Page 1

Aviation Economics & Finance

Professor David Gillen (University of British Columbia )&Professor Tuba Toru-Delibasi (Bahcesehir University)

Module 11 : 26 November 2015Istanbul Technical UniversityAir Transportation Management M.Sc. Program

Page 2

OUTLINE

• Introduction

• Mergers and Acquisitions (M&A)

• Process and Issues

• Economics of M&A

• Introduction to competition policy and regulation

– rationale for competition policy

– origins and historical development

– regimes: EU, UK, USA and TR

– utility privatisation and regulation

• Examples3

November 23-28

Page 3

A. INTRODUCTION

November 23-28 4

Page 4

• The airline industry is cyclical and its performance is closely linked to

the gross domestic product (GDP).

Figure 1: GDP Growth and TK Air Traffic Growth

TURKISH AIRLINE STRATEGY

5November 23-28

Page 5

US AND WORLD’S GDP 2004-2012

6November 23-28

Page 6

Figure 2: Turkish Airlines Total Passengers and Net Income

TURKISH AIRLINES STRATEGY

7November 23-28

Page 7

• Competitive Cost Structure

Figure 3: Network Development of Turkish Airlines

TURKISH AIRLINES STRATEGY

8November 23-28

Page 8

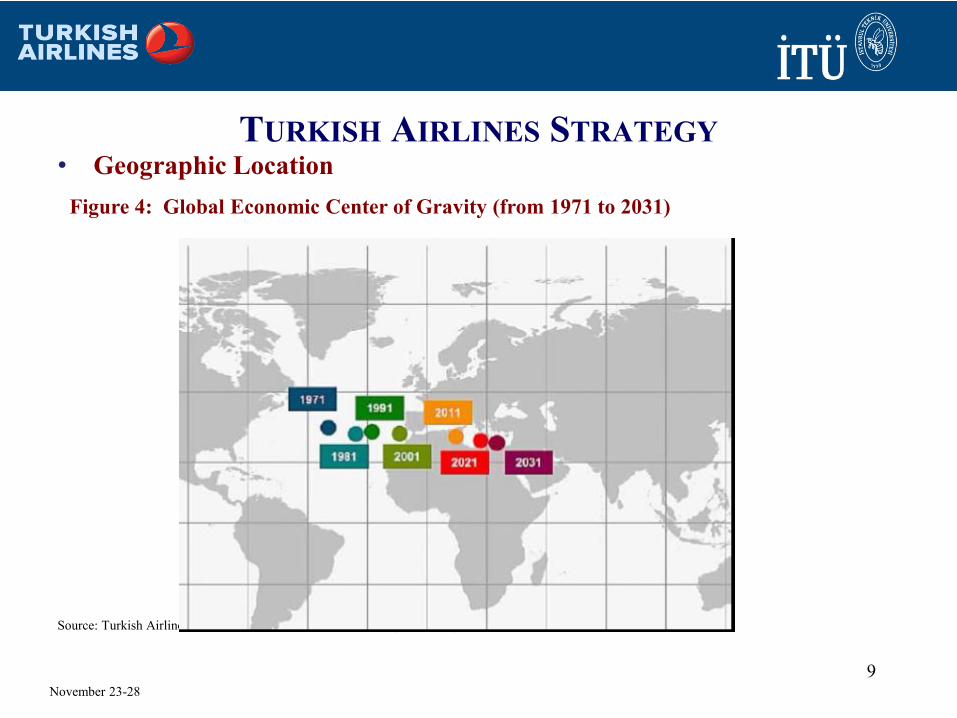

• Geographic Location

Figure 4: Global Economic Center of Gravity (from 1971 to 2031)

Source: Turkish Airlines from Airbus Global Market Forecast (2012-2031)

TURKISH AIRLINES STRATEGY

9November 23-28

Page 9

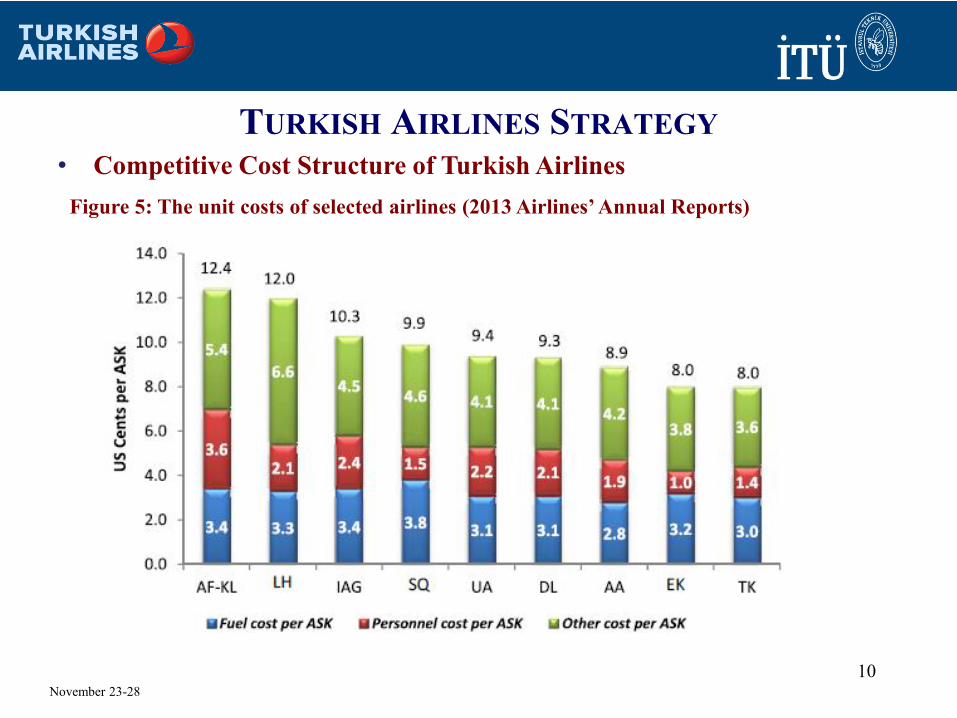

• Competitive Cost Structure of Turkish Airlines

Figure 5: The unit costs of selected airlines (2013 Airlines’ Annual Reports)

TURKISH AIRLINES STRATEGY

10November 23-28

Page 10

AIRLINE COOPERATION AND CONSOLIDATION

• Aviation is a fast changing world – Ethiad has teamed with Air France/KLM.

