121

2013

2013

Binder Regulations

2

Topics 1. Principles informing the Binder Regulations

2. Binder functions

3. Remuneration

4. Information Letter 8/2012

5. Draft Information Letter 3/2013

6. FAQ’s

3

1. Principles informing Binder Regulations

• Accountability of insurer

• Responsible outsourcing

• Policyholder protection

• Avoid conflicts of interest

4

2. Binder functions On behalf of the insurer

• Entering into, varying or renewing of policies

• Determining policy wording

• Determining premiums

• Determining the value of policy benefits

• Settling claims

5

Binder functions (cont)

• Functions that a binder holder performs as agent of the insurer

• As if the binder holder were the insurer when interacting with policy holders

• Actual entering into, varying or renewing of a policy

• Insurer only knows after the fact

6

3. Remuneration

Principle

• a policy holder should not pay twice for the provision of the same or similar service

• NB when an intermediary performs binder functions and intermediary services

7

Remuneration (cont)

• Must be reasonable commensurate with the actual costs associated with rendering the services under the binder agreement

• Reasonable rate of return

• Binder fee may be expressed as a % of gross premium or fixed Rand amount

8

Remuneration (cont) • UM

Profit share and/or binder holder fee

Outsourcing fee

• NMI

Binder holder fee

Outsourcing fee

Commission

Section 8(5) fee

9

4. Information Letter 8/2012

• Published 4 December 2012

• Guidance

Activities constituting binder functions

Remuneration

• Supervisory approach

10

Info Letter 8/2012 (cont)

Monitoring

Reporting template

Reasonableness of remuneration

On-site visits

Regulatory and/or enforcement action

1 January 2013

Diligent efforts

90 Days alignment period

11

Info Letter 8/2012 (cont)

System changes

Policyholder information

Detailed actions plans

1 January 2014

ACORD standard encouraged

12

5. Draft Information Letter 3/2013

• Still in draft

• Published 30 April 2013

• Public comment 31 May 2013

• Guidance:

Activities constituting binder functions

Remuneration

13

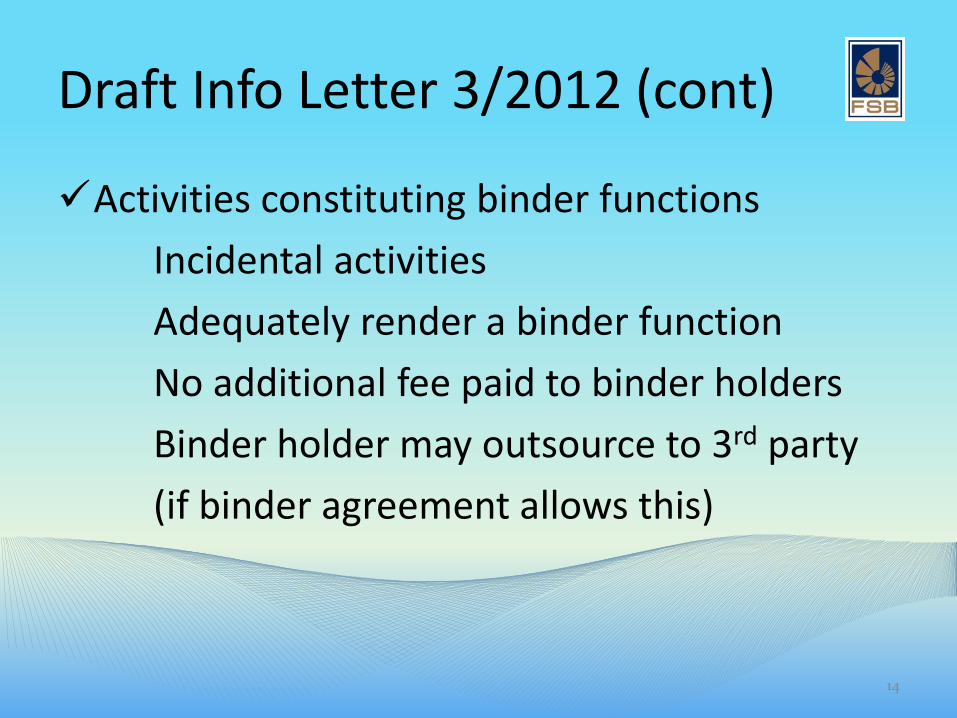

Draft Info Letter 3/2012 (cont)

Activities constituting binder functions

Incidental activities

Adequately render a binder function

No additional fee paid to binder holders

Binder holder may outsource to 3rd party

(if binder agreement allows this)

14

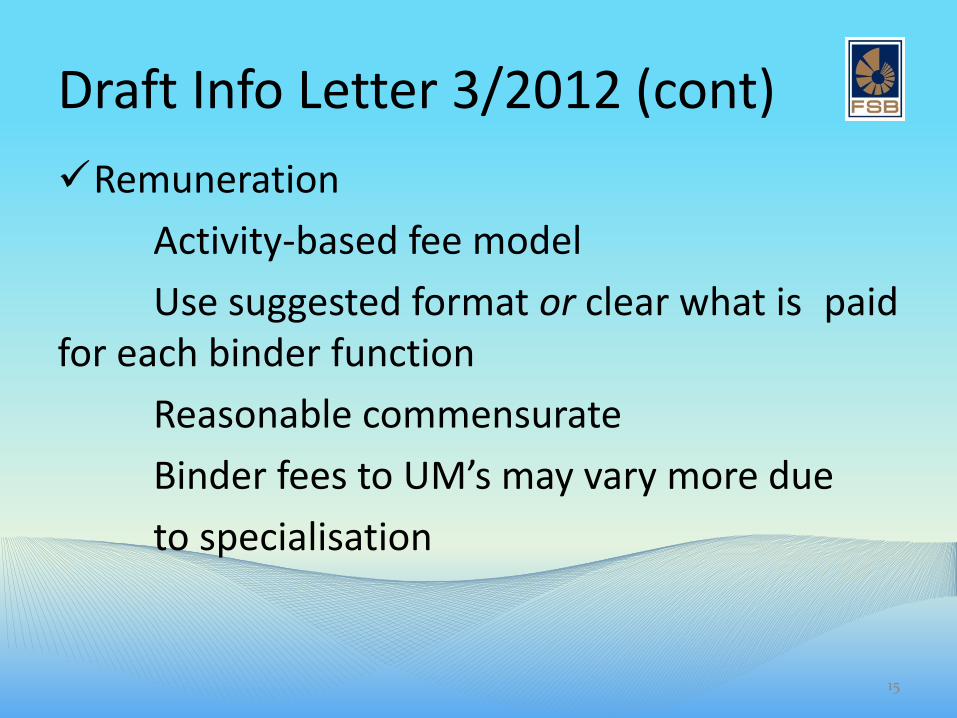

Draft Info Letter 3/2012 (cont)

Remuneration

Activity-based fee model

Use suggested format or clear what is paid for each binder function

Reasonable commensurate

Binder fees to UM’s may vary more due

to specialisation

15

Replacement Policies

16

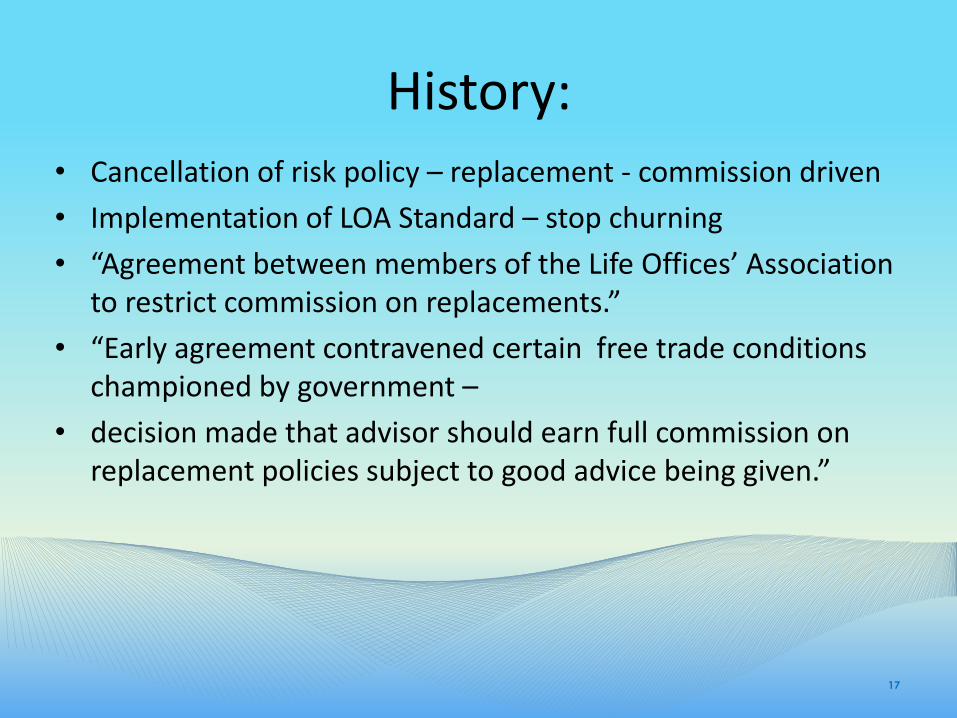

History:

17

• Cancellation of risk policy – replacement - commission driven

• Implementation of LOA Standard – stop churning

• “Agreement between members of the Life Offices’ Association to restrict commission on replacements.”

• “Early agreement contravened certain free trade conditions championed by government –

• decision made that advisor should earn full commission on replacement policies subject to good advice being given.”

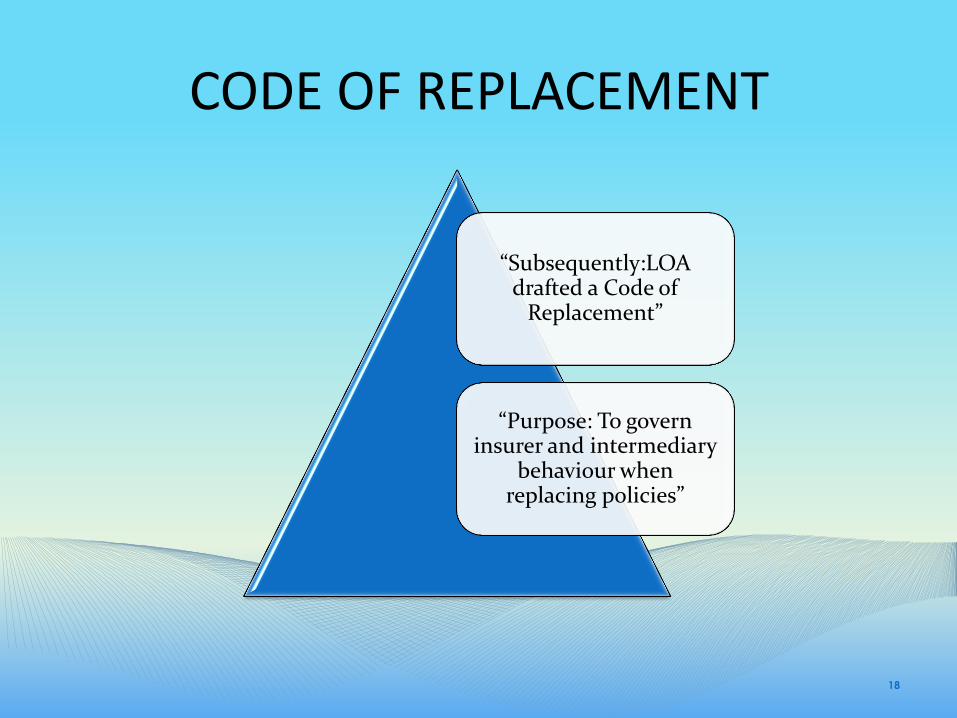

CODE OF REPLACEMENT

18

“Subsequently:LOA drafted a Code of

Replacement”

“Purpose: To govern insurer and intermediary

behaviour when replacing policies”

• “Code reconstituted by Asisa from 1 January 2012”

• “Member life offices of ASISA have agreed to“ASISA STANDARD ON REPLACEMENT”- applicable to all business effected in RSA”

• “Purpose: To provide Rules to govern instances where one member life office (the replacing insurer) has or intends to replace a policy or policies of another member life office (the replaced insurer).”

