PRE BUDGET MEMORANDUM 2014-15 KEY CONCERNS OF INDIAN TYRE INDUSTRY 1 Submitted by : Automotive Tyre Manufacturers’ Association (ATMA) Phone : 91-11-26851187, 26564291, 91-11-2686 4799 [email protected]; www.atmaindia.org Meeting with Chairman, CBEC & Sr. Officials from Finance Ministr y Day & Date : Fri. 23 rd May,’14 Time : 2:30pm -3:30pm Venue : Kalpavrisksha, Room No. 158 A North Block (MoF), New Delhi.

Transcript

PRE BUDGET MEMORANDUM 2014-15 KEY CONCERNS OF INDIAN TYRE INDUSTRY

1

Submitted by :

Automotive Tyre Manufacturers’ Association (ATMA) Phone : 91-11-26851187, 26564291, 91-11-2686 4799

- Tyre Industry (Including Capacity & Investment by Tyre Industry)

Key Issues / Major Concerns of the Indian Tyre Industry

- Natural Rubber : Inverted Duty Structure

- Major Raw Materials of Tyre Industry

- Demand Supply Gap

- Duty Structure – Existing &Proposed

- Customs Duty on Tyres

• ATMA Submissions

Indian Tyre Industry 2013-14 – A Profile

• No. of Tyre Companies - 39 • No. of Tyre Plants - 60 • Turnover + - Rs. 47,500 crores /US$ 8 billion

• Export in value terms - Rs. 4800 crores • Production + - 123 million tyres

• Exports* - 8.4 million tyres /US$ 830 million • Imports - 8.9 million tyres /US$ 465 million

• Product Profile - From Moped Tyres (weighing 1.5 kg) to

Giant Earthmover Tyres (weighing over 1.5 Tons), Steel Belted Radial Truck Tyres, High Performance Tubeless Passenger Car Tyres and Tyres for Fighter Aircraft of Indian Air Force + Est.

*ATMA Member Companies only

3

ATMA Member Companies

10 Large Co's (comprising of)

- Global MNCs - Indian Tyre Co's (having presence overseas) - Leading Indian Players

• (accounting for) 90%+ of Industry (in Value/Tonnage)

4

Locational Map – Tyre Plants (ATMA Member Co’s)

5

• Recent investments by Tyre Industry have been to the tune of over Rs. 20,000 crores in greenfield projects as also major expansions

Industry, Environment & Outlook Current Economic & Sectoral Environment

Auto Sector

The ongoing economic turndown has adversely affected the India’s Automobile Industry. As per Society of Indian Automobile manufactures (SIAM), Commercial Vehicle witnessed a (-)16% YoY drop in production during 2013-14 over 2012-13. This is on top of the decline of (-)28% in the previous fiscal. Passenger Vehicle production also witnessed a (-) 5% YoY in 2013-14 over 2012-13 for the first time in a decade.