– Qatar Airways is now firmly part of Oneworld

– Rumors: Emirates and Lufthansa are talking

• Turkish has chosen to not use mergers as a strategy,

and only uses weak alliances– TK could change strategy

– Future success is highly dependent on negotiationg new bilateral

rights to further expand its hub network

11November 23-28

Page 11

MANY FORMS OF COOPERATION POSSIBLE

• Code-sharing agreements between two

airlines

• Membership in global airline alliances

• Joint ventures to share both revenues and

costs

• Mergers and acquisitions

12November 23-28

Page 12

B. MERGERS AND ACQUISITIONS

November 23-28 13

Page 13

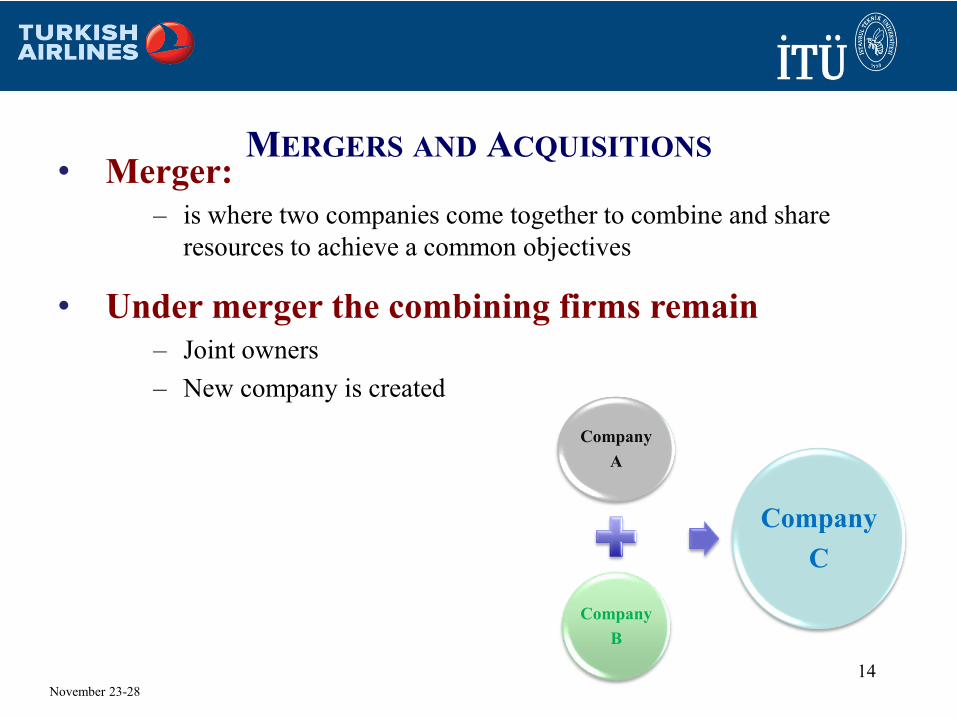

MERGERS AND ACQUISITIONS• Merger:

– is where two companies come together to combine and share

resources to achieve a common objectives

• Under merger the combining firms remain

– Joint owners

– New company is created

Company

A

Company

B

Company

C

14November 23-28

Page 14

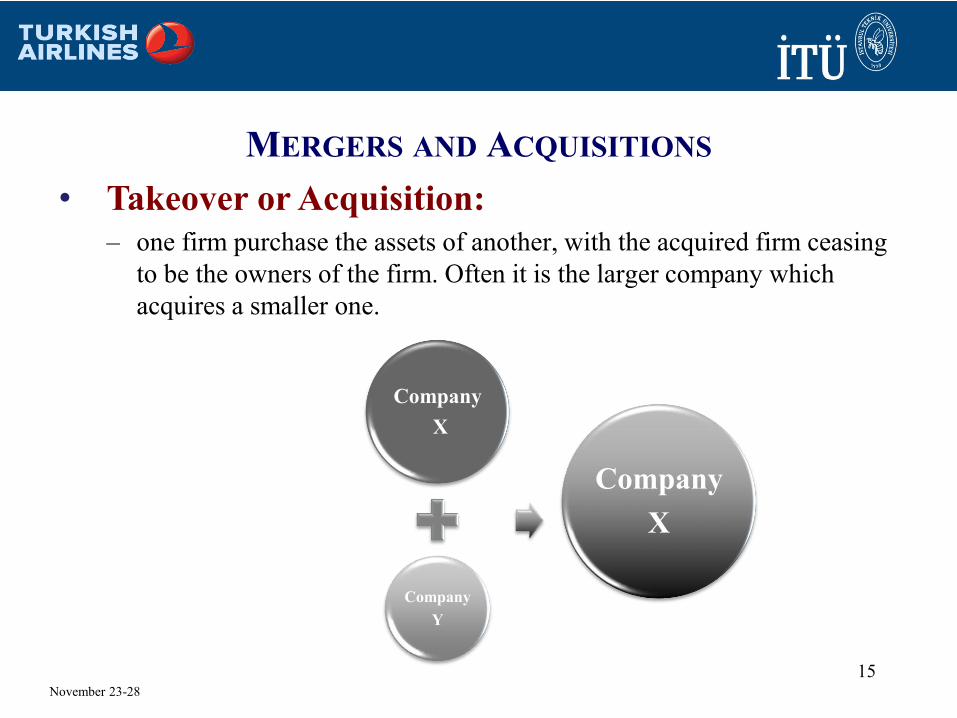

MERGERS AND ACQUISITIONS

• Takeover or Acquisition:

– one firm purchase the assets of another, with the acquired firm ceasing

to be the owners of the firm. Often it is the larger company which

acquires a smaller one.

Company

X

Company

Y

Company

X

15November 23-28

Page 15

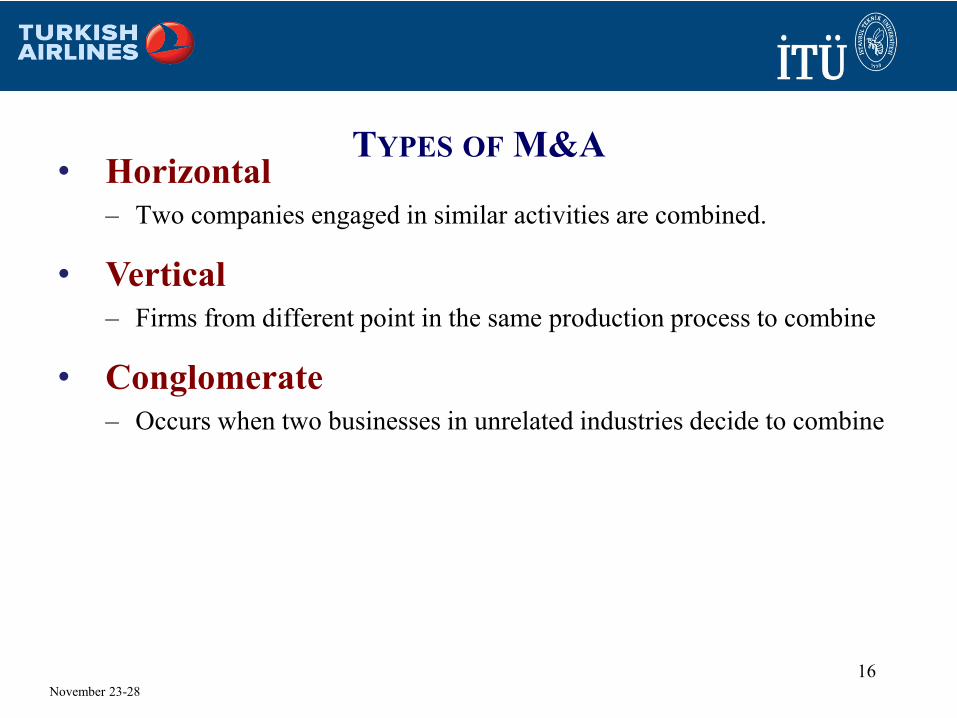

TYPES OF M&A• Horizontal

– Two companies engaged in similar activities are combined.

• Vertical

– Firms from different point in the same production process to combine

• Conglomerate

– Occurs when two businesses in unrelated industries decide to combine

16November 23-28

Page 16

GAINS FROM M&A• Increase market power

– To have access to another network

– Value creation by exploiting collusive synergies

• Operational gains– Reducing operational cost by synergy effects

• Economies of Scale– To enable benefits of scale to be achieved

– Better contracts with suppliers

17November 23-28

Page 17

FACTORS AFFECTING M&A ACTIVITY OF

AIRLINES• Airline industry is a challenging industry with low profit margins and

high volatility of returns

Figure 6: EBIT margin and Net post-tax profit margin

Source: ICAO and IATA

18November 23-28

Page 18

FACTORS AFFECTING M&A ACTIVITY OF

AIRLINES• What was happening on TK side?

