22

BALANCE SHEET April Vivienne M. Ancheta

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| Upload: | jaysonfredmarin |

| View: | 15 times |

| Download: | 0 times |

BALANCE SHEET

April Vivienne M. Ancheta

shows the financial condition of the business in a point in timecan be completed at any time

Elements

Balance Sheet

Liability

Equity

Asset

how much assets the company has to protect shareholdershow efficiently management is using capitalhow fast a business can growthe risk of bankruptcy

Purpose

are resources owned by a company and which future economic benefits are expected to flow in the company and can be measured reliably

Classification:Current Assets – realizable within one year from the balance sheet dateNon Current Assets – realizable beyond one year from the balance sheet date

Assets

are present obligations of the enterprise arising from past events, the settlement of which is expected to result in an outflow from the enterprise’s resources embodying economic benefits.

Classification:Current Liabilities – expected to be liquidated within one year from the

balance sheet dateNon Current Liabilities – expected to be liquidated more than one year

from the balance sheet date

Liabilities

the amount invested by the owners in the company. This also includes the result of operations.

Equity

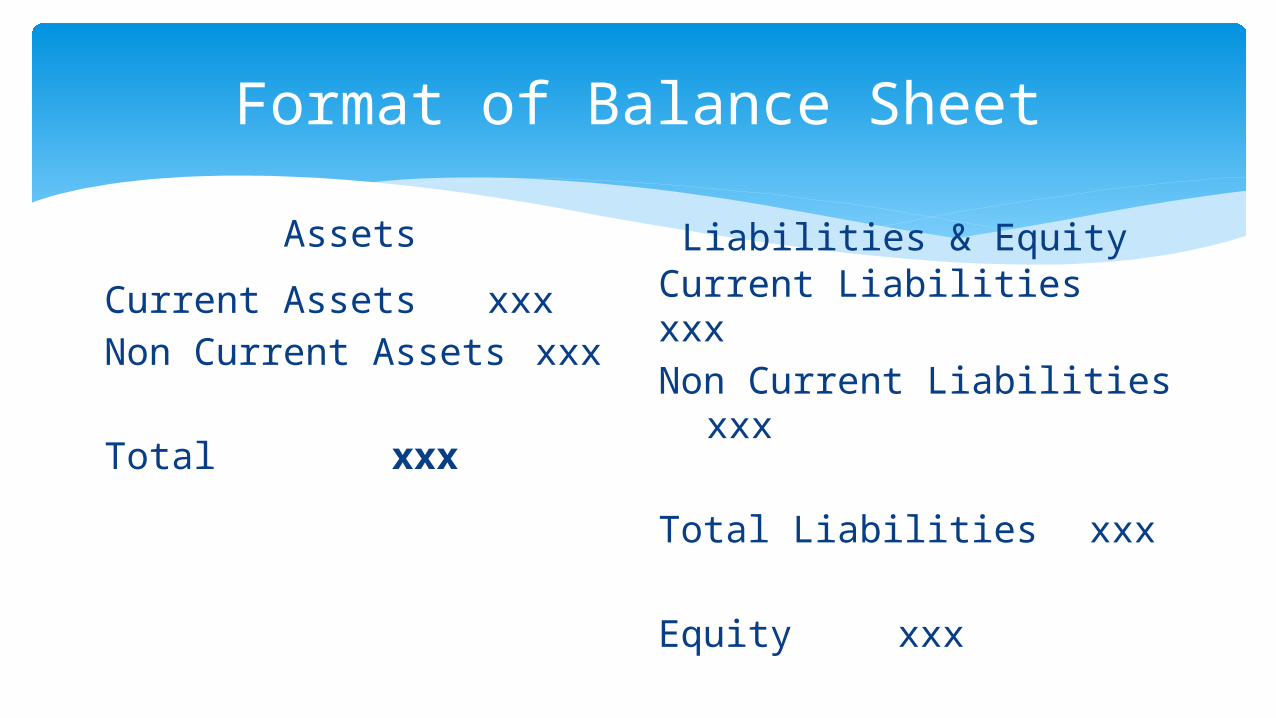

Format of Balance Sheet

Assets

Current Assets xxxNon Current Assets xxx

Total xxx

Liabilities & Equity Current Liabilities xxxNon Current Liabilities xxx

Total Liabilities xxx

Equity xxx

Total Liabilities & Equity xxx

AssetsCurrent Assets xxxNon Current Assets xxx

Total Assets xxx

Liabilities & Equity

Current Liability xxxNon Current Liability xxx

Equity xxx

Total Liabilities & Equity xxx

Format of Balance Sheet

Liquidity Ratio – measures the ability of the firm to pay its obligations as they become due