Tyre Sector

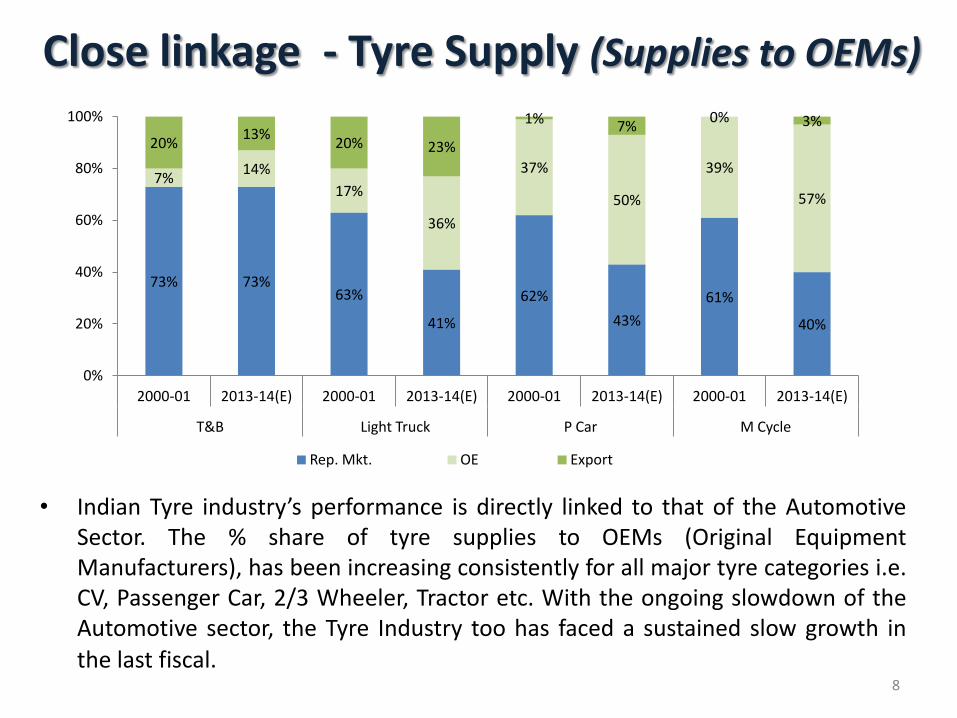

Indian Tyre industry’s performance is directly linked to that of the Automotive Sector. The percentage share of tyre supplies to OEMs (Original Equipment

Manufacturers), has been increasing consistently for all major tyre categories i.e. CV, Passenger Car, 2/3 Wheeler, Tractor etc. With the ongoing slowdown of the Automotive sector, the Tyre Industry too faces a slow growth in the current fiscal and uncertainty prevails for the future.

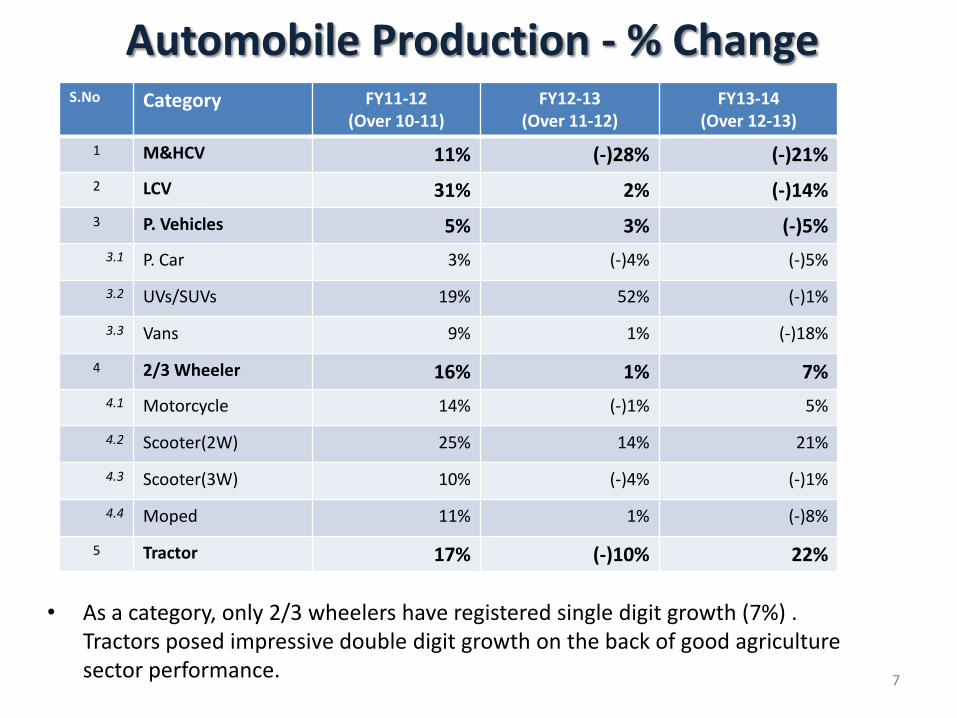

Automobile Production - % Change

7

S.No Category FY11-12 (Over 10-11)

FY12-13 (Over 11-12)

FY13-14 (Over 12-13)

