38

Babu Ram Dawadi

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | naomi-lawson |

| View: | 214 times |

| Download: | 1 times |

Babu Ram Dawadi

E-Business

The Internet is a powerful channel that presents new opportunities for an organization to:Touch customersEnrich products and services with information

Reduce costs

E-BusinessBusiness Model: set of planned activities

designed to result a profit in a market place.

Business plan: document that describes a firms business model

How do e-commerce and e-business differ?E-commerce – the buying and selling of goods and

services over the Internet

E-business – the conducting of business on the Internet including, not only buying and selling, but also serving customers and collaborating with business partners

E-commerce business model: aims to use and leverage the unique qualities of internet and web

E-Business

Industries Using E-Business

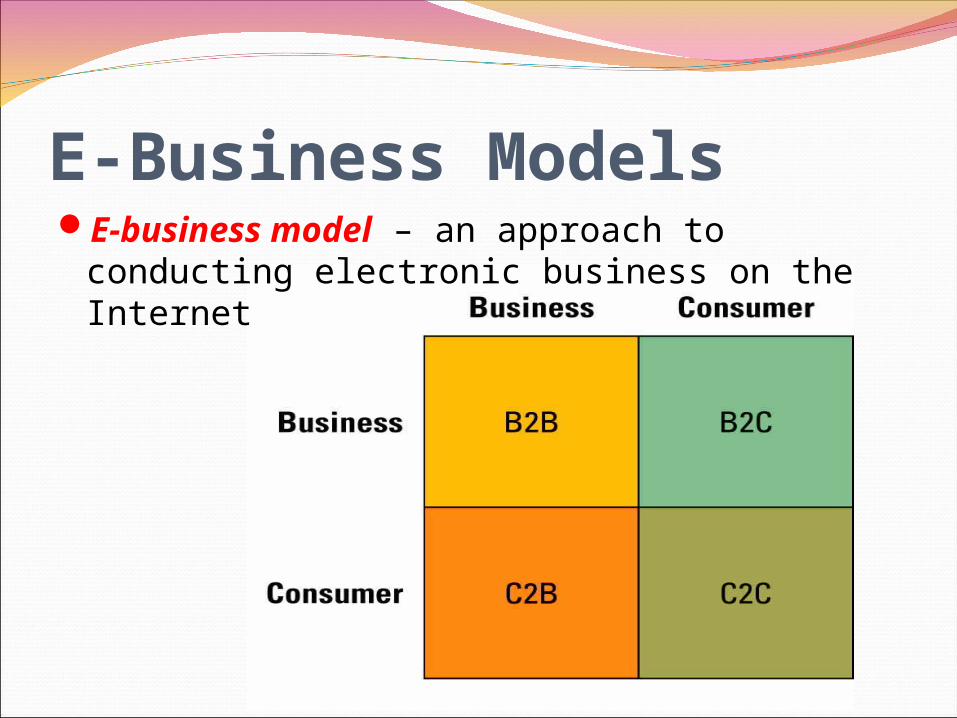

E-Business ModelsE-business model – an approach to

conducting electronic business on the Internet

E-Business Models

E-Business Models

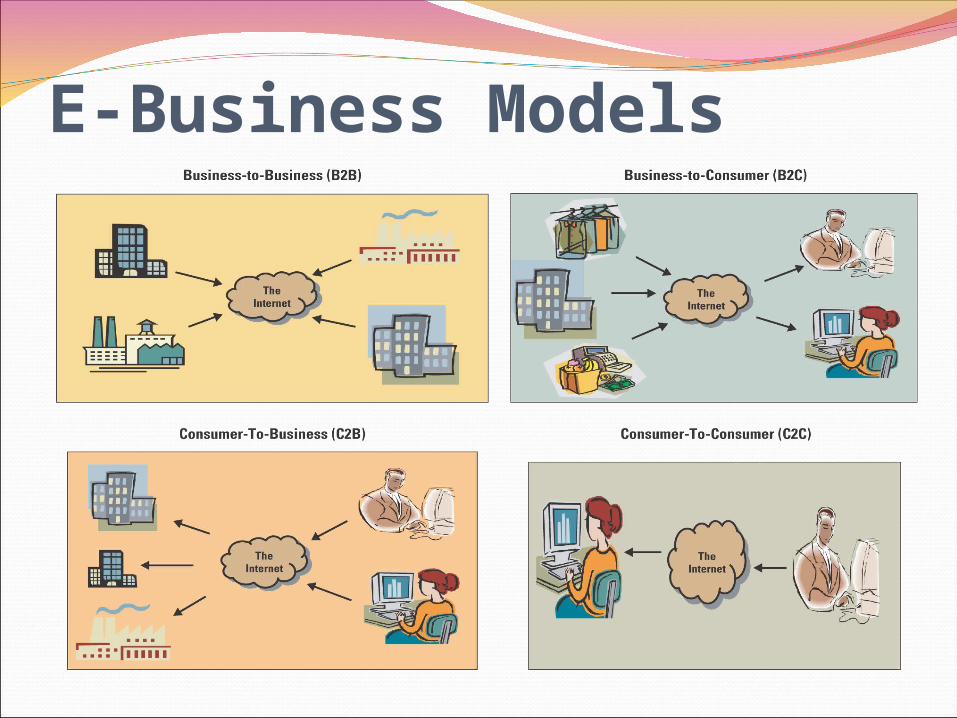

Business-to-Business (B2B)

Electronic marketplace (e-marketplace) – interactive business communities providing a central market where multiple buyers and sellers can engage in e-business activities

Business-to-Consumer (B2C)Common B2C e-business models

include:e-shop – a version of a retail store where customers can shop at any hour of the day without leaving their home or office

e-mall – consists of a number of e-shops; it serves as a gateway through which a visitor can access other e-shops

