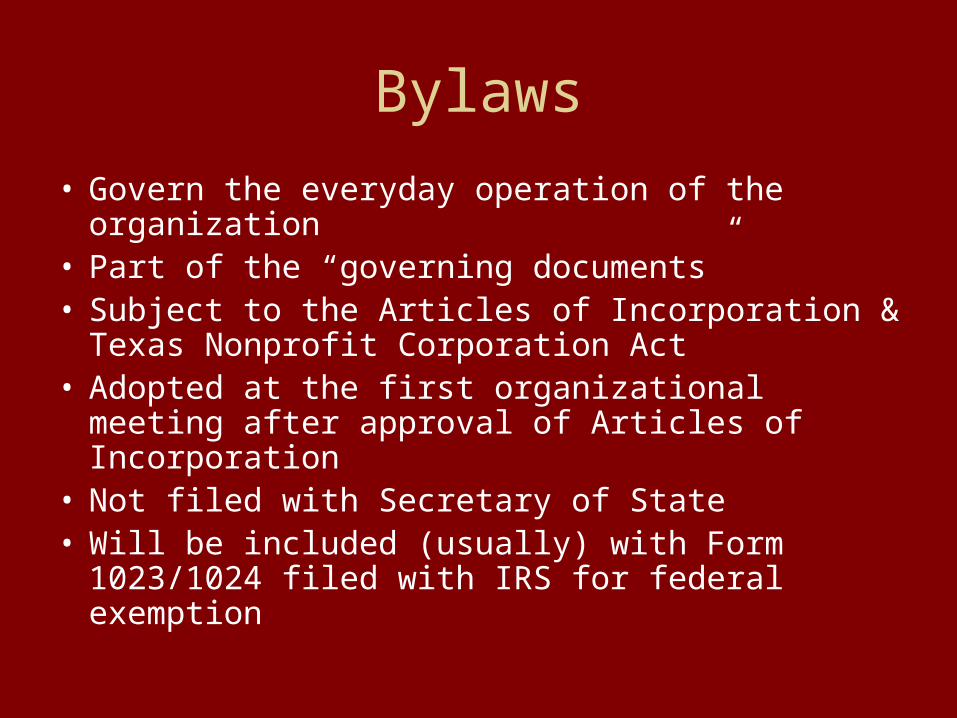

• Govern the everyday operation of the organization

• Part of the “governing documents”• Subject to the Articles of Incorporation & Texas

Nonprofit Corporation Act• Adopted at the first organizational meeting after

approval of Articles of Incorporation• Not filed with Secretary of State• Will be included (usually) with Form 1023/1024

filed with IRS for federal exemption

Components of Bylaws

• Name, purposes, powers and offices• Members (if applicable)• Board of Directors (if applicable)• Committees• Notices• Officers, Employees and Agents• Contracts, checks, deposits and funds• Miscellaneous• Amendments• Operation and Dissolution

