32

Badlands NGLs, LLC A US Ethane Project Case Study Feb 24, 2016 Badlands NGLS, LLC 1

Badlands NGLs, LLC

A US Ethane Project Case Study

Feb 24, 2016

Badlands NGLS, LLC1

Badlands Background

• Badlands NGLS, LLC (“Badlands”) was incorporated in

August of 2012. Since its inception, Badlands has been

engaged in the development of an ethane gas to

polyethylene (“PE”) petrochemical business.

• Badlands business plan contemplates PE manufacturing

as close to the wellhead as is feasible in order to take

advantage of physically and economically stranded

natural gas liquid (“NGL”) sourced ethane gas from such

resource plays as the Permian, the Marcellus and the

Bakken.

Badlands NGLS, LLC2

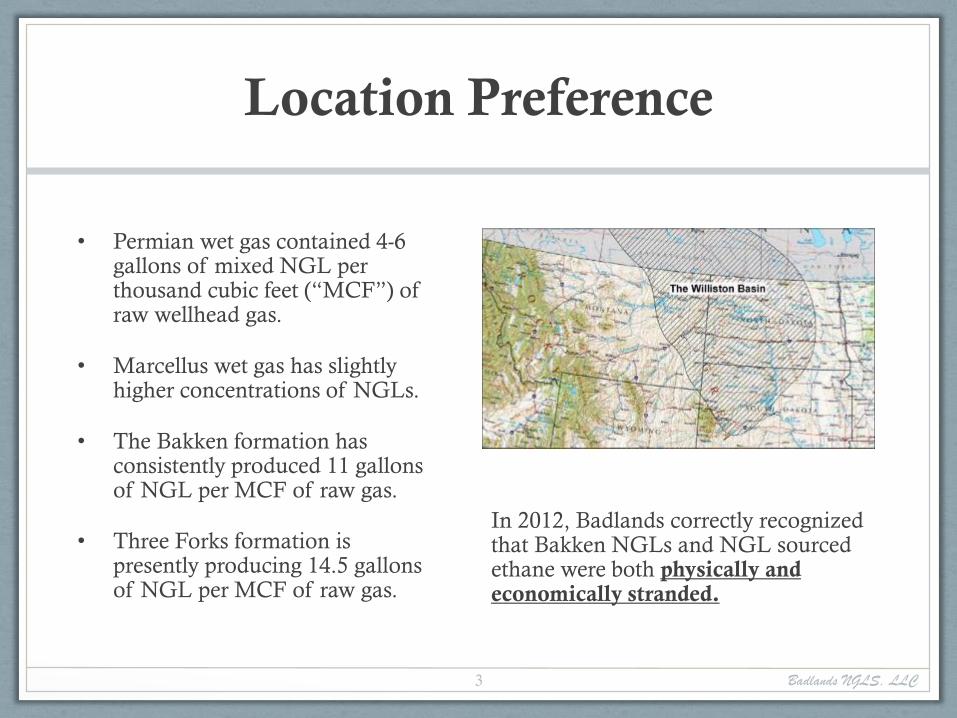

Location Preference

• Permian wet gas contained 4-6 gallons of mixed NGL per thousand cubic feet (“MCF”) of raw wellhead gas.

• Marcellus wet gas has slightly higher concentrations of NGLs.

• The Bakken formation has consistently produced 11 gallons of NGL per MCF of raw gas.

• Three Forks formation is presently producing 14.5 gallons of NGL per MCF of raw gas.

Badlands NGLS, LLC3

In 2012, Badlands correctly recognized that Bakken NGLs and NGL sourced ethane were both physically and economically stranded.

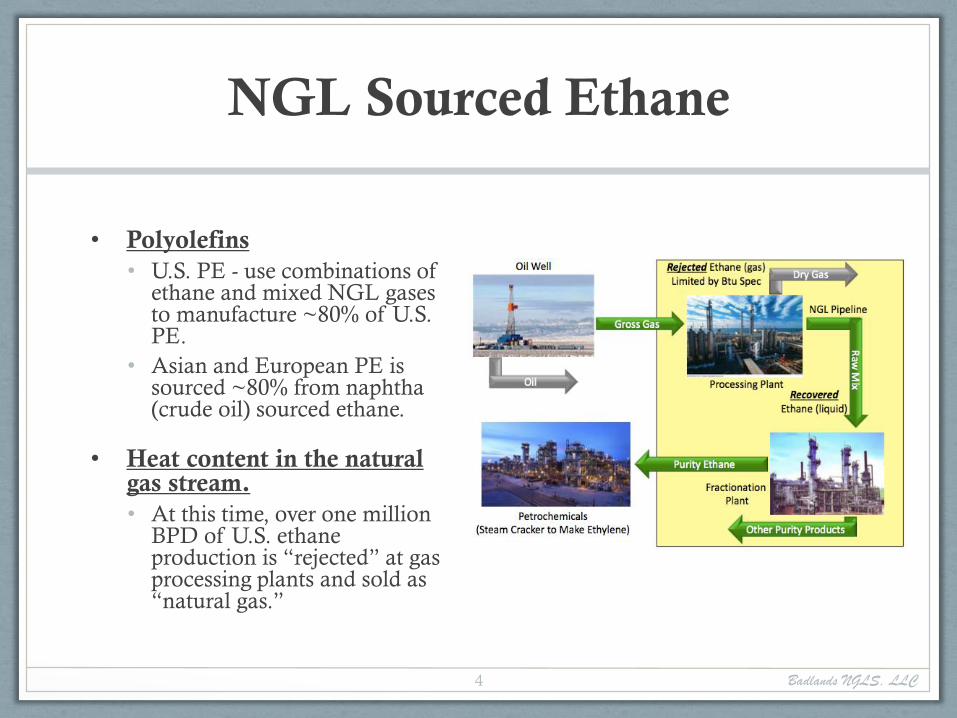

NGL Sourced Ethane

• Polyolefins

• U.S. PE - use combinations of ethane and mixed NGL gases to manufacture ~80% of U.S. PE.

• Asian and European PE is sourced ~80% from naphtha (crude oil) sourced ethane.

• Heat content in the natural gas stream.

• At this time, over one million BPD of U.S. ethane production is “rejected” at gas processing plants and sold as “natural gas.”