• In implementation of the “Standard” outcomes must be in line with the requirements of Treating Customers Fairly ( TCF)

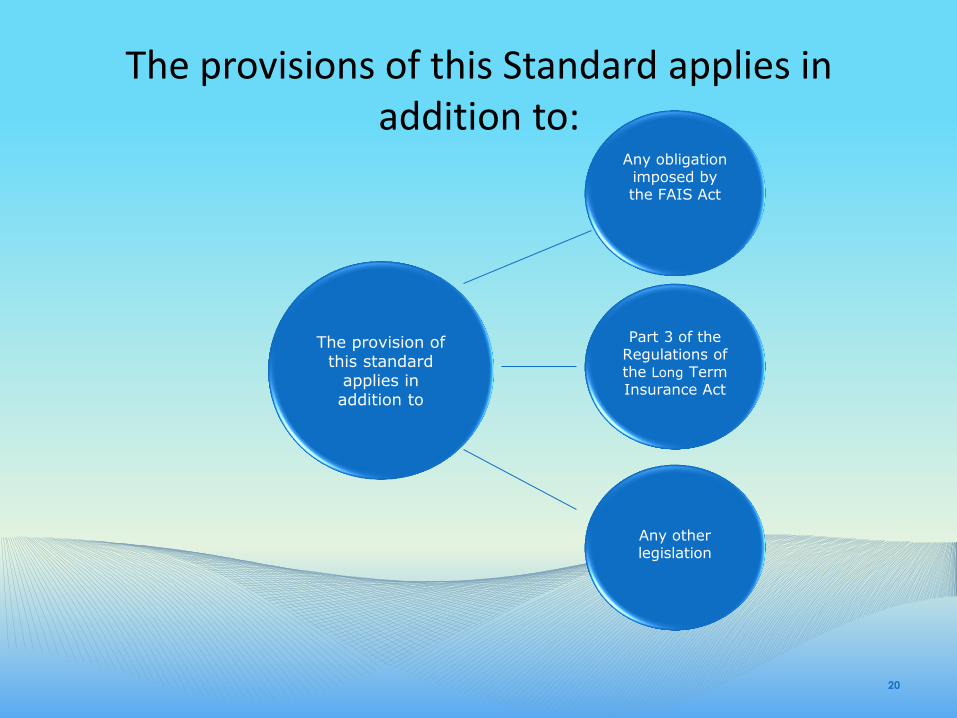

19

The provisions of this Standard applies in addition to:

20

The provision of this standard

applies in addition to

Part 3 of the

Regulations of the Long Term Insurance Act

Any obligation imposed by the FAIS Act

Any other legislation

21

If conflict arises

22

Then legislation prevails

• “August 2012 the Standard on Replacement was tweaked to introduce a more comprehensive Replacement Policy Advice Record (RPAR) – applicable to all stakeholders.”

• “From 1 January 2013: Both financial Advisors and direct marketers will complete and submit the same questionnaire - on behalf of the client to the insurer”

23

WHAT DOES THE ASISA STANDARD

REQUIRES ADVISORS TO DO ?

24

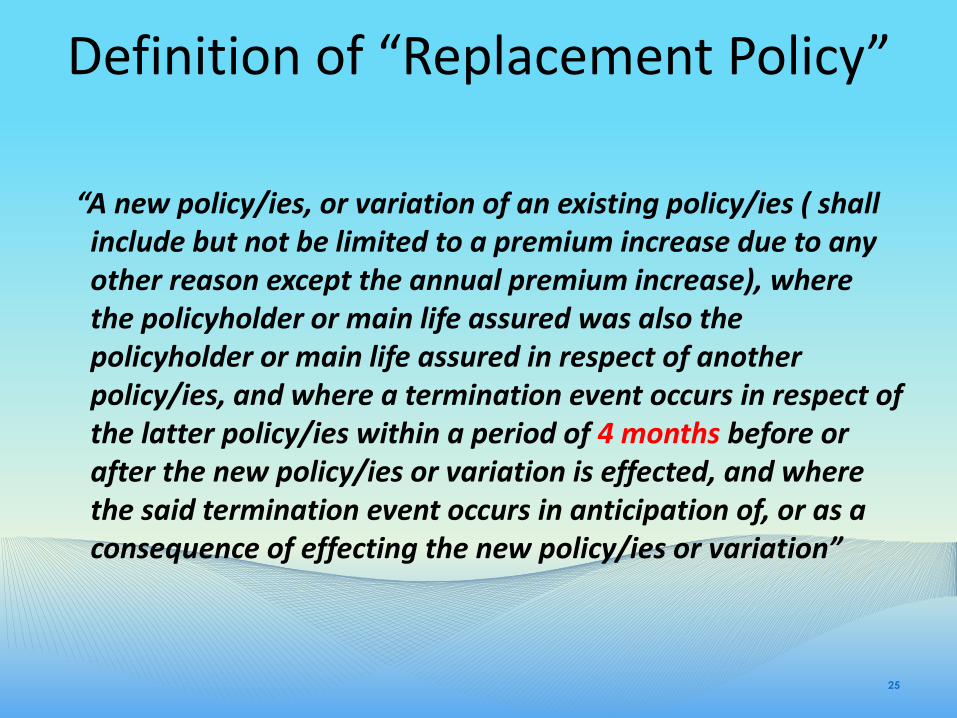

Definition of “Replacement Policy”

“A new policy/ies, or variation of an existing policy/ies ( shall include but not be limited to a premium increase due to any other reason except the annual premium increase), where the policyholder or main life assured was also the policyholder or main life assured in respect of another policy/ies, and where a termination event occurs in respect of the latter policy/ies within a period of 4 months before or after the new policy/ies or variation is effected, and where the said termination event occurs in anticipation of, or as a consequence of effecting the new policy/ies or variation”

25

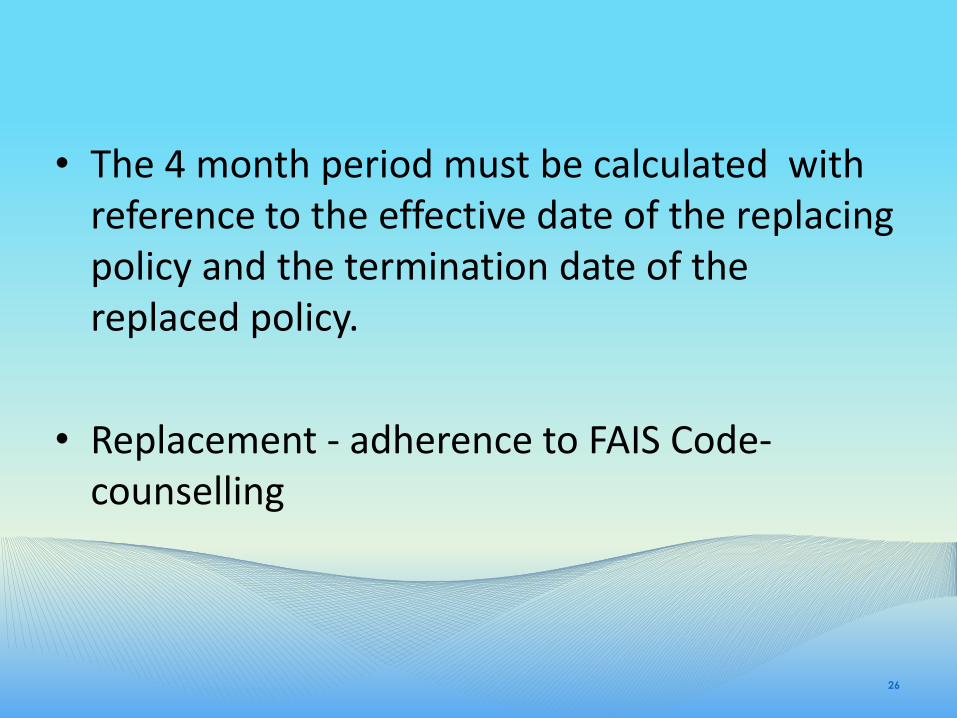

• The 4 month period must be calculated with reference to the effective date of the replacing policy and the termination date of the replaced policy.

• Replacement - adherence to FAIS Code- counselling

26

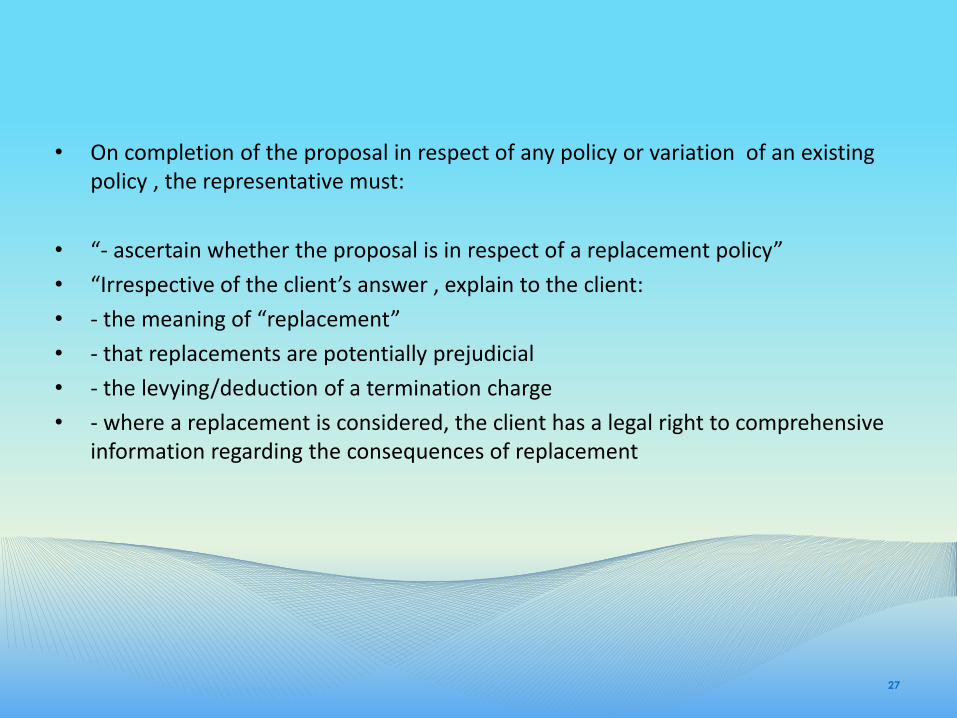

• On completion of the proposal in respect of any policy or variation of an existing policy , the representative must:

• “- ascertain whether the proposal is in respect of a replacement policy”

• “Irrespective of the client’s answer , explain to the client:

• - the meaning of “replacement”

• - that replacements are potentially prejudicial

• - the levying/deduction of a termination charge

• - where a replacement is considered, the client has a legal right to comprehensive information regarding the consequences of replacement

27

• “The Standard does not limit the rights of the policyholders,

RATHER:

• It affirms the legal requirement that the replacement is done on a fully informed decision”

28

WHAT IS THE RESPONSIBILITY OF THE MEMBER LIFE OFFICES?

