Da

ibo

ch

i Pla

stic &

P

ac

ka

gin

g In

du

stry

Be

rha

d

Inv

esto

rs’ Brie

fing

FY2

01

1 Fin

an

cia

l Re

sults &

Co

rpo

rate

Up

da

te

20

Feb

rua

ry 2

01

2

IR A

dv

ise

r

AQ

UIL

AS

•Operatio

nal H

ighlights

•Financial Review

•FY2012 Growth Stra

tegies

2

•FY2012 Growth Stra

tegies

•Appendix:

»Corporate Profile

»Industry

Insight

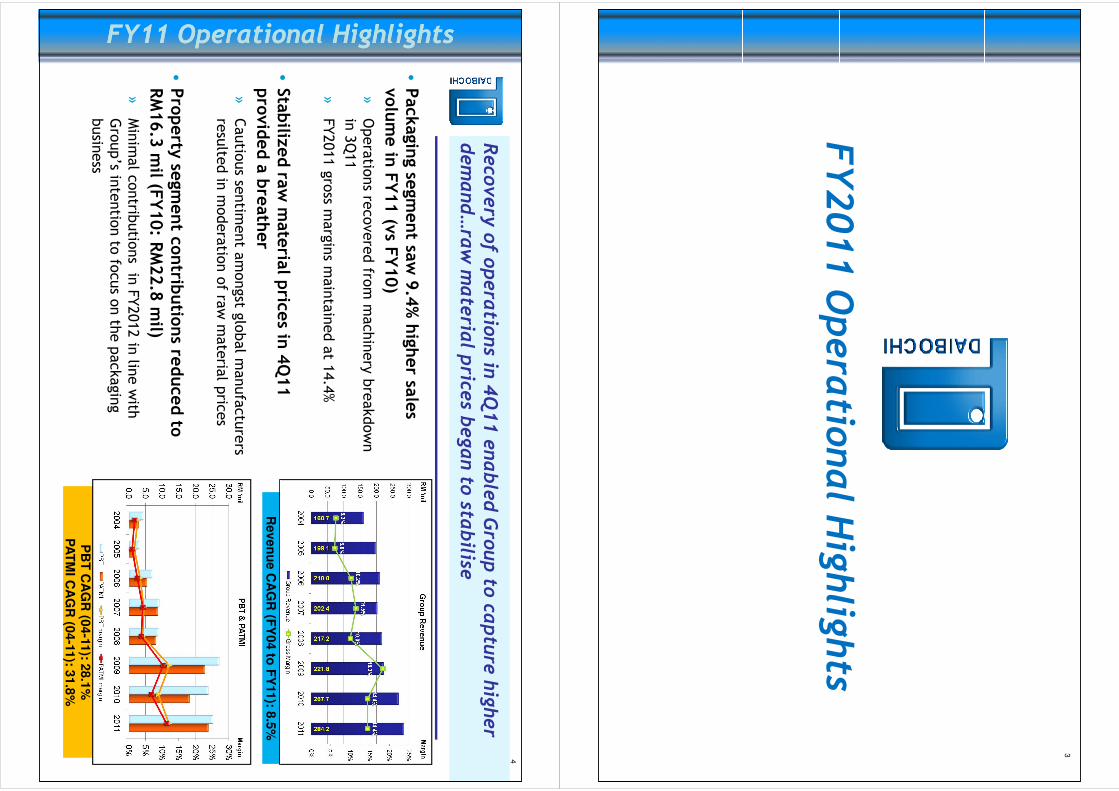

FY2011 Operational Highlights

3

FY2011 Operational Highlights

•Pack

agin

g segm

ent sa

w 9.4%high

er sa

les

volume in

FY11 (v

sFY10)

»Operatio

ns re

covered fro

m machinery breakdown

in 3Q11

»FY2011 gross m

argins m

aintained at 1

4.4%

•Sta

biliz

ed ra

w m

ateria

l price

s in 4Q11

4

FY11 Operational HighlightsFY11 Operational Highlights

Recovery of operations in 4Q11 enabled Group to capture higher

demand…raw material price

s began to sta

bilise

•Sta

biliz

ed ra

w m

ateria

l price

s in 4Q11

provided a breather

»Cautio

us se

ntim

ent a

mongst g

lobal m

anufacturers

resulte

d in moderatio

n of ra

w materia

l prices

•Property

segm

ent co

ntrib

utio

ns re

duce

d to

RM16.3 m

il (FY10: R

M22.8 m

il)

»Minimal contrib

utio

ns in

FY2012 in lin

e with

Group’s in

tentio

n to

focus o

n th

e packaging

busin

ess

FY11 Operational HighlightsFY11 Operational Highlights

Reven

ue C

AG

R (F

Y04 to

FY

11): 8

.5%

PB

T C

AG

R (0

4-1

1): 2

8.1

%P

AT

MI C

AG

R (0

4-1

1): 3

1.8

%

4Q11 and FY2011

5

4Q11 and FY2011

Financial Review

6

FY11 Income StatementFY11 Income Statement

4Q11 the best p

erforming quarter in the year, on the back of higher

revenue and favourableproduct m

ix…

4Q11 to

31.12.11

3Q11 to

30.9.11

Change vs

preceding qtr

RM'm

il

FY11 to

31.12.11

FY0 to

31.12.10

Change vs

previous F

Y

75.70

67.67

11.9%

Revenue

284.23

267.75

6.2%

9.57

7.97

20.1%

EBITDA

34.82

32.56

6.9%

7.35

5.88

25.0%

Operatin

g Profit

26.57

24.56

8.2%

0.24

(0.08)

