46

Austrian models of housing finance and subsidy Astrid Kratschmann Erste Bank AG - s Bausparkasse Bukarest, 11 th October 2006

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | roderick-parker |

| View: | 217 times |

| Download: | 1 times |

Austrian models of housing finance and subsidy

Astrid KratschmannErste Bank AG - s Bausparkasse

Bukarest, 11th October 2006

EB grows home market to 120 million people

Clients: 0.3m; ~#9Retail deposits: 2%Branches: 66

Clients: 2.5m; #1Retail deposits: 32%Branches: 300

Clients: 0.9m; #2Retail deposits: 6%Branches: 171

Clients: 2.8m; #1Retail deposits: 34%Branches: 381

Clients: 5.3m; #1Retail deposits: 33%Branches: 637

Clients: 0.6m; # 2Retail deposits (inc. SBs): 21%Branches: - „Own“ :142 - Subsidiaries: 134

Clients: 0.6m; #3Retail deposits: 11%Branches: 124

Clients: 2.2mBranches: 711

Bank Prestige Founded in Dec 2005

The Ukraine further strengthens EB’s long-term growth prospects

4 core strategies

1. Focus on core business potential

2. Building a strong joint brand with the Austrian savings banks

3. Targeting a home market of 120 million people in Central Europe

4. Transferring the multi-channel distribution model throughout Central Europe

Astrid KratschmannHead “Housing CEE affairs”

integration of Erste Bank business policy „housing & real estate finance“ in the CE subsidiaries and Austrian savings banks

know how transfer within Erste Bank Group attendance of Austrian customers in

expanding their business to CE partner for CE subsidiaries and Austrian

savings banks in all questions of „housing finance“, especially large scale mortgages

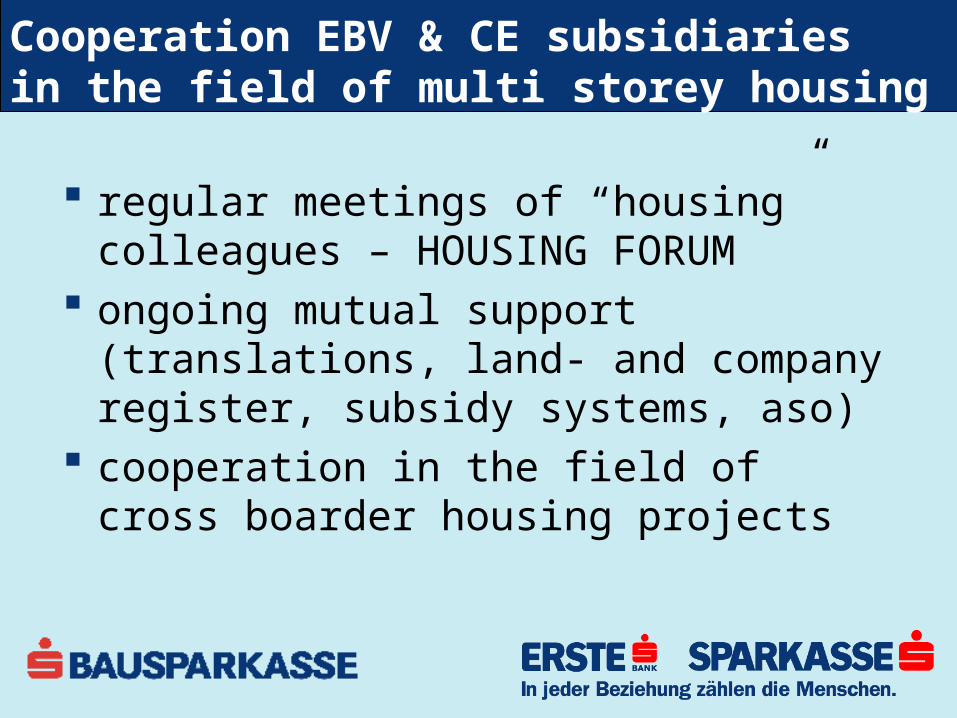

regular meetings of “housing” colleagues – HOUSING FORUM

ongoing mutual support (translations, land- and company register, subsidy systems, aso)

cooperation in the field of cross boarder housing projects

Cooperation EBV & CE subsidiariesin the field of multi storey housing

Agenda

TOP 2

TOP 3

TOP 4

role of communities

TOP 1

housing policy in Austria

living in selected CEE countries

TOP 5 excursion I: the Austrian “Wohnbauanleihe”

housing aspects

TOP 6 excursion II: building societies’ housing loans

TOP 7

TOP 8

excursion III: real estate securities

contact

political aspects of housing

living = basic need basis for social peace crucial for trust in social policy

initiatives economic importance of building and

real estate economy (7 % of GDP in Austria, 6 % in Romania)

reasons for state involvement Property is not optionally augmentable high and long term amounts to be invested

sustainable affordability regional aspects (private investors would not invest in

unattractive regions) interference with transport policy (people switch to

owner occupied homes) environmental policy (40 % of energy for heating) employment effects (1 bn € building volume initiates

