46

ATLAS COPCO GROUP Atlas Copco Capital Markets Day 2015 Ronnie Leten, President and CEO Hans Ola Meyer, CFO

ATLAS COPCO GROUP

Atlas Copco Capital Markets Day 2015

Ronnie Leten, President and CEO

Hans Ola Meyer, CFO

ATLAS COPCO

A world leading provider of sustainable

productivity solutions

Consistent strategy

Agile and resilient operations

Strong global service business

Strong cash generation and value creation

Group Presentation

Atlas Copco Capital Markets Day 2015

2

1. Facts in Brief

2. Vacuum Solutions

- Status update

3. Innovation

4. Service

5. Summary

1. Business development

2. Global trends

3. Strategy and priorities

4. Agility and resilience

5. Summary

AGENDA

Group Presentation

Atlas Copco Capital Markets Day 2015

3

BUSINESS DEVELOPMENT

Group Presentation

Atlas Copco Capital Markets Day 2015

4

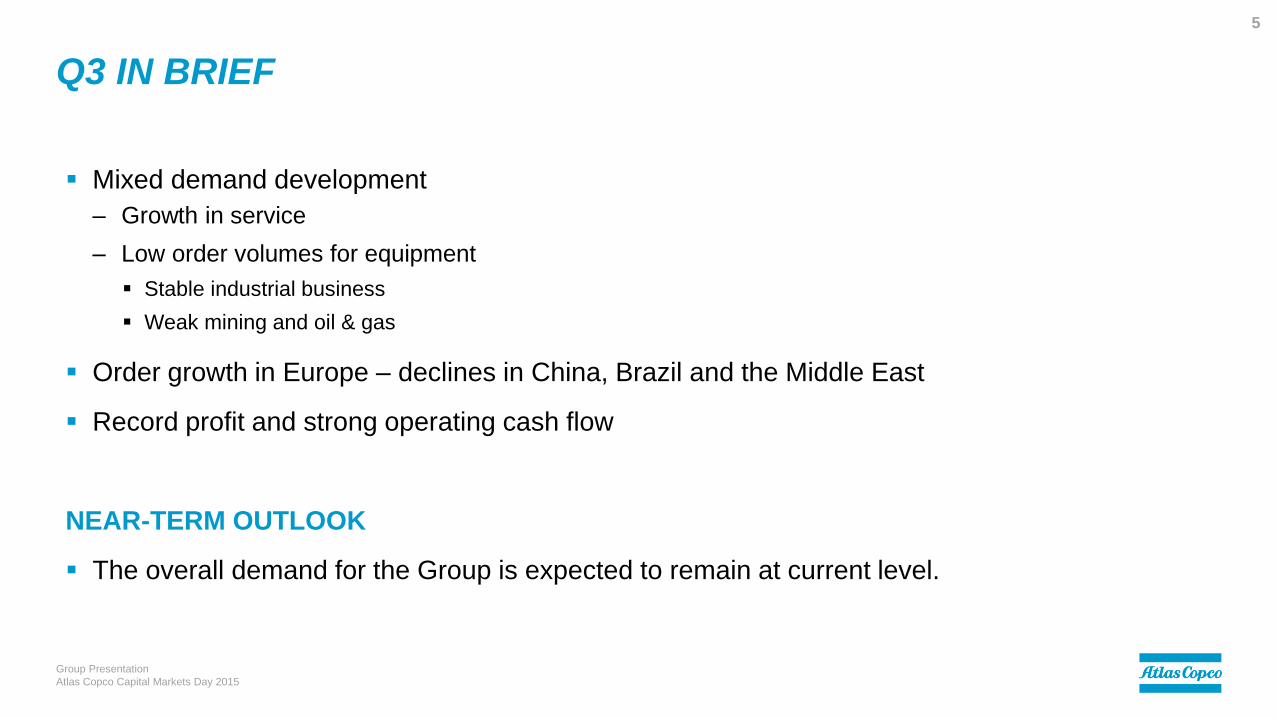

Q3 IN BRIEF

Mixed demand development

– Growth in service

– Low order volumes for equipment

Stable industrial business

Weak mining and oil & gas

Order growth in Europe – declines in China, Brazil and the Middle East

Record profit and strong operating cash flow

NEAR-TERM OUTLOOK

The overall demand for the Group is expected to remain at current level.