Business types:Brick-and-mortar business: operates in a

physical store without an Internet presence.

Pure-play (virtual) business - a business that operates on the Internet only without a physical store. Examples include Amazon.com and Expedia.comClick-and-mortar business

Click-and-mortar business – a business that operates in a physical store and on the Internet

Consumer-to-Business (C2B)

Priceline.com is an example of a C2B e-business model

The demand for C2B e-business will increase over the next few years due to customer’s desire for greater convenience and lower prices

Consumer-to-Consumer (C2C)

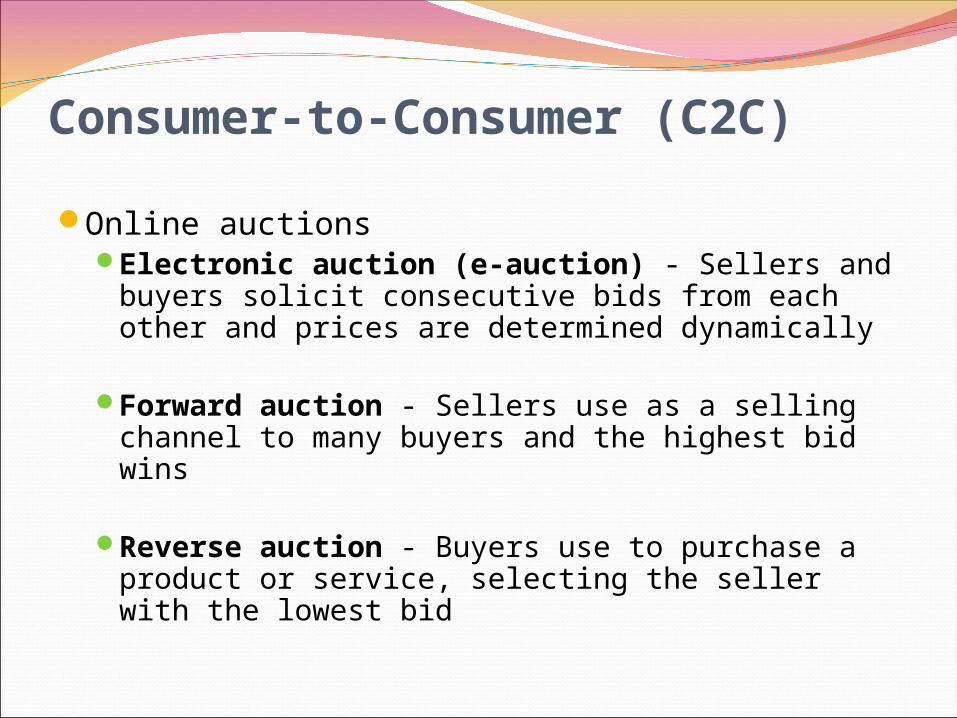

Online auctionsElectronic auction (e-auction) - Sellers and

buyers solicit consecutive bids from each other and prices are determined dynamically

Forward auction - Sellers use as a selling channel to many buyers and the highest bid wins

Reverse auction - Buyers use to purchase a product or service, selecting the seller with the lowest bid

Consumer-to-Consumer (C2C)

C2C communities include:Communities of interest - People interact with

each other on specific topics, such as golfing and stamp collecting

Communities of relations - People come together to share certain life experiences, such as cancer patients, senior citizens, and car enthusiasts

Communities of fantasy - People participate in imaginary environments, such as fantasy football teams and playing one-on-one with Michael Jordan

E-Business Benefits and ChallengesE-Business benefits include:

Highly Accessible - Businesses can operate 24 hours a day, 7 days a week, 365 days a year

