1 1 | Page Auditing Notes AUDI 101 1- TEXTBOOK USED ETC: 9 OWN QUESTIONS AND ANSWERS 10 EFT : Electronic funds transfer............................................................10 terms: 12 INTRODUCTION 14 CHAPTER 1 :INTRODUCTION TO AUDITING 15 WHAT is an AUDITOR?:.........................................................................15 WHY IS THERE A NEED FOR AUDITORS ?:..........................................................16 Split between Mngmnt & Ownership:...........................................................16 Confidence in Financial Information........................................................16 Accountability:............................................................................16 ASSURANCE AND NON-ASSURANCE ENGAGEMENTS......................................................16 ASSURANCE ENGAGEMENTS:.....................................................................16 NON-ASSURANCE ENGAGEMENT (do not meet definition of an – or do not contain the Elements)...16 Reasonable Assurance.........................................................................17 Limited Assurance Engagements:...............................................................17 Statutory and Non-Statutory Engagements......................................................17 Auditing postulates. 8 of by mautz & sharaf in philosophy of auditing 1961.................17 The accounting profession :..................................................................18 Accounting bodies in sa......................................................................18 pronouncements which regulate the profession.................................................19 The financial statement audit engagement.....................................................19 Introduction...............................................................................19 A MODEL OF INDEPENDANT AUDIT OF FIN STATS ARISING OUT OF COMPANIES ACT (STATUTORY AUDIT)...19 The roles of the various parties.................................................19 Role of companies act......................................................................20 assertions:................................................................................20 SUMMARY:...................................................................................20 CHAPTER 2 : GENERAL PRINCIPLES OF AUDITING.(ch 3 in book) 21 internal control.............................................................................21 Introduction...............................................................................21 Definition of Internal control.............................................................21 definition (per SAICA booklet :'guidance for directors:reporting on internal controls').......................................................................21 four ASPECTS of internal control from above definition..........................21 (ISA 315). 5 components of internal control (in ch 7)...........................21 internal control objectives................................................................21 limitations of internal control............................................................21 the accounting system......................................................................22 1

Transcript

1 1 | P a g e Auditing Notes AUDI 1011- TEXTBOOK USED ETC: 9

WHAT is an AUDITOR?:................................................................................................................................................. 15

WHY IS THERE A NEED FOR AUDITORS ?:...........................................................................................................................16

Split between Mngmnt & Ownership:.................................................................................................................16

Confidence in Financial Information..................................................................................................................16

Statutory and Non-Statutory Engagements........................................................................................................................17

Auditing postulates. 8 of by mautz & sharaf in philosophy of auditing 1961...............................................................................17

The accounting profession :........................................................................................................................................... 18

Accounting bodies in sa................................................................................................................................................ 18

pronouncements which regulate the profession..................................................................................................................19

The financial statement audit engagement........................................................................................................................19

A MODEL OF INDEPENDANT AUDIT OF FIN STATS ARISING OUT OF COMPANIES ACT (STATUTORY AUDIT)........19

The roles of the various parties...............................................................................................................................................19

Role of companies act........................................................................................................................................ 20

Definition of Internal control..............................................................................................................................21

definition (per SAICA booklet :'guidance for directors:reporting on internal controls')..........................................................21

four ASPECTS of internal control from above definition........................................................................................................21

(ISA 315). 5 components of internal control (in ch 7).............................................................................................................21

internal control objectives.................................................................................................................................21

limitations of internal control.............................................................................................................................21

the accounting system.......................................................................................................................................22

who is interested in what?.................................................................................................................................22

The characteristics of good internal control.......................................................................................................22

2 2 | P a g e Auditing Notes AUDI 101appropriate evidence..............................................................................................................................................................24

Influenceing factors in determining whether sufficient appropriate evidence has been obtained.........................................25

DIAGRAM OF ASSERTIONS:.....................................................................................................................................................26

EXAMPLES OF ASSERTION CLASSIFICATION IN PRACICE:........................................................................................................26

The Auditors toolbox:................................................................................................................................................... 27

TESTS OF CONTROLS......................................................................................................................................... 27

steps in the sampling exercise...........................................................................................................................29

Chapter 6 : an overview of the audit process. 31

Stages of the audit process: (know whole chapter per lecturer )..............................................................................................31

How the stages are linked:............................................................................................................................................ 31

role of ISA's : International standards on auditing................................................................................................................32

DETAILS OF EACH STAGE OF THE AUDIT PROCESS:...............................................................................................................32

CHAPTER 7 : UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT. 37

UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT:........................................................................................................37

DEFINITIONS: as per isa 315..............................................................................................................................37

THE ENTITY AND ITS ENVIRONMENT..................................................................................................................38

Internal Control of Entity....................................................................................................................................39

1) component : the control environment............................................................................................................................40

ENTITYS RISK ASSESSMENT PROCESS :....................................................................................................................................40

Component : Control Activities: (internal controls)................................................................................................................40

Component : Monitoring of Controls:.....................................................................................................................................40

COMPONENT: THE INFORMATION SYSTEM:...........................................................................................................................41

THE CONCEPT OF MATERIALITY....................................................................................................................................... 42

3 3 | P a g e Auditing Notes AUDI 101planning materiality and final materiality..........................................................................................................42

the nature of materiality.................................................................................................................................... 43

Planning for qualitative assessment:......................................................................................................................................43

the 4 Factors to be considered when quantifying planning materiality..................................................................................43

Final materiality................................................................................................................................................. 43

1) The Auditor must do the following to make a final materiality decision:........................................................................43

Factors to be considered in evaluating unresolved audit differences.....................................................................................43

the risk Based approach to auditing..................................................................................................................44

The components of audit risk:............................................................................................................................44

Control Risk.............................................................................................................................................................................44

Risk and materiality........................................................................................................................................... 45

Assessment of audit risk....................................................................................................................................45

levels of risk....................................................................................................................................................... 45

THE AUDITORS RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS.....................................................46

DEFINITIONS (LECTURER SAYS KNOW THESE WELL)..........................................................................................46

resposibility of management and those charged with governance:...................................................................47

resposibility of the auditor.................................................................................................................................48

responses to the risk of material misstatement due to fraud (DO LEARN THIS as per lecturer).........................48

At Financial Statement level:..................................................................................................................................................48

At Assertion level:...................................................................................................................................................................48

Evaluation of Evidence:...........................................................................................................................................................49

fraud risk factors (do learn)...............................................................................................................................50

2) fraud risk factors relating to misstatements resulting from misappropriation of assets:................................................51

communication with management and those charged with governance (not learn).........................................52

fraud and retention of clients (do learn)............................................................................................................52

3

4 4 | P a g e Auditing Notes AUDI 101CHAPTER 8: COMPUTER AUDIT THE BASICS. 54

DEFINITION OF A GENERAL CONTROL:...............................................................................................................56

CATEGORIES OF GENERAL CONTROLS...............................................................................................................57

CONTROL ENVIRONMENT AND SECURITY POLICY:.............................................................................................57

ORGANISATIONAL STRUCTURE AND PERSONNEL PRACTICES............................................................................57

STANDARDS AND STANDARD OPERATING PROCEDURES...................................................................................58

SYSTEMS DEVELOPMENT CONTROLS (NB know very well).................................................................................59

program change controls...................................................................................................................................60

APPLICATION CONTROL FRAMEWORK : MASTERFILE AMENDMENTS..................................................................62

NB ..................................................................................................................................................................... 62

APPLICATION CONTROL FRAMEWORK : INPUT....................................................................................................62

APPLICATION CONTROL FRAMEWORK : PROCESSING.........................................................................................63

APPLICATION CONTROL FRAMEWORK : OUTPUT................................................................................................63

MENU AND DESCRIPTION OF CONTROLS above:................................................................................................64

HOW DO CAATS FIT IN AUDIT PROCESS.............................................................................................................67

SYSTEM ORIENTATED CAATS.............................................................................................................................67

DATA ORIENTATED CAATS.................................................................................................................................67

FACTORS WHICH WILL INFLUENCE DECISION TO USE CAATS.............................................................................67

AUDIT FUNCTIONS WHICH CAN BE PERFORMED USING DATA ORIENTATED CAATS...........................................67

APPENDIX 1: ILLUSTRATION OF WHAT A DATA ORIENTED caat CAN DO:...........................................................68

THE USE OF MOBILE INFORMATION &COMMUNICATION TECHNOLOGY ON AUDITS.....................................................................68

WHAT THIS TECHNOLOGY CAN DO....................................................................................................................68

SECURITY IMPLICATIONS OF USING MOBILE INFORMATION AND COMMUNICATIONS TECHNOLOGY ON AUDITS........................................................................................................................................................................... 68

Security of clients files:...................................................................................................................................... 68

the ifac code of ethics........................................................................................................................................ 69

General guidance: Ethics and Professional Conduct..........................................................................................69

The Public Interest............................................................................................................................................. 69

4

5 5 | P a g e Auditing Notes AUDI 101Pronouncements relating to ethics and professional conduct in South Africa....................................................69

THE IFAC (SAICA) CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS..........................................................69

1) PART A - GENERAL APPLICATION OF THE CODE..............................................................................................................70

PART B PROFESSIONAL ACCOUNTANTS IN PUBLIC PRACTICE.................................................................................................73

