Hardwood Chip Price AnalysisLike all commodities, hardwood chip prices (and volumes) are subject to global conditions and situations.

In particular, hardwood chip markets are impacted by pulp prices that are themselves driven by the demand for

paper.

Historical Price Analysis

In 2011, Australia’s average hardwood chip export price was USDFob181.56/t and in 2012, it was

USDFob172.75/t. However, the national average price is not indicative of any one situation.

Excluding the impact of foreign exchange rates, Australian average hardwood chip prices have been heavily

influenced by four major factors since 2010, as follows:

• Slow demand growth for printing and writing papers, especially in Europe, North America and Japan as the effects of the global financial crisis linger.

The primary utilisation of hardwood chips is the manufacture of bleached pulp for the production of printing and writing papers.

Since 2008-09, global demand for printing and writing papers has declined by 18.0% to the end of February 2013. North American (-33.0%) and Western European (-27.0%) demand have led the decline. The rest of the world (dominated by China and Japan) was down just 2.0% over the same period.1

As a result of the declining demand, current global capacity utilisation across all grades of printing and writing papers is 81.0%. 2 This near 20.0% under-utilisation is driving continued pressure on paper prices which in turn are suppressing global pulp and hardwood chip prices.

IndustryEdge notes this differential in regional demand is reflected in expanding printing and writing paper production in China, at the same time as contractions continue to occur in Western Europe and to a lesser extent in North America.

Emerging economy demand from countries such as India and China for uses outside of writing papers is also growing. In particular, demand for woodchips is occurring to satisfy use in hygiene products such as tissue paper and toilet paper, however, the majority of this demand is met by softwood fibre supplies. These emerging trends are expected to continue as the standards of living in these countries improve over the coming years.

Japanese demand for hardwood chip declined sharply during the global financial crisis. Supplies from all exporting countries declined in line with demand.

Demand improved from MQ’09, although events have caused it to be quite turbulent. Demand has not returned to its original levels.

Proportions of supply from importing countries have changed markedly over a period of just less than five years, as the following chart shows.

1 & 2 EMGE, Global Monthly Monitor, February 2013

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

Japanese Hardwood Chip Imports by Country of Origin: MQ’08 – DQ’12 (kt)

Source: Japan Customs

In MQ’08, Australia supplied 1 006.8 kt of hardwood chips to Japan, which constituted 34.1% of total supply. In DQ’12, Australia supplied 574.8 kt or 25.2% of total supply. The decline of Australian supply over the period has been 42.9%, down from approximately 4.0 million bone dry metric tonnes per annum (circa 8.0 million GMT equivalent) in calendar 2008 to approximately 2.3 million bone dry metric tonnes in calendar 2012 (circa 4.6 million GMT equivalent). South African supply has suffered a similar fate to that of Australia.

Chile has retained a relatively stable supply volume and now delivers 26.0% of all hardwood chips, up from 20.1% in MQ’08.

It is lower priced supply from Vietnam that has grown a substantial position in the Japanese market. In MQ’08, Vietnam supplied 225.9 kt of hardwood chip to Japan, or 7.6% of the total quarterly supply. In DQ’12, that had risen to 426.9 kt or 18.7% of total supply.

Hardwood chip quality from Vietnam has reportedly been, on average, relatively sub-optimal, resulting in price discounts being applied. Plantation resource such as E.nitens, delivers a higher quality product, and is therefore likely to attract higher prices than those being paid to Vietnamese suppliers.

International industry expectations are for a tailing off of supplies from Vietnam and other south-east Asian producers over the next two to three years and a simultaneous improvement in average quality and price for hardwood chip supplies from that country.

This change in both market demand and supply factors in Japan has had significant price implications for Australian hardwood chip volumes and prices.

JQ'08

MQ'09DQ'09

SQ'10JQ

'11MQ'12

DQ'120

500

1000

1500

2000

2500

3000

3500

kt

Quarter

Australia

Brazil

Chile

Sth Africa

Thailand

Viet Nam

Other

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

At least one major (post MIS) owner has engaged in significantly discounted sales to realise cash flows and optimise opportunities for sale of land which is sub-optimal (or worse) for growing trees and/or for which there are lower harvest costs.

It is notable that this strategy is currently deployed for the preferred E.globulus plantations, which is suppressing weighted average export prices for all hardwood chips, and is also limiting opportunities for E.nitens resource. Industry intelligence suggests that the liquidations are coming to an end and pricing normality will return as more profitable plots are harvested.

• DebateandcampaignsoverTasmaniannativeforestry,leadingtooneoffliquidationsfrom Tasmanian ports, including of old stock.

