Cautionary Statement Regarding Forward Looking Statements Forward-Looking Statements In order, among other things, to utilise the 'safe harbour' provisions of the US Private Securities Litigation Reform Act 1995 e are pro iding the follo ing ca tionar statement This presentation contains certain for ard looking Act 1995, we are providing the following cautionary statement: This presentation contains certain forward-looking statements with respect to the operations, performance and financial condition of the Group. Although we believe our expectations are based on reasonable assumptions, any forward-looking statements, by their very nature, involve risks and uncertainties and may be influenced by factors that could cause actual outcomes and results to be materially different from those predicted The forward-looking statements reflect knowledge and information be materially different from those predicted. The forward looking statements reflect knowledge and information available at the date of preparation of this presentation and AstraZeneca undertakes no obligation to update these forward-looking statements. We identify the forward-looking statements by using the words 'anticipates', 'believes', 'expects', 'intends' and similar expressions in such statements. Important factors that could cause actual results to differ materially from those contained in forward-looking statements, certain of which are beyond our control, include, among other things: the loss or expiration of patents, marketing exclusivity or trade marks, or the risk of failure to obtain patent protection; the risk of substantial adverse litigation/government investigation claims and insufficient insurance coverage; exchange rate fluctuations; the risk that R&D will not yield new products that achieve commercial success; the risk that strategic alliances or the integration of acquired b i ill b f l th i t f titi i t l d i d ti t ti ik th businesses will be unsuccessful; the impact of competition, price controls and price reductions; taxation risks; the risk of substantial product liability claims; the impact of any failure by third parties to supply materials or services; the risk of failure to manage a crisis; the risk of delay to new product launches; the difficulties of obtaining and maintaining regulatory approvals for products; the risk of failure to observe ongoing regulatory oversight; the risk that new products do not perform as we expect; the risk of environmental or occupational health and safety that new products do not perform as we expect; the risk of environmental or occupational health and safety liabilities; the risks associated with conducting business in emerging markets or the failure to develop our business in such markets; the risk of reputational damage; the risk of product counterfeiting; and the risk of failure to successfully implement planned cost reduction measures through productivity initiatives and restructuring programmes. Nothing in this presentation should be construed as a profit forecast.

In order, among other things, to utilise the 'safe harbour' provisions of the US Private Securities Litigation Reform Act 1995 e are pro iding the follo ing ca tionar statement This presentation contains certain for ard lookingAct 1995, we are providing the following cautionary statement: This presentation contains certain forward-looking statements with respect to the operations, performance and financial condition of the Group. Although we believe our expectations are based on reasonable assumptions, any forward-looking statements, by their very nature, involve risks and uncertainties and may be influenced by factors that could cause actual outcomes and results to be materially different from those predicted The forward-looking statements reflect knowledge and informationbe materially different from those predicted. The forward looking statements reflect knowledge and information available at the date of preparation of this presentation and AstraZeneca undertakes no obligation to update these forward-looking statements. We identify the forward-looking statements by using the words 'anticipates', 'believes', 'expects', 'intends' and similar expressions in such statements. Important factors that could cause actual results to differ materially from those contained in forward-looking statements, certain of which are beyond our control, include, among other things: the loss or expiration of patents, marketing exclusivity or trade marks, or the risk of failure to obtain patent protection; the risk of substantial adverse litigation/government investigation claims and insufficient insurance coverage; exchange rate fluctuations; the risk that R&D will not yield new products that achieve commercial success; the risk that strategic alliances or the integration of acquired b i ill b f l th i t f titi i t l d i d ti t ti i k thbusinesses will be unsuccessful; the impact of competition, price controls and price reductions; taxation risks; the risk of substantial product liability claims; the impact of any failure by third parties to supply materials or services; the risk of failure to manage a crisis; the risk of delay to new product launches; the difficulties of obtaining and maintaining regulatory approvals for products; the risk of failure to observe ongoing regulatory oversight; the risk that new products do not perform as we expect; the risk of environmental or occupational health and safetythat new products do not perform as we expect; the risk of environmental or occupational health and safety liabilities; the risks associated with conducting business in emerging markets or the failure to develop our business in such markets; the risk of reputational damage; the risk of product counterfeiting; and the risk of failure to successfully implement planned cost reduction measures through productivity initiatives and restructuring programmes. Nothing in this presentation should be construed as a profit forecast.

AstraZeneca believes emerging g gmarkets are a sustainable opportunityopportunity

Our goal is to continue double-digit growth, with emerging markets becoming ~25% of AZ sales by 2014emerging markets becoming ~25% of AZ sales by 2014

AZ emerging markets revenue goalg g g

$12bn

$8bn

$4bn

20142009$0bn

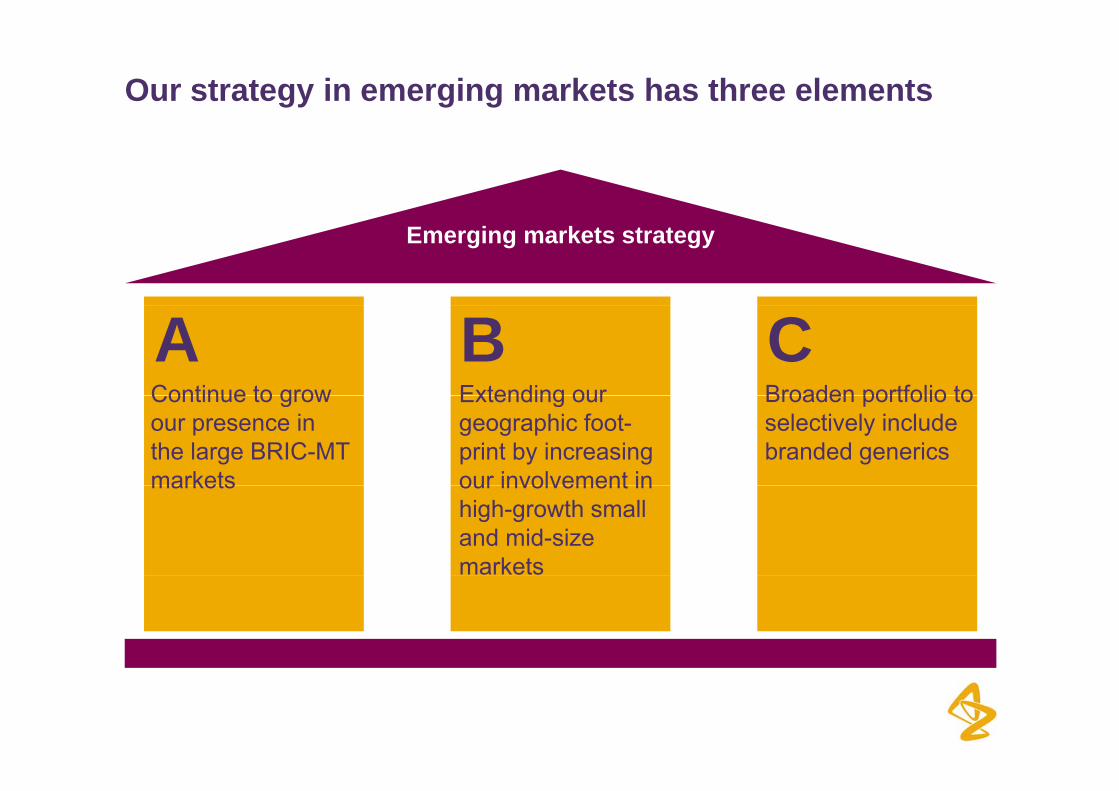

Our strategy in emerging markets has three elements

Emerging markets strategy

Continue to grow Extending our Broaden portfolio to

A B CContinue to grow our presence in the large BRIC-MT markets

Extending our geographic foot-print by increasing our involvement in

Broaden portfolio to selectively include branded generics

markets our involvement in high-growth small and mid-size markets

Executing our strategy will create double-digit growth

CB

C

A

Growth in small and mid-sized

markets

2009 2014Branded generics

Growth in BRIC-MT

markets

We will grow our presence in the largest emerging marketsemerging markets

G t tf li f i ti b dGrow our strong portfolio of existing brands

• Drive increased share

E dContinue to grow

A• Expand our coverage

(geographic, customers & channels)

