Introduction Define Accounting & discuss its functions. Meaning of Accounting – Accounting is an art of recording, classifying, summarizing & reporting of transactions with the aim of showing the financial health of an entity which has its income & expenses. Accounting has two distinct functions. Historical functions & Managerial functions. Historical function is related to recording, classifying, summarizing

Transcript

Introduction

Define Accounting & discuss its functions.

Meaning of Accounting – Accounting is an art of recording, classifying, summarizing & reporting of transactions with the aim of showing the financial health of an entity which has its income & expenses.

Accounting has two distinct functions.

Historical functions &

Managerial functions.

Historical function is related to recording, classifying, summarizing & interpreting past transactions of an enterprise. The reporting of the result is done through B/S, P&L A/c etc.

• The managerial functions provides information for managers at all levels for planning, coordinating, controlling day today activities, appraising the performance by comparing actual with pre determined standards. These functions helps to achieve maximum efficiency. Like cash flow statement, Ratio analysis etc.

• Explain Accrual basis of Accounting. Define double entry system of Accounting & its features.

• Accrual basis of accounting – It is the basis which recognizes revenue & expenses as they are earned or incurred without regard to the accounting period to which it belongs.

• Double entry system of Accounting is a system of recording business transactions which recognizes that each transaction has a dual aspect i.e., Debit & Credit is affected.

• Features :• This method records both aspects of each

transaction.• Both Debit & Credit entries are made for every

transaction in two different accounts.• All transactions are recorded fully.

• Under this system Trial balance can be prepared to check arithmetic accuracy of the transactions.

• Profit & Loss A/c can be prepared by showing in detail the incomes & expenses.

• Balance sheet can also be prepared in detail.

• What are the advantages & limitations of Double entry system?

• Advantages :• A complete record of all the transaction relating to

a business unit are maintained.• The financial position of the firm can be

ascertained.• The arithmetical accuracy of the books of A/c can

be ensured.• Locating & Rectifying errors are easier.• The system can be applied to any form of

organization.• Profit earned or losses made can be ascertained.

• Amounts due to supplier or due from customers can be easily ascertained.

• It helps taking managerial decisions.• Greater control over accounts can be exercised.• Business transactions does not get mixed up

with private transactions of the owner.• Limitations :• The system adopts only money as the basic unit

of measurement.• Many important events can not be recorded

simply because they can not be expressed in monetary terms.

• Transactions are all historical records & not future probabilities.

• If a transaction is omitted by mistake then it may remain undiscovered.

• If a transaction is wrongly recorded then it is difficult to detect the error.

• A compensating error may also remain undetected.

• The system requires personal judgment of the accountant.

• What are the characteristics of Modern accounting? State the advantages & its limitations.

• With the growth of corporate activity in the 20th century, the field of accounting has increased greatly in importance and has seen many improvements in theory and techniques. The chief causes of changes in accounting methods have been more complex tax laws and regulations and the need to keep uniform accounts for possible governmental or public scrutiny. Contemporary accounting firms also have taken on managerial functions and are no longer concerned simply with ascertaining and reporting financial condition but also with advising a client how to act on this information; they also consult on information-technology systems and other services.

• Main characteristics of Modern accounting are :• Use of Double entry system of Accounting.• Use of computer based programmes for faster

& accurate accounting.• Use of electronic media to transfer accounting

data.• Advantages :• Accurate accounting.• Faster processing & completion of accounting.• Human errors are removed.• Accountants are relieved of lengthy process of

making entry in the books of A/cs.

• Limitations :• If any error takes place then it becomes very

difficult to identify it.• Accounting becomes more dependent on use of

computers.

• What do you mean by Accounting cycle? Explain the various parts of the Accounting cycle.

• Accounting cycle – It refers to the sequence of accounting procedures used to record, classify & summarize the business transactions. It begins with identification of business transactions, preparation of business document, recording of transactions through journal, posting of transactions into ledger, preparation of Trial balance, passing of adjustment entries, preparation of Final account, passing of closing entries and lastly passing of reverse entries.

• Various parts of Accounting cycle are :• Identification of business transactions.• Preparation of business document.• Recording of transactions through journal.

• Posting of transactions into ledger.

• Preparation of Trial balance.

• Passing of adjustment entries.

• Preparation of Final account.

• Passing of closing entries and lastly

• Passing of reverse entries.

• What do you mean by GAAP?• GAAP stands for generally accepted accounting

principles. These are the conventions, rules & procedures necessary to define accepted accounting practice at a particular time. These principles provide a foundation for measuring & disclosing the results of business transactions & events.

• Generally accepted accounting principles are conventional – that is, they become generally accepted by agreement rather than by formal derivation from a set basic concepts. The principles are developed on the basis of experience, reason, custom, usage & to a significant extent out of practical necessity.

Introduction – Accounting concept, standard & equation.

• Explain business entity, cost & realization concepts.

• Business entity – A firm possesses an existence which is distinct from its owner or owners. An entity can be a sole proprietor, partnership firm, company or a non profit making organization.

• Cost concept - A business transaction is recorded in terms of the amount actually passing through the transaction. For example A purchases a machine from B for Rs.20000. the real worth of the machine may be more or less than Rs.20000.

But the transaction must be recorded at cost of Rs.20000. The balance sheet therefore normally shows the asset at cost price.

• Realization concept – In a normal business an order is executed after signing of contract. Then goods are delivered which creates an obligation for the buyer to pay. Under realization concept the profit is normally regarded as being earned at the time when goods or services are passed on to the buyer.

• Money measurement – Money is medium of exchange. Accounting is only concerned with those events which can be measured in terms of money.

• Going concern – Accounting is based on the assumption that the business unit will continue to operate for an indefinitely long period of time.

• Dual aspect concept – This concept shows two aspects of accounting, one representing the Asset & the other representing the claims against assets which recognizes that each transaction has a dual aspect i.e., Debit & Credit.