21.000 jobs) 8,2 % of EU labour force are directly occupied in the

building industry, high employment density of housing

fundraising for housing

private capital/personal contribution (home owners)

5-10 % on rented flats 10 – 15 % on condominiums Up to 50 % on homes

free capital market about 50 – 80 % of total costs

public funds/public authorities About 20 % of total costs – at the beginning of 20th century

up to 100 %

Agenda

TOP 2

TOP 3

TOP 4

role of communities

TOP 1

living in selected CEE countries

TOP 5 excursion I: the Austrian “Wohnbauanleihe”

housing aspects

TOP 6 excursion II. building societies’ housing loans

TOP 7

TOP 8

excursion III: real estate securities

contact

housing policy in Austria

potential objectives of housing policy

adequate supply with dwellingsnew construction, in regions, refurbishment, price categories,…

raise of quality refurbishment, ecological measures, energy saving, accessible

for disabled persons economic and employment policy regional policy aspects environmental policy property and distributional policy

subsidy system I

object subsidy long term public loans interest subsidies / annuity subsidies/

contribution to construction costs (limitation of cost components)

liabilities/guarantees subject subsidy

equity surrogate loans rent support

subsidy system IIindirect subsidies

liabilities/guarantees

tax concessions

housing development by state

institutionalisation of housing development (non profit

housing providers)

right-to-buy for tenants

capital allocation measures

land procurement and -zoning

housing institutions

subsidy processing by Federal States housing developers, investors

– limited profit housing companies(3rd sector)

– commercial housing developers

– institutional investors (insurance companies, pension funds, real estate investment funds)

banks, savings and loan associations, mortgage (housing) banks

legal framework I

rent regulations (tenancy law, non profit housing developer law, subsidy and fundraising regulation,…)

residence property law

clear regulation of maintenance

subsidy laws

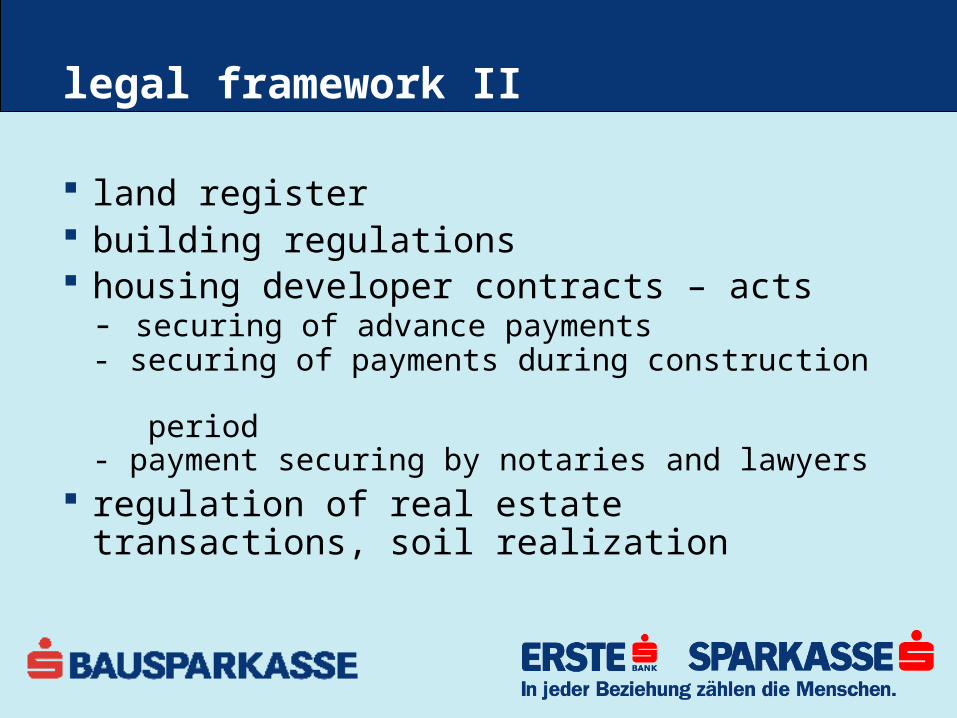

legal framework II

land register building regulations housing developer contracts – acts

- securing of advance payments- securing of payments during construction period- payment securing by notaries and lawyers

regulation of real estate transactions, soil realization

success components of the Austrian housing finance system fund raisers and housing institutions form a

risk community and are interdependent

they have always known this and thus been acting in a correspondent and mutual way

housing policy = economic policy, only indirectly social policy

the subsidy system has been developed to the respective framework of all housing institutions

housing policy has always been prepared to adapt legal framework to the partner´s economic prerequisites and possibilities

crucial points of a housing concept

different instruments in parallel definition of clear priorities attention to execution of subsidy

instruments creating a short-, mid- and long-term

concept (seeking for a broad political consensus)

