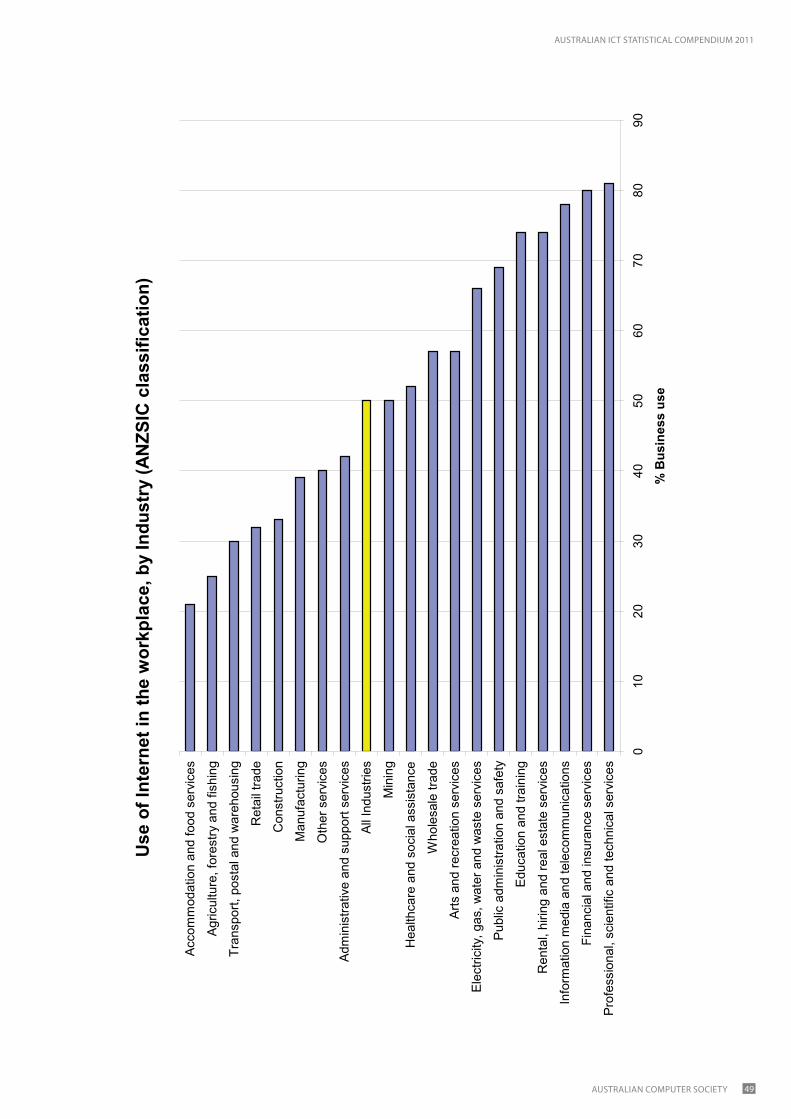

76

Australian ICT Statistical Compendium 2011 www.acs.org.au/2011compendium

AustrAliAn iCt stAtistiCAl Compendium 2011

1AustrAliAn Computer soCiety

AUSTRALIANCOMPUTERSOCIETY

Australian ICT StatisticalCompendium 2011

www.acs.org.au/2011compendium

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety2

AustrAliAn iCt stAtistiCAl Compendium 2011

2 Australian Computer society

AustrAliAn iCt stAtistiCAl Compendium 2011

3AustrAliAn Computer soCiety

Contents 4 Why this publication?