PART C - PROFESSIONAL ACCOUNTANTS IN BUSINESS...........................................................................................................75

PART d - PROFESSIONAL ACCOUNTANTS IN SOUTH AFRICA...................................................................................................75

Trends in IT............................................................................................................................................................... 78

Audit Implications of Networks:...................................................................................................................................... 78

audit and control implications:.......................................................................................................................................79

Audit and control implications of EDI:................................................................................................................80

THE INTERNET............................................................................................................................................................ 81

Risks and controls:trading on the internet:........................................................................................................81

CATEGORIES of VIRUS:....................................................................................................................................... 82

AUdit and control implications:..........................................................................................................................83

Chapter 10 : Revenue AND RECEIPTS CYCLE 84

ACCOUNTING SYSTEM AND INTERNAL CONTROLS:..............................................................................................................84

DOCUMENTS USED IN THE (Revenue+receipts)CYCLE.......................................................................................84

CHARATERISTICS OF GOOD INTERNAL CONTROL...............................................................................................84

FLOW CHARTS AND DESCRIPTION OF THE CYCLE..............................................................................................85

Auditing the CYCLE:........................................................................................................................................... 87

financial statement assertions -in this cycle-(Isa 500).......................................................................................87

Important accounting aspects : specially for this cycle......................................................................................88

Fraud in the cycle.............................................................................................................................................. 88

TEsts of controls and substantive procedures....................................................................................................89

tests of controls................................................................................................................................................. 89

DIAGRAM OF ASSERTIONS:.....................................................................................................................................................90

substantive procedures for the audit of debtors:...................................................................................................................90

Use of audit software (substantive procedures) for debtors..............................................................................92

substantive procedures for auditing bank/cash.................................................................................................92

5

6 6 | P a g e Auditing Notes AUDI 101Chapter 11 : Acquisitions and payments cycle: 94

The accounting system and internal controls:.....................................................................................................................94

documents in the cycle:.....................................................................................................................................94

characteristics of good internal control:.............................................................................................................94

flowchart and description of cycle.....................................................................................................................95

auditing the cycle:....................................................................................................................................................... 96

Financial statement assertions and this cycle....................................................................................................96

FRAUD in the cycle............................................................................................................................................ 97

TESTS OF CONTROLS:........................................................................................................................................ 97

Characteristics of the cycle..............................................................................................................................100

Documents in the cycle...................................................................................................................................100

3 Objectives of the cycle..................................................................................................................................100

Risks of the cycle............................................................................................................................................. 101

Auditing the cycle:........................................................................................................................................... 104

Important accounting aspects –ias2 –inventories.................................................................................................................104

fraud in the cycle:............................................................................................................................................ 105

tests of controls and substantive procedures:.................................................................................................106

Tests of controls....................................................................................................................................................................106

POST INVENTORY COUNT PROCEDURES: (bit nb sort of)......................................................................................................107

the use of audit soft ware (substantive testing)....................................................................................................................108

chapter 13 payroll and personell cycle 110

accounting system and internal controls.............................................................................................................110

Documents used in the cycle:..........................................................................................................................110

characteristics of good internal control:...........................................................................................................110

flowchart & description of cycle :.....................................................................................................................110

Auditing the cycle................................................................................................................................................ 112

fraud in the cycle............................................................................................................................................. 113

audit procedures: salaries & related accounts......................................................................................................................113

audit procedures :Wages & related Accounts:.....................................................................................................................114

6

7 7 | P a g e Auditing Notes AUDI 101the use of audit soft ware (substantive procedures)........................................................................................115

HOW TO DO A RECONCILLIATION FOR SALARIES AND WAGES AS PER IAS ACC. STANDARDS IN THE NOTES TO THE FIN. STATS................................................................................................................................................ 116

7

8 8 | P a g e Auditing Notes AUDI 101

8

9 9 | P a g e Auditing Notes AUDI 101

1-1-TEXTBOOK USED ETC:TEXTBOOK USED ETC: AUDITING NOTES FOR SOUTH AFRICAN STUDENTS : JACKSON AND STENT : LEXIS NEXIS PUBLISHERS 2000 6TH EDITIONGRADED QUESTIONS ON AUDTING GOWAR & JACKSONPOOPEDI

9

10 10 | P a g e Auditing Notes AUDI 101

OWN QUESTIONS AND ANSWERSOWN QUESTIONS AND ANSWERS1) A SUBJECT MATTER: Eg: Financial Position or Results of operations 2) WHAT IS STATEMENT of changes in equity and Cash Flow Statement? : fin position or fin performance ?3) Assertions: account balances,pg 5/13 eg valuations &allocation ;does this heading include for lower down allocation

eg in journal level , so is it too much in repairs ,or too much in vehicles and not machines,BEFORE it all gets to Inc.Stat heading of TOTAL repairs + maintenance.

4) Are creditors (from Account Balances) Rights or Obligations or Both? How?(no rights – only obligations!)pg 5/135) Do assertions form the 'BASIS' of the fin stats.6) Ask where : duty of fin acc. to ensure best capital structure : find best interest rates of all banks, each month,esp.

special rates for large sums / personal atttention. 7) (2)how do you find the current usury rates for b2b and b2c. (are they different? Where and how?)8) Can you segregate backwards ; ie: 2= executing-sales clerk takes order 1= credit controler authorise 3= custody=

store clerk picks order and sends out. (or what is execute = delivery note made up + or delivery man checks order+or security guard check +or not storeman does stock count– which number do these fit into)

9) Assertions :Account balances +classes of transactions&events ;?difference is it –Bal Sheet + Income Stat. ONLY or ?10) Presentation& disclosure pg5/12 –what is this . Also the example :'contingent liabilities'is this a 'note' or just

Creditors/ –ONLY in NOTES or also general format of balance sheet,methods used in journals+ledgers etc?11) What about pg 5/13 assertions –disclosure and presentation- occourance and rights and obligations- shouldnt these

2 be separated and what is rights and obligations here?12) Pg 5/13 3.3.4 accuracy and valuation : should this be broken up into accuracy and valuation and allocation? Why

does this (former) heading not appear in table below this??13) It seems assertions not very exactly classified- why pg 5/16 4.3 transactions= presentation&disclosure and not

classification&understandability. Is measurement = accuracy. Is classifiction & UNDERSTAND only for presentation/disclose not for transactionas/

14) Is pg 5/19 -18 sampling risk mixed up where two types give explanation- visa versa for 1 st test of controls thing maybe ??

15) Is Gov. Audit Statutory or Not : Answer : YES16) What is ISA stand for eg ISA 506 Answer : international standards on auditing :17) ACCESS CUSTODY CONTROLS:

(a) Information =ASSET :eg destroy debtors masterfile,make electronic payments, etc.(b) info can be regarded as an asset which must be controlled/guarded in same way(c) Computers can enhance : this by features eg:??? regular mini – stock counts (cycle counts)? ???to

recon theoretical to actual. How does this work between ????18) When an auditor comes to check your stuff: how should fin accountant treat the following issues:

a) How do you ask if the software used was thoughtroughly tested by a computer audit specialist?wont corrupt your files.can you ask to phone some of his other clients to ask if no problems?i) Are any CAATS notorious / or any specific procedures/ notorious for causing a problem.

b) How do you grant only read accessc) What should one watch out for /some pointers on how to treat an audit –

i) with a computer audit(eg: corruption of files )ii) with other type of audits.

SEMESTER II

Q1- what is yellow highlight below:ie: ”client held”

EFT : ELECTRONIC FUNDS TRANSFER1) 2 Important points to remember with EFT:

10

11 11 | P a g e Auditing Notes AUDI 101a) It is Transfer of CASH : in a flash – so bad controls =gone.b) 1 function in a CYCLE: eg wage cycle – all controls contribute to VAC of payment.

2) Whatever the system : EFT payments should be in 4 steps:(eg for a wage payment system)a) MASTERFILE AMENDMENTS:

i) Any amendments to it must be VAC – V=not ficticious employee A=no errors on account details of employee C-…..

b) PREPARE THE EFT PAYMENT ( before the payment): i) Payments to be made must be VAC :

(1) V= fin.Accountant must authorize it –AFTER CHECK supporting DOCS etc.(2) A=fin.Acc should TEST COMPUTATIONS on payroll before authorizing.(3) C=fin Acc. Should CONFIRM NO. OF TRANSFERS = No. of employees.(4) NOTE: just examples- the full range of controls to be effected befor payment is in the ‘Cycle’ chapters.

c) EFFECT THE PAYMENT: d) AFTER THE PAYMENT: Controls to ensure that transfers actually made WERE VAC.

i) System MUST supply an AUDIT TRAIL of all EFT’s made to date.(Hardcopy or Onscreen)ii) Audit TRAIL TO BE REVIEWED BY SENIOR personnel and tied back to “client held” documentation.