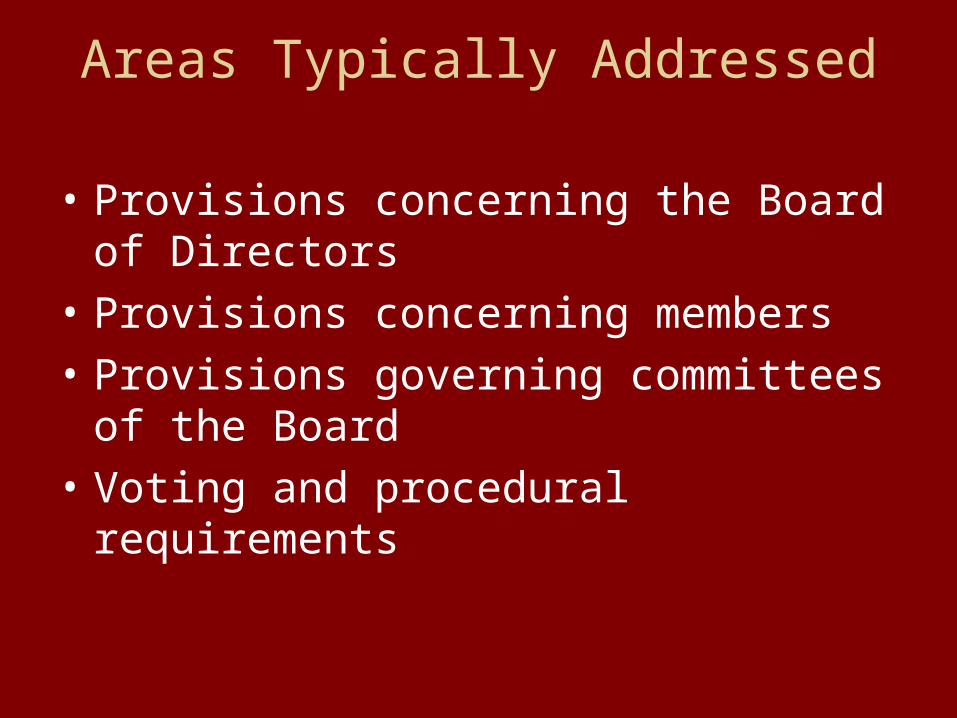

Areas Typically Addressed

• Provisions concerning the Board of Directors

• Provisions concerning members

• Provisions governing committees of the Board

• Voting and procedural requirements

Bylaws: Purposes

• Must be organized and operated exclusively for purposes within appropriate code section (e.g. 501(c)(3) – religious, charitable or educational)

Bylaws: Membership

• Member or no member (classes of membership)• Election of members• Qualifications and rights of members (or classes

of members)• Eligibility• Meetings, notice, voting, etc.• Removal/exclusion from membership• Quorum• May restrict voting to certain members

Bylaws: Board of Directors

• General powers• Number (at least 3)• Qualification (e.g. educational or certifications)• How elected/removed• Term of office• Filling of vacancies• Meetings (annual, regular, special), quorum,

manner of acting• Absolute prohibition against loans to directors• Take care to watch for inurement

Bylaws: Type of Governance

1. Member led

2. Board of director led

3. Hybrid (some decisions presented to and made by the members and the rest by the directors)

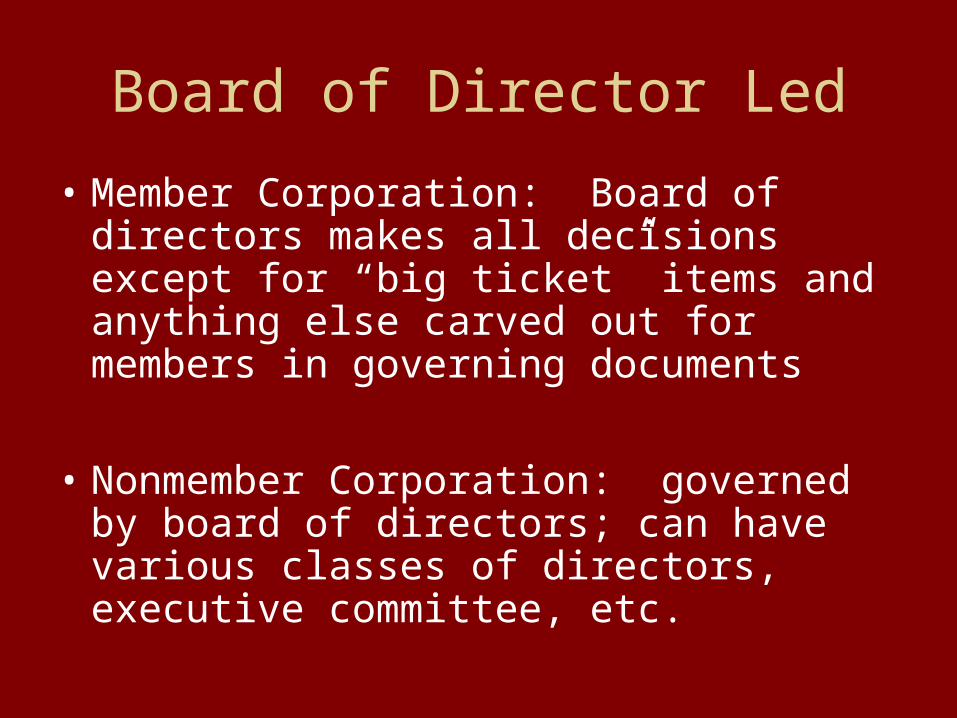

Board of Director Led

• Member Corporation: Board of directors makes all decisions except for “big ticket” items and anything else carved out for members in governing documents

• Nonmember Corporation: governed by board of directors; can have various classes of directors, executive committee, etc.

