67

BHARTI AIRTEL LIMITED AND SUBSIDIARIES (formerly Bharti Tele-Ventures Limited) Consolidated Financial Statements – for the years ended March 31, 2005, 2006 and 2007

BHARTI AIRTEL LIMITED AND SUBSIDIARIES

(formerly Bharti Tele-Ventures Limited)

Consolidated Financial Statements – for the years ended March 31, 2005, 2006 and 2007

Report of Independent Auditors

To the Board of Directors and Shareholders of Bharti Airtel Limited (Formerly, Bharti Tele-Ventures Limited)

In our opinion, the accompanying consolidated Balance Sheet and the related consolidated Statement of Operations, of Cash Flows and of Changes in Stockholders’ Equity, present fairly, in all material respects, the financial position of Bharti Airtel Limited and its subsidiaries (together the “Group”) at March 31, 2007 and 2006, and the results of their operations and their cash flows for each of the years in the three year period ended March 31, 2007, in conformity with accounting principles generally accepted in the United States of America. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these statements in accordance with auditing standards generally accepted in United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

Price Waterhouse

New Delhi, India

Date :- April, 27th 2007

- 2 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Consolidated Balance Sheets (Amounts in thousands of Indian Rupees, except per share data and as stated otherwise)

The accompanying notes form an integral part of these consolidated financial statements.

Sunil B. Mittal Akhil Gupta Sarvjit S. Dhillon Deven Khanna Chairman and Managing Director

Joint Managing Director Chief Financial Officer Group Financial Controller

New Delhi, India April 27, 2007

3

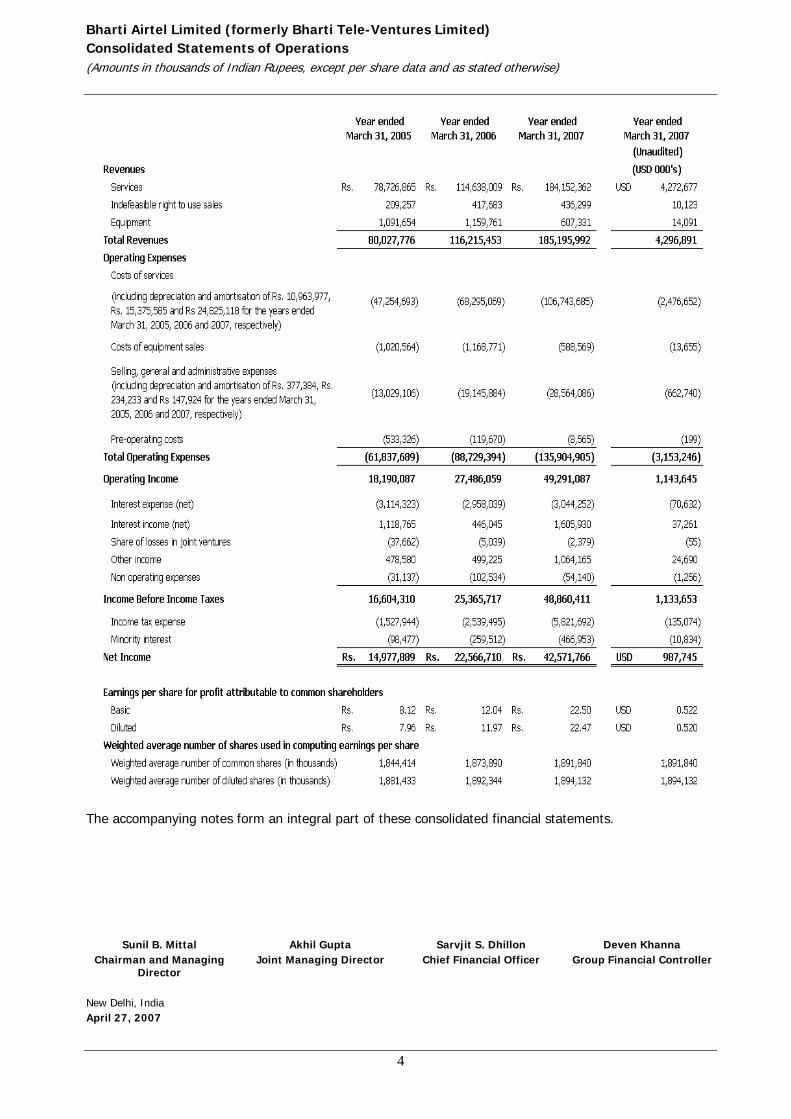

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Consolidated Statements of Operations (Amounts in thousands of Indian Rupees, except per share data and as stated otherwise)

The accompanying notes form an integral part of these consolidated financial statements.

Sunil B. Mittal Akhil Gupta Sarvjit S. Dhillon Deven Khanna Chairman and Managing

Director Joint Managing Director Chief Financial Officer Group Financial Controller

New Delhi, India April 27, 2007

4

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Consolidated Statement of Stockholders’ Equity (Amounts in thousands of Indian Rupees, except per share data and as stated otherwise)

- 5 -

The accompanying notes form an integral part of these consolidated financial statements. The movement in treasury stock is due to exercise of stock options by the employees of the Group.

Sunil B. Mittal Akhil Gupta Sarvjit S. Dhillon Deven Khanna Chairman and Managing Director Joint Managing Director Chief Financial Officer Group Financial Controller

New Delhi, India April 27, 2007

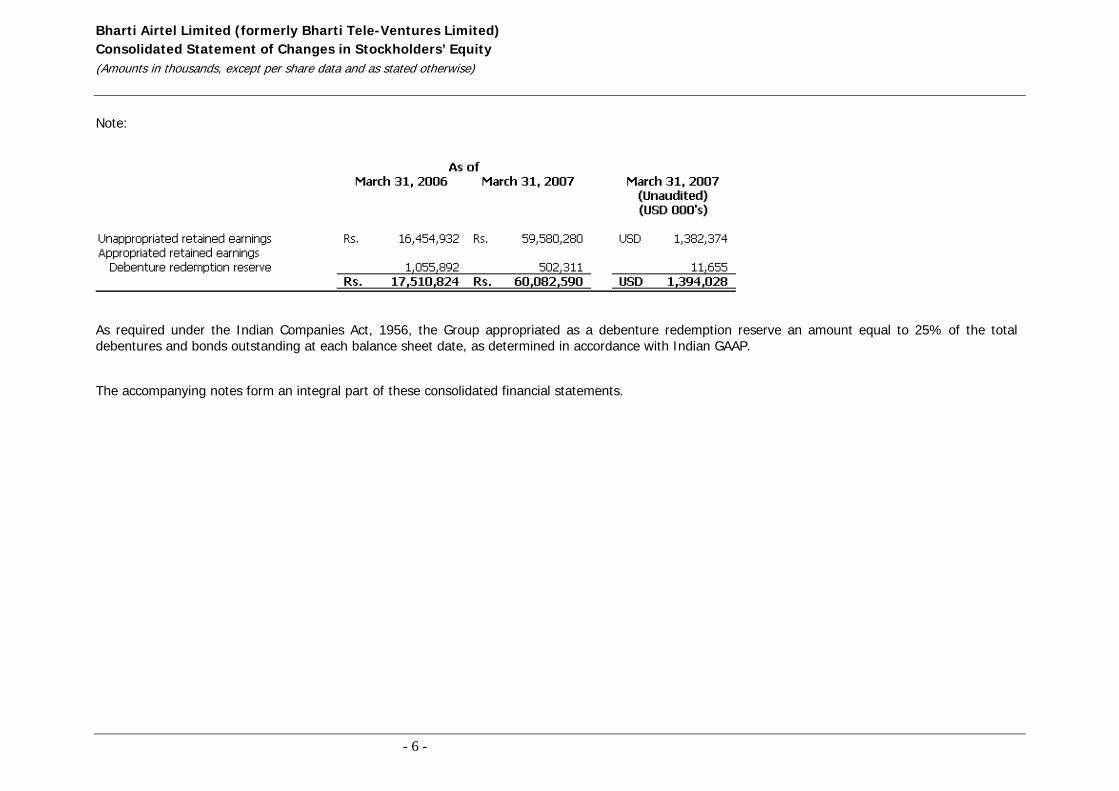

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Consolidated Statement of Changes in Stockholders’ Equity (Amounts in thousands, except per share data and as stated otherwise)

Note:

As required under the Indian Companies Act, 1956, the Group appropriated as a debenture redemption reserve an amount equal to 25% of the total debentures and bonds outstanding at each balance sheet date, as determined in accordance with Indian GAAP.

The accompanying notes form an integral part of these consolidated financial statements.

- 6 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Consolidated Statement of Cash Flows (Amounts in thousands of Indian Rupees, except per share data and as stated otherwise)

The accompanying notes form an integral part of these consolidated financial statements.

Sunil B. Mittal Akhil Gupta Sarvjit S. Dhillon Deven Khanna Chairman and Managing

Director Joint Managing Director Chief Financial Officer Group Financial Controller

New Delhi, India April 27, 2007

- 7 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Consolidated Statement of Cash Flows (Amounts in thousands, except per share data and as stated otherwise)

Supplementary information to consolidated statement of cash flows

Cash paid during the year:

Non – cash items:

The accompanying notes form an integral part of these consolidated financial statements.

- 8 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands of Indian Rupees, except per share data and as stated otherwise)

1. BACKGROUND

a. Incorporation and history

Bharti Airtel Limited (‘Bharti Airtel’ or ‘the Company’) (formerly ‘Bharti Tele-Ventures Limited - BTVL’) was incorporated on July 7, 1995 under the laws of India for promoting investments in telecommunication services. Bharti Airtel together with its subsidiaries is hereinafter referred to as ‘the Group’. The Group is a leading telecommunication service provider in India.

The Group’s principal shareholders include Bharti Telecom Limited, Singapore Telecommunication International Pte Limited and Vodafone International Holdings B.V.