Formulas: Current Ratio = Current Assets/Current Liabilities Quick Ratio = (Current Assets-Inventory)/Current

Liabilities Operating CF Ratio = CF from Operations/Current

Liabilities

Test of Financial Strength and Liquidity

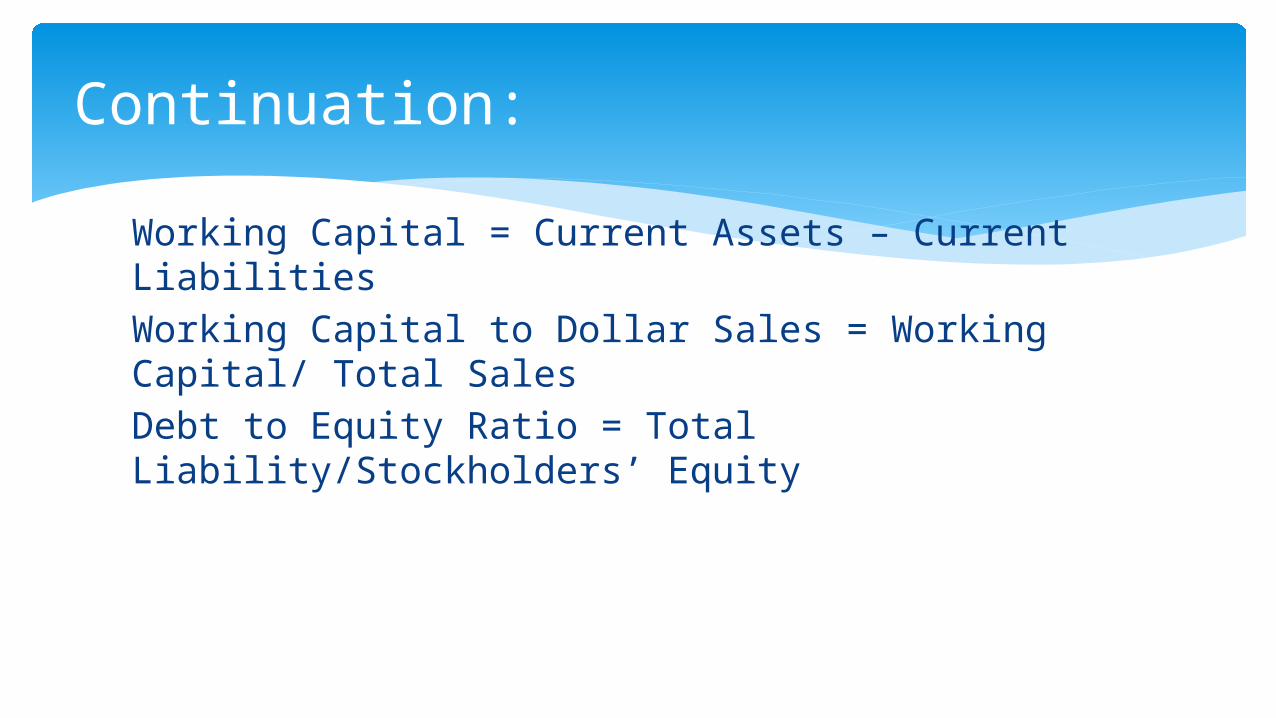

Working Capital = Current Assets – Current LiabilitiesWorking Capital to Dollar Sales = Working Capital/ Total SalesDebt to Equity Ratio = Total Liability/Stockholders’ Equity

Continuation:

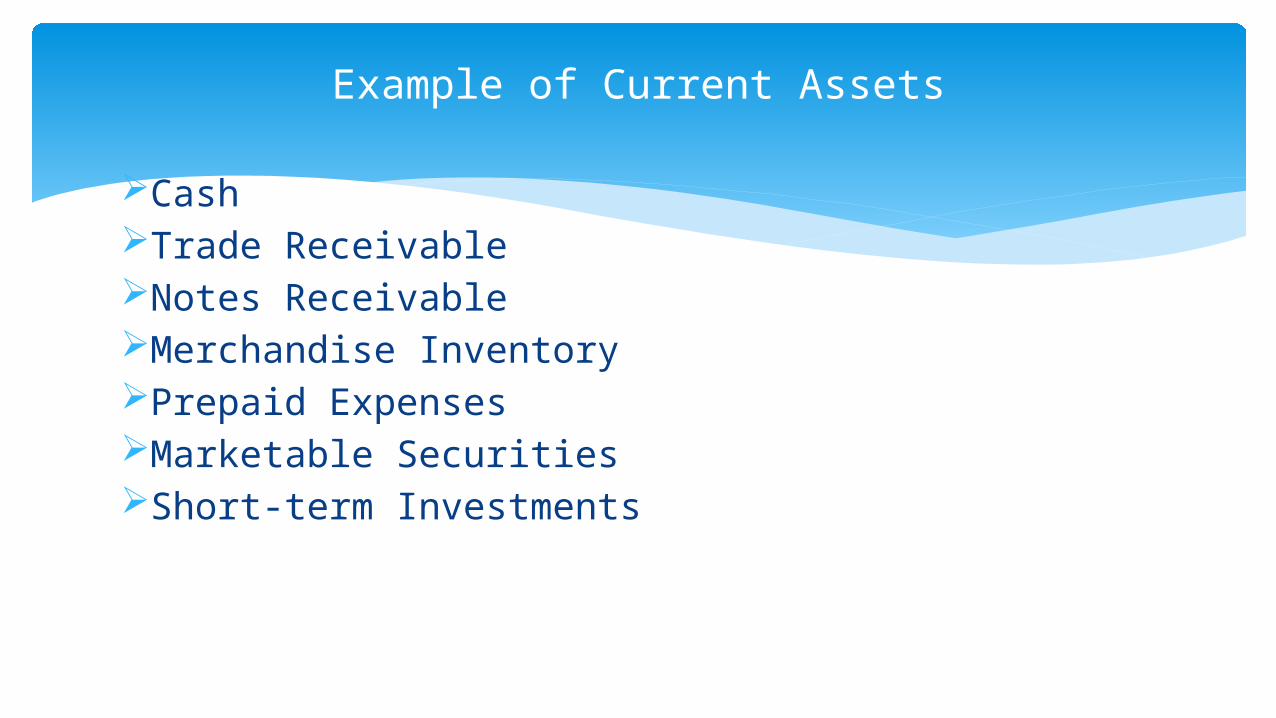

CashTrade ReceivableNotes ReceivableMerchandise InventoryPrepaid ExpensesMarketable SecuritiesShort-term Investments

Example of Current Assets

ComputerFurniture & FixturesBuildingEquipmentHeld to Maturity SecuritiesInvestment in Subsidiaries/Affiliates

