AUSTRALIAN AUTOMOBILE DEALERS ASSOCIATION Motor Trades Association House, 39 Brisbane Avenue, Barton ACT 2600 PO Box 6278, Kingston, ACT 2604 Telephone: +61 2 6273 8222 Facsimile: +61 2 6273 9399 CCAAC Automotive Repair Industry Review C/- Ms Danielle Staltari Manager Consumer Policy Framework Unit Infrastructure, Competition and Consumer Division Treasury Langton Crescent PARKES ACT 2600 Dear Ms Staltari I am writing to you on behalf of the Australian Automobile Dealers Association (AADA). AADA represents the interests of approximately 1500 dealers in Australia, who operate something in the order of 2600 new vehicle outlets. In many instances the local motor vehicle dealership is the mainstay of a local area or community and a significant member of the local business community. I provide the attached submission to the Discussion Paper released by the Commonwealth Consumer Affairs Advisory Committee (CCAAC) titled Sharing of Repair Information in the Automotive Industry. Clearly, the subject of that Paper is one of considerable interest to motor vehicle dealers and it is for that reason that the Association is well placed to provide comment on that Paper to the Committee and to stand at the ready to provide the Committee with any other assistance it may require. Please do not hesitate to contact me in the event that you have any queries, or require any clarification. I can be contacted on 02 6273 8222 Yours sincerely COLIN DUCKWORTH Principal Officer and Director Policy Australian Automobile Dealers Association 22 September 2011

Transcript

AUSTRALIAN AUTOMOBILE DEALERS ASSOCIATION Motor Trades Association House, 39 Brisbane Avenue, Barton ACT 2600

PO Box 6278, Kingston, ACT 2604

Telephone: +61 2 6273 8222

Facsimile: +61 2 6273 9399

CCAAC Automotive Repair Industry Review

C/- Ms Danielle Staltari

Manager

Consumer Policy Framework Unit

Infrastructure, Competition and Consumer Division

Treasury

Langton Crescent

PARKES ACT 2600

Dear Ms Staltari

I am writing to you on behalf of the Australian Automobile Dealers Association (AADA). AADA

represents the interests of approximately 1500 dealers in Australia, who operate something in the

order of 2600 new vehicle outlets. In many instances the local motor vehicle dealership is the

mainstay of a local area or community and a significant member of the local business community.

I provide the attached submission to the Discussion Paper released by the Commonwealth

Consumer Affairs Advisory Committee (CCAAC) titled Sharing of Repair Information in the

Automotive Industry. Clearly, the subject of that Paper is one of considerable interest to motor

vehicle dealers and it is for that reason that the Association is well placed to provide comment on

that Paper to the Committee and to stand at the ready to provide the Committee with any other

assistance it may require.

Please do not hesitate to contact me in the event that you have any queries, or require any

Submission to the Commonwealth Consumer Affairs Advisory Committee (CCAAC)

Discussion Paper - ‘Sharing of Repair

Information in the Automotive Industry’

1. KEY POINTS

� The Australian Automobile Dealer Association Pty Ltd (AADA) does not believe there is sufficient evidence of consumer detriment through a lack of sharing of repair information, and therefore there are no drivers for government intervention.

� The provision of information is not a motor vehicle dealer’s responsibility. The decision on what information is made available to any third party outside the dealership network and when and for what price information is supplied is the domain of motor vehicle manufacturers and / or their suppliers.

� Australian motor vehicle dealers invest millions of dollars to secure tenure for the right to sell, service and maintain a vehicle marque, or marques, within a limited franchise agreement term.

� Despite this heavy investment, the majority of dealerships achieve only a 1.25% -1.5%

profit before tax on turnover.

� The long term viability of a dealership, contrary to popular belief, is not dependent exclusively on the sale of new motor vehicles. The parts and service operations of a dealership are core to the ongoing viability of that dealership. It is these operations that can alone sustain a dealership through periods of challenging market conditions.

� Manufacturers / suppliers provide strict guidelines and procedures for the equipping,

tooling and operations of workshops; the training and development of technicians, and; the methodologies and responsibilities for accessing information at cost to the dealer. The options available to manufacturers / suppliers for any breaches of these requirements can be cause for the termination of a dealer’s franchise agreement.

