Members, Committee on Audit Shailesh J. Mehta, Chair Kyriakos Tsakopoulos, Vice Chair Debra Farar William Hauck Frederick W. Pierce IV Staff University Auditor: Larry Mandel Senior Director: Michael Redmond Senior Auditors: Michael Caldera, Danica Roso, and Kathryn Upton Internal Auditor: Sandy Skalla BOARD OF TRUSTEES THE CALIFORNIA STATE UNIVERSITY AUXILIARY ORGANIZATIONS CALIFORNIA STATE UNIVERSITY, HAYWARD Report Number 02-52 June 6, 2003

Transcript

Members, Committee on Audit Shailesh J. Mehta, Chair

Kyriakos Tsakopoulos, Vice Chair Debra Farar William Hauck

Frederick W. Pierce IV

Staff University Auditor: Larry Mandel

Senior Director: Michael Redmond Senior Auditors: Michael Caldera, Danica Roso, and Kathryn Upton

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES CAMPUS

Legal and Regulatory Compliance.............................................................................................................. 16 Public Relations Policy ........................................................................................................................ 16 Conflict of Interest................................................................................................................................ 17

Trusts and Other Liabilities ........................................................................................................................ 19 Student Body Fees................................................................................................................................ 19 Custodial Funds.................................................................................................................................... 20

CALIFORNIA STATE UNIVERSITY, HAYWARD FOUNDATION, INC.

Legal and Regulatory Compliance.............................................................................................................. 22 Auxiliary Authorization........................................................................................................................ 22 Dissolution of Auxiliary ....................................................................................................................... 23 Leasing of Facilities ............................................................................................................................. 23 Delegation of Authority........................................................................................................................ 24 Salaries and Benefits ............................................................................................................................ 25 Reserves................................................................................................................................................ 25 Risk Management................................................................................................................................. 26 Non-Discrimination Policies ................................................................................................................ 27 Administrative Services Agreement..................................................................................................... 27 Segregation of Duties ........................................................................................................................... 28

Cash Receipts and Handling ....................................................................................................................... 29

Information Technology ............................................................................................................................. 43 User Access .......................................................................................................................................... 43 Physical and Environmental Controls .................................................................................................. 44 Disaster Recovery Plan......................................................................................................................... 44

UNIVERSITY UNION OF CALIFORNIA STATE UNIVERSITY, HAYWARD

Legal and Regulatory Compliance.............................................................................................................. 46 Written Agreements ............................................................................................................................. 46 Salaries and Benefits ............................................................................................................................ 47 Segregation of Duties ........................................................................................................................... 48

Cash Receipts and Handling ....................................................................................................................... 48 Investments ................................................................................................................................................. 50

Fees, Revenues, and Receivables................................................................................................................ 51

Information Technology ............................................................................................................................. 70

CAL STATE HAYWARD EDUCATIONAL FOUNDATION

Legal and Regulatory Compliance.............................................................................................................. 71 Auxiliary Authorization........................................................................................................................ 71 Public Meetings.................................................................................................................................... 71 Board Meetings .................................................................................................................................... 72 Delegation of Authority........................................................................................................................ 72 Budget Approval .................................................................................................................................. 73 Reserves................................................................................................................................................ 74

Cash Receipts and Handling ....................................................................................................................... 75

ABBREVIATIONS AD Accounting Department Coded Memorandum AS Associated Students, California State University, Hayward CFR Code of Federal Regulations Childhood Center Early Childhood Education Center CSU California State University CSUH California State University, Hayward Educational Foundation Cal State Hayward Educational Foundation EO Executive Order Foundation California State University, Hayward Foundation, Inc. FPPC Fair Political Practices Commission FSR Faculty and Staff Relations – Office of the Chancellor IRA Instructionally Related Activity IRC Internal Revenue Code IRS Internal Revenue Service MOU Memorandum of Understanding NIH National Institutes of Health NSF National Science Foundation OMB Office of Management and Budget PHS Public Health Service Union University Union of California State University, Hayward

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 1

INTRODUCTION PURPOSE The principal audit objectives were to determine compliance with the Education Code, Title 5, and directives of the Board of Trustees and the Office of the Chancellor and to assess the adequacy of controls and systems. Specifically, we sought assurances that legal and regulatory requirements are complied with regarding the: Formation of the auxiliary. Functions the auxiliary performs on the campus. Creation and operation of the auxiliary’s board of directors. Establishment of policies and procedures based upon sound business practices. Observance of mandates to maintain an “arms-length” in business transactions between the auxiliary

and the campus. Campus oversight of auxiliary operations.

In addition, we reviewed internal controls to assure that: Accounting data is provided in an accurate, timely, complete, or otherwise reliable manner. Assets are adequately safeguarded from loss, damage, or misappropriation. Duties are appropriately segregated consistent with appropriate control objectives. Transactions, accounting entries, or systems output is reviewed and approved. Management does not intentionally override internal controls to the detriment of the overall internal

control objectives. Accounting and fiscal tasks, such as reconciliations, are prepared properly and completed timely. Deficiencies in internal controls previously identified were corrected satisfactorily and timely. Management seeks to prevent or detect erroneous record keeping, inappropriate accounting,

fraudulent financial reporting, financial loss, and exposure.