Q2-ask yellow why queries from debtors not by the person who is in charge of debtors ie:debtors clark , eg: the person in charge of creditors, debtors, etc.8-Recording of Receipts

1-deposits not recorded/or timeously2-recorded deposits may (a)inaccurate (b)overstated(fictitious) (c)cr to wrong debtor

1-CRJ daily by date & number from receipts (if rec. issued)2-Queries from debtors : by person independent of 1’debtors’ & 2’banking&recording of cash functions.’3-recon1 bank statement TO cash book mnthly + independentof banking&recording employee + reviewed by senior official.4-recon2 CRJ supervisor (a)CRJ vs gaps 1dates 2sequential (b) test CRJ to DL5-recon3 DL to GL control acc. Independent employee regular

Assertion : valuation & allocation : isn’t it a bit similar to ‘classification and presentation’ , what the difference between italics.1) What is a year end creditors recon? what is a creditors list- a ledger Y/N?

1. HOW DO the method for doing a inventory count while there is dispatch going on in the background?2. What is the yellow here, so variable selling costs eg marketing or commission must be subtracted from ‘closing

stock’ in the financial statement or how??normall this is a period cost is it not :? Definition:Net Realisable value :

i. The estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale.

3.

11

12 12 | P a g e Auditing Notes AUDI 101

TERMS:TERMS:

1) Verify : means determine somethings truth or falsity.2) AUDIT OBJECTIVE 3) FORMING AN OPINION : make up your mind.4) FAIR PRESENTATION of fin info/ fin stats : properly ,correct5) Cycles of company.( in duty segregation)6) Function s of company( in duty segregation)7) material : do make a difference.8) misstatement : wrong entry/number etc.9) appropriately : 10) Corroborative Evidence : evidence which confirms/corroborates something eg: to obtain info from a debtor to

confirm his account is what it says. 11) ASSURANCE GIVER . 12) ASSURANCE ENGAGEMENT 13) Audit Differences : show a material misstatement in Fin.Stats. or Not.( OVERS AND UNDERS SCHEDULE)14) OVERS AND UNDERS SCHEDULE : shows all the “Audit Differences” which are the differences between what the fin.

Stats. Say and what auditor works out to be the real figures.1) Definition; ISA315 :risks that require : Special audit consideration15) Emoluments :16) Misallocate : eg an expense to wrong account 17) Batch Control System: system of controlling physical movement of data (eg invoices,wage cards,printouts output)

to and from user Depts.18) Compilation engagement : 19) Agreed upon procedure engagement : 20) Conducted : done,eg employees conducted a control procedure21) Casts: means addition in accounting of number of fields.22) Extentions: 23) Allocate : overheads for job costing/manufacturing/std.costing. or allocate expenses etc to correct account in

ledger24) Accumulate : costs eg direct labour and materials, to each specific account by journalizing it for job costing or

std.costing25)

12

13 13 | P a g e Auditing Notes AUDI 101

13

14 14 | P a g e Auditing Notes AUDI 101

INTRODUCTIONINTRODUCTION1. Text Book :Jackson & Stent :Auditing notes for SA students. + Graded Questions edition 9 from same authors

second book.2. Coursework semester 1: Chapter 1+5+7+8 then briefly back to 3 one or 2 sections3. 2/3 tests +3/4 assignments4. Lect: Mr Poopedi, 3rd floor Kblock 1st room on left.5. Lectures :mon 1st ,wed 2+3 , fri some or other.

14

15 15 | P a g e Auditing Notes AUDI 101

CHAPTER 1 :INTRODUCTION TO AUDITINGCHAPTER 1 :INTRODUCTION TO AUDITING -------------------------------------------------------------------------------------------------------------------------------------

WHAT IS AN AUDITOR?: 1. An Auditor = ASSURANCE GIVER. : from word “audire” Latin means “to hear” from owner hear/audit to employ

a auditor.2. An Audit = ASSURANCE ENGAGEMENT. : “ expresses a conclusion designed to enhance the degree of

confidence of the intended users other than the responsible party ,about the outcome of the evaluation or measurement of a subject matter against the criteria (attempt to enhance credibility of a “statement; event ; figures)

3. International Framework for Assurance Engagements : defines an assurance engagement as: “ in which thea practitioner expresses a conclusion designed to enhance the degree of confidence of the intended user…”

4. The basic premise = ‘Enhance credibility of information’ or ‘increasing degree of confidence of users’5. TYPES OF AUDITOR :

1-Enhance whos confidence2-Independant of what3-What do they do 4 anything else might want to add

a. EXTERNAL AUDITORSi. 1-Independent of company audited opinion - 2-fin stat fairly present fin pos + results – 3-lend

credibility + enhance confidence users of fin stats.4-for statutory purposes, more for external users needs,less ,but also,for internal(head office confidence subsidiary)

6. COMMON ESSENTIAL CHARACTERISTIC : 1. Characteristic of INDEPENDENCE. …….if not independent=NOT A VALID AUDIT.

7. OTHER ESSENTIAL CHARACTERISTICS: IFAC code ethics for Prof. Accountants.

15

Income Statement

Statement of Equity

16 16 | P a g e Auditing Notes AUDI 1011 INTEGRITY :straightforward , honest , moral2 OBJECTIVITY : impartial, fair, not influenced by prejudice/bias (independent)3 PROFESSIONAL COMPETENCE and DUE CARE:maintain professional knowledge/skill at

required level &performing work diligently.( eg auditors must attend min 1 symposium on IFRS per year by SAICA law to be a member)

4 CONFIDENTIALITY: respecting the confidentiality of client information.5 PROFESSIONAL BEHAVIOUR: comply laws ®ulations , avoid behavior which discredits

the profession.

WHY IS THERE A NEED FOR AUDITORS ?: SPLIT BETWEEN MNGMNT & OWNERSHIP: 1) Owners -Management split –need Auditor to verify : truth,correct,fair presentation for owner.(owner not

time/expertise to do it)as business evolved …

CONFIDENCE IN FINANCIAL INFORMATION. 1. Investors in businesses that fin info is reliable2. Gov. can trust Fin Info to set the tax rate equitable basis, run economy3. Investors direct toward needs which?-risk/return4. Develop economy as a whole- ensure funds go to sound mngmnt,strong productiveity,sound FinPos5. Inspire confidence in how gov handles its finances

ACCOUNTABILITY:1. Directors to company etc –Gov. to taxpayers – Companies for treatment of Environment etc + SOUND

CORPORATE GOVERNANCE.

ASSURANCE AND NON-ASSURANCE ENGAGEMENTS. ASSURANCE ENGAGEMENTS:1) As per International Framework for Assurance Engagements :An assurance engagement is one in which the

professional accountant: “ expresses a conclusion designed to enhance the degree of confidence of the intended users other than the responsible party ,about the outcome of the evaluation or measurement of a subject matter against the criteria “

2) Elements of an Assurance Engagement.: a) THREE PARTY RELATIONSHIP :1-Prof. accountant 2-Responsible Party 3-Intended User

i) Eg: 1-registered auditor 2-directors responsible for AFS 3-shareholdersb) A SUBJECT MATTER: Eg: Financial Position or Results of operations c) SUITABLE CRITERIA : Eg: International Fin. Reporting Standards (IFRS)d) SUFFICIENT APPRORIATE EVIDENCE : Eg: evidence needed to conclude Fin Stats free of material misstatementse) WRITTEN ASSURANCE REPORT : Eg: The Audit Report on Fair Presentation.

3) Examples :Assurance Engagements : a) Audit of Fin Stats : The Registered auditor gathers sufficient appropriate evidence to be in a position to pass an

opinion on whether the directors ,who are responsible for the AFS , have applied the IFRS standards appropriately in presenting fairly,the fin pos fin perf. and cash flow info.

b) Other types: 1-effectiveness of internal control system ( there are criteria/standards) 2-COMPLIANCE WITH SARBANNES-OXLEY ACT.

NON-ASSURANCE ENGAGEMENT (DO NOT MEET DEFINITION OF AN – OR DO NOT CONTAIN THE ELEMENTS)

a) Where does not :enhance credibility, and pass an opinion , but rather perform a task eg:

16

17 17 | P a g e Auditing Notes AUDI 101b) Eg: no 3rd party involved , or client does not require assurance, or no suitable criteria/benchmarks.c) Eg: Tax Return , or compile(collect+classify+summarise) certain info. Etc,efficiency,correct sales strategy,

REASONABLE ASSURANCE. 1) Auditor DOES NOT ever CERTIFY / or CONFIRM CORRECTNESS :he only EXPRESSES AN OPINION on it's FAIR

PRESENTATION.2) Reasonable assurance THAT NO misstatement done- NOT 100% correct to be sure! A REASONED OPINION IS GIVEN.3) WHY AUDITOR CANNOT CERTIFY FINANCIAL STATEMENTS :

a) The use of testing :ONLY % OF ALL TRANSACTIONS CHECKED-Called 'TEST CHECKING'- expensive /time constraints.

b) INHERENT LIMITATIONS OF ACCOUNT & INTERNAL CONTROL SYSTEMS: -must place reliance on clients safety features inherent limitations-no system is 100% foolproof.

c) Audit evidence is usually (Docs etc.) PERSUASIVE not CONCLUSIVE. – eg: documents only persuade that a transaction took place –not prove it(must rely on documenty!

d) SUBJECTIVITY OF FINANCIAL STATEMENTS & AUDITORS APPROACH to audit.- i) Eg : Subjective estimates of Eg : Fixed & Current Assets -bad debts /depreciation impairment,stock

obsolescence-e) SUBJECTIVITY OF FINANCIAL STATEMENTS & AUDITORS APPROACH to audit.-

i) Auditors choice & timing of tests varies one to the next auditor.