29

Responsibility of the member life offices:

• To ensure:

• - All representatives are properly trained - they understand the potential and real disadvantage of inappropriate replacements

• - They follow all practices that prevent inappropriate replacements – giving effect to the Standard

• - They make compliance with this Standard a term of their contractual

relationship with all representatives – non compliance equates to a breach of contract / misconduct

30

• “Onus is on the advisor to ensure whether the client is replacing an existing policy.”

• “To “remind” advisors of this requirement , the insurers have included a prescribed replacement questionnaire on their new business application form."

• “The ASISA Standard on Replacement requires the advisor to ask the client whether the new policy replaces all or part of their existing policy”

• “If the answer is yes then the RPAR needs to be completed.”

• “Must be submitted together with the proposal form to the replacing insurer”

31

• Replacing insurer must within 5 working days of receipt of the proposal , transmit the RPAR to the replaced insurer by email

• Member life offices may not deviate from the prescribed format of the RPAR unless express consent has been obtained from ASISA

32

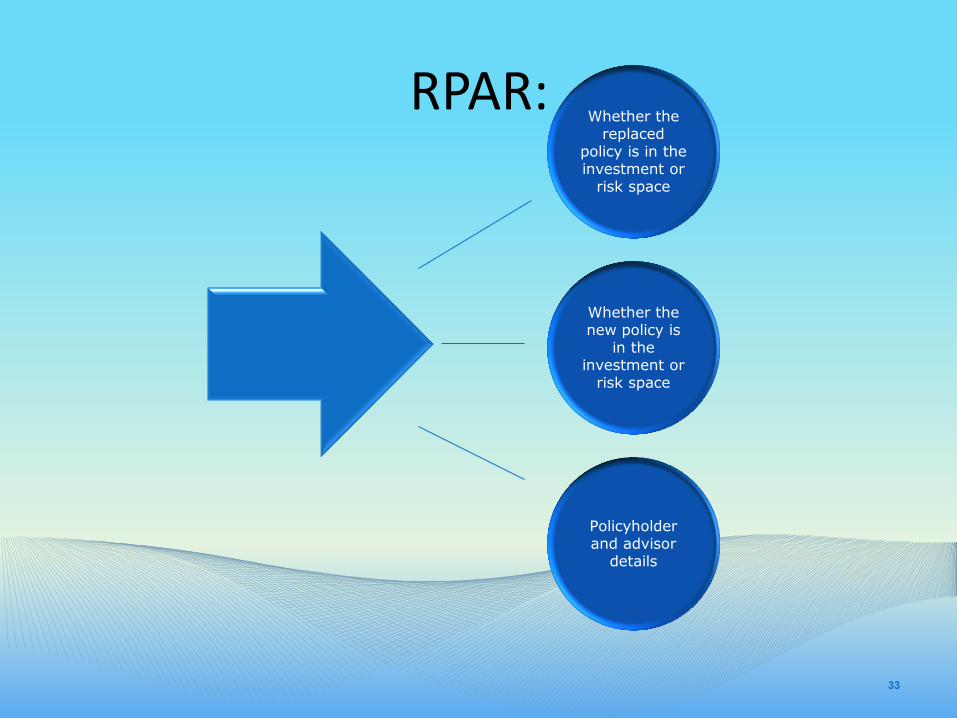

RPAR:

33

Whether the replaced

policy is in the investment or

risk space

Whether the new policy is

in the investment or

risk space

Policyholder and advisor

details

• Replacing insurer may not directly or indirectly provide the representative with any commission, fee, incentive, remuneration for the replacement policy until all requirements have been satisfied

• Upon replacement: the replaced insurer may take whatever action it deems appropriate to advise the client of the clients rights in terms of this Standard and FAIS or to attempt to conserve the replaced policy

• The replaced insurer is required to take action in good faith and with due regard to the interests of policyholders, representatives and the industry as a whole

34

WHAT ARE THE DANGERS OF REPLACEMENTS?

35

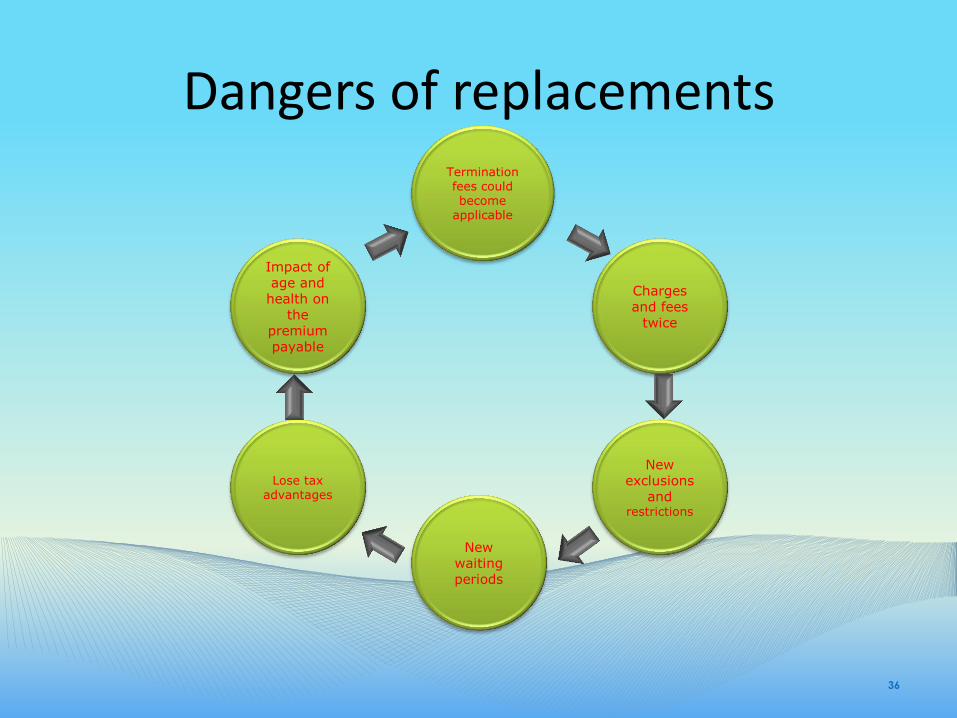

Dangers of replacements

36

Termination fees could become

applicable

Impact of age and

health on the

premium payable

New exclusions

and restrictions

Charges and fees

twice

New waiting periods

Lose tax advantages

WHAT IS NON - COMPLIANCE?

37

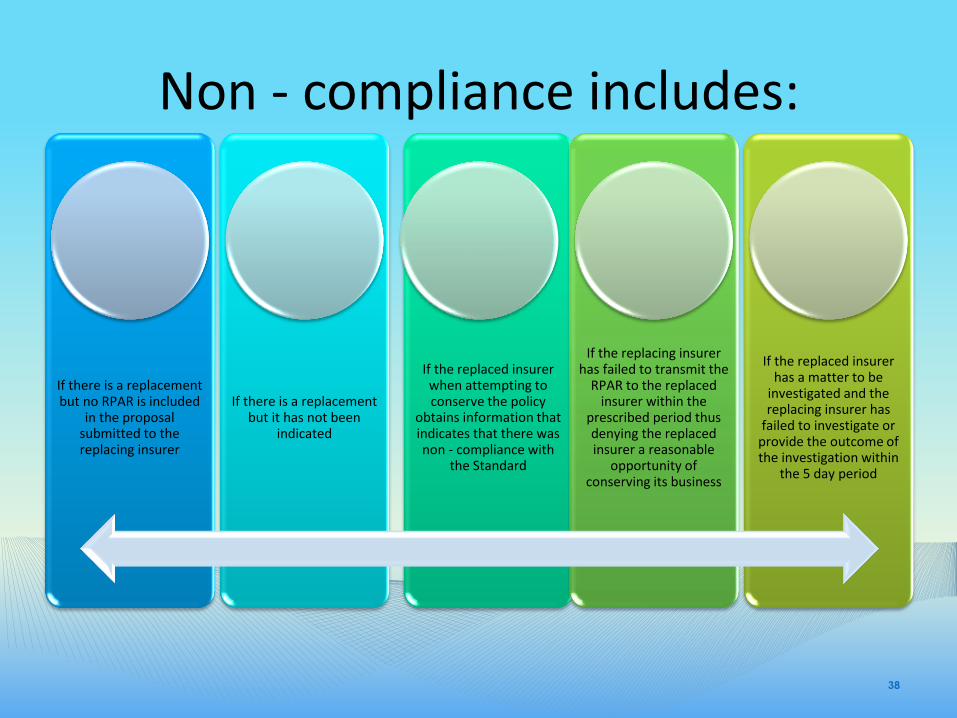

Non - compliance includes:

If there is a replacement but no RPAR is included

in the proposal submitted to the replacing insurer

If there is a replacement but it has not been

indicated

If the replaced insurer when attempting to conserve the policy

obtains information that indicates that there was non - compliance with

the Standard

If the replacing insurer has failed to transmit the

RPAR to the replaced insurer within the

prescribed period thus denying the replaced insurer a reasonable

opportunity of conserving its business

If the replaced insurer has a matter to be

investigated and the replacing insurer has

failed to investigate or provide the outcome of the investigation within

the 5 day period

38

WHAT IS THE PURPOSE OF THE TRIBUNAL?