Group Presentation

Atlas Copco Capital Markets Day 2015

5

ORDERS RECEIVED - LOCAL CURRENCY

Group Presentation

Atlas Copco Capital Markets Day 2015

6

Atlas Copco Group

100 -1 -3

24 -3 -7

8 -13 -17

30 +5 +7

10 -3 -18

25 -1 +2

3 -13 -20September 2015

A Share of orders received, year-to-date, %

B Year-to-date vs. previous year, %

C Last 3 months vs. previous year, %

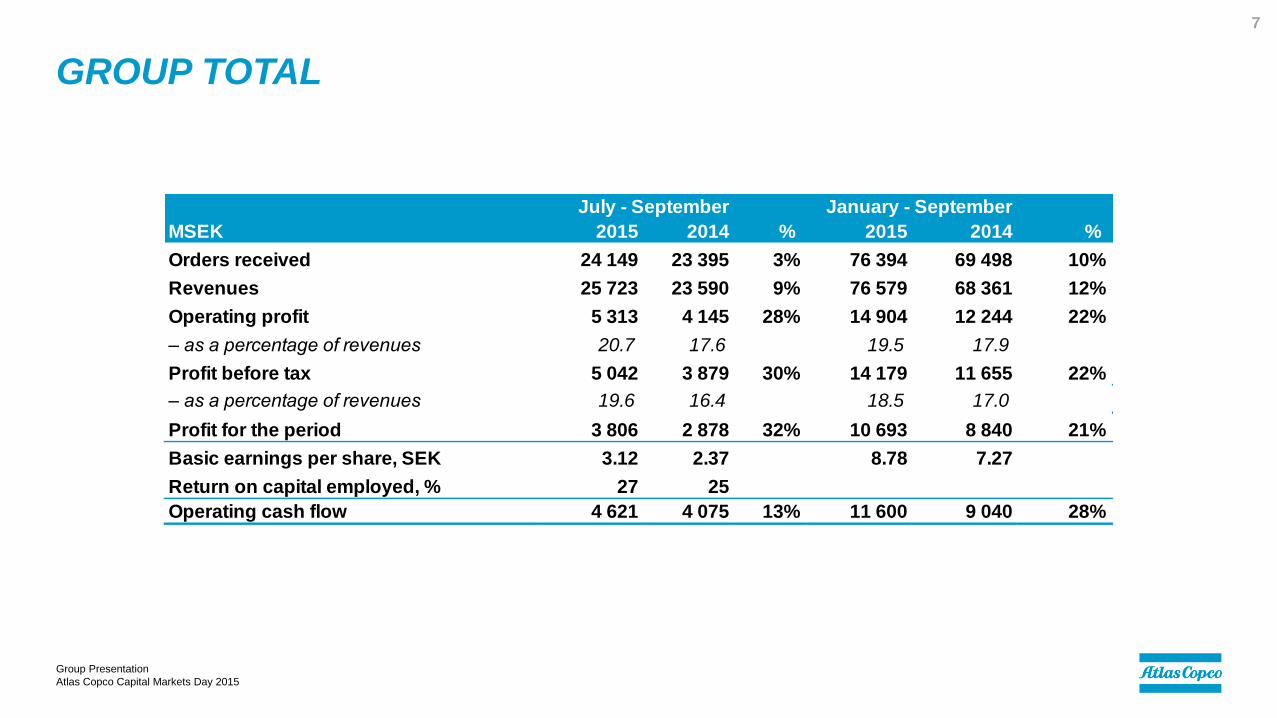

MSEK 2015 2014 % 2015 2014 %

Orders received 24 149 23 395 3% 76 394 69 498 10%

Revenues 25 723 23 590 9% 76 579 68 361 12%

Operating profit 5 313 4 145 28% 14 904 12 244 22%

– as a percentage of revenues 20.7 17.6 19.5 17.9

Profit before tax 5 042 3 879 30% 14 179 11 655 22%

– as a percentage of revenues 19.6 16.4 18.5 17.0

Profit for the period 3 806 2 878 32% 10 693 8 840 21%

Basic earnings per share, SEK 3.12 2.37 8.78 7.27

Return on capital employed, % 27 25

Operating cash flow 4 621 4 075 13% 11 600 9 040 28%

July - September January - September

GROUP TOTAL

Group Presentation

Atlas Copco Capital Markets Day 2015

7

ORDERS RECEIVED BY CUSTOMER CATEGORY

Manufacturing25%

Process industry

11%

Mining28%

Construction24%

Other 12%

2010MSEK 75 178

Manufacturing34%

Process industry

14%

Mining20%

Construction19%

Other13%

September 2015MSEK 100 769

Group Presentation

Atlas Copco Capital Markets Day 2015

8

36%

52% 48%39%

12 month figures.