• Accrual concept - It is the basis which recognizes revenue & expenses as they are earned or incurred without regard to the date of receipt or payment.

• Define Accounting equation with example. • The accounting equation is the basis for double

entry system of accounting. It implies that every time a transaction takes place, there is always a two sided effect.

• Accounting equation can be expressed as :• Asset - Liability = Capital• For example owner introduces capital results in –

Increase in Asset & Capital.• Purchase of P & M on credit results in – Increase

in Asset & Liability.• Sale of P & M in Cash results in - Decrease in

Asset & increase in another Asset i.e., Cash.

• Explain Traditional classification of A/cs & rules for Debit & Credit.

• Traditional classification is the old system of classifying A/cs.

Credit all incomes & gains.• Note – when some prefix or suffix is added to a

nominal A/c it becomes a personal A/c.• O/s Rent A/c, Rent Prepaid A/c, O/s Interest A/c,

Prepaid Salary A/c, O/s Comm. A/c etc.

• What are accounting standards? What is the need for such standards?

• Accounting standards are accounting rules & procedures relating to measurement, valuation & disclosure issued by the Institute of the chartered accountants of India.

• Need for accounting standard are : • Accounting standards promote better

understanding of accounting statements.• Accounting information is more useful if it is

published on a comparable basis.• Accounting standards provide a generally

accepted language for financial statements.

• Accounting standard may be regarded as a means to establish that the collective wisdom & experience prevail over an individual.

• Examples :• AS 2 – Valuation of Inventories – 1.4.99• AS 6 – Depreciation Accounting – 1.4.95• AS 7 – Accounting for cons. contracts – 1.4.91• AS 19 – Leases – 1.4.01• AS 20 – Earning per share – 1.4.01• AS 21 – Consolidated Financial stmt –1.4.01 etc.

• What are the recognized accounting doctrines?• Recognized accounting doctrines are :• Consistency – This implies that the basis followed

in several accounting periods should be consistent. If a change becomes necessary, the change & its effect should be mentioned clearly.

• Disclosure – This requires that all significant information should be disclosed. Accounting statements should be honest representation of true facts of the business. It should follow generally accepted accounting principles.

• Conservatism – “Anticipate no profit & provide for all possible losses” is the teaching of conservatism.

Conservatism always leads to understatement of income in the profit & loss A/c, over statement of liabilities & understatement of Assets in the B/S. So it does not show the true position of A/c, hence not permitted.

• Materiality – This doctrine emphasises that matters which are significant require accounting in greater details than the matters which are less significant.

Journal Entries• Define Journal & explain its nature. Explain the

various parts of a journal.• The journal records all transactions of a business

in the order in which they occur. A journal can therefore be defined as a book containing chronological record of transactions. It is the book in which the transactions are recorded first under the double entry system.

• It contains from the left to right side Date, Particulars, L.F., Debit & Credit. Amounts.

• A journal is a tool for analyzing & describing the impact of various transactions upon a business unit. A journal is an analysis of the effects of a transaction on the accounts, usually accompanied by an explanation as to its nature.

• The various parts of a Journal are :• Journal is divided by vertical lines into five

columns in which to enter transactions. Date, Particulars, Ledger Folio, Amount (Debit) & Amount (Credit).

• What is a Journal? What do you mean by simple & compound journal entries?

• Simple journal entry – A journal entry containing one Debit & one Credit entry is called a simple journal entry. Example,

• Dr Cr• Date Particulars L.F. Amt(Rs.) Amt(Rs.)• Cash A/c Dr. 50000 • To Sales A/c 50000• (Being goods sold for cash)• Compound journal entry – A journal entry which

contains more than one Debit entry or more than one Credit entry or both is called a compound journal entry.

• Dr Cr• Date Particulars L.F. Amt(Rs.) Amt(Rs.)• B/L A/c Dr. 150000• Furniture A/c Dr., 100000• Cash A/c Dr. 50000 • To Capital A/c 300000• (Being the different assets brought in as Capital)

• What is a Voucher? Explain it with example.• A voucher is a document which provides the

authorization to pay & specifies the accounts to be Debited & Credited. It is prepared for each expenditure.

• It contains written evidence that :• All expenditure have been incurred on the basis

of proper authorization, for example against purchase order.

• The goods & services have been received in full.• Payment has been made only for the goods &

services received.

• A clerk prepares voucher by filling up data from invoice such as Invoice No., Date Amount, Creditors name & Address. Then voucher with Invoice is sent to the employee who have placed the order for verifying Price, Quantity & terms with Purchase order. After verifying the employee sends it to the A/cs department who mentions the A/c No. to be Debited or Credited & sends it to Manager for his final approval. After this the voucher is paid & entered in the books of original entry.

Ledger• Distinguish between Journal & Ledger.• The transaction is first recorded in the books as

Journal.• Ledger is where Journals are posted.• Journal records transactions in a chronological

order.• Ledger records transactions in an analytical

order.• Journal is more reliable as compared to Ledger

since it is the book original entry.• The process of recording transactions is called

Journalizing.• The process of recording transactions in the

Ledger is called Posting.

• Journal is called as a book of prime entry.

• Ledge is called as book of final entry.

• Journal entry shows which accounts should be debited and which should be credited.

• Transactions are classified according to their nature and posted in their respective accounts in ledger.

• What are the subdivisions of Ledger? Explain.• Sales Ledger – It contains accounts with

Customers i.e., Debtors.• Purchase Ledger – It relates to recording the

accounts of Suppliers or Creditors.• General Ledger – It contains all the Real

accounts such as Building, Plant & Machinery, Furniture & Fixture etc.

• Nominal Ledger – It contains all the expenses such as Wages, Salaries, Rent, Insurance, Rates & Taxes & incomes like commission received, Discount received etc.

• Private Ledger – Accounts of Capital & Drawings which are of confidential nature may be maintained in a separate Private ledger.

• Cash book – It contains Cash & Bank related transactions.