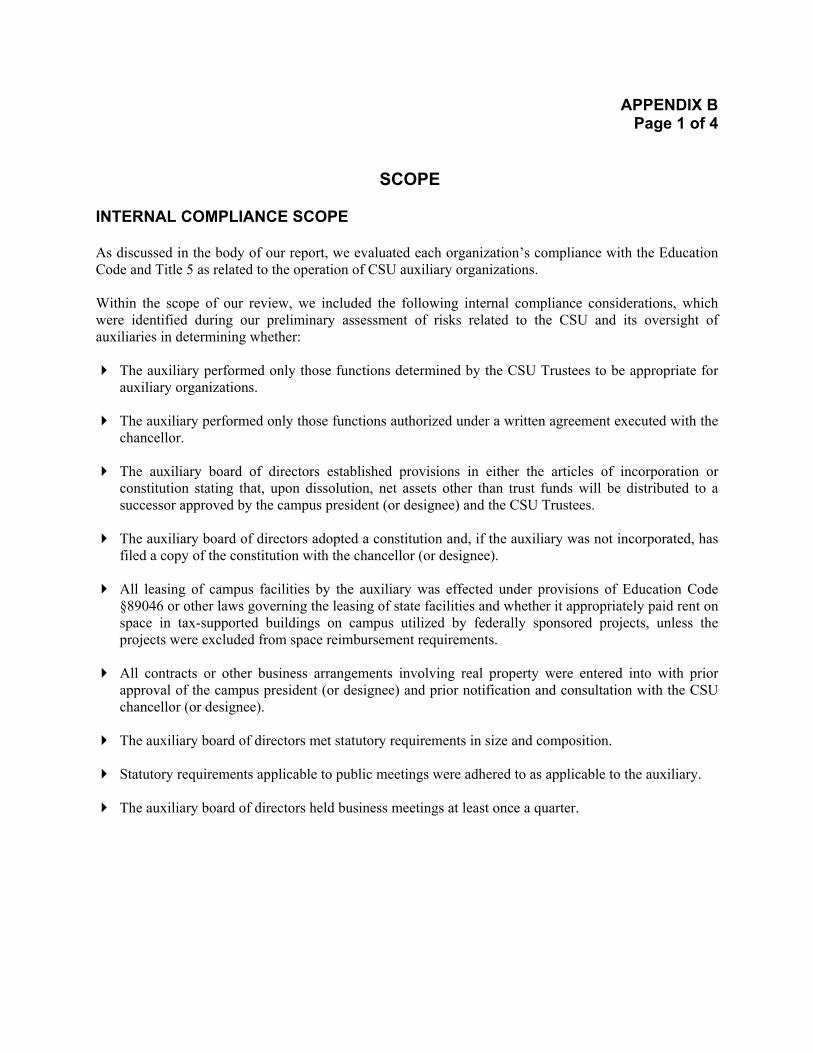

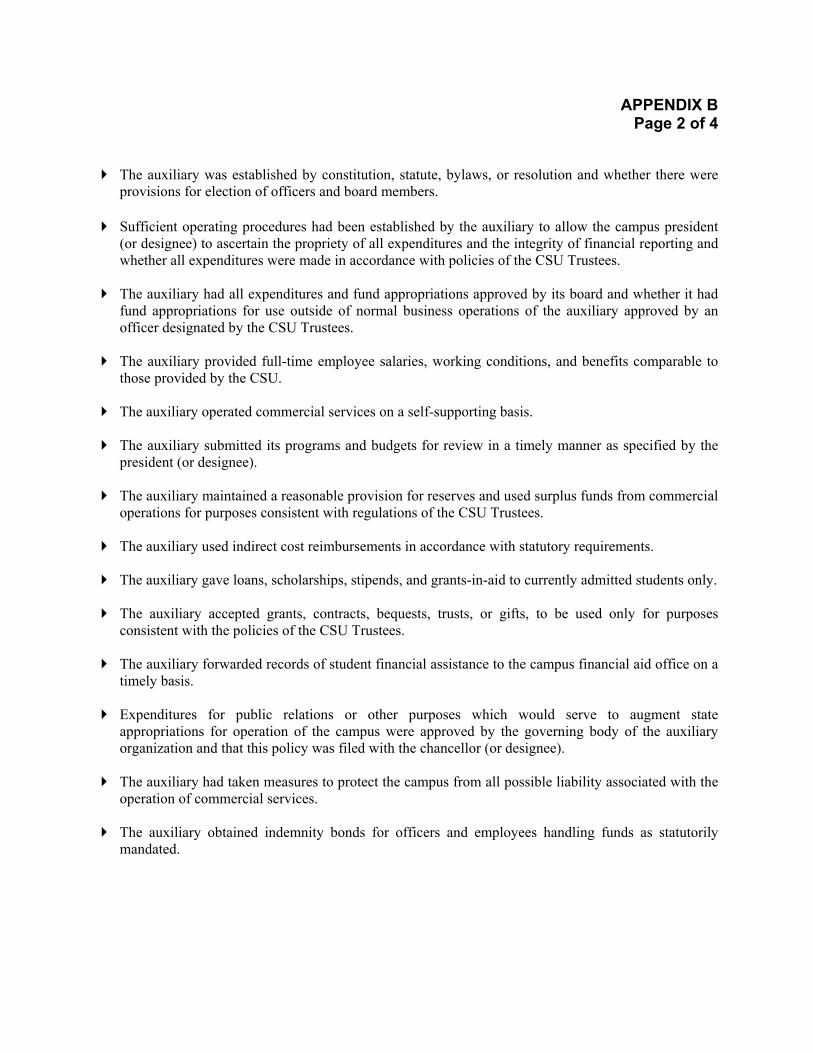

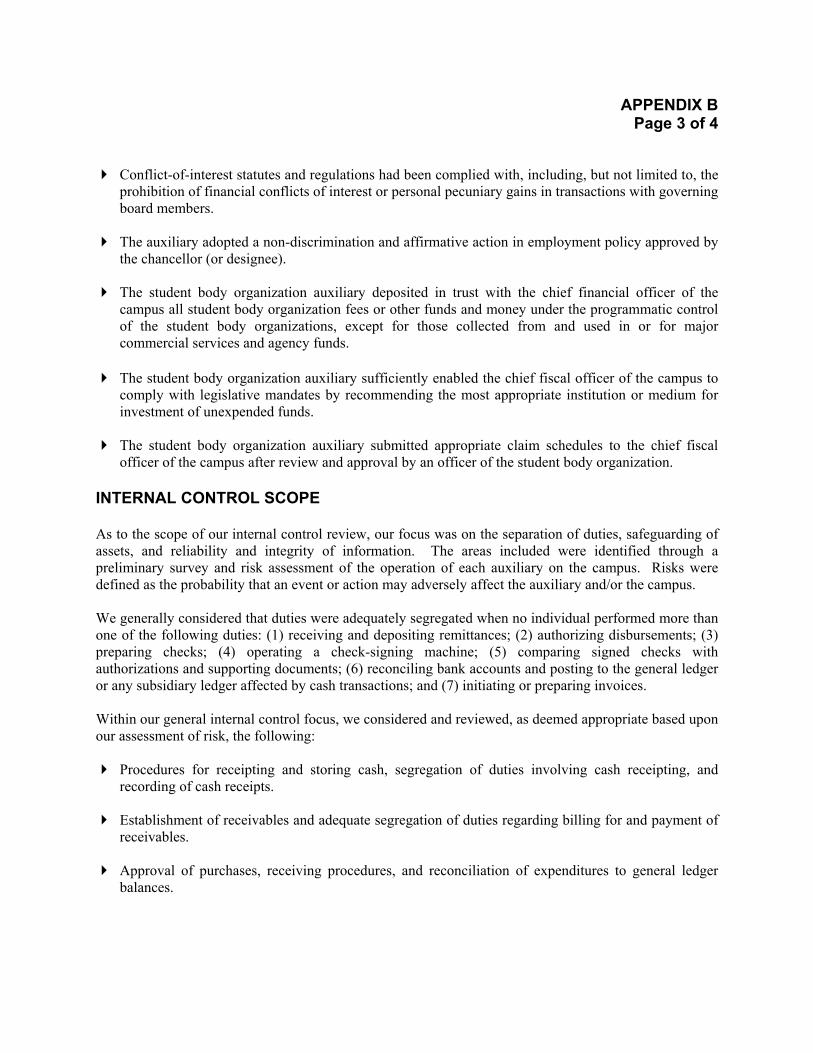

SCOPE AND METHODOLOGY Our management review emphasized, but was not limited to, compliance with state and federal laws and regulations, Board of Trustee policies, and Office of the Chancellor policies, letters, and directives as they relate to California State University (CSU) auxiliaries. For those audit tests that required annualized data, fiscal years 2000-2001 and 2001-2002 were the primary periods reviewed. In certain instances, we were concerned with representations of the most current data—in such cases, the test period was extended to December 2002. Our primary focus was on internal compliance and controls. Specifically, for the period reviewed, we examined compliance of the campus and each auxiliary with the Education Code and Title 5 as they relate to the operation of CSU auxiliary organizations. Individual codes and regulations included within the scope of our review were identified through an assessment of risk. Similarly, internal controls were included within our scope based upon risk. Therefore, the scope of our review varied from auxiliary to auxiliary.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 2

A preliminary survey of CSU auxiliaries at each campus was used to identify risks. Risk was defined as the probability that an event or action would adversely affect the auxiliary and/or the campus. Our assessment of risk was based upon a systematic process, using professional judgments on probable adverse conditions and/or events that became the basis for development of our final scope. We sought to assign higher review priorities to activities with higher risks. As a result, not all risks identified were included within the scope of our review. The scope of our review, regarding internal compliance considerations, focused on areas which were identified during our preliminary assessment of risks related to the CSU and its requirements to exercise oversight of auxiliaries. (See Appendix B.) The scope of our internal control review focused on separation of duties, safeguarding of assets, and reliability and integrity of information. Within these, we considered areas of risk identified during a preliminary survey of the campus’ auxiliary operations in addition to risks related to the CSU and its oversight of auxiliaries. (See Appendix B.) We have not performed reviews or analyses beyond the date of our report. Accordingly, our comments are based on our knowledge as of that date and should be read with that understanding. Since the purpose of our comments is to suggest areas for improvement, comments on favorable matters are not discussed.

BACKGROUND Education Code §89900 states, in part, that the operation of auxiliary organizations shall be conducted in conformity with regulations established by the Trustees. Education Code §89904 states, in part, that the Trustees of the California State University and the governing boards of the various auxiliary organizations shall: Institute a standard systemwide accounting and reporting system for businesslike management of the

operation of such auxiliary organizations. Implement financial standards which will assure the fiscal viability of such various auxiliary

organizations. Such standards shall include proper provision for professional management, adequate working capital, adequate reserve funds for current operations and capital replacements, and adequate provisions for new business requirements.

Institute procedures to assure that transactions of the auxiliary organizations are within the

educational mission of the state colleges. Develop policies for the appropriation of funds derived from indirect cost payments.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 3

Executive Order No. 698, superseding Executive Order No. 682, was issued on March 3, 1999. In that directive, the president of each campus was instructed, in part, as follows:

Section 2. Authority and Responsibility of the Campus President. Title 5, Section 42402 establishes the authority of campus presidents to require auxiliary organizations to operate in conformity with policy of the Board of Trustees and the campus. The president is required to review auxiliary programs and budgets and to require discontinuance of activities not in conformity with policies of the Board of Trustees and campus. The following Trustee policy supplements the existing policy of Section 42402 and provides an additional mechanism for the president to administer his or her responsibilities concerning auxiliary organizations. Action taken by the Trustees' Committee on Audit at the January 1999 meeting of the Board requires an internal compliance/internal control review to be performed by the University Auditor. The Office of the University Auditor will perform an internal compliance/ internal control review of auxiliary organizations. The review will be used to determine compliance with law, including statutes in the Education Code and rules and regulations of Title 5, and compliance with policy of the Board of Trustees and of the campus, including appropriate separation of duties, safeguarding of assets and reliability and integrity of information. This review of each auxiliary organization shall be completed on a triennial basis pursuant to procedures established by the chancellor.

This report represents our triennial review.

OPINION We visited California State University, Hayward from December 2, 2002, through January 10, 2003, and reviewed the internal compliance and internal control structures in effect at that time. Our study and evaluation were conducted in accordance with the Standards for the Professional Practice of Internal Auditing, issued by the Institute of Internal Auditors, and included the audit tests we considered necessary in determining that accounting and administrative controls are in place and operative. The campus and management at each auxiliary are responsible for establishing and maintaining adequate internal controls. This responsibility includes documenting internal controls, communicating requirements to employees, and assuring that internal controls are functioning as prescribed. In fulfilling this responsibility, estimates and judgments by management are required to assess the expected benefits and related costs of control procedures.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 4

The objectives of accounting and administrative controls are to provide management with reasonable, but not absolute, assurance that: Assets are safeguarded against loss from unauthorized use or disposition.

