1770 Bank of Hindustan - 1st bank est at Calcutta by British 1806 Bank of Calcutta est => renamed in 1809 as Bank of Bengal 1840 Presidency Bank of Bombay established 1843 Presidency Bank of Madras established 1865 Allahabad Bank established = 1st Indian bank 1895 Punjab Commercial Bank (PNB), est. in Lahore by Indian Merchants = 1st bank purely managed by Indians. 1904 Concept of Co - op Banks introduced by Curzon 1921 Imperial Bank Of India — all Presidency Banks merged by British Govt. — later became SBI 1926 Hilton Young Committee's Report on Central Bank 5 Mar 1934 RBI Act, 1934 - statutory basis 1 Apr 1935 RBI commences ops. Sir Osborne Smith = 1st Governor of Bank. The Bank was constituted as a shareholders' bank. 5 Jul 1935 Scheduled banks reqd to maintain CRR = hold cash balances with RBI - 5% of their Demand Liabilities and 2% of their Time Liabilities. Jan 1938 First Reserve Bank notes issued. 11 Mar 1940 RBI Accounting Year changed from Jan-Dec to July-June 11 Aug 1943 Sir CD Deshmukh assumes office of Governor ( 1st Indian Governor) 12 Jan 1946 High Denomination Bank Notes of Rs 500, Rs 1000 and Rs 10,000 Demonetised to curb unaccounted money. 1 Jan 1949 RBI nationalised 16 Mar 1949 Coming into force of Banking Companies Act, 1949 = statutory basis of bank supervision & regulation SLR introduced for 1st time Banking Companies Act later renamed => Banking Regulation Act. 19 Sep 1949 Rupee devalued by 30.5 % as a defensive measure consequent to devaluation by other 'sterling area' countries. 1 Jul 1955 Imperial Bank of India => state owned, State Bank of India 1959 State Bank of India (Subsidiary Banks) Act, 1959 made the banks of the erstwhile Princely Sates of India the subsidiaries of the State Bank of India. These were The Bank of Bikaner, The Bank of Jaipur, The Bank of Indore. The Bank of Mysore, The Bank of Patiala, The Bank of Hyderabad, The Bank of Saurashtra and The Bank of Travancore were made subsidiaries of The State Bank Of India. The Bank Of Bikaner and The Bank of Jaipur were amalgamated in 1963 to form the State Bank of Bikaner and Jaipur. Feb 1964 Unit Trust of India est to extend facilities for an equity type investment to small investors and also mobilize resources & channel them into investments to facilitate the growth of the economy. 1 Jul 1964 IDBI est as a subsidiary of RBI for providing long term industrial finance. 6 Jun 1966 Rupee devalued by 36.5 % - USD eqt from Rs 4.75 to Rs 7.50 17 Apr 1967 Size of Bank notes reduced. 19 Jul 1969 14 major Indian SCBs with deposits > Rs 50 crores nationalised to serve needs of devpt of economy in conformity with national policy objectives 01 Jan 1970 SDRs created by the IMF to enhance international liquidity. 01 Jan 1974 Foreign Exchange Regulation Act (FERA), 1973 came into force to conserve forex. Its admin entrusted to RBI. 09 Dec 1974 Asian Clearing Union (ACU) est to facilitate payments for current intl trxns on a multilateral basis. Clearing operations were to be denominated in member's currency or AMU which would be eqt to 1 SDR 76 Sep 1975 Regional Rural Banks set up as alternative agencies to provide credit to rural in context of 20 Point Programme 1975 20 point economic programme introduced. 02 May 1977 M. Narasimhan appointed Governor up to Nov 30, 1977. 27 May 1978 Deposit Insurance & Credit Guarantee Corp (DICGC) was formed. 15 Apr 1980 6 private sector banks nationalised 1. Andhra Bank 2. Corporation Bank 3 New Bank of India 4. Oriental Bank of Commerce 5. Punjab and Sindh Bank 6. Vijaya Bank 01 Jan 1982 EXIM Bank of India est to provide comprehensive financial and allied services to exporters and importers. 12 July 1982 B Shivraman Committee => NABARD 16 Sep 1982 Manmohan Singh appointed Governor. Apr 1988 SEBI est to deal with devpt & regulation of securities market & investor protection. Jul 1988 NHB est as an apex body of housing finance and to promote activities in housing development. Mar 1989 Certificates of Deposit (CDs) and Commercial Paper (CPs) introduced in India to widen monetary instruments and Banking System in India Monday, June 17, 2019 12:12 PM Finance Page 1

Transcript

1770 Bank of Hindustan - 1st bank est at Calcutta by British

1806 Bank of Calcutta est => renamed in 1809 as Bank of Bengal

1840 Presidency Bank of Bombay established

1843 Presidency Bank of Madras established

1865 Allahabad Bank established = 1st Indian bank

1895 Punjab Commercial Bank (PNB), est. in Lahore by Indian Merchants = 1st bank purely managed by Indians.

1904 Concept of Co-op Banks introduced by Curzon

1921 Imperial Bank Of India — all Presidency Banks merged by British Govt. — later became SBI

1926 Hilton Young Committee's Report on Central Bank

5 Mar 1934 RBI Act, 1934 - statutory basis

1 Apr 1935 RBI commences ops. Sir Osborne Smith = 1st Governor of Bank. The Bank was constituted as a shareholders' bank.

5 Jul 1935 Scheduled banks reqd to maintain CRR = hold cash balances with RBI - 5% of their Demand Liabilities and 2% of their Time Liabilities.

Jan 1938 First Reserve Bank notes issued.

11 Mar 1940 RBI Accounting Year changed from Jan-Dec to July-June

11 Aug 1943 Sir CD Deshmukh assumes office of Governor (1st Indian Governor)

12 Jan 1946 High Denomination Bank Notes of Rs 500, Rs 1000 and Rs 10,000 Demonetised to curb unaccounted money.

1 Jan 1949 RBI nationalised

16 Mar 1949 Coming into force of Banking Companies Act, 1949 = statutory basis of bank supervision & regulation SLR introduced for 1st timeBanking Companies Act later renamed => Banking Regulation Act.

19 Sep 1949 Rupee devalued by 30.5 % as a defensive measure consequent to devaluation by other 'sterling area' countries.

1 Jul 1955 Imperial Bank of India => state owned, State Bank of India

1959 State Bank of India (Subsidiary Banks) Act, 1959 made the banks of the erstwhile Princely Sates of India the subsidiaries of the State Bank of India. These were The Bank of Bikaner, The Bank of Jaipur, The Bank of Indore. The Bank of Mysore, The Bank of Patiala, The Bank of Hyderabad, The Bank of Saurashtra and The Bank of Travancore were made subsidiaries of The State Bank Of India. The Bank Of Bikaner and The Bank of Jaipur were amalgamated in 1963 to form the State Bank of Bikaner and Jaipur.

Feb 1964 Unit Trust of India est to extend facilities for an equity type investment to small investors and also mobilize resources & channel them into investments to facilitate the growth of the economy.

1 Jul 1964 IDBI est as a subsidiary of RBI for providing long term industrial finance.

6 Jun 1966 Rupee devalued by 36.5 % - USD eqt from Rs 4.75 to Rs 7.50

17 Apr 1967 Size of Bank notes reduced.

19 Jul 1969 14 major Indian SCBs with deposits > Rs 50 crores nationalised to serve needs of devpt of economy in conformity with national policy objectives

01 Jan 1970 SDRs created by the IMF to enhance international liquidity.

01 Jan 1974 Foreign Exchange Regulation Act (FERA), 1973 came into force to conserve forex. Its admin entrusted to RBI.

09 Dec 1974 Asian Clearing Union (ACU) est to facilitate payments for current intl trxns on a multilateral basis. Clearing operations were to be denominated in member's currency or AMU which would be eqt to 1 SDR

76 Sep 1975 Regional Rural Banks set up as alternative agencies to provide credit to rural in context of 20 Point Programme

1975 20 point economic programme introduced.

02 May 1977 M. Narasimhan appointed Governor up to Nov 30, 1977.

27 May 1978 Deposit Insurance & Credit Guarantee Corp (DICGC) was formed.

15 Apr 1980 6 private sector banks nationalised 1. Andhra Bank 2. Corporation Bank 3 New Bank of India 4. Oriental Bank of Commerce 5. Punjab and Sindh Bank 6. Vijaya Bank

01 Jan 1982 EXIM Bank of India est to provide comprehensive financial and allied services to exporters and importers.

12 July 1982 B Shivraman Committee => NABARD

16 Sep 1982 Manmohan Singh appointed Governor.

Apr 1988 SEBI est to deal with devpt & regulation of securities market & investor protection.

Jul 1988 NHB est as an apex body of housing finance and to promote activities in housing development.

Mar 1989 Certificates of Deposit (CDs) and Commercial Paper (CPs) introduced in India to widen monetary instruments and

Banking System in IndiaMonday, June 17, 2019 12:12 PM

Finance Page 1

Mar 1989 Certificates of Deposit (CDs) and Commercial Paper (CPs) introduced in India to widen monetary instruments and give investors greater flexibility.

1 & 3 Jul '91 External Payments (BOP) Crisis. Rupee Devalued in two stages. Cumulative devaluation about 18% in USD terms.

Nov 1991 Narsimhan Committee Report suggested widescale reforms - phased ↓ in SLR & CRR, accounting standards, income recognition norms and capital adequacy norms

Mar 1992 A dual exchange rate system - Liberalised Exchange Rate Management System (LERMS) introduced to enable a transition to a market determined exchange rate system.

22 Dec 1992 C. Rangarajan appointed Governor

1993 Unified Exchange rate

1994 'Committee on Reform of the Insurance Sector', RN Malhotra

3 Feb 1995 Bharatiya Reserve Bank Note Mudran Limited est as a fully owned subsidiary of RBI. Commenced printing of Notes at Mysore on June 1 and at Salboni on Dec 11.

Jun 1995 The Office of Banking Ombudsman est for expeditious & inexpensive resolution of customer complaints related to Banking services.

1 Apr 1997 WMA - RBI & GoI agree to replace system of ad hoc Treasury Bills with Ways and Means Advances ending automatic monetisation of fiscal deficits.

1999 FEMA, 1999 replaces FERA, 1973 - operative from Jun 2000 along with a sunset clause

2008 IDBI Nationalised

2008 NPCI Founded

2010 ICICI acquires Bank of Rajasthan

2012 'RuPay' launched by National Payments Corporation of India.

