are realised only if the artificial intelligence demanded by driverless cars is perfected to such an extent that it can operate in the chaotic environment of metropolitan city streets better than with human judgement.

Market Strategy:Google was one of the first companies to speak about driver less cars and actually invest in actively developing a road-worthy prototype. An internet company based out of Silicon Valley, Google has seemingly come out of nowhere to possibly herald the next big change in the automobile industry. Other traditional automakers such as Ford, Volvo and Nissan have made grandiose statements regarding their entry into the industry but have not followed through in action as much as Google. Traditional automakers are instead pursuing an incremental strategy whereby vehicles can be converted to driverless at times and can human-controlled at other times (shown in figure on the top right). Though the incremental strategy makes a lot of sense from a technology and business point of view, the longer term aspirations of Google may turn out to be the game-changer over time.

This is not considering the other automobile powerhouse from Silicon Valley, namely Tesla, who is also said to have invested massive funds into driver less technology. CEO

An example of Ford’s incremental approach to driverless technology

Elon Musk has gone so far as to say that the success of driver less vehicles with all of its precision and benefits (read above) could actually cause human control (considered by him to be more error-strewn) to be banned in future. Considering that both Google and Tesla were nowhere in the automobile industry picture a few years ago, the growing intersection of technology and the automotive industries seems to have developed a fresh crop of competitors to the traditional brands.

The UK Market:In the UK, so far, tests of driver less cars on the open road are not permitted though there is a proposal to allow tests in a structured manner from January 2016. While some states in the US, France and Japan have already allowed tests, the UK has been relatively slow. The UK’s first home-made driverless car the Lutz Pod, was unveiled in Greenwich in February 2015, as a vehicle that can be used to travel short distances. It is due to hit the streets later this year and it will interesting to understand the perception of the public.

The driver less automobile appears to be the next revolution in the automobile industry and the difference between whether it appears as a real life product on the streets or whether it remains a story of the future depends on how quickly the technology is perfected, how governments world-wide legalize and regulate the market and public acceptance of such a radical change.