Transactions are executed in accordance with management’s authorization and recorded properly to

permit the preparation of reliable financial statements. Financial operations are conducted in accordance with policies and procedures established in the State

Administrative Manual, Education Code, Title 5, and Trustee policy as applicable. Our audit disclosed conditions which, in our opinion, would result in significant errors and irregularities if not corrected. These conditions, along with other weaknesses, are described in the executive summary and in the body of the report. As a result of changing conditions and the degree of compliance with procedures, the effectiveness of controls change over time. Specific limitations that may hinder the effectiveness of an otherwise adequate system of controls include, but are not limited to: resource constraints, faulty judgments, unintentional errors, circumvention by collusion, and management overrides. Establishing controls to prevent these limitations would not be cost-effective; moreover, an audit may not always detect these limitations. (See Appendix C.)

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 5

EXECUTIVE SUMMARY The purpose of this section is to provide management with an overview of conditions requiring their attention. Areas of review not mentioned in this section were found to be satisfactory. Numbers in brackets [ ] refer to page numbers in the report.

CAMPUS LEGAL AND REGULATORY COMPLIANCE [16]

PUBLIC RELATIONS POLICY [16]

The campus had not established a current public relations policy applicable to its auxiliary organizations. Establishing a current public relations policy applicable to auxiliary organizations reduces the risk that funds will be accumulated and used improperly. CONFLICT OF INTEREST [17]

The campus had not provided guidance for its auxiliaries regarding the implementation of conflict-of- interest policies and procedures, including statements and disclosures from board members, management, and principal investigators for applicable federal and non-governmental projects. Adequately addressing and implementing conflict-of-interest code policies and procedures for auxiliary boards and management reduce liability for acts contrary to the code.

ROYALTY PAYMENTS [19] The campus had not developed sufficient and appropriate written policies and procedures concerning royalties paid to faculty members for the reproduction and sale of their own copyrighted materials. Fully developed and communicated written policies and procedures strengthen internal controls and reduce the risk that misunderstandings will occur.

TRUSTS AND OTHER LIABILITIES [19]

STUDENT BODY FEES [19] The chief fiscal officer of the campus was not acting as custodian of student body organization fees. Sufficient control and accounting over student body funds ensure that custodial responsibilities are met and reduce the risk of error or misappropriation of funds.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 6

CUSTODIAL FUNDS [20] The campus did not exercise sufficient control over custodial funds held in trust by its auxiliaries. Sufficient oversight over custodial funds held by auxiliaries reduces exposure to regulatory and legal consequences.

CALIFORNIA STATE UNIVERSITY, HAYWARD FOUNDATION, INC. LEGAL AND REGULATORY COMPLIANCE [22]

AUXILIARY AUTHORIZATION [22] The California State University, Hayward Foundation, Inc. (Foundation) operating agreement with the California State University (CSU) required revision as to functions managed, administered, and operated by the auxiliary organization. Operating with an up-to-date, written agreement reduces the risk of misunderstandings and miscommunication regarding rights and responsibilities. DISSOLUTION OF AUXILIARY [23] The Foundation’s articles of incorporation did not specify that the net assets of the dissolved auxiliary must be distributed to a successor approved by the campus president and the CSU Trustees. The inclusion of a dissolution clause in accordance with Title 5 reduces the risk of net assets not being properly distributed in the event the corporation is dissolved. LEASING OF FACILITIES [23] Certain Foundation lease and sublease arrangements were not properly supported by written agreements. Maintaining written agreements reduces the risk of misunderstandings and miscommunication regarding rights and responsibilities. DELEGATION OF AUTHORITY [24] The Foundation had not established a written delegation of authority for certain board members to sign contracts on behalf of the auxiliary. A written delegation of authority to sign contracts on behalf of the auxiliary reduces misunderstandings and may reduce legal liability. SALARIES AND BENEFITS [25] The Foundation had not documented an analysis of full-time employee salaries, wages, and benefits between its employees and campus employees serving in similar positions. Fully documenting the comparative analysis of positions reduces the risk that the auxiliary may be expending inappropriate amounts on salaries and benefits for employees who perform substantially similar services as employees for the campus or other organizations.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 7

RESERVES [25] The Foundation reserve policy required updating. Sufficient reserve planning and analysis reduce the auxiliary’s risk to fund future needs. RISK MANAGEMENT [26] Certain Foundation contracts did not indemnify the campus or CSU Trustees. The inclusion of appropriate indemnification clauses in contracts reduces the auxiliary’s exposure to potential liability. NON-DISCRIMINATION POLICIES [27]

The Foundation’s current non-discrimination policy did not address discrimination based on pregnancy or veterans’ status. An adequate non-discrimination policy reduces the auxiliary’s risk of non-compliance with state and federal laws and regulatory actions. ADMINISTRATIVE SERVICES AGREEMENT [27] The Foundation had not executed a written agreement for fiscal and accounting services provided to the Cal State Hayward Educational Foundation (Educational Foundation) and for payroll-related services associated with campus instructionally related activity (IRA) funds. Maintaining written agreements reduces the risk of misunderstandings and miscommunication regarding rights and responsibilities. SEGREGATION OF DUTIES [28]

The Foundation did not appropriately segregate certain accounting functions for bookstore purchasing and payroll and human resources. Adequate segregation of duties reduces the risk that errors and irregularities will not be detected in a timely manner.

CASH RECEIPTS AND HANDLING [29] Certain controls over Foundation cash handling were insufficient. Adequate controls over cash handling reduce the risk of a loss or misappropriation of funds.

PETTY CASH AND CHANGE FUNDS [31]

PETTY CASH FUNDS [31] The Foundation had not documented petty cash fund policies and procedures which required provisions for performing periodic and independent, unannounced cash counts. Fully developed and communicated written policies and procedures strengthen internal controls and reduce the risk that misunderstandings will occur.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 8

CHANGE FUNDS [32] The Foundation bookstore textbook buyback change fund was inappropriately used to extend advances to employees. Adequate controls over change funds reduce the risk that a misappropriation of funds will not be detected in a timely manner.

INVESTMENTS [33] Foundation written investment policies and procedures did not address controls over the transfer of investment funds. Fully developed and communicated written policies and procedures strengthen internal controls and reduce the risk that misunderstandings will occur.

FEES, REVENUES, AND RECEIVABLES [34] ACCOUNTS RECEIVABLE [34] Certain controls over Foundation accounts receivable were inadequate. Sufficient controls over accounts receivable reduce the risk of loss, errors, and irregularities. UNRECORDED REVENUE [35] The Foundation did not record and deposit, upon receipt, reward revenues collected from the confiscation of invalid credit cards. Appropriately processing revenue reduces the risk of errors, irregularities, and misappropriation.

PURCHASING AND ACCOUNTS PAYABLE [36] PURCHASE ORDER APPROVAL [36]

The Foundation bookstore had not developed and implemented policies and procedures addressing the review and authorization of inventory purchases exceeding specified dollar thresholds. Fully developed and communicated written policies and procedures strengthen internal controls and reduce the risk that misunderstandings will occur. CREDIT CARDS [36] Controls over the use of Foundation corporate credit cards were insufficient. Sufficient controls over credit card usage reduce the risk of errors, irregularities, and misappropriation of funds. CHECK PROCESSING [37] Certain controls over Foundation check processing were inadequate. Adequate controls over check processing reduce the risk of errors, irregularities, and misappropriation of funds.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 9

UNCLAIMED MONIES [38] The Foundation had not developed policies and procedures to escheat unclaimed monies to the state. Meeting the requirements of unclaimed property law could reduce the auxiliary’s exposure to potential penalties and fines.

PERSONNEL AND PAYROLL [39]

PAYROLL PROCESSING [39] Certain payroll processing controls for the Foundation and Foundation-managed entities were insufficient. Adequate controls over payroll processing reduce the risk of errors, irregularities, and misappropriation of funds. In addition, compliance with tax legislation reduces the potential of fines. EMPLOYEE SEPARATION [40] The Foundation’s controls over separated employees were inadequate. Fully documenting and completing employee clearance forms and removing or inactivating separated employees from the payroll system reduce the risk of loss, errors, and misappropriation.

FIXED ASSETS [41] Certain controls over Foundation fixed assets were inadequate. Adequate controls over fixed assets reduce the risk that property may be lost or stolen.

AUXILIARY PROGRAMS [42]

Documentation to evidence that final technical reports and other technical deliverables were submitted to the sponsor was not contained in Foundation project files. Adequate documentation reduces the risk of penalties and disallowances for non-compliance with contracts and grants terms.

INFORMATION TECHNOLOGY [43] USER ACCESS [43] Foundation user profiles did not provide for proper segregation of duties/functions. Adequate segregation of duties/functions reduces the risk of errors, irregularities, and misappropriation of funds.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 10

PHYSICAL AND ENVIRONMENTAL CONTROLS [44] The Foundation’s computer room was not equipped with smoke detection equipment. Adequate physical and environmental safeguards for the computing equipment reduce the probability of a significant adverse event affecting the computing system. DISASTER RECOVERY PLAN [44] The Foundation had not developed a sufficiently detailed, written information technology disaster recovery plan and corresponding business continuation procedures. A detailed, written disaster recovery plan and corresponding business continuation procedures enable the auxiliary to restore data processing operations within a reasonable time frame.

