EQUITY MARKETS Small & mid caps Benelux Expectations of a mid-cycle dip offer opportunities at discounted valuations ◆ In the current context, we prefer defensive and structural growth. Avoid high cyclical and US exposure ◆ Dutch top picks: Aalberts, Arcadis, Boskalis, Fugro, Imtech and Wessanen ◆ Belgian top picks: Arseus, Colruyt, Kinepolis, Telenet, Transics and Umicore ◆ Benelux Small & Mid Cap Team Benelux small & mid caps Sailing in rough seas January 2008 SEE THE DISCLOSURES APPENDIX FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATION

Transcript

il EQUITY MARKETS

Small & mid caps Benelux

Expectations of a mid-cycle dip offer opportunities at discountedvaluations ◆

In the current context, we prefer defensive and structural growth.Avoid high cyclical and US exposure ◆

Dutch top picks: Aalberts, Arcadis, Boskalis, Fugro, Imtech andWessanen ◆

Belgian top picks: Arseus, Colruyt, Kinepolis, Telenet, Transicsand Umicore ◆

Benelux Small & Mid Cap

Team

Benelux small & midcapsSailing in rough seas

January 2008

Ben

elu

x s

mall &

mid

cap

sJan

uary

2008

SEE THE DISCLOSURES APPENDIX FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATION

Research offices: legal entity/address/primary securities regulator Almaty Representative office, ING Bank N.V. in Kazakhstan, 85a, Dostyk Avenue, Office 510, 050010, Almaty, Kazakhstan.

Agency of the Republic of Kazakhstan on Regulation and Supervision of Financial Market & Financial Organizations

Amsterdam ING Bank N.V., Foppingadreef 7, Amsterdam, Netherlands, 1102BD. Netherlands Authority for the Financial Markets

Bratislava ING Bank N.V., pobocka zahranicnej banky, Jesenskeho 4/C, 811 02 Bratislava, Slovak Republic. National Bank of Slovakia

Brussels ING Belgium S.A./N.V., Avenue Marnix 24, Brussels, Belgium, B-1000. Banking Finance and Insurance Commission

Bucharest ING Bank N.V. Bucharest Branch, 11-13 Kiseleff Avenue, Sector 1, Bucharest, Romania, 71268. Romanian National Securities and Exchange Commission

Budapest ING Bank Zrt, Dozsa Gyorgy ut 84\B, H - 1068 Budapest, Hungary. Hungarian Financial Supervisory Authority

Dubai ING Bank N.V. Dubai Branch, Level 2, Gate Village 05, Dubai International Financial Center (DIFC), PO Box 121208. Dubai Financial Services Authority

Edinburgh ING Bank N.V. London Branch (Edinburgh office), 2 Canning Street Lane, Edinburgh, United Kingdom, EH3 8ER. Financial Services Authority

Hong Kong ING Bank N.V. Hong Kong Branch, 39/F, One International Finance Centre, Central Hong Kong. Hong Kong Monetary Authority

Kiev ING Bank Ukraine JSC, 30-a, Spaska Street, Kiev, Ukraine, 04070 Ukrainian Securities and Stock Commission

London ING Bank N.V. London Branch, 60 London Wall, London EC2M 5TQ, United Kingdom. Financial Services Authority

Madrid ING Bank NV, Sucursal en Espana, C/Genova, 27. 4th Floor, Madrid, Spain, 28004. Comisión Nacional del Mercado de Valores

Manila ING Bank N.V. Manila Branch, 21/F Tower I, Ayala Avenue, 1226 Makati City, Philippines. Philippine Securities and Exchange Commission

Mexico City ING Grupo Financiero (Mexico) S.A. de C.V., Bosques de Alisos 45-B, Piso 4, Bosques de Las Lomas, 05120, Mexico City, Mexico. Comisión Nacional Bancaria y de Valores

Milan ING Bank N.V. Milano, Via Paleocapa, 5, Milano, Italy, 20121. Commissione Nazionale per le Società e la Borsa

Moscow ING Bank (Eurasia) ZAO, 36, Krasnoproletarskaya ulitsa, 127473 Moscow, Russia. Federal Financial Markets Service

Mumbai ING Vysya Bank Limited, A Wing, Shivsagar Estate, 2nd Floor, South Wing, Dr. Annie Besant Road, Worli, Mumbai, 400 018. India Securities and Exchange Board of India

New York ING Financial Markets LLC, 1325 Avenue of the Americas, New York, United States,10019. Securities and Exchange Commission

Paris ING Belgium S.A., Succursale en France, Coeur Défense, Tour A, La Défense 4, 110 Esplanade du Général de Gaulle, Paris La Défense Cedex, 92931. l’Autorité des Marchés Financiers

Prague ING Bank N.V. Prague Branch, Nadrazni 25, 150 00 Prague 5, Czech Republic. Czech National Bank

Sao Paulo ING Bank N.V. Sao Paulo, Av. Brigadeiro Faria Lima n. 3.400, 11th Floor, Sao Paulo, Brazil 04538-132. Securities and Exchange Commission of Brazil

Singapore ING Bank N.V. Singapore Branch, 19/F Republic Plaza, 9 Raffles Place, #19-02, Singapore, 048619. Monetary Authority of Singapore

Sofia ING Bank N.V. Sofia Branch, 12 Emil Bersinski Str, Ivan Vazov Region,1408 Sofia, Bulgaria. Bulgarian Central Bank and Financial Supervision Commission

Warsaw ING Securities S.A., Plac Trzech Krzyzy, 10/14, Warsaw, Poland, 00-499. Polish Financial Supervision Authority

Disclaimer This report has been prepared on behalf of ING (being for this purpose the wholesale and investment banking business of ING Bank NV and certain of its subsidiary companies) solely for the information of its clients. ING forms part of ING Group (being for this purpose ING Groep NV and its subsidiary and affiliated companies). It is not investment advice or an offer or solicitation for the purchase or sale of any financial instrument. While reasonable care has been taken to ensure that the information contained herein is not untrue or misleading at the time of publication, ING makes no representation that it is accurate or complete. The information contained herein is subject to change without notice. ING Group and any of its officers, employees, related and discretionary accounts may, to the extent not disclosed above and to the extent permitted by law, have long or short positions or may otherwise be interested in any transactions or investments (including derivatives) referred to in this report. In addition, ING Group may provide banking, insurance or asset management services for, or solicit such business from, any company referred to in this report. Neither ING Group nor any of its officers or employees accepts any liability for any direct or consequential loss arising from any use of this report or its contents. Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. Any investments referred to herein may involve significant risk, are not necessarily available in all jurisdictions, may be illiquid and may not be suitable for all investors. The value of, or income from, any investments referred to herein may fluctuate and/or be affected by changes in exchange rates. Past performance is not indicative of future results. Investors should make their own investigations and investment decisions without relying on this report. Only investors with sufficient knowledge and experience in financial matters to evaluate the merits and risks should consider an investment in any issuer or market discussed herein and other persons should not take any action on the basis of this report. This report is issued: 1) in the United Kingdom only to persons described in Articles 19, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 and is not intended to be distributed, directly or indirectly, to any other class of persons (including private investors); 2) in Italy only to persons described in Article No. 31 of Consob Regulation No. 11522/98. Clients should contact analysts at, and execute transactions through, an ING entity in their home jurisdiction unless governing law permits otherwise. ING Bank N.V., London branch is authorised by the Dutch Central Bank and regulated by the Financial Services Authority for the conduct of UK business. It is incorporated in the Netherlands and its London branch is registered in the UK (number BR000341) at 60 London Wall, London EC2M 5TQ. ING Financial Markets LLC, which is a member of the NYSE, NASD and SIPC and part of ING, has accepted responsibility for the distribution of this report in the United States under applicable requirements. ING Vysya Bank Ltd is responsible for the distribution of this report in India. EQ Additional information is available on request

1

Benelux small & mid caps January 2008

Contents Index of companies 1

Index of companies by sector 2

Changes in target price 3

Summary 4

Top picks 12

Investment theme: Recession scenario analysis 20

Investment theme: Dutch share buybacks 35

Benelux SMC valuation 42 Small caps peaked in June 2007 ............................................................................43 Valuation of European small caps...........................................................................44 Valuation of Benelux small caps .............................................................................47

Eurozone: into a lower gear 52

Rankings 59

Companies 69

Disclosures Appendix 261

Cover photograph courtesy of Getty Images

Pricing date 2/1/08 unless stated otherwise

Publication date 9 January 2008

1

Benelux small & mid caps January 2008

Index of companies

Company Page Company Page

Aalberts 70 Kinepolis 166Ackermans & van Haaren 72 Leasinvest Real Estate 168Agfa 74 Macintosh 170Alfacam 76 Melexis 172AMG 78 Metris 174Arcadis 80 Mobistar 176Arseus 82 Montea 178ASM International 84 Nutreco 180Atenor 86 Nyrstar 182Ballast Nedam 88 Océ 184BAM 90 Omega Pharma 186Banimmo 92 OncoMethylome Sciences 188Barco 94 OPG 190Befimmo 96 Option 192Bekaert 98 Ordina 194BESI 100 Pinguin 196Beter Bed 102 Quest for Growth 198BinckBank 104 Randstad 200Boskalis 106 Recticel 202Brunel International 108 Resilux 204CFE 110 Roularta Media Group 206CMB 112 Royal TenCate 208Cofinimmo 114 Samas 210Colruyt 116 SBM Offshore 212Corporate Express 118 Sioen Industries 214CSM 120 Sligro 216Cumerio 122 Smit International 218Deceuninck 124 Super de Boer (Laurus) 220D'Ieteren 126 Telegraaf Media Group 222Draka 128 Telenet Group 224Duvel Moortgat 130 Tessenderlo 226Emakina 132 TiGenix 228Eriks 134 TKH Group 230Euronav 136 TomTom 232EVS 138 Transics 234Exact Holding 140 UCB 236Exmar 142 Umicore 238Fugro 144 Unit 4 Agresso 240Galapagos 146 USG People 242Gamma 148 Van de Velde 244Grontmij 150 Van Der Moolen 246Heijmans 152 Vopak 248Home Invest Belgium 154 Wavin 250Hunter Douglas 156 WDP 252IBA 158 Wereldhave Belgium 254ICOS Vision Systems 160 Wessanen 256Imtech 162 Wolters Kluwer 258Kendrion 164 _

2

Benelux small & mid caps January 2008

Index of companies by sector

Banks Food producers & processors Pharmaceuticals BinckBank 104 CSM 120 Galapagos 146 Nutreco 180 Omega Pharma 186 Beverages Pinguin 196 OncoMethylome Sciences 188 Duvel Moortgat 130 Wessanen 256 UCB 236 Chemicals General retailers Real estate Recticel 202 Beter Bed 102 Banimmo 92 Resilux 204 Macintosh 170 Befimmo 96 Tessenderlo 226 Cofinimmo 114 Umicore 238 Health Home Invest Belgium 154 Arseus 82 Leasinvest Real Estate 168 Construction & building materials IBA 158 Montea 178 Arcadis 80 OPG 190 WDP 252 Atenor 86 TiGenix 228 Wereldhave Belgium 254 Ballast Nedam 88 BAM 90 Household goods & textiles Software & computer services Boskalis 106 Hunter Douglas 156 Exact Holding 140 CFE 110 Sioen Industries 214 Ordina 194 Deceuninck 124 Van de Velde 244 Transics 234 Heijmans 152 Unit 4 Agresso 240 Wavin 250 Investment companies Ackermans & van Haaren 72 Specialty & other finance Distributors Quest for Growth 198 Van Der Moolen 246 Eriks 134 IT hardware Steel & other metals Diversified industrials ASM International 84 AMG 78 Gamma 148 BESI 100 Cumerio 122 Royal TenCate 208 ICOS Vision Systems 160 Nyrstar 182 Melexis 172 Electronic & electrical equipment Océ 184 Support services Barco 94 Option 192 Brunel International 108 Draka 128 Corporate Express 118 EVS 138 Leisure & hotels D'Ieteren 126 Metris 174 Kinepolis 166 Grontmij 150 TKH Group 230 Randstad 200 TomTom 232 Media & entertainment Samas 210 Agfa 74 USG People 242 Engineering & machinery Alfacam 76 Aalberts 70 Emakina 132 Telecommunication services Bekaert 98 Roularta Media Group 206 Mobistar 176 Imtech 162 Telegraaf Media Group 222 Telenet Group 224 Kendrion 164 Wolters Kluwer 258 Transport Food & drug retailers Oil & gas CMB 112 Colruyt 116 Fugro 144 Euronav 136 Sligro 216 SBM Offshore 212 Exmar 142 Super de Boer (Laurus) 220 Smit International 218 Vopak 248