1 M&HCV 11% (-)28% (-)21%

2 LCV 31% 2% (-)14%

3 P. Vehicles 5% 3% (-)5%

3.1 P. Car 3% (-)4% (-)5%

3.2 UVs/SUVs 19% 52% (-)1%

3.3 Vans 9% 1% (-)18%

4 2/3 Wheeler 16% 1% 7%

4.1 Motorcycle 14% (-)1% 5%

4.2 Scooter(2W) 25% 14% 21%

4.3 Scooter(3W) 10% (-)4% (-)1%

4.4 Moped 11% 1% (-)8%

5 Tractor 17% (-)10% 22%

• As a category, only 2/3 wheelers have registered single digit growth (7%) . Tractors posed impressive double digit growth on the back of good agriculture sector performance.

8

Close linkage - Tyre Supply (Supplies to OEMs)

• Indian Tyre industry’s performance is directly linked to that of the Automotive Sector. The % share of tyre supplies to OEMs (Original Equipment Manufacturers), has been increasing consistently for all major tyre categories i.e. CV, Passenger Car, 2/3 Wheeler, Tractor etc. With the ongoing slowdown of the Automotive sector, the Tyre Industry too has faced a sustained slow growth in

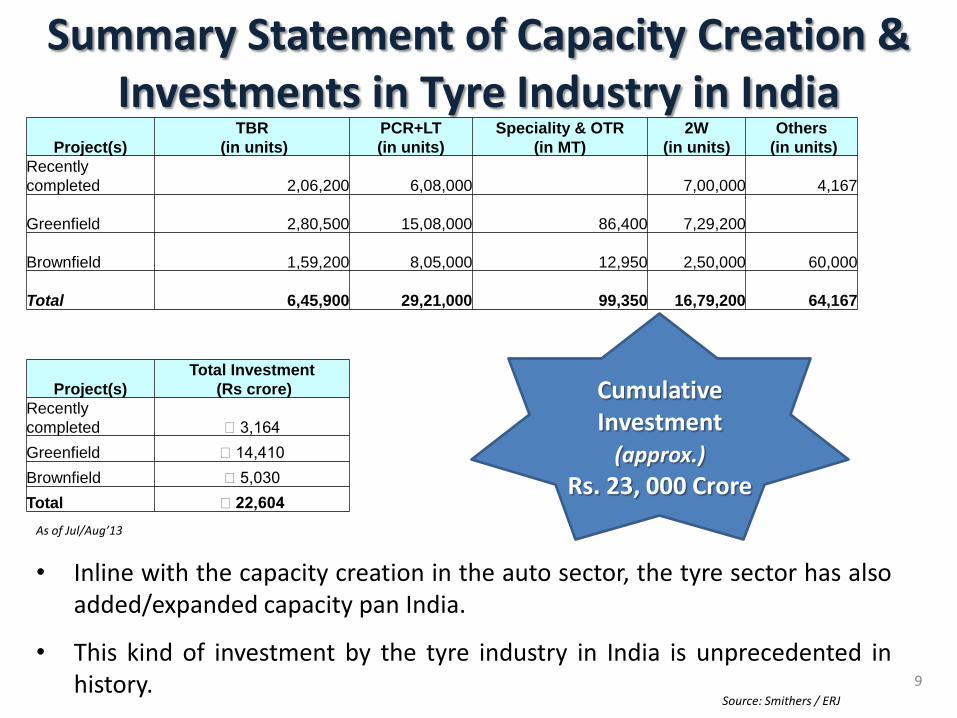

• Inline with the capacity creation in the auto sector, the tyre sector has also added/expanded capacity pan India.

• This kind of investment by the tyre industry in India is unprecedented in history.

