Bangladesh Positioning Survey for the Dutch water sector Aidenvironment Commissioned by RVO/NWP April 2015 Project number 2526 Aidenvironment Barentszplein 7 1013 NJ Amsterdam The Netherlands + 31 (0)20 686 81 11 [email protected]www.aidenvironment.org

Transcript

Bangladesh Positioning Survey for the Dutch water sector

1% of GDP (2011), FDI stock at home USD 7,04 billion, the

Netherlands are the third largest investor (after Egypt and US)

investing USD 116.75 million (WTO 2012)

Imports USD 32.94 (2013 est.)

Import partners

China 21.7%, India 16.3%, Malaysia 5.2%, Republic of Korea

4.5%, Japan 4.1% (2013 est.)

BTI index on banking system 5 (out of 10)

Doing business index 173 (out of 189)

WEF Global competitive index 3,7 (position is 110 out of 148)

Transparency Index 145 out of 174

Source: CIA Intelligence 2012-2014, BTI 2014, World Bank Statistics, World Economic Forum, others

1.2 The water situation

This section describes the physical water situation (including flooding of river systems, coastal zones

and maritime areas), the influence of climate change, the effect of irrigation and the water pressure.

1.2.1 Physical description of the water situation

Rainwater:

Bangladesh is divided into seven hydrological regions. The Ganges basin in the western part of

Bangladesh is drought prone and receives the least average rainfall in the country. Khulna in the

Southwest suffers from salinity intrusion from the sea. The Southeast Hill basin experiences heavy

rainfall owing to its location on the Bay of Bengal. The Meghna basin in the Northeast region receives

the highest average rainfall in the country. The other basins are Cox’s Bazar and Rajshahi (see figure

below).

Figure 1 Hydrological Regions

Two major basins

Source: Google maps

Project number 2526 8

Groundwater

The availability of groundwater resources in Bangladesh is determined by the properties of the

groundwater storage reservoir and the volume of annual recharge. The source of recharge is rainfall,

flooding, and stream flow in rivers. The quaternary alluvium of Bangladesh comprises a huge aquifer

with reasonably good transmission and storage properties. Heavy rainfall and inundation during the

monsoon substantially recharge aquifers annually.

Seawater:

Bangladesh has a 580 kilometer coast line. Seawater is more a threat than a solution to the people of

Bangladesh. Seawater causes flooding and leads to salinity intrusion in the coastal region, having

increasing negative impact on food production and the provision of drinking water.

Surface Water:

The ratio of peak to low season flow is approximately 25:1. Only 7% of the country's water surface

flow has a source within the country borders, the other 93% comes from trans-boundary rivers

shared with India, Myanmar, Nepal, Butan and China1. Bangladesh has limited control over rivers

entering its borders; future developments, (especially in India), will increasingly have an effect on the

availability of water in the rivers in Bangladesh.

1.2.2 Climate and climate change

Climate vulnerability is high in Bangladesh particularly to disasters (cyclones and flooding). The

National Water Management Plan (formulated in 1999) has considered the effect of climate change in

estimating water demand in various regions of the country and mentions the impacts of climate

change like increase water demand particularly in Ganges basin, prolonged floods and drainage

congestions and negative impacts in coastal zone due to rising sea-level2 which all has implications for

food security of the country. The Water Act (2013) is designed for integrated development,

management, extraction, distribution, usage, protection and conservation of water resources in

Bangladesh.

Climate change is likely to increase river salinity leading to shortages of drinking water and

irrigation, and significant changes in the aquatic ecosystems in the Southwest coastal areas of

Bangladesh during dry season by 2050.

Increase in soil salinity may lead to decline yield by 15.6 percent of high-yielding-variety rice and

reduce the income of farmers significantly in coastal area.

Source: World Bank website February 2015

1.2.3 Pressures on water sources3

Total renewable water resources 1,227 km2

Fresh water withdraw 35.87 km2 / yr

Especially in the Northwestern part the level of groundwater is declining rapidly. The areas face

frequently drought while high water consuming agriculture (rice) is the common way of making a

living. Surface water is often polluted and not suitable for drinking purposes. In Bangladesh,

approximately one third of the country’s population is drinking ground water from shallow tube wells

containing 10 to 50 times the amount of Arsenic (As) that is considered safe.

Water management for adequate food production is absolutely vital for Bangladesh. Sixty percent

1 Kahn, 2011

2 NGO Forum, 2009

3 CIA Intelligence 2012-2014

Project number 2526 9

(60%) of the rice in Bangladesh is produced during the dry season mainly using groundwater.

Competing water claims are emerging. Overexploiting groundwater leads to declining groundwater

levels (3 meters per year in the Dhaka area) and results in Arsenic contamination and especially in

the coastal areas increasing salinity of well water, creating an additional risk for an adequate supply

of drinking water.

1.2.4 Irrigation4

The agriculture sector uses 88% of all fresh water extracted in Bangladesh, especially from

groundwater5. Bangladesh has 50,500 sq km irrigated land, which is 59% of the 85,490 sq km

cultivated land. The country area is 144,000 sq km. Surface irrigation is the only technology used in

large irrigation schemes. In 2008, the total area equipped for full control irrigation covered by large

irrigation schemes (major irrigation) was an estimated 0.14 million ha (3%). Small irrigation schemes

covered a total area of 4.91 million ha (97%).

Though there has been a significant increase in irrigated agriculture over the last decade that would

have contributed to the positive increase in the agriculture net production index, most minor and

major irrigation systems have shown poor field performances owing to a lack of technical know-how,

as well as poor on-farm water management practices. Canal irrigation shortage is a major constraint

to cropping, alleviated by pumping of groundwater. Other water resource concerns are flooding,

drainage congestion and the cost of pumping of canal and / or groundwater. It is clear that improving

agriculture production in Bangladesh requires achieving greater control of water resources

throughout the year, and that an integrated approach to water resources management is desirable.

Shrimp farming has become a principle activity in coastal brackish aquaculture, as it is one of the

fastest growing export industries in Bangladesh6. Around 1 million people are employed in the shrimp

sector. Inland capture fisheries have been declining, due to loss of wetlands, pollution and irrigation

abstraction. Brackish water aquacultures are not so affected. According to FAO Fishery Statistics

(2012), the production in Bangladesh increased from around 50,000 tons (1950) to 1.3 million tons

(2010).

1.2.5 Flooding of river systems

Inland waterways in Bangladesh cover some 11% of its total surface area. With some 700 rivers and

tributaries, Bangladesh has one of the largest inland waterways networks in the world (24,000 km).

In Bangladesh 80% of the land is covered by the floodplains of the Brahmaputra, Ganges and

Meghna rivers. The discharge of these three rivers is second only to that of the Amazon River.

Of the country, 60% is lower than 6 meters above sea level. Flood events occur frequently during the

wet season, which are able to inundate up to 65% of the country, while droughts are a general cause

of water scarcity during the dry season7.

1.2.6 Coastal zones and maritime areas

Bangladesh’s coastal zone spans over580km and includes territory where 28 percent of the

population resides. Bangladesh is a maritime nation with 166,000 km coastal zone, about 90% of all

foreign trade is moved by sea transportation. There are some 200 shipbuilding and repairing yards in

various locations in the country. Much of these shipbuilding yards are engaged in building and

4 CIA intelligence 2012-2014

5 Market Scan on the Bangladesh Water Sector, MottMacDonald, 2010 6 Exploring the Water Sector in Bangladesh. Trends, opportunities and practical information, Nyenrode University, 2014

7 World Bank Strategy paper 2005

Project number 2526 10

repairing small inland and costal vessels up to 3,500 DWT8. However many of these yards were never

adequately operational. Currently several private sector initiatives are being taken to establish dry

docks for ship repair and also shipyards for shipbuilding.

There are three main ports in Bangladesh: Chittagong, Mongla, and Dhaka–Narayanganj, with 80%

of the trade flowing through the port of Chittagong. Chittagong Port is an integral part of the sub

regional transport and logistics chain connecting northeastern India, Bhutan, and Nepal to Europe,

North America, and Southeast Asia. The efficiency of the transportation system in the Dhaka–

Chittagong corridor and the port of Chittagong in particular, is considered vital for sustained

economic growth9.

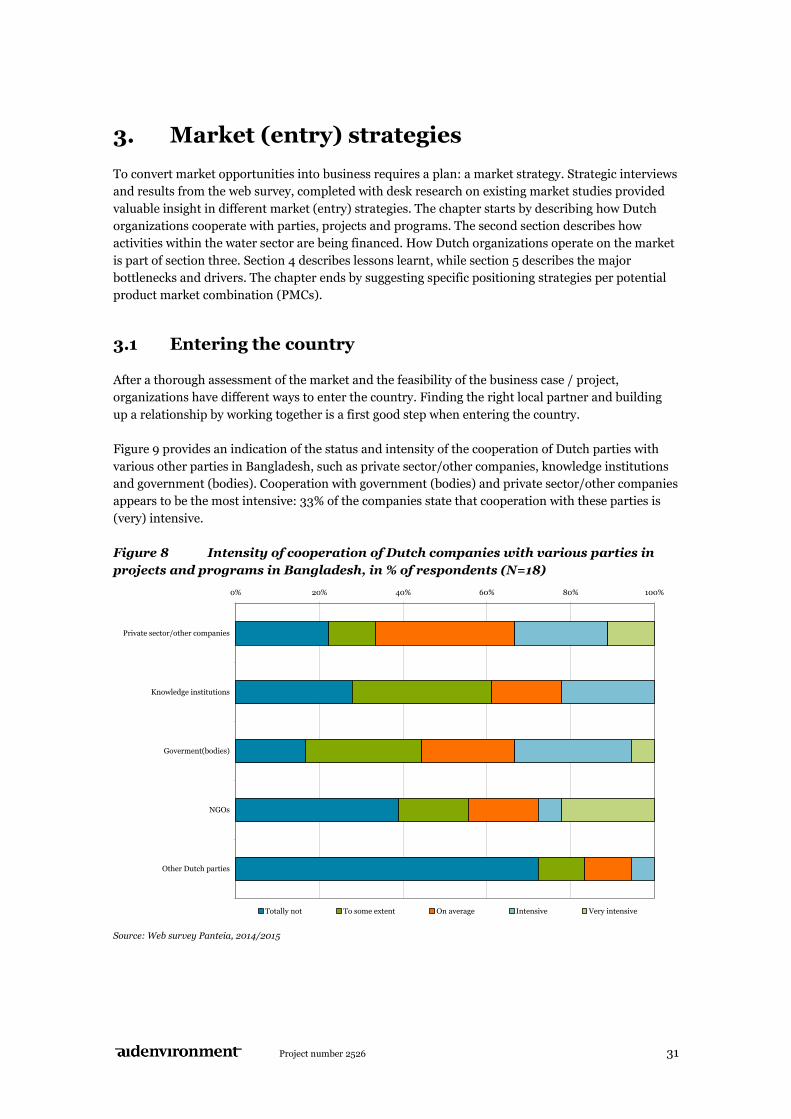

1.3 The water sector

This section describes the public sector, the legislation, the spending and investment planning and

the role of the private sector, NGOs and knowledge institutes. This section ends by identifying the

pressing needs and explaining the Dutch Government engagement strategy.

1.3.1 Public sector

Central Level:

The public sector within the water market plays a dominant role in the overall planning, design and

implementation of programs and projects. In the majority of cases, the agencies within the public

sector act as the regulatory body, and are responsible for the management and operation of relevant

activities. The planning commission, chaired by the prime minister is one of the most powerful

bodies and plays an important role in the decision making process of development plans.

The Ministry of Water Resources (MoWR) is responsible for flood management, irrigation, drainage

control, erosion protection, land reclamation, integrated management of coastal polders, river flow

augmentation, water sharing from trans boundary rivers and wetland conservation through

participation of local people and coordinated programs with all ministries dependent on water

resources. Part of MoWR is The National Water Resources Council, (NWRC). This is the highest

national body for the formulation of water policy. It coordinates different water agencies and advises

the cabinet on all water policy issues. NWRC formulated its national water policy in 1999.

The Bangladesh Water and Development Board develop and manages water resources projects,

manages and mitigates river bank erosion, organizes stakeholders participation in project planning,

design and implementation, and promotes food production by surface water irrigation. The Minister

of Water Resources chairs the board.

WARPO is a principal agency of the GoB under the Ministry of Water Resources. It has a mandate to

ensure coordination of all relevant ministries through the NWRC and to plan all aspects of water

development, including major and minor irrigation, navigation, fisheries and domestic water supply.

WARPO is responsible for developing the National Water Management Plan.