REVENUES BY BUSINESS AREA

Compressor Technique

43%

Industrial Technique

9%

Mining and Rock

Excavation Technique

32%

Construction Technique

16%

2010MSEK 69 875

Compressor Technique

45%

Industrial Technique

14%

Mining and Rock

Excavation Technique

26%

Construction Technique

15%

September 2015MSEK 101 939

Group Presentation

Atlas Copco Capital Markets Day 2015

9

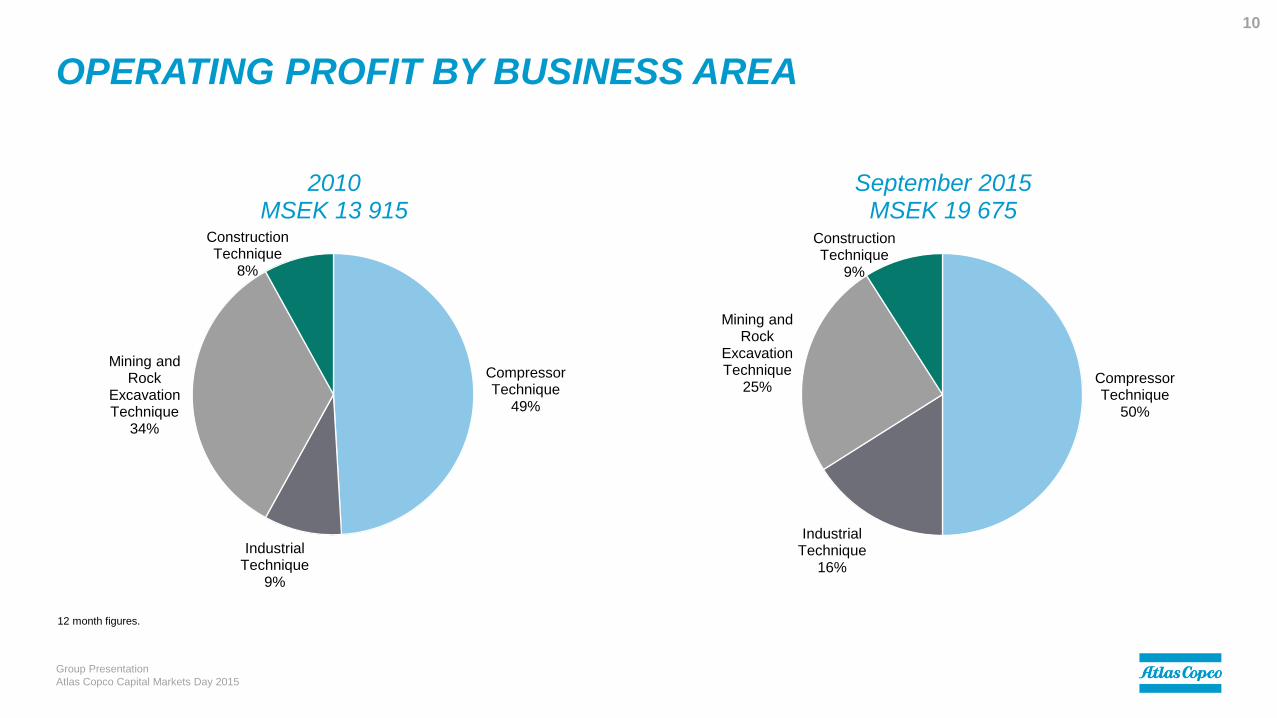

12 month figures.

OPERATING PROFIT BY BUSINESS AREA

Compressor Technique

49%

Industrial Technique

9%

Mining and Rock

Excavation Technique

34%

Construction Technique

8%

2010MSEK 13 915

Compressor Technique

50%

Industrial Technique

16%

Mining and Rock

Excavation Technique

25%

Construction Technique

9%

September 2015MSEK 19 675

Group Presentation

Atlas Copco Capital Markets Day 2015

10

12 month figures.

ORGANIC GROWTH

- 15

- 10

- 5

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015 YTD

Growth % - Total Growth % - Total organic

- 15

- 10

- 5

0

5

10

15

20

25

30

35

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Q115

Q215

Q315

Growth % - Equipment organic Growth % - Service organic

Growth % - Consumables organic

Group Presentation

Atlas Copco Capital Markets Day 2015

11

Revenues

GLOBAL TRENDS

Group Presentation

Atlas Copco Capital Markets Day 2015

12

GLOBAL TRENDS – EQUIPMENT

Group Presentation

Atlas Copco Capital Markets Day 2015

13

Urbanization drive investments

in infrastructure and demand for

minerals

The energy efficiency and productivity

requirements from industry

Continued expansion

in growth markets

GLOBAL TRENDS – SERVICE

Group Presentation

Atlas Copco Capital Markets Day 2015

14

Customers focus

on core activity

Connectivity

Expansion of

installed base

The energy efficiency and

productivity requirements

from industry

STRATEGY AND PRIORITIES

Sustainable profitable growth

Group Presentation

Atlas Copco Capital Markets Day 2015

15

WHY SHOULD ATLAS COPCO SUCCEED TO GROW?

Market leader with strong portfolio of businesses

and products

Commitment to innovation

Strong service offering

Acquisition potential

Top organization, world-class people, top execution

Group Presentation

Atlas Copco Capital Markets Day 2015

16

8% growth

High ROCE

WHY SHOULD ATLAS COPCO DELIVER HIGH ROCE?