Project(s)

TBR

(in units)

PCR+LT

(in units)

Speciality & OTR

(in MT)

2W

(in units)

Others

(in units)

Recently

completed

2,06,200

6,08,000 7,00,000 4,167

Greenfield

2,80,500

15,08,000

86,400 7,29,200

Brownfield

1,59,200

8,05,000

12,950 2,50,000

60,000

Total

6,45,900

29,21,000

99,350

16,79,200

64,167

Project(s)

Total Investment

(Rs crore)

Recently

completed ₹ 3,164

Greenfield ₹ 14,410

Brownfield ₹ 5,030

Total ₹ 22,604

Summary Statement of Capacity Creation & Investments in Tyre Industry in India

As of Jul/Aug’13

Source: Smithers / ERJ

Cumulative Investment

(approx.) Rs. 23, 000 Crore

Key Issues / Concerns of the

Indian Tyre Industry

10

Key issues & Concerns of Indian Tyre Industry

• Related to Raw Materials (RMs) – Tyre industry is RM intensive

– Raw materials accounts for 72% of Production cost

– Natural Rubber (NR) , the principal raw material, accounts for approx. 42% of RM cost

• Tyre Industry consumes over 65% of Total NR consumption in India (domestic production + imports).

• Key Tyre related issues relate to: – Trade Agreements

– Tyre Imports

11

Domestic NR Demand – Supply Imbalance

• Current Gap (between Domestic Production : Consumption) is given below:

• On a YoY basis, the gap has increased by approx 75,000 MT.

FY 2013-14

8.44 9.77

0.0

2.0

4.0

6.0

8.0

10.0

Production Consumption

9.14 9.73

0.0

2.0

4.0

6.0

8.0

10.0

Production Consumption

Gap Increased by 74,395 MT

FY 2012-13

Gap = 59,005MT

12

Gap = 133,400 MT

NR Availability / Gap

13

• For the last 7 successive years, India has experienced shortfall/deficit- of varying degree- between domestic NR production & consumption. The situation in FY 14-15 is also projected to close with a shortfall.

32590

-36110

-7220

-99165 -85765

-35000

-59005

-133400

-60000

-100000

-160000

-140000

-120000

-100000

-80000

-60000

-40000

-20000

0

20000

40000

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 As per Rubber Board

NR Imports are necessary: • To bridge the demand/supply gap

• For quality specific requirement of new technology driven Radial Truck & Bus (TBR) Tyres

• To maintain international competitiveness in Tyre Exports

• For reasons cited above, Tyre Industry seeks regular supply and competitive domestic & international pricing/sourcing of its critical raw-material.

• Customs duty on Tyres has been reduced over the last few years with no corresponding reduction in basic rate of customs duty on Natural Rubber.

14

Period Rate of Duty Specific duty

(converted to % on

current May'14 NR RSS-

3 prices)

Advalorem Specific

Upto 31st Mar'11 20% N.A. N. A.

w.e.f. 01.04.2011 20% Rs. 20/kg* 16%+

w.e.f 20.12.2013 20% Rs. 30 kg* 20%++ *whichever is lower ; +if the earlier duty (@Rs.20/kg) was applicable in May'14 ++As per current rate of duty

NR Duty in India : Recent Changes

NR Duty Structure : India vs other major NR Producing / Consuming Countries

15

• India’s effective NR duty is the highest amongst all countries.

Major NR Producing Countries

S.*

No

Name of

the

Countries

Customs Duty(%)

1 Thailand 0%

2 Malaysia 0%

3 Vietnam 3%

4 Indonesia 5%

5 Combodia 7%

6 Sri Lanka 15%

7 India 20% or Rs. 30/kg

whichever is lower

Major NR Consuming Countries

S*.

No

Name of the

Countries

Customs

Duty(%)

@ Specific

Duty+

1 China 20% 9.5%

2 USA 0% As per

Calculation

below

3 Russia 0%

4 Japan 0%

5 Mexico 0%

6 India

20% or Rs. 30/kg

whichever is

lower 20%

+ Levied on specific rates converted into % at current NR prices

Basic & Concessional Customs Duty on NR in India – No relief to Consumer Sector

*Under SAFTA, 5% concessional duty for NR applies for imports from Pakistan & Sri Lanka. However, the tariff is Nil for imports from other SAFTA nations where there is no NR Production.