Table 2: TK Airlines summary profit and loss account (USD million): 2009-2013,

1H2013-1H2014

Source: Turkish Airlines

Income Statement

(million USD)

2009 2010 2011 2012 2013 1Q2013 1Q2014 13/12

Change

Operating Revenue 4552 5488 7070 8234 9826 2015 2315 19%

Operating Expenses

(-)

4058 5149 6855 7616 9249 2062 2418 21%

Operating Profit 494 299 215 618 577 -48 -102 -6.6%

Net Profit 362 185 11 657 357 -14 -102 -45.6%

Net profit

% of Revenue 7.9% 3.4% 0.15% 7.9% 3.6%

19November 23-28

Page 19

FACTORS AFFECTING M&A ACTIVITY OF

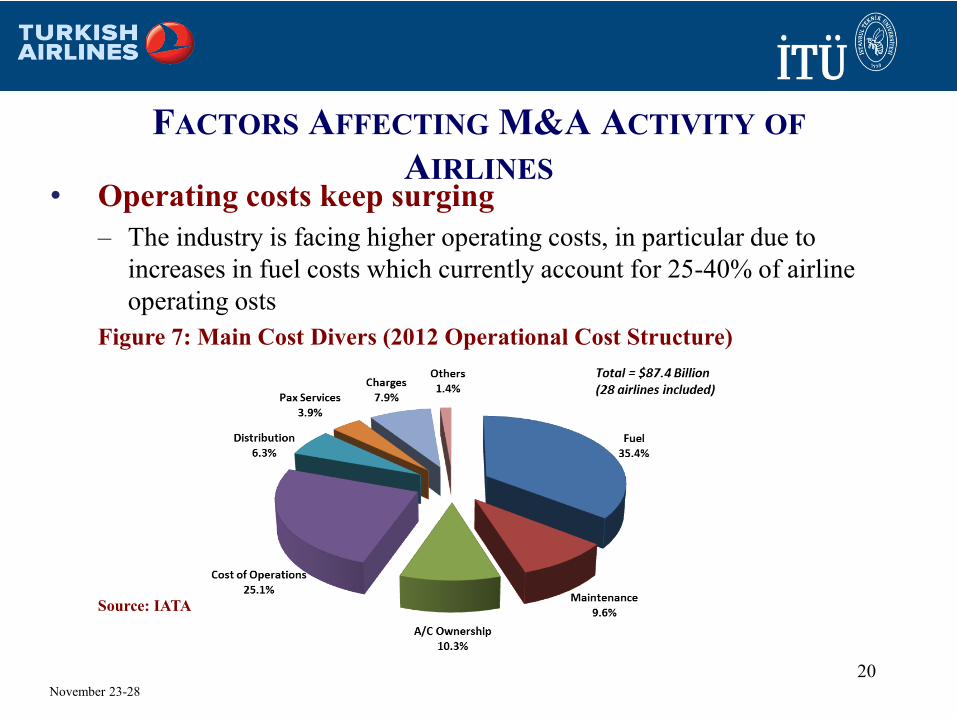

AIRLINES• Operating costs keep surging

– The industry is facing higher operating costs, in particular due to

increases in fuel costs which currently account for 25-40% of airline

operating osts

Figure 7: Main Cost Divers (2012 Operational Cost Structure)

Source: IATA

20November 23-28

Page 20

FACTORS AFFECTING M&A ACTIVITY OF

AIRLINES• Saving fuel costs

Figure 8: Fuel efficiency and the price of jet fuel

21November 23-28

Page 21

FACTORS AFFECTING M&A ACTIVITY OF

AIRLINES

• Bankruptcies

– Cost advantage due to economics of scale and scope

– Higher demand due to better connectivity, greater range of destinations

and increased service frequenct

• High incidence of bankruptcies in the airline

industry following deregulation

– Continuing trend among major carriers to restructure under bankruptcy

protection in the US

22November 23-28

Page 22

• Mergers and acquisitions (M&A) are complex, involving

many parties.

• Mergers and acquisitions involve many issues, including

– Corporate governance.

– Form of payment.

– Legal issues.

– Contractual issues.

– Regulatory approval.

• M&A analysis requires the application of valuation tools

to evaluate the M&A decision.

MERGERS AND ACQUISITIONS (M&A)

23November 23-28

Page 23

Country Limits on foreign ownership

Australia-New Zealand 49% for airlines engaged in international operations, 100% for

solely domestic

Canada, Mexico 25%

China 35%

Chile 100% as long as airline’s principle place of business is in Chile

EU 49%, applies to non-EU citizens

India 49%, but foreign airlines cannot hold shares in Indian airlines

Japan, Taiwan 33.33%

Korea 49%

Malaysia 45%

Singapore 27.51%

Thailand 30%

United States 25%, one-third of the board of directors, chairman/woman,

CEO/president must be US national

Turkey Majority of the shares must be hold by Turkish national24

November 23-28

Page 24

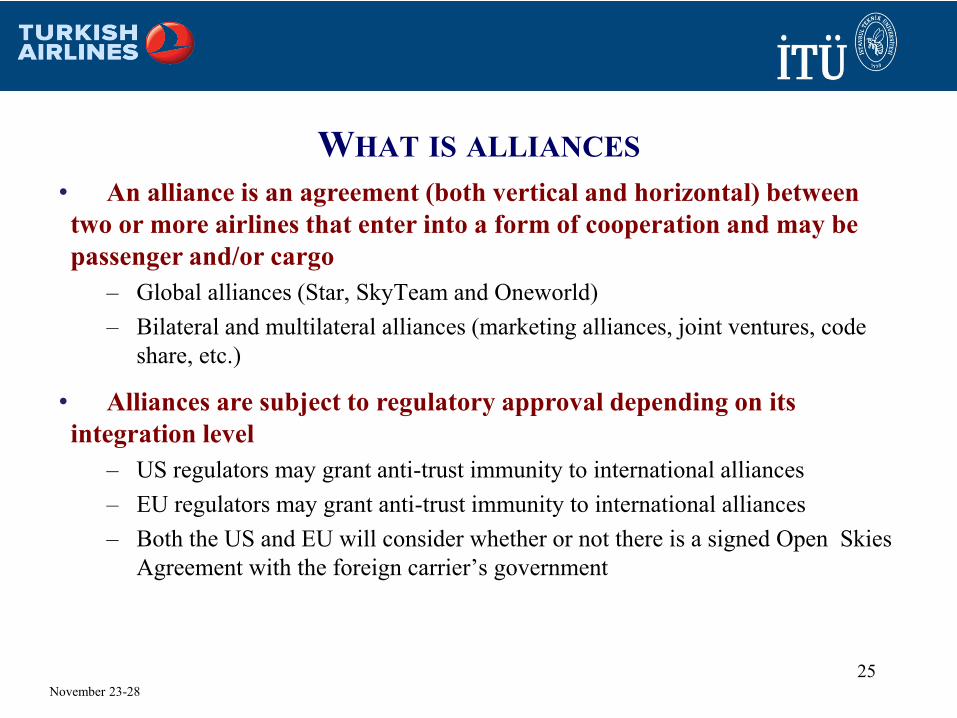

WHAT IS ALLIANCES

• An alliance is an agreement (both vertical and horizontal) between

two or more airlines that enter into a form of cooperation and may be

passenger and/or cargo

– Global alliances (Star, SkyTeam and Oneworld)

– Bilateral and multilateral alliances (marketing alliances, joint ventures, code

share, etc.)

