56

www.openinnovate.co.uk/bib

| Date post: | 24-Mar-2016 |

| Category: |

Documents |

| Upload: | pedro-parraguez |

| View: | 215 times |

| Download: | 0 times |

www.openinnovate.co.uk/bib

Presentation Roadmap

-The Problem-The Opportunity

-Our Proposal-The Business Model

-Our Team-Marketing Analysis

-Financials-The Road Ahead

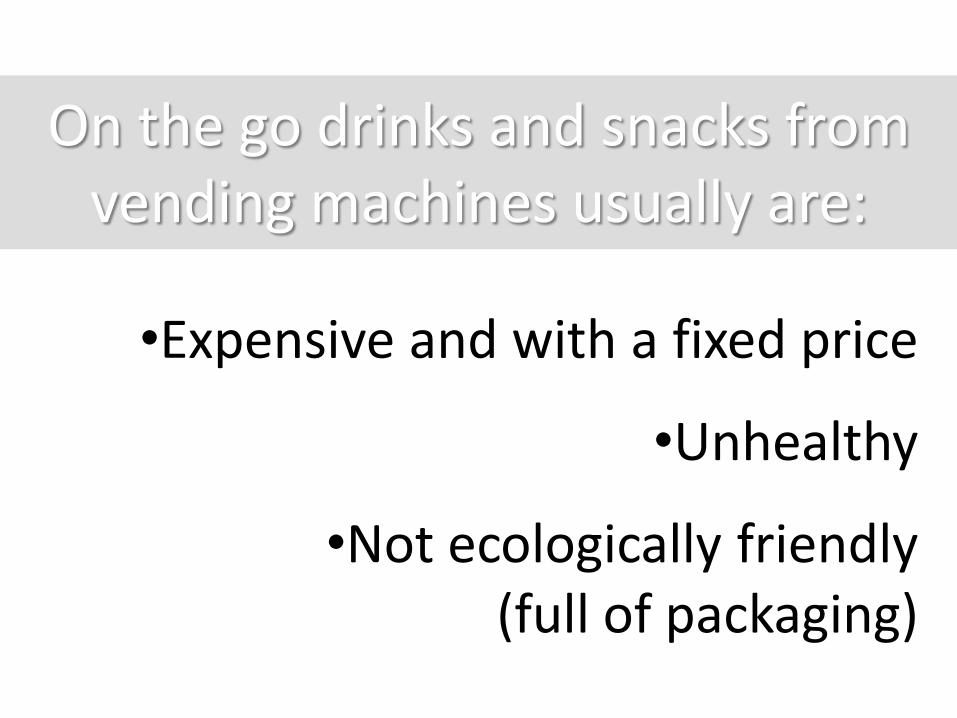

The Problem

On the go drinks and snacks from vending machines usually are:

•Expensive and with a fixed price

•Unhealthy

•Not ecologically friendly(full of packaging)

This has led to the stagnation of the industry

The Opportunity

Changes in customer wants and technology, create new spaces for innovation

Customers are:

•Looking for healthier snack alternatives

•More aware of their environmental impact

•Demanding more value for money

The technology is cheaper than ever, nevertheless, few innovations have been

introduced in vending machines

Our Proposal

Bringing this experience

And these quality snacks...

To the world of vending machines

Designing the ideal vending machine...

To create the ideal vending machine we need to combine

creatively:

•The principle of current bulk candy vending machines

•The “post-mix” drink dispensing mechanism

•The “pay per litre” system of petrol pumps

+ +

Combination of...