_

3

Benelux small & mid caps January 2008

Changes in target price

Company Recommendation Target price Previous target price

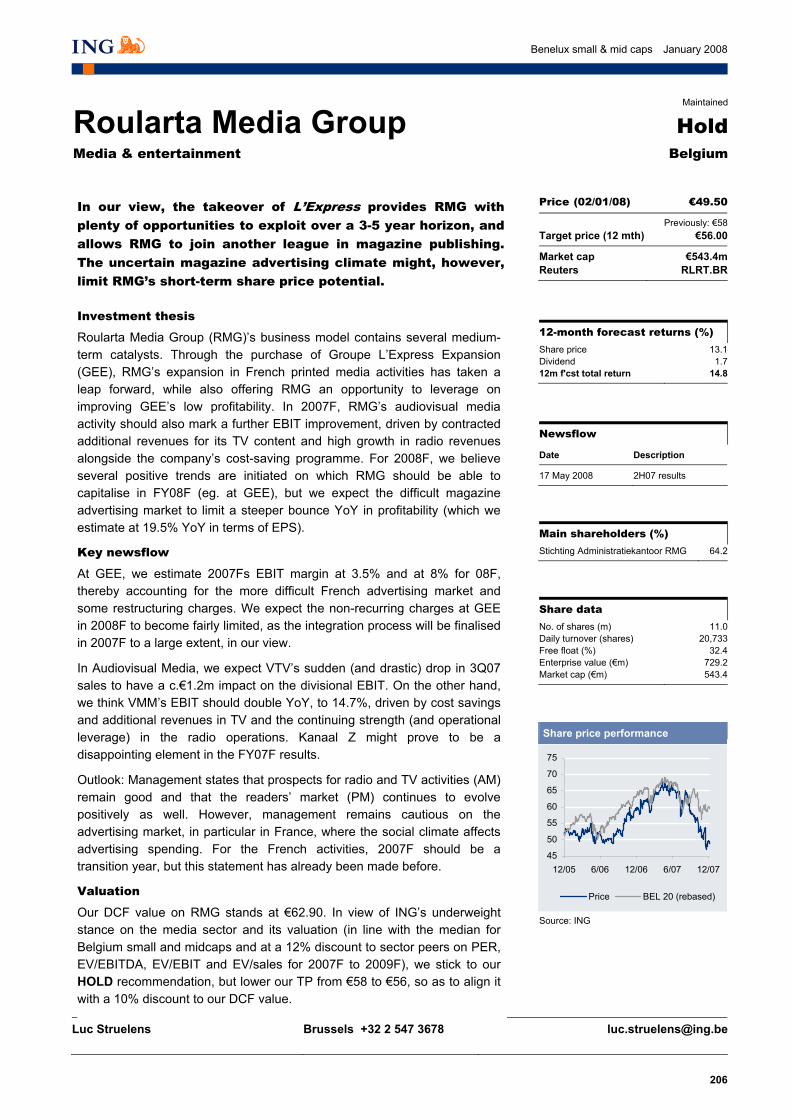

Ackermans & van Haaren Buy 83.00 85.00ASM International Hold 17.00 19.00Ballast Nedam Hold 32.00 39.00BAM Buy 21.00 27.00Corporate Express Hold 5.50 8.00Deceuninck Hold 17.50 20.50Eriks Hold 49.00 62.00Grontmij Hold 27.00 32.00Home Invest Belgium Hold 53.00 60.00IBA Hold 21.00 22.00Océ Hold 12.50 13.50Recticel Hold 11.30 10.60Roularta Media Group Hold 56.00 58.00Royal TenCate Hold 22.00 27.00Umicore Buy 211.00 191.00Wavin Hold 9.50 10.80

Source: ING

_

4

Benelux small & mid caps January 2008

Summary

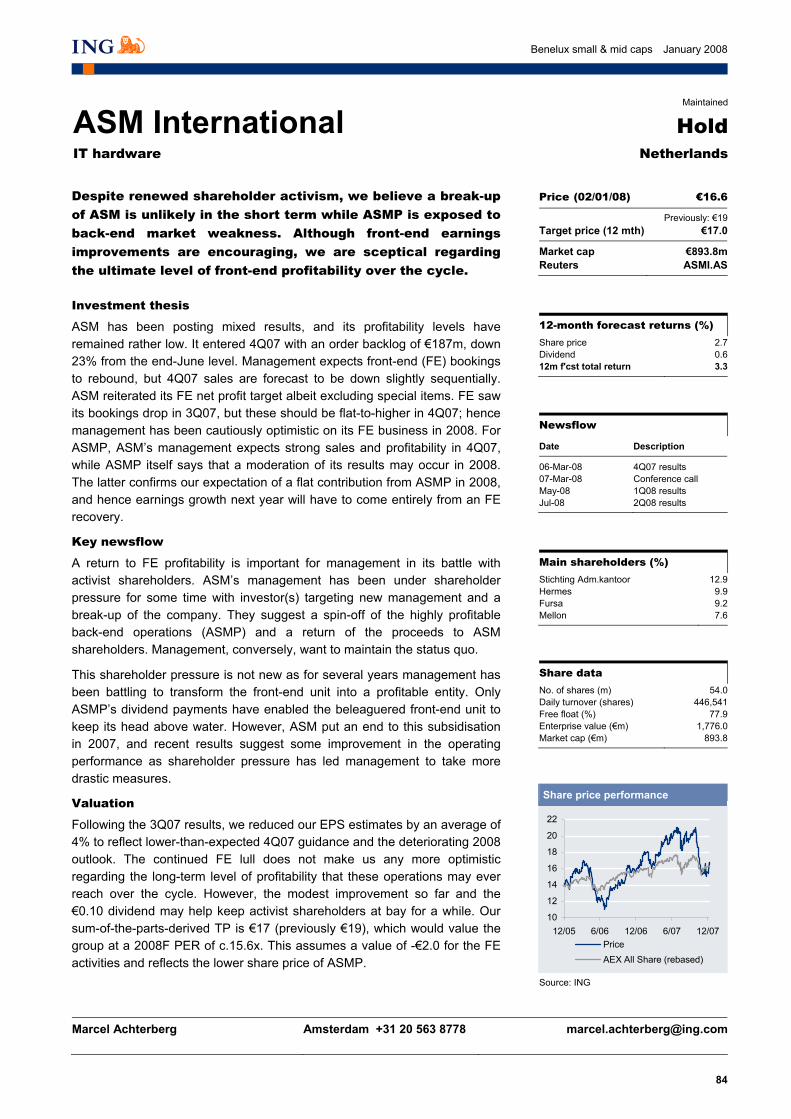

Benelux small and mid caps have been de-rated since mid-2007, like other European small and mid caps (SMCs), albeit to a lesser extent. Rising aversion to risk, fears of slowing growth and liquidity concerns are behind the SMC meltdown. Our base-case scenario is for a mid-cycle dip but no recession and, as such, we expect Benelux SMCs to deliver slowing, but still double-digit earnings growth, beating the European average in 2008F and matching it in 2009F.

The sell-off has led to more attractive valuations: Benelux SMCs now trade below their long-term average 12-month-forward PERs and at a discount to domestic large caps. In addition, Dutch SMCs trade at a discount to their European peers, while Belgian SMCs are now at a premium. Our preference in terms of investment opportunity is again for Dutch SMCs given their more attractive valuation and growth prospects. The Belgian SMC market is, however, more defensive and growth-oriented.

12 top picks. Although stock picking remains the name of the game among small and mid caps, our selection reflects a preference for the following criteria: (1) defensive profile; (2) earnings visibility; (3) structural versus cyclical growth; (4) strong value chain positioning; (5) limited exposure to the US economy and the US dollar; (6) strong balance sheet; and (7) liquidity.

Fig 1 ING Benelux small- and mid-cap top picks

Country Rec Mkt cap Price Target Upside PER (x) (€m) (€) price (€) (%) 2007F 2008F 2009F

Average 1,980 32.0 18.5 14.1 12.4 Benelux median 673 13.8 14.0 12.6 11.2

Source: ING estimates

_

Investment theme 1: recession impact analysis of Benelux SMCs

We explicitly expect a mid-cycle dip scenario and not the beginning of a recession in 2008. However, parts of the equity markets have had sharply negative reactions to the slowing trend in economic activity indicators in the US and Europe. We have conducted an analysis of what might happen in a recession scenario. Our main conclusions are as follows:

Benelux SMCs do NOT fully discount a recession; we expect 39% downside to current share prices in a recession scenario. All the stocks in our research universe would see downside, ranging from 6% to 90%. We calculate that downward earnings revisions account for 31% of the downside, while multiple contraction, from PER 12.5x to 10.5x, accounts for a further 13%.

5

Benelux small & mid caps January 2008

Summary (cont’d)

We would expect a further 40% downside for Dutch stocks and 30% for Belgian stocks. Earnings for Dutch stocks would go down 34% relative to our 2008F EPS. We find that the trough valuation would be at 9.5x PER (vs 11x currently). Earnings for our Belgian stocks would go down 30% relative to our 2008F EPS. Belgian SMCs would see a trough valuation at 12.5x PER (vs 14x currently).

Most attractive stocks in a market recovery: In the Netherlands, Randstad (Buy), USG People (Buy), Heijmans (Buy), Wavin (Hold), Brunel (Hold) and Aalberts (Buy). In Belgium, Kinepolis (Buy), Omega Pharma (Buy), Tessenderlo (Buy), Metris (Buy), CFE (Buy) and D’Ieteren (Buy), which all score highly on a combination of high share price decline from 2007 highs and a high score in a 50% recession risk/reward analysis

Stocks to avoid in a recession: Stocks with high downside risk in a recession scenario are typically companies with a low level of earnings in 2007, high net debt, cyclical earnings and no significant change in their structural outlook relative to history.

Fig 3 Benelux SMC stocks with high downside in a recession scenario

Netherlands Rec Downside (%)

Current price (€)

Recession price (€)

Belgium Rec Downside (%)

Current price (€)

Recession price (€)

Samas Hold -90 5 0.5 Emakina Hold -68 10.8 3.5Van Der Moolen Hold -79 3 0.6 CMB Buy -56 58.5 26BESI Hold -73 3.7 1 Pinguin Buy -55 16.2 7.2Ballast Nedam Hold -69 27.9 8.6 Agfa Sell -53 10.7 5Vopak Hold -66 38 13.1 Euronav Hold -51 24.3 12Unit 4 Agresso Buy -63 19.3 7.2 ICOS Vision Sys. Buy -48 31 16.1Smit International Hold -62 69 26.1 Barco Buy -46 51.9 28Beter Bed Buy -59 18.2 7.4 Exmar Hold -45 19.9 11Ordina Hold -59 12.2 5 Option Hold -44 5.7 3.2Corporate Express Hold -58 5.2 2.2 Sioen Industries Buy -41 9.8 5.8

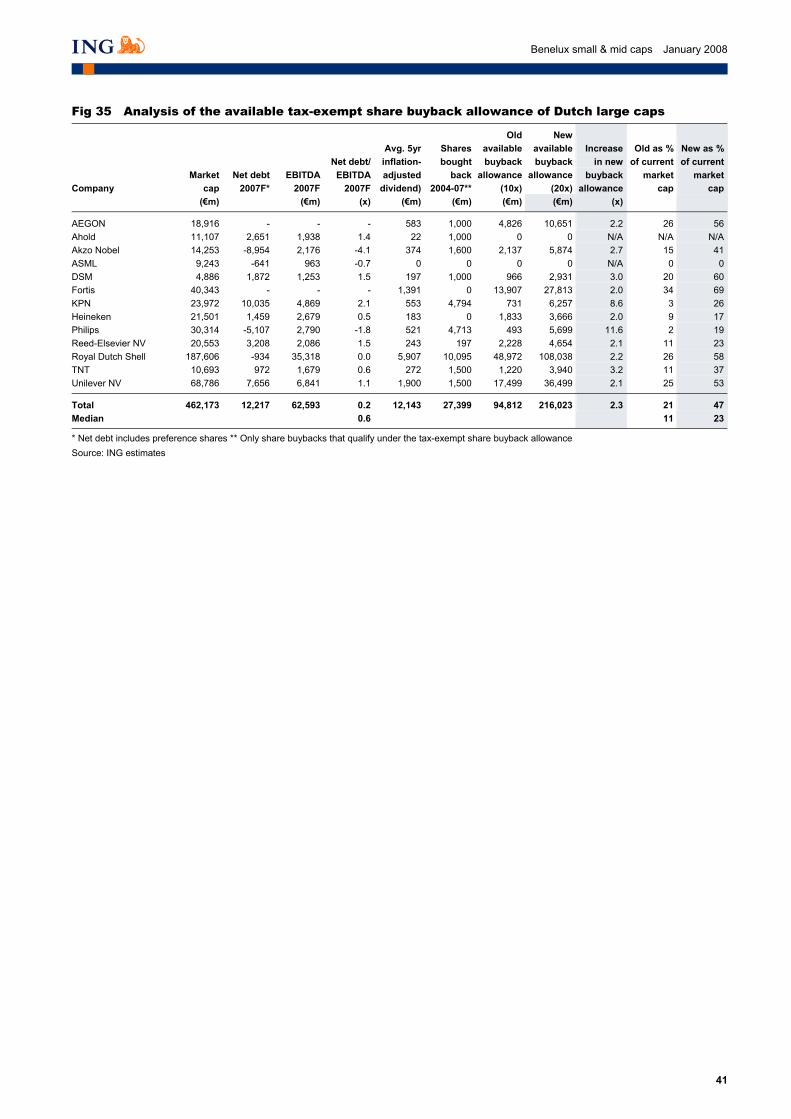

The Dutch government has changed the law to allow more dividend-tax-exempt share buybacks as of 2008. As a result, Dutch listed companies’ calculated tax-free share buyback allowance doubles. Companies with strong recent share buyback activity (2004-07) see a significant increase in their available allowance for tax-free share buybacks. We expect a limited impact on small and mid caps (CSM and Wolters Kluwer benefit most) and a significant impact on large caps (particularly Philips, KPN, DSM and TNT).