� Any free, unilateral transfer of information, without the accompanying skills development, training and workshop tooling and equipping, provides a competitive advantage to independent repairers and distorts the market, which currently accommodates all players.

� Australian motor vehicle dealers, not independent repairers, are the first conduit between manufacturers / suppliers and consumers. Only dealers bear the risk and cost of ensuring workshops initially have the necessary tools, equipment, trained personnel and knowledge, to deal with the raft of technological advances occurring in models as soon as they are released.

� Suggestions that dealers are preventing the share of information on increasingly complex and sophisticated motor vehicles to gain further market share, or to stifle competition in the repair sector, is a gross distortion of the facts and not supported by any evidence of market failure. Such suggestions show contempt at worst, or little understanding at best, of the nuances of the dealership business model, the unique Australian motor vehicle market, and the motor vehicle repair sector more generally.

� There is no capacity in the Australian Dealer network to cater for the entire Australian 16 million plus motor vehicle fleet and, in the view of AADA, nor will there be for the foreseeable future.

� AADA’s members generally have a healthy relationship with independent third party

repairers. AADA and its members recognise the need for the independent repair sector and believe the consumer is well represented with choice.

� In many cases, AADA’s members sub-contract specific repair and maintenance tasks to independent repairers who specialise either in a specific component or skill area of motor vehicle repair and maintenance. Such examples include differentials and transmissions, electrical, steering, and engine reconditioning.

� If consumer detriment exists at all, then it comes from the potential exposure and increased risk associated with mechanical repair work being undertaken by ill-equipped, poorly trained and/or ill-informed technicians.

� If government were to ignore AADA’s views and intervene and establish legislative /

regulatory frameworks to enforce the sharing of information, AADA suggests that appropriate regulatory arrangements would also need to occur to enforce that when information was obtained, correct workshop equipping and the training of personnel is also mandated. It is incomprehensible that all information might be made available, but one sector is then not required to equip and train to use that information while dealers are.

� AADA does not support models or legislative ‘fixes’ from other overseas jurisdictions

as a panacea to non existent problems in the Australian market.

3. Background The Typical Australian Motor Dealership Motor vehicle dealerships are typically family-owned, franchised, small businesses and have a relationship with their suppliers that is unique when compared to more generic retail operations. Indeed, the whole business model of motor vehicle dealerships is unique. Motor vehicle dealership businesses are high-turnover operations of almost impossibly small margins. When the level of investment required is compared to the return, the vast majority of dealerships profit before tax is in the order of only 1.25%-1.5% on turnover. Even for the most progressive, ‘best practice’, dealerships the order of profit before tax is still marginal. Deloitte Motor Vehicle Services consultancy data, which seeks to establish ‘benchmarks’ for the industry, reveals the following typical dealership characteristics1.

� A dealership will only break even on 25 days out of every 30;

� The average dealership will have 40 – 55 days vehicle stock;

� The average dealership turns over its stock 7 to 9 times a year;

� Every dollar of salary paid requires $17 of sales;

� New vehicle sales represent 37% of dealership orientation for a gross profit

contribution in the order of 7 to 9%;

� Used vehicle sales represent 17% of dealership orientation for a gross profit

contribution in the range of 13 to 15%;

� Parts sales represent 15% of dealership orientation for a gross profit contribution

around 24 to 28%;

� Service operations represent 31% of dealership orientation with a gross profit

contribution of in the region of 66 to 70% (mainly labour cost related).