LIMITED ASSURANCE ENGAGEMENTS: International framework for assurance engagements further classifies assurance engagements into Limited Assurance Engagements and Reasonable Assurance Engagements –further done in ch 19.

STATUTORY AND NON-STATUTORY ENGAGEMENTS. 1) Statutory Engagements : required by Act of Parliment. eg: 1-company annual audit.(companies Act) 2-

Fin.Institutions Act=bank annual audit2) Non-Statutory Engagements :NOT required by law. Eg: audited Fin. Stats. For a loan or if a partnership/C.C. builds

into partnership/ association agreement or if a Regulatory Body requires assurance with Corporate Governance requirements.

AUDITING POSTULATES. 8 OF BY MAUTZ & SHARAF IN PHILOSOPHY OF AUDITING 1961 Definition: Postulate. Thing claimed as a basis for reasoning, and, Provides a starting point/fundamental condition as a basis for thinking about things & arriving at solutions.The very foundation on which the discipline is built.

1) No neccessary conflict of interests exist between the auditor and 1-Management OR 2-Employees of the enterprise. a) Both client and auditor want Fin Stats to achieve fair presentation ,management is not trying to cheat.b) It becomes impossible to do a conventional (normal) audit if mngmnt are trying to cheat.- economicly &

operationally feasablec) In current times relevance becoming questionable due to rising fraud etc of mngmnt.d) For todays times and latest auditing standards newly developed : AUDITOR CANNOT ACCEPT THIS POSTULATE

AS BEING TRUE, HE MUST EVALUATE MNGMNT INTEGRITY WITH {'PROFESSIONAL SCEPTICISM' –ONE OF PRINCIPLES OF Generally Accepted Auditing Standards }–NOT BE LED AROUND BY THE NOSE-

e) Similar to (5) – very expensive or impossible audit if Mngmnt Unreliable.2) An Auditor must Act 1-Exclusively As An Auditor in order to be able to Offer an 1-Independant and 2-Objective

Opinion on the 1-Fair Presentation of Fin. Info. ( to be INDEPENDANT)a) Free of bias,independant ,cannot do other work for client eg: accounting.b) Currently under fire eg: enron+anderson accounting etc.

3) The Professional Status of the independant auditor Imposes commensurate Professional Obligations.

17

18 18 | P a g e Auditing Notes AUDI 101a) Concepts of 1-Due Care , 2-Service before personal interest , 3-Efficiency ,4-Competence.

4) Financial data is Verifiable.a) It is possible to verify clients data.- there will be sufficient evidence to support transactions.b) Audit Objective of forming an opinion on fair presentation of fin info/ fin stats. Needs verification or cannot.c) Eg e-commerce ...must develop new ways of verification.d) Poor internal controls make fin. Info. NOT verifiable.

5) Internal Controls reduce the Risk of Errors & Irregularities.a) Makes errors possible not plausible ,eg sequential numbering makes duplication/omission of source docs.

Reduced.b) The more controls, the less detailed investigation/less samples. Zero controls =cannot do audit /or very

expensive.6) Application of IFRS results in fair presentation .(international financial reporting standards)

a) If you adhere to GAAP FRAMEWORK –it results in fair presentation.( not his own personal preference ,but GAAP)

7) That which Held True in the Past will Hold True in the Future, in the absence of any Contrary Evidence.a) Factual historical evidence more powerful than speculation, eg: measure Prov. Bad Debts. By history of

debtors.-But eg: directors integrity may decline. 8) The Fin. Stats. submitted to auditor for verification are free of Collusive and other unusual Irregularities.

a) Unless contrary evidence, it can be taken for granted that management took steps to prevent collusion, and they were not involved in any.

b) These Made in1961 –current cynisism- current focus on Corporate Governance – Introduction of Professional Sceptisism as important prereqiusite for auditors lately –The objective of auditors is: fair presentation – NOT an all out search for fraud.

THE ACCOUNTING PROFESSION : 1) Professional Status is achieved by the PUBLIC recognising a BODY OF PRACTITIONERS.2) SAICA says a profession is distinguished by:

a) Professional offers : mastery specialised skills ( by study,practical training)b) Render services to a High standard of conduct +performance .(Regulatory mechanism/ regulatory body -laws

restricting admittance,freedom from uninhibited competition, voluntary advancement of profession,ethical code)

c) Accept duties to society as a whole + to client+employer. d) Objective outlook . Members of profession show ethical commitment above monetary gain.(peer evaluation

not 'most moneye) OF PARTICULAR IMPORTANCE IS PRINCIPLE OF OBJECTIVITY. f) Integrity + Prof Skills&due care +Objectivity +Confidentiality.

ACCOUNTING BODIES IN SA 1) SAICA S A institute of chartered accountants.

a) Registeredwith IFAC international federation of accountants – looks after interests of professional accountants.(all types)

2) ACCA Assosiation of chartered certified accountants.3) CIMA Chartered institute of management accountants4) IRBA Independant regulatory board for auditors brought intp being by Auditing Profession Act.to replace PAAB

public accountants and auditors board.public accountants and auditors act was repealed same timea) Looks after intersts of auditors + pulic + discipline auditor members.b) ALL AUDITORS must register with the IRBA after passing part 1+2 of saica exam and be member of saica-AS PER

LAW.5) IAASB- international auditing and assurance standards board formulate the:6) IFAE :International Framework for Assurance Engagements

18

19 19 | P a g e Auditing Notes AUDI 1017) IFRS –international fin. reporting standards.8) IFAC (international federation of accountants)9) ISA –International standards on auditing

PRONOUNCEMENTS WHICH REGULATE THE PROFESSION. 1) In order to ensure high standards of ethics conduct & skill,

a) ISA 200 states ; objectives & general principles governing an audit of Fin Stats. :i) Comply with IFAC code of ethics for professional accountantsii) Conduct audit accordance International standards on auditing.

b) Legislation to ensure : ( some examples of 8 or more)i) Companies Act 2008ii) SAICA constitution and by-laws.iii) Auditing profession act 2005iv) IRBA rules& codev) IFAC code of ethics for professional accountantsvi) International auditing practice statements(IAPS)vii) South African auditing practice statements(SAAPS)viii)International standards on

(1) Auditing(ISA)(2) Review engagements(ISRE)(3) Assurance engagements(ISAE)(4) Related services(ISRS)

THE FINANCIAL STATEMENT AUDIT ENGAGEMENT. INTRODUCTION.1) An EXTERNAL Audit Engagement is called an ASSURANCE engagement + must be conducted by a registered

auditor.2) The OBJECTVE of an AUDIT is (as per ISA 200)

a) Enable AUDITOR to EXPRESS OPINION on whether FIN STATS . , is Fairly Presented.in all MATERIAL aspects, in accordance with AN IDENTIFIED REPORTING FRAMEWORK – International Reporting Framework and/or statuory requirements,

b) ISA 200 warns objective is NOT to DISCOVER FRAUD or ENSURE COMPLIANCE WITH THE LAW. (this is mngmnts responsibility.) Auditor ONLY : " REASONABLE EXPECTATION of DETECTING SUCH IF they AFFECT FAIR PRESENTATION ie: IF Fin. Info. CONTAINS MATERIA L MISSTATEMENT.

A MODEL OF INDEPENDANT AUDIT OF FIN STATS ARISING OUT OF COMPANIES ACT (STATUTORY AUDIT)1) Statutory laws arose from need to protect investors + economic system as a whole. 2) Most common audit engagement is the audit of private & public companies Fin.Stats. by registered auditors in

public practice. THE ROLES OF THE VARIOUS PARTIES

1) SHAREHOLDERS

a) Provide finance for businessb) Appoint directorsc) Appoint auditors (to opinion assertions of directors to shareholders fair)d) Receive Annual Fin. Stats.

2) DIRECTORS

a) Running company19

20 20 | P a g e Auditing Notes AUDI 101b) Reporting results OF THEIR STEWARDSHIP to shareholders.

3) AUDITOR

a) Independant opinion Fin info. fairly presents fin. Pos + fin Res.b) Report to shareholdersl

ROLE OF COMPANIES ACT.1) States all companies must be audited2) Duty on shareholders to appoint auditor.3) Duty on shareholders appoint directors.4) Regulates who may be appointed as director + auditor and how/when may resign or be dismissed.5) Form & Content of report from directors to shareholders – Annual Fin. Ststs. + 4th schedule.6) Legal backing for Financial Reporting Standards.7) Requires Audit Commitees to enhance audit function be appointed.8) Right of auditor to access company records.9) Requirements fulfilled by auditor (eg accounting records in agreement with fin stat) before can report to

shareholders.10) Duty on auditor to report to shareholders.11) CLEARLY stipulates : auditors report must contain OPINION –if Fin Stat. = fairly presents FIN Pos + Res.

ASSERTIONS:1) The REPORT to the SHAREHOLDERS from the DIRECTORS take the FORM of Fin.STATS. in form of GAAP(ifrs+isa)

+CONTROLLED by COMPANIES ACT (fin stats + 4th schedule)2) EMBODIED in Fin.Stats. are the ASSERTIONS OF MANAGEMENT – are RERESENTATIONS on

assets,liab.,transactions,events.3) AUDITORS RESPONSIBILITY: 1- obtain SUFFICIENT APPROPRIATE EVIDENCE that that assertions embodied in fin

stats are fairly presented. 2-REPORT to Shareholders.