The Disaster Management and Relief Division (DMRD) (MoDMR) has been given the mandate to

drive national risk reduction reform programs, as Bangladesh encounters varies types of water

related disasters, e.g. flooding and cyclones. The mission of MoDMR is: “To achieve a paradigm shift

8 Market Scan on the Bangladesh Water Sector, MottMacDonald, 2010

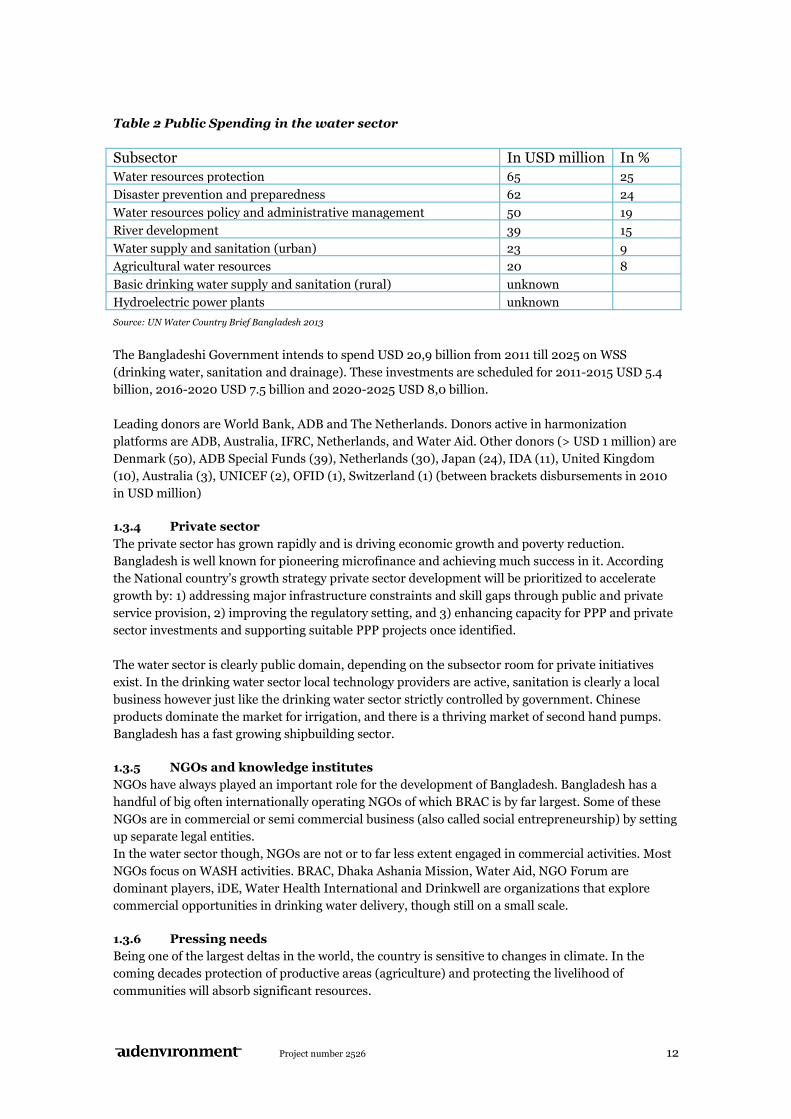

Water resources policy and administrative management 50 19

River development 39 15

Water supply and sanitation (urban) 23 9

Agricultural water resources 20 8

Basic drinking water supply and sanitation (rural) unknown

Hydroelectric power plants unknown

Source: UN Water Country Brief Bangladesh 2013

The Bangladeshi Government intends to spend USD 20,9 billion from 2011 till 2025 on WSS

(drinking water, sanitation and drainage). These investments are scheduled for 2011-2015 USD 5.4

billion, 2016-2020 USD 7.5 billion and 2020-2025 USD 8,0 billion.

Leading donors are World Bank, ADB and The Netherlands. Donors active in harmonization

platforms are ADB, Australia, IFRC, Netherlands, and Water Aid. Other donors (> USD 1 million) are

Denmark (50), ADB Special Funds (39), Netherlands (30), Japan (24), IDA (11), United Kingdom

(10), Australia (3), UNICEF (2), OFID (1), Switzerland (1) (between brackets disbursements in 2010

in USD million)

1.3.4 Private sector

The private sector has grown rapidly and is driving economic growth and poverty reduction.

Bangladesh is well known for pioneering microfinance and achieving much success in it. According

the National country’s growth strategy private sector development will be prioritized to accelerate

growth by: 1) addressing major infrastructure constraints and skill gaps through public and private

service provision, 2) improving the regulatory setting, and 3) enhancing capacity for PPP and private

sector investments and supporting suitable PPP projects once identified.

The water sector is clearly public domain, depending on the subsector room for private initiatives

exist. In the drinking water sector local technology providers are active, sanitation is clearly a local

business however just like the drinking water sector strictly controlled by government. Chinese

products dominate the market for irrigation, and there is a thriving market of second hand pumps.

Bangladesh has a fast growing shipbuilding sector.

1.3.5 NGOs and knowledge institutes

NGOs have always played an important role for the development of Bangladesh. Bangladesh has a

handful of big often internationally operating NGOs of which BRAC is by far largest. Some of these

NGOs are in commercial or semi commercial business (also called social entrepreneurship) by setting

up separate legal entities.

In the water sector though, NGOs are not or to far less extent engaged in commercial activities. Most

NGOs focus on WASH activities. BRAC, Dhaka Ashania Mission, Water Aid, NGO Forum are

dominant players, iDE, Water Health International and Drinkwell are organizations that explore

commercial opportunities in drinking water delivery, though still on a small scale.

1.3.6 Pressing needs

Being one of the largest deltas in the world, the country is sensitive to changes in climate. In the

coming decades protection of productive areas (agriculture) and protecting the livelihood of

communities will absorb significant resources.

Project number 2526 13

Population in urban areas is still growing; Dhaka is one of the fastest growing cities in the world. The

provision of water, sanitation and wastewater treatment in urban context will have a high priority.

Besides, increasing population will put pressure on the availability of land, leading to a higher

demand for e.g. land reclamation.

Due to the lack of international agreements about trans-boundary water issues regarding rivers

flowing into Bangladesh, and effects of climate change, the coastal areas will face increasing salinity

of groundwater and soil, causing decreasing yields and less access to drinking water.

The agriculture sector in Bangladesh is the largest water consumer. The government subsidizes rice

production and irrigation (using groundwater) to enhance food security. As a result ground water

levels are expected to drop increasingly, especially in the Northwestern region. Facing conflicts

between water for direct consumption and productive use, irrigation techniques must improve.

1.3.7 Dutch cooperation and priorities

Bangladesh and the Netherlands’ relationship is transitioning from a traditional aid to trade

relationship. This means that the Embassy’s development cooperation program more and more links

trade and investment to the three priority areas: water, food security and sexual reproductive health

and rights. The transition relationship between Bangladesh and the Netherlands aims at phasing out

development cooperation in the run up to middle income status (planned 2020), for which 2025

seems to be a more realistic date for achieving that.

With respect to the priority theme water, the aim of the support is to contribute to a healthy living

environment and wellbeing that supports economic growth in a country where more extreme rainfall

is anticipated, higher sea water levels, increasing industrial pollution and further slum development.

Bangladesh, as one of the five delta countries included in the ‘Water Mondiaal Program’, continues to

have high expectations for close bilateral cooperation in the area of water management, an area that

faces significant challenges. The program has a focus on 1) sustainable participative water

management in the existing polders and in the reclaimed land of the coastal zone, 2) river

management, 3) drinking water and sanitation in rural and urban areas and 4) institutional

strengthening. The total budget adds up to EUR 95.4 million (2014-2017).

The Dutch and Bangladesh Government signed a MoU on May 22, 2012 to develop a Delta Plan for

Bangladesh. The aim is to develop a plan to realize a sustainable water management plan for

Bangladesh. The Delta plan is a long-term framework for water management and the prevention of

flooding. It is an integrated plan and it will be the reference for investments of the Bangladeshi

Government in infrastructure, especially water related infrastructure.

Project number 2526 14

2. Chances and opportunities

This chapter presents the results of the web survey among Dutch water sector players, completed by

the main observations derived from previous (existing) market studies and interviews with water

professionals and strategic actors within the Dutch water sector (please refer to Appendix 1 providing

an overview of the method of research). The first section describes the current situation. The second

section describes the most important trends, linking the current situation with future opportunities,

which is the topic of the third section. This chapter ends by identifying promising product market

combinations (PMCs).

2.1 Current situation

The section starts by describing the current situation, how the Dutch water sector is involved, the

type of activities performed, client groups and performance on specific development indicators.

2.1.1 Dutch sector involvement

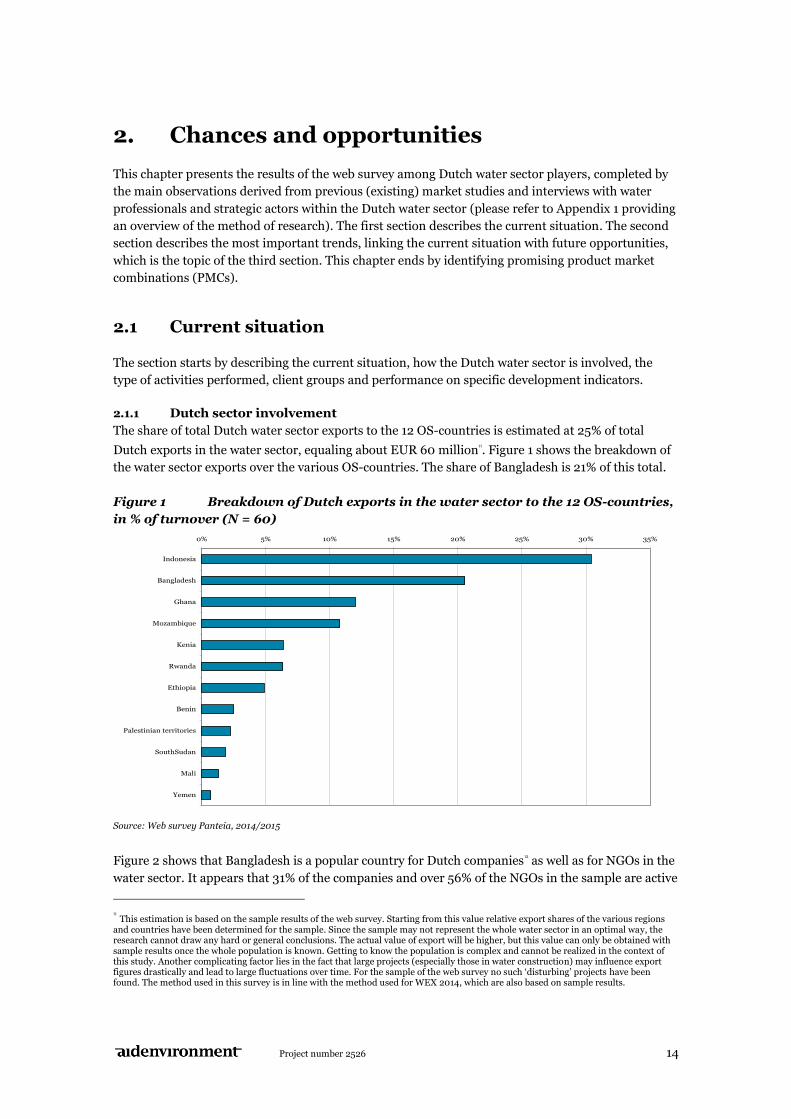

The share of total Dutch water sector exports to the 12 OS-countries is estimated at 25% of total

Dutch exports in the water sector, equaling about EUR 60 million11. Figure 1 shows the breakdown of

the water sector exports over the various OS-countries. The share of Bangladesh is 21% of this total.

Figure 1 Breakdown of Dutch exports in the water sector to the 12 OS-countries,

in % of turnover (N = 60)

Source: Web survey Panteia, 2014/2015

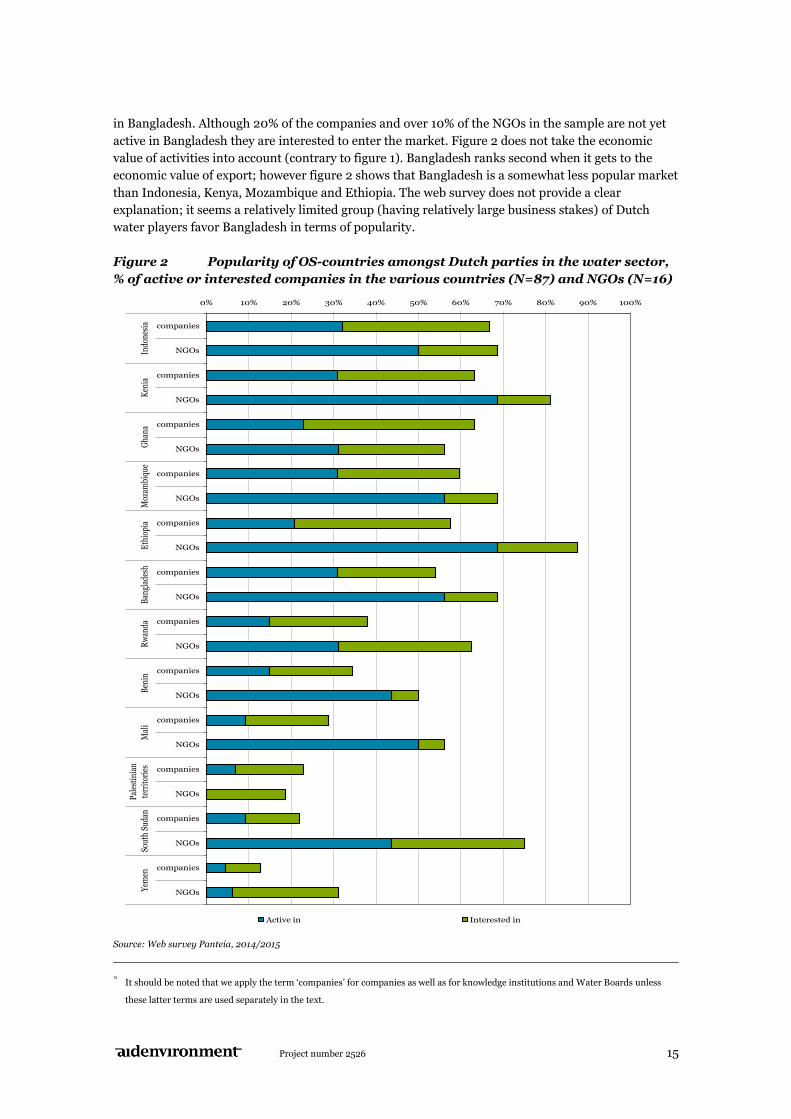

Figure 2 shows that Bangladesh is a popular country for Dutch companies12 as well as for NGOs in the

water sector. It appears that 31% of the companies and over 56% of the NGOs in the sample are active

11 This estimation is based on the sample results of the web survey. Starting from this value relative export shares of the various regions

and countries have been determined for the sample. Since the sample may not represent the whole water sector in an optimal way, the research cannot draw any hard or general conclusions. The actual value of export will be higher, but this value can only be obtained with sample results once the whole population is known. Getting to know the population is complex and cannot be realized in the context of this study. Another complicating factor lies in the fact that large projects (especially those in water construction) may influence export figures drastically and lead to large fluctuations over time. For the sample of the web survey no such ‘disturbing’ projects have been found. The method used in this survey is in line with the method used for WEX 2014, which are also based on sample results.