2013 Bhartiya Mahila Bank formed. 19 November, 2013.

1 April 2017 Associate banks of SBI - State Bank of Bikaner and Jaipur (SBBJ), State Bank of Mysore (SBM), State Bank of Travancore (SBT), State Bank of Hyderabad (SBH) and State Bank of Patiala (SBP) and Bhartiya Mahila Bank Merged with SBI.

Banking licence round= 1993, 2001

History of Banking in India

Presidency bank of Bengal in 1806 •Presidency bank of Bombay in 1840 •Presidency bank of Madras in 1842 •1861: All 3 were given right to issue currency •1921: Formation of Imperial Bank of India by merging all above 3 banks

•

1955: Nationalization of imperial bank => SBI •

East India Company established 3 presidency banks Pre Independence banks in India

Bombay, Bengal, Madras Presidency Banks => Imperial Bank' 21 => SBI in '55

•

Catered British Army, Bureaucrats, Judges, merchants •

Foreign Banks

Allahabad Bank (est. 1865) •Punjab National Bank (est. 1894, HQ Lahore •Bank of India (est. 1906)•Bank of Baroda (est. 1908)•Central Bank of India (est. 1911)•

Indian Banks

By 1930 India had > 1000 banks working solely on company's law

•

In Oct 24, 1929, stock market bubble finally burst, as investors began dumping shares en masse.

•

A record 12.9 million shares traded that day = Black Thursday •1934, to check such situation, RBI as banker's bank. •

RBI SBI, ICICI, PNB, BOB •Catered Merchant & industrial houses •Bank branches ↑ but only to cater industrial markets •no expansion in rural areas •=> for rural Govt began nationalizing the banks •

Post-independence banks in India

Nationalisation of banks-I 14 commercial banks nationalized 19th July, 1969, Indira G

1. Central Bank of India 2. Bank of India 3. Punjab National Bank 4. Bank of Baroda 5. United Commercial Bank 6. Canara Bank 7. Dena Bank

8. United Bank 9. Syndicate Bank 10. Allahabad Bank 11. Indian Bank 12. Union Bank of India 13. Bank of Maharashtra 14. Indian Overseas Bank

Nationalisation of banks-2

Andhra Bank 1.Corporation Bank 2.New Bank of India 3.Oriental Bank of Commerce 4.Punjab & Sindh Bank 5.Vijaya Bank6.

6 more commercial banks nationalized in April 1980. These were:

to overhaul banking sector of India & to overcome its problems viz.

Bank licences 1st Round (1993) Total 10 private banks given licenses => 6 still running + 4 closed

Narsimhan Committee Il — 1998 Introduced Voluntary retirement scheme (VRS) in PSBs. •Legal reforms for loan recovery => SARFAESI act 2002 •

Payment and Settlement Act ○

Retail Transaction => ECS, NEFT, Credit Card ○

Wholesale Transaction => RTGS ○

Permit new private / foreign banks ○

Computerization, electronic fund transfer, legal framework

•

Finance Page 2

Total 10 private banks given licenses => 6 still running + 4 closed

ICICI, HDFC, UTI (Axis bank (2007)), IDBI, IndusInd, DCB (Development Credit Bank)

•6 Running

Global Trust Bank merged with Oriental bank of Commerce, •Bank of Punjab merged with Centurion bank, •Centurion bank merged with HDFC bank, •Times Bank merged with HDFC bank•

4 Closed

Permit new private / foreign banks ○

New Bank licenses 2nd round (2001) RBI gave license only to 2 strongest contenders viz.

1. Kotak Mahindra 2. Yes Bank

10 years successful work-ex with min capital Rs. 500Cr •Get its shares listed on stock exchange w/i 3 years; •bring down voting rights to 15% within 12 years. •foreign shareholding must not be > 49% for 1st 5 years •50% directors = independent •bank must not invest in shares/bonds of its parent group. •Must open at-least 25% branches in unbanked rural areas •Have to comply with PSL norms •

New Bank licenses 3rd Round (2013—14) — RBI conditions RBI — Bimal Jalan Committee Based on committees recommendations RBI gave license only 2 strongest contenders viz. 1. Bandhan Microfinance 2. IDFC

To meet the specific requirement from different sectors (i.e. agriculture, housing, foreign trade, industry)

Classification of banks

All banks included in 2nd Schedule to Reserve Bank of India Act, 1934 are Scheduled Banks. •These banks comprise Scheduled Commercial Banks and Scheduled Co-operative Banks. •

having a paid up capital and reserves of at least 25 Lakh ○

satisfying the RBI that its affairs are not being conducted in a manner prejudicial to interests of its depositors. ○

To be included under this schedule of RBI Act, banks have to fulfill certain conditions: •

Types Of Commercial Scheduled commercial Banks •

majority stake is held by Govt - SBI, Bank of India, Canara Bank, etc. ○

Public Sector Banks

majority of share capital of bank held by private individuals. ○

regd as companies with limited liability.○

Eg: ICICI Bank, Axis bank, HDFC, etc. ○

Private Sector Banks

These banks are regd and have their headquarters in a foreign country but operate their branches in our country. ○

Examples: HSBC, Citibank, Standard Chartered Bank, etc ○

Foreign Banks

Est 1975 during 5th FYP period (1974-79)○

under an Ordinance promulgated on 26th September 1975 and RRB Act, 1976 ○

to develop rural economy and supplement Coop Credit Structure' to enlarge institutional credit for rural and agri sector. ○

Area of ops limited to as notified by Gol - one or more districts in the State. ○

are jointly owned by GoI, concerned State and Sponsor Banks (27 SCBs and 1 State Cooperative Bank); ○

issued capital of a RRB = 50%, 15% and 35% resp○

Prathama bank = 1st RRB - Moradabad in UP○

Source of funds = owned funds, borrowings from NABARD, sponsor banks, others including SIDBI and NHB○

RRBs mobilise deposits primarily from rural/semi-urban areas and provide loans/advances mostly to small & marginal farmers, agri labourers, rural artisans and other segments of priority sector

○

Regional Rural Banks

A co-operative bank is a financial entity which belongs to its members, who are at the same time the owners and the customers of their bank.

○

Often created by persons belonging to the same local or professional community or sharing a common interest. ○

generally provide their members with a wide range of banking and financial services (loans, deposits, banking accounts, etc).○

Cooperative Banks •

Scheduled Banks

Finance Page 3

generally provide their members with a wide range of banking and financial services (loans, deposits, banking accounts, etc).○

provide limited banking products and are specialists in agriculture-related products. ○

Cooperative banks are the primary financiers of agricultural activities, some small-scale industries and self-employed workers. ○

Co-operative banks function on the basis of "no-profit no-loss"○

Anyonya Co-operative Bank Limited (ACBL) = 1st - Vadodara○

Non —scheduled Banks = not included in 2nd schedule of RBI Act, 1934

Commercial banks dominate credit off take in all sectors and among them esp PSBs•

A/c should be denominated in Indian Rupees. ○

may be opened / maintained as current, savings, FD/RD accounts. ○

Interest rates offered by banks on NRO deposits can't be higher than corresponding domestic rupee deposits. ○

includes sale proceeds of immovable properties held by NRls/PlOs. ▪

NRI/PIO cant remit from balances held in NRO a/c > 1 Mn USD per FY, subject to payment of applicable taxes. ○

Loans upto Rs1 Cr against security of funds held in FCNR (B) deposit either to depositors or 3rd parties. ○

Interest rates are stipulated by Dept of Banking Ops & Devpt, RBI○

Foreign Currency Non Resident (Bank) A/c — FCNR (B) A/c3.

Italian word 'nostro' means 'ours'. Hence, Nostro account points at - "Our account with you" ○

Nostro a/c are generally held in a foreign country (with a foreign bank), by a domestic bank (from our perspective, our bank) . It obviates that a/c is maintained in that foreign currency

○

Nostro A/c4.

Italian word 'vostro' means 'yours'. Hence, Vostro account points at - "Your account with us" ○

Vostro accounts are generally held by a foreign bank in our country (with a domestic bank). It generally maintained in IndianRupee (if we consider India)

○

For example, HSBC account is held with SBI in India○

Vostro A/c5.

Italian 'loro' means 'theirs'. Therefore, it points at - "Their account with them" ○

Loro accounts are generally held by a 3rd party bank, other than the account maintaining bank or with whom account is maintained.

○

For example, BOI wants to transact with HSBC, but doesn't have any account, while SBI maintains an account with HSBC in U.K. Then BOI could use SBI a/c.

○

LORO A/c6.

While a bank maintains Nostro account with a foreign bank, it has to keep an account of the same in its books. ○

This is more or less a reflection or a shadow of the nostro account. ○

The entries in the mirror account are used for reconciliation of entries in the nostro account. ○

The mirror account is maintained in two currencies, one of which is the foreign currency and other = home currency○

Mirror A/c7.

Types Of Accounts

Negotiable Instruments Act, 1881 A/c to Sec 13 of Negotiable Instruments Act,"A negotiable instrument = a promissory note, bill of exchange or cheque payable either to orderer or to bearer= any agreed upon medium of exchange of payment is a negotiable instrument. Maker of a negotiable instrument = DrawerPerson directed to pay = Drawee

Types Of negotiable instruments

Promissory Note - explained in Sec 4 of the act = an instrument in writing (not a currency-note) containing an unconditional promise signed by maker, to pay a specified sum of money only to, or to order of a particular person, or to the bearer of the instrument.

•

Bill of Exchange- Sec 5 = an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of a certain person or to the bearer of the instrument.

•

Cheque- Sec 6 = It is a bill of exchange drawn on a specified bank & not expressed to be payable except on demand•

Other negotiable instruments not defined in the act can also be used so long as they •

Finance Page 4

Other negotiable instruments not defined in the act can also be used so long as they •(i) are easily transferable by trade; (ii) are free of conditions, defects and the person getting it in good faith is entitled to the amount specified.