Badlands NGLS, LLC4

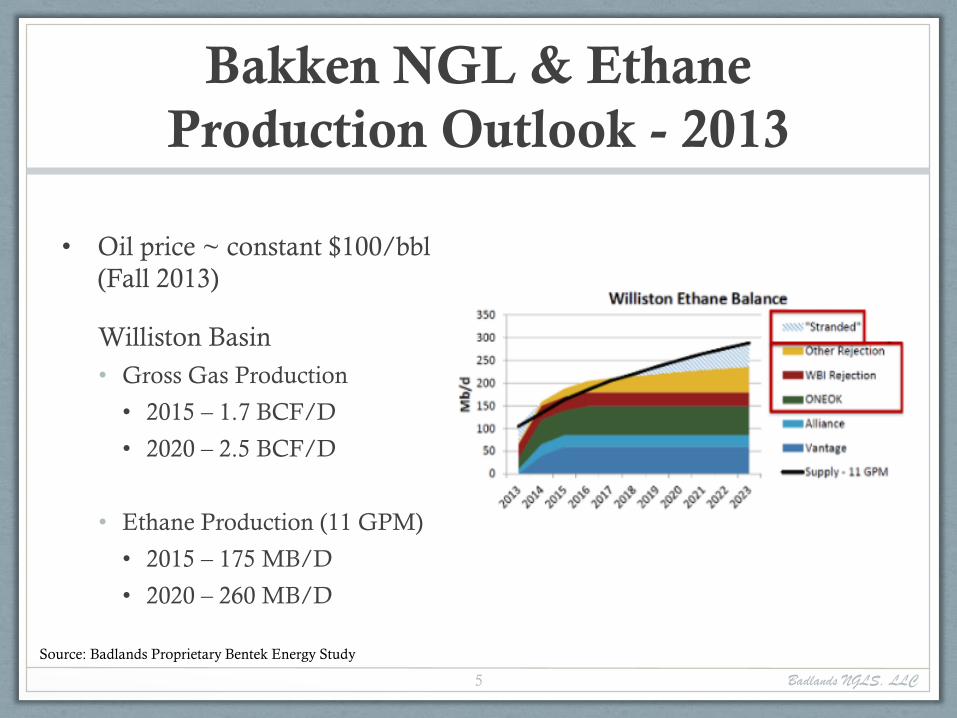

Bakken NGL & Ethane

Production Outlook - 2013

• Oil price ~ constant $100/bbl

(Fall 2013)

Williston Basin

• Gross Gas Production

• 2015 – 1.7 BCF/D

• 2020 – 2.5 BCF/D

• Ethane Production (11 GPM)

• 2015 – 175 MB/D

• 2020 – 260 MB/D

Badlands NGLS, LLC5

Source: Badlands Proprietary Bentek Energy Study

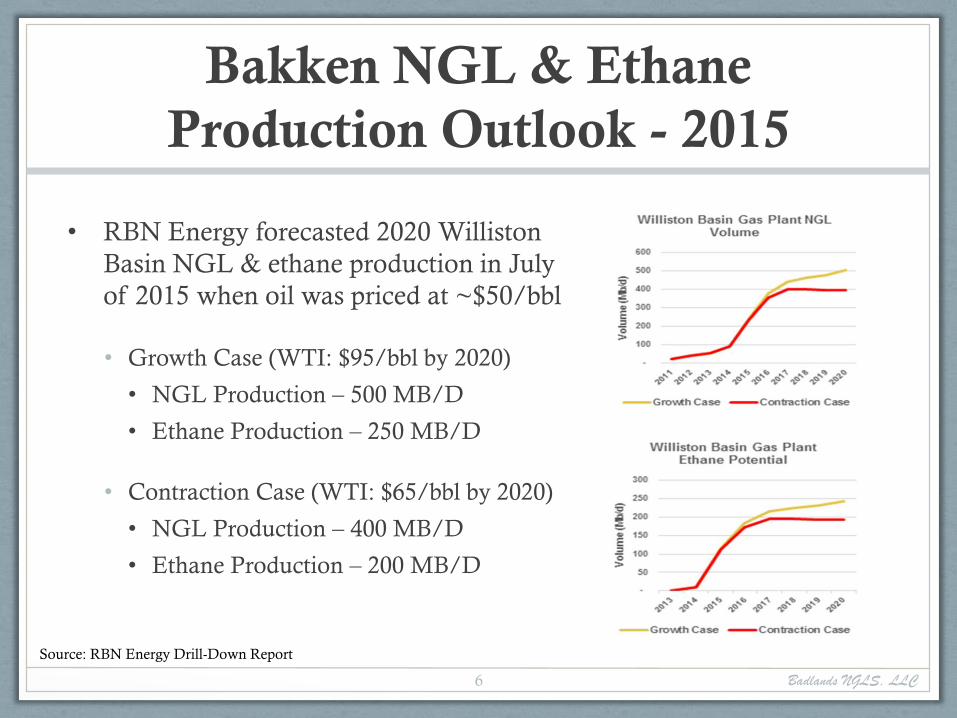

Bakken NGL & Ethane

Production Outlook - 2015

• RBN Energy forecasted 2020 Williston

Basin NGL & ethane production in July

of 2015 when oil was priced at ~$50/bbl

• Growth Case (WTI: $95/bbl by 2020)

• NGL Production – 500 MB/D

• Ethane Production – 250 MB/D

• Contraction Case (WTI: $65/bbl by 2020)

• NGL Production – 400 MB/D

• Ethane Production – 200 MB/D

Badlands NGLS, LLC6

Source: RBN Energy Drill-Down Report

Bakken NGL & Ethane

Production – July 2015

• July 2015 ND (includes Montana) Gas Production –

1.76 BCF vs. 1.7 BCF (2013)

• July 2015 Ethane Production – 250 MB/D vs. 175

MB/D (2013)

• Actual Bakken NGL and ethane production in the

summer of 2015 was greater than the amount

originally forecasted by Bentek in their 2013 study.

Badlands NGLS, LLC7

Source: North Dakota Industrial Commission

The Marcellus/Bakken

“Disparity”

• Marcellus producers have commitments to export 300 MB/D

of Marcellus ethane to Europe and India at take or pay pricing.

• These shipments will supply feedstock to approximately 25%

of European PE capacity.

• Who pays? - European and Indian PE manufacturers pay BTU

ethane price plus $0.35/gal. transportation costs.

• In contrast, the value of the ethane produced and sold for

North Dakota oil and gas producers bears no resemblance to

the market-plus-freight price realized by Marcellus oil and gas

producers.

