22

The Future of Europe: Capital Markets 14th Barcelona GSE Trobada October 2016 Fernando Broner CREI, UPF, Barcelona GSE

| Date post: | 08-Feb-2017 |

| Category: |

Economy & Finance |

| Upload: | barcelona-graduate-school-of-economics-gse |

| View: | 67 times |

| Download: | 2 times |

TheFutureofEurope:CapitalMarkets

14thBarcelonaGSETrobada

October2016

FernandoBronerCREI,UPF,BarcelonaGSE

Financialstructure:SizeandcomposiIonofcapitalmarkets(%GDP)

Financialstructure:Financingofnon-financialfirms(%GDP)

Equitymarkets

• EuropeanSecuriIesandMarketsAuthority(ESMA)– createdin2011– butweakcoordinaIonmechanismratherthaneffecIveregulator

• InternaIonalFinancialReporIngStandards(IFRS)– adoptedin2002– butimplementaIonandenforcementislimited

• HomebiasinequityissIlllarge– 64%ofEUand61%ofeuro-areaequityhelddomesIcally

• Especiallylowforbanks– interbankflowsareintheformofdebt

BankconcentraIonanddiversificaIon

Shareofassetsheldbyforeignbanks

Banks

• LowdiversificaIonofbankrisks– smallonaverage

• especiallyinGermany,ItalyandBelgium• lesssoinSpain,FranceandNetherlands

– geographicallyconcentrated• homebias• subsidiariesinsteadofbranches

– cross-countryexposureviadebtinstruments

Banks:CurrentinsItuIonalarrangement

Banks:CrisisprevenIon

• Rulemaking– EuropeanCommission(EC)andBankingAuthority(EBA)

• Supervision– ECBunderSingleSupervisoryMechanism(SSM)

Banks:SingleSupervisoryMechanism

Banks:CrisisprevenIon

• Rulemaking– EuropeanCommission(EC)andBankingAuthority(EBA)

• Supervision– ECBunderSingleSupervisoryMechanism(SSM)– atregulatedenIty(subsidiary)level

• consolidatedlevelwouldfavorintegraIon• butinconsistentwithnaIonaldepositinsurance

Banks:Crisismanagement

• Lenderoflastresort– NaIonalCentralBanks

• accesstoECBfundsbutNCB’sholdrisk• Depositinsurance

– naIonallevel• ResoluIon

– SingleResoluIonMechanism/Fund(SRM/SRF)• SRFfundedfrombankcontribuIons• bail-in:8%ofliabiliIesfromshareholdersandcreditors• bail-out:5%ofliabiliIes

• Fiscalbackstop– EuropeanStabilityMechanism(ESM)

