Exemptions are the laws that shield a debtor’s assets from their creditors and permit debtors to retain property after the conclusion of their bankruptcy.

4

IN THE FULL GUIDE YOU WOULD GET: A basic understanding of the 2 main types of consumer bankruptcy, valuable insights into evaluating bankruptcy as a debt reduction tool, and practical guidance for finding a quality bankruptcy attorney. Topics covered: - An overview of the bankruptcy process. - Key bankruptcy terms like: “discharge,” “automatic stay,” and “exemptions.” - Chapter 7 bankruptcy: what it is, how it works, and when it is preferred. - Chapter 13 bankruptcy: what it is, how it works, and when it is preferred. - How bankruptcy can save a home from foreclosure or a car from repossession. - 5 good reasons to file bankruptcy. - 5 good reasons not to file bankruptcy. - 3 alternatives to filing for bankruptcy. - 5 questions to ask when interviewing a prospective bankruptcy attorney. CONSUMER’S GUIDE TO BANKRUPTCY Want a free copy of this guide? Just send an email to [email protected]and look for it in your inbox! This is an excerpt from the

Transcript

IN THE FULL GUIDE YOU WOULD GET:

A basic understanding of the 2 main types of consumer bankruptcy, valuable insights into evaluating bankruptcy as a debt reduction tool,

and practical guidance for finding a quality bankruptcy attorney.

Topics covered:

- An overview of the bankruptcy process. - Key bankruptcy terms like: “discharge,” “automatic stay,” and “exemptions.” - Chapter 7 bankruptcy: what it is, how it works, and when it is preferred. - Chapter 13 bankruptcy: what it is, how it works, and when it is preferred. - How bankruptcy can save a home from foreclosure or a car from repossession. - 5 good reasons to file bankruptcy. - 5 good reasons not to file bankruptcy. - 3 alternatives to filing for bankruptcy. - 5 questions to ask when interviewing a prospective bankruptcy attorney.

CONSUMER’S GUIDE TO

BANKRUPTCY

Want a free copy of this guide? Just send an email to [email protected] and look for it in your inbox!

This is an excerpt from the

WHAT ARE EXEMPTIONS?

Exemptions are the laws that shield a debtor’s assets from their creditors and permit debtors to retain property after the conclusion of their bankruptcy.

THE MYTH One of the most common misconceptions about bankruptcy is that you lose everything you own when you file. For the vast majority of consumers, this is simply not true. In 2010, there were 1.139 million Chapter 7 bankruptcies, and less than 6% of these case resulted in a debtor losing assets.

THE TRUTH How is this possible? Well, first off, the purpose of bankruptcy is not to punish you for your past. Second, when you come out of your bankruptcy, you need to retain certain necessities of life in order to make the most of your fresh start. By applying exemptions against your personal property and your home, you shield your assets from your creditors, and you retain them after the conclusion of your bankruptcy.

LIMITATIONS There are limitations to how much property you can protect. Any personal property or home equity that is not protectable can potentially be seized for the benefit of creditors. Some common Tennessee exemptions are listed on the next page.

Got a question about your situation or something you read in this guide? Feel free to email me at [email protected], call me at 615-807-1064,

or visit the website at www.llgtn.com.