Bank, Tagline and their headquarters Bank Tagline HQ

SBI With you all the way, Pure Banking Nothing Else, The Nation banks on us Mumbai

Union Bank of India Good People to Bank With Mumbai

Central Bank of India Central To you Since 1911 Mumbai

Dena Bank Trusted Family Bank Mumbai

IDBI Banking For All, "Aao Sochein Bada" Mumbai

Bank of India Relationship Beyond Banking Mumbai

Yes Bank Experience our Expertise Mumbai

HDFC Bank We understand your world Mumbai

Bank of Maharashtra One Family One Bank Pune

Bank of Baroda India's International Bank Vadodara

PNB The Name You Can Bank Upon New Delhi

Punjab & Sind Bank Where Service Is A Way Of Life New Delhi

Oriental Bank of Commerce Where Every Individual Is Committed Gurgaon

Canara Bank Together We Can Bangalore

Corporation Bank A Premier Public Sector Bank Mangalore

Vijaya Bank A Friend You Can Bank On Bangalore

Syndicate Bank Your Faithful And Friendly Financial Partner Manipal

Indian Overseas Bank Good People to Grow With Chennai

Indian Bank Your Tech-Friendly Bank Chennai

Allahabad Bank A Tradition of Trust Kolkata

UCO Bank Honours Your Trust Kolkata

South Indian Bank Experience next generation banking. Kerala

Andhra Bank Where India Banks Hyderabad

HSBC The world's local bank London

Some Important Facts related to banking in India Allahabad Bank, est 1865 — oldest PSB in India having branches all over India and serving the customers for the last 145 years. •Imperial Bank of India was later renamed in 1955 as SBI•1st Bank of India with Ltd Liability to be managed by Indian Board was Oudh Commercial Bank - est in 1881 at Faizabad. •Punjab National Bank = 1st bank purely managed by Indians, est in Lahore in 1895. •First Truly Swadeshi bank — Central Bank of India est in 1911 and wholly owned and managed by Indians. •Union Bank of India was inaugurated by Mahatma Gandhi in 1919. •Savings a/c system in India was started by Presidency Bank, 1833. •Central Bank of India = 1st public bank to introduce Credit card. •

internet banking•mobile ATM•

ICICI Bank = 1st Indian bank to provide •

1st Indian bank to open overseas branch = Bank of India - in London in 1946•Bank of Baroda has max overseas branches•

Finance Page 5

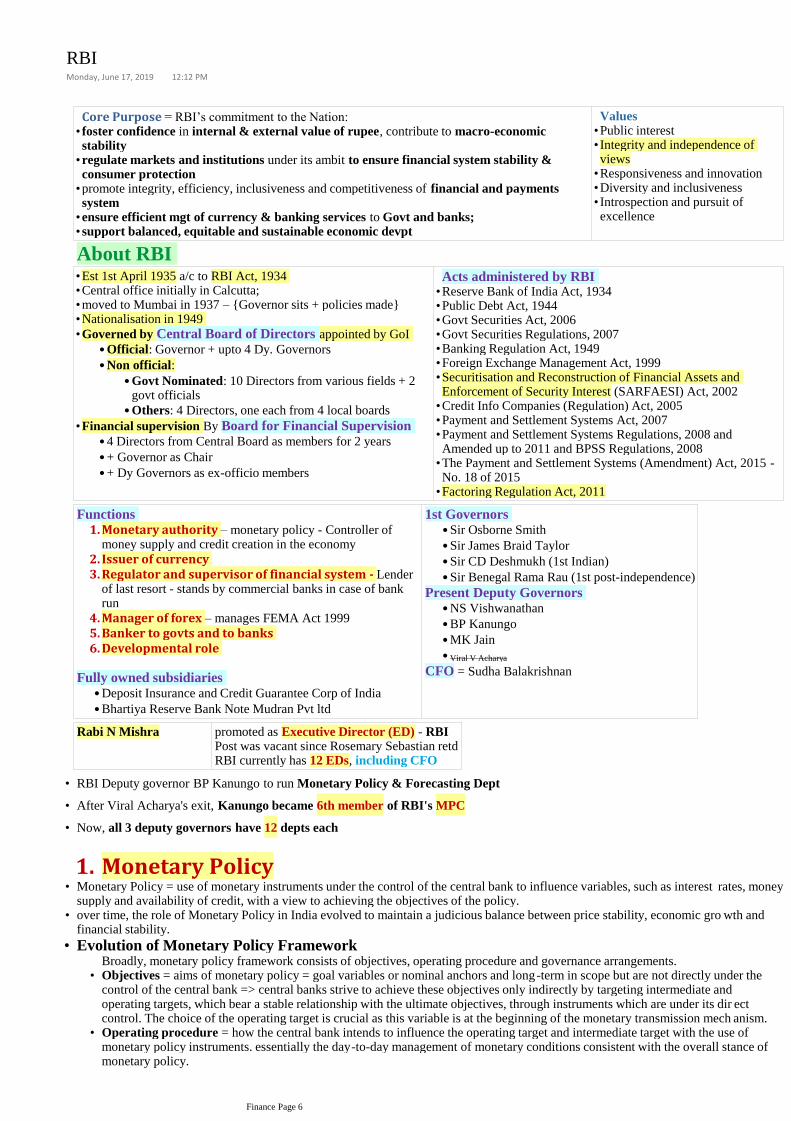

Core Purpose = RBI’s commitment to the Nation: foster confidence in internal & external value of rupee, contribute to macro-economic stability•

regulate markets and institutions under its ambit to ensure financial system stability & consumer protection•

promote integrity, efficiency, inclusiveness and competitiveness of financial and payments system•

ensure efficient mgt of currency & banking services to Govt and banks; •support balanced, equitable and sustainable economic devpt•

Values Public interest •Integrity and independence of views•

Responsiveness and innovation•Diversity and inclusiveness•Introspection and pursuit of excellence •

About RBI Est 1st April 1935 a/c to RBI Act, 1934 •Central office initially in Calcutta; •moved to Mumbai in 1937 – {Governor sits + policies made}•Nationalisation in 1949 •

Official: Governor + upto 4 Dy. Governors•

Govt Nominated: 10 Directors from various fields + 2 govt officials

•

Others: 4 Directors, one each from 4 local boards •

Non official:•

Governed by Central Board of Directors appointed by GoI •

4 Directors from Central Board as members for 2 years •+ Governor as Chair •+ Dy Governors as ex-officio members •

Financial supervision By Board for Financial Supervision •

Acts administered by RBI Reserve Bank of India Act, 1934 •Public Debt Act, 1944 •Govt Securities Act, 2006 •Govt Securities Regulations, 2007 •Banking Regulation Act, 1949 •Foreign Exchange Management Act, 1999•Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002

•

Credit Info Companies (Regulation) Act, 2005 •Payment and Settlement Systems Act, 2007 •Payment and Settlement Systems Regulations, 2008 and Amended up to 2011 and BPSS Regulations, 2008

•

The Payment and Settlement Systems (Amendment) Act, 2015 -No. 18 of 2015

•

Factoring Regulation Act, 2011•

Monetary authority – monetary policy - Controller of money supply and credit creation in the economy

1.

Issuer of currency 2.Regulator and supervisor of financial system - Lender of last resort - stands by commercial banks in case of bank run

3.

Manager of forex – manages FEMA Act 1999 4.Banker to govts and to banks 5.Developmental role 6.

Functions

Deposit Insurance and Credit Guarantee Corp of India •Bhartiya Reserve Bank Note Mudran Pvt ltd •

Fully owned subsidiaries

Sir Osborne Smith •Sir James Braid Taylor •Sir CD Deshmukh (1st Indian)•Sir Benegal Rama Rau (1st post-independence)•

1st Governors

NS Vishwanathan •BP Kanungo •MK Jain •

Viral V Acharya •

Present Deputy Governors

CFO = Sudha Balakrishnan

Rabi N Mishra promoted as Executive Director (ED) - RBIPost was vacant since Rosemary Sebastian retdRBI currently has 12 EDs, including CFO

RBI Deputy governor BP Kanungo to run Monetary Policy & Forecasting Dept•

After Viral Acharya's exit, Kanungo became 6th member of RBI's MPC•

Now, all 3 deputy governors have 12 depts each•

Monetary Policy1.Monetary Policy = use of monetary instruments under the control of the central bank to influence variables, such as interest rates, money supply and availability of credit, with a view to achieving the objectives of the policy.

•

over time, the role of Monetary Policy in India evolved to maintain a judicious balance between price stability, economic gro wth and financial stability.

•

Broadly, monetary policy framework consists of objectives, operating procedure and governance arrangements.Objectives = aims of monetary policy = goal variables or nominal anchors and long-term in scope but are not directly under the control of the central bank => central banks strive to achieve these objectives only indirectly by targeting intermediate andoperating targets, which bear a stable relationship with the ultimate objectives, through instruments which are under its dir ect control. The choice of the operating target is crucial as this variable is at the beginning of the monetary transmission mech anism.

•

Operating procedure = how the central bank intends to influence the operating target and intermediate target with the use of monetary policy instruments. essentially the day-to-day management of monetary conditions consistent with the overall stance of monetary policy.

•

Governance arrangements = process of decision making and focus on responsibilities, powers and accountability of monetary •

Evolution of Monetary Policy Framework•

RBIMonday, June 17, 2019 12:12 PM

Finance Page 6

Governance arrangements = process of decision making and focus on responsibilities, powers and accountability of monetary authority.

•

Historically, bank reserves and short-term interest rates = 2 dominant operating targets - post 1990s & de-regulation era mein the overnight rate emerged as most commonly pursued operating target in conduct of monetary policy.

•

=> Financial repression with interest rate prescriptions, statutory pre-emptions and directed credit partly crowded out the private sector => Committee to Review the Working of Monetary System (Sukhamoy Chakravarty) recommended in 1985 a new monetary policy framework based on monetary targeting with feedback, drawing on empirical evidence of a stable demand function for money.

•

During 1971-1985, monetisation of fiscal deficit exerted a dominant influence on conduct of monetary policy. Resultant inflationary consequences of high public expenditure necessitated frequent recourse to CRR to neutralize secondary effects of the expansion

•

broad money = intermediate target while reserve money = main operating instrument for achieving control on broad money growth. Accordingly, monetary (M3) projection was made consistent with the expected real GDP growth and a tolerable level of inflation. This framework was in operation during mid-1980s to 1997-98

•

But, targets were rarely met. biggest impediment to monetary targeting was lack of control over RBI's credit to the central government, which accounted for the bulk of reserve money creation.

