The Year Ahead | 2016 Business Outlook The Year Ahead | 2016 HIGHLIGHTS Fiscal Policy in 2016 Monetary Policy in 2016 Banking Sector in 2016 Capital Market Outlook in 2016 Six key Events to shape Businesses in 2016 A Publicaon of Research & Market Intelligence Unit, Diamond Bank Plc www.diamondbank.com | See Disclaimer on page 9

Transcript

Business Outlook The Year Ahead | 2016

Business Outlook The Year Ahead | 2016 HIGHLIGHTS

Fiscal Policy in 2016

Monetary Policy in 2016

Banking Sector in 2016

Capital Market Outlook in 2016

Six key Events to shape Businesses in 2016

A Publication of Research & Market Intelligence Unit, Diamond Bank Plc

www.diamondbank.com | See Disclaimer on page 9

Business Outlook The Year Ahead | 2016 2

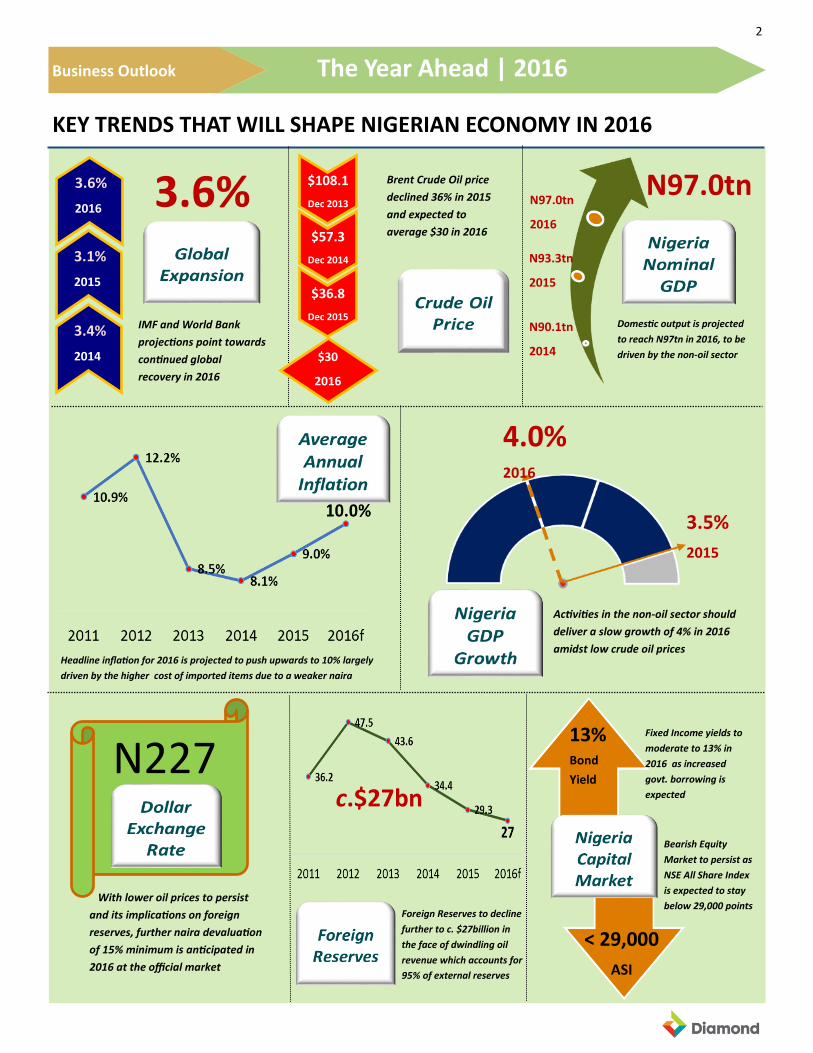

KEY TRENDS THAT WILL SHAPE NIGERIAN ECONOMY IN 2016

Brent Crude Oil price

declined 36% in 2015

and expected to

average $30 in 2016

IMF and World Bank

projections point towards

continued global

recovery in 2016

Domestic output is projected

to reach N97tn in 2016, to be

driven by the non-oil sector

Fixed Income yields to

moderate to 13% in

2016 as increased

govt. borrowing is

expected

Bearish Equity

Market to persist as

NSE All Share Index

is expected to stay

below 29,000 points Foreign Reserves to decline

further to c. $27billion in

the face of dwindling oil

revenue which accounts for

95% of external reserves

3.6%

Headline inflation for 2016 is projected to push upwards to 10% largely

driven by the higher cost of imported items due to a weaker naira

With lower oil prices to persist

and its implications on foreign

reserves, further naira devaluation

of 15% minimum is anticipated in

2016 at the official market

N227

3.6%

2016

3.1%

2015

3.4%

2014

$36.8

Dec 2015

$57.3

Dec 2014

$108.1

Dec 2013

$30

2016

N97.0tn

N93.3tn

2015

N97.0tn

2016

N90.1tn

2014

3.5%

2015

4.0% 2016

Activities in the non-oil sector should

deliver a slow growth of 4% in 2016

amidst low crude oil prices

13%

Bond

Yield

< 29,000

ASI

c.$27bn

Business Outlook The Year Ahead | 2016 3

Business Outlook The Year Ahead | 2016 4

Fiscal Policy in 2016 2016 Budget of “Change”

The proposed 2016 Budget has a total expenditure of N6.08trillion, comprising of N1.8trillion Capital expenditure (N557 billion in 2015) and non-debt recurrent spending of N2.65trillion.

Basic assumptions of the budget as proposed are an optimistic $38pb crude oil price, 2.2mbpd oil output and a 4.4% GDP growth.

The budget is to be financed through N820 billion oil revenues, N1.45 trillion non oil revenues, N1.51 trillion from independent revenues, a domestic borrowing of N984 billion, and foreign borrowing of N900 billion.

Fiscal policy in 2016 will be largely expansionary as the government seeks to stimulate economic activities and generate employment.

