A A A N N N N N N E E E X X X U U U R R R E E E S S S & & & F F F O O O R R R M M M A A A T T T S S S BIODIVERSITY CONSERVATION & RURAL LIVELIHOOD IMPROVEMENT PROJECT PREPARED BY GOVERNMENT OF INDIA MINISTRY OF ENVIRONMENT & FOREST 2011 VERSION 1.0

Transcript

AAANNNNNNEEEXXXUUURRREEESSS &&&

FFFOOORRRMMMAAATTTSSS BIODIVERSITY CONSERVATION &

RURAL LIVELIHOOD IMPROVEMENT

PROJECT

PREPARED BY

GOVERNMENT OF INDIA

MINISTRY OF ENVIRONMENT & FOREST

2011

VERSION 1.0

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 2 | P a g e

PREAMBLE

TITLE

This document is the “Financial Management Manual Annexures” for the Biodiversity

Conservation and Rural Livelihood Improvement Project. This manual needs to be read in

conjunction with the main FM Manual. A separate manual exists for Procurement procedure

and hence the same is not reproduced in this manual.

OBJECTIVE

The purpose of the manual is to provide assistance and guidance to the users and stake

holders on the relevant reporting requirements.

VERSION

This is the first version of the manual. It would be revised from time to time as per the

project needs in consultation and concurrence with World Bank and Ministry of Environment

and Forests (MOEF).

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 3 | P a g e

TABLE OF CONTENTS

Annexure I. STATUTORY AUDIT TOR (AG) ........................................ 4

Annexure II. STATUTORY AUDIT TOR (CA FIRM) .................................. 20

Annexure III. INTERNAL AUDIT TOR ............................................. 38

Annexure IV. INTERIM UNAUDITED FINANCIAL REPORT ............................. 46

Annexure V. MOU ............................................................ 57

Annexure VI. GFR RULES FOR GIA .............................................. 62

Annexure VII. CONDITIONS FOR IMPLEMENTING AGENCIES ........................... 64

Annexure VIII. DFP RULE – 20 ................................................. 66

Annexure IX. FORM GFR 19- AFORM OF UTILIZATION CERTIFICATE………………………………………………67

Annexure X. GFR RULES ...................................................... 68

Annexure XI. AUDIT OF GIA ................................................... 72

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 4 | P a g e

ANNEXURE I. STATUTORY AUDIT TOR (AG)

Background

Government of India and World Bank are embarking on a BCLRIP project which will support

Government of India’s efforts to prevent degradation of biodiversity within the country.

It will help GOI mainstream biodiversity and improve rural livelihoods in development

planning in areas that surround biodiversity sensitive areas, including protected areas.

In the long term, it will assist the country to protect its valuable forests and

biodiversity, improve the viability of its protected area network and ensure the survival

of critical species. It will contribute towards improving the contribution of

biodiversity to local livelihoods so as to enhance the incentives for conservation and

help alleviate poverty in remote rural forested areas. A broad implementation set-up

envisaged for the project is described below:

• The Ministry of Environment and Forests (MOEF) through its Conservation and Survey

Division (CS&D) will be overall responsible for overseeing and coordinating the

implementation of the project.

• At the state level, each of the two States (Gujarat & Uttarakhand) will have a

landscape Society for implementation and monitoring of project activities.

• Below the landscape level, there will be community level societies in case of

Gujarat and Van Panchayat in case of Uttarakhand.

• Apart from the above there will be learning centres at Periyar, Kalakad, Gir and

WII which will be carried by respective societies.

Objective

The essence of the World Bank1 audit policy is to ensure that the Bank receives adequate

independent, professional audit assurance that the proceeds of World Bank loans were used

for the purposes intended,2 that the annual project financial statements are free from

material misstatement, and that the terms of the loan agreement were complied with in all

material respects.

The objective of the audit of the Project Financial Statement (PFS) is to enable the

auditor to express a professional opinion as to whether (1) the PFS present fairly, in

all material respects, the sources and applications of project funds for the period under

1 “World Bank” includes the International Development Agency and the International Bank for Reconstruction and Development. “Loans” includes credits and grants to which the TORs would apply; and “borrower” includes recipients of such loans.

2 The Bank’s charter [Article III Section V(b) of IBRD’s Articles of Agreement and Article V Section 1(g) of IDA’s Articles of Agreement]

specify that: “The Bank shall make arrangements to ensure that the proceeds of any loan are used only for the purposes for which the

loan was granted, with due attention to considerations of economy and efficiency and without regard to political or other non-

economic influences or considerations.”

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 5 | P a g e

audit examination, (2) the funds were utilized for the purposes for which they were

provided, and (3) expenditures shown in the PFS are eligible for financing under the

relevant loan or credit agreement. In addition, where applicable, the auditor will

express a professional opinion as to whether the Interim Unaudited Financial Reports

submitted by project management may be relied upon to support any applications for

withdrawal, and whether adequate supporting documentation has been maintained to support

claims made by project management for reimbursement of expenditures incurred. The books

of account that provide the basis for preparation of the PFS are established to reflect

the financial transactions of the project and are maintained by the project

implementation agency– MEF(BCRLIP).

Standards

The audit will be carried out in accordance with the Auditing Standards promulgated by

the Comptroller and Auditor General of India. The auditor should accordingly consider

materiality when planning and performing the audit to reduce audit risk to an acceptable

level that is consistent with the objective of the audit. Although the responsibility

for preventing irregularity, fraud, or the use of loan proceeds for purposes other than

as defined in the legal agreement remains with the borrower, the audit should be planned

so as to have a reasonable expectation of detecting material misstatements in the project

financial statements

Scope3

C&AG of India will audit MEF (BCRLIP), WII and Uttarakhand Forest Department whereas the

downstream entities like the landscape societies and learning centers would be audited by

CA firms empanelled with and appointed by C&AG in this regard.

Ministry of Environment and Forests shall, while sanctioning funds to the implementing

societies emphasize the project accounts shall be subject to audit by C&AG and the

implementing agencies shall produce the accounts to audit.

Ministry of Environment and Forests as an Implementing Agency or any other entity in its

behalf shall prepare consolidated project Financial Statements. The implementing agency

wise audit report for the project shall be prepared by auditors concerned and the

consolidated audit report of the consolidated project Financial Statements shall be

prepared by the C&AG, which shall be based on;

• Audit conducted by the C&AG of MEF(BCRLIP, WII and Uttarakhand Forest

Department.

• Audit Reports of other entities carried out by CAs subject to directions and

test check of their work wherever considered necessary by C&AG or offices

designated by him.

3 In response to identified project risks, the scope may be expanded to include a report or the expression of an opinion on specific

aspects of the operation such as internal controls, compliance with Bank procurement policies, or efficiency and effectiveness in the use of loan proceeds.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 6 | P a g e

The auditor would be required to audit the consolidated IUFRs, including the IUFRs

submitted by the MEF (BCRLIP) to the bank. In conducting the audit, special attention

should be paid to the following:

(a) All external funds have been used in accordance with the conditions of the

relevant legal agreements and only for the purposes for which the financing was

provided. Relevant legal agreements include the Financing Agreement, the Project

Agreement, and the Minutes of Negotiations;

(b) Counterpart funds have been provided and used in accordance with the relevant

legal agreements and only for the purposes for which they were provided;

(c) All necessary supporting documents, records, and accounts have been kept in

respect of all project transactions including expenditures reported via IUFRs

where applicable. (Clear linkages should exist between the books of account and

reports presented to the Bank); and

(d) The project accounts have been prepared in accordance with consistently applied

Government Accounting Standards4 and present fairly, in all material respects, the

financial situation of the project at the year end and of resources and

expenditures for the year ended on that date.

