The workings under the heading of “Additional Working” are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net 2001 Compiled and Solved by: S.Hussain B.COM – II – ADVANCED AND COST ACCOUNTING REGULAR / PRIVATE

Transcript

The workings under the heading of “Additional Working” are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 2

ADVANCED AND COST

ACCOUNTING – 2001

REGULAR / PRIVATE Instructions: Attempt any five questions, three from Section – A and two from Section – B.

SECTION “A” (ADVANCED ACCOUNTING)

Q.No.1 COMPANY ACCOUNTING – AMALGAMATION (a) Differentiate between amalgamation and absorption. (b) GIVEN Shan Ltd. and Adnan Ltd. decided to amalgamate their business and a new company S

and A Co. is formed to take over all assets and liabilities of the two concerns. The new Co. S and A Ltd. issue 110,000 shares of Rs.10 each at Rs.20 to Shan Ltd. and 90,000 shares of Rs.10 each at Rs.20 to Adnan Ltd. The following are the balance sheets:

Shan Limited Balance Sheet December 31, 2000

Cash Rs.120,000 Accounts payable Rs.180,000 Accounts receivable 400,000 General reserves 300,000 Merchandise inventory 600,000 Share capital Machines 1,200,000 (190,000 shares of Rs.10 each) 1,900,000 Furniture 60,000

2,380,000 2,380,000

Adnan Limited Balance Sheet December 31, 2000

Cash Rs.250,000 Accounts payable Rs.200,000 Accounts receivable 300,000 General reserves 100,000 Merchandise inventory 700,000 Share capital Machines 800,000 (185,000 shares of Rs.10 each) 1,850,000 Office equipment 100,000

2,150,000 2,150,000

REQUIRED (i) Give entries in General Journal form in the books of Shan Ltd. (ii) Prepare amalgamated balance sheet in the books of S and A Co. (iii) Compute purchase consideration for each liquidating Co.

SOLUTION 1 (a)

Amalgamation: The combination of two or more companies in which the old companies merge to form a new company is called amalgamation. For example Company “A” and Company “B” amalgamate to form a Company “C”. All the assets and liabilities of both old companies (A and B) are transferred to new company (C). In that sense the company “C” is acquiring the company “A” and company “B”.

Absorption: The combination of two or more companies in which one company acquires the other company and the other company absorbs in the acquiring company is called absorption. For example Company “A” acquires the Company “B”. So that after the acquiring the name of Company “B” will not exist but the name of Company “A” will exist. All the assets and liabilities of old company (B) are transferred to purchasing company (A).

Q.No.2 ACCOUNTING FOR INSTALLMENT SALES GIVEN A-One Co. follows the perpetual inventory system and FIFO method for inventory valuation and closes its book twice in a year at June 30, and December 31. Balances at January 1, 2001 Installment accounts receivables – 1999 Rs.75,000 Deferred gross profit – 1999 25,000 Installment accounts receivables – 2000 150,000 Deferred gross profit – 2000 45,000 At June 30, 2001 Installment sales made at 25% above cost during the 6 – month period Rs.450,000 An installment accounts receivable – 1999 cancelled 5,000 Repossessed merchandise was assigned a value of Rs. 2,500 Installment accounts receivables – 1999 30,000 Installment accounts receivables – 2000 45,000 Installment accounts receivables – 2001 175,000 REQUIRED

(i) Compute gross profit rates of the installment sales originated in 1999 and 2000. (ii) Prepare a statement showing collection of installment accounts receivables of 1999, 2000 and

2001 at June 30, 2001. (iii) Give all necessary entries under installment method for recording transactions concerning

installment sales including an adjusting entry for recording realized gross profit. (iv) Record repossession without recognizing loss or gain.

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 6

SOLUTION 2 (iv) Computation of Gain or Loss on Repossession: Installment accounts receivable cancelled (1999) 5,000 Less: Unrealized gross profit (5,000 x 33.33%) (1,667)

Book value 3,333 Less: Merchandise repossessed at fair market value (2,500)

Loss on repossession 833

A – ONE CO.

GENERAL JOURNAL

Date Particulars P/R Debit Credit

1 Merchandise repossessed 3,333 Unrealized gross profit (1999) 1,667 Installment accounts receivable (1999) 5,000 (To adjust the repossession of merchandise)