SUMMARY: Scan in pg1/16 bottom

20

SHAREHOLDERS

DIRECTORS

AUDITORS

21 21 | P a g e Auditing Notes AUDI 101

CHAPTER 2 : GENERAL PRINCIPLES OF AUDITING.(CH 3 IN CHAPTER 2 : GENERAL PRINCIPLES OF AUDITING.(CH 3 IN BOOK)BOOK)

INTERNAL CONTROL INTRODUCTION1) ISA 315- before an auditor can audit a thorough understanding of a clients internal control systems should be

obtained –(do a walk through)2) Internal Contols: + acc.sys. produce balances & totals –good acc.sys. = generates good ( 1-valid,2-accurate,3-

complete,4-timeous = “FVACT”) info.3) Auditor more interested in acc. info. less in other info : eg sales analysis,budgeting info,marketing info etc.

DEFINITION OF INTERNAL CONTROL.DEFINITION (PER SAICA BOOKLET :'GUIDANCE FOR DIRECTORS:REPORTING ON INTERNAL CONTROLS')Internal Control is a PROCESS effected by the 1- COMPANIES BOARD OF DIRECTORS ,2-MANAGEMENT AND 3-OTHER PERSONNEL.Designed to provide REASONABLE ASSURANCE regarding the achievement of OBJECTIVES in the following 3 categories:

i) 1-ECONOMY 2- EFFICIENCY 3-EFFECTIVENESS.ii) INTERNAL FINANCIAL CONTROL iii) COMPLIANCE with applicable LAWS & REGULATIONS.

FOUR ASPECTS OF INTERNAL CONTROL FROM ABOVE DEFINITION.1. Internal control is a PROCESS , a means to an end, not an end in itself.2. AFFECTED BY PEOPLE ,not just procedures/policies.3. Only REASONABLE ,NOT ABSOLUTE ASSURANCE.4. To achieve objectives in 3 CATEGORIES , which are INTERLINKED. (3 in definit.)

(ISA 315). 5 COMPONENTS OF INTERNAL CONTROL (IN CH 7)1. CONTROL ENVIRONMENT (all) : +attitudes,awareness,actions, of those responsible for

governance,mngmnt2. ENTITIES RISK ASSESMENT PROCESS: 3. INFORMATION SYSTEM : transactions 4. CONTROL ACTIVITIES : actual sys.5. MONITORING OF CONTROLS : eg internal audit dept.

INTERNAL CONTROL OBJECTIVES.1) Policies & Procedures (internal controls) to ensure orderly & efficient conduct of business.incl. controls to :

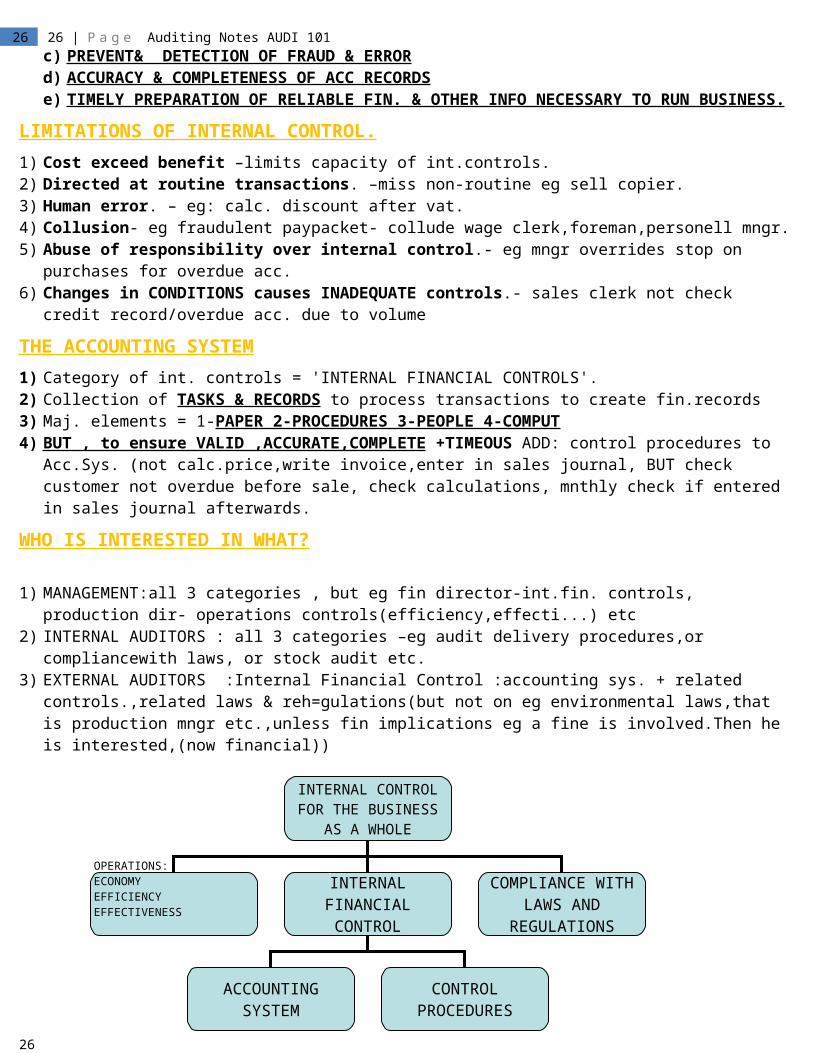

a) ADHERE TO MNGMNT POLICIES (INCL. APPLICABLE LAWS & REGULATIONS!) b) SAFEGUARD ASSETS c) PREVENT& DETECTION OF FRAUD & ERROR d) ACCURACY & COMPLETENESS OF ACC RECORDS e) TIMELY PREPARATION OF RELIABLE FIN. & OTHER INFO NECESSARY TO RUN BUSINESS.

LIMITATIONS OF INTERNAL CONTROL.1) Cost exceed benefit –limits capacity of int.controls.2) Directed at routine transactions. –miss non-routine eg sell copier.3) Human error. – eg: calc. discount after vat.

21

22 22 | P a g e Auditing Notes AUDI 1014) Collusion- eg fraudulent paypacket- collude wage clerk,foreman,personell mngr.5) Abuse of responsibility over internal control.- eg mngr overrides stop on purchases for overdue acc.6) Changes in CONDITIONS causes INADEQUATE controls.- sales clerk not check credit record/overdue acc. due to

volume

THE ACCOUNTING SYSTEM1) Category of int. controls = 'INTERNAL FINANCIAL CONTROLS'.2) Collection of TASKS & RECORDS to process transactions to create fin.records 3) Maj. elements = 1-PAPER 2-PROCEDURES 3-PEOPLE 4-COMPUT4) BUT , to ensure VALID ,ACCURATE,COMPLETE +TIMEOUS ADD: control procedures to Acc.Sys. (not calc.price,write

invoice,enter in sales journal, BUT check customer not overdue before sale, check calculations, mnthly check if entered in sales journal afterwards.

WHO IS INTERESTED IN WHAT?

1) MANAGEMENT:all 3 categories , but eg fin director-int.fin. controls, production dir- operations controls(efficiency,effecti...) etc

2) INTERNAL AUDITORS : all 3 categories –eg audit delivery procedures,or compliancewith laws, or stock audit etc.3) EXTERNAL AUDITORS :Internal Financial Control :accounting sys. + related controls.,related laws &

reh=gulations(but not on eg environmental laws,that is production mngr etc.,unless fin implications eg a fine is involved.Then he is interested,(now financial))

THE CHARACTERISTICS OF GOOD INTERNAL CONTROL.

INTERNAL CONTROL is only ever: POLICIES & PROCEDURES .

1) Control Environment (strong) : Attitude and awareness of managers & directors to internal controls and their importance to entity.1. Eg : fin accountant does not bother to check recon of creditors ledger to creditors statements made by creditors

clerk PROPERLY ,only HALF,before paying ,.So soon clerk wont bother to actually reconcile properly.2. ISA 315 : says good control environment characterised by:

23 23 | P a g e Auditing Notes AUDI 101iii) Mngmnt Acts/displays : Integrity & Ethical.iv) Mngmnt Acts/displays : Leadership , Sound judgement , (+Ethical behaviour).v) Organisation Structure promotes this : Authority + Responsibility + Reporting : relationships vi) Organisation Structure promotes this : Planning + Execution control + Review vii) Good HR policies : Training & development , Compensation fair & benefits ,get competent ethical staff.

2) Competent ,Trustworthy Personnel. – esp. at internal controls.3) Segregation of Duties. – collusion is necessary.

1. Eg: E.F.T. control, or storeman signs a gate pass delivery note+ falsify stock record+takes goods2. A TRANSACTION PASSES THROUGH 4 STAGES:

i) Authorising (1) Purchase order authorised by chief buyer(2) Checking & approve supporting docs. For a payment to a creditor.

ii) Executing (1) Order placed with supplier by the order clerk(2) Preparing the cheque realisation and cheque (SEPARATE CUSTODY OF CHEQUE)

iii) Custody of Asset (1) Goods rec. by receiving clerk & placed in store.(2) Signing cheque (NB person who has signing power auto has SEPARATE HAS CUSTODY OF CASH)

iv) Recording (1) Transactions entered into acc. records by acc. clerk.(2) Recording payment in records & posting to ledgers.