• Ledger is a book of final entry. Explain.• Ledger is the main book of accounts. It is the

most important book of accounting system.It contains an account for each asset, liability,revenue and expenses account to which the transactions recorded in the book of original entry are posted. Ledger is theultimate destination of all transactions.

• It is also called book of “final entry”. In ledger the information is classified by nature and relevance. The ledger includes all the basic accounts needed for the preparation of the financial statements.

• Ledger is the principal book of Accounts. Do you agree? Give reasons.

• The individual accounts are normally maintained in a book referred to as Ledger. It is the most important book of accounts as it includes all the summaries of transactions and hence it is called the Principal book of Accounts.

• Ledger is called Principal book of accounts because :

• It summaries all the transactions.• It provides a permanent record of the financial

transactions of a Firm.• It is the principal or primary book of accounts. • The transactions are classified under appropriate

heads called accounts.

• The information contained in the ledger account can be used to draw the conclusion regarding status of any account.

• The accounts contain the summaries of all the related transactions.

• It is the basic of preparing the final account. • It helps us in achieving the objectives of

accounting.

Cash Book – Meaning & Types

• What are the different types of Cash books? What are contra entries?

A Cash book can be of following types.1. Simple cash book or single column cash book.2. Two columnar cash book or Double column

cash book.3. Three Columnar cash book or Triple column

cash book.4. Petty Cash Book.Single column cash book – It consists of Cashcolumn i.e., column for cash received & cash paid in the book.Double column cash book – This cash book has two

columns i.e., Cash & Bank column.

Triple column cash book - It contains three columns

on each side of cash book i.e.,

i) Cash column for cash received and cash paid.

ii) Discount column for discount received and allowed.

iii) Bank column for money deposited and money withdrawn from bank.

Petty Cash Book – It records Petty/small Expenses

& Receipts.

Contra entry – A double column cash book contains

columns for both cash and bank transactions. This is

an account where both cash and bank accounts are involved. This transaction is recorded on both sides of the cash book.For example : Cash of Rs.10,000 is withdrawn from bank.Entry on the debit side of the cash book will beCash A/c Dr. 10,000To Bank A/c 10,000Entry on the credit side of the cash book will beBank A/c Cr 10,000By Cash A/c 10,000So, Cash book is Debited with cash column on the Debit side and bank column is credit on the credit side of the cash book. This is a contra entry.

• Explain single & double column cash books.Single column cash book – It consists of Cashcolumn i.e., column for cash received & cash paid in the book. All cash receipts are recorded on the left-hand (Debit) side & all cash payments are recorded on the right-hand (Credit) side. A specimen of single column cash book consists of Date, Particulars, Voucher No., Ledger Folio & Amount on both Debit & Credit side of the Cash book.Double column cash book – This cash book has two columns i.e., Cash & Bank column. It is the cash book where cash & transactions involving receipts

& payments by cheques are recorded is called

Double column cash book. A Double column cash

book is one where both cash & bank transaction are

• What is the purpose of the discount column maintained in the cash book? Explain Triple column cash book.

• The most exhaustive cash book is the Triple-column cash book, which has three amount columns on either side, viz., Cash, Bank & Discount. The discount column is provided for recording discount. It is suited to large business houses which make & receive payments in cash & by cheques & which receive / allow cash discount. Discount column maintained separately helps management to know the value of Discount received & foregone by the organization.

• Triple column cash book contains Cash, Bank & Discount column.

• Cash book is a Journalized Ledger. Explain.• The cash book is a subdivision of the book of

original entry. It records transactions involving receipt or payment of cash.

• All cash transactions are first entered in the cash book & then posted from cash book into the ledger. Cash book is maintained in the form of a ledger with narration like done in journal. Thus cash book is called a journalized ledger.

• What is a Petty cash book? Explain the imprest system of Petty cash.

• Chief cashier generally deals with cash receipts & payments of high value. He delegates the responsibility for small day-to-day transactions to some senior staff of accounts department. The person records these transactions in a petty cash book. Petty cash expenditures are like bus fares, tea & snacks purchases, purchase of news paper etc.

• A petty cash fund is established by transferring a small amount of cash from head cashier to the petty cashier. The petty cashier records all the petty transactions in a separate book called Petty

• cash book. All receipts of cash are entered on the debit side & payments are entered in the credit side of the petty cash book.

• Imprest system of petty cash – It is a system of controlling petty cash. Under this system, a fixed sum or float is allocated as sufficient to meet petty cash expenditure for an agreed period of time. At the end of the agreed period, the petty cashier submits his account of expenditure. The sum expended by the petty cashier is reimbursed, thus making up the balance to the original sums.

Cash Book• Distinguish between Debit Note & Credit Note.• Credit note is a document evidencing that a credit

entry has been passed to a Debtors Account. • Debit note is a commercial document evidencing

that a debit entry has been passed to a Debtors Account.

• Credit note is passed to record return of material due to defect in quality, quantity, damage to parts of the material etc.

• Debit note is prepared by the supplier if he forget to include some of the charges while preparing Invoice. It can be Freight, Insurance charges etc.

• Credit note is a document issued to account for goods returned by the customer.

• Debit Note is a document which is raised on customer to debit certain expenses which were not charged at the time of raising Invoice.

• Distinguish between Cash & Trade Discount. Cash Discount - A reduction granted by a supplier from

the Invoice price in consideration of immediate / prompt payment or payment within a stipulated period.

Cash discount is allowed to encourage a Debtor to payoff his debt within a specified period. The Invoice sent by the supplier or to the customer usually contains details of cash discount. For example :

(i) Payment made within 7 days, 10% Discount. (ii) Payment made with in 14 days, 7.5% Discount. (iii) Payment made within 30 days, 5% Discount. (iv) If payment is made after 30 days, over due interest

@ 14% will be chargeable.

Cash discounts are allowed : (i) To improve cash flow of the organization. (ii) To reduce the possibility of Bad Debt. Trade Discount – A reduction granted by a

supplier from the list price of goods or services on business considerations other than for prompt payment.