Project Financial Statements

The Project Financial Statements should include-

• Statement of Sources and Applications of Funds

• Reconciliation of Claims to Total Applications of Funds.

• Statement showing entity wise transfer

Management Assertion

Management Assertion: Management should sign the project financial statements and

provide a written acknowledgement of its responsibility for the preparation and fair

presentation of the financial statements and an assertion that project funds have been

expended in accordance with the intended purposes as reflected in the financial

statements. An example of a Management Assertion Letter is shown below.

Interim Unaudited Financial Reports

In addition to the audit of the PFS, the auditor is required to audit all Interim

Unaudited Financial Reports (IUFRs) for withdrawal applications made during the period

under audit examination. The auditor should apply such tests as the auditor considers

necessary under the circumstances to satisfy the audit objective. In particular, these

expenditures should be carefully examined for project eligibility by reference to the

relevant financing agreements. Where ineligible expenditures are identified as having

4 Until such time as the pronouncements of the Government Accounting Standards Advisory Board are accepted and prescribed by the

Ministry of Finance, the accounting standards followed by the Government of India will be defined by the General Financial Rules,

PWD codes, Treasury codes and similar financial rules and codes as are in effect and applicable to the operations of the project.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 7 | P a g e

been included in withdrawal applications and reimbursed against, these should be

separately noted by the auditor.

Audit Report

An audit report on the project financial statements should be prepared in accordance with

the Auditing Standards promulgated by the Comptroller and Auditor General of India.

Those standards require an audit opinion to be rendered related to the financial

statements taken as a whole, indicating “unambiguously whether it is unqualified or

qualified and, if the latter, whether it is qualified in certain respects or is adverse

or a disclaimer of opinion.”5 In addition, the audit opinion paragraph will specify

whether, in the auditor’s opinion, (a) with respect to IUFRs, adequate supporting

documentation has been maintained to support claims to the World Bank for reimbursements

of expenditures incurred; and (b) except for ineligible expenditures as detailed in the

audit observations, if any, appended to the audit report, expenditures are eligible for

financing under the Loan/Credit Agreement. A sample audit report wording for an

unqualified audit opinion is shown below.

The project financial statements and the audit report should be received by the Bank not

later than 6 months after the end of the fiscal year. The auditor should also submit two

copies of the audited accounts and audit report to the Implementing Agency.

The audit report is issued without prejudice to CAG’s right to incorporate the audit

observations in the Report of CAG of India for being laid before Parliament/State or UT

Legislature.

Management Letter

In addition to the audit report on the project financial statements, the auditor may

prepare a management letter containing recommendations for improvements in internal

control and other matters coming to the attention of the auditor during the audit

examination.

Where a management letter is prepared by the auditor, a copy of the same will be supplied

to the Bank. Else, a written advice may be made that no management letter was prepared

together with the audit report on the project financial statements.

General

The auditor should be given access to any information relevant for the purposes of

conducting the audit. This would normally include all legal documents, correspondence,

and any other information associated with the project and deemed necessary by the

auditor. The information made available to the auditor should include, but not be

limited to, copies of the Bank’s Project Appraisal Document, the relevant Legal

5 See relevant portions of Auditing Standards of the Comptroller and Auditor General of India as applicable from time to time.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 8 | P a g e

Agreements, a copy of these Guidelines, and a copy of the Bank’s Financial Management

Assessment of the project entity. It is highly desirable that the auditor become

familiar with other Bank policy documents, such as OP/BP 10.02, the Bank's internal

guidelines on Financial Management that include financial reporting and auditing

requirements for projects financed by the World Bank. The auditor should also be

familiar with the Bank's Disbursement Manual. Both documents will be provided by the

Project staff to the auditor.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 9 | P a g e

Sources and Application of Funds

Name of the project ___________ Loan/Credit/Grant No._______

Report for the year ended_______________________

(in Rs. thousands)

Particulars Current

Year

Previous

Year

Receipts

Funds from Government through Budget

Total Receipts (A)

Expenditures/Transfer by Component

A. Demonstration of Landscape Conservation Approaches in

selected pilot sites

B. Strengthening Knowledge Management and National Capacity for

Landscape Conservation (transfers)

C. Scaling Up and Replication of Successful Models of

Conservation in Additional Landscape Sites.

D. National Coordination for Landscape Conservation.

(transfers)

Total Expenditures (B)

Notes:

1. This financial statement is prepared on a cash basis of accounting as per provisions of the Government Financial Rules and codes applicable.

2. The above figures will be based on monthly/quarterly abstract accounts prepared by the accounts compiling officers, duly reconciled by the respective agencies, with

details of un-reconciled amounts to be furnished.

3. Names of accounting units whose financial statements are aggregated to prepare the consolidated accounts.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 10 | P a g e

4. Only in case of MEF (BCRLIP) the actual expenditure would be shown in the audit report while in case of other agencies the transfers would be shown in the

statement. The expenditure done by these agencies would be audited by separate CA

firm

5. Any other project specific Note.

Entity wise transfers and utilisation certificates received

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 11 | P a g e

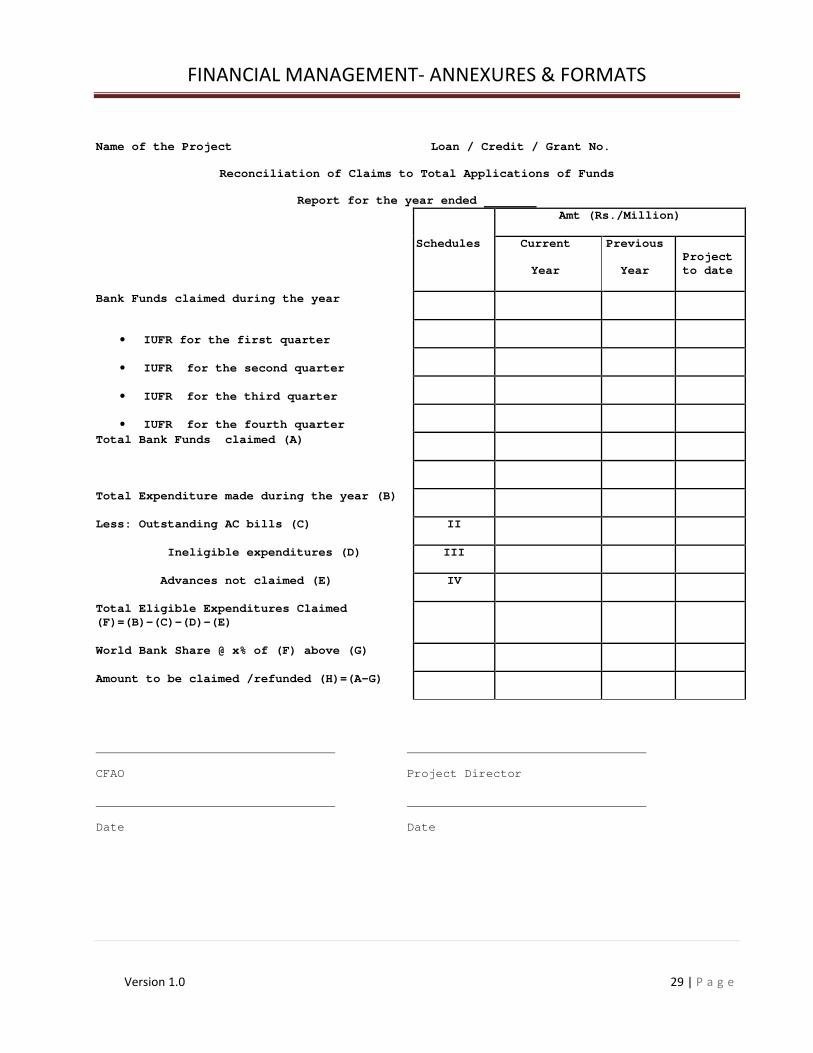

Name of the Project Loan / Credit / Grant No.

