18

BASF – our experience in China Joerg Wuttke, BASF China April 2005

| Date post: | 21-Aug-2018 |

| Category: |

Documents |

| Upload: | truongngoc |

| View: | 213 times |

| Download: | 0 times |

BASF –our experience in China

Joerg Wuttke, BASF ChinaApril 2005

BASF in Greater China

BASF has been trading in China since 1885

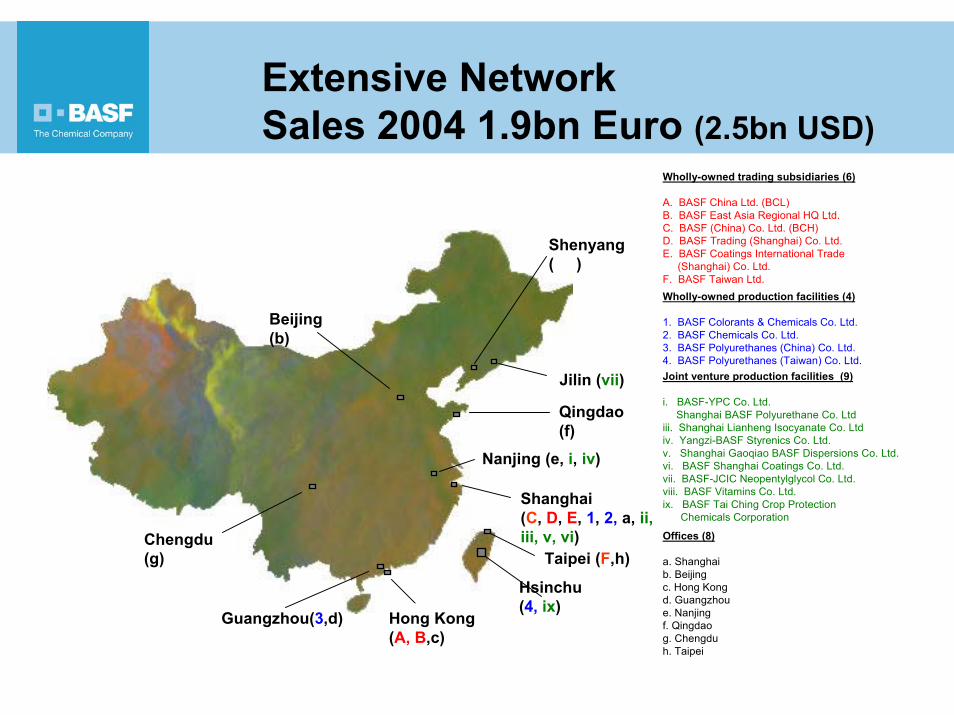

Extensive NetworkSales 2004 1.9bn Euro (2.5bn USD)

Wholly-owned trading subsidiaries (6)

A. BASF China Ltd. (BCL)B. BASF East Asia Regional HQ Ltd.C. BASF (China) Co. Ltd. (BCH)D. BASF Trading (Shanghai) Co. Ltd.E. BASF Coatings International Trade

(Shanghai) Co. Ltd.F. BASF Taiwan Ltd.Wholly-owned production facilities (4)

1. BASF Colorants & Chemicals Co. Ltd.2. BASF Chemicals Co. Ltd.3. BASF Polyurethanes (China) Co. Ltd.4. BASF Polyurethanes (Taiwan) Co. Ltd.Joint venture production facilities (9)

i. BASF-YPC Co. Ltd.ii. Shanghai BASF Polyurethane Co. Ltdiii. Shanghai Lianheng Isocyanate Co. Ltdiv. Yangzi-BASF Styrenics Co. Ltd.v. Shanghai Gaoqiao BASF Dispersions Co. Ltd.vi. BASF Shanghai Coatings Co. Ltd.vii. BASF-JCIC Neopentylglycol Co. Ltd.viii. BASF Vitamins Co. Ltd.ix. BASF Tai Ching Crop Protection

Chemicals Corporation

Nanjing (e, i, iv)

Jilin (vii)

Beijing(b)

Shenyang (viii)

Taipei (F,h)

Hong Kong(A, B,c)

Guangzhou(3,d)

Shanghai(C, D, E, 1, 2, a, ii, iii, v, vi)

Hsinchu(4, ix)

Offices (8)

a. Shanghai b. Beijingc. Hong Kong d. Guangzhou e. Nanjing f. Qingdao g. Chengdu h. Taipei