39

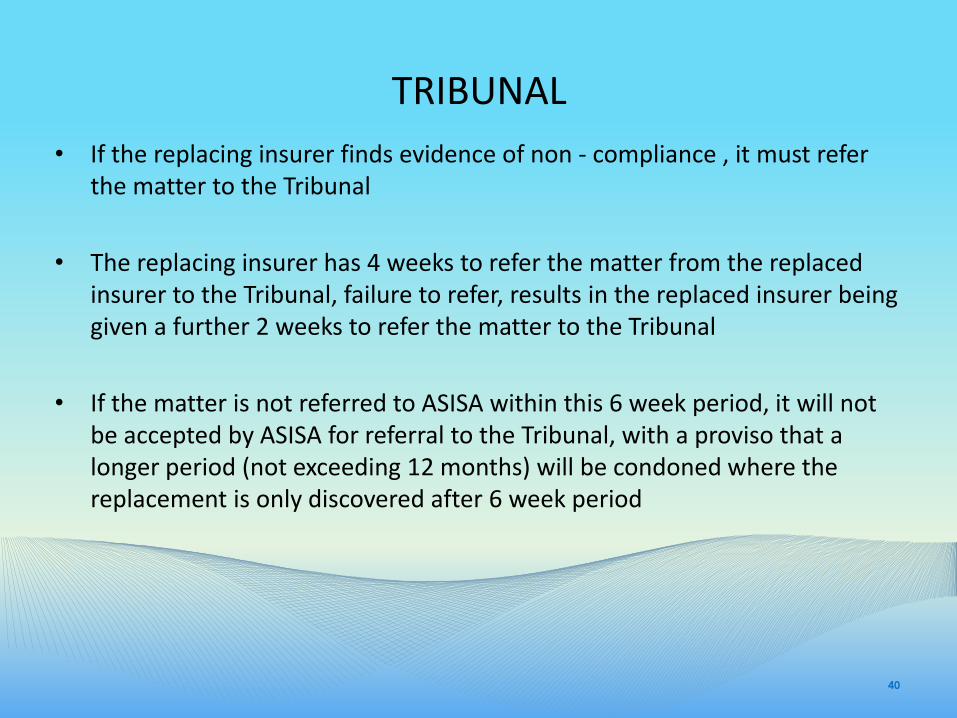

TRIBUNAL

• If the replacing insurer finds evidence of non - compliance , it must refer the matter to the Tribunal

• The replacing insurer has 4 weeks to refer the matter from the replaced insurer to the Tribunal, failure to refer, results in the replaced insurer being given a further 2 weeks to refer the matter to the Tribunal

• If the matter is not referred to ASISA within this 6 week period, it will not be accepted by ASISA for referral to the Tribunal, with a proviso that a longer period (not exceeding 12 months) will be condoned where the replacement is only discovered after 6 week period

40

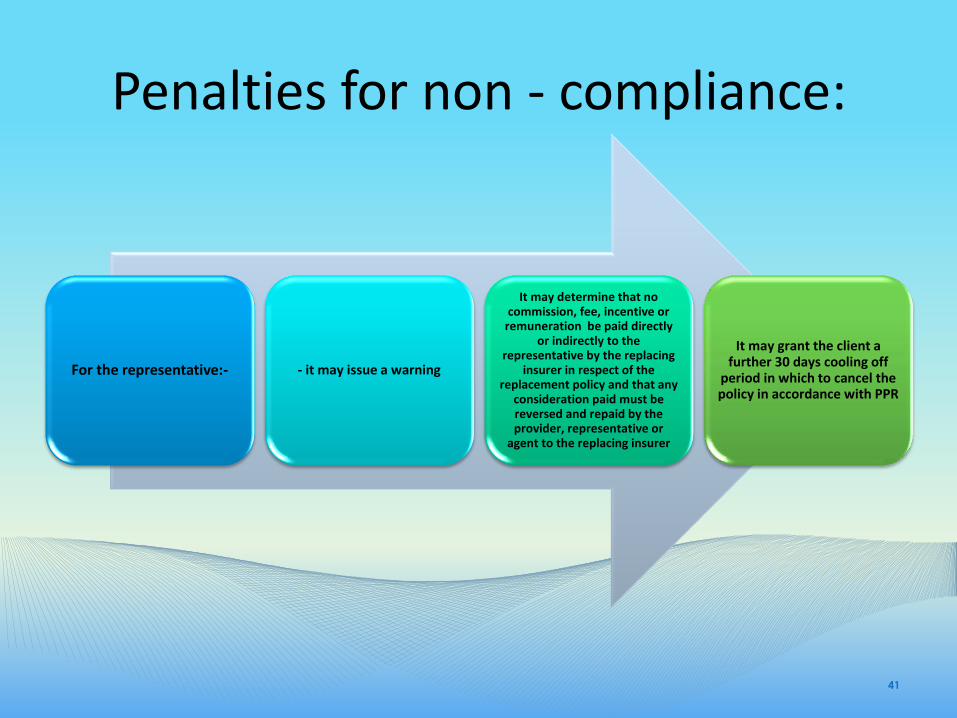

Penalties for non - compliance:

For the representative:- - it may issue a warning

It may determine that no commission, fee, incentive or

remuneration be paid directly or indirectly to the

representative by the replacing insurer in respect of the

replacement policy and that any consideration paid must be reversed and repaid by the provider, representative or

agent to the replacing insurer

It may grant the client a further 30 days cooling off

period in which to cancel the policy in accordance with PPR

41

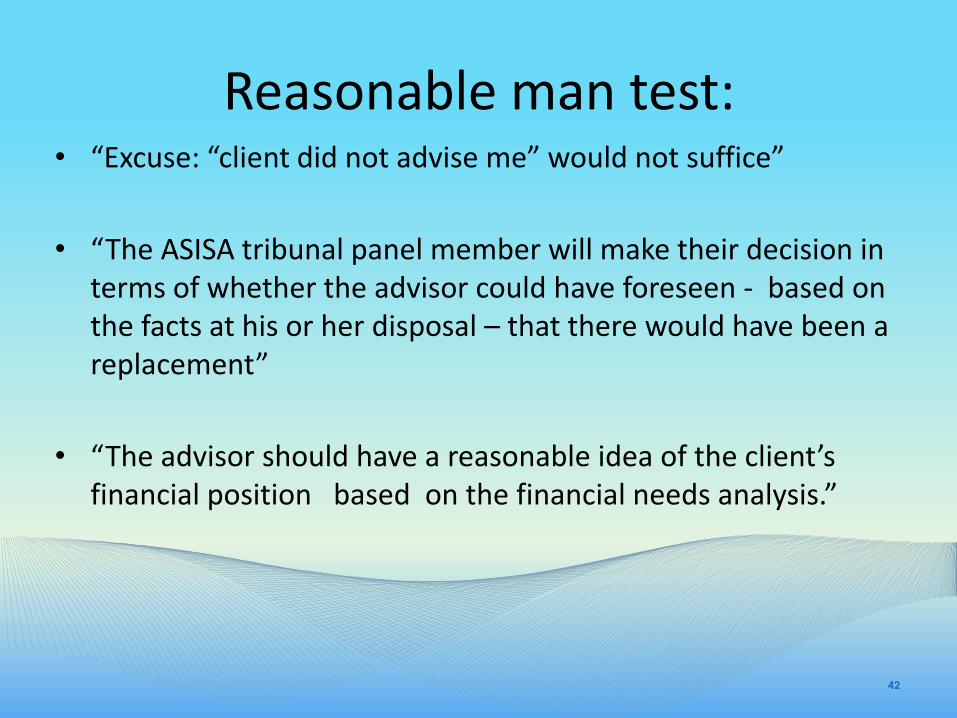

Reasonable man test: • “Excuse: “client did not advise me” would not suffice”

• “The ASISA tribunal panel member will make their decision in terms of whether the advisor could have foreseen - based on the facts at his or her disposal – that there would have been a replacement”

• “The advisor should have a reasonable idea of the client’s financial position based on the financial needs analysis.”

42

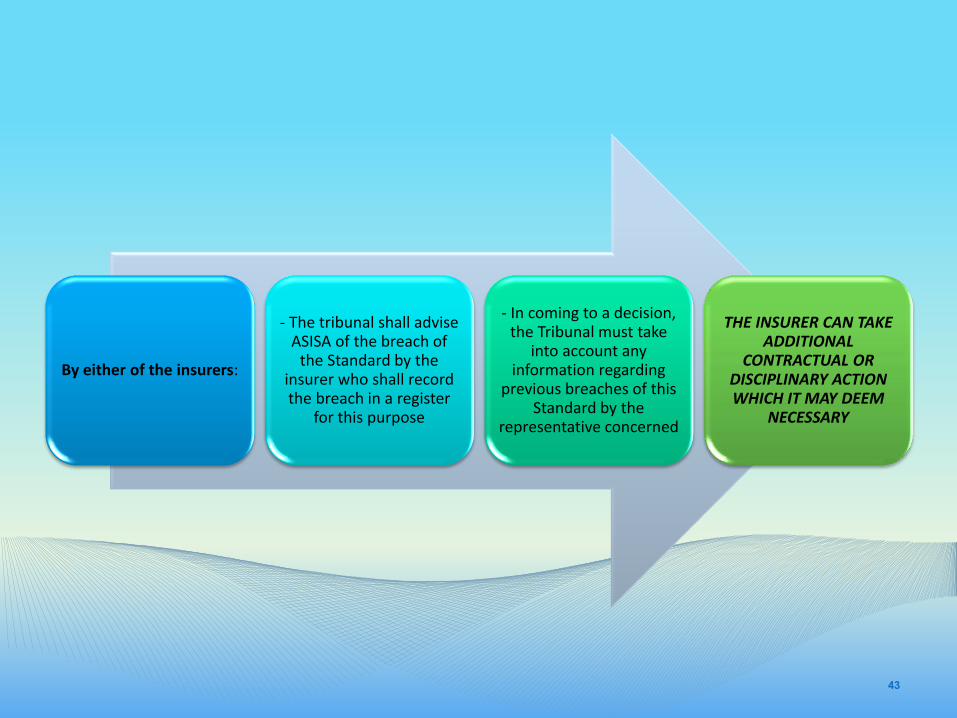

By either of the insurers:

- The tribunal shall advise ASISA of the breach of

the Standard by the insurer who shall record the breach in a register

for this purpose

- In coming to a decision, the Tribunal must take

into account any information regarding

previous breaches of this Standard by the

representative concerned

THE INSURER CAN TAKE ADDITIONAL

CONTRACTUAL OR DISCIPLINARY ACTION WHICH IT MAY DEEM

NECESSARY

43

REALITY............

44

• “If correct procedures are followed, then there is no need for the regulator to intervene”

• “By adhering to the ASISA Standard, the advisors can ensure that the replacement was handled on an informed basis.”

45

Replacement Policies

• Huge concern: Churning – Twisting or churning is the process of using the cash value of one

policy to purchase another policy with a larger benefit.

– Churning can also refer to a practice where the broker encourages the policy holder to cash in policies with a cash value and persuading them to pay for new cover with the proceeds.

– Churning thus refers to the practice where a FSP or representatives of a FSP convince a customer (new or existing) to replace an existing policy for another policy or product which has similar features and benefits.

46

Why does this happen?

• The reason why this is done is to enable the FSP/ representative to:

• meet sales targets that are set by either the FSP or product supplier or both, and

• to earn commission.

47

Some possible effects

• While the policyholder may acquire a policy with a larger death benefit, replacements often uses up the cash value that has built up in the original policy over the years. In some instances, the policyholder could be starting over regarding the accumulation of cash.

• What it means for the policy holder is that they are often exposed to risks that were not prevalent when the original policies were taken out. If a health condition develops and there has been no mention on the application because it seemed insignificant the insurer could reject any subsequent claim.

48

What should clients do?

• While the replacement of a life insurance policy may, in many cases, be appropriate the purchaser should be encouraged to look carefully at the policy.

• When replacing a policy the client will be expected to sign documentation confirming the policy replacement and that the adviser has explained certain matters relating to the change.

49

When it may be beneficial to replace an old policy:

• If there are added enhancements to an existing policy and the insurer is the same.

• Be sure that the client will not be disadvantaged by changing to the new cover.

• The broker should explain what the client may be missing out on by changing.

• If clients are increasing the cover, for example, and the insurer will cover the existing amount under the same conditions as the old cover only attaching any loadings or exclusions to the new sum assured.