3. MOST IMPORTANT DIVISION : 3 & 4 are the most 'incompatible'. 'Defalcation' is easiest if both are same ou. Esp: SMALL BUSINESSES.i) NEXT BEST is 2 & 3 & 4 . :For the same reasons.ii) 1 & 2 can be combined most easily : because if the others are segregated ,defalcation is likely to be

identified. iii) GOOD SEGREGATION : starts with divide the companies CYCLES into FUNCTIONS , then further segregate

duties within FUNCTIONS. ( each Function = Segregated duty./a New person and each cycle = authorisation/executing/custody/recording)

4) Isolation of responsibility – 1. FULLY AWARE OF THEIR RESPONSIBILITIES : Internal controlsER must be .2. ACCOUNTABLE FOR THEIR PERFORMANCE ; Internal controlsER must be .3. Acknowledge in writing that they have peformed control procedure :IDENTIFY & ISOLATE employee responsible.

i) SIGNITURE fulfils 2 functions :(or fingerprint login)(1) ISOLATE+IDENTIFY which person was responsible for delivery.(2) ACKNOWLEDGEMENT of delivery.from supplier . to purchaser.

5) Custody / Access Controls. 1. ONLY to PROTECT COMPANIES ASSETS.( policies & procedures)

i) PHYSICAL & NON PHYSICAL ASSETS.Cash in Bank(only entry in book to show), Investments (only papers to show), Debtors (only an entry in book to show).

ii) Custody/access controls designed to;(1) Prevent damage to

(a) NON-PHYSICAL : Debtors get legal dont pay status from too long time wait to pay,with no court action.

(b) Physical : (2) Prevent deterioration of

(a) NON- PHYSICAL ASSETS eg: debtors get behind in payments.(b) Physical Assets.

(3) Unauthorised USE , THEFT , LOSS. Eg security

23

24 24 | P a g e Auditing Notes AUDI 101(a) NON-PHYSICAL : limit no. of personell with powers to cash payment / or sell investment. Or prevent

DEBTORS LEDGER from being altered.(b) Physical :

6) Source Document Design: ('PAPER') 1. Properly designed docs. can assist in achieving good internal control. by have following features -Esp. Fin

Control. i) Pre-printed – format leaves MINIMUM AMOUNT OF INFO. to be filled in.ii) Pre-numbered- facilitates IDENTIFICATION OF MISSING /Added FORMS (used by skelms)–by data entry

clerk end week.iii) Logicaly designed : eg : Prominent 'important info' spaces , + blocks per digit in acc. no. so allways 10 get

put in.iv) Contain Prominent Block each for 1-authorising / 2-approving / 3-preparer etc etc to sign in.v) (a) MULTI-COPIED (vi)CARBONISED SELF COPYING , (vii)DIFFERNT COLOURS EACH SHEET.-sales clerk fills

form for : 1-picking slip to stores 2 +to accounting, all in one go.7) Comparison and Reconcilliation.

1. 1-FREQUENT AND 2-TIMEOUS comparison & recons.2. INDEPENDANT from functions & records kept.

Following 2 make all recons far less effective as a control:3. AGAIN REVIEWED BY SENIOR PERSONEL.4. FOLLOWED UP / investigated and pursued.(+ report where it went or auditors fees go up!).5. Following recons & comparisons ARE IMPORTANT.

i) Stock & fixed assets to records. Eg: stock cycle counts. ii) Bank and investments accounts to Bank statements eg bank recon. iii) Creditors accounts to creditors statements. iv) Subsidiary ledgers to general ledger.

8) Efficient risk identification & monitoring system : ADDED later from a later chapter :: eg audit committees, internal control design committees, risk officer/manager/supervisor/appointee

AUDIT EVIDENCE. Audit evidence is absolutely crucial to audit function to Support opinion. ISA 500R- "The Auditor should obtain SUFFICIENT APPROPRIATE EVIDENCE to be able to draw a reasonable

conclusions on which to base audit opinion." : KEY PHRASE = sufficient appropriate evidence. Evidence usally relates to Assertions on Fin Stats.

SUFFICIENT APPROPRIATE EVIDENCE.Overall measure of whether enough sufficient appropriate evidence is gathered cannot be 100% exactly determined :BUT

1) SUFFICIENT EVIDENCE: 1) SUFFICIEN T means if QUANTIT Y of evidence is enough.2) Evidence is Cumulative : eg debtors test = 1-debtors circularisation +2-test if debtors pay( very good evidence they

exist!)3) To calc. quantity of evidence needed =NO hard and fast way ,only :USE professional Judgement + statistical

methods.This is done as part of the "AUDIT PLAN" stage.APPROPRIATE EVIDENCE.1) APPROPRIATE means if QUALITY of evidence is enough. Further broken down into:

a) RELIABILITY (source & nature)b) RELEVANCE (to assertion being tested)

r

24

25 25 | P a g e Auditing Notes AUDI 1012) RELIABILITY : Hierarchy of Reliability of Evidence:

a) Most Reliable =Developed by auditor : eg inspect stock.b) Reasonably Reliable =Evidence from 3rd party(not client) if 1-Independant 2-Reputable 3-Competent eg

attorneyc) Less Reliable = From 3rd party BUT passed through client. Eg: bank statement.d) Less Reliable = Evidence from clients SYSTEM and where related controls it passed through were Effectivee) Least reliable = Evidence provided by client (lacks independance)f) Written more reliable than oral.(easy denied)g) Original documents More than Photocopies /facsimiles.

Also, REM these are guidelines, eg if competence +integrity of directors&employees are strong &acc.sys and internal controls are strong, evidence from client could be very reliable.Eg sheet to shelf = existance BUT shelf to sheet =completeness.3) RELEVANCE :

a) Evidence MUST be MATCHED to assetion tested : eg; self stock count= 'existence'+some 'valuation' BUT not 'rights' eg could be uncollected but sold .NOR 'completeness' yet eg must first be traced to records to determine if all were included in records.

b) Eg tests of controls as to accuracy will not prove validity or completeness.c) A single procedure could be relevant to more than 1 assertion though.

INFLUENCEING FACTORS IN DETERMINING WHETHER SUFFICIENT APPROPRIATE EVIDENCE HAS BEEN OBTAINED.

Factors which MUST influence auditors decision.:

1) THE ASSESMENT of Inherent Risk and Control Risk at the client. :if higher risk – more evidence from most reliable source needed.

2) THE MATERIALITY Of Item Being Examined : eg if stock is very material – auditor must get more of appropriate evidence.-why –greater likelihood of material misstatement.

3) Experience from Previous audits (at same client). HISTORY 4) Results of audit procedures ALREADY CONDUCTED. – eg if test of debtors was good , then do less other tests.5) RELIABILITY and Source of info.available. if no reliable tests available, then much more of less reliable tests must

do.6) PERSUASIVENESS of the audit evidence : eg: evidence gathered on one section of audit which is Supported by

evidence from another section = more persuasive .If it Contradicts it = less pesuasive.

FINANCIAL STATEMENT ASSERTIONS:

1) The OBJECTIVE of an audit : is for an auditor to EXPRESS an OPINION on whether the FINANCIAL STATEMENTS are FAIRLY PRESENTED.(check other definitions of this before)

2) Embodiment of Assertions : the financial statements are the EMBODIMENT of the ASSERTIONS of the DIRECTORS of the COMPANY ,in the PRESCRIBED FORMAT , on the FINANCIAL RESULTS and PERFORMANCE of OPERATIONS ,which they are managing on behalf of shareholders.

3) ISA 500R : the auditor should use assertions for classes of transactions ,account balances,and presentation and disclosure,in sufficient detail to form a basis for the assesment of risks of material misstatement and the design and performance of further audit procedures.

4) It is the Auditors duty to gather sufficient evidence to support assertion being audited.5) Every assertion should be considered for audit, but those assert. presenting highest risk of MATERIAL

MISSTATEMENT by the AUDITOR in his'"OPINION on ... ", must be concentrated on.