Reconciliation of Claims to Total Applications of Funds

Report for the year ended

CFAO Project Director

Date Date

Schedule

s

Amt (Rs./Million)

Current

Year

Previous

Year

Project

to date

Bank Funds claimed during the year

• IUFR for the first quarter

• IUFR for the second quarter

• IUFR for the third quarter

• IUFR for the fourth quarter

Total Bank Funds claimed (A)

Total Expenditure/Transfers made during the

year (B)

Less: Outstanding AC bills (C) II

Ineligible expenditures (D) III

Transfers not claimable (E) IV

Total Eligible Expenditures Claimed

(F)=(B)-(C)-(D)-(E)

World Bank Share @ x% of (F) above (G)

Amount to be claimed /refunded (H)=(A-G)

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 12 | P a g e

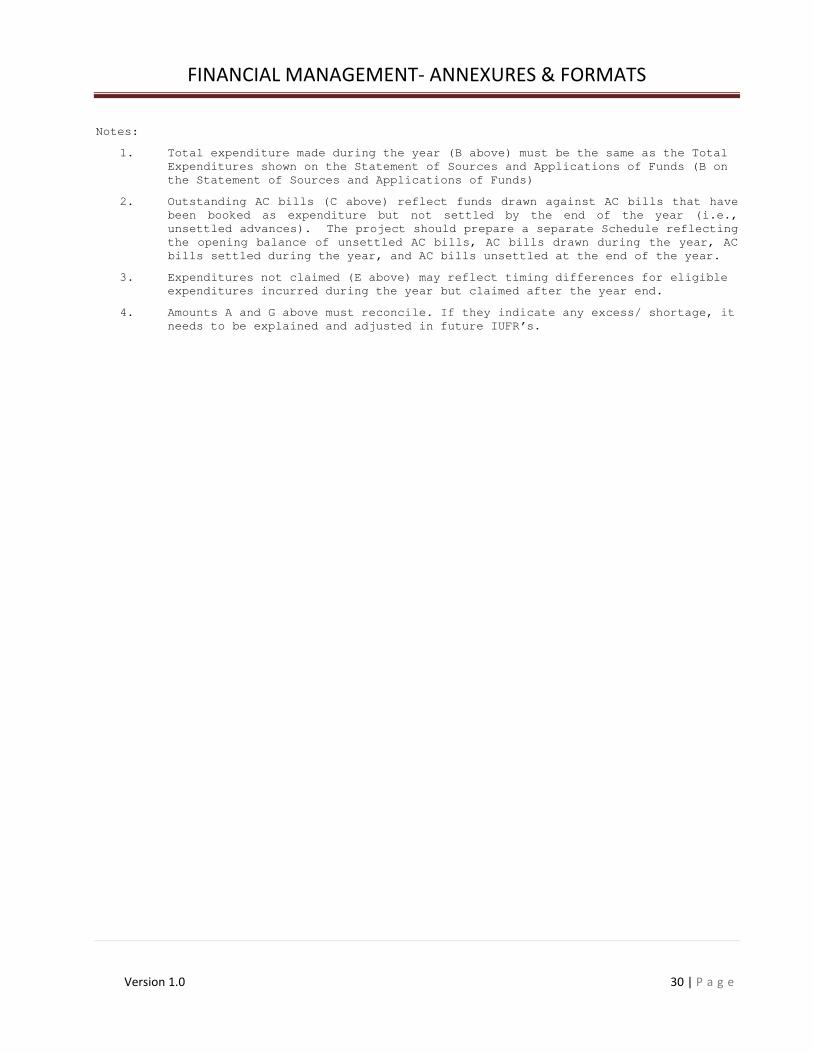

Notes:

1. Total expenditure made during the year (B above) must be the same as the Total

Expenditures shown on the Statement of Sources and Applications of Funds (B on

the Statement of Sources and Applications of Funds)

2. Outstanding AC bills (C above) reflect funds drawn against AC bills that have

been booked as expenditure but not settled by the end of the year (i.e.,

unsettled advances). The project should prepare a separate Schedule reflecting

the opening balance of unsettled AC bills, AC bills drawn during the year, AC

bills settled during the year, and AC bills unsettled at the end of the year.

3. Transfers not claimed (E above) reflects transferred made from one level to

another which would be claimed as expenditure in future.

4. Amounts A and G above must reconcile. If they indicate any excess/ shortage, it

needs to be explained and adjusted in future IUFR’s.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 13 | P a g e

List of Claims submitted to World Bank

Date Of Application Application Number Period Amount Claimed

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 14 | P a g e

MEF (BCRLIP)

Loan/Credit/Grant No.

MEF(BCRLIP) Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

current year

For the last

year Cumulative

1. Receipts from GOI

2. Government contribution for staff cost

Total sources

Expenditure:

A. Development of Landscape Biodiversity Cons. Mgmt

B. Project Administration

C. Recurring Cost Excluding Government Staff Cost

D. Government staff cost

Total Expenditure

* Government Staff Cost amounts to Rs. ……………

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

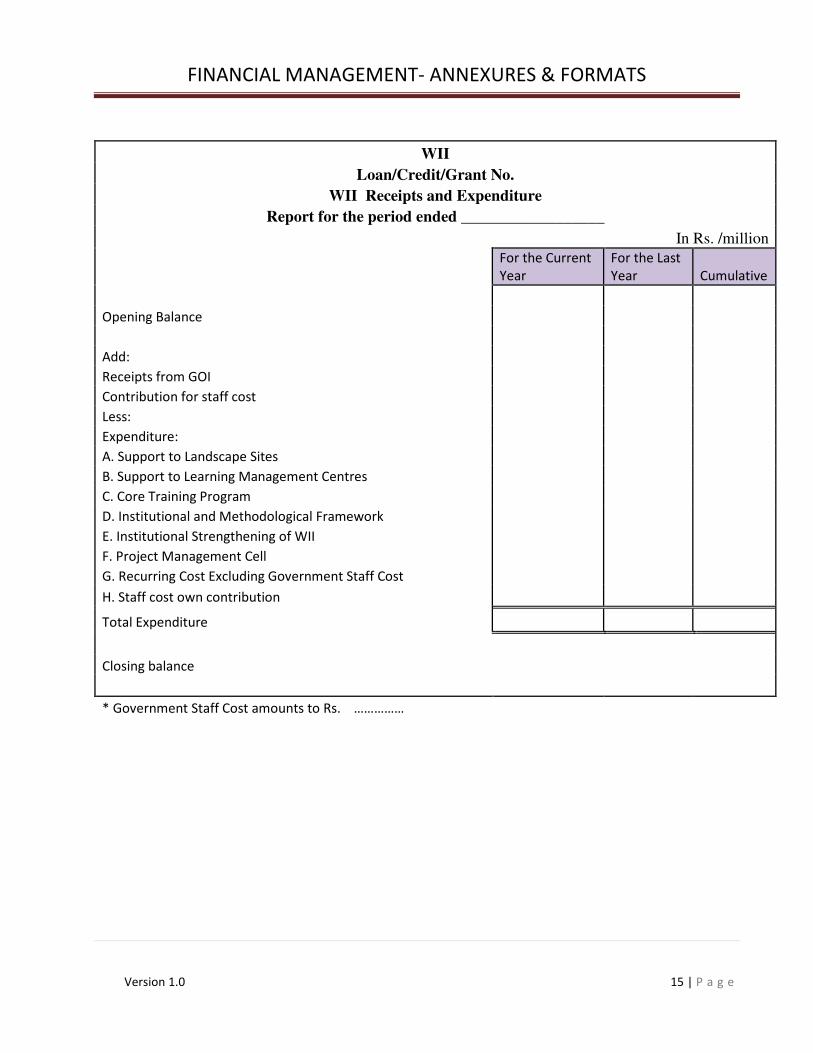

Version 1.0 15 | P a g e

WII

Loan/Credit/Grant No.

