21

Balancing Global Olefins Capacity and Demand Asian Petrochemical Market Conference Shanghai, China 19 th Apr 2017 Rajesh Rawat 1

Balancing Global Olefins Capacity and Demand

Asian Petrochemical Market Conference Shanghai, China

19th Apr 2017

Rajesh Rawat

1

Contents

2

Reliance at a Glance

Olefins – Changing Dynamics

New Capacities and Demand drivers

Regional Olefins Trade

Reliance at a Glance

3

India’s largest private company.

Global player in integrated energy value chain.

Growing presence in retail & digital services.

US$ 44.7 Billion Annual Revenue

US$ 4.2 Billion Net Profit (FY 15-16)

151 Major products & brands

Jio : fastest growing 4G network in India

2nd

Global Rankings

Polyester

PTA

PX

PP

MEG

4th

6th

6th

8th

Major Projects under implementation in Reliance

4

Ethane Feed Flexibility in Crackers

6 Nos VLEC (Very Large Ethane Carriers).

Cryogenic Storage & handling facility in India.

Provide feed security to Crackers with Minor increase in Ethylene capacity.

Cross Country pipeline (480 km) to transport Ethane across Reliance’s sites.

Refinery Offgas Cracker with PE & MEG

1.5 Million MT/yr Cracker using Refinery Offgas as feed integrates Refinery with Petrochemical Complex

Downstream LLDPE, LDPE & MEG Capacities

Coke Gasification in Refinery

Additional 2.2 Million MTA PX capacity

5

Olefins – Changing Dynamics

Raw Material Prices

6

US, post Shale, is now largest producer of oil (>12 mbbl/d) & has kept Nat Gas and Ethane prices low in US.

Fall in Crude prices has direct implication for Petchem Feedstocks

Low price stimulates demand apart from making production competitive.

0

20

40

60

80

100

120

0

200

400

600

800

1000

1200

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

$/bbl$/MT Naphtha SG US Propane Crude Brent

US – Nat Gas ($/mmbtu)

Source: Platts

Changes in US Olefins Business

7

Ethylene Margin in US Crackers is going down

New Ethane Crackers are under Construction

0

500

1000

1500

2000

2500

3000

0

200

400

600

800

1000

1200

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Mar

-17

KT/m$/MTPropane exports from US

US Propane Export Saudi CP US Price

Increasing US Propane Exports

New PDH Capacity starting in US

Source: PlattsSource: RIL Working/IHS

0

200

400

600

800

1000

1200

1400

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Mar

-17

$/MTEthylene Cash Cost in US

NA Margin (Wt Avg) Ethane (70%) Propane (15%) Naphtha (5%)

