University of the Witwatersrand, Johannesburg School of Accountancy Base Erosion and Profit Shifting in South Africa: A critical analysis of the effectiveness of the transfer pricing rules with regard to the elimination of profit shifting. Xolani Mpanza A research report submitted to the Faculty of Commerce, Law and Management, University of Witwatersrand, Johannesburg, in partial fulfilment of the requirements for the degree of Master of Commerce (specialising in Taxation). Johannesburg 2017

Transcript

University of the Witwatersrand, Johannesburg

School of Accountancy

Base Erosion and Profit Shifting in South Africa: A critical

analysis of the effectiveness of the transfer pricing rules

with regard to the elimination of profit shifting.

Xolani Mpanza

A research report submitted to the Faculty of Commerce, Law and Management,

University of Witwatersrand, Johannesburg, in partial fulfilment of the requirements for

the degree of Master of Commerce (specialising in Taxation).

Johannesburg 2017

DECLARATION

I declare that this research is my own unaided work. It is submitted for the degree of

Masters in Commerce in the University of Witwatersrand, Johannesburg. It has not

been submitted before for any other degree or examination at any other university.

~----

Xolani Mpanza

17 April 2017

2

ACKNOWLEDGEMENTS

I would like to extend my sincere appreciation to the following:

My Lord and my saviour for His enduring love and grace, I wouldn't have been able to complete this task if it wasn't for His mercy. He deserves the glory.

My wife and my son for their encouragement and support, your inspiration gave me strength to complete this research. Thank you for believing in me

My mother and my siblings for their support and interest in my studies, I really appreciate your unwavering support.

My study leader, Roy Blumenthal, for his guidance and support throughout the duration of the research.

3

ABSTRACT

Tax base erosion and profit shifting (BEPS) is a key tax issue both locally and

internationally. Multinational corporations are constantly trying to find means of

reducing the amount of taxation that is payable by identifying gaps in tax laws. The

aim is to lower the taxation that the group would be liable for. This study will analyse

the developments of tax base erosion and profit shifting. There will also be an

examination and comparison of South African transfer pricing laws with other

countries' tax laws (United State of America, United Kingdom, Australia and Nigeria),

specifically with regards to discouraging profit shifting in order not to obtain a tax

advantage. Section 31 of the Income Tax Act 58 of 1962, is one of the tools that is

currently being utilised by South Africa in addressing the issue of profit shifting. An

analysis of Section 31 will be undertaken and it will be necessary to consider whether

there are any loopholes or vagueness in the tax laws that may result in taxpayers

manipulating the interpretation of the law in order to obtain a tax advantage. Profit

shifting is a global problem that has left many countries deliberating on what could be

an ideal solution. This study will also propose recommendations that might be used by

Commissioner for the South African Revenue Service.

Key Words: tax base erosion, profit shifting, impermissible tax avoidance,

Organisation for Economic Co-operation and Development, aggressive tax planning,

transfer pricing, tax gap, tax avoidance, scheme, abnormalities, advanced pricing

agreement, commercial substance, base erosion and profit shifting,

4

LIST OF ACRONYMS

APA Advanced pricinq aqreement BEPS Base erosion and profit shiftinq CFC Controlled Foreiqn Company DTC Davis Tax Committee HMRC Her Majesty's Revenue and Customs IRS Internal Revenue Service, USA SAAS South African Revenue Sevice TP Transfer Pricing MAP Mutual agreement procedure MNEs Multinational enterprises OECD Organisation for Economic Co-operation

and Development, PE Permanent Establishment USA United State of America UK United Kinqdom

5

TABLE OF CONTENTS

DECLARATION

ACKNOWLDEGMENT

PROPOSED ABSTRACT

LIST OF ACRONYMS

CHAPTER 1 Introduction

1.1 Background

1 .2 Problem statement

1 .3 Sub-problems

1.4 Purpose statement

1 .5 Research and design methods

1.6 Brief oveNiew of chapters

CHAPTER 2 Analysis of Section 31

2.1 Introduction

2.2 The concept of transfer pricing

2.3 The old transfer pricing rules

2.4 The new transfer pricing rules

CHAPTER 3 Risk posed by base erosion and profit shifting

3.1 Introduction

3.2 The economic impact of BEPS

3.3 Tax havens' impact on the spread of BEPS

3.4 Impact of strict tax laws on investment

CHAPTER 4 Lack of commercial substance

4.1 Introduction

6

2

3

4

5

9

9

11

12

13

14

15

17

17

17

18

20

22

22

23

26

28

4.2 Simulating transactions to achieve BEPS

4.3 Advance Pricing Agreement

4.3.1 Advantages of APAs

4.3.2 Disadvantages of APAs

28

29

30

32

CHAPTER 5 Necessary actions to be taken to address base erosion and profit shifting

5.1 Introduction 33

5.2 Modification of transfer pricing rules 33

5.3 Comparison of South Africa's transfer pricing rules with international standards 35

5.3.1 United States of America (USA) 35

5.3.1.1 Affected transactions 35

5.3.1 .2 Preferable benchmarking set 35

5.3.1 .3 Advanced pricing agreements 36

5.3.2 United Kingdom 37

5.3.2.1 Advance pricing agreements 37

5.3.2.2 Affected transactions 37

5.3.3 Australia 38

5.3.3.1 Affected transactions 38

5.3.3.2 Advance pricing agreements 38

5.4 Progress made by OECD 39

5.5 Court cases 43

5.5.1 DSG and (others) v HMRC 43

5.5.2 Altera Corp v Commissioner and Xilinx Inc v Commissioner 45

7

CHAPTER 6 Discussion and conclusion

6.1 Introduction

6.2 Outcome of the research

6.3 Recommendation

6.3 Areas requiring further research

Reference List

8

48

48

48

50

51

1.1 BACKGROUND

CHAPTER 1

INTRODUCTION

BEPS is a tax term used to describe international tax planning strategies that rely on

mismatches and gaps that exist between the tax rules of different jurisdictions, to

minimise multinational entities' tax that is payable by the group, by either making tax

profits 'disappear' or shifting profits to low tax jurisdictions where there is little or no

genuine activity. According to the Financial Times (n.d.):

BEPS strategies are not illegal; rather they take advantage of different tax rules operating in different jurisdictions, which may not be suited to the current global and digital business environment.

Profit shifting can be regarded as a tax avoidance scheme and in terms of the OECD

(n.d.), tax avoidance is an:

... arrangement of a taxpayer's affairs that is intended to reduce its ability and that although the arrangement could be strictly legal, it is usually in contradiction with the intent of the law it purports to follow.

It is important to note that tax avoidance is not tax evasion. Tax evasion is where a

taxpayer unlawfully arranges his affairs in such a way that he escapes any tax liability

which he ought to pay. Multinational entities that are involved in profit shifting activities

usually take advantage of the poorly written tax laws. In an increasingly

interconnected world, national tax laws have not kept pace with global corporations,

fluid capital, and the digital economy, leaving gaps that can be exploited by companies

who avoid taxation in their home countries by pushing activities (genuine or otherwise)

abroad to low or no tax jurisdictions. This undermines the fairness and integrity of the

tax systems.

According to the OECD's Action Plan report on base erosion and profit shifting, there

are 15 specific actions that are needed in order to equip governments with instruments

that would address the arrangements those results to double non-taxation. These 15

actions include:

• Address the tax challenges of the digital economy.

• Neutralise the effects of hybrid mismatch arrangements.

• Limit base erosion via interest deductions and other financial payments.

• Counter harmful tax practices more effectively, taking into account

transparency and substance.

• Prevent treaty abuse.

• Prevent the artificial avoidance of permanent establishment status.

• Develop rules to prevent BEPS by moving intangibles among group members.

• Develop rules to prevent BEPS by transferring risks among, or allocating

excessive capital to, group members.

• Develop rules to prevent BEPS by engaging in transactions which would not, or

would only very rarely, occur between third parties.

• Establish methodologies to collect and analyse data on BEPS and the actions

to address it.

• Require taxpayers to disclose aggressive tax planning arrangements, this

would be a case whenever a taxpayer actively push limits of what is allowed in

terms of the law e.g. this may be stretching the definition of a term in legislation

to access a loophole, or dressing up an arrangement so that it appears to be

something else (Beattie, 2015).

• Make dispute resolution mechanisms more effective.

• Analyse the tax and public international law issues related to the development

of a multilateral instrument.

• Re-examine transfer pricing documentation.

In terms of the OECD (n.d.), profit shifting reduces government revenue and it

contributes to the increase in the tax gap, therefore it is critical for governments to

prevent it at all costs. Some of the effects of profit shifting include a corrosive effect

upon taxpayer compliance, the uneconomic allocation of resources, upward pressure

on marginal tax rates, an unfair redistribution of the tax burden and a weakening of the

ability of Parliament and National Treasury to set and implement economic policy.