4 About the Australian Computer society

5 At A Glance

6 defining iCt

14 Who We Are

15 iCt employment demographics

16 learning iCt

24 Vocational education & training (Vet)

29 Women in iCt

35 Where We Work

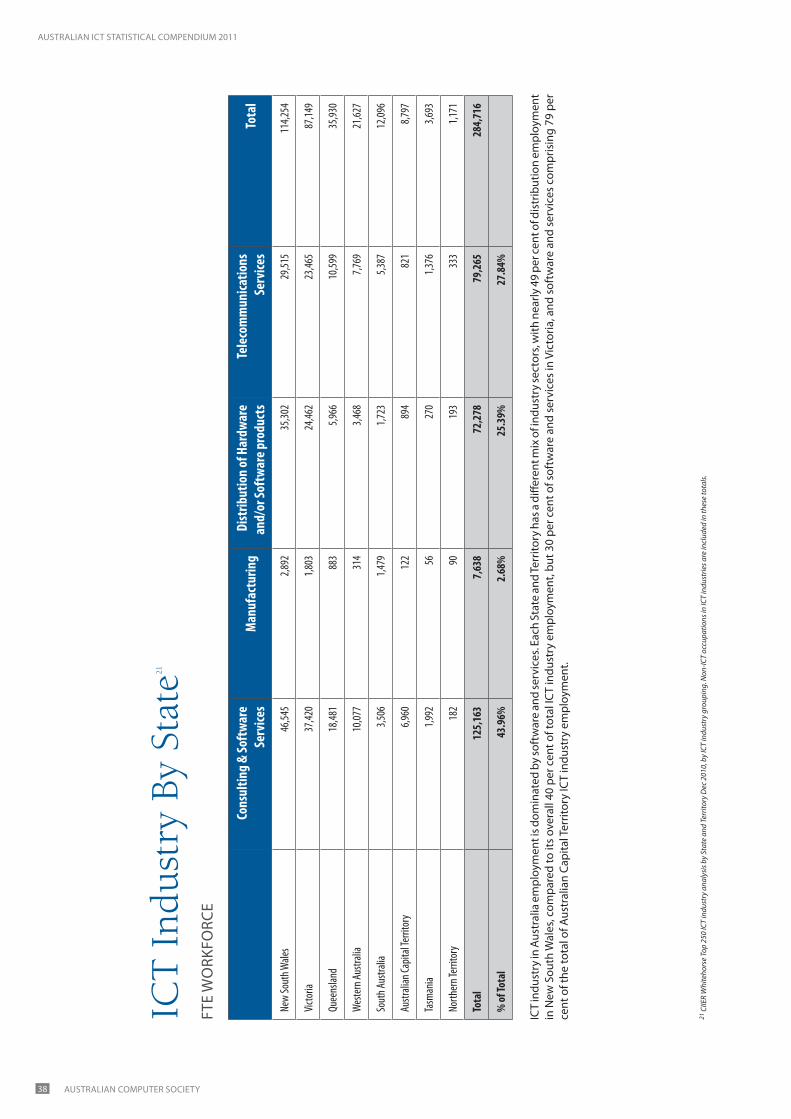

38 iCt industry By state

46 What We do

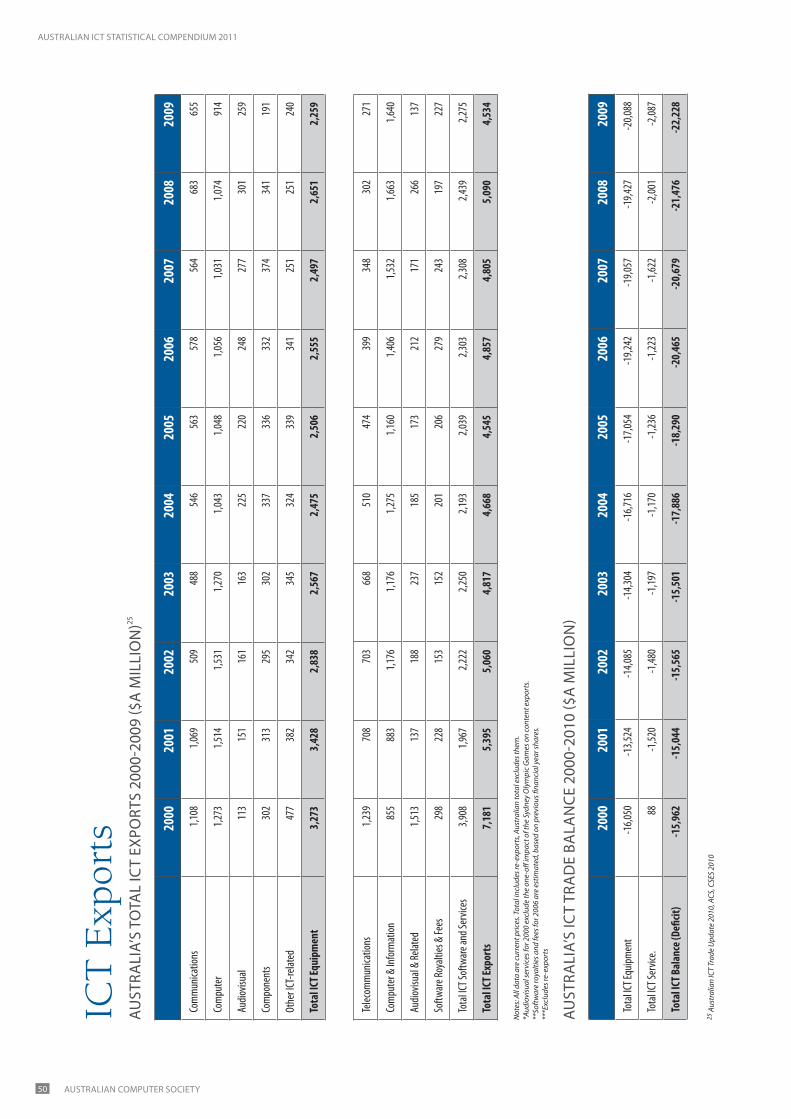

50 iCt exports

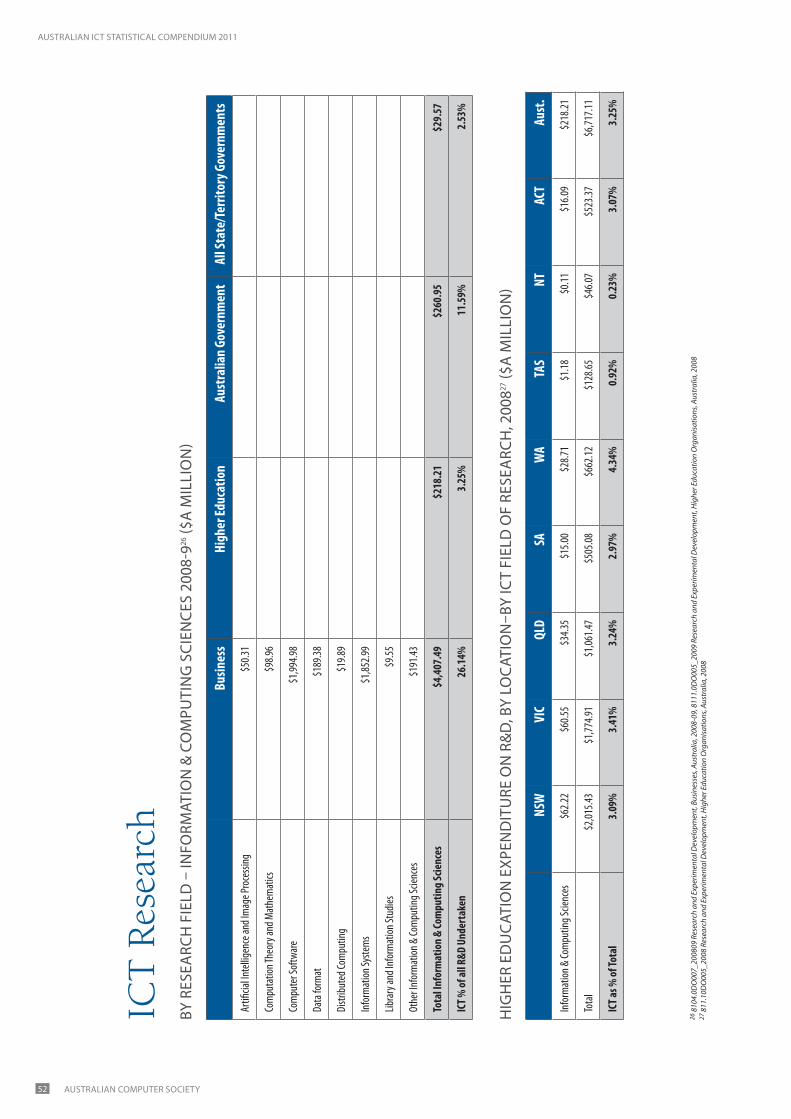

52 iCt research

55 How We do it

56 How do We Compare?

62 Where Have We Come From – And Where Are We Going?

67 the nBn effect

72 How should We read this document?

73 About the Centre For innovative industries economic research inc

74 sources And Acknowledgments

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety4

the Australian Computer society (ACs) is the recognised professional association for those working in information and Communications technology, seeking to raise the standing of iCt professionals and represent their views to government, industry and the community. A member of the Australian Council of professions, the ACs is the guardian of professional

ethics and standards in the iCt sector, committed to ensuring the beneficial use of iCt for all Australians. it provides both members and non-members with opportunities for professional education, networking and certification, as well as enabling them to contribute to the development of their profession. Visit www.acs.org.au for more information.

About TheAustralian Computer Society

AUSTRALIANCOMPUTERSOCIETY

po Box Q534, QVB post office,

sydney nsW 1234

tel: +61 2 9299 3666

Fax: +61 2 9299 3997

We all recognise the difficulty of easily accessing relevant data (employment, educational outputs, research spend, etc.) on iCt economic and social trends. ACs, in cooperation with the Australian Bureau of statistics (ABs) and other relevant Government departments, engaged Ciier in 2009 and 2010 to develop an iCt statistical Compendium to combine quality iCt-related data into a single summary report, as part of the ACs commitment to improving iCt outcomes in Australia. the Compendiums have been very well received by the iCt profession, iCt industry, and by Governments around Australia, so this year, Ciier has again been engaged to provide an expanded version of the Compendium, including new analysis on the digital economy, more trend analysis, and discussions on improving iCt-related statistical data.

As with each edition, this Compendium does not include

all of the available data, but we have tried to amass a range of data addressing the main questions that arise. some data

included in the first publication – e.g. ABs iCt industry data, has again been substituted with later data from Ciier in this edition, as no later information was available from ABs. Where no later data could be identified, but the data is considered still highly relevant, information has been repeated.

the objective of this project was to produce a series of ‘snapshots’ of statistical data on the iCt workforce for ACs members, industry and government, and a potential ‘bible’ for iCt users, incorporating statistics on the Australian iCt sector, iCt higher and vocational education, iCt trade, iCt employment and skills, iCt immigration, with some breakdowns of the statistical data on a national and state/territory basis.

our aim is to continue to assist policymakers involved in the iCt sector by providing the latest available data, and to provide a tool for iCt professionals and the iCt industry, and for businesses that deal with the iCt sector.

Why This Publication?messAGe From tHe ACs

© Data in this publication is copyright to the attributed and referenced organisations, and this publication itself is also copyright. Other than for the purposes of and subject to the conditions prescribed under the Copyright Act, no part of it may be in any form or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced, stored in a retrieval system or transmitted without prior written permission.

AustrAliAn iCt stAtistiCAl Compendium 2011

5AustrAliAn Computer soCiety

At

A G

lanc

esu

mm

Ary

tA

Ble

oF

Key

nAt

ion

Al

stAt

isti

Cs

1 CIIE

R tr

end

asse

ssm

ents

2 No

late

r ABS

dat

a av

aila

ble

Mea

sure

men

tSt

atist

icPe

riod/

curre

ncy

Sour

ceTr

end

1

Tota

l ICT w

orke

rs in

Austr

alia

554,7

00Fe

b 201

1AB

S Lab

our M

arke

t Sur

vey F

eb 20

11, IC

T Ind

ustry

log

istics

CIIER

2010

Cont

inuing

grow

th, d

eman

d is

appa

rent

Tota

l ICT T

echn

ical, P

rofes

siona

l, Man

agem

ent, T

rade

staff

in

Austr

alia

468,7

73Fe

b 201

1AB

S Lab

our M

arke

t Sur

vey F

eb 20

11, C

IIER e

xtra

ctCo

ntinu

ed gr

owth

over

20-y

ear c

ycle.

Dec

line i

n 20

09-1

0 and

2010

-11

Tota

l ICT T

echn

ical, P

rofes

siona

l and

Man

agem

ent

staff

in Au

strali

a 38

3,135

Feb 2

011

ABS L

abou

r Mar

ket S

urve

y Feb

2011

, CIIE

R ext

ract

Stea

dy gr

owth

to 20

08, s

tatic

in 20

09-1

0, sli

ght

grow

th in

2010

-11

Tota

l ICT D

omes

tic an

nual

com

men

cem

ents

in Au

strali

a 8,7

0420

10DE

EWR

4.5%

incre

ase i

n 201

0, af

ter c

ontin

uing d

eclin

e, slo

wing

in pa

st th

ree y

ears

Tota

l tem

pora

ry IC

T migr

ants

to Au

strali

a8,5

30 pe

r ann

um

2009

-10

DIM

IA, C

IIER c

alcula

tion

Has b

een i

ncre

asing

rapid

ly to

star

t of 2

008,

decli

ned i

n 200

8-9 a

nd 20

09-1

0

Emplo

yees

in IC

T Ind

ustry

. (Com

panie

s tha

t sup

ply IC

T go

ods a

nd Se

rvice

s)28

5,000

Dec 2

010

CIIER

T250

2010

Slo

w gr

owth

, reco

verin

g fro

m G

FC

Reve

nue o

f ICT I

ndus

try$8

2 billi

onDe

c 201

0 CII

ER T2

50 20

10Co

ntra

ction

from

2008

in te

lecom

mun

icatio

ns

reve

nue,

secto

ral v

ariat

ions

ICT R&

D$5

.206 b

illion

2008

-9 2

ABS 2

011

Reco

very

from

long

-term

decli

ne, c

ontin

uing t

o be

led by

busin

ess R

&D

ICT ex

ports

(exc

luding

re-e

xpor

ts)$4

.534 b

illion

2008

-9CS

ES 20

10, A

BS Tr

aded

ata

Dip i

n 200

9, af

ter g

radu

al re

cove

ry to

1999

-200

0 ex

port

levels

, but

with

an in

creas

ing tr

ade d

eficit

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety6

Defining ICT

one of the significant difficulties in understanding iCt in Australia is the frequent confusion between analysis of the iCt workforce in labour market terms (e.g. what job the individual performs), and analysing the iCt workforce in industry terms (e.g. what kind of organisation the individual worked for). Clearly iCt is evident in every industry sector, but unfortunately iCt is not yet always recognised statistically as an industry sector in its own right, and it will remain so until the current industry statistical metrics used in Australia are updated to reflect the pervasiveness and reality of iCt in the 21st century.

iCt broad employment occurs in a number of groupings. these include:

• the providers of iCt goods and services (usually called the iCt industry)

• the purchasers and users of iCt goods and services, including the government and private sectors, which also employ a large number of specialists to help them apply their iCt purchases

• the trainers, teachers and researchers in iCt who generally (but not always) operate within universities and colleges

• people who provide technical support to iCt, but who might, more properly, be categorised as electrical or electronics specialists

• people working in call-centres, or in desktop publishing and graphics design

there is a significant percentage of iCt professionals in the iCt industry, but iCt industry employment includes not only those professionals, but also many iCt non-professional technical, sales, logistical and administrative staff.

AnZsCo (Australia, new Zealand standard Classification of occupations) is a multi-level nomenclature essential to the understanding of employment statistics. the upper level (the 2-digit level) is meant to bring like occupations together so they can be aggregated. unfortunately, the iCt occupation grouping at this level leaves out some occupations that we, and others, would consider are, wholly or in part, within iCt. Accordingly, simple extracts from employment data of the “iCt” AnZsCo group can easily lead to inadvertent understatement of the actual position of iCt employment. in this report we have identified the key AnZsCo classes from which the iCt analysis is derived.

the ACs maintains a more appropriate classification of iCt occupations is required to understand the iCt sector and the “digital economy” in Australia, and thus inform iCt policy with a clear, verifiable set of metrics, potentially by reference to the skills Framework for the information Age.3

AnZsiC (Australia, new Zealand standard industry

Classification) is similarly structured to AnZsCo, and while it also has an upper-level iCt grouping (information media and telecommunications), which includes some small non-iCt elements, it unfortunately does not include the numerically larger software and services iCt industry sector, which is included as a misnamed subset (Computer

systems design) within the upper-level grouping “professional, scientific and technical services”.

“information media and telecommunications” also leaves out iCt hardware manufacture, iCt wholesale and retail trade, and iCt consulting sectors, which are scattered across a number of other AnZsiC classifications.

General economists, and other commentators, sometimes presume that “information media and telecommunications” in ABs data and government publications is the iCt industry, and make comment without realising that in employment terms, it is actually less than half of the employment of the “real” iCt industry.

this same analysis impacts their calculations of iCt revenue, exports and Gdp/GVA, which regularly become a synonym for economic importance, and are frequently understated for iCt, but overstated for the AnZsiC industry classifications in which the missing iCt industry sectors are hidden.