The shares of the Company are listed on the National Stock Exchange (‘NSE’) and the Mumbai Stock Exchange (‘BSE’), India. With effect from April 24, 2006, the name of the Company has been changed from Bharti Tele-Ventures Limited (‘BTVL’) to Bharti Airtel Limited (‘Bharti Airtel’). b. Description of business

The current businesses of the Group include:

• mobile services • broadband and telephone services

• enterprise services carriers; and • enterprise services corporate

c. Industry overview and licensing structure

The key regulations governing the Group’s businesses are detailed below: Mobile services In 1994, the telecommunications sector was partially deregulated for Cellular Mobile Telephony Services (‘CMTS’). The licenses were issued by the Department of Telecommunications (‘DoT’) to the Group upon payment of fixed amounts as annual license fees and were valid for an initial period of 10 years. In addition, the Group was required to pay a fixed amount for wireless and spectrum charges to the Wireless Planning Commission (‘WPC’) – a section of the DoT. This regime is collectively referred to herein as the “old license fee regime”. The Government of India (‘GoI’) approved the New Telecom Policy, 1999 (‘NTP-99’) on July 6, 1999, which came into effect from August 1, 1999, providing for the payment of a “one-time license entry fee” and annual fees payable under a revenue sharing arrangement. Also, the license period was extended from the original 10 years to 20 years. This regime is collectively referred to herein as the “NTP-99 license fee regime”. For the existing mobile and fixed line services operators, license fees payable up to July 31, 1999, under the old license fee regime, as adjusted for the notional extension of the effective date of the original licenses by six months, were deemed to be the one-time license entry fees. New licensees would pay a one time upfront fee plus the revenue share. The Group provided its unconditional acceptance of the terms and conditions for migrating to NTP-99 license fee regime.

- 9 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

In September 2001, the DoT fixed the license fees payable by the mobile service providers at 12% of adjusted gross revenues (‘AGR’) as defined in the regulation, in category A circles, 10% in category B circles and 8% in category C circles. AGR has been defined as the total income including service revenues, finance income, and non-operating income, reduced by access and interconnection costs, service tax and/or sales tax, if applicable. The rates for payment of license fees have since been further revised and currently a licensee is required to pay 10%, 8% and 6% of its AGR for A, B and C categories of circles, respectively

Broadband and telephone Services

In September 1994, the GoI announced guidelines for private sector entry into the fixed-line telecommunication services, which provided for the granting of licenses for the provision of fixed line services to one new licensee in each of the telecommunication circles. Within each circle, the new licensees would compete with Mahanagar Telephone Nigam Limited (‘MTNL’) (in Delhi and Mumbai) and Bharat Sanchar Nigam Limited (‘BSNL’) (in all other circles). The licenses would be valid for a period of 15 years. The Group obtained the licenses from the DoT to provide fixed line services in Madhya Pradesh, Delhi, Haryana, Karnataka and Tamil Nadu circles. These licences were granted by the DoT on a non-exclusive basis. The revenue share percentages have been fixed by the GoI at 10%, 8% and 6% of the AGR for A, B and C categories of circles, respectively.

Amendment to NTP 99: Introduction of a Unified Licensing Regime

In November 2003, the DoT decided to issue licenses for Unified Access (Basic and Cellular) Services. The services under UASL license cover collection, transmission and delivery of voice/non-voice messages in designated service areas and include provision of all type of access services utilizing any type of network equipment. Considering the option available to migrate to the new UASL regime, the Group migrated its CMTS licenses in Chennai, Delhi, Kolkata, Mumbai, Gujarat, Haryana, Himachal Pradesh, Kerala, Madhya Pradesh, Maharashtra, Tamilnadu, Uttar Pradesh (West), Andhra Pradesh, Karnataka and Punjab to UASL after obtaining the necessary approvals from the DoT with effect from April 27, 2004. Further, the Group surrendered its Basic Service Licenses in Delhi, Haryana, Karnataka and Tamilnadu effective October 1, 2004 and in Madhya Pradesh with effect from December 12, 2004. The Group continues to provide basic services in these circles on the basis of the UASL that it had received for these circles resulting from the conversion of the mobility licenses. The service area, roll out obligations, bank guarantees and revenue share payable as license fees by a UASL licensee are the same as specified for a fourth cellular operator. National and International Long Distance

On November 29, 2001, the Group entered into a license agreement with the DoT, on a non-exclusive basis, to install, operate and maintain national long distance services (‘NLD’) within India. The license is valid for a period of 20 years extendable for a period of 10 years. The Group commenced data services in December 2001 and voice services in January 2002. In addition to the entry fees, the annual license fees were in the form of a revenue share at 10% of its AGR plus a prescribed contribution towards a Universal Service Obligation Fund (‘USO’) with a maximum fee at 15% of its AGR. The rate for payment of license fee has been revised from 15% to 6% with effect from January 1, 2006. In March 2002, the Group was awarded a license to provide International Long Distance (‘ILD’) services. The license is valid for a period of 20 years. The Group commenced ILD operations in July 2002. The rate for payment of revenue share license fee has been revised from 15% to 6% with effect from January 1, 2006.

- 10 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

Interconnection between Operators

The Group has entered into interconnect agreements with BSNL and other private sector operators for terminating outgoing calls from its network. The interconnection agreements with BSNL require the Group to make payments based on the number of points of connectivity with BSNL’s network and permit sharing of revenue generated by outgoing calls. The Group’s interconnection agreements with other private sector operators are based on mutually agreeable terms and conditions. Interconnection between operators is now governed by the Interconnect Usage Charges (‘IUC’) Regulation, released by the Telecom Regulatory Authority of India (‘TRAI’), which defines charges payable on the principle of origination, carriage and termination. The IUC Regulation has been revised by the TRAI from time to time.

d. Business

The Group conducts its businesses through Bharti Airtel and it’s directly and indirectly held majority owned subsidiaries, which are as follows:

i) BCOL was incorporated on December 5, 1997, as a wholly owned subsidiary of Bharti Telecom Limited (‘BTL’) under the laws of India. On 26 March, 2001, it became a wholly owned subsidiary of Bharti Infotel Limited (‘BIL’), which subsequently amalgamated with Bharti Airtel. BCOL provides administrative support to Bharti Airtel’s operations and trades in VSATs and related equipment. BCOL was consolidated in the consolidated financial statements of the Group. ii) BAQL was incorporated on October 3, 2000, as a wholly owned subsidiary of Bharti Airtel, under the laws of India, to build, operate and maintain a cable landing station for the fibre optic submarine cable system linking India and Singapore. On September 29, 2001, Bharti Airtel transferred its equity holdings in BAQL in favor of Bharti Telesonic Limited. Through an agreement dated January 18, 2001, Singapore i2i Private Limited (‘i2i’) agreed to hold 49% equity interest in BAQL, and on December 26, 2001, i2i subscribed to these shares incorporating a 51:49 joint venture. i2i has substantive participative rights in the operation and management of BAQL. The application of EITF 96-16 “Investor’s Accounting for an Investee when the Investor Has a majority of the Voting Interest but the Minority Shareholder or Shareholders Have Certain Approval or Veto Rights” (‘EITF 96-16’), has therefore precluded the consolidation of BAQL by Bharti Airtel and as such, the investment in BAQL has been accounted for using the equity method.

- 11 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

iii) Hexacom provides CMTS in the circles of Rajasthan and North East. The Group entered into a Share Purchase Agreement with Shyam Telecom Group (‘Shyam’) to acquire and assume its 67.5% joint venture interest in Hexacom on May 7, 2004, an additional 1% equity interest on October 7, 2004 and a further 0.39% equity interest on September 14, 2006 thereby increasing its stake to 68.89% by March 31, 2007. The Group obtained full operational and management control on September 10, 2004 and has consolidated Hexacom since then (refer Note 3). iv) SBEL and its 100% subsidiary BBL provide enterprise services. The Group entered into a Share Purchase Agreement with Max India Limited to acquire and assume its 100% stake in SBEL on February 1, 2005, in order to provide a strategic fit to the Group's existing VSAT and broadband infrastructure and also to its Enterprise Services Corporate business. The Group obtained control over SBEL and its wholly owned subsidiary BBL on February 1, 2005, when the majority shareholding of 51% was transferred to the Group. The Group has consolidated SBEL and BBL from that date. The remaining 49% stake was transferred to the Group on April 16, 2005. e. New Operations During the year ended March 31, 2007, seven wholly owned subsidiaries were incorporated - Bharti Airtel (USA) Limited, Bharti Airtel (UK) Limited, Bharti Airtel (Hong Kong) Limited and Bharti Airtel (Canada) Limited with their principal business of providing international calling services and wholesale switching data products, Bharti Infratel Limited with its principal business of providing passive infrastructure for mobile services, Bharti Telemedia Limited with Direct to Home (‘DTH’) Venture as principal business and Bharti Airtel Lanka (Private) Limited with its principal business of Mobile Cellular Communication services.

