18

Bad debts and Provision for Bad debts

| Date post: | 04-Jun-2018 |

| Category: |

Documents |

| Upload: | iqra-afsar |

| View: | 213 times |

| Download: | 0 times |

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 1/18

Bad debts and Provision for

Bad debts

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 2/18

Bad DebtsWhen the firm finds that it is impossibleto collect a debt, that debt should bewritten off as a bad debt.

Accounting Entries:

Dr Bad Debts

Cr DebtorWith the irrecoverable amount of a

debt

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 3/18

ExampleDuring the year, a company sold goodsfor $2,000 to Mr. Lee, $1,500 toMr.Wong and $300 to Mr. Wu.

Mr. Lee and Mr. Wong paid thecompany $800 and $1,000 respectively

Later, Mr. Wong and Mr. Wu became

bankrupt, and it is impossible for thecompany to collect these debts.

The company decided to write these offas bad debts.

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 4/18

Mr. Lee$ $

Bank 800

Mr. Wong

$ $

Sales 1,500 Bank 1,000

Sales 2,000

2,000 2,000

Balance c/f 1,200

Bad Debts 500

Mr. Wu

$ $Sales 300 Bad Debts 300

Bad Debts

$ $

Mr. Wong 500

Mr. Wu 300

P/L 800

800 800

1,500 1,500

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 5/18

B. Provision for Bad / Doubtful Debts

A provision for bad and doubtful debtsmay be made when a firm thinks that

there will be problems in recovering adebt.

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 6/18

Accounting entries

1. Increase in

provision

Dr Profit and LossCr Provision for Bad

Debts

With the increase in the amount of

provision for bad debts

2. Decrease in

provision

Dr Provision for BadDebts

Cr Profit and Loss

With the decrease in the amount of

provision for bad debts

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 7/18

Increase in provision for bad debtsExample

A firm decided to make a provision for

bad debts at 10% of the debtors’ accounts which totalled $50,000 on 31December 1994.

On 31 December 1995, the debtorsaccounts totalled $60,000. The firmmaintained the provision at 10% of its

total debtors.

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 8/18

Provision for Bad Debts

1994 $ 1994 $

Dec 31 Balance c/d 5,000

($50,000 * 10%)

Dec 31 Profit and loss 5,000

Profit and Loss Account for the year ended 31 December (Extract)