However, in this report we have tried, wherever possible, while not altering figures derived from these misleading categorisations, to indicate the estimated “true” value of the iCt industry component of each of these measures.

3 Skills Framework for the Information Age © http://www.sfia.org.uk

tHe iCt seCtor

AnZsCo And AnZsiC

AustrAliAn iCt stAtistiCAl Compendium 2011

7AustrAliAn Computer soCiety

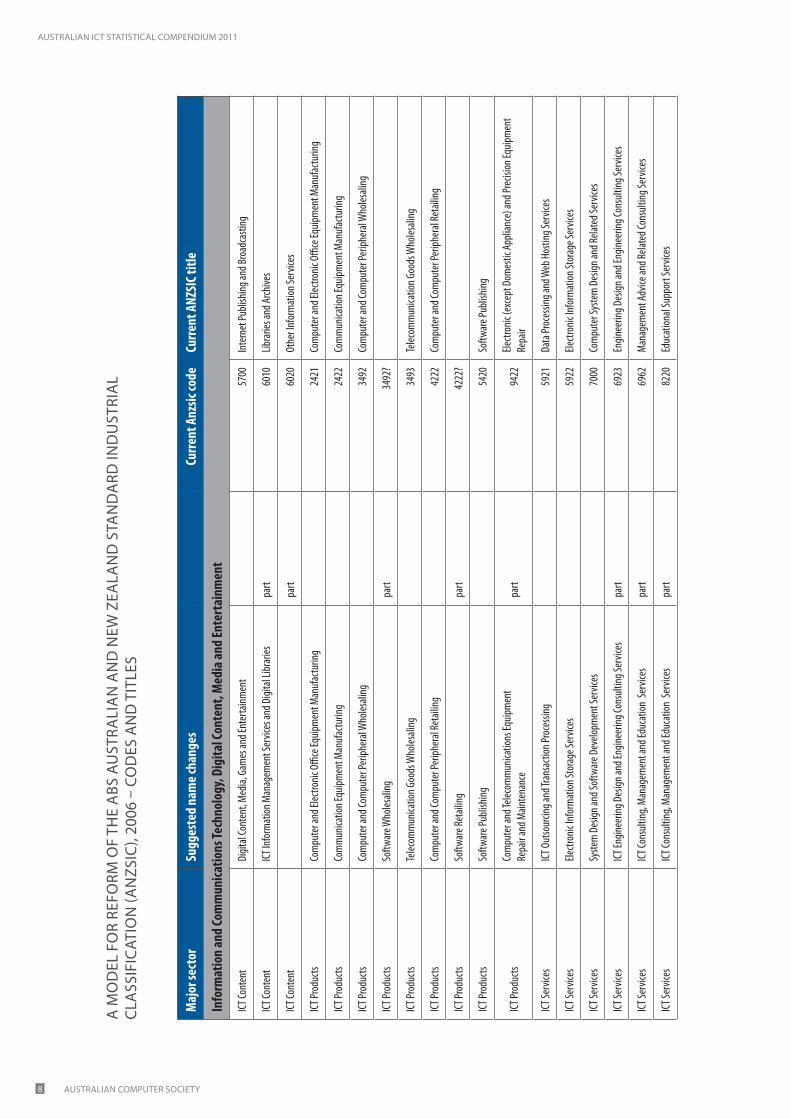

parts of the iCt industry can be found in the following AnZsiC categories:

• professional, scientific and technical services• information media and telecommunications• retail trade• manufacturing• education and training• Wholesale trade• Arts and recreation services

major sectors within the industry include:

• it services, systems integration and software support• internet services and telecommunications• software and digital content development• Wholesale and retail distribution of software and

hardware• manufacture of iCt products and components

the ABs has measured the iCt industry intermittently as a specific exercise since 1996, with its last report now over five years old representing the period 2006-7 (cat 8126.0) and published in october 2008. this report was referenced for the iCt industry data in the 2009 ACs iCt statistical Compendium.

the Centre for innovative industries economic research inc has conducted an annual survey, since 1998, on a smaller survey sample, modelling the iCt industry in a similar manner to ABs. the iCt industry data for the 2011 statistical Compendium will draw upon Ciier’s december 2010 data, as the 2006-7 ABs data is now too far out of date to add meaningful value.

Further confusion is now arising with the use of the terms “digital economy” and “internet economy” to describe both those elements of the economic processes of all industries impacted by iCt, or by the specifics of internet-based iCt, and in some cases the productive elements (labour, infrastructure, etc.) that make these possible.

it is easier to accurately define Australia’s digital economy by what it is not, rather than by what it is. in the

broadest sense it is almost the entire domestic economy, other than those very small components of the economy that do not use any iCt support at all (e.g. subsistence farming or street musicians – unless they also distribute their outputs electronically). more logically, it is all of the iCt industry, and a significant proportion of almost every other economic sector that uses iCt. mining, healthcare, education, government, wholesale and retail trade, manufacturing, transport and other sectors all rely on iCt goods and services, and are therefore participants in the digital economy.

the internet economy can be defined as a varying subset of the digital economy. the variation is because the decision whether to use internet-based iCt or internal organisational iCt is one that is made for lots of different reasons – technical, financial, data security or operational control – and those decisions change over time. the distinction is also economically irrelevant, other than for iCt suppliers whose markets are internet-focused products and services. unfortunately, these terms are used interchangeably, and the more narrow definition of internet economy may therefore lead to conservative interpretations of the significance of the digital economy, and thus of the iCt industry and iCt profession that creates and maintains it.

the term “iCt industry” is also often used for a confusing range of different things, ranging from the “tight” definition of companies solely concerned with the provision of iCt products and services, but which includes companies with major units supplying iCt goods and services, through to a “looser” definition that may include retail iCt, that may include call centres that are mainly parts of other industries (e.g. banking), that may include significant sections of the electronics industries and of other professional services (e.g. management consultants and, historically, accountants), to a “broad” definition that can include anyone working on iCt-related matters in any industry.

“iCt industry” in this publication refers to the tighter ABs

and Ciier definitions; we have used the term “iCt worker” for the broader definition. the table below sets out a suggested model for the redefinition of the iCt industry, drawing upon existing AnZsiC structures.

tHe iCt industry

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety8

Maj

or se

ctor

Sugg

este

d na

me c

hang

esCu

rrent

Anz

sic co

deCu

rrent

ANZ

SIC t

itle

Info

rmat

ion

and

Com

mun

icatio

ns Te

chno

logy

, Dig

ital C

onte

nt, M

edia

and

Ente

rtai

nmen

t

ICT Co

nten

tDi

gital

Cont

ent,

Med

ia, G

ames

and E

nter

tainm

ent

5700

Inte

rnet

Publi

shing

and B

road

casti

ng

ICT Co

nten

tICT

Info

rmat

ion M

anag

emen

t Ser

vices

and D

igita

l Libr

aries

part

6010

Libra

ries a

nd Ar

chive

s

ICT Co

nten

tpa

rt 60

20Ot

her I

nfor

mat

ion Se

rvice

s

ICT Pr

oduc

tsCo

mpu

ter a

nd El

ectro

nic O

ffice

Equip

men

t Man

ufac

turin

g24

21Co

mpu

ter a

nd El

ectro

nic O

ffice

Equip

men

t Man

ufac

turin

g

ICT Pr

oduc

tsCo

mm

unica

tion E

quipm

ent M

anuf

actu

ring

2422

Com

mun

icatio

n Equ

ipmen

t Man

ufac

turin

g

ICT Pr

oduc

tsCo

mpu

ter a

nd Co

mpu

ter P

eriph

eral

Who

lesali

ng34

92Co

mpu

ter a

nd Co

mpu

ter P

eriph

eral

Who

lesali

ng

ICT Pr

oduc

tsSo

ftwar

e Who

lesali

ngpa

rt34

92?

ICT Pr

oduc

tsTe

lecom

mun

icatio

n Goo

ds W

holes

aling

3493

Telec

omm

unica

tion G

oods

Who

lesali

ng

ICT Pr

oduc

tsCo

mpu

ter a

nd Co

mpu

ter P

eriph

eral

Reta

iling

4222

Com

pute

r and

Com

pute

r Per

ipher

al Re

tailin

g

ICT Pr

oduc

tsSo

ftwar

e Ret

ailing

part

4222

?