It is important for the Committee to note that these benchmarks represent the top 30% of all dealership operations in Australia. The majority of dealerships aspire to these to these benchmarks and there is significant variability from dealer to dealer. For example some dealers may carry up to 90 days of stock, while others carry less than the average 40-55 days. It is clear that service and parts operations – the ‘back of house’ aspect of a motor vehicle dealership – are vital to viability. As much as 46 per cent of dealership orientation is ‘back of

house’ and might contribute as much as 90 per cent of the gross profit. With overall net profit in the region of 1,25% to 1.5%, the significance of a dealership maintaining a viable parts and service department is clear. The Australian Motor Dealer Business Model / Dealer franchise agreements It was mentioned earlier that dealerships are invariably franchised businesses. This means an Australian Consumer Law compliant franchise agreement will exist between a dealer and a supplier. Dealership agreements might typically run to somewhere between 20 to 40 pages in length, but those agreements will also invariably refer extensively and exhaustively to a supplier’s ‘Policy and Procedures Manual’. Those manuals can run to as many as 400 pages and are, to some significant degree, a mechanism of control that exists between a dealer and their supplier. In that manual will be the boundaries and ‘rules’ by which matters such as the sharing of technical information are to be handled at the dealership level. The investment required to operate and establish a dealership is considerable. AADA’s National Secretariat is aware that some of its metropolitan dealer members represent a capital investment of over $10 million each. That capital investment includes land, buildings, new and used vehicle stock, workshop tools and equipment, spare parts and other fixtures. New vehicle stock will invariably be on bailment or, what is known in the industry as, ‘floor plan’ finance. This means that new vehicles in stock are in fact ‘owned’ by the dealership’s floor plan financier, which then ‘bails’ the vehicles to the dealer for sale. The cost to the dealer each month for this arrangement is the commercial rate of interest charged on the value of the stock on hand. This cost of the monthly ‘floorplan’ finance to a dealer is a significant component of a dealerships’ overheads. For example an average size dealership will be carrying around 50 days new vehicle stock at any point in time. It could be expected that this dealership might sell 80 vehicles a month. This means that this dealership will have between 100 and 130 vehicles in stock. Lets say the average cost of a vehicle is $32,000, then this example dealership has on hand, at any given time, some $4.16 million dollars worth of stock on bailment. While the above is an example there are many variables. Some dealerships with multiple brands may in fact have hundreds of vehicles in stock, representing a value of tens of millions of dollars. The Global Financial Crisis has placed further pressure on the commercial rates of interest, significantly increasing the costs of ‘floorplan’ finance to dealers. Despite the considerable investment that a dealership operation represents, there is little in the way of actual security of tenure. The AADA National Secretariat is aware of cases where dealers have been prepared to spend millions of dollars to establish a dealership, but offered only a small tenure over the franchise in return. In one case in particular, a dealer had been prepared to invest $8 million dollars in the construction of a dealership for a particular supplier

and, in return, that supplier offered only a one year agreement with an option of one further year. This exteme example is by no means an isolated or unique case. In the end, however, a five year agreement with the option on another three years was signed. Even in those terms, the dealership with an $8 million investment had 8 years, at a potential maximum, to get a return on that investment. It is perhaps understandable that dealers seek to ensure they receive some return on their not inconsiderable investment and risk. Service ‘leakage’ As mentioned earlier, having a successful parts and service operations is vital to dealership viability. Critical to the sustainability of dealership parts and service operations is maintaining a high level of throughput. A relatively recent survey of dealerships conducted by AADA revealed that while average dealership service departments were operating at around 92 to 95 per cent of capacity, there was also a considerable leakage of throughput as vehicles approached the third or fourth year of age. Benchmark figures for dealership service retention can be seen in Figure 1, below2.

Year after purchase Metro Rural

Handover / follow-up service 100 % 100% First year 90% 93% Second year 78% 85% Third year 65% 76% Fourth year 48% 59% Fifth year 40% 52%

Figure 1: Benchmark Dealership Service Retention (Average, top 30 percent of dealers)

AADA makes the observation that, by the fourth year of a vehicles life, more than 50% of the vehicles of that age are being serviced outside the dealer network. AADA is also of the opinion that this correlates with the flow information available for this age of vehicle and any technological enhancements they may have. At all points of a vehicles life, as depicted in Figure 1, it is clear that consumers have a choice and, in many respects, are exercising that choice. This could not be possible if information was not available or was quarantined exclusively to dealers for the duration of the warranty period. Of concern to AADA members is that any further dilution of the market will have significant and long term impacts not only on the viability of dealership operations but the employment and wellbeing of thousands of Australians. The cascade effects of such an outcome would be significant, particularly as dealerships carry the bulk of the burden for the training and skills development of Australia’s automotive technicians.