- 12 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

- 13 -

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES a) Basis of preparation

The consolidated financial statements for the years ended March 31, 2005, 2006 and 2007 have been prepared in accordance with accounting principles generally accepted in the United States of America (‘US GAAP’). The significant accounting policies adopted by Bharti Airtel and its subsidiaries, in respect of these consolidated financial statements, are set out below. These consolidated financial statements have been prepared in thousands of Indian Rupees, the national currency of India. The consolidated financial statements were authorized for issue on April 27, 2007 by the Board of Directors of the Company. The Group's financial statements have been prepared assuming the Group will continue as a going concern. The Group had a retained deficit and a net current ratio deficit as of March 31, 2005 and retained earnings and a net current ratio deficit as of March 31, 2006 and as of March 31, 2007. In addition, as further discussed in Note 30, the Group in its normal course of business has several significant pending claims that are also impacting the telecommunications industry as a whole. Management believes the Group generates sufficient operating cash flows and has access to adequate borrowing facilities to fund its working capital, its existing operations and the continued expansion of its network. b) Convenience translation The Group’s reporting currency is Indian National Rupees (‘Rupee(s)’ or ‘Rs.’ or ‘INR’) The translation of Rupee amounts into United States Dollars is unaudited and is included solely for the convenience of readers outside of India and has been calculated using the rate of USD (US$) 1 = Rs. 43.10, the noon buying rate in the city of New York for cable transfers in Rupees as announced by the Federal Reserve Bank of New York for customs purposes on March 31, 2007. Such translations should not be construed as representations that the Rupee amounts represent, or have been or could be converted into, United States Dollars at that or any other rate. c) Use of estimates

The preparation of financial statements in conformity with US GAAP requires the use of management estimates and assumptions that affect the amounts reported. These estimates are based on historical experience and information that is available to management about current events and actions that the Group may take in the future. Significant items subject to estimates and assumptions include the useful lives (other than for goodwill) and the evaluation of impairment of property, equipment and identifiable intangible assets and goodwill, the income tax and valuation reserves, the valuation of the assets and liabilities acquired in business combinations, the contingencies and legal reserves, and the provision for impairment of receivables and advances. Actual results could differ from these estimates.

d) Principles of consolidation The consolidated financial statements of the Group include the accounts of the Company and its subsidiaries. All intercompany transactions and balances are eliminated in consolidation. Operating results of companies acquired are included from the dates of acquisition. The Group includes in its consolidated financial statements the accounts of the variable interest entities (‘VIEs’) in which the Group is the primary beneficiary pursuant to the Financial Accounting Standards Board (‘FASB’) Interpretation No. 46(R) “Consolidation of Variable Interest Entities, an interpretation of ARB No. 51” (‘FIN 46R’). The Group consolidates entities not determined to be VIEs when it holds a majority of the entity's outstanding voting shares and control rests with the Group. Where the Group has a majority voting

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

- 14 -

interest in an entity but the minority shareholders have substantive participating rights, the Group accounts for its investment in the entity using the equity method of accounting in accordance with EITF 96-16. The Group accounts for investments in entities that are not VIEs where the Group owns a voting or economic interest of 20% to 50% and/or for which it has significant influence over operating and financing decisions using the equity method of accounting.

e) Joint ventures The Group’s interest in joint ventures in which the Group has a majority interest, but does not control due to the significant participatory rights of the minority shareholders are accounted for under the equity method of accounting and is initially recognized at cost. Under this method, the Group’s share of the post-acquisition profits or losses of the joint venture is recognized in the consolidated statement of operations and its share of post-acquisition movements in equity is recognized in equity. The cumulative post-acquisition movements are adjusted against the cost of the investment. Unrealized gains on transactions between the Group and its joint venture are eliminated to the extent of the Group’s interest in the joint venture; unrealized losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. The Group’s investment in joint venture includes goodwill identified on acquisition. The Group’s interest in jointly controlled entities is accounted for by the equity method of accounting and is initially recognized at cost. f) Restricted cash Restricted cash consists of deposits pledged with various government authorities and deposits restricted as to usage under lien to banks for guarantees and letters of credit given by the Group. The restricted cash is primarily invested in time deposits with banks. The classification of restricted cash into current and non-current is determined based on the maturity date of the deposits. g) Cash and cash equivalents Cash includes cash in hand, cash with banks and cash equivalents, which represent highly liquid deposits with an original maturity of ninety days or less. All the investments which includes government securities, treasury bills and mutual funds are classified as trading investments (refer Note 2 (i)) and are accordingly included in short term investments in the consolidated balance sheet (refer Note 7) h) Allowance for uncollectible accounts receivable The allowance for uncollectible accounts receivable reflects management’s best estimate of probable losses inherent in the accounts receivable balance. Management primarily determines the allowance based on the aging of accounts receivable balances and historical write-off experience, net of recoveries. The Group provides for amounts outstanding for more than 90 days in case of active subscribers and for all amounts outstanding from customers who have been deactivated as reduced by security deposits, or in specific cases where management is of the view that the amounts are not recoverable. For receivables due from the other operators on account of their NLD and ILD traffic, IUC and roaming charges, the Group provides for amounts outstanding for more than 120 days from the date of billing net of any amounts payable to the operators pertaining to the same period or in specific cases where management is of the view that the amounts are not recoverable. All amounts due from debtors that have been outstanding for more than three years are written off against the provision. The Group’s provisions created for uncollectible receivables are included in selling, general and administrative expenses in the consolidated statement of operations.

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

i) Investments All of the Group’s marketable securities are acquired principally for the purpose of generating a profit from short-term fluctuation in prices and are accordingly classified as trading investments. All purchases and sales of such investments are recognized on the trade date. Investments are initially measured at cost, which is the fair value of the consideration given for them, including transaction costs. Changes in the fair values of trading investments are recognized in the consolidated statement of operations as part of operating expense/income. Debt securities for which management has the positive intent and ability to hold to maturity are classified as held-to-maturity securities and are reported at amortized cost. j) Inventories Inventories primarily comprise VSAT equipment, handsets and SIM cards. Inventories are valued at the lower of cost on a first in first out (‘FIFO’) basis and estimated net realizable value. Inventory costs include purchase price, freight inwards and transit insurance charges. k) Property and equipment Property and equipment are stated at historical cost, net of accumulated depreciation. All direct costs relating to the acquisition and installation of property and equipment are capitalized. Depreciation is recorded on a straight-line basis over the estimated useful lives of the assets as follows:

Assets individually costing Rs. 5 or less are fully depreciated over a period of 12 months from the date placed in service.

Land is not depreciated. The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at each balance sheet date.

Gains and losses arising from retirement or disposal of property and equipment are determined as the difference between the net disposal proceeds and the carrying amount of the asset and are recognized in the consolidated statement of operations on the date of retirement and disposal. Costs of additions and substantial improvements to property and equipment are capitalized. The costs of maintenance and repairs of property and equipment are charged to operating expenses. l) Asset retirement obligations Asset retirement obligations associated with the Group’s wireless and wireline services cell sites, switch sites, retail, and administrative location operating leases are subject to the provisions of FAS No. 143 “Accounting for Asset Retirement Obligations”. The lease agreements entered into by the Group may contain clauses requiring restoration of the leased site at the end of the lease term and therefore create asset retirement obligations. The Group records the fair value of a liability for an asset retirement obligation

- 15 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

- 16 -

in the period in which it is incurred and capitalizes the cost by increasing the carrying amount of the related long-lived asset. Over time, the liability is accreted to its present value each period, and the capitalized cost is depreciated over the estimated useful life of the related asset. Upon settlement of the liability, the Group either settles the obligation for its recorded amount or incurs a gain or loss upon settlement m) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of the Group’s share of net identifiable assets of the acquired subsidiary or jointly controlled entity at the date of acquisition. Goodwill on acquisition of subsidiaries is disclosed separately. Goodwill arising on accounting for jointly controlled entities or entities in which the Group exercises significant influence is included in the investments in the related associates/jointly controlled entities. Goodwill is stated at cost less accumulated amortization and impairment losses, if any. Effective April 1, 2002, the Group adopted provisions of FAS No. 142, “Goodwill and Other Intangible Assets” (‘FAS 142’) which sets forth the accounting for goodwill and intangible assets subsequent to their acquisition. FAS 142 requires that goodwill and indefinite-lived intangible assets be allocated to the reporting unit level, which the Group defines as each circle. FAS 142 also prohibits the amortization of goodwill and indefinite-lived intangible assets upon adoption, but requires that they be tested for impairment at least annually, or more frequently as warranted, at the reporting unit level. The goodwill impairment test under FAS 142 is performed in two phases. The first step of the impairment test, used to identify potential impairment, compares the fair value of the reporting unit with its carrying amount, including goodwill. If the carrying amount of the reporting unit exceeds its fair value, goodwill of the reporting unit is considered impaired, and step two of the impairment test must be performed. The second step of the impairment test quantifies the amount of the impairment loss by comparing the carrying amount of goodwill to the implied fair value. An impairment loss is recorded to the extent the carrying amount of goodwill exceeds its implied fair value.

n) Other intangible assets Other intangible assets comprising enterprise resource planning software, bandwidth capacities, brands, customer relationships, distribution networks, licenses and noncompete clauses, are capitalized at the Group’s share of respective fair values on the date of acquisition. The methodologies used for valuation of these intangibles assets are as follows:

- Software is capitalized at the amounts paid to acquire the respective license for use and is amortized over the period of the license, not exceeding three years. - Bandwidth capacities are capitalized at the amounts paid to acquire the capacities and are amortized over the period of the agreement subject to a maximum of 15 years. - Brands are valued using the royalty relief approach, which calculates the fair value of the brand based on the hypothetical future royalties expected to be earned on leasing the brand. The approach assumes that if the brands had to be licensed from a third party there would be a royalty charge based on the revenues net of marketing expense, which would be levied for the privilege of using the brands. Brands are amortized on a straight-line basis over the period of their expected benefits, not exceeding the life of the licenses and are written off in their entirety when no longer in use. - Customer relationships reflect the estimated fair value of the customer accounts acquired from which the Group can expect to derive future benefits over the estimated life of such relationships. The customer relationships are amortized on a circle by circle basis over the estimated useful life of 40 to 52 months for VSAT customers as of March 31, 2007 (March 31, 2006 – 40 to 52 months and March 31, 2005 – 52 months). The customer relationships for mobile customers have been fully amortised by March 31, 2006 (March 31, 2005 - 16 months). - Distribution networks reflect the fair value of the estimated benefit which the Group can expect to accrue from the customers to be acquired using the acquisition date distribution network

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

over the next three years from the acquisition date. The distribution networks intangible assets are amortized over an estimated useful life of three years. - The fair values of licenses are valued using the market value approach, which determines the value of the assets by comparing the value to publicly traded comparables in similar lines of business. The approach assumes that the conditions and prospects of comparables in similar lines of business depend on universal factors affecting market conditions. The entry fee for the new operators is considered as an indicator of the market value of the license. The licenses are amortized over the remaining license period. - Noncompete clauses included in the agreements for the purchases of acquired entities are fair valued based on the actual and projected business plans. Under the agreements, the sellers and their affiliates shall not be in the business of the same operations, directly or indirectly for the period specified in the agreements. These are amortized on a straight-line basis over the remaining period of license.