Launch AstraZeneca’s highly relevant

Continue to grow our presence in the large BRIC-MT markets g y

pipeline products

Launch a highly selective portfolio of b d d i

markets

branded generics

Our highly relevant pipeline will be a large source of growth in emerging marketsgrowth in emerging markets

ExamplesLifecycle management on our core innovative brands

Key AZ launches with emerging market relevance Brilinta / BriliqueOnglyzaVimovoDapagliflozin

E i k t l t i li i C bi iEmerging market relevant in-licensing CubicinCeftarolineNXL104 combinationsPi illi / t b tPiperacillin / tazobactamCimziaNKTR-118TC5214TC5214

Now let us consider two of our most important markets

China

Xudong YinMarketing Company President, China

China

Rubens PedrosaMarketing Company President,

Brazil

Marketing Company President, Brazil

AstraZeneca believes emerging g gmarkets are a sustainable opportunityopportunity

Emerging MarketsEmerging Markets Investor DayInvestor Day ChinaChinaMarch 16, 2010

China is the single largest emerging market opportunity

China Rx market sales

Constant exchange rate ~$80bn

~$30bn

+20%

~$30bn

~$10bnSales rank among world h k t 9th 5th 3 d

201420092004pharma markets … 9th 5th 3rd

… and catching up to 8th 4th 2nd… and catching up to 8th 4th 2nd

Source: IMS Global Market Prognosis, June 2009

Reasons to believe in sustainable market growth

Economic growth Growing health burdengand large increases in middle class

g

Significant expansion of medical infrastructure

Healthcare reform driving large expansion of insurance coverage

AstraZeneca is the #2 pharma company in China

Rx market share, 2009, %, ,0 0.5 1.0 1.5 2.0 2.5

Pfizer/Wyeth

Bayer

AstraZeneca hospital demand sales in China grew 31% from 2008

Yangzijiang

Sanofi-Aventisgto 2009, outpacing market growth

Ke Lun

Roche

Hengrui

Shandong Qilu

NovartisSource: IMS

AstraZeneca has seen consistent above-market growth in Chinagrowth in China

AstraZeneca sales in China1

$811m$811m

+32%

$203

$437m

$203m

20092004 2007

1 Actual exchange rates. Source: AZ internal data

AstraZeneca: A strong culture of "In China for China"A strong culture of In China, for China

Sh h YYi X d F d i k Ch Shuhwa YangFinance, Commercial & Administration

Years with AZ: 5Finance commercial

Yin XudongMarketing Company President

Years with AZ: 7Experience: Sales

Fredrick Chu General Manager Hong Kong

Years with AZ: 3Experience: Sales Finance, commercialExperience: Sales,

Marketing, StrategyExperience: Sales, Marketing

Meade Zhang Human ResourcesIngrid Zhang

Sales & MarketingYears with AZ: 2Experience: HRYears with AZ: 6

Experience: Sales, Marketing, Strategy

Wayne ShiPC Marketing

Years with AZ: 8Experience: Sales, Marketing

Shan GuohongPrimary Care Sales

Years with AZ: 7Experience: Sales, Marketing

Allan ChanCommercial Excellence Academy

Years with AZ: 20Experience: Sales

Top commercial leaders are all Chinese and have been with AZ since 2004I d l di ff ( hi d l h )

Industry leading staff turnover rate (a third lower than average)

We have a strong business presence across China

Geographic coverage

• 5 Regions

People

• 2000+ sales reps added 5 eg o s

• 22 Branches

• 45 Offices

000 sa es eps addedsince 2003

• Rigorous semi-annual 45 Offices

• Covering 300 cities, with 200 being the focus

talent review to all 3,000+ employees

• Heavy investment in people gHeilongjiang

JilinInner Mongolia

• Heavy investment in people development including AZ Academy, EMBA/MBA, E t l t i i

Hebei

ShandongShanxiNingxia

Gansu

Qinghai

Xinjiang

Jiangsu

BeijingExternal trainings, International Assignments

Liaoning

Sichuan

FujianJiangxi

AnhuiHubei

Hunan

ShanghaiHenanShaanxi

Gansu

Guizhou

Xizhang

Jiangsu

ZhejiangChongqing

GuangdongGuangxi

Hainan

Guizhou

Yunnan

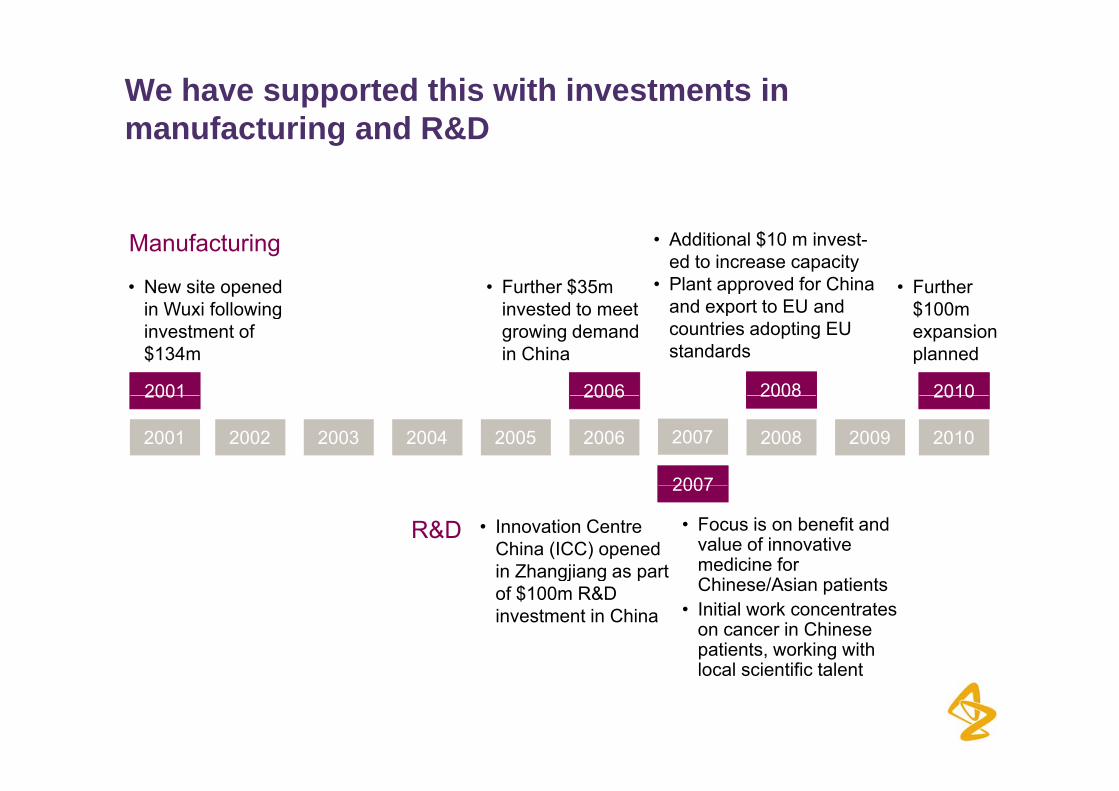

We have supported this with investments in manufacturing and R&Dmanufacturing and R&D