WII Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the Current

Year

For the Last

Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Support to Landscape Sites

B. Support to Learning Management Centres

C. Core Training Program

D. Institutional and Methodological Framework

E. Institutional Strengthening of WII

F. Project Management Cell

G. Recurring Cost Excluding Government Staff Cost

H. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 16 | P a g e

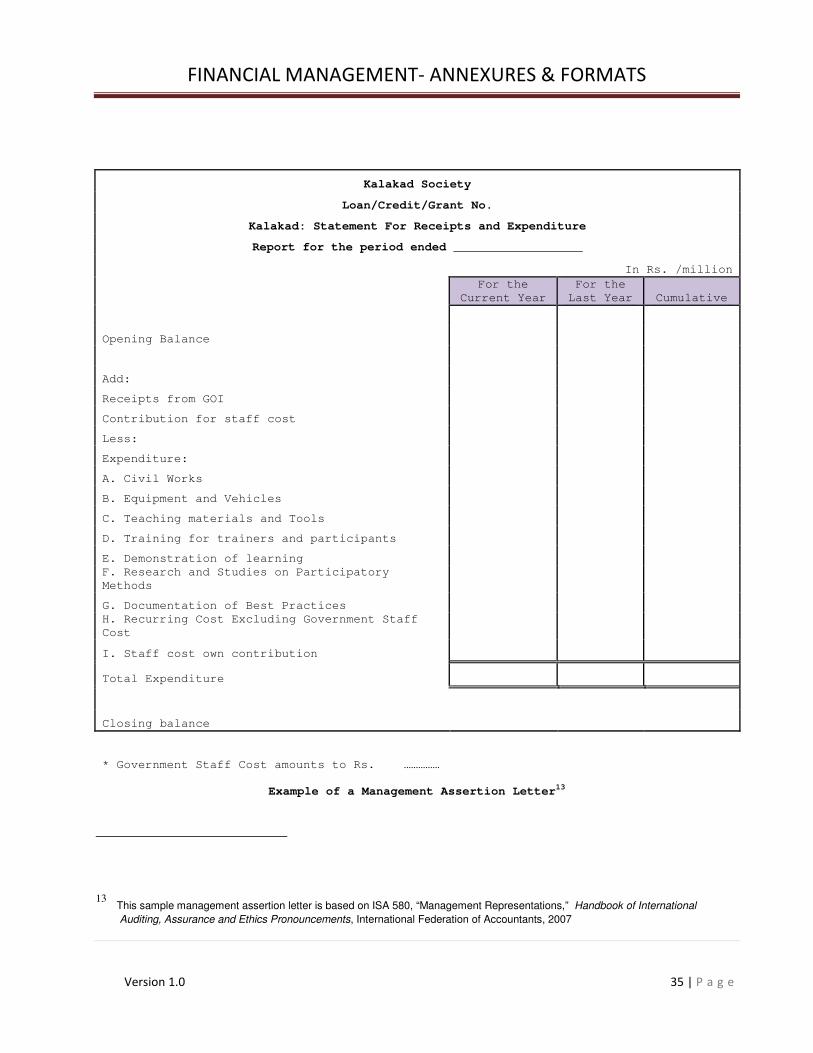

Kalakad

Loan/Credit/Grant No.

Kalakad: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the Current

Year

For the Last

Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Civil Works

B. Equipment and Vehicles

C. Teaching materials and Tools

D. Training for trainers and participants

E. Demonstration of learning

F. Research and Studies on Participatory Methods

G. Documentation of Best Practices

H. Recurring Cost Excluding Government Staff Cost

I. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 17 | P a g e

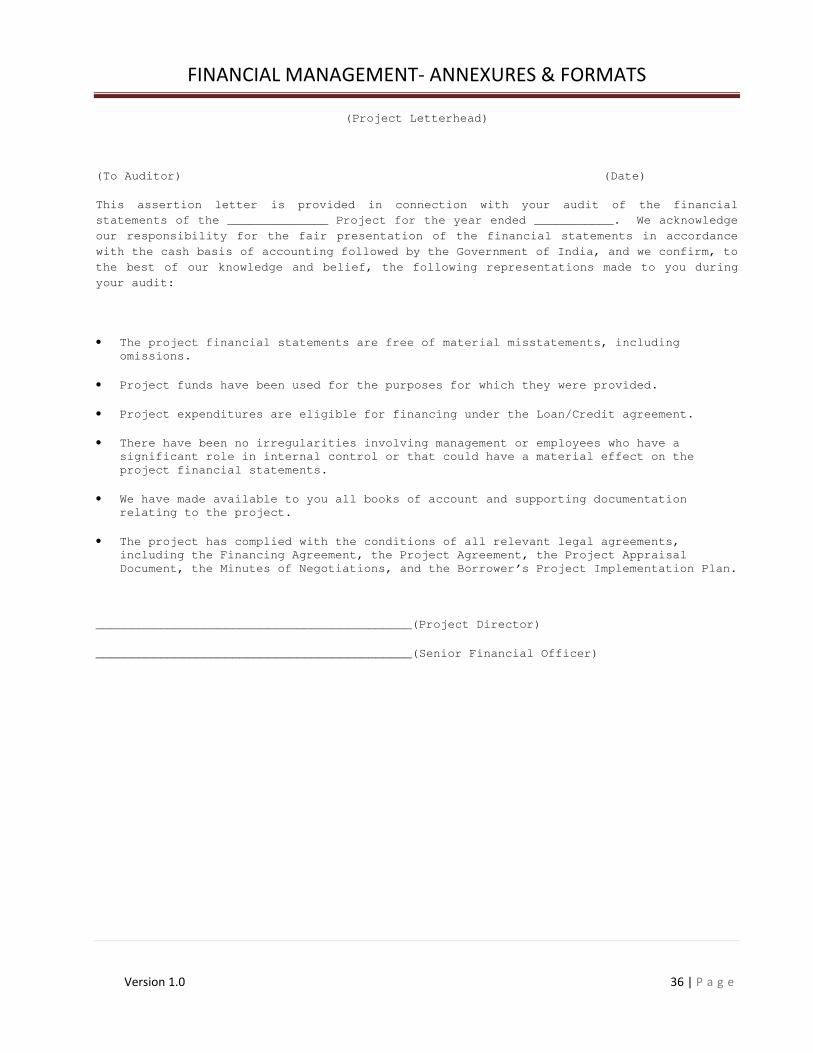

Example of a Management Assertion Letter6

(Project Letterhead)

(To Auditor) (Date)

This assertion letter is provided in connection with your audit of the financial

statements of the ______________ Project for the year ended ___________. We acknowledge

our responsibility for the fair presentation of the financial statements in accordance

with the cash basis of accounting followed by the Government of India, and we confirm, to

the best of our knowledge and belief, the following representations made to you during

your audit:

• The project financial statements are free of material misstatements, including

omissions.

• Project funds have been used for the purposes for which they were provided.

• Project expenditures are eligible for financing under the Loan/Credit agreement.

• There have been no irregularities involving management or employees who have a

significant role in internal control or that could have a material effect on the

project financial statements.

• We have made available to you all books of account and supporting documentation

relating to the project.

• The project has complied with the conditions of all relevant legal agreements,

including the Financing Agreement, the Project Agreement, the Project Appraisal

Document, the Minutes of Negotiations, and the Borrower’s Project Implementation Plan.