Badlands NGLS, LLC8

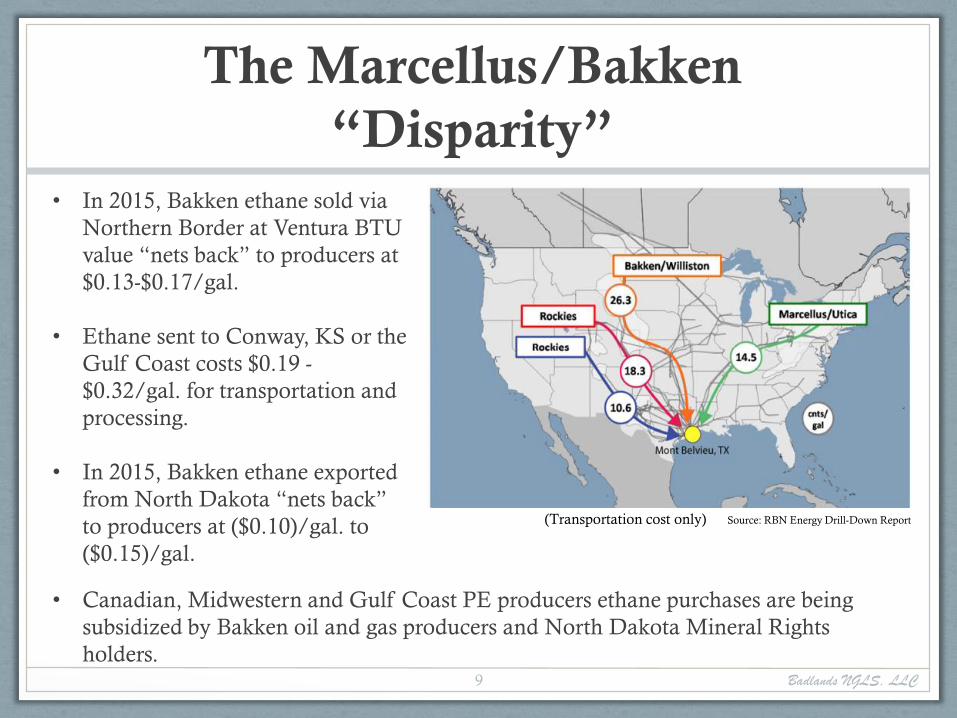

The Marcellus/Bakken

“Disparity”

Badlands NGLS, LLC9

• In 2015, Bakken ethane sold via

Northern Border at Ventura BTU

value “nets back” to producers at

$0.13-$0.17/gal.

• Ethane sent to Conway, KS or the

Gulf Coast costs $0.19 -

$0.32/gal. for transportation and

processing.

• In 2015, Bakken ethane exported

from North Dakota “nets back”

to producers at ($0.10)/gal. to

($0.15)/gal.

Source: RBN Energy Drill-Down Report

• Canadian, Midwestern and Gulf Coast PE producers ethane purchases are being

subsidized by Bakken oil and gas producers and North Dakota Mineral Rights

holders.

(Transportation cost only)

The Marcellus/Bakken

“Disparity”

• Marcellus Producers - get paid for both rejected ethane and PE feedstock ethane. Bakken

Producers - get paid for rejected ethane and subsidize PE producers and Bakken midstream

service providers for any and all non-rejected ethane.

• Assume oil price of only $60/BBL in 2020 and 100% of all Bakken ethane is transported

to the Gulf Coast and sold at today’s ethane market price, netback loss to Bakken

producers would be $8 billion annually.

• While it is possible to understand how Bakken oil and gas producers were less concerned

about their midstream business relationships when crude oil was priced at or above

$100/BBL, at this time, this level of losses constitute an unsustainable burden on the

Bakken E&P industry. Midstream/producer business models that are win/lose are

unsustainable at any WTI price level.

• The bottom line is that undervalued and stranded NGLs should not be subjected to

molecular tourism and transported by pipeline to distant markets solely for generating

tolling fees.

Badlands NGLS, LLC10

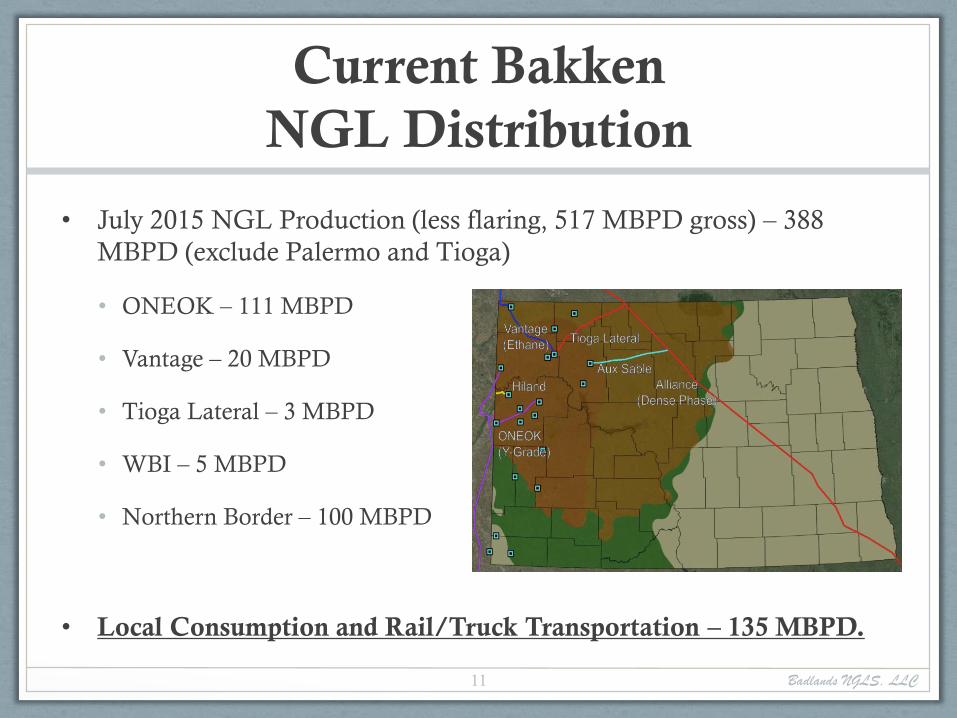

Current Bakken

NGL Distribution

• July 2015 NGL Production (less flaring, 517 MBPD gross) – 388

MBPD (exclude Palermo and Tioga)

• ONEOK – 111 MBPD

• Vantage – 20 MBPD

• Tioga Lateral – 3 MBPD

• WBI – 5 MBPD

• Northern Border – 100 MBPD

• Local Consumption and Rail/Truck Transportation – 135 MBPD.

Badlands NGLS, LLC11

Non-Pipeline NGL

Take Away

• Rail/Truck Transportation in excess of 100 MBPD.

• Based upon Williston Basin gas processing plant

capabilities, the 100 MBPD probably contains not

less than 25 MBPD, or 25% ethane.

• Ethane content of 25% is problematic for either rail

or truck transport.