Ne

gati

ve L

ist

16

%

Ne

gati

ve L

ist

5%

(o

r N

il*)

Ne

gati

ve L

ist

Ne

gati

ve L

ist

0%

4%

8%

12%

16%

20%

Basic Customs Duty

ASEAN FTA Asia Pacific Trade Agreement

Indo Sri Lanka SAFTA* India Singapore India - Malaysia

No Duty Concession

No Duty Concession

No Duty Concession

No Duty Concession

In India

20

% o

r R

s. 2

0/k

g, w

hic

hev

er

is lo

we

r

Although tyres (finished product) can be imported into India at preferential / concessional duties under various RTAs, the corresponding concessional duties for NR is not beneficial.

NR falls in the negative list across most FTA except for Asia Pacific and SAFTA. However, in both Asia Pacific and SAFTA, the concessional duties apply mainly for NR imports from Sri Lanka (which are insignificant and hence of no practical significance).

(To Allow) Limited Quantity of Natural Rubber (NR) Import on a Tariff Rate Quota (TRQ) Basis

• During FY 2013-14, the gap between domestic NR Production and Consumption was ~135,000 MT and for FY 2013-14, the gap is expected to exceed 60,000 MT (as per Rubber Board Projections).

• As per Industry estimates, during the current fiscal (FY 2014-15) the gap is likely to be over 100,000 MT. This quantity (to bridge the demand-supply gap) of NR has to be imported into India.

Submission

• Department to consider allowing import of limited quantity of NR (say 100,000 MT) under a Tariff Rate Quota (TRQ) basis for FY 2014-15 at a concessional rate of duty of 7.5% OR Rs. 10 per kg, whichever is lower. In Dec.`10, Finance Ministry has allowed 40,000 MT of NR at 7.5% concessional duty on TRQ basis .

17

CESS on NR imports under Advance License

• Cess on Natural Rubber is levied under Section 12 of the Rubber Act -1947. Under Sub Section (1) Cess is levied on rubber produced in India. NR Consumers’ are facing problems at the time of clearance of imported rubber due to insistence by the Customs at JNPT for payment of Cess, including on Advance License import of NR.

• Finance Ministry has been requested by Industry to issue clarification to Customs at JNPT on the issue.

18

Customs Duty on Tyres under Trade Agreements

• While basic customs duty on tyres is 10%, under various Trade Agreements the duty (on tyres) is actually much lower than the basic rate of customs duty (on its principal RM (i.e. Natural Rubber):

Item

Normal /Basic Rate of Duty

in India ASEAN FTA

Asia Pacific Trade

Agreement (Bangkok

Agreement) Indo Sri Lanka SAFTA

India Singapore

India Malaysia

Tyre 10% 6% 8.60% Nil 5% / Nil* Nil

(Bias Tyre) 6%

(Radial Tyre)

NR

20% OR Rs.30/kg whichever is lower

Negative List (No Duty

Concession) 16% **

Negative List (No Duty

Concession) 5% / Nil*

Negative List (No Duty

Concession)

Negative List (No Duty

Concession)

* Under SAFTA 5% concessional duty for Tyre when imports from Pakistan & Sri Lanka ,imports from other SAFTA countries Nil Duty.

** Under APTA although NR is at a concessional duty of 16% ,there is no NR production in APTA countries, except Sri Lanka.

• Tyre is perhaps the only finished product (vis-a-vis its basic RM) on which ‘duty inversion’ not only continues but has actually aggravated in recent years. This needs to be addressed and corrected on priority.