• Additional $10 m invest-ed to increase capacity

• Plant approved for China and export to EU and

• Further $35m invested to meet

• New site opened in Wuxi following

• Further $100m

Manufacturing

2001 2006 2008 2010

and export to EU and countries adopting EU standards

invested to meet growing demand in China

in Wuxi following investment of$134m

$100m expansion planned

2001 2004 2010

2007

2002 2003 2005 2006 20092007

2001 2006 2008 2010

2008

2007

• Focus is on benefit and value of innovative medicine for

• Innovation Centre China (ICC) opened in Zhangjiang as part

R&D

Chinese/Asian patients• Initial work concentrates

on cancer in Chinese patients, working with l l i tifi t l t

in Zhangjiang as part of $100m R&D investment in China

local scientific talent

Our strategy going forward

Begin to establish leadership

Drive growth with current core brands

Solidify leadership with new products

Begin to establish leadership in “Broad Market”

• Additional sales force• Capitalise on health

reforms with strategies tocore brands• Increasing productivity• Improve coverage in

~100 additional cities

• Additional sales force capacity in top cities

• Leading marketing and sales capabilities

reforms with strategies to reach a greater share of the Chinese patient population

1

100 additional cities sales capabilities

Key products entering reimbursement list in 2009

1

New ProductsCeftaro-line

Dapag-liflozin

80

Vimovo

1 IV formulation

We have successfully boosted growth in the past following NRDL listingfollowing NRDL listing

Sales

1

NRDL listing

Ɩ Ɩ Ɩ Ɩ Ɩ Ɩ Ɩ

200908070605042003

1 Oral formulation. Source: AZ

Our strategy going forward

Begin to establish leadership

Drive growth with current core brands

Solidify leadership with new products

Begin to establish leadership in “Broad Market”

• Additional sales force• Capitalise on health

reforms with strategies tocore brands• Increasing productivity• Improve coverage in

~100 additional cities

• Additional sales force capacity in top cities

• Leading marketing and sales capabilities

reforms with strategies to reach a greater share of the Chinese patient population

1

100 additional cities sales capabilities

Key products entering reimbursement list in 2009

1

New ProductsCeftaro-line

Dapag-liflozin

82

Vimovo

1 IV formulation

Our core portfolio has enjoyed high growth and still has high growth potential driven by brand loyalty

Segment growthAZ product growth

has high growth potential driven by brand loyalty

Sales in China 2009*

$146m

Segment growthCAGR, 2004-09**

AZ product growthCAGR, 2004-09**

32%19%

$117m

$130m 25%22%

26%24%

$65m

$66m 32%73%

30%34%

$56m

$62m 36%55%1

40%48%

$24m

$

$22m

28%

77%2

3 %4%

51%

31%

83

$18m 37%54%

1 2005-09. 2 2006-09. Source: *AZ; **IMS

Industry leading customer segmentation and targeting capability enables AZ to continue to increase productivitycapability enables AZ to continue to increase productivity

Proprietary customer insights Industry leading productivity –

• We profiled 250,000 doctors out

increasing at >10% a year

Sales rep productivity 1st half 2009

of 1.3m in China, building a valuable proprietary customer database

Roche

Novo Nordisk

• Using our database, we rigorously segmented and targeted the relevant physicians

Bayer

Pfizertargeted the relevant physicians

• This has allowed us to continue to boost the productivity of our

l f

Novartis

Sanofi A entis

MSD

sales force Sanofi-Aventis

GSK

Lilly

We are expanding our coverage into an additional 100 cities to extend the value of these core brands100 cities to extend the value of these core brands

Core coverage Increasing coverage (~200 cities)

• High frequency visits to doctors by sales reps

(~100 cities)

• Investing in sales force to increase coverage and sales rep frequencyby sales reps coverage and sales rep frequency

Coupled with a holistic segmentation of physicians and tailored promotional effortsand tailored promotional efforts

AZ China’s success will be enhanced by newly reimbursed productsnewly reimbursed products

AZ has had success in getting Our products are in large markets reimbursement for four key brands

• Update to National Reimbursement Drug List (NRDL) initiated in 2009

with high growth

Total market 2009, $mDrug List (NRDL) initiated in 2009 by government

- Last update to NRDL in 2004

CAGR 04-09

32% 30% 45% 25%

• Four AZ brands successfully added to NRDL

~$800m-1,200m

- Expected to get reimbursement in provinces in 2010 ~$200m-

400m~$200m-

400m ~$150m-300m

StatinsPPIs Beta-blockers

Asthma/COPD

Source: IMS; AZ analysis

AZ has built capabilities to launch our new highly relevant brands in China 1 2 years after majorrelevant brands in China 1-2 years after major established markets

Pipeline products Segment value1, 2009

Patient need

$300 500 >100m estimated to have heart disease in China$300-500m >100m estimated to have heart disease in China

$300-500m 40m diabetics with further

Dapagliflozin

$300-500m 40m diabetics with further 20m pre-diabetic patients

Ceftaroline

$350-700m ~5.2% of hospital patients in China have hospital-acquired infections, with one of the highest rates of antibiotic resistance

Vimovo $100-200m Surveys show 25-50% of adults over 50 in China suffer from osteoarthritis

1 Assumes the following IMS ATC classification: Brilinta (B1C), Onglyza (A10J, A10K, A10L, A10M, A10N), Cubicin (J1X), Ceftaroline (J1D, post-3rd generation cephalosporins). Source: IMS, AZ analysis; China Daily; International Diabetes Foundation; National Nasocomial Infections Surveillance System; Journal of Globalization and Health

Strong local customer insights allow us to launch new products with maximum impactproducts with maximum impact

AZ tailored its Symbicort strategy Symbicort share in Chinabased on China-specific insights

• Innovative and proprietary market research approaches across

Therapeutic segment sales, 2009

research approaches across multiple cities and physician types:

- Enabled a better physician and 16%

patient segmentation and identification of priority segments

- Supported differentiated 84%Supported differentiated messaging between pulmonologists and paediatricians (efficacy vs fast-control) – a S bi t h ld 16% h i k t

84%

( y )different distribution of messages vs. established markets

Symbicort held 16% share in market, despite not having reimbursement –unlike key competitors

Healthcare reform is creating an opportunity in the “Broad Market”Broad Market

The government is committed to investing $125bn to support healthcare g g $ ppreform between 2009 and 2011, which includes

• $64bn to expand basic healthcare insurance

• $38bn to build and upgrade community / rural hospitals

These investments will help stimulate a new “broad market”

89Source: MOH; China infobank; Literature research; AZ analysis

In part driven by government investment in insurance

Brazil is a high-growth market with strong fundamentals

Brazil market sales constant $25bexchange rate ~$25bn

~$17bnGrowth in the prescription (ethical)

8%+

$

~$10bn

prescription (ethical) drug segment is expected to continue to outpace overall market

