21

Bien-$tar- Bien-$tar- $avers $avers A Youth IDA A Youth IDA Program Program January, 2010 January, 2010

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | chrystal-davis |

| View: | 215 times |

| Download: | 2 times |

Bien-$tar-Bien-$tar-$avers$avers

A Youth IDA ProgramA Youth IDA ProgramJanuary, 2010January, 2010

Bien-$tar-$avers is a new project that is Bien-$tar-$avers is a new project that is coordinated by an AmeriCorps VISTA coordinated by an AmeriCorps VISTA

volunteervolunteer VISTAVISTA = = VVolunteers olunteers IIn n SService ervice TTo o AAmericamerica One year term of service to address the needs One year term of service to address the needs

of low-income communities. of low-income communities. Members generally do not provide direct Members generally do not provide direct

services services They build the organizational, administrative, They build the organizational, administrative,

and financial capacity of organizations that and financial capacity of organizations that fight illiteracy, improve health services, foster fight illiteracy, improve health services, foster economic develop, and otherwise assist low-economic develop, and otherwise assist low-income communities. income communities.

focus on building permanent infrastructure in focus on building permanent infrastructure in organizations - sustainability!organizations - sustainability!

What is an IDA?What is an IDA? IIndividual ndividual DDevelopment evelopment AAccountsccounts are special savings are special savings

accounts that match the deposits of low- and moderate-accounts that match the deposits of low- and moderate-income people. income people.

For every dollar saved in an IDA, savers receive a For every dollar saved in an IDA, savers receive a corresponding match which serves as both a reward corresponding match which serves as both a reward and an incentive to further the saving habit. and an incentive to further the saving habit.

Savers agree to complete financial education classes Savers agree to complete financial education classes and use their savings for an asset-building purpose – and use their savings for an asset-building purpose – typically for post-secondary education or job training, typically for post-secondary education or job training, home purchase, or to capitalize a small business. home purchase, or to capitalize a small business.

In addition to earning match dollars, savers learn In addition to earning match dollars, savers learn about budgeting, saving and receive additional training about budgeting, saving and receive additional training before purchasing an asset. before purchasing an asset.

IDAs make it possible for individuals to build the IDAs make it possible for individuals to build the financial assets they need to achieve the American financial assets they need to achieve the American Dream. Dream.

Why a Youth IDA?Why a Youth IDA? Youth IDAs give young people access to productive assets that

they would otherwise be unable to afford.

Youth IDAs also:

Introduce young people to banks and financial institutions

Teach children about financial concepts and economic literacy

Offer financial counseling with program staff or skilled adult mentors.

Encourage participation in discussion groups & entrepreneurial activities

Promote the develop the fundamental habits and understanding necessary to become successful and independent adults.

Why a Youth IDA? Why a Youth IDA? Continued…Continued…

According to research, holding assets is a key According to research, holding assets is a key determinant in predicting one’s expectations and determinant in predicting one’s expectations and confidence about the future, long term planning goals, confidence about the future, long term planning goals, reduced participation in high risk activities, and social reduced participation in high risk activities, and social connectedness. connectedness.

Assets provide benefits such as a stress-reducing Assets provide benefits such as a stress-reducing financial cushion, increased self esteem, and an financial cushion, increased self esteem, and an orientation toward the future. orientation toward the future.

By teaching children from asset poor families to set By teaching children from asset poor families to set clear financial goals and how to meet those challenges clear financial goals and how to meet those challenges through a progressive series of steps, IDAs provide the through a progressive series of steps, IDAs provide the structure for participants to receive a positive structure for participants to receive a positive psychological boost, promote long-term, goal oriented psychological boost, promote long-term, goal oriented thinking, and encourage the development of banking thinking, and encourage the development of banking habits at an early age.habits at an early age.

Goals & Anticipated Outcomesof Youth IDA Programs

Short-term and Intermediate Outcomes: Youth learn to set personal goals and plan for their future Develop a working relationship with financial institutions Gain an improved understanding of financial concepts Become more media savvy and learn to curb their impulse

spending Have the ability to peruse academic, athletic and artistic

activities Long-term Outcomes

Youths’ economic well-being and future prospects are improved

Attain lasting financial security through their increased understanding and better management of personal finances

Develop an increase in confidence and ability to save for a goal Share their healthy financial attitudes, skills and knowledge

with family

Savings Goals: The 3 A’sSavings Goals: The 3 A’s

Participants of Bien-$tar-$avers must save Participants of Bien-$tar-$avers must save for a for a Productive AssetProductive Asset or something of or something of value that is likely to return substantial value that is likely to return substantial long-term benefits.long-term benefits.