Badlands NGLS, LLC12

By 2020 Physically Stranded

Bakken NGLs – Northern Border

• NB is the sole WB natural gas pipeline outlet.

• The pipeline's Ventura gas marketing limits heat

content of the gas stream to 1067 Btu/cu.ft.

• By 2020, assuming no change in NB Canadian ethane

content, WB ethane could result in NB exceeding

Ventura gas BTU limits.

Badlands NGLS, LLC13

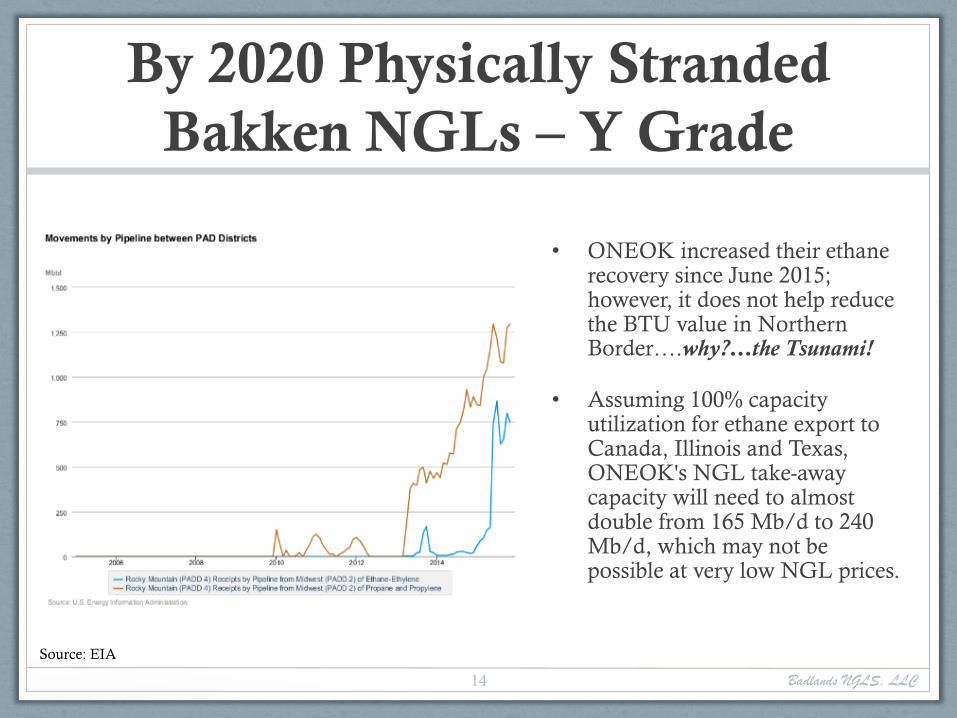

By 2020 Physically Stranded

Bakken NGLs – Y Grade

• ONEOK increased their ethane recovery since June 2015; however, it does not help reduce the BTU value in Northern Border….why?…the Tsunami!

• Assuming 100% capacity utilization for ethane export to Canada, Illinois and Texas, ONEOK's NGL take-away capacity will need to almost double from 165 Mb/d to 240 Mb/d, which may not be possible at very low NGL prices.

Badlands NGLS, LLC14

Source: EIA

Midstream Dilemma

• Midstream MLPs need to distribute the majority of their cash flows to investors instead of retaining a significant amount of their earnings for reinvestment.

• To build/expand pipelines to increase the capacity, pipeline operators and midstream operators need to either