Standardization and efficient flow

Asset light operations

Variable cost structure

Strong service business

Group Presentation

Atlas Copco Capital Markets Day 2015

17

8% growth

High ROCE

THE STRATEGIC PILLARS FOR PROFITABLE GROWTH

Group Presentation

Atlas Copco Capital Markets Day 2015

18

PeoplePresence Innovation ServiceOperational

excellence

PRIORITIES TO SUSTAIN PROFITABLE GROWTH

Group Presentation

Atlas Copco Capital Markets Day 2015

19

WE LIVE BY THE

HIGHEST ETHICAL

STANDARDS

WE INVEST IN

SAFETY AND

WELL-BEING

WE USE RESOURCES

RESPONSIBLY

AND EFFICIENTLY

WE BUILD THE

MOST COMPETENT

TEAMS

WE INNOVATE FOR

SUSTAINABLE

PRODUCTIVITY

Group Presentation

Atlas Copco Capital Markets Day 2015

20

SUSTAINABLE PROFITABLE GROWTH

PeoplePresence Innovation ServiceOperational

Excellence

8% growth

High ROCE

INCREASE PRESENCE IN FAST GROWING ECONOMIES

…AND STRENGTHEN IN MATURE MARKETS

Direct presence

Develop local competence

Create high brand awareness

Group Presentation

Atlas Copco Capital Markets Day 2015

21

Presence

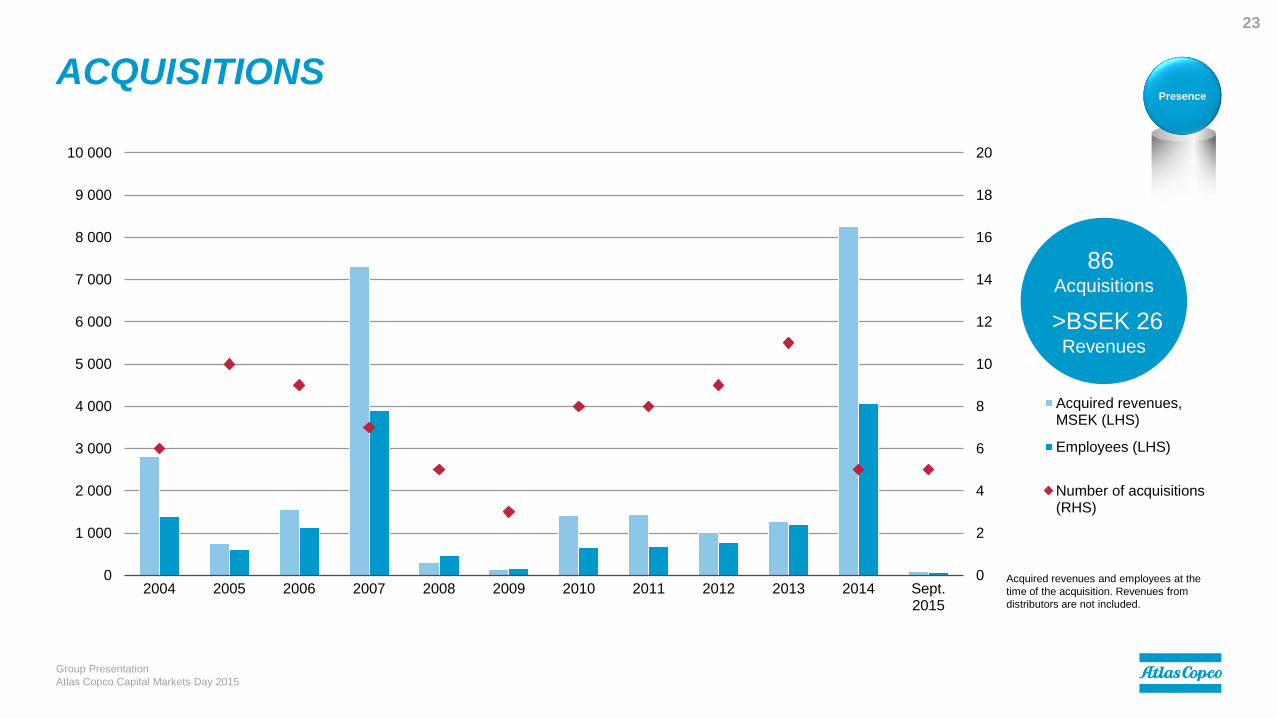

ACQUISITION STRATEGY

Acquisitions are primarily made in, or very close to, the already existing core businesses.

All acquired businesses are expected to make a positive contribution to economic value added.

Characteristics

Group Presentation

Atlas Copco Capital Markets Day 2015

22

Presence

Industry-to-industry

Geographically spread customer base

Leadership in niche markets

Differentiated core technology

Strong base of business partners

Healthy service potential

Leveraging...

Application knowledge

Efficient manufacturing and product

development processes

Capacity to swiftly market products and

services globally

ACQUISITIONS

0

2

4

6

8

10

12

14

16

18

20

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sept.2015

Acquired revenues,MSEK (LHS)

Employees (LHS)

Number of acquisitions(RHS)

Group Presentation

Atlas Copco Capital Markets Day 2015

23

Acquired revenues and employees at the

time of the acquisition. Revenues from

distributors are not included.

Presence

86 Acquisitions

>BSEK 26Revenues

Innovation

WHY DRIVE FOR INNOVATION?