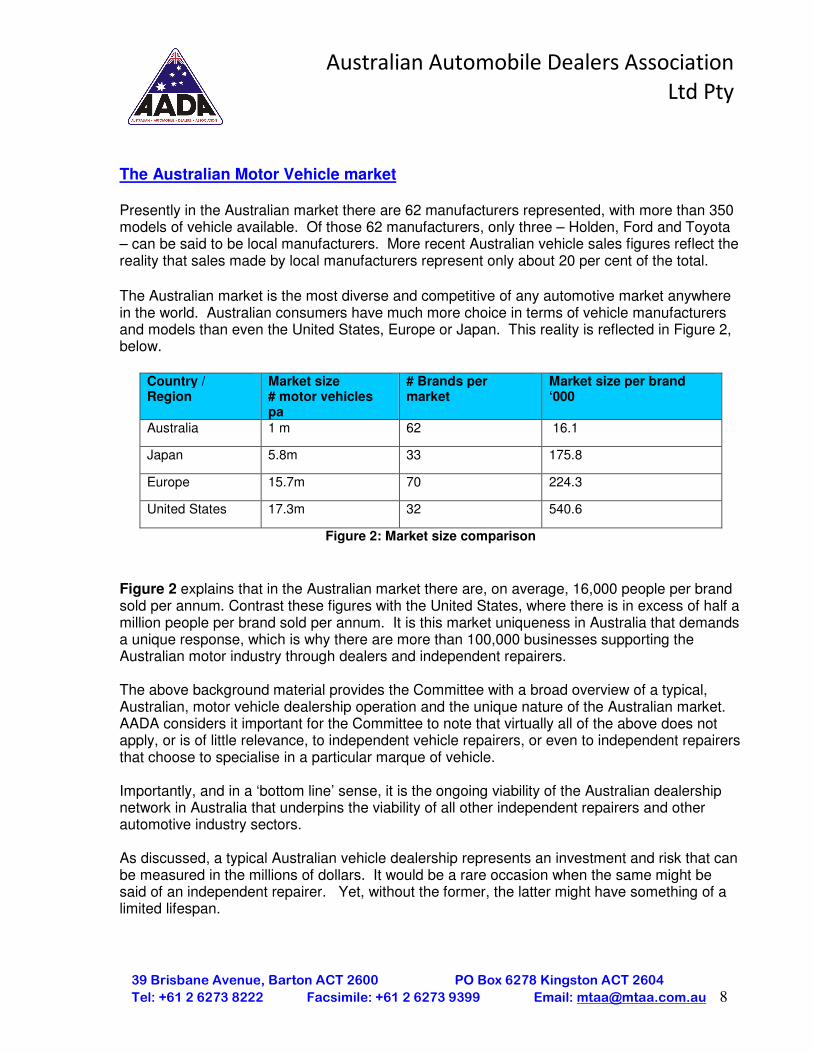

The Australian Motor Vehicle market Presently in the Australian market there are 62 manufacturers represented, with more than 350 models of vehicle available. Of those 62 manufacturers, only three – Holden, Ford and Toyota – can be said to be local manufacturers. More recent Australian vehicle sales figures reflect the reality that sales made by local manufacturers represent only about 20 per cent of the total. The Australian market is the most diverse and competitive of any automotive market anywhere in the world. Australian consumers have much more choice in terms of vehicle manufacturers and models than even the United States, Europe or Japan. This reality is reflected in Figure 2, below.