Qingdao(f)

Chengdu(g)

Major Investment Projects in China

Beijing

Nanjing

HongkongVerbund site

20062005

1,000*300*

Under constructionIsocyanates CaojingTHF / PTHF Caojing

20052,900*

Under construction

BYC Nanjing

Start upInvest.[Mio. USD]Company

Caojing

Chemical siteSite close to customers

* Total investment incl. utility / infrastructure

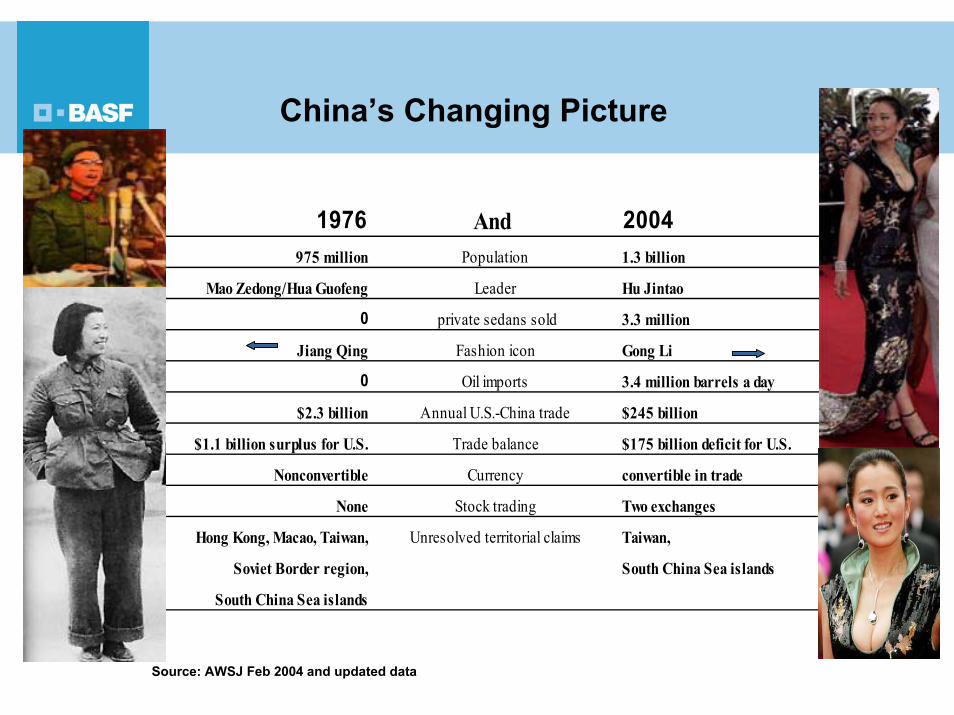

1976 And 2004975 million Population 1.3 billion

Mao Zedong/Hua Guofeng Leader Hu Jintao

0 private sedans sold 3.3 million

Jiang Qing Fashion icon Gong Li

0 Oil imports 3.4 million barrels a day

$2.3 billion Annual U.S.-China trade $245 billion

$1.1 billion surplus for U.S. Trade balance $175 billion deficit for U.S.

Nonconvertible Currency convertible in trade

None Stock trading Two exchanges

Hong Kong, Macao, Taiwan, Unresolved territorial claims Taiwan,

Soviet Border region, South China Sea islands

South China Sea islands

Source: AWSJ Feb 2004 and updated data

China’s Changing Picture

China’s GDP as a share of world GDP 1750 - Today

An early leader in technology, innovation, and the economy, China suffered a decline in global GDP generation and became increasingly marginalized by her Western competitors.

First Opium War(1839-1842)

Taiping Rebellion(1850-1865)

Second Opium War(1856-1860)

Sino-Japanese War (1894-1895)

Boxer Rebellion(1900)

0

10

20

30

40

1700 1820 1890 1952 1978 1995 2002

%

% of World GDPAt market prices

1913: China represents 15% of BASF’s worldwide revenues

2003: China represents 5% of BASF’s worldwide revenues

Source: Angus Maddison, OECD

0

2

4

6

8

10

0 200 400 600Segment size 2000 [€ bn]

Gro

wth

of s

egm

ents

2000

-201

5 [%

p.a

.]

Manufacturing

Services

Construction

Agriculture

= Segment size 2015

Mining

∅ 6.5 %

GDP: size 2000 = 1,169bn Eurogrowth = 6.5% p.a.