(400.0%)

Share of A

ssociates

(0.07)

0.17

(141.2%)

7.27

5.49

32.4%

Pre-ta

x Profit

25.28

23.83

6.1%

5.91

4.54

30.1%

Net P

rofit to

Shareholders

20.07

18.19

10.4%

�FY2011 margins

booste

d by

recovered 4Q11

revenue and

favourable

FY11 Income StatementFY11 Income Statement

55.855.8

57.657.6

53.853.8

54.654.6

59.759.7

61.261.2

71.471.4

75.575.5

67.767.7

73.273.2

67.767.7

75.775.7

20

.0

40

.0

60

.0

80

.0

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

Qu

arte

rly R

eve

nu

e (R

M ‘m

il)

+0.3

%

5.05.0

5.85.8

5.95.9

6.16.1

5.05.0

4.24.2

4.84.8

4.24.2

4.64.6

5.05.0

4.54.5

5.95.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

Qu

arte

rly P

AT

MI (R

M ‘m

il)

+42.0

%

8.08

6.04

33.8%

Basic

EPS (se

n)

26.78

24.17

10.8%

12.6%

11.8%

0.8

EBITDA m

argin

12.3%

12.2%

0.1

9.6%

8.1%

1.5

PBT m

argin

8.9%

8.9%

(0.0)

7.8%

6.7%

1.1

Net m

argin

7.1%

6.8%

0.3

favourable

product m

ix

711 Balance Sheet (Highlights)11 Balance Sheet (Highlights)

Maintaining healthy returns in FY2011…

RM

’ mil

As

at

31

.12

.11

(Un

au

dite

d)

As

at

31

.12

.10

(Au

dite

d)

Fix

ed

as

se

ts (e

xc

l as

so

cia

te in

ve

stm

en

t)8

3.2

16

6.2

1

As

so

cia

te in

ve

stm

en

t 2

3.0

12

3.0

8

Cu

rren

t as

se

ts

12

1.8

01

22

.72

�Higher fix

ed asse

ts in

FY2011 due to

purchases o

f prin

ting

machine and

metalliz

er, a

s well a

s

building expansio

n

FYFY11 Balance Sheet (Highlights)11 Balance Sheet (Highlights)

Cu

rren

t liab

ilities

70

.43

69

.26

Sh

are

ho

lde

rs’ e

qu

ity1

40

.21

31

.47

To

tal b

orro

win

gs

3

5.5

42

9.5

3

Ca

sh

& B

an

k B

ala

nc

es

10

.41

6.3

0

Ne

t ge

arin

g0

.18

x0

.18

x

Re

turn

on

Ave

rag

e S

ha

reh

old

ers

Eq

uity

1

4.8

%1

4.3

%

Re

turn

on

Ave

rag

e T

ota

l As

se

ts9

.1%

9.1

%

�Increased borro

wings

to fin

ance m

achinery

purchase and

facilitie

s expansio

n

�Net gearin

g

maintained at

health

y levels

8

Dividend HistoryDividend History

4thinterim tax exempt dividend of 4 sen/share payable on

23 March 2012, tra

nslating to 50.3% payout…

55

.8%

51

.3%

51

.6%

50

.3%

50.0

%

75.0

%

100.0

%

6.0

0

9.0

0

12.0

0

%R

M ‘m

ilD

ivid

en

d P

ayo

ut

Div

idend P

ayout (R

M 'm

il)•Dividends in

respect o

f FY2011

»1stinterim

tax exempt d

ividend of

3.0 se

n/share (p

aid on 10 Jun 2011)

»2ndinterim

tax exempt d

ividend of

3.5 se

n/share (p

aid on 14 Sep 2011)

Dividend HistoryDividend History

6.0

6.0

15.5

15.5

12.5

12.5

13.5

13.5

0.0

4.0

8.0

12.0

16.0

2008

2009

2010

2011

se

nD

ivid

en

d P

ayo

ut (s

en

)

4.5

511

.67

9.3

81

0.0

90.0

%

25.0

%

0.0

0

3.0

0

2008

2009

2010

2011

»3rdinterim

tax exempt d

ividend of

3.0 se

n/share (p

aid on 8 Dec 2011)

»4thinterim

tax exempt d

ividend of

4 se

n/share (p

ayable on 23 Mar

2012)