Hardwood chip sales from Australia’s native forests and especially from those in Tasmania, are occurring at lower prices as debate continues around native forestry.

Analysis of recent prices achieved for specifically plantation hardwood chips provides an additional and different perspective. IndustryEdge has selected the three Australian ports that export hardwood chips exclusively sourced from plantations (Bunbury and Albany in Western Australia, and Portland in Victoria).

The following table specifies the average price of hardwood chip exports from January 2011 to December 2012 from those ports, compared with the trade weighted average price for all exports of hardwood chips over the same period.

Quarterly Hardwood Chip Export Prices from ‘Plantation Only’ Ports:

2011 & 2012 (USDFob/bdmt)

Source: ABS and IndustryEdge research and analysis Note: E.globulus price ~ USDFob10/bdmt discount not applied for E.nitens

The differential against the trade weighted average price of all hardwood chip exports from Australia over the recorded period, for exports from plantation only ports has declined over the

MQ'11JQ

'11SQ'11

DQ'11MQ'12

JQ'12

SQ'12DQ'12

100

120

140

160

180

200

220

240

USD

Fob/

t

Quarter

Albany

Bunbury

Portland

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

period to DQ’12. This chart emphasises both the preference for plantation woodchips (consistently above the Australian average price) and the impact of what appear to be liquidation sales of hardwood chips from under-performing plots.

It is relevant to consider the prices paid in the major countries supplied by Australia. Hardwood chip buyers in Japan and China pay different prices for hardwood chips imported from Australia.

The following chart shows Australian average hardwood chip prices for Japan and China over 2010 to 2012.

Hardwood Chip Export Prices by Country of Delivery: 2010 - 2012 (USDFob/t)

Source: ABS Note: E.globulus price ~ USDFob10/t discount not applied for E.nitens

It is evident from the chart Chinese buyers have purchased hardwood chips at lower prices than Japanese buyers.

However, Chinese buyers have increasingly exhibited a willingness to pay higher prices for better chip quality. Evidence of this may be found in the gradually increasing prices paid for Australian supply which has significant quality advantages to the hardwood species produced from south-east Asian countries.

It is notable that from 2011 to 2012, the average price of Australian hardwood chips increased in China by 9.2%, while in Japan the average price declined by 6.8%. Nonetheless, Japan remains the preferred destination for Australian hardwood chip exports throughout the forecast period.