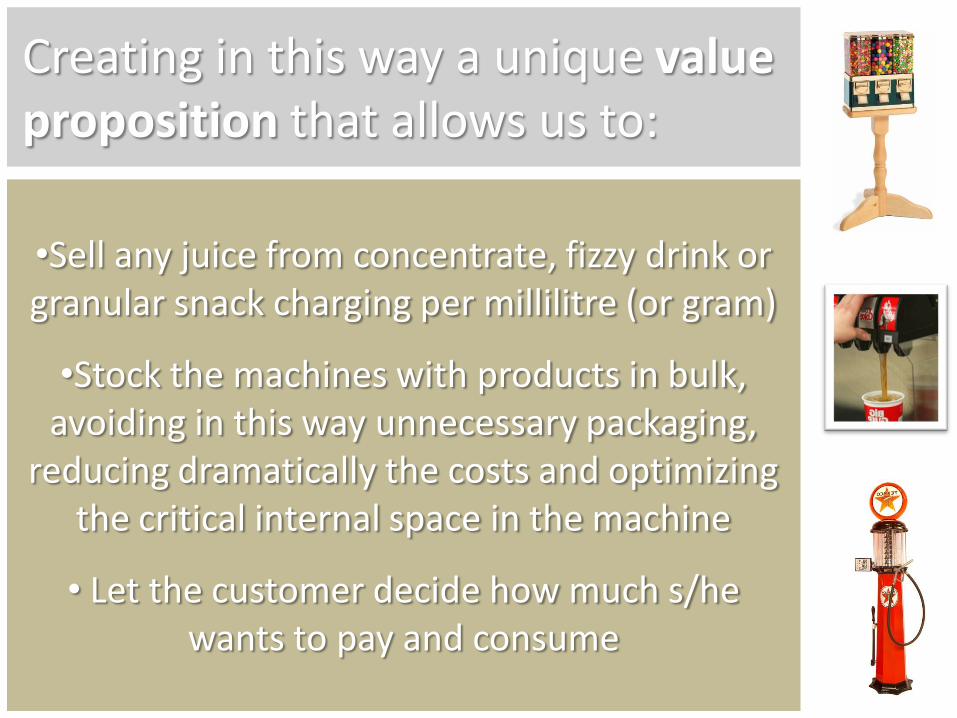

Creating in this way a unique value proposition that allows us to:

•Sell any juice from concentrate, fizzy drink or granular snack charging per millilitre (or gram)

•Stock the machines with products in bulk, avoiding in this way unnecessary packaging,

reducing dramatically the costs and optimizing the critical internal space in the machine

• Let the customer decide how much s/he wants to pay and consume

Some of these products have never been sold in bulk vending machines

(Usually they just stock sweets and spherical bubble gums because of their simplicity)

We allow nuts and dried fruits to be cheaper and more convenient than

ever...

But also sexier...

Upgrading their perceived value and consumer awareness

And this also applies for drinks in “bulk”

***Note that these are regular post-mix machines, not automated coin vending machines, our proposal is similar in format but different in functionality***

Some of the most important features of the machine are:

For drinks:There will be a selection of 3 Cup sizes with a cap and straw. A reusable optional plastic mug will be on sale. The customer will be able to use their own mug if wanted. There is a sensor to avoid overfilling of the container.

Some of the most important features of the machine are:

For drinks (cont):Internally the machine holds one big body of refrigerated water (and the juice and/or soda concentrates). This allows us to stock hundreds of litres at once, making it extremely cost efficient compared with cans or bottles.