• Issue bonds

• Sell stocks

• At current oil prices,

• Financing is extremely difficult, if not impossible, for MLPs

• It is difficult for MLPs to generate appropriate distributions

Badlands NGLS, LLC15

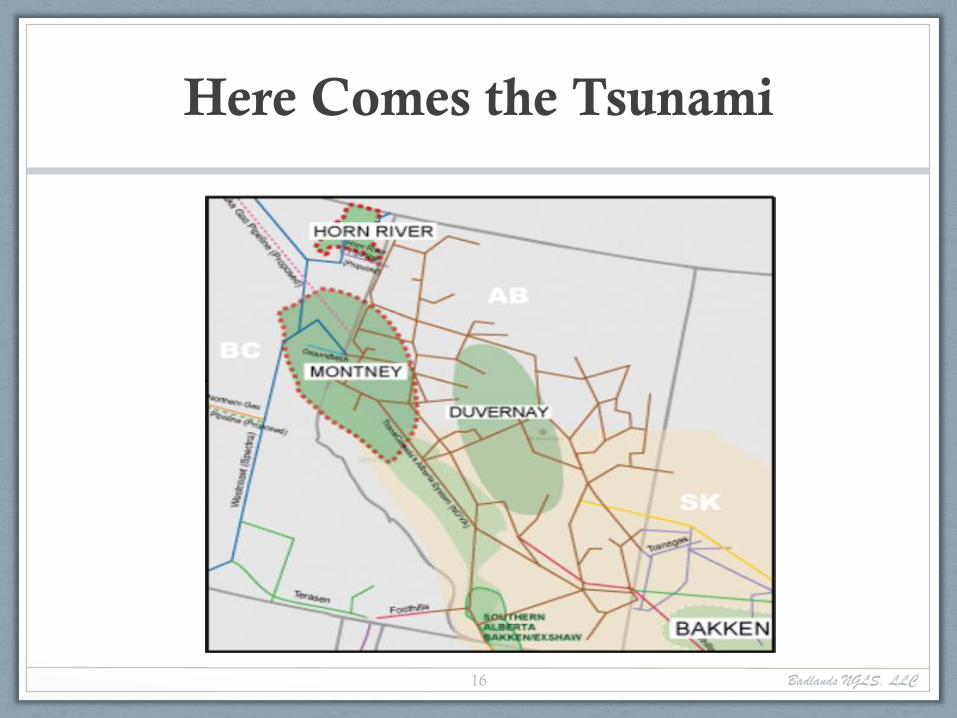

Here Comes the Tsunami

Badlands NGLS, LLC16

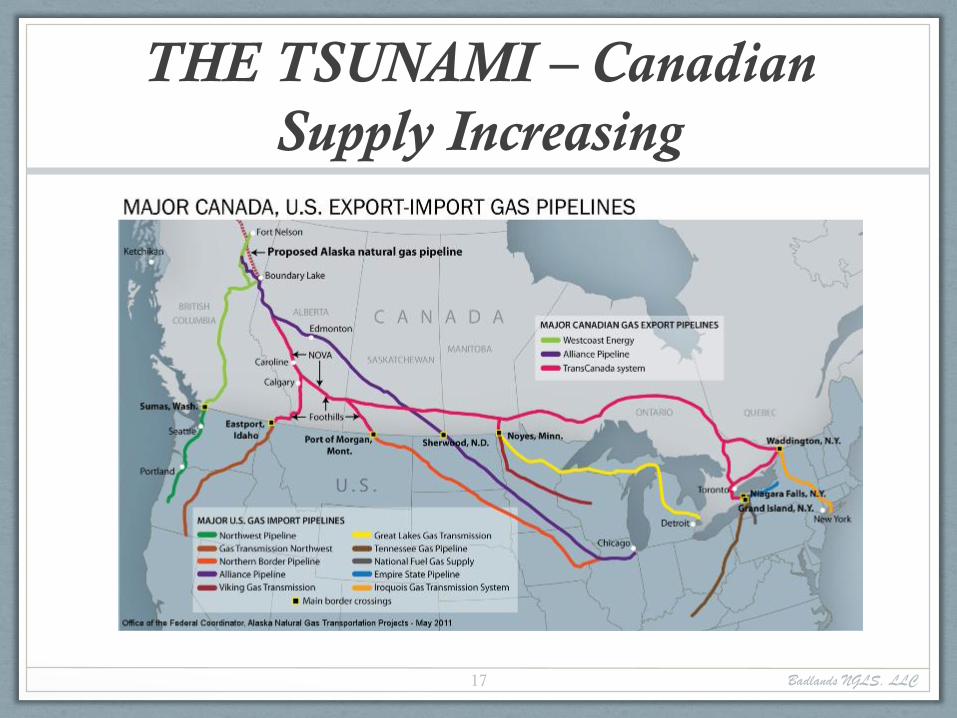

THE TSUNAMI – Canadian

Supply Increasing

Badlands NGLS, LLC17

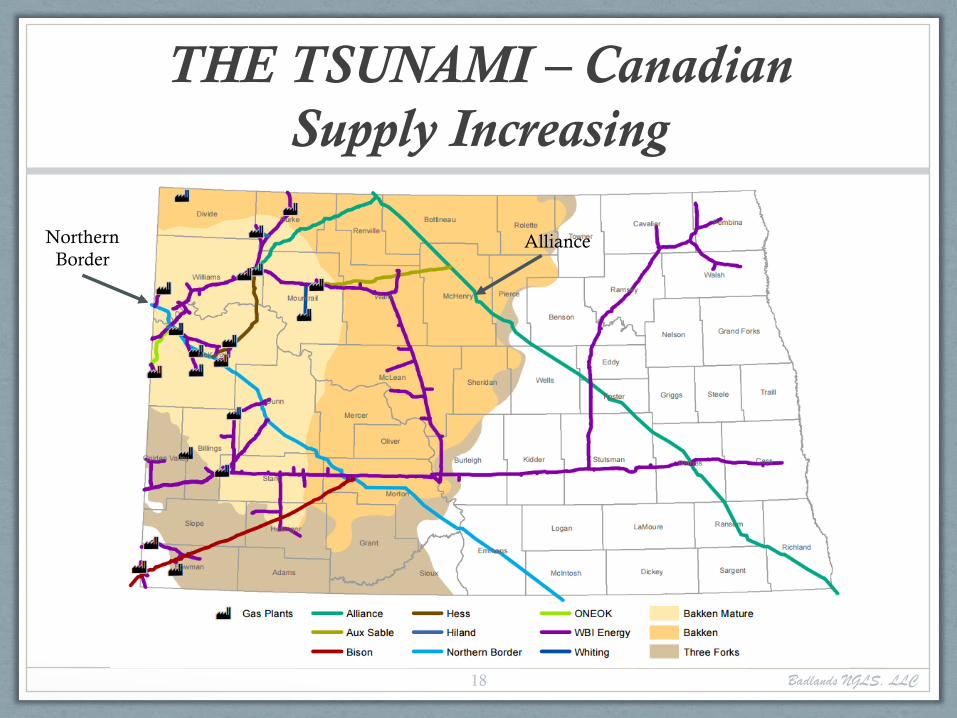

THE TSUNAMI – Canadian

Supply Increasing

Badlands NGLS, LLC18

Northern

BorderAlliance

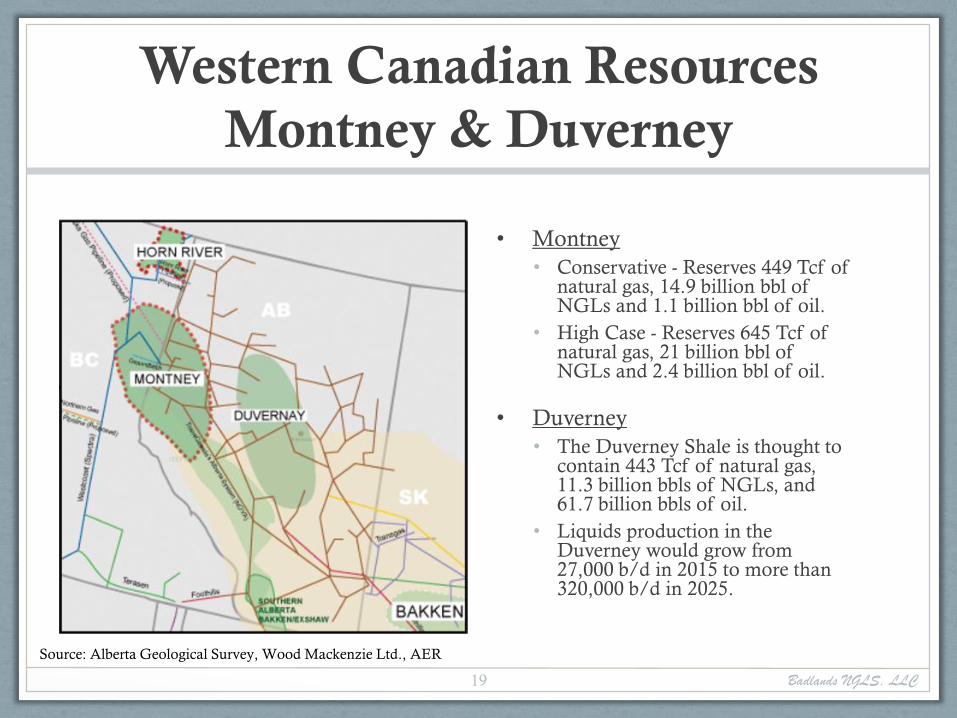

Western Canadian Resources

Montney & Duverney

• Montney

• Conservative - Reserves 449 Tcf of natural gas, 14.9 billion bbl of NGLs and 1.1 billion bbl of oil.