Trade discount represents an allowance which is made by the manufacturer to the wholesalers or by the wholesalers to the retailers & it is calculated as a percentage of List price of the goods.

Trade discounts are not separately recorded in the books of A/c. When entering invoices in the Purchase day book or Sales day book, only the net total of the invoices are shown.

Bank Reconciliation statement.• What do you mean by Bank reconciliation

statement?• A bank gives to every account holder, from time

to time, a copy of his account as it appears in the books of the bank. It takes the form of a book which is called Bank pass book.

• The bank pass book should agree with the bank column in the cash book. In actual practice, however, they rarely agree.

• In order to reconcile & explain the causes of difference between the bank balance as per cash book & the same as per pass book as on a particular date, a statement is prepared which is called a Bank reconciliation statement.

• What is the need for Bank reconciliation statement?

• Need for Bank reconciliation statement are the following -

• It reflects the actual bank balance position.• It helps to detect any mistake in the cash book &

in the pass book.• It prevents frauds in recording the banking

transactions.• It explains any delay in the collection of

cheques.• It identifies valid transactions recorded by one

party but not by the other.

• Mention some of the items that frequently cause the difference.

• Cheque paid into bank but not credited or collected by the Bank.

• Cheques or cash paid into bank & credited in the pass book but omitted to be recorded in the cash book.

• Cheques issued but not presented for payment.• Discounted bills dishonoured & debited in the

pass book but not recorded in the cash book.• Direct deposit by customer into bank but not

recorded in the cash book.• Incomes collected & credited by bank under

standing order not recorded in the cash book.

• Payments & remittances by bank under standing order debited in the pass book but not in cash book.

• Bank charges or collection charges debited in the pass book but not entered in the cash book.

• Interest on deposit allowed by the bank is credited in the pass book but not recorded in the cash book.

Bank Reconciliation Statement• What is a Bank reconciliation statement? Why is

it prepared?• Bank reconciliation statement is prepared to

ascertain discrepancy in the records as per Bank pass book & Cash book of the establishment.

• All the errors and mistakes made either in the cash book or the books of the bank are revealed.

• It also indicates the delays in the clearance of the outstation cheques.

• Another important purpose of preparing this statement is that it discourages the staff from committing any misappropriation of fund.

• What are the usual items that occur in a Bank reconciliation statement?

• Usual items that occur in a BRS are the following :

1. Cheques issued but not presented for payment – The firm issues cheque from time to time for making various payments. As soon as a cheque is issued, the firm debits the party account and credits the bank account. However bank records such transaction only when it is presented for payment. The bank therefore debits cash account of the firm only when the cheque is presented for payment. For example a firm issues a cheque in favor of X on 25th August 2009 for a sum of Rs.5000. The cheque is presented by X on 5th September 2009.

In case the Bank submits the statement of account to X on 31st August 2009, there will be a difference of Rs.5000 between balance in the bank’s pass book and X’s cash book.

2. Cheque sent for collection but not yet collected – A firm receives from time to time cheques from its customers which is sent to its banker for collection and crediting the proceeds to its account. A firm debits the bank account as soon as it sends the cheque to the bank for collection. However bank gives affect only when the cheques are actually collected. So on a particular day it may be possible that some of the cheques debited by the firm have not yet been collected by the Bank and not accounted.

Hence there will be a difference in the balance as shown in the Firm’s cash book & in the Bank’s pass book.

3. Bank charges – bank charges its customers for various services it renders to them. The bank may charge the customer for collecting outstation cheques, preparing Draft or remitting money at his instruction. Such charges are debited by bank immediately on performing the task. But customer is able to know and rectify its account only at month end when it receives its statement.

Hence for most part of the month, balance of firm’s cash book & the bank’s pass book does not tally.

4. Direct collection on behalf of customers – A bank may receive certain remittances through ECS or Cheque/Draft directly from the customers Banker or customer and credit is passed on to the firm Immediately. However Firm comes to know only when it receives statement of account from the bank. So on a particular date the Bank pass book and cash book maintained by the firm will not agree.

5. Errors –There may be errors in the account maintained by the customer as well as by the bank. A wrong credit or debit may be given by customer or the bank. The balances therefore will not tally.

• When is Bank reconciliation necessary?• Bank reconciliation is necessary for ensuring

Bank balance as per Cash book & balance as per Pass book / Bank statement of the organization matches.

• A bank reconciliation is usually done after receiving monthly statement of account from the Bank.

• It is necessary when the finance manager assess the financial position of the company.

• It is necessary to detect & rectify errors committed by bank in giving credit for money collected or debit for payments made by the organization.

• It must be completed before Quarterly/Half yearly/Annual audit of account of an organization.

Trial Balance

• What is a Trial Balance? Explain the errors which are disclosed by the T.B.

• Trial Balance – It is a statement containing the various Ledger balances (Debit & Credit balances) on a particular date.

• Errors disclosed by TB are :• Omission to post an amount in the Ledger - Cash

receipt of Rs.1000 from Ram has been recorded in the cash book but not posted on the credit side of Ram A/c. So, credit side of T.B. will fall short by Rs.1000.

• Debit or credit entries are not posted at all or posted twice.

• Debits are wrongly posted as credits & vice versa – Cash receipt of Interest Rs.500 is correctly debited in the cash book but has been wrongly recorded on the debit side of interest A/c. So, credit side of T.B. will fall short by Rs.1000.

• Wrong totaling of Subsidiary books.• Difference in amount between the entries.• Error in the computation of an account balance.• Omission of Account balance.• Balance of an Account is wrongly recorded in the

Trial Balance.• Errors in totaling of Trial Balance.

• Explain errors which are not disclosed by T.B.• Errors of Omission – A transaction is omitted

altogether.• Errors of Principle – Wages for installation of

machinery, instead of adding it with cost of Machinery, debited to Wages A/c.