Agenda

TOP 2

TOP 3

TOP 4

TOP 1

housing policy in Austria

living in selected CEE countries

TOP 5 excursion I: the Austrian “Wohnbauanleihe”

housing aspects

TOP 6 excursion II: building societies’ housing loans

TOP 7

TOP 8

excursion III: real estate securities

contact

role of communities

role of municipalities/communities– example city of Vienna

fundraising („Wohnbausteuer“, housing tax 1923)

municipal housing (development and maintenance)

direct investment in (ltd. profit) housing developers

land procurement (prevention of real estate speculation) Wohnfonds Wien

concepts of urban development

Agenda

TOP 2

TOP 3

TOP 4

role of communities

TOP 1

housing policy in Austria

TOP 5 excursion I: the Austrian “Wohnbauanleihe”

housing aspects

TOP 6 excursion II: building societies’ housing loans

TOP 7

TOP 8

excursion III: real estate securities

contact

living in selected CEE countries

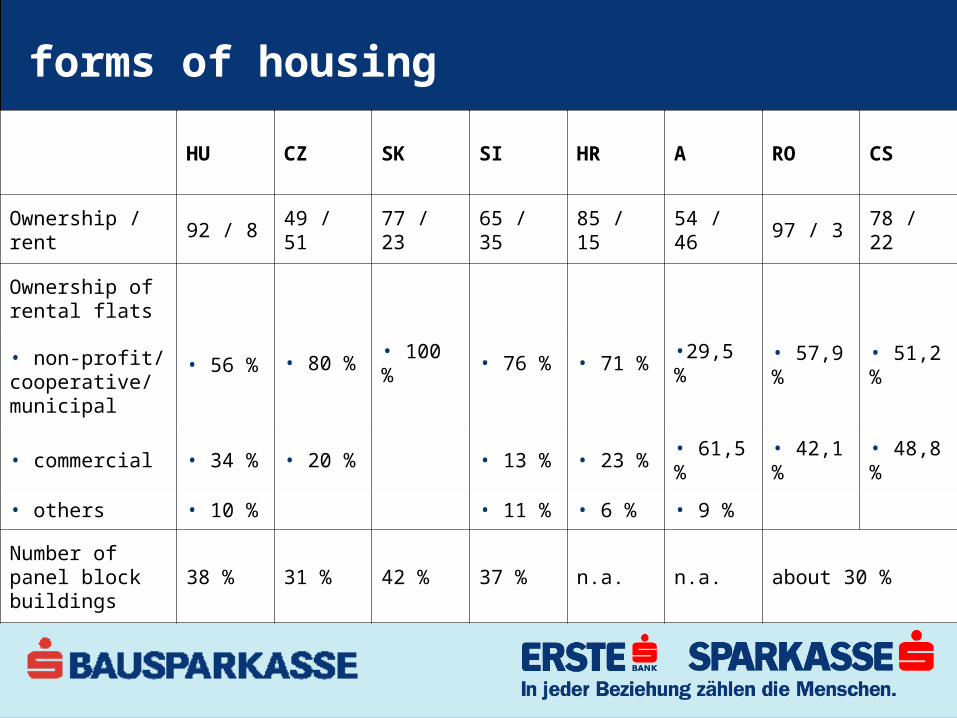

forms of housing

HU CZ SK SI HR A RO CS

Ownership / rent 92 / 8 49 / 51 77 / 23 65 / 35 85 / 15 54 / 46 97 / 3 78 / 22

Ownership of rental flats

• non-profit/ cooperative/ municipal

• 56 % • 80 % • 100 % • 76 % • 71 % •29,5 % • 57,9 % • 51,2 %

• commercial • 34 % • 20 % • 13 % • 23 % • 61,5 % • 42,1 % • 48,8 %

• others • 10 % • 11 % • 6 % • 9 %

Number of panel block buildings

38 % 31 % 42 % 37 % n.a. n.a. about 30 %

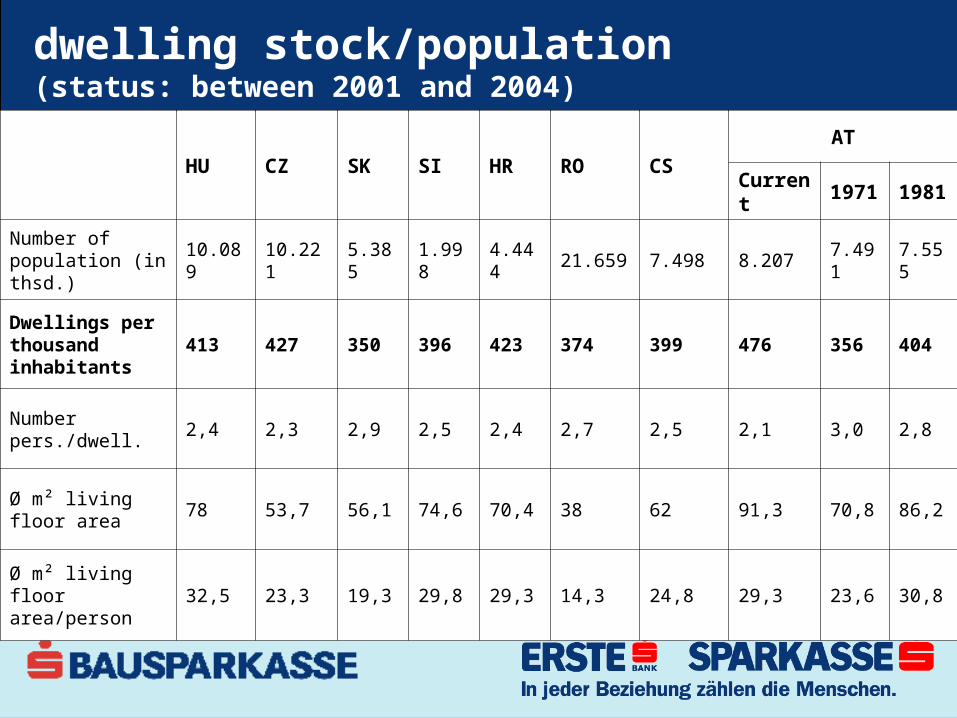

dwelling stock/population (status: between 2001 and 2004)

HU CZ SK SI HR RO CSAT

Current 1971 1981

Number of population (in thsd.)

10.089 10.221 5.385 1.998 4.444 21.659 7.498 8.207 7.491 7.555

Dwellings per thousand inhabitants

413 427 350 396 423 374 399 476 356 404