UNIVERSITY UNION OF CALIFORNIA STATE UNIVERSITY, HAYWARD LEGAL AND REGULATORY COMPLIANCE [46]

WRITTEN AGREEMENTS [46]

Certain written agreements between the University Union of California State University, Hayward (Union) and other entities were incomplete, expired, and/or lacking sufficient detail of business arrangements. Maintaining complete and up-to-date, written agreements reduces the risk of misunderstandings and miscommunication regarding rights and responsibilities. SALARIES AND BENEFITS [47] The Union had not sufficiently documented an analysis of full-time employee salaries, wages, and benefits between its employees and campus employees serving in similar positions. Fully documenting the comparative analysis of positions reduces the risk that the auxiliary may be expending inappropriate amounts on salaries and benefits for employees who perform substantially similar services as employees for the campus or other organizations. SEGREGATION OF DUTIES [48] The Union did not appropriately segregate certain accounting functions for cash receipts. Adequate segregation of duties reduces the risk that errors and irregularities will not be detected in a timely manner.

CASH RECEIPTS AND HANDLING [48]

Transfer accountability over the movement of Union cash receipts and change funds was not clearly established. Adequate controls over cash receipts and change funds reduce the risk of a loss or misappropriation of funds.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 11

INVESTMENTS [50] The Union did not perform timely analysis and reconciliations of their investments maintained by the campus. Performing investment account reconciliations on a timely basis reduces the risk that errors and irregularities will not be detected.

FEES, REVENUES, AND RECEIVABLES [51] Certain controls over Union accounts receivable processing were inadequate. Sufficient controls over accounts receivable processing reduce the risk of loss, errors, and irregularities.

PURCHASING AND ACCOUNTS PAYABLE [52]

ACCOUNTS PAYABLE [52] Certain controls over Union accounts payable processing were inadequate. Sufficient controls over accounts payable processing reduce the risk of errors and irregularities. TAX REPORTING [53] The Union had not clearly documented its determination that stipends paid to student board members were not reportable in accordance with Internal Revenue Service (IRS) requirements. Properly reporting amounts considered as income to the recipients could reduce the risk of potential fines. SALES TAX [55]

The Union had overpaid sales tax for meals sold to students. Payment of imputed sales tax on only non-student meals enhances the ability of food service units to operate within their budgeted plan.

FIXED ASSETS [55]

Certain controls over Union fixed assets were inadequate. Adequate controls over fixed assets reduce the risk that property may be lost or stolen.

INVENTORIES [57]

Certain controls over Union food inventory were insufficient. Sufficient controls over food inventory reduce the risk of food cost from falling outside an acceptable range.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 12

ASSOCIATED STUDENTS, CALIFORNIA STATE UNIVERSITY, HAYWARD

LEGAL AND REGULATORY COMPLIANCE [59]

AUXILIARY AUTHORIZATION [59]

Associated Students, California State University, Hayward (AS) had not executed an operating agreement with the CSU for the period under review. Operating with an up-to-date, written agreement reduces the risk of misunderstandings and miscommunication regarding rights and responsibilities.

BOARD MINUTES [59] AS board meeting minutes were incomplete. Maintaining sufficient and appropriately approved board meeting minutes reduces the risk of misunderstandings and may reduce legal liability. SALARIES AND BENEFITS [60]

AS had not sufficiently documented an analysis of full-time employee salaries, wages, and benefits between its employees and campus employees serving in similar positions. Fully documenting the comparative analysis of positions reduces the risk that the auxiliary may be expending inappropriate amounts on salaries and benefits for employees who perform substantially similar services as employees for the campus or other organizations. RESERVES [61]

The AS reserve policy required revision. Sufficient reserve planning and analysis reduce the auxiliary’s risk to fund future needs. RISK MANAGEMENT [62]

AS did not maintain participant accident insurance coverage for its recreational activities and did not have procedures in place to determine the need for special riders for extraordinary events. Maintaining appropriate insurance coverage reduces the auxiliary’s exposure to potential liability. SEGREGATION OF DUTIES [63]

AS did not appropriately segregate certain accounting functions for cash receipts. Adequate segregation of duties reduces the risk that errors and irregularities will not be detected in a timely manner.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 13

CASH RECEIPTS AND HANDLING [63]

Checks received by the AS Early Childhood Education Center (Childhood Center) were not restrictively endorsed at the time of receipt, and deposit receipts were not issued. Adequate controls over cash receipts reduce the risk of a loss or misappropriation of funds.

PETTY CASH AND CHANGE FUNDS [64]

Certain controls over AS petty cash and change funds were insufficient. Adequate controls over petty cash and change funds reduce the risk of a loss or misappropriation of funds.

INVESTMENTS [65]

AS inappropriately invested in an equity investment vehicle. Investing in authorized investment vehicles reduces the risk to future losses.

FEES, REVENUES, AND RECEIVABLES [66]

ACCOUNTS RECEIVABLE [66] Certain controls over AS accounts receivable were insufficient. Sufficient controls over accounts receivable reduce the risk of loss, errors, and irregularities. REVENUE RECONCILIATION [67] Revenues received by the AS Childhood Center were not reconciled to enrollment records. Adequately reconciling revenues reduces the risk that errors or misappropriation of funds would not be detected.

PURCHASING AND ACCOUNTS PAYABLE [67]

The AS had not clearly documented its determination that stipends paid to student board members were not reportable in accordance with IRS requirements. Properly reporting amounts considered as income to the recipients could reduce potential fines.

FIXED ASSETS [69]

Certain controls over AS fixed assets were inadequate. Adequate controls over fixed assets reduce the risk that property may be lost or stolen.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 14

INFORMATION TECHNOLOGY [70] Controls over information security at the AS Childhood Center were deficient. Implementing appropriate general computer controls reduces the potential for loss or corruption of personal information of child-care participants.

CAL STATE HAYWARD EDUCATIONAL FOUNDATION LEGAL AND REGULATORY COMPLIANCE [71]

AUXILIARY AUTHORIZATION [71]

The Educational Foundation had not executed an operating agreement with the CSU for the period under review. Operating with an up-to-date, written agreement reduces the risk of misunderstandings and miscommunication regarding rights and responsibilities. PUBLIC MEETINGS [71]

Notices of the Educational Foundation board of directors’ and committee meetings were not posted in a public area. Compliance with regulations for public meetings reduces the risk of misunderstandings and may reduce legal liability. BOARD MEETINGS [72] The Educational Foundation did not conduct the required number of board of directors’ meetings. When the board of directors meets on a regular basis in accordance with CSU policy, the board’s fiduciary responsibility over the operations of the auxiliary organization may be met. DELEGATION OF AUTHORITY [72] The Educational Foundation had not established a written delegation of authority for all named persons or positions to sign checks on behalf of the auxiliary. A written delegation of authority to sign contracts on behalf of the auxiliary reduces the potential for misunderstandings and legal liability. BUDGET APPROVAL [73]

The Educational Foundation did not prepare an annual budget subject to the approval of the campus president. Appropriate approval of auxiliary budgets reduces the risk that the auxiliary will operate in a manner inconsistent with the educational mission of the campus.

INTRODUCTION

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 15

RESERVES [74]

The Educational Foundation had not established a written surplus funds/reserve policy. Sufficient reserve planning and analysis reduce the auxiliary’s risk to fund future needs.

CASH RECEIPTS AND HANDLING [75]

Certain Educational Foundation cash receipts were transported unsecured and in the custody of only one person. Adequate controls over cash receipts processing reduce the risk of a loss or misappropriation of funds.

INVESTMENTS [75]

Educational Foundation written investment policies and procedures did not address control over the transfer of investment funds. Fully developed and communicated written policies and procedures strengthen internal controls and reduce the risk that misunderstandings will occur.

FEES, REVENUES, AND RECEIVABLES [76]

DONOR SYSTEM RECONCILIATION [76] Reconciliations between the Educational Foundation donor database system and the general ledger accounting system were not consistently performed. Complete reconciliations of donor and accounting records reduce the risk of reporting errors and misappropriations of funds.

PLEDGES RECEIVABLE [77] Certain controls over the collection of Educational Foundation pledges receivable were insufficient. Sufficient controls over pledges receivable reduce the risk that accounts will not be collected in a timely manner. DONATION PROCESSING [78] Certain controls over Educational Foundation donation processing were inadequate. Adequate controls over donation processing reduce the risk of a loss or misappropriation of funds.

TRUSTS [79]

The Educational Foundation had not implemented procedures to ensure that the corpus balances for each endowment fund are adequately maintained and that distributions from these funds are in accordance with the expectations of the donors. Sufficient management and accounting procedures for endowments reduce the risk that funds will be handled inappropriately and contrary to the expectations of the campus and donors.

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 16

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

CAMPUS

LEGAL AND REGULATORY COMPLIANCE

PUBLIC RELATIONS POLICY

The campus had not established a current public relations policy applicable to its auxiliary organizations. The campus public relations policy should address the following: Membership and participation in the activities of community groups, including, but not limited to,

service clubs and community-wide organizations of leading citizens in education, business, government, industry, and agriculture, with which campus administration should collaborate in order that the campus may properly serve the needs of the community.

