AUTO SECTOR: TRACTORS Eying new highs Chirag Shah Senior Research Analyst [email protected]+91 22 66121252 Siddhartha Bera Research Associate [email protected]+91 22 66242494 December, 2011 Tractors - Demand stable vs. Cars / M&HCVs. Demand drivers in place for sustainable double digit growth Moderation, if any, to be short lived. Growth in NABARD disbursements rather than Agri credit is more relevant Key beneficiary - M&M, valuations factoring in sharp drop in EBITDA / margins

Fragmented land holding----------------------------------------------------------------------------------------------------------------------------------------------5

Non farm usage of tractors – on a rise-----------------------------------------------------------------------------------------------------------------------------7

Replacement demand - Key near term support -----------------------------------------------------------------------------------------------------------------7

There have been rising concerns on the sustainability of tractor demand owing to

certain adverse developments and the strong performance of the tractor segment

over the last few years (17% CAGR during FY08-11 and 20% YTDFY12).

Recent adverse developments like (1) declining Agri terms of trade (ATOT) (2) lack of

buying support by FCI, resulting in produce being sold below MSPs and (3)slowdown in agri credit/rising NPAs (of PSU banks), have raised concerns over cash

flows of the farmers

Some of these concerns are overdone, while others are still nascent. If these

concerns materialize, then there can be pressure on tractor demand in the short

term. However, this would be a temporary blip as structurally, demand continues to

be on an upswing and it is nowhere near its peak. Our confidence stems from a

number of indicators highlighted below

¡ Indian tractor industry is more stable than Cars/M&HCVs. Since 1973, the tractor

industry has registered a CAGR of 8.6%.

¡ While India’s tractor penetration at 19 per 1000 hectares appears reasonable, we

believe it is misleading. Penetration per 1000 agricultural people is a betterindicator. At 5 per 1000, India’s tractor penetration is among the lowest.

¡ Across the globe, there has been a sharp reduction in population relying on

agriculture as a source of income. This is evident from the fact that current

penetration levels (per 1000 hectares) are significantly below their peak levels.

India is the only country, where there has been an increase in population relying

on agriculture, thereby supporting tractor demand

¡ Increasing focus of government has resulted in higher penetration of finance

amongst the target customers. Interestingly, there is no correlation between agri

lending and tractor demand. We found a much higher correlation between

NABARD disbursements and tractor demand

¡ Favorable cost dynamics and lack of restriction on use of tractors for otherpurposes have triggered additional demand for tractors. Non farm usage of

tractors is on the rise and constitutes ~40% currently.

¡ Shortening replacement age of tractors further supports short term demand. The

replacement age has reduced from ~12 years to ~8 years. In case of extensive

use of tractors for non farm purposes, the replacement age stands further

reduced to 5 years

¡ Rising multiplier effect, indicating higher demand for tractors vs. the earlier

periods

¡ Shortage of labor is a serious problem, which has acted as a key catalyst for

tractor demand

The above factors make us believe that the industry can register a strong growth of

12.5% CAGR over FY11-14E, with an upward bias (implying 12%/10% growth in

FY13E/FY14E). Even if the above mentioned concerns play out, we believe that 8%

growth is possible in FY13.

The key beneficiary of the structural demand in tractors will be M&M, given its

balanced regional and product mix as well as the ability to understand and adapt to

the market dynamics. We have a BUY on the stock with a TP of Rs 920 per share. We

find valuations attractive as they are pricing in a sharp drop in EBIDTA/margins in

Dependence of population on agriculture Rising share of agri population in India (indexed to 100)