•

LPG Reforms se shift in financing government and the commercial sector with increasing reliance on market -determined interest rates and exchange rate. Financial innovations/external swings in capital flows, volatility in exchange rate and global busin ess cycles imparted instability to demand for money + increasing evidence of changes in underlying transmission mechanism of monetary policy with interest rate and the exchange rate gaining importance vis -à-vis quantity variables => changed in 1998-99 to next approach

•

Monetary Targeting Framework {mid-1980s to 1997-98}•

Under this approach, a number of quantity variables such as money, credit, output, trade, capital flows and fiscal position a s well as rate variables such as rates of return in different markets, inflation rate and exchange rate were analyzed for drawing monet ary policy perspectives

•

forward looking indicators since the early 2000s drawn from the RBI's surveys of industrial outlook, credit conditions, capac ity utilization, professional forecasters, inflation expectations and consumer confidence

•

Worked well till 2008 => visible signs of stagflation + also no clarity in RBI's objective => Urjit Pate commtee 2014•

Multiple Indicator Approach (apr 1998 onwards)•

However, pursuant to the amendment to RBI Act, 1934, in May 2016, the primary objective of monetary policy is to maintaining price stability while keeping in mind the objective of growth

•

inflation target set by GoI, in consult with RBI, once in every 5 years ○

GoI notified 4% (±2%) CPI inflation = target for Aug 5, 2016 to Mar 31, 2021○

Failure = avg CPI beyond limits for any 3 consecutive quarters ○

Explicitly mandated under RBI Act, 1934 - amended in May 2016 - statutory basis for flexible inflation targeting framework •

Financial Markets Operations Dept (FMOD) operationalizes the monetary policy, mainly through day-to-day liquidity management operations.

•

The Financial Markets Committee (FMC) meets daily to review the liquidity conditions so as to ensure close alignment of the operating target - the weighted average call money rate (WACR) – with the policy repo rate.

•

•

Flexible Inflation Targeting•

Monetary Policy Committee (MPC) by GoI under Sec 45 ZB •determines policy interest rate to achieve inflation target •

Must meet atleast 4 times a year – presently 6 times {Bimonthly}•Quorum for meeting is 4 members •Governor has casting vote in case of a tie•

RBI people

RBI Governor – ex-officio Chairperson •Dy. Governor in charge of monetary policy (Kanungo)•1 RBI officer nominated by Central Board •

Govt nominees{for 4 yrs term - re-appointment}

Chetan Ghate from ISI•Pami Dua from DSE •Ravindra Dholakia from IIM-A •

(a) the resolution adopted by the MPC; •(b) the vote of each member on the resolution, ascribed to such member; •(c) the statement of each member on the resolution adopted. •

(a) the sources of inflation; ○

(b) the forecast of inflation for 6-18 months ahead.○

Once in every six months, the Reserve Bank is required to publish a document called the Monetary Policy Report to explain •

On the 14th day, the minutes of the proceedings of the MPC meeting are published which include •

maintain price stability while keeping growth in mind - Price stability is a necessary precondition to sustainable growth •Primary Obj of monetary policy •

Monetary policy conducted through interest rates and money supply - BIMONTHLY policy review•RBI uses following for conducting monetary policy•

CRR - average daily balance that a bank is required to maintain with the Reserve Bank as a share of such per cent of its ▪

Varying Reserve Requirements - CRR & SLR○

Quantitative tools: (affect volume of credit) - OMOs, SLR, CRR, bank rates, LAF, MSF, SDF/UDF•Instruments •

Finance Page 7

CRR - average daily balance that a bank is required to maintain with the Reserve Bank as a share of such per cent of its Net demand and time liabilities (NDTL) that the Reserve Bank may notify

▪

SLR - set aside this much money into safe liquid assets such as g-secs, cash or gold or RBI approved securities. Banks do earn interest

▪

Sells securities to reduce supply of high powered money□

RBI buys and sells govt securities in open market to control money supply - used for sterilization (control temporary mismatches in liquidity due to foreign capital flow)

▪

Open Market Operations: ○

Market Stabilization Scheme (MSS) = RBI uses another instrument to keep liquidity intact - Govt pays interest on MSS. Specifically is purpose k liye hai. RBI sells G-sec, T-bill and cash management bills (CMB) to suck excess liquidity of a more enduring nature arising from large capital inflows. The cash so mobilised is held in a separate government account with the Reserve Bank.

▪

Sterilizing against external shocks and inflation○

borrow long term funds from RBI, not the main tool to control money which is Repo rate/policy rate. If bank don’t maintain CRR, SLR, penalty as per bank rate. Bank Rate is published under Section 49 of RBI Act, 1934

▪

From 2012, Bank Rate = MSF

Bank rate - rate at which RBI buys or rediscounts bills of exchange or other commercial papers - aligned with MSF rate ○

Penal rate jispe banks borrow addl amount of overnight money from RBI over and above repo window by dipping into their SLR portfolio up to a limit - banks can use up to 1% of securities from SLR = (repo + 0.25). This provides a safety valve against unanticipated liquidity shocks to the banking system.

▪

Marginal Standing Facility ○

LAF - Consists of overnight as well as term repo auctions. Aim of term-repo is to help develop the inter-bank term-money○

Repo rate – fixed interest rate at which RBI provides overnight loans to any client of RBI (Union/state govt, banks, non-banks) against g-secs and other secs under the LAF - g-secs = collateral & buy those back - 7 day/14 days term repo

▪

Reverse repo rate – fixed interest rate at which RBI absorbs liquidity on an overnight basis under LAF. RBI pays banks to park excess funds into RBI. RBI pledges G-Secs as collaterals = repo – 0.25

▪

{Narasimham Committee (1998) recommendations, the RBI introduced the Interim Liquidity Adjustment Facility (ILAF) in April 1999 => LAF in 2000}

▪

market, which in turn can set market-based benchmarks for pricing of loans and deposits, and hence improve transmission of monetary policy. Both the below rates are overnight and create the benchmark for other overnight rates in the market.

(=50 basis points) shortened to align with call rates (gives better liquidity management control to RBI)▪

to further align weighted average call rate with the repo rate, the policy rate corridor around the policy repo rate was further narrowed to 50 bps in April 2017.

▪

Corridor - MSF rate & reverse repo rate determine the corridor for daily movement in weighted average call money rate ○

Standing deposit facility (SDF) / UDF (Uncollateralized Deposit Facility) - started budget 2018 - Similar to reverse repo but RBI will not pledge any G-sec as collateral. Objective - help RBI suck excess liquidity esp given lack of G-secs to pledge as was in DeMo. RBI can simply promise to pay (interest) without any ‘G-sec’ as guarantee / collateral to the other party

○

Negative/restrictive controls like take permission from RBI if loan to an individual over 1 cr (ye pre LPG reforms mein hota tha)

▪

credit rationing (PSL - Credit Guarantee Corp of India Ltd established in 71 to facilitate ), □Consumer Credit control/ EMI (min instalment & down-payments kitni, - if increased then lesser loans, if decreased then more loans),

□

Margin requirements/Loan to value ratio (Akshay kumar pays only x% of worth of gold/asset).□

Direct action - penalties imposed on violation of directives under Banking Regulation Act 1949 and Payment and Settlements Act, 2007, FEMA, 1999

○

Qualitative tools (affect distribution of credit) •

Some banks borrow money from RBI’s repo window, say Rs.60○

Some banks park their money in RBI’s reverse repo window, say Rs. 40○

At any point of time,•

So, NET 60 MINUS 40 = +20. It means RBI injected liquidity in the system. If answer was a negative figure, then It’s said tha t RBI absorbed liquidity from the system.

•

Central Bank Liquidity•

Cash, including foreign currency.1.Cash beyond CRR2.G-Sec beyond SLR3.Marketable securities backed by PSE, Multilateral development banks, Foreign Governments.4.

BASEL-III norms mandated that banks have to keep enough amount in high quality liquid assets (HQLA) so that bank can survive a 30 days stress-test scenario. HQLA eligible assets includes:

•

If bank has sufficient HQLA to survive total net cash outflow for next 30 calendar days => liquidity coverage ratio is 1 (or 100%).

•

RBI began implementing LCR gradually since 2015 (60%, 70% .. like that it was raised every year).•From 1/1/2019, banks must keep an LCR of 100% or MORE.•If SLR is kept high and LCR is also implemented, then Indians banks will have less loanable funds therefore, in recent times RBI has gradually reduced SLR while hiking the LCR requirement,

•

Liquidity Coverage Ratio (LCR) & HQLA

Finance Page 8

has gradually reduced SLR while hiking the LCR requirement,

•

Monetary policy can’t control supply side issues, Fiscal deficit, leakage of Govt money to informal money lenders - and their impact on the loan market.

1.

Repo borrowing is not major source of funding for Indian banks. So, changing repo will not immediately impact the bank loan rates.

2.

Even if RBI cuts repo rate, banks are not cutting lending rates due to NPA problem3.

Limitations of Monetary Policy in combating inflation•

Extension of MSF to Scheduled Primary (Urban) Cooperative Banks •Extension of LAF and MSF to Scheduled State Cooperative Banks •to permit Primary (Urban) Co-operative Banks to undertake eligible trxns for acquisition / sale of non-SLR investment in secondary market with mutual funds, pension / provident funds, and insurance companies

•

RBI Last year (3rd Bimonthly monetary policy mein)•

Issuer of currency 2.GoI = issuing authority of coins and supplies coins to RBI on demand => puts coins into circulation on behalf of GoI •

Dewas (MP), Mysore, Nasik & Salboni (WB) -- DEVMANUS•Presses in Dewas and Nasik owned by Security Printing and Minting Corp (owned by GoI) •Other 2 owned by Bhartiya Reserve Bank Note Mudran Pvt Ltd (owned by RBI) •

Printing presses •

Mumbai•Noida•Kolkata•Hyderabad•

Mints •

Coins are legal tender only for amounts < Rs 1000 as per Indian Coinage Act •

2000 Motif of Mangalyaan on reverse •Magenta •66x166 mm •

500

66x150 mm •Stone grey •Predominant new theme is Red Fort •Numerals in Devanagari in new notes •Gandhi face now at centre •Swachch bharat logo and slogan •

200 - Sanchi stupa •100 - Rani ki Vav; = Lavender •50 - Hampi = blue•10 - Konark = brown•

Currency note features •

RBI as Banker and Debt Manager to govt 3.

with all its money, remittance, exchange and banking transactions in India and the management of its public debt•RBI Act, 1934 requires GoI to entrust the RBI •

Govt also deposits its cash balances with RBI•RBI may also, by agreement, act as banker and debt manager to State Govts•

Currently, banker to all State Govts in India (incl UT of Puducherry), except Sikkim {state bank of Sikkim which merged into SBI = banker for Sikkim}