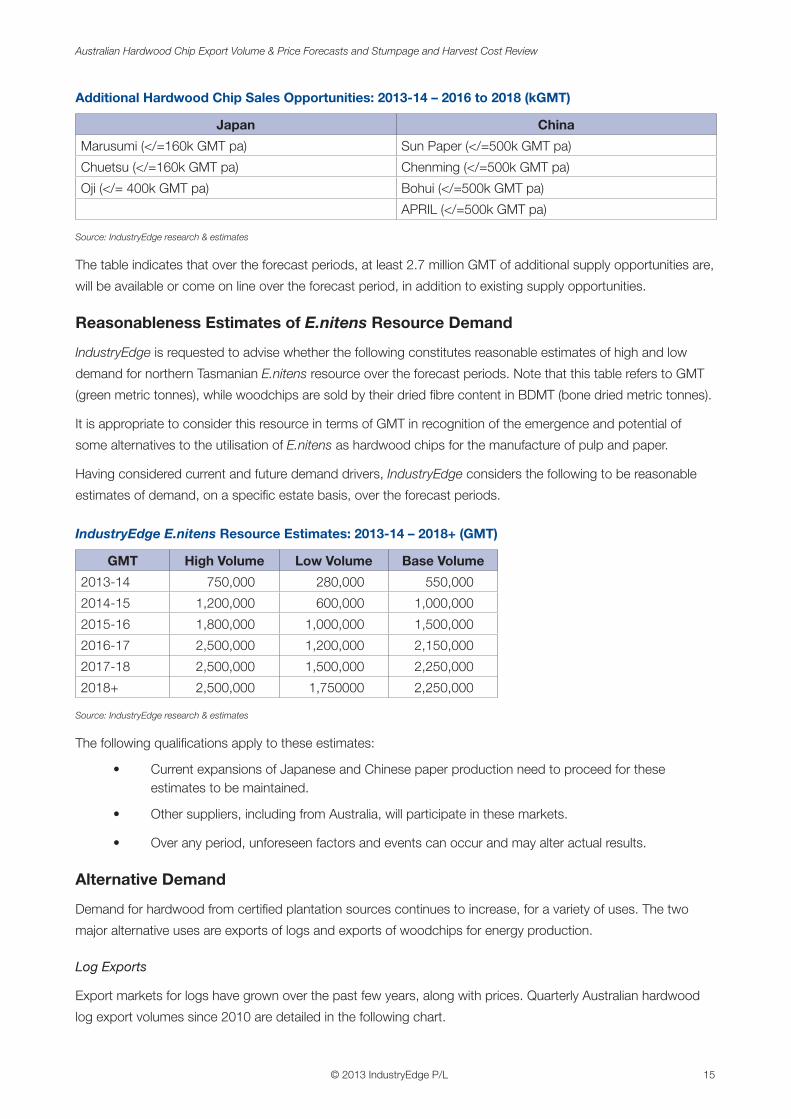

Price Forecasts

Based on historical pricing data and taking into account the range of demand, supply and general economic

factors that are anticipated to be prevalent through to 2018, IndustryEdge forecasts the following likely price

ranges for hardwood chip exported from FSC certified, E.nitens plantations in northern Tasmania.

MQ'10

JQ'10

SQ'10DQ'10MQ'11

JQ'11

SQ'11DQ'11MQ'12

JQ'12

SQ'12DQ'12

100

120

140

160

180

200

220

240

USDFob/bdmt

Quarter

China

Japan

Taiwan

TWA

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

Note: E.nitens price ~ includes USDFob10/bdmt discount

The following qualifications apply to these price forecasts:

• Highpriceforecastsonlyapplyforcertifiedplantations(becauseitassiststoensurevolumeandprovides a form of protection for buyers against environmentalist’s campaigns).

• Highpriceforecastsonlyapplyforvolumesuptoandincludingthe‘HighVolume’estimatesdetailed in this report for the forecast periods.

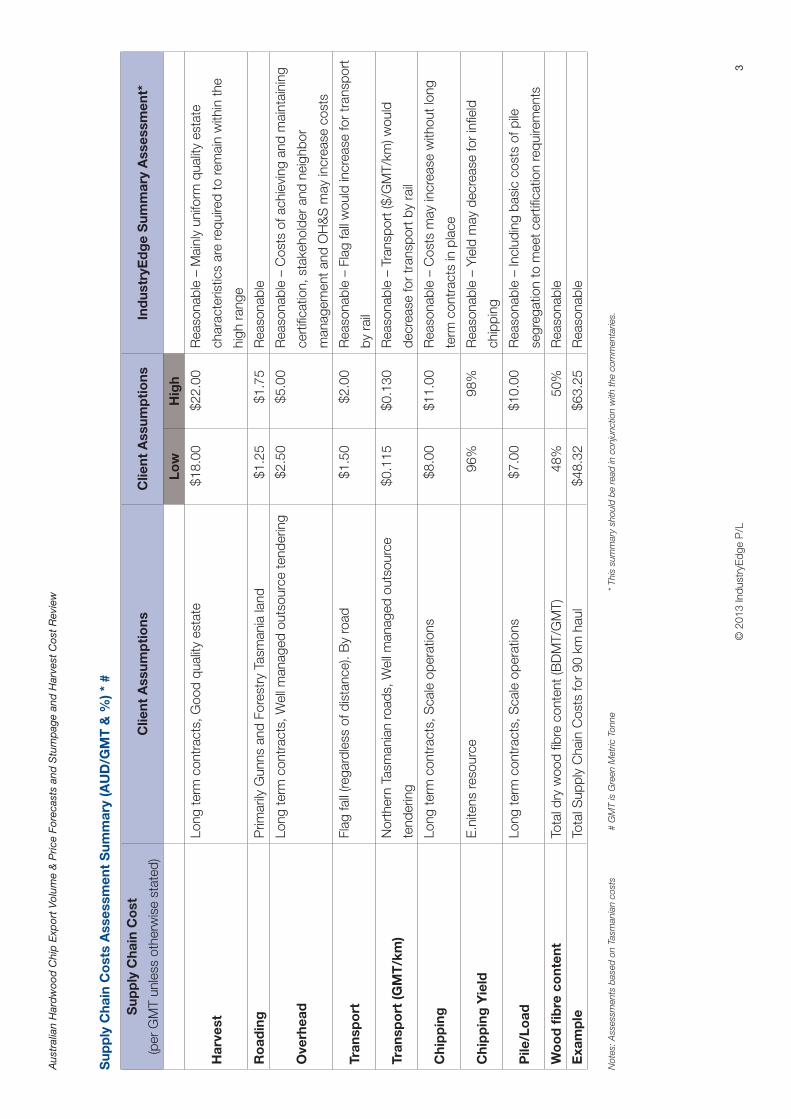

access and high automation. The mid-range of AUD20/GMT would be a better low end figure, especially for plots where growth rates are mixed and there are a number of smaller or undersized stems.