Transfer pricing rules play a critical role in ensuring that tax avoidance is reduced or

eradicated. According to the OECD (n.d.), 'transfer pricing is the price charged by a

company for goods, services or intangible property to a subsidiary or other related

10

company·. It results in the setting of prices among related entities. In terms of the

OECD (n.d.), ·Abusive transfer pricing occurs when income and expenses are

improperly allocated for the purpose of reducing taxable income·. For example, if a

subsidiary company sells goods to a parent company, the cost of those goods is the

transfer price. Legal entities considered under the control of a single corporation

include trusts and companies that are wholly or majority owned ultimately by the

parent corporation. Certain jurisdictions consider entities to be under common control

if they share family members on their boards of directors. Transfer price can be used

as a profit allocation method to attribute a multinational corporation's net profit (or

loss) before tax to other countries where it does business.

Appropriate clarification of transfer pricing laws by the South African government, will

make the implementation of transfer pricing laws easier and that might reduce non

compliance. In April 2012, an amendment to Section 31 of the Income Tax Act was

done in order to modernise South African transfer pricing rules and to bring it in line

with the latest transfer pricing guidelines issued by the OECD.

1.2 THE PROBLEM STATEMENT

There are a lot of uncertainties with regards to the practical application of transfer

pricing rules contained in Section 31 of the Income Tax Act.

The complexity of transfer pricing regulations and the continuously changing transfer pricing environment make it challenging for multinational companies to manage their transfer pricing position and to be compliant with the latest requirements (Wolf & Verhoosel 2014).

Non-compliance with the transfer pricing rules is increasing the tax gap and has

an impact on the economic stability of South Africa. There might still be a

substantial amount of uncertainty as to how SARS interprets and implements the

new transfer pricing rules. Of particular interest in this regard is how SARS intends

applying the arm's-length principle in the context of the thin capitalisation rules.

These uncertainties may create loopholes that weaken the fight against profit

shifting.

Section 31 is causing structural problems and uncertainty, as the literal wording unduly focuses on isolated transactions as opposed to arrangements driven by an overarching profit objective. In addition, SARS is of the opinion that the language gives rise to an excessive emphasis of the Comparable Uncontrolled Price (CUP) method as opposed to other more practical transfer pricing methodologies. Further, SARS is also of the opinion that the current legislative emphasis on "price" as opposed to "profits" does not align with the wording in the associated

11

enterprises articles in the tax treaties concluded by South Africa (South Africa Chartered Accountant, 2014).

Due to globalisation, foreign companies are investing in South African companies

or creating South African subsidiaries and the inconsistencies of the transfer

pricing rules between their countries and those of South Africa can be frustrating.

These inconsistencies may lead to disinvestments, therefore it is fundamental for

South Africa's transfer pricing laws to be in line with international standards.

Profit shifting has continued to grow and it's causing harm in South Africa's

economy. It's either that South Africa's transfer pricing laws are ineffective or they

are too complicated for taxpayers. A detailed analysis of South Africa's transfer

pricing laws will assist in diagnosing the root cause of the growth in profit shifting

and tax base erosion. It will also be worthwhile to look at other tax authorities and

the OECD to verify that South Africa's transfer pricing laws are aligned with

international standards. We may also have to revisit our double tax agreements,

to ensure that they do not encourage the increase of profit shifting.

The focus of this report is to determine whether the South Africa's transfer pricing

rules are able to address the challenges posed by BEPS.

1.3 THE SUB-PROBLEMS

1 .3.1 This research will analyse the impact of the allocation of taxable profits to

locations different from those where the actual business activity takes place

and how current tax laws can be adjusted to eliminate the unreasonable tax

avoidance by taxpayers. The writer will look at the remedies available to SARS

where such a contrived transaction has been entered into. A critical analysis of

the new Section 31 of the Income Tax Act will be done in order to ascertain

whether:

• It's clear and easy to understand;

• Its effectiveness in addressing profit shifting. This would be done by

ascertaining whether South African transfer pricing laws are in line with

international best practice. A comparison will be done between South

12

Africa's transfer pricing tax laws and those of some developed countries

like USA and UK

• It's able to achieve its objective.

As the world is affected by BEPS, it's important to understand South Africa's

exposure to BEPS and ascertain if South Africa's tax laws are stringent enough

to safeguard the economy from BEPS.

1 .3.2 A comparison will be done between the old and the new Section 31 of the

Income Tax Act. An analysis will be done to ascertain whether it was necessary

to amend the old section and if the new changes will improve compliance and

reduce profit shifting.

It is yet to be seen how the new Section 31 of the Income Tax Act would be

able to address challenges posed by BEPS, therefore this necessitate the

importance of doing a literature review of the Section 31 .

1 .3.3 A comparison will be done between transfer pricing rules in South Africa and

other major economies. English speaking countries that are leading tax

jurisdictions with high Gross Domestic Product (GDP), being the United States

of America (USA) and the United Kingdom (UK) have been selected for the

purposes of the comparison. Also, Australia was also selected for comparison,

as some of our legislation is borrowed from that country. The writer will look at

potential loopholes in the legislation of these different countries. An analysis of

the advantages and disadvantages of having an Advanced Pricing Agreement

(APA) will also be done. The writer will also look at significant judgments, both

locally and internationally. A critical analysis of precedents these judgments

have set and how they have influenced the approach that can be adopted

regarding the substance over form issue.

South Africa can't afford to be left behind while other tax authorities have

advanced tax laws which address challenges posed by BEPS. A comparison of

our tax laws is therefore significant in ensuring that our tax laws are in line with

those of major economies.

13

1.3.4 Profit shifting cannot be combated without harmony among other countries and

that is what the OECD has been striving to achieve. The writer will next look at

the role of the OECD regarding Base Erosion and Profit Shifting (BEPS). There

will be an assessment of the action plans proposed by the OECD in evaluating

the practicality of the OECD's action plan. South Africa's transfer pricing laws

will also be compared to the OECD's action plan.

Globalisation made the world to be small as most entities find themselves

interacting with stakeholders from all over the world. In ensuring that South

Africa is a good citizen of the global market we would have to ensure that our

tax laws are in line with the OECD.

1.4 PURPOSE STATEMENT

Profit shifting has continued to grow and it's causing harm in South Africa's economy.

It's either South Africa's transfer pricing laws are ineffective or they are too

complicated for taxpayers. The goal of this study is to analyse the effectiveness of

South Africa's transfer pricing laws in order to diagnose the root cause of growth in

profit shifting and tax base erosion.

This study will enable lawmakers on how to tighten transfer pricing laws in order to

minimise profit shifting. The study will assist in understanding variances between

South African's tax laws and those of other tax authorities.

1.5 RESEARCH METHODOLOGY

1.5.1 The research method adopted is of a qualitative, interpretive nature, based on a

detailed interpretation and analysis of amongst other things, case law.

An extensive literature review and analysis will be undertaken that includes the

following sources -

• Books;

• Cases;

• Electronic databases;

• Electronic resources - internet;

• Journals;

14

• Magazine articles;

• Publications;

• Statutes.

1.6 BRIEF OVERVIEW OF CHAPTERS

1.6.1 Chapter 1: Introduction

This chapter will introduce the background and significance of the research, the

problems and sub-problems identified and the research methodology used. The

research will also consist of an analysis of literature that is available on the

subject matter and a qualitative review.

1.6.2 Chapter 2: Analysis of transfer pricing legislation

With effect from 01 October 2011, South African Transfer Pricing legislation

was significantly changed by the implementation of an amendment to Section

31 to the Income Tax Act 58 of 1962. A comparison will be done between the

old and new Section 31 .

1.6.3 Chapter 3: Risk and challenges posed by base erosion and profit shifting

The purpose of this chapter is to look into the economic impact of base erosion

and profit shifting. It can be argued that to a certain extent the cause of

Greece's financial misfortunes can be attributed to tax evasion (Karnitschnig &

Stamouli 2015). Profit shifting has a potential of increasing the tax gap for a lot

of countries. Some countries are very cautious about tightening tax laws in

order not to discourage investment. This chapter will analyse the notion that

countries with strict tax laws are likely to lose direct foreign investment

compared to the so called tax havens.

1.6.4 Chapter 4: The Lack of Commercial Substance approach

This chapter examines the way in which some taxpayers avoid tax by entering

into a transaction with no commercial value. There are a number of simulated

transactions and schemes that have been created by taxpayers which involves

the claiming of excessive interest and incurring unnecessary debt or entering

into unnecessary transaction with connected parties. The Commissioner for the

15

SARS is currently imposing heavy penalties on taxpayers found to be evading

taxation as per Section 222 and 223 of the Tax Administration Act however the

effectiveness of such measures are still questionable. The chapter will analyse

whether it might be necessary to have an advance pricing agreement (APA) in

order to increase compliance. Sections BOA to SOL of Income Tax would also

be examined to ascertain the impact it might have on transfer pricing

compliance.