• Alliances are subject to regulatory approval depending on its

integration level

– US regulators may grant anti-trust immunity to international alliances

– EU regulators may grant anti-trust immunity to international alliances

– Both the US and EU will consider whether or not there is a signed Open Skies

Agreement with the foreign carrier’s government

25November 23-28

Page 25

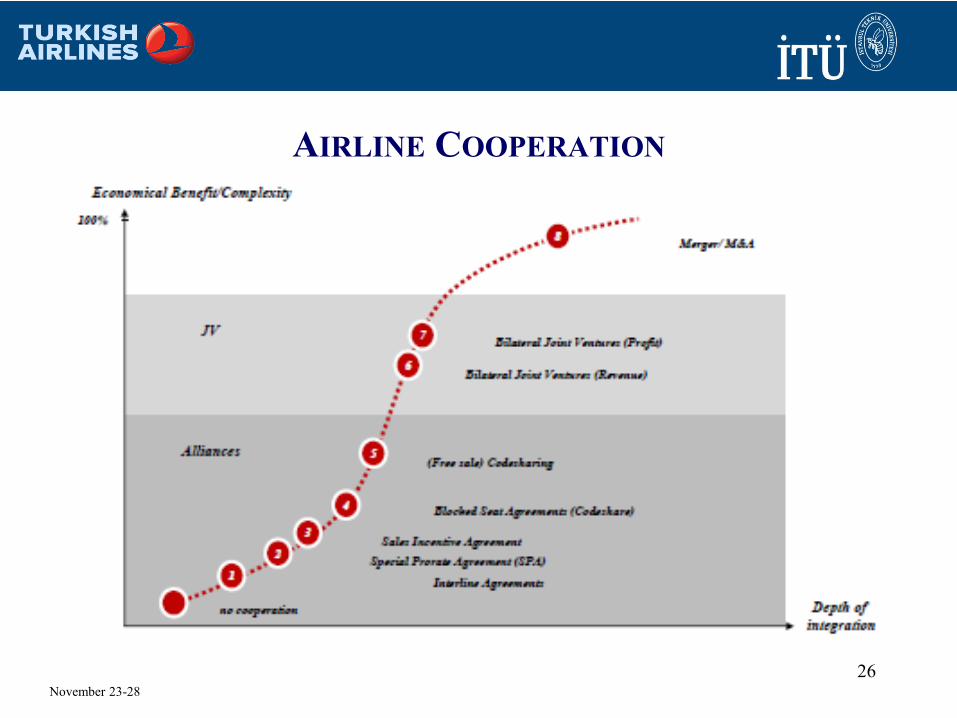

AIRLINE COOPERATION

26November 23-28

Page 26

METAL-NEUTRAL JOINT VENTURES

27

• Metal-neutral joint ventures

– High degree of integration

– The most intensive form of an airline alliance

– Revenue & profit sharing

– Joint setting of prices and schedules

– Similar to a merger but no ownership transfer

• Metal-neutral joint ventures in major aviation markets

– Transatlantic

• Star A++ (Lufthansa Group, Air Canada, United/Continental)

• SkyTeam Joint Venture (Air France / KLM, Delta and Alitalia)

• Oneworld Joint Venture (American, British Airways / Iberia)

– Transpacific

• Star Joint Venture (United / Continental, ANA)

• Delta/Virgin Australia Joint Venture

• American / JAL Joint Venture

November 23-28

Page 27

WHY ALLIANCES?• Foreign ownership rules

– Many countries prohibit or limit ownership of domestic airlines.

International or cross-border mergers are rare. Instead, the benefits of a

merger can be achieved through an alliance.

• Restrictions on cabotage rights

– Countries generally restrict foreign airlines from operating domestic

service. There are exceptions (e.g. the European Union, Australia

allowing some cabotage as extension of long haul routes).

• Access to a larger global network

– Airlines can increase service frequency and number of destinations

served by participating in an alliance. Increased connectivity may

improve load factors.

28November 23-28

Page 28

WHY ALLIANCES?• Marketing cooperation

– Frequent Flyer Programs

– Codeshare Agreements

– Lounge Access

– etc.

• Cost synergies

– Shared airport facilities

– Joint scheduling

– Reciprocal sales arrangements

– Increased buyer power

• Decrease in competition

– Airline alliances have a potential to diminish or exclude competition.

– Pro- and anti-competitive effects will be discussed in Module 10.

29November 23-28

Page 29

TRENDS IN AIRLINE ALLIANCES

• Many major airlines have joined a major alliance grouping (Star,

SkyTeam or Oneworld)

– Over 50 carriers are members of one of the three major alliances

– These carriers represent two-thirds of industry’s ASKs

– LCCs begin to join global alliances. In 2012, Airberlin joined oneworld

• There is a tendency towards seeking deeper cooperation by airlines

via bilateral and multilateral alliances

– “metal neutral” joint ventures are a form of a super-alliance which is very

similar to a merger.

• Several major carrier that have deliberately avoided alliances seek

increased cooperation on a bilateral basis (e.g. Emirates, Etihad)

30November 23-28

Page 30

C. PROCESS AND ISSUES

November 23-28 31

Page 31

ETIHAD’S STRATEGIC PARTNERSHIPS

32November 23-28

Page 32

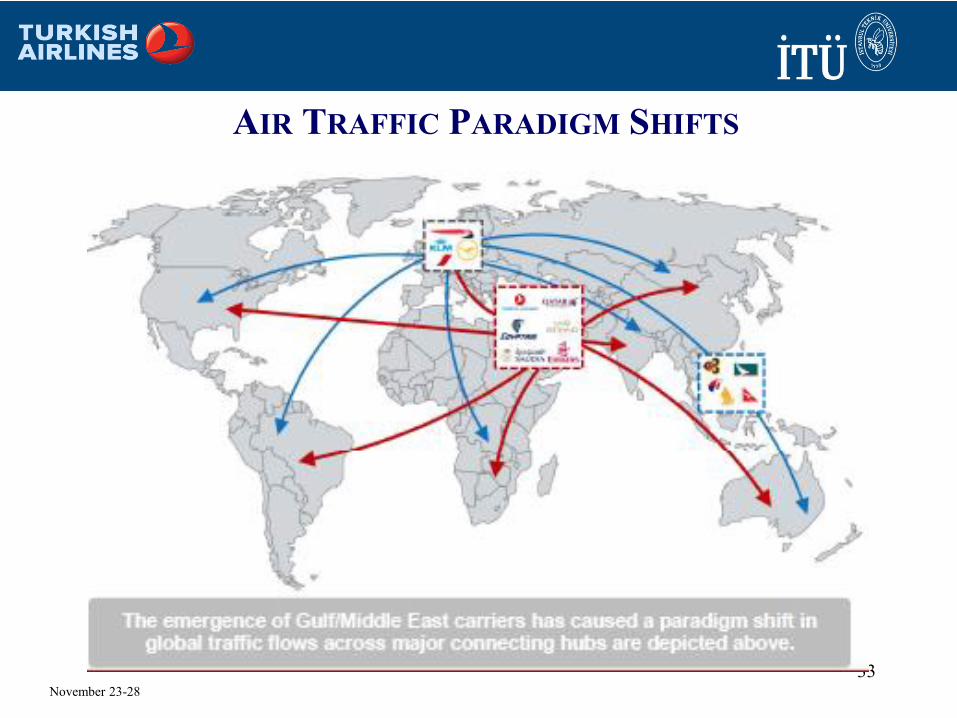

AIR TRAFFIC PARADIGM SHIFTS

33November 23-28

Page 33

QANTAS AND EMIRATES PARTNERSHIP

34

• Before

– Qantas had 5 one-stop destinations in Europe (via QF operations or

codeshares)

– No service to Middle East/North Africa

• After

– 32 once-stop destinations in Europe and 31 one-stop destinations in

Middle East/North Africa via DXB

– Revised service to SIN/HKG/KUL for better connectivity to Asia

November 23-28

Page 34

RECENT M&A AND JOINT VENTURES IN THE US

35November 23-28

Page 35

NORTH ATLANTIC ALLIANCE AND NON-ALIGNED

MARKET SHARES

36November 23-28

Page 36

NORTH ATLANTIC ALLIANCE STRUCTURE

37November 23-28

Page 37

WHAT MAKES AN ALLIANCE SUCCESSFUL?

• Factors that affect success of an alliance:

– Aligned expectations

– Win-win financial provisions

– Cultural compatibility (corporate and national)

– Consistent quality and other customer relations

– Network fit

– Well-coordinated IT systems

• E.g. WestJet-Southwest failure

– Smooth airport interfaces

– Coordinated selling and distribution

38November 23-28

Page 38

DISCUSSION: LUFTHANSA AND TURKISH AIRLINES

RELATION

• In 2006, LF sponsored TK’s application to join Star

Alliance

• Since 2010, TK and LF had been seeking closer co-

operation

• In 2013, LF decided to end its codeshare agreement with

TK

• Reasons:

– Strong growth of TK in Germany in particular secondary German cities

(TK has more than three times LF’s weekly frequencies between

Germany and Turkey)

– LF cannot match the fares with TK

39November 23-28

Page 39

D. ECONOMICS OF M&A

November 23-28 40

Page 40

ECONOMICS OF M&A• Key airline industry trends:

– Increased penetration of mergers and alliances

– Industry consolidation

– “Hub and spoke” route systems post-deregulation

• On the one hand, increased industry consolidation and

hub-and-spoke systems allow airlines to benefit from cost

economies and passengers from better connections, higher

frequency of service and a wider range of destinations.