Focus on Infrastructure

Capital expenditure of N1.8trillion in the 2016 Budget is expected to focus on infrastructural development to deliver inclusive growth, while fostering further progress in industry, commerce and investment. While the N635billion allocated to transport; works, power and housing ministries can be considered as “seed capital”, public-private partnership initiatives are expected to dominate governments’ infrastructure initiatives. There is however a deliberate attempt to focus on infrastructural developments that will transform agriculture, solid minerals and key job creating sectors of the economy.

Fiscal Discipline and a Larger Tax Base

Full implementation of the Treasury Single Account is expected to yield significant improvements in the collection and remittance of independent revenues to government coffers. Greater oversight is to be directed at the Ministries, Departments and Agencies (MDAs) to ensure that their budget and remittances are in compliance with the Fiscal Responsibility Act. In addition , the government intends to broaden the country’s tax base and improve the effectiveness of revenue collecting agencies in a bid to grow non-oil revenues. Further, subsidies will come in the form of lower tax rates for smaller businesses as well as subsidized funding for priority sectors such as agriculture and solid minerals.

2016 Priorities

2016 budget largely focus on infrastructure development and non-oil revenue particularly from agriculture and solid minerals. Further, the proposed recurrent spending for 2016 prioritized education, defense and health sectors. The adoption of a zero based budgeting approach should ensure that resources are aligned with government’s priorities and allocated efficiently. This is a right step in the right direction.

Reccurrent Expenditure (N'tn) 2.65

Capital Expenditure (N'tn) 1.85

Projected Revenue (N'tn) 3.86

Fiscal Deficit (N'tn) 2.20

Fiscal Deficit (% of GDP) 2.20

Debt Service (N'tn) 1.36

The 2016 Proposed Budget

Key ParametersRecurrent (N' bn) Capital (N' bn)

Education 369.6 Works, Power and Housing 433.4

Defence 294.5 Transport 202.0

Health 221.7 Special Interventions 200.0

Interior Ministry 145.3 Defence 134.6

Top 2016 Expenditure Allocations

Source: Budget Office

Business Outlook The Year Ahead | 2016 5

Monetary Policy in 2016

The CBN will most likely pursue a loose monetary policy in 2016. The MPR will not go higher than the current 11%; while the CRR might witness another downward review.

Banks’ lending rate might however remain at current levels until marked infrastructure improvements and policy initiatives translate to lower cost of doing business for the banks.

A number of fresh intervention funds might be introduced to stimulate economic activities in the non oil sector. Agriculture, solid minerals and SMEs remain key focal points.