9

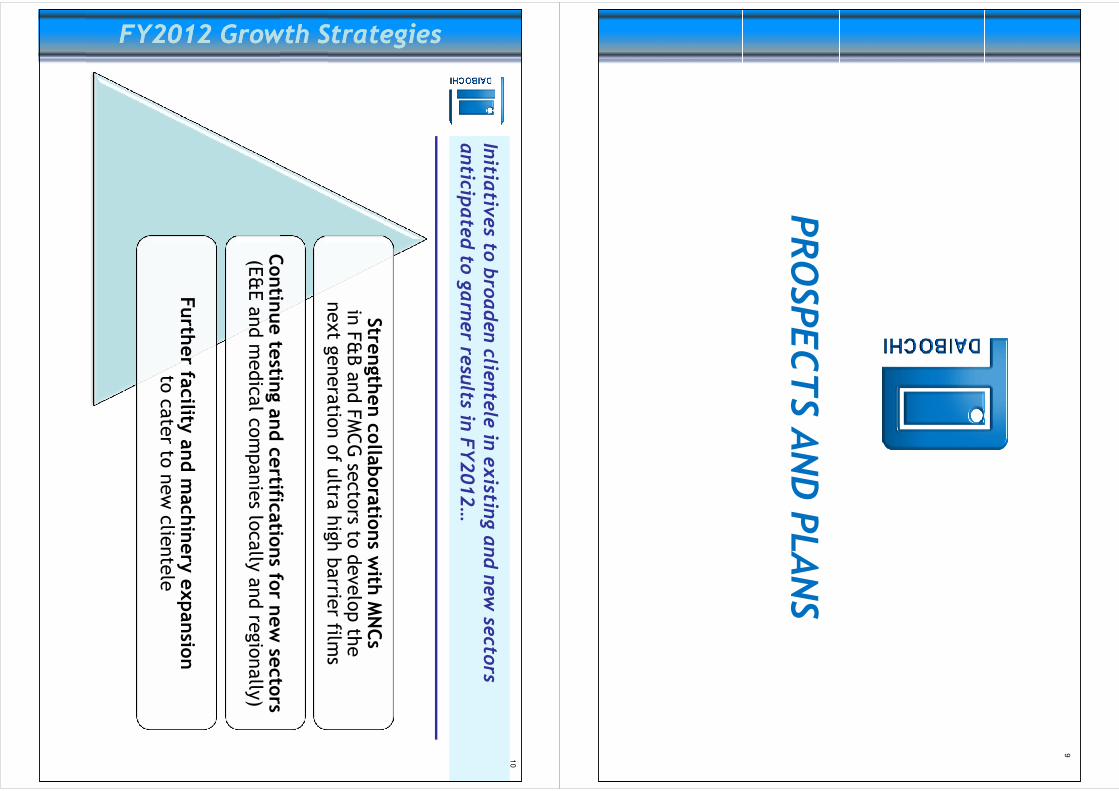

PROSPECTS AND PLANS

Strength

en co

llaboratio

ns w

ith MNCs

in F&B and FMCG se

ctors to

develop th

e

next g

eneratio

n of u

ltra high barrie

r films

Contin

ue te

sting a

nd ce

rtificatio

ns fo

r new se

ctors

10

Initia

tives to

broaden clie

ntele in existin

g and new sectors

anticip

ated to garner re

sults in

FY2012…

FY2012 Growth StrategiesFY2012 Growth Strategies

Contin

ue te

sting a

nd ce

rtificatio

ns fo

r new se

ctors

(E&E and medical companies lo

cally and re

gionally)

Furth

er fa

cility and m

ach

inery expansio

n

to cater to

new clientele

FY2012 Growth StrategiesFY2012 Growth Strategies

THANK YOU

11

THANK YOU

Bursa

: DAIBOCI/8125

Bloomberg: D

PP:M

KReute

rs: DPPM.K

L

IR Contacts:

Thomas Lim

E: to

[email protected]

om

T: 06-231 9779

JuliaPong

E: [email protected]