ICT Pr

oduc

tsSo

ftwar

e Pub

lishin

g54

20So

ftwar

e Pub

lishin

g

ICT Pr

oduc

tsCo

mpu

ter a

nd Te

lecom

mun

icatio

ns Eq

uipm

ent

Repa

ir and

Main

tena

nce

part

9422

Electr

onic

(exc

ept D

omes

tic Ap

plian

ce) a

nd Pr

ecisi

on Eq

uipm

ent

Repa

ir

ICT Se

rvice

sICT

Out

sour

cing a

nd Tr

ansa

ction

Proc

essin

g59

21Da

ta Pr

oces

sing a

nd W

eb H

ostin

g Ser

vices

ICT Se

rvice

sEle

ctron

ic In

form

ation

Stor

age S

ervic

es59

22Ele

ctron

ic In

form

ation

Stor

age S

ervic

es

ICT Se

rvice

sSy

stem

Des

ign an

d Sof

twar

e Dev

elopm

ent S

ervic

es70

00Co

mpu

ter S

yste

m D

esign

and R

elate

d Ser

vices

ICT Se

rvice

sICT

Engin

eerin

g Des

ign an

d Eng

ineer

ing Co

nsult

ing Se

rvice

spa

rt 69

23En

ginee

ring D

esign

and E

ngine

ering

Cons

ulting

Serv

ices

ICT Se

rvice

sICT

Cons

ulting

, Man

agem

ent a

nd Ed

ucat

ion S

ervic

espa

rt 69

62M

anag

emen

t Adv

ice an

d Rela

ted C

onsu

lting

Serv

ices

ICT Se

rvice

sICT

Cons

ulting

, Man

agem

ent a

nd Ed

ucat

ion S

ervic

espa

rt 82

20Ed

ucat

ional

Supp

ort S

ervic

es

A m

od

el F

or

reFo

rm o

F tH

e A

Bs A

ust

rAli

An

An

d n

eW Z

eAlA

nd

stA

nd

Ard

ind

ust

riA

lCl

Ass

iFiC

Atio

n (A

nZs

iC),

2006

– C

od

es A

nd

tit

les

AustrAliAn iCt stAtistiCAl Compendium 2011

9AustrAliAn Computer soCiety

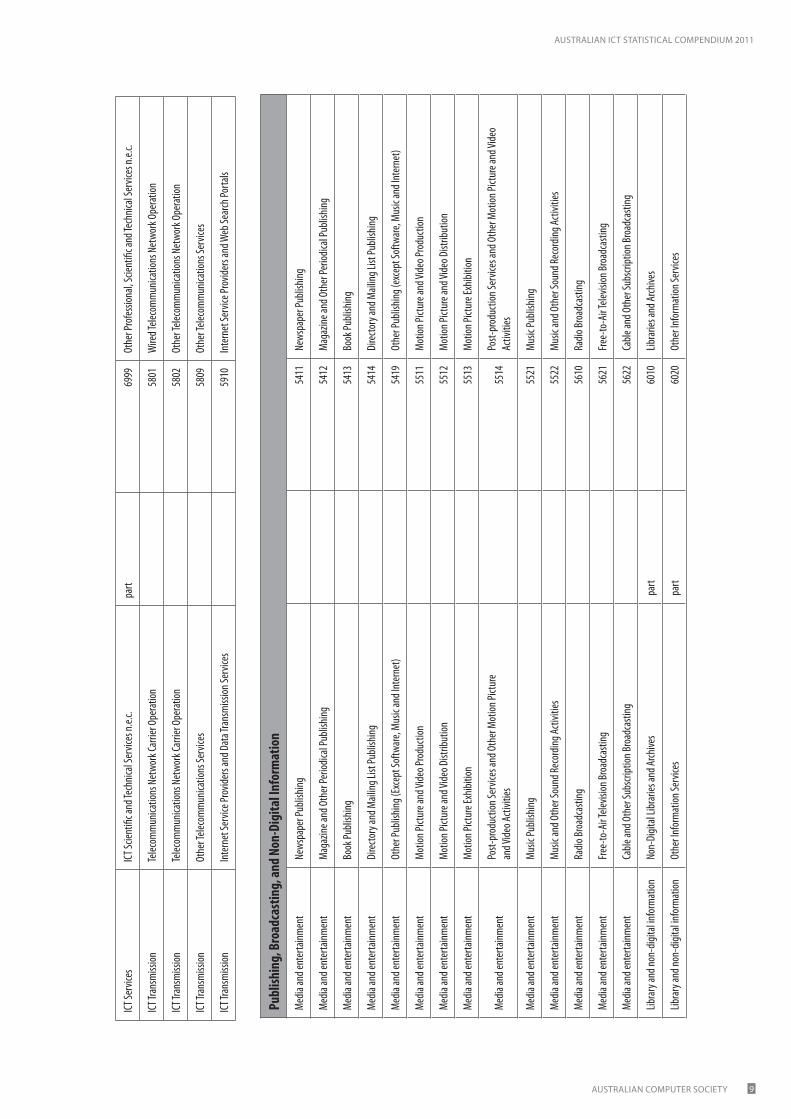

ICT Se

rvice

sICT

Scien

tific a

nd Te

chnic

al Se

rvice

s n.e.

c.pa

rt 69

99Ot

her P

rofes

siona

l, Scie

ntifi

c and

Tech

nical

Serv

ices n

.e.c.

ICT Tr

ansm

ission

Telec

omm

unica

tions

Net

work

Carri

er O

pera

tion

5801

Wire

d Tele

com

mun

icatio

ns N

etwo

rk O

pera

tion

ICT Tr

ansm

ission

Telec

omm

unica

tions

Net

work

Carri

er O

pera

tion

5802

Othe

r Tele

com

mun

icatio

ns N

etwo

rk O

pera

tion

ICT Tr

ansm

ission

Othe

r Tele

com

mun

icatio

ns Se

rvice

s58

09Ot

her T

eleco

mm

unica

tions

Serv

ices

ICT Tr

ansm

ission

Inte

rnet

Serv

ice Pr

ovide

rs an

d Dat

a Tra

nsm

ission

Serv

ices

5910

Inte

rnet

Serv

ice Pr

ovide

rs an

d Web

Sear

ch Po

rtals

Publ

ishin

g, B

road

cast

ing,

and

Non-

Digi

tal I

nfor

mat

ion

Med

ia an

d ent

erta

inmen

tNe

wspa

per P

ublis

hing

5411

News

pape

r Pub

lishin

g

Med

ia an

d ent

erta

inmen

tM

agaz

ine an

d Oth

er Pe

riodic

al Pu

blish

ing54

12M

agaz

ine an

d Oth

er Pe

riodic

al Pu

blish

ing

Med

ia an

d ent

erta

inmen

tBo

ok Pu

blish

ing54

13Bo

ok Pu

blish

ing

Med

ia an

d ent

erta

inmen

tDi

recto

ry an

d Mail

ing Li

st Pu

blish

ing54

14Di

recto

ry an

d Mail

ing Li

st Pu

blish

ing

Med

ia an

d ent

erta

inmen

tOt

her P

ublis

hing (

Exce

pt So

ftwar

e, M

usic

and I

nter

net)

5419

Othe

r Pub

lishin

g (ex

cept

Softw

are,

Mus

ic an

d Int

erne

t)

Med

ia an

d ent

erta

inmen

tM

otion

Pictu

re an

d Vide

o Pro

ducti

on55

11M

otion

Pictu

re an

d Vide

o Pro

ducti

on

Med

ia an

d ent

erta

inmen

tM

otion

Pictu

re an

d Vide

o Dist

ribut

ion55

12M

otion

Pictu

re an

d Vide

o Dist

ribut

ion

Med

ia an

d ent

erta

inmen

tM

otion

Pictu

re Ex

hibiti

on55

13M

otion

Pictu

re Ex

hibiti

on

Med

ia an

d ent

erta

inmen

tPo

st-pr

oduc

tion S

ervic

es an

d Oth

er M

otion

Pictu

re

and V

ideo A

ctivit

ies55

14Po

st-pr

oduc

tion S

ervic

es an

d Oth

er M

otion

Pictu

re an

d Vide

o Ac

tiviti

es

Med

ia an

d ent

erta

inmen

tM

usic

Publi

shing

5521

Mus

ic Pu

blish

ing

Med

ia an

d ent

erta

inmen

tM

usic

and O

ther

Soun

d Rec

ordin

g Acti

vities

5522

Mus

ic an

d Oth

er So

und R

ecor

ding A

ctivit

ies

Med

ia an

d ent

erta

inmen

tRa

dio Br

oadc

astin

g56

10Ra

dio Br

oadc

astin

g

Med

ia an

d ent

erta

inmen

tFre

e-to

-Air T

elevis

ion Br

oadc

astin

g56

21Fre

e-to

-Air T

elevis

ion Br

oadc

astin

g

Med

ia an

d ent

erta

inmen

tCa

ble an

d Oth

er Su

bscri

ption

Broa

dcas

ting

5622

Cable

and O

ther

Subs

cript

ion Br

oadc

astin

g

Libra

ry an

d non

-digi

tal in

form

ation

Non-

Digit

al Lib

rarie

s and

Arch

ives

part

6010

Libra

ries a

nd Ar

chive

s

Libra

ry an

d non

-digi

tal in

form

ation

Othe

r Inf

orm

ation

Serv

ices

part

6020

Othe

r Inf

orm

ation

Serv

ices

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety10

in 2008, according to an Australian treasury paper4 and the ABs, it was not the mining sector that “rescued” Australia from the global financial crisis, but the services sectors, with the exception of the finance and insurance sector.

prior to the current resources boom, and notwithstanding data set limitations, Australian iCt contributed more to Australia’s Gdp than the mining sector.5

iCt services represent a large proportion of the remaining services.

iCt eConomiC ContriBution

Sectoral contributions to GDP growth Sep 2008-May 2008

Source ABS 5206.0 and Treasury

-1.20%

-1.00%

-0.80%

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%Agriculture Mining Manufacturing

ICT and other servicesexcluding Finance and

Insurance Finance and Insurance Other sectors

4 The Australian economy and the global downturn – Part 2: The key quarters5 ABS ICT Satellite Account 2003, published 2006

AustrAliAn iCt stAtistiCAl Compendium 2011

11AustrAliAn Computer soCiety

in early 2011, the eminent economic analysts iBis published an industry sectoral analysis of fiscal contribution to Gross domestic product (Gdp) in 2010, derived from ABs data. Ciier reviewed this analysis, and found that (even excluding iCt manufacture, iCt

wholesaling and iCt retail, and some iCt consulting) the iCt industry sector contributes nearly 8 per cent of Australian Gdp. this was as much as the mining industry, and more than all other industry sectors, other than manufacturing, and finance and insurance.

Industry sector contribution to Australian GDP (2010)

7.74%

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00%

Finance and Insurance

Manufacturing

Mining

Ownership of Dwellings

ICT, excluding ICT manufacture, wholesale and retail

Construction

Industry taxes et al

Property & Business Services (excluding ICT)

Health/Comm Services

Government Administration

Transport

Wholesale Trade

Retail trade

Education

Agriculture

Accommodation and Restaurants

Utilities

Personal Services

Cultural and Recreational Services

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety12

6 Del

oitt

e Ac

cess

Eco

nom

ics,

“The

Con

nect

ed C

ontin

ent”

Aug

201

17 C

IIER/

ABS

2011

in A

ugus

t 20

11, d

eloi

tte

Acce

ss e

cono

mic

s re

leas

ed a

pub

licat

ion

title

d “t

he C

onne

cted

Co

ntin

ent”,

whi

ch a

ttem

pted

to a

scrib

e a

valu

e to

the

“inte

rnet

eco

nom

y”. t

hey

appl

ied

two

met

hods

, one

focu

sed

on t

he v

alue

of “

inpu

ts” (

e.g.

the

val

ue o

f sta

ff w

ages

and

ret

aine

d pr

ofits

, etc

.) an

d th

e ot

her f

ocus

ed o

n “o

utpu

ts” (

esse

ntia

lly G

dp)

.

the

repo

rt e

stim

ated

the

valu

e of

the

“inte

rnet

eco

nom

y” a

t $22

bill

ion

base

d on

inpu

ts,

larg

ely

of a

n id

entifi

ed 1

90,0

00 jo

bs, a

nd $

46.8

bill

ion

(roun

ded

up to

$50

bill

ion

for

pres

s pu

rpos

es) b

y th

e ou

tput

s m

etho

dolo

gy.