Pressure on the Naira is not expected to abate. The CBN will continue a “demand focused” management strategy until reserves improves. A 10%—15% devaluation appear inevitable.

Inflation should inch towards double digit in 2016. Our best case forecast gave a 10% average; driven primarily by FX scarcity and increased money supply.

All Eyes on FX Policy

The naira came under intense pressure in 2015 as the CBN struggle to cope with an unprecedented slump in

dollar inflows due to declining crude oil prices. While rates remained N197—N198 at the official market, the

parallel market experienced greater volatility, trading as high as N260 per Dollar in December 2015. Year

2016 will likely be another challenging year for the Naira as oil price is forecast to slump further.

Nevertheless, we expect more stability and precision in CBN’s FX management policies.

Lower Interest Rates

In a bid to give the economy some monetary stimulus and stimulate growth, the CBN is expected to keep

interest rate low in 2016. The 11% Monetary Policy Rate (MPR) is unlikely to go higher, while the Cash

Reserve Ratio (CRR) might witness another downward review. On the flip side, the economy will have to

invariably cope with a double digit inflation and a lower inflow of Foreign Portfolio Investments with

attendant consequences for real returns and capital market outlook respectively.

More Real Sector Intervention Funds

In addition to the new Anchor Borrowers programme, the CBN will most likely float more intervention funds

for solid minerals, agriculture and SMEs in a bid to ensure that private sector is not crowded out of the debt

market.

Source: CBN

0

10

20

30

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

May

-15

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

Oct

-15

Nov

-15

Dec-

15Monetary Policy Rate Cash Reserve Ratio

17.50

18.00

18.50

19.00

19.50

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Credit to Private Sector Broad Money (M2)

Business Outlook The Year Ahead | 2016 6

Banking Sector in 2016

Competition for retail deposits will be intensified across the industry in 2016 as the industry's competitive frontier shifts to efficiency and margin.

Interest income from investment securities will be muted year-on-year as emerging markets’ capital markets are bound to remain bearish in 2016. Banks that creates quality risk assets will be most competitive.

Another stress test might be conducted in H1:2016 should oil price and economic/business outlook remain depressed.

The integration of BVN with other databases, coupled with the expected asset registry infrastructure should stimulate appetite for retail lending across the banking industry.

2016 Operating Environment: Murky Waters

The operating environment in 2016 will be defined by weak global growth (c.3.6%), depressed crude oil price

outlook (c. $30pb), flat economic growth outlook (c. 4%), further naira depreciation (c. 15%), improved

systemic liquidity, expansionary fiscal policy and a more stable monetary policy. Nevertheless, we see

compelling opportunities in retail, SME, Agriculture, Solid minerals, Hospitality and Entertainment sectors.

Banking in 2016 is Retail

Banks will compete aggressively in the retail front in 2016 in a bid to optimize Net Interest Margin with

cheaper retail deposits. Product development and marketing campaigns strategies will be more of “customer

orientation”, rather than “product orientation”. Emphasis will be placed largely on value-chain marketing and

customer experience, particularly for the middle class market segment.

CBN Regulations—An Eye on FX Policy

We expect the apex bank to review a number of its FX policy in the first Monetary Policy Committee meeting

of the year. Emphasis will be placed on the trade impact of FX shortages and its inherent sovereign risks.

Further, the ripple effect of increasing NPLs and capital inadequacy issues amidst exchange rate exposures

might push the CBN to undertake another stress test in H1:2016.

4.3

3.8

2.9 2.5 2.4

1.8

1.3 1.2

3.0

2.5 2.2

1.6 1.6 1.3

0.8 0.8

1.9 1.8

1.0 1.3 1.3

0.8 0.7 0.5

First Bank Zenith UBA GTBank Access Diamond Skye Fidelity

Banks' 9M:2015 Financials (N'tn)