m.my

T: 012-3909258

APPENDIX

12

APPENDIX

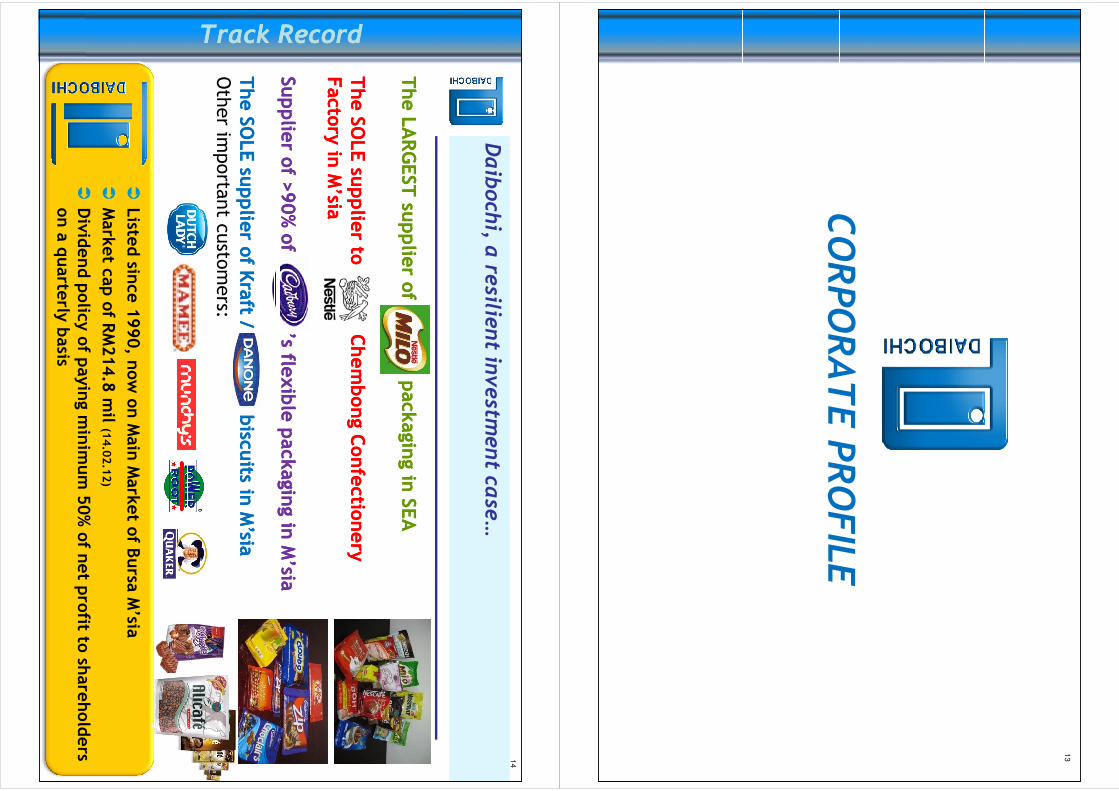

CORPORATE PROFILE

13

CORPORATE PROFILE

The LARGEST

supplie

r of p

ack

agin

g in SE

AThe LARGEST

supplie

r of p

ack

agin

g in SE

A

14

Daibochi, a resilie

nt investm

ent ca

se…

Track RecordTrack Record

The SO

LE su

pplie

r toThe SO

LE su

pplie

r toChembong

ChembongConfectio

nery

Confectio

nery

Facto

ry in

Facto

ry in

M’sia

M’sia

Supplie

r of

Supplie

r of >

90% of ’s fle

xible pack

agin

g in

>90% of ’s fle

xible pack

agin

g in M’sia

M’sia

Track RecordTrack Record

Supplie

r of

Supplie

r of >

90% of ’s fle

xible pack

agin

g in

>90% of ’s fle

xible pack

agin

g in M’sia

M’sia

The SO

LE su

pplie

r of K

raft / b

iscuits in

The SO

LE su

pplie

r of K

raft / b

iscuits in

M’sia

M’sia

Other im

porta

nt c

usto

mers:

�Liste

d sin

ce 1990, n

ow on Main Market o

f Bursa

M’sia

�Market ca

p of R

M214.8 m

il (14.02.12)

�Dividend policy

of p

aying m

inim

um 50% of n

et p

rofit to

shareholders

on a quarte

rly basis

DA

IBO

CH

I PL

AS

TIC

& P

AC

KA

GIN

G IN

DU

ST

RY

BE

RH

AD

Lis

ted

Main

Mark

et,

Burs

a M

ala

ysia

sin

ce 1

990

(Tra

nsfe

rred fro

m S

econd B

oard

in 2

003)

Secto

rIn

dustria

lP

roducts

15

Liste

d since 1990…

Corporate InformationCorporate Information

Secto

rIn

dustria

lP

roducts

Codes

Burs

a: 8

125 / D

AIB

OC

I

Blo

om

berg

: DP

P:M

K

Reute

rs: D

PP

M.K

L

Share

Capita

lR

M75.9

mil

(75.9

02

mil s

hare

s o

f RM

1 e

ach)

Mark

et C

apita

lizatio

nR

M214.8

mil (R

M2.8

3 a

s a

t 14 F

eb 2

012)

Corporate InformationCorporate InformationCorporate ProfileCorporate Profile

16

Leading flexible packaging solutions provider, w

ith enviable

reputation exceeding 35 years…

20

09

-A

cq

uire

d 9

thp

rintin

g m

ach

ine

; Ob

tain

ed

HA

LA

L C

ertific

atio

n;

20

08

–A

cq

uire

d w

ide

we

b p

oly

pro

pyle

ne

film m

akin

g m

ach

ine

20

07

-R

ece

ive

d G

old

Aw

ard

for th

e C

olo

rpa

kP

acka

gin

g

Exp

ort A

wa

rd a

t Au

stra

lian

Pa

cka

gin

g A

wa

rds

20

04

–A

cq

uire

d M

’sia

’s1

st5

-laye

r-blo

wn

film m

ach

ine

to

pro

du

ce

tran

sp

are

nt b

arrie

r films

Re

gio

na

l su

pp

lier fo

r BA

T

20

10

–O

bta

ine

d L

ette

r of V

alid

atio

n fro

m U

SA

for e

lectro

nic

pa

cka

gin

g

20

11

–A

cq

uire

d h

igh

-sp

ee

d p

rintin

g m

ach

ine

; Acq

uire

d m

eta

llize

rto

pro

du

ce

u

ltra h

igh

ba

rrier film

s; A

ccre

dite

d w

ith IS

O:1

40

01

Corporate ProfileCorporate Profile

19

94

–A

cq

uire

d fa

ste

st e

xtru

sio

n la

min

ato

r in S

EA

19

96

-M

ove

d to

cu

rren

t pre

mis

es w

ith >

32

5,0

00

sq

ft bu

ilt-up

are

a

20

01

–In

co

rpo

rate

d A

ustra

lian

su

bsid

iary

; Accre

dite

d w

ith IS

O:9

00

1

19

99

–S

up

plie

r to N

estle

M’s

ia

20

02

–A

cq

uire

d m

eta

llize

rw

ith P

lasm

a T

ech

to p

rod

uce

hig

h-b

arrie

r films;