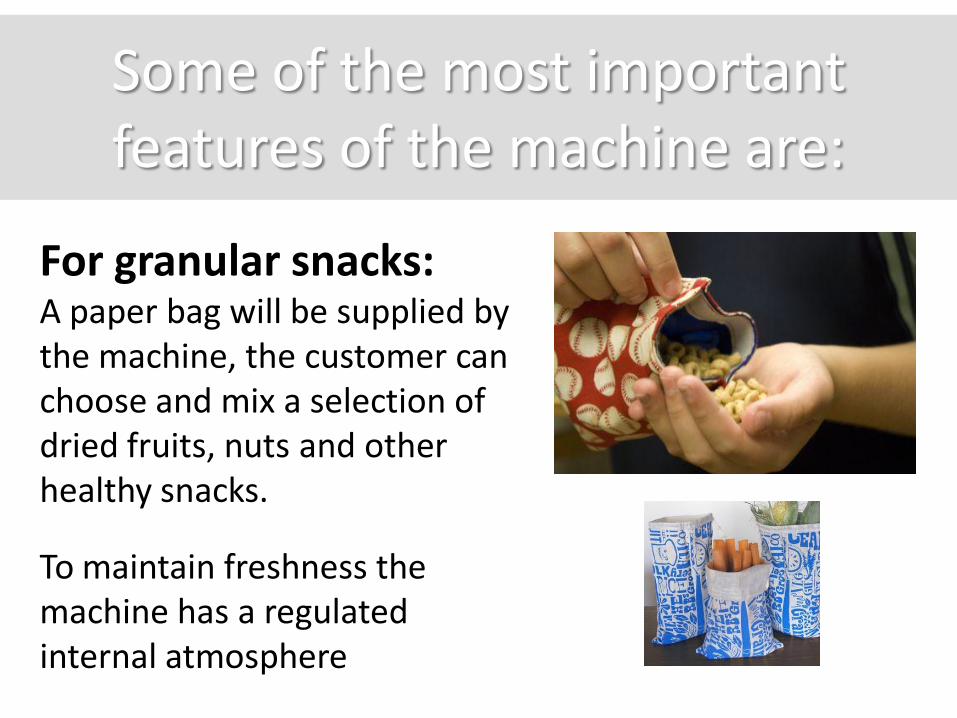

Some of the most important features of the machine are:

For granular snacks:A paper bag will be supplied by the machine, the customer can choose and mix a selection of dried fruits, nuts and other healthy snacks.

To maintain freshness the machine has a regulated internal atmosphere

Key Differentiation and Advantages

Spare change?

What makes us unique is that our customers can buy with any amount of

cash that they choose.

For example, if £1.00 buys 100 grams £1.10 can buy 110 grams and £0.90 can

buy 90 grams

Why is this so important?

For the customer:It is more convenient. S/he can always buy something starting from as low as 35p. If the customer has spare change, they can spend it and get a little more, making good use of the often useless low denomination coins (1p, 5p, 10p...)

Why is this so important?For our business: This can increase substantially the revenues in 2 ways:

-We are able to sell to more people because they can buy less grams/millilitres if they don’t have enough cash

-People with additional spare change can spend it to get more of a product.

In economic terms this means that we can extract more value under the demand curve.

Eco-Friendly

•We only use recyclable packaging and as little as possible.

•Our transport costs are substantially lower; each machine requires less restocking and there is no wasted space between the products.

•We are energy efficient, it is easier to keep the machines cold and insulated

Business Model

Design and prototype of the machine

Intellectual Property Licences

Production of the machines

Self operated machines

Third party operatedmachines

(With their own brands)

Brand Franchise

$(products)

$(Licences)

$(Commission

and licences)

$(Licences)

Business Model

The Action Plan

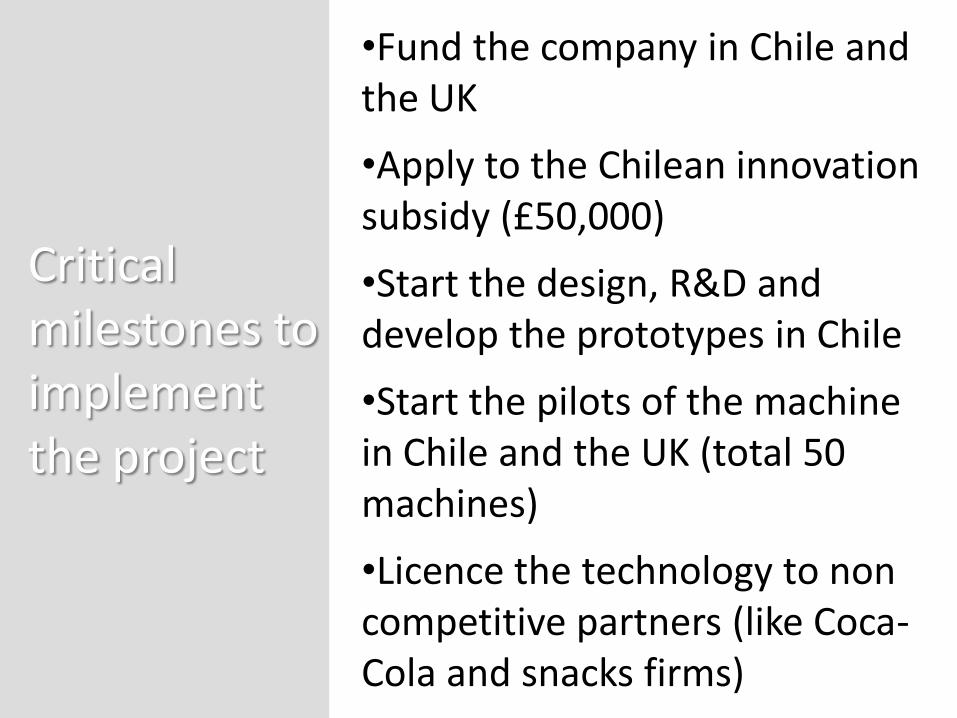

Critical milestones to implement the project

•Fund the company in Chile and the UK

•Apply to the Chilean innovation subsidy (£50,000)