3

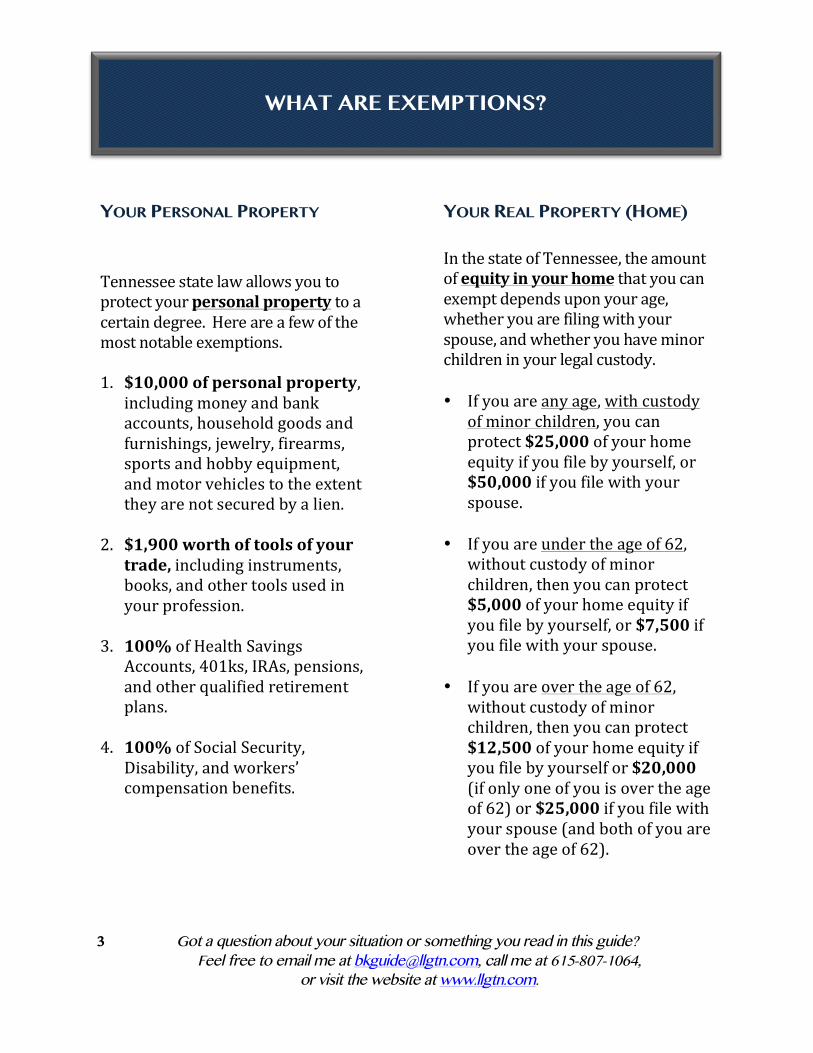

WHAT ARE EXEMPTIONS?

YOUR PERSONAL PROPERTY Tennessee state law allows you to protect your personal property to a certain degree. Here are a few of the most notable exemptions. 1. $10,000 of personal property,

including money and bank accounts, household goods and furnishings, jewelry, firearms, sports and hobby equipment, and motor vehicles to the extent they are not secured by a lien.

2. $1,900 worth of tools of your trade, including instruments, books, and other tools used in your profession.

3. 100% of Health Savings

Accounts, 401ks, IRAs, pensions, and other qualified retirement plans.

4. 100% of Social Security, Disability, and workers’ compensation benefits.

YOUR REAL PROPERTY (HOME) In the state of Tennessee, the amount of equity in your home that you can exempt depends upon your age, whether you are filing with your spouse, and whether you have minor children in your legal custody. • If you are any age, with custody

of minor children, you can protect $25,000 of your home equity if you file by yourself, or $50,000 if you file with your spouse.

• If you are under the age of 62, without custody of minor children, then you can protect $5,000 of your home equity if you file by yourself, or $7,500 if you file with your spouse.

• If you are over the age of 62, without custody of minor children, then you can protect $12,500 of your home equity if you file by yourself or $20,000 (if only one of you is over the age of 62) or $25,000 if you file with your spouse (and both of you are over the age of 62).

Got a question about your situation or something you read in this guide? Feel free to email me at [email protected], call me at 615-807-1064,

or visit the website at www.llgtn.com.

4

ABOUT THE AUTHOR

Gordon H. Boutwell, Atty Lodestone Legal Group 198 E. Main St., Ste. 4 Franklin, TN 37064 615-‐807-‐1064 [email protected] www.llgtn.com

GORDON BOUTWELL is a bankruptcy and consumer protection attorney in Franklin, Tennessee. He has practiced law since 2006, with most of that time dedicated to bankruptcy, personal finance, and consumer advocacy. Over the years he has helped hundreds of individuals, couples, and families with their financial problems. He believes in treating other people the way he would want to be treated in the same situation. He takes the time to get to know his clients, and he educates them on their options for getting out of debt, helping them to understand and evaluate them. He believes bankruptcy is a worthwhile tool to help some (but not all) people get out of debt, and, when combined with financial education and counseling, can be a springboard to financial independence. In March 2011, Gordon and R. Keith Gordon formed the Lodestone Legal Group in Franklin Tennessee, with the purpose of assisting business and private clients by exploring legal options, navigating the legal pitfalls, and providing measurable results through custom solutions and a commitment to the lost art of personal care and client service. Lodestone Legal Group practices in the areas of bankruptcy, debt negotiation and settlement, financial counseling, residential and commercial real estate, estate planning (wills and trusts), and small business and corporate law.