Re

gio

na

l Su

pp

lier to

Ne

stle

in S

EA

20

03

–T

ran

sfe

r to M

ain

Bo

ard

(no

w M

ain

Ma

rke

t); Accre

dite

d w

ith H

AC

CP

19

90

–A

cq

uire

d m

eta

llize

rto

pro

du

ce

in-h

ou

se

me

taliz

ed

films; L

iste

d o

n 2

nd

Bo

ard

of K

LS

E (B

urs

a M

’sia

)

19

87

–A

cq

uire

d p

oly

pro

pyle

ne

film-m

akin

g m

ach

ine

to p

rod

uce

in-h

ou

se

films

19

84

–S

tarte

d in

-ho

use

prin

ting

cylin

de

r ma

kin

g

19

72

–E

sta

blis

he

d in

Me

laka

with

10

,00

0 s

q ft p

lan

t; Mo

ve

d to

larg

er p

rem

ise

s w

ith 1

65

,52

7 s

q ft

Corporate Profile (Corporate Profile (con’tcon’t))

••Accre

dite

d and w

orld

Accre

dite

d and w

orld

--class

class

productio

n fa

cilities

productio

n fa

cilities

»Atta

ined ISO

:9001and ISO

:14001

certific

atio

ns

»Hazard Analysis C

ritical C

ontro

l Points

(HACCP) compliant to

ensure

17

Internationally-certifie

d productio

n facilitie

s that co

mply

with all fa

ctory audits b

y our MNC clie

ntele…

Corporate Profile (Corporate Profile (

(HACCP) compliant to

ensure

adherence to

food sa

fety re

quire

ments

»Obtained HALALcertific

atio

n

••Well

Well--e

quipped la

boratory te

sting

equipped la

boratory te

sting

facilitie

sfacilitie

s»

To ensure our p

roducts e

xceed custo

mers’

pack

aging barrie

r (MVTR ASTM F1249, O

2TR

ASTM D3895-35), re

tentio

n(GC with

Headspace) and m

igra

tion(COF ASTM

D1894) re

quire

ments.

18

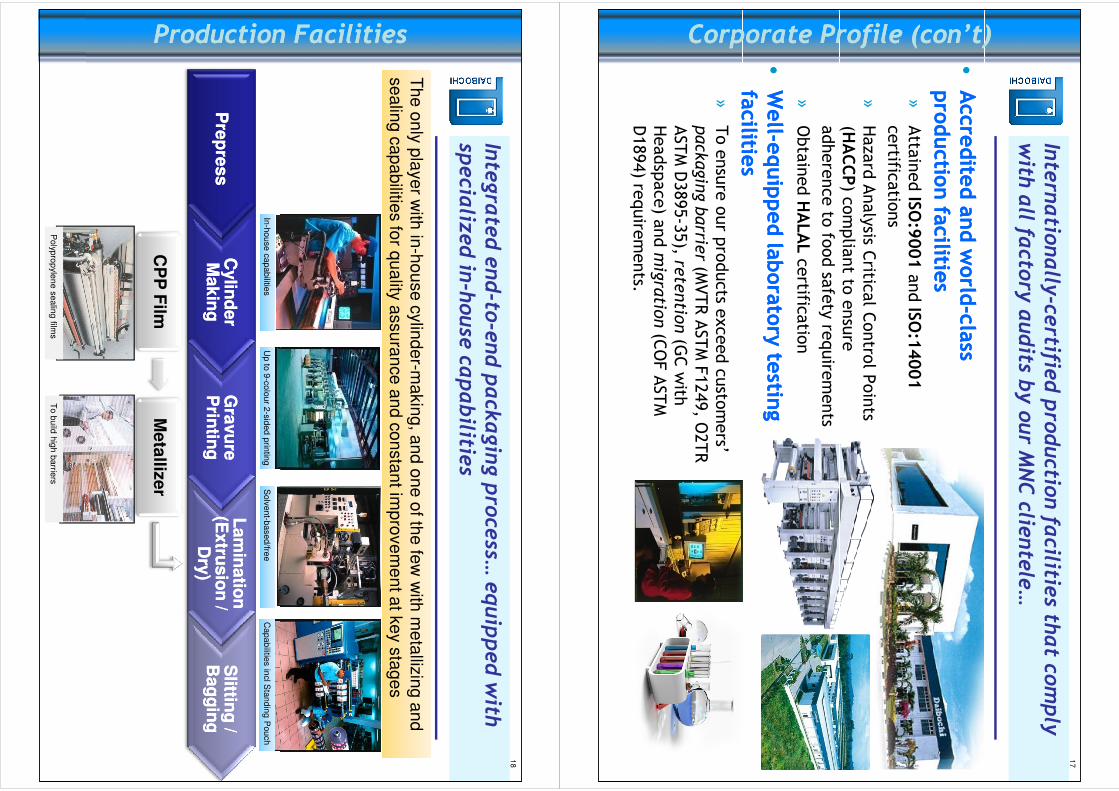

Production FacilitiesProduction Facilities

Integrated end-to-end packaging process… equipped with

specialized in-house capabilitie

s

Th

e o

nly

pla

ye

r with

in-h

ou

se

cylin

de

r-ma

kin

g, a

nd

on

e o

f the

few

with

me

talliz

ing

an

d

se

alin

g c

ap

abilitie

s fo

r qu

ality

assu

ran

ce

an

d c

on

sta

nt im

pro

ve

me

nt a

t ke

y s

tag

es

Production FacilitiesProduction Facilities

Pre

pre

ss

Pre

pre

ss

Cylin

de

r C

ylin

de

r M

ak

ing

Ma

kin

gG

ravu

re

Gra

vu

re

Prin

ting

Prin

ting

La

min

atio

n

La

min

atio

n

(Ex

trus

ion

/ (E

xtru

sio

n /

Dry

)D

ry)