• High Case - Reserves 645 Tcf of natural gas, 21 billion bbl of NGLs and 2.4 billion bbl of oil.

• Duverney

• The Duverney Shale is thought to contain 443 Tcf of natural gas, 11.3 billion bbls of NGLs, and 61.7 billion bbls of oil.

• Liquids production in the Duverney would grow from 27,000 b/d in 2015 to more than 320,000 b/d in 2025.

Badlands NGLS, LLC19

Source: Alberta Geological Survey, Wood Mackenzie Ltd., AER

Montney & Duverney

Badlands NGLS, LLC20

• The Montney formation contains significant amounts

of NGL liquids and the Duverney formation contains

high concentrations of condensate and NGL liquids.

• The Duverney produces significant amounts of

condensate. Condensate is priced at a premium to the

WTI oil price. The price realized for NGLs is

secondary to the pricing received from the condensate

sales.

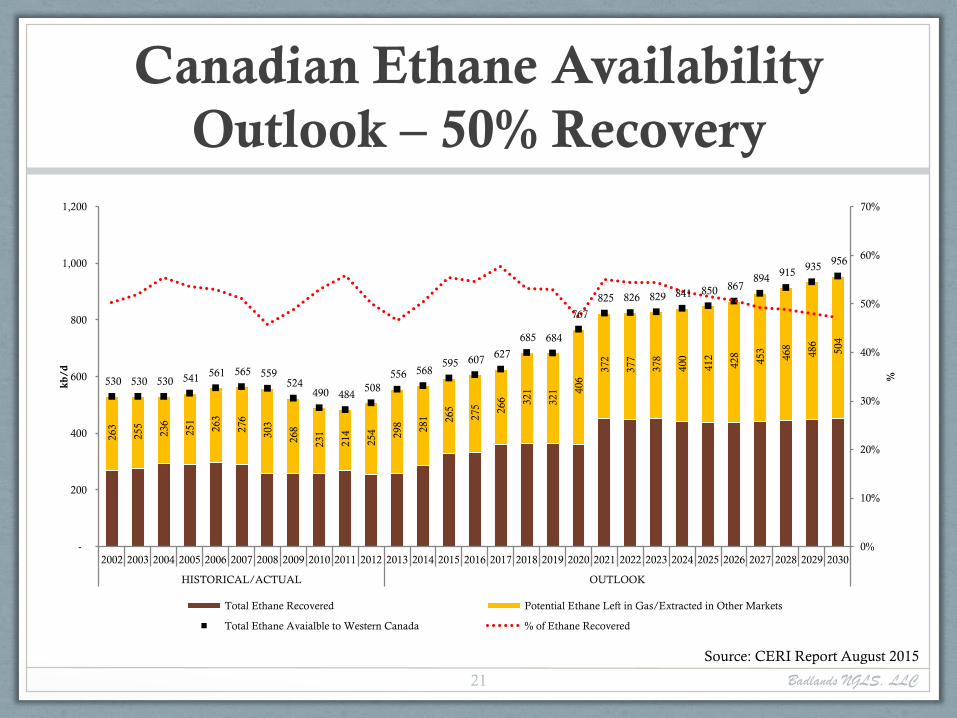

Canadian Ethane Availability

Outlook – 50% Recovery

Badlands NGLS, LLC21

Source: CERI Report August 2015

263

255

236

251

263

276

303

268

231

214

254

298

281

265

275

266

321

321 406 3

72

377

378

400

412

428

453

468

486

504

530 530 530 541 561 565 559

524 490 484

508

556 568 595 607

627

685 684

767

825 826 829 841 850 867 894

915 935

956

0%

10%

20%

30%

40%

50%

60%

70%

-

200

400

600

800

1,000

1,200

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

HISTORICAL/ACTUAL OUTLOOK

%

kb

/d

Total Ethane Recovered Potential Ethane Left in Gas/Extracted in Other Markets

Total Ethane Avaialble to Western Canada % of Ethane Recovered

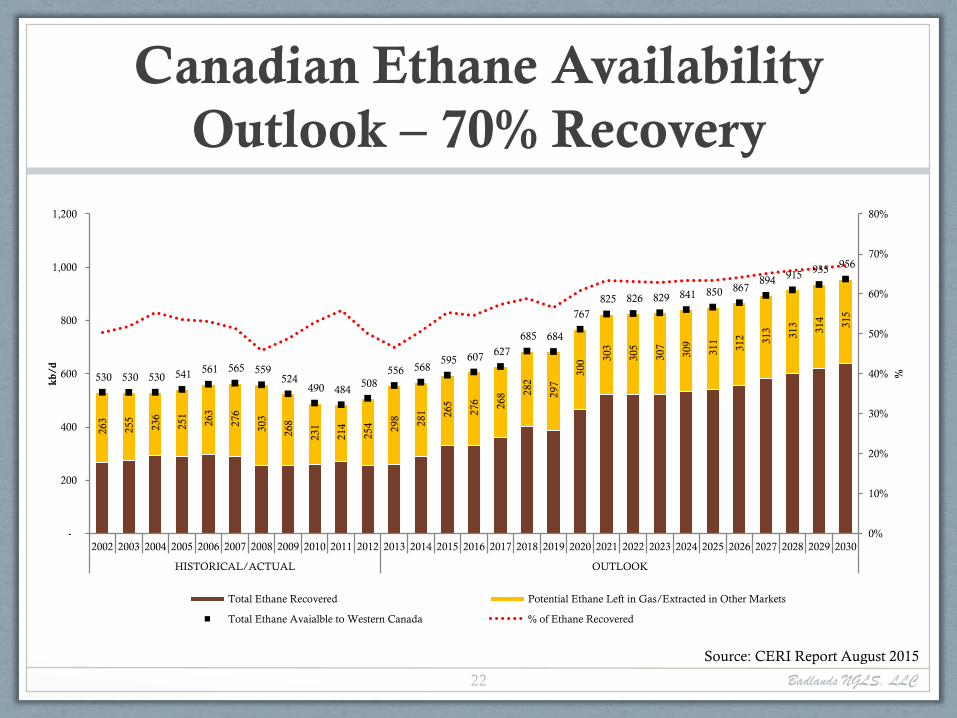