• Compensating Errors • Recording wrong amount in the books of original

entry.• Recording a Transaction more than once in the

books of A/c.• Error in recording a transaction in wrong account

head – Instead of debiting Ram, Raman A/c is debited.

• Suspense Account – When it is not possible to locate the errors in spite of trying different means to locate it, the difference in the Trial Balance is transferred temporarily to an account known as Suspense Account. Afterwards, when the errors have been located, they can be rectified through the Suspense Account.

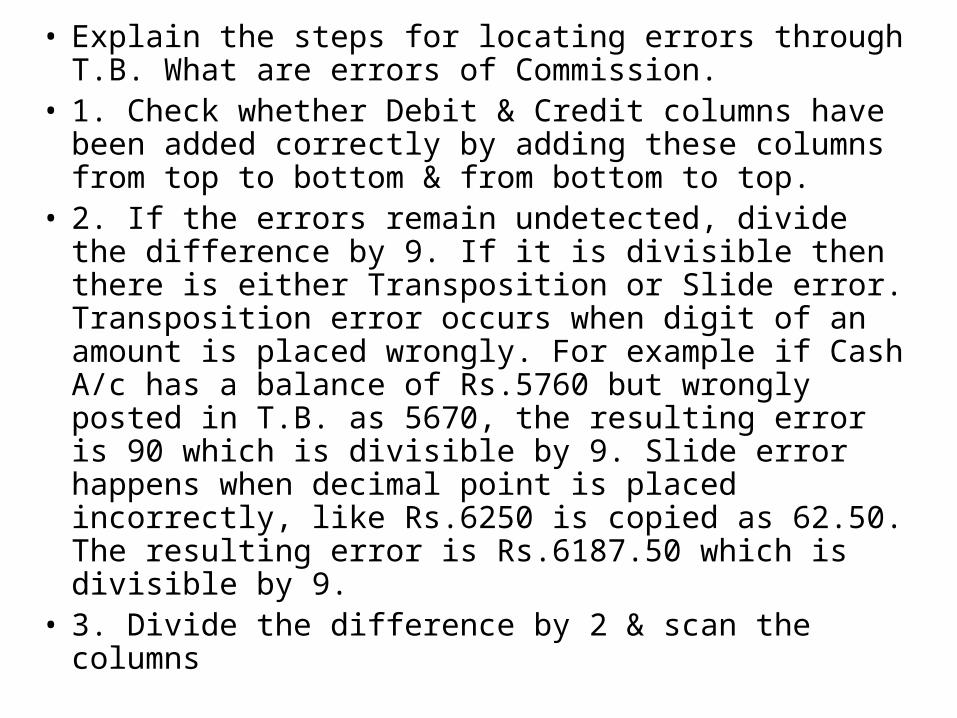

• Explain the steps for locating errors through T.B. What are errors of Commission.

• 1. Check whether Debit & Credit columns have been added correctly by adding these columns from top to bottom & from bottom to top.

• 2. If the errors remain undetected, divide the difference by 9. If it is divisible then there is either Transposition or Slide error. Transposition error occurs when digit of an amount is placed wrongly. For example if Cash A/c has a balance of Rs.5760 but wrongly posted in T.B. as 5670, the resulting error is 90 which is divisible by 9. Slide error happens when decimal point is placed incorrectly, like Rs.6250 is copied as 62.50. The resulting error is Rs.6187.50 which is divisible by 9.

• 3. Divide the difference by 2 & scan the columns

• for an identical amount. If Debit balance of Rs.250 has been entered in the Credit column of the T.B. it will cause a difference of Rs.500 in the T.B. total.

• 4. Check in the Ledger if any account shows a balance equal to the difference in the T.B.

• 5. Re-check the opening balances of all the accounts from the previous balance sheet.

• 6. Cross check the amount in the T.B. with the balances in the Ledger.

• 7. Re-compute the balances of each Ledger Account.• 8. If the errors remain undetected, check the postings

from Journal & other books of original entry.• 9. If the errors still remain undetected, repeat the

above steps with the help of other members of the staff.

Trial Balance is a conclusive proof of accuracy of accounts. Do you agree? If not, explain how & why? The main objective of preparing a Trial balance is checking of the arithmetical accuracy of the accounting entries. Trial balance represents a summary of all Ledger balances and, therefore, if the two sides of the Trial balance tally, it is an indication of the fact that the books of Account are arithmetically accurate. However, there may be certain errors in the books of Account in spite of an agreed Trial Balance. Different classes of errors are discussed below.

1. Errors of Omission – Such an error arises when any Transaction is either wholly or partially omitted to be recorded in the books. In the former case Trial balance will not be affected but for the later case the Trial balance will disagree.

2. Errors of commission – This error arise when transactions are incorrectly recorded, either wholly or partially. In the former case Trial balance will have no affect but for the later case Trial balance will not tally.

3. Clerical errors – It is a form of error of commission. This may consist of an incorrect posting, posting to the wrong account etc., Incorrect posting will make the Trial balance to

disagree but posting to the wrong account will not affect the agreement of the Trial balance.

4. Errors of Principle – An error of principle arises dueto recording of the transaction in a fundamentallyincorrect manner. It may be caused by treating arevenue item as an Asset or Liability, or vice versa.These errors will not make the T.B. to disagree.5. Compensating Errors – This is an error which iscounterbalanced by another error or errors of thesame amount either in the same account or differentaccounts. Such an error will not cause the Trialbalance to disagree.From the above it is clear that T.B. will agree in spiteof presence of many errors. Hence an agreed T.B.can not be regarded as a conclusive evidence of thecorrectness of the books of accounts, rather it may beregarded as a prima facie proof that the postings arein order.

Correct the following Trial Balance.