• Policies do change over time and are often improved with added benefits

50

Make clients aware:

• Changes in their health or occupation. A new policy may end up with exclusions and loadings (an increase in premium due to perceived risk).

• Suicide clauses will start again. There is usually a period where suicide is not covered.

• As clients get older premiums may end up costing more as the premiums may be calculated differently to when they were younger and took out the original policy.

• Certain benefits that were on the old policy may not be on the new one.

51

2nd Hand Policies

52

Why Second Hand Policies?

• Endowment policies: Sec 54 restrictive period

• Buy & sell policies

• Employer owned policies

• Preferred compensation

Role of Intermediary

• Licensed for Product

• Fit and Proper Requirements

• Code of Conduct

Role of Intermediary: Code of Conduct

Information about financial service (Par 7)

• Reasonable & appropriate general explanation of nature & material terms of relevant contract/transaction to a client, & full disclosure of information reasonably be expected to enable client to make informed decision

• Material contractual information

Role of Intermediary: Code of Conduct

Full and appropriate information:

(i) Name, class or type of financial product concerned;

(ii) nature & extent of benefits to provided, including details of manner in which benefits derived/calculated & manner in which they will accrue/be paid;

Role of Intermediary: Code of Conduct

(iii) where financial product is positioned as investment:

(aa) details of manner in which value of investment is determined, including details of underlying assets /other financial instruments;

(bb) disclosure of charges /fees levied against product,; and

(cc) on request, information concerning past performance & warning that past performances are not necessarily indicative of future performances;

Role of Intermediary: Code of Conduct

(iv) nature & extent of monetary obligations by client in favour of product supplier, provider etc

(v) details of special terms or conditions, exclusions of liability, waiting periods, loadings, penalties, excesses, restrictions/circumstances in which benefits will not be provided;

(vi) any guarantees;

(vii) to what extent the product is realisable/ funds accessible;

Role of Intermediary: Code of Conduct

(x) restrictions /penalties for early termination/ withdrawal;

(xi) material tax considerations;

(xii) whether cooling off rights & procedures;

(xiii) investment/other risks of product; and

(xiv) insurance product where provision made for increase of premiums, amount of increased premium for first five years & thereafter on five year basis but not exceeding twenty years;

Role of Intermediary: Code of Conduct

Suitability of Advice (Par 8)

• Provider must, prior to providing advice:

Obtain appropriate & available information regarding client’s financial situation, financial product experience & objectives

Conduct an analysis, for purposes of advice

Identify the financial product(s) appropriate to the client’s risk profile and financial needs,

Role of Intermediary: Code of Conduct

where financial product to replace existing financial product held fully disclose to client actual and potential financial implications, costs & consequences of replacement, as discussed per Code of Conduct

Role of Intermediary: Code of Conduct

• Ensure client understands advice & in a position to make informed decision.

• Where replacing an long term insurance product with any other financial product notify issuer of existing long-term insurance product of such advice.

Role of Intermediary: Code of Conduct

• Where a client (a) has not provided all information, as part of the

analysis, or where provider has been unable to do analysis because of circumstances surrounding the case, there was not reasonably sufficient time to do so, provider to inform client thereof and ensure that client understands:

(i) full analysis could not be undertaken; (ii) may be limitations on appropriateness of advice

provided; and (iii) client to take care to consider whether advice

appropriate considering client’s objectives, financial situation and needs;

Role of Intermediary: Code of Conduct

(b) elects to conclude transaction differing from recommended by provider, or elects not to follow advice furnished, or elects to receive more limited information /advice than provider is able to provide, provider must alert client as soon as possible of the clear existence of any risk to client & must advise client to take particular care to consider whether any product selected is appropriate to client’s needs, objectives and circumstances.

Role of Intermediary: Code of Conduct

Record of Advice

• Record of advice: basis on which advice was given:

(a) brief summary of information and material on which advice based;

(b) financial products considered; and

(c) the financial product(s) recommended & why product(s) selected to satisfy client’s needs and objectives

• Record of advice maintained where transaction/contract in respect of financial product concluded by or on behalf of the client as a result of the advice furnished.

• Provider provide client with copy of the record .

Liquidity of Product

• Sec 54 of Long Term Insurance Act: 5 year period, 1 loan, 1 withdrawal, 20% Increase in Premiums

Capital Gains Tax

• General Rule: CGT payable on 2nd Hand Policy

• Exceptions

Original Beneficial Owner of Policy

Spouse, nominee (see SARS Binding Private Ruling: BPR 098 dated 24 March 2011), dependant or estate of Original Beneficial Owner & no amount payable as a result of cession to spouse, nominee or dependant

Former ‘spouse’ of Original Beneficial Owner ceded in terms of divorce order/court order

Capital Gains Tax

Example (All CGT examples: SARS CGT Guide)

Facts:

John and Jack are the original beneficial co-owners of an endowment policy. They donate the policy to Jill. Jill then cedes the policy back to Jack. Finally, Jack receives the policy proceeds on maturity from the insurer.

Result:

Capital Gains Tax

Disposal by John and Jack to Jill:

Since the policy was donated, John and Jack are deemed to have received or accrued proceeds equal to the market value of the policy under para 38. However, under para 55(1)(a)(i) they must disregard any capital gain or loss on disposal of the policy as they were original beneficial owners at the time of the donation.

Capital Gains Tax

Disposal by Jill to Jack:

Under para 38 Jill is deemed to have acquired the policy at market value on the date of acquisition. She must account for any capital gain or loss arising on the cession to Jack, as she was not an original beneficial owner.

Capital Gains Tax

Receipt of proceeds on maturity by Jack:

Under para 55(1)(a)(i) Jack must disregard any capital gain or loss arising on termination of the policy, as he was one of the original beneficial owners.

Capital Gains Tax

Example – Cession of policy between spouses Facts: Paul and Steve are involved in a same-sex union

which the Commissioner is satisfied is likely to be permanent. Paul is the original beneficial owner of a policy, which he cedes to Steve. What are the CGT implications for Steve upon surrender of the policy if

(a) Paul donates the policy to him, or (b) he pays Paul something for the policy?

Capital Gains Tax

Result:

Paul and Steve are spouses as defined in s 1 and the roll-over provisions of para 67 apply. In other words, Steve takes over Paul’s expenditure and any valuation date market value for the purpose of determining the base cost of the policy.

Capital Gains Tax

Policy ceded for no consideration:

Any gain or loss arising in Steve’s hands will be excluded by para 55(1)(a)(ii).

Policy ceded for consideration:

Steve will be subject to CGT when he surrenders the policy. The exclusion in para 55(1)(a)(ii) does not apply if any amount was paid or is payable for the cession of the policy.

Capital Gains Tax

Example – Cession of policy to nominee

Facts:

Sam is the original beneficial owner, but not the life assured, of an endowment policy. He nominates Hazel as the beneficiary and thereafter cedes the policy to her for R1. What are the implications for Hazel when she surrenders the policy?

Capital Gains Tax

Result:

Hazel is the nominated beneficiary (nominee), but despite this, any capital gain or loss arising in her hands on surrender of the policy will be subject to CGT because she paid R1 for the policy. The exclusion in para 55(1)(a)(ii) only applies when the nominee does not pay an amount for the policy.

Capital Gains Tax

Example – Surrender of policy acquired from former spouse under a divorce order

Facts: Zeb and Agnes were married under customary

law in 1956 and their marriage complies with the requirements set out in the Recognition of Customary Marriages Act 120 of 1998. Zeb is the original beneficial owner of an endowment policy. Zeb and Agnes divorce and it is ordered by the court that Zeb’s policy be ceded to Agnes. Agnes surrenders the policy.

Capital Gains Tax

Result:

Under para 55(1)(a)(iii) no capital gain or loss will arise in Agnes’ hands when she surrenders the policy.

Capital Gains Tax

• Result:

• Under para 55(1)(a)(iii) no capital gain or loss will arise in Agnes’ hands when she surrenders the policy.

Capital Gains Tax

Policy, where a person is or was an employee or director whose life was insured in terms of that policy and any premiums paid by that person’s employer were deducted in terms of section 11(w);

Capital Gains Tax

Policies for purposes of Buy & Sell agreements, ceded back to the life insured,

and no premium on the policy was paid or borne by the life insured while the other person was the beneficial owner of the policy.

Capital Gains Tax

Example – The buy-and-sell exclusion

Facts:

Abe and Bart are partners, and have drawn up a properly structured buy-and-sell agreement, funded by long-term policies. Under the arrangement Abe is the owner (payer and beneficiary) of a policy on the life of Bart and Bart is the owner (payer and beneficiary) of a policy on the life of Abe. The partnership is dissolved and the parties wish to retain the policies on their own lives. Abe cedes his policy to Bart and Bart cedes his policy to Abe.

Capital Gains Tax

Result:

Any capital gain or loss in the hands of Abe and Bart on ultimate surrender of the policies will be excluded under para 55(1)(c).

Capital Gains Tax

Policy originally taken out on the life of a person, where that policy is provided to that person or dependant by or in consequence of that person’s membership of a pension fund, pension preservation fund, provident fund, provident preservation fund or retirement annuity fund;

Capital Gains Tax Example – Policy ceded to member of

retirement fund

Facts:

Dave is a member of a pension fund. He is the life assured on an individual policy held by the fund. On retirement the policy is ceded by the fund to Dave. Dave surrenders the policy.

Result:

Any capital gain or loss arising in Dave’s hands on surrender of the policy will be excluded for CGT purposes.

Capital Gains Tax

Example – Proceeds of policy paid to dependant of member of retirement fund

Facts: Shirley is a member of a provident fund. She is

the life assured on a policy that was taken out by the fund. She has one legal dependant being her son Denys. She dies and the policy proceeds are paid to Denys.

Result: Any capital gain or loss arising in Denys’ hands

will be excluded for CGT purposes.

Capital Gains Tax

in respect of a risk policy with no cash value or surrender value;

if the amount received or accrued constitutes an amount contemplated in section 10(1)(gG) or (gH).

Capital Gains Tax

• Policies subject to CGT • Determination of base cost • The base cost of 2nd hand policy acquired before

1 October 2001: any of the prescribed methods. Most likely: time-apportionment basis or the market value.

• Para 31(1)(b): market value of policy = higher of surrender value, and Fair market value determined by the insurer

assuming that the policy runs to maturity.

Capital Gains Tax

Example – Part-disposal of second-hand policy

• Facts:

• In 1996 Brenda took out a 5-year endowment policy as the original beneficial owner. Keith purchased the policy from Brenda in 2000 for R100 000. The market value of the policy on 1 October 2001 was R90 000. Keith made the following withdrawals:

Capital Gains Tax

• 1 July 2002: Withdrawal R5 000; Market Value immediately Before Withdrawal 100 000

• 1 July 2003: Withdrawal R6 000 Market Value immediately Before Withdrawal R108 000

• 1 July 2006: Withdrawal R120 000 Market Value immediately Before Withdrawal R120 000

• Keith adopts the market value method for determining the valuation date value of the policy.