Slittin

g /

Slittin

g /

Ba

gg

ing

Ba

gg

ing

CP

P F

ilmM

eta

llize

r

Up to

9-c

olo

ur 2

-sid

ed p

rintin

gIn

-house c

apabilitie

sS

olv

ent-b

ase

d/fre

eC

apabilitie

s in

clS

tandin

g P

ouch

To b

uild

hig

h b

arrie

rsP

olyp

rop

yle

ne s

ealin

g film

s

19

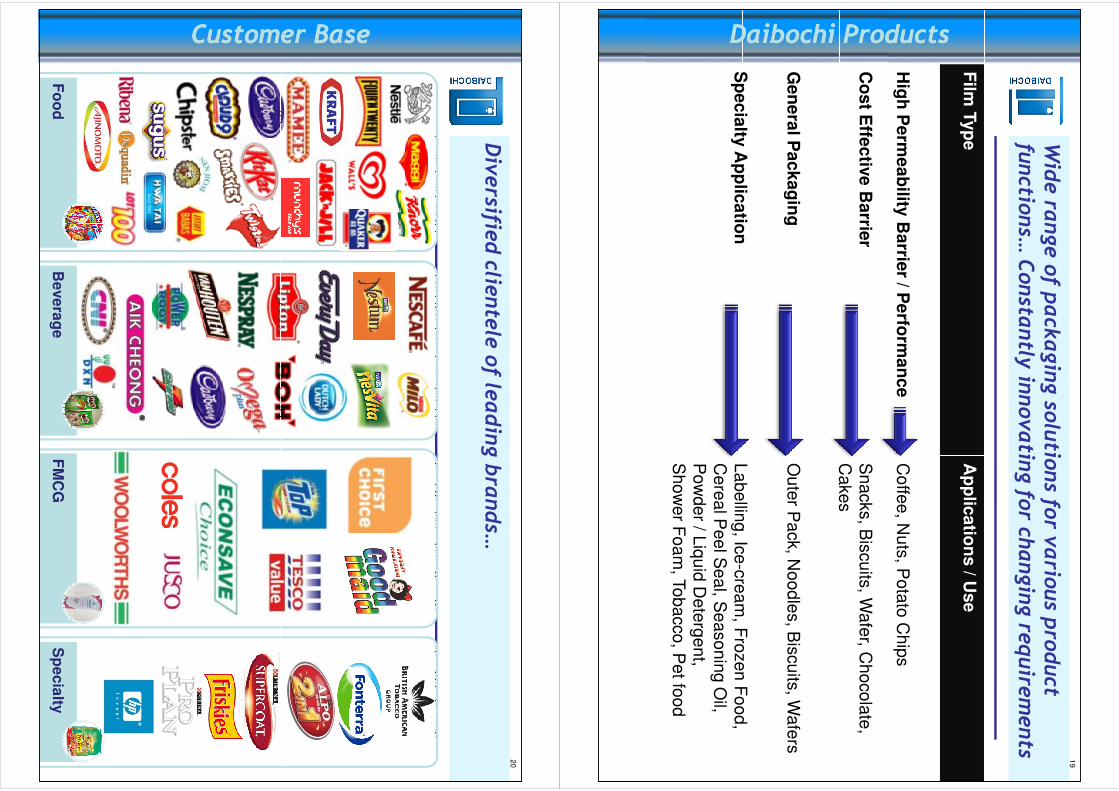

Daibochi ProductsDaibochi Products

Wide range of packaging solutions fo

r various product

functio

ns… Constantly innovating for ch

anging requirements

Film

Typ

eA

pp

lica

tion

s/ U

se

Hig

h P

erm

ea

bility

Ba

rrier / P

erfo

rma

nc

eC

offe

e,N

uts

, Po

tato

Ch

ips

Co

st E

ffec

tive

Ba

rrier

Sn

acks, B

iscu

its, W

afe

r,C

ho

co

late

,

Ca

ke

s

Daibochi ProductsDaibochi Products

Ca

ke

s

Ge

ne

ralP

ac

ka

gin

gO

ute

r Pa

ck, N

oo

dle

s, B

iscu

its, W

afe

rs

Sp

ec

ialty

Ap

plic

atio

nL

ab

ellin

g, Ic

e-c

rea

m,

Fro

ze

n F

oo

d,

Ce

rea

l Pe

el S

ea

l, Se

aso

nin

g O

il, P

ow

de

r / Liq

uid

De

terg

en

t, S

ho

we

r Fo

am

, To

ba

cco

, Pe

t foo

d

Customer BaseCustomer Base

Diversifie

d clie

ntele of leading brands…

20

Fo

od

Be

ve

rag

eF

MC

GS

pe

cia

lty

Customer BaseCustomer Base

21

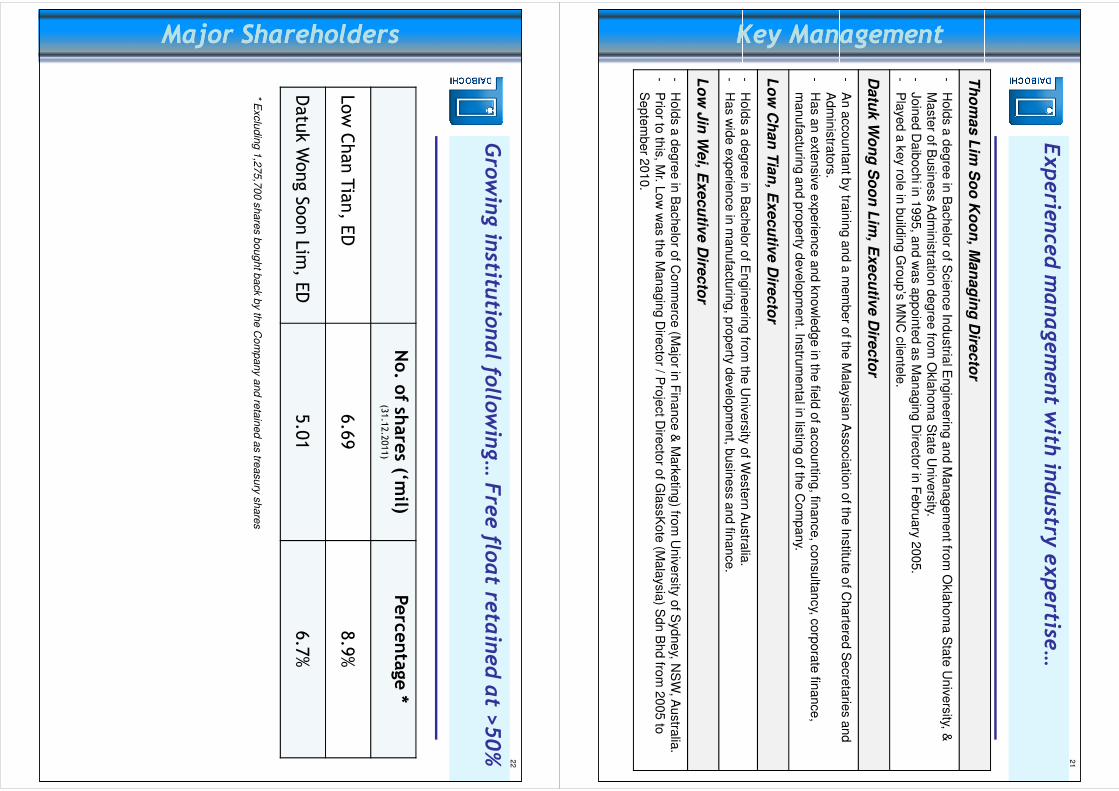

Key ManagementKey Management

Experienced management with industry

expertise

…

Th

om

as

Lim

So

oK

oo

n, M

an

ag

ing

Dire