0% 5% 10% 15% 20% 25% 30% 35%

Indonesia

Bangladesh

Ghana

Mozambique

Kenia

Rwanda

Ethiopia

Benin

Palestinian territories

SouthSudan

Mali

Yemen

Project number 2526 15

in Bangladesh. Although 20% of the companies and over 10% of the NGOs in the sample are not yet

active in Bangladesh they are interested to enter the market. Figure 2 does not take the economic

value of activities into account (contrary to figure 1). Bangladesh ranks second when it gets to the

economic value of export; however figure 2 shows that Bangladesh is a somewhat less popular market

than Indonesia, Kenya, Mozambique and Ethiopia. The web survey does not provide a clear

explanation; it seems a relatively limited group (having relatively large business stakes) of Dutch

water players favor Bangladesh in terms of popularity.

Figure 2 Popularity of OS-countries amongst Dutch parties in the water sector,

% of active or interested companies in the various countries (N=87) and NGOs (N=16)

Source: Web survey Panteia, 2014/2015

12 It should be noted that we apply the term ‘companies’ for companies as well as for knowledge institutions and Water Boards unless

these latter terms are used separately in the text.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

companies

NGOs

Indo

nes

iaK

enia

Gha

na

Moz

ambi

que

Eth

iopi

aB

angl

ades

hR

wan

daB

enin

Mal

i

Pal

esti

nia

n

terr

itor

ies

Sout

h Su

dan

Yem

en

Active in Interested in

Project number 2526 16

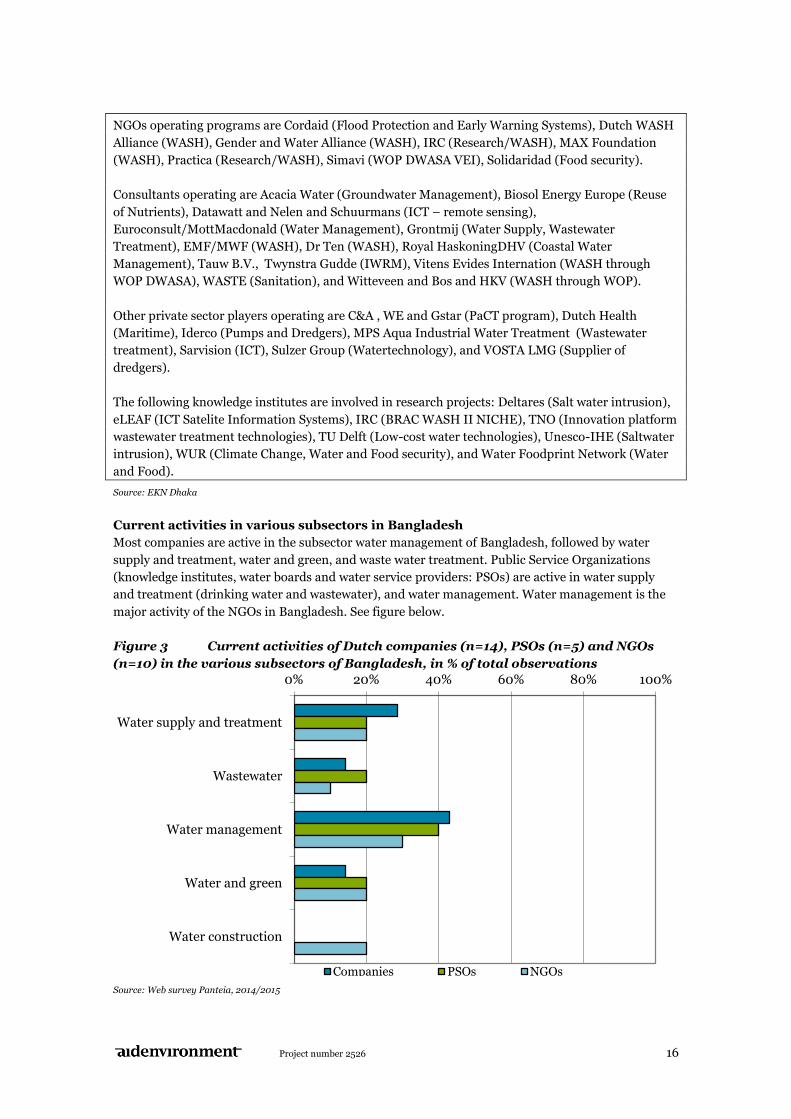

NGOs operating programs are Cordaid (Flood Protection and Early Warning Systems), Dutch WASH

Alliance (WASH), Gender and Water Alliance (WASH), IRC (Research/WASH), MAX Foundation

private commercial banks (PCBs) and 9 foreign commercial banks (FCBs).

The micro finance sector has a clear presence in Bangladesh. The Grameen Bank, BRAC, and local

savings-societies play an important role in rural areas by extending microcredit loans to the poor.

They often have better loan repayment rates than state-run banks (source BTI). The local financial

sector does not play a significant role in financing the water sector.

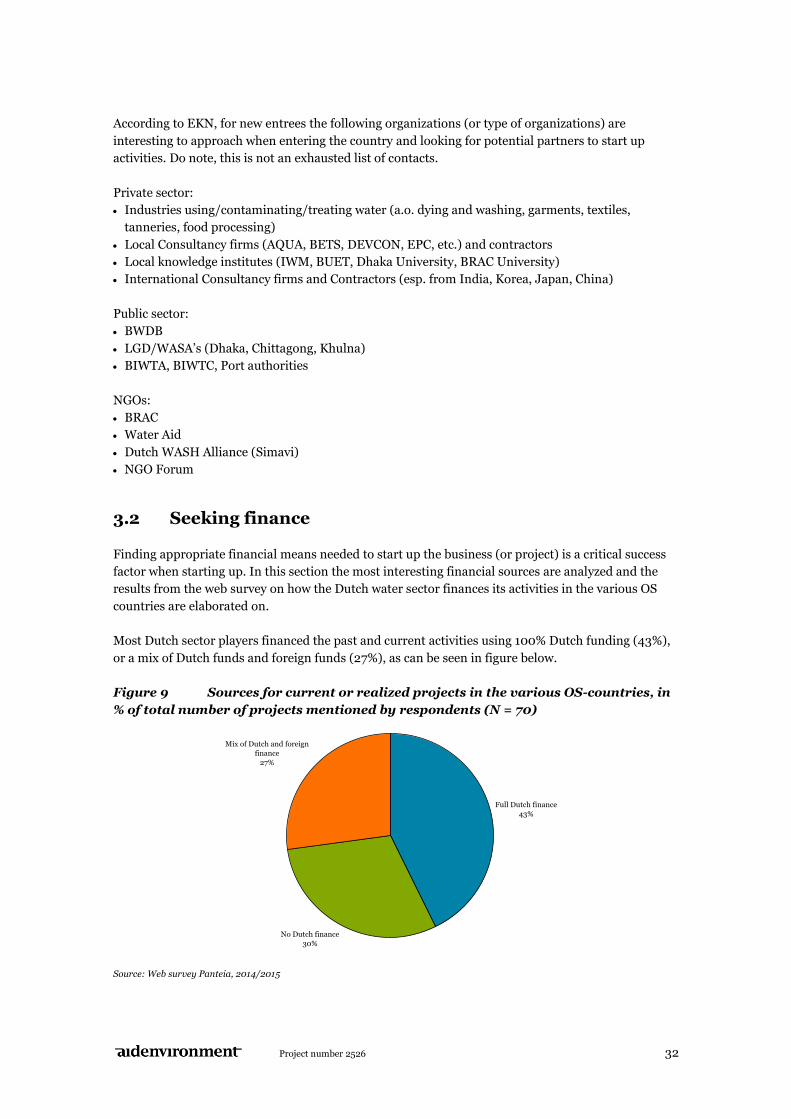

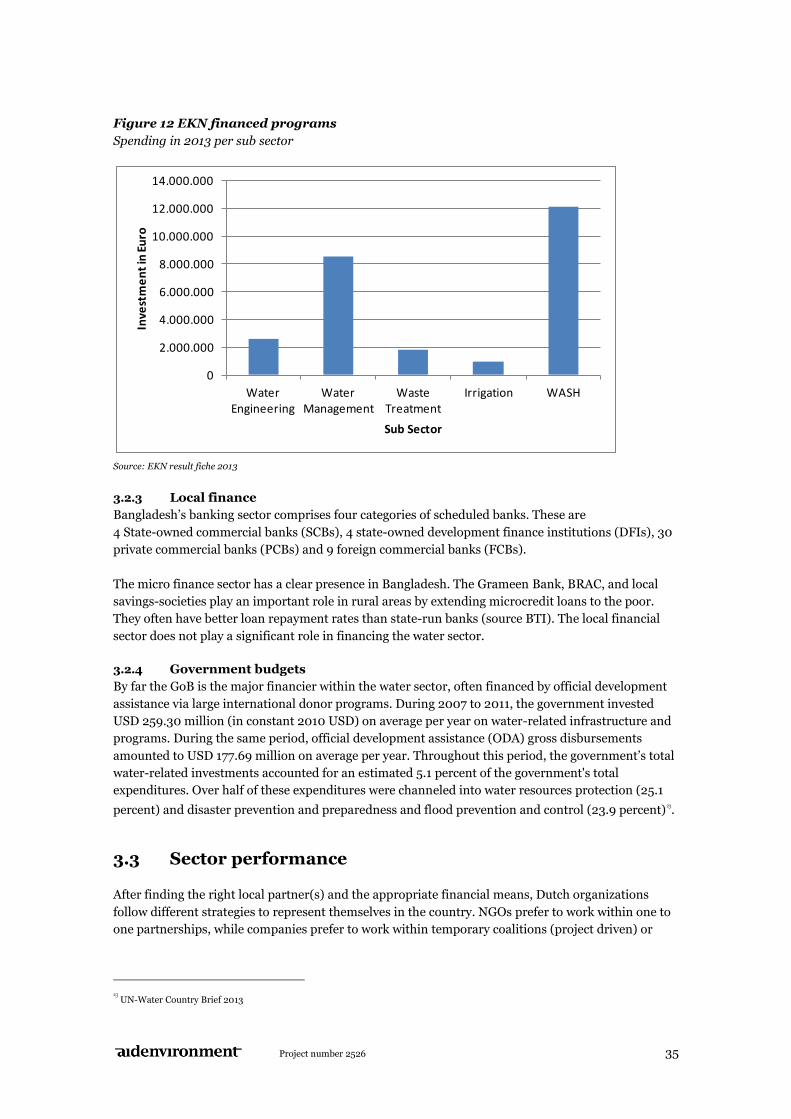

3.2.4 Government budgets

By far the GoB is the major financier within the water sector, often financed by official development

assistance via large international donor programs. During 2007 to 2011, the government invested

USD 259.30 million (in constant 2010 USD) on average per year on water-related infrastructure and

programs. During the same period, official development assistance (ODA) gross disbursements

amounted to USD 177.69 million on average per year. Throughout this period, the government’s total

water-related investments accounted for an estimated 5.1 percent of the government's total

expenditures. Over half of these expenditures were channeled into water resources protection (25.1

percent) and disaster prevention and preparedness and flood prevention and control (23.9 percent)23.