Canadian Ethane Availability

Outlook – 70% Recovery

Badlands NGLS, LLC22

Source: CERI Report August 2015

263

255

236

251

263

276

303

268

231

214

254

298

281

265

276

268 282

297

300 303

305

307

309

311

312

313

313

314

315

530 530 530 541 561 565 559

524 490 484

508

556 568 595 607

627

685 684

767

825 826 829 841 850 867 894

915 935

956

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

200

400

600

800

1,000

1,200

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

HISTORICAL/ACTUAL OUTLOOK

%

kb

/d

Total Ethane Recovered Potential Ethane Left in Gas/Extracted in Other Markets

Total Ethane Avaialble to Western Canada % of Ethane Recovered

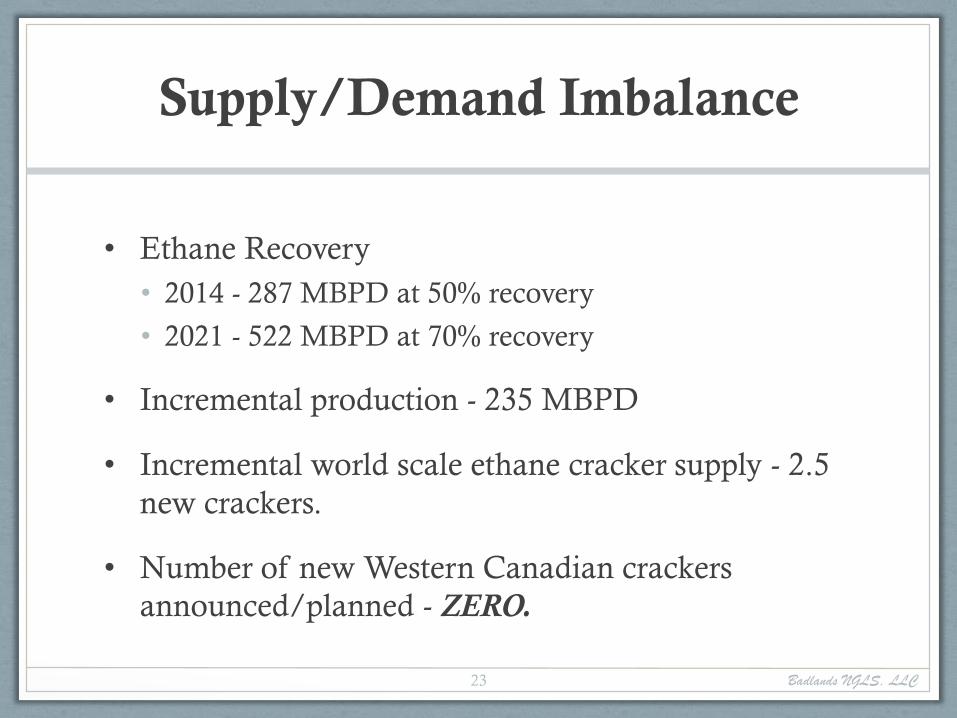

Supply/Demand Imbalance

• Ethane Recovery

• 2014 - 287 MBPD at 50% recovery

• 2021 - 522 MBPD at 70% recovery

• Incremental production - 235 MBPD

• Incremental world scale ethane cracker supply - 2.5

new crackers.

• Number of new Western Canadian crackers

announced/planned - ZERO.

Badlands NGLS, LLC23

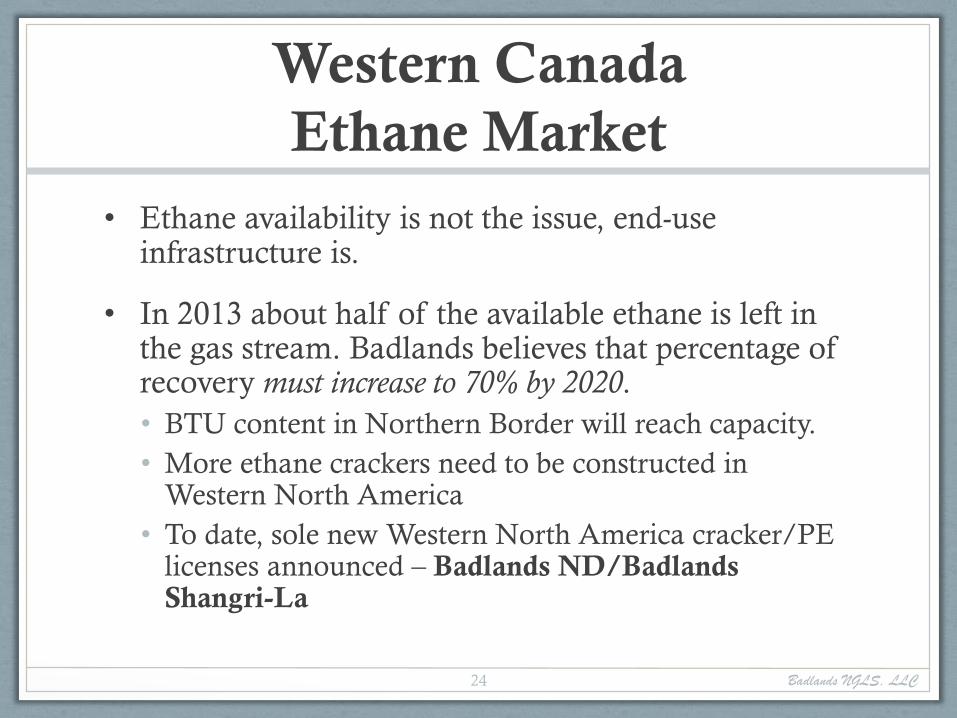

Western Canada

Ethane Market

• Ethane availability is not the issue, end-use infrastructure is.

• In 2013 about half of the available ethane is left in the gas stream. Badlands believes that percentage of recovery must increase to 70% by 2020.

• BTU content in Northern Border will reach capacity.

• More ethane crackers need to be constructed in Western North America

• To date, sole new Western North America cracker/PE licenses announced – Badlands ND/Badlands Shangri-La