Increased Customer Loyalty - Additional channels to contact, respond to, and access customers helps contribute to customer loyalty

Improved Information Content- In the past, customers had to order catalogs or travel to a physical facility before they could compare price and product attributes. Electronic catalogs and Web pages present customers with updated information in real-time about goods, services, and prices

Increased Convenience - E-business automates and improves many of the activities that make up a buying experience

Increased Global Reach - Businesses, both small and large, can reach new markets

Decreased Cost - The cost of conducting business on the Internet is substantially smaller than traditional forms of business communication

E-Business Benefits and Challenges

E-business challenges include:Protecting consumersLeveraging existing systemsIncreasing liabilityProviding securityAdhering to taxation rules

E-Business Benefits and ChallengesThere are numerous advantages and

limitations in e-business revenue models including: Transaction feesLicense feesSubscription feesValue-added feesAdvertising fees

Case7-Eleven’s Dream Team 7-Eleven Japan has integrated its online

site 7dream.com with its physical stores

Through the 7dream.com Web site, 7-Eleven Japan enables consumers to choose from an online assortment of 100,000 products which are picked up from one of 8,400 store locations

e-Payment System-----

Payments, Protocols and Related IssuesSET Protocol is for Credit Card Payments

Electronic Cash and Micropayments

Electronic Fund Transfer on the Internet

Stored Value Cards and Electronic Cash

Electronic Check Systems

Security requirements

Payments, Protocols and Related Issues (cont.)

Authentication: A way to verify the buyer’s identity before payments are made

Integrity: Ensuring that information will not be accidentally or maliciously altered or destroyed, usually during transmission

Encryption: A process of making messages indecipherable except by those who have an authorized decryption key

Non-repudiation: Merchants need protection against the customer’s unjustifiable denial of placed orders, and customers need protection against the merchants’ unjustifiable denial of past payment

Security SchemesSecret Key Cryptography (symmetric)

Scrambled Message

Original Message

Sender

InternetScrambled Message

Keysender (= Keyreceiver)

Encryption

Original Message

Receiver

Keyreceiver

Decryption

Electronic Credit Card System on the InternetThe Players

Cardholder

Merchant (seller)

Issuer (your bank)

Acquirer (merchant’s financial institution, acquires the sales slips)

Brand (VISA, Master Card)

Credit Card paymentStep 1: customer sends a purchase order with an

encrypted credit card number (encrypted with credit card company’s bank’s key)to the merchant.

Step 2: the merchant send the amount of purchase with the customer’s credit card number (encrypted) to the credit card company’s bank. The bank decrypts the card number, authenticates signature and check credit balance on the card

Step 3: if it is ok, it checks with credit card company to see if card is ok

SET Protocol….Step 4: credit card company OKs the transaction and

signs it showing customers transaction details in customer account

Step 5: the bank when it receives the signed authorization from the credit card company sends a message to the merchant to honour the purchase order and credits the merchant account by appropriate amount

Step 6: the merchant accepts customer’s purchase order and informs him about delivery details

Step 7: at the end of the month the credit card company sends a consolidated bill to the customer

Merchant

Customer

BankCredit Card Company

Step 1: Send P.O.

Step 2: check C.C. and signature

Step 3: C.C. OK?

Step 4: OK

Step 5: OK transaction And Merchant credit account

Step 6: Delivery Details

Step 7: Bill to Customer

Electronic Fund Transfer (EFT) on the Internet

An Architecture of Electronic Fund Transfer on the Internet

InternetPayer

Cyber Bank

Bank

Cyber Bank

Payee

AutomatedClearinghouse

VANBank

VAN

PaymentGateway

PaymentGateway

Financial EDIIt is an EDI used for financial transactions

EDI is a standardized way of exchanging messages between businesses

EFT can be implemented using a Financial EDI system

Safe Financial EDI needs to adopt a security scheme used for the SSL protocol

Extranet encrypts the packets exchanged between senders and receivers using the public key cryptography

Electronic Cash and MicropaymentsSmart Cards

The concept of e-cash is used in the non-Internet environment

Plastic cards with magnetic stripes (old technology) Includes IC chips with programmable functions on

them which makes cards “smart” One e-cash card for one application Recharge the card only at designated locations,

such as bank office or a kiosk. Future: recharge at your PC

e.g. Mondex & VisaCash

Smart Cards

• Smart card processors hold more information than credit card magnetic strips– Store credit-card numbers, contact information, etc.