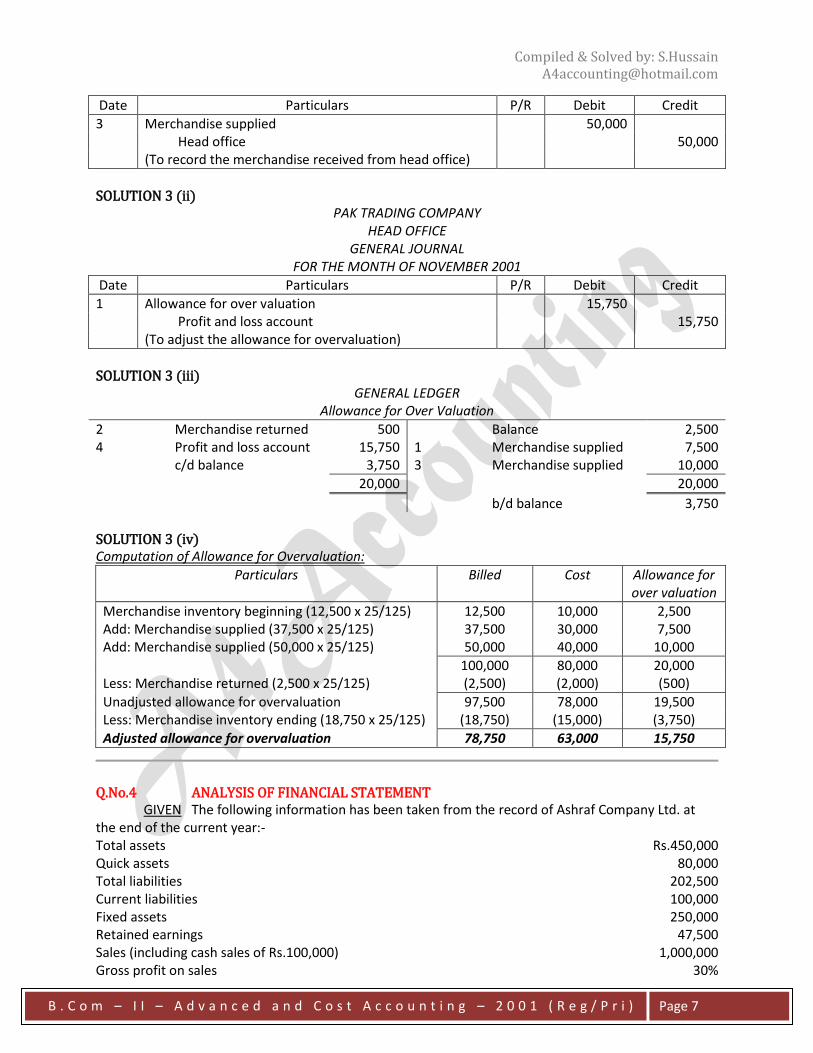

Q.No.3 BRANCH ACCOUNTING GIVEN Pak Trading Co. with its head office in Karachi has a number of branches operating independently almost in all the cities of Pakistan. Given below are the transactions and accounting data concerning head office and its Multan branch for the month of November 2001. The head office bills merchandise to all its branches at 25% above cost.

1. Multan branch reported merchandise inventory at November 01 valued at Rs.12,500 (comprising exclusively of shipments from head office).

2. Multan branch received merchandise shipment from head office at billed price of Rs.37,500. 3. Multan branch returned merchandise against shipment in (2) at billed price of Rs.2,500. 4. Multan branch received another shipment from head office at billed price of Rs.50,000. 5. A November 30, Multan branch valued its inventory at Rs.18,750. The branch is not authorized

to make merchandise purchases from its local market. REQUIRED

1) Give entries in General Journal of Multan branch to record transactions numbered 2, 3 and 4. 2) Give an adjusting entry in the General Journal of head office to record profit from allowance for

over-valuation. 3) Set up a T-account for allowance for over-valuation in the ledger of head office, post relevant

entries into it. Balance and rule off the account. 4) Show all the necessary computations on head office books.

SOLUTION 3 (i)

PAK TRADING COMPANY MULTAN BRANCH

GENERAL JOURNAL FOR THE MONTH OF NOVEMBER 2001

Date Particulars P/R Debit Credit

1 Merchandise supplied 37,500 Head office 37,500 (To record the merchandise received from head office)

2 Head office 2,500 Merchandise supplied returned 2,500 (To record the merchandise returned to head office)

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 7

Date Particulars P/R Debit Credit

3 Merchandise supplied 50,000 Head office 50,000 (To record the merchandise received from head office)

SOLUTION 3 (ii)

PAK TRADING COMPANY HEAD OFFICE

GENERAL JOURNAL FOR THE MONTH OF NOVEMBER 2001

Date Particulars P/R Debit Credit

1 Allowance for over valuation 15,750 Profit and loss account 15,750 (To adjust the allowance for overvaluation)

SOLUTION 3 (iii)

GENERAL LEDGER Allowance for Over Valuation

2 Merchandise returned 500 Balance 2,500 4 Profit and loss account 15,750 1 Merchandise supplied 7,500 c/d balance 3,750 3 Merchandise supplied 10,000

20,000 20,000

b/d balance 3,750 SOLUTION 3 (iv) Computation of Allowance for Overvaluation:

Particulars Billed Cost Allowance for over valuation

Merchandise inventory beginning (12,500 x 25/125) 12,500 10,000 2,500 Add: Merchandise supplied (37,500 x 25/125) 37,500 30,000 7,500 Add: Merchandise supplied (50,000 x 25/125) 50,000 40,000 10,000

100,000 80,000 20,000 Less: Merchandise returned (2,500 x 25/125) (2,500) (2,000) (500)

Unadjusted allowance for overvaluation 97,500 78,000 19,500 Less: Merchandise inventory ending (18,750 x 25/125) (18,750) (15,000) (3,750)