• Harvestingcontractsshouldbenegotiatedforthelong-term.However,itisalsoimperativetheharvesting manager/contractor is certified with AFS and FSC supply chain management.

• Ifinfieldchippingistooccur,thenharvestingcontractorsusuallyundertakethemobilechippingoperations. While this increases the cost of field operations, it will remove the cost of chipping at major chipping facilities. We estimate that an infield chipping cost of approximately AUD 26-28/GMT is reasonable.

• HarvestingcostswillbehigherthanAUD22/GMTiftheplantationregimeistogrowonselectivestems for sawlogs or peeler logs, thereby necessitating thinning operations within the plantations. The cost of thinning operations is very much site specific, but will raise the high end of the harvesting range to be closer to AUD30/GMT in some instances. However, if the plantations are managed to deliver sawlog or peeler log they will generally command a much higher price than woodchips.

purposes, and in most instances would require little maintenance to enable harvesting to proceed. The most likely issues to arise with roading if not maintained for a while are washed out culverts, incline corrugation and bridge upkeep.

• Thehighandlowestimatesforroadingarewellwithinexpectedranges,however,thereisnonoteif FT levies have been included. The prices shown would cover private, as well as local government and state roads, but FT levies would be applicable in many instances which are not stated.

in application. Often overheads are calculated by a set sum per hectare, possibly in the region of AUD25/ha, then a certain amount per tonne of wood, usually at the lower end of the range being AUD2.50/GMT.

• Thelowandhighoverheadcostestimatesdonotappeartocovercertification,OH&S,contractmanagement, neighbour management or stakeholder management. Each of these issues is required to be addressed if certification by either the Forest Stewardship Council (FSC) or Australian Forestry Standard (AFS) is to be attained and maintained.

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

Transport – Flag fall • Thelowandhighestimatesfortransportflagfallareinthecorrectrangeforlogstransportedfor

wood chipping at a major facility. However, they may be higher than the cost for the transportation of product from infield chipping. This statement is dependent on a number of variables, but the essence of the costing is that more volume (weight) can be carried in the form of chips since the air space between logs is not a factor in loading.

• Estimatedtransportflagfallisreasonableontheunderstandingalltransportisbyroad,andnotbyrail freight. Rail may become pertinent for resource managed in Southern Tasmania, then moved north to either the Longreach or Hampshire mills.

Transport – Rate • ThelowandhighestimatesfortransportratesstatedbyAUD/GMT/kmareaccurate.This

assessment is provided on the basis that most harvesting will be undertaken in a catchment of not much more than 90 kms around either the Longreach or Hampshire mills and that roads are in good condition, which they generally are.

• OutsourcetenderingfortransportwouldnormallybearrangedbytheResponsibleEntity,and would be for given volumes over a set period. There is ample available capacity in log transportation in Tasmania. As a result, prices will be towards the lower end of the range.

• InthenorthofTasmania,90kmcatchmentsaroundbothLongreachandHampshiremillswouldcover upwards of 80% of the specific resources. Major blocks, such as Surry Hills, are within the 90 km catchment zone.

not be necessarily relevant for infield operations, where chipping would be part of the harvesting operations.

• Thestatedlowandhighestimatesarewithinrangeforfacilitieswhichareownedbythemanagingentity or for which it has open access. However, the estimates may be on the low side if contract chipping is undertaken by a third party and is not contracted.

• Long-termcontractsforexpandingvolumeswillmovechippingcoststowardsthelowerendofthegiven range, but not below the stated, estimated low costs.

Both Longreach and Hampshire have historically achieved yields within these ranges, however may require maintenance to achieve correct quality chip size.

• Problemsreducingchipyieldareshattercausedbybluntorpoorpositioningofchippingequipment, making chip sizes too large or non-uniform and the increase in fines falling to waste.

• Infieldchipping,whileoftenasmalleroperation,canalsoimpactfibreyieldifproductisleftonthe harvesting operation site for an extended period and moisture loss or gain is not managed within acceptable bounds. A corresponding increase in yield is able to be achieved with infield chipping because trees are taken down to a much lower small end diameter – meaning additional merchantable timber of approximately 1% to 2% is produced than for logs which go to a static chipping facility. Management of chip quality is critical to optimise outcomes from infield chipping

operations.