GDP more driven by service sector and construction (infrastructure)

Manufacturing and chemical demand expected to grow in line with GDP

Combined growth rate of manufacturing, agriculture and construction below 6% p.a.

Size and growth of

GDP segments 2000 - 2015

SIMPLY PUT…….CHINA IS GOING TO GROW FASTER THAN ANY OTHER ECONOMY(Urbanization of 10m people p.a. !!!!!) BASE CASE

GDP at PPPCAGR10-25

CAGR03-10

Real GDP development for selected economiesUS$ Billions (in 2002 US$) 2010F2003 2025F

823

713

585

498

415

1,921

2,217

2,252

4,671

13,566

2.0%

1.8%

2.6%

7.4%

5.7%

5.6%

3.7%

4.3%

5.2%

US

Japan

Germany

China*

UK

India

Korea

Brazil

Russia

Taiwan

3.4%

7,737

11,539

558

488

453

370

292

1,348

1,602

1,993

4,066

10,764

834

686

1,184

1,062

1,774

2,769

2,905

5,598

6,018

20,643 2.8%

1.7%

6.4%

1.7%

2.5%

5.3%

3.4%

4.1%

3.5%

3.4%

Germany

UK

India

Korea

Brazil

Russia

Taiwan

US

China** 23,031

US

JapanJapan

Germany

U.K

China

India

Korea

Brazil

Russia

Taiwan

* High case: real GDP of US$2.4 tri (8.6% CAGR) and GDP at PPP of US$11.4 tril (5.7% CAGR). Low case: real GDP of US$2.0 tri (5.9% CAGR) and GDP at PPP of US$11.7 tri (6.1% CAGR)

** High case: real GDP of US$7.2 tri (7.6% CAGR) and GDP at PPP of US$21.9 tri (4.4% CAGR). Low case: real GDP of US$3.7 tri (4.1% CAGR) and GDP at PPP of US$ 21.2 tri (4.1% CAGR)

Source: WEFA-WMM; McKinsey analysis

Development of Chemical Markets in Asia Pacific 2002-2015

374 bn EUR

598 bn EUR+3.7% p.a.