Creates sustainable customer productivity

Reduces life cycle cost

– Drives energy efficiency

– Increase safety

Drives organic growth

Supports/drives profitability

– Pricing power

– Cost savings

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2007 2008 2009 2010 2011 2012 2013 2014 Sept.2015

Research and development expenses, including capitalized expenditures, MSEK

Total as % of revenues

Group Presentation

Atlas Copco Capital Markets Day 2015

24

INNOVATION

Group Presentation

Atlas Copco Capital Markets Day 2015

25

Compressor Technique 2011 – 2015 Innovation

INNOVATION

Group Presentation

Atlas Copco Capital Markets Day 2015

26

Industrial Technique 2011 – 2015 Innovation

INNOVATION

Group Presentation

Atlas Copco Capital Markets Day 2015

27

Mining and Rock Excavation Technique 2011 – 2015 Innovation

INNOVATION

Group Presentation

Atlas Copco Capital Markets Day 2015

28

Construction Techniqe 2011 – 2015 Innovation

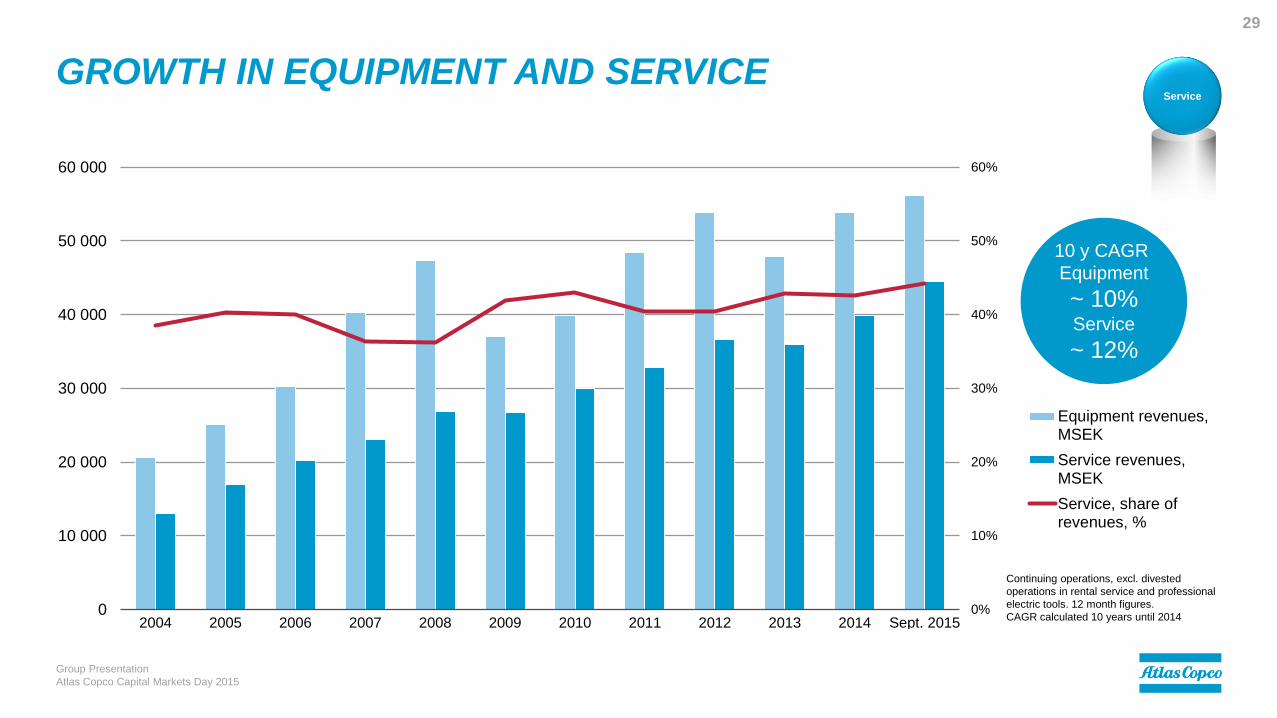

0%

10%

20%

30%

40%

50%

60%

0

10 000

20 000

30 000

40 000

50 000

60 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sept. 2015

Equipment revenues,MSEK

Service revenues,MSEK

Service, share ofrevenues, %

Group Presentation

Atlas Copco Capital Markets Day 2015

29

Service

Continuing operations, excl. divested

operations in rental service and professional

electric tools. 12 month figures.

CAGR calculated 10 years until 2014

10 y CAGR

Equipment

~ 10%Service

~ 12%

GROWTH IN EQUIPMENT AND SERVICE

OPERATIONAL EXCELLENCE

Group Presentation

Atlas Copco Capital Markets Day 2015

30

Work more efficiently

through lean and

standardized solutions

and processes

Spend less time on

administration and more

time with customers

Have consistent

business processes

Improve

financial performance

and increase

customer loyalty!