Amortization of intangible assets is disclosed as part of cost of services and selling, general and administrative expenses in the consolidated statement of operations. o) Foreign currency transactions Monetary assets and liabilities denominated in foreign currencies are expressed in the functional currency Indian Rupees at the rates of exchange in effect at the balance sheet date. Transactions in foreign currencies are recorded at rates ruling on the transaction dates. Gains or losses resulting from foreign currency transactions are included in the consolidated statement of operations. p) Operating leases Lease payments under operating leases are recognized as an expense on a straight-line basis over the lease term. q) Capital leases

(i) Lessee accounting

Assets acquired under capital leases are capitalized as assets by the Group at the lower of the fair value of the leased property or the present value of the related lease payments or where applicable, the estimated fair value of such assets. Amortization of leased assets is computed on straight line basis over the useful life of the assets. Amortization charge for capital leases is included in depreciation expense.

(ii) Lessor accounting

Assets leased to others under capital leases are recognized as receivables at an amount equal to the net investment in the leased assets. The finance income is recognized based on the periodic rate of return on the net investment of the lessor outstanding in respect of the capital lease.

r) Impairment of long – lived assets and intangible assets The Group reviews its long-lived assets, including identifiable intangible assets with finite lives, for impairment whenever events or changes in business circumstances indicate that the carrying amount of assets may not be fully recoverable. Such circumstances include, though are not limited to, significant or sustained declines in revenues or earnings and material adverse changes in the economic climate. For assets that the Group intends to hold for use, if the total of the expected future undiscounted cash flows produced by the assets or asset Group is less than the carrying amount of the assets, a loss is recognized for the difference between the fair value and carrying value of the assets. For assets the Group intends to dispose of by sale, a loss is recognized for the amount by which the estimated fair value less cost to sell is

- 17 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

- 18 -

less than the carrying value of the assets. Fair value is determined based on quoted market prices, if available, or other valuation techniques including discounted future net cash flows. s) Revenue recognition

(i) Service revenues

Service revenues include amounts invoiced for usage charges, fixed monthly subscription charges and VSAT/ internet usage charges, roaming charges, activation fees, processing fees and fees for value added services (‘VAS’). Service revenues also include revenues associated with access and interconnection for usage of the telephone network of other operator for local, domestic long distance and international calls.

Service revenues are recognized as the services are rendered and are stated net of discounts and taxes. Revenues from pre-paid cards are recognized based on actual usage. Activation revenue and related activation costs, not exceeding the activation revenue, are deferred and amortized over their estimated useful life of 12 to 74 months for the year ended March 31, 2007 (March 31, 2006 – 31 to 69 months and March 31, 2005 – 29 to 50 months), which is consistent with the estimated churn of the related customers on a circle by circle basis. The excess of activation costs over activation revenue, if any, is expensed as incurred. Subscriber acquisition costs are expensed as incurred. On introduction of new prepaid products, processing fees on recharge coupons is being recognized over the estimated customer relationship period or coupon validity period, whichever is lower. Service revenues from the internet and VSAT business comprise revenues from registration, installation and provision of internet and satellite services. Registration fee and installation charges are deferred and amortized over the expected customer relationship period. Service revenue is recognized from the date of satisfactory installation of equipment and software at the customer site and provisioning of internet and satellite services. Revenue from prepaid dialup packs is recognized on an actual usage basis and is net of sales returns and discounts. Revenues from national and international long distance operations comprise revenue from provision of voice services which are recognized on completion of services while revenue from provision of bandwidth services is recognized over the period of use. Revenue is stated net of discounts and waivers. Unbilled receivables represent revenues recognized from the bill cycle date to the end of each month. These are billed in subsequent periods based on the terms of the billing plans. Unearned revenue includes amounts in respect of monthly rentals billed in advance and amounts received in advance on pre-paid cards. The related services are expected to be performed within the next operating cycle. (ii) Equipment sales Equipment sales consist primarily of revenues from sale of VSAT and internet equipment (hardware), SIM cards, fixed line service handsets and related accessories to subscribers. Equipment sales are treated as activation revenue and are deferred and amortized over the customer relationship period.

(iii) Multiple element arrangements

The Group has entered into certain multiple-element revenue arrangements where it recognizes revenue in accordance with the SEC Staff Accounting Bulletin No. 104 “Revenue Recognition”. These arrangements involve the delivery or performance of multiple products, services or rights to use assets including VSAT and internet equipment, internet and satellite services, indefeasible right to

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

use and hardware and equipment maintenance. The Group evaluates all deliverables in an arrangement to determine whether they represent separate units of accounting at the inception of the arrangement in accordance with EITF 00-21 “Revenue Arrangements with Multiple Deliverables”. Objective and reliable evidence of fair value is determined using the price of a deliverable when it is regularly sold separately. The Group has determined that objective and reliable evidence of fair value does not exist for undelivered items in arrangements involving the bundling of sales of VSAT and internet equipment with provision of internet and satellite services. Accordingly, as highlighted in Note 2 (s)(ii) above, equipment sales for these arrangements are deferred and amortized over the customer relationship period. The arrangement consideration allocated to delivered items that do not qualify as separate units of accounting are combined with the other applicable undelivered items within the arrangement. The Group then recognizes revenue for those combined deliverables as a single unit of accounting. For other arrangements, the Group has established that objective and reliable evidence of fair value for all units of accounting in the arrangement exists. Accordingly, the arrangement consideration is allocated to the separate units of accounting based on their relative fair values. Revenue recognized by the Group on a delivered item is limited to the amount that is not contingent upon the delivery of additional items or conditional on meeting other specified performance criteria.

t) Indefeasible right to use (‘IRU’)

Fibre and duct are sold as part of the operations of Group’s Enterprise Services Carriers business. The Group has decided to view these as integral equipment. Under the agreements, title is not transferred to the lessee. The transactions are therefore recorded as operating lease agreements. Direct expenditures incurred in connection with agreements are capitalized and written off over the term of the agreement. The contracted sales price is chiefly paid in advance and is recognized as revenue during the period of the agreement. IRU sales not recognized in the consolidated statement of operations, net of the amount recognizable within one year is recorded as unearned income in noncurrent liabilities and the amount recognizable within one year as unearned income in current liabilities.

u) License fees

(i) Licenses signed prior to NTP-99

Annual license fees incurred by the Group under the old license fee regime until the date of migration to NTP - 99, i.e. July 31, 1999 and revenue-share fees from the date of migration to NTP – 99 were expensed as incurred. However, the Group’s share of licenses acquired under business combinations during the old license regime, prior to July 31, 1999, were accounted for at their respective fair values as at the date of acquisition and were amortized on a straight-line basis over the remaining period of the license from the date of acquisition of respective circles. Upon the migration to NTP - 99, the remaining unamortized cost of such licenses acquired had been carried over to form a part of the new cost basis for the licenses signed under NTP - 99. Amortization of licenses is disclosed as part of depreciation and amortization in the consolidated statement of operations. (ii) Licenses signed under NTP - 99

The license agreements signed/awarded under NTP - 99 stipulated the payments of: 1) a one time fee termed as ‘license entry fee’ to obtain the right to operate services; and 2) annual usage charges on the basis of the percentage of revenues i.e. ‘revenue share’. The one time entry fee was not required for licenses obtained under the old license fee regime which were migrated to NTP -99 licenses as noted in Note 2 u(i) above.

- 19 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

License entry fees were recognized as an intangible asset and measured initially at cost. After initial recognition, license entry fees were measured at cost less accumulated amortization and any other impairment losses. License entry fees were amortized on a straight-line basis over the period of the license from the date of commencement of commercial operations in the respective circles. The Group’s share of licenses acquired under business combinations arising after the ‘applicability’ of NTP - 99 were accounted for at their respective fair values as at the date of acquisition and were amortized on a straight line basis over the remaining period of the license. Amortization of license entry fees was disclosed as part of depreciation and amortization in the consolidated statement of operations. The revenue-share fee was computed on the basis of the AGR and was expensed as incurred. (iii) UASL and license fees The Group during the year ended March 31, 2005 migrated its cellular mobile licenses in 15 circles to UASL after obtaining the necessary approvals from the DoT. Upon the migration of the NTP–99 licenses to UASL, the remaining unamortized cost of the NTP-99 licenses was carried over to form the carrying value of the UASL. As a consequence of the migration of the licenses, the Group reviewed its licenses for impairment in accordance with Note 2 (r) above. The undiscounted cash flow analysis indicated that the carrying amount of the licenses would be recoverable and accordingly, no impairment existed and no loss was recognized.

UASL entry fees were recognized as an intangible asset and measured initially at cost. After initial recognition, license entry fees were measured at cost less accumulated amortization and any other impairment losses. License entry fees were amortized on a straight-line basis over the period of the license from the date of commencement of commercial operations in the respective circles.

v) Borrowing costs

Capitalized interest The interest cost incurred for funding a qualifying asset during the construction period is capitalized based on actual investment in the asset at the average interest rate. The capitalized interest is included in the cost of the relevant asset and is depreciated over the estimated useful life of the asset. Debt issue expenses

The Group amortizes debt issue expenses over the term of the related borrowing based on the effective interest method.

w) Stock based compensation

The Group uses a fair value based method of accounting for stock-based compensation provided to our employees in accordance with FAS No. 123, “Accounting for Stock-Based Compensation” (‘FAS 123’). In December 2004, the FASB issued the revised FAS No. 123, "Share-Based Payment" (‘FAS 123(R)’), which is a revision of FAS 123 and supersedes APB Opinion No. 25, “Accounting for Stock Issued to Employees”. FAS 123(R) requires all stock-based payments to employees including grants of employee stock options, to be valued at fair value on the date of grant, and to be expensed over the applicable vesting period and contains certain other amendments to existing guidance. Further, in March 2005, the SEC issued Staff Accounting Bulletin 107, “Share Based Payment” (‘SAB 107’) providing guidance on the application of FAS 123 (R). The initial adoption of this statement did not have a material impact on the Group’s results of operations, financial position or cash flows. Stock options issued are valued using Black Scholes option-pricing model and the fair value is recognized as an expense over the period in which the options vest using the graded vesting method. The expected volatility assumption is based on historical data.