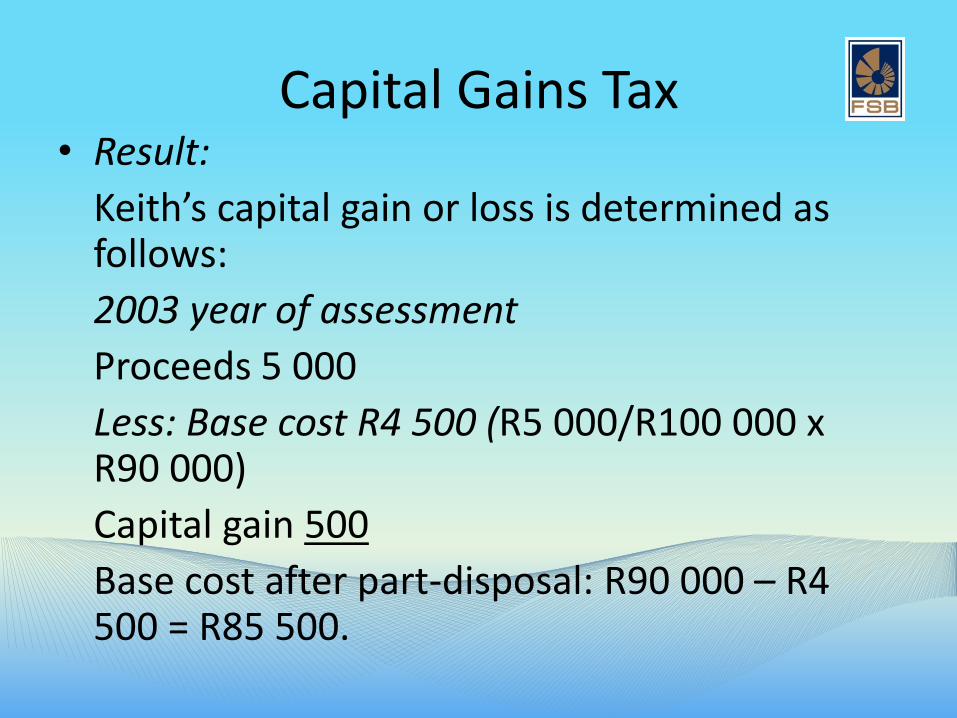

Capital Gains Tax • Result:

Keith’s capital gain or loss is determined as follows:

2003 year of assessment

Proceeds 5 000

Less: Base cost R4 500 (R5 000/R100 000 x R90 000)

Capital gain 500

Base cost after part-disposal: R90 000 – R4 500 = R85 500.

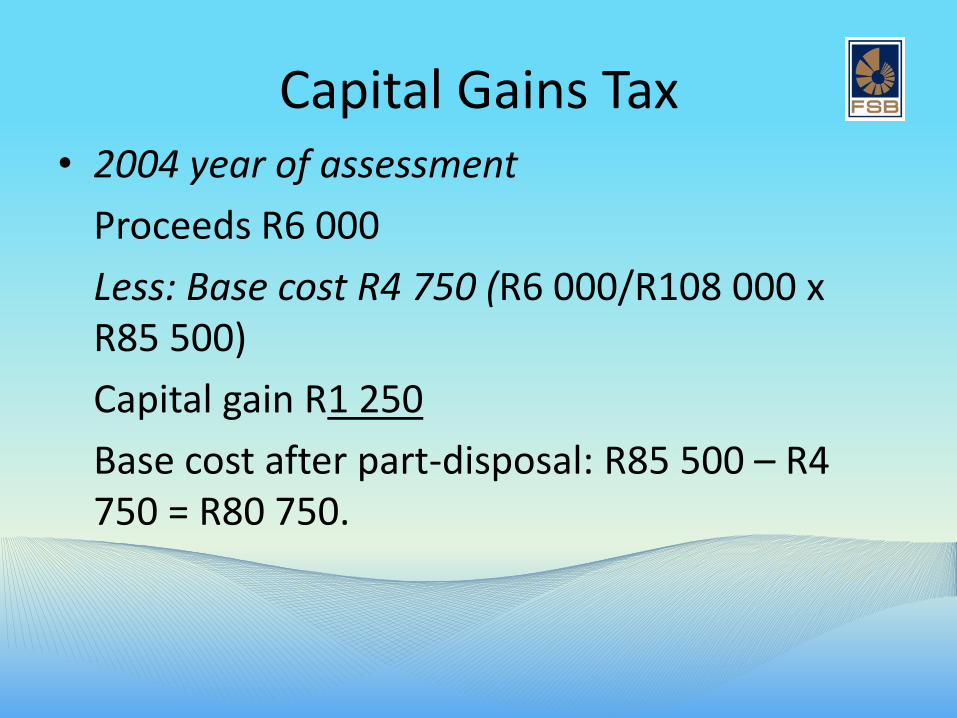

Capital Gains Tax • 2004 year of assessment

Proceeds R6 000

Less: Base cost R4 750 (R6 000/R108 000 x R85 500)

Capital gain R1 250

Base cost after part-disposal: R85 500 – R4 750 = R80 750.

Capital Gains Tax

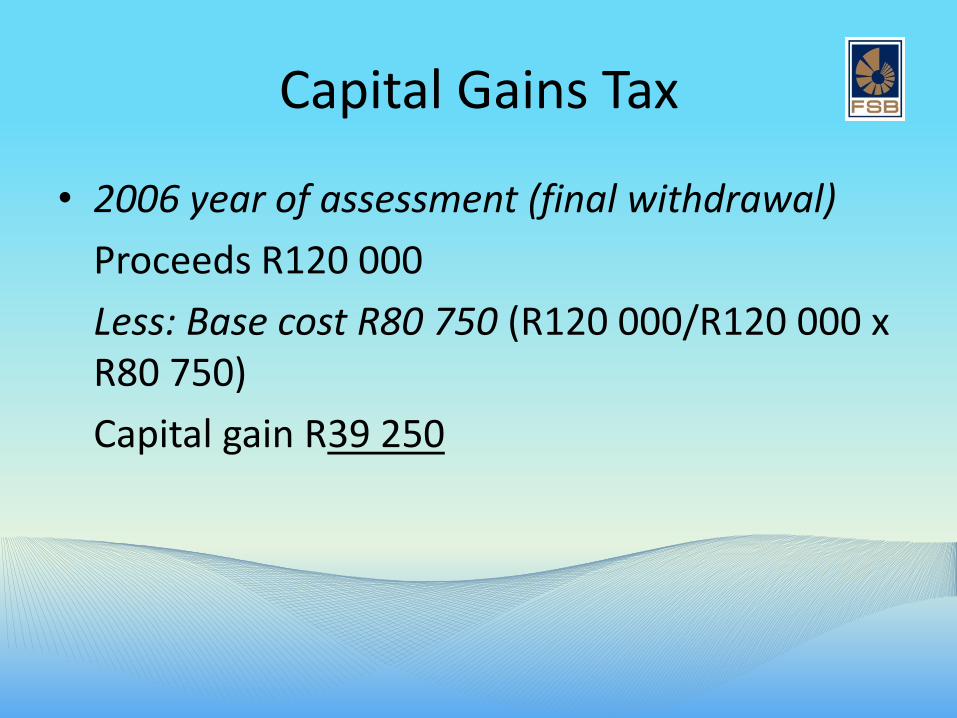

• 2006 year of assessment (final withdrawal)

Proceeds R120 000

Less: Base cost R80 750 (R120 000/R120 000 x R80 750)

Capital gain R39 250

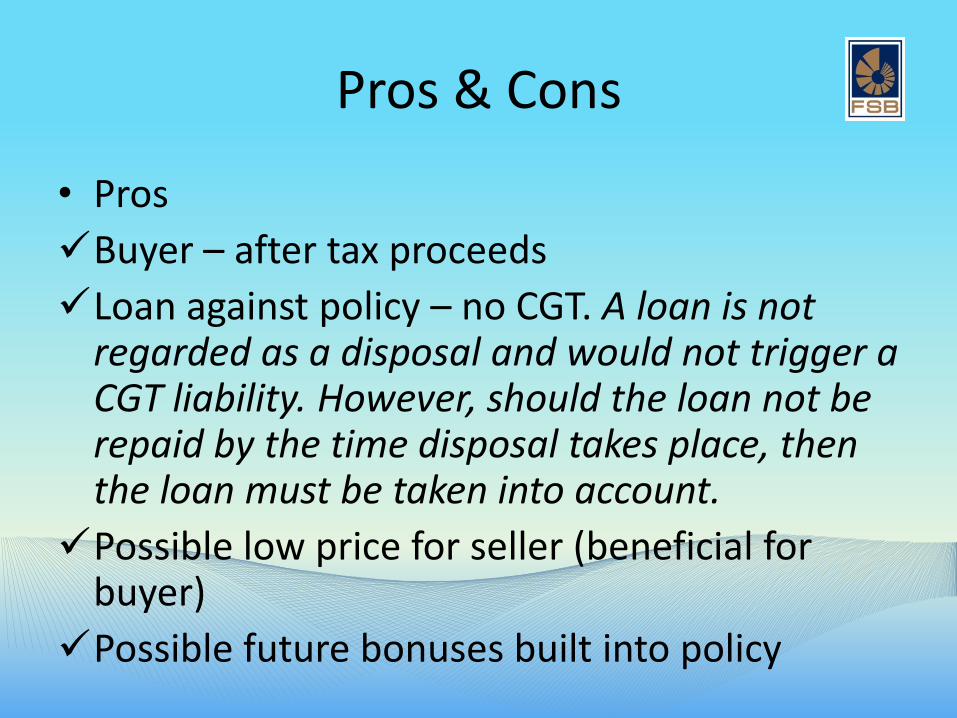

Pros & Cons

• Pros

Buyer – after tax proceeds

Loan against policy – no CGT. A loan is not regarded as a disposal and would not trigger a CGT liability. However, should the loan not be repaid by the time disposal takes place, then the loan must be taken into account.

Possible low price for seller (beneficial for buyer)

Possible future bonuses built into policy

Pros & Cons

• Cons

CGT Additional tax

Restrictive periods

Possible low price for seller (detriment for seller)

Pitfalls of 2nd Hand Policies

• Possible pitfalls:

Loans Against Policy

Policy ceded for security

Possible upfront costs

Look at tax rate for individual purchasing (taxed at 30% within fund)

Cell Captives – An introduction

International Context

SA Context

Cell Captives Structure

First Party Cells

Third Party Cells

Market Information

Agenda

Cell Captives – International Context

Cell Captives are mainly used for self insurance of Corporates own

liabilities such as EB liabilities

Various domiciles available – Tax, Regulatory Environment, Skills,

(Bermuda, Bahamas, Guernsey, Jersey, Malta, Mauritius).

Corporates pool cross border insurance risks for price efficiency and

appoint specialist Advisors/Managers to assist in managing Captive via

Captive board (Actuarial Consultants, Benefit Consultants, Audit, Legal

and Tax Advisors, Administrators).

Develop benefit structure and execute ALM strategy using Reinsurers and

Asset Managers/Banks.

Protected Cell Companies exist (PCC) (Operate as distinct Insurer, not

“rent a license”).

PCC not in SA yet.

International Topical Issues

Solvency assessment and management

European economic climate

Tax treaties

Investment markets (Equities)

Reinsurance rates

Cell Captives – SA Context

Long term insurer or Short term insurer governed under South African

Company and Insurance Laws.

Approved by the FSB with it’s own license conditions and restrictions.

Insurer have the flexibility to issue a different class (other than ordinary

equity) of participating equity to clients.