Types of official activities that will commonly be engaged in by the campus which would generally be recognized as essential for promoting and maintaining student, faculty, and staff morale and for developing and maintaining effective relations with the community. Such activities may include but are not limited to campus receptions, public ceremonies, and lay advisory committee meetings held in support of certain campus instructional programs.

Providing essential accommodations and sustenance for official guests of the campus.

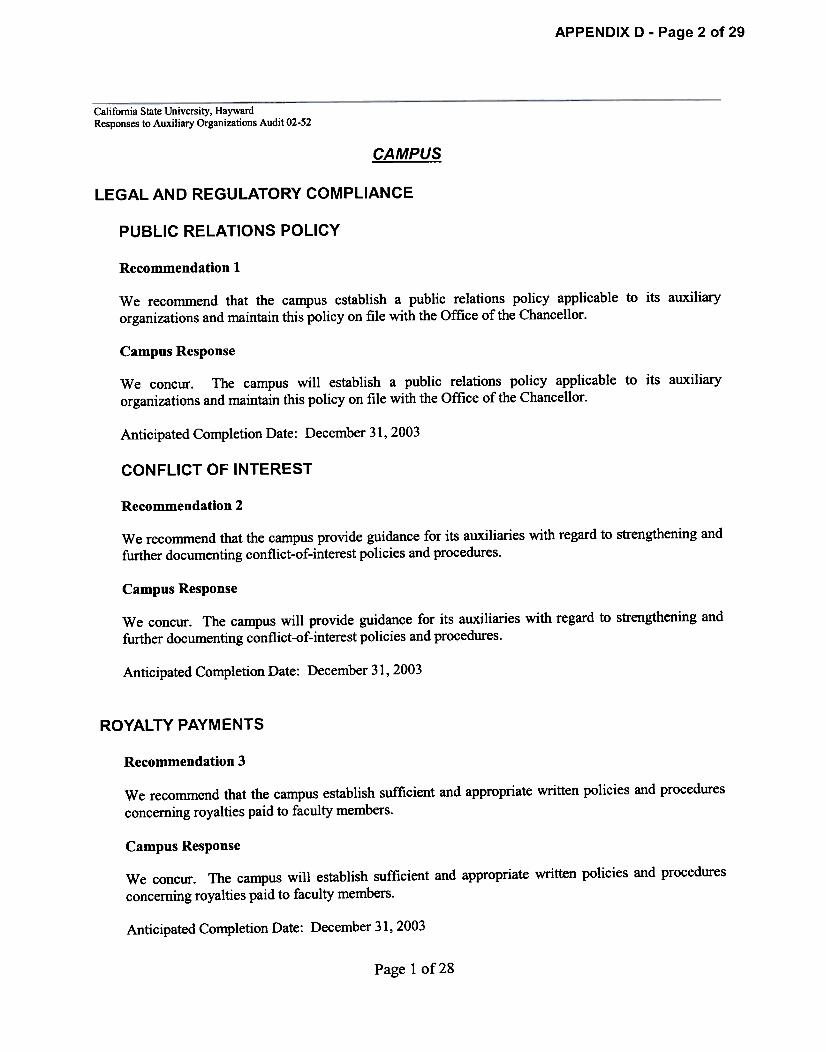

Title 5 §42502 requires the campus president to file, with the chancellor, a policy on the accumulation and use of public relations funds for all auxiliary organizations. The statement will include the policy and procedure on solicitation of funds, source of funds, amounts, purpose for which the funds will be used, allowable expenditures, and procedures of control. The associate vice president of business and financial services indicated his belief that the campus hospitality policy adequately addressed public relations. Failure to establish a current public relations policy applicable to auxiliary organizations increases the risk that funds will be accumulated and used improperly. Recommendation 1 We recommend that the campus establish a public relations policy applicable to its auxiliary organizations and maintain this policy on file with the Office of the Chancellor.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 17

Campus Response We concur. The campus will establish a public relations policy applicable to its auxiliary organizations and maintain this policy on file with the Office of the Chancellor. Anticipated Completion Date: December 31, 2003 CONFLICT OF INTEREST

The campus had not provided guidance for its auxiliaries regarding the implementation of conflict-of- interest policies and procedures, including statements and disclosures from board members, management, and principal investigators for applicable federal and non-governmental projects. Each auxiliary on campus addressed, in some manner, conflict-of-interest requirements placed upon auxiliaries by the Education Code and Title 5. However, such policies and procedures should also consider the following areas:

Conflict-of-interest procedures. Records of proceedings relating to a possible or actual conflict. Compensation. Annual statements. Periodic reviews. Use of outside experts. Duty to disclose. Determination whether a conflict of interest exists. Actions required in association with a conflict. Actions to be taken when violations of conflict-of-interest policy are discovered.

Education Code §89906 states that no member of the governing board of an auxiliary organization shall be financially interested in any contract or other transaction entered into by the board of which he is a member, and any contract or transaction entered into in violation of this section is void. Title 5 §42401, §42402, §42500 and Education Code §89900 establish a responsibility to operate in accordance with sound business practices in the interest of the campus. Sound business practice mandates establishing conflict-of-interest policies and procedures to implement Education Code §89906 and other similar provisions to prevent imprudent or improper decisions by auxiliary board and management members. Code of Federal Regulations (CFR) Title 42, Part 50.604, Institutional Responsibility Regarding Conflicting Interests of Investigators, states, in part, that each institution must (a) maintain an appropriate written, enforced policy on conflict of interest and inform each investigator of that policy, the investigator’s reporting responsibilities, and of these regulations; (b) designate an institutional official(s) to solicit and review financial disclosure statements from each investigator who is planning to participate in Public Health Service (PHS) funded research; (c)(1) require that by the time an application is submitted to PHS, each investigator who is planning to participate in the PHS-funded research has submitted to the designated official(s) a listing of his/her known significant financial

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 18

interests (and those of his/her spouse and dependent children) (i) that would reasonably appear to be affected by the research for which PHS funding is sought and (ii) in entities whose financial interests would reasonably appear to be affected by the research. The National Institutes of Health (NIH) Grants Policy Statement, Part II, Conflict of Interest, states, in part, that NIH requires grantees and investigators to comply with the requirements of 42 CFR, Part 50, Subpart F, “Responsibility of Applicants for Promoting Objectivity in Research for which NIH Funding is Sought,” pertaining to investigators’ actual or potential conflicts of interest. The National Science Foundation (NSF) Grant Policy Manual §510, states, in part, that an institutional conflict-of-interest policy should require that each investigator disclose to a responsible representative of the institution all significant financial interests of the investigator (including those of the investigator’s spouse and dependent children) (i) that would reasonably appear to be affected by the research or educational activities funded or proposed for funding by NSF or (ii) in entities whose financial interests would reasonably appear to be affected by such activities. California State University (CSU) directive, Faculty and Staff Relations – Office of the Chancellor (FSR) 86-05(P), Principal Investigator – Fair Political Practices Commission (FPPC), Approval List of Non-Profit Organization, dated July 11, 1986, indicates that employees with principal responsibility for research projects funded in any part by a contract or grant from a non-governmental entity, including non-profit organizations, are required to file financial disclosure statements. The associate vice president of business and financial services indicated that the need for a policy may have been overlooked. Failure to adequately address implementation of conflict-of-interest code policies and procedures for auxiliary boards and management increases liability for acts contrary to the code.

Recommendation 2 We recommend that the campus provide guidance for its auxiliaries with regard to strengthening and further documenting conflict-of-interest policies and procedures. Campus Response We concur. The campus will provide guidance for its auxiliaries with regard to strengthening and further documenting conflict-of-interest policies and procedures. Anticipated Completion Date: December 31, 2003

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 19

ROYALTY PAYMENTS The campus had not developed sufficient and appropriate written policies and procedures concerning royalties paid to faculty members for the reproduction and sale of their own copyrighted materials. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates that policies and procedures concerning royalties paid to faculty members be properly documented. The associate vice president of business and financial services indicated that the lack of policy was due to oversight. Failure to fully develop and communicate written policies and procedures weakens internal controls and increases the risk that misunderstandings will occur. Recommendation 3 We recommend that the campus establish sufficient and appropriate written policies and procedures concerning royalties paid to faculty members. Campus Response We concur. The campus will establish sufficient and appropriate written policies and procedures concerning royalties paid to faculty members. Anticipated Completion Date: December 31, 2003