Member Led

• Member controlled: members control daily operation

• Board of director controlled: simple day to day operations decided by board but most decisions presented to and decided by members

• Keep in mind there may be a single member or there may be classes of members with only one class having voting rights or voting rights as to certain decisions (take care here when forming public charities)

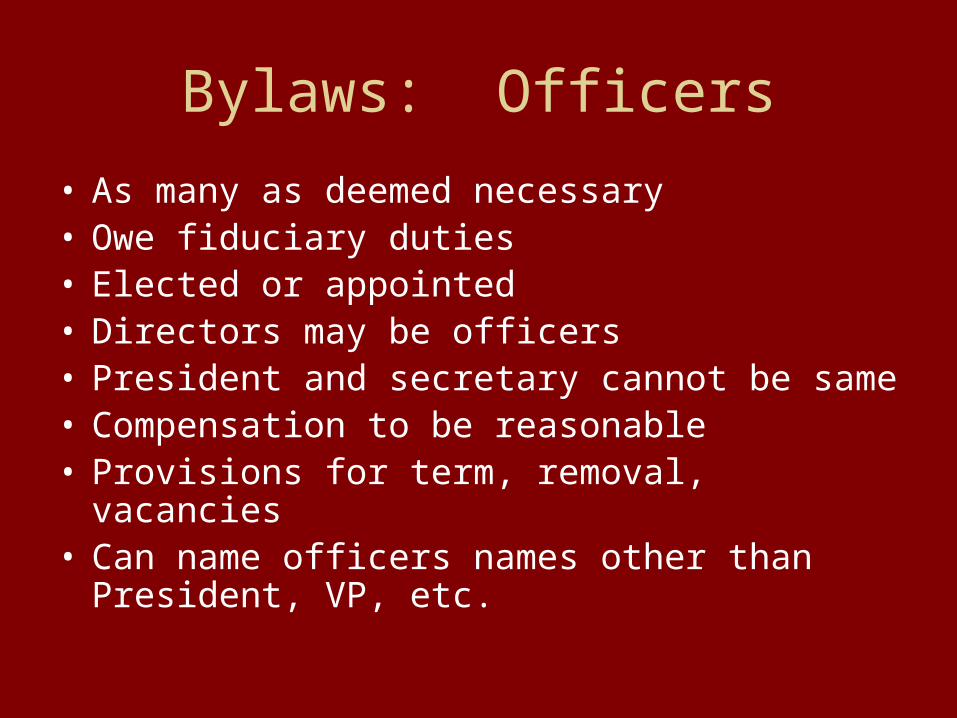

Bylaws: Officers

• As many as deemed necessary• Owe fiduciary duties• Elected or appointed• Directors may be officers• President and secretary cannot be same• Compensation to be reasonable• Provisions for term, removal, vacancies• Can name officers names other than President,

VP, etc.