Participating equity gives certain rights and obligations to holder (i.e. a

Corporate has the obligation to fund CAR, but the right to earn profits in cell

(and losses)).

SA Topical Issues

Solvency Assessment and Management

Treat Customers Fairly (TCF)

Binder Regulations and Outsourcing

Investment markets

Reinsurance rates

Tax developments

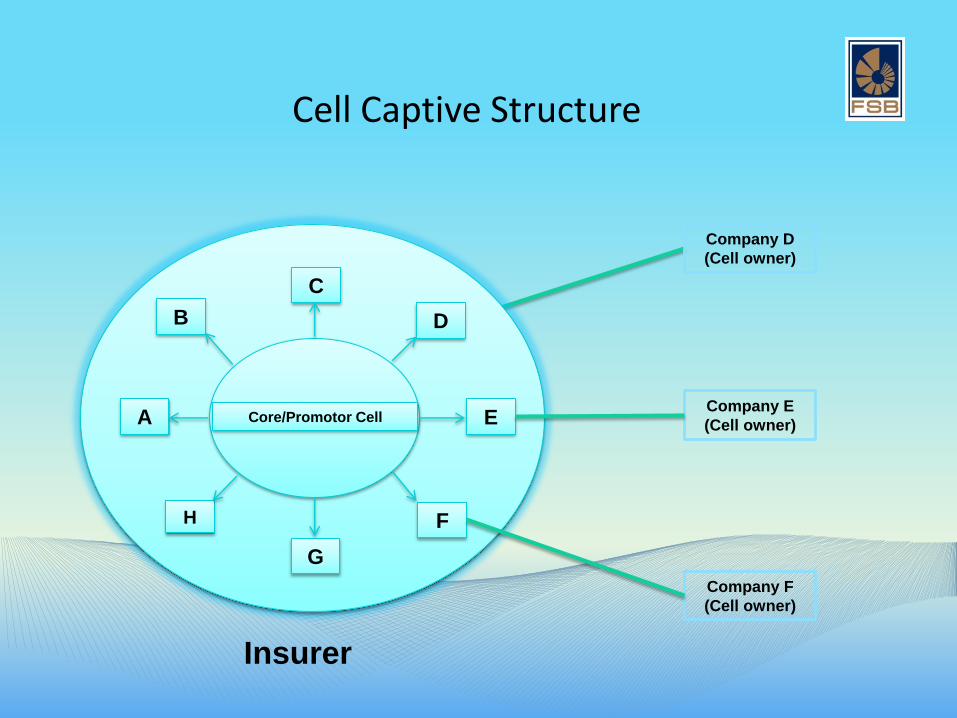

Cell Captive Structure

Insurer

Core/Promotor Cell

C

G

A E

B D

F H

Company D

(Cell owner)

Company E

(Cell owner)

Company F

(Cell owner)

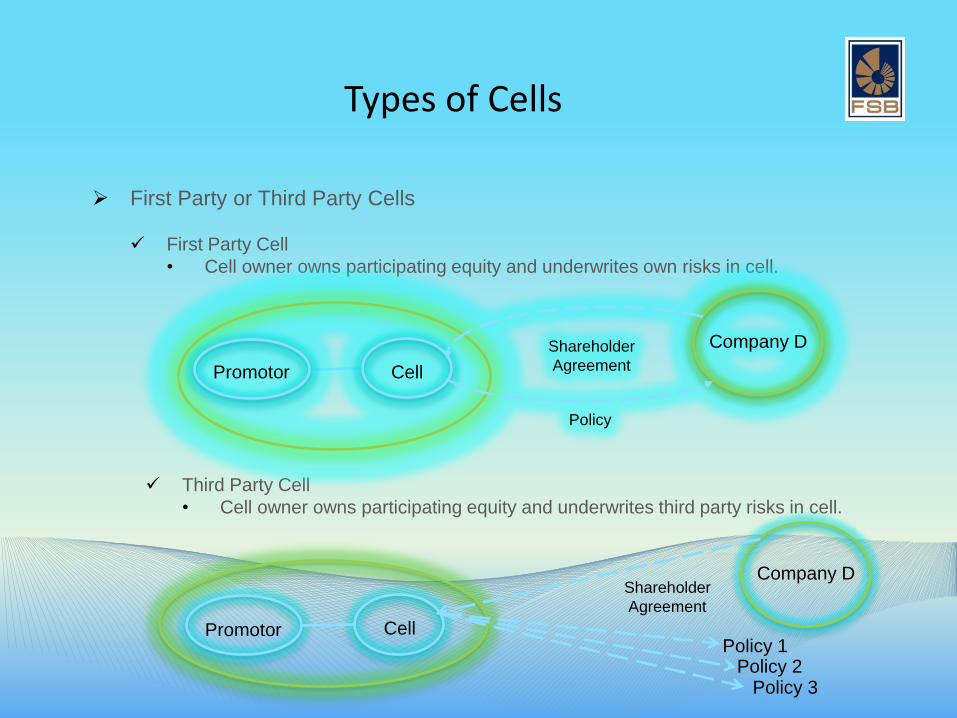

Types of Cells

First Party or Third Party Cells

First Party Cell

• Cell owner owns participating equity and underwrites own risks in cell.

Third Party Cell

• Cell owner owns participating equity and underwrites third party risks in cell.

Promotor Cell

Company D Shareholder

Agreement

Policy

Promotor Cell

Company D Shareholder

Agreement

Policy 1

Policy 3 Policy 2

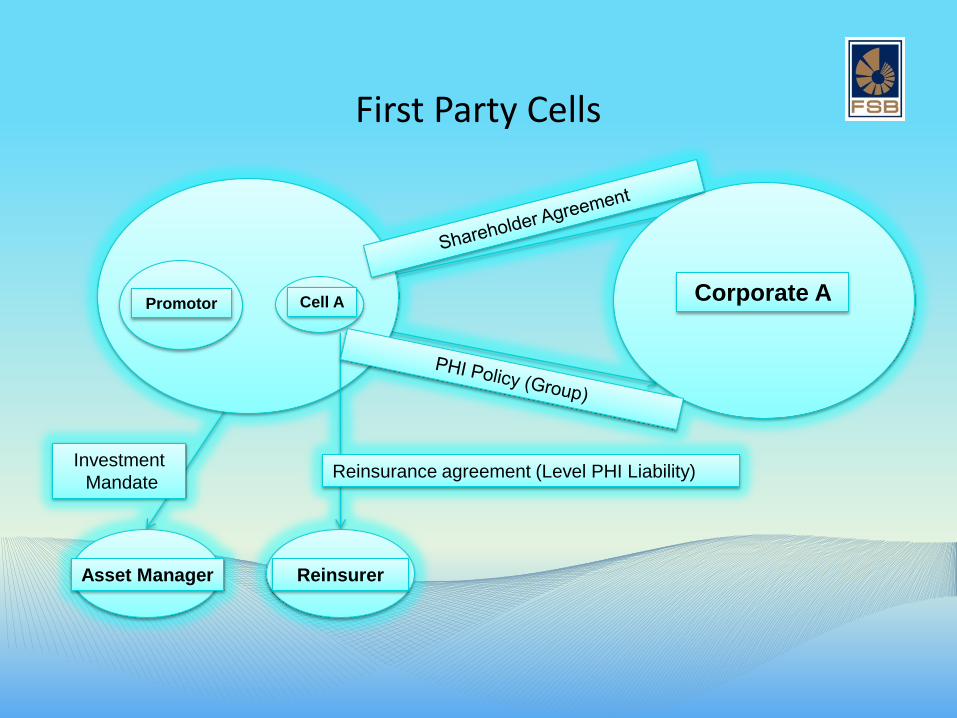

First Party Cells

Investment

Mandate

Corporate A Promotor Cell A

Reinsurance agreement (Level PHI Liability)