Adjusted allowance for overvaluation 78,750 63,000 15,750

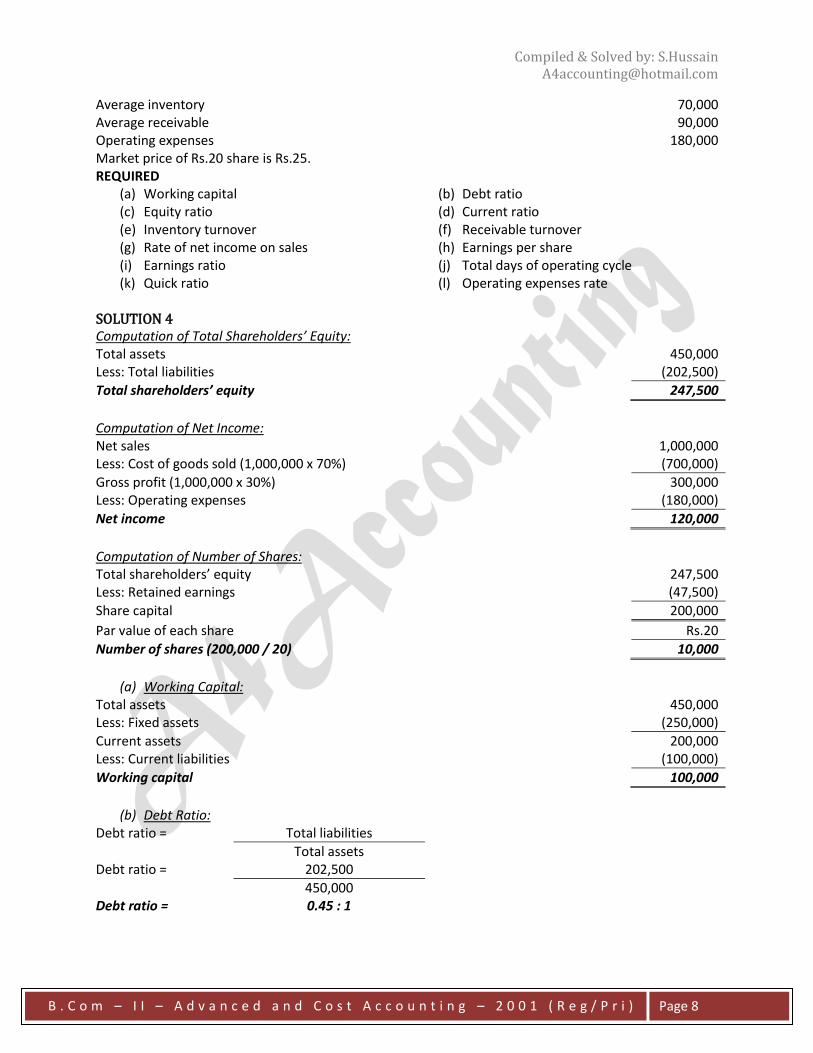

Q.No.4 ANALYSIS OF FINANCIAL STATEMENT GIVEN The following information has been taken from the record of Ashraf Company Ltd. at the end of the current year:- Total assets Rs.450,000 Quick assets 80,000 Total liabilities 202,500 Current liabilities 100,000 Fixed assets 250,000 Retained earnings 47,500 Sales (including cash sales of Rs.100,000) 1,000,000 Gross profit on sales 30%

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 8

Average inventory 70,000 Average receivable 90,000 Operating expenses 180,000 Market price of Rs.20 share is Rs.25. REQUIRED

(a) Working capital (b) Debt ratio (c) Equity ratio (d) Current ratio (e) Inventory turnover (f) Receivable turnover (g) Rate of net income on sales (h) Earnings per share (i) Earnings ratio (j) Total days of operating cycle (k) Quick ratio (l) Operating expenses rate

SOLUTION 4 Computation of Total Shareholders’ Equity: Total assets 450,000 Less: Total liabilities (202,500)

Total shareholders’ equity 247,500

Computation of Net Income: Net sales 1,000,000 Less: Cost of goods sold (1,000,000 x 70%) (700,000)

Gross profit (1,000,000 x 30%) 300,000 Less: Operating expenses (180,000)

Net income 120,000

Computation of Number of Shares: Total shareholders’ equity 247,500 Less: Retained earnings (47,500)

Share capital 200,000

Par value of each share Rs.20

Number of shares (200,000 / 20) 10,000

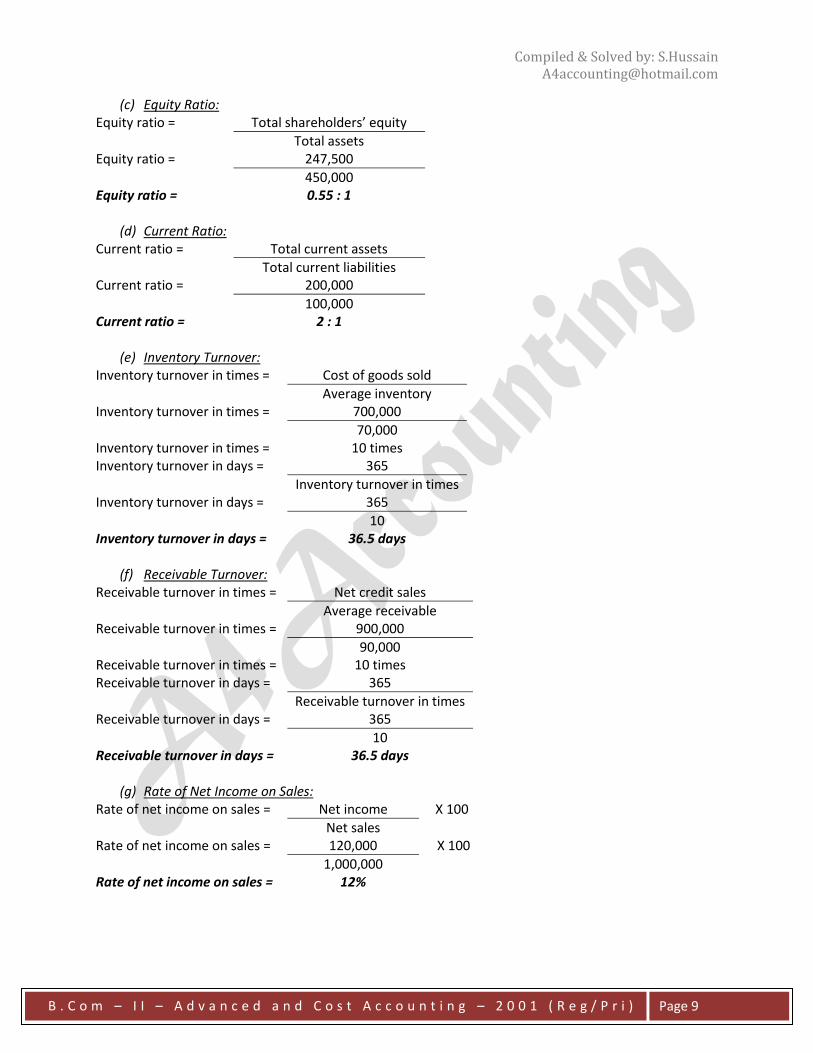

(a) Working Capital:

Total assets 450,000 Less: Fixed assets (250,000)

Current assets 200,000 Less: Current liabilities (100,000)

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 10

(h) Earnings Per Share: Earnings per share = Operating income

Number of shares Earnings per share = 120,000

10,000 Earnings per share = Rs.12

(i) Earnings Ratio: Earnings ratio = Earnings per share X 100

Market price per share Earnings ratio = 12 X 100

25 Earnings ratio = 48%

(j) Total Days of Operating Cycle: Total days of operating cycle = Inventory turnover in days + Receivable turnover in days Total days of operating cycle = 36.5 + 36.5 Total days of operating cycle = 73 days

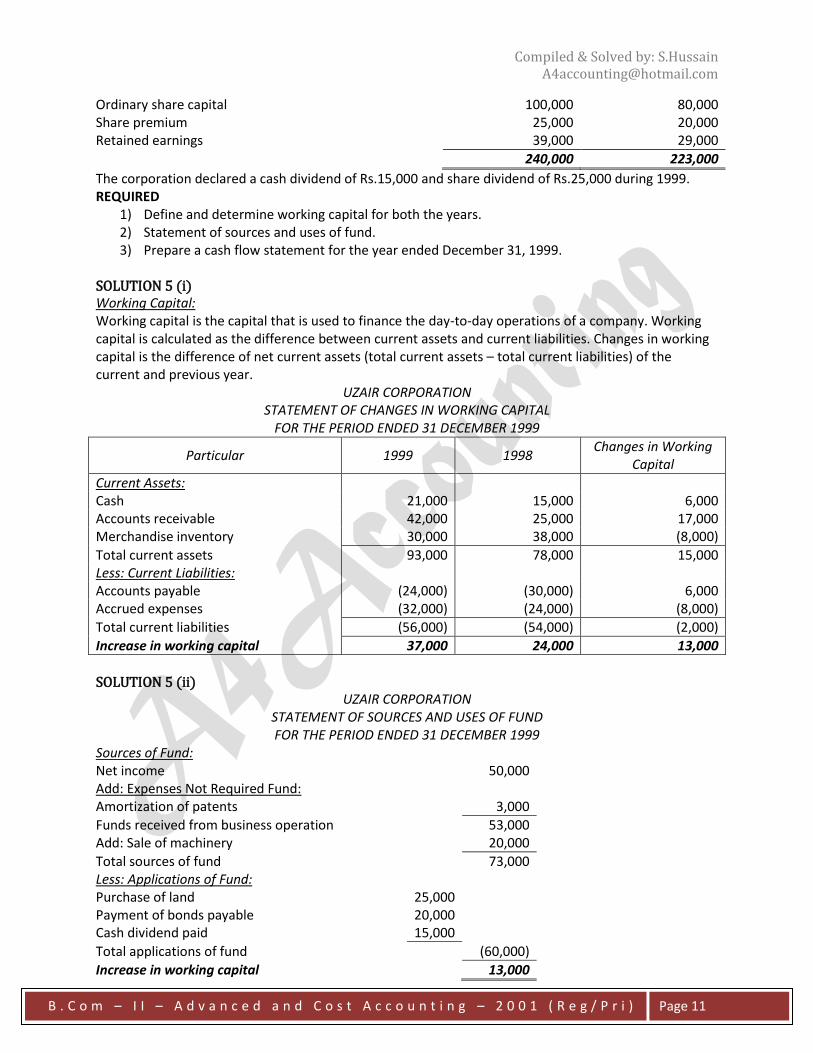

The corporation declared a cash dividend of Rs.15,000 and share dividend of Rs.25,000 during 1999. REQUIRED

1) Define and determine working capital for both the years. 2) Statement of sources and uses of fund. 3) Prepare a cash flow statement for the year ended December 31, 1999.

SOLUTION 5 (i) Working Capital: Working capital is the capital that is used to finance the day-to-day operations of a company. Working capital is calculated as the difference between current assets and current liabilities. Changes in working capital is the difference of net current assets (total current assets – total current liabilities) of the current and previous year.

