Benchmarking Study: Local Financial Management Framework for Good Governance* RUFO R. MENDOZA, Ph.D. Ateneo School of Government Ateneo de Manila University 45 th Annual Conference and Meeting PHILIPPINE ECONOMIC SOCIETY Nov. 14-16, 2007 *draws largely from the research of the Economic Policy Reform and Advocacy project of the USAID and the Ateneo de Manila University

Transcript

Benchmarking Study:

Local Financial Management Framework

for Good Governance*

RUFO R. MENDOZA, Ph.D.

Ateneo School of Government

Ateneo de Manila University

45th Annual Conference and Meeting

PHILIPPINE ECONOMIC SOCIETY

Nov. 14-16, 2007

*draws largely from the research of the Economic Policy Reform and Advocacy project

of the USAID and the Ateneo de Manila University

11/21/07 Local Financial Management for

Good Governance

2

Introduction

• Over a decade of Local Government Code of

1991: an opportune time to examine the

progress of LGUs in managing their finances

– LGC governs the conduct and management of

financial affairs, transactions, and operations

– LGC outlines the fundamental principles in local

fiscal administration

11/21/07 Local Financial Management for

Good Governance

3

• Minimal efforts to examine LGUs’ compliance to legal provisions

• Mechanisms for innovations and excellence in handling financial responsibilities not adequately in place

• Champions of sound LFM not given appropriate attention and rewards

wasted opportunities for coming out with norms and standards that may be adopted and replicated by

other LGUs.

11/21/07 Local Financial Management for

Good Governance

4

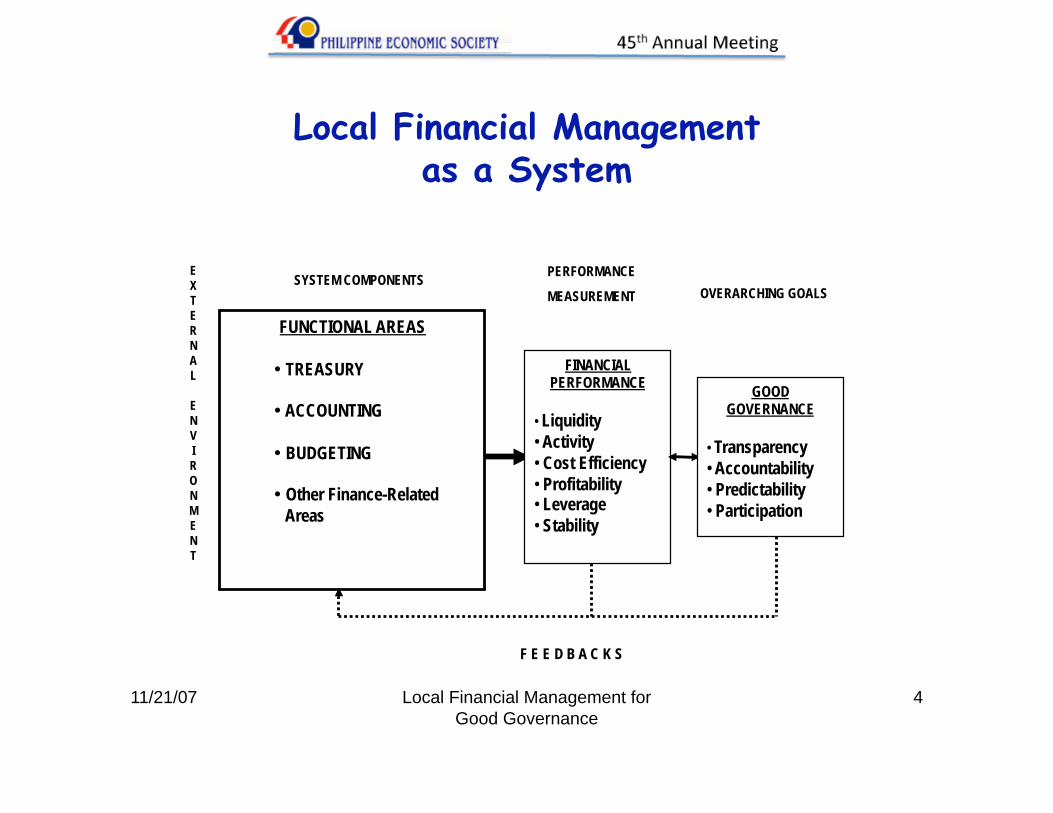

Local Financial Management as a System

FUNCTIONAL AREAS

• TREASURY

• ACCOUNTING

• BUDGETING

• Other Finance-Related

Areas

FINANCIAL PERFORMANCE

• Liquidity

• Activity

• Cost Efficiency

• Profitability • Leverage

• Stability

GOOD GOVERNANCE

• Transparency

• Accountability

• Predictability

• Participation

F E E D B A C K S

SYSTEM COMPONENTS PERFORMANCE

MEASUREMENT OVERARCHING GOALS E

X

T

E

R

N

A

L

E

N

V

I

R

O

N

M

E

N

T

11/21/07 Local Financial Management for

Good Governance

5

Methodology

COMPONENT A

IDENTIFYING PRACTICES COMPONENT B

AWARD SYSTEM

Phase 1

Identify key

measures of

financial

performance

Phase 3

Identify current

good practices

in LFM

(utilizing shortlist

of LGUs from

Phase 2)

Phase 4

Develop a

framework for

assessing LFM

in LGUs

Phase 5

Establish an

award system

in LFM

Phase 2

Select a shortlist

of relatively

high-performing

LGUs

(utilizing key

measures from

Phase 1)

11/21/07 Local Financial Management for

Good Governance

6

Key Measures of Financial Performance

Revenue Indicators

1 Local Revenues per capita = Total local revenue collection / LGU population

2 IRA dependency ratio = IRA revenues / Total revenue collection

Expenditure Indicators

3 Expenditures per capita = Total expenditures / LGU population

4 Personal services ceiling = Expenditures for personal services / Total

revenue collection

Liquidity Indicators

5 Current ratio = Current assets / Current liabilities

6 Quick ratio = (Cash + Very short-term assets) / Current liabilities

11/21/07 Local Financial Management for

Good Governance

7

Asset Turnover Indicators

7 Total asset turnover = Internally-generated revenues / Total assets