Cracker Feed

8

Source: RIL Working

0

100

200

300

400

500

600

700

800

900

-200

0

200

400

600

800

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Jan-1

6

Jan-1

7

Jan-1

8

Jan-1

9

Jan-2

0

Jan-2

1

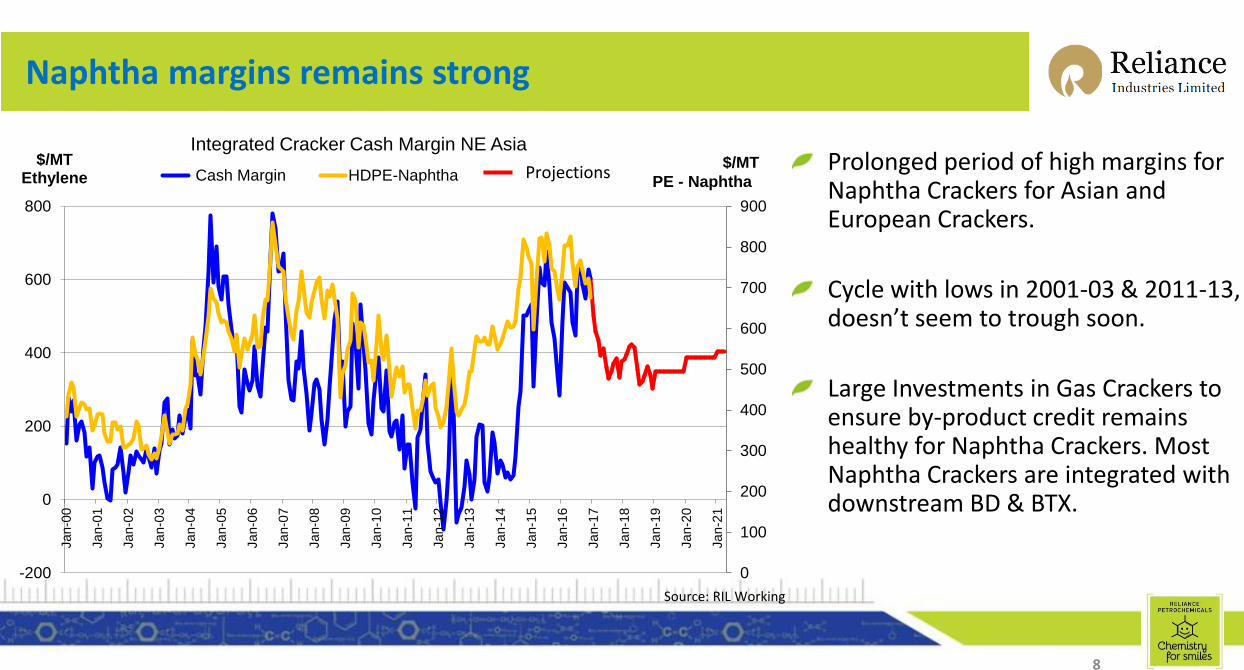

$/MT Ethylene

Integrated Cracker Cash Margin NE Asia

Cash Margin HDPE-Naphtha Projections$/MT

PE - Naphtha

Naphtha margins remains strong

Prolonged period of high margins for Naphtha Crackers for Asian and European Crackers.

Cycle with lows in 2001-03 & 2011-13, doesn’t seem to trough soon.

Large Investments in Gas Crackers to ensure by-product credit remains healthy for Naphtha Crackers. Most Naphtha Crackers are integrated with downstream BD & BTX.

Cracker Feedstock

9

-

5

10

15

20

25

30

35

2011 2016

Mn MT North America

Coal to Olefins Methanol to Propylene

Methanol to Olefins Gas Oil

Naphtha Butane

Propane Ethane

-

5

10

15

20

25

2011 2016

West Europe

-

5

10

15

20

25

30

35

40

45

2011 2016

NE Asia

US Crackers are predominantly Ethane/Propane after plentiful

supply post Shale revolution

Europe, mainly Naphtha, is now importing Ethane from US

NEA relies on Naphtha with some capacity now from MTO/CTO

Ethane40%

Propane9%

Butane5%

Naphtha37%

Gas Oil3%

Methanol to Olefins

2%Methanol

to Propylene

0.06%

Coal to Olefins

3%

Others1%

World: 2021 Ethylene Production by Feedstock

Source: IHS © 2016 IHS

Production = 174.7 Million Metric Tons

36% in

2016

43% in

2016

Cash Cost Curve for Crackers

10

Cost Curve is flattening

0

200

400

600

800

1000

1200

1400

1600

0 20 40 60 80 100 120 140 160

Apr-13 Dec-14 Mar-17JKT & European

Naphtha Crackers

CTO &

MTO

Middle EastGas Crackers

Asian Naphtha Crackers

US Gas Crackers

Cash Cost Curve$/MT

Million MT

1000

500

@ 100 $/bblCrude

@ 50 $/bblCrude

11

New Capacities & Demand Drivers

US Capacity additions

12

6 Million MT of Low Cost (Ethane) capacity in US by 2018

Ethylene Downstream capacity by 2018 is 4.5 Mn MT and

would result in lower Op rate of Crackers in US.

No new Crackers envisaged in Mid East.

Company LocationEthylene

Cap KTA

Start-up

Estimates

Oxy/Mexichem JV Ingleside, TX 550 Started

Dow Freeport, TX 1,500 Q3 2017

Chevron Phillips Cedar Bayou, TX 1,500 Q4 2017

ExxonMobil Baytown, TX 1,500 Q1/Q2 2018

FPC USA Point Comfort, TX 1,150 Q4 2018

Shin Etsu Plaquemine, LA 500 2019

SASOL Lake Charles, LA 1,550 2019

Shell Pennsylvania 1,500 2020

Propylene

750 KTA PDH by Enterprise in Q2 2017 without

downstream Polymers would result in surplus

Propylene in US

On Purpose Propylene Production is around 20%

of overall propylene Globally and is expected to

rise to 25% by 2020

US Production of Butadiene is now lower by 30%

from pre 2014 as feed gets lighter.

India Capacity additions

13

Country is doubling its Ethylene capacity after

completion of these projects.

No major plans in Propylene expansions.

New Capacities are with mix feed

OPaL is dual feed while BRPL has Naphtha feed

GAIL & RIL Crackers are Gas based

India is surplus in Naphtha – New Naphtha

Cracker may be expected beyond 2020

Company LocationEthylene

Cap KTA

Start-up

Estimates

BRPL Assam 220 Started 2016

OPaL Dahej, Gujarat 1,100 Started 2016

GAIL Auraiya, UP 450Started – under

stabilisation

Reliance Jamnagar, Gujarat 1,550 Q2 2017

No major capacity planned in the Mid-East, but Iran may start producing in future with gas availability

China Capacity additions

14

Around 1.9 Mn MT/yr capacity CTO plants are

commissioned, but operating at lower capacity

More than 4 Mn MT/yr of MTO & CTO based

capacity addition planned in China

Some delays expected as economic viability for

these projects is challenged, so are issues with

Environment and Water stress.