Debit Amount

(Rs.') Credit Amount

(Rs')

Return Outward 16000 Debtors 15,000

Opening Stock 34200 Carriage

Outward 5,000

Salaries 12000 Capital 55,200

Creditors 28000 Machinery 18,000

Bank 45000 Return Inward 3,000

Carriage Inward 6000 Discount

Received 4,000

Rent Received 3000 Trade Expenses 6,000

Discount Allowed 2000 Sales 140,000

Purchases 100000 Building 20,000

Bills Payable 20000

266,200 266,200

Debit Amount

(Rs.') Credit Amount

(Rs')

Building 20000 Capital 55,200

Machinery 18000 Sales 140,000

Purchases 100000 Creditors 28,000

Opening Stock 34200 Bills Payable 20,000

Debtors 15000 Return Outward 16,000

Bank 45000 Discount Received 4,000

Salaries 12000 Rent Received 3,000

Carriage Outward 5000

Carriage Inward 6000

Return Inward 3000

Discount Allowed 2000

Trade Expenses 6000

266,200 266,200

Preparation of Trading & Profit & Loss A/c

• What is a Profit & Loss A/c – Profit & Loss A/c discloses Net Profit or Loss made by a businessman or Trader by purchase & selling of goods.

• Why P&L A/c is prepared – It provides Net Profit or Loss earned during a particular period.

• It helps in comparing Profit or Loss of other periods.

• By comparing current year expenses with those of other years – It helps in controlling expenses.

• Allocation of profit & setting aside a part of it can be done.

• Adjustment entries required at the time of preparing Final A/c.

• Closing Stock – Closing Stock A/c Dr.• To Trading A/c.• O/s Expenses – Expenses due but not been paid.• Expenses A/c Dr.• To O/s. Exps A/c.• Prepaid Exps.- Exps paid in advance & relate to other

A/cing period. Prepaid Exps A/c Dr.• To Expenses A/c.• O/s Income – Income fallen due but not received.• O/s Income A/c Dr.• To Income A/c.

• Income recvd in Advance – Income of Subsequent A/cing period is recvd.

• Income A/c Dr.• To Income Recvd in advance A/c.• Depreciation - Normal Wear & Tear • Depreciation A/c Dr.• To Fixed Asset A/c.• Bad Debt - Debtors which is not receivable.• Bad Debt A/c Dr.• To Debtors A/c.• Prov. For Bad Debt – P & L A/c Dr.• To Prov. For Bad debt A/c.• Interest on Capital A/c- Interest on Cap A/c Dr.• To Capital A/c.• Interest on Drawing – Capital A/c Dr.• To Interest on Drawing A/c.

• Distinguish between TB & Balance Sheet – • Trial Balance - Debit & Credit balances of Ledger

A/cs are recorded.• It helps in checking Arithmetical accuracy of

Accounting entries. It forms the basis of preparing Final A/c.

• Balance Sheet – It is a statement & not Account.• It records Assets on the right side & Liabilities on

the left side of the statement.• It helps management to know financial position

of the firm.

• Distinguish between P&L A/c & B/S• P&L A/c – It discloses Net Profit or Loss made

during a particular period.• It records all income & expenses other than

those related to Trading A/c.• It is an A/c & not a statement.• It measures Profit or Loss made from the

business.• Balance Sheet – It is a statement & not Account.• It records Assets on the right side & Liabilities on

the left side of the statement.• It helps management to know financial position

of the firm.

• Advantages of preparing Accounts in Vertical form.

• Here Trading Profit & Loss Account is presented in the form of a statement in a vertical form.

• It is easier to read & understand specially by those who are not from commercial background.

• It records Income from operations i.e., credit side of P&L A/c first then expenses relating to operation of business are deducted i.e., debit side of Trading & P&L A/c.

• Presently Income & expenditure from operations from businesses are presented by many organization in the vertical format. Since it is easier for common person to understand and it has their acceptability.

Preparation of Balance sheet.

• Discuss the treatment of Prepaid expenses & Outstanding expenses at the time of preparation of Final account.

• Outstanding Expenses - Expenses due but not been paid.

• Expenses A/c Dr.• To O/s. Expenses A/c.• Prepaid Expenses - Expenses paid in

advance & relate to other Accounting period.

• Prepaid Expenses A/c Dr.• To Expenses A/c.

• Discuss the treatment of Depreciation & Closing Stock at the time of preparation of Final account.

• Closing Stock - Closing Stock A/c Dr.

• To Trading A/c.

• Depreciation - Normal Wear & Tear

• Depreciation A/c Dr.

• To Fixed Asset A/c.

• What are Capital reserves? How are they created?

• Capital reserves are those which are not generally distributed as Profits. They arise mainly out of the following :

• 1. Capital receipts, e.g. issue of shares or debentures at a premium.

• 2. Non-trading incomes during the period prior to incorporation.

• Capital reserves may or may not involve any receipts of cash.

• Differentiate between Reserve & Reserve fund.• Funds are referred to as assets for specific

purposes, which are not generally available for normal business activities.

• Reserves are not usually represented by earmarking assets. If they are, they are expressed as Reserve fund.

• For example, if an organization sets aside profits for Building construction, the reserve so created is known as Building Funds.

• A reserve fund is usually created either to replace a fixed asset at the end of its useful life or to repay a liability in the future, e.g. redemption of Debentures.

• What are Secret reserve?• A secrete reserve is a reserve that is created but

not stated in a balance sheet. There are various ways of creating secrete reserves. The banks, insurance companies and other financial institutions wants to win public confidence for there successful working. These concerns can create secret reserves. It is a technique to show poor financial position and in case of need such reserves are available to meet crisis.

• A secret reserve is created by the following methods:

• 1. By under valuation of assets much below their cost or market value.

• 2. By not writing up the value of an asset, the price of which has permanently gone up.

• 3. By creating excessive reserve for bad & doubtful debts.

• 4. By providing, excessive depreciation on fixed assets.

• 5. By writing down goodwill to a nominal value.• 6. By omitting some of the assets altogether from B/S.• 7. By overvaluing the liabilities.• 8. By the inclusion of fictitious liabilities.• 9. By showing contingent liabilities as actual liabilities.• Object of creating secret reserve• Secret reserves strengthen the financial position of a

concern, losses can be made good without disclosing their occurrence to the shareholders & others. This helps the concern to remain financially strong in spite of a period of adversity.