•

For Sikkim, has limited agreement for mgt of its public debt •

RBI as banker to banks 4.E-Kuber = Core Banking solution of RBI •

Finance Page 9

E-Kuber = Core Banking solution of RBI •Guarantor against bank run•

Regulator & Supervisor of Financial system5.Commercial banking striving towards a more competitive, efficient and heterogeneous banking structure. •Licensing policies regarding Universal Banks, Small Finance Banks and Payments Banks => building a heterogeneous banking system. •

How does RBI regulate •

Licensing of universal banks – IDFC and Bandhan given licenses in 2013 ○

Now RBI accepts applications under on-tap licensing policy○

licenses to differentiated/niche banks like Small Finance Banks and Payments Banks – furthering Fin-clu○

Issues licenses for opening of banks •

Authorization for opening of branches •Governing entry and expansion of foreign banks in India and Indian banks abroad •Resolution mechanisms•

Basel III regulations for Indian banks by 31st March 2019, instead of 31st March 2018 as announced earlier. ○

Monitoring of maintenance of CRR and SLR by banks ○

According prior approval for 5%+ shares or voting rights of pvt banks ○

Risk mgt norms •

Internationally agreed date = 1st Jan 2019 •

= apex (but non-statutory) body constituted by GoI ○

No funds allocated to it separately ○

FM is Chair ○

Members = RBI Governor, Chairs of SEBI, IRDA, PFRDA, IBBI, Secys to Depts. in MoF, CEA etc ○

Coordinate with Financial Stability and Development Council •

Cooperative banking Cooperative credit structure = 3-tier system •

outside purview of Banking Regulation Act 1949 => not regulated by RBI ○

Central Cooperative Banks @distt level and State Cooperative banks @state level under State Cooperative Societies Act and regulated by RBI – powers to NABARD to conduct inspection of these

•

urban and semi-urban areas ○

primarily regd as cooperative societies under State Cooperative Societies Acts ○

Banking laws made applicable to cooperative societies only in 1966 by amending Banking Regulation Act 1949, •

banking related fxns regulated by RBI ○

mgt related fxns regulated by resp State govts/Central govt ○

thus duality of control over these banks •

NBFCs NBFC = company regd under Sec 3 of Companies Act, 1956 engaged in business of NBFI as under Sec 45 1(a) of RBI Act, 1934•loans and advances, •acquisition of shares/stocks/bonds/debentures/securities issued by Govt or local authority or other marketable securities of a like nature, •leasing, hire-purchase, insurance business, chit business•

company’s financial assets constitute > 50% total assets ○

and income from financial assets constitute > 50% gross income○

50-50 rule - Financial activity as principal business is when •

A company which fulfils both above will be regd as NBFC by RBI •Minimum Net Owned Fund (NOF) of ₹ 2 Cr•(Minimum NOF reqd for specialized NBFCs like NBFC-MFIs, NBFC-Factors, CICs are different)•Systemically Important NBFCs = whose asset size ≥ ₹ 500 Cr as per last audited balance sheet•

BanksLicence from RBI under Banking Regulation Act•All supervised by RBI•

Time Deposits (FDRD)○

Deposits from Public - both•

NBFCLicensed under Company Act•Not All, Insurance cos = IRDA, Merchant banking Cos = SEBI•Can accept Time Deposits (Deposit taking NBFCs) •but not Demand Deposits •

~RBI as Regulator of Financial systemWednesday, July 31, 2019 11:47 AM

Finance Page 11

Time Deposits (FDRD)○

Demand Deposits (CASA)○

Can•Are•available•

but not Demand Deposits •

cannot issue cheques drawn on itself •Not part of Payment system, CTS•Deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation is not available to depositors of NBFC

•

NBFCs accepting public deposit (hold a deposit accepting certificate of regn)○

NBFCs not accepting/holding public deposit (no such certificate)○

NBFCs classified into 2 broad categories

Presently, max interest rate which can be offered by an NBFC = 12.5%•Interest may be paid or compounded at rests not shorter than monthly rests•NBFCs allowed to accept/renew public deposits for a min period of 12 months and maximum period of 60 months (5 yrs)•No demand deposits allowed•The deposits with NBFCs are not insured•RBI does not ensure the repayment of deposits by NBFCs•

Deposits in an NBFC

NBFCs regulation

related to banking, lending RBI

related to stock broking, merchant banking, Venture Capital Fund, shares/stocks SEBI

Insurance & other Insurance companies IRDAI

Housing NBFCs & other Housing Finance Companies NHB

Chit funds state govts

Nidhi companies MoCA

Nidhi company = mutual benefit society; borrowing from members and lending to members only; membership limited to individuals

Misc Imp Regulatory InfoCoop banks, RRBs - NABARD regulates and supervises the functions •Priority sectors decided by RBI & not GoI•Small banks = 75% PSL + SLR + CRR•Co op banks no PSL norms, only members can borrow•Wholesale banks exempted from SLR•Payment Banks - Only CASA, no loans, hence no PSL or SLR•MFIs are regulated by RBI, but only those which are regd with it as NBFCs•MUDRA Bank regulates + refinances other MFIs which lend to MSMEs associated with mfg, trading and service activities•

Financial Markets RBI has designated industry bodies

Fixed Income, Money Markets and Derivatives Asso. of India (FIMMDA) - benchmark administrator for Rupee interest rate•Foreign Exchange Dealers Asso. of India (FEDAI) - benchmark administrators for forex •FIMMDA, FEDAI and IBA have since jointly floated an independent company•

an anonymous order matching trading platform •G-secs markets - Trading largely on Negotiated Dealing System-Order Matching (NDS-OM)•

Call money market - repo rates•

Payment Systems Board for regulation and supervision of payment and settlement systems (BPSS) #UpdateA sub-committee of Central Board of RBI •highest policy making body on payment systems•Members = Governor as Chair + 4 •Dy. Govs (Kanungo is Vice Chair) + 2 other Central Board members •

Finance Page 12

Dy. Govs (Kanungo is Vice Chair) + 2 other Central Board members •

Paper based payments {#Update}Instruments (like cheques, drafts, and the like) = ~60% volume of total non-cash trxns•In value terms, share presently ~11%•been steadily ↓ •

speeding up ▪

and bringing in efficiency in processing of cheques ▪

(9 digits – first 3 city code, next 3 bank code and last 3 branch code)▪

RBI introduced Magnetic Ink Character Recognition (MICR) tech for •

Electronic paymentsElectronic Fund Transfer (EFT) in 1990s •

More secure Nation-wide payment system facilitating one-to-one fund transfer ▪

Info of date/time of credit to the beneficiary a/c available in the system ▪

Accepts cash for originating trxns => Even individuals w/o bank a/c can, @NEFT enabled branches (limit of Rs. 50k per txn) ▪

from any NEFT enabled branch even to a beneficiary w/o a NEFT enabled a/c in Nepal. •beneficiary paid in Nepalese Rupees•Max Rs. 50k per trxn•

NEFT facilitates one way cross border transfer from India to Nepal under Indo-Nepal Remittance Facility Scheme. ▪

Other than above 2, no limit to amount through NEFT ▪

Necessary for beneficiary to have a bank a/c with a NEFT enabled destination bank ▪

on half-hourly basis – 23 batches from 8am to 7pm on all working days of the week •NEFT works on a Deferred Net Settlement (DNS) basis which settles trxns in batches ▪

NEFT Clearing Centre in RBI is operated by National Clearing Cell ▪

Unique ID of a bank branch participating in NEFT system •

1st 4 = bank

5th char = 0

last 6 chars = branch

11 digit code •

IFSC (Indian Financial System Code) ▪

NEFT is a credit push system ▪

NEFT (National Electronic Funds Transfer) since 2005 •

real time => payment trxn not subjected to any waiting period ▪

Gross settlement => trxn settled on 1-to-1 basis w/o bunching or netting with any other transaction ▪

Since funds settlement takes place in books of RBI, once processed, payments are final and irrevocable ▪

settles all inter-bank payments and customer transactions > 2 lakh▪

continuous (real-time) settlement of funds individually on an order by order basis without netting▪

For large value trxns - Min 2 lakhs with no upper ceiling ▪

9.00 am to 4.30pm on week days •9.00 am to 2pm on Saturdays •

RTGS service window for settlement at the RBI end ▪

for customer trxns from 7 AM to 6 PM ▪

for inter-bank transactions from 7 AM to 7.45 PM▪

At present, RTGS System is available ▪

RTGS (Real Time Gross Settlement) system - since 2004•

to handle bulk & repetitive payments like salary, dividend etc▪

Mainly for credit/debits of low value in large or frequent trxns▪

ECS Debit, which involves a transfer of funds from your account ○

ECS Credit which takes place when money comes into your account○

2 types: ▪

Electronic Clearing Service (ECS) in 1990s•

@National Clearing Cell (NCC) in Mumbai ▪

multiple credits to beneficiary a/cs against a single debit from sponsor account▪

National Electronic Clearing Service (NECS) in 2008 •

Education – loans upto 10 lakh 4.Housing – loans upto 28 lakh in metropolitan cities and 20 lakh in other places (loans to banks own employees not eligible)

5.

Social infra – loans upto 5 Cr per borrower for social infra in non-Tier I cities, bank credit to MFIs for on lending to individuals, SHGs or JLGs for water & sanitation facilities

6.

RE – loans upto 15 Cr for RE, non-conventional energy based public utilities like street lighting, remote village electrification; for individual households, loan limit = 10 lakh per borrower

7.

Others 8.

Targets and sub-targets

Domestic SCBs (excluding RRBs and Small Finance Banks) + foreign banks ≥ 20 - (comply by march

2018 )

Foreign banks < 20 branches

Adjusted Net Bank Credit or Credit Equivalent Amount of Off-Balance Sheet Exposurewhichever is higher.

Total Priority Sector - 40% of 40% - phased manner by 2020 export credit upto 32% = eligible.

Agri (farm credit, agri infra, ancillary activities)– 18% w/i this 18%, 8% for Small (1-2 ha) and Marginal (< 1 ha)Farmers {phased manner - 7% by Mar 2016 & 8% by Mar 2017}

NA

Micro enterprises – 7.5% NA

Advances to weaker sections – 10% NA

What else PSL•social infra - loans up to Rs 5 crore a borrower for building social infra for activities in tier-II to tier-VI centres○

renewable energy {Rs 15 crore for solar-based power generators, biomass-based power generators, wind mills, micro-hydel plants, etc}

○

Bank credit to MFIs for lending to individuals, SHGs and JLGs provided MFIs meet norms prescribed for micro lending (loan pricing, amount, etc). Every quarter, MFIs to furnish certi from a CA, stating guidelines have been followed.