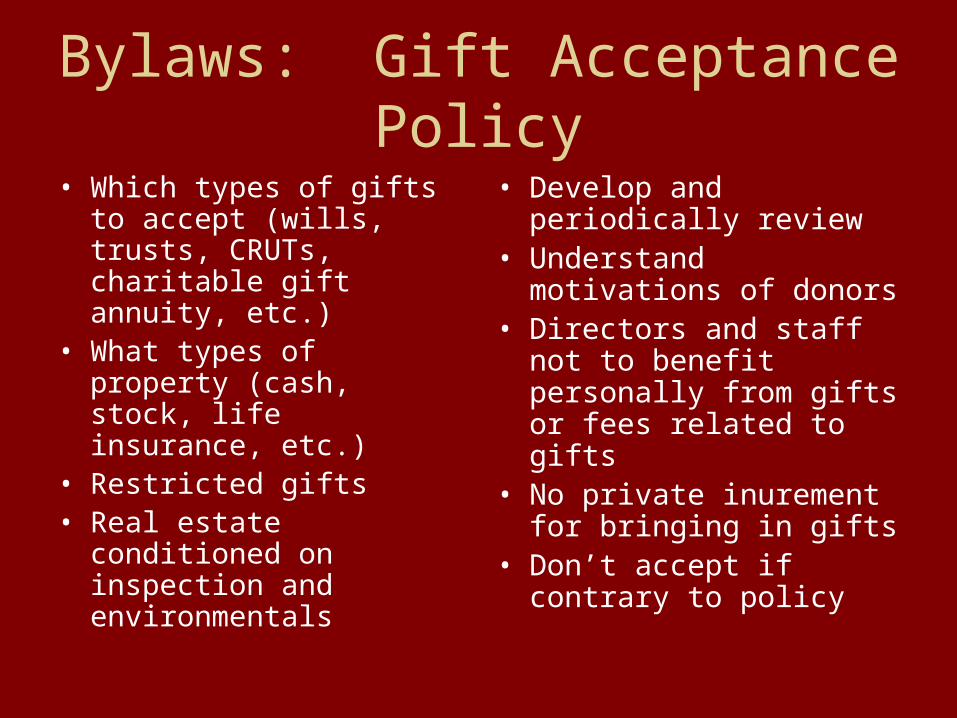

Bylaws: Gift Acceptance Policy

• Which types of gifts to accept (wills, trusts, CRUTs, charitable gift annuity, etc.)

• What types of property (cash, stock, life insurance, etc.)

• Restricted gifts• Real estate conditioned

on inspection and environmentals

• Develop and periodically review

• Understand motivations of donors

• Directors and staff not to benefit personally from gifts or fees related to gifts

• No private inurement for bringing in gifts

• Don’t accept if contrary to policy

Duties of Board Members(Fiduciary Duties)