Final Account Adjustments

• How is Goods in Transit & Goods lost by Fire are treated in Final A/c?

• INSURANCE IN TRANSIT:while bringing goods from outside, they may be destroyed or stolen in transit .such loss may be insured against. The amount of premium paid to the insurance company is debit to the insurance in Transit a/c and is transferred to the debit side of the trading a/c being an expense connected with the purchased of goods.Trading A/c Dr.

To Insurance in Transit A/c

• If a portion of good is lost by Fire then the value of such loss is first to be ascertained. Then pass

Accidental Loss A/c Dr.

To Trading A/c• If the above loss is covered under Insurance then

pass

Insurance claim A/c Dr.

Profit & Loss A/c Dr. (Claim not admitted)

To Accidental Loss A/c. • When the claim is settled then pass

Bank A/c Dr.

To Insurance claim A/c.

• What are the uses & limitations of Balance sheet?• Uses of Balance sheet :• The lender can ascertain the financial position of

the business.• It helps to ascertain capital employed in the

business.• It serves as the basis for the acquisition of the

business.• Trends of W.C. of the business can be determined

& corrective measures taken if required.• It helps to ascertain owners interest in the

business.• Different ratios calculated & can be used for better

management of the enterprise.

• Limitations of Balance sheet :• Fixed assets shown in the balance sheet are at

historical cost less depreciation which is not the true value of the assets.

• Balance sheet can not reflect the value of certain factors such as skill & loyalty of employees.

• Conventional balance sheet may mislead a reader in inflationary situation.

• The value of Current assets depend upon some estimates, so it can not reflect the true liquidity position of the business.

• Define Assets & their classification.• Assets are resources, tangible & intangible, from

which probable future economic benefits are obtained & the rights to which have been acquired by the entity as a result of past transactions.

• The assets are the valuable resources owned by a business. Assets are classified into following four groups :

• Fixed Assets.• Current Assets.• Fictitious Assets. (Preliminary expenses,

• Define Liabilities & their classification.• Liabilities are obligations which arise from

transactions or other events that have already been occurred. Liabilities are the claims of the outsiders against the business or the amount that the business owes to its providers other than its owners.

• Liabilities can be classified into the following three groups :

• Fixed Liabilities. (Long term liabilities)• Current Liabilities.• Contingent Liabilities. (Not recorded in the

Balance sheet but are disclosed as note to accounts in the audit report)

Accounting of Non Trading organizations-I.

• Explain the meaning of Subscription, Donation & Life Membership Fees.

• Subscription – These are amounts received or receivable from the members of a Non Profit making organization for being entitled to the service rendered by it. This is a major source of Income of a Non Trading concern. For example a Club receives membership fees, Society receives monthly subscription from its members etc., The Receipt & Payment A/c records actual subscription received while the Income & Expenditure A/c records only the subscriptions which relate to the Accounting period, whether received or not.

• Donation – Are amounts given by members or outsiders for the general functioning of a Non Profit organization or for a particular purpose, not in anticipation of any return, but simply as a token of appreciation of the organization’s services to the society.

• (i) Specific Donation is received for a specific purpose. For example donation given for construction of Building or for giving prizes to a the best sportsman. It is taken on the Liability side of the Balance sheet & used only for the purpose for which it is meant.

• (ii) General Donation is received not for a specific purpose. If the donation is small &

• Recurring in nature then it can be taken to the Income & Expenditure A/c. If the donation amount is substantial & non recurring in nature then it is taken in the Liability side of the B/s.

• Life Membership Fee – is received for making life time member. Members will have to pay fees only once in their life time & enjoy benefit of the institution for the whole life. The amount received can be dealt in the A/c by any of the following methods.

• (i) The amount is treated as Capital receipt & shown in the Liability side of the B/s.

• (ii) It may be credited to a separate A/c i.e., Life membership Fee A/c. Normal annual subscription

may be transferred to Income & Expenditure A/c & balance may be carried forward till it is exhausted. In the case of death of a member balance may be transferred to Capital Fund A/c.

• (iii) The amount received is credited to Life membership fee A/c. Annual contribution according to average life of a member may be transferred from this A/c to the Income & Expenditure A/c.

• Differentiate between Receipt & Payment A/c & Income & Expenditure A/c.

• 1. R&P A/c shows inflow & outflow of cash similar to Cash book of non trading concern. I&E A/c is a revenue A/c of a non trading concern resembling the P&L A/c of a Trading concern.

• 2. R&P A/c includes both capital & revenue items but I&E A/c represents only revenue items.

• 3. R&P A/c deals with income & expenses in cash during the current period. But I&E includes prepaid & outstanding incomes & expenses.

• 4. R&P A/c includes expenses & incomes of previous, current & future periods. But an I&E A/c include only expenses & income for the current accounting period.

• 5. Depreciation of assets, Bad debt, Provisions etc. are not included in R&P A/c but included in I&E A/c.

• 6. In R&P A/c income is shown on debit side & expense is shown on the credit side as in a cash book. But in I&E A/c the expense is shown on the debit side & income is on credit side as in a P&L A/c.

• 7. A R&P A/c starts with opening & closing balance whereas I&E A/c does not start with opening balance but usually ends with a closing balance (deficit or surplus)

• 8. The closing balance of R&P A/c is to be carried forward in the same A/c but closing balance of I&E A/c is transferred to capital fund of the concern.

• 9. R&P A/c is not followed by B/S but I&E A/c is usually followed by a B/S.

Accounting of Non Trading organizations-II.

• Distinguish between accounting for a trading A/c & accounting for a non trading A/c.

• 1. Main objective of a Trading concern is to earn profit for the owners, but the objective of a Non Trading concern is to render social service.

• 2. Trading A/c includes Trading P&L A/c followed by B/S whereas in non trading A/c I&E A/c is prepared followed by B/S.