Their productive asset(s) must be related Their productive asset(s) must be related to:to:

AcademicsAcademicsAthleticsAthleticsArtArt

Matching fundsMatching funds Bine-$tar-$avers Bine-$tar-$avers

offers a 3:1 matchoffers a 3:1 match Children in grades 1st Children in grades 1st

through 5ththrough 5th can receive a maximum can receive a maximum

of $375of $375 savings + maximum savings + maximum

match = $500match = $500 Teens in grades 6th Teens in grades 6th

through 12ththrough 12th can receive a maximum can receive a maximum

of $600 of $600 (savings + maximum (savings + maximum

match = $800)match = $800)

IDA Participant Eligibility IDA Participant Eligibility requirementsrequirements

Live in a Bienestar apartmentLive in a Bienestar apartment Be enrolled in school Be enrolled in school Be in good academic standingBe in good academic standing Children in 1Children in 1stst - 5 - 5thth grades must have grades must have

completed a Bienestar Financial Fitness completed a Bienestar Financial Fitness ClassClass

Teens in grades 6Teens in grades 6thth - 12 - 12thth will take financial will take financial literacy training as part of the IDA programliteracy training as part of the IDA program

Submit a completed application and a Submit a completed application and a signed contractsigned contract

Ongoing Participation Ongoing Participation RequirementsRequirements

Make a monthly deposit into their account – at Make a monthly deposit into their account – at least $5 - $10 is recommendedleast $5 - $10 is recommended 3 missed deposits in a 6 month period or 2 in a row will 3 missed deposits in a 6 month period or 2 in a row will

result in early exit from the program result in early exit from the program Monthly deposits must be made while the account is Monthly deposits must be made while the account is

open, regardless if savings goal is metopen, regardless if savings goal is met Participate in fundraising events and attend all Participate in fundraising events and attend all

workshops and meetingsworkshops and meetings Meet with the Bien-$tar-$avers IDA program Meet with the Bien-$tar-$avers IDA program

coordinator at least one timecoordinator at least one time Those I grades 6Those I grades 6thth – 12 – 12thth must Complete a must Complete a

Bienestar financial literacy courseBienestar financial literacy course Children in grades 1Children in grades 1stst – 5 – 5thth must participate in must participate in

monthly IDA workshopsmonthly IDA workshops

Financial LiteracyFinancial Literacy B-$-$’s Financial Literacy is based on two B-$-$’s Financial Literacy is based on two

curriculums:curriculums: Financial Fitness for LifeFinancial Fitness for Life –created by the National –created by the National

Council for Economic EducationCouncil for Economic Education Hands on BankingHands on Banking – Created by Wells Fargo – Created by Wells Fargo

Children in 1Children in 1stst – 5 – 5thth grades have already grades have already completed a financial fitness class using completed a financial fitness class using Financial Fitness for LifeFinancial Fitness for Life

Those who haven’t are divided into 2 groups:Those who haven’t are divided into 2 groups: 66thth – 8 – 8thth grade and 9 grade and 9thth – 10 – 10thth grade grade

There are 10 one hour class sessions for each There are 10 one hour class sessions for each group held every other weekgroup held every other week

Ways for Participants to Ways for Participants to Earn MoneyEarn Money

Past SavingsPast Savings Jobs – babysitting, mowing Jobs – babysitting, mowing

lawns etc.lawns etc. Money from allowances, Money from allowances,

birthdays, holidaysbirthdays, holidays Saving IncentivesSaving Incentives

Good grades or attendance Good grades or attendance in schoolin school

Participating in a focus Participating in a focus groupgroup

Surpassing monthly Surpassing monthly deposit savings goal for deposit savings goal for three consecutive monthsthree consecutive months

FundraisersFundraisers Valentines day flower saleValentines day flower sale Car WashCar Wash RecyclingRecycling Movie NightMovie Night

What are Some of the What are Some of the Outcome Indicators?Outcome Indicators?

Number of youth who make an asset purchaseNumber of youth who make an asset purchase Total number of approved purchases and types of Total number of approved purchases and types of

purchase madepurchase made Total amount saved the youths and total matching Total amount saved the youths and total matching

funds disbursed by Bienestarfunds disbursed by Bienestar Number of participants for which Bien-$tar-$avers Number of participants for which Bien-$tar-$avers

is their first bank accountis their first bank account Number of youth who demonstrate an increase in Number of youth who demonstrate an increase in

financial literacyfinancial literacy Total number of hours of community service Total number of hours of community service

completedcompleted Number of youths that open additional accounts Number of youths that open additional accounts

after graduationafter graduation

Partner OrganizationsPartner Organizations

CASA of Oregon is CASA of Oregon is the administer of the administer of the IDA Accounts. the IDA Accounts. CASA is a CDFI as CASA is a CDFI as well as the well as the administrator of administrator of VIDA, the largest VIDA, the largest IDA program in IDA program in OregonOregon

Wells Fargo holds Wells Fargo holds the bank accountsthe bank accounts

Bien-$tar-$aversBien-$tar-$avers

Who are some of the participants?Who are some of the participants?