TRUSTS AND OTHER LIABILITIES

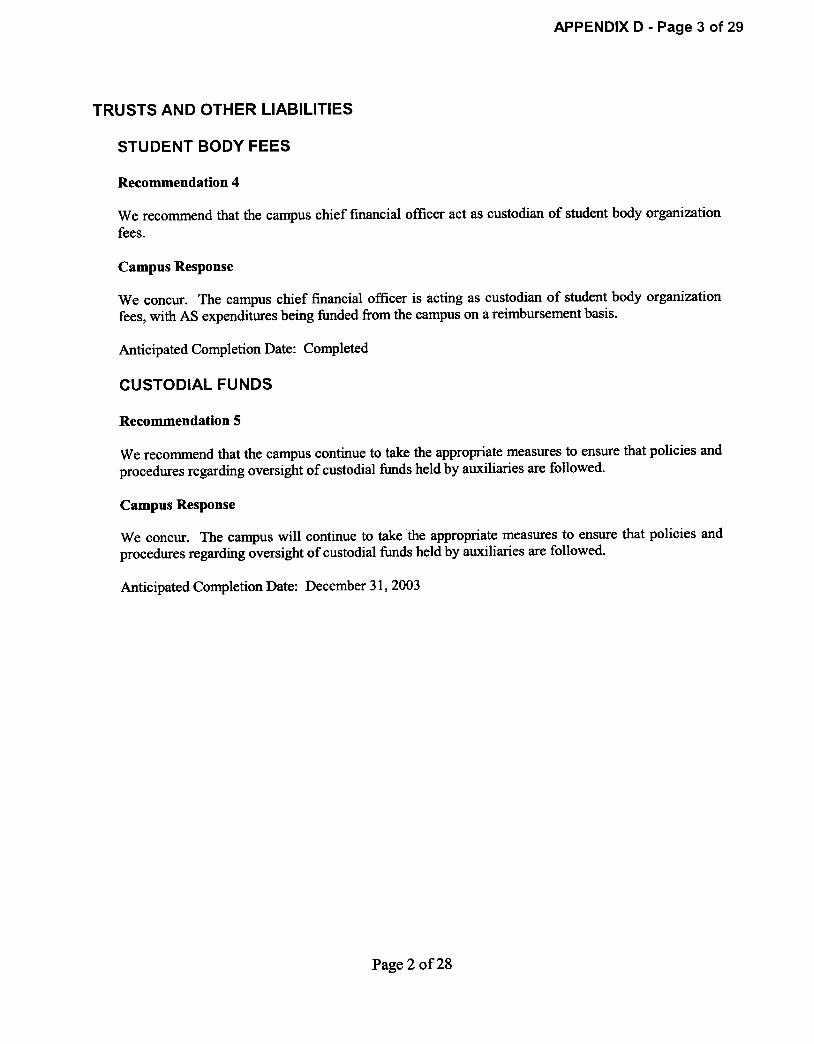

STUDENT BODY FEES The chief fiscal officer of the campus was not acting as custodian of student body organization fees. The campus collects Associated Students, California State University, Hayward (AS) student body fees and immediately transmits these monies to AS. AS then invests and disburses the fees and other revenue from their organizational banking and investment accounts and acts as custodian of the funds. Title 5 §42403(a) requires the campus chief fiscal officer to manage and serve as custodian of student body fees.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 20

The associate vice president of business and financial services indicated that the campus provided oversight by acting as an authorized signer for all AS disbursements. He further indicated that custody of these funds was just recently transferred to the control of AS. Insufficient control and accounting over student body funds increase the risk that custodial responsibilities are not met and increase the risk of error or misappropriation of funds. Recommendation 4 We recommend that the campus chief financial officer act as custodian of student body organization fees.

Campus Response We concur. The campus chief financial officer is acting as custodian of student body organization fees, with AS expenditures being funded from the campus on a reimbursement basis. Anticipated Completion Date: Completed CUSTODIAL FUNDS The campus did not exercise sufficient control over custodial funds held in trust by its auxiliaries. Funds were held in trust by three of the four campus auxiliary organizations on behalf of student organizations, campus academics and administrators, and other entities. We found that: State revenues were held in trust accounts maintained at the California State University, Hayward

Foundation, Inc. (Foundation) and were not accurately recorded in state accounting records. Revenues and expenses associated with contracts and grants, excluding indirect cost revenues,

were recorded within an agency account on the statement of Foundation net assets, rather than reflected in the statement of activities. Additionally, the revenues and expenses were not reflected in the campus’s financial statements.

Foundation trust/agency agreements did not address the disposition of unexpended funds or

include disclosure of management fees (when applicable) or that (for certain types of accounts) interest earned would be retained by the Foundation.

Signature cards for several Foundation trust and agency accounts were not current. The

Foundation was in the process of updating signature cards during our review.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 21

Written trust agreements, which contain the purpose of the account, source of funds, disposition of unexpended funds, reporting requirements and describe the use of investment earnings as well as other restrictions, were not executed between AS and campus clubs. Student organization trust accounts were established solely on the approval of the office of student life and the completion of a signature card.

Negative student organization account balances were not periodically reviewed and cleared in a

timely manner. We noted eight student organizations with overdrawn account balances. Title 5 §42401, §42402, §42500 and Education Code §89900 establish a responsibility to operate in accordance with sound business practices in the interest of the campus. Education Code §89721 and various chancellor’s office mandates establish standards for such operations and related funds management. The CSU Investment Manual for California State University Trust Funds, Accounting Department Coded Memorandum (AD) 97-08, indicates that all CSU trust fund money, pending disbursement for its intended purpose, will be managed in custodial accounts in the name of the CSU system. The associate vice president of business and financial services stated that the campus had recently issued auxiliary organization policies and procedures that specifically address the administration of custodial funds held by auxiliaries. A lack of sufficient oversight over custodial funds held by auxiliaries exposes the campus and the CSU system to regulatory and legal consequences. Recommendation 5 We recommend that the campus continue to take the appropriate measures to ensure that policies and procedures regarding oversight of custodial funds held by auxiliaries are followed.

Campus Response We concur. The campus will continue to take the appropriate measures to ensure that policies and procedures regarding oversight of custodial funds held by auxiliaries are followed. Anticipated Completion Date: December 31, 2003

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 22

CALIFORNIA STATE UNIVERSITY, HAYWARD FOUNDATION, INC. LEGAL AND REGULATORY COMPLIANCE

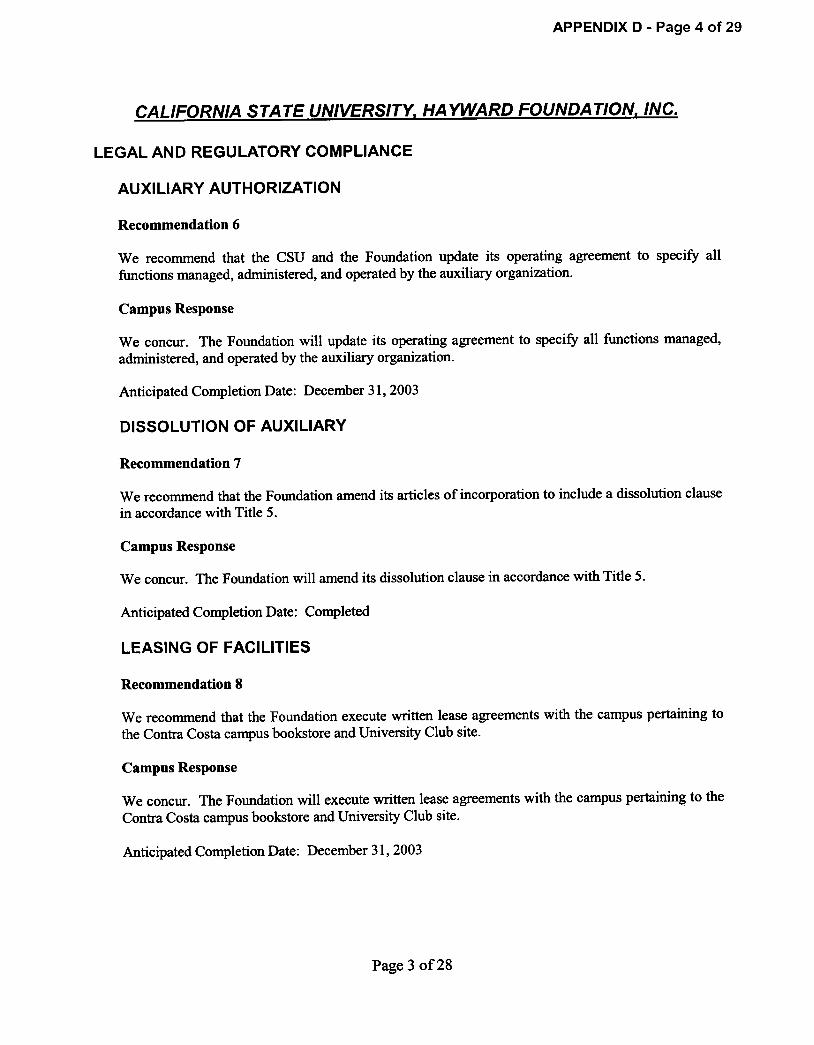

AUXILIARY AUTHORIZATION The California State University, Hayward Foundation, Inc. (Foundation) operating agreement with the California State University (CSU) required revision as to functions managed, administered, and operated by the auxiliary organization. Functions not articulated in the operating agreement included the Foundation’s acquisition and development of real and personal property, public relations activities, and fiscal management services related to trust and similar funds. Title 5 §42501 states that a written agreement on behalf of the State of California by the Chancellor of The California State University and Colleges and the auxiliary organization is required for the performance by such auxiliary organization of any of the functions listed in §42500. Title 5 §42502 states that the operating agreement should specify the function or functions that the organization is to manage, operate, or administer. The Foundation interim executive director indicated that management was unaware of the need to update the language in the operating agreement, as the Foundation’s activities had not changed since the operating agreement was executed in 1994. Operating in the absence of an up-to-date, written agreement increases the risk of misunderstandings and miscommunication regarding rights and responsibilities. Recommendation 6 We recommend that the CSU and the Foundation update its operating agreement to specify all functions managed, administered, and operated by the auxiliary organization. Campus Response We concur. The Foundation will update its operating agreement to specify all functions managed, administered, and operated by the auxiliary organization. Anticipated Completion Date: December 31, 2003