• Duty of Care

1. Act in good faith

2. Use care that a person of ordinary prudence would use in same or similar circumstances

3. Make decisions believed to be in the best interest of the corporation (must be reasonably informed)

• Duty of Loyalty

1. Loyal to the corporation

2. Look to best interest of corporation rather than private gain

3. Corporate opportunity doctrine

4. Disclose personal interest

5. Transactions with organization must be fair to the nonprofit

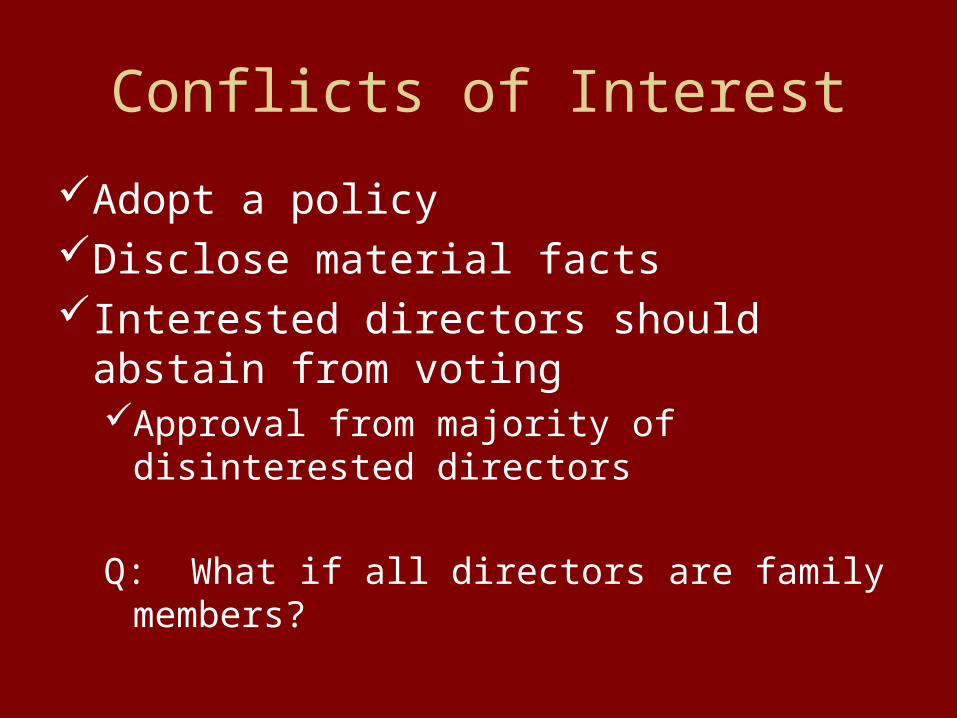

Conflicts of Interest

Adopt a policyDisclose material factsInterested directors should abstain from

votingApproval from majority of disinterested

directors

Q: What if all directors are family members?

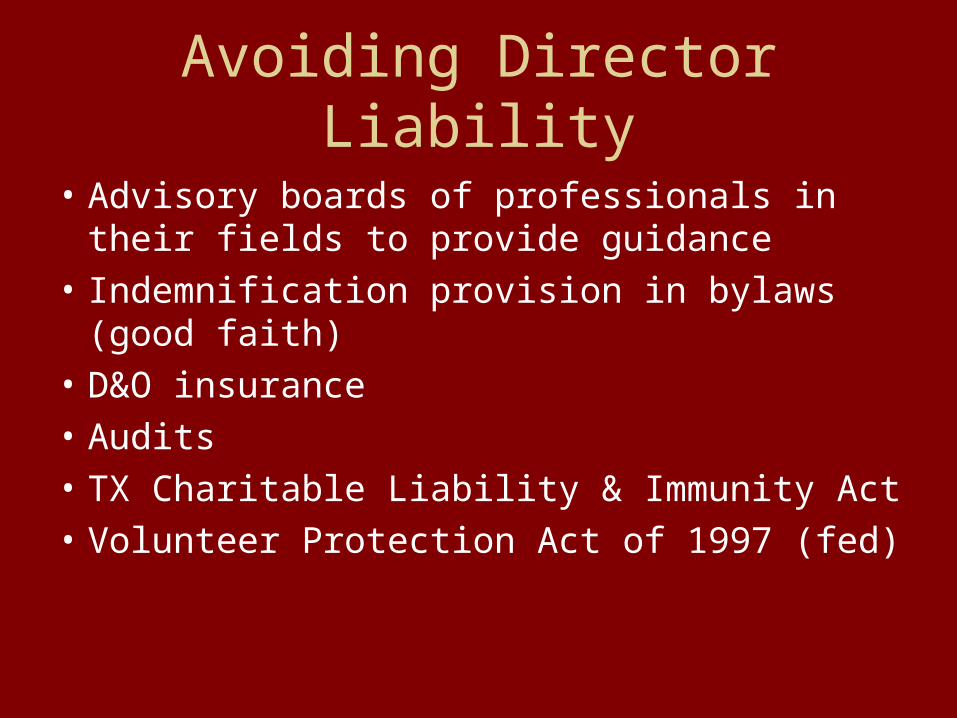

Avoiding Director Liability

• Advisory boards of professionals in their fields to provide guidance

• Indemnification provision in bylaws (good faith)

• D&O insurance

• Audits

• TX Charitable Liability & Immunity Act

• Volunteer Protection Act of 1997 (fed)

Bylaws: Professional Management/Advisory Boards

• May be an executive committee

• Day to day management can be delegated

• CPA’s• Attorneys• Money Managers

No personal liability if director relies on information from others so long as director does not have knowledge that the information is incorrect

Investing

• Trusts: Prudent investor rule (no investment per se imprudent and may delegate investment decisions – look to how overall investment strategy developed for test of fiduciary duty)

• Corporations: to avoid personal liability, directors must simply act in good faith and with ordinary care in selecting advisors

Indemnification

• Permissive– Director in good faith– Director reasonably

believed she acted in the best interests of the corporation (or, if not conduct in official capacity, not in opposition to corporation’s interests)