- 20 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

- 21 -

x) Employee benefits

(i) Gratuity Plan

In accordance with Indian law, the Group provides for gratuity obligations through a defined benefit retirement plan (the ‘Gratuity Plan’) covering all employees. Under the Gratuity Plan, a lump sum payment to vested employees is made at retirement or termination of employment based on the respective employee’s salary and the number of years of employment with the Group. The Group provides for the Plan based on actuarial valuations in accordance with FAS No. 87, “Employers’ Accounting for Pensions”. The Group makes annual contributions to the Life Insurance Corporation of India (‘LIC’) for the gratuity plan in respect of employees at certain circles.

(ii) Superannuation Plan

Some employees of the Group are entitled to superannuation, a defined contribution plan (the ‘Superannuation Plan’) which is administered through an insurance scheme. Superannuation benefits are recorded as an expense as incurred.

(iii) Provident Fund and employees’ state insurance schemes

In accordance with Indian law, all employees of the Group are entitled to receive benefits under the Provident Fund, which is a defined contribution plan. Both the employees and the employer make monthly contributions to the plan at a predetermined rate (presently 12.0%) of the employees’ basic salary. These contributions are made to the fund administered and managed by the GoI. In addition some employees of the Group are covered under the employees’ state insurance schemes, which are also defined contribution schemes recognized by the Indian Revenue Authorities, and are administered through the GoI.

The Group’s contributions to both these schemes are expensed in the consolidated statement of operations. The Group has no further obligations under these plans beyond its monthly contributions. (iv) Compensated absences

The employees of the Group are entitled to compensated absences based on the unavailed leave balance and the last drawn salary of the respective employees. The Group has provided for the liability on account of compensated absences in accordance with FAS No. 43, “Accounting for Compensated Absences”.

y) Advertising costs

The advertising costs are expensed as incurred. z) Legal costs

Legal costs expected to be incurred in connection with a loss contingency are expensed as and when incurred.

aa) Income taxes

In accordance with the provisions of FAS 109, “Accounting for Income Taxes”, income taxes for the years ended March 31, 2005, 2006 and 2007 are accounted for under the asset and liability method. Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of assets and liabilities and their respective tax bases and operating loss carry-forwards. Deferred tax assets and liabilities are

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the consolidated statement of operations in the period in which the change is enacted. Based on management's judgment, the measurement of deferred tax assets is reduced, if necessary, by a valuation allowance for any tax benefits for which it is more likely than not that some portion or all of such benefits will not be realized.

bb) Preoperating costs

Preoperating costs represent certain marketing and administrative expenses incurred prior to the commencement of commercial operations of the new circles. These costs are expensed as incurred.

cc) Derivative financial instruments

The Group enters into derivative instruments, including interest rate swaps and foreign currency forward contracts, to manage interest rate movements of its debt obligations and foreign currency exposures related to the import of equipment used in operations and its foreign currency denominated debt instruments.

FAS No. 133, ‘‘Accounting for Derivative Instruments and Hedging Activities’’ (‘FAS 133’), requires that all derivative instruments be recorded on the balance sheet at their fair value. Changes in the fair value of derivatives are recorded each period in current earnings or in other comprehensive income, depending on whether a derivative is designated as part of a hedging relationship and, if it is, depending on the type of hedging relationship.

None of the Group’s derivative contracts qualified for hedge accounting pursuant to FAS 133. As such, these contracts are accounted for by adjusting the carrying amount of the contracts to market at each period end and recognizing any gain or loss in earnings. Market value of the Group’s interest rate and foreign currency derivative instruments are determined based on quoted market prices, traded exchange market prices or broker quotes and represent the estimated amounts that the Group would pay or receive to terminate the contracts.

The Group occasionally enters into contracts that do not in their entirety meet the definition of a derivative instrument that may contain “embedded” derivative instruments – implicit or explicit terms that affect some or all of the cash flow or the value of other exchanges required by the contract in a manner similar to a derivative instrument. The Group assesses whether the economic characteristics and risks of the embedded derivative are clearly and closely related to the economic characteristics and risks of the remaining component of the host contract and whether a separate, non-embedded instrument with the same terms as the embedded instrument would meet the definition of a derivative instrument. When it is determined that (1) the embedded derivative possesses economic characteristics and risks that are not clearly and closely related to the economic characteristics and risks of the host contract and (2) a separate, stand-alone instrument with the same terms would qualify as a derivative instrument, the embedded derivative is separated from the host contract, carried at fair value as a trading or non-hedging derivative instrument.

dd) Earnings per share

In accordance with FAS 128, “Earnings Per Share”, basic earnings per equity share is computed using the weighted average number of equity shares outstanding during the period. Diluted earnings per equity share is computed using the weighted average number of common and dilutive common equivalent equity shares outstanding during the period including FCCBs, OCRDs and ESOP (using the treasury stock method for options), except where the result would be anti-dilutive.

- 22 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

- 23 -

ee) Recent accounting pronouncements

Recently issued accounting pronouncements

In February 2007, the FASB issued FAS No. 159, "The Fair Value Option for Financial Assets and Financial Liabilities" (‘FAS 159’). FAS 159 permits entities to choose to measure many financial instruments and certain other items at fair value that are not currently required to be measured at fair value. The objective is to improve financial reporting by providing entities with the opportunity to mitigate volatility in reported earnings caused by measuring related assets and liabilities differently without having to apply complex hedge accounting provisions. FAS 159 is expected to expand the use of fair value measurement, which is consistent with the Board's long-term measurement objectives for accounting for financial instruments. The provisions of FAS 159 will be applied prospectively to fair value measurements and disclosures beginning in the first quarter of 2008 (i.e. from April 1, 2008). The Group is currently assessing the impact of the adoption of this Statement on its consolidated financial statements. In September 2006, the FASB issued FAS No. 157, "Fair Value Measurements" (FAS 157). This Statement defines fair value, establishes a framework for measuring fair value in generally accepted accounting principles, and expands disclosures about fair value measurements; however, it does not require any new fair value measurements. The provisions of FAS 157 will be applied prospectively to fair value measurements and disclosures beginning in the first quarter of 2008 (i.e. from April 1, 2008). The Group is currently assessing the impact of the adoption of this Statement on its consolidated financial statements. In June 2006, the FASB issued FASB Interpretation No. 48, "Accounting for Uncertainty in Income Taxes—an interpretation of FASB Statement No. 109" (FIN 48). FIN 48 clarifies the accounting and reporting for uncertainties in income tax law. This Interpretation prescribes a comprehensive model for the financial statement recognition, measurement, presentation and disclosure of uncertain tax positions taken or expected to be taken in income tax returns. The provisions of FIN 48 will be applied beginning in the first quarter of 2007 (i.e. from April 1, 2007), with the cumulative effect of the change in accounting principle recorded as an adjustment to retained earnings. The Group is currently assessing the impact of the adoption of this Interpretation on its consolidated financial statements. In February 2006, the FASB issued FAS No. 155, "Accounting for Certain Hybrid Financial Instruments—an amendment of FASB Statements No. 133 and 140", (FAS 155), to permit fair value remeasurement for any hybrid financial instrument that contains an embedded derivative that otherwise would require bifurcation in accordance with the provisions of FAS No. 133, “Accounting for Derivative Instruments and Hedging Activities." The provisions of FAS 155 will be applied beginning in the first quarter of 2007 (i.e. from April 1, 2007). The adoption of this Statement is not expected to have a material effect on the Group’s consolidated financial statements.

Recently adopted accounting pronouncements In September 2006, the FASB issued FAS No. 158, "Employers’ Accounting for Defined Benefit Pension and Other Postretirement Benefit Plans" (FAS 158). This Statement requires companies to recognize the over-funded or under-funded status of a defined benefit postretirement plan as an

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

asset or liability in its statement of financial position. The Group applied FAS 158 as at March 31, 2007, consequent to which there has been no impact on the financial statements. In May 2005, the FASB issued FAS No. 154, "Accounting Changes and Error Corrections-a replacement of APB Opinion No. 20 and FASB Statement No. 3" (FAS 154). This Statement replaces APB Opinion No. 20, "Accounting Changes," and FASB Statement No. 3, "Reporting Accounting Changes in Interim Financial Statements." This Statement requires retrospective application to prior periods' financial statements for changes in accounting principle, unless it is impractical to determine either the period-specific effects or the cumulative effect of the change. FAS 154 also requires that a change in depreciation, amortization, or depletion method for long, non-financial assets be accounted for as a change in accounting estimate effected by a change in accounting principle. The Group adopted FAS 154 with effect from April 1, 2006 for accounting changes and corrections of errors made after the adoption date. The adoption of the provisions of FAS 154 did not have an impact on the Group's consolidated financial statements.

In September 2006, the Securities and Exchange Commission (‘SEC’) staff issued Staff Accounting Bulletin No. 108, "Considering the Effects of Prior Year Misstatements when Quantifying Misstatements in Current Year Financial Statements" (‘SAB 108’). SAB 108 provides guidance on how prior year misstatements should be taken into consideration when quantifying misstatements in current year financial statements for purposes of determining whether the current year’s financial statements are materially misstated. The provisions of SAB 108 are required to be applied by registrants in their annual financial statements covering fiscal years ending on or before November 15, 2007. The Group has adopted SAB 108 for the fiscal year ending March 31, 2007. The adoption of the provisions of SAB 108 did not have an impact on the Group’s consolidated financial statements. ff) Reclassification Certain items previously reported in specific captions of the consolidated financial statements have been reclassified to conform to the current year’s presentation.