•Start the design, R&D and develop the prototypes in Chile

•Start the pilots of the machine in Chile and the UK (total 50 machines)

•Licence the technology to non competitive partners (like Coca-Cola and snacks firms)

33

Our Team

MSc in Innovation and Technology Management

Work Experience as Trade Manager, Project Manager, Consultant and Part time Lecturer

Founder partner of Rnovo

Experienced in public and private innovation projects. From funding to execution. Pedro Parraguez

Chief Executive Officer

Serial Entrepreneur and partner of HarneckerCarey

MBA & Licentiate in Economics and Management Sciences

Senior Consultant Allan Jarry

Chief Financial Officer

Chief Engineering Officer

Senior Intellectual Property and Technology Transfer Specialist

MBA & Mechanical Engineer

Innovation Consultant

Jorge Fuentes

Shareholders and Start-up Organization

Marketing Analysis

RetailingUS$11,171 bn

Non-store:vending

US$66 bn

Store-based:grocery

US$4,707 bn

Non-store:homeshopping

US$219 bn

Non-store:Internetretailing

US$253 bn

Packaged foods

vendingUS$6 bn

Packaged drinks

vendingUS$32 bn

Tobaccoproductsvending

US$19 bn

Unpackageddrinks

vendingUS$5 bn

Personalhygiene

products Vending US$1 bn

Other productsvendingUS$3 bn

Store-based:non-groceryUS$5,809 bn

Non-store:Directselling

US$118 bn

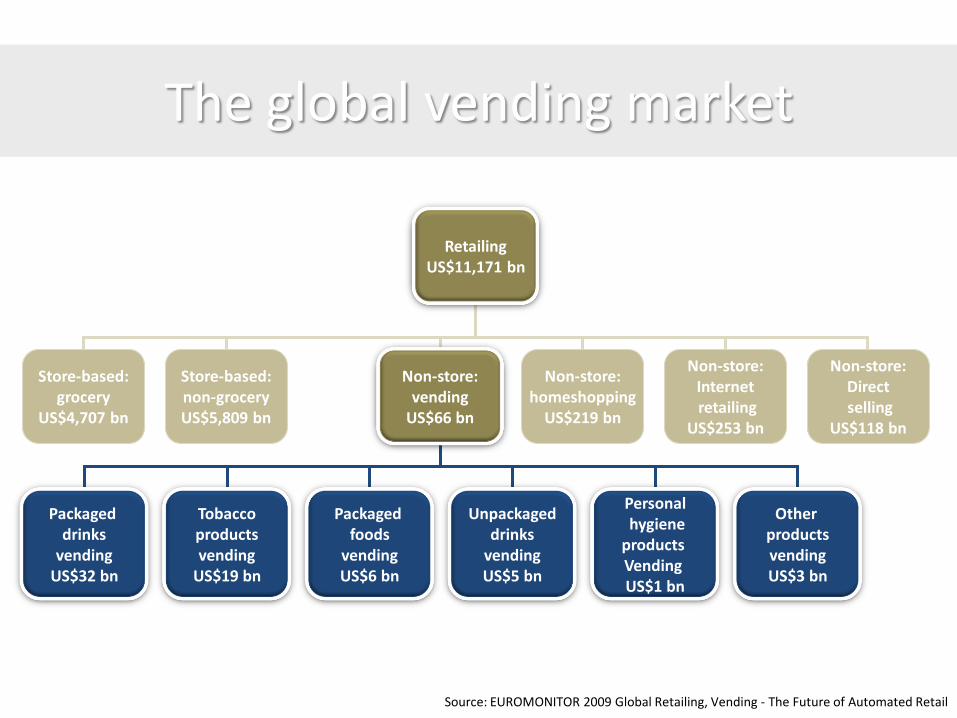

The global vending market

Source: EUROMONITOR 2009 Global Retailing, Vending - The Future of Automated Retail