6 This sample management assertion letter is based on ISA 580, “Management Representations,” Handbook of International Auditing,

Assurance and Ethics Pronouncements, International Federation of Accountants, 2007

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 18 | P a g e

Sample Audit Report—Unqualified Opinion7

Report of the Comptroller and Auditor General of India

Addressee8

Report on the Project Financial Statements

We have audited the accompanying financial statements of the _______ Project financed

under World Bank Loan No._____/IDA, which comprise the Statement of Sources and

Applications of Funds and the Reconciliation of Claims to Total Applications of Funds9

for the year ended ______. These statements are the responsibility of the Project’s

management. Our responsibility is to express an opinion on the accompanying financial

statements based on our audit.

We conducted our audit in accordance with the Auditing Standards promulgated by the

Comptroller and Auditor General of India. Those Standards require that we plan and

perform the audit to obtain reasonable assurance about whether the financial statements

are free of material misstatement. Our audit examines, on a test basis, evidence

supporting the amounts and disclosures in the financial statements. It also includes

assessing the accounting principles used and significant estimates made by management, as

well as evaluating the overall statement presentation. We believe that our audit provides

a reasonable basis for our opinion.

In our opinion, the financial statements present fairly, in all material respects, the

sources and applications of funds of ________ Project for the year ended __________ in

accordance with Government of India accounting standards.10

7 See relevant portions of Auditing Standards of the Comptroller and Auditor General of India as applicable from time to time for

conditions where unqualified, qualified, adverse or disclaimers of opinion may appropriately be rendered.

8 The auditor’s report should be addressed to the person stipulated in the underlying loan agreement as responsible for providing

audited project financial statements.

9 Insert titles of other required statements and schedules included in or annexed to the project financial statements, if any.

10 Until the Ministry of Finance prescribes adoption of the accounting standards pronounced by GASAB or other body such as IPSAS, the accounting standards followed by the Government of India shall be the cash basis of accounting applied with due regard to the General Financial Rules, PWD codes, Treasury codes and similar financial rules and codes as are in effect and applicable to the operations of the project.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 19 | P a g e

In addition, in our opinion, (a) with respect to IUFRs, adequate supporting documentation

has been maintained to support claims to the World Bank for reimbursements of

expenditures incurred; and (b) except for ineligible expenditures as detailed in the

audit observations, if any, appended to this audit report, expenditures are eligible for

financing under the Loan/Credit Agreement. During the course of the audit, IUFRs (each

application no. and amount to be indicated) and the connected documents were examined and

these can be relied upon to support reimbursement under the Loan/Credit Agreement.

This report is issued without prejudice to CAG’s right to incorporate the audit

observations in the Report of CAG of India for being laid before Parliament/State or UT

Legislature.

[Auditor’s Signature]

[Auditor’s Address]

[Date]

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 20 | P a g e

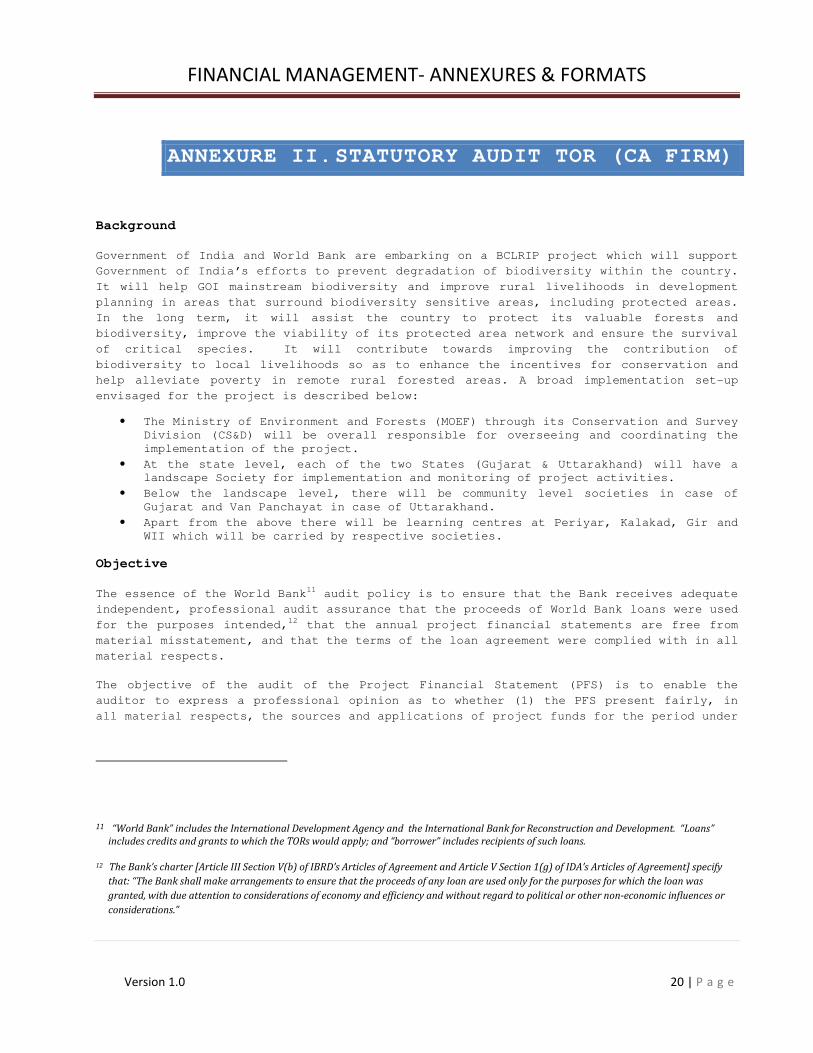

ANNEXURE II. STATUTORY AUDIT TOR (CA FIRM)

Background

Government of India and World Bank are embarking on a BCLRIP project which will support

Government of India’s efforts to prevent degradation of biodiversity within the country.

It will help GOI mainstream biodiversity and improve rural livelihoods in development

planning in areas that surround biodiversity sensitive areas, including protected areas.

In the long term, it will assist the country to protect its valuable forests and

biodiversity, improve the viability of its protected area network and ensure the survival

of critical species. It will contribute towards improving the contribution of

biodiversity to local livelihoods so as to enhance the incentives for conservation and

help alleviate poverty in remote rural forested areas. A broad implementation set-up

envisaged for the project is described below:

• The Ministry of Environment and Forests (MOEF) through its Conservation and Survey

Division (CS&D) will be overall responsible for overseeing and coordinating the

implementation of the project.

• At the state level, each of the two States (Gujarat & Uttarakhand) will have a

landscape Society for implementation and monitoring of project activities.

• Below the landscape level, there will be community level societies in case of

Gujarat and Van Panchayat in case of Uttarakhand.

• Apart from the above there will be learning centres at Periyar, Kalakad, Gir and

WII which will be carried by respective societies.

Objective

The essence of the World Bank11 audit policy is to ensure that the Bank receives adequate

independent, professional audit assurance that the proceeds of World Bank loans were used

for the purposes intended,12 that the annual project financial statements are free from

material misstatement, and that the terms of the loan agreement were complied with in all

material respects.

The objective of the audit of the Project Financial Statement (PFS) is to enable the

auditor to express a professional opinion as to whether (1) the PFS present fairly, in

all material respects, the sources and applications of project funds for the period under

11 “World Bank” includes the International Development Agency and the International Bank for Reconstruction and Development. “Loans”

includes credits and grants to which the TORs would apply; and “borrower” includes recipients of such loans.

12 The Bank’s charter [Article III Section V(b) of IBRD’s Articles of Agreement and Article V Section 1(g) of IDA’s Articles of Agreement] specify

that: “The Bank shall make arrangements to ensure that the proceeds of any loan are used only for the purposes for which the loan was

granted, with due attention to considerations of economy and efficiency and without regard to political or other non-economic influences or

considerations.”