Reinsurer Asset Manager

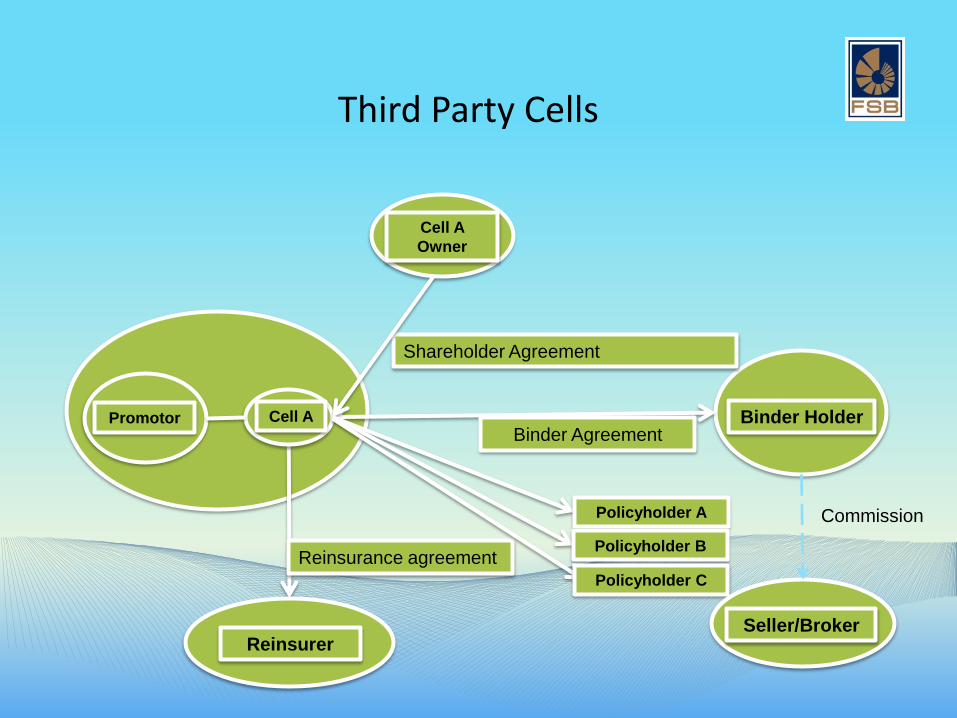

Third Party Cells

Cell A

Owner

Binder Holder

Reinsurance agreement

Shareholder Agreement

Reinsurer

Promotor Cell A

Binder Agreement

Policyholder A

Policyholder B

Policyholder C

Seller/Broker

Commission

Long Term Insurance Market

34%

28%

1%

1%

14%

2%

20%

Guardrisk Life

Momentum

Centriq Life

Other

Old Mutual ART

Sanlam Customised

RMB Structured Life

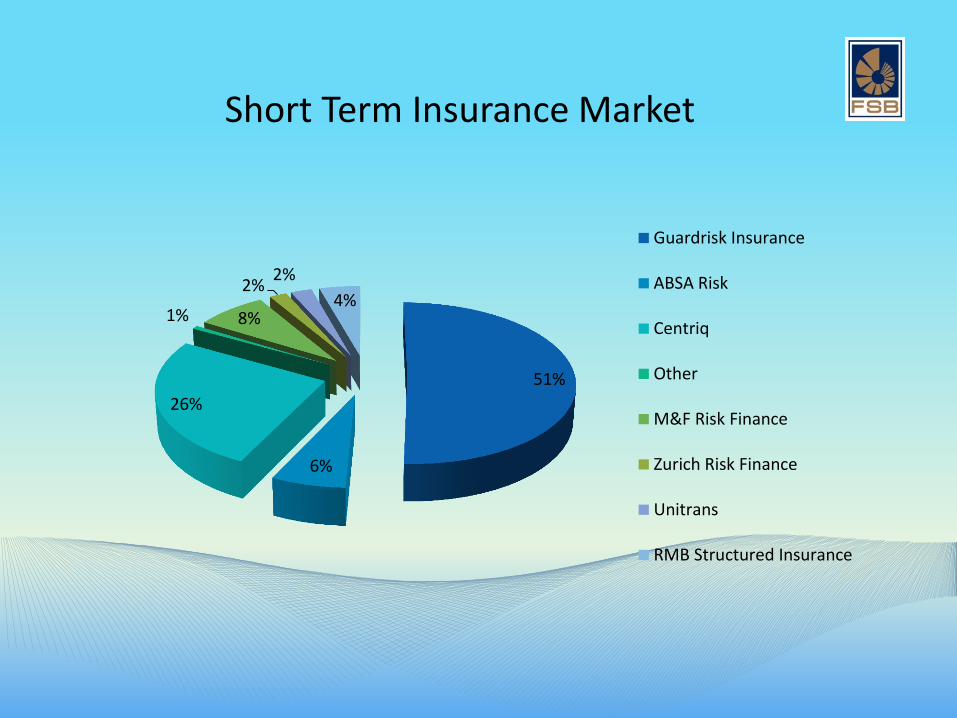

Short Term Insurance Market

51%

6%

26%

1% 8%

2% 2%

4%

Guardrisk Insurance

ABSA Risk

Centriq

Other

M&F Risk Finance

Zurich Risk Finance

Unitrans

RMB Structured Insurance

REVIEW OF 3RD PARTY CELL

CAPTIVE INSURANCE AND

SIMILAR ARRANGEMENTS

Agenda

1. Background

2. Introduction

3. Overall Findings

4. Key regulatory proposals

5. Way forward

110

Background Information letter 2/2011

• Focus on 3rd party cell captives

• Concerns: – Different standard registration conditions

– Licensing conditions not fully effective

– Potential conflicts of interest

• Review to consider: – Managing of conflict of interest

– Limiting 3rd party cell owners to UMAs

– Prohibition on independent intermediaries owning a cell

– Affinity schemes to be prohibited or allowed subject to regulatory conditions

• Moratorium placed on new 3rd party cell captive

insurers

111

Introduction

• 2012 assessment of 3rd cell arrangements:

– Existing ownership structures and business models

(including similar arrangements)

– Financial soundness and market conduct risks

– Conflict or potential conflict of interest

– Mitigation of risks and conflict of interest

– Which structures/ arrangements or activities should

be prohibited

• Report submitted to FSB end-Sept 2012

112

Overall findings

113

Cell owners

• Independent intermediaries

• Underwriting managers

• Corporates

• Affinity schemes

• Other insurers

• Pension Funds

114

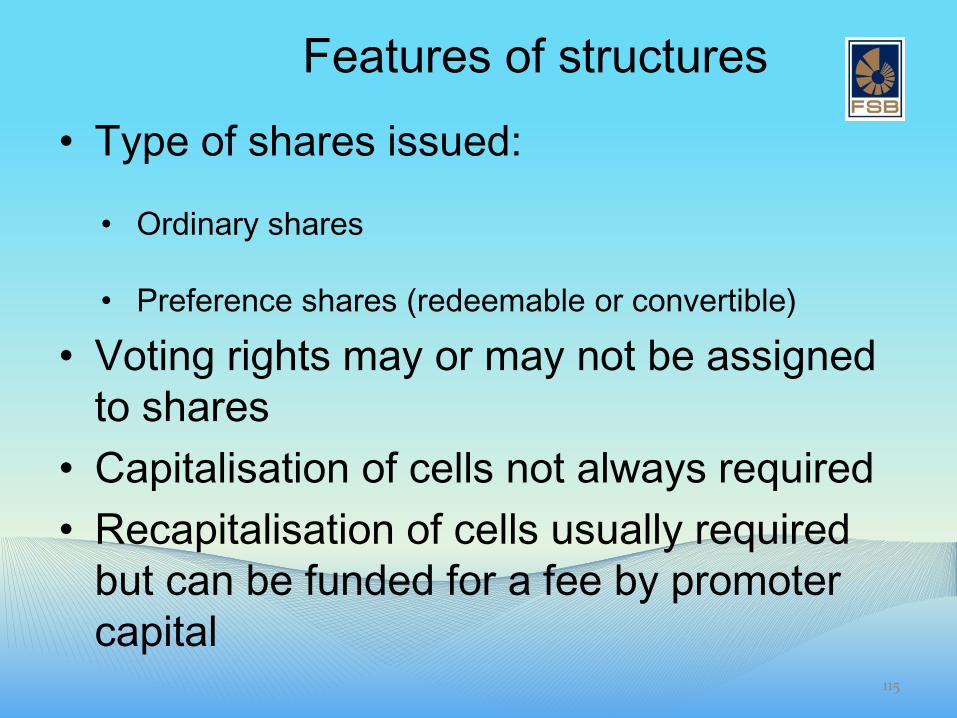

Features of structures

• Type of shares issued:

• Ordinary shares

• Preference shares (redeemable or convertible)

• Voting rights may or may not be assigned

to shares

• Capitalisation of cells not always required

• Recapitalisation of cells usually required

but can be funded for a fee by promoter

capital 115

Specific risks identified

Risks to cell captive insurers:

• Contractual and exit strategy risk

• Operational risk

• Insurance risk

• Credit risk

• Reputational and market conduct

risk

116

Specific risks identified

Risks to policyholders:

• Risks to fair conduct of business

• Conflicts of interest

• Risks to ability to pay claims

Risks relating to regulation and

supervision:

• Conditions of registration

• Supervisory oversight

117

Key regulatory proposals

118

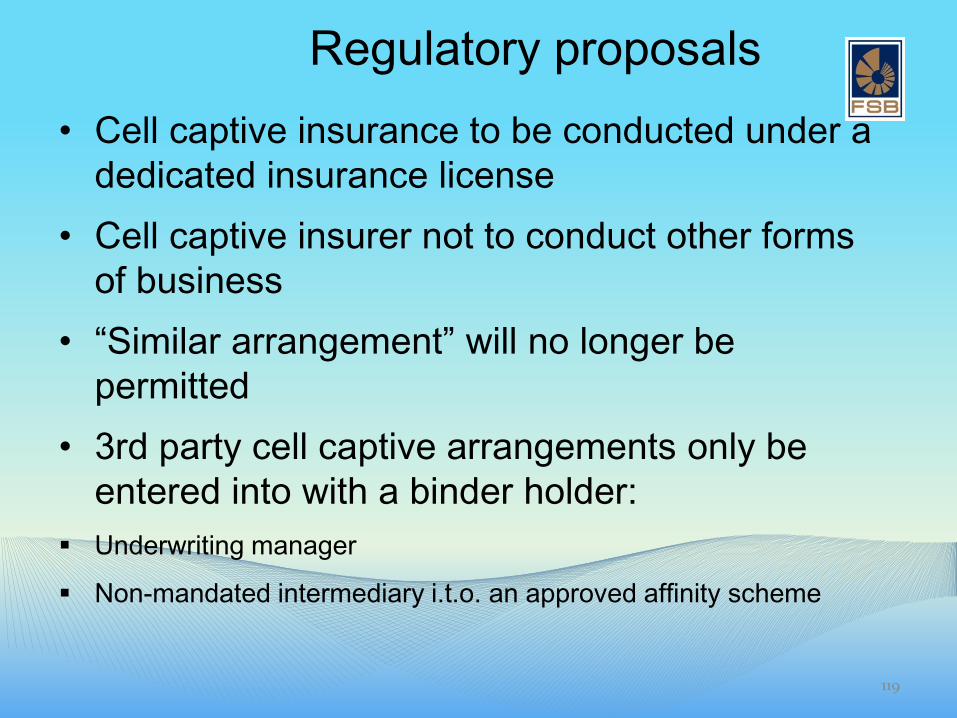

Regulatory proposals

• Cell captive insurance to be conducted under a

dedicated insurance license

• Cell captive insurer not to conduct other forms

of business

• “Similar arrangement” will no longer be

permitted

• 3rd party cell captive arrangements only be

entered into with a binder holder:

Underwriting manager

Non-mandated intermediary i.t.o. an approved affinity scheme

119

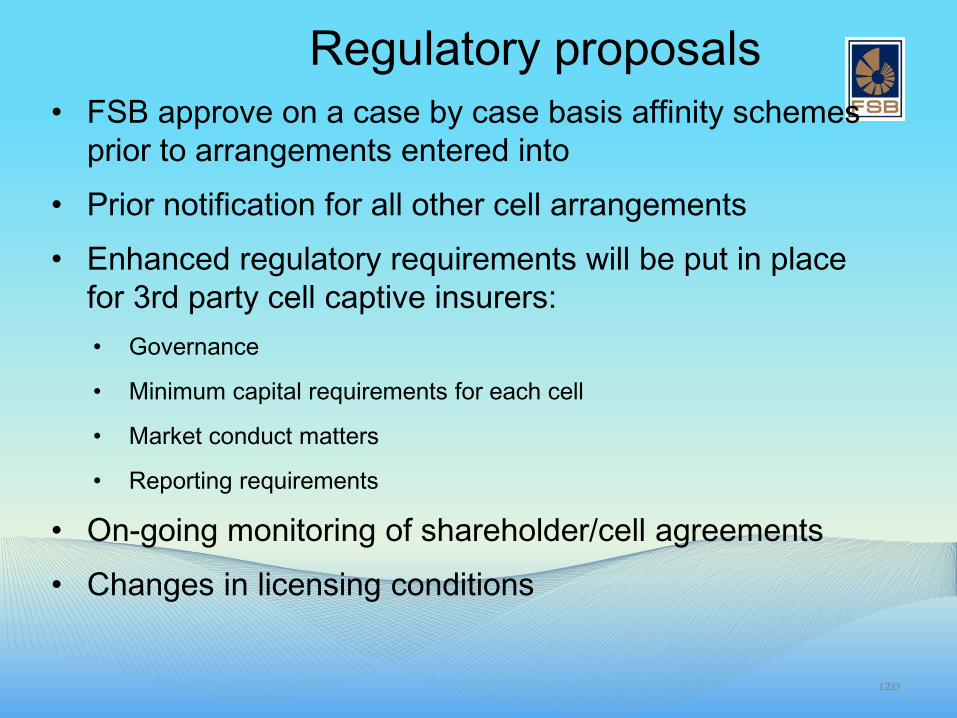

Regulatory proposals

• FSB approve on a case by case basis affinity schemes

prior to arrangements entered into

• Prior notification for all other cell arrangements

• Enhanced regulatory requirements will be put in place

for 3rd party cell captive insurers:

• Governance

• Minimum capital requirements for each cell

• Market conduct matters

• Reporting requirements

• On-going monitoring of shareholder/cell agreements

• Changes in licensing conditions

120

Way forward

• Discussion Document was issued

to all insurers on 11 June 2013

• Comments due by 31 July 2013

121