1.6% 2.0%

61%

1.7%

48%

11% 8% 8%

0%

10%20%

30%

40%

50%

60%

70%

G e r m a n y

F r a n c e

C h i n a

U S

I n d i a

B r a z i l

A r g e n t i n a

R u s s i a

20

40

60

80

100

120

140

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

Brazil Canada ChinaIndia Russia United States

Source: FAO, Emkay Research

Penetration per 1000 hectare Penetration per 1000 agri pop

Year Peak Current Corres. Period Current

Argentina 1988 10 6 66 64

Brazil 199415 13

24 38

Russia 1992 10 3 67 31

USA 1967 31 25 na 810

France 1981 85 64 344 741

Germany 1986 138 65 410 508

Source: FAO, Emkay Research

Fragmented land holding – an important reason for higher dependence

The farmer landholding is very fragmented in India. As can be seen from the graph below,

62% of farmers account for 19% of land holding in India. Also, average land holding at ~2.6

acre is significantly low as compared to 444 acre in US, 675 acre in Canada and 45 acre in

EU. Given the shortage of labor and easy finance availability, we understand that there has

been sharing of tractors by small farmers. But for concerns to arise with respect to demand,the consolidation has to be far more significant.

Population of farmers Area under operations

62%19%

12%6% 1%

Marginal Small Semi-Medium Medium Large

19%

20%

24%

24%

13%

Marginal Small Semi-Medium Medium Large

Source: Ministry of Agriculture, GOI, Emkay Research

Rising penetration of finance

The clear focus of the government to increase the penetration of finance in rural areas is

evident from rising rural credit and more importantly, increase in bank’s rural network.

Another interesting point to note is that the increase in coverage is driven by reduction in

branches and increase in mobile units. This indicates focus on low cost/profitable businessmodel. This makes us believe in the sustenance and increase in rural penetration of banks

There have been rising concerns over availability of finance given slowdown in agri credit

by banks and rising NPAs in the agri portfolio of PSU banks. However, our analysis

indicates 1) PSU banks account for only ~15% of tractor sales 2) There is no co-relation

between agri credit growth and tractor demand. Infact, we observed a strong co-relationbetween NABARD’s farm mechanization disbursement and tractor growth.

Tractor and NABARD credit– strong correlation Tractor and Agri credit – no correlation

-30%

-10%

10%

30%

50%

F Y

8 9

F Y

9 1

F Y

9 3

F Y

9 5

F Y

9 7

F Y

9 9

F Y

0 1

F Y

0 3

F Y

0 5

F Y

0 7

F Y

0 9

F Y

1 1

Farm Mechanisation disbursement Tractors

(YoY change)

-30%

-20%

-10%

0%

10%

20%

30%

40%

F Y 9 0

F Y 9 2

F Y 9 4

F Y 9 6

F Y 9 8

F Y 0 0

F Y 0 2

F Y 0 4

F Y 0 6

F Y 0 8

F Y 1 0

H 1 F Y

1 2

Agri credit Tractors

(YoY change)

Source: NABARD, CRISIL, Emkay Research Source: RBI, Emkay Research

5 yr multiplier effect on tractor demand 3 yr multiplier effect on tractor demand

(8)

(6)

(4)

(2)

-

2

4

6

F Y 9 8

F Y 9 9

F Y 0 0

F Y 0 1

F Y 0 2

F Y 0 3

F Y 0 4

F Y 0 5

F Y 0 6

F Y 0 7

F Y 0 8

F Y 0 9

F Y 1 0

F Y 1 1

Vols/GDP Vols/Agri

Trendline (Vols/GDP) Trendline (Vols/Agr i)

(4)

(2)

-

2

4

6

8

F Y 9 6

F Y 9 7

F Y 9 8

F Y 9 9

F Y 0 0

F Y 0 1

F Y 0 2

F Y 0 3

F Y 0 4

F Y 0 5

F Y 0 6

F Y 0 7

F Y 0 8

F Y 0 9

F Y 1 0

F Y 1 1

Vols/GDP Vols/Agri

Trendline (Vo ls/GDP) Trendline (Vo ls/Agri)

Source: CRISIL, CMIE, Emkay Research

Labor shortage - a serious problem due to increase in alternative options

Labor shortage is the most important structural change that will drive farm mechanization.