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 21 | P a g e

audit examination, (2) the funds were utilized for the purposes for which they were

provided, and (3) expenditures shown in the PFS are eligible for financing under the

relevant loan or credit agreement. In addition, where applicable, the auditor will

express a professional opinion as to whether the IUFRs submitted by project management

may be relied upon to support any applications for withdrawal, and whether adequate

supporting documentation has been maintained to support claims. The books of account that

provide the basis for preparation of the PFS are established to reflect the financial

transactions of the project and are maintained by the project implementation agencies.

Standards

The audit will be carried out in accordance with the Auditing Standards promulgated by

ICAI. The auditor should accordingly consider materiality when planning and performing

the audit to reduce audit risk to an acceptable level that is consistent with the

objective of the audit. Although the responsibility for preventing irregularity, fraud,

or the use of loan proceeds for purposes other than as defined in the legal agreement

remains with the borrower, the audit should be planned so as to have a reasonable

expectation of detecting material misstatements in the project financial statements

Scope

The auditor is required to prepare a consolidated audit report as well as implementing

agency wise audit report for the project downstream entities. The auditor is required to

carry out the audit for the following entities Askote society, LRK society, Periyar, GIR

& KMTR LCS would be covered under this audit. The PFS submitted would have both the

consolidated PFS and implementing agency wise PFS. The auditor would be required to audit

the IUFRs made at each level.

In conducting the audit, special attention should be paid to the following:

(a) All external funds have been used in accordance with the conditions of the

relevant legal agreements and only for the purposes for which the financing was

provided. Relevant legal agreements include the Financing Agreement, the Project

Agreement, and the Minutes of Negotiations;

(b) Counterpart funds have been provided and used in accordance with the relevant

legal agreements and only for the purposes for which they were provided;

(c) All necessary supporting documents, records, and accounts have been kept in

respect of all project transactions including expenditures reported via IUFRs

where applicable. Clear linkages should exist between the books of account and

reports presented to the Bank; and

(d) The project accounts have been prepared in accordance with consistently applied

Accounting Standards and present fairly, in all material respects, the financial

situation of the project at the year end and of resources and expenditures for the

year ended on that date.

Project Financial Statements

The Project Financial Statements should include-

• Statement of Sources and Applications of Funds (consolidated PFS and implementing

agencies PFS)

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 22 | P a g e

• Reconciliation of Claims to Total Applications of Funds.

• A statement showing major heads of expenditure. (say by Project Component/Sub-

components)

• Statement showing entity wise transfer

Management Assertion

Management Assertion: Management should sign the project financial statements and

provide a written acknowledgement of its responsibility for the preparation and fair

presentation of the financial statements and an assertion that project funds have been

expended in accordance with the intended purposes as reflected in the financial

statements. An example of a Management Assertion Letter is shown below.

Interim Unaudited Financial Reports

In addition to the audit of the PFS, the auditor is required to audit all Interim

Unaudited Financial Reports (IUFRs) for withdrawal applications made during the period

under audit examination. The auditor should apply such tests as the auditor considers

necessary under the circumstances to satisfy the audit objective. In particular, these

expenditures should be carefully examined for project eligibility by reference to the

relevant financing agreements. Where ineligible expenditures are identified as having

been included in withdrawal applications and reimbursed against, these should be

separately noted by the auditor.

Audit Report

An audit report on the project financial statements should be prepared in accordance with

the Auditing Standards promulgated by the ICAI. Those standards require an audit opinion

to be rendered related to the financial statements taken as a whole, indicating

“unambiguously whether it is unqualified or qualified and, if the latter, whether it is

qualified in certain respects or is adverse or a disclaimer of opinion.” In addition,

the audit opinion paragraph will specify whether, in the auditor’s opinion, (a) with

respect to IUFRs, adequate supporting documentation has been maintained to support claims

to the World Bank for reimbursements of expenditures incurred; and (b) except for

ineligible expenditures as detailed in the audit observations, if any, appended to the

audit report, expenditures are eligible for financing under the Loan/Credit Agreement. A

sample audit report wording for an unqualified audit opinion is shown below.

The project financial statements and the audit report should be received by the Bank not

later than 6 months after the end of the fiscal year. The auditor should also submit two

copies of the audited accounts and audit report to the Implementing Agency.

Management Letter

In addition to the audit report on the project financial statements, the auditor should

prepare a management letter containing recommendations for improvements in internal

control and other matters coming to the attention of the auditor during the audit

examination. The management letter copy should be submitted to the Bank.

General

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 23 | P a g e

The auditor should be given access to any information relevant for the purposes of

conducting the audit. This would normally include all legal documents, correspondence,

and any other information associated with the project and deemed necessary by the

auditor. The information made available to the auditor should include, but not be

limited to, copies of the Bank’s Project Appraisal Document, the relevant Legal

Agreements, a copy of these Guidelines, and a copy of the Bank’s Financial Management

Assessment of the project entity. It is highly desirable that the auditor become

familiar with other Bank policy documents, such as OP/BP 10.02, the Bank's internal

guidelines on Financial Management that include financial reporting and auditing

requirements for projects financed by the World Bank. The auditor should also be

familiar with the Bank's Disbursement Manual. Both documents will be provided by the

Project staff to the auditor.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 24 | P a g e

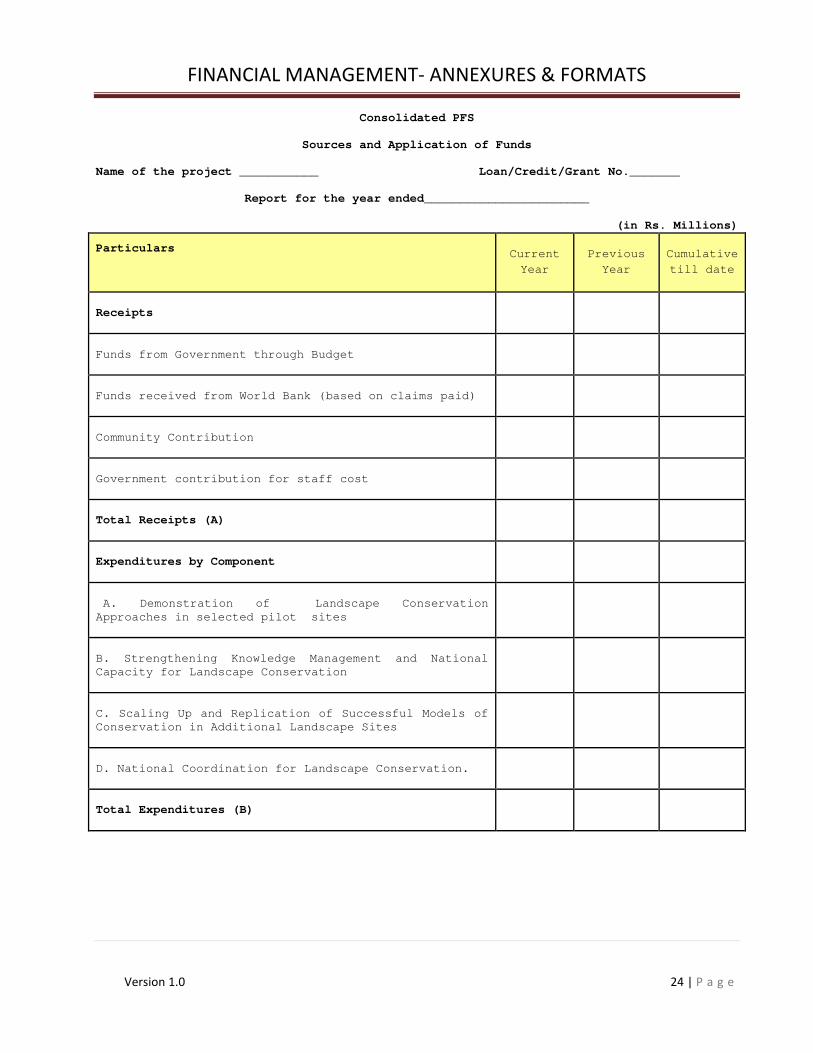

Consolidated PFS

Sources and Application of Funds

Name of the project ___________ Loan/Credit/Grant No._______

Report for the year ended_______________________

(in Rs. Millions)