SareliaSarelia Age: 9Age: 9 Savings Goal: $125Savings Goal: $125 Match needed: $375Match needed: $375 Desired Asset: A Desired Asset: A

laptoplaptop Interests and Interests and

activities: Sarelia’s activities: Sarelia’s favorite subjects are favorite subjects are science and math. She science and math. She enjoys readingenjoys reading

Future goals: To Future goals: To become a doctor or become a doctor or nursenurse

ArmandoArmando Age:Age: 10 10 Savings Goal:Savings Goal: $125 $125 Match needed: $375Match needed: $375 Desired Asset:Desired Asset: A computer A computer

or Guitar. He’s not sure yet. or Guitar. He’s not sure yet. He wants a computer to He wants a computer to research things that interest research things that interest him as he is a very him as he is a very intelligent and inquisitive intelligent and inquisitive boy. He wants a guitar to boy. He wants a guitar to learn how to play and learn how to play and possibly become a possibly become a professional musician. professional musician.

Interests and activities:Interests and activities: Armando enjoys creating Armando enjoys creating origami and playing baseball origami and playing baseball in his free timein his free time

Future goals:Future goals: To become a To become a scientistscientist

IlyneIlyne Age: 10Age: 10 Savings Goal: $125Savings Goal: $125 Match needed: $375Match needed: $375 Desired Asset: Ilyne is Desired Asset: Ilyne is

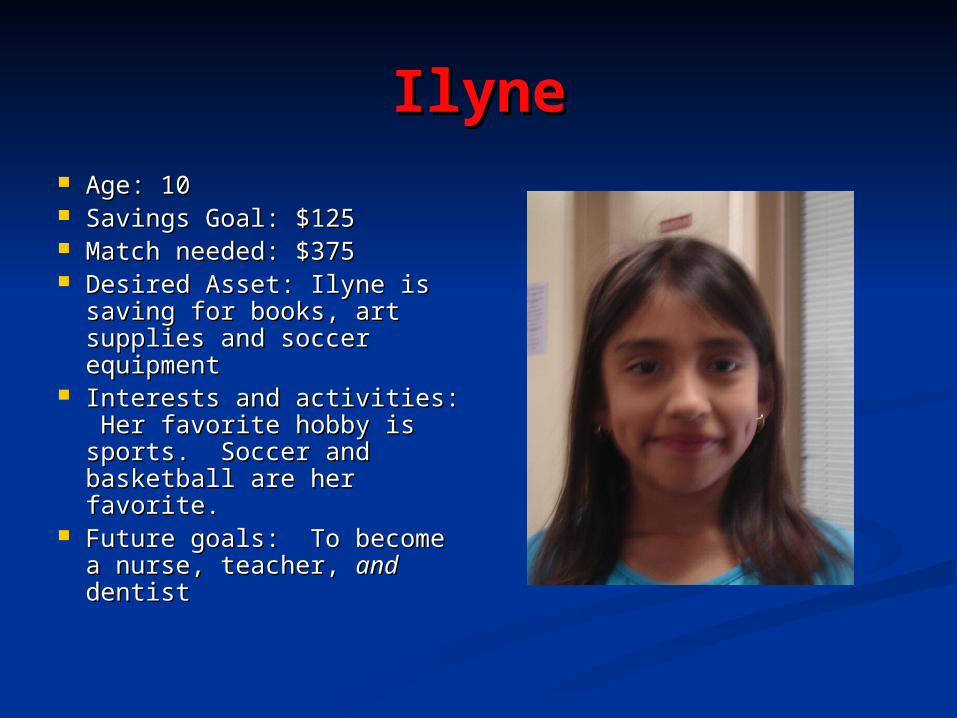

saving for books, art saving for books, art supplies and soccer supplies and soccer equipmentequipment

Interests and activities: Interests and activities: Her favorite hobby is Her favorite hobby is sports. Soccer and sports. Soccer and basketball are her basketball are her favorite.favorite.

Future goals: To become Future goals: To become a nurse, teacher, a nurse, teacher, andand dentistdentist

AngelAngel Age: 11Age: 11 Savings Goal: $200Savings Goal: $200 Match needed: $600Match needed: $600 Desired Asset: Angel Desired Asset: Angel

is saving for his own is saving for his own computer and for computer and for booksbooks

Angels favorite Angels favorite subjects are Math subjects are Math and Scienceand Science

Future goals: To Future goals: To become a scientistbecome a scientist

GerardoGerardo Age: 13 Age: 13 Savings Goal: $200Savings Goal: $200 Match needed: $600Match needed: $600 Desired Asset: A TrumpetDesired Asset: A Trumpet Interests and activities: Interests and activities:

Gerardo enjoys playing Gerardo enjoys playing trumpet in his school band trumpet in his school band and on his own.and on his own.

Future goals: Gerardo isn’t Future goals: Gerardo isn’t sure what he wants to be sure what he wants to be when he grows up but he’s when he grows up but he’s pretty sure that whatever it pretty sure that whatever it will be will involve math, will be will involve math, one of his other passions. one of his other passions. He would also like to be an He would also like to be an expert trumpet player.expert trumpet player.

Thank You!Thank You!

Questions? Comments?Questions? Comments?

Contact Aleksi MerilainenContact Aleksi [email protected]

503-693-2937 ext 109503-693-2937 ext 109