201420092004

Sales rank among world pharma markets … 11th 10th 9th

pgrowth through 2014

… and catching up to

10th 9th 8th

Source: IMS Global Market Prognosis, June 2009

Reasons to believe in sustainable market growth

• GDP-growth boosting household incomes g gand leading to middle class growth

• Primarily out of pocket payment for medicines• Primarily out-of-pocket payment for medicines with patients willing to pay for innovation, quality, and services

• Targeted increases in government spend on health care

• Ageing population is driving a disease profile that favours chronic therapies and long termthat favours chronic therapies and long-term engagement with healthcare stakeholders

GDP growth fuelling expansion of the middle class

% of Households

30

15 to 20 million new consumers b iddl

20became middle class during the last decade

201010

Household income0 70605040302010

02002

Source: Economist Intelligence Unit, 2010

ouse o d co e$ '000

AstraZeneca is the #7 multi-national pharmaceutical company in Brazil but has significantly increased its rankcompany in Brazil but has significantly increased its rankRx market share, 2009, %

Local player Growth rate, 2004-09 %

EMS

0 1 2 3 4 5 6 7 8

Novartis

2004-09, %

28%38%

Aché Labs

EMS

RocheSanofi-Aventis

38%19%30%17%

MedleyEurofarma

Aché LabsPfizer

17%14%32%33%Eurofarma

MerckAbbott

AstraZeneca has improved from #15 in

33%35%10%30%

Castro MarquesGlaxoSmithKlineBayer

improved from #15 in Brazil in 2004

30%

16%13%

28%Cas o a quesJohnson & Johnson

Source: IMS

18%8%

AstraZeneca has seen consistent above-market growth in Brazilgrowth in Brazil

AstraZeneca sales in Brazil1

$457m30%

$330m

~30% p.a.

We have grown

$134m

consistently at twice the market, which averaged 10-12% growth per year $134mover the same period

200920072004

1 Actual exchange rate. Source: AZ internal

AstraZeneca Brazil has built a strong local organisation

Thomaz BonattoRubens Pedrosa Sergio Pompilio Jose E. NevesCFO

Years with AZ: 13

Marketing Company President

Years with AZ: 3

Legal and Corporate Communications Director

Years with AZ: 2

Medical Director

Years with AZ: 12

Jeroen CommissarisPrimary Care BU Head

Jerson FibraMarket Research, Training & Business Support Director

Years with AZ: 10

Jorge MazzeiRegulatory, Corporate Affairs & Business Development Director

Christian SchneiderSpecialty Care BU Head

Years with AZ: 4

Daniela Castanho

Years with AZ: 6Years with AZ: 10

Miguel Monzu

Years with AZ: 4

Cecilia Abe a e a Cas a oOperations Director

Years with AZ: 11

gue o uHuman Resources Director

Years with AZ: 5

Cec a beCompliance Officer

Years with AZ: 6We have over 580 sales reps in Brazil covering ~15 products

AstraZeneca recognized as one of the “Great Places to Work in Brazil”

AstraZeneca elected “Best Pharmaceutical Company in

across ~10 therapeutic areas

the Great Places to Work in Brazil for 5 consecutive years (2005-09)Brazil” due to distinguished

performance in 2008

Our strategy going forward

Introduce AstraZeneca’s new global launch

Launch selected branded generics and local in-licensed

Drive share and existing innovative brands

Grow our business in public reimbursement

new global launch products products

BrandedgenericsCeftaroline

Vimovo

Dapag-liflozinliflozin

Our capabilities allow us to continue our momentum

We have improved our …to boost our sales of Crestorsegmentation and targeting…

Crestor salesNumber of GPs i it d f C t

Average details peri it d GP

$67m

visited for Crestor visited GP per year

~9,000 -25%90

~120+29%

$22m

+208%~6,500 ~90

$

% of all Brazilian GPs visited 2009

F th l b t ibl l i li i l t i l lt

% of all Brazilian GPs visited, 200916%

20092006

Source: AstraZeneca

Further sales boost possible leveraging clinical trial results

We have successfully entered the growing public segmentpublic segment

The government is investing to cover …and AZ has already achieved success a limited set of major diseases…

• Coverage for a targeted set of chronic diseases including cancer and

positioning products for reimbursement

• Positioned Seroquel for public reimbursement in schizophrenia

schizophrenia

• 100% coverage of all health costs

G t d j t d t

• Ongoing discussions for Crestor and Brilinta

• Government spend projected to increase further

Seroquel sales in public reimbursementDrug sales in public reimbursement$45

$2.2bn

$3.7bn$45m

20092004 2007

$14m

2009

Source: Ministry of Health, AstraZeneca

20092004 2007 2009

Our pipeline products are well-suited for patientneeds in Brazilneeds in Brazil

Pipeline products Segment value1, 2009

Patient need

$150 200 32% of all deaths in Brazil attributable to$150-200m 32% of all deaths in Brazil attributable to cardiovascular disease

$250-300m About 8 million people in Brazil have diabetes

Dapagliflozin

$250-300m About 8 million people in Brazil have diabetes. An additional 1.5 million are pre-diabetic

Ceftaroline

$200-250m Roughly 1.5 million hospital-associated infections with several associated fatalities. Doctors are keen for new therapeutic options with activity against MRSA and Gram-negative pathogensMRSA and Gram negative pathogens

Vimovo $550m More than 5 million people affected by osteoarthritis in Brazil with increasing role of NSAIDs that present positive patient safety profiles

1 Assumes the following IMS ATC classification: Brilinta (B1C), Onglyza/Dapagliflozin (A10J, A10K, A10L, A10M, A10N), Cubicin (J1X), Ceftaroline (J1D), Vimovo(N2B). Source: IMS; British Journal of Medicine, International Diabetes Foundation, Globocan

present positive patient safety profiles

AstraZeneca is also launching locally relevant in-licenses and branded genericslicenses and branded generics

Cimzia is an exciting local opportunity We are also launching a selective branded in Brazil

• AstraZeneca in-licensed Cimzia from UCB as a Brazil-specific opportunity

generics portfolio…

You will hear more detail on our branded generics strategy later in the presentation

• Cimzia will enter an ~$300m market for rheumatoid arthritis and Crohn’s disease

Ci i h b fi i l f t d• Cimzia has beneficial safety and simplicity of administration versus other therapies available on the market

• AstraZeneca has a very strong record in delivering technical content to medical specialists that will be active in treatment

• AZ has capabilities to obtain public reimbursement

Our aspiration in Brazil

• Enter the top 10 in the next 5 years and continue to outgrow the market

• Drive increased share in our existing brands

- Leverage our strong commercial capabilities

G t t d t bli- Grow our targeted access to public reimbursement

• Launch AZ’s new brands as well as branded generics and local in-licenses

AstraZeneca believes emerging g gmarkets are a sustainable opportunityopportunity

Our strategy in emerging markets has three elements

Continue to grow Extending our Broaden portfolio to

A B CContinue to grow our presence in the large BRIC-MT markets

Extending our geographic foot-print by increasing our involvement in

Broaden portfolio to selectively include branded generics

markets our involvement in high-growth small and mid-size markets

Beyond BRIC-MT, AZ sees many important markets

2009 Rx market value

Market value CAGR 2004 09Market value CAGR 2004-09

GDP per capita, 2009 (PPP)PolandPoland$6.9bn7.0%$17,989

Thailand$3.0bn14.9%$7,998

V l

Romania$2.8bn19.0%$11,755

Philippines$2.3bn8.5%$

$ ,

Venezuela$4.8bn24.2%$12,496

Algeria$2.3bn13.1%$6 855

$3,536

Indonesia$2.5bn9 5%Argentina

$3.8bn16.8%$14,126

$6,855

South Africa$2 0bn

Saudi Arabia$2 9bn

9.5%$4,149

$2.0bn9.4%$9,961

$2.9bn11.2%$23,388

Source: IMS; IMF World Economic Outlook

Small and mid-sized markets outside BRIC-MT are material and could add $60bn in the 5 yearsmaterial and could add $60bn in the 5 years

Emerging markets incremental sales forecast 2009-14g g

~$150bn+10-12% p.a.