7 8

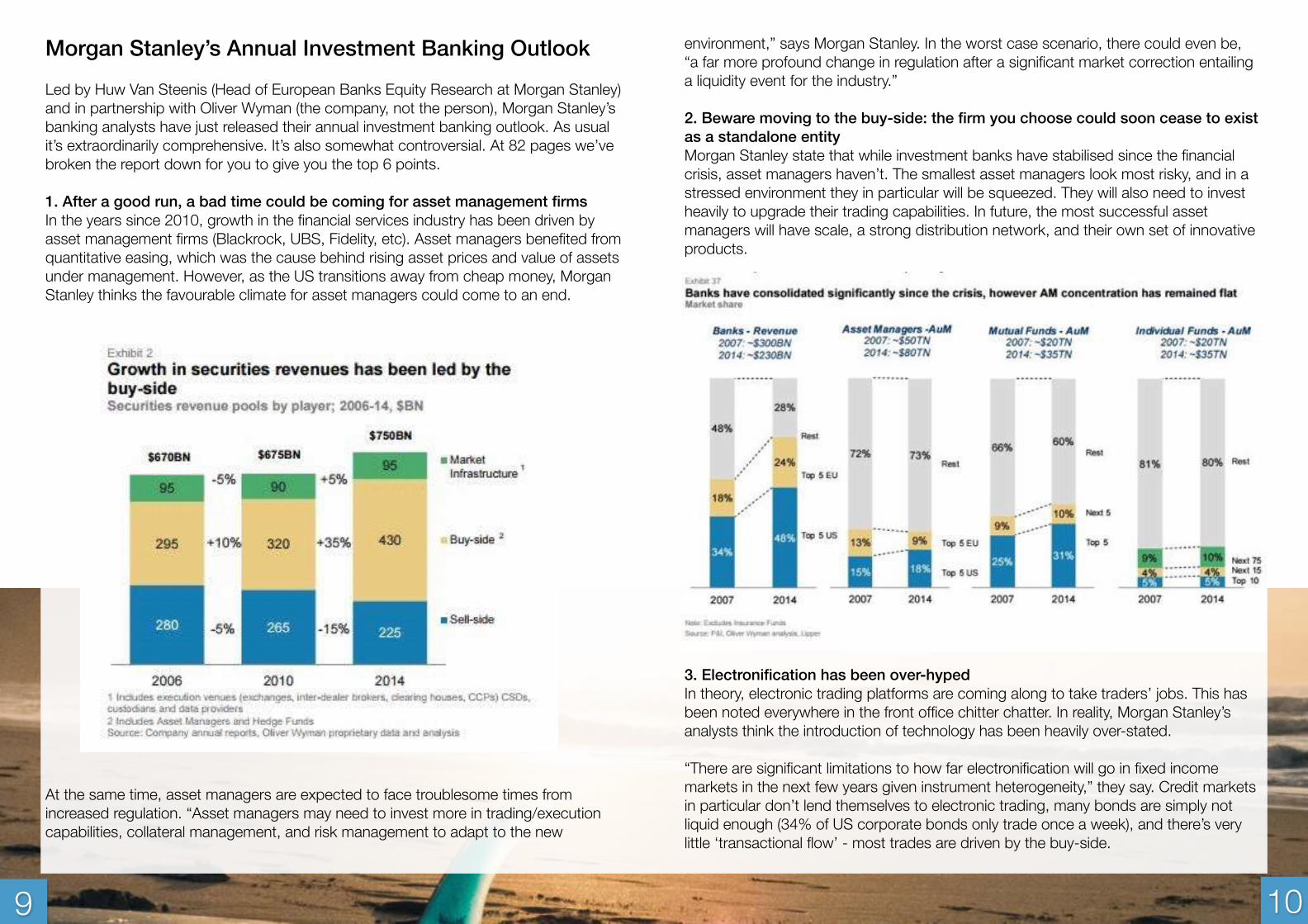

Morgan Stanley’s Annual Investment Banking Outlook Led by Huw Van Steenis (Head of European Banks Equity Research at Morgan Stanley) and in partnership with Oliver Wyman (the company, not the person), Morgan Stanley’s banking analysts have just released their annual investment banking outlook. As usual it’s extraordinarily comprehensive. It’s also somewhat controversial. At 82 pages we’ve broken the report down for you to give you the top 6 points.

1. After a good run, a bad time could be coming for asset management firms In the years since 2010, growth in the financial services industry has been driven by asset management firms (Blackrock, UBS, Fidelity, etc). Asset managers benefited from quantitative easing, which was the cause behind rising asset prices and value of assets under management. However, as the US transitions away from cheap money, Morgan Stanley thinks the favourable climate for asset managers could come to an end.

At the same time, asset managers are expected to face troublesome times from increased regulation. “Asset managers may need to invest more in trading/execution capabilities, collateral management, and risk management to adapt to the new

environment,” says Morgan Stanley. In the worst case scenario, there could even be, “a far more profound change in regulation after a significant market correction entailing a liquidity event for the industry.”

2. Beware moving to the buy-side: the firm you choose could soon cease to exist as a standalone entity Morgan Stanley state that while investment banks have stabilised since the financial crisis, asset managers haven’t. The smallest asset managers look most risky, and in a stressed environment they in particular will be squeezed. They will also need to invest heavily to upgrade their trading capabilities. In future, the most successful asset managers will have scale, a strong distribution network, and their own set of innovative products.

3. Electronification has been over-hyped In theory, electronic trading platforms are coming along to take traders’ jobs. This has been noted everywhere in the front office chitter chatter. In reality, Morgan Stanley’s analysts think the introduction of technology has been heavily over-stated.

“There are significant limitations to how far electronification will go in fixed income markets in the next few years given instrument heterogeneity,” they say. Credit markets in particular don’t lend themselves to electronic trading, many bonds are simply not liquid enough (34% of US corporate bonds only trade once a week), and there’s very little ‘transactional flow’ - most trades are driven by the buy-side.

9 10

“15% of volume in credit is electronically traded today, and aggressive estimates are unlikely to see it grow to more than 25%,” say Morgan Stanley’s analysts.

Similarly, Morgan Stanley calms the notion that says traders are also about to lose their jobs to aggressive e-trading platforms: “The impact on sell-side economics [of electronification] should not be over-stated - we estimate that only 25% of rates and 10% of credit revenues are likely to be affected over the next 2-3 years.”

So if you want to go into trading and are worried about a computer taking over your job, your fears should be calmed.

4. Barclays is well placed for the future (or at least its stock is) As per the chart on the right, Morgan Stanley thinks Barclays is well placed to increase its return on equity over the next two years (although it still won’t be as impressive as UBS). Barclays is also liked on account of its strong equities business, its ‘restructuring potential’ and the clear-up of its non-core unit.

5. Securitisation is the best place to work now, followed by emerging markets As per the chart below, Morgan Stanley suggests that both securitisation and emerging markets (shown by “EM” in the chart) are generating profits whilst using a low proportion of banks’ capital. This is a holy grail in today’s world.