3.3 Sector performance

After finding the right local partner(s) and the appropriate financial means, Dutch organizations

follow different strategies to represent themselves in the country. NGOs prefer to work within one to

one partnerships, while companies prefer to work within temporary coalitions (project driven) or

23

UN-Water Country Brief 2013

0

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

14.000.000

Water Engineering

Water Management

Waste Treatment

Irrigation WASH

Inve

stm

en

t in

Eu

ro

Sub Sector

Project number 2526 36

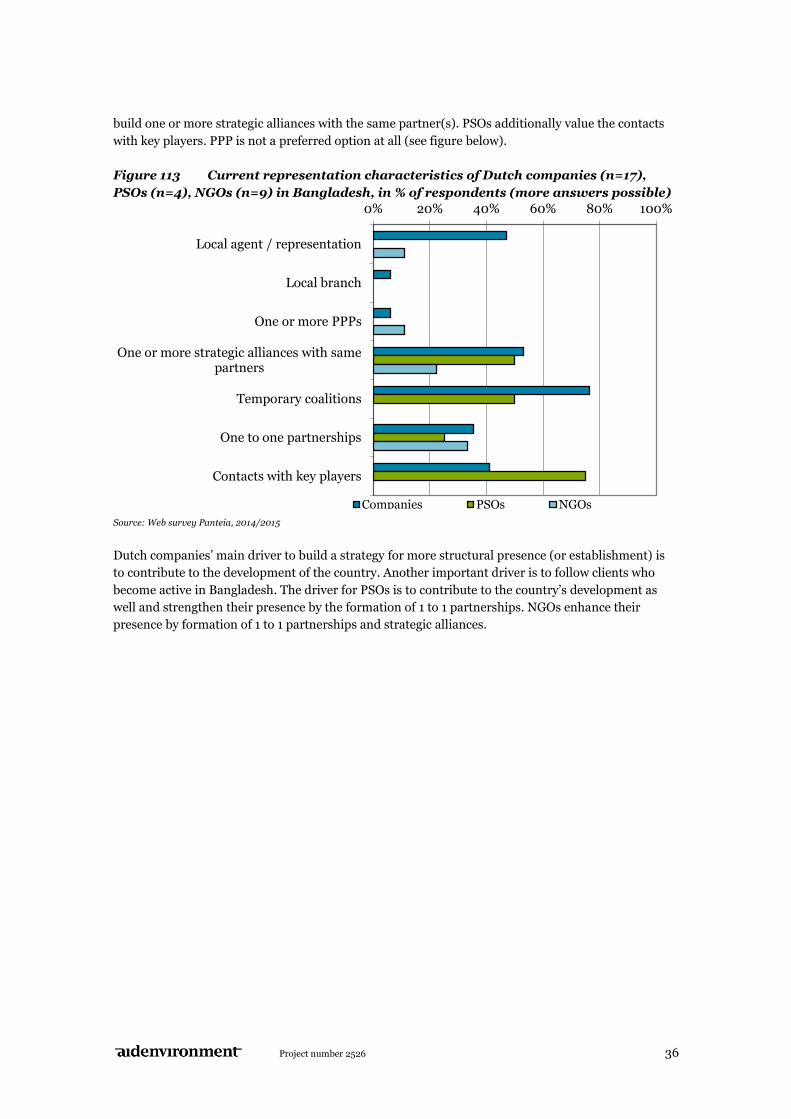

build one or more strategic alliances with the same partner(s). PSOs additionally value the contacts

with key players. PPP is not a preferred option at all (see figure below).

Figure 113 Current representation characteristics of Dutch companies (n=17),

PSOs (n=4), NGOs (n=9) in Bangladesh, in % of respondents (more answers possible)

Source: Web survey Panteia, 2014/2015

Dutch companies’ main driver to build a strategy for more structural presence (or establishment) is

to contribute to the development of the country. Another important driver is to follow clients who

become active in Bangladesh. The driver for PSOs is to contribute to the country’s development as

well and strengthen their presence by the formation of 1 to 1 partnerships. NGOs enhance their

presence by formation of 1 to 1 partnerships and strategic alliances.

0% 20% 40% 60% 80% 100%

Local agent / representation

Local branch

One or more PPPs

One or more strategic alliances with same partners

Temporary coalitions

One to one partnerships

Contacts with key players

Companies PSOs NGOs

Project number 2526 37

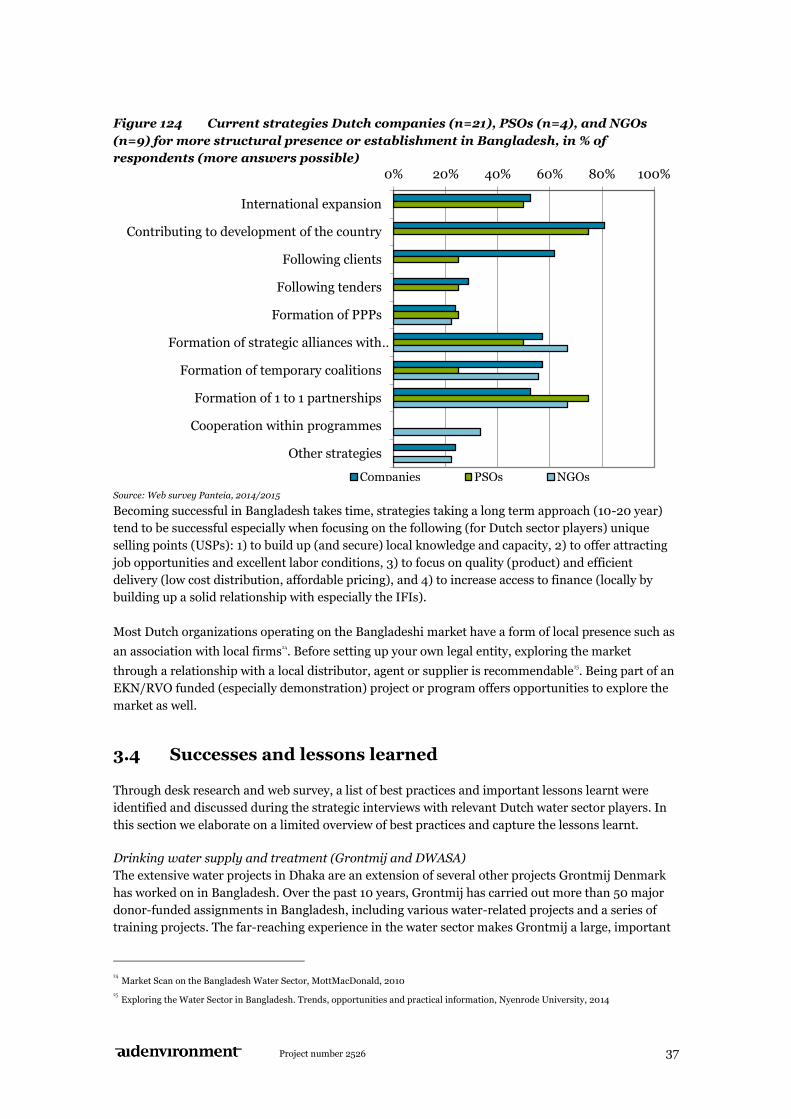

Figure 124 Current strategies Dutch companies (n=21), PSOs (n=4), and NGOs

(n=9) for more structural presence or establishment in Bangladesh, in % of

respondents (more answers possible)

Source: Web survey Panteia, 2014/2015

Becoming successful in Bangladesh takes time, strategies taking a long term approach (10-20 year)

tend to be successful especially when focusing on the following (for Dutch sector players) unique

selling points (USPs): 1) to build up (and secure) local knowledge and capacity, 2) to offer attracting

job opportunities and excellent labor conditions, 3) to focus on quality (product) and efficient

delivery (low cost distribution, affordable pricing), and 4) to increase access to finance (locally by

building up a solid relationship with especially the IFIs).

Most Dutch organizations operating on the Bangladeshi market have a form of local presence such as

an association with local firms24. Before setting up your own legal entity, exploring the market

through a relationship with a local distributor, agent or supplier is recommendable25. Being part of an

EKN/RVO funded (especially demonstration) project or program offers opportunities to explore the

market as well.

3.4 Successes and lessons learned

Through desk research and web survey, a list of best practices and important lessons learnt were

identified and discussed during the strategic interviews with relevant Dutch water sector players. In

this section we elaborate on a limited overview of best practices and capture the lessons learnt.

Drinking water supply and treatment (Grontmij and DWASA)

The extensive water projects in Dhaka are an extension of several other projects Grontmij Denmark

has worked on in Bangladesh. Over the past 10 years, Grontmij has carried out more than 50 major

donor-funded assignments in Bangladesh, including various water-related projects and a series of

training projects. The far-reaching experience in the water sector makes Grontmij a large, important

24 Market Scan on the Bangladesh Water Sector, MottMacDonald, 2010

25 Exploring the Water Sector in Bangladesh. Trends, opportunities and practical information, Nyenrode University, 2014

0% 20% 40% 60% 80% 100%

International expansion

Contributing to development of the country

Following clients

Following tenders

Formation of PPPs

Formation of strategic alliances with …

Formation of temporary coalitions

Formation of 1 to 1 partnerships

Cooperation within programmes

Other strategies

Companies PSOs NGOs

Project number 2526 38

international player on this market. These latest projects in Bangladesh will further strengthen the

company’s position and help to win new contracts both in Bangladesh and in neighboring countries.

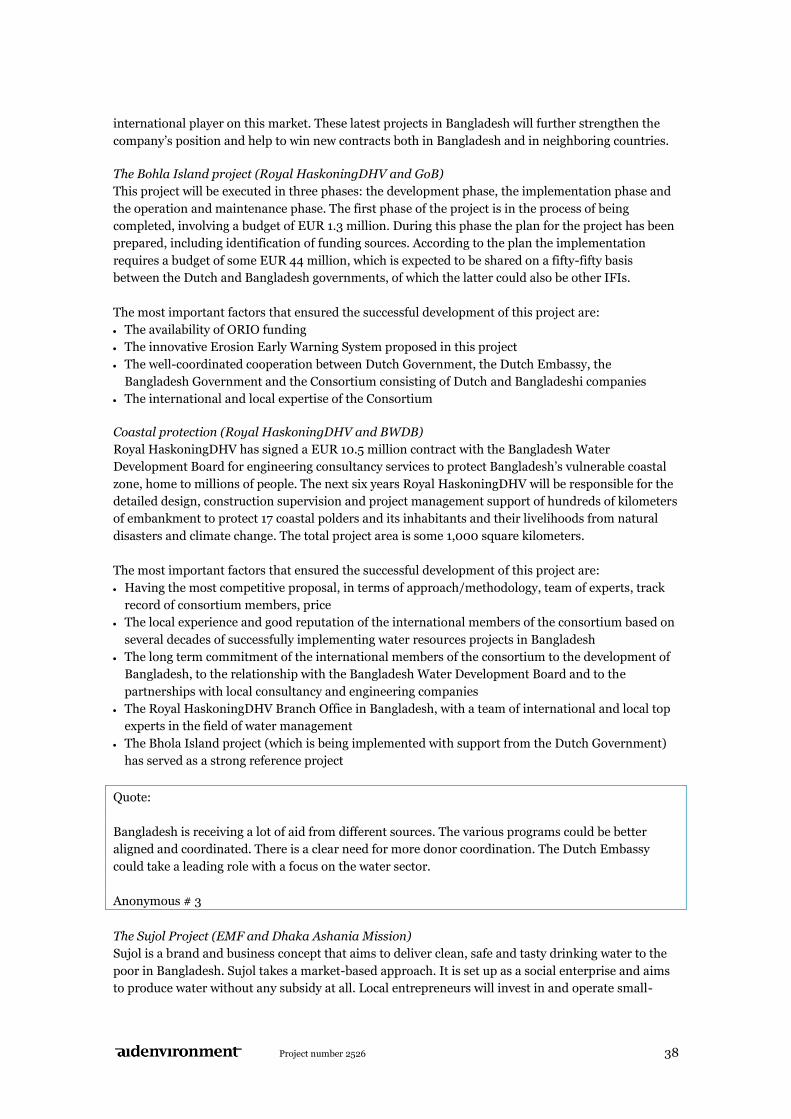

The Bohla Island project (Royal HaskoningDHV and GoB)

This project will be executed in three phases: the development phase, the implementation phase and

the operation and maintenance phase. The first phase of the project is in the process of being

completed, involving a budget of EUR 1.3 million. During this phase the plan for the project has been

prepared, including identification of funding sources. According to the plan the implementation

requires a budget of some EUR 44 million, which is expected to be shared on a fifty-fifty basis

between the Dutch and Bangladesh governments, of which the latter could also be other IFIs.

The most important factors that ensured the successful development of this project are:

The availability of ORIO funding

The innovative Erosion Early Warning System proposed in this project

The well-coordinated cooperation between Dutch Government, the Dutch Embassy, the

Bangladesh Government and the Consortium consisting of Dutch and Bangladeshi companies

The international and local expertise of the Consortium

Coastal protection (Royal HaskoningDHV and BWDB)

Royal HaskoningDHV has signed a EUR 10.5 million contract with the Bangladesh Water

Development Board for engineering consultancy services to protect Bangladesh’s vulnerable coastal

zone, home to millions of people. The next six years Royal HaskoningDHV will be responsible for the

detailed design, construction supervision and project management support of hundreds of kilometers

of embankment to protect 17 coastal polders and its inhabitants and their livelihoods from natural

disasters and climate change. The total project area is some 1,000 square kilometers.

The most important factors that ensured the successful development of this project are:

Having the most competitive proposal, in terms of approach/methodology, team of experts, track

record of consortium members, price

The local experience and good reputation of the international members of the consortium based on

several decades of successfully implementing water resources projects in Bangladesh

The long term commitment of the international members of the consortium to the development of

Bangladesh, to the relationship with the Bangladesh Water Development Board and to the

partnerships with local consultancy and engineering companies

The Royal HaskoningDHV Branch Office in Bangladesh, with a team of international and local top

experts in the field of water management

The Bhola Island project (which is being implemented with support from the Dutch Government)

has served as a strong reference project

Quote:

Bangladesh is receiving a lot of aid from different sources. The various programs could be better

aligned and coordinated. There is a clear need for more donor coordination. The Dutch Embassy

could take a leading role with a focus on the water sector.

Anonymous # 3

The Sujol Project (EMF and Dhaka Ashania Mission)

Sujol is a brand and business concept that aims to deliver clean, safe and tasty drinking water to the

poor in Bangladesh. Sujol takes a market-based approach. It is set up as a social enterprise and aims

to produce water without any subsidy at all. Local entrepreneurs will invest in and operate small-

Project number 2526 39

scale plants and sell water to the local communities. Sujol offers entrepreneurs use of the CapDI

technology, (produced by Dutch based Voltea, a Unilever spin-off), which improves both the quality

and taste of salty shallow well water.