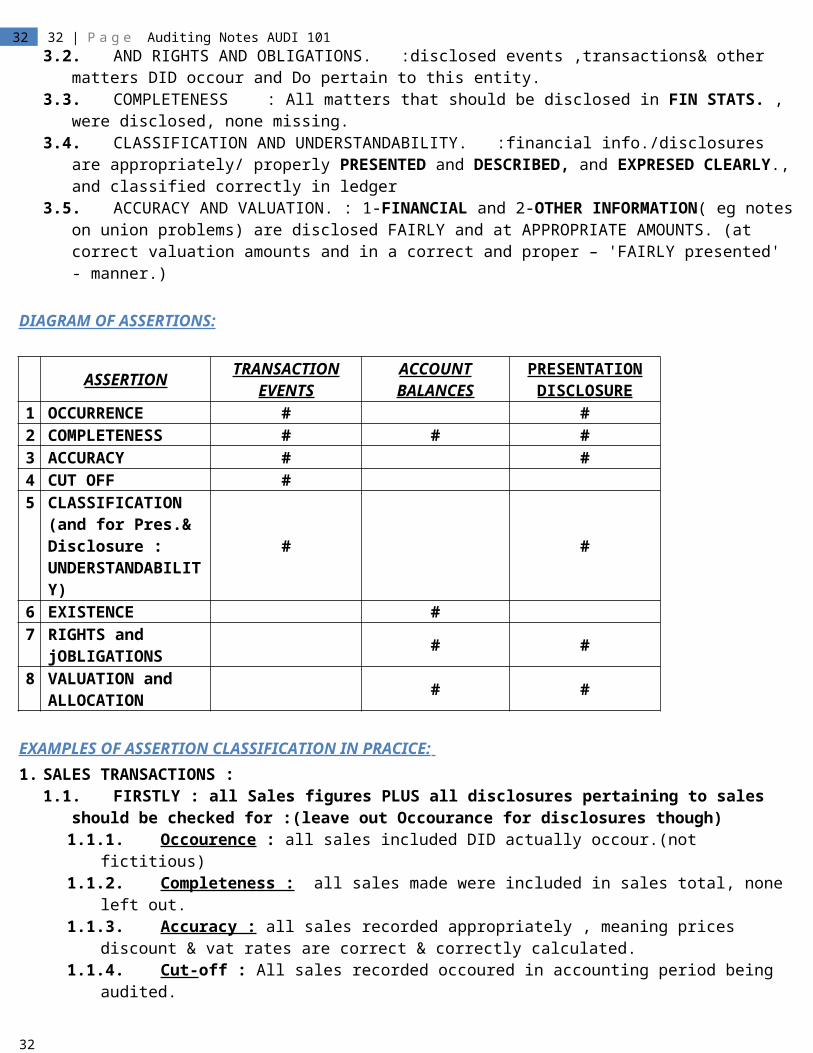

6) CATEGORIES OF ASSERTIONS: ISA 500R Categorises the Assertions as follows.:a) Classes of Transactions and Events (for period) eg:sales, purchases, interest received

25

26 26 | P a g e Auditing Notes AUDI 101b) Account Balances carried forward to next year (at year end) eg:property plant &equipment ,accounts

receivable.c) Presentations and Disclosure : eg:notes to bal.sheet , contingent liabilities

1. Classes of TRANSACTIONS AND EVENTS: Assertions about (during period)1.1. OCCURENCE :recorded trans.& events DID occour and DO PERTAIN to THIS entity.1.2. COMPLETENESS :all that should have been recorded, were recorded ,none missing.1.3. ACCURACY :1-Amounts & 2-Data were recorded appropriately.1.4. CUT-OFF : in right accounting period.1.5. CLASSIFICATION (and UNDERSTANDABILITY) : recorded in correct account names.

2. ACCOUNT BALANCES :Assertions about (end period). 2.1. EXISTENCE : assets, liabilities, equitys DO actually exist.2.2. RIGHTS AND OBLIGATIONS : entity holds rights to assets , liabitities are obligations of this entity , named

shareholders . : do hold the rights to the equity.+2-ALL ENCUMBERENCES on ownership must be . .. . :Disclosed

2.3. COMPLETENESS : all that should have been recorded,were recorded,none missing.2.4. VALUATION AND ALLOCATION. : assets ,liabilities , equity recorded at appropriate valuation amounts and any

resulting : valuation adjustments or allocation adjustments are appropriately recorded .ALSO , :DEPRECIATION and OBSOLECENCE ALSO allocated to correct accounts in ledger

3. PRESENTATION AND DISCLOSURE :Assertions about. 3.1. OCCURENCE 3.2. AND RIGHTS AND OBLIGATIONS. :disclosed events ,transactions& other matters DID occour and Do pertain to

this entity. 3.3. COMPLETENESS : All matters that should be disclosed in FIN STATS. , were disclosed, none missing.3.4. CLASSIFICATION AND UNDERSTANDABILITY. :financial info./disclosures are appropriately/ properly

PRESENTED and DESCRIBED, and EXPRESED CLEARLY., and classified correctly in ledger3.5. ACCURACY AND VALUATION. : 1-FINANCIAL and 2-OTHER INFORMATION( eg notes on union problems) are

disclosed FAIRLY and at APPROPRIATE AMOUNTS. (at correct valuation amounts and in a correct and proper – 'FAIRLY presented' - manner.)

EXAMPLES OF ASSERTION CLASSIFICATION IN PRACICE: 1. SALES TRANSACTIONS :

26

27 27 | P a g e Auditing Notes AUDI 1011.1. FIRSTLY : all Sales figures PLUS all disclosures pertaining to sales should be checked for :(leave out

Occourance for disclosures though)1.1.1. Occourence : all sales included DID actually occour.(not fictitious)1.1.2. Completeness : all sales made were included in sales total, none left out.1.1.3. Accuracy : all sales recorded appropriately , meaning prices discount & vat rates are correct & correctly

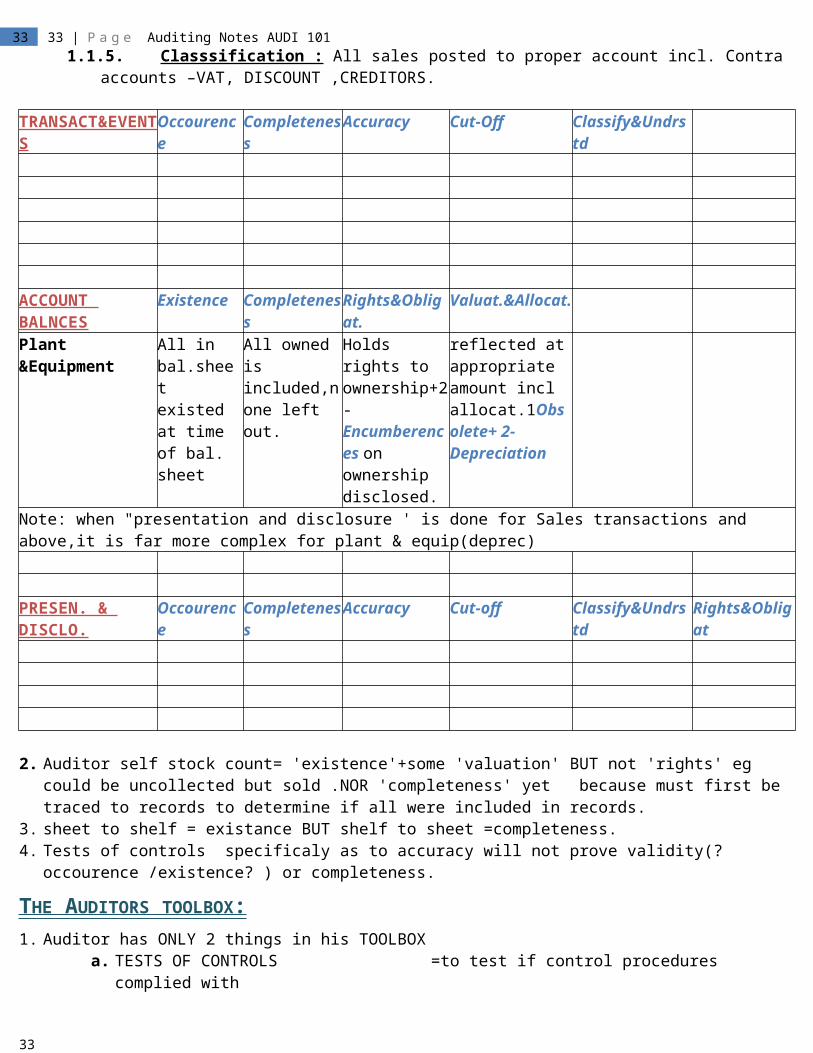

calculated. 1.1.4. Cut- off : All sales recorded occoured in accounting period being audited.1.1.5. Classsification : All sales posted to proper account incl. Contra accounts –VAT, DISCOUNT ,CREDITORS.

2. Auditor self stock count= 'existence'+some 'valuation' BUT not 'rights' eg could be uncollected but sold .NOR

'completeness' yet because must first be traced to records to determine if all were included in records.3. sheet to shelf = existance BUT shelf to sheet =completeness.4. Tests of controls specificaly as to accuracy will not prove validity(?occourence /existence? ) or completeness.

THE AUDITORS TOOLBOX: 1. Auditor has ONLY 2 things in his TOOLBOX

a. TESTS OF CONTROLS =to test if control procedures complied withb. SUBSTANTIVE PROCEDURES. =to test if verify / substantiate 1-TRANSACTIONS 2-BALANCES

TESTS OF CONTROLS1) CATEGORIES OF TESTS OF CONTROLS:

i) REPERFORMANCE : repeating 1-Wholly 2- In Part control procedures eg: reperform bank recon.ii) INSPECTION : verify on docs. if contrl procedures did happen : eg: verify if transaction authorisation

signiture is there. iii) ENQUIRY; ask person CONCERNED with control procedure as to effective operation of.,NOT just

accept mngmnts word. Eg : find out who performs each procedure and what they do.