Conversely, if you're looking at flow rates or repo, you might want to reconsider…

6. Fixed income sales and trading revenues are still falling and Goldman Sachs is very exposed to the FICC sector Although Jefferies had a bad first quarter in fixed income, most other banks have been suggesting that things didn’t go too badly in FICC. Morgan Stanley suggests that this optimism may be premature.

11 12

And if you’re of the opinion that fixed income revenues aren’t going to recover any time soon, Goldman Sachs, Credit Suisse, or Deutsche Bank aren’t the places to be at the moment…

13 14

George Osborne’s Tax Levy George Osborne is facing a huge backlash from the City of London after he dealt British and foreign banks a major blow with a £5.3bn tax raid to pay for personal tax cuts. The Chancellor raised the bank levy for the eighth time in four years in the biggest single money-raising exercise in Wednesday’s Budget, taking the controversial tax to a level more than four times the rate proposed in 2010. The move is likely to hit HSBC the hardest after it was heavily criticised in recent weeks over the tax evasion scandal at its Swiss private bank. If you’ve not read our article a couple Issues back on HSBC’s tax evasion, we recommend you do.

George Osborne said a recovery in banks’ profitability since the crisis meant they could make a “bigger contribution to the repair of our public finances” as he announced a 35% increase in the bank levy. The chancellor lifted the levy from 0.156% of banks’ liabilities to 0.21%, which he said would raise an extra £900m a year.

Antony Browne, chief executive of the British Bankers’ Association, said “The bank levy imposes a significant cost on banking businesses in the UK, which is making many banks move work and jobs to other parts of the world, and is deterring international banks from investing in the UK. This major increase in the bank levy is likely to

accelerate that process and damage the competitiveness of the UK economy.” Mr Browne was also keen to mention banks already paid £40bn of taxes a year.

Mr Osborne also cut corporation tax relief for bank fines, and the Government’s spending watchdog upgraded revenue forecasts for restrictions on tax relief announced in December. The combined effect of the three measures is now expected to be £9bn in extra tax payments from banks over the course of the next Parliament. Critics have slammed these policies, in particular the hike to the bank levy, saying it would force foreign banks out of Britain, hit lending and put UK lenders at a disadvantage compared to international peers. That £9bn is outlined below.

Mr Osborne has raised the rate of the levy eight times from an initial 0.075% because he has consistently undershot his target of collecting £2.9bn a year from the 30 banks and building societies that are liable to pay it. The Office for Budget Responsibility forecast the levy would raise £3.7bn a year from 2017-18, up from £2.8bn in the fiscal year to this April.

In addition to the higher bank levy, banks will now not be able to deduct compensation payments for misconduct, such as PPI, when calculating the profits that are liable for corporation tax. The Office for Budget Responsibility (OBR) predicts the move will raise £965m over five years.

15 16

The tax, branded “a location levy” by British lenders, is levied as a percentage of total global liabilities. Foreign banks also contribute, but pay only a percentage of their UK liabilities. “There is a saying in tax circles that raising taxes is like plucking feathers from a goose: you should not make it shriek, but this is going to cause some shrieking,” said Tom Aston, a tax partner at KPMG. “It is a huge slap in the face for the banking industry”.

It puts British banks operating abroad at a disadvantage, since their international liabilities, as well as domestic ones, are taxed. Standard Chartered, Britain’s fourth-biggest bank, takes the effect of the levy into account when it reviews whether it should move headquarters abroad, according to sources at the bank. The OBR said in its review of the Budget that the higher levy could “affect banks’ ability to meet capital requirements… the measures could affect the supply of credit and therefore GDP growth”. Additionally, Mr Osborne announced the sale of £13bn of assets held from the bail-outs of Northern Rock and Bradford and Bingley, and said he planned to sell £9bn of Lloyds shares in the coming year, a move that would take its percentage holding in the bank into single digits. Selling the £22bn in assets allows the Chancellor to say that public debt will fall as a percentage of GDP next year.

Mr Osbourne was very quick to say “As our banking sector becomes more profitable again, I believe they can make a bigger contribution to the repair of our public finances. The banks got support going into the crisis; now they must support the whole country as we recover from the crisis.” Thing is though, banks aren’t loyal. They go where the most profit is made. If the UK goes out of Europe along with this increased tax levy expect to see a number of banks relocate their operations.

17 18

Help to Buy ISA On 18th March, the Chancellor of the Exchequer, George Osborne unveiled the Help-To-Buy ISA to assist first-time homeowners who are looking to get on to the property market in the UK

Is the Help-To-Buy ISA scheme a boon or a bane?