• On the other hand, these trends can lead to enhanced

ability by carriers to exercise market power, exclude

competition and cause consumer harm.

November 23-28

41

Page 41

COMPETITIVE LANDSCAPE• Characteristics of the airline industry that favour anti-

competitive practices

– Hub concentration

– Airports slot constraints

– Price Transparency

– Multi-market contact

November 23-28

42

Page 42

COMPETITIVE LANSCAPE• Competition from other modes of transport is limited or

ineffective

– High speed trains may be a substitute on some route

– Other ground transport is generally not an effective substitute

– For most routes, airlines have no substitutes

• Business travellers account for a disproportionate share of

airline profits

– The 20/80 rule

– Time-sensitive travellers are typically the focus of antitrust concerns

November 23-28

43

Page 43

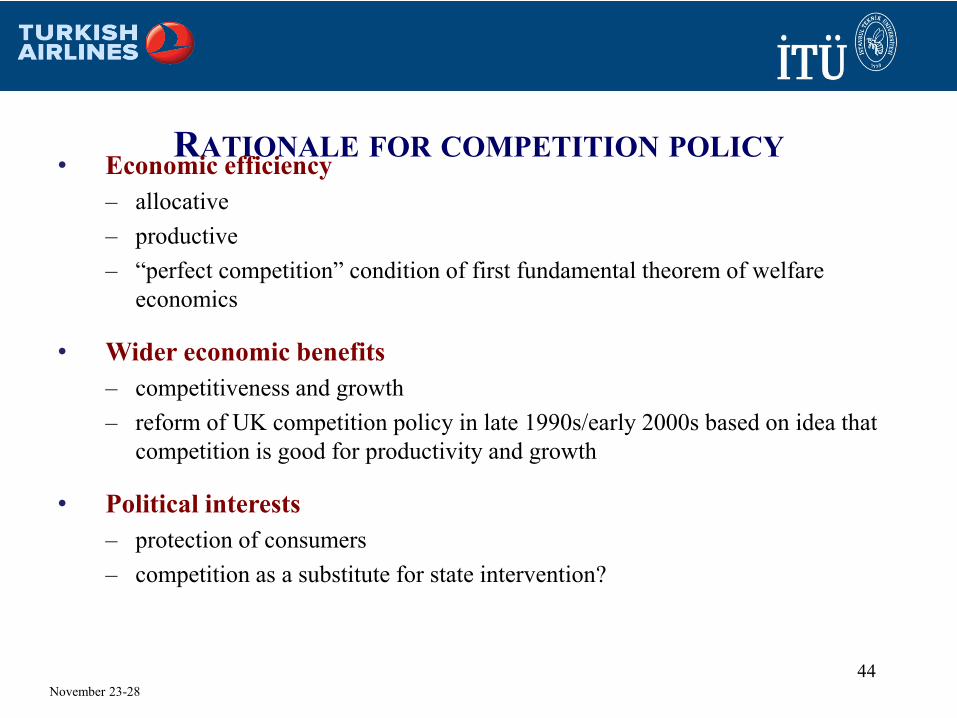

RATIONALE FOR COMPETITION POLICY• Economic efficiency

– allocative

– productive

– “perfect competition” condition of first fundamental theorem of welfare

economics

• Wider economic benefits

– competitiveness and growth

– reform of UK competition policy in late 1990s/early 2000s based on idea that

competition is good for productivity and growth

• Political interests

– protection of consumers

– competition as a substitute for state intervention?

November 23-28

44

Page 44

E. INTRODUCTION TO COMPETITION

POLICY AND REGULATION

November 23-28 45

Page 45

COMPETITION POLICY REGIMES

• European Union

– agreements between firms: Article 101 (formerly 81) TFEU

– single-firm conduct: Article 102 (formerly 82) TFEU

– merger control: EC Merger Regulation (1989, amended 2004)

• United Kingdom

– agreements between firms: Chapter I of Competition Act 1998;

Enterprise Act 2002 (stronger measures against cartels)

– single-firm conduct: Chapter II of Competition Act 1998

– merger control: Enterprise Act 2002

• United States

– monopolisation (agreements & single-firm conduct): Sherman Act 1890

– merger control: Clayton Act 1914

• Turkey

– Article 4054 (Turkish Competition Authority)

November 23-28

46

Page 46

US ANTITRUST LAWS• Sherman Act 1890

– Section 1: prohibits contracts, combinations & conspiracies in restraint

of trade

– Section 2: prohibits monopolisation, attempts to monopolise &

conspiracies to monopolise trade

• Clayton Act 1914

– prohibits price discrimination & some vertical restraints, where these

“substantially lessen competition” (SLC)

– merger control: SLC test

• Federal Trade Commission (FTC) Act 1914: set up

FTC

November 23-28

47

Page 47

EU & UK: AGREEMENTS BETWEEN FIRMS

• Art. 101 / Chapter I of Competition Act 1998 prohibits

“ … all agreements between undertakings … which have as their object

or effect the prevention, restriction or distortion of competition”

• Includes

– price fixing

– limiting production or investment

– market sharing

– applying dissimilar conditions or supplementary obligations

• Exemptions: agreements that are necessary to

– improve production or distribution

– promote technical progress

November 23-28

48

Page 48

EU & UK: ABUSE OF DOMINANCE

• Art. 102 / Chapter II of Competition Act 1998 prohibits

“Any abuse ... of a dominant position”

• Abuse includes

– imposing unfair prices or conditions

– limiting production or technical development

– applying dissimilar conditions or supplementary obligations

• What is “dominance”? Is it the same as monopoly?

– “position of economic strength … which enables it to prevent effective competition”

(United Brands, 1978)

– “does not preclude some competition” (Hoffman-La Roche)

• What is the “relevant market” within which the firm operates?

– econometric evidence on substitution between products

November 23-28

49

Page 49

INTERNATIONAL COOPERATION

• Since 1991 the European Union and the United States have been

coordinating regulatory reviews

– transatlantic alliances

– mergers and acquisitions affecting the transatlantic market

– joint studies on the impact of alliances

• Different approaches in different jurisdictions may lead to

inconsistent decisions or remedies

– E.g. Transborder Joint Venture between Air Canada and United/Continental

• The US Department of Transport granted antitrust immunity (with

carveouts on 6 routes in total)

• Canada’s Competition Bureau challenged the JV in court with a

subsequent settlement (additional carve-outs on 10 routes in total)

November 23-28

50

Page 50

ANTITRUST ANALYSIS OF M&A

• Competition authorities are likely to start with the

view that a merger that may lessen competition is

undesirable, especially if:

– The merged airline has dominant position

– There is no effective competition

• Thus, the merging airlines must show that the

benefits of the merger will offset the costs

November 23-28

51

Page 51

BENEFITS OF THE MERGER

• Cost efficiencies for airlines

– Benefits to airlines from reducing costs matter

• Increased revenues/prices for airlines

– Benefit to airlines from higher fares that result from reduced

competition is not a benefit from an antitrust law point of view

• Benefits for passengers

– Better service (connectivity, scheduling, FFp integration, lounge

access, etc.)