Country / Region

Market size # motor vehicles pa

# Brands per market

Market size per brand ‘000

Australia 1 m 62 16.1

Japan 5.8m 33 175.8

Europe 15.7m 70 224.3

United States 17.3m 32 540.6

Figure 2: Market size comparison

Figure 2 explains that in the Australian market there are, on average, 16,000 people per brand sold per annum. Contrast these figures with the United States, where there is in excess of half a million people per brand sold per annum. It is this market uniqueness in Australia that demands a unique response, which is why there are more than 100,000 businesses supporting the Australian motor industry through dealers and independent repairers. The above background material provides the Committee with a broad overview of a typical, Australian, motor vehicle dealership operation and the unique nature of the Australian market. AADA considers it important for the Committee to note that virtually all of the above does not apply, or is of little relevance, to independent vehicle repairers, or even to independent repairers that choose to specialise in a particular marque of vehicle. Importantly, and in a ‘bottom line’ sense, it is the ongoing viability of the Australian dealership network in Australia that underpins the viability of all other independent repairers and other automotive industry sectors. As discussed, a typical Australian vehicle dealership represents an investment and risk that can be measured in the millions of dollars. It would be a rare occasion when the same might be said of an independent repairer. Yet, without the former, the latter might have something of a limited lifespan.

It is true and beyond refute that dealerships and dealership networks are the watershed of vehicle service and repair information. This has been the case for as long as motor vehicles and dealerships have existed. But it is not at all true to assert that dealerships retain that knowledge and information in quarantine and exercise extreme prejudice in its dissemination. Rather, dealerships treat information in accordance with their supplier’s instructions, usually outlined in that supplier’s Policy and Procedures Manual. AADA suggests such requirements are quite reasonable given the level of research and development, investment and risk represented in the initial development and application of technology to motor vehicles and in the dealership operations which sell, service and maintain them. Therefore the Committee should note that it is understandable that manufacturers / suppliers and AADA’s members will have a position with respect to the sharing of information that is reflective of this investment and of the need to anticipate a reasonable level of return upon it. Training and Development Without the training provided by suppliers, technicians are more likely to incorrectly diagnose system faults and / or perform repairs to vehicles that only partially remedy faults. In extreme cases, this could see situations where damage to safety items such as anti-lock braking (ABS) sensors and modules occur, leading to supplementary restraint system (SRS) and electronic stability control (ESC) systems being compromised. Technicians in franchised dealerships undergo accreditation exams – often at the dealer’s expense – to ensure that they have the appropriate knowledge and skills to service and maintain the vehicles they see daily. In many respects those technicians become specialists in a particular make, or even model, of vehicle. It might be argued that such is the level of skill required to work on today’s new vehicles. Franchised dealers have a significant and ongoing financial investment in the sale, supply and servicing of their supplier’s product. Often, ‘information’ is a part of the supply process, with it being available essentially as a ‘spare part’ in some form or another. The requirement of a dealership to provide all the necessary links in the purchase and ownership of a vehicle requires each component of the dealership’s operations to provide a positive financial return relative to its various departmental costs and overall franchise operation. Franchised dealers are required to invest in training for technicians, technical and service information and special tools regardless of the volumes of a particular model from their supplier that they service. Clearly the level of fixed overheads will be significantly greater for a franchised dealer when compared to an independent repairer. Consumers quite reasonably anticipate that a dealer for a specific make and model of vehicle will be ‘the expert’ with respect to the servicing and repair of that vehicle. Dealership technicians are certified to a standard so as to earn that level of

consideration by consumers. Whereas, in the majority of jurisdictions in Australia, no formal qualifications or demonstration of competency are at all needed before an individual may perform work on a complex and sophisticated piece of transport technology. Vehicle Technology and the question of Intellectual Property The sophistication and complexity of the modern motor vehicle, and the information that supports it, is the proverbial ‘elephant in the room’ in the sharing of information issue. Independent repairers will claim that central to the consumer’s ability to have freedom of choice is for those repairers to have the ability to access real time, current information, on any motor vehicle. It is AADA’s opinion however, that this simplistic view fails to properly understand the dynamics of a modern motor vehicle, its component parts and, most importantly, the interoperability of its systems. It is that latter point which, in the opinion of AADA, differentiates dealer servicing from that of other repairers. For the Committee to be able to successfully assess the validity of such arguments, AADA considered it may be helpful to provide it with the following overview of the technological capacity of contemporary motor vehicles. What AADA is showcasing to the Committee is that the integrated and interdependent nature of many of the operating systems to be found in modern motor vehicles, and the complexity and sophistication this provides, are all factors that dealership servicing operations have a critical awareness of, are trained in and, are properly equipped for.