19

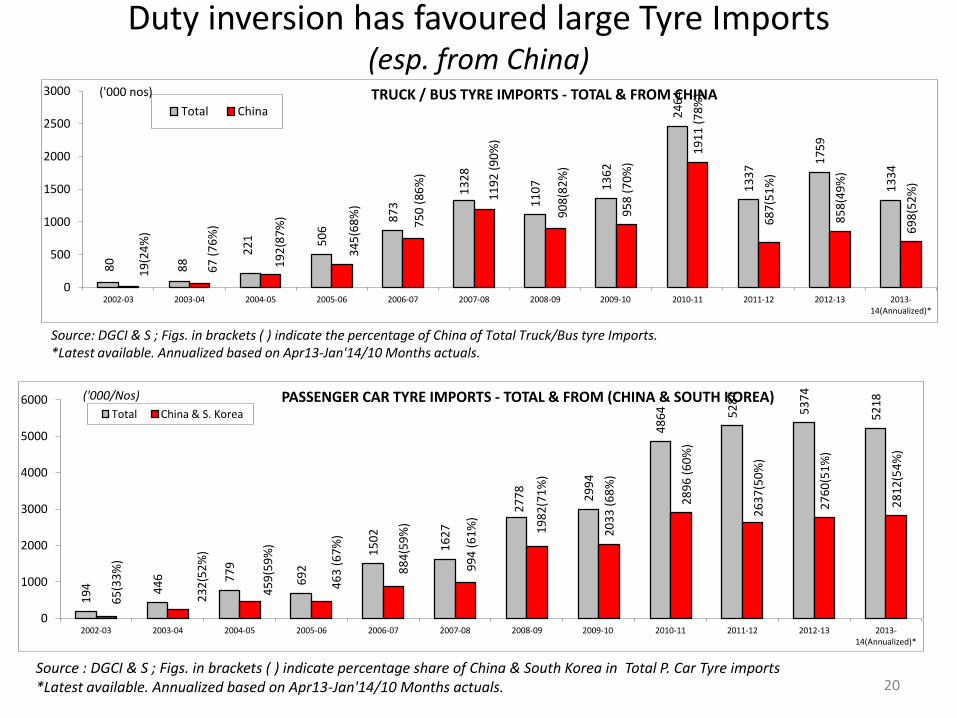

Duty inversion has favoured large Tyre Imports (esp. from China)

Source: DGCI & S ; Figs. in brackets ( ) indicate the percentage of China of Total Truck/Bus tyre Imports. *Latest available. Annualized based on Apr13-Jan'14/10 Months actuals.

Source : DGCI & S ; Figs. in brackets ( ) indicate percentage share of China & South Korea in Total P. Car Tyre imports *Latest available. Annualized based on Apr13-Jan'14/10 Months actuals.

PASSENGER CAR TYRE IMPORTS - TOTAL & FROM (CHINA & SOUTH KOREA) Total China & S. Korea

('000/Nos)

20

Tyre Imports into India favoured by FTAs

• Low import tariffs in India have encouraged large & growing volume of tyre imports, despite adequate domestic capacity & investments.

• Hence, based on compelling need and circumstances, the Government of India can increase the customs duty on tyres from existing rate of 10% (to a higher rate of duty) without any corresponding action / explanation to the world body (WTO).

21

Major RMs of Tyre Industry

Raw Material(s)

Domestic Production

(est.)

Domestic Consumption

(est.)

Shortfall / Deficit

Shortfall as a % to consumption

MT / Year

Nylon Tyre Cord Fabric 65000 125000 60000 48%

Rubber Chemicals 35000 55000 20000 36%

Steel Tyre Cord 15000 40000 25000 62%

Polyester Tyre Cord 3000 9000 6000 66%

Polybutadine Rubber (PBR)

85000 113000 28000 25%

Process Oil 96000 150000 54000 36%

(Gap between Domestic Demand and Supply / Capacity)

Butyl Rubber NIL 58000 100% 100%

EPDM Nil 3700 100% 100%

SBR (Tyre Grade) Nil 110000 100% 100%

RMs with Domestic Demand : Supply Gap – Case for Reduction in Customs Duty

RMs of Tyre Industry having no Domestic Production – Case for Exemption from Customs Duty

Significant gap between domestic Production : Consumption of critical RMs, yet NTCF, Rubber Chemicals, Carbon Black & Capital Equipment are burdened with Anti Dumping / Safeguard Duties affecting Industry competitiveness.

22

RM Imports – A Necessity

• Due to gap between domestic production & consumption varying between 12% - 70% as also ‘No Domestic Production’ in India, import of key RM of Tyre Industry is a necessity.