Ciie

r ac

cept

s d

eloi

tte

Acce

ss e

cono

mic

s ex

pert

ise,

and

has

use

d th

e sa

me

met

hodo

logy

to

calc

ulat

e th

e in

puts

res

ult

for

the

“dig

ital e

cono

my”

, bas

ed u

pon

Ciie

r an

d A

Bs e

mpl

oyee

da

ta, a

nd a

pplie

d th

e iB

is/C

iier

calc

ulat

ions

of G

dp

cont

ribut

ion

to t

he o

utpu

ts e

quat

ion.

the

resu

lt fo

r th

e “d

igita

l eco

nom

y” (e

ssen

tially

the

iCt

indu

stry

and

iCt

wor

kers

in o

ther

in

dust

ries)

is $

65.1

bill

ion

base

d on

inpu

ts, a

nd o

ver $

100

billi

on, b

ased

on

outp

uts.

Inpu

ts A

naly

sisIn

dust

ry Se

gmen

t“In

tern

et Em

ploy

ees”

6 In

tern

et Va

lue-

Adde

d$b

illio

nDi

gita

l Eco

nom

yEm

ploy

ees 7

Digi

tal E

cono

my

Valu

e-Ad

ded

$bill

ion

ISPs

15,00

0$4

Hard

ware

4,000

$17,6

54$0

.86

IT So

ftwar

e and

Cons

ulting

40,00

0$5

125,3

68$1

4.10

Onlin

e Inf

orm

ation

Serv

ices

4,000

$14,0

00$1

Adve

rtisin

g and

Ente

rpris

e Site

s75

,000

$675

,000

$6

Gove

rnm

ent

2,000

$22,0

00$2

e-Co

mm

erce

50,00

0$5

50,00

0$5

Telec

omm

unica

tions

/ISPs

77,96

3$8

.77

Distr

ibutio

n of H

ardw

are a

nd/o

r So

ftwar

e Pro

ducts

71,77

4$8

.07

Othe

r ICT

wor

kers

not i

nclud

ed in

Delo

itte

Acce

ss Ec

onom

ics da

ta14

0,941

Tota

l19

0,00

0$2

255

4,70

0$6

5.10

inpu

ts A

nA

lysi

s

Outp

uts A

naly

sisIn

tern

et Va

lue-

Adde

d $b

illio

nIC

T Val

ue-A

dded

$bill

ion

Perce

ntag

e of G

DP3.6

0%7.7

4%

Value

$46.8

0$1

00.62

AustrAliAn iCt stAtistiCAl Compendium 2011

13AustrAliAn Computer soCiety

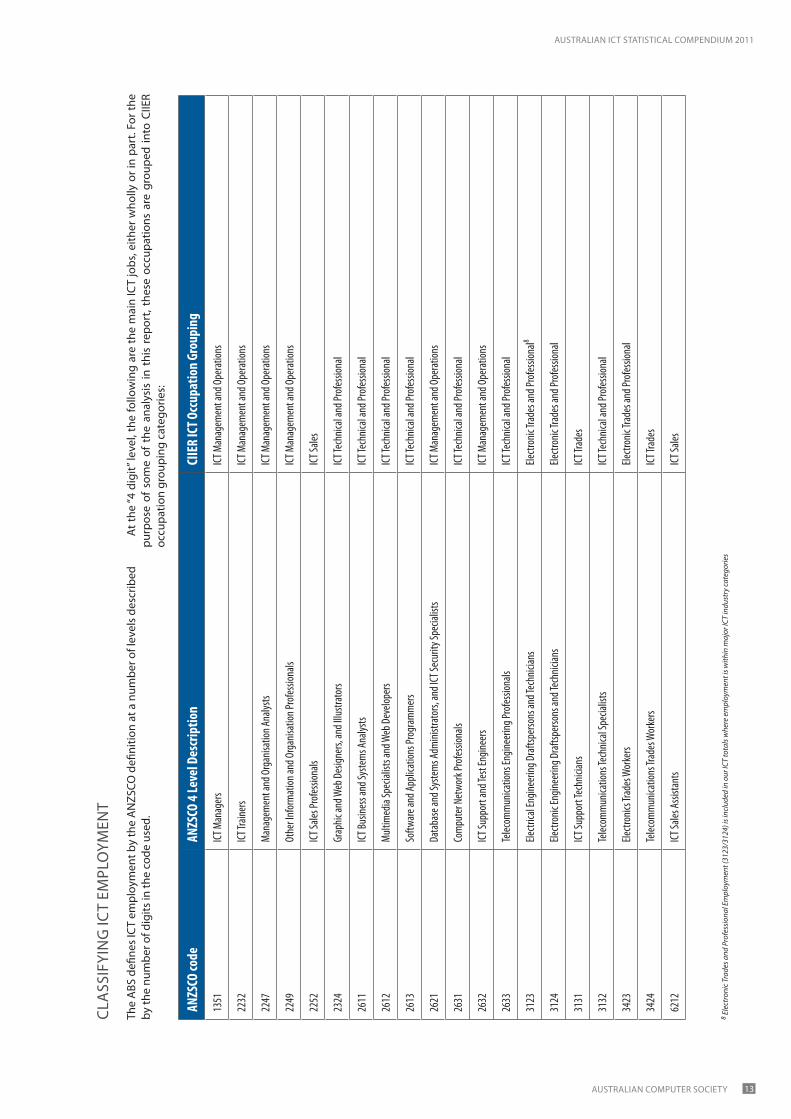

the

ABs

defi

nes

iCt

empl

oym

ent b

y th

e A

nZs

Co d

efini

tion

at a

num

ber o

f lev

els

desc

ribed

by

the

num

ber o

f dig

its in

the

code

use

d.

At t

he “4

dig

it” le

vel,

the

follo

win

g ar

e th

e m

ain

iCt

jobs

, eith

er w

holly

or i

n pa

rt. F

or th

e pu

rpos

e of

som

e of

the

ana

lysi

s in

thi

s re

port

, the

se o

ccup

atio

ns a

re g

roup

ed in

to C

iier

occu

patio

n gr

oupi

ng c

ateg

orie

s:

ClA

ssiF

yin

G iC

t em

plo

ymen

t

ANZS

CO co

deAN

ZSCO

4 Le

vel D

escr

iptio

nCI

IER

ICT O

ccup

atio

n Gr

oupi

ng

1351

ICT M

anag

ers

ICT M

anag

emen

t and

Ope

ratio

ns

2232

ICT Tr

ainer

sICT

Man

agem

ent a

nd O

pera

tions

2247

Man

agem

ent a

nd O

rgan

isatio

n Ana

lysts

ICT M

anag

emen

t and

Ope

ratio

ns

2249

Othe

r Inf

orm

ation

and O

rgan

isatio

n Pro

fessio

nals

ICT M

anag

emen

t and

Ope

ratio

ns

2252

ICT Sa

les Pr

ofes

siona

lsICT

Sales

2324

Grap

hic an

d Web

Des

igner

s, an

d Illu

strat

ors

ICT Te

chnic

al an

d Pro

fessio

nal

2611

ICT Bu

sines

s and

Syste

ms A

nalys

tsICT

Tech

nical

and P

rofes

siona

l

2612

Mult

imed

ia Sp

ecial

ists a

nd W

eb D

evelo

pers

ICT Te

chnic

al an

d Pro

fessio

nal

2613

Softw

are a

nd Ap

plica

tions

Prog

ram

mer

sICT

Tech

nical

and P

rofes

siona

l

2621

Data

base

and S

yste

ms A

dmini

strat

ors,

and I

CT Se

curit

y Spe

cialis

tsICT

Man

agem

ent a

nd O

pera

tions

2631

Com

pute

r Net

work

Prof

essio

nals

ICT Te

chnic

al an

d Pro

fessio

nal

2632

ICT Su

ppor

t and

Test

Engin

eers

ICT M

anag

emen

t and

Ope

ratio

ns

2633

Telec

omm

unica

tions

Engin

eerin

g Pro

fessio

nals

ICT Te

chnic

al an

d Pro

fessio

nal

3123

Electr

ical E

ngine

ering

Dra

ftspe

rsons

and T

echn

ician

sEle

ctron

ic Tra

des a

nd Pr

ofes

siona

l8

3124

Electr

onic

Engin

eerin

g Dra

ftspe

rsons

and T

echn

ician

sEle

ctron

ic Tra

des a

nd Pr

ofes

siona

l

3131

ICT Su

ppor

t Tec

hnici

ans

ICT Tr

ades

3132

Telec

omm

unica

tions

Tech

nical

Spec

ialist

sICT

Tech

nical

and P

rofes

siona

l

3423

Electr

onics

Trad

es W

orke

rsEle

ctron

ic Tra

des a

nd Pr

ofes

siona

l

3424

Telec

omm

unica

tions

Trad

es W

orke

rsICT

Trad

es

6212

ICT Sa

les A

ssista

nts

ICT Sa

les

8 Ele

ctro

nic

Trad

es a

nd P

rofe

ssio

nal E

mpl

oym

ent (

3123

/312

4) is

incl

uded

in o

ur IC

T to

tals

whe

re e

mpl

oym

ent i

s with

in m

ajor

ICT

indu

stry

cate

gorie

s

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety14

Who

We

Are

iCt

teCH

niC

Al

An

d p

roFe

ssio

nA

l em

plo

ymen

t

9 CIIE

R ex

trac

t fro

m A

BS la

bour

mar

ket s

tatis

tics F

eb 2

011

10 C

IIER

estim

ate

from

Top

250

ICT

Indu

stry

mod

el D

ec 2

010

11 M

ost o

f the

se o

f the

se p

eopl

e w

ork

in th

e 28

5,00

0 st

rong

ICT

indu

stry

12 E

xclu

des E

lect

roni

cs e

mpl

oym

ent o

utsi

de m

ain

ICT

indu

stry

sect

ors

ICT W

orkf

orce

, All

Indu

strie

s 9IC

T Tec

hnica

l &

Prof

essio

nal

ICT M

anag

emen

t &

Oper

atio

nsIC

T Tra

des

ICT S

ales

Elec

troni

c Tra

des

& Pr

ofes

siona

lIC

T Ind

ustr

y Adm

in

& Lo

gist

ics Su

ppor

tIC

T Wor

kers

(ACS

/CI

IER

defin

ition

)