• Fundsgovernmentssothattheycanfundbanks

Sovereigndebt:Spreads

Sovereigndebt

• ReducIonofspreadsdueto– expectedbail-outs– highercostofdefault

• Notnecessarilyefficient– excusabledefaults

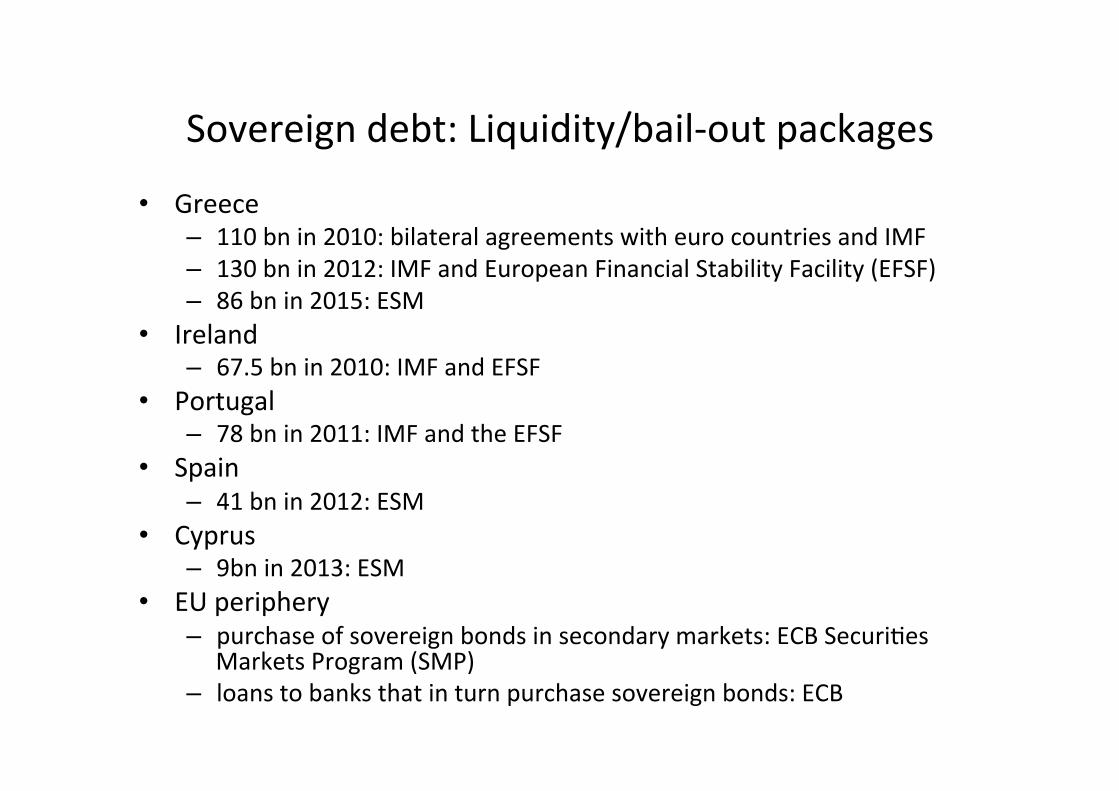

Sovereigndebt:Liquidity/bail-outpackages

• Greece– 110bnin2010:bilateralagreementswitheurocountriesandIMF– 130bnin2012:IMFandEuropeanFinancialStabilityFacility(EFSF)– 86bnin2015:ESM

• Ireland– 67.5bnin2010:IMFandEFSF

• Portugal– 78bnin2011:IMFandtheEFSF

• Spain– 41bnin2012:ESM

• Cyprus– 9bnin2013:ESM

• EUperiphery– purchaseofsovereignbondsinsecondarymarkets:ECBSecuriIes

MarketsProgram(SMP)– loanstobanksthatinturnpurchasesovereignbonds:ECB

Sovereigndebt:Liquidity/bail-outpackages

• ECB:“Monetarypolicy”– purchaseofsovereignbondsinsecondarymarkets– loanstobanksthatinturnpurchasesovereignbonds

• ESM:Financialassistance– loanstogovernments– debtpurchases:primaryandsecondarymarkets– bankrecapitalizaIons:throughgovernmentsordirect

• ESM:EssenIallyabank– capitalprovidedbyalleuroareacountries– borrowsverycheaply

• ESM:unclearrole– providesliquidityassistance– improvescredibility– isatransferscheme

Sovereigndebt:ESM-IMFmaturityandrates

Sovereigndebt:ESM-IFMloansizes

0

20

40

60

80

100

120

03/2008

08/2008

01/2009

06/2009

11/2009

04/2010

09/2010

02/2011

07/2011

12/2011

05/2012

10/2012

03/2013

08/2013

01/2014

06/2014

11/2014

Cyprus

ESMdebt(%GDP) IMFdebt(%GDP) Marketdebt(%GDP)

0

50

100

150

200

12/2008

04/2009

08/2009

12/2009

04/2010

08/2010

12/2010

04/2011

08/2011

12/2011

04/2012

08/2012

12/2012

04/2013

08/2013

12/2013

04/2014

08/2014

12/2014

Greece

ESMdebt(%GDP) IMFdebt(%GDP) Marketdebt(%GDP)

020406080100120140

12/2008

04/2009

08/2009

12/2009

04/2010

08/2010

12/2010

04/2011

08/2011

12/2011

04/2012

08/2012

12/2012

04/2013

08/2013

12/2013

04/2014

08/2014

12/2014

Ireland

ESMdebt(%GDP) IMFdebt(%GDP) Marketdebt(%GDP)

020406080100120140

12/2008

04/2009

08/2009

12/2009

04/2010

08/2010

12/2010

04/2011

08/2011

12/2011

04/2012

08/2012

12/2012

04/2013

08/2013

12/2013

04/2014

08/2014

12/2014

Portugal

ESMdebt(%GDP) IMFdebt(%GDP) Marketdebt(%GDP)