This project faced challenges during the pilot phase (2011-2014):

Local partners in Bangladesh are less interested to run relatively small projects

It is hard to capture knowledge within the team as staff changes jobs regularly

The bad condition of roads and the occurrence of many power breaks hamper operational business

The harsh political situation and many strikes hamper good management of the local operation

Project number 2526 40

3.5 Drivers and bottlenecks

Companies and NGOs being part of the web survey identified the access to finance and the ability to

find the right partners as the main bottlenecks for entering the market (figure below).

Figure 135 Top 5 challenges for scaling up activities in Bangladesh for companies

and NGOs, in % of respondents (more answers possible)

Source: Web survey Panteia, 2014/2015

These observations match the overall findings within the scope of 12 Water OS countries to a large

extend. More specifically existing market research and observations of EKN identify the following

market barriers:

The lack of governance and transparency in policy, trade regulations and in procurement practices,

e.g. import duties tend to change annually and range between manufacturing and raw inputs from

0-5% till finished products up to 25%26.

The lack of forum for private sector to engage in a dialogue/discussions with the public sector,

together with a tough enforcement of contracts.

Poor infrastructure like inadequate availability of energy, continuous disruptions of main ports,

and frequent strike actions hamper businesses and projects in executing activities

According to EKN, price competition, Dutch firms are being perceived as relatively. Most tariffs are

too low to cover O&M leaving less room for investments, this leads to a strong focus of GoB on

lowest price when tendering work.

Working with relatively weak counter parts (in particular financially) and the level of knowledge

and experience, puts pressure on a continuous delivery of quality which in general is one of the

USPs of the Dutch water sector.

26 Exploring the Water Sector in Bangladesh. Trends, opportunities and practical information, Nyenrode University, 2014

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

get to financial rescources

realisation of the right contacts

formation of strategic alliances with same partners

improvement of current results

formation of temporarily coalitions

get to institutional funding voor progamme management and coordination

get to local financial rescources for implementation

finding the right partners

scaling up current programmes

formation of strategic alliances with same partners

Top 5 Challenges Companies (N=47)

Top 5 Challenges NGOs (N=13)

Project number 2526 41

On the other hand, specific market incentives exist, not specifically for the water sector, but more in

general:

Bangladesh has one of the most liberal investment climates in the region, no distinctions are being

made between foreign and domestic private investors, 100% foreign equity and full repatriation of

capital are allowed.

So called EPZs (economic zones) provide a diversified and flexible package of investment options

Tax agreements with The Netherlands avoiding double taxation.

Setting up a JV is quite easy.

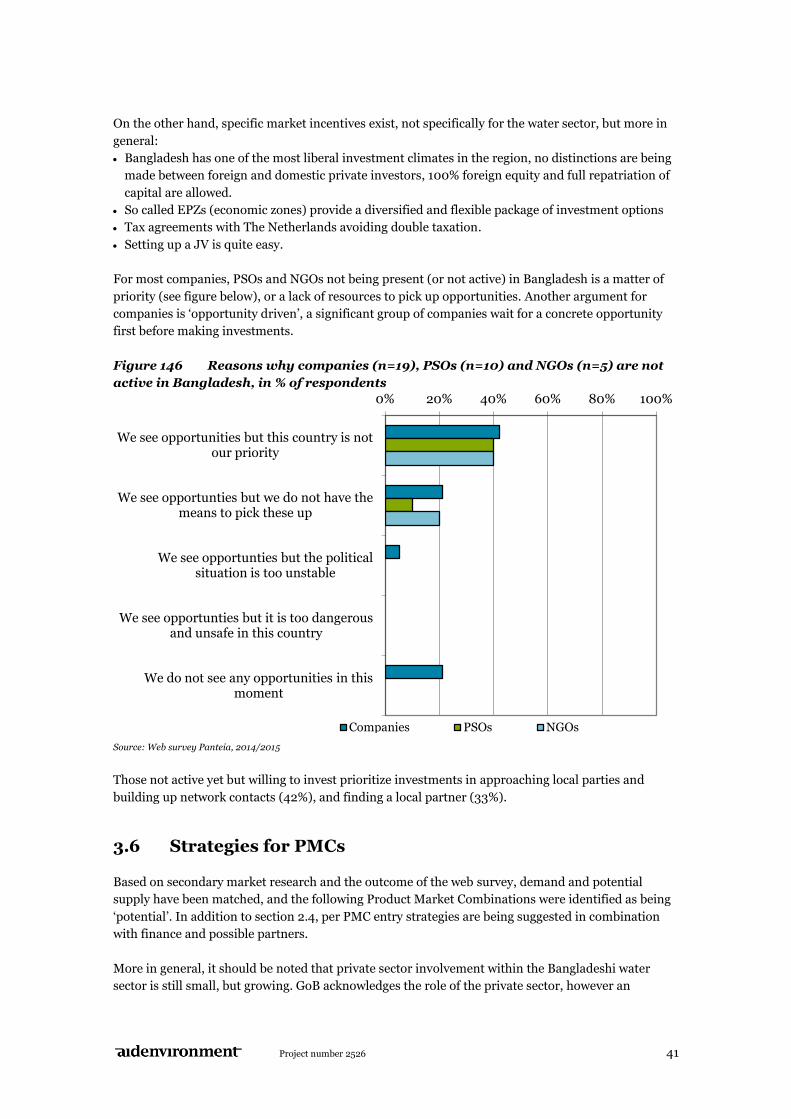

For most companies, PSOs and NGOs not being present (or not active) in Bangladesh is a matter of

priority (see figure below), or a lack of resources to pick up opportunities. Another argument for

companies is ‘opportunity driven’, a significant group of companies wait for a concrete opportunity

first before making investments.

Figure 146 Reasons why companies (n=19), PSOs (n=10) and NGOs (n=5) are not

active in Bangladesh, in % of respondents

Source: Web survey Panteia, 2014/2015

Those not active yet but willing to invest prioritize investments in approaching local parties and

building up network contacts (42%), and finding a local partner (33%).

3.6 Strategies for PMCs

Based on secondary market research and the outcome of the web survey, demand and potential

supply have been matched, and the following Product Market Combinations were identified as being

‘potential’. In addition to section 2.4, per PMC entry strategies are being suggested in combination

with finance and possible partners.

More in general, it should be noted that private sector involvement within the Bangladeshi water

sector is still small, but growing. GoB acknowledges the role of the private sector, however an

0% 20% 40% 60% 80% 100%

We see opportunities but this country is not our priority

We see opportunties but we do not have the means to pick these up

We see opportunties but the political situation is too unstable

We see opportunties but it is too dangerous and unsafe in this country

We do not see any opportunities in this moment

Companies PSOs NGOs

Project number 2526 42

effective platform supporting a public-private sector dialogue is still lacking. Being the third largest

investor, The Netherlands would benefit from such platform.

Besides the lack of a platform for dialogue, the long tradition of public sector involvement has created

market distortion and inefficiency. To enhance private sector participation the main bottlenecks

should be addressed: 1) the lack of integrated sector strategies and investment master plans, 2) the

lack of an effective PPP policy and framework, 3) the lack of awareness and political will to increase

service fees in such way OandM costs will be recovered, and 4) ‘unfair’ procurement and tendering.

Assessing the buying power of clients and profound (financial) risk mitigation are important aspects

of the market entry strategy in Bangladesh. Service and work providers largely depend on public or

international funding (IFIs), providers of goods and products depend on the strength of their

counterpart (private sector partner), especially the financial strength is an important factor to

consider (MM). When exporting to Bangladesh, common risk mitigation measures like export credit,

bank guarantees, and letters of credit are applicable.

Participating in tenders is a traditional way to get business, however tender processes are not always

transparent, require local presence (contacts), a clear integrity policy and sufficient resources (to

manage long bidding processes) to maintain a strong business development capacity in a very

competitive market . Especially for Dutch consultancy firms, this route to the market seems to be

effective. Joint bidding with some of the bigger international firms should not be excluded as a piece

of the cake may be more attractive than no cake at all.

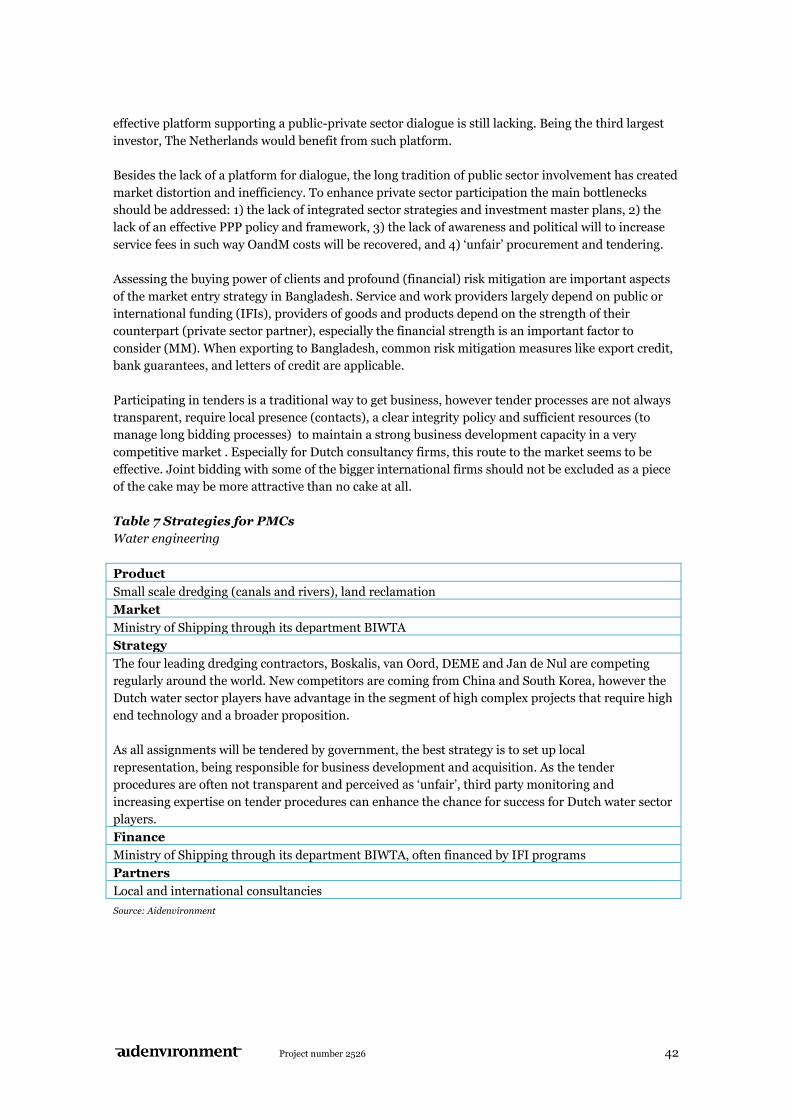

Table 7 Strategies for PMCs

Water engineering

Product

Small scale dredging (canals and rivers), land reclamation

Market

Ministry of Shipping through its department BIWTA

Strategy

The four leading dredging contractors, Boskalis, van Oord, DEME and Jan de Nul are competing

regularly around the world. New competitors are coming from China and South Korea, however the

Dutch water sector players have advantage in the segment of high complex projects that require high

end technology and a broader proposition.

As all assignments will be tendered by government, the best strategy is to set up local

representation, being responsible for business development and acquisition. As the tender

procedures are often not transparent and perceived as ‘unfair’, third party monitoring and

increasing expertise on tender procedures can enhance the chance for success for Dutch water sector

players.

Finance

Ministry of Shipping through its department BIWTA, often financed by IFI programs

Partners

Local and international consultancies

Source: Aidenvironment

Project number 2526 43

Table 8 Strategies for PMCs

Waste Water Treatment

Product

Small scale water treatment plants for agriculture and industrial wastewater (B2B)

Market

Ready Made Garment Sector (Tier 1 companies)

Strategy

Capacity building: by creating a center of expertise first, followed by a demonstration site.

Part of the PaCT program is a Textile Technology Business Center. The Textile Technology Business

Center (TTBC) supports the textile sector in adopting best practices and technologies that improve

business and environmental sustainability.

The tier 1 companies seem to be the best entry point for making deals. Tier-1 Factories are usually

inside the ‘compliance net’ of buyers and hence obliged to align their policy and activities to comply

with the corporate values of their buyer brands.

The propositioning of the Dutch water sector can be enhanced by extensive lobby from EKN and

other important donors to improve enforcement of legislation, and advocacy (e.g. sponsoring of

research, studies) towards raising tariffs that are needed to recover the operational costs.

Finance

Dutch private sector contributions matched by grants (Partners for Water, IFC PaCT).

Partners

PaCT partners (especially TNO being responsible for the set up of the TTBC), Bangladesh Garment

Manufacturers and Exporters Association (BGMEA), Local Government Bodies, NGOs

(International and Local), DWASA.