Gross profit

Less: Expenses

Increase in provision for bad debt 5,000

$X$

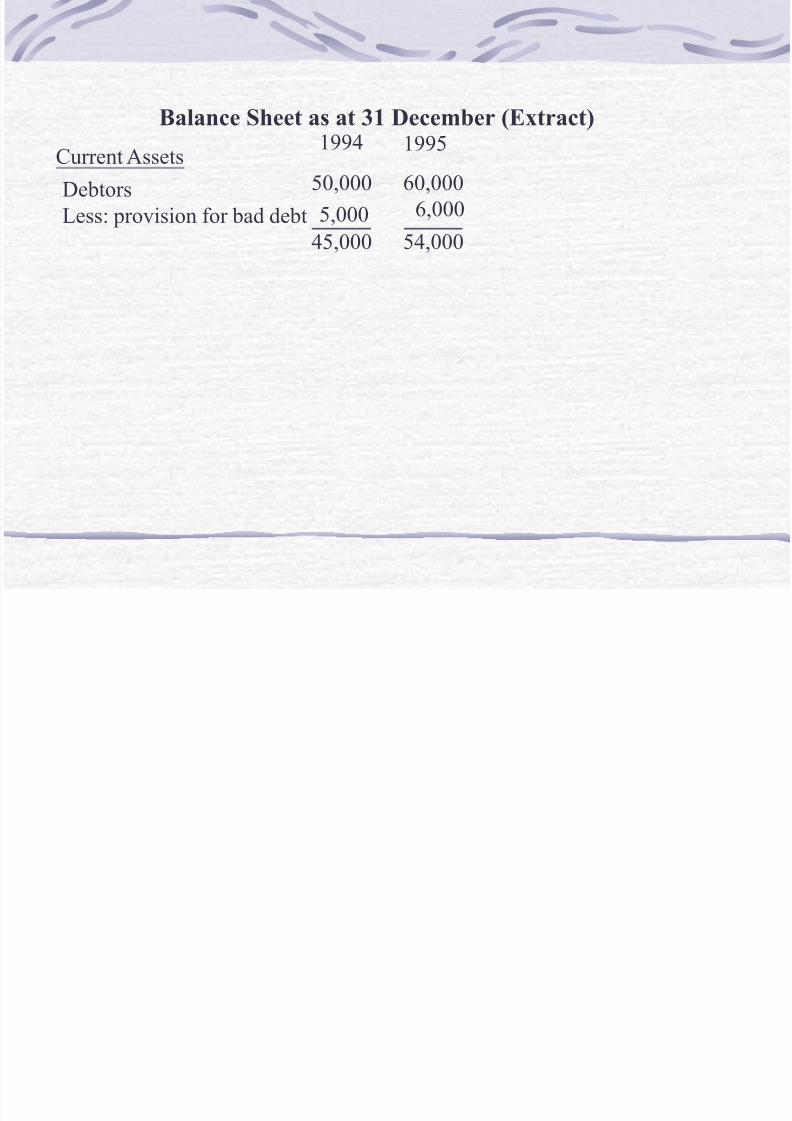

Balance Sheet as at 31 December (Extract)

1994

Current Assets1994

Debtors

Less: provision for bad debt

50,000

5,000

45,000

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 9/18

Provision for Bad Debts

1994 $ 1994 $

Dec 31 Balance c/d 5,000($50,000 * 10%)

Dec 31 Profit and loss 5,000

1995

Dec 31 Balance c/f

($60,000*10%) 6,000

1995Jan 1 Balance b/d 5,000

Dec 31 Profit and Loss 1,000

6,000 6,000

Profit and Loss Account for the year ended 31 December (Extract)

Gross profit

Less: Expenses

Increase in provision for bad debt 5,000

$X$

1994 1995

$ $X

1,000

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 10/18

Balance Sheet as at 31 December (Extract)

Current Assets 1994

Debtors

Less: provision for bad debt

50,000

5,000

45,000

1995

60,000

6,000

54,000

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 11/18

Decrease in Provision for bad debtsExample

The debtors’ accounts on 31 December

1996 totalled $40,000. The firm decidedto maintain the provision at 10% of thetotal debtors.

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 12/18

Provision for Bad Debts

1994 $ 1994 $

Dec 31 Balance c/d 5,000

($50,000 * 10%)

Dec 31 Profit and loss 5,000

1995

Dec 31 Balance c/f

($60,000*10%) 6,000

1995Jan 1 Balance b/d 5,000

Dec 31 Profit and Loss 1,000

6,000 6,000

1996 $ 1996 $

6,000

Jan 1 Bal b/f 6,000Dec 31 Profit and Loss 2,000

6,000

31 Balance c/f

($40,000*10%) 4,000

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 13/18

Profit and Loss Account for the year ended 31 December (Extract)

Gross profit

Less: Expenses

Increase in provision for bad debt 5,000

$X

$

1994 1995

$ $X

1,000

1996

$ $X

Add: Decrease in provision for bad debts 2,000

Balance Sheet as at 31 December (Extract)

Current Assets1994

Debtors

Less: provision for bad debt

50,000

5,00045,000

1995

60,000

6,000

54,000

1996

40,000

4,000

36,000

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 14/18

C. Bad Debts RecoveredBad debts recovered refers to debtsformerly written off to be recovered

later.

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 15/18

Accounting entries

Dr Debtors

Cr Bad Debts Recovered

With the debt reinstated in the debtor’saccount

Dr Cash/BankCr Debtors

With the amount received

Dr Bad Debts Recovered

Cr Bad Debts

ORDr Bad Debts Recovered

Cr Profit and Loss

With the debt written off in this year tobe recovered

OR

With the debt written off in a previousyear to be recovered

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 16/18

Example

The following balances were part of the trialbalance of Mr. Chan on 31 December 1996:

$

Debtors 10,000

Bad Debts 1,000

During the year, Mr. Chan received $300 and

$1,200 from debtors, whose debts had beenpreviously written off as bad debts in thecurrent year and last year respectively. Noentry has been made for these transactions

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 17/18

Bank1996 $

Dec 31 Debtors 1,500

Debtors1996 $

Dec 31 Bal b/d 10,000

1996 $

Dec 31 Bank 1,500

Dec 31 B.D.R. 300

Dec 31 B.D.R. 1,200

Bad Debt1996 $

Dec 31 Bal b/d 1,000

1996 $

Dec 31 B.D.R. 300

Dec 31 P & L 700

Bad Debt Recovered1996 $

Dec 31 P & L 1,200

1996 $

Dec 31 Debtors 300Dec 31 Bad Debt 300

Dec 31 Debtors 1,200

1,000 1,000

1,500 1,500

8/13/2019 Bad_debt

http://slidepdf.com/reader/full/baddebt 18/18

Profit and Loss Account for the year ended 31 December (Extract)

Gross profit

Less: Expenses

Bad Debt 700

1996

$ $

XAdd: Bad Debt Recovered 1,200