1.6.5 Chapter 5: Necessary actions to be taken to address base erosion and profit shifting

This study will examine possible actions that can be taken to simplify the

transfer pricing rules and to increase compliance. The OECD has already made

significant progress in trying to come up with the means of discouraging tax

avoidance. This study will critically analyse the work that has already been

done by the OECD and ascertain if it is sufficient. The transfer pricing laws of

other countries (the United State of America, the United Kingdom, and

Australia) will also be examined and assessed if it will be ideal in South Africa.

The study will also look into the court cases such as DSG and others v HMRC,

Lankhorst-Hohorst Gmbh v Finanzamt Steinfrut and CSARS v NWK Ltd. A

critical analysis will be done on the precedence that has been set by the

outcome of these court cases.

1.6.6 Chapter 6: Conclusion

This chapter will summarise the findings of the research, suggest

recommendations and propose areas requiring further research.

16

2.1 Introduction

CHAPTER 2

ANALYSIS OF SECTION 31

Transfer pricing legislation was implemented to address tax avoidance resulting from

intercompany transactions across borders. The lawmakers decided to make

amendments to Section 31 of the Income Tax Act in 2012. The amended wording in

the new Section 31 of the Income Tax Act, which is effective from 01 April 2012,

changed the structure of the section but not the fundamental principles. The author

would analyse the new Section 31 and also compare it will the previous legislation in

order to assess if it's able to halt base erosion and profit shifting.

2.2 The concept of transfer pricing

2.2.1 Introduction

Globalisation created an environment whereby entities have representation throughout

the world. This resulted in entities acquiring subsidiaries and establishing subsidiaries

in other countries in order to grow revenue. Some multinational companies are

targeting countries with low tax rates by shifting their profits to these so called tax

havens in order to reduce their tax liability. The prices of items sold between

connected companies might not be at arm's length as this is usually done in order to

reduce the tax liability. This can be illustrated in the example below:

Take a beverage company located, say, in Mexico, which has a subsidiary in France. Let's assume that the French subsidiary pays royalties to the Mexican headquarters for the rights to sell its drinks.Taxes are owed in France based on the French subsidiary's results. The higher the royalties paid by the French subsidiary, the lower the taxable profits in France. The French tax authorities will be satisfied if they see that the royalties paid by the French company to its headquarters in Mexico are not higher than those that would be paid to an independent enterprise for a similar transaction. But if the royalties are too high, there is a possibility that profits are being shifted out of France to reduce tax liabilities there. The "arm's length principle" is used to address such issues. Under the arm's length principle, one compares the remuneration from cross border controlled transactions within multinationals with the remuneration from transactions made between independent enterprises in similar circumstances (Silberztein n.d)

17

Transfer pricing legislation was designed to ensure that intercompany transactions

across borders are at arm's lengths and there is no profit shifting between different

jurisdictions.

It is critical for Section 31 to properly address profit shifting otherwise there will be a

major loss to the fiscus. According to Schussler (2012) South Africa's companies pay

the second highest effective tax rate among the biggest 60 economies in the world.

This means that South Africa is among the countries with a high tax rate, therefore it is

likely that companies operating in South Africa would consider shifting profit to

jurisdictions with lower tax rates.

2.3 Old transfer pricing rules

2.3.1 Introduction

The new Section 31 came into operation on 1 April 2012. This meant the principles

that were proposed by the old legislation would have to be disregarded. A brief

summary of the old legislation will enable us to ascertain whether the new legislation

is progressive and there won't be recurring errors from the previous legislation, if any.

The old Section 31 focused on ensuring that a transfer price charged by connected

parties is at an arm's length. The previous section granted the Commissioner of SARS

the discretion to adjust the price paid should he or she not be satisfied that it reflected

an arm's length price. The old section deemed such an adjusted amount to be a

dividend which was historically subject to secondary tax on companies (Hart 2014)

2.3.1 The necessity for changing Section 31

The old Section 31 of the Income Tax Act had to be modernised in order to ensure

that South African transfer pricing laws are in line with the latest transfer pricing

guidelines issued by the OECD. In terms of the old Section 31, the concept of arm's

length was linked to price and not necessary the transaction, operation or scheme

entered into on terms and conditions which would have applied had the parties

involved been independent persons dealing with each other at arm's length

18

(Steenkamp n.d.) This meant should a difference occur or a tax benefit result to one of

the parties, the taxpayer is required to calculate their taxable income based on the

arm's length terms and conditions of the affected transaction.

The wording of the old legislation was causing structural problems and uncertainty, as

the literal wording unduly focused on isolated transactions as opposed to

arrangements driven by an overarching profit objective. In addition, the language gave

rise to an excessive emphasis of the comparable uncontrolled price (CUP) method as

opposed to other more practical transfer pricing methodologies. By not looking into the

whole arrangement, SARS could overlook simulated transactions which have

unprecedented terms and conditions.

The old Section 31 provided that the Commissioner could adjust the consideration in

respect of the transaction to reflect an arm's length price for the goods or services.

This meant that taxpayers were not obliged to make the adjustments on their tax

returns for transactions even if such transactions were not conducted on an arm's

length basis. Taxpayers could therefore file tax returns with excessive deductions, and

then sit and wait and hope for the best - which would be that the Commissioner did not

pick up these excessive deductions. The Commissioner doesn't have capacity to

review all the return submitted by multinational entities, therefore a number of entities

might not comply with transfer pricing legislation and still not be picked up for a tax

audit.

Therefore it is clear that the old legislation had a number of challenges and it was

necessary to make amendments in order to address the shortcomings of the old

Section 31 . Some taxpayers took advantage of the old Section 31 by conducting

aggressive tax planning, which involved shifting extensive amount of profit into tax

havens. The legislation did not concern its self with ensuring that the terms and

conditions of the whole arrangements conducted by South African taxpayers with their

foreign related entities are normal and are not conducted with the motive of obtaining

a tax benefit. Moreover, SARS was heavily burdened with checking that all the

transactions were at arm's length and had to process all the necessary adjustments

into the taxpayers return.

2.4 The new transfer pricing rules

19

In order to eliminate uncertainties brought by the old legislation, the new rules have

been worded similarly to the wording of Article 9 of the OECD Model Tax Convention

on Income and on Capital (OECD 2015), with the focus on the economic substance of

the arrangements between related parties, rather than the pricing of specific

transactions.

The new Section 31 will be applicable whereby:

• Any transaction, operation, scheme, agreement or understanding has been

directly or indirectly entered into between connected persons with a cross

border nexus;

• Any term or condition of that transaction, operation, scheme, agreement or

understanding is different from any term or condition that would have existed

had those parties been independent persons dealing at arm's length; and

• The transaction, operation, scheme, agreement or understanding results or will

result in a tax benefit being derived by any party to it.

The new Section 31 successfully shifts the focus from separate transactions to the

entity-based approach desired by SARS. Section 31 (2) of the Income Tax Act

provides that the new rules are to apply to an "affected transaction" if (i) any term or

condition of that transaction is different from what would have been agreed to between

independent persons dealing at arm's length, and (ii) it results in any tax benefit being

derived by a person who is party to the transaction, operation, scheme, agreement or

understanding. Analysing the new wording leads one to believe that the arm's length

principle is more far-reaching than before; being applicable to any party to a

transaction, operation, scheme, agreement or understanding. Large corporates will

now be required to ensure that the overall transaction does not result in an undue tax

benefit that is contrary to the arm's length principle (Hart 2014). Aggressive taxpayer

can get into transactions which are not commercially viable in other to obtain a tax

benefit, the new legislation will assist in ensuring that such transactions are

challenged and profit shifting is halted.

20

The new rules stipulate that the taxable income of a party to the affected transaction

who derives a tax benefit must be calculated as if the affected transaction had been

entered into on the terms and conditions that are expected between parties dealing

with each other on an arm's length basis. This requirement effectively removes the

Commissioner's discretion to make an adjustment and shifts the responsibility to make

a voluntary transfer pricing adjustment onto each party to the transaction. Determining

whether the terms and conditions of a transaction are different to what would have

been agreed to between independent persons dealing at arm's length might not

always be an easy excise to conduct. Certain businesses don't have a standard model

and therefore it might be difficult to come up with a benchmark. For example, a bank

might fund Project A at 11 % interest rate, with a 5 year payment term, while Project B

might be funded at 8% interest rate, with a 5 year payment term. Should a connected

foreign entity decides to run Project C, it will be difficult to ascertain an appropriate

interest rate that will convince SARS that the transaction is at arm's length. (Hart

2014)

Transfer pricing adjustments (whether voluntary or through a SARS audit) are no

longer considered to be a deemed dividend, but rather the adjusted amount is seen to

be a loan on which interest is due (on an arm's length basis). The interest to be

charged on this deemed loan may be discharged if the loan is repaid in the same

financial year. This further indicates that the interest charge will be indefinite, pending

the settlement of the debt created through the adjustment (Hart 2014).

21

CHAPTER 3

Risks and challenges posed by base erosion and profit shifting

3.1 Introduction

BEPS poses a serious risk to a number of countries, especially the developing

countries like South Africa. Government expenditure should mainly be funded by tax

revenue instead of borrowed funds, for a country to have a healthy financial status,

this impact of BEPS might make it hard for a lot of countries to attain this. The purpose

of this chapter is to look into the economic impact of base erosion and profit shifting

and the challenges that it poses to society at large.