Non-Current Assets

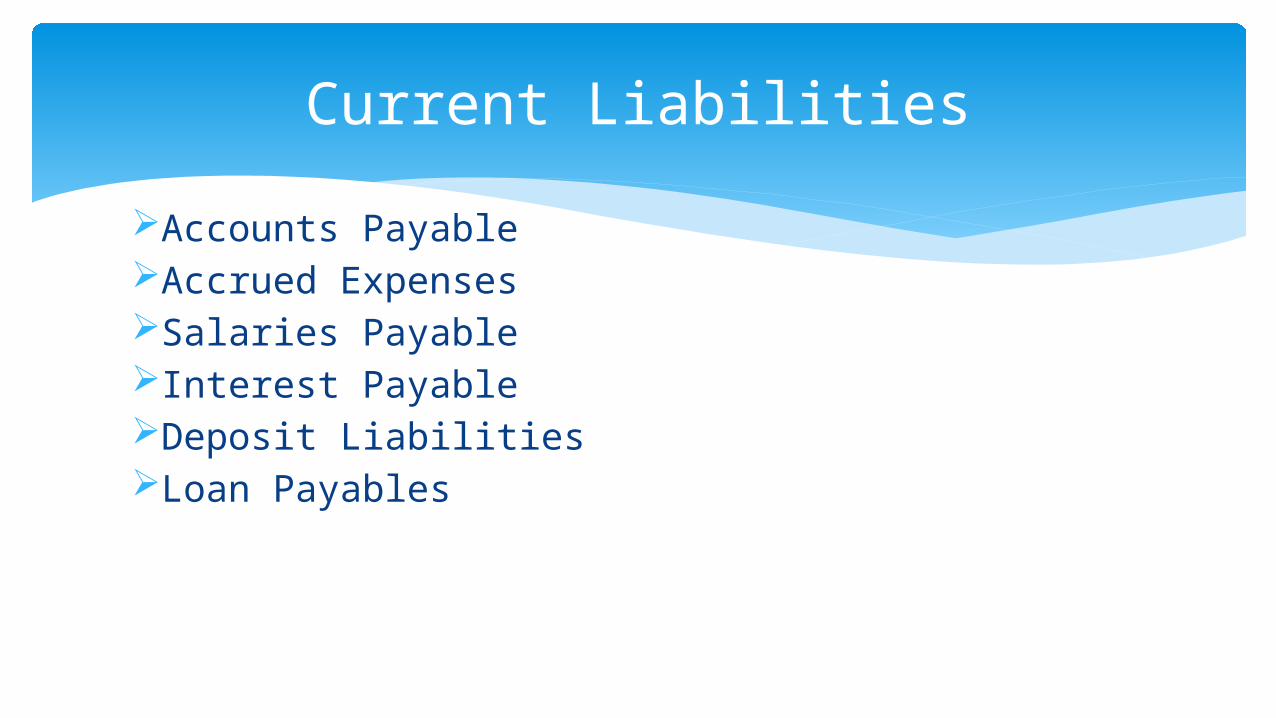

Accounts PayableAccrued ExpensesSalaries PayableInterest Payable Deposit LiabilitiesLoan Payables