Number pers./dwell.

2,4 2,3 2,9 2,5 2,4 2,7 2,5 2,1 3,0 2,8

Ø m² living floor area

78 53,7 56,1 74,6 70,4 38 62 91,3 70,8 86,2

Ø m² living floor area/person

32,5 23,3 19,3 29,8 29,3 14,3 24,8 29,3 23,6 30,8

necessary construction to achieve EU-15 level

HU CZ SK SI HR RO CSEU-15

Number of dwellings per thousand inhabitants

413 427 350 396 423 374 399 450

Additional number of flats to achieve EU-15 level

373.626 235.083 538.500 107.892 119.9881,646.084

382.398

New dwellings construction

41.084

(05)

32.863

(05)

14.863

(05)

7.516

(05)

19.995

(05)

30.127

(04)

16.351

(04)

Achievement of EU- Ø if new construction remains constant

9,1 years

7,2 years

36,2 years

14,4 years

6,0 years

54,6 years

23,4 years

In relation to new construction - achieve EU-level in 10 years

- - 362 % 144 % - 546 % 234 %

ratio construction costs and incomeHU CZ SK SI HR AT RO CS

Ø construction cost per m² living floor area in EUR

500,-- 625,-- 500,-- 800,-- 650,-- 1.400,-- 1.000,- 950,--

Ø construction cost per dwelling in EUR

35.000,-

(70 m²)

43.750,-

(70 m²)

35.000,-

(70 m²)

56.000,-

(70 m²)

45.500,-

(70 m²)

126.000,-

(90 m²)

70.000

(70 m²)

66.500,-

(70 m²)

Ø monthly gross wage, in EUR

600,-- 673,-- 482,-- 1.212,-- 824,-- 2.302,-- 276,-- 212,--

Construction cost : annual income

4,9 5,4 6,1 3,9 4,6 4,6 21,1 26,1

ratio purchase price and GDPHU CZ SK SI HR AT RO CS

GDP per capita in EUR

8.697 9.888 6.927 13.700 6.752 30.031 3.662 2.434

Ø purchase price, new construction in capital city (EUR)

80.500

(70 m²)

120.680

(70 m²)

112.000

(70 m²)

119.000

(70 m²)

119.000

(70 m²)

324.000

(90 m²)

140.000

(70 m²

84.000

(70 m²)