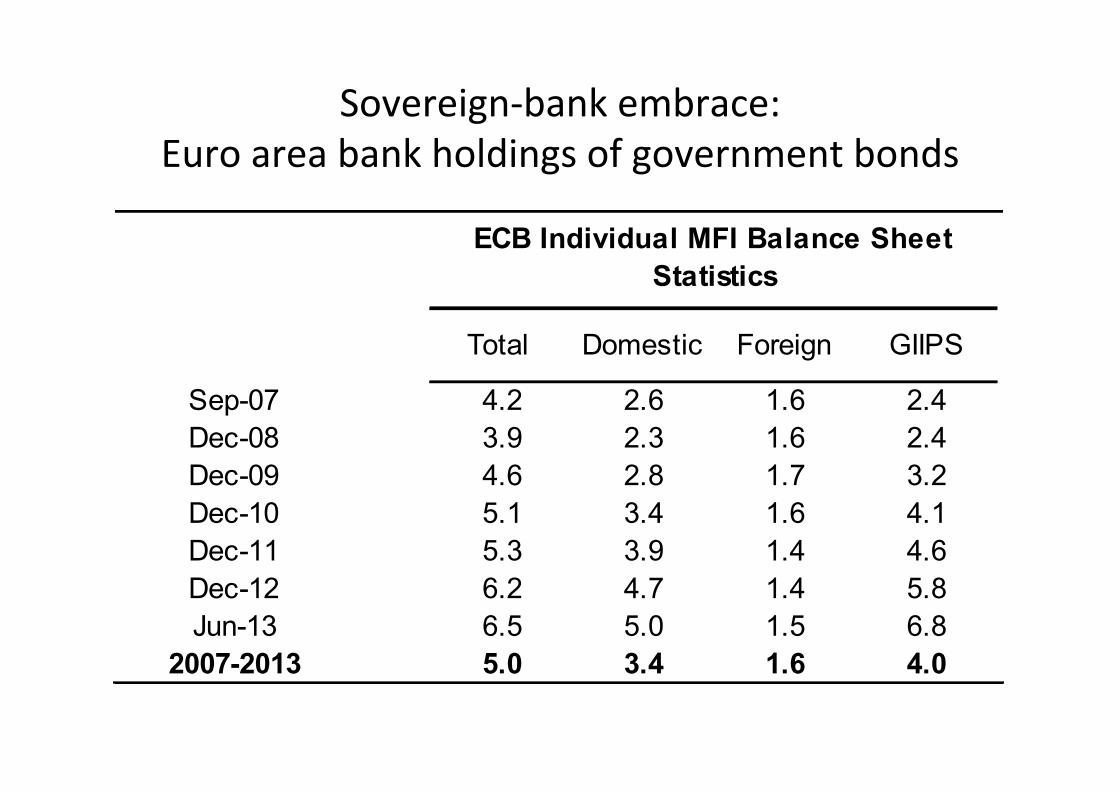

Sovereign-bankembrace:Euroareabankholdingsofgovernmentbonds

Bankscope

Total Domestic Foreign GIIPS Total

Sep-07 4.2 2.6 1.6 2.4 Dec-07 4.5Dec-08 3.9 2.3 1.6 2.4 Dec-08 4.0Dec-09 4.6 2.8 1.7 3.2 Dec-09 4.8Dec-10 5.1 3.4 1.6 4.1 Dec-10 5.1Dec-11 5.3 3.9 1.4 4.6 Dec-11 5.2Dec-12 6.2 4.7 1.4 5.8 Dec-12 5.7Jun-13 6.5 5.0 1.5 6.8 Dec-13 6.0

2007-2013 5.0 3.4 1.6 4.0 2007-2013 5.1

ECB Individual MFI Balance Sheet Statistics

Sovereign-bankembrace:Fiscalcostofbankingcrises

0

10

20

30

40

50

60

70

80Italy

Luxembo

urg

Austria

Germ

any

Belgium

Unite

dStates

Unite

dKingdo

m

Denm

ark

Netherland

s

Latvia

Ukraine

Spain

Gree

ce

Iceland

Ireland

FiscalCosts(%ofGDP) Increaseinpublicdebt(%ofGDP)

Sovereign-bankembrace

• Holdingsofgovernmentdebtaffectsbanksby– crowdingoutlendingtoprivatesector– exposuretosovereignrisk

• Bankexposureaffectsgovernments– fiscalcosts

• InsItuIonalsetupencouragessovereign-bankembrace– ECBsupportsgovernmentsthroughbanks(lowriskweights)

– ECBlenderoflastresortthroughNCBs– ESMbankresoluIonthroughgovernments

Thefuture(?)• ReduceremainingbarrierstointernaIonaldiversificaIoninequity• Improvebankrisksharing

– equityexposure– consolidaIonacrosscountries– internaIonalbranches– regulatebanksubsidiariesasconsolidates

• Movelenderoflastresortanddepositinsurancetoeuro-arealevel• Reducesovereign-bankembrace

– directlenderoflastresort– directESMfundingtorecapitalizebanks– limitexposuretoindividualsovereigns– appropriateriskweightsforsovereignexposure