Current Liabilities

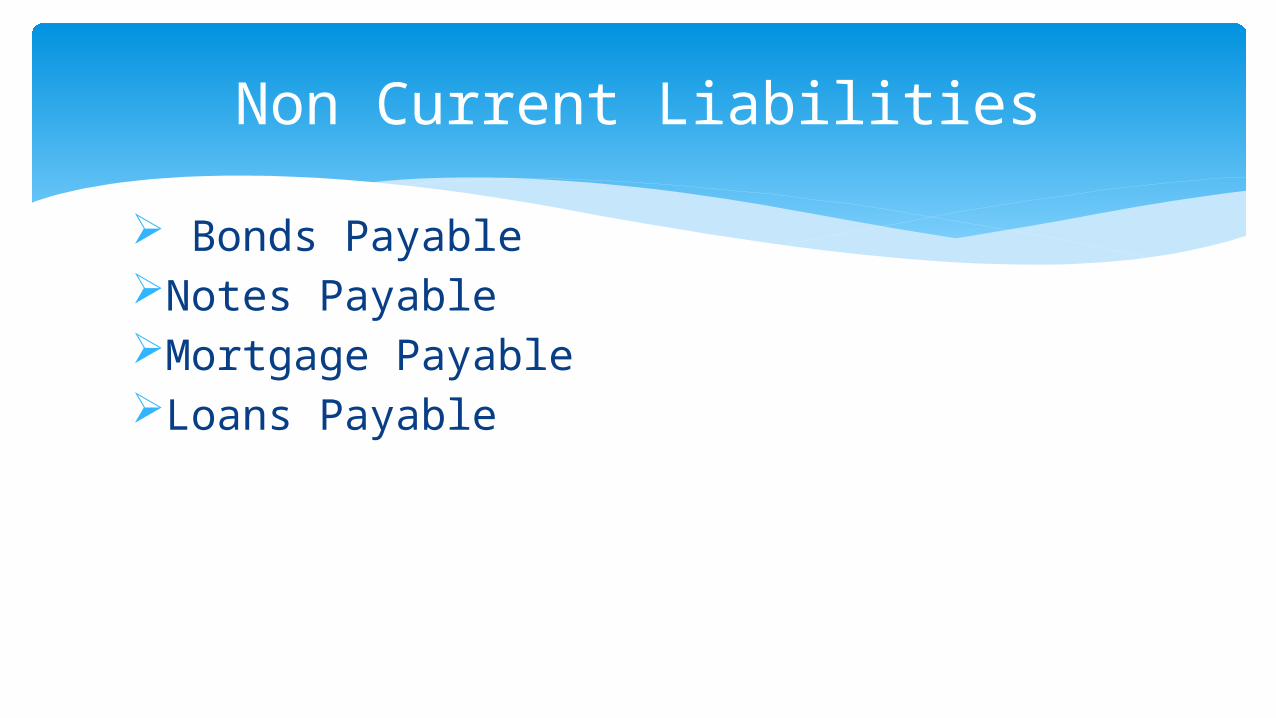

Bonds PayableNotes PayableMortgage PayableLoans Payable

Non Current Liabilities

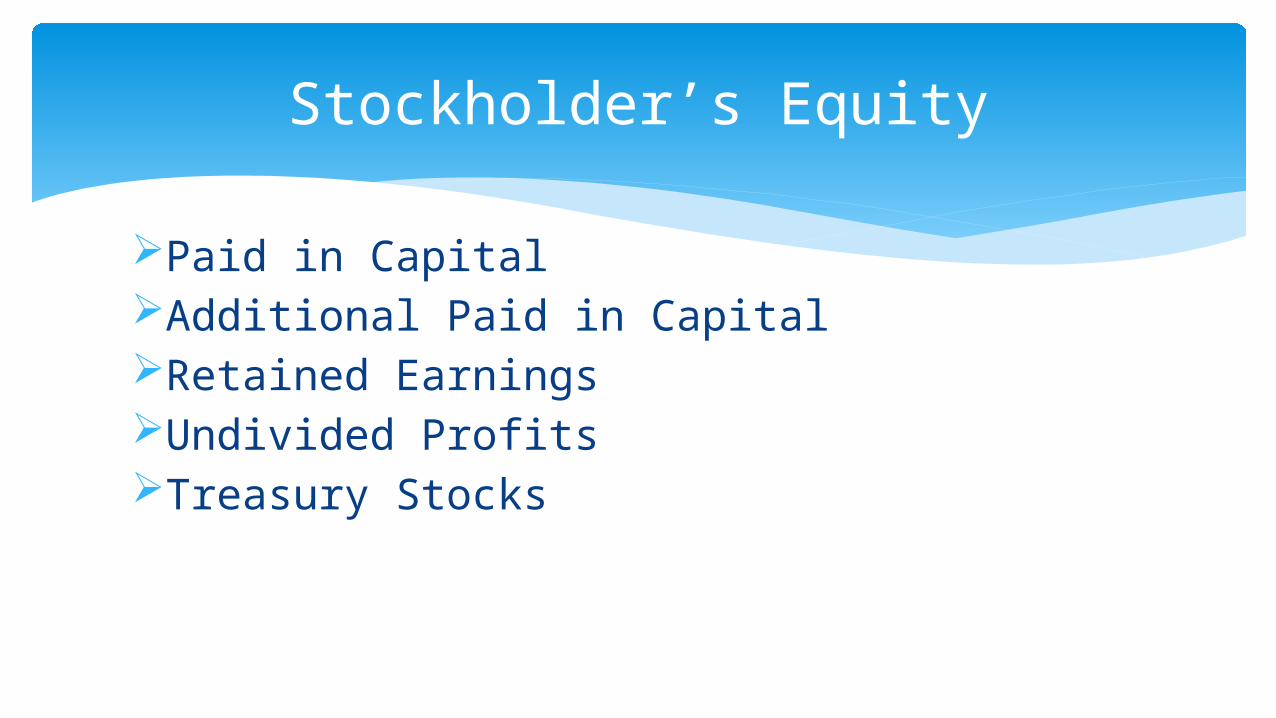

Paid in CapitalAdditional Paid in CapitalRetained EarningsUndivided ProfitsTreasury Stocks