Total Assets

Deposits

Risk Assets

Source: NSE

Business Outlook The Year Ahead | 2016 7

Capital Market in 2016

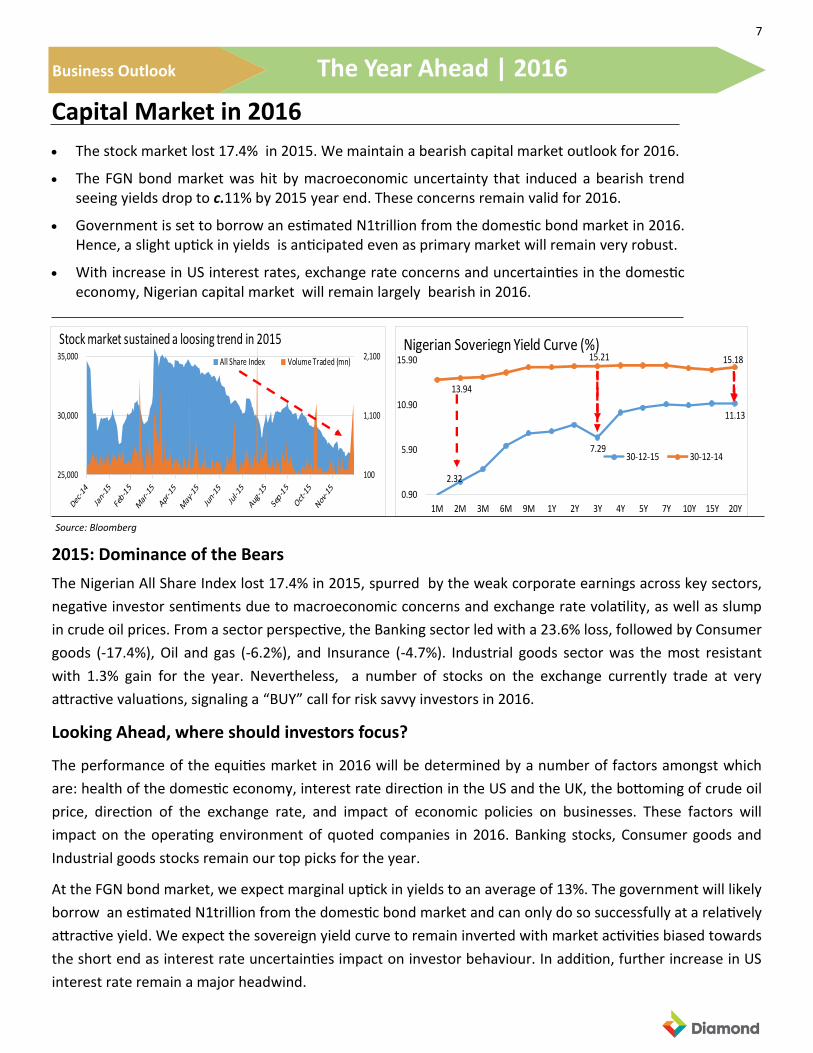

The stock market lost 17.4% in 2015. We maintain a bearish capital market outlook for 2016.

The FGN bond market was hit by macroeconomic uncertainty that induced a bearish trend seeing yields drop to c.11% by 2015 year end. These concerns remain valid for 2016.

Government is set to borrow an estimated N1trillion from the domestic bond market in 2016. Hence, a slight uptick in yields is anticipated even as primary market will remain very robust.

With increase in US interest rates, exchange rate concerns and uncertainties in the domestic economy, Nigerian capital market will remain largely bearish in 2016.

2015: Dominance of the Bears

The Nigerian All Share Index lost 17.4% in 2015, spurred by the weak corporate earnings across key sectors,

negative investor sentiments due to macroeconomic concerns and exchange rate volatility, as well as slump

in crude oil prices. From a sector perspective, the Banking sector led with a 23.6% loss, followed by Consumer

goods (-17.4%), Oil and gas (-6.2%), and Insurance (-4.7%). Industrial goods sector was the most resistant

with 1.3% gain for the year. Nevertheless, a number of stocks on the exchange currently trade at very

attractive valuations, signaling a “BUY” call for risk savvy investors in 2016.

Looking Ahead, where should investors focus?

The performance of the equities market in 2016 will be determined by a number of factors amongst which

are: health of the domestic economy, interest rate direction in the US and the UK, the bottoming of crude oil

price, direction of the exchange rate, and impact of economic policies on businesses. These factors will

impact on the operating environment of quoted companies in 2016. Banking stocks, Consumer goods and

Industrial goods stocks remain our top picks for the year.