Particulars Current

Year

Previous

Year

Cumulative

till date

Receipts

Funds from Government through Budget

Funds received from World Bank (based on claims paid)

Community Contribution

Government contribution for staff cost

Total Receipts (A)

Expenditures by Component

A. Demonstration of Landscape Conservation

Approaches in selected pilot sites

B. Strengthening Knowledge Management and National

Capacity for Landscape Conservation

C. Scaling Up and Replication of Successful Models of

Conservation in Additional Landscape Sites

D. National Coordination for Landscape Conservation.

Total Expenditures (B)

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 25 | P a g e

Notes:

1. This financial statement is prepared on a cash basis of accounting as per provisions of the Government Financial Rules and codes applicable.

2. The above figures will be based on monthly/quarterly abstract accounts prepared by the accounts compiling officers, duly reconciled by the respective agencies, with

details of un-reconciled amounts to be furnished.

3. Names of accounting units whose financial statements are aggregated to prepare the consolidated accounts.

4. Any other project specific Note.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 26 | P a g e

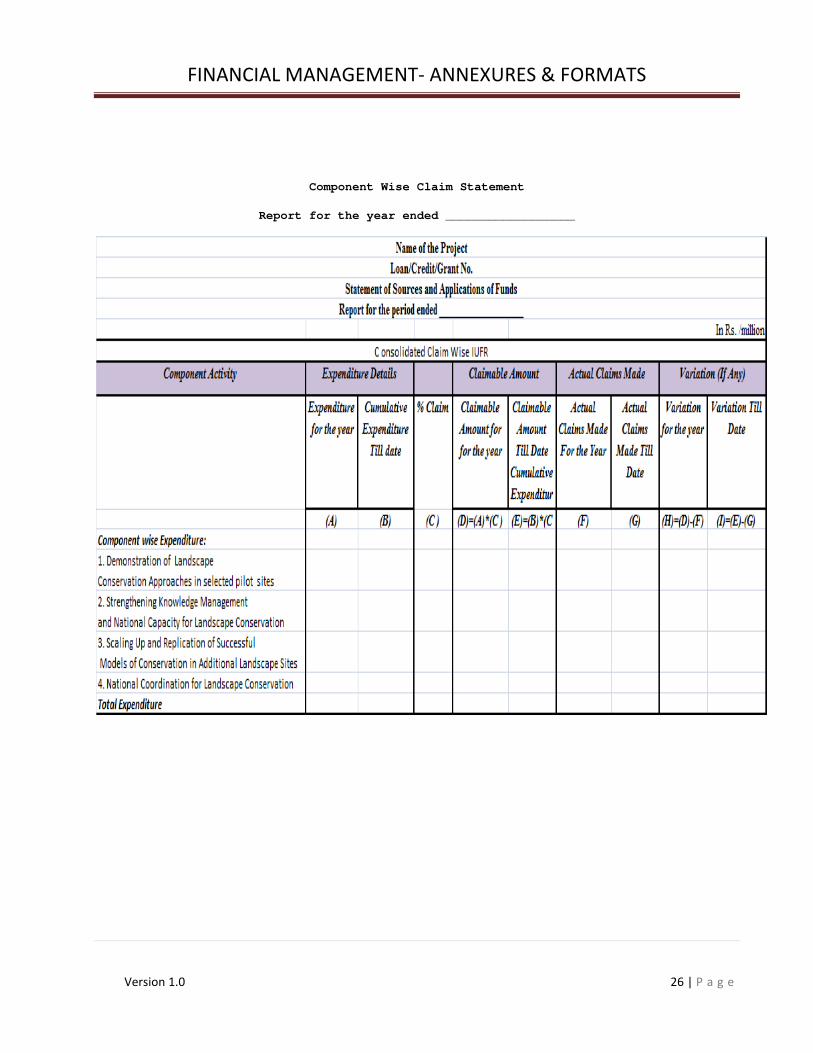

Component Wise Claim Statement

Report for the year ended __________________

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 27 | P a g e

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 28 | P a g e

List of Claims submitted to World Bank

Date Of Application Application Number Period Amount Claimed

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 29 | P a g e

Name of the Project Loan / Credit / Grant No.

Reconciliation of Claims to Total Applications of Funds

Report for the year ended

CFAO Project Director

Date Date

Schedules

Amt (Rs./Million)

Current

Year

Previous

Year

Project

to date

Bank Funds claimed during the year

• IUFR for the first quarter

• IUFR for the second quarter

• IUFR for the third quarter

• IUFR for the fourth quarter

Total Bank Funds claimed (A)

Total Expenditure made during the year (B)

Less: Outstanding AC bills (C) II

Ineligible expenditures (D) III

Advances not claimed (E) IV

Total Eligible Expenditures Claimed

(F)=(B)-(C)-(D)-(E)

World Bank Share @ x% of (F) above (G)

Amount to be claimed /refunded (H)=(A-G)

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 30 | P a g e

Notes:

1. Total expenditure made during the year (B above) must be the same as the Total

Expenditures shown on the Statement of Sources and Applications of Funds (B on

the Statement of Sources and Applications of Funds)

2. Outstanding AC bills (C above) reflect funds drawn against AC bills that have

been booked as expenditure but not settled by the end of the year (i.e.,

unsettled advances). The project should prepare a separate Schedule reflecting

the opening balance of unsettled AC bills, AC bills drawn during the year, AC

bills settled during the year, and AC bills unsettled at the end of the year.

3. Expenditures not claimed (E above) may reflect timing differences for eligible

expenditures incurred during the year but claimed after the year end.

4. Amounts A and G above must reconcile. If they indicate any excess/ shortage, it

needs to be explained and adjusted in future IUFR’s.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 31 | P a g e

Askot

Loan/Credit/Grant No.

Askot Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

Current Year

For the

Last Year Cumulative

Opening bank balance

Add:

Receipts from GOI

Contribution for staff cost

Community contribution

Less:

Transfer To Communities

Expenditure:

A. Strengthening Biodiversity Conservation Management

B. Mainstreaming Conservation and participatory

practices

C. Support to Participation in Learning networks

D. Communications

E. Recurring Cost Excluding Government Staff Cost

F. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

*Community contribution received in kind amounts to Rs._______

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 32 | P a g e

Kutch

Loan/Credit/Grant No.