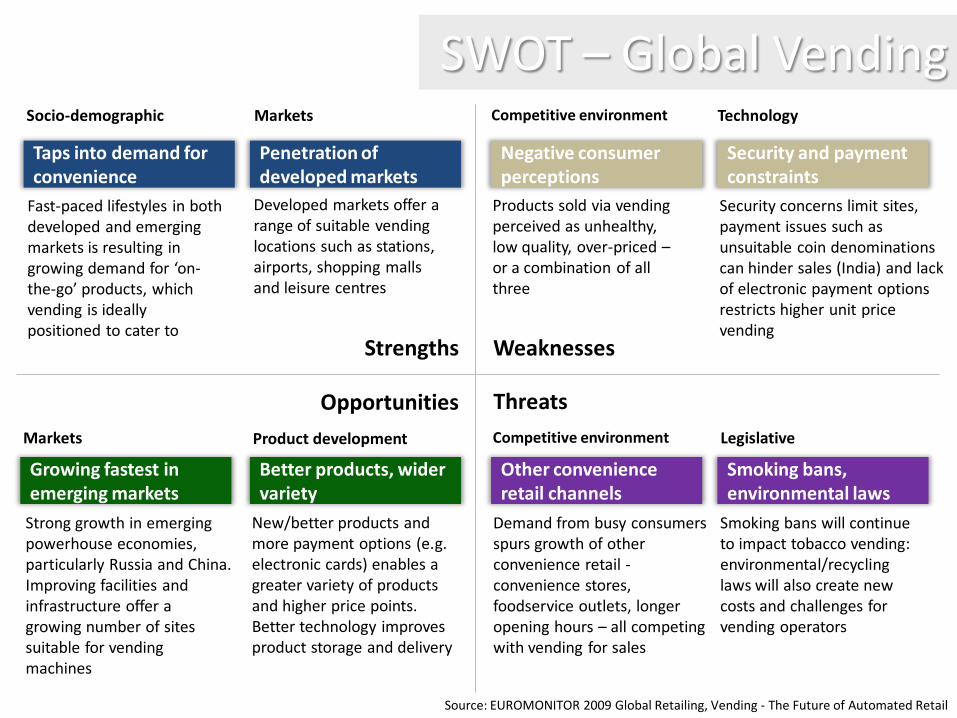

Opportunities

WeaknessesStrengths

Threats

Taps into demand for convenience

Socio-demographic

Negative consumer perceptions

Competitive environment

Growing fastest in emerging markets

Markets

Other convenience retail channels

Competitive environment

Penetration of developed markets

Better products, wider variety

Product development

Security and payment constraints

Technology

Smoking bans, environmental laws

Legislative

Markets

Fast-paced lifestyles in both developed and emerging markets is resulting in growing demand for ‘on-the-go’ products, which vending is ideally positioned to cater to

Products sold via vending perceived as unhealthy, low quality, over-priced –or a combination of all three

Security concerns limit sites, payment issues such as unsuitable coin denominations can hinder sales (India) and lack of electronic payment options restricts higher unit price vending

Developed markets offer a range of suitable vending locations such as stations, airports, shopping malls and leisure centres

Strong growth in emerging powerhouse economies, particularly Russia and China. Improving facilities and infrastructure offer a growing number of sites suitable for vending machines

New/better products and more payment options (e.g. electronic cards) enables a greater variety of products and higher price points. Better technology improves product storage and delivery

Smoking bans will continue to impact tobacco vending: environmental/recycling laws will also create new costs and challenges for vending operators

Demand from busy consumers spurs growth of other convenience retail -convenience stores, foodservice outlets, longer opening hours – all competing with vending for sales

SWOT – Global Vending

Source: EUROMONITOR 2009 Global Retailing, Vending - The Future of Automated Retail

Vending accounted for 0.6% of the US$11 trillion global retail market in 2008

The global vending market experienced solid growth in the early part of the 2003-2008 period, but decline in the important tobacco products category meant that by 2008 global value sales had returned to 2003 levels

Global sales are expected to continue falling to 2013.