Fig 2 Downside in recession scenario for Benelux small and mid caps

Median, in %

Recent decline from 12m

high*Expected downside

Expected decline from 12m high

Decline in previous bear market from high**

Dutch small and mid caps -28 -40 -60 -67Belgian small and mid caps -13 -30 -45 -56

Benelux small and mid caps -21 -39 -53 -65

* Recent decline based on the current price and the highest monthly share price in 2007. ** Actual decline in previous bear market measured excluding the lowest share price and the highest share price since 2000 on a monthly basis Source: ING estimates, Bloomberg

6

Benelux sm

all & m

id caps January 2008

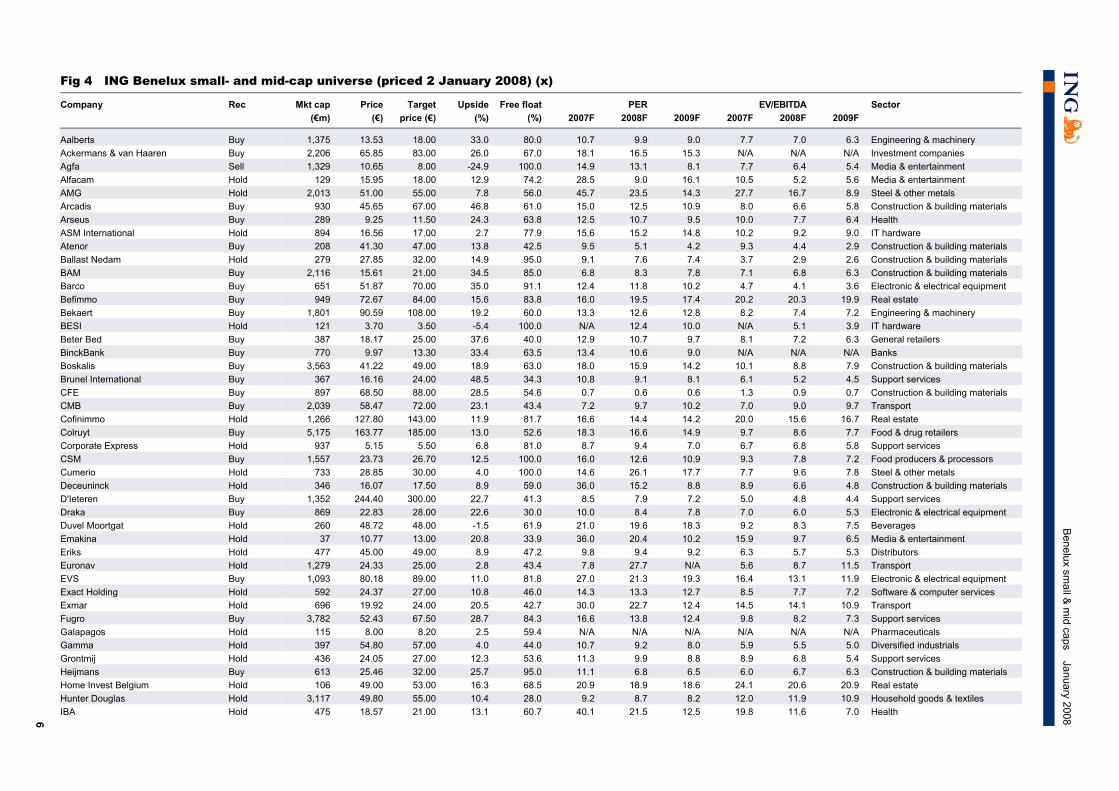

Fig 4 ING Benelux small- and mid-cap universe (priced 2 January 2008) (x)

Our small- and mid-cap universe includes all the Belgian and Dutch companies we cover with a market cap of up to €3bn, plus a few larger companies that we believe are perceived to be local Benelux companies.

The total number of companies covered in this report is 94, of which 45 are Dutch and 49 Belgian. Within our universe, we have selected 12 stocks as our top picks, which are summarised in the tables below. We provide the main points for our investment case over the following pages.

Average 1,980 32 18.5 14.1 12.4 9.2 7.8 6.8Benelux median 673 14 14.0 12.6 11.2 8.4 7.4 6.5

Source: ING estimates

_

As Figure 6 shows, the 32% average upside for our top picks is clearly superior to the average in our Benelux universe (14%). Valuation multiples are more demanding than the Benelux average, but the gap is limited.

As Figure 7 highlights, liquidity, as measured by average free float and market cap, is higher among our top picks than the rest of our SMR universe, and, interestingly, balance sheets are less highly leveraged than the average of our universe. In addition, the rate of de-gearing is stronger, which suggests superior cash generation.

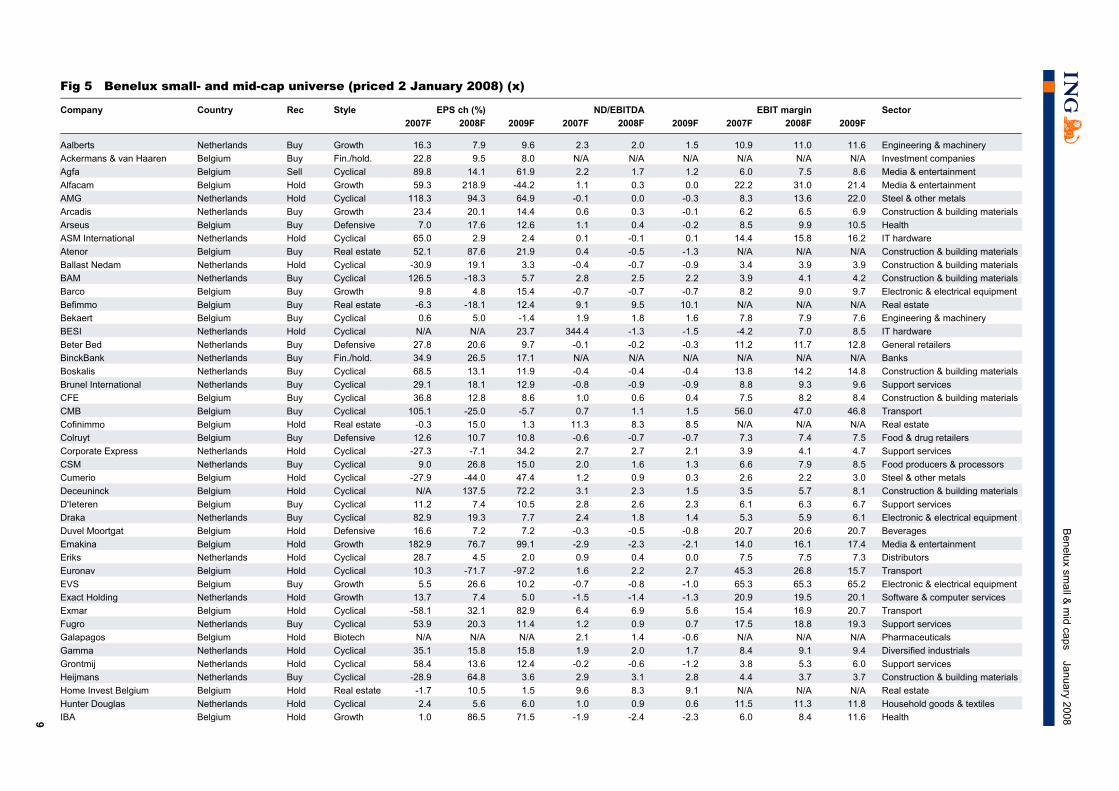

Fig 7 Sector, liquidity, growth and balance sheet metrics

EPS growth (%) Net debt/EBITDA (x) Company Sector Free float (%) 2007F 2008F 2009F 2007F 2008F 2009F

Median 62.0 30.7 18.9 11.7 0.7 0.3 -0.2Benelux median 60.4 15.4 15.0 11.1 1.1 0.9 0.5

Source: ING estimates

_

Universe of 94 stocks

12 top picks

Attractive upside

Superior liquidity and balance sheet strength

13

Benelux small & mid caps January 2008

Aalberts: BUY, TP €18.00 (33% upside) Strong niche player. Aalberts has successfully carried out an impressive string of acquisitions, strengthening its market positions and offering ample room for cross-selling. In terms of its current business mix, Industrial Services generates 31% of turnover and 30% of EBIT, versus 69% and 70%, respectively, for Flow Control. Its leading positions in niche markets give Aalberts strong pricing power, while, on the supply side, its increased scale is very beneficial for its purchasing power, in our view.

Growth story to continue. Aalberts targets top-line growth of 20% pa through acquisitions (10-15%) and organically (5-10%). This has in the past resulted in healthy double-digit EPS growth (c20% on average) over the past ten years. Looking at acquisitions, we believe Aalberts’ war chest is well filled (€250-300m). If the company were to use it, we estimate that it could add 10-15% to EPS. In fact, Aalberts has made a good start to 2008 with an attractive acquisition in Industrial Services.

Sustainable profitability in a recession. The company is more recession-proof than it looks at first sight; history shows that profitability is sustainable in an economic downturn. During the previous recession, Aalberts managed to keep the top line up well (zero organic growth) and to maintain its EBITA margin at high levels (11%).

Valuation: recent share price drop overdone. After reaching a peak of close to €22 in the summer, the stock was hit strongly, declining to its current €13.5 level, implying a very attractive valuation, trading at a 2008F PER of 9.9x, well below its historical range of 12-14x. Taking into account its improved business mix but some slowdown in market conditions, we see a valuation in the middle of the range as justified, giving a target price of €18.00, which is supported by our DCF and SOTP valuations.

Arcadis: BUY, TP €67.00 (47% upside) Arcadis is an international engineering firm with worldwide operations and a bias towards the Netherlands and the US. Half of its €1.2bn revenue is from consultancy on infrastructural work, while c.40% is derived from environmental services. Its main financial objectives are 10% top-line growth (5% organic and 5% from acquisitions) and a 10% EBIT margin. As it is exceeding its EBITA margin target in 2007, we expect the company to raise its target to 11-12% soon.

A compelling story in the Benelux small- and mid-cap arena. Arcadis is firing on all cylinders, fuelled by sound organic sales growth (>10% in 2007F) thanks to favourable market conditions. Furthermore, active portfolio management involving acquisitions and divestments with a shift to higher added value is bearing fruit, together with organic growth, supporting Arcadis’s objective of reaching its margin target soon.

Arcadis is a major-league player in environmental services. Its environmental services business generates double-digit growth and margins. It is a top-five worldwide player in this field after the acquisition of US firm BBL (which added 15% to turnover), a more profitable organisational model in the US and significant synergies (cross-selling and expanding the product/service line with products such as GRiP).

We expect 20% EPS growth pa until 2009 despite very strong growth in the past (40%-plus). Arcadis is a rock-solid investment, supported by a strong balance sheet, a clear strategy and strong execution. At a 2008F EV/EBITDA of 6.6x, the stock trades at a 24% discount to its peer group, which we see as unjustified, particularly given its superior growth and leading position in environmental services. We believe the stock should trade at a 10% premium to the sector; hence our target price of €67.

14

Benelux small & mid caps January 2008

Arseus: BUY, TP €11.50 (24% upside) Arseus was Omega Pharma’s business-to-business (B2B) activity, providing products and services to European healthcare professionals and institutions, such as pharmaceutical compounding products and services, dental consumables and equipment, integrated medical IT solutions (hardware and software). It was spun off through an IPO in October 2007.

Arseus aims to become a pan-European market leader, through acquisitions of companies and selective greenfield operation start-ups. The company targets €500m in sales by 2010F from €300m in 2007F, driven almost equally by internal and external growth. The “Buy and Build” strategy is hence the cornerstone of its business model.

In view of the company’s still limited scale and its still highly Benelux-oriented geographical scope, the potential for expansion is substantial and should offer Arseus major opportunities to benefit from economies of scale, leading to earnings growth above our current forecasts as these are based purely on organic growth.

We rate Arseus a BUY as: (1) the 3Q07 trading update was reassuring; (2) the company’s valuation is low (a 2008F PER of 9.8x, a 2008F EV/EBIT of 8.6x, 37% below sector peers and 24% below the median for Belgian SMCs when comparing PER and EV/EBIT for 2008F and 2009F; our DCF value points to €13.50 per share); and (3) management has indicated that takeovers should come in the very short term. We consider this last point as the main trigger for Arseus’s shares as we believe the external growth should be earnings-accretive. Our €11.50 target price is set at a 15% discount to our estimated DCF value.