UZAIR CORPORATION STATEMENT OF CHANGES IN WORKING CAPITAL

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 12

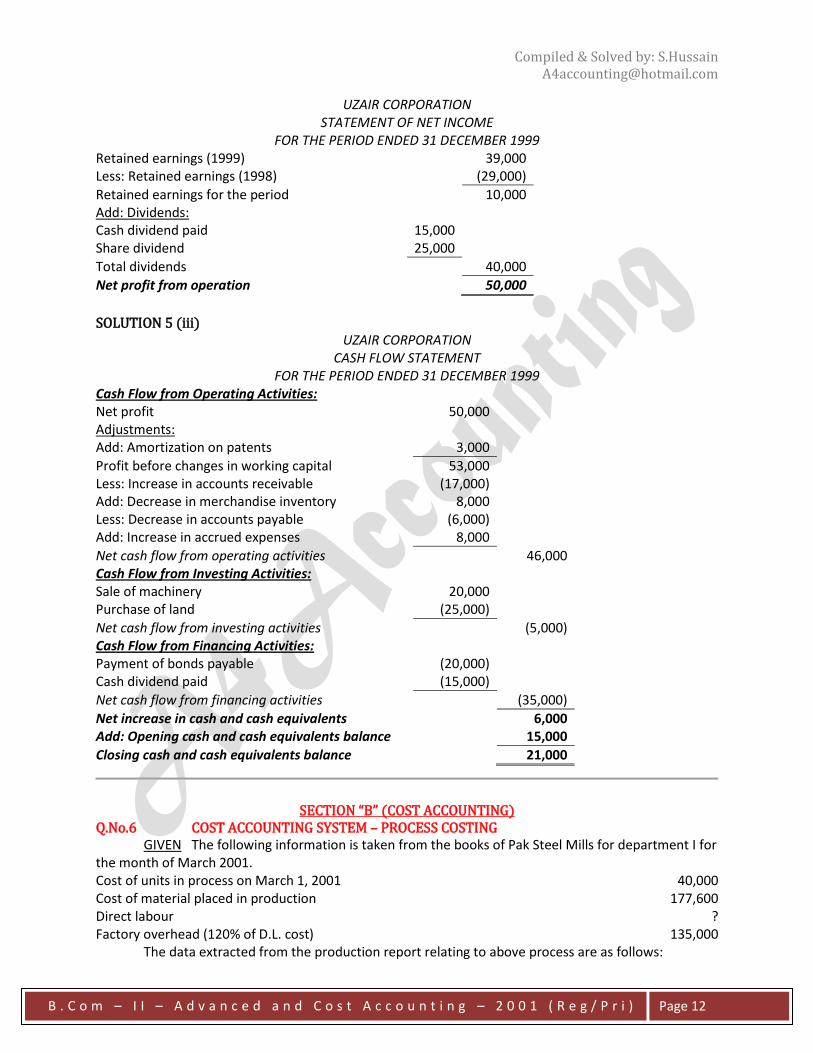

UZAIR CORPORATION STATEMENT OF NET INCOME

FOR THE PERIOD ENDED 31 DECEMBER 1999 Retained earnings (1999) 39,000 Less: Retained earnings (1998) (29,000)

Retained earnings for the period 10,000 Add: Dividends: Cash dividend paid 15,000 Share dividend 25,000

Total dividends 40,000

Net profit from operation 50,000

SOLUTION 5 (iii)

UZAIR CORPORATION CASH FLOW STATEMENT

FOR THE PERIOD ENDED 31 DECEMBER 1999 Cash Flow from Operating Activities: Net profit 50,000 Adjustments: Add: Amortization on patents 3,000

Profit before changes in working capital 53,000 Less: Increase in accounts receivable (17,000) Add: Decrease in merchandise inventory 8,000 Less: Decrease in accounts payable (6,000) Add: Increase in accrued expenses 8,000

Net cash flow from operating activities 46,000 Cash Flow from Investing Activities: Sale of machinery 20,000 Purchase of land (25,000)

Net cash flow from investing activities (5,000) Cash Flow from Financing Activities: Payment of bonds payable (20,000) Cash dividend paid (15,000)

Net cash flow from financing activities (35,000)

Net increase in cash and cash equivalents 6,000 Add: Opening cash and cash equivalents balance 15,000

Closing cash and cash equivalents balance 21,000

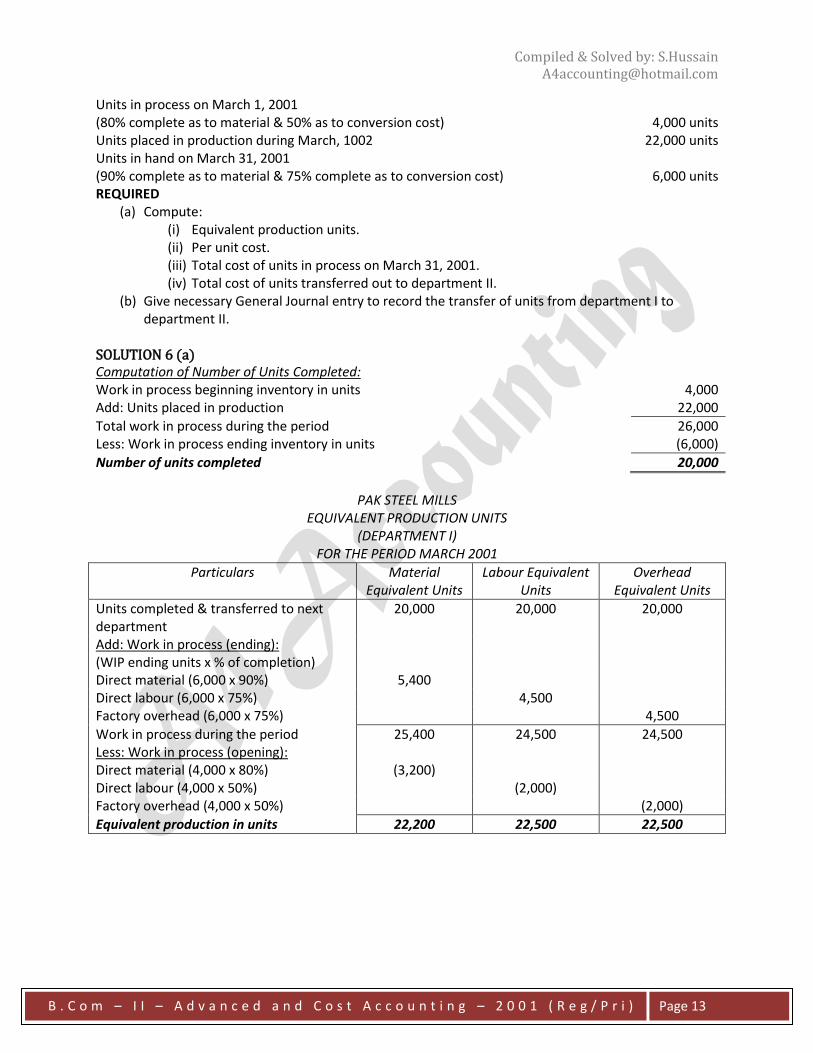

SECTION “B” (COST ACCOUNTING) Q.No.6 COST ACCOUNTING SYSTEM – PROCESS COSTING GIVEN The following information is taken from the books of Pak Steel Mills for department I for the month of March 2001. Cost of units in process on March 1, 2001 40,000 Cost of material placed in production 177,600 Direct labour ? Factory overhead (120% of D.L. cost) 135,000 The data extracted from the production report relating to above process are as follows:

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 13

Units in process on March 1, 2001 (80% complete as to material & 50% as to conversion cost) 4,000 units Units placed in production during March, 1002 22,000 units Units in hand on March 31, 2001 (90% complete as to material & 75% complete as to conversion cost) 6,000 units REQUIRED

(a) Compute: (i) Equivalent production units. (ii) Per unit cost. (iii) Total cost of units in process on March 31, 2001. (iv) Total cost of units transferred out to department II.