– Better price that may result from cost savings

November 23-28

52

Page 52

BENEFITS VS COST OF AN AIRLINE MERGER

• Competition authorities will compare potential

benefits to the costs of an airline merger

– Fare

• Complementary vs parallel (overlapping) networks

• City-pair vs inter hub passengers

– Reduced capacity

• A cost if fewer passengers are served

• A cost if less choices for passengers

• A benefit if capacity reduction leads to costs savings

November 23-28

53

Page 53

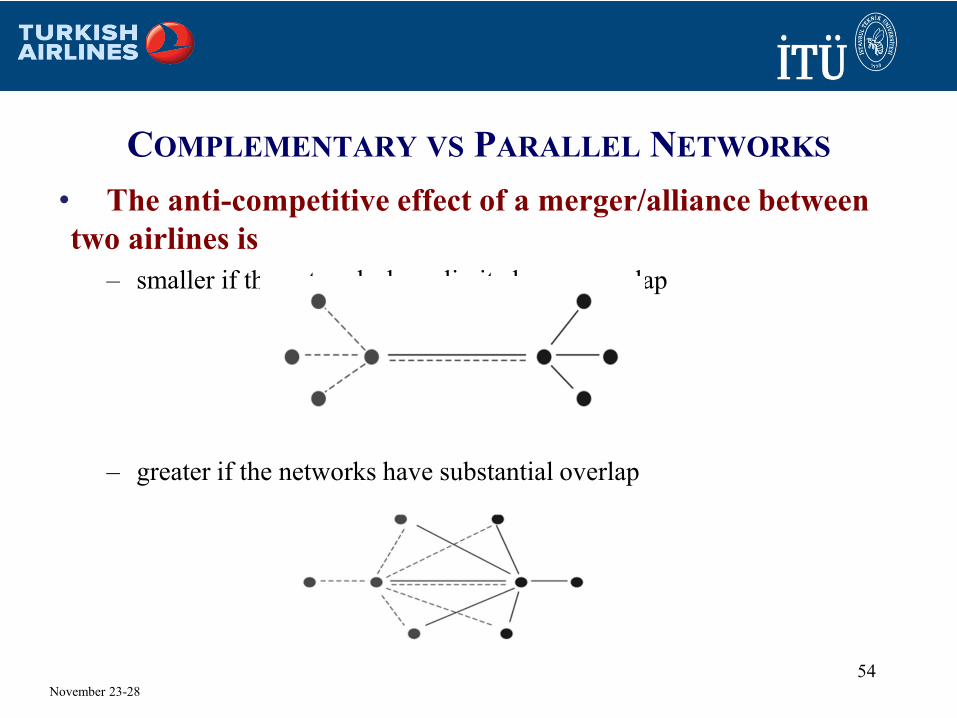

COMPLEMENTARY VS PARALLEL NETWORKS

• The anti-competitive effect of a merger/alliance between

two airlines is

– smaller if the networks have limited or no overlap

– greater if the networks have substantial overlap

November 23-28

54

Page 54

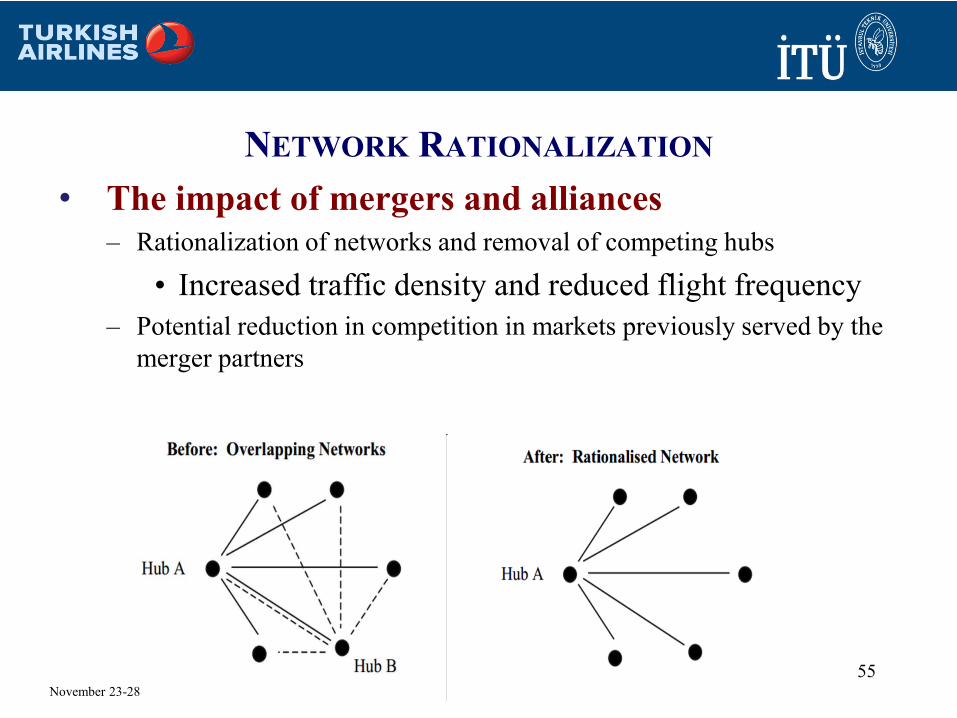

NETWORK RATIONALIZATION

• The impact of mergers and alliances

– Rationalization of networks and removal of competing hubs

• Increased traffic density and reduced flight frequency

– Potential reduction in competition in markets previously served by the

merger partners

November 23-28

55

Page 55

ANTITRUST ANALYSIS

• The presence of remaining competition in the market

– A major focus

• Based on the idea that effective outstanding competition

disciplines exercise of market power

– Prevents the cost of higher fares

– Prevents the cost of reduced passenger choices

– Allows for the benefit of the merger

• Competition from carriers operating indirect

service will be considered

– Generally not a good substitute for non-stop service

November 23-28

56

Page 56

MERGER GUIDELINES

• Clarify when government agencies are likely to act

to impede merger

• Articulate a 5-step procedure

1. Market Definition

2. Is there a substantial share of the market?

3. Is the exercise of market power probable?

4. What are the efficiencies?

5. Are the costs of exercising market power greater than the generated

efficiencies?

November 23-28

57

Page 57

1. MARKET DEFINITION

• Product market

– Business travellers/Leisure travellers

– Economy/Business/First Class

– Connecting/Non-stop passengers

• Different time and price sensitivity

• Different preferences for low cost and full service

airlines

– Virgin estimated that time sensitive passenger on london-NY value

time at $240 per hour

November 23-28

58

Page 58

1. MARKET DEFINITION

• Airline Relevant Geographic Market

– Airport pairs

– City pairs

• Airline markets are usually defined as city pairs

– Entire networks

– Hub airport

November 23-28

59

Page 59

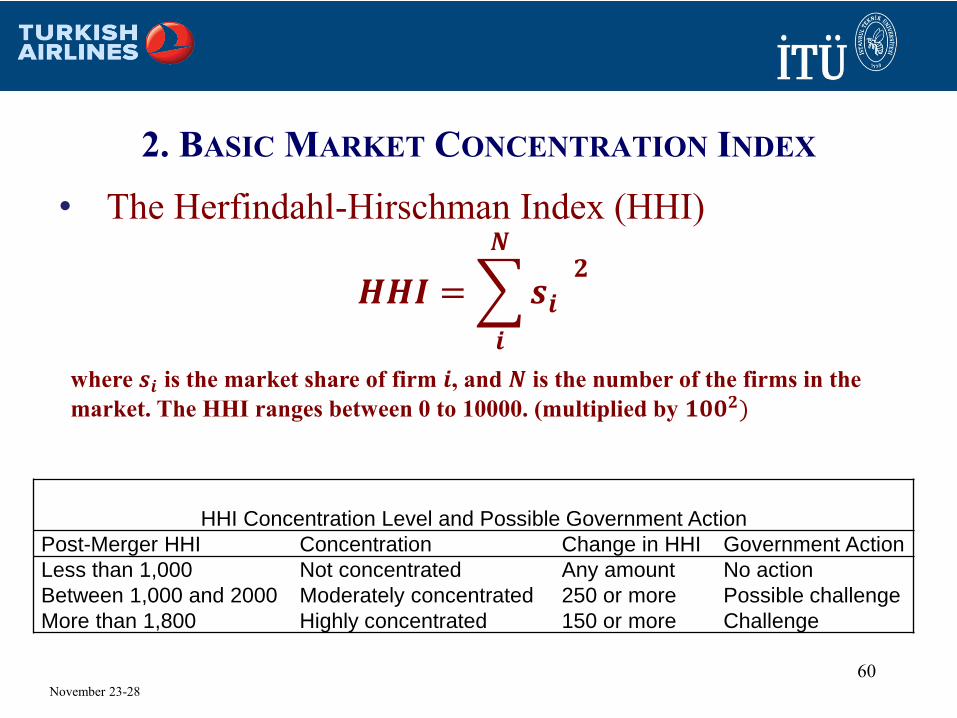

2. BASIC MARKET CONCENTRATION INDEX

• The Herfindahl-Hirschman Index (HHI)