Boskalis: BUY, TP €49.00 (19% upside) Boskalis is the market leader in the international dredging market. Dominated by four players, the international dredging market forms a nice oligopoly. This power block operates a large, well diversified and highly efficient dredging fleet, which creates an impregnable barrier to market entry.

Industry book-to-bill at an unprecedented level. In the past two-and-a-half years, the dredging industry has been overwhelmed with orders. As a result, the sector has an average of three years of work, providing excellent visibility. Looking at the global project pipeline, we expect a continuation of large dredging and land reclamation project awards. In this scenario, we expect market demand to exceed current market capacity for a considerable time.

Project picking and bottleneck on supply side boosting prices. The supply side of the dredging market remains tight until end-2011. Project picking is the right strategy to follow in order to enhance operating margins further. In Boskalis’s case, we believe the two harbour-extension and three LNG-related projects won in 2007 will fuel higher operating margins going into 2008, particularly as these types of projects are of vital importance to its customers.

The quality of the 2007 margin improvement provides us with comfort that margins will expand further. The stock trades at a 2009F PER of 14.2x and an EV/EBITDA of 7.9x, the latter matching its previous peak multiple, although comparing the current market situation with previous upturns really understates present market dynamics. Hence, we feel comfortable with our €49 DCF-based target price, which suggests a 2009F target EV/EBITDA of 9.5x.

15

Benelux small & mid caps January 2008

Colruyt: BUY, TP €185.00 (13% upside) A high-growth and high-margin Belgian food retailer. Colruyt realises over 90% of its EBIT through its highly profitable Belgian Colruyt (21% market share) and Okay banners. Other activities include general retail operations under the Dreamland banner, French foodservice and some other smaller operations. Earnings growth is almost completely driven by the Colruyt banner. In case of a consumer spending slowdown, Colruyt is relatively well protected, being low-cost, selling at considerably lower prices than the competition, and having the highest sales densities and margins.

We are optimistic about the group’s sustainable sales growth potential. In the next few years, Colruyt aims to add 12,000m2 of new selling space per annum (+3.5% YoY). Together with estimated like-for-like sales growth of 3% for the Colruyt banner and faster growth at other operations, this should lead to a sustainable 7% organic sales growth rate at high incremental returns.

Highly cash-generative. With a group EBIT margin for 2007F of 7.3%, capex under control and high sales growth, the group should be able to increase free cash flow levels towards €250m per annum. To deal with an over €400m net cash position, Colruyt already bought back €170m worth of own shares in 2007.

Best-in-class player trading below par on 2008F EV/EBIT. We are BUYers of Colruyt as we foresee further high-single-digit organic sales growth in combination with a sustainable 10% net profit growth outlook and a valuation that does not reflect its sound growth profile. The shares currently trade at a 5% discount to peers on 2008F EV/EBIT (10.8x), which adds to the attractiveness of the stock as suggested by the 13% upside to our DCF-based €185 target price.

Fugro: BUY, TP €67.50 (29% upside) Dominant player in specific niches of the oil services industry. Fugro is a global engineering firm, with 71% of its €1.4bn revenues related to oil & gas, 21% to construction and 6% to mining. Fugro has leading (often dominant) global market positions in all of its three divisions: Geotechnical (on- and offshore); Survey (on- and offshore and positioning); and Geoscience (airborne, seismic and reservoir modelling).

Capex boom in oil & gas offers upbeat long-term prospects. Oil majors have underinvested for years, and are having difficulties maintaining reserves and output at adequate levels. As a result, the oil & gas industry is experiencing an unprecedented investment boom, leading to double-digit increases in capex. This structural boom could continue for as long as a decade. Note that we are particularly upbeat on Fugro’s seismic and survey activities over the next few years (together c.62% of sales).

We expect a 27% EPS 2006-09F CAGR, significantly higher than the 15% of its peers in the European oil services sector. This is on the back of: (1) double-digit organic revenue growth (2007F: 20%), mainly because Fugro’s late 2006 extra investments in equipment and ships were well received by clients who seem to have an insatiable demand for Fugro’s services in seismic and survey; and (2) small to medium-sized acquisitions that offer valuable add-on services in exchange for Fugro’s worldwide network considerably raising their productivity and earnings.

Our favourite in the sector and one of our favourites among Benelux small and mid caps. At a 2008F EV/EBITDA of 8.2x, Fugro is valued at a 15% discount to the European oil services sector. Given its strong outlook, dominant market positions and superior earnings growth, we believe Fugro should be valued in line with the sector.

16

Benelux small & mid caps January 2008

Imtech: BUY, TP €25.00 (51% upside) Dominant player in Benelux and German markets. Imtech derives c.32% of sales from the Benelux market and c.30% from Germany. Fortunately for the company, both markets happen to be in recovery mode. Imtech also operates very profitable branches in the UK and Spain (together c.12% of sales), and via its ICT & Technology division (26% of sales) it offers high-added-value technical services, ranging from mechanical engineering to IT services.

Our model assumes a 5.7% EBITA margin in 2008F. Although this is in line with management’s long-term margin target (6% before holding costs), the consensus is well below this number at c.5%. We strongly believe the market is underestimating the late-cyclical nature of the technical services business. Non-listed peer group analysis shows that industry margins bottomed in 2005-06. We therefore expect a strong rebound in profitability over the next two years.

Imtech’s vigorous acquisition path has repositioned the business model. Imtech has bought many companies over the past few years, not only strengthening its market positions, but, in our view, also enhancing its profitability footprint. These acquisitions are expected to surprise on the upside, and this could be a vital driver to the group reaching management’s margin targets, surprising consensus expectations.

Our favourite in Dutch construction. Based on our €25 target price, Imtech would trade at a 2009F EV/EBITDA of 8.4x. Our target price is backed by a DCF analysis, which uses an unleveraged balance sheet. Our model does not incorporate further acquisitions. The reality is likely to be different. Assuming a more leveraged balance sheet structure, our DCF valuation would easily exceed €30.

Kinepolis: BUY, TP €57.00 (71% upside) Kinepolis is a digital media group that operates 318 cinema screens, mainly in Belgium, France and Spain. In Belgium (51% of sales), it is the leading operator with 139 screens. The company owns 860,000m² of real estate assets.

We believe Kinepolis is a defensive stock, with good visibility on earnings growth. Top-line growth should come from: (1) higher ticket prices (digital projection, which should account for 100% of the showings by mid-2009, allows Kinepolis to increase ticket prices by close to 11%); and (2) increased spend by visitors through the remodelling of the theatres that will be rolled out internationally within the next three years. Based on Kinepolis’s pilot projects, we conservatively assume that food and beverage spending will increase by 30% internationally by 2010 (versus 1H07 figures).

There is also value in its real estate. We estimate the value of Kinepolis’s property portfolio (860,000m², made up of cinema theatres, concessions and parking spaces) at €353m, compared with a book value of €247m. We expect Kinepolis to split the company internally into two divisions: real estate and cinema. As such, the real estate division would rent out its theatres to the cinema division. We expect the real estate division to gradually develop its properties, and hence realise important capital gains.

We rate Kinepolis a BUY, with a target price of €57, based on a SOTP model in which we value the company’s real estate at €353m and its cinema activities at €190m, implying a very cautious 2008F EV/EBITDA of 7x ‘after real estate rent’. Kinepolis’s peers trade at 7.5-8.5x 2008F EV/EBITDA on average.

17

Benelux small & mid caps January 2008

Telenet: Buy, TP €23.50 (19% upside) Market leader in Flanders for broadband internet and TV business. Telenet is one of the most advanced cable operators in Europe. Its network is limited to Flanders, which makes its 33% broadband market share even more impressive, and it is the only company that has been able to rival Belgacom’s domination of Belgium.

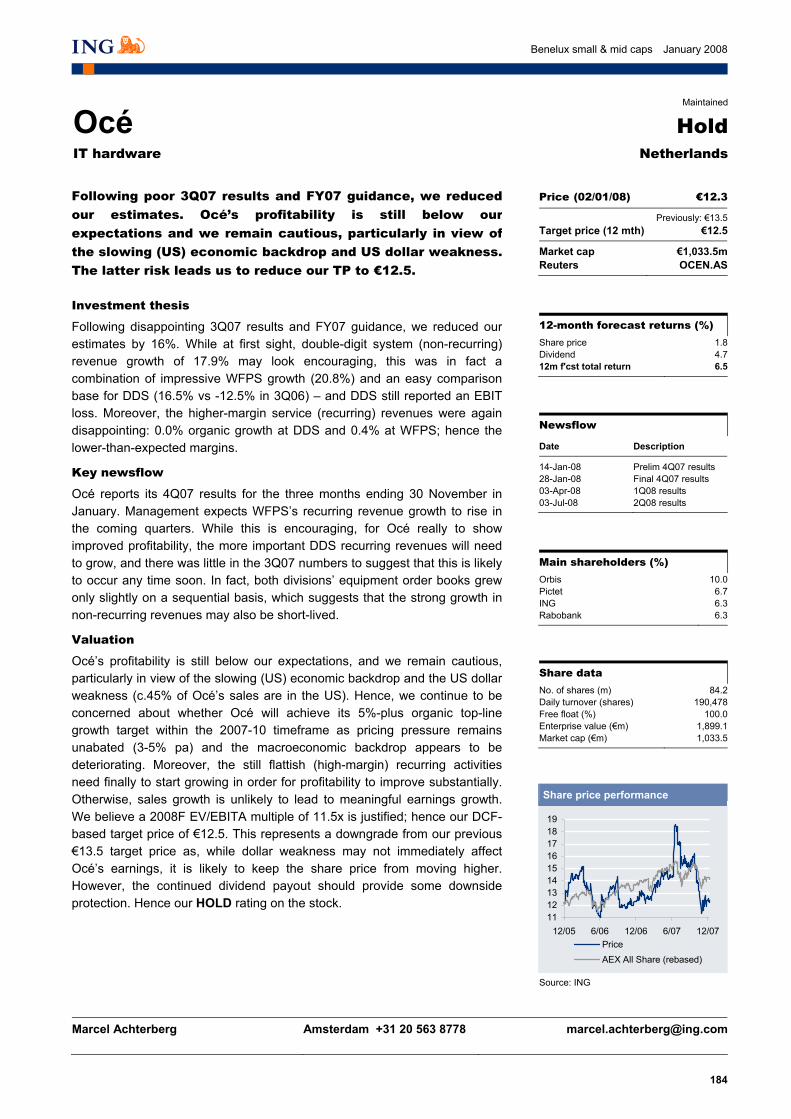

At the end of 2007, Telenet announced a promising deal with Interkabel. The firm obtained an agreement in principle to acquire Interkabel’s 0.8m TV customers (vs 1.7m existing customers at Telenet) for 8x EV/EBITDA, which appears to us a fair price. We estimate that this should add approximately €1.5 of fair value per share (coming from cost synergies and incremental customer intakes) if it proceeds in the current framework. The closing of the transaction (to be approved by inter-municipalities), expected for early 2Q08, should act as a catalyst for the stock.

Telenet, engaged in the upgrade of its network (expected to increase its access speed significantly), released a good set of results last year, seeing its EBITDA margin gradually increase to 50% in 3Q07. Broadband internet and digital TV, its two most promising and revenue-generating products, show strong growth of 16% and 86%, respectively. Furthermore, unlike traditional telecom companies, Telenet’s cable network is not subject to any regulation.

A defensive stock with little downside risk. The stock trades at 7.8x EV/EBITDA, which compares with 7.3x for US peers and M&A transaction multiples of 9-10x. In our opinion, the market has not yet factored in the completion of the refinancing plan (expected to allow the transaction with Interkabel and a potential further capital reduction of €1 per share).

Transics: BUY, TP €24 (35% upside) Transics is the number-two player in Europe in the fleet management solutions (FMS) market, with a 7% market share. FMS is a complex information system that enables companies in the transport and logistics sector to manage all aspects relating to a fleet of vehicles with real-time information in order to increase efficiency, reduce costs and improve customer services. Offering exclusively high-end FMS to customers, Transics has a strong track record of growth and profitability, with 2004-06 organic revenue and EBITDA growth of 39% and 193%, respectively.

Transics is a pure growth company that should benefit from: (1) strong expected market growth; (2) market share gains; and (3) industry consolidation. The industry growth is driven by the increasing need for transport and logistics companies to increase efficiency, reduce costs and differentiate their offer as well as a favourable regulatory environment. Transics should, in our view, gain further market share thanks to a sound development strategy: a high-end product portfolio offer, rapid international expansion into Europe where the market is still under-equipped, and a strong and stable management team.

Attractive valuation. In terms of valuation, at the current share price, Transics trades at a 2007F EV/EBIT of 14.6x and an EV/EBITDA of 11.7x and at a 2008F EV/EBIT of 10.8x and EV/EBITDA of 8.8x. The average discount to peers is c.50%. We believe the discount is unjustified given the company’s strong growth prospects and strong cash generation (FCF yield of 5%).