23

Proposal for Reduction of Customs Duty on Raw-Materials having gap (shortfall) in domestic Capacity : Consumption & Waiver of Customs

Duty on Raw - Materials of Tyre Industry NOT manufactured domestically

24

Raw Material Existing Duty Suggested / Proposed Duty

Natural Rubber 20% or Rs.20/kg 10% of Rs.10/kg

Natural Rubber Compound 10% Waive Off

Nylon Tyre Cord Fabric (NTCF) 10% 5%

Poly Butadiene Rubber (PBR) 10% 5%

Rubber Chemicals 7.5% 2.5%

Polyester Tyre Cord 5% 2.5%

Steel Tyre Cord 10% 5%

Process Oil 10% 5%

Butyl Rubber* 5% Waive off

EPDM* 10% Waive off

Styrene Butadiene Rubber (SBR)* (Tyre Grades) 10% Waive off

* No Domestic Production

Safeguard Duty on Carbon Black import – Advance License Imports

• Under Para 4.1.4 of Foreign Trade Policy, Government has granted exemption from payment of all kind of duties under Advance License Authorization imports.

• Safeguard Duty was imposed on imports of Carbon Black vide Notification No.4/2012-Customs(SG) dated 5th Oct. 2012.

• Customs authorities at various ports have been demanding Safeguard Duty on imports of Carbon lack against Advance License Authorization.

Submission:

• Finance Ministry may issue clarification by exempting Safeguard Duty under Advance Authorization import.

25

Operational & Procedural Issues – Tyre Industry Concern

26

Central Excise

• Rate of Interest for delayed payment of excise duty/ service tax should be restored back to 13% p.a. from existing 18%.

• Interest on pre-deposit of duty demanded, penalty levied etc. while filing the Appeal

• Interest on diversion of goods for home consumption from a warehouse registered under Rule 20 of Central Excise Rules,2002 – present @24% is exorbitant.

• Expiry of Stay Order if appeal is not disposed of within the period of 180 days - provisions are not in favour of Industry

• Short payment of duty due to genuine clerical errors – Treat as defaults under Rule -8

Cenvat Credit Rules, 2004:

• Capital goods:

– 100% CENVAT credit on capital goods in the year of receipt - Otherwise funds are blocked.

• Inputs

– Expand the scope of definition of Rules (k) of Cenvat Credit Rules, 2004 – to include diesel & motor spirit.

27

Service Credit

– Definition of input service and its eligibility under Cenvat Credit Rules, 2004

– Condition of non availement of Cenvat Credit by the GTA Service Provider should be removed

– Cenvat credit for Input services without making payment

– Service tax credit on goods manufactured on job work basis;

– Distribution of credit by Input Service Distributor

Service Tax ( Finance Act, 1994 & Rules There under)

– Reverse Charge Mechanism – imposes burden of transaction cost and compliance issues

28

Key Submission(s)

• There is an urgent need to correct the existing (and continuing) anomaly of ‘inverted duty’ structure as it prevails for the domestic Tyre Industry by way of the following:

• Reduction in Customs Duty on Natural Rubber, from 20% (or Rs. 30/kg whichever is lower) at present to a suggested rate of 10% (or Rs.10/kg, whichever is lower).

or alternatively

• Increase in customs duty on Tyres from 10% at present to 20%, the same rate as its principal raw-material (i.e. Natural Rubber);

• To meet the definite shortfall between domestic NR production : consumption (gap in availability for which imports are indispensible), limited quantity of NR import- on Tariff Rate Quota (TRQ) basis- @ 7.5% for a quantity of 100,000 MT for Fy 14-15. Such TRQ based volume of NR import be allowed on a recurring basis each year as per demand : supply gap as established by the Rubber Board (Govt. of India) each year.

29

Key Submission(s) (contd…)

For other key RMs of Tyre Industry, the duty inversion / anomalies continue and need to be corrected by way of:

Waiver of customs duty on raw materials NOT manufactured domestically,