66.2 66.2 62.6

0

10

20

30

40

50

60

70

2003 2008 2013

US

$b

n, F

ixe

d 2

00

8 E

xch

an

ge

Ra

tes

Global Vending MarketValue 2003-2113

Global Vending – a US$66 Billion Market

Source: EUROMONITOR 2009 Global Retailing, Vending - The Future of Automated Retail

Bubble size shows product sector share of market, range displayed: 1.3 - 48.8%

Traditional Vending Products Lead Category Sales

Source: EUROMONITOR 2009 Global Retailing, Vending - The Future of Automated Retail

Asia Pacific

Eastern Europe

Latin America

Middle Eastand Africa

North America

Australasia

WesternEurope-10

-5

0

5

10

15

20

-5 0 5 10 15

Gro

wth

(C

AG

R 2

00

3-2

00

8, %

)

Growth (CAGR 2008-2013, %)

Regional Vending Markets: Comparison 2003-2008, 2008-2013

Bubble shows total market size 2008, US$

World Markets, Growth and Size

Source: EUROMONITOR 2009 Global Retailing, Vending - The Future of Automated Retail

New Demands New Technology

Convenience

Vending products responding to consumers’ ‘on-the-go’ lifestyles range from umbrellas and books to hot pizzas and freshly-made French fries

Health

Increasing consumer concerns about health and wellness have widened the choice of healthy vended products such as bottled water, sports drinks, low-calorie foods and even fresh fruit

“Premiumisation”

Development in captive vending and changing consumer tastes have led to a premiumisation trend. This has influenced product quality, but also other factors such as a focus on vending Fairtrade products

Customer interface

Innovations such as touch-screen controls help vending machines to

offer information and advice on more complex products, such as OTC

healthcare and consumer electronics

Packaging

New packaging options widen product options, such as drinks pouches which enable drinks to be mixed to demand

from concentrates

Delivery mechanisms

New systems such as vending machine manufacturer Sielaff’s ‘SoftDrop’

delivery or Wurlitzer’s ‘Smart Waiter’ machine means that fragile items such

as glass bottles, yoghurts and digital cameras can now be vended

Payment

Electronic payment technology has allowed vending to branch out beyond its traditional low-price product range

M

a

r

k

e

t

D

y

n

a

m

i

c

s

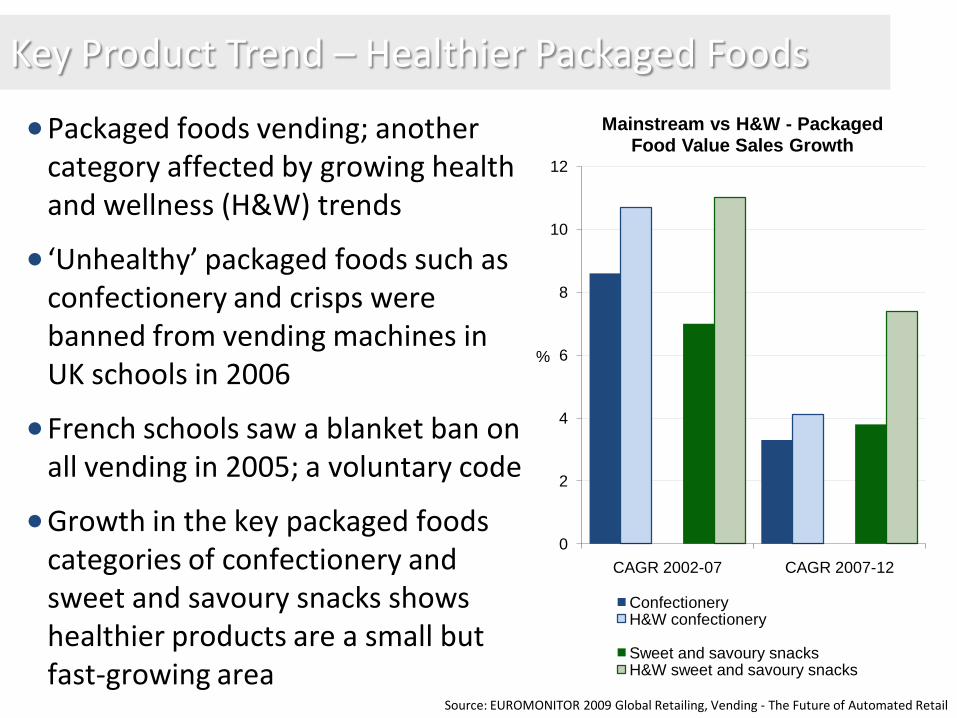

Packaged foods vending; another category affected by growing health and wellness (H&W) trends