~$90bn If growth continues at historical rates (10-12% per

Small and mid-

historical rates (10 12% per annum), small and mid-sized markets will add $60bn in sales by 2014 Small and mid-

sized markets20142009

y

Source: IMS for 2009; AZ Projections for 2014 at historical growth

We believe we have significant upside potential in small and mid sized marketsand mid-sized markets

Middle East / North Africa

Maged GobranArea Vice President, Middl E /N h Af i

Middle East / North Africa(MENA)

Middle East/North Africa

Emerging MarketsEmerging Markets Investor DayInvestor Day Middle East / NorthMiddle East / North Africa (MENA)Africa (MENA)March 16, 2010

Middle East & North Africa (MENA) a collection of small and mid sized markets– a collection of small and mid-sized markets

Tunisia

LebanonSyria

Iraq

Tunisia

Morocco

Qatar

BahrainKuwait

q

Jordan

EgyptLibya

Algeria

West Bank

Oman

Saudi Arabia

UAE

gyp

Yemen

17 markets, ~300 million population

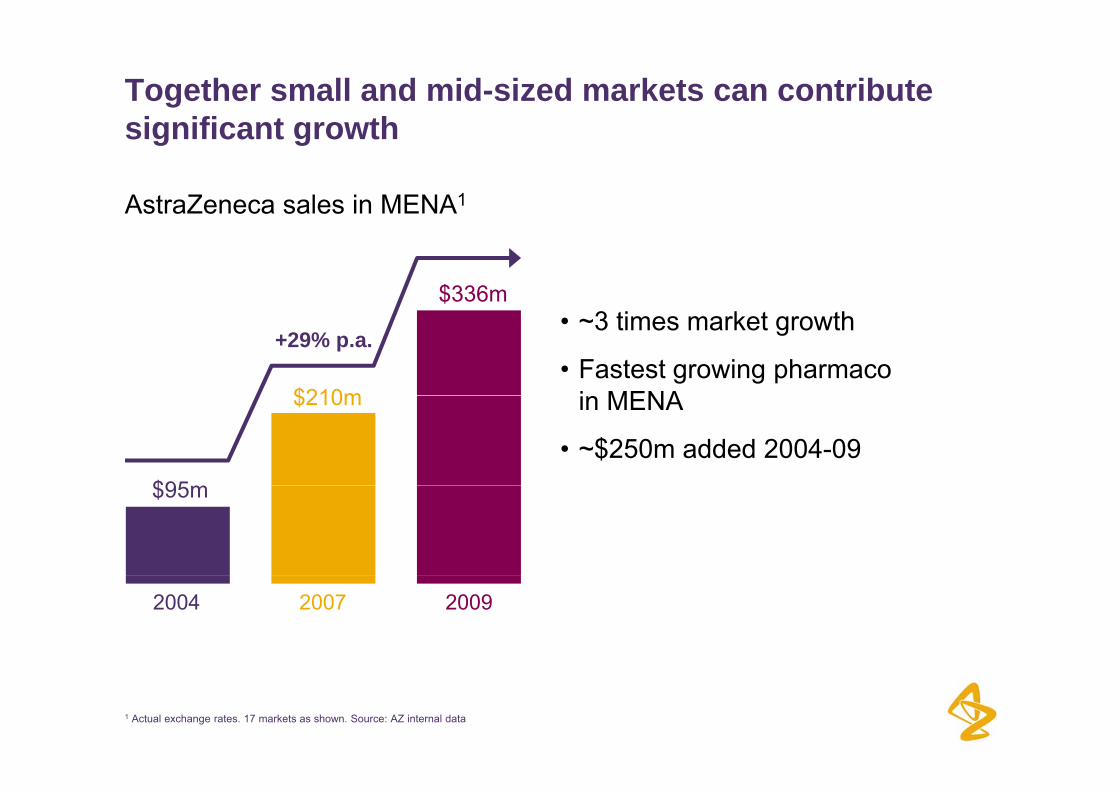

Together small and mid-sized markets can contribute significant growthsignificant growth

AstraZeneca sales in MENA1

$336m• ~3 times market growth

• Fastest growing pharmacoi MENA

+29% p.a.

$210m in MENA

• ~$250m added 2004-09$95

$210m

$95m

200920072004

1 Actual exchange rates. 17 markets as shown. Source: AZ internal data

Growth in small and mid-sized markets like MENA is possible with empowered local leaderspossible with empowered local leaders

Mehdi FerdjiouiTarek Rabah Mohamed Makhlouf jCountry Manager Algeria

AlgerianWorked in Algeria

President Gulf

Lebanese / CanadianWorked in Gulf and Brazil

President Saudi Arabia

EgyptianWorked in UAE, Egypt, Saudi Arabia

Mehtap ArslanHR Gulf

Hicham MirghaniMarketing Maghreb

Issam Abu GhaidaFinance Middle East

TurkishWorked in Turkey, UAE

French / SudaneseWorked in France, Morocco

Palestinian / AustrianWorked in Austria, Switzerland, Germany, Saudi Arabia, Egypt

Nibal ZarourMarketing Levant

Michel BennajiLegal Middle East

Rula KassemMarketing Company President Levant

LebaneseWorked in Lebanon

French / TunisianWorked in France, Belgium

JordanianWorked in Jordan

Have added ~600 FTEs since 2004 (now at ~1 000) while building qualityHave added 600 FTEs since 2004 (now at 1,000) while building quality

Our strategy going forward

Expand our market

Example – AlgeriaDrive share in our currently marketed portfolio

Introduce AZ’s new global launch products

coverage

Example – Saudi Arabiap

Example – Saudi Arabia

p

Saudi Arabia is an attractive market with high growth

Saudi Arabia Rx market sales Key growth drivers

Saudi Arabia

y g

• Strong economic fundamentals and natural resource wealth$4.3-5.2bn

• Increasing unmet medical need – especially cardio-metabolic

$4.3 5.2bn

• Growth in private insurance coverage

I t t t i$1 7bn

$2.9bn

• Investments to improve healthcare quality and access in public payers

$1.7bn

2009 2014E12004

1 Projection based on sustained growth at 8-12% per annum. Source: IMS Global Market Prognosis, June 2009; AZ analysis

In Saudi Arabia, we have tailored our approach to the three different segments of the marketthree different segments of the market

Saudi Arabia

Traditional focus of AZ Saudi Arabia Expanding our business in Saudi Arabia

Private physicians & clinics% of market value – 61%

Ministry of Health% of market value – 17%

Institutions% of market value – 22%

We rapidly deployed resources and built capabilities to grow across all three markets segmentsac oss a t ee a ets seg e ts