Source: Aidenvironment

Project number 2526 44

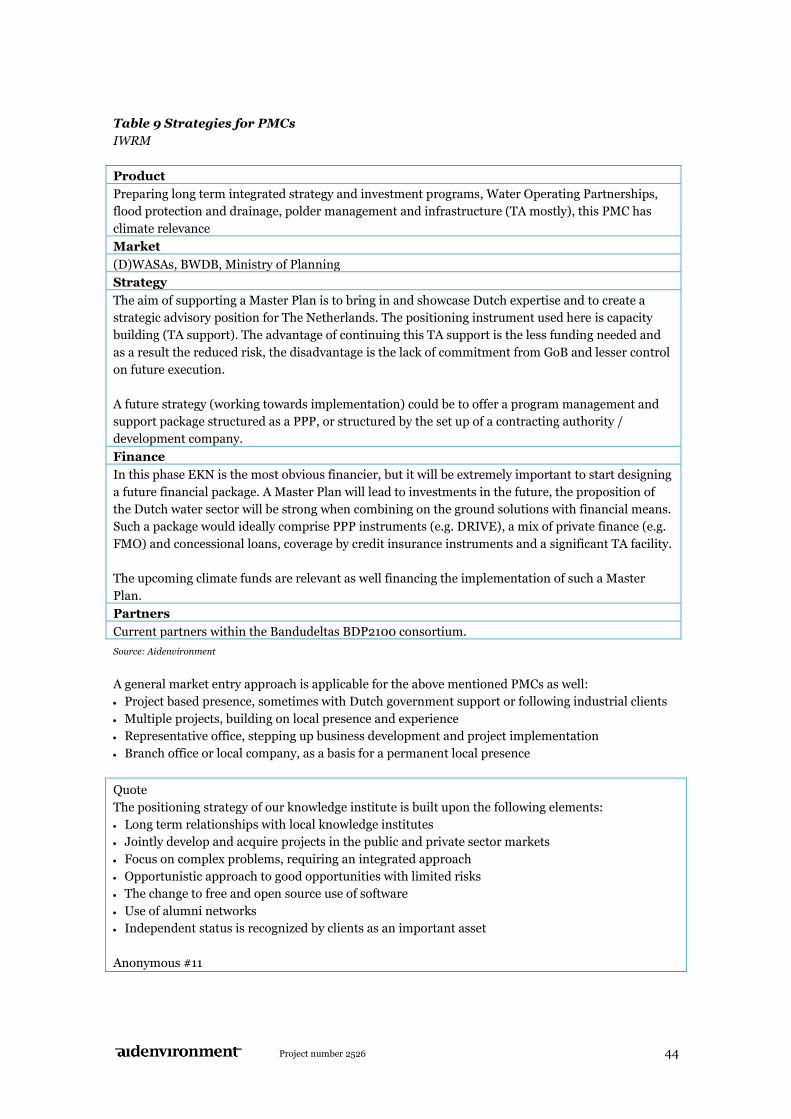

Table 9 Strategies for PMCs

IWRM

Product

Preparing long term integrated strategy and investment programs, Water Operating Partnerships,

flood protection and drainage, polder management and infrastructure (TA mostly), this PMC has

climate relevance

Market

(D)WASAs, BWDB, Ministry of Planning

Strategy

The aim of supporting a Master Plan is to bring in and showcase Dutch expertise and to create a

strategic advisory position for The Netherlands. The positioning instrument used here is capacity

building (TA support). The advantage of continuing this TA support is the less funding needed and

as a result the reduced risk, the disadvantage is the lack of commitment from GoB and lesser control

on future execution.

A future strategy (working towards implementation) could be to offer a program management and

support package structured as a PPP, or structured by the set up of a contracting authority /

development company.

Finance

In this phase EKN is the most obvious financier, but it will be extremely important to start designing

a future financial package. A Master Plan will lead to investments in the future, the proposition of

the Dutch water sector will be strong when combining on the ground solutions with financial means.

Such a package would ideally comprise PPP instruments (e.g. DRIVE), a mix of private finance (e.g.

FMO) and concessional loans, coverage by credit insurance instruments and a significant TA facility.

The upcoming climate funds are relevant as well financing the implementation of such a Master

Plan.

Partners

Current partners within the Bandudeltas BDP2100 consortium.

Source: Aidenvironment

A general market entry approach is applicable for the above mentioned PMCs as well:

Project based presence, sometimes with Dutch government support or following industrial clients

Multiple projects, building on local presence and experience

Representative office, stepping up business development and project implementation

Branch office or local company, as a basis for a permanent local presence

Quote

The positioning strategy of our knowledge institute is built upon the following elements:

Long term relationships with local knowledge institutes

Jointly develop and acquire projects in the public and private sector markets

Focus on complex problems, requiring an integrated approach

Opportunistic approach to good opportunities with limited risks

The change to free and open source use of software

Use of alumni networks

Independent status is recognized by clients as an important asset

Anonymous #11

Project number 2526 45

Appendix I: Methodology

The Water OS positioning survey is part of the Water OS program: a facility of the Ministry of

Foreign Affairs. The Water OS program aims at providing support to the Dutch Embassies in 12

partner countries in the formulation and implementation of their water programs. Central element of

the program is the involvement of the Dutch water sector, i.e. companies, NGOs, knowledge

institutes and governmental organizations.

In order to generate more evidence for effective continuation of the Water OS Program and to

‘trigger’ Dutch water sector players, RVO contracted Aidenvironment, in collaboration with Panteia,

Chris Engelsman and Jan Oomen, to conduct a “Positioning Survey”. This survey identifies

opportunities, strategies and approaches for the Dutch water sector, and more specifically seeks high

potential Product/Market Combinations (PMCs) in the 12 Water OS countries included in the Survey.

The final deliverables of the survey are twelve positioning survey reports (one for each country) and

one overarching management summary. Primary target group for the Positioning Survey Reports are

the Technical Experts (TDs) at the Netherlands Embassies in the 12 OS countries, with all Dutch

water sector players as secondary target group.

The methodology comprises desk research, a web survey and additional strategic interviews:

The desk research studied the most essential reports and documents per country (market scans,

market reports, strategic papers of Embassies and International Financial Institutions). The Key

Advisors within the Water OS program played an important role in rendering accessible and

prioritizing the data available.

In the period November 2014 – January 2015, Panteia carried out a web survey. Two different

questionnaires have been applied, one for companies, knowledge institutions and water boards,

and another questionnaire for NGOs. Despite the length of the survey and thanks to a considerable

effort of the project team and NWP, the response rates were not disappointing and for a web survey

in general above average: NGOs: 16 out of 48 implying a response rate of 33,3%, and companies

(including knowledge institutions and water boards): 87 out of 531 implying a response rate of

16,4%.

Based on the outcomes of the desk study and web survey, Aidenvironment selected 27 companies, 3

(semi) commercial financiers, 7 NGOs, and 8 knowledge institutes (including Water Boards

(‘waterschappen’) and water service providers) to be interviewed on strategic topics focusing on

market opportunities and applicable market entry strategies (and business models). Through these

strategic interviews, the research team gained more detailed information on projects of front

runners. These projects gave more information on lessons learned, success factors, and

opportunities for up scaling.

Regarding the web survey, two important remarks can be made:

Value and limitation of the survey results

The web survey results have provided very useful data for this study. The value of the results

especially lies in the provision of relative figures on various aspects enabling comparisons between

countries, opportunities, bottlenecks, groups or respondents, etc. and to monitor the developments in

these figures over time. The limitation of the study lies in the inability to provide reliable absolute

figures on for instance turnover values.

OS-study versus WEX

For the web survey a similar methodology has been applied as is done for the WEX (Water Export

Index) – study, which is carried out twice a year. A sample of companies and institutions is asked to

provide data on national and export turnover in the water sector and the division of this turnover

Project number 2526 46

over regions and over subsectors. The samples do not have the same composition. Also over time the

samples may differ in the WEX, but never provide a bottleneck though to assess the WEX and to

make reliable comparisons over time. Like in the WEX, the estimation of the export turnover is based

on the sample results of a survey. Starting from this value relative export shares of the various

regions and countries have been determined for the sample. Since the sample may not represent the

whole water sector in an optimal way, we cannot draw any hard or general conclusions about the

export turnover figure and division of this figure over subsectors, regions and countries. The real

value will be higher, but this value can only be obtained with sample results once the whole

population is known. Getting to know the population is difficult and cannot be realized in the context

of this study nor in the WEX-study. Another complicating factor for generalizing study results lies in

the fact that large projects (especially those in water construction) may influence total and regional

export figures drastically and lead to large fluctuations over time. For the sample of the web survey

no such ‘disturbing’ projects have been found. The sample results of the OS-study regarding relative

export shares of regions are in line with the results of the WEX 2014.

The average budget per country positioning report is EUR 7,000. Therefore, the positioning survey

cannot be seen as a fully fledged market research. An in-depth assessment of the markets (the OS

Water countries) was not part of this research, instead the research relied on secondary information

(reports available) and expert opinions (Key Advisors Water OS program, TD staff on Embassies,

YEP network, and a network of ‘water professionals’).

An important disadvantage of the web survey – in contrast with a telephone survey for which a

stratified sample has been selected - is that the characteristics of the total population are unknown.

By lack of a stratified sample, the outcome of the web survey does not offer the opportunity to level

up the sample results to the total population and to calculate absolute figures for turnover and export

volumes for each subsector and region. Despite this limitation of the web survey, it does provide very

useful information for the positioning studies.

Additionally to the country specific positioning reports, a management summary was drafted. The

management summary elaborates on the overall findings and provides overall conclusions.

Project number 2526 47

Appendix II: Finance

The Dutch Government is able to support activities performed by the water sector in developing

countries (in this case the 12 Water OS countries) in different ways. On a strategic level, financial

support can be labeled as:

Bilateral support (country to country)

Multilateral support (to different countries often funneled through International Financial

Institutes or UN related organizations)

Specific instruments (e.g. managed by RVO or commercial organizations like Atradius and FMO)

The financial support from Dutch Government related to the 12 Water OS countries aims to combine

trade and aid perspectives. The policy focuses on three key points: 1) improved management of water

catchments and safe deltas, 2) efficient use of water, especially in the agriculture sector, and 3)

improved access to clean drinking water and sanitation.

This appendix provides an overview of the support provided on different strategic levels: bilateral,

multilateral and specific instruments. The content is structured following the most important

organizations involved in funneling these funds starting with the Ministry of Foreign Affairs, The

Dutch Embassies, RVO, Dutch (Semi) Commercial Players, and the most relevant International

Finance Institutes. At the end, the appendix provides a non exhausted list of foundations financing

water related projects and activities.

Centralized programs managed by IGG/Water DGIS/Ministry of Foreign Affairs

DGIS (within the Ministry of Foreign Affairs) focuses on the Dutch international cooperation with

partnering countries. The cooperation involving the water sector is mandate of the section water

within the department of DME (future: IGG (Inclusive Green Growth)). This section manages the

water related portfolio of programs providing regional and multilateral support. The funding is often

labeled and does not provide direct opportunities for the Dutch water sector.

Decentralized programs managed by Embassies:

The Multi Annual Strategic Plans (MASP) is the nucleus of Dutch bilateral support to a country.

Projects, programs or businesses being part of the Embassies’ program to implement the MASP fit

into the country specific strategy and are aligned with the overall water policy of Dutch government.

The funding of Dutch Embassies provides opportunities for the Dutch water sector.

Specific Instruments: RVO

RVO has developed different type of instruments depending on the phase the

project/program/business is in, starting at the development of an idea, testing the concept in a pilot,

scaling up the pilot to significant size to start building a business or self financing project on. We

follow this structure when presenting the different instruments.

To finance the development of an idea, innovation or R&D:

VIA water:

This is a relatively small fund (EUR 10 million over 4 years) to finance out of the box ideas and small-

scale innovations using grants. Aqua for all manages the fund, which started operating in 2015.

Maximum size of the grant is EUR 200,000 per project.

Project number 2526 48

To finance a pilot:

Partners for Water:

This is a funding program (grants) financed by different Ministries runs from 2010 till 2014. After

2015 the program will continue following the same strategy. In 2015 the facility is not open for new

application. The program financed 80 projects of which 50 included a pilot. The average subsidy size

was EUR 200,000 financing 20-80% of the budget. The new program will start with a total budget of

EUR 10.5 million.

DHK:

This instrument provides grants and aims to finance demonstration pilots, feasibility studies and

acquiring of knowledge. The program has a specific EUR 3 million window for DGGF countries of

which EUR 1 million is allocated to the least developed countries. This facility is specifically

applicable for projects in fragile states.

DRR:

DRR finances the Dutch Risk Reduction Team, a database of Dutch Water Experts that are available

for solving water related issues with respect to disasters. DRR is not a facility financing disaster

response or aid, though DRR provides knowledge that can be used to e.g. avoid disasters. RVO in

close cooperation with NWP manages the facility.

To finance the scale up of activities or pilots:

ORIO / DRIVE:

ORIO was cancelled in 2014. ORIO used to be a grant facility financing investments related to the

development, implementation and operation of infrastructure in developing countries. Governments

of these countries submit the applications and the private sector is involved in the development and

execution of projects.

DRIVE is the successor of the ORIO program and provides concessional loans to governments of

developing countries to develop, construct and operate infrastructure. DRIVE will be launched in

April 2015 and has an available budget of EUR 100.000.000 annually expecting to finance 10-15

projects. The facility aims to actively involve the Dutch Water sector and contribute to development

of the receiving country.

G4AW:

G4AW stands for Geodata for Agriculture and Water and finances projects, programs and businesses

aiming to improve food security in developing countries by using satellite data. Netherlands Space

Office (NSO) is executing this program, commissioned by the Dutch Ministry of Foreign Affairs. In

2014-2015 the facility has EUR 30.5 million available to provide grants (EUR 0.5-5.0 million)

financing up to 70% budgets. Proposals and partnerships should be based on a business plan geared

towards satellite data at the start of the information chain.