27

28 28 | P a g e Auditing Notes AUDI 101iv) OBSERVATION: watch process/procedure being performed eg:watch what a receiving clerk does when

supplier delivers goods.2) Tests of Control are performed to obtain evidence of whether

i) Controls suitably Designed to (1) PREVENT (2) DETECT (3) CORRECT material misstatements

ii) Operated effectively THROUGHOUT PERIOD AUDITED.

3) Good results reduce control risk and hence audit risk , then less time need spent on substantive tests.4) LIMITATIONS OF : tests of controls:

a) Good when checked but not in the rest of the Fin. Year. b) Inherent risk? ch7eg 1-only test some 2- subjectivity-auditor own method 3-

5) LIMITATIONS OF : internal controls: i) Cost exceed benefit –limits capacity of int.controls.ii) Directed at routine transactions. –miss non-routine eg sell copier.iii) Human error. – eg: calc. discount after vat.iv) Collusion- eg fraudulent paypacket- collude wage clerk,foreman,personell mngr.v) Abuse of responsibility over internal control.- eg mngr overrides stop on purchases for overdue acc.vi) Changes in CONDITIONS causes INADEQUATE controls.- sales clerk not check credit record/overdue acc.

due to volume6) Example:

a) If control procedures in credit purchase procedure are sound- related balances/transactions rec. will be soundi) Ie: control when purchase acc and creditors acc debited /reconciled authorised, also controls at creditor

payment and creditor acc. DR etc.

SUBSTANTIVE PROCEDURES.1) Tests controls cannot provide 100% assure so sustant.tests need be done.2) SUBSTANTIVE TESTS BROADLY DISTIGUISHED INTO;

a) Tests Of Detail. b) Analytical Procedures.( very powerful tool)

3) CATEGORIES OF SUBSTANTIVE PROCEDURES: i) REPERFORMANCE : repeating 1-Wholly 2- In Part same procedures performed by client eg:debtors age

analysis.ii) INSPECTION : inspect 1-docs+records, or 2-tangible assets eg: inspect fixed asset to verify existence or

inspect . "Confirmation Of Balance Certificate" from long term loan creditor.iii) CONFIRMATION + ENQUIRY; :seek info. from knowledgeable person inside or outside entity

(1) Enquiry : 1-oral or 2-formal written : to inside or outside entity to get 1-Corroborative evidence or 2-Plain . .. Information did not know.

(2) Confirmation : procedure of obtain response to an enquiry to corroborate info. in the acc. records. iv) RECALCULATION : check arithmatic on source docs & records. Eg: check depreciation calc.v) ANALYTICAL PROCEDURES : analysis of ratios + trends , then investigate inconsistent deviations .(statistics)

4) Substantive procedures are performed on a) Balances Assertions= ; Existence, Completeness,Rights&Obligations,Valuation&Allocation.,b) Transactions Assertions= ; Occourence,Completeness,Cut-off,Classification&Understandability,Accuracy

5) Financial stat. consist of onlya) Collection of balances - bal sheetb) Summary of totals – inc.stat

6) VOUCHING AND VERIFYING: a) Vouching: (To Vouch) TRANSACTIONS auditing.

28

29 29 | P a g e Auditing Notes AUDI 101b) Verifying : BALANCES auditing.c) Example:

i) VOUCH – a sales transaction = inspect docs + enquire discounts + recalculate ii) VERIFY – a debtors balance = confirmation in writing from debtors + enquiries as to calc. of prov.bad debts.

+reperform aging analysis of debtors.7) DUAL PURPOSE TESTS : some tests can be a test of control and substantive test at same time eg: bank recon.

Reperform = test of control(recon is a control) and substantive test (bank balance).

AUDIT SAMPLING DEFINITIONS:1) From ISA 530 : 'audit sampling and other means of testing': gives definitions2) AUDIT SAMPLING

a) application of PROCEDURES to LESS THAN 100% OF ITEMS in balance or class of transactions ,to EVALUATE AUDIT EVIDENCE on the some characteristic of sample to form CONCLUSION ON POPULATION

3) ERROR:a) 1-Test of Controls =Control deviations 2-Substantive testing= Misstatements OR

4) TOTAL ERROR :a) 1-Rate of Deviations 2-Total Misstatement . AND

5) ANOMOLOUS ERROR:a) ERROR FROM ISOLATED EVENT,not representative of population.

6) POPULATION :a) Total set of data from which samples are selected.eg all items in an account balance or class of transactions.

7) SAMPLING RISK:a) RISK THAT the auditors conclusion is not true for total population because sample is not representative of the

total population .(Sample could be selected by stat or non-stat approach-any).There are 2 types of Auditing Risk:i) Risk 1-tests of control =auditor judges them to be more effective than they actually are. 2- Tests of Detail-

error exists where it does not : this type 1-AFFECTS AUDIT EFFICIENCY :causes more work for auditor to establish that initial conclusions were incorredt.

ii) Risk 2-tests of control = auditor judges them to be less effective than they actually are. 2- Tests of Detail- error does NOT exist where it does. : This type2-AFFECTS AUDIT EFFECTIVENESS : more likely to lead to an inappropriate audit opinion than assesing risk to be higher than it is..

8) NON-SAMPLING RISK : risk of a) apply sampling plan incorrectly, or b) used inappropriate procedure c) misunderstood results of sampling exercise.

9) SAMPLING UNIT. a) :INDIVIDUAL ITEMS making up a population eg: cheques listed on deposit slips/credit entries on bank

statements.10) STATISTICAL SAMPLING :

a) any approach that has following characteristics or it is non-statistical.i) Random selection of a sample.ii) Use of probability theory -to evaluate sample results (INCL.MEASUREMENT OF SAMPLING RISK.)

11) STRATIFICATION :a) DIVIDING a population into sub-populations each with similar characteristics eg : debtors balance >1000.

INTRO.1. Only some items all are tested eg:loans to directors,but mostly sampling is used due to Resource & Time efficients.2. Sample results must be EXTRAPOLATED over population(3 mistakes * xxx= 1000 mistakes total) statistical sampling

will result in more defensable results than non-statistical sampling.29

30 30 | P a g e Auditing Notes AUDI 1013. Other ebvidence is used together with sampling results like a jigsaw puzzle eg: Analytical procedures on same

population.4. ISA 500 –says auditor must selecyt appropriate means of selecting samples when design audit procedures.

STEPS IN THE SAMPLING EXERCISE.1) Determine objectives of procedure2) Determine procedure3) Confirm population is appropriate & complete4) Define units5) Get sample size6) Select sample7) Perform audit procedure8) Analyse nature & cause of errors9) Project results over population10) Evaluate11)

30

31 31 | P a g e Auditing Notes AUDI 101

CHAPTER 6 : AN OVERVIEW OF THE AUDIT PROCESS.CHAPTER 6 : AN OVERVIEW OF THE AUDIT PROCESS.KNOW/LEARN WHOLE CHAPTER PER LECTURER :

STAGES OF THE AUDIT PROCESS: (KNOW WHOLE CHAPTER PER LECTURER ) STAGE 1 : PRELIMINARY ENGAGEMENT ACTIVITIES:

i) ESTABLISH/CONTINUE : Performing Procedures to decide whether to Establish/Continue a Relationship.ii) CAPACITY :Establish if auditor has the Capacity / Resources / if Client can be appropriately serviced or not.iii) ETHICAL :Evaluate if Firm can comply with ethical requirements. Eg independanceiv) TERMS OF ENGAGEMENT :Formulate the terms of engagement.

STAGE 2 : PLANNING: 1) AUDIT STRATEGY :Establish an overall audit strategy.2) AUDIT PLAN :develop one.to be in a position to develop one audit team must first do the next 3 things:3) Obtain Understanding : of Entity and Environment incl. Internal Control.4) Risk : of Material Mistatement :Assess risk of in the financial statements.5) Materiality : Determine guidelines.

STAGE 3 : PUTTING AUDIT -PLAN AND STRATEGY - INTO ACTION.1) RESPOND RISK FIN.STAT. LEVEL ('overall response') :Respond to assesed risk at financial statement level,

eg: assign more experienced staff.2) RESPOND RISK ASSERTION. LEVEL :By carrying out Tests Of Controls +Substantive Tests (to gather

sufficient evidence to reduce risk to an acceptable level.)3) RESPOND TO SIGNIFICANT RISKS : By carrying out Tests Of Controls +Substantive Tests + Investigation eg

laws regulations etc.

STAGE 4 : EVALUATE & CONCLUDE.1) EVALUATE AND CONCLUDE :Evaluate and Conclude on Audit Evidence gathered.2) AUDIT REPORT :Formulate Audit Report.

HOW THE STAGES ARE LINKED: The preliminary stage is not really linked to the other stages , except for the fact that the info gathered here will be used in the rest of the audit in eg: evaluating the client The rest of the stages are closely linked

1- The planning stage is linked to Putting into action stage because the Nature/Timing /Extent of tests done in executing stage are determined in planning stage

2- The executing linked to reporting because : all info gathered here is used in reporting + evaluate stage.ALSO :(Note: The stages are NOT standalone units and the activities within each stage do not fit neatly into the order presented.Planning :is not standalone because \1-as they do current audit, next years audit is being planned.2- if problems develop in audit then new planning must again be done to implement additional procedures / audit strategy if needed. –so if you are in stage 3 , you must go and do some stage 2 things again, but you are already in stage 3.)

31