We have more than doubled our sales in Saudi Arabia

Saudi Arabia

AZ sales in Saudi Arabia

+20%$97m

$39m

20092004

Source: AstraZeneca

Our major brands have significant momentum

Sales in Saudi Arabia

Saudi Arabia

Sales in Saudi Arabia of our top brands*2009

$22

AZ product growthCAGR, 2004-09**

Segment growthCAGR, 2004-09**

20% 15%

$22m

$22m 20% 15%

22% 20%$22m 22% 20%

29% 14%$10m

$9m 17% 16%

$8m 39%1 19%

1 2005-09 growth. Source: *AstraZeneca **IMS

Our pipeline products are well-suited to patient needs across Saudi Arabiaacross Saudi Arabia

Saudi Arabia

Pipeline products

Segment value1, 2009

Patient need

$50 150 30% f d th l t d t h t$50-150m 30% of deaths are related to heart disease or atherosclerosis

$100-300m Out of the top 10 countries for diabetes

Dapagliflozin

$100-300m Out of the top 10 countries for diabetes prevalence worldwide, six are in the MENA region including Saudi Arabia

Ceftaroline

$100-200m ~4% of all Saudi Arabian hospital patients are infected by MRSA

Vimovo $50-150m ~53% of men and ~61% of women in Saudi Arabia suffer from Osteoarthritis

• Started building sales force focusing on large cities- 100 reps- 10 FLSM- 2 SLSM2 SLSM

• Grew to #10 pharma company with 30% YoY sales growth2009

Source: AZ

In Algeria we continue to expand our local presence and will be launching key productswill be launching key products

AZ will now introduce 5-10 of Our products are in large markets its large global brands in the next 3 years

Brands have seen very strong

with high growth

Total market 2009Brands have seen very strong performance in other markets

E l

CAGR 04-09

~$60mExamples $60m

~$45m

~$30m~$40m

~$30m

~$15m

Statins Calcium-channel blockers

Anti-psyschotics

Hormone antagonists

PPIs

24% 14% 6% 25%31%

Source: IMS

blockers

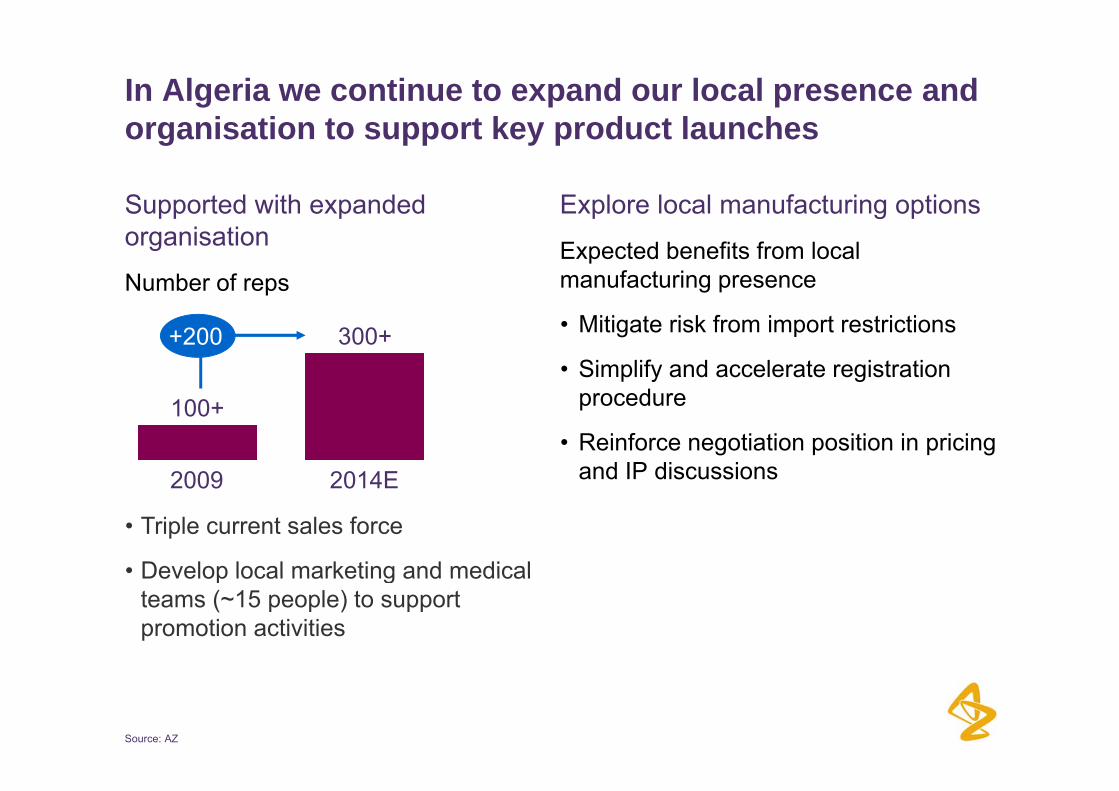

In Algeria we continue to expand our local presence and organisation to support key product launchesorganisation to support key product launches

Supported with expanded Explore local manufacturing optionspp porganisation

Number of reps

p g p

Expected benefits from local manufacturing presence

• Mitigate risk from import restrictions

• Simplify and accelerate registration procedure

300++200

procedure

• Reinforce negotiation position in pricing and IP discussions2014E2009

100+

2014E2009

• Triple current sales force

• Develop local marketing and medicalDevelop local marketing and medical teams (~15 people) to support promotion activities

Source: AZ

MENA – an example of the potential of small and medium sized marketsmedium-sized markets

• Small and mid-size markets can aggregate up to form a material business

• We have significant untapped potential in some large marketsin some large markets

• We have a portfolio and pipeline that is incredibly relevant to the MENA regionincredibly relevant to the MENA region

• A larger number of small markets may reflect a higher level of complexity, but can be managed effectively as a portfolio

AstraZeneca believes emerging g gmarkets are a sustainable opportunityopportunity

Our strategy in emerging markets has three elements

Continue to grow Extending our Broaden portfolio to

A B CContinue to grow our presence in the large BRIC-MT markets

Extending our geographic foot-print by increasing our involvement in

Broaden portfolio to selectively include branded generics

markets our involvement in high-growth small and mid-size markets

Brands dominate the market as brands are the best proxy for qualitythe best proxy for quality

Emerging market sales1, 2009, Ex-manufacturerg g , ,

~$50bn

~$30bn(~17%) ~$180bn

(~28%)

~$90bn(~50%)( 50%)

Branded Branded Commodity

~$10bn (~5%)

Patented originalsgenericsgenerics Totaloriginals

1 Projected from 17 selected markets (China, Turkey, India, South Korea, Brazil, Mexico, Poland, Russia, Taiwan, Hungary, Romania, Egypt, Algeria, Saudi Arabia, South Africa, Ukraine, UAE) to reflect total in emerging markets. Source: IMS; AZ analysis.