Prof

essio

nal, S

cient

ific a

nd Te

chnic

al Se

rvice

s11

2,028

49,77

519

,085

10,20

04,5

70–

–

Info

rmat

ion M

edia

and T

eleco

mm

unica

tions

26,83

710

,820

20,59

012

,903

982

––

Tota

l of M

ain “I

CT” S

ecto

rs13

8,865

60,59

539

,675

23,10

35,5

5244

,99510

312,7

8511

Publi

c Adm

inistr

ation

and S

afety

16,54

120

,194

6,387

02,4

30–

45,55

2

Finan

cial a

nd In

sura

nce S

ervic

es16

,509

12,81

83,9

220

0–

33,24

9

Man

ufac

turin

g15

,114

8,315

3,303

401

2,872

–30

,005

Reta

il Tra

de5,0

944,5

114,3

969,1

863,7

09–

26,89

6

Educ

ation

and T

raini

ng9,3

198,4

815,2

2439

91,9

21–

25,34

4

Who

lesale

Trad

e7,0

324,4

942,6

316,1

562,9

40–

23,25

3

Cons

tructi

on2,9

382,0

145,6

240

6,802

–17

,378

Othe

r Ser

vices

4,434

2,271

1,256

411

8,911

–17

,283

Healt

hcar

e and

Socia

l Assi

stanc

e5,0

505,6

122,0

650

366

–13

,093

Trans

port,

Posta

l and

War

ehou

sing

4,042

4,011

2,212

072

1–

10,98

6

Adm

inistr

ative

and S

uppo

rt Se

rvice

s3,0

504,6

5836

550

679

9–

9,378

Electr

icity,

Gas

, Wat

er an

d Was

te Se

rvice

s1,7

543,9

6770

734

241

1–

7,181

Arts

and R

ecre

ation

Serv

ices

2,932

954

432

01,0

76–

5,394

Mini

ng1,2

221,7

301,3

300

699

–4,9

81

Rent

al, H

iring

and R

eal E

state

Serv

ices

1,253

1,152

039

749

2–

3,294

Acco

mm

odat

ion an

d Foo

d Ser

vices

588

1,286

390

00

–2,2

64

Agric

ultur

e, Fo

restr

y and

Fish

ing22

810

716

70

0–

502

235,

965

147,

170

80,0

8640

,901

39,7

0144

,995

??10

554,

66912

AustrAliAn iCt stAtistiCAl Compendium 2011

15AustrAliAn Computer soCiety

ICT

Em

ploy

men

t D

emog

raph

ics

13 E

xtra

ct fr

om A

BS la

bour

mar

ket s

tatis

tics,

Feb

2009

ANZS

CO Jo

b-ty

pe%

over

40%

over

55Gr

and T

otal

Med

ian

age

3420

Elec

tronic

s and

Telec

omm

unica

tions

Trad

es W

orke

rs nf

d10

0.00%

48.33

%1,0

4553

.54

2232

ICT T

raine

rs75

.00%

24.58

%4,7

4046

.20

3132

Telec

omm

unica

tions

Tech

nical

Spec

ialist

s87

.18%

0.00%

3,954

45.26

3124

Elec

tronic

Engin

eerin

g Dra

ftspe

rsons

and T

echn

ician

s64

.44%

23.67

%8,2

4744

.23

2247

Man

agem

ent a

nd O

rgan

isatio

n Ana

lysts

54.25

%19

.39%

50,57

641

.92

2249

Oth

er In

form

ation

and O

rgan

isatio

n Pro

fessio

nals

51.10

%15

.26%

14,37

540

.73

1351

ICT M

anag

ers

53.23

%8.2

9%43

,771

40.35

2600

ICT P

rofes

siona

ls nf

d50

.98%

15.11

%13

,372

40.21

3423

Elec

tronic

s Tra

des W

orke

rs49

.25%

12.72

%41

,025

39.31

3424

Telec

omm

unica

tions

Trad

es W

orke

rs47

.67%

6.25%

13,95

739

.12

2633

Telec

omm

unica

tions

Engin

eerin

g Pro

fessio

nals

42.41

%6.9

0%8,5

2438

.28

2611

ICT B

usine

ss an

d Sys

tem

s Ana

lysts

40.71

%7.5

1%22

,010

38.06

3131

ICT S

uppo

rt Te

chnic

ians

39.66

%11

.33%

48,37

437

.95

2632

ICT S

uppo

rt an

d Tes

t Eng

ineer

s47

.61%

1.57%

9,199

37.83

2621

Dat

abas

e and

Syste

ms A

dmini

strat

ors,

and I

CT Se

curit

y Spe

cialis

ts39

.14%

6.47%

41,81

737

.66

2252

ICT S

ales P

rofes

siona

ls38

.69%

10.33

%12

,216

37.61

2613

Softw

are a

nd Ap

plica

tions

Prog

ram

mer

s38

.19%

6.03%

74,56

537

.44

2631

Com

pute

r Net

work

Prof

essio

nals

34.06

%3.5

3%23

,629

36.40

2324

Gra

phic

and W

eb D

esign

ers,

and I

llustr

ator

s30

.77%

7.33%

48,46

036

.09

2612

Mult

imed

ia Sp

ecial

ists a

nd W

eb D

evelo

pers

20.48

%10

.10%

11,32

634

.85

6212

ICT S

ales A

ssista

nts

27.94

%7.6

0%21

,921

34.44

AG

e d

emo

GrA

pHy

oF

iCt

Wo

rKer

s13

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety16

Lear

ning

IC

TIC

T E

duca

tion

And

Tra

inin

g St

atis

tics

14

Leve

l of C

ours

e20

0820

10Va

riatio

n

Docto

rate

by Re

sear

ch35

237

220

Docto

rate

by Co

urse

work

3<

10

Mas

ter’s

by Re

sear

ch56

8832

Mas

ter’s

by Co

urse

work

5,947

5,038

-909

Postg

rad.

Qual/

Preli

m.

4<

10

Grad

.(Pos

t) Di

p. –

new

area

586

663

77

Grad

.(Pos

t) Di

p. –

ext a

rea

201

155

-46

Grad

uate

Certi

ficat

e43

448

955

Sub-

tota

l Pos

tgra

duat

e7,5

836,8

14-7

69

Bach

elor’s

Gra

duat

e Ent

ry4

0-4

Bach

elor’s

Hon

ours

6010

141

Bach

elor’s

Pass

10,77

011

,339

569

Asso

ciate

Deg

ree

5618

012

4

Adva

nced

Dipl

oma (

AQF)

9018

393

Diplo

ma (

AQF)

736

829

93

Othe

r und

ergr

adua

te aw

ard c

ourse

s63

674

Sub-

tota

l Und

ergr

adua

te11

,779

12,69

992

0

Enab

ling C

ourse

s4

139

Non-

Awar

d Cou

rses

00

0

TOTA

L19

,366

19,5

2616

0

14 D

EEW

R 20

11

Com

men

Cin

G iC

t st

ud

ents

By

leVe

l o

F Co

urs

e A

nd

Gen

der

, Fu

ll y

eAr

AustrAliAn iCt stAtistiCAl Compendium 2011

17AustrAliAn Computer soCiety

Stat

e/Pr

ovid

erIn

form

atio

n Te

chno

logy

Do

mes

tic

Tota

l Do

mes

tic (a

)

ICT

Inte

rnat

iona

l St

uden

ts

Tota

l In

tern

atio

nal

Info

rmat

ion

Tech

nolo

gy

Tota

l

TOTA

L Do

mes

tic &

In

tern

atio

nal (

a)

ICT %

of To

tal

Stud

ents

at

Prov

ider

Dom

estic

ICT %

of

Tota

l ICT

at

this

Prov

ider

New

Sout

h W

ales

Char

les St

urt U

niver

sity

404

14,55

934

82,6

6775

217

,226

4.37%

53.72

%

Inse

arch

3532

111

782

715

21,1

4813

.24%

23.03

%

Mac

quar

ie Un

iversi

ty22

98,4

5096

5,911

325

14,36

12.2

6%70

.46%

Raffl

es KV

B Ins

titut

e30

130

1314

843

278

15.47

%69

.77%

Sout

hern

Cros

s Univ

ersit

y74

4,851

691,3

4714

36,1

982.3

1%51

.75%

Sydn

ey In

stitu

te of

Busin

ess a

nd

Tech

nolog

y34

394

512,6

5985

3,053

2.78%

40.00

%

The U

niver

sity o

f New

Engla

ndnp

6,895

np61

113

47,5

061.7

9%np

The U

niver

sity o

f New

Sout

h Wale

s22

512

,763

197

6,700

422

19,46

32.1

7%53

.32%

The U

niver

sity o

f New

castl

e24

211

,741

222

2,666

464

14,40

73.2

2%52

.16%

The U

niver

sity o

f Syd

ney

234

14,86

322

35,6

5645

720

,519

2.23%

51.20

%

Unive

rsity

of Te

chno

logy,

Sydn

ey46

68,2

1540

44,3

6187

012

,576

6.92%

53.56

%

Unive

rsity

of W

este

rn Sy

dney

484

13,34

494

2,319

578

15,66

33.6

9%83

.74%

Unive

rsity

of W

ollon

gong

263

6,340

1008

4,984

1,271

11,32

411

.22%

20.69

%

Woll

ongo

ng Co

llege

Austr

alia

1023

3115

141

174

23.56

%24

.39%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts2,

811

114,

423

2,92

642

,313

5,73

715

6,73

63.