Operational

excellence

PEOPLE

Results-driven and committed culture

Time to competence

Diversity

Attract and retain talent

Group Presentation

Atlas Copco Capital Markets Day 2015

31

People

CULTURE, VALUES AND BUSINESS PRINCIPLES

Group Presentation

Atlas Copco Capital Markets Day 2015

32

“We grow loyal

and experienced

local leaders in

all countries”

People

AGILITY AND RESILIENCE

Group Presentation

Atlas Copco Capital Markets Day 2015

33

AGILE AND RESILIENT OPERATIONS

Group Presentation

Atlas Copco Capital Markets Day 2015

34

Volu

me / P

rofits

Deteriorating business climate

Reduce variable costs

Working capital reduction

Improving business climate

Add variable costs

Working capital increase

Small incremental

investments

Variable cost structure and asset light operations

Stable service business

Continuous investments in innovation

Competent and committed employees

Resilience

Agile

operational

set-up

- 800

- 600

- 400

- 200

0

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sept.2015

Restructuring costs,MSEK

-2,0%

-1,5%

-1,0%

-0,5%

0,0%

0,5%

in % of revenues

RESTRUCTURING WITHOUT RESTRUCTURING COSTS

Group Presentation

Atlas Copco Capital Markets Day 2015

35

Reported restructuring costs,

including impairments.

12 months figures

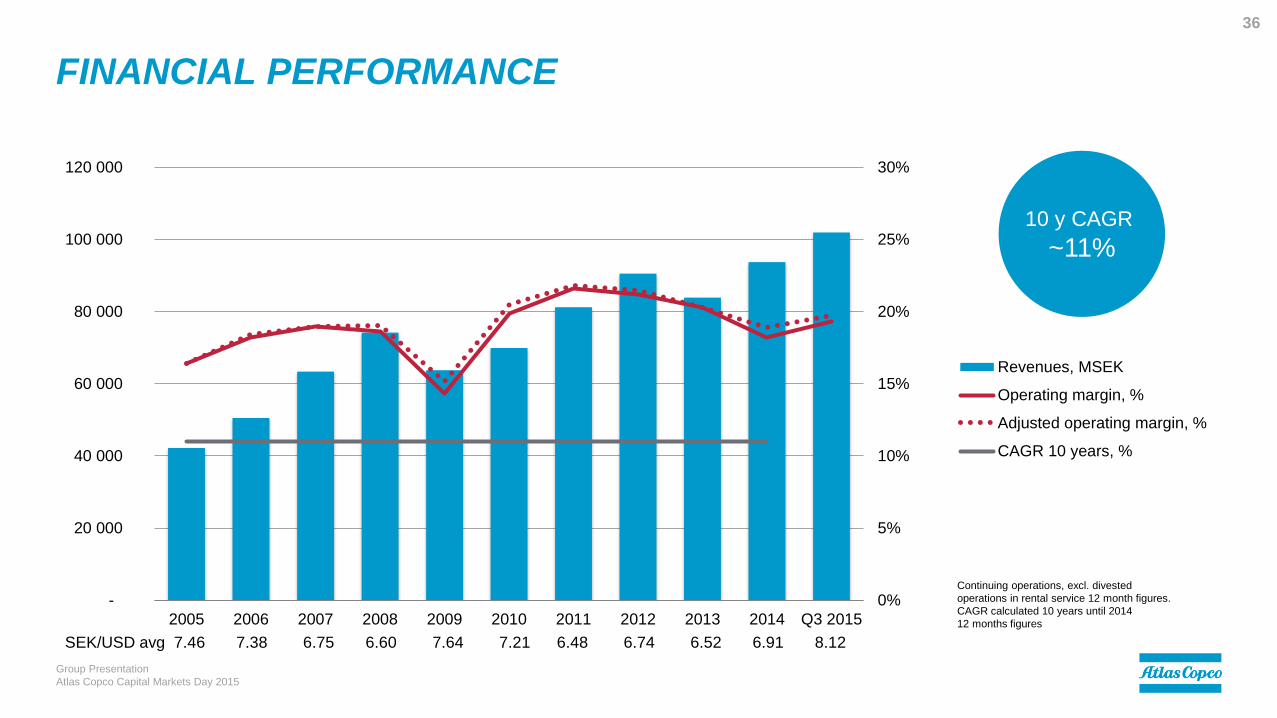

FINANCIAL PERFORMANCE

0%

5%

10%

15%

20%

25%

30%

-

20 000

40 000

60 000

80 000

100 000

120 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q3 2015

Revenues, MSEK

Operating margin, %

Adjusted operating margin, %

CAGR 10 years, %

Group Presentation

Atlas Copco Capital Markets Day 2015

36

Continuing operations, excl. divested

operations in rental service 12 month figures.