(b) Give necessary General Journal entry to record the transfer of units from department I to department II.

SOLUTION 6 (a) Computation of Number of Units Completed: Work in process beginning inventory in units 4,000 Add: Units placed in production 22,000

Total work in process during the period 26,000 Less: Work in process ending inventory in units (6,000)

Number of units completed 20,000

PAK STEEL MILLS

EQUIVALENT PRODUCTION UNITS (DEPARTMENT I)

FOR THE PERIOD MARCH 2001

Particulars Material Equivalent Units

Labour Equivalent Units

Overhead Equivalent Units

Units completed & transferred to next department

20,000 20,000 20,000

Add: Work in process (ending): (WIP ending units x % of completion) Direct material (6,000 x 90%) 5,400 Direct labour (6,000 x 75%) 4,500 Factory overhead (6,000 x 75%) 4,500

Work in process during the period 25,400 24,500 24,500 Less: Work in process (opening): Direct material (4,000 x 80%) (3,200) Direct labour (4,000 x 50%) (2,000) Factory overhead (4,000 x 50%) (2,000)

Equivalent production in units 22,200 22,500 22,500

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 14

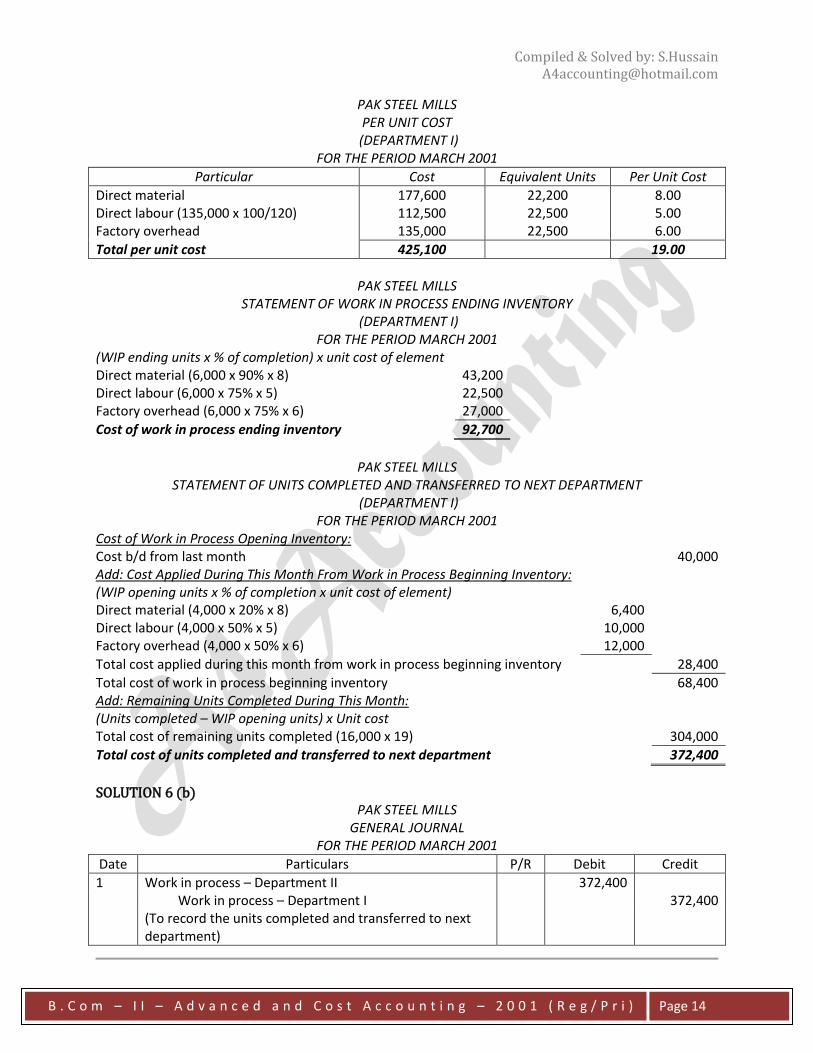

PAK STEEL MILLS PER UNIT COST

(DEPARTMENT I) FOR THE PERIOD MARCH 2001

Particular Cost Equivalent Units Per Unit Cost

Direct material 177,600 22,200 8.00 Direct labour (135,000 x 100/120) 112,500 22,500 5.00 Factory overhead 135,000 22,500 6.00

Total per unit cost 425,100 19.00

PAK STEEL MILLS

STATEMENT OF WORK IN PROCESS ENDING INVENTORY (DEPARTMENT I)

FOR THE PERIOD MARCH 2001 (WIP ending units x % of completion) x unit cost of element Direct material (6,000 x 90% x 8) 43,200 Direct labour (6,000 x 75% x 5) 22,500 Factory overhead (6,000 x 75% x 6) 27,000

Cost of work in process ending inventory 92,700

PAK STEEL MILLS

STATEMENT OF UNITS COMPLETED AND TRANSFERRED TO NEXT DEPARTMENT (DEPARTMENT I)

FOR THE PERIOD MARCH 2001 Cost of Work in Process Opening Inventory: Cost b/d from last month 40,000 Add: Cost Applied During This Month From Work in Process Beginning Inventory: (WIP opening units x % of completion x unit cost of element) Direct material (4,000 x 20% x 8) 6,400 Direct labour (4,000 x 50% x 5) 10,000 Factory overhead (4,000 x 50% x 6) 12,000