18

Benelux small & mid caps January 2008

Umicore: BUY, TP €211 (25% upside) Umicore is a materials technology group with leading market shares in most of its activities, which range from automobile catalytic converters (close to number-one worldwide), to cobalt and germanium processing (worldwide leader) and precious metals recycling (worldwide leader). The company has transformed itself from a metals and mining firm into a company focused on high-value-added materials, providing Umicore with a more structural growth profile (not yet reflected in its valuation).

We see significant upside in valuation terms as the expected re-rating triggered by the Nyrstar (zinc smelting) disposal has been overshadowed by market turmoil. The valuation discount highlights Umicore’s speculative appeal with its 100% free float and its rising scarcity value via its exposure to the prized auto catalyst market. (Engelhard was taken out in 2006 by BASF at 10x EV/EBITDA, leaving Johnson Matthey (JM) and Umicore as sole sector plays.) Umicore is a clear takeover target.

Umicore is also proactively rewarding shareholders with: (1) a €400m share buyback programme (financed by the €700m net proceeds from the Nyrstar disposal); (2) a 1.2m share cancellation; and (3) a five-for-one stock split expected soon. The balance sheet should remain strong from €250m pa FCF generation expected, despite our forecast of a sharp fall in Hoboken’s contribution on lower precious metal prices.

Umicore’s growth and return profile should improve radically post the Nyrstar disposal. We expect enhanced returns, lower earnings volatility and a more attractive overall profile, which should fuel a re-rating towards peer multiples, from a 30% discount to JM currently. Our SOTP-derived TP is €211, at which level the stock would trade at an 11% discount to JM. The strength of precious metal prices could lead to earnings surprises. Finally, we see strong support from Umicore’s speculative appeal.

Wessanen: BUY, TP €13.00 (19% upside) Market leader in natural and organic food. Almost half of Wessanen’s 2008F sales are generated from natural and organic brands. The other half comes from its distribution arms in Europe and the US (TOL). Wessanen seems to have resolved the problems at TOL after two years of downturns. EBIT growth is expected to follow suit. In European branded, benefits from restructuring will kick in at Favory Frozen in 2008.

EBIT margins should accelerate. TOL has passed the inflection point, with positive sales revisions likely at the 2007 results. In 2008, Wessanen might consider disposing of TOL, which would be a major trigger. Furthermore, with the restructuring of Favory Frozen paid for in 2007 and cash flow set to increase quickly in 2008F, Wessanen might opt for a gradual reduction of its 60% stake, perhaps with an opportunity to deconsolidate in 2009. Finally, the European branded portfolio should not be held back by the loss of sole agency contracts and further support from step-up in A&P spending.

Further reduction in NWC. NWC should recover (from 3Q07) towards the year-end from a good sell-through. With net debt to EBITDA of c.1.2x for 2008F, Wessanen is well positioned to engage in further share buybacks or to consolidate on its number-one position in natural and organic European branded products.

Low valuation in a food & beverage context. Wessanen is currently at a 2009F PER of 12.1x, which represents more than a 40% discount to its large-cap peers. On a 2009F EV/EBITDA of 7.8x, the discount is 43%. Wessanen’s dividend yield of 5.9% should provide further support for the shares. The two ‘call options’ on a sale of TOL and deconsolidation of Favory Frozen are the potential icing on the cake.

19

Benelux small & mid caps January 2008

September 2007 top picks’ performance Fig 8 Share price performance of ING’s September 2007 top picks

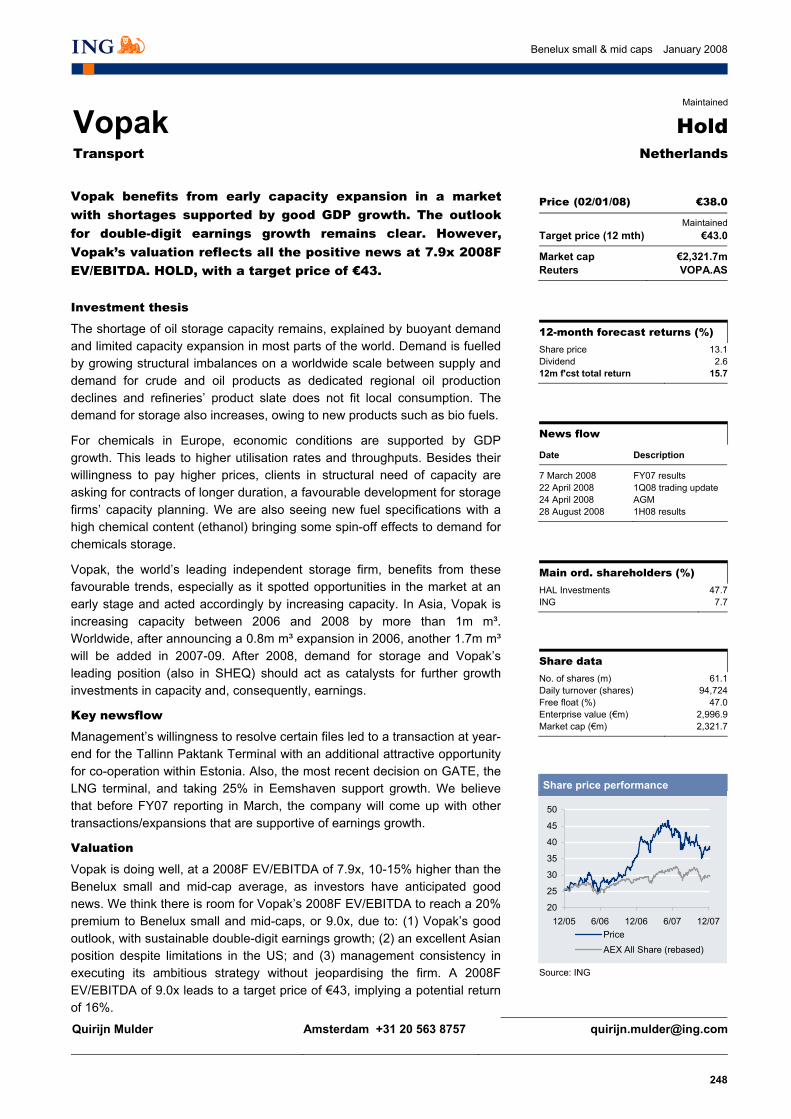

While our two previous selections of top picks performed strongly (up 13% in our September 2007 review and 37% in our May 2007 review), the performance of the selection chosen in September 2007 has suffered dearly from a small- and mid-cap sell-off, particularly among our Belgian selection. Omega Pharma issued an unfortunate profits warning in mid-October, which sent the stock down, reaching a low of €38.76 on 21 November, followed by a recovery. Barco suffered from its US$ exposure, and Kinepolis reported weaker-than-expected ticket sales in mid-November.

On the Dutch side, Wavin was hit by its profits warning and its cyclical/construction exposure, while Boskalis continued to ride the dredging wave, which remains very strong. The performance of Vedior was boosted by Randstad’s bid on the stock in early December 2007.

Sharp underperformance from

the Belgian selection

20

Benelux small & mid caps January 2008

Investment theme: Recession scenario analysis

Conclusions In general, our bottom-up share price recommendations are based on a mid-cycle dip scenario, in line with the view of ING’s economists and strategists. However, parts of the equity markets have had sharply negative reactions to the slowing trend in economic activity indicators and lowered economic growth expectations in both the US and Europe. It seems that some parts of the equity markets are pricing in a high chance of recession. We believe it is time to ask the question: “Are equity markets pricing in a recession in Benelux SMCs, and even if not, what would the downside be?” We have carried out a bottom-up recession analysis of our Benelux SMC universe in an attempt to answer this question and include an impact analysis of a recession on share prices, earnings, balance sheets and valuation as well as a risk/reward analysis between a mid-cycle dip and a recession scenario at an individual stock level.

Our main conclusions are as follows:

• The share prices of Benelux SMCs do not fully discount a recession as we see a further 39% downside on top of the recent 21% since the highs in 2007. All the stocks in our universe would see downside in a recession, ranging from 6% to 90%.

• Downward earnings revisions account for 31% of the downside, while the de-rating from the current 12.5x PER to a 10.5x PER accounts for a further 13%.

• We would expect Dutch stocks to see 40% further downside in a recession. Earnings in our Dutch universe would go down 34% relative to our 2008F EPS. We find that the trough valuation would be at 9.5x PER (vs 11x currently).

• We would expect Belgian stocks to see 30% further downside. Earnings for our Belgian stocks would go down 30% relative to our 2008F EPS. Belgian SMCs would see a trough valuation at 12.5x PER (vs 14x currently).

• The total share price correction from 2007 highs to a recession low would be 53%, lower than the 65% decline seen in the 2001-03 bear market.

Fig 9 Downside in recession scenario for Benelux small and mid caps

Median (%) Recent decline from 12m high* Expected downsideExpected decline from 12m

highDecline in previous bear

market from high**

Dutch small and mid caps -28 -40 -60 -67Belgian small and mid caps -13 -30 -45 -56

Benelux small and mid caps -21 -39 -53 -65

* Recent decline based on the current price and the highest monthly share price in 2007 ** Actual decline in previous bear market measured taking the lowest share price and the highest share price since 2000 on a monthly basis Source: ING estimates, Bloomberg

_

Our recommendations are based on a mid-

cycle dip scenario…

… but what would the downside to share prices be should a

recession materialise?

9% downside potential with 6% to 90% range

Earnings are more at risk than multiple

contraction

Dutch SMCs to bottom at c.9.5x PER and

Belgians at c.12.5x

21

Benelux small & mid caps January 2008

Fig 10 Breakdown of downside risk by PER contraction and EPS decline

Median, in % Downside share price

(%) Decline in EPS from

2008FCurrent 12m forward

PER 2008F (x)Est. recession 12m

forward PER (x) Estimated de-rating in

12m forward PER (x)

Dutch small and mid caps -40 -34 10.9 9.5 -17Belgian small and mid caps -30 -30 14.1 12.5 -8Benelux small and mid caps -39 -32 12.5 10.5 -15

Source: ING estimates

_

Please find below a selection of Dutch and Belgian stocks that we would expect to see the highest and lowest downside, respectively, in a recession.

• Stocks with high downside risk in a recession scenario are typically companies with a low level of earnings in 2007, high net debt, cyclical earnings and no significant change in their structural outlook relative to history. We would advise investors fearing a recession to avoid these stocks.

• Stocks with the lowest downside risk have a more defensive growth profile, have seen a significant change in their structural outlook relative to their history and are lowly valued relative to their history.

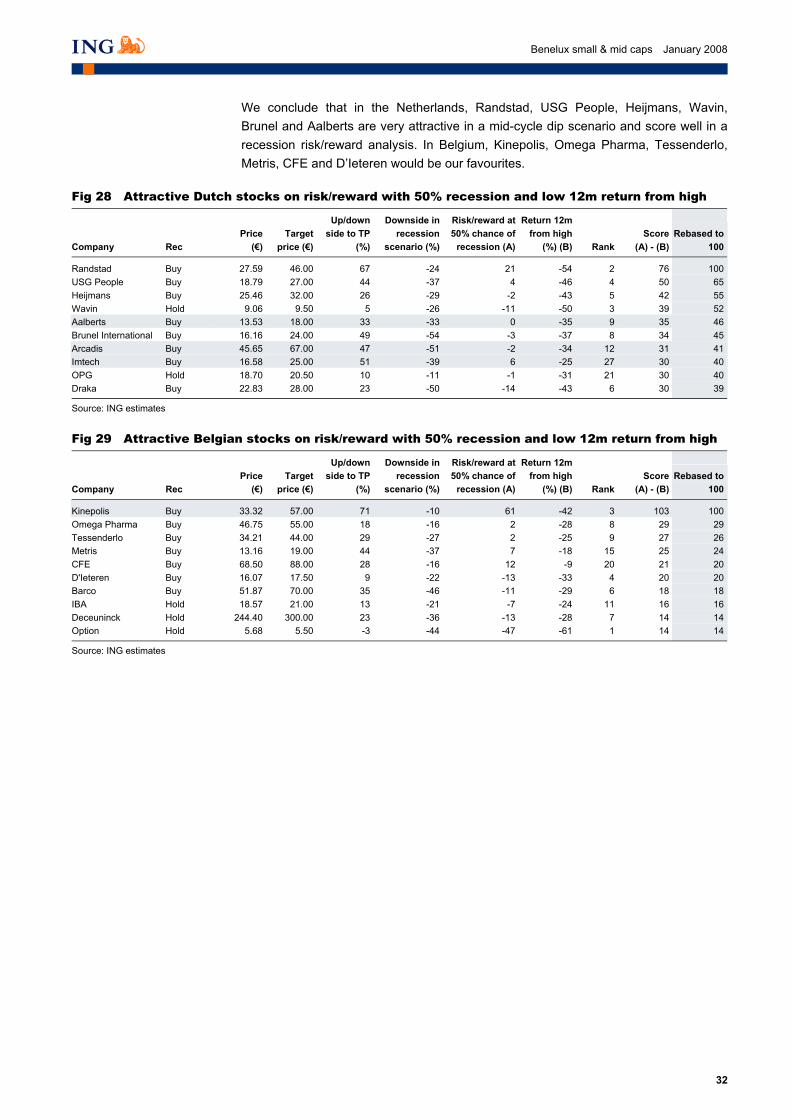

• We have run a risk/reward analysis with a 50% probability of a recession and the stock performance since the high in 2007 and find that, among Dutch stocks, Randstad (Buy), USG People (Buy), Heijmans (Buy), Wavin (Hold) and Brunel (Buy) are most attractive if investors purely want to play a mid-cycle dip scenario, Omega Pharma (Buy), Tessenderlo (Buy), Metris (Buy), CFE (Buy) and D’Ieteren (Buy) are the most attractive Belgian stocks.