Ø purchase price : GDP per capita

9,26 12,2 16,17 8,69 17,62 10,79 38,23 34,51

finished dwellings since 1990Number of finished dwellings

comparison Austria - selected CEE-countries

0

10

20

30

40

50

60

70

1990 1992 1994 1996 1998 2000 2002 2004year

nu

mb

er

of d

we

llin

gs

in th

ou

san

d

AT (data 2003 estimated by WIFO) CZ SK HU SI HR RO CS

Agenda

TOP 2

TOP 3

TOP 4

role of communities

TOP 1

housing policy in Austria

living in selected CEE countries

TOP 5

housing aspects

TOP 6 excursion II: building societies’ housing loans

TOP 7

TOP 8

excursion III: real estate securities

contact

excursion I: the Austrian “Wohnbauanleihe”

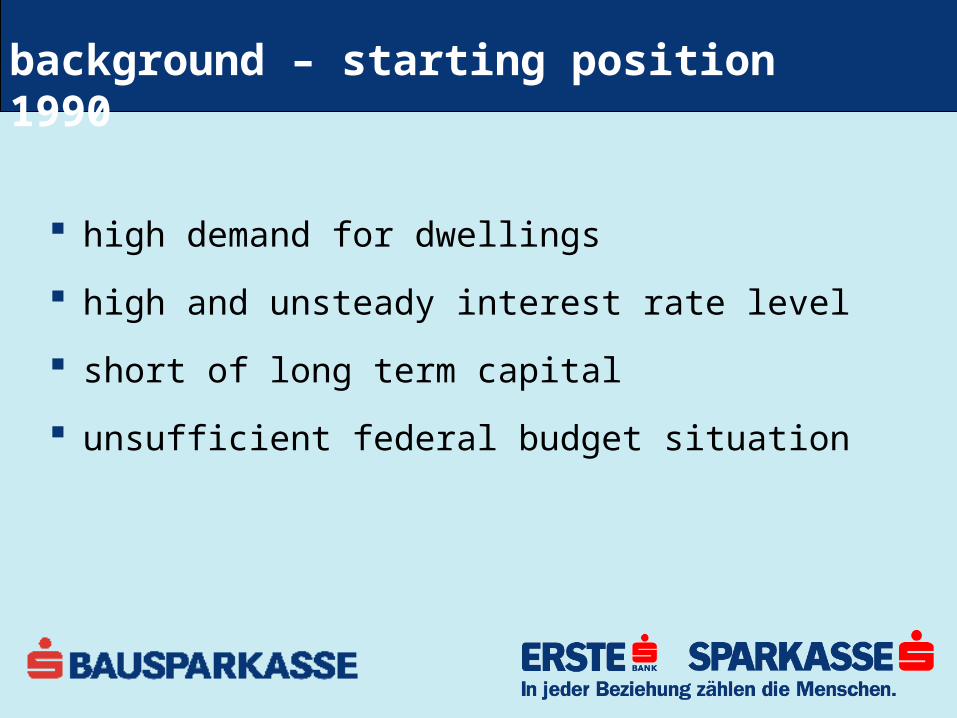

background – starting position 1990

high demand for dwellings

high and unsteady interest rate level

short of long term capital

unsufficient federal budget situation

capital market direction measures

term transformation

capital allocation for housing measures

capital allocation in the inland

incentives for private investors interesting yield return

tax concessions safety of investment

by earmarking of funds for housing purposes providing surety by means of mortgages consumer protection measures for issuing securities right of issuing only for special banks and housing developers with state licence

qualification as measure of provision

surety by mortgages product with current revenues from real estates

tax concessions

capital gains tax exemption (25 %) up to 4 % interest rate 4 % accord to 5,33 % alternative investment

purchase of mortgage bonds is deductible as special expense in assessing income tax