FDW/FDOV and GWW:

RVO developed three facilities to finance Public Private Partnerships (PPP) in the water (and

agriculture) sector. These facilities aim to: 1) increase access to drinking water and sanitation, 2)

enhance efficient and sustainable water use (especially in the agriculture sector), 3) improve

management of catchment areas and safe deltas, and 4) (specifically for FDOV) improve food security

and private sector development. GWW (Ghana Wash Window) is a specific window financing water

related PPPs in Ghana.

Project number 2526 49

The three facilities are in place since 2012, in 2014 FDW and FDOV launched and closed its second

call, the GWW second call for proposals closes in February 2015. The facilities are planning the third

call to be executed in 2016. Because the facilities just started operating, (impact) results have not

been reported yet.

The facilities provide grants and have different modalities. The facilities received many applications

and resulted into the finance of new initiatives. The application process is being perceived by a

significant group of applicants as complex, and requires a clear business case, or theory of change

aiming to enhance the enabling environment as part of the proposal, plus a significant contribution

by the private sector. The facilities are especially applicable for large applications fitting into

investment agenda’s or strategic objectives of the private sector players involved.

DGGF:

The Dutch Good Growth Fund started operations in mid 2014 and aims to combine aid and trade

goals. DGGF is a revolving fund, providing finance (not grants) to initiatives with a ‘healthy risk

profile’. DGGF focuses on 66 countries (called the DGGF countries), including the Water OS

countries. DGGF is build on three pillars: 1) a fund financing activities of Dutch SMEs in DGGF

countries (managed by RVO), 2) a fund financing local SMEs and banks in DGGF countries

(managed by PWC and Tripple Jump), and 3) a fund financing export credit insurance and export

finance activities (managed by Atradius).

In Pillar 1, RVO works closely together with Dutch banks. The fund is equipped to provide guarantees

to banks up till 60% of the credit risk, loans to banks and investment funds (equity). The maximum is

EUR 10 million per project or business. A TA facility will be in place to provide assistance on

improvement of the business plan or investment proposal.

Pillar 2 is under construction; this pillar will provide fund to fund investments up to EUR 175,000.

Pillar 3 provides export credit insurances covering non-market risks up till a maximum claim amount

of EUR 15 million. Besides insurances, this fund provides export finance instruments. Products focus

on Dutch SMEs needs, covering small and large transactions.

Besides these above mentioned programs and facilities, the following instruments can

be useful and applicable for financing water related activities.

PSI:

PSI was grant program available for non-Dutch and Dutch companies wishing to make an innovative

investment, in cooperation with a local partner in one of the PSI countries. This program stopped

operating mid 2014.

MMF:

MMF is a match making program, aiming to establish a long term business relationship between a

Dutch entrepreneur and an entrepreneur from a developing country.

OS Partner Countries:

This program finances the projects, managed by the local Dutch Embassies. These projects fit into the

Multi Annual Strategic Plans of the specific Embassies.

TDs / economic diplomacy:

Project number 2526 50

This program finances the so called thematic experts working at the Dutch Embassies in a limited

number of OS Partner Countries.

TMEA:

Managed by DDE / DGIS, this large program focuses on the East African region financing initiatives

contributing to the enhancement of trade relations within the region. The facility is applicable for

financing initiatives linked to port development.

Water Mondiaal:

Water Mondiaal is a program launched by the Dutch government to cooperate actively with countries

in low-lying delta areas, protecting them against floods and ensuring sufficient, clean water. Partners

for Water is managing this program, the program aims creating long lasting cooperation agreements

between the public and private sector , and civil society and knowledge institutes. Water Mondiaal

focuses on five deltas: Egypt, Bangladesh, Indonesia, Mozambique and Vietnam.

(Semi) Commercial Organizations managing funds on behalf of Dutch Government

The following facilities or organizations are in some way closely linked to RVO or the Ministry of

Foreign Affairs.

Atradius:

Atradius offers a comprehensive range of credit management solutions that protect businesses of all

sizes against the commercial and political risks inherent in domestic and global trade. Atradius

provides credit insurance, debt collection services, bonding, reinsurance and a range of special

products.

Atradius Dutch State Business performs different facilities on behalf of and for account of the Dutch

State. There is no direct link with the RVO organization, though Atradius products can be combined

with RVO instruments (e.g. ORIO/DRIVE).

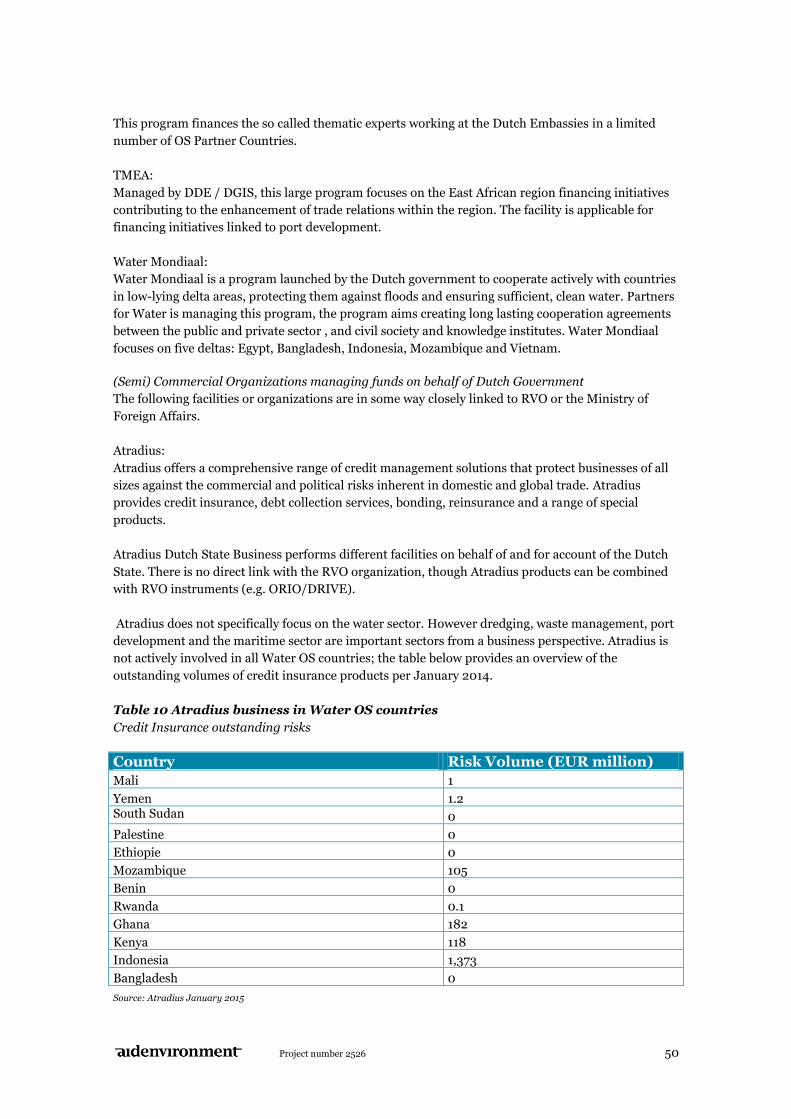

Atradius does not specifically focus on the water sector. However dredging, waste management, port

development and the maritime sector are important sectors from a business perspective. Atradius is

not actively involved in all Water OS countries; the table below provides an overview of the

outstanding volumes of credit insurance products per January 2014.

Table 10 Atradius business in Water OS countries

Credit Insurance outstanding risks

Country Risk Volume (EUR million)

Mali 1

Yemen 1.2 South Sudan 0

Palestine 0

Ethiopie 0

Mozambique 105

Benin 0

Rwanda 0.1

Ghana 182

Kenya 118

Indonesia 1,373

Bangladesh 0

Source: Atradius January 2015

Project number 2526 51

Atradius manages the third pillar of DGGF. In the first six months Atradius received 7-8 requests,

one of these came from the maritime sector. The DGGF facility provides support on smaller

transactions; therefore this product is applicable for Dutch small and medium enterprises.

FMO:

FMO manages three funds relevant for the Dutch water sector.

FOM-OS

The first pillar of the DGGF program will replace this fund. The fund offered loans to private sector

players investing in non (commercially) bankable projects or businesses in developing countries.

Innovative Finance Fund for Development

This fund aims to catalyze private sector investments.

IDF

IDF stands for Infrastructure Development Fund. The IDF is aimed at creating reliable infrastructure

in many sectors, ranging from potable water and mobile telecommunication services to roads and

power. By providing risk capital through the IDF, FMO takes on definite risk while acting as a

gateway for other financers.

IDF offers finance through equity, mezzanine and debt products that can be used even in early stage

of projects. The fund has the following fund limits:

Individual transaction amounts maximized at EUR 25 million

Financing about 25% of total project investment

Shareholding maximum 25%

Maximum tenor of 20 years

Convertible contributions are selectively available for financing during the development phase of

projects (up to 49% of total development cost)

About 8% of the portfolio is allocated to water related projects (mainly water related to energy:

dams). IDF hardly finances projects in other sub sectors of the water sector, this is due to: 1) the

limited willingness to pay (drinking water), 2) the strong involvement of a weak public sector, 3) the

limited role of the private sector, 4) the lack of involvement by Dutch water sector as a strategic

operator or investor.

Within the FMO organization the department NL Business manages the IDF fund and provides

(financial) transaction advisory support to Dutch businesses aiming to become active in developing

markets. NL business brings in the financial perspective when Dutch businesses want to develop a

consortium. Regarding consortium development within the Dutch water sector, port development,

dredging and waste (water) treatment are potential sectors. Thinking along the lines of so called

corridor concepts (infrastructure connection points like transfer utilities) seems to be a promising

market entry point.

EP - Nuffic:

EP-Nuffic is the main expertise and service centre for internationalization in Dutch education, from

primary and secondary education to higher professional and academic higher education and

research. EP – Nuffic runs several programs, the NICHE program is relevant for the water sector.

The Netherlands Initiative for Capacity development in Higher Education (NICHE) is a Netherlands-

funded development cooperation program. By sustainably strengthening higher education and

Project number 2526 52

technical and vocation education and training (TVET) capacity in partner countries, it contributes to

economic development and poverty reduction. The program focuses on four policy priorities: 1)

Water, 2) Food security, 3) Sexual and Reproductive Health and Rights (SRHR) and 4) Security and

the rule of Law.

Dutch Commercial Banks:

Looking at the global networks of the larger Dutch international operating banks (ABN AMRO, Rabo

bank and ING), the Rabobank has the most visible overall presence in the 12 Water OS. In the

strategic interviews, this bank was the only commercial bank mentioned a couple of times as being

active in the international water sector.

The water sector is not a specific priority sector for Rabobank. From an international perspective

Rabobank focuses on the agriculture sector. However Rabobank is involved in financing the Dutch

water sector in The Netherlands. From this perspective, Rabobank ‘follows its clients abroad’

(especially the dredging and water engineering sector plus larger consultancies are being mentioned).

Rabobank has branches in Kenya and Indonesia, participations in Rwanda and Mozambique and

operates in partnership with e.g. Standard Charter Bank in Mali, Ghana, and Bangladesh.

Export finance, guarantees and currency risk management are the most common services/products

offered to international operating clients.

International Financial Institutes (IFIs):

The so-called multilateral aid program of governments is being managed by IFIs like the Worldbank,

ADB, AfDB and EU (EU grant program and EIB). The following IFIs play an important role financing

water sector related projects, programs and businesses.

World Bank (WB):

In 2014 WB announced reorganization. The new structure has five relevant departments focusing on

water: GP14 Water, GP1 Agriculture, GP3 Energy and Extractives, GP 4 Environment and Natural

Resources, GP12 Transport and ICT, and GP13 Urban and Rural Social Development.GP14 Water

department integrates WASH, irrigation, and Water Resource Management. One global staff pool is

in place to partner with outside organizations. More weight is put on knowledge into operations. WB

offers loans to developing countries, projects have to fit the multiyear WB strategy, and the fund

receiving countries lead the tender procedure. About 20% of the annual budget is allocated to water

projects of which 53% WASH, 13% irrigation, 24% water and energy, and 10% flood protection and

delta technology.

The Asian Development Bank:

Programs of ADB are complementary to other donors and have the starting point to promote

inclusive water policies (including the poor). Focus on mainstreaming water efficiency in supply and

use and enhanced cooperation with the private sector. From 2010-2020 the budget is USD 20-25

billion.

The African Development Bank (AfDB):

Looking at the AfDB strategy 2013-2022 paper, the 10 year focus will be on inclusive growth and

green growth. The bank identifies five operational priorities: 1) infrastructure development, 2)

private sector development, 3) governance and accountability, 4) regional economic integration, and

5) skills and technology. In implementing its ten-year Strategy, the Bank will pay particular attention

to fragile states, agriculture and food security, and gender. Supporting the water sector is specifically

part of the agenda on infrastructure and agriculture and food security.

Project number 2526 53

In view of its important contribution to the achievement of all the MDG goals and therefore its

unique contribution to poverty reduction on the continent, the water sector has received major

attention as a strategic priority of the Bank. Since 2000, following the adoption of its Integrated

Water Resources Management (IWRM) Policy, the Bank has increased its focus on the water sector,

especially on drinking water, sanitation and hygiene, and the promotion of integrated management

of water resources.

The African Water Facility is an interesting facility that can be used to finance WASH related

activities.

The EU:

These funds are the main source of EU development aid for the African, Caribbean and Pacific (ACP)

countries and the overseas territories (3% of the annual EU budget in 2008-13). The funds are

connected to the Cotonou Treaty. The European Investment Bank invests significant amounts in the

water sector. The grant programs do not have a specific focus on water related projects, the EU Water

Facility, one of the grant programs focusing specifically on water will be cancelled.