Why we believe we can succeed in branded generics

We are well positioned for success / profitabilityp p y

• We have the capabilities needed

- AstraZeneca is a world leader across emerging and establishedAstraZeneca is a world leader across emerging and established markets at building brands

• We will follow a highly focused branded generics strategy

- Stringent criteria to select only markets and products where we can achieve success

• Branded generics planned for:

~30 markets out of 100+ selected

~100 molecules out of 2,000+ originally profiled

Our strategy is focused on where we can compete profitablycan compete profitably

We focus on products where we can…p

• Leverage AZ infrastructure, sales force, strength, and presence

• Focus on quality as a primary factor in customer product selectionFocus on quality as a primary factor in customer product selection

• Differentiate our product through dosage, formulation, combinations, etc…

• Create a ‘new’ market where products have demand but are not promoted or are under promoted by the originator

• Strengthen AZ positioning across the portfolio in government tenders without addition sales force resources

… and where we can obtain favourable pricing – e.g. similar to our branded originals

We have chosen a highly selective initial portfolio of ~100 molecules~100 molecules

Molecules to be launched as branded generics, number of g ,molecules by TA

~30-40

~20-3015 25

~20-30

~5-15~10-20~15-25

Other2RespiratoryGIOncologyCV1CNS

Aligned to areas of AstraZeneca expertise

1 Including Diabetes; 2 Most common drugs in this group are anticoagulants, painkillers and anti-infectives. Source: AZ Internal

We will expand our relationship with Torrent to support the ramp up of our branded generics businessthe ramp-up of our branded generics business

• Torrent has a proven ability to manufacture to AstraZeneca’s high p y gstandards and a strong track record in a wide range of products

• We have a license and supply contract with Torrent for 18 products in 9 markets

• AstraZeneca will expand the agreement to cover additional products and markets to support the roll out of its branded generics businessmarkets to support the roll-out of its branded generics business

• AstraZeneca and Torrent have agreed a “heads of terms” defining the key pillars of a long-term strategic partneringy p g g p g

Let us show you two examples of our BGx country strategyof our BGx country strategy

Poland

Jerzy GarlickiMarketing Company President, Poland

M i

Ricardo Alvarez-TostadoMarketing Company President, MexicoMexico Mexico

Poland is a growing market with the government serving as the primary payeras the primary payer

Poland Rx market salesConstant exchange rate

• Government is the i

~$10bn

~10% p.a.primary payer

• Patients make significant co-pays for drugs listed

~$7bnp y g

for reimbursement

• Physicians are largest influencers in medicine /

~$5bn

Sales rank among world pharma markets

influencers in medicine / brand selection

• Prescriptions written for f

19th 18th 17th

specific brands, with limited switching

201420092004

Source: IMS Global Market Prognosis, June 2009

AstraZeneca has seen consistent above-market growth in Polandgrowth in Poland

AstraZeneca sales in Poland1

AZ tl k d• AZ currently ranked as #9 MNC in Poland (2009), up from #14 in 2004

$133m~14% p.a.

• Largest products in Poland are Zoladex, Pulmicort, Seloken and Symbicort

$68m

• Sales force of 300+ FTEs across ~10 therapeutic areastherapeutic areas

20092004

1 Actual exchange rate. Source: AZ internal data

Poland has a large BGx market estimated at ~$4.6bn

Total Rx sales1, 2009,

Branded generics

• ~75% of the market by value is branded

d ff t t

37%and off-patent

• Only 4% of the market by value is unbranded

4%Commodity generics

22%Patented y%originals

37%

Branded originals

1 Categorisation based on Q1-Q2 2008 data; retail market only. Source: IMS, AZ analysis

Why AZ believes Poland provides a sustainable BGx marketsustainable BGx market

• Physicians strongly prefer branded products; preferences y g y p p ; punlikely to shift significantly in next 3-5 years

• Unprompted switching at pharmacies occurs rarely (<5%)Unprompted switching at pharmacies occurs rarely (<5%)

• BGx market expected to grow at 5-6% through 2015

• Branded generics are attractively priced, with discounts from originator product prices typically limited to 5-30%

• Feasible for AZ to register branded BGx in ~18 months through the EU Mutual Recognition Process

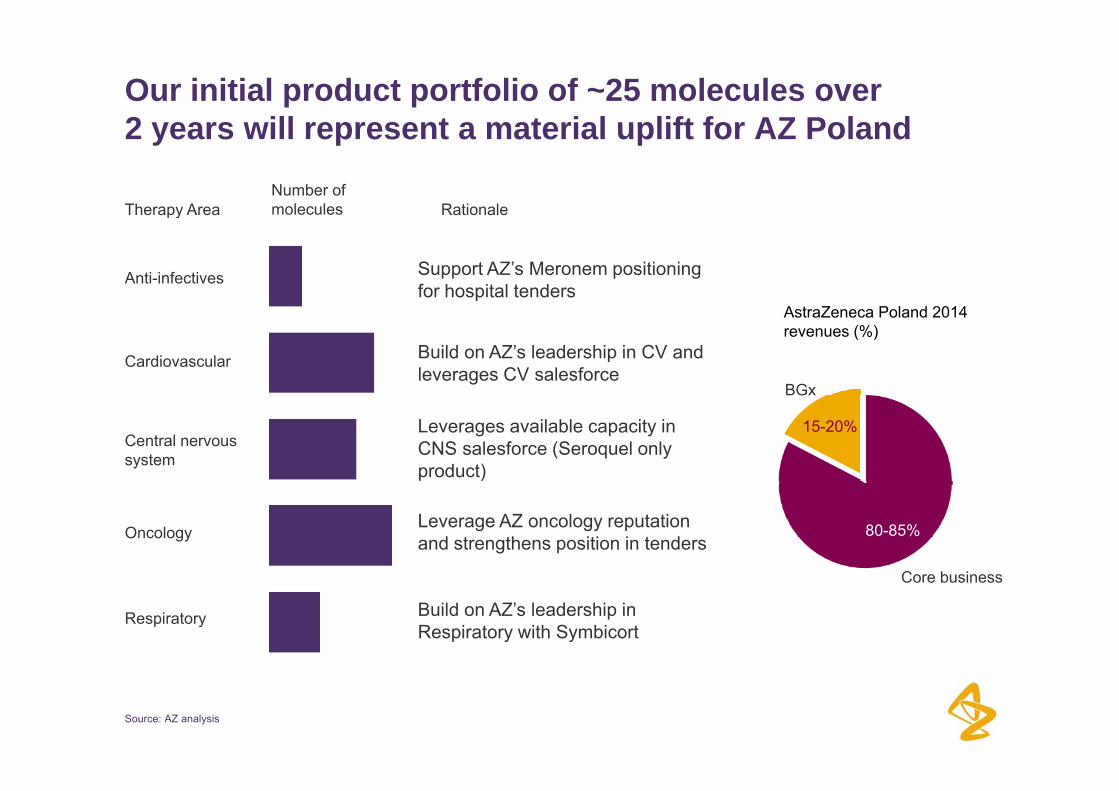

Our initial product portfolio of ~25 molecules over 2 years will represent a material uplift for AZ Poland2 years will represent a material uplift for AZ Poland

Therapy Area RationaleNumber of moleculespy

Support AZ’s Meronem positioning for hospital tenders

Anti-infectives

Build on AZ’s leadership in CV and leverages CV salesforce

AstraZeneca Poland 2014 revenues (%)

BGx

Cardiovascular

Leverages available capacity in CNS salesforce (Seroquel only product)

15-20%Central nervous system

Leverage AZ oncology reputation and strengthens position in tenders

80-85%

Core business

Oncology

Build on AZ’s leadership in Respiratory with Symbicort

Core business

Respiratory

Source: AZ analysis

We have ‘proof of concept’ in Poland

Pliva had little success with a generic version f T id

…With success coming only after partnering with AZ b d d iof Torasemide…

• Menarini first launched Trifas in 2000 in Poland

AZ on a branded generic

• By 2006, market underdeveloped with Menariniunderpromoting Trifas

- Trifas is a branded version of torasemide, a loop diuretic

• Pliva launched a commodity generic version

• AstraZeneca partnered with Pliva in 2006 to sell branded generic torasemide as Diuver

of torasemide in 2004

- Pliva supported the product with minimal promotion or engagement with stakeholders