What is the scheme?The scheme essentially says that for every 200 GBP that a buyer deposits in the account (ISA), the government will top it up with a further 50 GBP, effectively creating extra savings of 25%. The bonus can go up to 3000 GBP in total, which means that a minimum of 12,000 GBP deposited by the buyer can utilise the full breadth of savings from the scheme, taking the total to 15,000 GBP. The scheme also contains the provision of applying the savings bonus to each individual applicant. This means that joint owners of property can obtain a savings bonus of up to 6000 GBP. The ISA can be set up for four years and once set up, there is no upper limit to the time for which you can continue to save using the account. The bonus is valid for properties in London worth up to 450,000 GBP and properties outside London worth up to 250,000 GBP.

The ISAs, as of now, should be available from autumn 2015.

The ProsEspecially in London at the present moment, the property market is extremely steep for many prospective young professionals or families. The proposal of the government to top up a saved 12,000 GBP amount with an additional 3000 GBP seems extremely generous and is designed to reduce the hurdles faced by first time property buyers to get on to the market. The possibility of doubling this contribution through joint ownership of the property increases the flexibility afforded to the buyers. Moreover clauses in the policy also prevent buying the property and then letting it out, ensuring that shrewd property moguls do not swoop in to take advantage.

The move is also of benefit to building societies and letting agents as more first-time business comes their way.

The ConsThe primary concern lies with the mode of payments to the account. After an initial deposit of 1000 GBP to the account, a monthly payment of not more than 200 GBP needs to be made. At that rate of payment, it would take four and a half years for the prospective buyer to save enough to take full advantage of the benefits of the scheme. For buyers who can save at a faster rate, this represents inflexibility. During this period, property prices could also jump, thus making the benefit of the scheme redundant.

Another concern is that as it gets easier for first time buyers to obtain the means to purchase property, property prices could go up due to the increased demand, thus once again making the savings redundant. A section of analysts maintain that working solely on the demand side, while not increasing the number of property developments on the supply side is asking for trouble, a point that is not entirely without merit.

ConclusionThough the Help to Buy ISA scheme is of relevance to first time property buyers in reducing the hurdles faced in getting on to the property market, there is a degree of inflexibility involved in the scheme that can act as deterrent. Moreover, popularity of the scheme could result in rising property prices, thus making the whole exercise redundant.

19 20

Interest Rates Remain At Record Lows The FOMC meeting this week resulted in no change in Fed rates policy; keeping the funds rate between 0 and 0.25 percent. The FOMC is facing a tough set of factors in the global economy: dangerously low inflation, strengthening dollar, and struggling economies in Europe, Japan and emerging markets; making the rates rise timing particularly difficult. The Fed has stated they would not raise rates in the April FOMC meeting and might wait until much later in the year; searching for ‘reasonable confidence’ that the inflation rate would be moving towards their 2% target. This being particularly unlikely in the near term given low oil prices and the strong dollar.

The Fed has kept rates at record lows for over 6 years after the last recession. Monetary policy in the USA currently has no recession fighting tools other than QE, which has yet to prove effective in the long term. However, the Fed is sound to be careful in their timing, given that nominal interest rates are negative in some of the EU’s stronger countries, more capital is flooding to the USA. If the Fed raises rates, even more capital will flow into the USA, further strengthening the dollar, dragging exports lower and causing significant harm to the USA’s global competitive position.

In addition to causing domestic harm, appreciation in the US dollar can cause global harm. Much of the world’s debt is denominated in dollars, with the dollar strengthening this will increasingly make interest payments a bigger burden for foreign borrowers, given that the incoming receipts are in a depreciating currency on a relative basis. The Fed has a dual mandate; maximise employment whilst controlling for inflation. Raising rates could result in job losses in manufacturing and other exported services/goods assuming the dollar rallies as expected, making US goods relatively more expensive.

The maintenance of their accommodative stance had a bearish effect on the dollar; which on the day fell by around 2% against the Euro, and over 3% against a basket of trading partners as measured by the DXY index. I presume this is a temporary bearish move in the dollar, given the increasing speculation around the FOMC meetings as the rates are inevitably to rise soon. In the long run, the status quo remains, there will be a divergence in monetary policy by the UK and US (who will be less accommodative) whilst the ECB & BOJ will remain accommodative; this dichotomy should increase the value of the USD and GBP relative to the other currencies over time.

The chart on the right shows the EUR/USD, the sharp spike on Wednesday as soon as the Fed released their meeting minutes.