‘Unhealthy’ packaged foods such as confectionery and crisps were banned from vending machines in UK schools in 2006

French schools saw a blanket ban on all vending in 2005; a voluntary code

Growth in the key packaged foods categories of confectionery and sweet and savoury snacks shows healthier products are a small but fast-growing area

0

2

4

6

8

10

12

CAGR 2002-07 CAGR 2007-12

%

Mainstream vs H&W - Packaged Food Value Sales Growth

ConfectioneryH&W confectionery

Sweet and savoury snacksH&W sweet and savoury snacks

Key Product Trend – Healthier Packaged Foods

Source: EUROMONITOR 2009 Global Retailing, Vending - The Future of Automated Retail

Our Consumers

Demographically they are between 13 and 35 years old, live or works in urban areas desiring convenience, a healthy lifestyle and the desire for affordable food on the go.

Our Industrial Customers (B2B)

Big drinks and snacks companies like Coca-Cola and Pepsi + potential licensees like vending machine manufacturers + Entrepreneurial Franchisers

Competitors

Competitive landscape

The Single Brand Operator:

The Coca-Cola Co

Market leader in global vending: over 2% value share in 2008

Present throughout Europe, Asia Pacific, the Americas and Middle East/Africa 0.0

0.5

1.0

1.5

2.0

2004 2005 2006 2007 2008

US

$ b

nat fixed 2

008

exchange r

ate

s

The Coca-Cola Co, Global Vending Sales 2004-2008

The Multi-brand Operators:

Lekkerland

Europe-based LekkerlandDeutschland GmbH & Co KG is vending’s second biggest global operator with value share of just under 2% in 2008

Key markets are Germany, Belgium and the Netherlands

Selecta AG

The company operates both captive and public vending machines across 23 markets, with 150,000 machines serving 25,000 companies and total annual sales of nearly US$900 million

50

Financials

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Chile – (CLP m) 37262.6 38357 38987.3 39590.9 41740.9 39833.7 41902.4 44344.6 47254.3 50457.6 54021

United Kingdom – (£ m) 848.6 944.2 834.8 628.8 470.5 446.2 438.2 435.4 434.1 434.5 436.8

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014

Chile - CLP to £ mn

United Kingdom - £ mn

UK – Chile potential market sales forecast

Source: EUROMONITOR 2009 Global Retailing, Vending - The Future of Automated Retail

Machines

Buying

Leasing

Replacing

Upgrading

R&D

Distribution

Delivery

Refilling

Commission

Payments

to site

owners

Product

Products

Ingredients

Packaging

Operation

Repair

Maintenance

Power

What Do Vending Purchases Pay For?