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

Pile and Load • TheestimatedpilemanagementandloadingcostsAUD/GMTarewithinbounds.However,these

may be impacted through reduced costs if infield chipping operations are applied.

• Pilemanagementcostsmaybeslightlyhighersincesegregationofpilesmayberequired.Segregation would be by certified chain of custody, being:

– FSC must be managed in accordance with FSC product requirements,

– AFS pile not to contaminate any pile carrying FSC certification, and

– FSC controlled wood chip pile. This would not mean the wood has been certified, but the supply chain of management would be certified as meeting FSC requirements.

• CurrentlytheLongreachandHampshirechipmillsareclosed,alongwiththerespectivechippilesand loading facilities at the ports. It is understood these facilities are not ready to start immediate operations. In addition, it is also doubtful if the TasPorts contracted preferential treatment for Gunns

at the Burnie wharf could be transferred to a new incumbent.

• Variancefromthelowof48%andhighof50%generallyarisesonanaveragebasis,ifthereispoorchipping yield due to shatter and fines, which will most likely arise where insufficient maintenance has been undertaken at a substantial chipping facility or where poor infield chipping management occurs. Other factors which may influence dry fibre content include climate, harvest timing and the amount of time logs are left out in the forest.

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

8-12%. For assets that are sold under distressed conditions or perceived forced sales, buyers will typically apply

an additional discount. This is often the case in situations where there is an owner (or seller) of timber assets that

are perceived to be in distress, such as that which has applied in the Australian hardwood plantation sector in

recent years. It is not reasonable to assume that a discount rate of 20-30% may be sought in these situations.

The effect of discount rates on potential purchase prices can be illustrated using the following simplified

example. Assume, the cash flows that are expected to be generated by a timber asset in 3 years time is $100. If

a discount rate of 8% is used, the purchaser would attribute a value of $79.38. Conversely, (and using the other

end of the spectrum) if a discount rate of 30% is used the attributable value would be $45.52.

In the current circumstances and for a sale conducted in the near term (concluding in 4 to 6 months), the small

universe of potential investors is likely to focus on steep discounts. This is as much the case for estates that are

available for sale free of encumbrances, as those for which the encumbrances may be significant.

There are several relevant considerations:

• Encumbrance of Estates – Plantation estates established under Managed Investment Schemes (MIS) generally include some encumbrances that increase transactional and reputational risks. These include multiple counter-parties in the form of grower-investors.

• Uncertainty of Recent Estate Management – Plantations require constant management, maintenance and up-keep, including of infrastructure of the type detailed in the Supply Chain Considerations and Costs section of this Report. Additionally, ongoing rationalization of an estate on an orderly basis is critical to presenting an estate for sale in its best condition, without introducing market shocks such as significant liquidation volumes from under-performing plots. Uncertainty of the current condition of the plantation estate is increased where consistency of management may have been impacted by the financial capacity of the estate manager.

• Limited Potential Buyers – IndustryEdge considers the universe of potential buyers to be limited to vertically integrated pulp and paper manufacturers (most likely from Japan and China) and institutional investors, operating through established managers.

Established managers and their institutional investors have made extensive purchases of Australia’s hardwood plantation assets in the last three years. This has reduced the number of potential buyers. Additionally, the capacity of the remaining entities to fund further, significant acquisitions is not without limits. One of the major entities has expressed itself unwilling to participate in Tasmania at all.

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review

Japanese pulp and paper manufacturers are unlikely to have capacity or interest in significant direct expansions of their plantation estate holdings in Australia.

Chinese pulp and paper manufacturers may be interested in securing long-term access to a plantation estate. Their intentions are however unknown and as yet untested.

• Demand and Supply of Hardwood Chips – Japanese and Chinese pulp and paper manufacturers are currently able to secure hardwood chip resource as required, at prices that still include liquidation volumes and at a time when most paper prices are stagnant and global production to capacity of printing and writing papers is around 80% (as described in this Report).

In this context, IndustryEdge considers there is uncertainty about the interest, capacity and desirability (from a buyer

stand point) of the current E.nitens plantation estates, particularly if the assets are perceived to be a distressed

sale. As a result, IndustryEdge considers a reasonable assessment of integrated pulp and paper manufacturer and

institutional investor discount expectations would range between 20% and 30% per annum of the assessed NPV.

In the circumstance of estates where evident distress is not a feature, there is potential to significantly improve

return prospects and the potential purchase price that can be achieved from a buyer. In such a circumstance,

there is likely to be a higher degree of competitive pricing tension between potential purchasers.

Australian Hardwood Chip Export Volume & Price Forecasts and Stumpage and Harvest Cost Review