Stockholder’s Equity

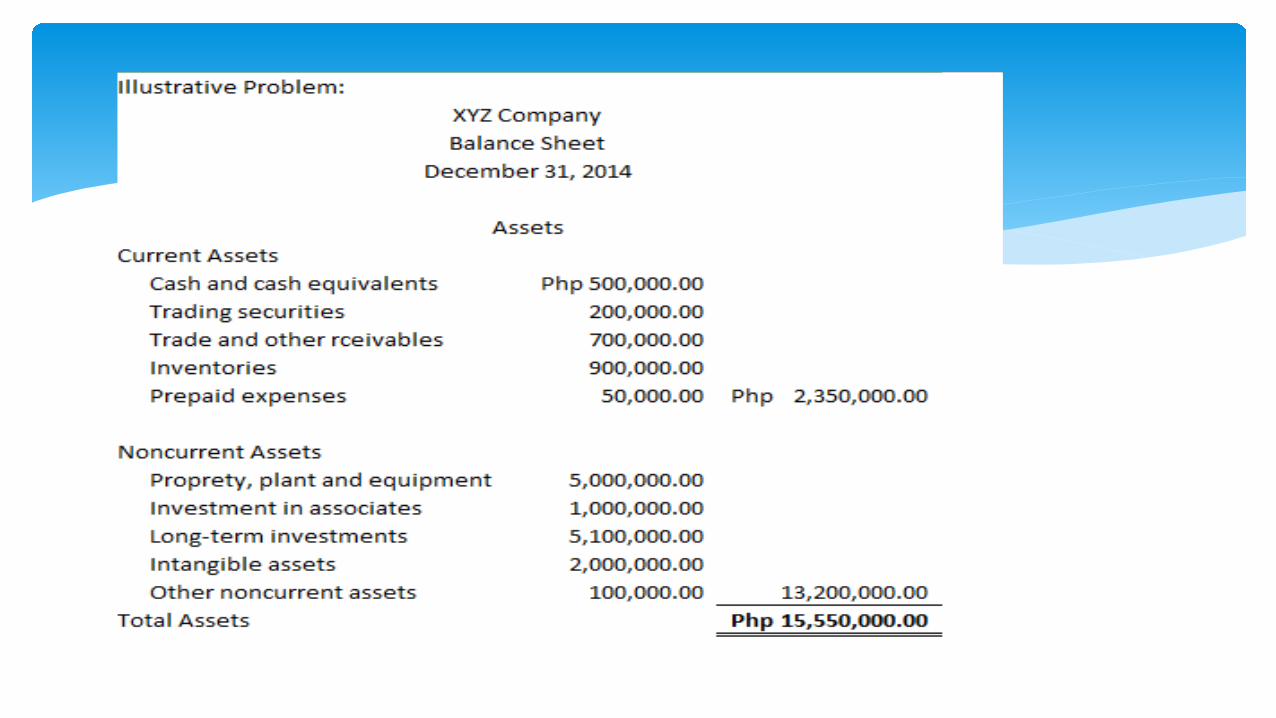

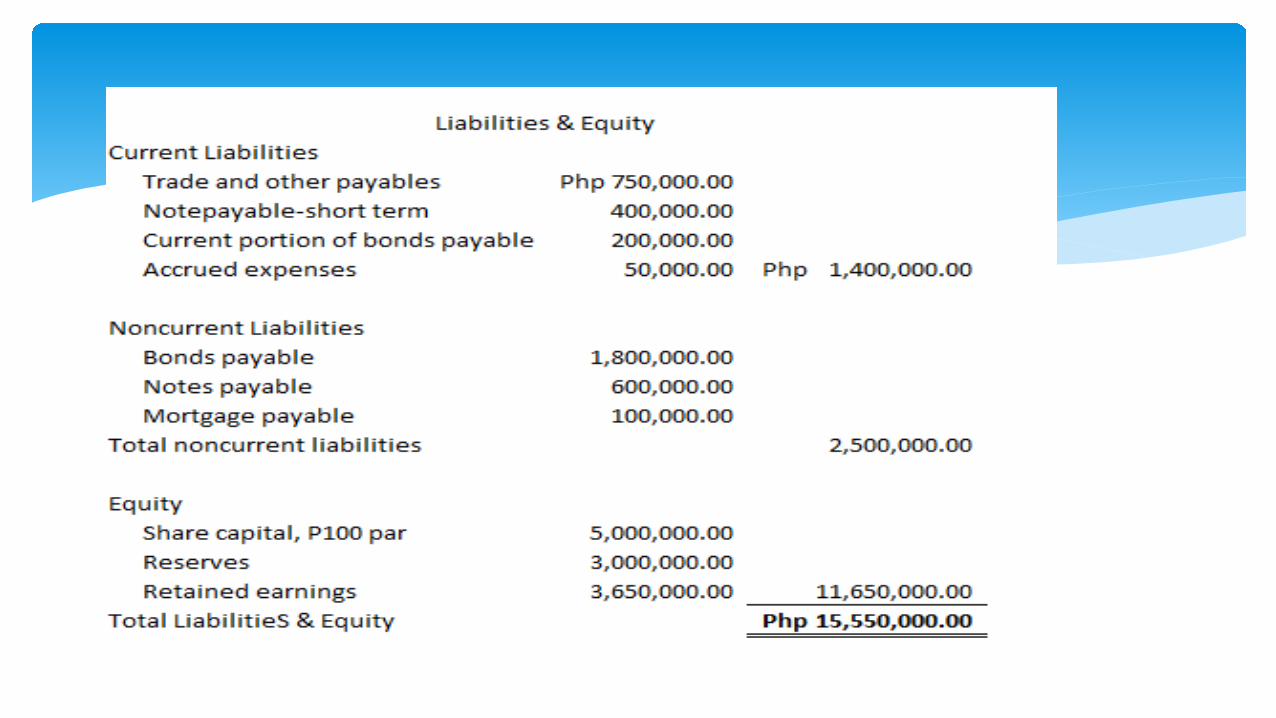

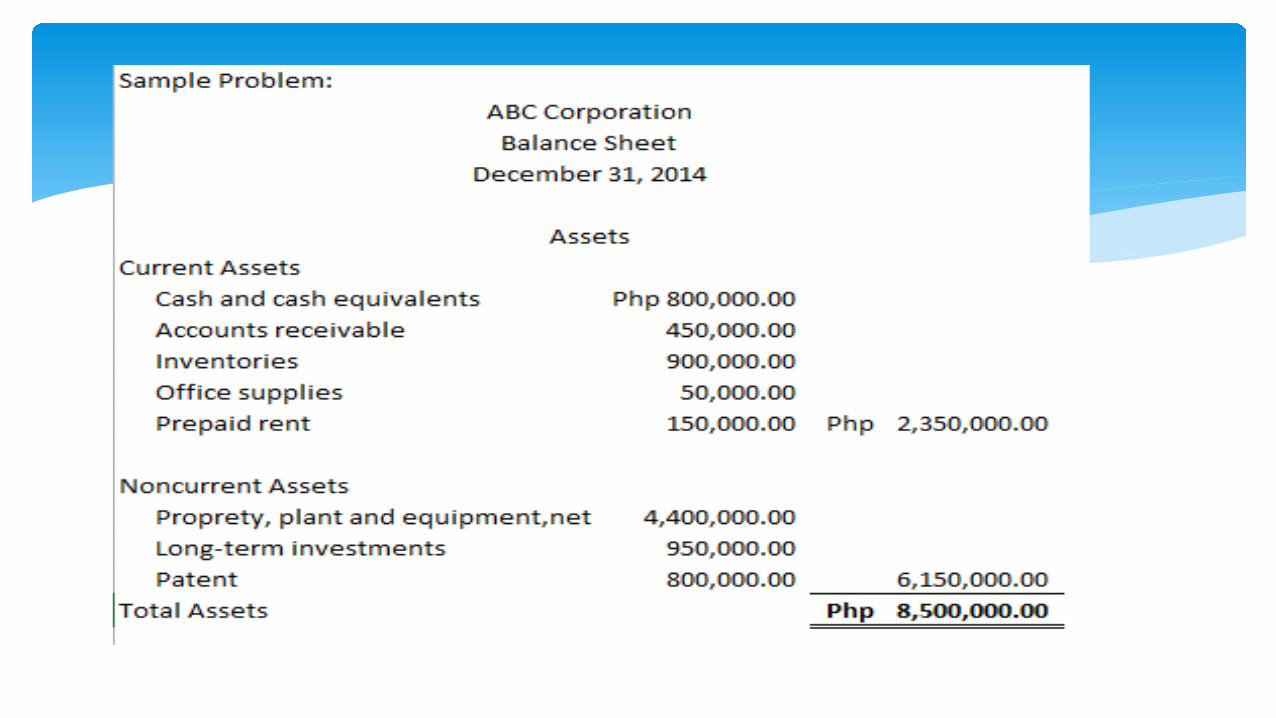

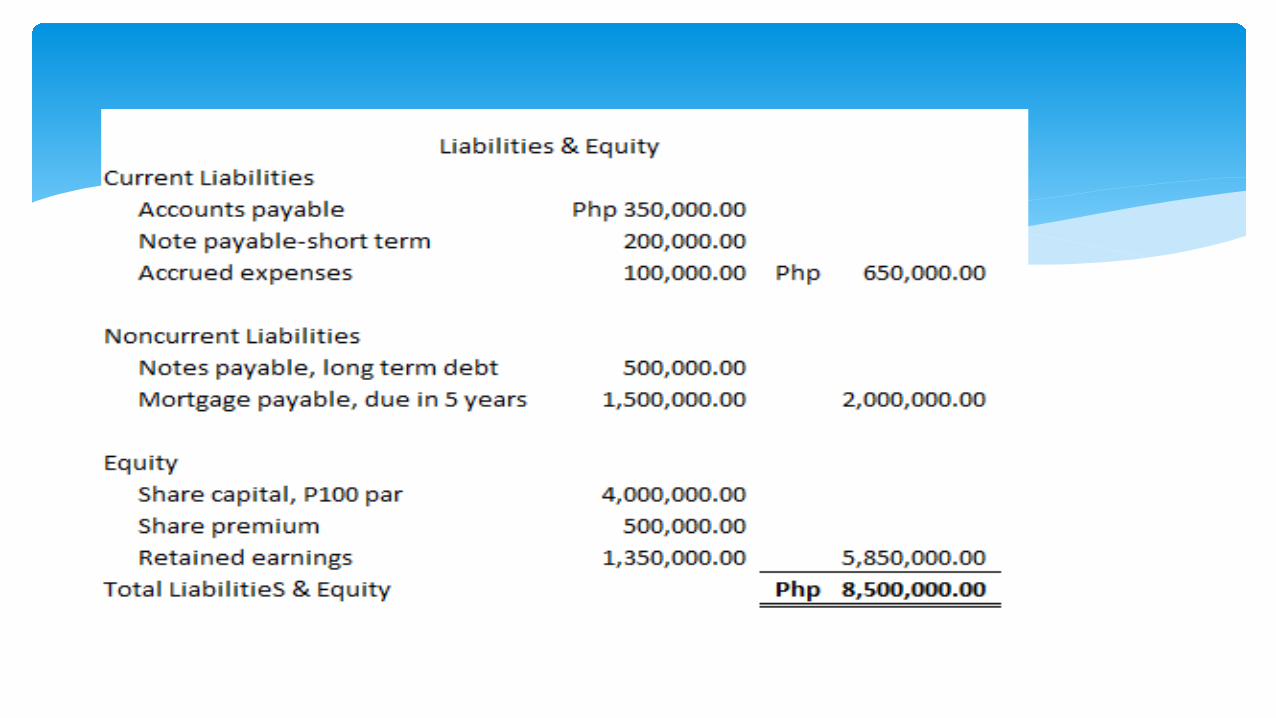

Sample Problem:

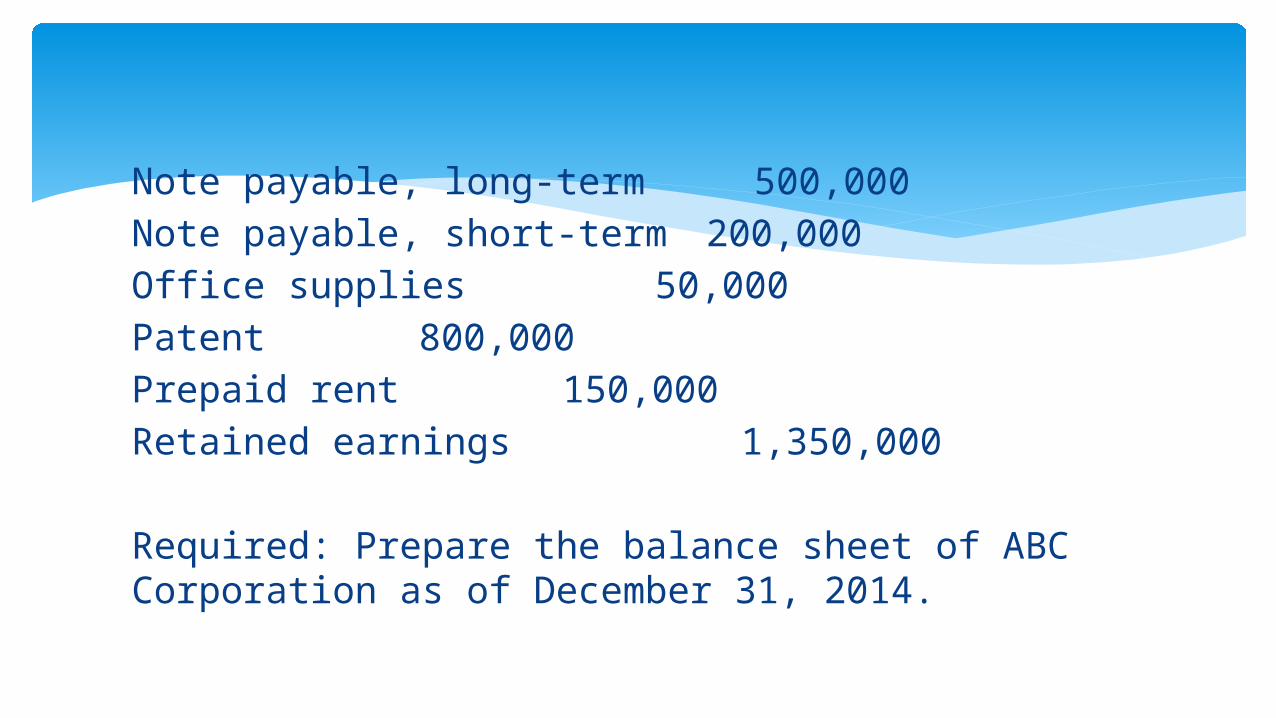

Accounts payable 350,000Accounts Receivable 450,000Property, plant and equipment 5,600,000Accumulated depreciation 1,200,000Mortgage payable, due in 5 years 1,500,000Share capital, P100 par 4,000,000Share premium 500,000Cash and cash equivalent 800,000Accrued expenses 100,000Inventories 900,000Long term investments 950,000

Note payable, long-term 500,000Note payable, short-term 200,000Office supplies 50,000Patent 800,000Prepaid rent 150,000Retained earnings 1,350,000

Required: Prepare the balance sheet of ABC Corporation as of December 31, 2014.

Thank You!