○

All loans to MSME will qualify as PSL against the earlier limit of loans up to 10 Cr○

food and agro processing units ▪

Distinction b/w direct and indirect agri removed => banks can meet their entire agri lending target by funding indirect agri, which includes loans to companies engaged in agri sector.

▪

agri infra such as storage, soil conservation and watershed dev▪

ancillary activities like agro clinics and agribusiness centres▪

What's now under Agriculture ○

For individual households, loan limit = Rs 10 lac a borrower▪

Rs 28 lakh to individuals in metros - provided overall cost of dwelling unit is Rs 35 lakh ▪

Rs 20 lakh in others - provided overall cost of dwelling unit is Rs 25 lakh▪

Home finance - loans upto ○

For foreign banks > 20 branches - sub-targets for small/marginal farmers and MSMEs = applicable after 2018. •For long-term bonds to fund affordable housing/infra projects, RBI exempted banks for maintaining CRR, SLR and PSL•Housing loans backed by long-term bonds exempted from PSL mandate○

if a bank categorises a home loan under PSL, it won't get exemption in terms of CRR and SLR •Priority Sector Lending Certificates – surplus banks can sell•Priority sector guidelines do not lay down any preferential rate of interest for priority sector loans•PSL: What if targets not met? •

Desi (+Foreign ≥ 20) Foreign < 20

Remaining $$ to RIDF = Rural Infra Devpt fund - managed by NABARD

To SEDF (Small Enterprises Devpt Fund) - managed by SIDBI

NABARD pays interest to bank SIDBI pays interest to bank

State govt get cheap infra loans State industrial fin corp get cheap loans

Banking ombudsman scheme Under Sec 35A of Banking Regulation Act 1949 •wef 1995 •Banking ombudsman = senior official appointed by RBI to redress customer complaints •All SCBs, RRBs covered •For amounts upto 20 lakh •Can award compensation upto 1 lakh for mental agony and harassment •Appellate authority vested with a Dy. Governor of RBI •

Deposit Insurance and Credit Guarantee Corp Deposit Insurance and Credit Guarantee Corporation Act 1961 •Board of Directors – Chairman is an RBI Dy Gov + 1 RBI Officer + 1 govt officer + 5 Directors nominated by the govt in consultation •

Finance Page 14

Board of Directors – Chairman is an RBI Dy Gov + 1 RBI Officer + 1 govt officer + 5 Directors nominated by the govt in consultation with RBI

•

Head office at Mumbai •Kanungo = Chairman•

All commercial banks – incl branches of foreign banks, RRBs, local area banks ▪

All cooperative banks – all state, central and primary cooperative banks (aka urban cooperative banks) ▪

Primary cooperative societies are not insured by DICGC ▪

Banks included •

Foreign govts ▪

Central/state govts ▪

Inter-bank deposits ▪

Insures all deposits such as savings, fixed, current, recurring etc upto 1 lakh except those of •

Bhartiya Reserve Bank Note Mudran Ltd Est 1995 •Wholly owned by RBI •Head office @ Bengaluru •Presses at Mysore and Salboni (WB) •Kanungo - Chairman (non-Executive) •S K Maheshwari is ME and CEO •

Security Printing and Minting Corp of India Incorporated in 2006; •Mini-Ratna wholly owned by GoI •Head office in Delhi •Security paper, minting coins, printing currency, non-judicial stamp papers of state govts, passports and visa stickers for MEA etc

•

Under Dept of Economic Affairs, FM •Presses at Nashik and Dewas •Security paper mill at Hoshangabad (MP)•Mints at Mumbai, Hyderabad, Kolkata, Noida •Tripti Patra Ghosh = CMD •

Bank Note Paper Mill India Pvt Ltd JV of SPMCIL and BRBNMPL •Incorporated in 2010 •office in Mysuru •Total capacity of 12000 MT per annum (recently received nod to increase to 16000 MT) •Tripti Patra Ghosh is CMD of this as well •

MSMEs Current definition a/c to MSME Devpt Act, 2006•

3 general kinds of commodities - representative of all commodities being produced within economy: ○

Consumers who decide what and how much to consume. •Producers who decide what and how much to produce. •

Macroeconomic policies are pursued by State itself or statutory bodies like RBI, SEBI, etc○

Entities like govt, corps, banks which also take different economic decisions like how much to spend, what interest rate to charge on the credits, how much to tax, etc.

•

Economic Units/Economic Agents - individuals or institutions which take economic decisions. ○

Factors of Production: Capital, land and labour and entrepreneurship○

Firms•Govt•Household sector•External Sector (imports and exports)•

Entities in Economy:○

Revenue = Money earned by selling goods/services○

Profit = Earning of Entrepreneurs after cost of capital, land and wages paid off○

Investment Expenditure: Investment to raise productive capacity○

Private ownership of means of production •production for selling output in market •sale and purchase of labour services at a price = wage rate (labour sold and purchased against wages = wage labour)•

Capitalist economy: in which most of the economic activities have the following characteristics ○

Intermediate Goods: goods used by other producers like material inputs (ex, steel sheets for automobiles, etc.)○

Consumption Durables: durable consumables like TV, washing machine, etc. which last long (unlike food, etc. which doesn’t)○

Consumption/Consumer Goods - goods like food, clothing, recreation and services•

Capital Goods - Enable production (tools, machines, etc.), undergo wear and tear and have to be replaced•

Final Good = An item meant for final use - no more stages of production or transformations○

Inventory = The stock of raw materials, semi-finished goods, unsold finished goods which a firm carries one year to the next ○

Stock : a variable measured at one specific time Flow : a variable measured over an interval of time.Change in stocks over a particular interval of time becomes a flow

Eg a person or a country might have stocks of money, financial assets, liabilities, wealth, capital, inventories, human capital

Eg : income, production, profits

○

Part of final output that comprises capital goods = Gross Investment of an economy○

Net Investment = Gross investment – Depreciation○

Depreciation = Consumption of Fixed Capital = Replacement Investment: annual allowance for wear/tear of a capital good = cost of good divided by no of years of useful life. No real expenditure may have actually been incurred each year yet depreciation is annually accounted for.

○

by producing consumption goods•generating income for those involved in production process•

Production makes consumption feasible in 2 ways○

If an economy produces more consumer goods, it is producing less of investment goods and vice-versa•But more capital goods produced now, more productive capacity of system in future. Hence a larger volume of consumption goodscan be produced in future => If, presently, economy sets aside a greater fraction of output for investment, capacity to produce more output in future rises.

•

Because capital goods, unlike non-durable consumer goods, do not get immediately exhausted with their use – they add to stock of capital in quantitative terms - thus make production of other commodities possible.

•

In a specific time period, say year, total production of final goods can be either in consumption (consumer goods) or investment (capital goods) and thus a trade-off.

○

Firms’ demand for FoP to run production process creates payments to public. In turn, public’s demand for goods and services creates payments to firms and enables sale of products they produce

○

Money & its SupplyIn India financial Regulators are RBI & SEBI

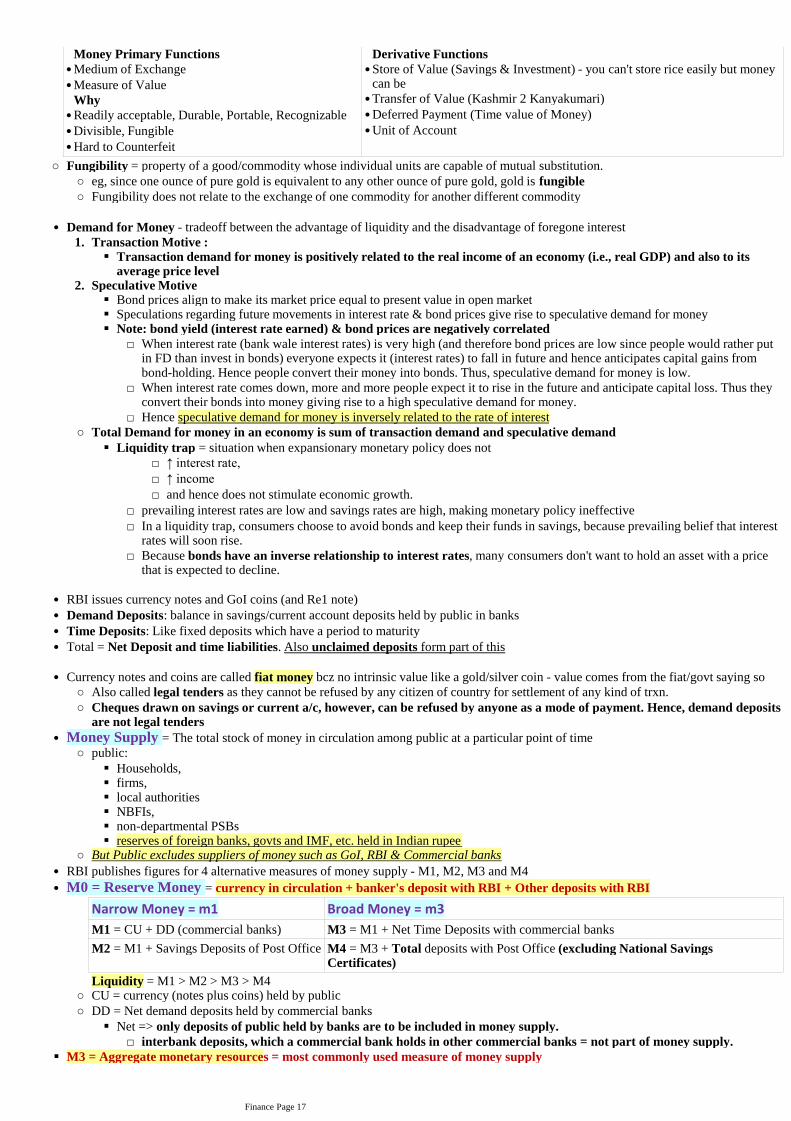

Money Primary Functions Derivative Functions

Macroeconomics & Money SupplyTuesday, July 30, 2019 7:45 PM

Store of Value (Savings & Investment) - you can't store rice easily but money can be

•

Transfer of Value (Kashmir 2 Kanyakumari) •Deferred Payment (Time value of Money) •Unit of Account•

eg, since one ounce of pure gold is equivalent to any other ounce of pure gold, gold is fungible ○

Fungibility does not relate to the exchange of one commodity for another different commodity○

Fungibility = property of a good/commodity whose individual units are capable of mutual substitution. ○

Transaction demand for money is positively related to the real income of an economy (i.e., real GDP) and also to its average price level

▪

Transaction Motive : 1.