NAFTA 29%

WE 23%

SA 5%

2002 2015

37%

11%

11%4%

15%

22%

30%

11%8%4%11%

34%

NAFTA 31%

WE 25%

SA 5%

Asia Pacific

31%

AsiaPacific34%

20151,740 bn EUR

Greater China

Japan

OtherIndia

ANZAsean

South Korea

2%

20021,210 bn EUR

1 Euro = 0.945 USD

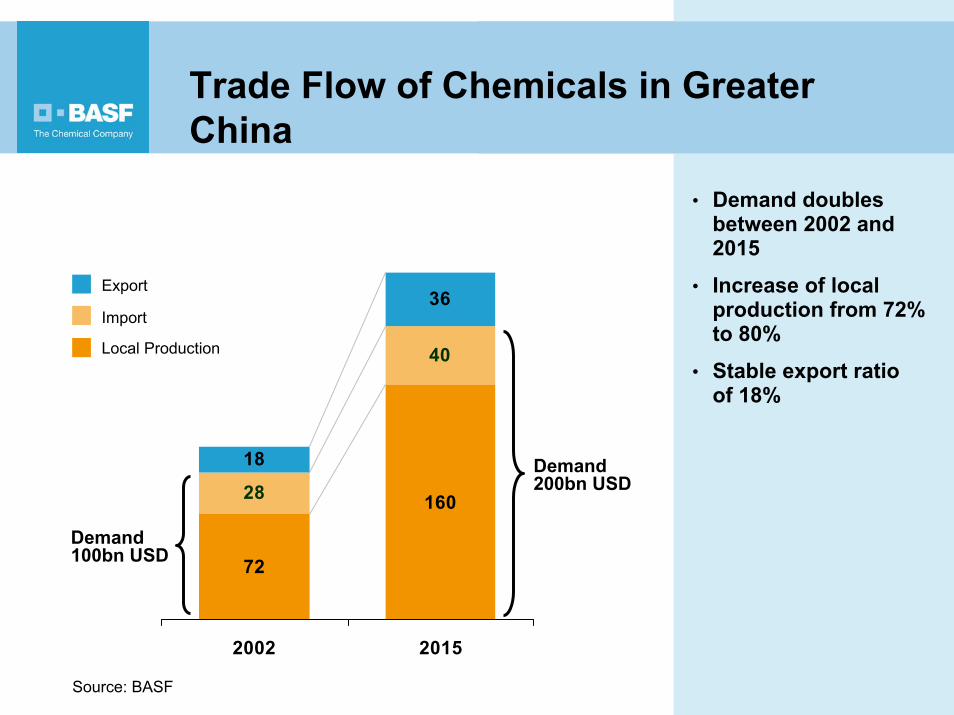

• Demand doubles between 2002 and 2015

• Increase of local production from 72% to 80%

• Stable export ratio of 18%

Trade Flow of Chemicals in Greater China

Demand100bn USD

Demand200bn USD

Source: BASF

72

16028

40

18

36

2002 2015

Local Production

Import

Export

Demand will Shift to Higher Value Chemicals

Source: A.T. Kearney, Frost & Sullivan, Henkel, DZ Bank

40 %58 %

7 %

6 %

18 %

15 %

35 %

21 %

2003 2015 (e)

Specialties

Intermediates forPharma

Agricultural Products

Base Chemicals

Segmentation of the Chinese chemical market:

100 bn USD

200 bn USD• Consumer industries

will shift to higher value products.

• This trend will be mirrored in the increased demand of specialty chemicals.

Plastics in Cars saves money and the environment

Amount of Plastics used in sedans in China:Santana 50 kg, Audi 94kg, Cherokee Jeep 103kg

Reducing the weight of a

car by 100 kg saves about

3,5 liters fuel per 1000 km.

Saving 150m liters fuel each year !

Competitive Environment Highly Fragmented

2002 2015Imports

24%Local production

76%

3%3%

15%

18%

15%

22%

9%

15%

KoreaOthers

MNC*

MNC*

Strong local companies

Others

Others

40%

12%

10%

4%1%

20%

13%

OthersMNC*

Taiwan

Sinopec / PetroChina

MNC*

Imports33%

Local fragmentedcompanies

Local production67%

Taiwan

Sinopec / PetroChina

* MNC= Multinational Companies (e.g. Dow, DuPont, Bayer)Source: BASF

Additions of Local Cracker Capacities Cannot Catch up With Demand Growth

Hainan

Hong Kong

Tianjin

Shandong

LiaoningHebei

BeijingShanxi

Anhui

Jiangsu

Hubei

Gansu

Inner Mongolia

Ningxia

Xinjiang

Xizang

Qinghai

GuizhouHunan

GuangdongGuangxiYunnan

Heilongjiang

Jilin

Henan

Sichuan Zhejiang

Fujian

JiangxiChongqing

ShaanxiShanghai

North China

South China

East China

2900

5100

1500

6100

0

10000

750

2800

0

10000

West China

4501800

0

10000

15.5005.5002003

28.50016.0002010

Total Demand

[kt/a]

Total Capacity

[kt/a]

capacity [kt/a]