Fig 11 Benelux SMC stocks with high downside in a recession scenario

Netherlands Rec Downside

(%)Current

price (€)Recession

price (€) Belgium Rec Downside

(%)Current

price (€)Recession

price (€)

Samas Hold -90 5.0 0.5 Emakina Hold -68 10.8 3.5Van Der Moolen Hold -79 3.0 0.6 CMB Buy -56 58.5 26.0BESI Hold -73 3.7 1.0 Pinguin Buy -55 16.2 7.2Ballast Nedam Hold -69 27.9 8.6 Agfa Sell -53 10.7 5.0Vopak Hold -66 38.0 13.1 Euronav Hold -51 24.3 12.0Unit 4 Agresso Buy -63 19.3 7.2 ICOS Vision Systems Buy -48 31.0 16.1Smit International Hold -62 69.0 26.1 Barco Buy -46 51.9 28.0Beter Bed Buy -59 18.2 7.4 Exmar Hold -45 19.9 11.0Ordina Hold -59 12.2 5.0 Option Hold -44 5.7 3.2Corporate Express Hold -58 5.2 2.2 Sioen Industries Buy -41 9.8 5.8

Source: ING estimates _

Fig 12 Benelux SMC stocks with low downside in a recession scenario

Netherlands Rec Downside

(%)Current

price (€)Recession

price (€) Belgium Rec Downside

(%)Current

price (€)Recession

price (€)

OPG Hold -11 18.7 16.7 Mobistar Hold -6 61.5 57.8Wolters Kluwer Hold -13 22.1 19.2 Kinepolis Buy -10 33.3 30.0Kendrion Hold -13 17.3 15.0 Omega Pharma Buy -16 46.8 39.3Randstad Buy -24 27.6 21.0 CFE Buy -16 68.5 57.3SBM Offshore Hold -25 21.2 16.0 Telenet Group Buy -17 19.8 16.4Hunter Douglas Buy -25 49.8 37.2 Atenor Buy -19 41.3 33.5Wavin Hold -26 9.1 6.7 Alfacam Hold -20 16.0 12.7Sligro Hold -27 27.4 20.0 IBA Hold -21 18.6 14.8CSM Buy -29 23.7 16.9 Van de Velde Buy -21 37.5 29.4Heijmans Buy -29 25.5 18.0 Colruyt Buy -22 163.8 128.5

Source: ING estimates

_

Avoid high net debt, low level earnings, cyclical

earnings and lack of structural changes

Look for more defensive growth profile, low

valuation relative and structural change

Some cyclical stocks seen to discount a lot of

bad news

22

Benelux small & mid caps January 2008

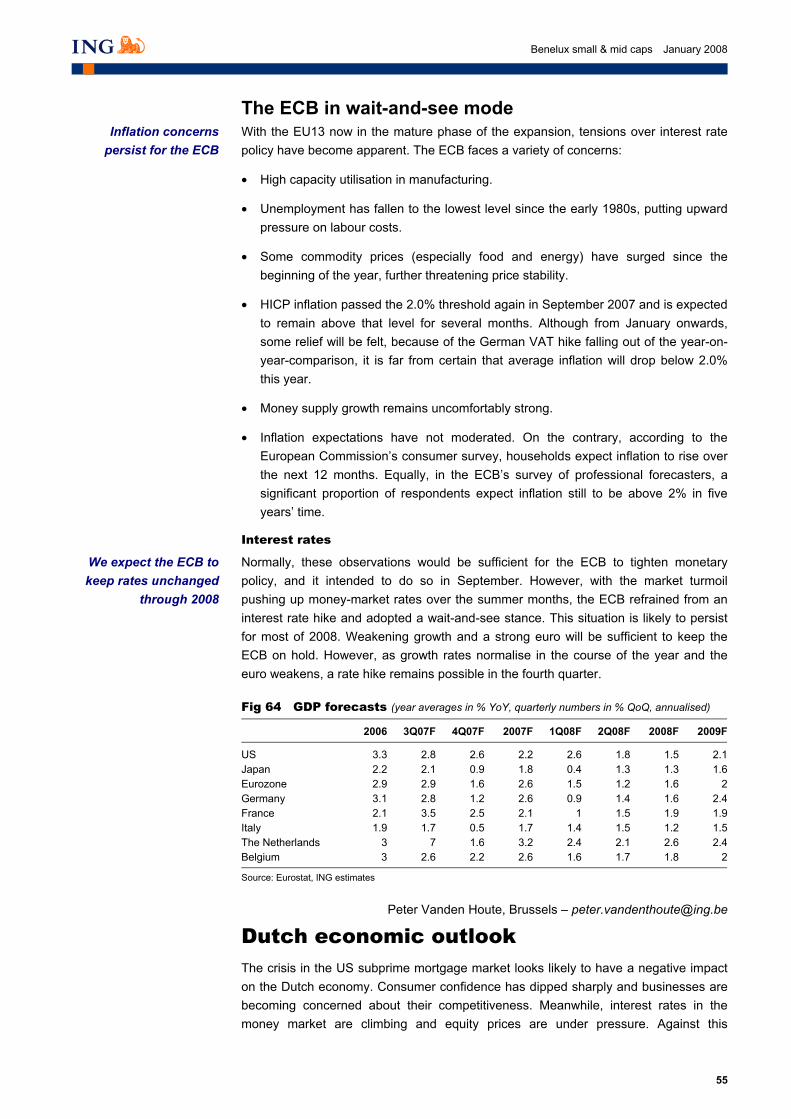

Introduction Our current earnings forecasts, recommendations and target prices for Benelux small- and mid-cap companies are in general based on still benign economic growth in Europe and Asia and a slowdown in the US economy (but not a recession). This is in line with the view of ING’s economists and strategists. They have adjusted their forecasts for economic growth for Europe downward and are of the opinion that the slowdown in the US might actually feel like a recession. We think the market consensus is more positive on economic growth in Europe and the US.

The current forecast weakness (or slowdown) in economic growth in the US and Europe in 2008F should still be seen within the context of a mid-cycle dip scenario, and growth is expected to pick up in 2009F. Our view of a broad-based turning of the cycle and recession is still a couple years out.

However, we cannot ignore recent declines in some important economic indicators (such as the US ISM Manufacturing Index), continued weakness in the US housing market, a standstill in the financial sector and record oil prices, which might lead to a recession in the US and the chance that a US recession will spill over into Europe as happened with the recessions in the early 1980s, 1990s and 2000s.

Moreover, the recent heavy fall in (certain segments of) the equity markets might be taken as an indicator of lower future economic growth. The least we can say is that equity markets seem to be pricing in a higher chance of a broader-based economic slowdown. And while we are of the opinion that valuations among Benelux SMCs are attractive in light of recent historical levels and forecast earnings growth, we feel the uncertainty in the market with regards to the direction of the economy justifies an analysis of what could happen to the earnings, valuations, balance sheets and share prices of Benelux SMCs in case of a broad-based recession and an accompanying bear market in equities. This ultimately demands an assessment of the downside risk to current share prices should a recession materialise. We have carried out a bottom-up stock analysis to do so. A detailed discussion of the methodology used can be found later in this section.

Basic recession scenario assumptions Assessing the earnings potential of individual SMC stocks during a recession is a difficult exercise and we would not advise investors to see the outcome of our analysis as an absolute projection of where earnings will end up, as many factors play a role in the determination of such a forecast.

We have taken the following basic assumptions regarding a recession scenario:

• Economic growth to slow down severely in 2008-10, with the market realising peak earnings in 2007-08. This implies a recession environment in 2009-10 and earnings to reach a trough at the end of 2009 and early 2010. This scenario is similar to the last recession that hit Benelux SMCs in 2002-03, when earnings peaked in 2000/01 and economic growth slowed severely in 2001-03. Earnings forecasts troughed at the end of 2002 and the beginning of 2003.

• An assessment of the performance of companies and stocks in the previous recession period (2000-03) has been made based on organic sales growth, EBITA margin development and share prices.

Our forecasts are based on a mid-cycle dip

scenario, in line with ING economists’ view

2008F GDP for the US is weak; Europe and Asia

should be good…

… but markets seem to have priced in a higher

chance of a broader based slowdown...

… which justifies a recession impact

analysis for Benelux stocks

A bottom-up analysis of earnings, financial

positions, valuations and share prices

23

Benelux small & mid caps January 2008

• We have taken into account: changes in activities, segmental exposure and competitive positions; the outlook for the sector; geographical exposure; currency exposure; management; cost structure; debt positions; and other factors that could result in a deviation from the historical performance.

• Not taken into account are possible future events such as M&A, increased capital returns, restructurings in the broadest sense and management changes.

• Today’s currency spot rates have been taken as a proxy for future spot rates.

• We have used the Benelux SMCs currently under ING coverage, excluding stocks that are currently bid for, real estate, holdings and biotech stocks.

Earnings in a recession scenario Performance in the 2000-03 recession: strong decline in EBITA

We find that, in the previous recession period of 2001-03, Dutch companies experienced a 5% organic decline in sales and a 470bp decline in EBITA margin, from 8.7% (in peak year 2000) to 4.0% (through year 2003).

Belgian companies saw a less pronounced decline in organic sales of 2%, but a slightly higher decline in the EBITA margin of 510bp, from 10.3% (in peak year 2000) to 5.2% (through year 2002).

Fig 13 Operating performance of Benelux SMCs in previous recession, 2000-03

Median (%) Organic sales

change Peak EBITA

margin YearThrough EBITA

margin Year Change

(bp)

Dutch small and mid caps -5 8.7 2000 4.0 2003 -470Belgian small and mid caps -2 10.3 2000 5.2 2002 -510

Benelux small and mid caps -4 9.2 2000 4.1 2003 -512

Source: ING estimates

_

We have not calculated the net earnings and EPS declines in this period as such an analysis would be too distorted by changes in tax rates, minorities, associates, debt positions, interest rates and shares outstanding due to restructurings, profit-to-loss swings, acquisitions and divestitures, and return of capitals, among other things.

Expected performance in recession scenario: still severe impact on EPS

Fig 14 Operating performance of Benelux SMCs in our recession scenario

Median (%) Organic sales

change Peak EBITA

margin 2008F

Trough or recession low EBITA margin

Change 2008F - Trough (bps)

EPS change 2007F - recession

low

EPS change 2008F - recession

low

Dutch small and mid caps -4 8.0 6.0 -197 -25 -34Belgian small and mid caps -1 13.1 8.0 -507 -22 -30

Benelux small and mid caps -2 9.0 7.0 -198 -23 -32

Source: ING estimates

_

Our analysis of the operating performance of Benelux SMCs shows that the sales and margin declines in our recession scenario are estimated to be less severe than in the previous recession. However, the impact on earnings can still be called severe, with earnings down 32% from our current 2008F EPS.

24

Benelux small & mid caps January 2008

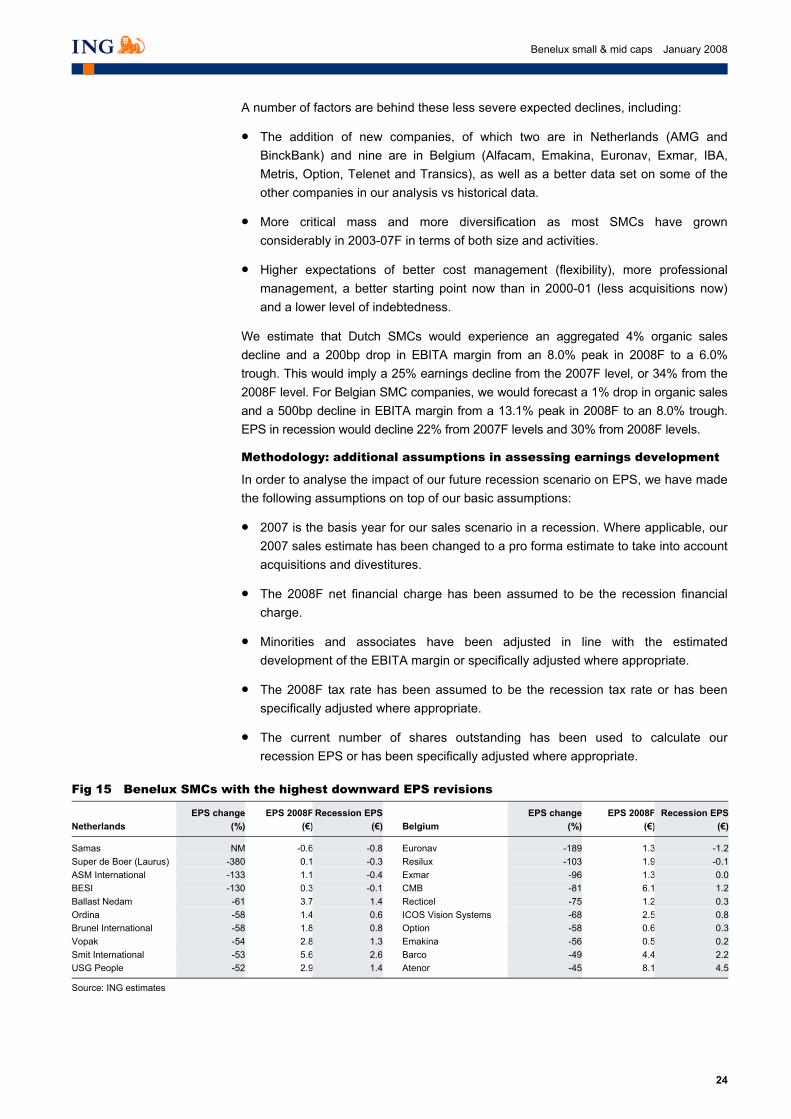

A number of factors are behind these less severe expected declines, including:

• The addition of new companies, of which two are in Netherlands (AMG and BinckBank) and nine are in Belgium (Alfacam, Emakina, Euronav, Exmar, IBA, Metris, Option, Telenet and Transics), as well as a better data set on some of the other companies in our analysis vs historical data.