66%

49.0

0%

Com

men

Cin

G d

om

esti

C st

ud

ents

By

stAt

e, H

iGH

er e

du

CAt

ion

pro

Vid

er A

nd

Bro

Ad

Fie

ld o

F ed

uC

Atio

n, F

ull

yeA

r 20

10

NO

TE: n

p =

not p

ublis

hed/

not p

ublic

ised

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety18

Stat

e/Pr

ovid

erIn

form

atio

n Te

chno

logy

Do

mes

tic

Tota

lDo

mes

tic (a

)

ICT

Inte

rnat

iona

l St

uden

ts

Tota

l In

tern

atio

nal

Info

rmat

ion

Tech

nolo

gy

Tota

l

TOTA

LDo

mes

tic &

In

tern

atio

nal (

a)

ICT %

of To

tal

Stud

ents

at

Prov

ider

Dom

estic

ICT %

of

Tota

l ICT

at

this

Prov

ider

Vict

oria

Box H

ill In

stitu

te of

TAFE

6026

637

7197

337

28.78

%61

.86%

Deak

in Un

iversi

ty (b

)37

310

,870

193

3,801

566

14,67

13.8

6%65

.90%

La Tr

obe U

niver

sity

127

9,530

126

3,826

253

13,35

61.8

9%50

.20%

Melb

ourn

e Ins

titut

e of B

usine

ss an

d Tec

hnolo

gy30

724

139

1,740

169

2,464

6.86%

17.75

%

Melb

ourn

e Ins

titut

e of T

echn

ology

np18

8np

359

183

547

33.46

%np

Mon

ash C

olleg

e Gro

up10

7547

1,220

571,2

954.4

0%17

.54%

Mon

ash U

niver

sity

514

13,78

669

08,1

181,2

0421

,904

5.50%

42.69

%

RMIT

Unive

rsity

620

9,122

1043

10,49

31,6

6319

,615

8.48%

37.28

%

Swinb

urne

Univ

ersit

y of

Tech

nolog

y34

45,5

3644

23,6

1078

69,1

468.5

9%43

.77%

The U

niver

sity o

f Melb

ourn

e29

11,74

779

4,466

108

16,21

30.6

7%26

.85%

Unive

rsity

of Ba

llara

tnp

2,570

np2,6

2868

95,1

9813

.26%

np

Victo

ria U

niver

sity

131

6,645

389

2,900

520

9,545

5.45%

25.19

%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts2,

382

73,3

853,

913

46,1

956,

295

119,

580

5.26

%37

.84%

Com

men

Cin

G d

om

esti

C st

ud

ents

By

stAt

e, H

iGH

er e

du

CAt

ion

pro

Vid

er A

nd

Bro

Ad

Fie

ld o

F ed

uC

Atio

n, F

ull

yeA

r 20

10

AustrAliAn iCt stAtistiCAl Compendium 2011

19AustrAliAn Computer soCiety

Stat

e/Pr

ovid

erIn

form

atio

n Te

chno

logy

Do

mes

tic

Tota

lDo

mes

tic (a

)

ICT

Inte

rnat

iona

l St

uden

ts

Tota

l In

tern

atio

nal

Info

rmat

ion

Tech

nolo

gy

Tota

l

TOTA

LDo

mes

tic &

Inte

rnat

iona

l (a)

ICT %

of To

tal

Stud

ents

at

Prov

ider

Dom

estic

ICT %

of

Tota

l ICT

at

this

Prov

ider

Quee

nsla

nd

Bond

Univ

ersit

y33

1,622

321,8

4365

3,465

1.88%

50.77

%

Cent

ral Q

ueen

sland

Univ

ersit

y17

55,9

1372

53,9

7090

09,8

839.1

1%19

.44%

Griffi

th U

niver

sity

247

12,32

515

25,8

9539

918

,220

2.19%

61.90

%

Jam

es Co

ok U

niver

sity

120

5,100

225

2,577

345

7,677

4.49%

34.78

%

Quee

nslan

d Ins

titut

e of B

usine

ss an

d Tec

hnolo

gy27

230

391,2

3066

1,460

4.52%

40.91

%

Quee

nslan

d Univ

ersit

y of

Tech

nolog

y66

612

,723

323

3,319

989

16,04

26.1

7%67

.34%

The U

niver

sity o

f Que

ensla

nd22

611

,158

155

5,039

381

16,19

72.3

5%59

.32%

Unive

rsity

of So

uthe

rn Q

ueen

sland

139

8,045

224

2,812

363

10,85

73.3

4%38

.29%

Unive

rsity

of th

e Sun

shine

Coas

t56

3,564

497

460

4,538

1.32%

93.33

%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts1,

689

62,9

111,

879

27,6

973,

568

90,6

083.

94%

47.3

4%

Com

men

Cin

G d

om

esti

C st

ud

ents

By

stAt

e, H

iGH

er e

du

CAt

ion

pro

Vid

er A

nd

Bro

Ad

Fie

ld o

F ed

uC

Atio

n, F

ull

yeA

r 20

10

Wes

tern

Aus

tral

ia

Curti

n Int

erna

tiona

l Coll

ege

1010

528

1213

381,3

182.8

8%26

.32%

Curti

n Univ

ersit

y of T

echn

ology

215

10,07

120

275

0841

717

,579

2.37%

51.56

%

Edith

Cowa

n Univ

ersit

y28

29,4

2332

627

1460

812

,137

5.01%

46.38

%

Mur

doch

Univ

ersit

y13

24,5

4413

120

6526

36,6

093.9

8%50

.19%

Perth

Insti

tute

of Bu

sines

s and

Te

chno

logy

1041

2048

230

523

5.74%

33.33

%

The U

niver

sity o

f Wes

tern

Austr

alia

104

5,831

5718

5816

17,6

892.0

9%64

.60%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts73

933

,513

778

16,2

241,

517

49,7

373.

05%

48.7

1%

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety20

Stat

e/Pr

ovid

erIn

form

atio

n Te

chno

logy

Do

mes

tic

Tota

lDo

mes

tic (a

)

ICT

Inte

rnat

iona

l St

uden

ts

Tota

l In

tern

atio

nal

Info

rmat

ion

Tech

nolo

gy

Tota

l

TOTA

LDo

mes

tic &

In

tern

atio

nal (

a)

ICT %

of to

tal

Stud

ents

at

Prov

ider

Dom

estic

ICT %

of

Tota

l ICT

at

this

Prov

ider

Sout

h Au

stra

lia

Carn

egie

Mell

on U

niver

sity

1010

1444

2454

44.44

%41

.67%

Educ

ation

al En

terp

rises

Austr

alia

Pty L

td10

1214

322

2433

47.1

9%41

.67%

Sout

h Aus

tralia

n Ins

titut

e of

Busin

ess a

nd Te

chno

logy

1717

233

526

5069

87.1

6%34

.00%

The F

linde

rs Un

iversi

ty

110

6,178

411,5

9215

17,7

701.9

4%72

.85%

The U

niver

sity o

f Ade

laide

606,0

9315

02,9

6721

09,0

602.3

2%28

.57%

Unive

rsity

of So

uth A

ustra

lia30

48,5

4891

4,270

395

12,81

83.0

8%76

.96%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts49

421

,644

360

10,1

3885

431

,782

2.69

%57

.85%

Com

men

Cin

G d

om

esti

C st

ud

ents

By

stAt

e, H

iGH

er e

du

CAt

ion

pro

Vid

er A

nd

Bro

Ad

Fie

ld o

F ed

uC

Atio

n, F

ull

yeA

r 20

10

Tasm

ania

Unive

rsity

of Ta

sman

ia20

68,5

7258

62,7

0579

211

,277

7.02%

26.01

%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts20

68,

621

586

2,70

679

211

,327

6.99

%26

.01%

Nort

hern

Terri

tory

Char

les D

arwi

n Univ

ersit

y40

3,474

2829

768

3,771

1.80%

58.82

%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts40

3,66

428

297

683,

961

1.72

%58

.82%

AustrAliAn iCt stAtistiCAl Compendium 2011

21AustrAliAn Computer soCiety

Stat

e/Pr

ovid

erIn

form

atio

n Te

chno

logy

Do

mes

tic

Tota

l Do

mes

tic(a

)

ICT

Inte

rnat

iona

l St

uden

ts

Tota

l In

tern

atio

nal

Info

rmat

ion

Tech

nolo

gy

Tota

l

TOTA

L Do

mes

tic &

In

tern

atio

nal(a

)

ICT %

of To

tal

Stud

ents

at

Prov

ider

Dom

estic

ICT %

of

Tota

l ICT

at

this

Prov

ider

Aust

ralia

n Ca

pita

l Ter

ritor

y

Canb

erra

Insti

tute

of Te

chno

logy

1554

00

1554

27.78

%10

0.00%

The A

ustra

lian N

ation

al Un

iversi

ty90

4,931

942,3

2518

47,2

562.5

4%48

.91%

Unive

rsity

of Ca

nber

ra19

95,0

7923

31,8

2343

26,9

026.2

6%46

.06%

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

ts30

410

,064

327

4,14

863

114

,212

4.44

%48

.18%

Aust

ralia

n To

tal

2010

8,704

336,3

7110

,822

151,5

4619

,526

487,9

174.0

0%44

.58%

2009

8,328

315,9

6812

,243

154,5

6920

,571

470,5

374.3

7%40

.48%

2008

7,470

288,2

2811

,896

141,1

3119

,366

429,3

594.5

1%38

.57%

2007

7,839

281,6

2510

,384

126,7

0918

,223

408,3

344.4

6%43

.02%

2006

8,198

270,2

3610

,087

111,4

6318

,285

381,6

994.7

9%44

.83%

tota

l iC

t hi

gher

edu

catio

n co

mm

ence

men

ts h

ave

decl

ined

to 2

008

leve

ls, b

ut w

ith a

hig

her p

ropo

rtio

n of

dom

estic

stu

dent

s, al

mos

t to

2006

leve

ls.

iCt

com

men

cem

ents

con

tinue

d to

de

clin

e in

200

9 –

as a

per

cent

age

of to

tal s

tude

nts,

to 4

per

cen

t of t

he to

tal s

tude

nt b

ody.