3.2 The economic impact of BEPS

It can be argued that BEPS is one of the causes of many countries' recent financial

hardships. In the Davis Tax Committee Interim Report (2014), it is stated that

Tax Justice Network report "The Missing Billions" which estimates that GBP12 billion of corporate income tax is lost each year due to tax avoidance by the 700 largest companies in the United Kingdom. For developing countries Oxfam, a non-profit organisation, attributes a revenue loss of USD50 billion to tax avoidance by multinationals (Davis Tax Committee Interim Report, 2014).

This is a serious challenge for many states, as the government can't deliver on its

mandate without having financial resources. According to the Tax Justice Network

report, few issues can be more important to a modern democracy than the integrity of

its tax system. It is deeply troubling, therefore, to discover that the tax system is being

increasingly undermined by the practice of tax avoidance.

The gap between the rich and poor people will increase even further if BEPS is not

properly addressed.

Tax justice and the struggle against tax havens has to be a central part of any inequalityfocused agenda. With some $21-32 trillion in financial assets sitting offshore, largely untaxed, the offshore system of tax havens clearly has mind-bending effects on inequality within and between countries. All that offshore wealth is held by the world's 10 million wealthiest people: and a large share of that by the wealthiest 100,000. Because of tax havens, inequality is certainly significantly worse than what economists measure (read more about that here). Worse still, tax competition is 'compressing' tax systems around the world, with the effect of reducing tax rates on the wealthy and increasing tax rates on the poor. Many other unjust features of tax systems make the problem still worse: corporate tax avoidance, for instance, routinely facilitated by offshore tax shenanigans (Tax Justice Network n.d)

22

Some Global multinational enterprises (MNEs) are obsessed with accumulating wealth

and they have no regard for economic upliftment in countries where they operate.

MNEs need to realise that paying their fair share of tax is to their benefit. A country

with an effective economic system will enable citizens to have buying power which

would enable them to buy MNEs' products.

3.3 Tax havens impact on the spread of BEPS

Tax haven can be defined as a 'country with little or no taxation that offers foreign

individuals or corporations residency so that they can avoid tax at home'. Naturally,

most MNEs would prefer to be in countries where they would pay little or no taxation.

Does this mean countries should compete to have the lowest tax possible in order to

attract foreign investors or would minimum tax revenue received by these countries

collapse their economy?

The Republic of Ireland can be regarded as a tax haven as they have a 12.5%

corporate tax rate, which is lower than international standard's. Ireland is one of the

worst tax havens in the world, it has helped big business to dodge billions of euro.

Bermuda and the Cayman are also used by some big businesses to avoid tax (Irish

Times 2016). Ireland came out of the economic crisis as one of the best performing

economies, with GDP growth rates of 8.5% in 2014 and an extraordinary 26.3% in

2015 (Tax Justice Network 2017). Moreover, it is important to note that Ireland is an

economy dominated by foreign companies. The foreign controlled affiliates provide

almost 50% of employment in the country and 80% of exports (90% of manufacturing

exports), it is clear that foreign investment is plays a significant role in Ireland's

economy. This, combined with Ireland's status as a tax haven, makes Irish GDP

figures particularly vulnerable to profit shifting, therefore most companies will consider

shifting their profits in Ireland, in order to take advantage of low tax rates. Through

transfer pricing, which involves the Irish subsidiary overcharging other parts of the

company based elsewhere for goods and services, profits can be moved from the rest

of the world to Ireland. It can be argued that this kind of internal profits shifting does

very little for the domestic workforce. In some certain cases you would notice that

headquarter companies based in Ireland may be employing very few people or not

23

employing anyone at all. What is even more disappointing is that profits declared in

Ireland are likely to quickly be taken out of the country again (Tax Justice Network

2017).

It can be noticed that tax havens don't really benefit from having little or no taxation.

Moving MNEs headquarters to a tax haven doesn't necessary mean the citizens would

benefit from job creation. The main beneficiaries of BEPS are the MNEs. They pocket

maximum profits without paying their fair share of tax. Employment in Ireland could not

reach crisis levels in Ireland, despite the fact that the country has been experiencing

net emigration, which should decrease the work force. It was also noticed that the

wage share, that is the amount of national income that is paid out as wages, has

declined severely. This means investors did not born the economic costs provoked by

the financial crisis (Tax Justice Network 2017)

The Republic of Ireland's GDP growth, as a tax heaven, is questionable and is it even

possible for countries to follow the Irish development model, which relies on

freeloading of profits earned elsewhere.

This result puts the Irish role as a blueprint for other countries into question. Ireland's strategy of attracting foreign owned companies by low corporate taxation rates can be seen as a beggar-they neighbour strategy, increasing downward competition for taxation in the EU. The strategy is not even clearly positive for Irish citizens, at least not for those relying on wage income. Therefore, it is surprising that the government seems to be willing to continue to compete for foreign owned companies by low corporate taxation rates, as a series of publications of the Department of Finance (2014) seems to indicate as well as the discussion of having to accept tax payments of Apple (Tax Justice Network 2017)

Tax heavens enable the spread of BEPS and they don't get meaningful benefit from it.

We don't have an international watchdog that can stop countries from becoming tax

havens. Perhaps all countries should decide to be tax heavens, then no country would

be a tax haven, however this won't benefit anyone, except for the MNEs.

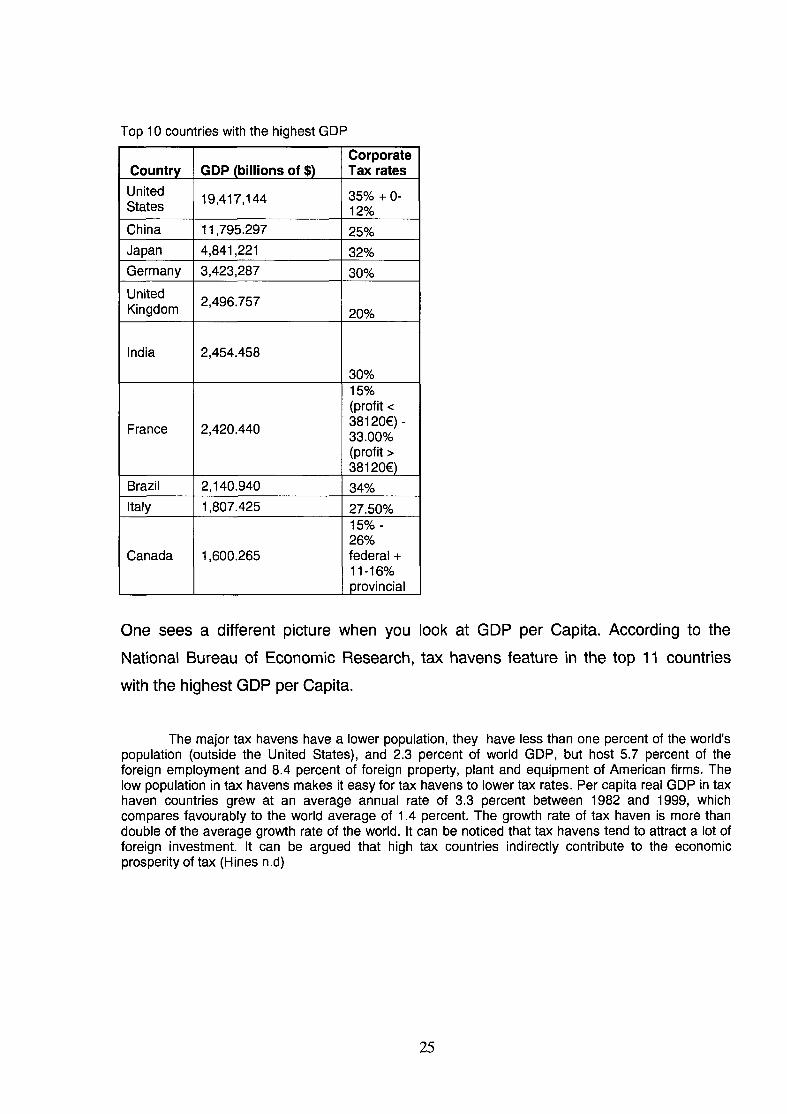

The top 1 O countries with the highest gross domestic product (Statistics times, 2017)

have an average tax rate of 27% (OECD, 2017). This is a clear indication that a

healthy tax rate has a significant impact on the countries' GDP growth. It is no surprise

that none of the countries who are considered to be tax havens feature in the top 1 O

countries with the highest GDP.