Bond prices align to make its market price equal to present value in open market▪

Speculations regarding future movements in interest rate & bond prices give rise to speculative demand for money▪

When interest rate (bank wale interest rates) is very high (and therefore bond prices are low since people would rather put in FD than invest in bonds) everyone expects it (interest rates) to fall in future and hence anticipates capital gains from bond-holding. Hence people convert their money into bonds. Thus, speculative demand for money is low.

□

When interest rate comes down, more and more people expect it to rise in the future and anticipate capital loss. Thus they convert their bonds into money giving rise to a high speculative demand for money.

□

Hence speculative demand for money is inversely related to the rate of interest□

Note: bond yield (interest rate earned) & bond prices are negatively correlated▪

Speculative Motive2.

↑ interest rate, □↑ income □and hence does not stimulate economic growth.□

prevailing interest rates are low and savings rates are high, making monetary policy ineffective□In a liquidity trap, consumers choose to avoid bonds and keep their funds in savings, because prevailing belief that interestrates will soon rise.

□

Because bonds have an inverse relationship to interest rates, many consumers don't want to hold an asset with a price that is expected to decline.

□

Liquidity trap = situation when expansionary monetary policy does not ▪

Total Demand for money in an economy is sum of transaction demand and speculative demand○

Demand for Money - tradeoff between the advantage of liquidity and the disadvantage of foregone interest•

RBI issues currency notes and GoI coins (and Re1 note)•Demand Deposits: balance in savings/current account deposits held by public in banks•Time Deposits: Like fixed deposits which have a period to maturity•Total = Net Deposit and time liabilities. Also unclaimed deposits form part of this•

Also called legal tenders as they cannot be refused by any citizen of country for settlement of any kind of trxn. ○

Cheques drawn on savings or current a/c, however, can be refused by anyone as a mode of payment. Hence, demand deposits are not legal tenders

○

Currency notes and coins are called fiat money bcz no intrinsic value like a gold/silver coin - value comes from the fiat/govt saying so•

Households, ▪

firms, ▪

local authorities▪

NBFIs, ▪

non-departmental PSBs▪

reserves of foreign banks, govts and IMF, etc. held in Indian rupee▪

public: ○

But Public excludes suppliers of money such as GoI, RBI & Commercial banks○

Money Supply = The total stock of money in circulation among public at a particular point of time•

RBI publishes figures for 4 alternative measures of money supply - M1, M2, M3 and M4•

Narrow Money = m1 Broad Money = m3

M1 = CU + DD (commercial banks) M3 = M1 + Net Time Deposits with commercial banks

M2 = M1 + Savings Deposits of Post Office M4 = M3 + Total deposits with Post Office (excluding National Savings Certificates)

Liquidity = M1 > M2 > M3 > M4CU = currency (notes plus coins) held by public ○

interbank deposits, which a commercial bank holds in other commercial banks = not part of money supply. □Net => only deposits of public held by banks are to be included in money supply. ▪

DD = Net demand deposits held by commercial banks○

M0 = Reserve Money = currency in circulation + banker's deposit with RBI + Other deposits with RBI•

M3 = Aggregate monetary resources = most commonly used measure of money supply▪

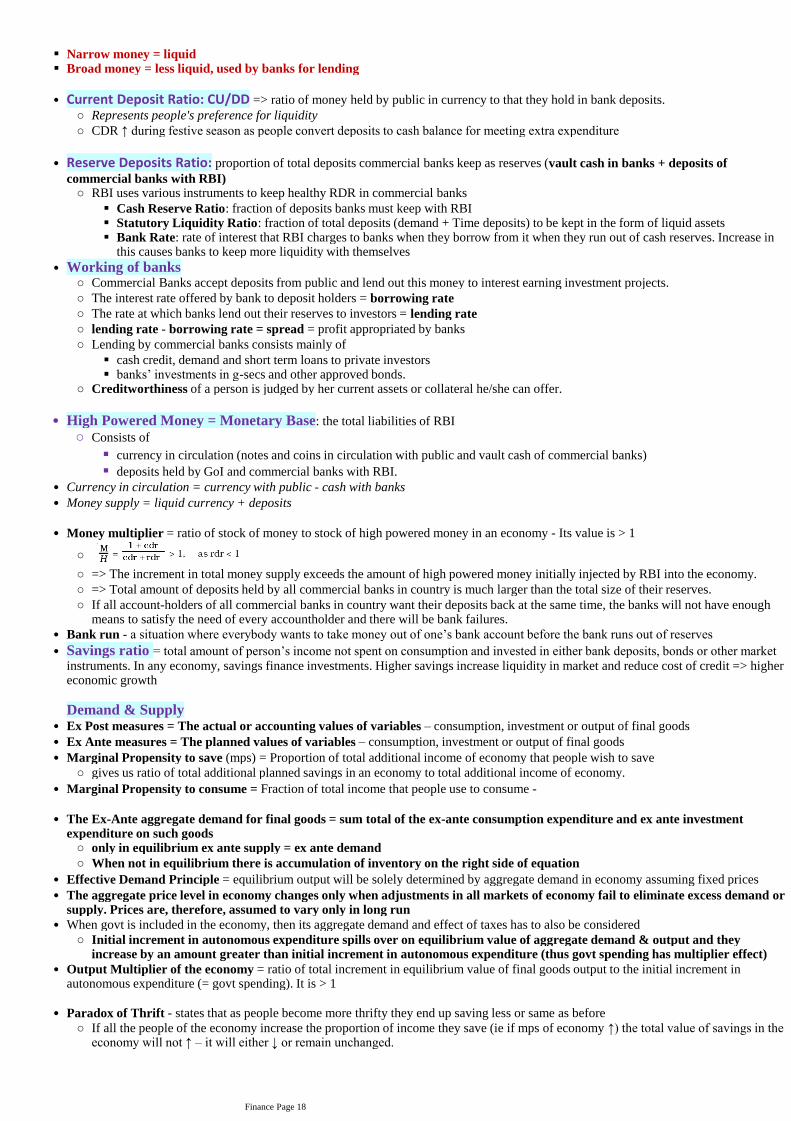

Narrow money = liquid▪

Finance Page 17

Narrow money = liquid▪

Broad money = less liquid, used by banks for lending▪

Represents people's preference for liquidity○

CDR ↑ during festive season as people convert deposits to cash balance for meeting extra expenditure○

Current Deposit Ratio: CU/DD => ratio of money held by public in currency to that they hold in bank deposits. •

Cash Reserve Ratio: fraction of deposits banks must keep with RBI▪

Statutory Liquidity Ratio: fraction of total deposits (demand + Time deposits) to be kept in the form of liquid assets▪

Bank Rate: rate of interest that RBI charges to banks when they borrow from it when they run out of cash reserves. Increase in this causes banks to keep more liquidity with themselves

▪

RBI uses various instruments to keep healthy RDR in commercial banks ○

Reserve Deposits Ratio: proportion of total deposits commercial banks keep as reserves (vault cash in banks + deposits of

commercial banks with RBI)

•

Commercial Banks accept deposits from public and lend out this money to interest earning investment projects. ○

The interest rate offered by bank to deposit holders = borrowing rate○

The rate at which banks lend out their reserves to investors = lending rate○

cash credit, demand and short term loans to private investors ▪

banks’ investments in g-secs and other approved bonds. ▪

Lending by commercial banks consists mainly of ○

Creditworthiness of a person is judged by her current assets or collateral he/she can offer.○

Working of banks•

currency in circulation (notes and coins in circulation with public and vault cash of commercial banks)▪

deposits held by GoI and commercial banks with RBI.▪

Consists of ○

High Powered Money = Monetary Base: the total liabilities of RBI •

Currency in circulation = currency with public - cash with banks•Money supply = liquid currency + deposits•

○

=> The increment in total money supply exceeds the amount of high powered money initially injected by RBI into the economy. ○

=> Total amount of deposits held by all commercial banks in country is much larger than the total size of their reserves. ○

If all account-holders of all commercial banks in country want their deposits back at the same time, the banks will not have enough means to satisfy the need of every accountholder and there will be bank failures.

○

Money multiplier = ratio of stock of money to stock of high powered money in an economy - Its value is > 1•

Bank run - a situation where everybody wants to take money out of one’s bank account before the bank runs out of reserves•

Savings ratio = total amount of person’s income not spent on consumption and invested in either bank deposits, bonds or other market instruments. In any economy, savings finance investments. Higher savings increase liquidity in market and reduce cost of credit => higher economic growth

•

Demand & SupplyEx Post measures = The actual or accounting values of variables – consumption, investment or output of final goods •Ex Ante measures = The planned values of variables – consumption, investment or output of final goods•

gives us ratio of total additional planned savings in an economy to total additional income of economy. ○

Marginal Propensity to save (mps) = Proportion of total additional income of economy that people wish to save•

Marginal Propensity to consume = Fraction of total income that people use to consume -•

only in equilibrium ex ante supply = ex ante demand○

When not in equilibrium there is accumulation of inventory on the right side of equation○

The Ex-Ante aggregate demand for final goods = sum total of the ex-ante consumption expenditure and ex ante investment expenditure on such goods

•

Effective Demand Principle = equilibrium output will be solely determined by aggregate demand in economy assuming fixed prices•The aggregate price level in economy changes only when adjustments in all markets of economy fail to eliminate excess demand or supply. Prices are, therefore, assumed to vary only in long run

•

Initial increment in autonomous expenditure spills over on equilibrium value of aggregate demand & output and they increase by an amount greater than initial increment in autonomous expenditure (thus govt spending has multiplier effect)

○

When govt is included in the economy, then its aggregate demand and effect of taxes has to also be considered•

Output Multiplier of the economy = ratio of total increment in equilibrium value of final goods output to the initial increment in autonomous expenditure (= govt spending). It is > 1

•

If all the people of the economy increase the proportion of income they save (ie if mps of economy ↑) the total value of savings in the economy will not ↑ – it will either ↓ or remain unchanged.