CAGR calculated 10 years until 2014

12 months figures

10 y CAGR

~11%

SEK/USD avg 7.46 7.38 6.75 6.60 7.64 7.21 6.48 6.74 6.52 6.91 8.12

Q4 94 - Q3 96 Q4 97 - Q3 99 Q2 00 - Q1 02 Q4 07 - Q3 09 Q1 12 – Q4 13

10.2%10.6%

12.6%13.2%

13.4%

12.7%

19.7%

15.9%

20.7%19.5%

20.7%

0%

5%

10%

15%

20%

25%

94

Q4

95

Q4

96

Q4

97

Q4

98

Q4

99

Q4

00

Q4

01

Q4

02

Q4

03

Q4

04

Q4

05

Q4

06

Q4

07

Q4

08

Q4

09

Q4

10

Q4

11

Q4

12

Q4

13

Q4

14

Q4

Operating margin, %

14%

-1%

3%

-3%

8%

-3%

14%

-18%

7%

-5% -4%-3%

-20%

-10%

0%

10%

20%

Average volume change in the period, %

RESILIENCE

Larger share of service

Lean foot-print – asset light

Decentralized Group

Group Presentation

Atlas Copco Capital Markets Day 2015

37

In periods of volume declines

Average volume change. Quarterly reported

operating margin, excluding Rental Service

0

5 000

10 000

15 000

20 000

25 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sept.2015

Average property, plantand equipment, MSEK

Average net workingcapital, MSEK

0%

10%

20%

30%

40%

50%

in % of revenues

in % of revenues

ASSET LIGHT

Group Presentation

Atlas Copco Capital Markets Day 2015

38

Average working capital and property,

plant and equipment Including

discontinued operations.

0%

50%

100%

150%

200%

0

5 000

10 000

15 000

20 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Sept.2015

Profit for the period,MSEK (continuingoperations)

Operating cash flow,MSEK

Cash conversion, %

Group Presentation

Atlas Copco Capital Markets Day 2015

39

CASH GENERATION

Cash conversion=operating cash flow / net

profit from continuing operations.

Operating cash flow adjusted from 2012 for

cash flows from currency hedges of loans

12 months figures

10 year cash

conversion

89%

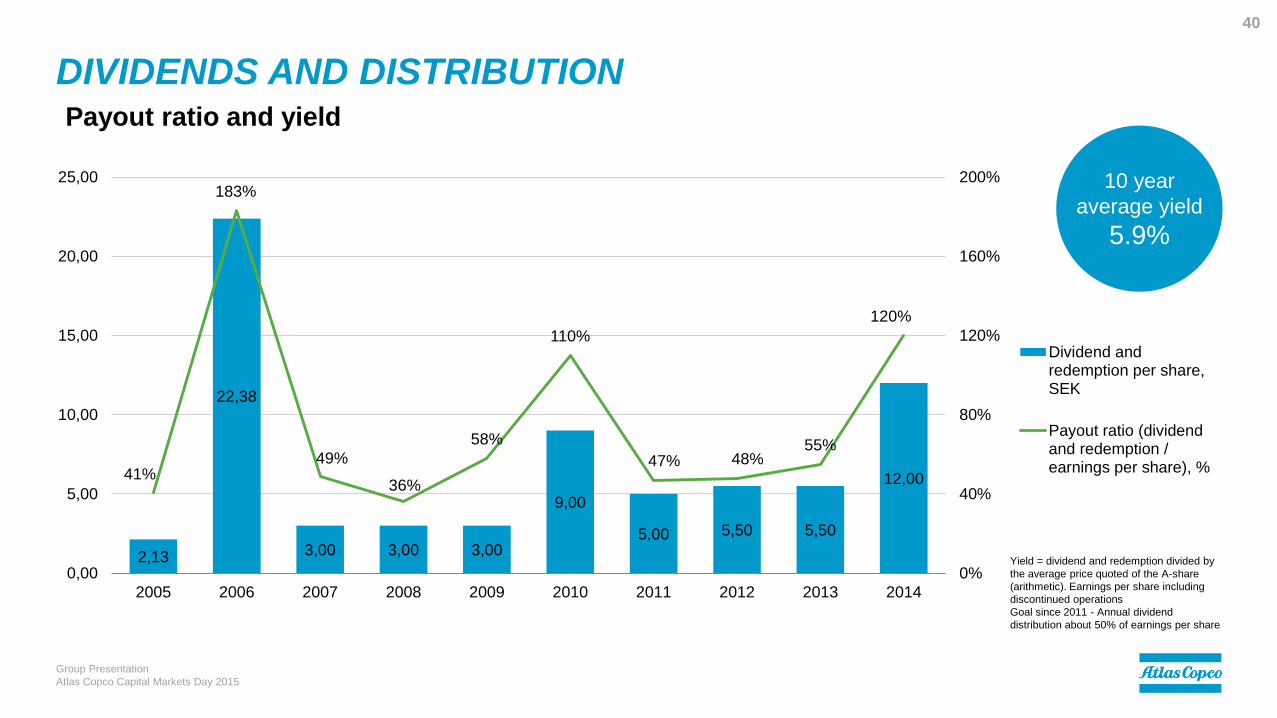

DIVIDENDS AND DISTRIBUTION

2,13

22,38

3,00 3,00 3,00

9,00

5,00 5,50 5,50

12,0041%

183%

49%

36%

58%

110%

47% 48%55%

120%

0%

40%

80%

120%

160%

200%

0,00

5,00

10,00

15,00

20,00

25,00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Dividend andredemption per share,SEK