We understand that shortage of labor is a serious issue faced by the farmers. Theshortages are arising from two sources – (1) various government schemes like MGNREGA

(2) choice of alternative profession for the young population. Both of these have resulted in

We believe that the demand for tractors in India is nowhere near its peak. Given the

increasing (1) awareness amongst farmers (2) higher income in the hands of farmer and (3)

labor shortage, demand will continue to remain strong. It should be noted that during the

green revolution in Punjab, tractor demand grew at a scorching pace of >20% for more thana decade. We believe that the tractor industry is well positioned to achieve above average

growth rates in the near future led by rising participation and awareness in other key states.

We believe that the tractor industry can report a strong double digit growth in FY13. We are

modeling a growth of 12%/10% in FY13/FY14 in our estimates, with an upward bias.

Punjab – Volume CAGR for tractors during green revolution

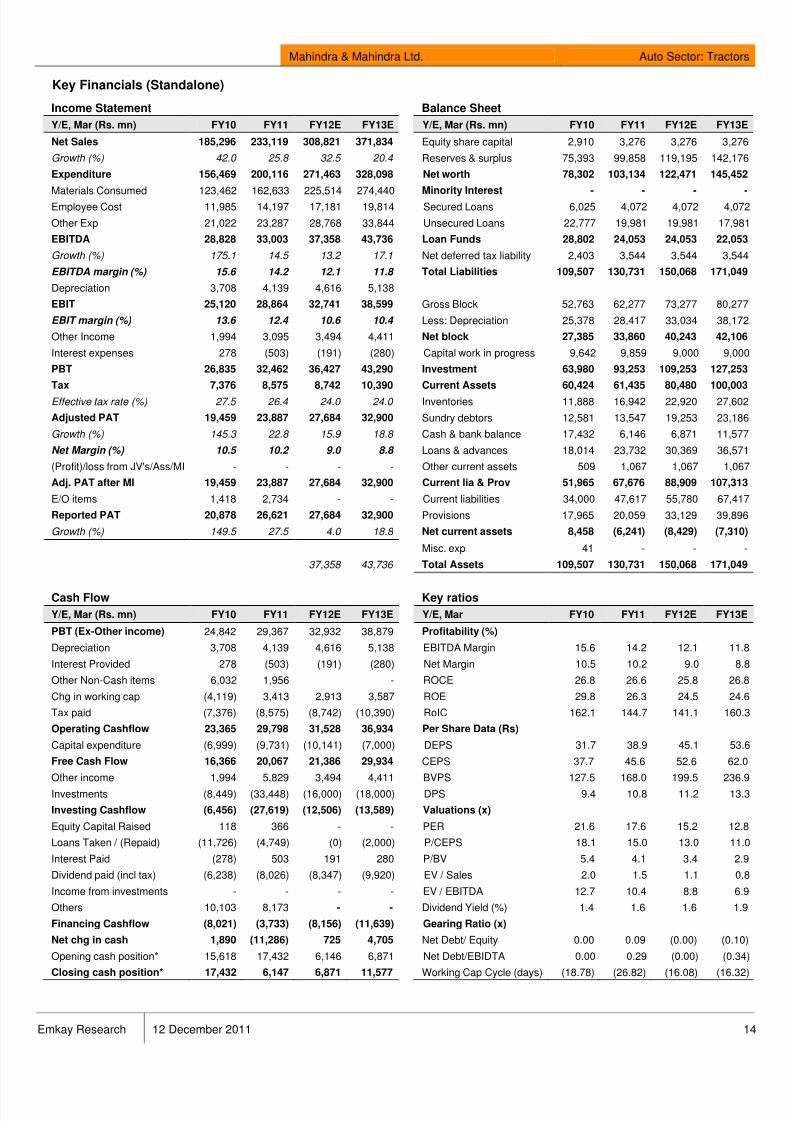

Valuations – factoring in ~38% drop in EBIDTA in FY13

Current valuations are factoring in ~38% drop in EBIDTA in FY13 vs our estimates(implying, 27% YoY decline). We believe that such a sharp drop in EBIDTA is unlikely,

thereby providing cushion against further downside.