Badlands NGLS, LLC24

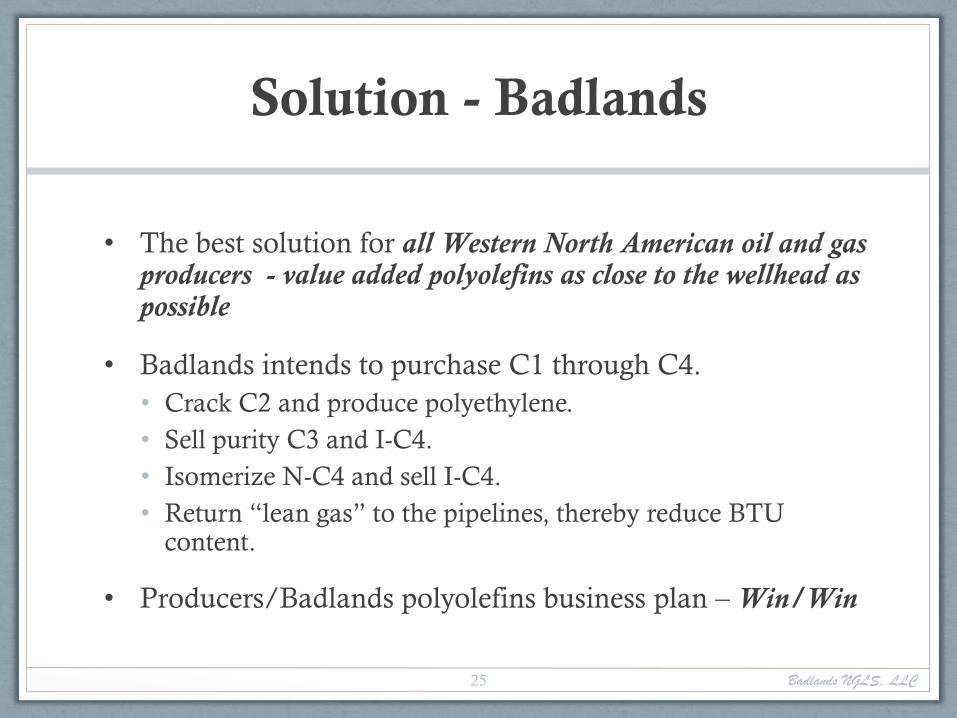

Solution - Badlands

• The best solution for all Western North American oil and gas producers - value added polyolefins as close to the wellhead as possible

• Badlands intends to purchase C1 through C4.

• Crack C2 and produce polyethylene.

• Sell purity C3 and I-C4.

• Isomerize N-C4 and sell I-C4.

• Return “lean gas” to the pipelines, thereby reduce BTU content.

• Producers/Badlands polyolefins business plan – Win/Win

Badlands NGLS, LLC25

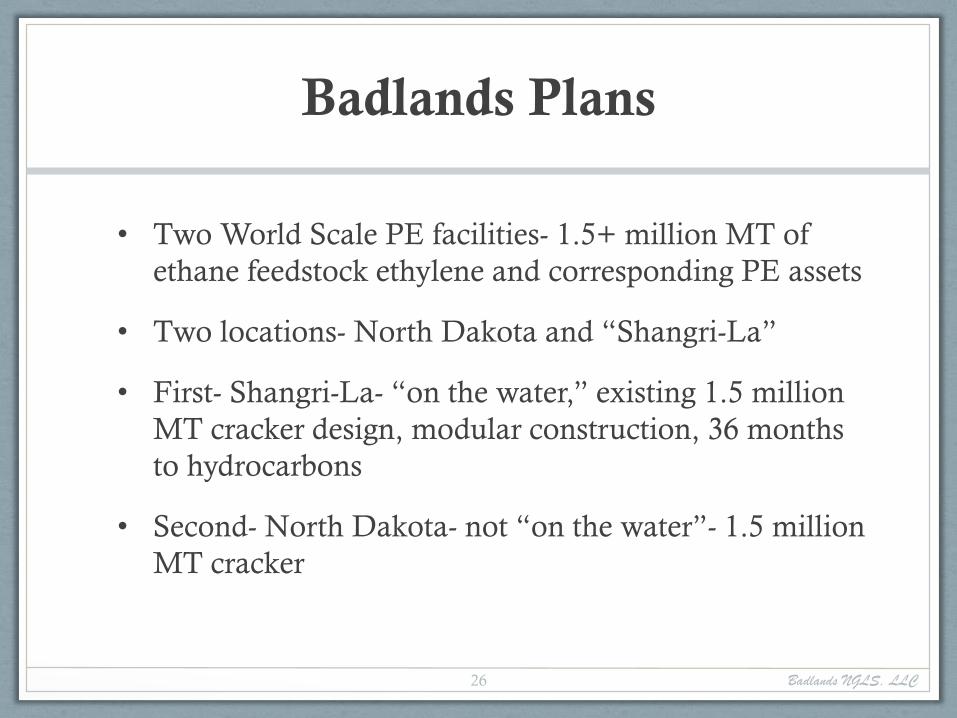

Badlands Plans

• Two World Scale PE facilities- 1.5+ million MT of

ethane feedstock ethylene and corresponding PE assets

• Two locations- North Dakota and “Shangri-La”

• First- Shangri-La- “on the water,” existing 1.5 million

MT cracker design, modular construction, 36 months

to hydrocarbons

• Second- North Dakota- not “on the water”- 1.5 million

MT cracker

Badlands NGLS, LLC26

Badlands Plans - Technology

• Cracker technology - Technip – currently market leader and

building three plants in the U.S. for Sasol, CP Chem and Dow.

• PE technology - Univation – market leader in PE products

owned by Dow.

• Captive Co-Monomer Manufacture – “Name Brand”

• Product Off-Take - “Name Brand”

Badlands NGLS, LLC27

Badlands Plans - Agreements

• Feedstock Agreement(s) in advanced discussion in both

locations

• EPC - Agreement in principal, lump sum turn key

• Financing - advanced stage

• Site Selection - Advanced stage, Shangri-La site close to

selection, North Dakota close to selection

Badlands NGLS, LLC28

Shangri-La Facility Cracker

• Technip cracker- 1.53 million MT…same design being built for

SASOL and Chevron Phillips

• 94 Modules fabricated in Mexico- delivered “on the water” to

Gulf Coast

• SASOL most advanced- Firm module delivered price and =/-

10% cracker installed cost

• Shangri-La Transportation Study confirms “on the water”

delivery of 94 modules….2000 construction headcount versus

9000 stick built headcount….time and money savings

Badlands NGLS, LLC29

Shangri-La Facility PE and

Related Assets

• Two Univation 600 KT gas phase PE reactors- up to 24

different PE products (HDPE, bimodal HDPE, butene

LLDPE, hexene LLDPE, metallocene LLDPE)

• According to Univation (formerly Union Carbide) Badlands will

produce the most diverse product line of any Univation licensee

• Co-monomer facility will reduce PE production costs by

$0.11/lb.

Badlands NGLS, LLC30

North Dakota PE And Related

Assets

• Identical Univation reactors and capacity- Duplicate

Shangri-La facility but assign different catalyst families to

each reactor

• “Name Brand” co-monomers for Univation products

• Own electrical generation assets

• Over 500 permanent and high paying North Dakota jobs

Badlands NGLS, LLC31

Sponsor Questions

• Does ND polyolefin plant improve or eliminate the

Western Canadian/ND gas heat content?

• How long will it take to build and how much will it cost?

• Engineering/Technology issues

• Site Selection

• Infrastructure

• End markets

Badlands NGLS, LLC32