• More critical mass and more diversification as most SMCs have grown considerably in 2003-07F in terms of both size and activities.

• Higher expectations of better cost management (flexibility), more professional management, a better starting point now than in 2000-01 (less acquisitions now) and a lower level of indebtedness.

We estimate that Dutch SMCs would experience an aggregated 4% organic sales decline and a 200bp drop in EBITA margin from an 8.0% peak in 2008F to a 6.0% trough. This would imply a 25% earnings decline from the 2007F level, or 34% from the 2008F level. For Belgian SMC companies, we would forecast a 1% drop in organic sales and a 500bp decline in EBITA margin from a 13.1% peak in 2008F to an 8.0% trough. EPS in recession would decline 22% from 2007F levels and 30% from 2008F levels.

Methodology: additional assumptions in assessing earnings development

In order to analyse the impact of our future recession scenario on EPS, we have made the following assumptions on top of our basic assumptions:

• 2007 is the basis year for our sales scenario in a recession. Where applicable, our 2007 sales estimate has been changed to a pro forma estimate to take into account acquisitions and divestitures.

• The 2008F net financial charge has been assumed to be the recession financial charge.

• Minorities and associates have been adjusted in line with the estimated development of the EBITA margin or specifically adjusted where appropriate.

• The 2008F tax rate has been assumed to be the recession tax rate or has been specifically adjusted where appropriate.

• The current number of shares outstanding has been used to calculate our recession EPS or has been specifically adjusted where appropriate.

Fig 15 Benelux SMCs with the highest downward EPS revisions

Companies with the highest downward earnings revisions in a recession scenario are:

• Companies with a low earnings base turning into losses, such as Samas, Super de Boer, BESI in the Netherlands. ASM International, Euronav and Resilux are also expected to generate losses in a recession scenario.

• Cyclical companies in general, such as ASM International, Ballast Nedam, Ordina, Brunel, Vopak, Smit International, USG People in the Netherlands, and Euronav, Resilux, Exmar, CMB, Recticel, ICOS, Option, Emakina, Barco and Atenor in Belgium.

The latter category also includes companies that have seen exceptionally high earnings because of very favourable sector circumstances, which we do not expect to be sustainable in a two- to three-year recession period, including Vopak and Smit International in the Netherlands and Euronav, Exmar, CMB and Atenor in Belgium.

Fig 16 Benelux SMCs with the lowest downward EPS revisions

* Kendrion benefits from recent changes in its activity portfolio, lifting its margin profile ** TomTom based on a stand alone scenario, excluding the proposed takeover of Tele Atlas Source: ING estimates

_

We find that Benelux companies with expected low earnings revisions (some even managing to grow) are:

• Defensive (OPG, SBM Offshore, Wolters Kluwer, Sligro, CSM in the Netherlands; and Mobistar, Telenet, Duvel and Colruyt in Belgium).

• Experiencing a significant change in their activity portfolio due to a changed profile or sector outlook (Kendrion and Royal TenCate in the Netherlands; and Pinguin, CFE and Umicore in Belgium).

• Growth companies (TomTom in Netherlands; IBA, EVS in Belgium).

• Contrary to intuition, cyclical companies such as Aalberts, Océ, Melexis and Umicore.

Financial position in a recession scenario To assess the financial position of Benelux SMCs, we have used net debt to 2008F EBITDA as a proxy. We find that the overall financial position of both Dutch and Belgian SMCs is currently healthy (at 0.9x for 2008F), with a slightly higher ratio in the Netherlands (at 0.9x) than Belgium (at 0.7x). In a recession scenario, the ratio would be slightly higher, as shown in Figure 17.

26

Benelux small & mid caps January 2008

Fig 17 Current (2008F) and recession financial position of Benelux small and mid caps

Median (x) Net debt/EBITDA 2008FRecession net

debt/EBITDA Change

Dutch small and mid caps 0.9 1.0 0.1Belgian small and mid caps 0.7 0.9 0.2

Benelux small and mid caps 0.9 0.9 0.1

Source: ING estimates

_

Methodology: assumptions behind recession net debt/EBITDA

We have used the following additional assumptions behind our forecast net debt and EBITDA in a recession scenario:

• Recession EBITDA is analysed by taking the recession EBITA as forecast under the assumptions set in the earnings section above and adding our current 2008 estimate for depreciation.

• Recession net debt is forecast by taking our current 2008 net debt estimate as a proxy for net debt at the end of the recession. While this method has its limitations (as it might under- or overestimate actual net debt in a recession), it keeps the analysis simple.

Financial position: divergence in balance sheet strength

Fig 18 Benelux small and mid caps with high net debt to EBITDA in a recession scenario (x)

We would expect the market to dislike leveraged balance sheets in times of recession. While we consider a 3.0x net debt/EBITDA ratio to be safe for cyclical companies, we expect ratios over 2.0x to weigh on the equity value of leveraged companies.

The companies that score badly in the Netherlands on financial leverage are Samas and Super de Boer (Laurus), and we would expect financiers to aggressively push these companies to reduce debt and find additional cash (through disposals) and/or equity financing (debt for equity swap).

Our assessment of Heijmans and Corporate Express, which would have net debt/EBITDA ratios over 3.0x, is that their financial position would not become critical but that they could come under close monitoring by their financiers.

In Belgium, we find shipping companies Exmar, Euronav and CMB to have the highest net debt positions in a recession scenario. While their ratios are high, this should be seen within the context of how these companies operate and finance their fleets. With this in mind, we do not foresee many problems with financing, not least because these

27

Benelux small & mid caps January 2008

companies’ assets are liquid enough to be sold and could be used to generate cash to pay down debt.

Exmar’s current and recession net debt positions are inflated by the heavy external financing of LNG ships, which are backed by long-term (up to 20-year) non-recourse contracts. Taking LNG out of Exmar’s balance sheet would see ratios for the remainder of the company decline considerably to less than 2x for 2008F and to 4.7x in a recession, which would not be a problem as the LPG business has contracts for the mid segment of one to five years.

Euronav’s spot-driven business could lead to EBITDA pressure in a recession. However, on entering a recession, Euronav would be able to sell assets at market prices in order to generate cash. Although revenues from asset sales could disappoint in weak markets, we would expect banks to look beyond a downturn as Euronav has a relatively good balance sheet within the sector (and a young double-hull fleet).

CMB’s net debt to EBITDA could increase sharply in a recession, but fleet coverage of 100% for 2008 and 70% for 2009 implies limited risk of a downturn. For 2010, CMB indicates that it has covered 40% of its Capesizes; this means that only if bulk prices sink below US$17,000 per day (from US$160,000 now) would net debt to EBITDA reach 3.4x.

Recticel and Sioen could find themselves under close monitoring from their financiers, but their financial position would not come into critical territory.

Fig 19 Benelux small and mid caps with low net debt to EBITDA in a recession scenario

In Figure 19, we show the companies that would have the strongest financial positions in a recession scenario. Most companies are currently estimated to have net cash positions in 2008F, and most companies (with the exception of IBA) should see their net cash position improve due to continued cash flow generation. These companies should have the balance sheet strength to potentially return excess capital to shareholders to support the share price.

We have excluded TomTom and Randstad from the analysis above as their estimated net cash positions are likely to be converted to net debt positions if and when they finalise the acquisitions of Tele Atlas and Vedior, respectively. We have excluded BAM (3.3x) and SBMO (2.8x), where the net debt position reflects specific project financing and non-recourse debt, and Wolters Kluwer (2.7x), where earnings are defensive. We also excluded ASMI and BESI because of their expected generation of losses in a recession scenario, even though they would maintain their net cash position.

28

Benelux small & mid caps January 2008

We would expect Van der Moolen, Emakina and ICOS Vision Systems to maintain their net cash position and a rise in the net debt to EBITDA ratio, but the latter is solely due to a sharply lower EBITDA; as such, we have excluded them.