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 23

DISSOLUTION OF AUXILIARY The Foundation’s articles of incorporation did not specify that the net assets of the dissolved auxiliary must be distributed to a successor approved by the campus president and the CSU Trustees. Title 5 §42600(b) states that upon dissolution of the organization, net assets, other than trust funds, shall be distributed to a successor approved by the president of the campus and by the Board of Trustees. The Foundation interim executive director indicated that the non-compliant dissolution clause was due to oversight. The lack of a dissolution clause in accordance with Title 5 could result in net assets not being properly distributed in the event the corporation is dissolved. Recommendation 7 We recommend that the Foundation amend its articles of incorporation to include a dissolution clause in accordance with Title 5. Campus Response We concur. The Foundation will amend its dissolution clause in accordance with Title 5. Anticipated Completion Date: Completed LEASING OF FACILITIES Certain Foundation lease and sublease arrangements were not properly supported by written agreements. We found that the Foundation had no facilities or ground lease agreements with the campus pertaining to the Contra Costa campus bookstore and University Club site. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates that facility lease arrangements be properly supported by written agreements. The campus vice president of administration and business affairs indicated that the campus was in the process of executing the Contra Costa bookstore lease. He further stated that the lack of a ground lease for the University Club site was due to oversight.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 24

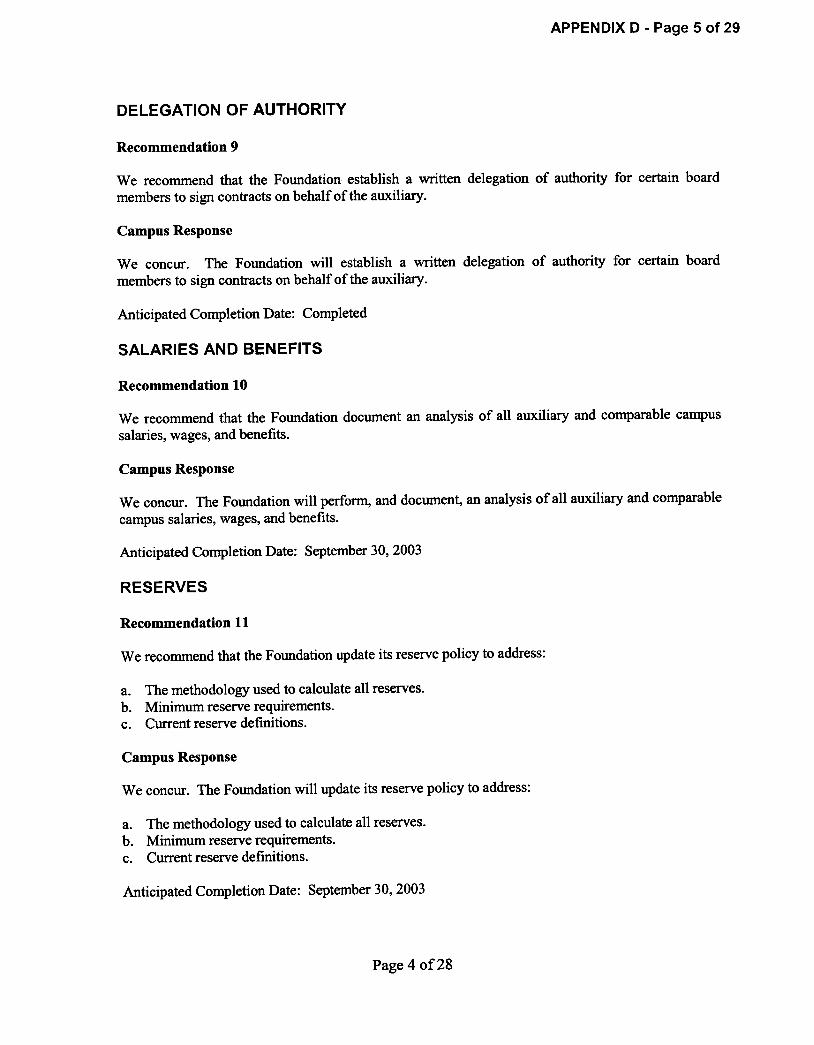

The absence of written agreements increases the risk of misunderstandings and miscommunication regarding rights and responsibilities. Recommendation 8 We recommend that the Foundation execute written lease agreements with the campus pertaining to the Contra Costa campus bookstore and University Club site. Campus Response We concur. The Foundation will execute written lease agreements with the campus pertaining to the Contra Costa campus bookstore and University Club site. Anticipated Completion Date: December 31, 2003 DELEGATION OF AUTHORITY The Foundation had not established a written delegation of authority for certain board members to sign contracts on behalf of the auxiliary. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates that signature authority be delegated by official policy and action and be conveyed in written documents, authorizing named individuals to sign specific types of agreements on behalf of the organization. The Foundation interim executive director indicated that the lack of written authorization was due to oversight. The lack of a written delegation of authority to sign contracts on behalf of the auxiliary increases misunderstandings and may increase legal liability. Recommendation 9 We recommend that the Foundation establish a written delegation of authority for certain board members to sign contracts on behalf of the auxiliary. Campus Response We concur. The Foundation will establish a written delegation of authority for certain board members to sign contracts on behalf of the auxiliary. Anticipated Completion Date: Completed

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 25

SALARIES AND BENEFITS The Foundation had not documented an analysis of full-time employee salaries, wages, and benefits between its employees and campus employees serving in similar positions. Title 5 §42405 states that the governing board of each auxiliary organization shall provide salaries, working conditions, and benefits for its full-time employees, which are comparable to those provided campus employees performing substantially similar services. For those full-time employees who perform services that are not substantially similar to the services performed by campus employees, the salaries established shall be at least equal to the salaries prevailing in other educational institutions in the area or commercial operations of like nature. The Foundation interim executive director indicated management was unaware that a written comparison was required, although the Foundation diligently updated its salary ranges and benefits to mirror campus salaries and benefits. Failure to fully document the comparative analysis of positions increases the risk that the auxiliary may be expending inappropriate amounts on salaries and benefits for employees who perform substantially similar services as employees for the campus and other organizations. Recommendation 10 We recommend that the Foundation document an analysis of all auxiliary and comparable campus salaries, wages, and benefits. Campus Response We concur. The Foundation will perform, and document, an analysis of all auxiliary and comparable campus salaries, wages, and benefits. Anticipated Completion Date: September 30, 2003 RESERVES The Foundation reserve policy required updating. We noted that certain: Reserve definitions did not specify the methodology used for the calculation of reserves. Reserve definitions did not include minimum reserve requirements. Reserve definitions were inconsistent with the reserves defined in the reserve policy.

Education Code §89904(b), §89904.5, and §89905 indicate that adequate reserve planning is necessary.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 26

The Foundation interim executive director indicated that the lack of specificity in the reserve definitions regarding calculations and minimum reserve requirements was due to oversight. She further stated that management believed the annual board review and update of the reserve definitions sufficiently constituted a change in the reserve policy. Insufficient reserve planning and analysis increase the auxiliary’s risk to fund future needs. Recommendation 11 We recommend that the Foundation update its reserve policy to address: a. The methodology used to calculate all reserves. b. Minimum reserve requirements. c. Current reserve definitions. Campus Response We concur. The Foundation will update its reserve policy to address: a. The methodology used to calculate all reserves. b. Minimum reserve requirements. c. Current reserve definitions. Anticipated Completion Date: September 30, 2003 RISK MANAGEMENT Certain Foundation contracts did not indemnify the campus or CSU Trustees. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates that contracts contain essential clauses, including indemnification clauses that indemnify all appropriate parties. The Foundation interim executive director indicated that the lack of an adequate indemnification clause was the result of attorney oversight. The lack of appropriate indemnification clauses in contracts increases the auxiliary’s exposure to potential liability. Recommendation 12 We recommend that the Foundation ensure that contracts include appropriate indemnification clauses.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 27

Campus Response We concur. The Foundation will ensure that contracts include appropriate indemnification clauses. Anticipated Completion Date: December 31, 2003 NON-DISCRIMINATION POLICIES