○

Paradox of Thrift - states that as people become more thrifty they end up saving less or same as before•

Finance Page 18

Consumers & firms can choose b/w domestic & foreign goods = product market linkage•Investors can choose b/w domestic & foreign assets = financial market linkage•Firms can choose where to locate prodn and workers can choose where to work = factor market linkage. •Labour market linkages have been relatively less due to various restrictions on movement of people through immigration laws•

Interaction with other economies of world widens choice in 3 broad ways•

Total foreign trade (exports + imports) as a proportion of GDP = common measure of degree of openness of an economy•

In Open Economy Domestic demand for goods ports (ie foreign demand) Imports

because part of domestic demand falls on foreign goods. •It also results in a deterioration of trade balance•

Open Economy Govt Spending Multiplier is smaller than that in a closed economy •

Domestic income ↑ => ↑ imports spending => Trade deficit•An increase in foreign income ↑ => ↑ exports => ↑ domestic output => improves trade balance.•In inflation exports invariably get fucked {bcz we lose competitiveness}•

Smaller saving {matlab pvt corporate investments are ↓}○

In such cases country’s capital stock will not rise rapidly enough to yield enough growth (called ‘growth dividend’) it needsto repay its debt

▪

or a larger budget deficit {matlab bahar k paise se sarkaar chal rahi hai}○

But reason to worry about country’s long-run prospects if trade deficit reflects •Trade deficits not alarming if country invests borrowed funds yielding a growth rate > interest rate•

Twin deficits = when economy has both trade deficit and budget deficit•

Balance of PaymentsBoP record trxns in goods, services & assets •b/w residents of country with rest of world for a specified time period typically a year•Two main accounts in BoP•

1. Current Account: records exports and imports in goods and services and transfer payments

pvt transfers by citizens of one country to those of another○

3 basic categories of invisible imports/exports:•Invisible imports and exports not taken into consideration for calculation of trade deficit or surplus•

=> possible to have trade deficit yet current account surplus (invisible exports are way larger than trade balance)•Adding trade in services and net transfers to trade balance, we get Current Account balance, surplus and deficit•

Current account balance: sum of balance of merchandise trade, services and net transfers received from rest of world. •

=> potentially spurs economic growth because we can import now & make them into finished products later and export them thus causing a temporary deficit

○

or high rate of investment •

or both (India's CAD is 1.5 - 2.5% of GDP)•

CAD reflects •

Reduce fossil fuel dependence •

Will ensure savings are invested into economy rather than Gold ○

↓ Inflation & ensure +ve Real Interest rate •

boost services but alone insufficient => Make in India•Promote FDI - Capital PLUS but Current MINUS => promote tech and stds upgradation to develop competitive indigenous industry to finally boost exports

•

To reduce CAD ?•

2. Capital Account: records all international purchases and sales of assets such as money, stocks, bonds, etc.

Any trxn resulting in a payment to foreigners = debit = −ve sign•Any trxn resulting in a receipt from foreigners = credit = +ve sign•

Capital Account Inflow

Most Stable Most volatile

Capital Account Outflow

Profits of foreign investors•

Open Economy Macroeconomics Wednesday, July 31, 2019 11:10 AM

Finance Page 19

Most StableFDIExternal assistance (Soft loans) ECB

Most volatileFII (FPI) FCNR Foreign Currency Non. Resident a/c

Profits of foreign investors•Indian investments abroad•Repatriation of FCNR A/cs or other foreign savings invested in India

•

Capital account balance: capital flows from rest of world, minus capital flows to rest of the world

BOPBOP deficit or surplus is obtained after adding current and capital account balances•The ↓ (or ↑) in official reserves = overall BOP deficit (or surplus)•

How to face BOP crisis?

Great depreciation of currency•↓ CAD or make it into surplus•Capital surplus should be large (attract investment, Business reforms, EoDB)•Central Bank must have large-FOREX reserve•

BOP crisis occurs when capital account surplus insufficient to finance current deficit •

Twin deficit = High CAD and High FD•

Currency Exchange

Foreign currency assets (FCA) (USD, Euro, Pound Sterling, Canadian Dollar, Australian Dollar and Japanese Yen etc.)•Gold•Special Drawing Rights (SDRs) of IMF •Reserve tranche position (RTP) IMF •

Components of FOREX Reserves•

Devaluation vs Depreciation •

Devaluation - in a fixed rate regime, if own currency value is decreased deliberately. Eg like China does to its Renminbi to boost its exports

Revaluation - ulta

Deprecation - In a floating rate regime, if a currency loses its value bcz of lack of demand for it or its over-supply. Eg when Rupee falls in case of lot of FPI outflows

Appreciation - ulta

Nominal exchange rate = price of one unit of foreign currency in terms of domestic currency•

= nominal exchange rate *

•

It measures international competitiveness of country in intl trade•When real exchange rate = 1, the 2 countries are in purchasing power parity (PPP)•

Real exchange rate = relative price of foreign goods in terms of domestic goods. •

Nominal Effective Exchange Rate (NEER)multilateral rate •= weighted avg of nominal exchange rates of foreign currencies, each weighted by importance to domestic country in intl trade.

•

NEER > 1 => apni currency ka worth zada hai compared to the basket•

Real Effective Exchange Rate (REER)= weighted average of real exchange rates of all its trade partners, the weights being shares of respective countries in its foreign trade.

One foreign currency is traded for another without having to first exchange the currencies into USD•Cross Currency = arrangement where a pair of currencies traded in forex that does not include USD•

↑ interest rates in US => appreciation of USD => everyone starts putting money in various devices at home => demand increase => currency appreciation => INR falls compared to USD

○

Interest rate differential b/w countries.1.

Speculation2.

If one country has higher inflation than another, its exchange rate ↓○

Exchange rates b/w any two national currencies adjust to reflect differences in price levels in two countries○

According to PPP theory, differences in domestic inflation & foreign inflation = major cause 3.

Other things equal, a country whose aggregate demand grows faster than rest of world’s normally finds its currency depreciating because its imports grow faster than its exports

4.

Other factors are more important than relative prices for exchange rate determination in short run. However, in the long run,

purchasing power parity plays an important role5.

Factors affecting exchange rate

ConvertibilityWhy restrictions on convertibility?

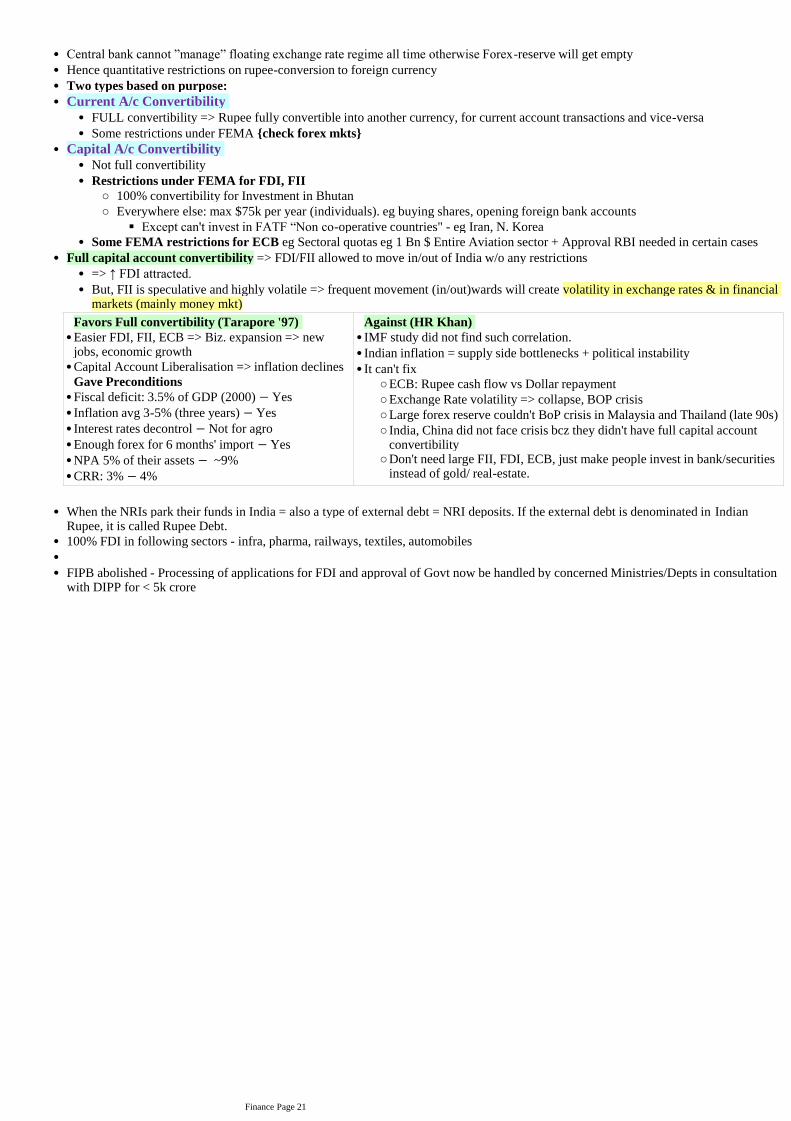

Central bank cannot ”manage” floating exchange rate regime all time otherwise Forex-reserve will get empty•

Finance Page 20

Central bank cannot ”manage” floating e change rate regime all time otherwise Fore -reserve will get empty•Hence quantitative restrictions on rupee-conversion to foreign currency•Two types based on purpose:•

FULL convertibility => Rupee fully convertible into another currency, for current account transactions and vice-versa•Some restrictions under FEMA {check forex mkts}•

Current A/c Convertibility •

Not full convertibility•

100% convertibility for Investment in Bhutan○

cept can't invest in FATF “Non co-operative countries" - eg Iran, N. Korea▪

Everywhere else: max $75k per year (individuals). eg buying shares, opening foreign bank accounts○

Restrictions under FEMA for FDI, FII•

Some FEMA restrictions for ECB eg Sectoral quotas eg 1 Bn $ Entire Aviation sector + Approval RBI needed in certain cases•

Capital A/c Convertibility •

=> ↑ FDI attracted. •But, FII is speculative and highly volatile => frequent movement (in/out)wards will create volatility in exchange rates & in financial markets (mainly money mkt)

•

Full capital account convertibility => FDI/FII allowed to move in/out of India w/o any restrictions•

Large forex reserve couldn't BoP crisis in Malaysia and Thailand (late 90s) ○

India, China did not face crisis bcz they didn't have full capital account convertibility

○

Don't need large FII, FDI, ECB, just make people invest in bank/securities instead of gold/ real-estate.

○

It can't fix •

When the NRIs park their funds in India = also a type of external debt = NRI deposits. If the external debt is denominated in Indian Rupee, it is called Rupee Debt.

•

100% FDI in following sectors - infra, pharma, railways, textiles, automobiles••