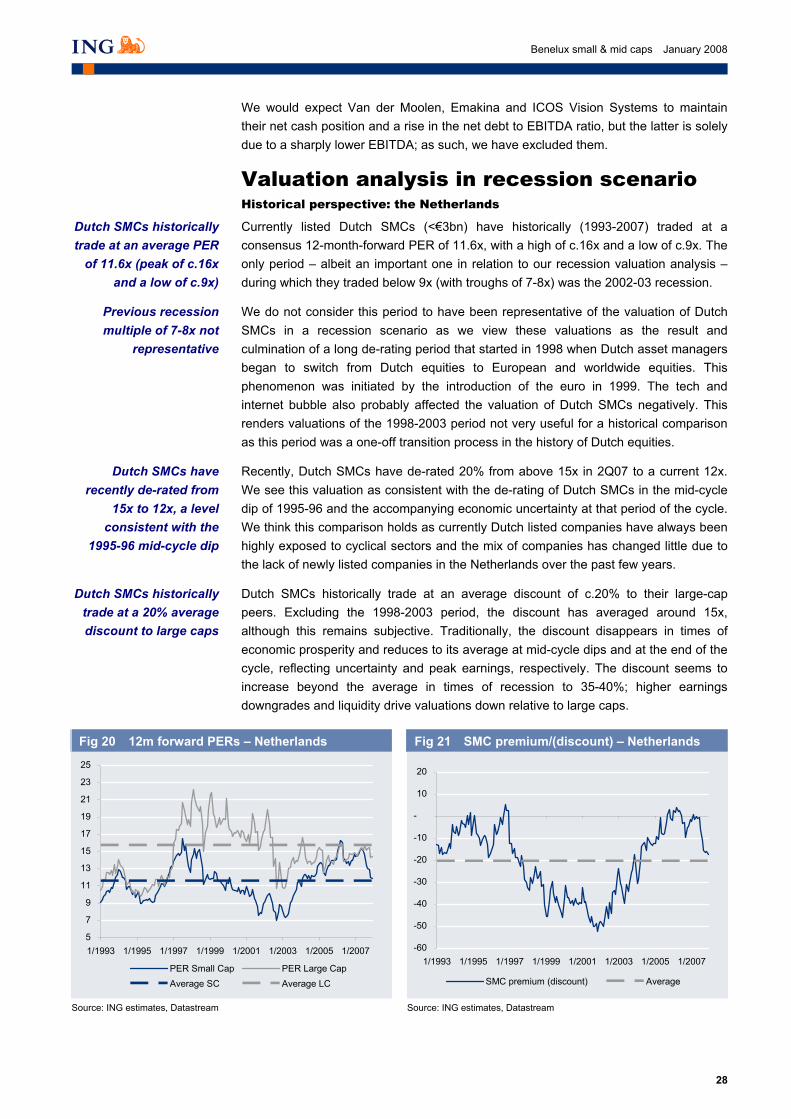

Valuation analysis in recession scenario Historical perspective: the Netherlands

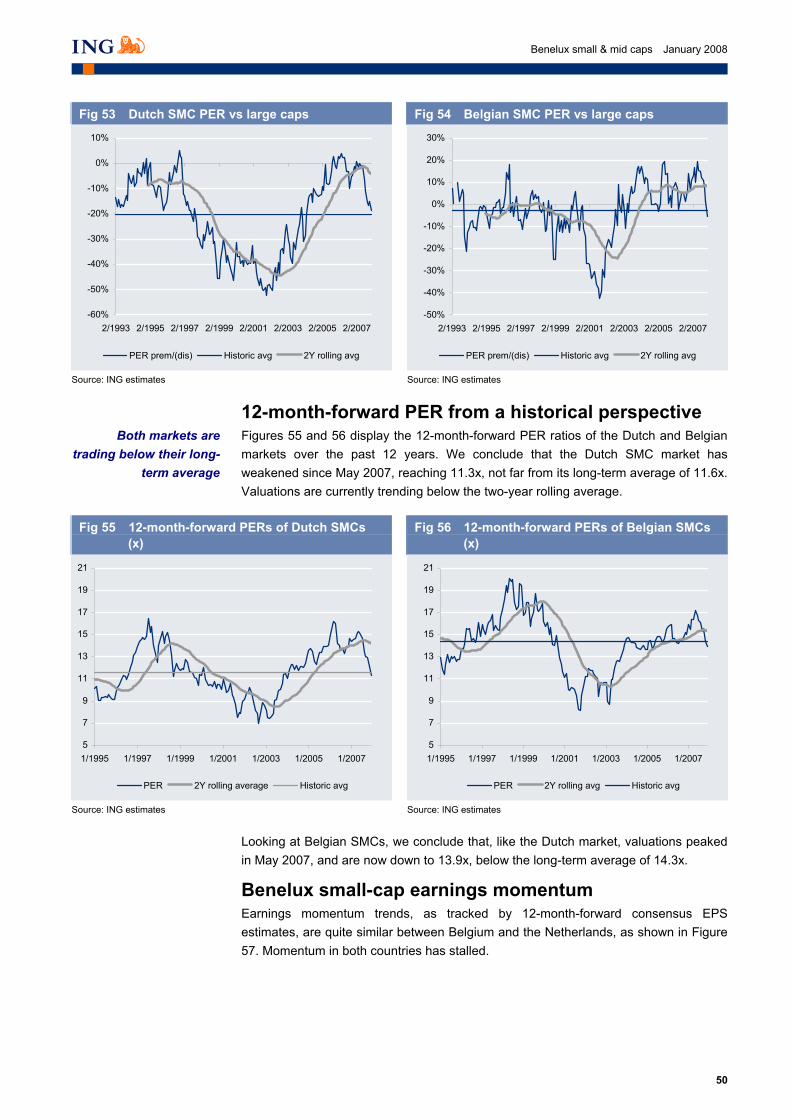

Currently listed Dutch SMCs (<€3bn) have historically (1993-2007) traded at a consensus 12-month-forward PER of 11.6x, with a high of c.16x and a low of c.9x. The only period – albeit an important one in relation to our recession valuation analysis – during which they traded below 9x (with troughs of 7-8x) was the 2002-03 recession.

We do not consider this period to have been representative of the valuation of Dutch SMCs in a recession scenario as we view these valuations as the result and culmination of a long de-rating period that started in 1998 when Dutch asset managers began to switch from Dutch equities to European and worldwide equities. This phenomenon was initiated by the introduction of the euro in 1999. The tech and internet bubble also probably affected the valuation of Dutch SMCs negatively. This renders valuations of the 1998-2003 period not very useful for a historical comparison as this period was a one-off transition process in the history of Dutch equities.

Recently, Dutch SMCs have de-rated 20% from above 15x in 2Q07 to a current 12x. We see this valuation as consistent with the de-rating of Dutch SMCs in the mid-cycle dip of 1995-96 and the accompanying economic uncertainty at that period of the cycle. We think this comparison holds as currently Dutch listed companies have always been highly exposed to cyclical sectors and the mix of companies has changed little due to the lack of newly listed companies in the Netherlands over the past few years.

Dutch SMCs historically trade at an average discount of c.20% to their large-cap peers. Excluding the 1998-2003 period, the discount has averaged around 15x, although this remains subjective. Traditionally, the discount disappears in times of economic prosperity and reduces to its average at mid-cycle dips and at the end of the cycle, reflecting uncertainty and peak earnings, respectively. The discount seems to increase beyond the average in times of recession to 35-40%; higher earnings downgrades and liquidity drive valuations down relative to large caps.

Source: ING estimates, Datastream Source: ING estimates, Datastream

Previous recession multiple of 7-8x not

representative

Dutch SMCs have recently de-rated from

15x to 12x, a level consistent with the

1995-96 mid-cycle dip

Dutch SMCs historically trade at a 20% average discount to large caps

Dutch SMCs historically trade at an average PER

of 11.6x (peak of c.16x and a low of c.9x)

29

Benelux small & mid caps January 2008

Historical perspective: Belgium

Currently listed Belgian small and mid caps (<€3bn) have historically (1993-2007) traded at a consensus 12-month-forward PER of 14.3x, with highs of 17-20x and lows of 11-12x.The only period – much like in The Netherlands – during which they traded below 11-12x (with troughs of 8-9x) was the 2001-03 recession.

Much like the valuation of Dutch SMCs, we do not view this period as representative of the valuation of Belgian SMCs in a recession scenario. Belgian equities have also been subject to domestic asset managers switching out of Belgian equities into European and worldwide equities. Although this process started earlier in the Netherlands, it seems to have had an equally negative effect in Belgium, topped off by the 2001-03 recession period. This renders valuations of the 1998-2003 period not very useful for a historical comparison.

Belgian SMCs have recently de-rated 17.5% from c.17x in 2Q07 to 14x. Although we view this de-rating as consistent with their Dutch SMC peers, an absolute valuation comparison with the previous mid-cycle dip of 1995-96 is more difficult due to the fact that many companies have seen a strong transformation and many new companies have entered the market since then, particularly in biotechnology and other growth-oriented sectors.

Belgian SMCs have historically traded at a very small average discount of 2-3% to their large-cap peers. Excluding the 2001-03 period, SMCs have probably traded at a small premium, although this correction remains subjective.

Like Dutch SMCs, the discount usually disappears and even shifts into a significant 20% premium in times of economic strength. It falls back to its average at mid-cycle dips and at the end of the cycle, reflecting uncertainty and peak earnings, respectively. The discount seems to increase above the average in times of recession to c.20%. Higher earnings downgrades and liquidity drive valuations down relative to large caps.

Fig 22 12m forward PERs – Belgium

Fig 23 SMC premium/(discount) – Belgium

5

7

9

11

13

15

17

19

21

23

25

1/1993 1/1995 1/1997 1/1999 1/2001 1/2003 1/2005 1/2007PER small cap PER large capAverage SC Average LC

Source: ING estimates, Datastream Source: ING estimates, Datastream

_

Benelux SMC valuations in a recession scenario Our bottom-up valuation analysis for Benelux SMCs finds an applicable PER of 10.5x, which implies a 16% de-rating from the current 12-month-forward PER (2008F). In the 2001-03 recession, we found that Benelux SMC stocks traded as low as 7.5x, meaning that on aggregate we have applied a 41% premium over the previous recession valuation. However, if we compare our bottom-up applicable PER of 10.5x with an

Belgian SMCs historically trade at

14.3x PER (peak of 17-20x and low 11-12x

Like in NL, previous recession valuations

not very useful

Belgian SMCs have recently de-rated from

17x to 14x

Belgian SMCs historically trade at a

small average discount to large caps

30

Benelux small & mid caps January 2008

(albeit arbitrary) adjusted PER of 9.5x, the implied premium to the previous recession scenario is only 10.5%. We think this is justified for reasons explained below.

Fig 24 Benelux valuations applicable in a recession scenario

Median (x)

Applied recession 12m

forward PER

Current 12m forward PER

(2008F)Change

(%)PER previous

recessionChange

(%)

Adjusted PER previous

recession Change

(%)

Dutch small and mid caps 9.5 10.9 -12 6.3 51 8.5 12Belgian small and mid caps 12.5 14.1 -12 9.1 37 11.5 9

Benelux small and mid caps 10.5 12.5 -16 7.5 41 9.5 11

Source: ING estimates

_

Methodology: additional assumptions to reach appropriate PER

To assess the valuation of Benelux small and mid caps in times of recession, we use historical 12-month-forward PERs when the share prices of individual companies were at their cycle lows in the 2000-04 period. We make adjustments for:

• The extremely low valuations seen in the 2001-03 previous recession period as we view these as an overreaction to a long de-rating process (see previous paragraphs) in combination with the recession itself.

• The current improved financial positions of many Benelux companies, which should lead to a higher valuation than previously.

• Changes in the structural position of the relevant company, or the sector in which it is active, particularly if these changes are seen as sustainable over a two- to three-year recession period.

• When PER-based valuations do not apply, we use appropriate other valuation methods, such as price to book, asset-based valuations, EV/sales and EV/EBIT.

Fig 25 Benelux high PER applied in recession scenario vs current PER

We have re-rated staffing companies to a significantly higher PER level than they currently trade at (which suggests that the market expects severe downgrades). We have also applied a relatively high recession multiple to other cyclical companies. This is also true for most Belgian cyclical companies as well as for some defensive stocks, such as Wolters Kluwer, OPG, Kinepolis and Omega Pharma.

For companies where we have applied a relatively low PER, this is due to low current earnings, a high current PER relative to history that we do not find to be structurally justified, and the lack of a market-based valuation history.

31

Benelux small & mid caps January 2008

Fig 26 Benelux low PER applied in recession scenario vs current PER

Risk/reward analysis We have carried out two risk/reward analyses on the basis of the outcome of our recession scenario downside to individual share prices.

A. Risk/reward analysis in the basis of a 50% chance of recession

We have run a risk/reward analysis on the basis of a 50% chance of a recession and a 50% chance of our mid-cycle dip scenario. We multiply these probabilities by the downside risk reached in a recession scenario and the current upside to our target price as a proxy for the upside in a mid-cycle dip scenario. Ranking the results shows the stocks with the highest return in this scenario.

Fig 27 Stocks with highest risk/reward at 50% chance of recession and 50% of mid-cycle dip

B. Risk/reward on the basis of a 50% chance of recession, coupled with the recent share price decline

We have also run a risk/reward analysis on the basis of a 50% chance of a recession and a 50% chance of a mid-cycle dip scenario. We multiply these probabilities by the downside risk that we find in a recession scenario and the current upside to our target price as a proxy of the upside in a mid-cycle dip scenario. We then subtract from the result the recent fall in the share price of the stock.

Ranking the result shows the stocks that show the highest potential upside in case of a mid-cycle dip scenario and an accompanying rally in the market, coupled with the best risk/rewards. In other words, a stock with a high risk/reward score and a high recent decline in share price should have a high ranking.

32

Benelux small & mid caps January 2008

We conclude that in the Netherlands, Randstad, USG People, Heijmans, Wavin, Brunel and Aalberts are very attractive in a mid-cycle dip scenario and score well in a recession risk/reward analysis. In Belgium, Kinepolis, Omega Pharma, Tessenderlo, Metris, CFE and D’Ieteren would be our favourites.

Fig 28 Attractive Dutch stocks on risk/reward with 50% recession and low 12m return from high

At the end of December, the Dutch Senate approved a proposal to allow for more dividend-tax-exempt share buybacks, effective as of 2008. The changes made to the Dividend Tax Act 1965 imply a more than doubling in the potential value of tax-free share buybacks. This is important for shareholders in Dutch listed companies as they could potentially receive a higher tax-free capital return through share buybacks. This could create a positive reaction, particularly in the stocks of Dutch companies that were previously limited in their amount of tax-exempt share buybacks. Furthermore, companies considering share buybacks in the future now have more room to undertake them. An overview by company is included at the end of this section.

Limited impact on small and mid caps: CSM and Wolters Kluwer benefit most. We find that among the small and mid caps, the tax-exempt share buyback allowance doubles, but that the impact is only limited as most of the companies in our universe are currently not engaged in or planning on returning capital through share buybacks. Only seven of the 45 companies (16%) have made buybacks in the last four years, and these companies are the ones that see their allowances for tax-exempt share buybacks increase the most. The new regime is particularly favourable for CSM and Wolters Kluwer.

Significant impact on Dutch large caps, particularly Philips, KPN, DSM and TNT. Dutch large caps benefit much more significantly from the change in regulation as 75% of the (16) large-cap companies have been engaged in share buybacks over the last four years. We find that the change in regulation is highly favourable for Philips and KPN as they were very limited in their tax-exempt allowance under the previous regulation. DSM and TNT also benefit more than most.

Background to the Law: Article 4c (*1) of the Dividend Tax Act 1965 discusses tax-free share buybacks within the limits of the Dividend Tax Act. This article was set up to protect the income that the Dutch government receives in taxes on cash dividends as Dutch companies could potentially avoid paying dividend taxes by buying back shares. However, the law makes a specific exemption to allow for tax-exempt share buybacks and gives Dutch listed companies the opportunity to return capital to shareholders in a tax-efficient way. The law determines the maximum share buyback allowance based on a number of specifications.

Calculation of the allowance for tax-exempt share buybacks

The allowance for tax-exempt share buybacks is based on the average of cash dividends paid to ordinary shareholders (inflation-adjusted) over the last seven years, excluding the highest and lowest payments. Previously, the historical average dividend had to be multiplied by 10 to calculate the value of the allowance for tax-exempt share buybacks. The allowance is lowered by the amount of share buybacks over the past four years. However, the multiplier has been changed to 20 in the new regulation valid from 1 January 2008, meaning that a significantly higher amount can be returned to shareholders tax-free annually.

Changes in Dutch dividend tax allow for an

increase in share buybacks from 2008 for Dutch listed companies