At the FGN bond market, we expect marginal uptick in yields to an average of 13%. The government will likely

borrow an estimated N1trillion from the domestic bond market and can only do so successfully at a relatively

attractive yield. We expect the sovereign yield curve to remain inverted with market activities biased towards

the short end as interest rate uncertainties impact on investor behaviour. In addition, further increase in US

interest rate remain a major headwind.

Sources: NSE

100

1,100

2,100

25,000

30,000

35,000

Stock market sustained a loosing trend in 2015

All Share Index Volume Traded (mn)

2.32

7.29

11.13

13.94

15.21 15.18

0.90

5.90

10.90

15.90

1M 2M 3M 6M 9M 1Y 2Y 3Y 4Y 5Y 7Y 10Y 15Y 20Y

Nigerian Soveriegn Yield Curve (%)

30-12-15 30-12-14

Source: Bloomberg

Business Outlook The Year Ahead | 2016 8

Summary—6 key Events to Shape Businesses in 2016

The year 2016 will no doubt be another challenging year for businesses, given the expectation of lower crude

oil price, naira devaluation, inflationary pressures and low foreign portfolio investments. Nevertheless, there

are growth boosters coming from expansionary fiscal and monetary policy, coupled with more responsible

fiscal regime and a focus on key priority sectors of the economy: Infrastructure, Security, Education and the

Non-oil sector. Amidst a slow global growth and the headwinds of higher rates in the US, we present six

major events that will most likely shape Nigerian business environment in 2016.

1. The 2016 “Change” Budget: The N6.08 trillion budget shows a clear deviation from the past in terms of

capital spend, fiscal discipline and policy priority. Budget deficit is to double to N2.2trillion even as the

government plans to revive the economy by tripling capital expenditure to N1.9trillion. If properly

implemented, the 2016 budget should place the country on a sustainable growth path.

2. Lower Crude Oil Prices: There is no end in sight for the global crude oil glut, implying that crude oil

price might fall below $30pb in 2016 since both Iran, OPEC and the US appear convinced that production

is still profitable at such a low price. For the Nigerian economy, this will translate to more pressure on

government oil revenue and foreign reserves, weaker naira and double digit inflation.

3. Loose Monetary and Fiscal Policy: To reverse the declining economic growth trend and achieve the

4.4% budgeted GDP growth for 2016, the economy has to experience significant policy induced liquidity

injections in 2016. This will come in the form of low interest rate environment, more CBN intervention

funds in support of the real sector, increased government expenditure to stimulate activities in critical

sectors, and increased private finances from public-private partnership initiatives. The immediate cost of

this will be higher inflation and a shrink in real returns to approximately 3%.

4. 4% GDP Growth: The economy will experience higher quarterly growth rates of approximately 4% in

2016 relative to the 3% average growth in 2015. This will be driven by the Non-oil sector, particularly

Agriculture, Solid minerals and the SME sectors. A number of businesses and opportunities will be

stimulated across the value chain of these sectors.

5. Lower Consumer Spending: The 2016 is intuitively a year for austerity measures. The constraints of

slow economic growth and low oil prices might imply that some state governments will not be able to

meet salary obligations in 2016. Aggregate disposable income will be impacted, hence consumer

expenditure will head south. This will impact effective demand, private investment and employment.

6. Weaker Naira: Businesses will need to brace up and devise means of hedging the inevitability of a

weaker naira in 2016. More worrisome is that the FX challenge confronting the country is an obvious

“unavailability” of foreign exchange due to low crude prices. While this presents a rare opportunity for

few businesses that depend on locally available inputs, a larger segment of the economy where

international financial flows are indispensable will be hard hit.

Business Outlook The Year Ahead | 2016 9

How Diamond

Can Help

We will help you achieve your financial objectives by

sticking to our mission of consistently exceeding

customer expectation by providing value-adding

solutions through professional and highly motivated

people to deliver excellent financial performance in all

markets where we operate. Based on our experience in

working with broad based customer groups, Diamond

Bank has the right combination of capabilities,

knowledge, operational footprint, technology and

people to create an awesome customer experience.

Registered Office

Diamond Bank PLC

Plot 4, Block 5, BIS Way, off Lekki-Epe Expressway