The Foundation’s current non-discrimination policy did not address discrimination based on pregnancy or veterans’ status. Executive Order (EO) No. 774, Systemwide Guidelines for Nondiscrimination and Affirmative Action Programs in Employment, dated May 17, 2001, prohibits “discrimination on the basis of race, color, religion, national origin, sex, sexual orientation, marital status, pregnancy, age, disability, and covered veterans’ status.” The Foundation interim executive director indicated that management was unaware that the policy was incomplete. An inadequate non-discrimination policy increases the auxiliary’s risk of non-compliance with state and federal laws and may result in regulatory actions. Recommendation 13 We recommend that the Foundation revise its non-discrimination policy in accordance with CSU policy. Campus Response We concur. The Foundation will revise its non-discrimination policy in accordance with CSU policy. Anticipated Completion Date: Completed ADMINISTRATIVE SERVICES AGREEMENT The Foundation had not executed a written agreement for fiscal and accounting services provided to the Cal State Hayward Educational Foundation (Educational Foundation) and for payroll-related services associated with campus instructionally related activity (IRA) funds. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates that written agreements be executed which fully define the expectations, rights, and responsibilities of the parties involved.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 28

The Foundation interim executive director indicated that the Foundation assumed the Educational Foundation accounting duties at the request of the campus and that due to the urgent need for the Foundation to take over these duties, a written agreement was not executed. The absence of written agreements increases the risk of misunderstandings and miscommunication regarding rights and responsibilities. Recommendation 14 We recommend that the Foundation establish a written agreement for fiscal and accounting services provided to the Educational Foundation and for payroll-related services associated with campus IRA funds. Campus Response We concur. The Foundation will establish a written agreement for fiscal and accounting services provided to the Educational Foundation and for payroll-related services associated with campus IRA funds. Anticipated Completion Date: December 31, 2003 SEGREGATION OF DUTIES

The Foundation did not appropriately segregate certain accounting functions for bookstore purchasing and payroll and human resources.

Bookstore Purchasing

We found that the same individual was responsible for ordering and receiving bookstore merchandise. The Foundation bookstore general manager indicated that the lack of segregation of duties is due to the small number of shipping/receiving staff. Payroll and Human Resources We found that: The Foundation payroll clerk was responsible for entering new personnel, making personnel

The AS office manager was responsible for entering new AS/University Union of California State

University, Hayward (Union) personnel, making personnel master file changes (wage rate, address changes, etc.), entering benefits information, processing payroll, approving payroll of employees under her supervision, verifying payroll accuracy, and disbursement of payroll checks.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 29

The Foundation payroll manager stated that resource constraints did not allow for an appropriate separation of duties between the human resource and payroll functions. EO No. 698, Board of Trustees Policy for The California State University Auxiliary Organizations, dated March 3, 1999, states that the review of auxiliary organizations will be used to determine appropriate separation of duties, safeguarding of assets, and reliability and integrity of information. Inadequate segregation of duties increases the risk that errors and irregularities will not be detected in a timely manner. Recommendation 15 We recommend that the Foundation properly segregate accounting functions for bookstore purchasing and payroll and human resources or institute mitigating procedures approved by the campus.

Campus Response We concur. The Foundation will segregate accounting functions for bookstore purchasing and payroll and human resources or institute mitigating procedures approved by the campus. Anticipated Completion Date: December 31, 2003

CASH RECEIPTS AND HANDLING

Certain controls over Foundation cash handling were insufficient. Cash Room We noted the following:

Without escort, cash receipts were transported from auxiliary entities to the bookstore customer service counter.

A sufficient written record of the names of individuals who had access to the cash room and the

date the combination was last changed was not maintained. The cash room combination was last changed over two years ago despite the departure of three

employees within the last year. The Foundation interim executive director indicated that the Foundation believed that current cash room practices were sufficient.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 30

Bookstore We found that the customer service safe and change drawer was not adequately secured. The key was maintained in an unlocked drawer at a customer service workstation and was accessible to all employees during work hours. The Foundation bookstore general manager indicated that the failure to adequately secure the key was due to oversight. Contra Costa Campus Bookstore Cash Room We noted the following: Cash receipts were hand carried unsecured from the Contra Costa bookstore to the California State University, Hayward (CSUH) bookstore cash office.

A sufficient written record of the names of individuals who had access to the cash room safe and the date the combination was last changed was not maintained.

The Foundation bookstore general manager indicated that cash controls at the Contra Costa bookstore should be similar to those at the campus; however, due to the remote location, certain procedures may not be consistently adhered to. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice requires sufficiently controlled cash handing and movement procedures for the exchange of funds. Sound business practice also mandates that a record be kept showing the date the combination was last changed and the names of individuals knowing the present combination. Inadequate controls over cash handling increase the risk of a loss or misappropriation of funds. Recommendation 16 We recommend that the Foundation improve cash handling controls by: a. Increasing the level of security present when transporting cash funds. b. Establishing procedures to ensure that a record is maintained of individuals having cash room

combinations and the date the combinations were last changed. c. Ensuring the combination to the cash room is changed when staffing changes occur. d. Adequately securing the customer service safe and change drawer keys.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 31

Campus Response We concur. The Foundation will improve cash handling controls related to: a. Level of security when transporting cash funds. b. Maintaining a record of individuals having combinations and the date the combinations were last

changed.

c. Ensuring the safe combination is changed when staffing changes occur.

d. Securing the customer service safe and change drawer keys. Anticipated Completion Date: December 31, 2003

PETTY CASH AND CHANGE FUNDS PETTY CASH FUNDS The Foundation had not documented petty cash fund policies and procedures which required provisions for performing periodic and independent, unannounced cash counts. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates that periodic and independent, unannounced counts be performed to ensure that assets are sufficiently safeguarded. The Foundation interim executive director indicated that, although procedures did not reference periodic and independent cash counts, informal counts of these funds were performed periodically. Failure to fully develop and communicate written policies and procedures weakens internal controls and increases the risk that misunderstandings will occur. Recommendation 17 We recommend that the Foundation develop written petty cash fund policies and procedures which require periodic and independent, unannounced cash counts.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 32

Campus Response We concur. The Foundation will document petty cash fund policies and procedures which require periodic and independent, unannounced cash counts. Anticipated Completion Date: December 31, 2003 CHANGE FUNDS The Foundation bookstore textbook buyback change fund was inappropriately used to extend advances to employees. We noted six advances (totaling $1,500) that were made from the textbook buyback change fund. These advances dated back to 1999 and were supported by IOU documents signed by the advance recipients. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates that change funds be sufficiently controlled and used for their intended purpose. The Foundation interim executive director indicated that she was aware of the situation and believed the advances had been cleared. She further indicated that existing policy prohibits advances from Foundation change funds. Inadequate controls over change funds increase the risk that misappropriated funds will not be detected in a timely manner. Recommendation 18 We recommend that the Foundation: a. Take appropriate measures to ensure that the practice of issuing advances from change funds is

discontinued. b. Seek immediate repayment of outstanding cash advances.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 33

Campus Response We concur. The Foundation will: a. Discontinue issuing advances from change funds. b. Seek immediate repayment of outstanding cash advances. Anticipated Completion Date: Completed

INVESTMENTS

Foundation written investment policies and procedures did not address controls over the transfer of investment funds. Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates detailed instructions regarding the transfer of investment funds. The Foundation controller stated that the failure to include instructions regarding the transfer of investment funds was due to oversight. Failure to fully develop and communicate written policies and procedures weakens internal controls and increases the risk that misunderstandings will occur.

Recommendation 19

We recommend that the Foundation update its written investment policies and procedures to include controls over the transfer of investment funds.

Campus Response We concur. The Foundation will update its written investment policies and procedures to include controls over the transfer of investment funds. Anticipated Completion Date: Completed

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 34

FEES, REVENUES, AND RECEIVABLES ACCOUNTS RECEIVABLE Certain controls over Foundation accounts receivable were inadequate. We found that: Collection efforts over inter-auxiliary accounts receivable required improvement. We noted approximately $30,000 of Union and AS receivables that had been outstanding since 1999.

Accounts receivable reconciliations were not signed and dated by the preparer and reviewer.

Title 5 §42401 and §42402 indicate that the campus president shall require that auxiliary organizations operate in conformity with policy of the Board of Trustees and the campus. One of the objectives of the auxiliary organizations is to provide fiscal procedures and management systems that allow effective coordination of the auxiliary activities with the campus in accordance with sound business practices. Sound business practice mandates policies and procedures over, and management oversight of, accounts receivable. The Foundation interim executive director indicated that the receivables due from AS and the Union remained outstanding because there was a question as to the validity of these receivables. The Foundation controller indicated that the failure to sign and date the accounts receivable reconciliations every month was due to workload issues. Insufficient controls over accounts receivable increase the risk of loss, errors, and irregularities. Recommendation 20 We recommend that the Foundation: a. Take immediate action to recover long-outstanding accounts receivable or use appropriate

write-off measures to bring accounts current. b. Take appropriate measures to improve inter-auxiliary accounts receivable collection efforts.

c. Ensure that all accounts receivable reconciliations are signed and dated by the preparer and the

reviewer. Campus Response We concur. The Foundation will: a. Take immediate action to recover long-outstanding accounts receivable or use appropriate

write-off measures to bring accounts current.

OBSERVATIONS, RECOMMENDATIONS, AND CAMPUS RESPONSES

Auxiliary Organizations/California State University, Hayward/Report No. 02-52 Page 35

b. Take appropriate measures to improve inter-auxiliary accounts receivable collection efforts.