Com

men

Cin

G d

om

esti

C st

ud

ents

By

stAt

e, H

iGH

er e

du

CAt

ion

pro

Vid

er A

nd

Bro

Ad

Fie

ld o

F ed

uC

Atio

n, F

ull

yeA

r 20

10

Mul

ti-St

ate

Stat

e Sub

-Tota

l, In

cludi

ng

Inst

itutio

ns W

ithou

t ICT

Co

mm

ence

men

tsnp

8,14

61,

828

649,

974

0.64

%np

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety22

C

omm

enci

ng IC

T st

uden

ts in

Hig

her E

duca

tion,

200

6-20

10

0

5000

10,0

00

15,0

00

20,0

00

25,0

00

2006

2007

2008

2009

2010

Dom

estic

ICT

stud

ent c

omm

ence

men

ts

Inte

rnat

iona

l IC

T st

uden

t com

men

cem

ents

Tota

l IC

T st

uden

t com

men

cem

ents

AustrAliAn iCt stAtistiCAl Compendium 2011

23AustrAliAn Computer soCiety

C

omm

enci

ng IC

T st

uden

t per

cent

ages

200

6-20

10

ICT

% o

f all

dom

estic

stu

dent

s,

2.59

%

ICT

% o

f all

stud

ents

, 4.0

0%

0.00

%

1.00

%

2.00

%

3.00

%

4.00

%

5.00

%

6.00

%

2006

2007

2008

2009

2010

ICT

% o

f all

dom

estic

stu

dent

s

ICT

% o

f all

stud

ents

AustrAliAn iCt stAtistiCAl Compendium 2011

AustrAliAn Computer soCiety24

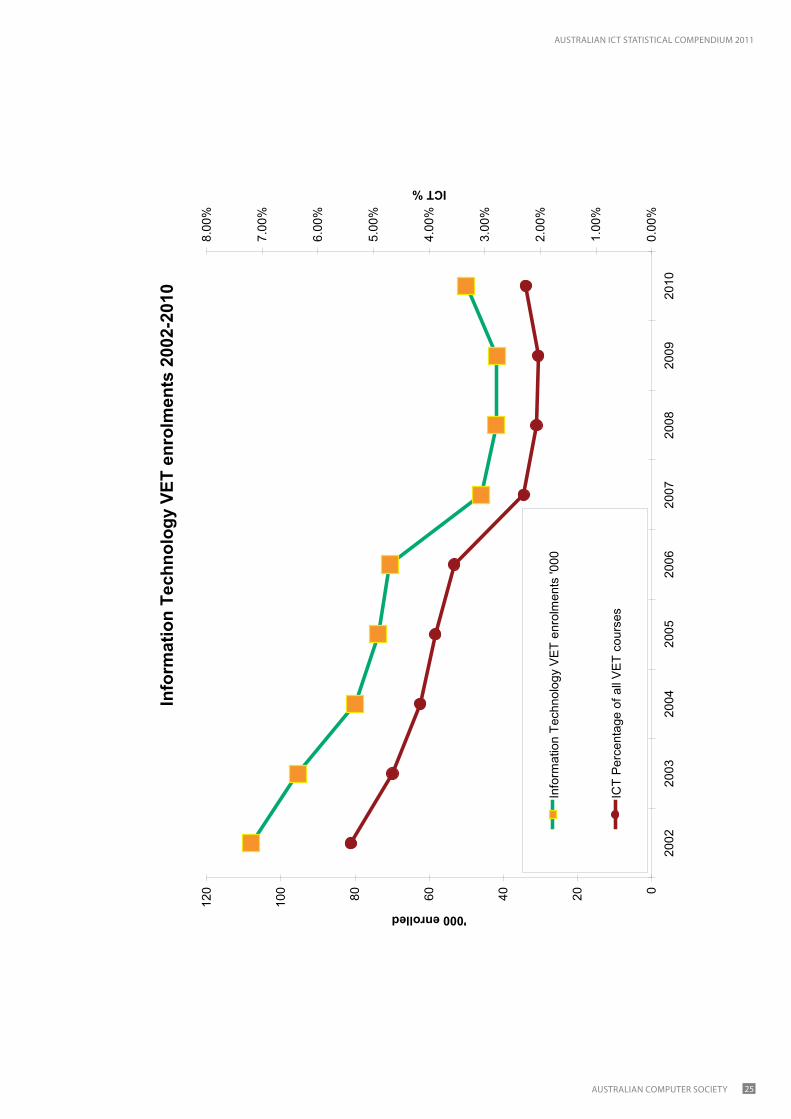

Voca

tion

al E

duca

tion

& T

rain

ing

(VE

T)

20

0220

0320

0420

0520

0620

0720

0820

0920

10

ICA –

Info

rmat

ion an

d Com

mun

icatio

ns Te

chno

logy E

nrolm

ents

(ICA Q

ualifi

catio

ns in

this

Cont

ext R

elate

to IT

Skills

)60

,282

63,76

955

,284

52,10

354

,855

50,02

749

,066

47,22

544

,197

ICT –

Telec

omm

unica

tions

Enro

lmen

ts

(ICT Q

ualifi

catio

ns in

this

Cont

ext R

elate

to Te

lecom

mun

icatio

ns Sk

ills)

12,53

812

,336

10,52

69,9

759,8

8710

,694

12,52

35,5

511,8

81

Tota

l of t

hese

Qua

lifica

tions

74,8

2278

,108

67,8

1464

,083

66,7

4862

,728

63,5

9752

,776

46,0

78

20

02(‘0

00)

2003

(‘000

)20

04(‘0

00)

2005

(‘000

)20

06(‘0

00)

2007

(‘000

)20

08(‘0

00)

2009

(‘000

)20

10(‘0

00)

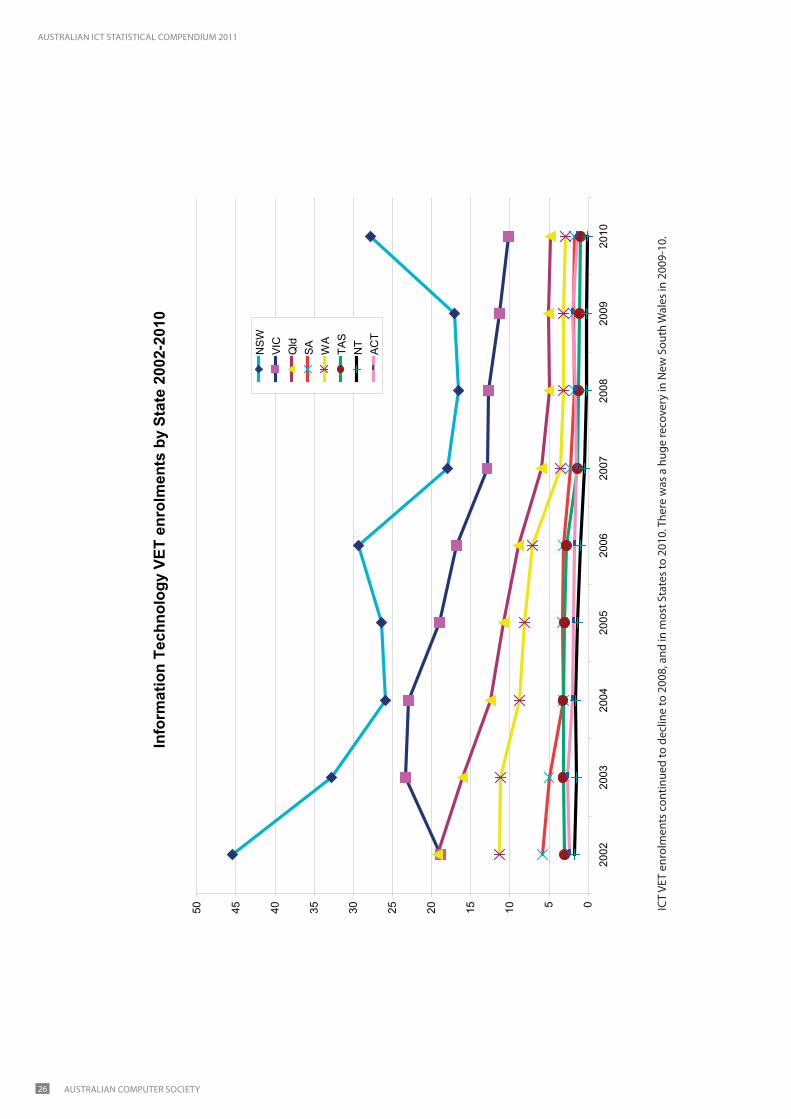

New

Sout

h Wale

s45

.532

.825

.926

.429

.318

.016

.517

.127

.8

Victo

ria18

.923

.322

.919

.016

.812

.912

.711

.310

.2

Quee

nslan

d19

.216

.012

.510

.88.9

6.05

5.14.8

Sout

h Aus

tralia

5.85.0

3.23.3

3.12.3

1.81.9

1.8

Wes

tern

Austr

alia

11.3

11.2

8.88.1

7.13.5

3.13.2

2.9

Tasm

ania

3.03.2

3.23.0

2.81.3

1.21.1

1

North

ern T

errit

ory

1.71.5

1.61.3

1.00.4

0.20.2

0.1

Austr

alian

Capit

al Te

rrito

ry2.4

2.62.0

1.91.7

1.51.6

21.4

Austr

alia

108.0

95.5

80.0

73.8

70.6

45.9

4241

.850

Austr

alia A

ll Cou

rses

1995

.520

50.1

1923

.019

00.0

1988

.819

93.8

2031

2044

.722

14.2

ICT Pe

rcent

age

5.41%

4.66%

4.16%

3.89%

3.55%

2.30%

2.07%

2.04%

2.26%

nCV

er n

ote

that

this

dat

a is

lim

ited

to p

ublic

ly fu

nded

Vet

act

ivity

. the

priv

ate

Vet

trai

ning

mar

ket i

s al

so s

ubst

antia

l. n

CVer

indi

cate

d in

200

5 th

at it

was

app

roxi

mat

ely

the

sam

e si

ze a

s th

e pu

blic

ly fu

nded

Vet

mar

ket.

the

qual

ifica

tions

dat

a is

lim

ited

to th

ose

trai

ning

pac

kage

qua

lifica

tions

with

in th

e iC

A a

nd iC

t tr

aini

ng p

acka

ges.

in a

dditi

on to

the

liste

d qu

alifi

catio

ns a

la

rge

num

ber o

f stu

dent

s un

dert

ake

Vet

with

no

inte

ntio

n of

ach

ievi

ng a

qua

lifica

tion,

just

to s

tudy

par

t of a

qua

lifica

tion,

ther

efor

e th

ere

are

man

y ‘su

bjec

t onl

y’ s

tude

nts

who

may

mee

t th

e iC

t pr

ofile

, but

as

they

are

not

list

ed a

s be

ing

enro

lled

in a

qua

lifica

tion

they

are

not

refle

cted

in th

e en

rolm

ents

dat

a. A

dditi

onal

ly, m

any

Vet

stud

ents

und

erta

ke n

on-t

rain

ing

pack

age

qual

ifica

tions

(e.g

. nat

iona

lly o

r loc

ally

end

orse

d qu

alifi

catio

ns);

som

e of

thes

e m

ay b

e iC

t qu

alifi

catio

ns. e

nrol

men

ts in

clud

e al

l tho

se e

nrol

men

ts w

ithin

a g

iven

yea

r; bo

th c

omm

enci

ng

and

cont

inui

ng s

tude

nts.

spec

ific

qual

ifica

tion

data

whe

n m

easu

red

over

tim

e sh

ould

be

trea

ted

with

car

e as

qua

lifica

tions

tend

to ta

ke a

few

yea

rs to

bec

ome

wid

ely

adop

ted,

and

are

gr

adua

lly p

hase

d ou

t onc

e th

ey a

re s

uper

sede

d.

15 H

isto

rical

tim

e se