24

Top 10 countries with the highest GDP

Corporate Country GDP (billions of $) Tax rates

United 19,417,144 35% + 0-States 12%

China 11,795.297 25% Japan 4,841,221 32% Germany 3,423,287 30%

United 2,496.757

Kingdom 20%

India 2,454.458

30% 15% (profit<

France 2,420.440 38120€)-33.00% (profit> 38120€)

Brazil 2,140.940 34%

Italy 1,807.425 27.50% 15% -26%

Canada 1,600.265 federal+ 11-16% provincial

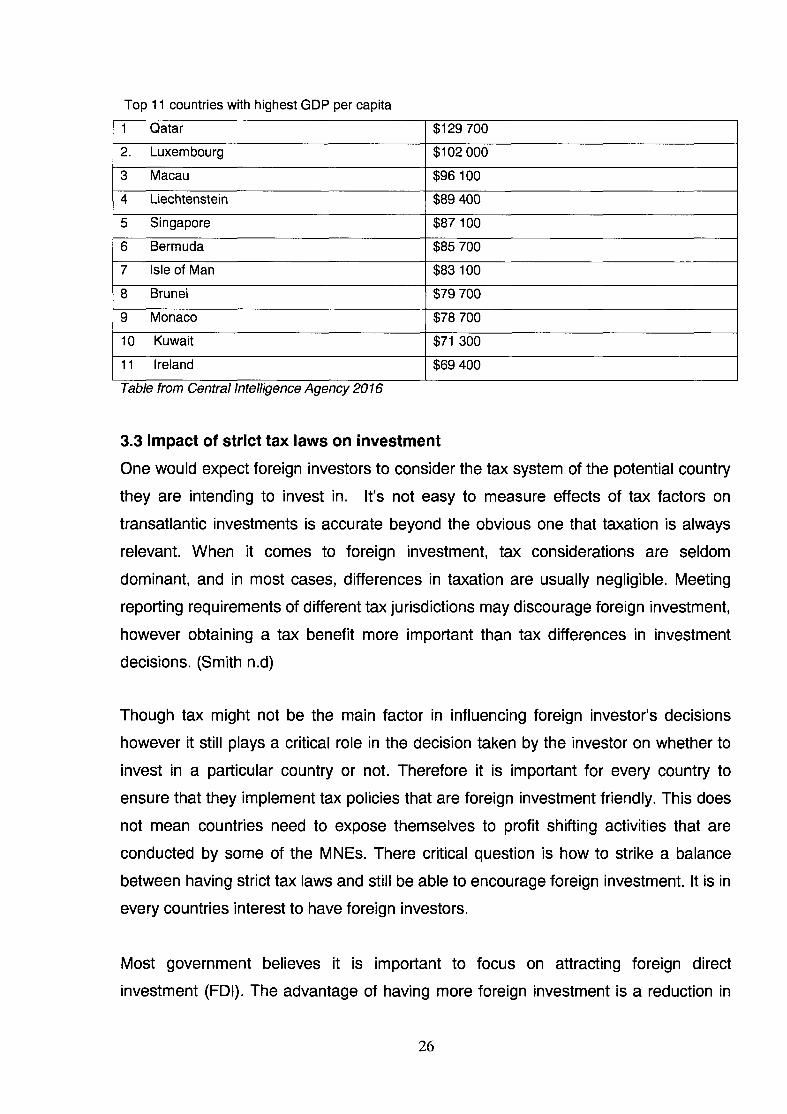

One sees a different picture when you look at GDP per Capita. According to the

National Bureau of Economic Research, tax havens feature in the top 11 countries

with the highest GDP per Capita.

The major tax havens have a lower population, they have less than one percent of the world's population (outside the United States), and 2.3 percent of world GDP, but host 5.7 percent of the foreign employment and 8.4 percent of foreign property, plant and equipment of American firms. The low population in tax havens makes it easy for tax havens to lower tax rates. Per capita real GDP in tax haven countries grew at an average annual rate of 3.3 percent between 1982 and 1999, which compares favourably to the world average of 1.4 percent. The growth rate of tax haven is more than double of the average growth rate of the world. It can be noticed that tax havens tend to attract a lot of foreign investment. It can be argued that high tax countries indirectly contribute to the economic prosperity of tax (Hines n.d)

25

Top 11 countries with highest GDP per capita

1 Qatar $129 700

2. Luxembourg $102 000

3 Macau $96 100

4 Liechtenstein $89 400

5 Singapore $87 100

6 Bermuda $85 700

7 Isle of Man $83 100

8 Brunei $79 700

9 Monaco $78 700

10 Kuwait $71 300

11 Ireland $69 400

Table from Central Intelligence Agency 2016

3.3 Impact of strict tax laws on investment

One would expect foreign investors to consider the tax system of the potential country

they are intending to invest in. It's not easy to measure effects of tax factors on

transatlantic investments is accurate beyond the obvious one that taxation is always

relevant. When it comes to foreign investment, tax considerations are seldom

dominant, and in most cases, differences in taxation are usually negligible. Meeting

reporting requirements of different tax jurisdictions may discourage foreign investment,

however obtaining a tax benefit more important than tax differences in investment

decisions. (Smith n.d)

Though tax might not be the main factor in influencing foreign investor's decisions

however it still plays a critical role in the decision taken by the investor on whether to

invest in a particular country or not. Therefore it is important for every country to

ensure that they implement tax policies that are foreign investment friendly. This does

not mean countries need to expose themselves to profit shifting activities that are

conducted by some of the MNEs. There critical question is how to strike a balance

between having strict tax laws and still be able to encourage foreign investment. It is in

every countries interest to have foreign investors.

Most government believes it is important to focus on attracting foreign direct

investment (FOi). The advantage of having more foreign investment is a reduction in

26

unemployment, economic growth and infrastructure development. FOi is very

important for governments as it contributes to the domestic country's income through

introduction of new technologies and skills development. It is therefore important for

the policy makers to ensure that tax laws are friendly toward foreign investors, in order

to take advantage of the FOi. In trying to attract FOi, it is important for government to

ensure that they still attain appropriate share of domestic tax from MNEs. While

offering a competitive tax environment, it is important to ensure that the country's

economy is not disadvantaged.

One of the major considerations in the analysis done by foreign investors would be the

tax rate. The increase or decrease in the tax rate would have an impact on the

investor's attitude towards a country. Foreign direct investment is like to decrease

following an increase in tax rate on FOi, as they are becoming increasingly sensitive to

taxation. When evaluation how FOi react to tax reform, it's not easy to ascertain how

tax factors into FOi decisions, and what tax rates which investors consider to be

reasonable. In most cases the comparisons may focus on statutory corporate income

tax (CIT) rates and little attention might be given to indirect taxes. Or it may be that

average effective tax rates or marginal effective tax rates matter more than corporate

income tax (headline rates), as they play a significant role in the determination of the

percentage of profits that are taxable. Corporate income tax rates may differ

significantly from effective tax rates, to the extent that taxable profits differ from the

real profits, therefore some investors look beyond the CIT rate, they also consider the

expenses that are deductible, as they are interested in the effective interest rate.

(OECO n.d)

Foreign investors compare the economic climate of different countries and invest on

countries that have tax policies that a conducive to their needs. In today's global

business environment, tax competition for FOi exists and government always need to

take it into consideration when introducing tax policies. Governments can't make a

mistake of thinking that investors don't conduct a comparison of tax policies across

countries that are similar in location and market size.

27

CHAPTER4

Lack of commercial substance

4.1 Introduction

The way of doing business has evolved over the years and this requires the tax

legislation to be amended in order to keep up with changes that have emerged. It is

becoming difficult to place absolute reliance on old court cases to address the current

complex business transactions. Most taxpayers are constantly looking for loopholes in

the tax legislation in order to minimize their tax liability. Moreover the current economic

crisis has also served as a motive for taxpayer to get involved in transactions that

would result in minimum or no tax expenses. South Africa might have a reduction in

simulated transactions if the Advance Pricing Agreements (APAs) proves to be

advantageous. The impact of general anti-avoidance rules on simulated transaction

need to be analysed, in order to ascertain if they need to be tightened.

4.2 Simulating transactions to achieve BEPS

Most taxpayers avoid tax by entering into contracts that disguised their true nature in

order to qualify for a tax benefit that would not be available if the true contract between

them were revealed (SAICA 2009). Transactions that lack commercial substance are

often simulated.

There's no definition of simulated transaction in the Income Tax Act and therefore we

rely on court cases to ascertain whether a transaction was simulated. In a string of

cases such as Zandberg v van Zyl 1910, Commissioner of Customs and Excise v

Randles, Brothers and Hudson Ltd, it was understood that a transaction will not be

regarded as simulated if the parties genuinely intended that their contract will have the

effect in accordance with its tenor and the rule applies even if the transaction is

devised solely for the purpose of avoiding tax. There are a number of gaps that can be

found in the above principle. The mere fact that the parties genuinely intended to

execute what is in the contract should not protect a transaction from being regarded

as simulated.

28

During the C:SARS V NWK Ltd 2011 court case, Lewis JA stated that if the purpose of

the transaction is only to allow the avoidance of tax, then the transaction will be

regarded as simulated. Transactions that involve prices which are not at arm's length

are often lacking commercial substance and they are simulated transactions. The

purpose of schemes or transaction formed to achieve profit shifting is to avoid tax and

therefore they meet the definition of simulated transactions.