cto

r

-H

old

s a

degre

e in

Bachelo

r of S

cie

nce In

dustria

l Engin

eerin

g a

nd M

anagem

ent fro

m O

kla

hom

a S

tate

Univ

ers

ity, &

Maste

r of B

usin

ess A

dm

inis

tratio

n d

egre

e fro

m O

kla

hom

a S

tate

Univ

ers

ity.

-Join

ed D

aib

ochi in

1995, a

nd w

as a

ppoin

ted a

s M

anagin

g D

irecto

r in F

ebru

ary

2005.

-P

layed

a k

ey ro

le in

build

ing G

roup’s

MN

C c

liente

le.

Da

tuk

Wo

ng

So

on

Lim

, Ex

ec

utiv

eD

irec

tor

-A

n a

ccounta

nt b

y tra

inin

g a

nd a

mem

ber o

f the M

ala

ysia

n A

ssocia

tion o

f the In

stitu

te o

f Charte

red S

ecre

tarie

s a

nd

Key ManagementKey Management

-A

n a

ccounta

nt b

y tra

inin

g a

nd a

mem

ber o

f the M

ala

ysia

n A

ssocia

tion o

f the In

stitu

te o

f Charte

red S

ecre

tarie

s a

nd

Adm

inis

trato

rs.

-H

as a

n e

xte

nsiv

e e

xperie

nce a

nd k

now

ledge in

the fie

ld o

f accountin

g, fin

ance, c

onsulta

ncy, c

orp

ora

te fin

ance,

manufa

ctu

ring a

nd p

roperty

develo

pm

ent. In

stru

menta

l in lis

ting o

f the C

om

pany.

Lo

w C

ha

nT

ian

, Ex

ec

utiv

eD

irec

tor

-H

old

s a

degre

e in

Bachelo

rof E

ngin

eerin

gfro

m th

e U

niv

ers

ity o

f Weste

rn A

ustra

lia.

-H

as w

ide e

xperie

nce in

manufa

ctu

ring, p

roperty

develo

pm

ent, b

usin

ess a

nd fin

ance.