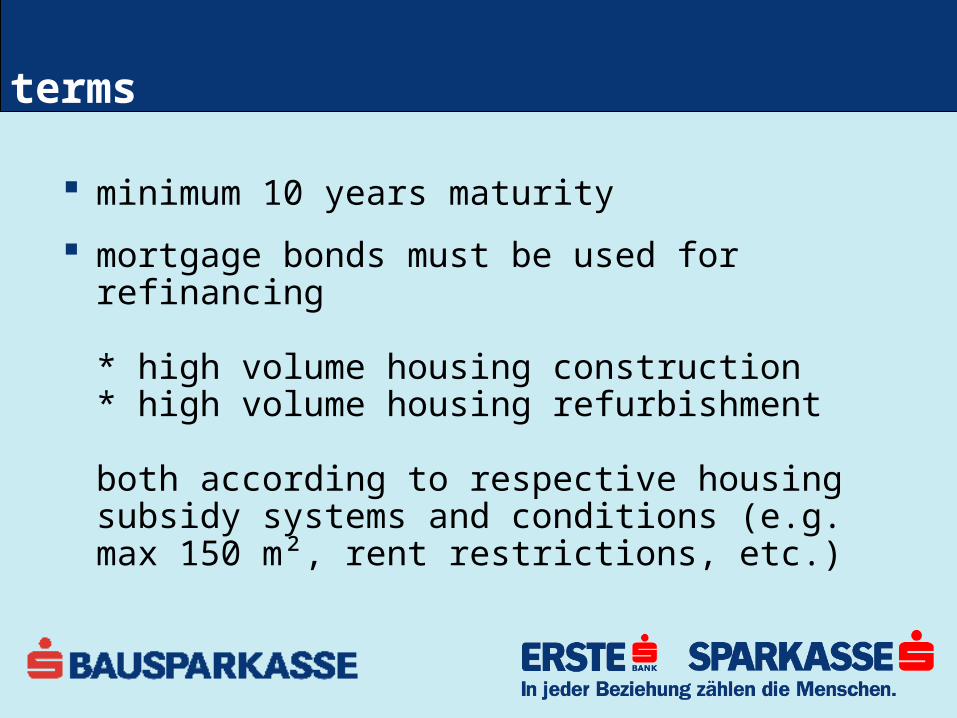

terms

minimum 10 years maturity

mortgage bonds must be used for refinancing

* high volume housing construction* high volume housing refurbishment

both according to respective housing subsidy systems and conditions (e.g. max 150 m², rent restrictions, etc.)

market Iannual issues "Wohnbaubanken"

-

200,00

400,00

600,00

800,00

1.000,00

1.200,00

1.400,00

1.600,00

1.800,00

2.000,00

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

year

in m

n EU

R

market II

issues "Wohnbauanleihen from 1994-2005

37%

9%23%

5%

11%

15%

BACA

Bawag

Hypo

Immo-Bank

Raiff eisen

s Wohnbaubank

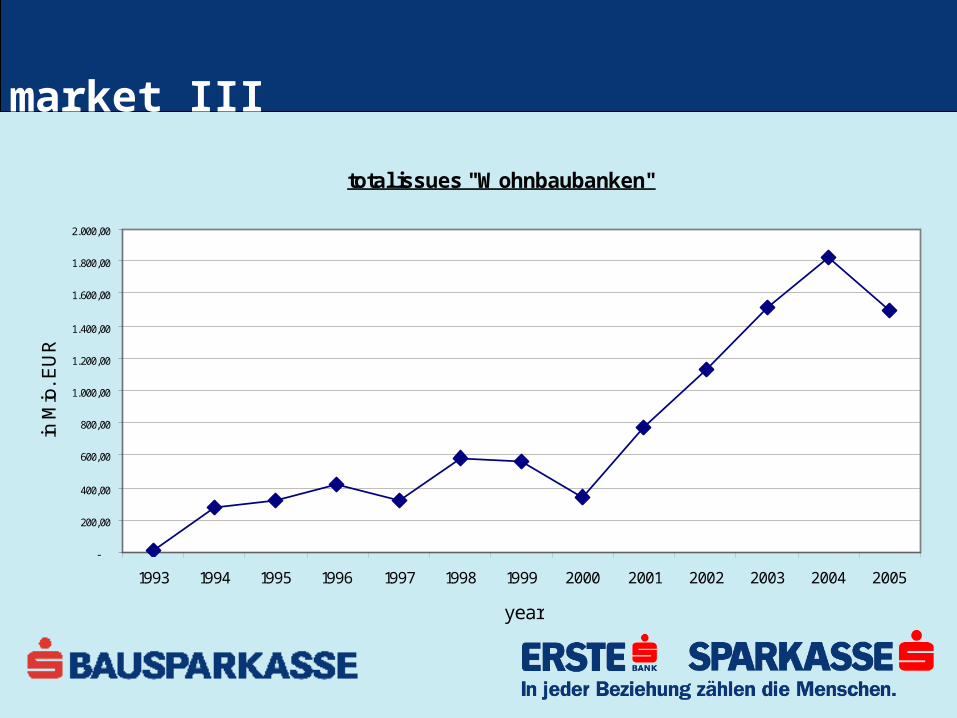

market III

total issues "Wohnbaubanken"

-

200,00

400,00

600,00

800,00

1.000,00

1.200,00

1.400,00

1.600,00

1.800,00

2.000,00

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

year

in M

io. E

UR

level of interest rateinterest rate for mortgage- and building society loans

2

3

4

5

6

7

8

9

10

11

12

1319

74

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

inte

rest

ra

te (

%)

mortgage loans (1996-06/2003 source ÖNB, estimated till 1995)

savings loans

provision of housing space (1996-06/2003 source ÖNB, estimated till 1995)