Total cost applied during this month from work in process beginning inventory 28,400

Total cost of work in process beginning inventory 68,400 Add: Remaining Units Completed During This Month: (Units completed – WIP opening units) x Unit cost Total cost of remaining units completed (16,000 x 19) 304,000

Total cost of units completed and transferred to next department 372,400

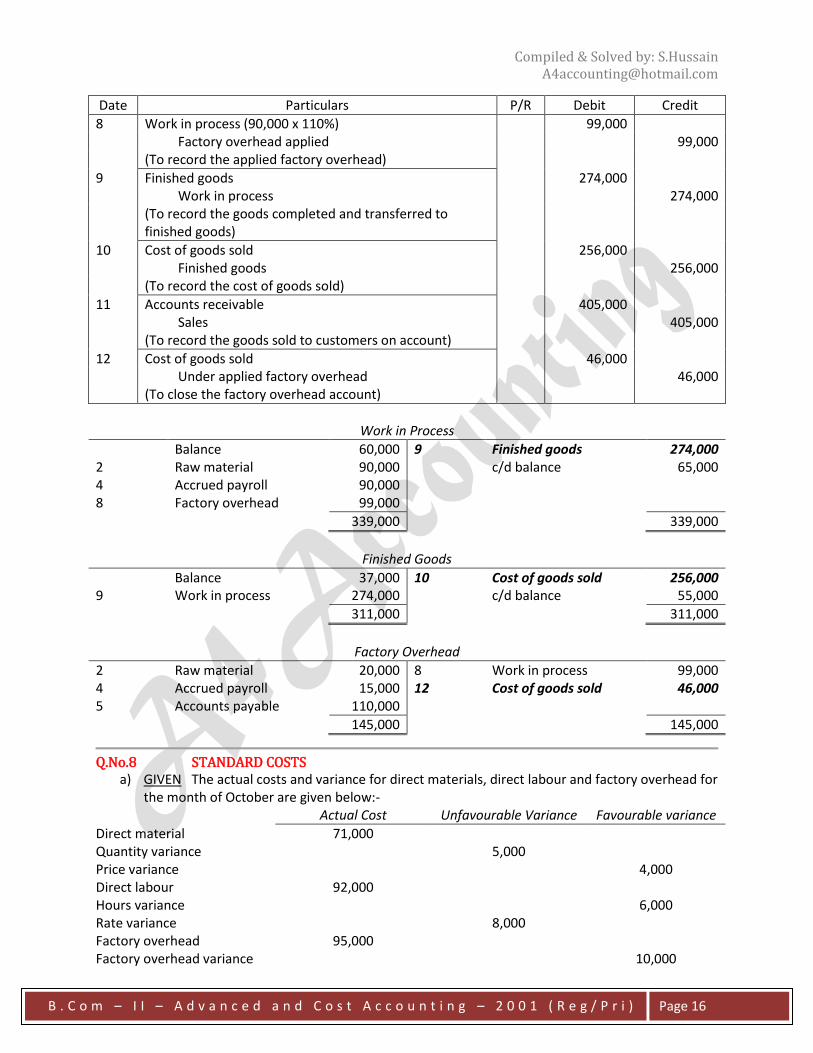

SOLUTION 6 (b)

PAK STEEL MILLS GENERAL JOURNAL

FOR THE PERIOD MARCH 2001

Date Particulars P/R Debit Credit

1 Work in process – Department II 372,400 Work in process – Department I 372,400 (To record the units completed and transferred to next