- 24 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

3. Business Combinations

(i) The Group entered into a Share Purchase Agreement with Max India Limited to acquire and assume its 100% stake in SBEL on February 1, 2005, in order to provide a strategic fit to the Group's existing VSAT and broadband infrastructure and also to its Enterprise Services Corporate business. The Group obtained control over SBEL and its wholly owned subsidiary BBL on February 1, 2005 when the majority shareholding of 51% was transferred to the Group. The Group has consolidated SBEL and BBL from that date. The balance 49% stake was transferred to the Group on April 16, 2005. (ii) During the year ended March 31, 2005, the Group entered into a Share Purchase Agreement with Shyam to acquire and assume its 67.5% joint venture interest in Hexacom on May 7, 2004, in order to expand its mobile service operation in Rajasthan and North East circles. Since the Group did not have full control over operation and management of Hexacom, under EITF 96-16, this precluded consolidation of Hexacom by Bharti Airtel and as such, the equity method was applied to the investment in Hexacom. In September 2004, the Group obtained full operational and management control of Hexacom and has consolidated Hexacom since then. On October 7, 2004, the Group acquired an additional 1% equity interest in Hexacom from Al Ghanim. (iii) Further, on the merger of Bharti Cellular Limited (‘BCL’) and BIL with Bharti Airtel on June 9, 2005, the shares of Bharti Airtel were issued to DSS Enterprises Private Limited (“DSS”), the minority shareholders in BCL and consequently, the excess of fair value of shares issued to DSS over the fair value of net assets of BCL was recognized as goodwill which amounted to Rs. 359,197. (iv) During the year ended March 31, 2007, Bharti Airtel acquired additional shares in Hexacom being the unsubscribed portion by the other existing shareholders for an aggregate consideration of Rs. 18,750, pursuant to a rights issue offer, thereby increasing its stake from 68.50% to 68.89%. Consequently, the excess of purchase consideration over its share of net assets acquired of Rs. 982 was recognized as goodwill. The assets and liabilities acquired as a result of above business combinations were recorded at fair values, with the excess of the purchase consideration over fair value of the net assets acquired recorded as goodwill. The following table summarizes the Group’s share of the estimated fair values of the assets acquired and liabilities assumed at the date of acquisition during the years ended March 31, 2005 and 2006:

- 25 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

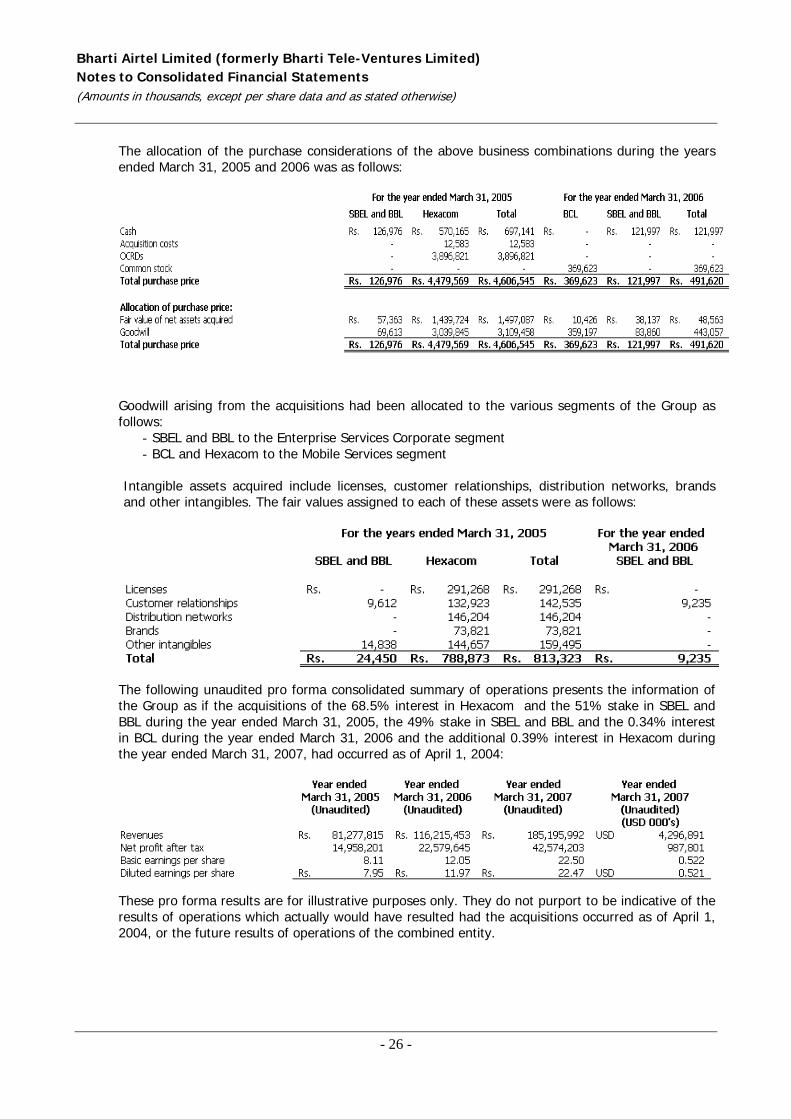

The allocation of the purchase considerations of the above business combinations during the years ended March 31, 2005 and 2006 was as follows:

Goodwill arising from the acquisitions had been allocated to the various segments of the Group as follows:

- SBEL and BBL to the Enterprise Services Corporate segment - BCL and Hexacom to the Mobile Services segment

Intangible assets acquired include licenses, customer relationships, distribution networks, brands and other intangibles. The fair values assigned to each of these assets were as follows:

The following unaudited pro forma consolidated summary of operations presents the information of the Group as if the acquisitions of the 68.5% interest in Hexacom and the 51% stake in SBEL and BBL during the year ended March 31, 2005, the 49% stake in SBEL and BBL and the 0.34% interest in BCL during the year ended March 31, 2006 and the additional 0.39% interest in Hexacom during the year ended March 31, 2007, had occurred as of April 1, 2004:

These pro forma results are for illustrative purposes only. They do not purport to be indicative of the results of operations which actually would have resulted had the acquisitions occurred as of April 1, 2004, or the future results of operations of the combined entity.

- 26 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

4. Cash and cash equivalents

5. Restricted cash

6. Accounts receivable, net

The following table sets forth the movement in the allowance for bad and doubtful debts:

Concentration of credit risk with respect to trade receivables is limited due to the Group’s large number of customers.

- 27 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

7. Short term investments

Trading investments included Rs. (3,603) as of March 31, 2007 (March 31, 2006 – Rs. 8,116) of net unrealised gains/ (loss). The market values of investments were assessed on the basis of the quoted prices as of the balance sheet date.

8. Prepaid expenses and other current assets

“Others” include: (1) Advance tax (net of provision for current tax) of Rs. 1,020,093 and Rs 264,641 as of March 31, 2006 and 2007, respectively. (2) Other taxes and duties recoverable (net of provision) of Rs. 4,092,044 and Rs. 8,305,928 as of March 31, 2006 and 2007, respectively. Employee receivables principally consisted of advances given for business purposes.

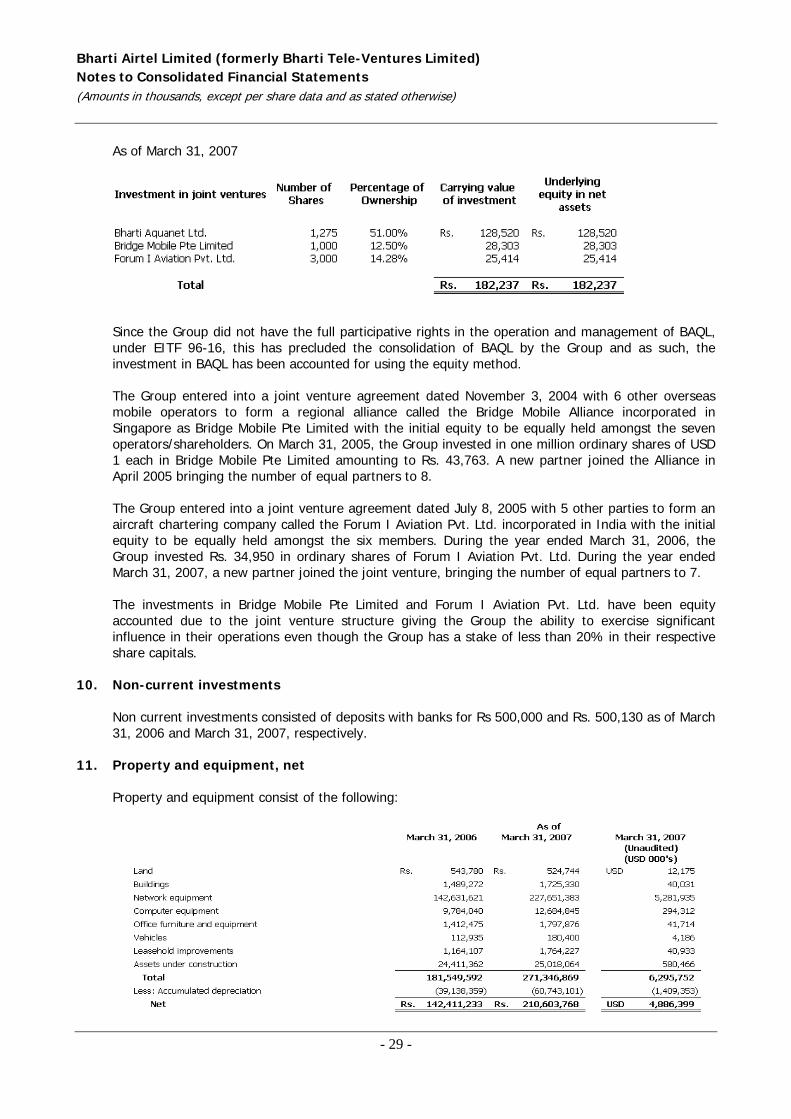

9. Investment in joint ventures

Investment in joint ventures comprises of the following as of March 31, 2006 and 2007: As of March 31, 2006