May 2005

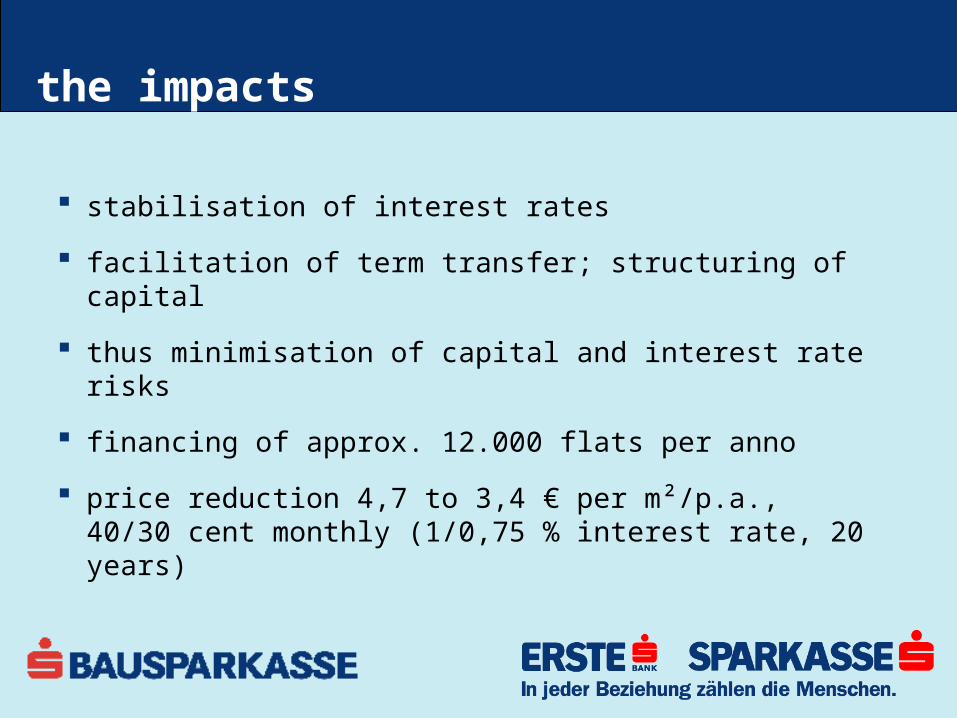

the impacts

stabilisation of interest rates

facilitation of term transfer; structuring of capital

thus minimisation of capital and interest rate risks

financing of approx. 12.000 flats per anno

price reduction 4,7 to 3,4 € per m²/p.a.,40/30 cent monthly (1/0,75 % interest rate, 20 years)

conclusion successful in raising long term private capital for housing

purposes

reduction and stabilisation of interest rates

measure of local creating value

study:Karl Czasny/Peter Moser, Einsatz und Gesamtwirkung der Wohnbauförderungsmittel (application and total impact of housing subsidies), Vienna: Lang Verlag 2000

„....in its functioning machinery principally successful and important supplementation of existent subsidy modules...“

„...distribution effects viewing social, sectoral and regional aspects are complementary to the effects of bausparen...“

Agenda

TOP 2

TOP 3

TOP 4

role of communities

TOP 1

housing policy in Austria

living in selected CEE countries

TOP 5 excursion I: the Austrian “Wohnbauanleihe”

housing aspects

TOP 6

TOP 7

TOP 8

excursion III: real estate securities

contact

excursion II: building societies’ housing loans

share of Bauspar-loans and FX-loans in private housing loans

Anteile Bausparfinanzierungen und FW-Kredite an gesamten Wohnkrediten28.6

42.5

72

31.3

55.0

53

33.3

05.6

84

35.1

93.8

37

37.5

17.9

72

40.7

19.6

11

45.9

10.3

46

52.5

93.2

10

55.1

70.8

65

60.0

47.3

22

62.5

63.3

32

63.4

49.2

03

64.5

24.7

61

65.8

47.2

09

67.3

64.6

59

67.4

31.3

94

0,19% 0,53% 1,19%2,94%

6,06%7,57%

13,95%

42,06%

38,82%37,41%

34,47%

30,55%

32,59%30,68%

20,57%

30,12%29,88%28,73%27,84%

24,29%

21,30%

28,34%29,68% 29,98%

20,62%

21,02%

21,11%

21,16%

21,59%

24,14%22,10%

26,20%

0

10.000.000

20.000.000

30.000.000

40.000.000

50.000.000

60.000.000

70.000.000

80.000.000

1995 1996 1997 1998 1999 2000 2001 2002 2003 Jun2004

Dez2004

Mär2005

Jun2005

Sep2005

Dez2005

Jän2006

in E

UR

0

0,05

0,1

0,15

0,2

0,25

0,3

0,35

0,4

0,45

Wohnkredite gesamt Wohnbaukredite in FW Wohnbaukredite in EUR

Bausparkasse gesamt Anteil FW-Kredite Anteil Bausparfinanzierungen

Agenda

TOP 2

TOP 3

TOP 4

role of communities

TOP 1

housing policy in Austria

living in selected CEE countries

TOP 5 excursion I: the Austrian “Wohnbauanleihe”