• 3. Excess of revenue income over expenditure in a trading concern is called Profit & in non trading concern it is termed as excess of income over expenditure.

• 4. In case of trading concern profit accrues to the owner whereas in non trading concern surplus enhances the capital fund of the concern to be utilized by the concern only.

• 5. Profit of a trading concern arises out of excess of sales revenue over cost of sales but in a non trading concern it is the difference of income from subscription, donation etc., over expenses.

• Meaning of Receipt & Payment A/c.• It is a summary of cash transactions under proper

heads during the accounting period. It is a summary of cash book. Cash book contains record of cash receipt & payments in the chronological order of date while the R&P A/c is a summary of receipts & payments under different heads. For example a club receives subscription from its members on different dates, they will be recorded on these dates separately in the cash book but R&P A/c will contain total subscription received during the accounting year. It records all cash receipts & payments, irrespective of the fact

• whether they are of capital or revenue in nature or whether they relate to the current year or not. R&P A/c generally starts with opening balance & ends with balance at the end of the accounting year.

• Meaning of Income & Expenditure A/c.• An I&E A/c records all revenue income &

expenses relating to the period for which account is being prepared. It is similar in form to the P&L A/c of a trading concern. It shows all revenue expenses on the debit side & revenue incomes on the credit side. In case of both income & expenses, adjustments are to be made for amount due & prepaid.

• Items like Depreciation on fixed assets, bad debt etc are to be brought in the A/c. Final balance represents surplus income over expenditure or a surplus expenditure over income for the period. This is added or deducted form an A/c called Capital fund or Accumulated fund or General fund.

Capital & Revenue Expenditure

• What is capital & revenue expenditure. Distinguish between them.

• Capital expenditure is an expenditure the benefits of which is consumed in several accounting periods. It is, therefore, of non-recurring nature. Examples are :

• Expenses incurred for acquiring fixed assets, for making additions to existing fixed assets, benefits of enduring nature, like goodwill, patent & copy right.

• Revenue expenditure is an expenditure incurred in an accounting period & benefits of which is also consumed in the same period. It is of recurring in nature.

• Examples are :• It includes expenses incurred for acquiring assets

for resale or for conversion into finished products, repairs & maintenance, various trade charges like rent, rates & taxes, salaries, wages, carriage etc.

• Distinction between capital & revenue expenditure are :

• Benefits of capital expenditure is spread over several accounting periods but of revenue expenditure is consumed in one accounting period.

• CE is of non recurring nature & RE is of recurring nature.

• CE increases the earning capacity of the business

but not Revenue Expenditure.

• All items of CE appear in the Asset side of the balance sheet & that of RE appear in the debit side of the P&L A/c.

• What are capital & revenue receipts? Distinguish between them.

• Capital receipts comprises contribution by proprietors or partners towards the capital of their business or in case of a company subscription towards share capital or debenture, any loan etc. Thus CR generally create a liability either to outsiders or to the proprietors.

• Revenue receipts, do not create any liability & comprise sale proceeds of stock, interest on investment, commission earned, discount received etc. Thus Revenue receipt is of recurring in nature.

• Distinction between CR & RR are :• CR is of non recurring nature & RR is of recurring

nature.• CR creates liability but RR does not create nay

liability to the organization.• CRs are shown in the Liability side of the balance

sheet but RRs are shown on the credit side of the P&L A/c.

• Capitalised expenditure – It is an expenditure which is of revenue in nature but incurred for acquiring any asset or for adding value to it.

• Examples are : • Repair charges, purchase of material & wages

as part of construction or erection, carriage & legal expenses.

• Deferred revenue expenditure – This is an expenditure of a revenue in nature the benefits of which extends beyond the accounting period. The unwritten portion which is carried forward to the subsequent years is referred to as deferred

revenue expenditure & is shown on the asset side of the balance sheet.

• Examples are :• Discount allowed on issue of debentures,

expenditure on an advertisement campaign or on a scientific experiment.

Rectification of Errors

• Explain the different stages of rectification of errors.• Errors in accounts may be discovered & might call

for rectification in any of the following stages :• Before preparation of Trial Balance-First stage• Before preparation of Final Account-Second stage• After the preparation of the Final Accounts-Third

stage.• First stage rectification – The errors may come to

light during the course of the accounting period & before the books are closed. If it is a double sided error, a suitable entry will have to be passed in order to reverse the effect & bring about the correct situation.

• Furniture purchased for Rs.1000 is wrongly debited to purchase account. So rectifying entry to be passed is Debit Furniture A/c & credit Purchase A/c with Rs.1000.

• If the error is one sided then rectification will be made directly in the ledger by debiting or crediting the account affected by the error.

• If an item of Rs.700 on the credit side of the cash book in respect pf salaries paid is posted to the debit of salaries account as Rs.70, the error is one sided & will be rectified by debiting salaries account to error due to wrong posting from cash book with Rs.630.

• Second stage rectification – here the error remained undetected at the time of preparation of Trial balance & Trial balance is made to agree by transferring the difference to Suspense A/c.

• Any double sided error is rectified in the same way as in the first stage. One sided error will however be rectified by passing a journal entry through Suspense A/c. Thus in the above case the rectifying entry to be passed will be Debit salary A/c & credit Suspense A/c with Rs.630.

• Third stage rectification – If in spite of repeated efforts, the errors can not be detected, Final A/c may be prepared showing the suspense A/c in it. Debit balance being shown on the Asset side & Credit balance shown on the Liability side.

• An error in the previous accounting period affected a revenue or an expense account & effect would creep into the P&L A/c & subsequently into Capital A/c. Thus for rectification of such an error, the P&L A/c or the Capital A/c is to be Debited or Credited as the case may be.

• The two errors cited above will be rectified as follows :

• Furniture A/c Dr. Rs.1000• To Capital A/c Rs.1000• Capital A/c Dr. Rs.630• To Suspense A/c Rs.630