Practice Note 5 states that a taxpayer who has carried out a legitimate tax avoidance scheme i.e. who has arranged his affairs so as to minimise his liability, in a manner which does not involve fraud, dishonesty, misrepresentation or other actions designed to mislead the Commissioner, will have met his duties and obligations under the Act (Department of finance, 1987).

This means if a taxpayer structure their transaction in a way that would minimise the tax liability, the taxpayer won't be at fault if it's a legitimate tax avoidance scheme.

It's not clear cut what would constitute a simulated transaction which lacks commercial

substance. Courts are usually requested to resolved disputes between taxpayers and

the tax authorities to resolve matters relating to simulated transactions. Transactions

relating to profit shifting usually lack commercial substance e.g goods are not sold at

market related prices to connected parties. Tightening the general anti-avoidance

rules which are contained in sections 80A to 80L of the Income Tax Act legislation

dealing with simulated transaction would therefore play a critical role in eliminating

profit shifting.

4.3 Advance Pricing Agreement.

According to the OECD's guideline for Advanced Pricing Agreement (APA), an APA is an administrative approach that attempts to prevent transfer pricing disputes from arising by

determining criteria for applying the arm's length principle to transactions in advance of those transactions taking place (OECD n.d).

The South African Revenue Service (SARS) does not enter into advance pricing

agreements with taxpayers at the moment. In trying to ensure that taxpayers are

comfortable about their transfer pricing approach and methods used to arrive at an

arm's-length price, jurisdictions such as the United Kingdom and the United States of

America, make use of 'Advance Pricing Agreements' ('APAs'). Having APAs proved to

be helpful in resolving transfer-pricing disputes. Unfortunately APAs are currently not

in use in South Africa and SARS doesn't seem to be keen on introducing it in the

foreseeable future. This means South African taxpayers are currently not able to

benefit from the advantages of having an APA. (Oguttu n.d)

29

Denying taxpayers an opportunity to enter into these agreements has advantages and

disadvantages. It is important to do a detailed analysis to ascertain whether it would

be worthwhile for South Africa to incorporate APAs in the Tax Administration Act.

4.3.1 Advantages of APAs

The APAs offer better assurance on transfer pricing methods and are conducive in

providing certainty and unanimity of approach (Garg 2016). Having APAs avoids

unnecessary audits which waste both the taxpayers and the tax authorities' time. This

would also enable taxpayers to do proper tax planning and remove uncertainties. The

basic idea behind having an APA is to increase the efficiency of tax administration by

encouraging taxpayers to voluntary disclose before the tax authorities all the facts

relating to their affected transactions, this would then enable a taxpayer to work

towards a mutual agreement. Tax authorities also benefit from having an APA, as it

reduces the burden of compliance. This means there will be a reduction in the number

of transfer pricing audits. Having an APA also gives taxpayers greater certainty

regarding their transfer pricing methods, as it is always a challenge to choose an

appropriate method, moreover an APA gives a platform to the taxpayer and the tax

authorities to have a discussion and a resolution in advance.

A significant amount money is spent on transfer pricing audit, tax administrator have to

allocate lot of resources to resolve transfer pricing disputes and this could be avoided

through the introduction of transfer pricing. The developed countries like the United

States of America and the United Kingdom adopted APA, one would expect a

developing country like South Africa would to the same, so as to take advantage of the

benefits listed below

• Complex and high risk transactions are addressed and resolved early-APA

enable taxpayers to minimize the risk of a transfer pricing adjustment and they

provide certainty through a negotiation process. APAs are likely to be

undertaken by companies that have extremely complex inter-company

transactions, which have a high degree of transfer pricing adjustment risk that

30

may result in penalties. Having APA would ensure that taxpayers have certainty

with regard to their transfer pricing policies.

• An APA will assist with avoiding double taxation - Most Multinationals' pricing

of goods and services for transactions among themselves are usually governed

by a global pricing policy. These global policies generally ensures to provide an

arm's length return to various constituents of the MNE group, based on the

functions performed, assets employed and risks assumed by each member of

the group. When a revenue authority in a particular jurisdiction audits and

disputes such pricing policy and raises a consequential demand, it might lead

to double taxation for the Group as a whole. The process of APA will play a

significant role in doing avoiding a situation whereby there is a double taxation.

• Taxpayers will avoid costs relating to tax audits - Tax audits are costly and

APA will reduce compliance cost and costs associated with audit and appeals

by eliminating the risk of transfer pricing audit and resolving unnecessary time

consuming disputes and litigations. This will also help revenue to allocate their

resources on other things

• Transfer pricing documents require a lot of record keeping, having an APA will

certainly reduce the burden of record keeping as taxpayer will knows in

advance the required documents to be maintained to substantiate the agreed

terms and conditions of the agreement.

• The negotiation between the taxpayer and revenue authority is good for both

parties as the authorities get to understand the business better and the

taxpayer can learn from competent authority guides on how transactions should

be structure in order to ensure that prices for goods and service are at arm's

length.

(Garg 2016)

APAs would also play a significant role in reducing simulated transactions. The

reduction in compliance cost that would encourage taxpayers to rather enter into an

APA instead of participating in simulated transactions which may result in heavy

penalties.

31

4.3.2 Disadvantages of APA

APAs can also be disadvantageous, they require extensive voluntary disclosure and

this could result in concern about exposure to adjustments for open tax years. In most

cases the non-factual representations made during the APA process cannot be used

as evidence in legal or administrative proceedings, unless the proceedings regard a

tax year, transaction and person covered by a successfully completed APA (Hansen

n.d).

The disclosure process can also be expensive and time consuming because the

disclosure is generally more extensive than for private letter ruling. This means a

taxpayer would have to pay for provisional fees, expert opinion fees and employees'

salaries.

The advantages of having APAs seem to outweigh the disadvantage and it would be

worthwhile for South Africa to consider implementing it. This would also ensure that

South Africa's legislation is in line with that of the developed countries.

32

CHAPTERS

Actions to be taken to address base erosion and profit shifting

5.1 Introduction

Base erosion and profit shifting (BEPS) by multinational corporations has entered the

public consciousness as a potentially important impediment to tax collections (Hines

n.d). Therefore it is critical for BEPS to be urgently addressed in order to end further

loses to the fiscus. The impact of BEPS on tax revenues is not easily quantified.

MNEs are going all out to ensure that they to ensure they pay minimum or no tax in

order for more profit to be allocated to shareholders. This means that a corporation

that is located in a country with a 20 percent tax rate, and that has the opportunity to

reallocate some of its taxable income to a country with a 15 percent tax rate, will

typically arrange its financial and other affairs to reallocate most of its income to the

lower-rate country. According to JR Hine (n.d.), the average member country of the

OECD in 2011 raised 8.8 percent of its total tax revenue from taxes on corporate

profits, portion of which represented taxes on multinational corporations. The tax

contribution of Multinational Corporation might seem lower, however any form of

contribution to Tax Revenue makes a difference.

The development of a country like South Africa is depended on tax revenue to be able

to finance government expenditure. A shortfall in tax revenue caused by BEPS would

further deteriorate South Africa's economic growth plans. Simplifying transfer pricing

rules and ensuring they are in line with OECD would play an important role in

increasing compliance. Aligning our transfer pricing law with that of other countries'

would enable us to stay abreast will the latest trends.

5.2 Modification of transfer pricing rules.

According to the OECD, it is important for countries to understand modern business

models and how MNEs operate in a globalised economy in order to curtail BEPS.

Globalisation, the gradual removal of trade barriers, the increase in technological and

telecommunication developments has caused products and operational models to

evolve, changing the way modern MNEs are structured and managed and thereby

33

creating the conditions for the development of global strategies aimed at maximising

South Africa's TP legislation is contained in Section 31 of the Income Tax Act 58 of

1962 and is supported by SAAS Practice Note 7, which outlines the important

principles and guidelines that taxpayers have to follow in determining an arm's length

price. South Africa's transfer pricing laws were enacted in 1995 and Practice Note 7

was released in 1999, until recently there were no changes in the legislating to still

remain relevant in the modern way of doing business. The changes that were recently

made, which became effective as of the 1 April 2012 is focusing on all aspect of the

contracting parties and not only on the pricing of transactions. The other changes in

the TP legislation relates to the triggering of TP adjustments and the consequences

for a South African taxpayer entity of such an adjustment. Transfer pricing

adjustments will have to be made by the taxpayer that is party to the affected

transaction in its tax return. This is different from the previous rules, which prohibited

taxpayers from making Transfer Pricing adjustment themselves, but rather provided

the SAAS with the discretion to make such an adjustment if SAAS was of the opinion

that the transaction had not been priced on an arm's length basis.