Payout ratio (dividendand redemption /earnings per share), %

Group Presentation

Atlas Copco Capital Markets Day 2015

40

Payout ratio and yield

10 year

average yield

5.9%

Yield = dividend and redemption divided by

the average price quoted of the A-share

(arithmetic). Earnings per share including

discontinued operations

Goal since 2011 - Annual dividend

distribution about 50% of earnings per share

CAPITAL STRUCTURE

Group Presentation

Atlas Copco Capital Markets Day 2015

41

Net Debt*/EBITDA

* Net Debt adjusted for the fair value of interest rate swaps

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q3

Net Debt/EBITDA

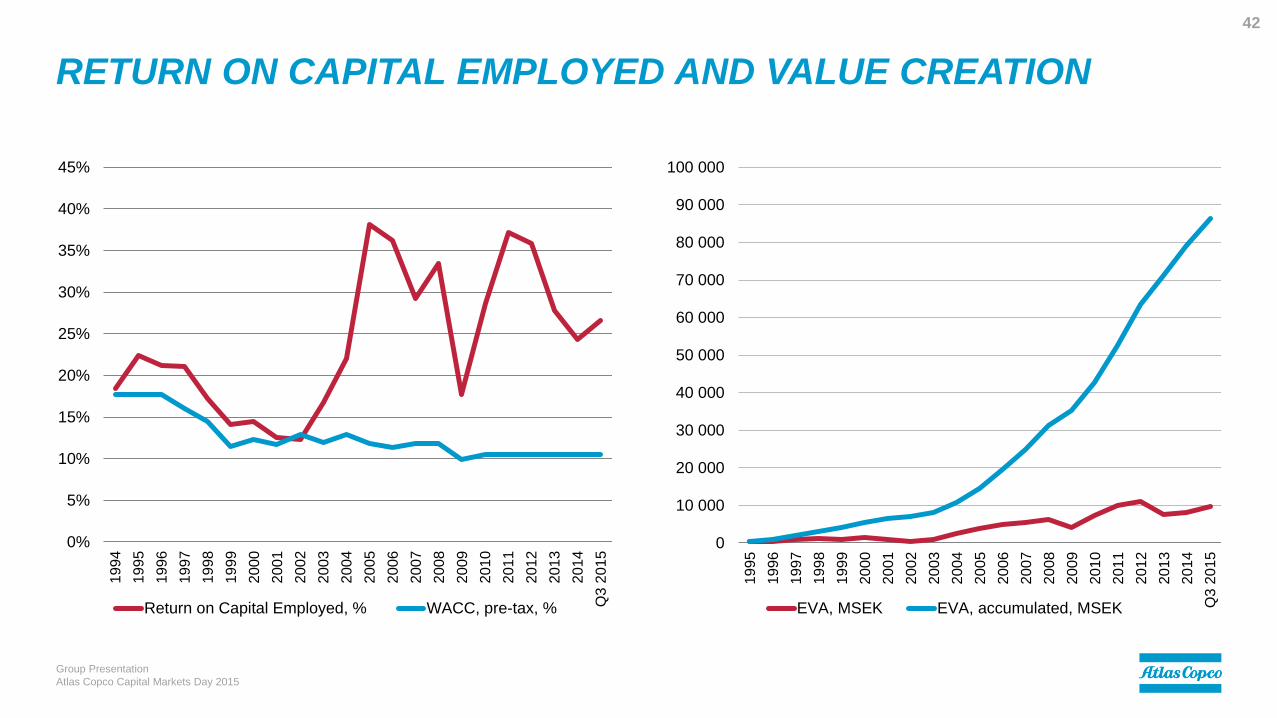

RETURN ON CAPITAL EMPLOYED AND VALUE CREATION

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Q3

20

15

Return on Capital Employed, % WACC, pre-tax, %

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Q3

20

15

EVA, MSEK EVA, accumulated, MSEK

Group Presentation

Atlas Copco Capital Markets Day 2015

42

SUMMARY

A world leading provider of sustainable

productivity solutions

Agile and resilient operations

Strong global service business

Consistent strategy

Strong cash generation and value creation

Fit for more

Group Presentation

Atlas Copco Capital Markets Day 2015

43

COMMITTED TO

SUSTAINABLE PRODUCTIVITY.

Group Presentation

Atlas Copco Capital Markets Day 2015

44

CAUTIONARY STATEMENT

“Some statements herein are forward-looking and the actual outcome could be materially

different. In addition to the factors explicitly commented upon, the actual outcome could be

materially and adversely affected by other factors such as the effect of economic conditions,

exchange-rate and interest-rate movements, political risks, the impact of competing products

and their pricing, product development, commercialization and technological difficulties, supply

disturbances, and major customer credit losses.”

Group Presentation

Atlas Copco Capital Markets Day 2015

46