The FOMC’s decision to keep rates low had worldwide implications, particularly in the equity markets. Nasdaq rose to 15 year highs, closing at 5026, and the FTSE 100 hit 7000 for the first time amid signs that interest rates are to remain low. Closing at 7,022, which is the highest in its 31 year history; fuelled by cheap money and low oil prices favouring higher consumer spending.

EUR/USD

21 22

2015/16 Committee To all of those interested in being in the new committee here’s what’s on offer.

Chairman The Chair is essentially there to guide the President, bring ideas and expectations as to how the society will be run, and provide support. Essentially act as a father figure and make sure everything is running smoothly. If the President have any issues then he/she should talk to them immediately. The main thing we are looking for is experience and leadership skills. This was Daniel’s job last year.

President You will be the face of the society, and we expect you to work tirelessly for the good of ATIS, not for you. The President is responsible for the day-to-day running of the society and will be in constant communication with the committee. You need to ensure that there are events at least every other week and that these events will be high quality and relevant to ATIS. You will have a hand in every say of every single job, and so you need to be incredibly well organised and be very good at keeping on top of everything. You will also be in charge of sponsorship for the society, in which you will be given a very useful contact list to work with. The main thing we are looking for in this role is energy, passion, and relentless persistence to see ambitious challenges through. Your attitude is everything here. This was Oliver’s job last year.

Vice President You will support the President. The President will be delegating jobs to you in order to support them in their daily tasks. This was Yunal’s job last year.

Operations You will be in charge of booking rooms and making sure keys are collected in plenty of time before events. You should be in good contact with the booking staff. This was Ryan’s job last year.

Trading Officers (x2) The Trading Officers will lead talks on trading, investment, finance, the economic situation, and so on. The main thing we are looking for in this role is knowledge and passion about the financial industry, combined with comfortable and confident public speaking skills. Desirable is one person to focus towards fundamental analysis with the other being focussed towards technical analysis. You will both contribute to the ATIS Market Roundup with articles every fortnight. These jobs were Joel’s and Anil’s last year.

Marketing/Social You will be in constant communication with the members, be in charge of the Facebook page, and organise all socials. A lot of work will happen before the academic year starts because there needs to be a lot of material prepared for Freshers Fayre. Experience in Marketing is desirable, and energy is a big thing we are looking for in this role. This was Sophie’s role last year in Term 1, and Amanda’s role in Term 2.

Market Roundup Editor You will be the person in charge of the Market Roundup we send out every fortnight. You need to be very comfortable in researching financial topics, and be comfortable in designing a professional document. We will also be ensuring that the articles you write are not straight copy and pasted from the internet; this should not happen as writing articles for the Roundup along with designing it is your only job. This should also not happen due to copyright laws. The vast majority of your interview will be discussing financial topics, however we will be the ones choosing the topics most of the time. We will also be quizzing you on what is going on in the financial world. This is to ensure we are comfortable the person we appoint is truly passionate about the financial industry. This is a new role for the academic year, and last year was performed by Oliver, Joel, Anil, and a contributing writer called Sharandas.

Everyone: - Needs to work to bring in Companies/People to give talks relevant to ATIS. - Needs to work together and communicate. - Represents the society and so should act accordingly. - Should be supportive to the Chair and President. - Should be ‘bigging' the society up at every occasion!!

The only requirements we have are: - Must be an Aston student in the 2015/2016 academic year. - Must be on campus in the 2015/16 academic year (i.e. not on placement and not

studying part-time at the University). - Must demonstrate interest in the financial industry.

IN ORDER TO APPLY WE NEED - Your CV. - A Cover Letter of no more than 300 words

Both emailed to [email protected]. All applications will be reviewed on a rolling basis thus we encourage you to apply ASAP. If you wish to gain a heads up on the competition send it by Wednesday midnight (25th), and on Thursday we will be encouraging the public (i.e. everyone at Aston) to apply.

Look forward to seeing your applications!

23 24

@FactSetCareers www.FactSet.com/careers

www.facebook.com/FactSet

@FactSetCareers www.FactSet.com/careers

www.facebook.com/FactSet

FactSet is a leading provider of financial data and analytic applications for investment management and investment banking professionals around the globe.

We hire Graduate Consultants every year. Combining knowledge of the industry and the technical expertise, Consultants work closely with our clients to ensure they are seamlessly integrating our software into their investment process.

Joining FactSet gives you an unequalled view into the investment world, working closely with high profile clients, helping then utilise the FactSet product suite effectively.

Find out more at www.FactSet.com/careers

Everyone wants to eat but few are willing to hunt

To contact the editors responsible for the ATIS Market Roundup: Oliver Ward [email protected] Joel Ntamirira [email protected], Sharan Thampi [email protected]