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 15

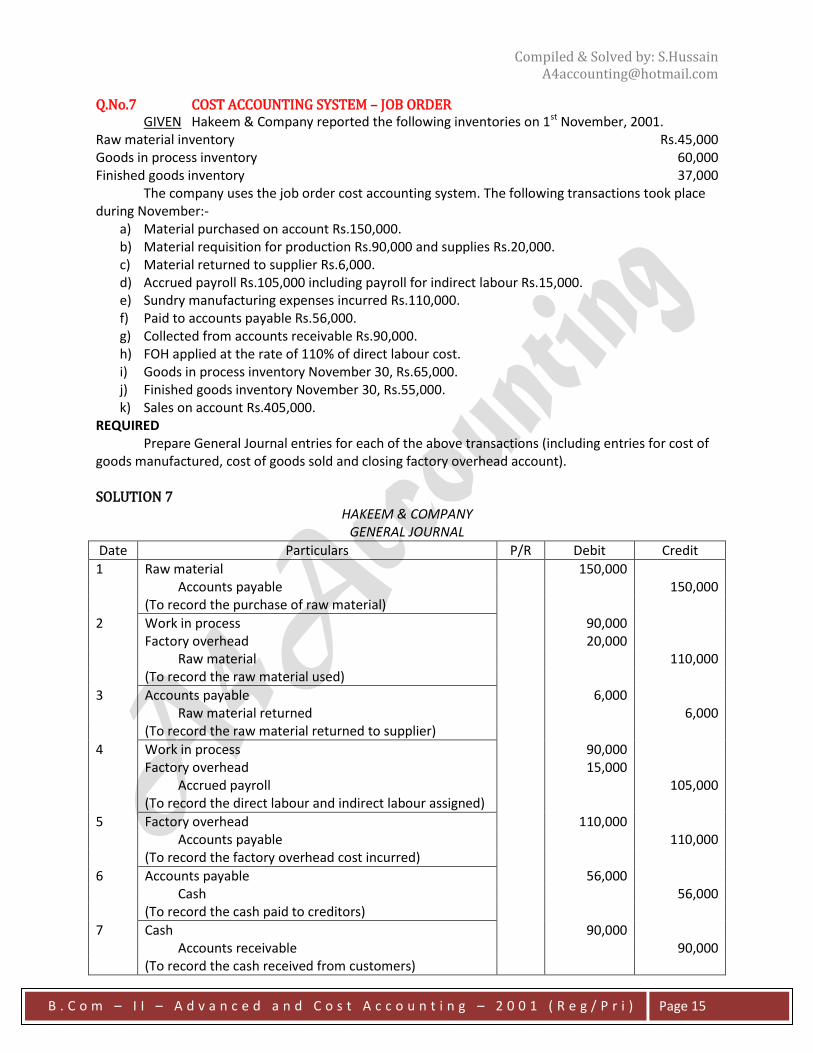

Q.No.7 COST ACCOUNTING SYSTEM – JOB ORDER GIVEN Hakeem & Company reported the following inventories on 1st November, 2001. Raw material inventory Rs.45,000 Goods in process inventory 60,000 Finished goods inventory 37,000 The company uses the job order cost accounting system. The following transactions took place during November:-

a) Material purchased on account Rs.150,000. b) Material requisition for production Rs.90,000 and supplies Rs.20,000. c) Material returned to supplier Rs.6,000. d) Accrued payroll Rs.105,000 including payroll for indirect labour Rs.15,000. e) Sundry manufacturing expenses incurred Rs.110,000. f) Paid to accounts payable Rs.56,000. g) Collected from accounts receivable Rs.90,000. h) FOH applied at the rate of 110% of direct labour cost. i) Goods in process inventory November 30, Rs.65,000. j) Finished goods inventory November 30, Rs.55,000. k) Sales on account Rs.405,000.

REQUIRED Prepare General Journal entries for each of the above transactions (including entries for cost of goods manufactured, cost of goods sold and closing factory overhead account). SOLUTION 7

HAKEEM & COMPANY GENERAL JOURNAL

Date Particulars P/R Debit Credit

1 Raw material 150,000 Accounts payable 150,000 (To record the purchase of raw material)

2 Work in process 90,000 Factory overhead 20,000 Raw material 110,000 (To record the raw material used)

3 Accounts payable 6,000 Raw material returned 6,000 (To record the raw material returned to supplier)

4 Work in process 90,000 Factory overhead 15,000 Accrued payroll 105,000 (To record the direct labour and indirect labour assigned)

5 Factory overhead 110,000 Accounts payable 110,000 (To record the factory overhead cost incurred)

6 Accounts payable 56,000 Cash 56,000 (To record the cash paid to creditors)

7 Cash 90,000 Accounts receivable 90,000 (To record the cash received from customers)

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 17

REQUIRED 1) Compute the standard costs of direct material, direct labour and factory overhead. 2) Give the entries in General Journal to record the actual and standard costs and their variances.

b) GIVEN Rashid Product Co. uses standard costs system. The cost data for various elements of

cost for manufacture of 8,000 units is following: Direct material 5,000 units @ Rs.8.00 4,800 units @ Rs.9.00 Direct labour 2,000 units @ Rs.11.00 2,300 units @ Rs.12.00 Factory overhead 90% of direct labour Rs.137,000 REQUIRED Calculate:-

i) Material quantity variance & material price variance. ii) Labour time variance & labour rate variance. iii) Factory overhead variance.

SOLUTION 8 (a) Computation of Direct Material Standard Cost: Direct materials standard cost = Material actual cost + Favourable variance – Unfavourable variance Direct materials standard cost = 71,000 + 4,000 – 5,000 Direct materials standard cost = 70,000 Computation of Direct Labour Standard Cost: Direct labour standard cost = Labour actual cost + Favourable variance – Unfavourable variance Direct labour standard cost = 92,000 + 6,000 – 8,000 Direct labour standard cost = 90,000 Computation of Factory Overhead Standard Cost: Factory overhead standard cost = FOH actual cost + Favourable variance – Unfavourable variance Factory overhead standard cost = 95,000 + 10,000 Factory overhead standard cost = 105,000

M/S. _____________ GENERAL JOURNAL

FOR THE MONTH OF OCTOBER

Date Particulars P/R Debit Credit

1 Work in process 70,000 Material quantity variance 5,000 Material price variance 4,000 Raw material 71,000 (To record the material price and quantity variance)

2 Work in process 90,000 Labour rate variance 8,000 Labour hours variance 6,000 Accrued payroll 92,000 (To record the labour rate and efficiency variance)

3 Work in process 105,000 Factory overhead variance 10,000 Factory overhead 95,000 (To record the factory overhead variance)

B . C o m – I I – A d v a n c e d a n d C o s t A c c o u n t i n g – 2 0 0 1 ( R e g / P r i )

Page 18

SOLUTION 8 (b) Computation of Material Price Variance: Material price variance = (Standard price – Actual price) x Actual quantity Material price variance = (8 – 9) x 4,800 Material price variance = (4,800) (Unfavourable) Computation of Material Quantity Variance: Material quantity variance = (Standard quantity – Actual quantity) x Standard price Material quantity variance = (5,000 – 4,800) x 8 Material quantity variance = 1,600 Favourable Computation of Labour Rate Variance: Labour rate variance = (Standard price – Actual price) x Actual units Labour rate variance = (11 – 12) x 2,300 Labour rate variance = (2,300) (Unfavourable) Computation of Labour Time Variance: Labour time variance = (Standard units – Actual units) x Standard price Labour time variance = (2,000 – 2,300) x 11 Labour time variance = (3,300) (Unfavourable) Computation of Factory Overhead Variance: Factory overhead variance = Standard cost – Actual cost Factory overhead variance = (2,000 x 11) x 90% – 137,500 Factory overhead variance = 19,800 – 137,000 Factory overhead variance = (117,200) (Unfavourable)