housing aspects

TOP 6 excursion II: building societies’ housing loans

TOP 7

TOP 8 contact

excursion III: real estate securities

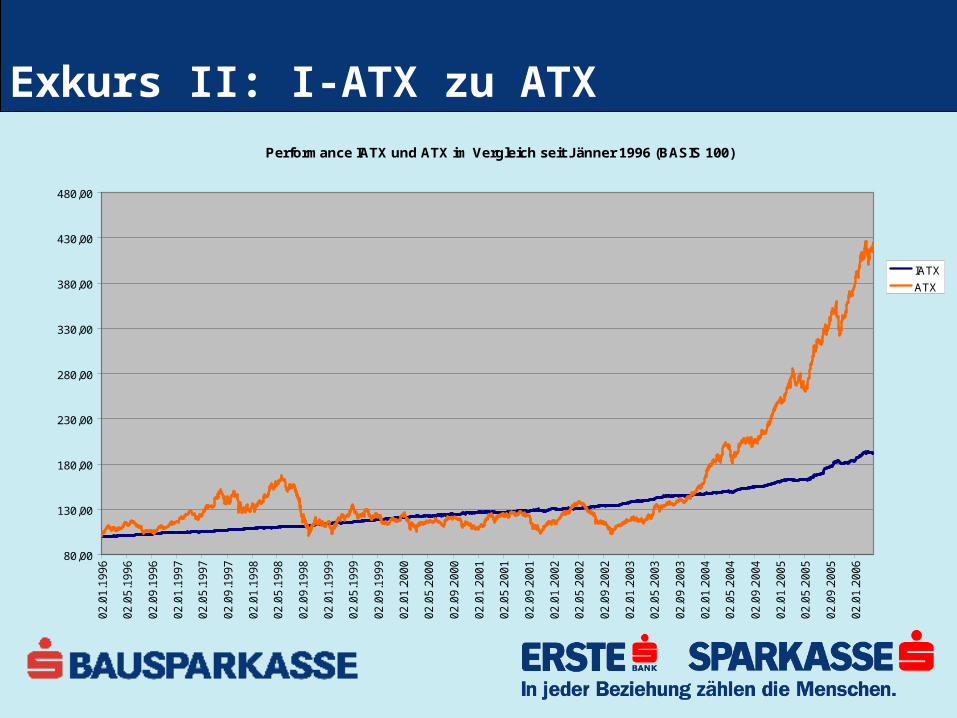

Exkurs II: I-ATX zu ATXPerformance IATX und ATX im Vergleich seit Jänner 1996 (BASIS 100)

80,00

130,00

180,00

230,00

280,00

330,00

380,00

430,00

480,00

02

.01

.19

96

02

.05

.19

96

02

.09

.19

96

02

.01

.19

97

02

.05

.19

97

02

.09

.19

97

02

.01

.19

98

02

.05

.19

98

02

.09

.19

98

02

.01

.19

99

02

.05

.19

99

02

.09

.19

99

02

.01

.20

00

02

.05

.20

00

02

.09

.20

00

02

.01

.20

01

02

.05

.20

01

02

.09

.20

01

02

.01

.20

02

02

.05

.20

02

02

.09

.20

02

02

.01

.20

03

02

.05

.20

03

02

.09

.20

03

02

.01

.20

04

02

.05

.20

04

02

.09

.20

04

02

.01

.20

05

02

.05

.20

05

02

.09

.20

05

02

.01

.20

06

IATX

ATX

Exkurs III: market capitalisation of the 8 Austrian real estate stock companies

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

H1

1996

H2

1996

H1

1997

H2

1997

H1

1998

H2

1998

H1

1999

H2

1999

H1

2000

H2

2000

H1

2001

H2

2001

H1

2002

H2

2002

H1

2003

H2

2003

H1

2004

H2

2004

H1

2005

H2

2005

H1

2006

Agenda

TOP 2

TOP 3

TOP 4

role of communities

TOP 1

housing policy in Austria

living in selected CEE countries

TOP 5 excursion I: the Austrian “Wohnbauanleihe”

housing aspects

TOP 6 excursion II: building societies’ housing loans

TOP 7

TOP 8

excursion III: real estate securities

contact

contact

Astrid Kratschmann

Beatrixgasse 271031 WienTel.: 050100/[email protected]

Monika Gröger

Beatrixgasse 271031 WienTel.: 050100/[email protected]