- 28 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

As of March 31, 2007

Since the Group did not have the full participative rights in the operation and management of BAQL, under EITF 96-16, this has precluded the consolidation of BAQL by the Group and as such, the investment in BAQL has been accounted for using the equity method. The Group entered into a joint venture agreement dated November 3, 2004 with 6 other overseas mobile operators to form a regional alliance called the Bridge Mobile Alliance incorporated in Singapore as Bridge Mobile Pte Limited with the initial equity to be equally held amongst the seven operators/shareholders. On March 31, 2005, the Group invested in one million ordinary shares of USD 1 each in Bridge Mobile Pte Limited amounting to Rs. 43,763. A new partner joined the Alliance in April 2005 bringing the number of equal partners to 8. The Group entered into a joint venture agreement dated July 8, 2005 with 5 other parties to form an aircraft chartering company called the Forum I Aviation Pvt. Ltd. incorporated in India with the initial equity to be equally held amongst the six members. During the year ended March 31, 2006, the Group invested Rs. 34,950 in ordinary shares of Forum I Aviation Pvt. Ltd. During the year ended March 31, 2007, a new partner joined the joint venture, bringing the number of equal partners to 7. The investments in Bridge Mobile Pte Limited and Forum I Aviation Pvt. Ltd. have been equity accounted due to the joint venture structure giving the Group the ability to exercise significant influence in their operations even though the Group has a stake of less than 20% in their respective share capitals.

10. Non-current investments

Non current investments consisted of deposits with banks for Rs 500,000 and Rs. 500,130 as of March 31, 2006 and March 31, 2007, respectively.

11. Property and equipment, net

Property and equipment consist of the following:

- 29 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

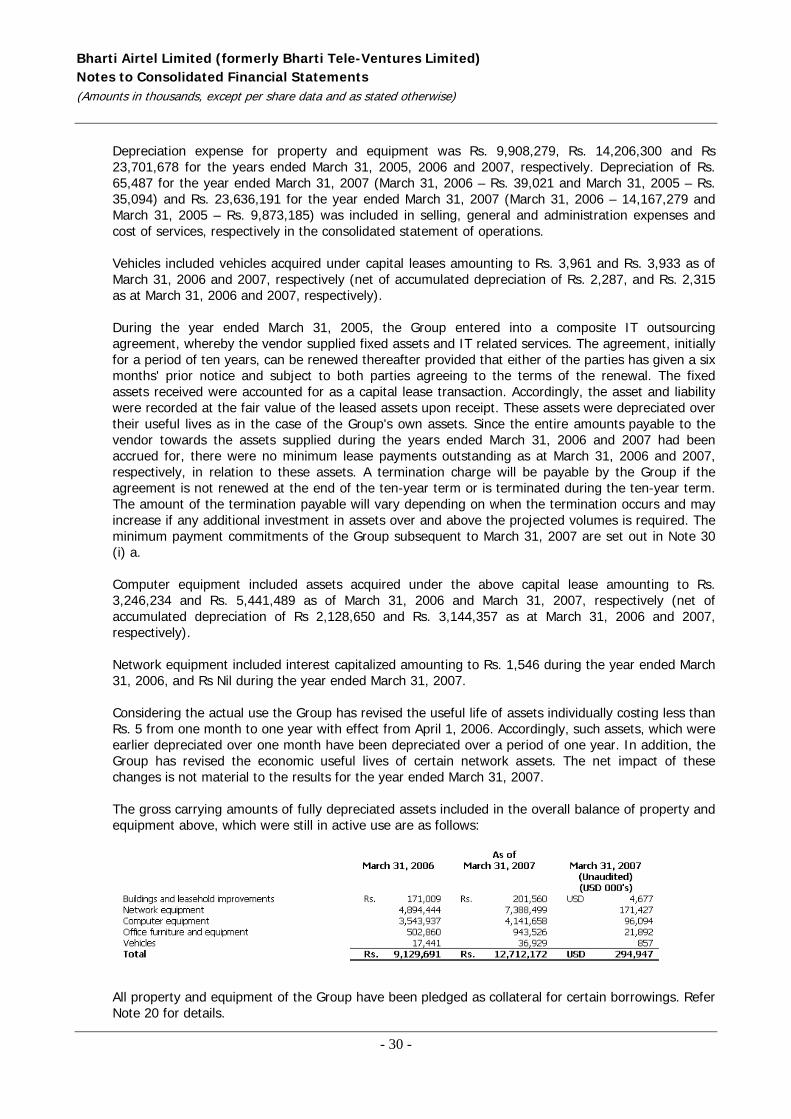

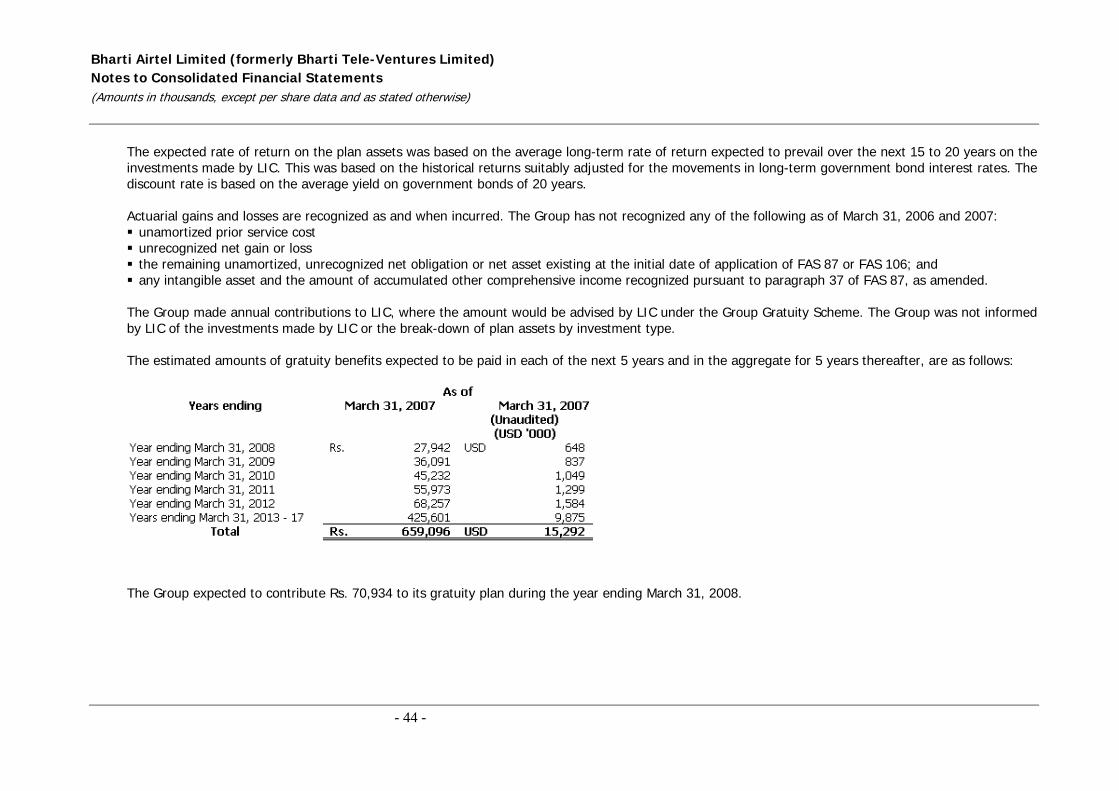

Depreciation expense for property and equipment was Rs. 9,908,279, Rs. 14,206,300 and Rs 23,701,678 for the years ended March 31, 2005, 2006 and 2007, respectively. Depreciation of Rs. 65,487 for the year ended March 31, 2007 (March 31, 2006 – Rs. 39,021 and March 31, 2005 – Rs. 35,094) and Rs. 23,636,191 for the year ended March 31, 2007 (March 31, 2006 – 14,167,279 and March 31, 2005 – Rs. 9,873,185) was included in selling, general and administration expenses and cost of services, respectively in the consolidated statement of operations. Vehicles included vehicles acquired under capital leases amounting to Rs. 3,961 and Rs. 3,933 as of March 31, 2006 and 2007, respectively (net of accumulated depreciation of Rs. 2,287, and Rs. 2,315 as at March 31, 2006 and 2007, respectively). During the year ended March 31, 2005, the Group entered into a composite IT outsourcing agreement, whereby the vendor supplied fixed assets and IT related services. The agreement, initially for a period of ten years, can be renewed thereafter provided that either of the parties has given a six months' prior notice and subject to both parties agreeing to the terms of the renewal. The fixed assets received were accounted for as a capital lease transaction. Accordingly, the asset and liability were recorded at the fair value of the leased assets upon receipt. These assets were depreciated over their useful lives as in the case of the Group's own assets. Since the entire amounts payable to the vendor towards the assets supplied during the years ended March 31, 2006 and 2007 had been accrued for, there were no minimum lease payments outstanding as at March 31, 2006 and 2007, respectively, in relation to these assets. A termination charge will be payable by the Group if the agreement is not renewed at the end of the ten-year term or is terminated during the ten-year term. The amount of the termination payable will vary depending on when the termination occurs and may increase if any additional investment in assets over and above the projected volumes is required. The minimum payment commitments of the Group subsequent to March 31, 2007 are set out in Note 30 (i) a. Computer equipment included assets acquired under the above capital lease amounting to Rs. 3,246,234 and Rs. 5,441,489 as of March 31, 2006 and March 31, 2007, respectively (net of accumulated depreciation of Rs 2,128,650 and Rs. 3,144,357 as at March 31, 2006 and 2007, respectively). Network equipment included interest capitalized amounting to Rs. 1,546 during the year ended March 31, 2006, and Rs Nil during the year ended March 31, 2007. Considering the actual use the Group has revised the useful life of assets individually costing less than Rs. 5 from one month to one year with effect from April 1, 2006. Accordingly, such assets, which were earlier depreciated over one month have been depreciated over a period of one year. In addition, the Group has revised the economic useful lives of certain network assets. The net impact of these changes is not material to the results for the year ended March 31, 2007. The gross carrying amounts of fully depreciated assets included in the overall balance of property and equipment above, which were still in active use are as follows:

All property and equipment of the Group have been pledged as collateral for certain borrowings. Refer Note 20 for details.