Foundations:

Especially for development related activities within the water sector, foundations provide interesting

opportunities to finances projects and programs. Below an unexhausted list of foundations provides a

first entry point to seek for funds. As each foundation has its own finance policy, we refer to the

individual websites for more information.

Blood:Water.

Blue Planet Network Foundation

Charity Water

ExxonMobil Foundation

Global Water Challenge

Millennium Water Alliance

Project Concern International

ActionAid International USA

Alcoa Foundation

Boeing Company Charitable Trust

BP Foundation

Global Green USA

Habitat For Humanity International, Inc.

Lemelson Foundation

McKnight Foundation

Prem Rawat Foundation

Water 1st International

Water Environment Research Foundation

Wateraid America, Inc.

World Vision, Inc.

Project number 2526 54

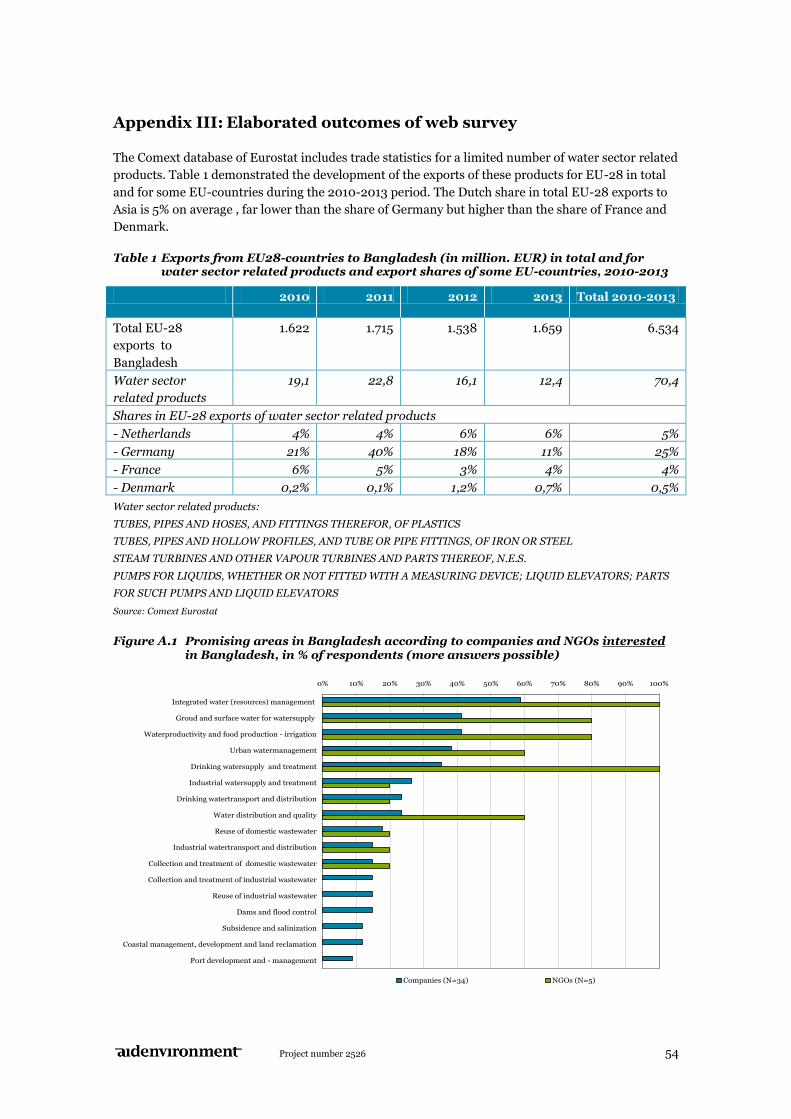

Appendix III: Elaborated outcomes of web survey

The Comext database of Eurostat includes trade statistics for a limited number of water sector related

products. Table 1 demonstrated the development of the exports of these products for EU-28 in total

and for some EU-countries during the 2010-2013 period. The Dutch share in total EU-28 exports to

Asia is 5% on average , far lower than the share of Germany but higher than the share of France and

Denmark.

Table 1 Exports from EU28-countries to Bangladesh (in million. EUR) in total and for

water sector related products and export shares of some EU-countries, 2010-2013

2010 2011 2012 2013 Total 2010-2013

Total EU-28

exports to

Bangladesh

1.622 1.715 1.538 1.659 6.534

Water sector

related products

19,1 22,8 16,1 12,4 70,4

Shares in EU-28 exports of water sector related products

- Netherlands 4% 4% 6% 6% 5%

- Germany 21% 40% 18% 11% 25%

- France 6% 5% 3% 4% 4%

- Denmark 0,2% 0,1% 1,2% 0,7% 0,5%

Water sector related products:

TUBES, PIPES AND HOSES, AND FITTINGS THEREFOR, OF PLASTICS

TUBES, PIPES AND HOLLOW PROFILES, AND TUBE OR PIPE FITTINGS, OF IRON OR STEEL

STEAM TURBINES AND OTHER VAPOUR TURBINES AND PARTS THEREOF, N.E.S.

PUMPS FOR LIQUIDS, WHETHER OR NOT FITTED WITH A MEASURING DEVICE; LIQUID ELEVATORS; PARTS

FOR SUCH PUMPS AND LIQUID ELEVATORS

Source: Comext Eurostat

Figure A.1 Promising areas in Bangladesh according to companies and NGOs interested

in Bangladesh, in % of respondents (more answers possible)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Integrated water (resources) management

Groud and surface water for watersupply

Waterproductivity and food production - irrigation

Urban watermanagement

Drinking watersupply and treatment

Industrial watersupply and treatment

Drinking watertransport and distribution

Water distribution and quality

Reuse of domestic wastewater

Industrial watertransport and distribution

Collection and treatment of domestic wastewater

Collection and treatment of industrial wastewater

Reuse of industrial wastewater

Dams and flood control

Subsidence and salinization

Coastal management, development and land reclamation

Port development and - management

Companies (N=34) NGOs (N=5)

Project number 2526 55

Source: Web survey Panteia, 2014/2015

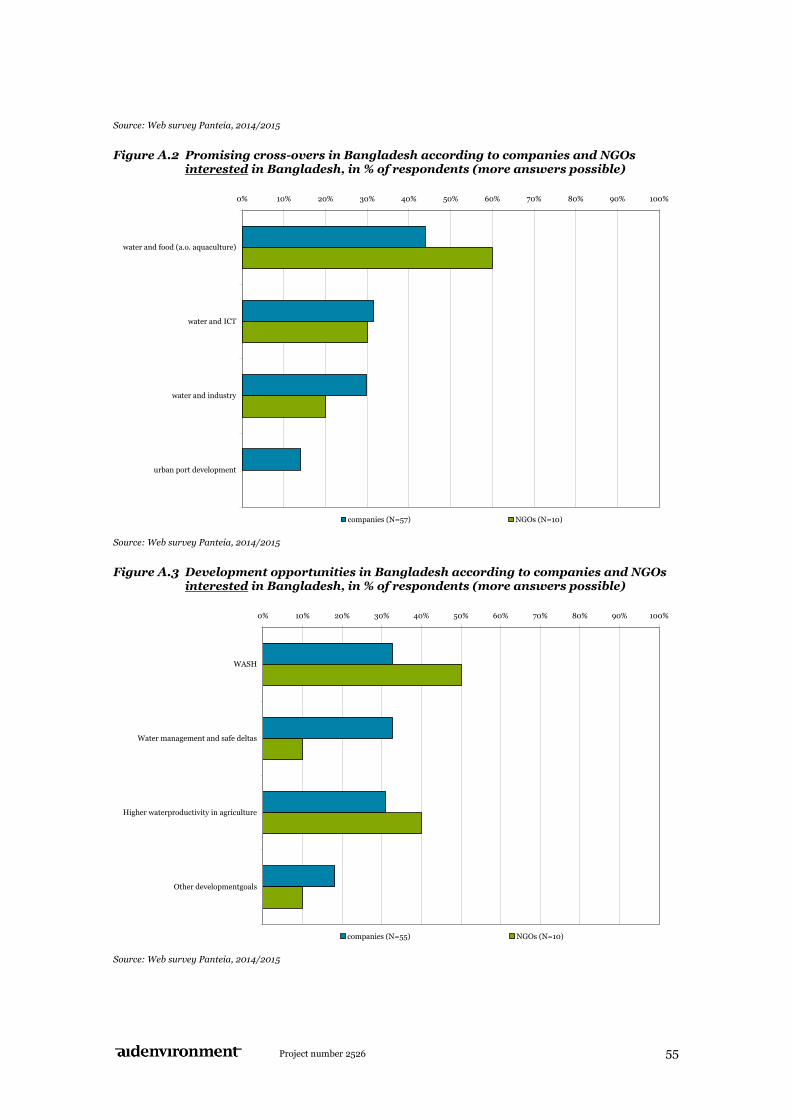

Figure A.2 Promising cross-overs in Bangladesh according to companies and NGOs interested in Bangladesh, in % of respondents (more answers possible)

Source: Web survey Panteia, 2014/2015

Figure A.3 Development opportunities in Bangladesh according to companies and NGOs interested in Bangladesh, in % of respondents (more answers possible)

Source: Web survey Panteia, 2014/2015

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

water and food (a.o. aquaculture)

water and ICT

water and industry

urban port development

companies (N=57) NGOs (N=10)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

WASH

Water management and safe deltas

Higher waterproductivity in agriculture

Other developmentgoals

companies (N=55) NGOs (N=10)

Project number 2526 56

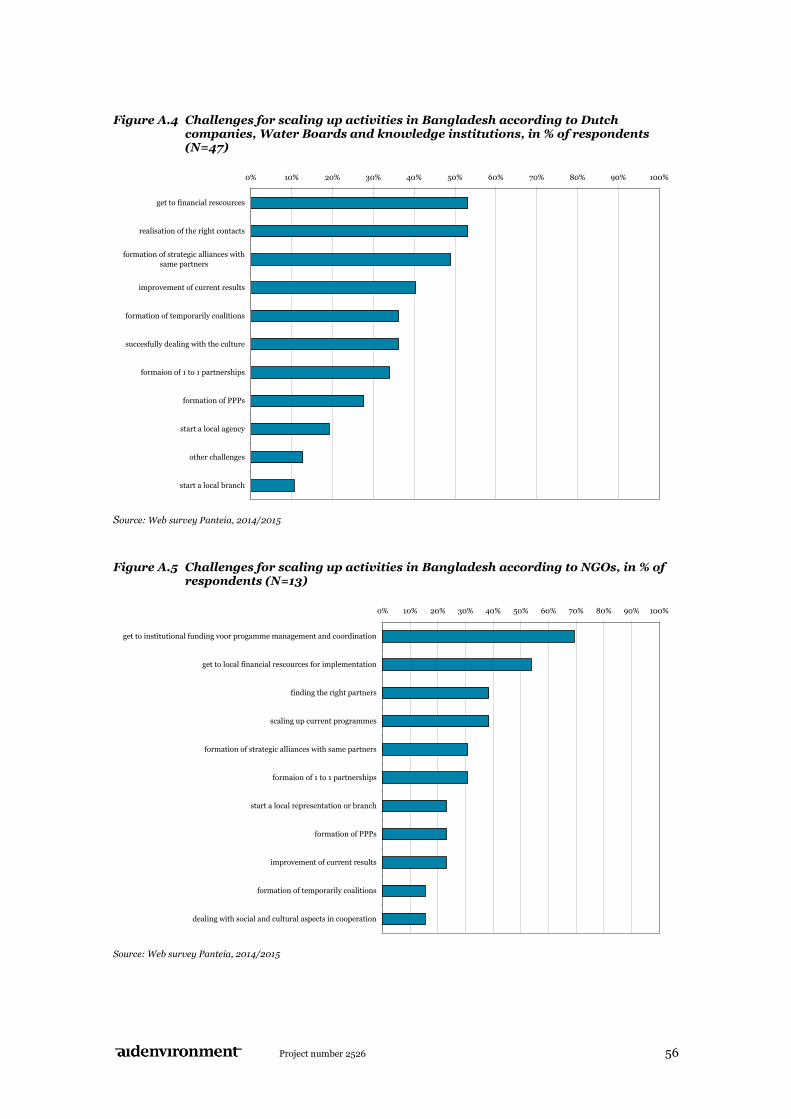

Figure A.4 Challenges for scaling up activities in Bangladesh according to Dutch companies, Water Boards and knowledge institutions, in % of respondents (N=47)

Source: Web survey Panteia, 2014/2015

Figure A.5 Challenges for scaling up activities in Bangladesh according to NGOs, in % of

respondents (N=13)

Source: Web survey Panteia, 2014/2015

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

get to financial rescources

realisation of the right contacts

formation of strategic alliances with

same partners

improvement of current results

formation of temporarily coalitions

succesfully dealing with the culture

formaion of 1 to 1 partnerships

formation of PPPs

start a local agency

other challenges

start a local branch

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

get to institutional funding voor progamme management and coordination

get to local financial rescources for implementation

finding the right partners

scaling up current programmes

formation of strategic alliances with same partners

formaion of 1 to 1 partnerships

start a local representation or branch

formation of PPPs

improvement of current results

formation of temporarily coalitions

dealing with social and cultural aspects in cooperation

Project number 2526 57

Appendix IV: Sources

Exploring the Water Sector in Bangladesh. Trends, opportunities and practical information

Nyenrode University, 2014

Market Scan on the Bangladesh Water Sector

MottMacDonald, 2010

UN-Water Country Brief FAO, 2013