𝑯𝑯𝑰 =

𝒊

𝑵

𝒔𝒊𝟐

where 𝒔𝒊 is the market share of firm 𝒊, and 𝑵 is the number of the firms in the

market. The HHI ranges between 0 to 10000. (multiplied by 𝟏𝟎𝟎𝟐)

HHI Concentration Level and Possible Government Action

Post-Merger HHI Concentration Change in HHI Government Action

Less than 1,000 Not concentrated Any amount No action

Between 1,000 and 2000 Moderately concentrated 250 or more Possible challenge

More than 1,800 Highly concentrated 150 or more Challenge

November 23-28

60

Page 60

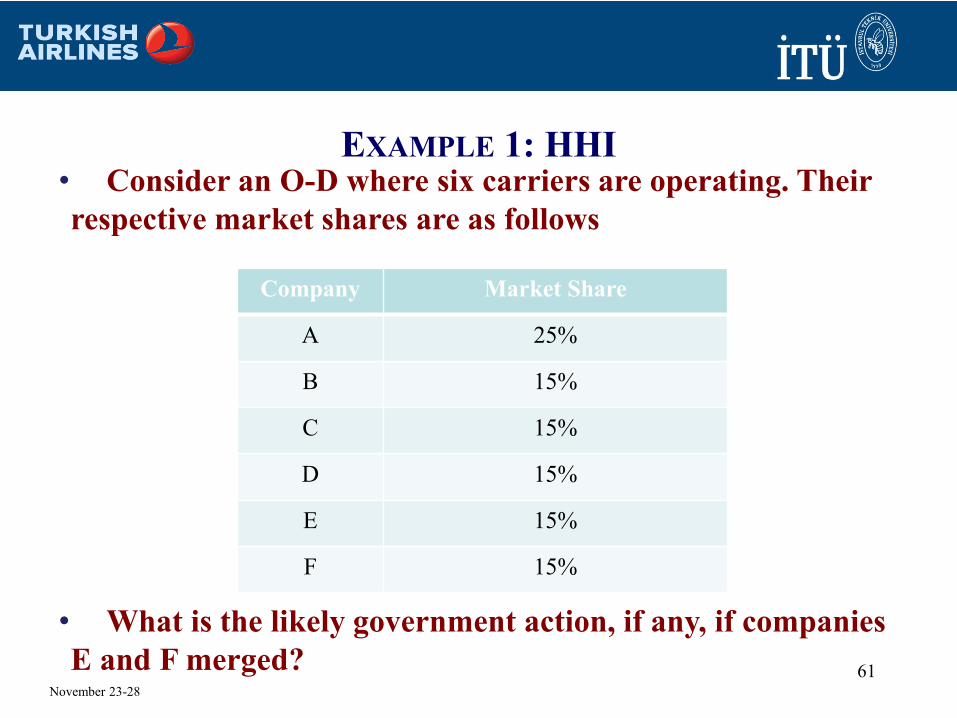

EXAMPLE 1: HHI• Consider an O-D where six carriers are operating. Their

respective market shares are as follows

• What is the likely government action, if any, if companies

E and F merged?

Company Market Share

A 25%

B 15%

C 15%

D 15%

E 15%

F 15%

November 23-28

61

Page 61

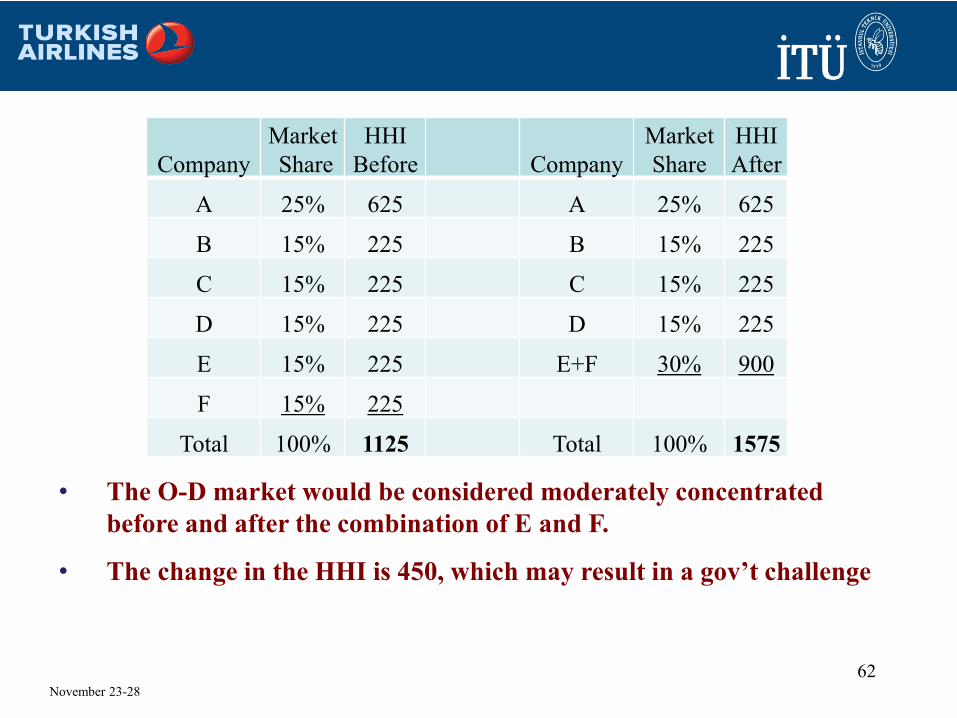

EXAMPLE 1: HHI

• The O-D market would be considered moderately concentrated

before and after the combination of E and F.

• The change in the HHI is 450, which may result in a gov’t challenge

Company

Market

Share

HHI

Before Company

Market

Share

HHI

After

A 25% 625 A 25% 625

B 15% 225 B 15% 225

C 15% 225 C 15% 225

D 15% 225 D 15% 225

E 15% 225 E+F 30% 900

F 15% 225

Total 100% 1125 Total 100% 1575

November 23-28

62

Page 62

EXAMPLE 2: HHI

• From Tuscon to New York

𝑯𝑯𝑰 =𝟐

𝟑

𝟐

+𝟏

𝟑

𝟐

∗ 𝟏𝟎𝟎𝟎𝟎 = 𝟓𝟓𝟓𝟓. 𝟔

Likely to challenge because highly concentrated

operated only by two unequal size firms.

Airlines Route Tickets Sold Market Share

AA TUS-Newark 400 0.67

UA TUS-Newark 200 0.33

November 23-28

63

Page 63

3. ASSESSING MARKET POWER

• Market power is defined as:

– I the ability to protably sustain prices above competitive levels

OR

– the ability to restrict output or quality below competitive levels.

• A firm with the market power may harm the competition by

– weakening existing competition

– raising entry barriers

– slowing innovation

• Market power can be possessed by a single firm or group of

firms

November 23-28

64

Page 64

MARKET SHARE

• High market share may be an indication of market power

– Determined in reference to the relevant market

– Measured in traffic, revenue, frequency, etc.

– Safe harbours

• A market share below 35% will not raise concerns

• A market share above 60% will likely raise concerns

November 23-28

65

Page 65

HIGH MARKET SHARE BUT NO MARKET POWER

• But high market share does not automatically

equal market power– Barriers to entry need to be analyzed

– Contestable market theory

November 23-28

66

Page 66

ENTRY BARRIERS• Airport slot constraints

– Large airports operate nearly at capaciy

• E.g. Heathrow is currently at 99% capacity

• Other major airports in NY, London, Tokyo etc. are also slot constrained

– Dominant airlines hold slots and limit new entry

• Access to airport facilities

– Terminals, gates, check counters, etc.