- Product supported exclusively by AZ reps

• AstraZeneca successfully promoted the product with no added infrastructure or increase in sales force

- Generic gained almost zero share with Trifas maintaining almost constant share

increase in sales force

- AZ leveraged existing coverage of target customers (e.g. cardiologists) and strong reputation in CVreputation in CV

Success of an AstraZeneca promoted branded generic in Polandgeneric in Poland

Torasemide sales, 2004-09, $m, , $

• Diuver is the leader inDiuver Diuver is the leader in Torasemide with 37% sales share in therapeutic segment

Trifas

AstraZeneca begins exclusive promotion of

• Entire Torasemide market has grown >5x since AZ launch

exclusive promotion of Diuver

• Have also launched branded generics in oncology (Pamisol –pamidronic acid) and anti-pamidronic acid) and antiinfectives (Sumamed –azithromycin IV)

Mexico is a growing market with patients typically self paying for medicinesself-paying for medicines

Mexico Rx market salesConstant exchange rate

• Market primarily patient t f k t t

~$13bnCAGR ~6%

out-of-pocket payment

• Government spending on health limited to poorest

~10bnp

populations and social security targeted to lower income populations

~$7bn

Sales rank among world pharma markets

• Physicians largest influencers and prefer branded products10th 13th 14th

• Prescriptions rarely required with patients preferring brands

201420092004

144Source: IMS Global Market Prognosis, June 2009

AstraZeneca has been highly successful in Mexico

AstraZeneca sales in Mexico1• AstraZeneca is the fastest growing• AstraZeneca is the fastest growing

of the top 20 companies from 2001 to 2009 moving from rank #17 in 2001 to rank #8 in 2009$334m

• AZ are leaders in key therapeutic segments including:− Losec and Nexium for PPIs

$261m

$334m

$206m− Crestor in statins− Tenormin and Seloken for

beta-blockers

200920072004

− Pulmicort in inhaled corticosteroids

• Sales share of Seroquel XR in• Sales share of Seroquel XR in Mexico is highest of any market worldwide

• Sales force total of ~600 FTEs

Dip in 2009 sales due to massive contraction in Mexico economy (-7% GDP growth, 2008-09) and

one-time charge due to change in distribution model

1451 Actual exchange rate. Source: AZ internal data

• Sales force total of 600 FTEs across ~15 therapeutic areas

one time charge due to change in distribution model

Mexico has the highest prices for branded generics among large Emerging Marketsamong large Emerging Markets

Retail price comparison across Emerging Markets1, Indexp p g g ,

Mexico

Russia

Brazil

Poland

Turkey

1 Sample size includes 19 large BGx products. Source: IMS; AZ analysis

Using the AZ criteria and approach, our initial BGx portfolio will represent a material uplift for AZ Mexicoportfolio will represent a material uplift for AZ Mexico

Th A R ti lNumber of

l lTherapy Area Rationale

Build on AZ’s leadership in CV

Leverage reputation and relationships

molecules

Cardiovascular

Build on AZ’s leadership in GI with

Leverage reputation and relationships with GPs, Internal Medicine, and Endocrincologists to support market development for Onglyza AstraZeneca Mexico 2014

revenues (%)

Diabetes

Gastro intestinal pLosec and Nexium

Build on AZ’s relationships with psychia-trists and leverage additional CNS sales force capacity

BGx

Neurology

Gastro-intestinal

10-20%

Oncology

Pain/ Support market development for

Leverage AZ oncology reputation

80-90%

Build on AZ’s leadership in Respiratory with Symbicort

Core business

Respiratory

Pain/inflammation

Support market development for Vimovo

Source: AZ

~30

Example product Diabetes fixed dose combinationDiabetes fixed dose combination

Product overview Why AstraZeneca can win

• Diabetes product prescribed heavily by GPs (~70% of all scripts) and internists (~20%)

• AstraZeneca has high recognition with GPs and internists due to strong primary care brands (e g Nexiuminternists (~20%)

• Product has favourable clinical profile and dosing versus key competitors,

primary care brands (e.g. Nexium, Crestor, Seloken, Symbicort)

• Product can leverage existing sales though captures low share due to lack of physician awareness of benefits

• Physicians switching to fixed-dose

force relationships and capacity to ensure physicians are aware of benefits vs competitors

Physicians switching to fixed dose combinations due to improved patient compliance

• Will also help build AstraZeneca diabetes franchise

A t Z j t th t it illAstraZeneca projects that it will capture 10-15% of this type of combination by 2015

Source: Interviews; IMS; team analysis

Example product – We understand how to successfully position branded genericsposition branded generics

Average unit Mexico oralanti-diabetics

We can successfully

Pricing Volume ValueNo. ofplayers

~16

price premium in segment

8-10x8%High 37% yand profitably position our branded generic anti-diabetic in these

16 8-10xMedium 13%

8%High 37%

segments~16 3-5x22%

Low cost, highly competitive commoditised mass

~125 1xLow 41%79%

market – (low priced BGx, commodity Gx)

Source: IMS

Key takeaways on our branded generics plan

• We are taking a selective approach in branded generics, focused g pp g ,on the markets and products where we can compete profitably

• Our plan will create a material business amounting to 10-15% of ourOur plan will create a material business amounting to 10-15% of our emerging markets business by 2014

We have the capabilities required to successfully execute on our plans• We have the capabilities required to successfully execute on our plans

• The business is ‘real’ – we are putting in place the partnerships to source our initial 100 molecule portfolio

Our strategy in emerging markets has three elements

Emerging markets strategy

Continue to grow Extending our Broaden portfolio to

A B CContinue to grow our presence in the large BRIC-MT markets

Extending our geographic foot-print by increasing our involvement in

Broaden portfolio to selectively include branded generics

markets our involvement in high-growth small and mid-size markets

Our goal is to continue double-digit growth, with emerging markets becoming ~25% of AZ sales by 2014emerging markets becoming ~25% of AZ sales by 2014

AZ emerging markets revenue goalg g g

$12bn

$8bn

$4bn

20142009$0bn

Emerging MarketsEmerging Markets Investor Day y

16 March 2010

Drivers of AstraZeneca success to date

We were 1st to invest in China, the largest Emerging Market opportunity, g g g pp y

We have been successful at catching up quickly in other markets

We have built strong local organisations to successfully manage local market dynamics

We support our local organisations with the best practice of our global capabilities

We have a diverse portfolio of relevant products

Our strategy in emerging markets has three elements

Emerging markets strategy

Continue to grow Extending our Broaden portfolio to

A B CContinue to grow our presence in the large BRIC-MT markets

Extending our geographic foot-print by increasing our involvement in

Broaden portfolio to selectively include branded generics

markets our involvement in high-growth small and mid-size markets

Emerging markets are forecast to contribute ~70% of pharma growth in the next 5 years~70% of pharma growth in the next 5 years

Worldwide pharmaceutical sales$955bn$130bn

Emerging Markets 70%

$55bnEstablished Markets 30%

$765bn

2009E 2014E

Emerging markets projected to grow at a 12% CAGR from 2009-2014

1 Emerging markets are all markets outside EU-15, Norway, Switzerland, Iceland; US, Canada, Japan, Australia, New Zealand. Source: IMS extrapolation.