Product profile – strong brand equity and balanced mix

M&M continues to enjoy strong brand equity across product segments (Market share of

~53% in UVs and ~42% in tractors), which led to its above industry growth rates in

H2FY12. We expect the current product portfolio to sustain volume momentum, driven by

strong non-urban demand. M&M’s tractor volumes will benefit from presence across India

and across HP segments (Yuvraj in low HP to Arjun in high HP).

New launches – the key volume driver in FY13

Recent launches (Maximmo, Genio, XUV5OO etc) have filled the gap in their productportfolio (no presence or weak presence). More importantly, new launches have achieved

reasonable success. We understand there is a waiting period for some of its products.

This, coupled with potential new launches (mini Xylo, etc), should ensure M&M

outperforming the industry growth in FY13. We forecast volume CAGR of ~12% for FY11-

13E in the UV segment and ~23% CAGR in pick-up segments (including Gio and

Maxximo) with an upward bias.

MVML and Ssangyong – future value creators

We see value in MVML, 100% manufacturing subsidiary, given the fact, most of the new

product will be manufactured at the subsidiary (16% of FY13 volumes). This will result in

pressure on margins in the standalone entity. Ssangyong which is in a turnaround phase

can also bring in value as and when the operations stabilize.

Valuations

We value the company on a SOTP basis. We have assigned a value of Rs 713 to its

standalone business and Rs 137 to listed subsidiaries and Tech Mahindra. We value

MVML business at Rs 70 per share on FY13 estimates. We believe there exists a strong

potential for higher value from MVML as and when product ramp up happens and

BUY Expected total return (%) (stock price appreciation and dividend yield) of over 25% within the next 12-18 months.

ACCUMULATE Expected total return (%) (stock price appreciation and dividend yield) of over 10% within the next 12-18 months.

HOLD Expected total return (%) (stock price appreciation and dividend yield) of upto 10% within the next 12-18 months.

REDUCE Expected total return (%) (stock price depreciation) of upto (-)10% within the next 12-18 months.

SELL The stock is believed to under perform the broad market indices or its related universe within the next 12-18 months.

Emkay Rating Distribution

DISCLAIMER: This document is not for public distribution and has been furnished to you solely for your information and may not be reproduced or redistributed to anyother person. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. Personsinto whose possession this document may come are required to inform themselves of, and to observe, such restrictions. This material is for the personal information of theauthorized recipient, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any securityin any jurisdiction where such an offer or solicitation would be illegal. No person associated with Emkay Global Financial Services Ltd. is obligated to call or initiate contactwith you for the purposes of elaborating or following up on the information contained in this document. The material is based upon information that we consider reliable, butwe do not represent that it is accurate or complete, and it should not be relied upon. Neither Emkay Global Financial Services Ltd., nor any person connected with it,accepts any liability arising from the use of this document. The recipient of this material should rely on their own investigations and take their own professional advice.Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable basis the information discussed

in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may be subject to change without notice. We and our affiliates, officers, directors, and employees world wide, including personsinvolved in the preparation or issuance of this material may; (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company (ies)mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financialinstruments of the company (ies) discussed herein or may perform or seek to perform investment banking services for such company(ies)or act as advisor or lender / borrower to such company(ies) or have other potential conflict of interest with respect to any recommendation and related information and opinions. The same persons mayhave acted upon the information contained here. No part of this material may be duplicated in any form and/or redistributed without Emkay Global Financial ServicesLtd.’sprior written consent. No part of this document may be distributed in Canada or used by private customers in the United Kingdom. In so far as this report includescurrent or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.