Lo

w J

in W

ei, E

xe

cu

tive

Dire

cto

r

-H

old

s a

degre

e in

Bachelo

rof C

om

merc

e (M

ajo

r in F

inance &

Mark

etin

g) fro

m U

niv

ers

ity o

f Sydney, N

SW

, Austra

lia.

-P

rior to

this

, Mr. L

ow

was th

e M

anagin

g D

irecto

r / Pro

ject D

irecto

r of G

lassK

ote

(Mala

ysia

) Sdn B

hd fro

m 2

005 to

Septe

mber 2

010.

22

Major ShareholdersMajor Shareholders

Growing institu

tional following… Free float re

tained at >50%

No. o

f shares (‘m

il)(31.12.2011)

Perce

ntage

*

Low Chan Tian, E

D6.69

8.9%

Datuk Wong Soon Lim, E

D5.01

6.7%

Major ShareholdersMajor Shareholders

* Exclu

din

g 1

,27

5,7

00

sh

are

s b

ou

gh

t ba

ck b

y th

e C

om

pa

ny a

nd

reta

ine

d a

s tre

asu

ry s

ha

res

INDUSTRY INSIGHT

23

INDUSTRY INSIGHT

••Flexible pack

agin

g market, w

orth

Flexible pack

agin

g market, w

orth

$58.3

$58.3 bil

bilin 2011, e

stimated to

in 2011, e

stimated to

reach

$71.3

reach

$71.3 bil

bilin 2016

in 2016*

»Favoured fo

r its versa

tility, comparative

low cost a

nd potentia

l for in

novatio

n.

24

Industry InsightIndustry Insight

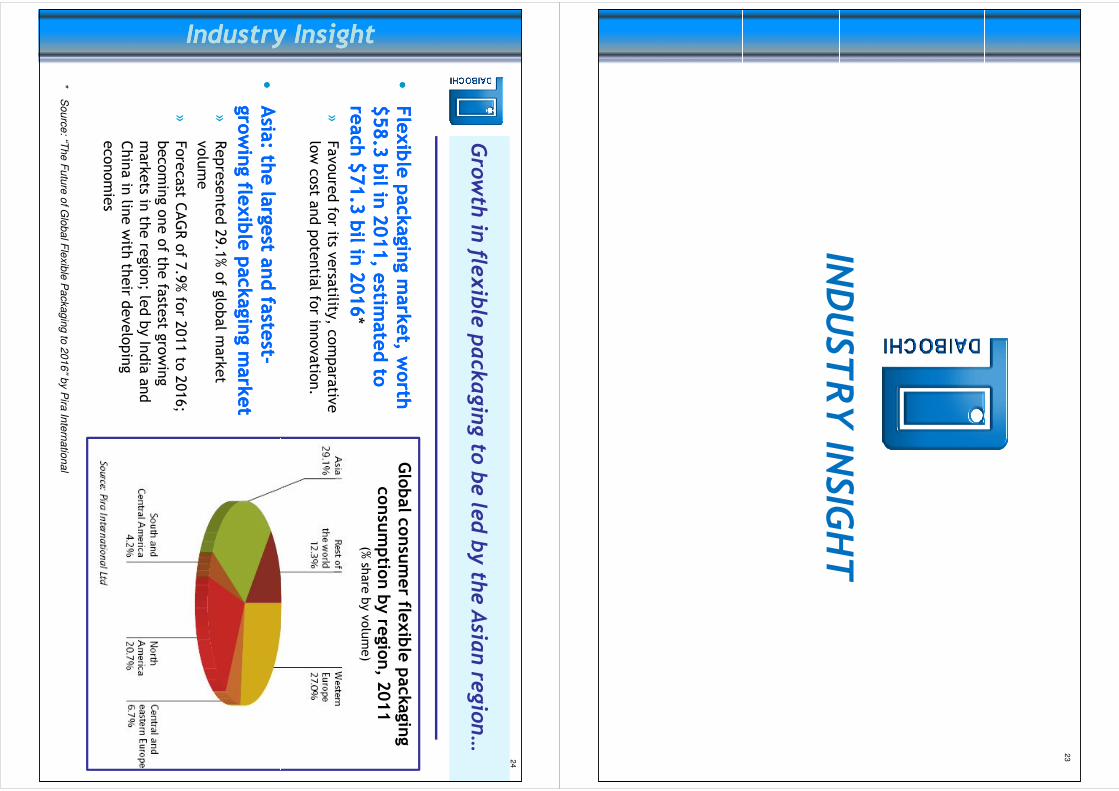

Growth in flexible packaging to be led by the Asian region…

Global co

nsumer fle

xible packa

ging

consumptio

n by re

gion, 2

011

(% sh

are by volume)

••Asia

: the la

rgest a

nd fa

stest

Asia

: the la

rgest a

nd fa

stest--

growing fle

xible pack

agin

g market

growing fle

xible pack

agin

g market

»Represented 29.1% of global m

arket

volume

»Forecast C

AGR of 7

.9% fo

r 2011 to

2016;

becoming one of th

e fa

stest g

rowing

markets in

the re

gion; le

d by India and

China in lin

e with

their d

eveloping

economies

Industry InsightIndustry Insight

*S

ou

rce

: “Th

e F

utu

re o

f Glo

ba

l Fle

xib

le P

acka

gin

g to

20

16

” by P

iraIn

tern

atio

na

l