- 30 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

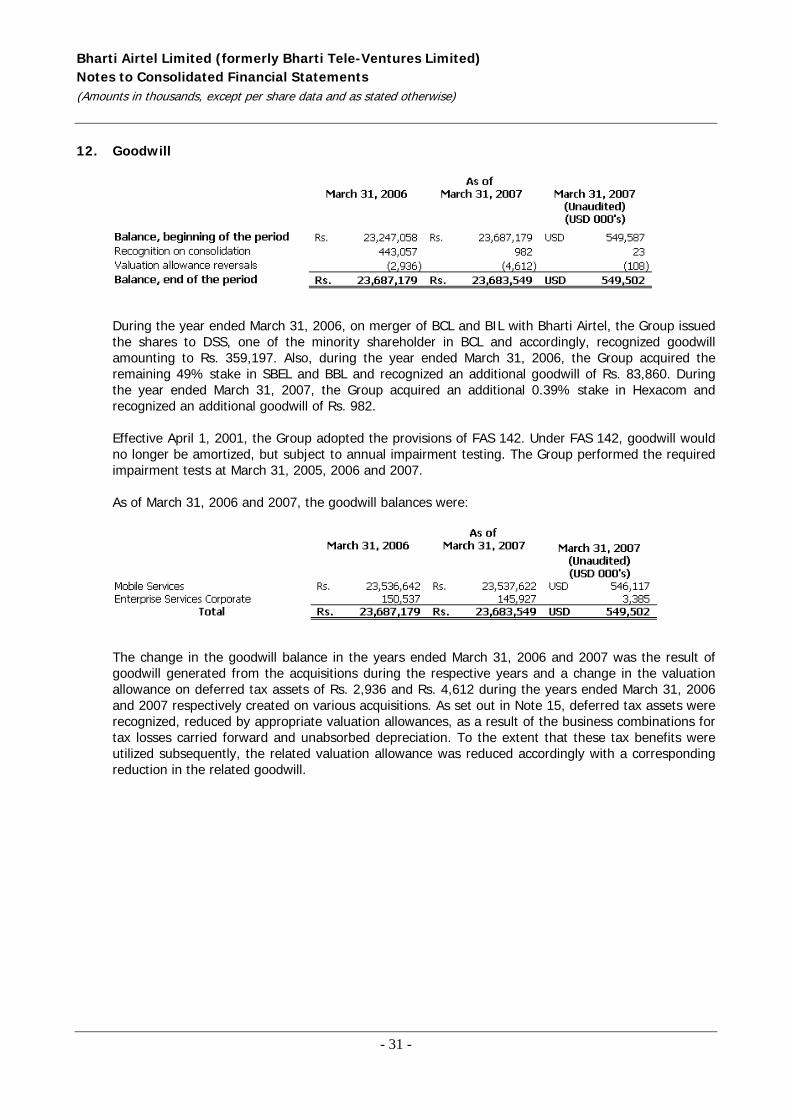

12. Goodwill

During the year ended March 31, 2006, on merger of BCL and BIL with Bharti Airtel, the Group issued the shares to DSS, one of the minority shareholder in BCL and accordingly, recognized goodwill amounting to Rs. 359,197. Also, during the year ended March 31, 2006, the Group acquired the remaining 49% stake in SBEL and BBL and recognized an additional goodwill of Rs. 83,860. During the year ended March 31, 2007, the Group acquired an additional 0.39% stake in Hexacom and recognized an additional goodwill of Rs. 982. Effective April 1, 2001, the Group adopted the provisions of FAS 142. Under FAS 142, goodwill would no longer be amortized, but subject to annual impairment testing. The Group performed the required impairment tests at March 31, 2005, 2006 and 2007. As of March 31, 2006 and 2007, the goodwill balances were:

The change in the goodwill balance in the years ended March 31, 2006 and 2007 was the result of goodwill generated from the acquisitions during the respective years and a change in the valuation allowance on deferred tax assets of Rs. 2,936 and Rs. 4,612 during the years ended March 31, 2006 and 2007 respectively created on various acquisitions. As set out in Note 15, deferred tax assets were recognized, reduced by appropriate valuation allowances, as a result of the business combinations for tax losses carried forward and unabsorbed depreciation. To the extent that these tax benefits were utilized subsequently, the related valuation allowance was reduced accordingly with a corresponding reduction in the related goodwill.

- 31 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

13. Acquired intangible assets There were no indefinite–life intangible assets. Finite–life intangible assets, including license fees and other intangible assets, comprise the following:

Licenses reflected the fair values of the licenses acquired under business combinations while license entry fees represented the one time entry fees paid for licenses granted to the Group. Licenses and license entry fees were amortized over the license period varying from 11 to 20 years on a straight line basis. Amortization expense for intangible assets was Rs. 1,433,082, Rs. 1,403,518 and Rs. 1,271,364 for the years ended March 31, 2005, 2006 and March 31, 2007, respectively. Included in selling, general and administration expenses and cost of services in the consolidated statement of operations for the year ended March 31, 2007 was amortization of Rs 82,437 (March 31, 2006 – Rs. 195,212 and March 31, 2005 – 342,290) and Rs. 1,188,927 (March 31, 2006 – Rs. 1,208,306 and March 31, 2005 – Rs. 1,090,792) respectively. The estimated aggregate amortization expense for all the intangible assets, for the next 5 years is as follows:

- 32 -

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

- 33 -

14. Employee stock compensation

In December 2004, the FASB issued FAS No. 123(R), "Share-Based Payment" (‘FAS 123(R)’), which is a revision of FAS 123 and supersedes APB Opinion No. 25, “Accounting for Stock Issued to Employees”. FAS 123(R) requires all stock-based payments to employees including grants of employee stock options, to be valued at fair value on the date of grant, and to be expensed over the applicable vesting period and contains certain other amendments to existing guidance. Further, in March 2005, the SEC issued Staff Accounting Bulletin 107, “Share Based Payment” (‘SAB 107’) providing guidance on the application of FAS 123(R).

On April 1, 2006, the Group adopted FAS 123(R) using the modified prospective application method. Upon the adoption of FAS 123(R), the Group started applying an estimated forfeiture rate to the unvested awards and the grants made after April 1, 2006 while computing the stock compensation expense, which were earlier recorded as incurred under FAS 123. Upon the adoption of FAS 123(R), the Group reclassified its deferred stock based compensation amount, as recorded in equity as of April 1, 2006 to the additional paid-in capital (‘APIC’). The related benefits of tax deductions in excess of recognized compensation expense are now reported as a financing cash flow, rather than an operating cash flow as prescribed under FAS 123.

(i) 2001 Employee Stock Option Scheme (“Scheme I”)

In 2001 the Group announced an employee stock ownership plan (‘ESOP’) that covered eligible employees and formed a Bharti Tele-Ventures Employees’ Welfare Trust (the ‘Trust’) for the implementation of the ESOP scheme. The Group allotted 1,360,000 equity shares and 80,000 equity shares of Rs 10 each on August 31, 2001 and September 28, 2001, respectively to the trust to give effect to the ESOP.

In 2001, the Group issued bonus shares in the ratio of 10 equity shares for every one equity share held as of September 30, 2001. As a result the total number of shares allotted to the Trust increased to 15,840,000 equity shares. The Trust’s accounts were consolidated with the Group’s consolidated financial statements as the Group controlled the Trust. Accordingly, the loan advanced to the Trust was eliminated and the shares allotted to the Trust (available for grant) were recorded as treasury stock and were carried in the books of the Group at cost. The grant date’s fair value of the options as determined by the Black Scholes model is being amortized over the vesting period. The Scheme I is broken up into the different plans as follows:- a. 2001 Employee Stock Option Plan (the ‘2001 Plan’)

The Group granted 11,447,307 common stock options under Scheme I, net of forfeiture through March 31, 2007. The shares were allocated by the Trust to eligible employees who received stock option grants from the Group at an exercise price of Rs. 22.50 per share representing a 50% discount to the price at which shares were issued in the Indian IPO in February 2002.

The options vest on a graded basis as follows:

For options with a vesting period of 36 months:

Bharti Airtel Limited (formerly Bharti Tele-Ventures Limited) Notes to Consolidated Financial Statements (Amounts in thousands, except per share data and as stated otherwise)

On completion of 1 year (from the effective grant date) 20% On completion of 2 years (from the effective grant date) 30% On completion of 3 years (from the effective grant date) 50% For options with a vesting period of 42 months: On completion of 1 year (from the effective grant date) 15% On completion of 1 year and 6 months (from the effective grant date) 15% On completion of 2 years and 6 months (from the effective grant date) 30% On completion of 3 years and 6 months (from the effective grant date) 40% For options with a vesting period of 48 months: On completion of 1 year (from the effective grant date) 10% On completion of 2 years (from the effective grant date) 20% On completion of 3 years (from the effective grant date) 30% On completion of 4 years (from the effective grant date) 40%