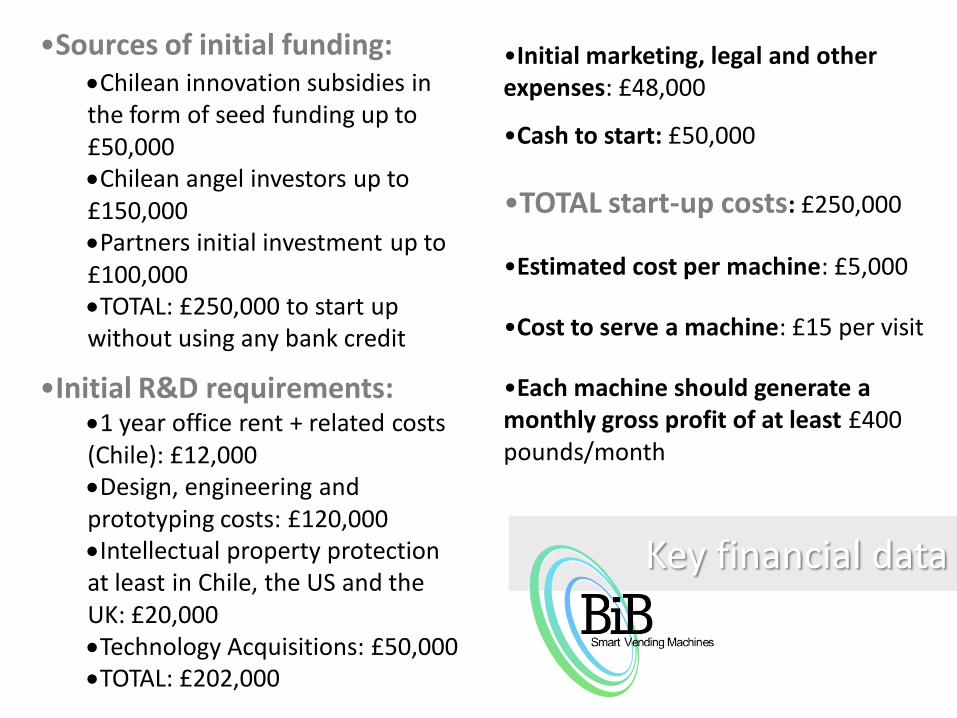

•Sources of initial funding: Chilean innovation subsidies in the form of seed funding up to £50,000Chilean angel investors up to £150,000Partners initial investment up to £100,000TOTAL: £250,000 to start up without using any bank credit

•Initial R&D requirements:1 year office rent + related costs (Chile): £12,000Design, engineering and prototyping costs: £120,000Intellectual property protection at least in Chile, the US and the UK: £20,000Technology Acquisitions: £50,000TOTAL: £202,000

•Initial marketing, legal and other expenses: £48,000

•Cash to start: £50,000

•TOTAL start-up costs: £250,000

•Estimated cost per machine: £5,000

•Cost to serve a machine: £15 per visit

•Each machine should generate a monthly gross profit of at least £400 pounds/month

Key financial data

***All the values are in pounds

Highlights and sales by year

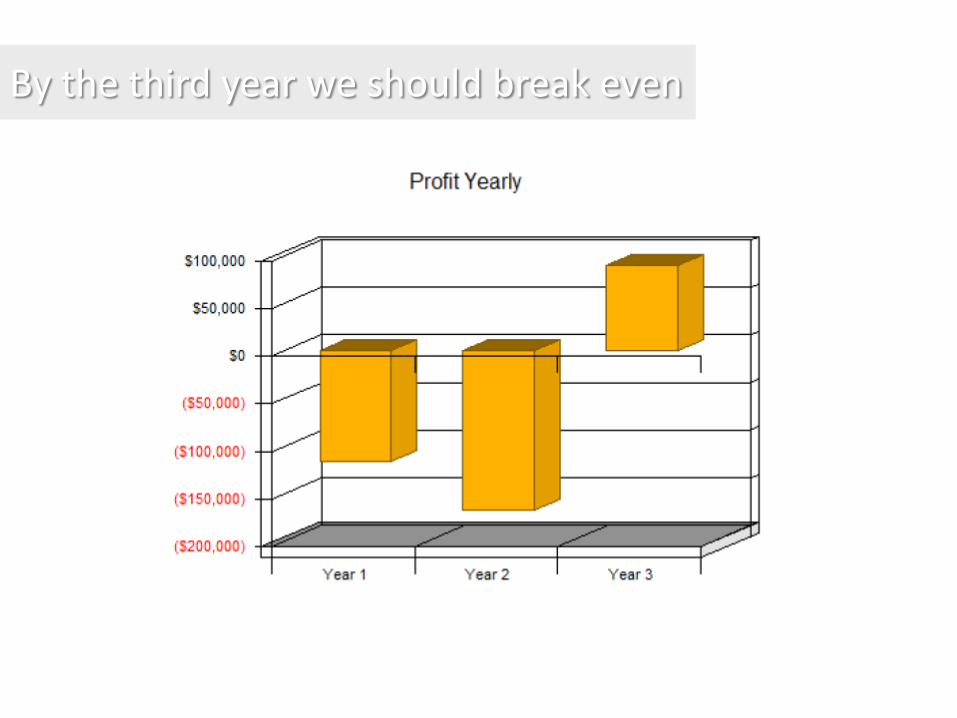

By the third year we should break even

In sum: lots of challenges ahead but a big business in the horizon!