System interoperability The motor vehicle has more often than not been the showcase for the practical application of cutting-edge engineering and technology. Advances in electronics, computers and micro-processor technology have arguably brought the most impact in terms of advances in automotive technology. Even if not by direct application, advances in those and similar fields have impacted upon vehicle engineering, design and systems modeling processes significantly. Anti-lock Braking and Supplementary Restraint Systems One of the first production examples of these advances and also arguably the first instance of integrated electronic / hydraulic / mechanical systems was 33 years ago when Mercedes Benz presented it’s (by then) second-generation anti-lock braking system (ABS). This was also about the same time as supplementary restraint systems (SRS, or airbag systems) – which were actually invented in 1952 as mechanical devices – started to appear in vehicles. ABS systems are now commonplace and, in some vehicles, also serve as the basis for the operation for other systems such as acceleration skid control (ASR or traction control), electronic stability control (ESC) and other speed related functions.

For example, the wheel sensor data that ABS systems continually read is used in some vehicles in their navigation computers, or in electronically adaptive transmissions3, or the windscreen wiper speed control, in fact, virtually any function in the vehicle that is controlled on the basis of speed. SRS systems in contemporary vehicles also take data feed information from the ABS system and are themselves now highly integrated systems. Contemporary SRS systems are now much more than just an airbag. They are increasingly combined with sub-systems such as seat belt pre-tensioning devices. More recently there has been the appearance in the market of vehicles fitted with SRS systems that undertake an active assessment of the likelihood of a collision at all times of that vehicle’s operation (even when stationary). Electronic stability control (ESC) systems Electronic stability control (ESC) systems monitor and acquire data on a vast amount of a vehicle’s dynamic characteristics – such as a vehicle’s yaw, pitch and roll rates when cornering, steering angle, vehicle speed, throttle position and so on – and then conduct an analysis of the data received to make an ‘assessment’ as to the capability of the vehicle to safely complete a particular vehicle manoeuvre (such as might be experienced at the time of a driver taking collision avoidance action). The ESC system will, while making these assessments, simultaneously communicate and ‘collude’ with other onboard systems – such as ABS – and may then automatically provide additional control inputs to the vehicle (such as selective individual wheel application of braking force) in an effort to improve the vehicle’s stability, controllability and, hence, its chances of a successful completion of the manoeuvre the driver of the vehicle is attempting. In a more recent developments of the interaction between SRS, ABS and ESC systems, there is now a vehicle available on the Australian market that effectively remains vigilant at all times as to the risk of collision and makes an ongoing assessment as to the likelihood of a collision occurring. In the event of a collision unavoidably occurring – even if evasive actions are being undertaken by the driver – the vehicle, having assessed that a collision is nevertheless inevitable, effectively takes over all control of the vehicle in terms of its braking and suspension settings and commences to adopt control inputs measured to minimise, to the fullest extent possible, the effects of the collision on the occupants. It does this at the same time as activating the SRS system in the manner described above by the measuring of the weight of the occupants and calculating the extent of airbag and seat belt tension device deployment required to counter the inertial effects of the collision upon the vehicle’s occupants.

3 That is, automatic transmissions that ‘learn’ a driver’s patterns of behaviour and then ‘programme’ the operation

and shifting of the transmission for the most efficient operation of the vehicle in accordance with the driver’s needs.

All of these advances in technological application are in response to a diverse set of demands being placed either directly or indirectly on motor vehicle manufacturers. These demands come from governments, regulators and consumers. Vehicles need to be more comfortable, safer (both passively and actively), more fuel efficient or energy efficient and have as small an environmental impact as possible.

This is not to say that other independent repairers are not qualified or trained or equipped to undertake such work, but the complexities of these integrated systems on a single marque alone provides significant enough challenges for the dealership of that marque before trying to contemplate how a business might adapt to 61 other marques and more than 350 models in the Australian market. These are all current technologies representing the pinnacle of applied engineering. They represent considerable investment on behalf of vehicle manufacturers and vehicles with these technologies can be found virtually anywhere in Australia: a visit to any new vehicle dealership will demonstrate that fact.