There are still gaps in South Africa's transfer pricing legislation, as the following issues

are not property addressed, as required by the OECD. (Deloitte, 2016)

• Transfer pricing rules prevent excessive interest deduction. However the

currently legislative environment is complex and could create uncertainties for

taxpayers (Action 4)

• There was no clarity on which entities are supposed to have a TP document

and what should be contained in the document. A public notice was recently

issues which indicated that transfer pricing documentation would be required If

an entity enters into a potentially affected transaction and the aggregate of the

person's potentially affected transactions for the year of assessment, without

offsetting any potentially affected transactions against one another, exceeds or

is reasonably expected to exceed R100 million. This only applies to

assessment relating to periods after 1 October 2016 (Action 13).

34

• Draft regulation that specifies country by country reporting standards for

multinational enterprises was published on the 11th of April 2016. The

regulations are effective from tax years beginning on or after 1st January 2016.

The first CBC reports must be filed by 31 December 201 ?(Action 13).

• South Africa's CFC rules are complex and in some respect unclear, so the

application of the recommendation in the report on Action 3 may welcome in

helping to overhaul the legislation. However it is not clear whether South Africa

would make any changes to the current rules (Action 3).

5.3 Comparison of South Africa's transfer pricing rules with those of developed

countries

5.3.1 United State of America (USA)

The USA is very experienced when it comes to transfer pricing, as it has one of the

oldest and most mature transfer pricing regime in the world. (KPMG, 2015 a)

There a number of similarities between South Africa and the USA's transfer pricing

rules, below are the differences that were identified by the author. South African might

have to look into these differences and perhaps consider amending its transfer pricing

rules.

5.3.1.1 Affected transactions:

According to the USA's laws, the parties must be under common control. Control is

based on a facts and circumstances test, and not on specific ownership thresholds.

Currently, South African laws only look at ownership and do not consider a facts and

circumstances test. This means a number of transactions could be left unchallenged.

5.3.1.2 Preferable benchmarking set

The tax authorities in USA have a preference for local comparable benchmarking set.

The IRS expects that's to use US comparable to be used to benchmark a US tested

party, in certain instances, the Canadian comparable can be used. Moreover there are

detailed reporting requirement for public corporations that are used by providers who

35

create company databases and by practitioners who prepare transfer pricing reports.

(KPMG, 2015 a)

Having a standard comparable benchmarking is critical because it avoids a situation

whereby taxpayers could manipulate the benchmarking to suit their desired outcome.

South Africa lawmakers would have to consider adopting the same approach.

5.3.1.3 Advanced Pricing agreements

APA is a very important program that ensures that taxpayers comply with transfer

pricing laws and it enables companies incorporated in USA to reduce the transfer

pricing risk. According to the KPMG report, it was noticed that the I RS received 108

APA requests in 2014. Therefore it is clear that APAs remain an important instrument

that can be used by the authorities to achieve certainty and mitigate transfer pricing

risk for many multinationals. (KPMG 2015 )

This is testament to the fact that the introduction of APAs would accelerate efforts of

ensuring that multinationals comply with transfer pricing legislation. The IRS's

combination of the Advance Pricing Agreement (APA) program and the competent

authority program into a newly created group, the Advance Pricing & Mutual

Agreement program (APMA), has reduced long court dispute which require lot of

money to be spent on litigation fees. A more expedited processing and resolution of

transfer pricing disputes has now been facilitated by the APMA. A proposed guidance

which was issued in the late 2013 by IRS, it emphasised the importance of APMAs is

consistent with the objectives of APMA to enhance integration between competent

authority matters and APAs, to improve allocation of resources, and to increase

transparency and efficiency (KPMG n.d).

36

5.3.2 United Kingdom {UK)

The transfer pricing legislation was introduced in April 2008. (KPMG n.d). Given the

length of time that the transfer pricing legislation has been established in UK, South

Africa can look into UK's transfer pricing tax laws for guidance as some of South

Africa's laws are based on UK's laws. South Africa, like many other countries, bases

certain of their efforts to establish and implement domestic taxation rules and

regulations on the experience of the UK. In the past, South Africa has looked into a

country like the UK, in developing and enacting of most of income tax provisions and it

is therefore expected that it should also be the case when it comes to transfer pricing.

As an OECD member country, UK Income Tax Legislation on transfer pricing

emphasise and encourage the arm's length principle. The transfer pricing legislation is

based on a self-assessment system which requires all companies to determine

whether their intergroup transactions are always carried at arm's length. When

transfer pricing was first introduced to the UK, it was only in respect of cross-border

intergroup transactions. An amendment was done to the UK transfer pricing legislation

on April 2004, the amendment addressed deficiencies in the introductory legislation

which failed to counter a range of UK tax planning structures that allowed companies

to shift profits domestically to benefit from assessed tax losses. The scope of Transfer

pricing legislation is now broader as domestic transactions have been included,

providing the UK with one of the most aggressive transfer pricing regulation systems.

(Spearman 2013)

5.3.2.1 Advance pricing agreements

Similar to the transfer pricing laws in USA, the transfer price laws in the UK makes

provision for APA. The UK has had formal APA procedures since 1999.

5.3.2.1 Affected transactions:

According to UK's transfer pricing laws, the transfer pricing rules would apply when

the following conditions are met:

• A provision has been made or imposed between two persons by means of a

transaction or series of transactions;

37

• One of those persons was directly or indirectly participating in the management,

control and capital of the other, or the same person or persons were directly or

indirectly participating in the management, control and capital of both parties to

the provision;

• The actual provision differs from the arm's length provision which would have

been made between different enterprises and;

• The difference gives rise to a potential UK tax advantage.

The UK's affected transactions conditions are fairly similar to those of South African.

However there are developments and trends that South African lawmakers need to

take cognisance of.

5.3.3 Australia

Australia introduced new rules which apply to income tax years beginning on or after 1

July 2013. There are few differences between South Africa's transfer pricing laws with

those of Australia.

5.3.3.1 Affected transactions

The parties involved in relevant transfer pricing arrangements need not to be related

to one another and there are no control requirements or ownership threshold under

Australian laws (Deloitte 2015). This is something South Africa should consider

introducing as it would assist in eliminating schemes arranged by unrelated parties.

The statute of limitations on assessment of transfer pricing adjustments is seven years

while in South Africa its three years, unless SARS can prove that the taxpayer was

involved in fraud or there was misrepresentation.

5.3.3.2 Advance pricing agreement

Australian also has an APA program which is currently being updated to reflect

changes to the global economy, community and ATO's profit shifting work. Under the

38

ATO's Advance Pricing Agreement (APA) program, a taxpayer with an APA is

required to prepare and submit an Annual Compliance Report to the ATO disclosing

the covered transactions, according to the requirements of Practice Statement Law

Administration PS LA 2015/4. There is no formal requirement for taxpayers to provide

their transfer pricing documentation to the ATO with the tax return (KPMG 2015 b).

5.4 Progress made by OECD

The Organisation for European Economic Co-operation (OEEC) was established in

1947 to run the US-financed marshal plan for the reconstruction of continent ravaged

by war. It paved a way for a new era of cooperation that was to change the face of

Europe. Encouraged by its success and the prospect of carrying its work forward on a

global stage, other countries like Canada and the US joined OEEC members in

signing the new OECD Convention on December 14, 1960. The OECD was officially

established on September 30, 1961, when the Convention entered into force

(Telegraph, 2011 ). OECD plays a significant role in ensuring that the international

community works together to address global challenges.

With regards to dealing with BEPS, the most notable work done by the OECD is the

introduction of action plans that can be taken by its members to combat BEPS. In the

table below, one can see the progress made by South Africa regarding the

implementation of Actions recommended by OECD.