• Computer Reservation Systems

– Display Bias

– Booking Fees

– Travel agent incentives

November 23-28

67

Page 67

ENTRY BARRIERS• State ownership

– Limits sources of finance for new entrants

– Government “bailouts” or subsidies limit or impede new entry

• Loyalty programs

– Act as a volume discount

– Principle-agent problem (business travellers)

– The effect is greater for loyalty programs where points can be accumulated

faster or where an airline has a broader network

– Incumbent airlines may be required to grant competitor access to their frequent

flyer programs

• Discounts to large corporate customers

– On the condition that all or nearly all travel is booked with a specific airline

November 23-28

68

Page 68

REMEDIES

• If a merger is undesirable from an antitrust point of view, measures

can be adopted to reduce its harmful impact

– Reduce entry barriers to other competing airlines

• slot divestiture at congested airports

– Carve out selected routes from a joint venture

• applied primarily where the merging airlines are the only operators

• approach used by the United States in granting antitrust immunity to

international alliances

– the carriers can get approval without the carve outs but they

must present evidence that benefits will offset costs

– Agreement that the merged carriers will not undercut prices postmerger

• or engage in other forms of anticompetitive conduct

November 23-28

69

Page 69

REMEDIES

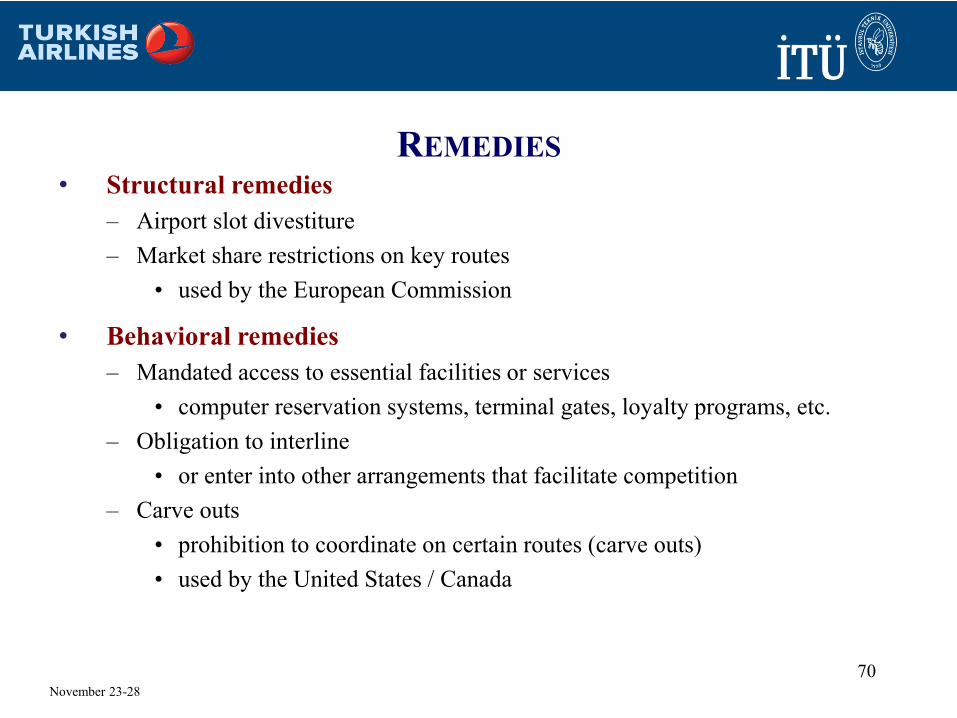

• Structural remedies

– Airport slot divestiture

– Market share restrictions on key routes

• used by the European Commission

• Behavioral remedies

– Mandated access to essential facilities or services

• computer reservation systems, terminal gates, loyalty programs, etc.

– Obligation to interline

• or enter into other arrangements that facilitate competition

– Carve outs

• prohibition to coordinate on certain routes (carve outs)

• used by the United States / Canada

November 23-28

70

Page 70

E. EXAMPLES

November 23-28 71

Page 71

SELECTED M&A CASES 2005-PRESENT

• Delta and Northwest Merger

– On April 14, 2008 DL and NW announced a $17.6 billion merger, DL

was the second and NW was the forth largest US carrier

– Both operated under hub-and-spoke system

– September 26, 2008, two airlines’ shareholders approved the merger

– October 29, 2008 DoJ approved their merger

• Claiming the potential for substantial cost efficiencies with little or no harmful

effects in competition.

– As of 2009, NW’s aircrafts have operated under Delta and NW’s hubs

have been fully consolidated with Delta’s brand

72November 23-28

Page 72

SELECTED M&A CASES 2005-PRESENT

• Lufthansa and Swiss Air (2005)

– LX is acquired by LH

– LH made a move on several smaller European carriers, Swiss Air,

Austrian Airlines and BMI (which they sold to British Airways in

2011) in separate deals

– LH also purchased 19% of U.S. carrier Jetblue in 2007

73November 23-28

Page 73

SELECTED M&A CASES 2005-PRESENT

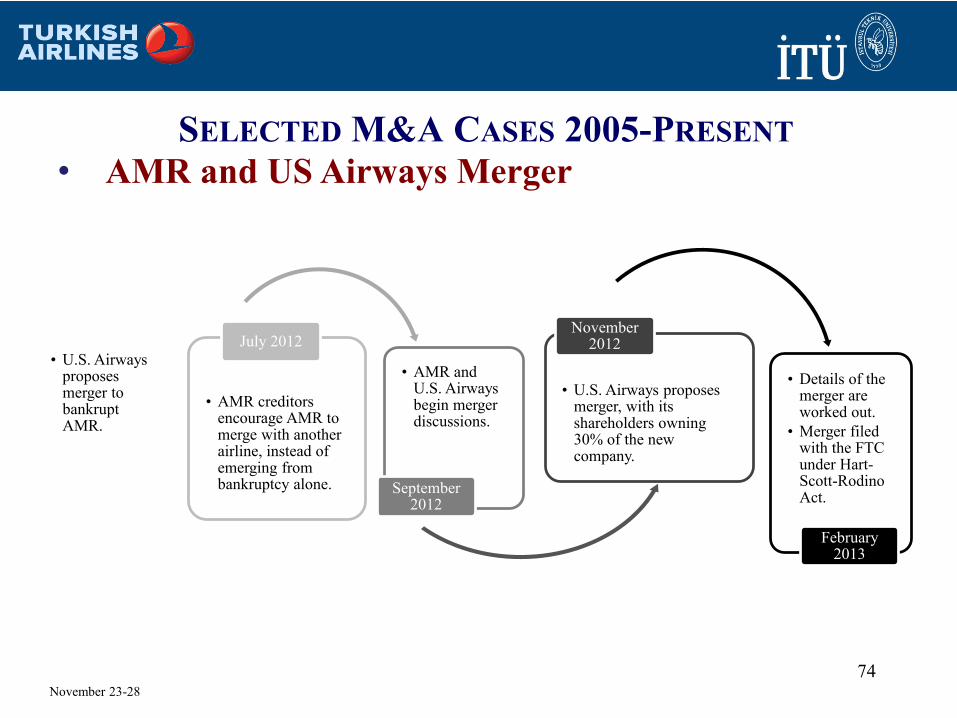

• AMR and US Airways Merger

• U.S. Airways proposes merger to bankrupt AMR.

April 2012

• AMR creditors encourage AMR to merge with another airline, instead of emerging from bankruptcy alone.

July 2012

• AMR and U.S. Airways begin merger discussions.

September 2012

• U.S. Airways proposes merger, with its shareholders owning 30% of the new company.

November 2012

• Details of the merger are worked out.

• Merger filed with the FTC under Hart-Scott-RodinoAct.

February 2013

74November 23-28

Page 74

END OF MODULE 11

November 23-28 75