– Criminal: no reason to believe conduct was unlawful

• Precluded– Found liable for receiving

personal benefit improperly– Found liable to the

corporation But: Can still be

indemnified for reasonable expenses incurred in connection with proceeding so long as not found liable for willful or intentional misconduct in performing corporate dutiesMust have a provision in the governing

documents

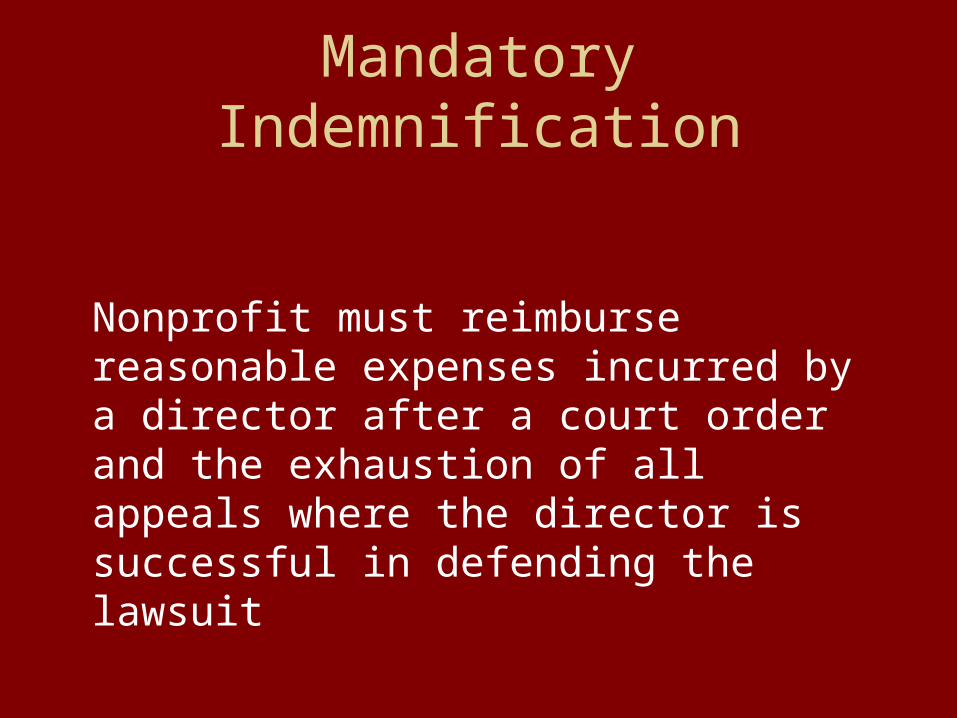

Mandatory Indemnification

Nonprofit must reimburse reasonable expenses incurred by a director after a court order and the exhaustion of all appeals where the director is successful in defending the lawsuit

D&O Insurance

Protects against unintentional wrongful acts (so long as not illegal or beyond authority)

Pays legal defenses and reimburses organization for indemnification costs

Coverage is made on a claims made basis

D&O Common Exclusions

o Fines and penaltieso Punitive damageso Pollutiono ERISA claimso Defamationo Intentional conducto Employment practiceso Sexual misconduct

D&O Considerations

Who chooses defense counselWhat are the coverage amountsWhat are the exclusions (e.g. employment

practices)Is there a duty to defend/provide defense

costsWhat is the retention amount (i.e.

deductible)

Records: Need

• IRS audits• Lawsuit over equipment, misconduct, etc.• Selling/purchasing real estate• Expulsion of member• Employee termination• Etc, etc, etc• Many nonprofits (especially churches) fail

to keep adequate records

Record-keeping: Methodology

• System should keep records organized, safe, easy to locate and access

• Records should be kept in a centralized location

• More than one person should understand and be able to locate records within the system

• Some type of redundancy should be built in to the system

Types of Records to be Kept• Governing documents (all restatements and amendments)• Certificate of Incorporation• 9.01 reports• Resolutions• Real Estate documents (deeds, deeds of trust, lien notes, tax

appraisals and ad valorem exemption records, plats and surveys, leases)

• Documents regarding personal property (bills of sale, receipts, warranty information, repair and maintenance records)

• Policies and procedures• Employee handbooks• Tax information/records received from governmental agencies• Insurance policies (especially occurrence-based)• Financial records• Personnel records (need to keep separate)

Policies: Need

Consistency in practicesReasonableness of procedures (i.e.