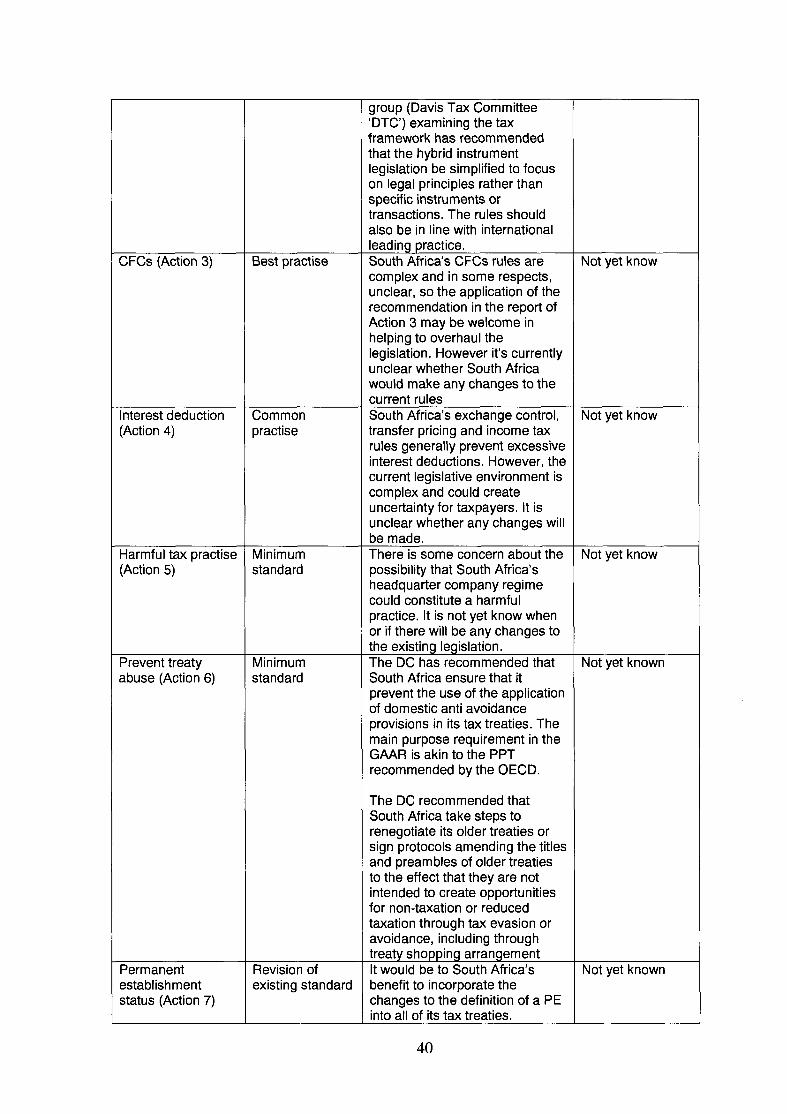

South Africa : BEPS implementation plan (Deloitte, 2016)

Action OECD Category Notes on local country Expected timing

implementation plan

VAT on digital Common VAT Act was amended with Not yet known business approach effect from 1st of April 2017 such (Action 1) that an enterprise rendering

certain electronic services must register as a VAT vendor in South Africa and charge VAT on the supply of services. These services include ebooks, films and music. It is not know yet whether there would be any changes to the current legislations.

Hybrid (Action 2) Common South Africa already has Not yet known approach legislation addressing hybrid

instruments, althouah an expert

39

group (Davis Tax Committee 'DTC') examining the tax framework has recommended that the hybrid instrument legislation be simplified to focus on legal principles rather than specific instruments or transactions. The rules should also be in line with international leading practice.

CFCs (Action 3) Best practise South Africa's CFCs rules are Not yet know complex and in some respects, unclear, so the application of the recommendation in the report of Action 3 may be welcome in helping to overhaul the legislation. However it's currently unclear whether South Africa would make any changes to the current rules

Interest deduction Common South Africa's exchange control, Not yet know (Action 4) practise transfer pricing and income tax

rules generally prevent excessive interest deductions. However, the current legislative environment is complex and could create uncertainty for taxpayers. It is unclear whether any changes will be made.

Harmful tax practise Minimum There is some concern about the Not yet know (Action 5) standard possibility that South Africa's

headquarter company regime could constitute a harmful practice. It is not yet know when or if there will be any changes to the existing legislation.

Prevent treaty Minimum The DC has recommended that Not yet known abuse (Action 6) standard South Africa ensure that it

prevent the use of the application of domestic anti avoidance provisions in its tax treaties. The main purpose requirement in the GAAR is akin to the PPT recommended by the OECD.

The DC recommended that South Africa take steps to renegotiate its older treaties or sign protocols amending the titles and preambles of older treaties to the effect that they are not intended to create opportunities for non-taxation or reduced taxation through tax evasion or avoidance, including through treaty shopping arrangement

Permanent Revision of It would be to South Africa's Not yet known establishment existing standard benefit to incorporate the status (Action 7) changes to the definition of a PE

into all of its tax treaties.

40

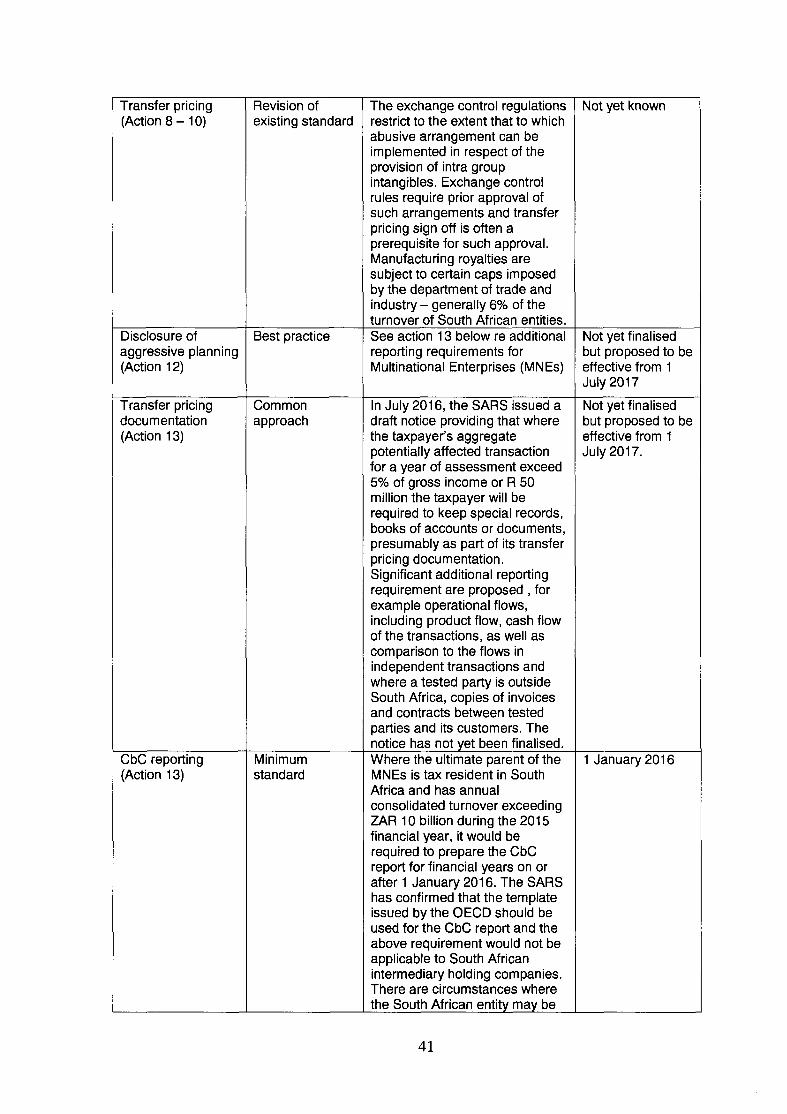

Transfer pricing Revision of The exchange control regulations Not yet known (Action 8 - 10) existing standard restrict to the extent that to which

abusive arrangement can be implemented in respect of the provision of intra group intangibles. Exchange control rules require prior approval of such arrangements and transfer pricing sign off is often a prerequisite for such approval. Manufacturing royalties are subject to certain caps imposed by the department of trade and industry - generally 6% of the turnover of South African entities.

Disclosure of Best practice See action 13 below re additional Not yet finalised aggressive planning reporting requirements for but proposed to be (Action 12) Multinational Enterprises (MNEs) effective from 1

July 2017

Transfer pricing Common In July 2016, the SAAS issued a Not yet finalised documentation approach draft notice providing that where but proposed to be (Action 13) the taxpayer's aggregate effective from 1

potentially affected transaction July 2017. for a year of assessment exceed 5% of gross income or R 50 million the taxpayer will be required to keep special records, books of accounts or documents, presumably as part of its transfer pricing documentation. Significant additional reporting requirement are proposed , for example operational flows, including product flow, cash flow of the transactions, as well as comparison to the flows in independent transactions and where a tested party is outside South Africa, copies of invoices and contracts between tested parties and its customers. The notice has not vet been finalised.

CbC reporting Minimum Where the ultimate parent of the 1 January 2016 (Action 13) standard MNEs is tax resident in South

Africa and has annual consolidated turnover exceeding ZAR 10 billion during the 2015 financial year, it would be required to prepare the CbC report for financial years on or after 1 January 2016. The SAAS has confirmed that the template issued by the OECD should be used for the CbC report and the above requirement would not be applicable to South African intermediary holding companies. There are circumstances where the South African entity mav be

41

required to submit the CbC report even though it is not the ultimate parent company of the MNE. This applies to so called constitute entities and the threshold that applies is EUR 750 million. South Africa is one of the countries that signed the multilateral competent authority agreement for the automatic exchange of CbC report.

Dispute resolution Minimum While South Africa is not one of Not yet known (Action 14) standard the countries that is committed to

complemented binding arbitration in its bilateral by best standard tax treaties, South Africa has tax

treaties with most of the countries that have so committed, so those treaties may need to be amended to include the specified timeframe for the resolution of disputes.

In March 2015, the SARS published guidance on MAP procedure, including an explanation of what MAP entails and how to submit a request.

South Africa is making significant progress in trying to address the action plans

recommended by the OECD, however as it can be seen in the table above, there are

issues that still need to be addressed. The Davis Tax Committee has been tasked with

the responsibility of addressing BEPS in South Africa and the main issues that they