– Contact smart cards

• Placed in smart-card reader for information transfer– Contactless smart cards

• Antenna enables information transfer

• Faster than contact smart card

• Security– Password protection

– Security designations assigned to information

– Encryption

Smart Card Example -- Mondex

• Smart-card-based, stored-value card (SVC)• Subsidiary of MasterCard• Secret chip-to-chip transfer protocol• Value is not in strings alone; must be on Mondex

card• Loaded through ATM

– ATM does not know transfer protocol; connects with secure device at bank

• Spending at merchants having a Mondex value transfer terminal

Mondex Makes Shopping Easy

Shopping with Mondex

Adding money to the card

Payments in a new era of electronic shopping

Paying on the Internet

Electronic MoneyDigiCash

The analogy of paper money or coins Expensive, as each payment transaction must be

reported to the bank and recorded Conflict with the role of central bank’s bill

issuance Legally, DigiCash is not supposed to issue more

than an electronic gift certificate even though it may be accepted by a wide number of member stores

Stored Value CardsElectronic Money (cont.)

No issuance of money Debit card — a delivering vehicle of cash in an

electronic form Either anonymous or onymous Advantage of an anonymous card

the card may be given from one person to another

Also implemented on the Internet without employment of an IC card

Smart card-based e-cashCan be recharged at home through the InternetCan be used on the Internet as well as in a non-

Internet environment

Ceiling of Stored Values To prevent the abuse of stored values in money

laundryS$500 in Singapore; HK$3,000 in Hong Kong

Multiple CurrenciesCan be used for cross border payments

Electronic Money (cont.)

Contactless IC Cards

Proximity CardUsed to access buildings and for paying in

buses and other transportation systemsBus, subway and toll card in many cities

Amplified Remote Sensing CardGood for a range of up to 100 feet, and can be

used for tolling moving vehicles at gatesPay toll without stopping (e.g. Highway 91 in

California)

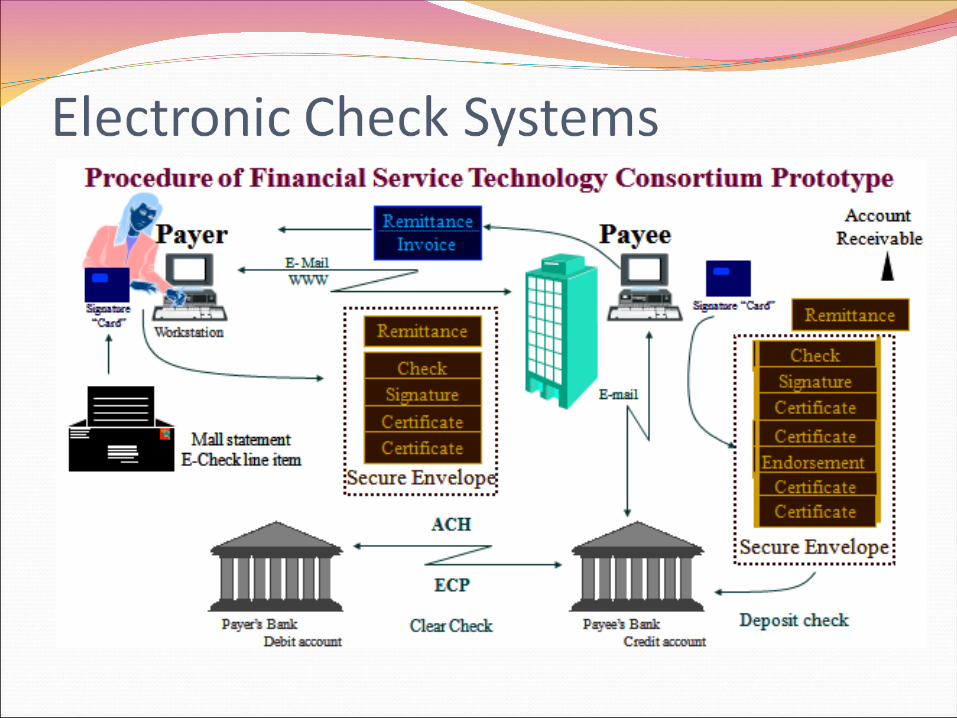

Electronic Checkbook

Electronic Check Systems (cont.)

Counterpart of electronic wallet To be integrated with the accounting information

system of business buyers and with the payment server of sellers

To save the electronic invoice and receipt of payment in the buyers and sellers computers for future retrieval

Example : SafeCheck Used mainly in B2B

Five Security Tips Don’t reveal your online Passcode to anyone. If

you think your online Passcode has been compromised, change it immediately.

Don’t walk away from your computer if you are in the middle of a session.

Once you have finished conducting your banking on the Internet, always sign off before visiting other Internet sites.

If anyone else is likely to use your computer, clear your cache or turn off and re-initiate your browser in order to eliminate copies of Web pages that have been stored in your hard drive.

Bank of America strongly recommends that you use a browser with 128-bit encryption to conduct secure financial transactions over the Internet.