4. The Dealer / Independent Repairer relationship Overarching those factors has to be the recognition that the dealer will invariably be bound to a particular marque of vehicle. The independent repairer faces no such restriction and can be available to service, or repair, any make and model of vehicle they choose. Nor is the independent repairer committed to the parallel activity of selling a particular product in the form of new vehicles. With a dealer’s investment expressed in the many millions of dollars, it might be quite reasonable, in return, that they enjoy some level of priority access to information.

FRANCHISED DEALER v INDEPENDENT REPAIRER COMPARISON (Mandatory obligations)

Conduct warranty work (usually at reduced labour rate) No Conform to franchisor requirements (premises, stock holding and the like). No

Promote and protect brand No

Meet factory performance indicators No

Factor above into hourly shop rate No

Budget for expenses associated with the above No

Figure 3: Comparison between franchised dealer and independent repairer operations

Australian motor dealers generally have good working relationships with the independent repair sector. While supplier rules dictate the quantum of expectations in regard to information sharing, the practicalities of doing business in a local community will usually see a dealership have

significant relationships if not, in some known cases, even partnerships with independent mechanical repairers. Often these relationships are built on a specialty or area unable to be addressed by the dealership and can involve vehicle components or sub systems. There is also significant anecdotal evidence of dealerships often assisting third party repairers with information, even to the extent of ‘loaning’ tools and equipment, particularly diagnostic apparatus, to simply answering a question over the phone on a particular model of the brand they sell. This is not uniform, nor is it well publicised, but is characteristic of the behaviours within many local business communities. In researching the sharing of information discussion paper, AADA commissioned some survey work in an attempt to quantify the relationship between dealers and independent repairers more formally. The approach was to garnish from members based on geographic location, large volume sales and multi brand groups their information provision habits with independent repairers. Five major groups responded with results depicted in the following table.

The Committee is reminded that it is not the dealers that are primarily accountable for the sharing of information, but the manufacturers / suppliers. Importantly, it needs to also be recognised that the independent repair sector have a myriad of other avenues and third party providers to source information.

Given these observations and the requirements of arrangements between manufacturers / suppliers and dealerships, the level of information sharing from dealerships to independent repairers, as indicated above, is admirable. Some may view these results as low, however the Committee needs to note that this information is being provided to potential competitors in the same market. AADA then went further to ascertain what information dealers were receiving from manufacturers / suppliers. A total of 11 manufacturers were requested to participate, which included a mix of non-luxury and luxury brands and represented a majority of the motor industry. The seven respondents represent 37.1% of the market for new vehicle sales in August 2011.

The provision of information from manufactures / suppliers to dealers is as expected and reflects, in part, requirements outlined in the franchise agreement and procedures manual between the manufacturer / supplier and dealer. Interestingly some manufacturers / suppliers withheld information pertaining to the security or theft prevention systems to be found on their models, even from the dealer. AADA National Secretariat is aware that one of the most often heard complaints from some sectors of the automotive industry is the inability to access information such as radio security or

immobiliser codes. Yet what is often not known is that some dealers, while provided with some information, may have to refer back to the manufacturer / supplier for specifics. With some brands, this information is not available at all. It is important to note that all the information / tools / information technology platforms / access depicted in the table above, is obtained or provided at the dealer cost.

5. Discussion Paper Questions The Discussion Paper poses a number of questions to stakeholders. The preceding section of this submission attempts to address those questions in an overarching sense and in the broad, or by placing those questions in a context that affects the answers to them. With the contextual references relating to dealership operations outlined, this submission turns now to the Discussion Paper’s specific questions. In doing so, this submission will only address those questions that the Association considers are relevant to dealership operations. Q 1.1: What repair information is required for the repair and maintenance of vehicles? From a dealer perspective the answer is entirely dependent on:

• the year, make, model and specification of the vehicle; • the nature and extent of the repair that is being conducted, and / or; • the nature and extent of the service that is being conducted on the vehicle.