China – CTO LocationEthylene

Cap KTA

Start-up

Estimates

Zongtiang Hechuang 2 Erdos 300 2017

SXY CPC Yan'an Yan'an 450 2018

Zhong'an Coal Chem Huainan 300 2019

Quinghai Damie Xining 200 2019

Shanxi Coking Corp Hongtong 300 2020

Yulin Energy & Chem Jingbian 300 2020

Baotou Shenua Baotao 300 2020

CPI / Total JV Erdos 330 2020

Quinghai Mining Haixi 270 2020

Apart from above, CNOOC Shell 1000 KTA & Shenhua 450 KTA Naphtha Crackers will be added in 2017

Demand Drivers - Ethylene

15

Polyethylene dominates the demand for Ethylene and is growing faster (4%) for its use in packaging & non durable applications. LLDPE demand growth leads with nearly 5% growth projections.

MEG too has robust growth (3%) for its use in Polyester fibres, PET, Antifreeze, etc

PVC has high growth (2.5%) in developing countries for its application in pipes, PVC films & Coatings.

Asia with high GDP countries is largest demand center. Overall we need nearly 5.5 – 6 Mn MT/yr of Ethylene for its derivatives.

Crackers to run at high Op Rate in mid term.

50%

60%

70%

80%

90%

100%

0.0

50.0

100.0

150.0

200.0

250.0

11 12 13 14 15 16 17 18 19 20

Alpha Olefins (3.9/4.2) Ethylbenzene (0.4/1.9)

EDC (0.7/2.3) Ethylene Oxide (3.0/3.0)

HDPE (3.4/3.9) LDPE (2.2/2.6)

LLDPE (5.1/4.7) Vinyl Acetate (1.5/2.2)

Other (3.0/2.7) Operating Rate

World: Ethylene Demand

Source: IHS © 2016 IHS(% AAGR = 11-16/16-26)

Forecast

Op

era

tin

gR

ate

Mil

lio

n M

etr

ic T

on

s

Demand Drivers - Propylene

16

Polypropylene is the major share as well as fastest growing (4.5%) derivative of Propylene.

Asia (India + China) lead the demand growth.

Other major Propylene consumer are

ACN for Acrylic fibres and ABS Polymers.

Propylene Oxide for antifreeze & Poly-Urethanes

Oxo Alcohols for coatings & plasticizers

Cumene/Phenol for Poly carbonates & resins

Acrylic Acid for coating, Adhesives & Super Absorbent Polymers

On Purpose Propylene gaining strength (PDH/MTP)

50%

60%

70%

80%

90%

100%

0.0

40.0

80.0

120.0

160.0

200.0

11 12 13 14 15 16 17 18 19 20

Acrylic Acid (3.1/3.4) Acrylonitrile (1.6/2.9)

Cumene (3.6/3.0) Isopropanol (4.1/1.4)

2-Ethyl Hexanol (4.6/2.1) Butanols (2.7/3.4)

Polypropylene (4.7/4.3) Propylene Oxide (4.7/3.5)

Others (6.5/4.2) Operating Rate

World: PG/CG Propylene Demand

Source: IHS © 2016 IHS(% AAGR = 11-16/16-26)

Forecast

Op

era

tin

gR

ate

Mil

lio

n M

etr

ic T

on

s

17

Regional Olefins Trade

Ethylene Trade

18

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

11 12 13 14 15 16 17 18 19 20

N. America S. America W. Europe C. Europe CIS & Baltics

Africa Middle East Indian Subc. NE Asia SE Asia

Regional Ethylene Monomer Net Trade

Forecast

Millio

n M

etr

ic T

on

s

Net Imports

Net Exports

Source: IHS © 2016 IHS

+ China currently imports 9 Mn MT of PE & 4 Mn MT of MEG

ME (KTA)

2011 1260

2015 400

2020 450

Asia (KTA)

2011 -900

2015 -400

2020 -800

US Export 120-180 KTA

US to take over Ethylene Exports from ME

Propylene Trade

19

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

11 12 13 14 15 16 17 18 19 20

N. America S. America W. Europe C. Europe CIS & Baltics

Africa Middle East Indian Subc. NE Asia SE Asia

Regional PG/CG Propylene Net Trade

Forecast

Millio

n M

etr

ic T

on

s

Net Imports

Net Exports

Source: IHS © 2016 IHS

+ China imports 8 Mn MT of Propylene derivatives (PP)

ME (KTA)

2011 200

2015 350

2020 500

SEA (KTA)

2011 150

2015 -120

2020 100

NEA Short by -250KTADeficit high in 2016-2019

C EU (KTA)

2011 100

2015 100

2020 200

Key Concerns

20

Ethylene

Delay in New Ethylene Capacity addition and also delays in downstream capacities to impact S-D Balances & Trade flow and firms up Cracker Operating rates (87+) in mid-term.

Prolonged delays in CTO & MTO capacity would impact China’s Ethylene & derivatives balances

Lighter feedstock changing downstream Butadiene availability & high price fluctuations

Propylene

On-Purpose PDH in US without downstream capacity (PP or others) to impact Propylene trade flow in the mid-term

Price volatility due to high regional imbalance in the mid-term.

PDH competing with MTP in China – Low Cost Propane v/s higher cost Coal to Methanol or with imported Methanol