Source: BASF

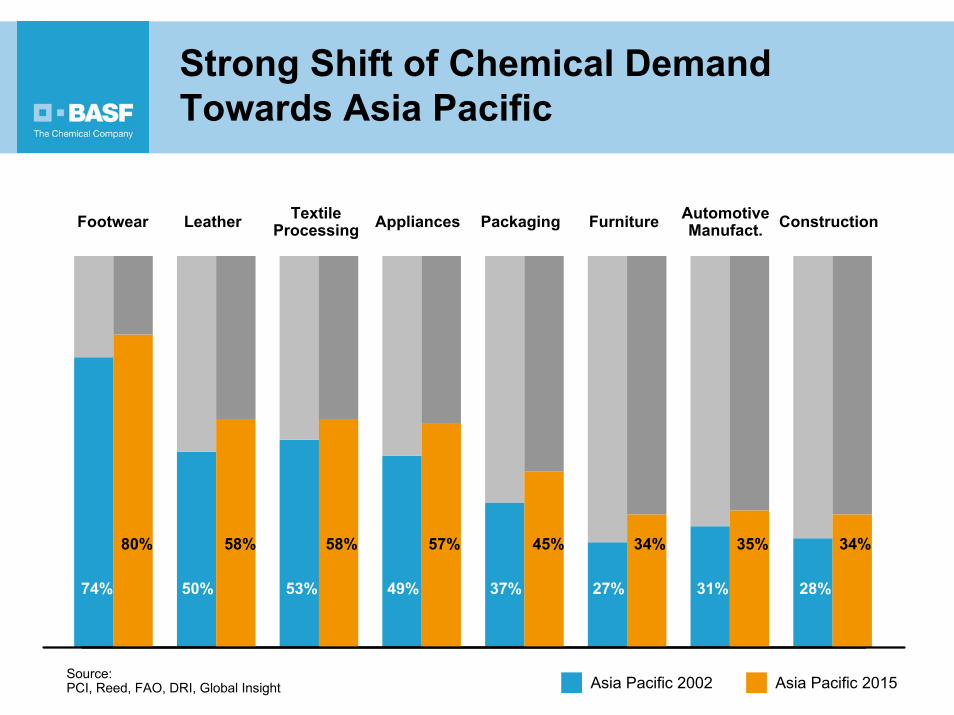

Strong Shift of Chemical Demand Towards Asia Pacific

AutomotiveManufact.Footwear Leather Textile

Processing Appliances FurniturePackaging Construction

50%74% 53% 49% 37% 27% 31% 28%

58%80% 58% 57% 45% 34% 35% 34%

Source: PCI, Reed, FAO, DRI, Global Insight Asia Pacific 2002 Asia Pacific 2015

Consumers of Chemical Products* in 2001

70mill. 76

mill.

Germany236 mill.

United States

JapanChina

110mill.

10 million consumers

2001 = 1.1 billion consumers (17% world population)Source: World Bank, EIU, US Census Bureau* A potential consumer of chemical products is defined by an annual income of 10.000 USD in purchasing power parity

Consumers of Chemical Products* in 2015

United StatesChina

76mill.

700 mill.

112mill.

284 mill.Germany

Japan

2015 = 2.0 billion consumers (29% world population)

10 million consumers

Source: World Bank, EIU, US Census Bureau* A potential consumer of chemical products is defined by an annual income of 10.000 USD in purchasing power parity

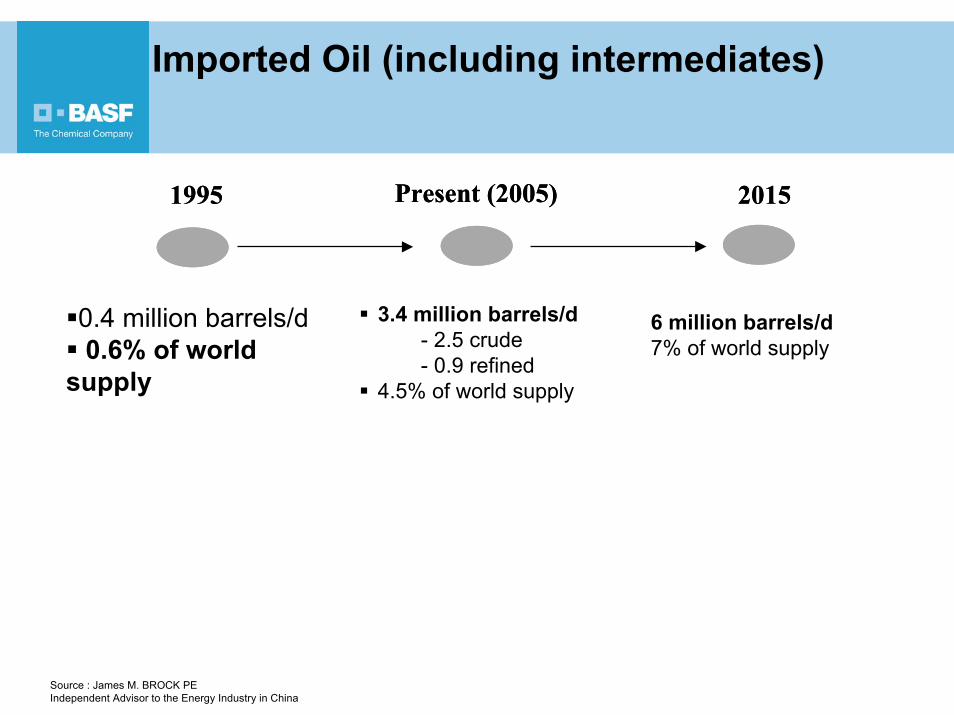

Imported Oil (including intermediates)

1995 2015Present (2005)1995 2015Present (2005)

0.4 million barrels/d0.6% of world

supply

3.4 million barrels/d- 2.5 crude- 0.9 refined

4.5% of world supply

Source : James M. BROCK PEIndependent Advisor to the Energy Industry in China

6 million barrels/d7% of world supply