There is a significant difference between the information and equipment required and accessible for a two to three year old vehicle being serviced by a specialist (of a specific marque) independent repairer and of that information and equipment required for a brand new vehicle being presented for servicing at the automotive department of a major retail chain. By extension, it can also be said that there is a significant difference between the information and equipment needed and accessible to service, or repair, a 20 year old vehicle (even if that vehicle is from a ‘prestige’ marque and, therefore, arguably of a more ‘advanced’ specification to other vehicles of similar age), than there is needed and accessible to service a brand new vehicle. Q 1.4: What intellectual property considerations are relevant to this issue? This issue has been extensively canvassed in the main body of this submission. It is important to restate that dealerships invest many millions of dollars. It is unreasonable to expect manufacturers to give IP access to independent repairers who are not required to make such financial commitments. Release of IP data by manufacturers to independent repairers would also implicate the manufacturers and place more liability on them should there be any misinterpretation of information resulting in faulty repairs. This may lead to exposure under Australian Consumer Laws.

Q 1.6: Does policy on sharing of repair information have implications for manufacturer’s express warranties on motor vehicles? The consumer expects, as qualified in aforementioned data and statistical analysis, that it is the dealership that will attend to any warranty issue. Service leakage generally starts from the second year of vehicle warranty onwards. That is not to say consumers cannot choose to go to an independent repairer. But, how would provision for the preservation of a manufacturer’s express warranty be maintained in an environment where all repair information was made freely available? How might an independent repairer – without any formal relationship or proximity to the manufacturer – possess the scope to perform work that might ordinarily be thought of as ‘warranty work’? Where might issues such as liability lie in circumstances? It is AADA National Secretariat’s experience from reported cases that invariably the dealer is still held accountable when all else fails. Q 2.3: Is there evidence that manufacturers or importers of motor vehicles cross-subsidise vehicle purchase prices through profits made on authorised repairs or servicing? No. It may come of interest that at the highest level in the Australian market manufacturers / suppliers with dealership operations are in many cases distanced from the corporate entities which govern the marque. For example the operations of a particular marque and its dealer network in Australia are removed from the actual manufacturing division of that marque. Q 3.3: Is there evidence to suggest that there are safety risks associated with withholding repair information from independent repairers? AADA and its members could argue that without proper tooling equipment and training to accompany the information that the opposite is true. In this submission the interaction between various vehicle systems and components details why. For instance incorrect reference to data can result in damage to safety items such as airbags, seat belt pre-tensioners, ABS sensors and modules and systems such as electronic stability control. Q 4.1 – Q4.7 AADA is privy to the views expressed in the submission prepared by the Australian Motor Industry Federation and agrees with arguments that the adoption of overseas legislative models into the Australian legislative, policy and market frameworks are inherently flawed. The factors that are generally overlooked in those arguments are ones of context and environment. The Australian policy, regulatory and policy framework is unique. Resultantly, it has distinct characteristics and operating nuances that need to be recognised and acknowledged. For example, the EU competition law framework has – by the Association’s understanding – an underpinning of significance that is not always recognised. That is simply that, within the EU, there exists the operation of layers of free trade agreements between the EU’s various member

states. It is those mechanisms and others like them that make possible, in the EU, fully factory authorised vehicle repair and service centres that will have no association with a dealership. It is also those agreements that compel manufacturers that wish to operate out of the EU to make information available under certain terms. These are underpinnings and frameworks that do not exist in Australia. It also needs to be remembered that the Australian market – comprised, as it is, of some 62 brands selling over 350 model of vehicles – has around 80 per cent of its vehicles imported, and only 20 per cent of its vehicles produced domestically. Contrast that with, say, Germany, where the Federation understands the reverse to be the case, with only 20 to 30 per cent of vehicles sold imported and 70 to 80 per cent domestically produced. There are simply too many glaring distinctions that can be made between the critical nuances of the Australian market, and those of overseas jurisdictions, as to provide much at all in the way of guidance for these issues in an Australian policy context.

The Australian Automobile Dealers Association Pty Ltd National Secretariat Canberra September 2011