Kutch Landscape: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

current

quarter

For the

Last Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Community contribution

Less:

Expenditure:

A. Strengthening Biodiversity Conservation Management

B. Mainstreaming Conservation and participatory

practices

C. Support to Participation in Learning networks (cross

visits)

D. Communications

E. Recurring Cost Excluding Government Staff Cost

F. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

*Community contribution received in kind is Rs.-_________

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 33 | P a g e

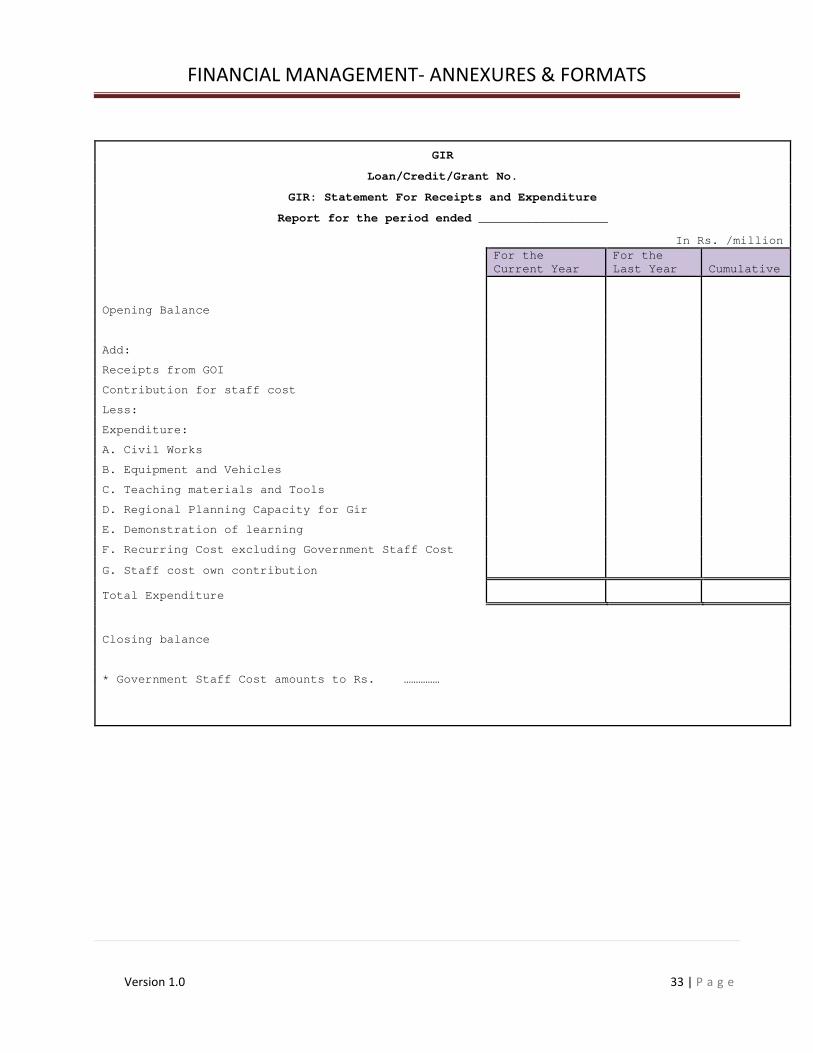

GIR

Loan/Credit/Grant No.

GIR: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

Current Year

For the

Last Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Civil Works

B. Equipment and Vehicles

C. Teaching materials and Tools

D. Regional Planning Capacity for Gir

E. Demonstration of learning

F. Recurring Cost excluding Government Staff Cost

G. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 34 | P a g e

Periyar

Loan/Credit/Grant No.

Periyar: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the Current year For the Last Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Civil Works

B. Equipment and Vehicles

C. Teaching materials and Tools

D. Training for trainers and participants

E. Demonstration of learning

F. Research and Studies on Participatory Methods

G. Documentation of Best Practices

H. Recurring Cost Excluding Government Staff Cost

I. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 35 | P a g e

Kalakad Society

Loan/Credit/Grant No.

Kalakad: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

Current Year

For the

Last Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Civil Works

B. Equipment and Vehicles

C. Teaching materials and Tools

D. Training for trainers and participants

E. Demonstration of learning

F. Research and Studies on Participatory

Methods

G. Documentation of Best Practices

H. Recurring Cost Excluding Government Staff

Cost

I. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

Example of a Management Assertion Letter13

13 This sample management assertion letter is based on ISA 580, “Management Representations,” Handbook of International

Auditing, Assurance and Ethics Pronouncements, International Federation of Accountants, 2007

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 36 | P a g e

(Project Letterhead)

(To Auditor) (Date)

This assertion letter is provided in connection with your audit of the financial

statements of the ______________ Project for the year ended ___________. We acknowledge

our responsibility for the fair presentation of the financial statements in accordance

with the cash basis of accounting followed by the Government of India, and we confirm, to

the best of our knowledge and belief, the following representations made to you during

your audit:

• The project financial statements are free of material misstatements, including

omissions.

• Project funds have been used for the purposes for which they were provided.

• Project expenditures are eligible for financing under the Loan/Credit agreement.

• There have been no irregularities involving management or employees who have a

significant role in internal control or that could have a material effect on the

project financial statements.

• We have made available to you all books of account and supporting documentation

relating to the project.

• The project has complied with the conditions of all relevant legal agreements,

including the Financing Agreement, the Project Agreement, the Project Appraisal

Document, the Minutes of Negotiations, and the Borrower’s Project Implementation Plan.

We have audited the accompanying financial statements of the _______ Project financed

under World Bank Loan No._____/IDA, which comprise the Statement of Sources and

Applications of Funds and relevant annexure for the year ended ______. These statements

are the responsibility of the Project’s management. Our responsibility is to express an

opinion on the accompanying financial statements based on our audit.

We conducted our audit in accordance with the Auditing Standards promulgated by the ICAI.

Those Standards require that we plan and perform the audit to obtain reasonable assurance

about whether the financial statements are free of material misstatement. Our audit

examines, on a test basis, evidence supporting the amounts and disclosures in the

financial statements. It also includes assessing the accounting principles used and

significant estimates made by management, as well as evaluating the overall statement

presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements present fairly, in all material respects, the

sources and applications of funds of ________ Project for the year ended __________ in

accordance with government accounting standards.

In addition, in our opinion, (a) with respect to SOEs, adequate supporting documentation

has been maintained to support claims to the World Bank for reimbursements of

expenditures incurred; and (b) except for ineligible expenditures as detailed in the

audit observations, if any, appended to this audit report, expenditures are eligible for

financing under the Loan/Credit Agreement. During the course of the audit, SOEs/FMRs

(each application no. and amount to be indicated) and the connected documents were

examined and these can be relied upon to support reimbursement under the Loan/Credit

Agreement.

[Auditor’s Signature]

[Auditor’s Address]

[Date]

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 38 | P a g e

ANNEXURE III. INTERNAL AUDIT TOR

INTRODUCTION

Government of India and World Bank are embarking on a BCLRIP project which will support

Government of India’s efforts to prevent degradation of biodiversity within the country.

It will help GOI mainstream biodiversity and improve rural livelihoods in development

planning in areas that surround biodiversity sensitive areas, including protected areas.

In the long term, it will assist the country to protect its valuable forests and

biodiversity, improve the viability of its protected area network and ensure the survival

of critical species. It will contribute towards improving the contribution of

biodiversity to local livelihoods so as to enhance the incentives for conservation and

help alleviate poverty in remote rural forested areas.

PROJECT COMPONENTS:

The main components of the project are as follows:

a) Demonstration of Landscape Conservation Approaches in selected pilot sites b) Strengthening Knowledge Management and National Capacity for Landscape

Conservation

c) Scaling Up and Replication of Successful Models of Conservation in Additional

Landscape Sites

d) National Coordination for Landscape Conservation.

PROJECT IMPLEMENTATION UNITS

A broad implementation set-up envisaged for the project is described below:

a The Ministry of Environment and Forests (MOEF) through its Conservation and Survey

Division (CS&D) will be overall responsible for overseeing and coordinating the

implementation of the project.

b At the state level, each of the two States (Gujarat & Uttarakhand) will have a

landscape Society (registered under an appropriate Act) for implementation and

monitoring of project activities.

c Below the landscape level, there will be community level societies in case of

Gujarat and Van Panchayat in case of Uttarakhand.

d Apart from the above there will be learning centres at Periyar, Kalakad, Gir and

WII which will be carried by respective societies.

ACCOUNTING ENTITIES

The project accounting would be maintained at following places:-

• MEF

• ASKOT Society

• LRK

• Communities/Van Panchayat

• Periyar

• WII

• GIR

• KMTR

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 39 | P a g e

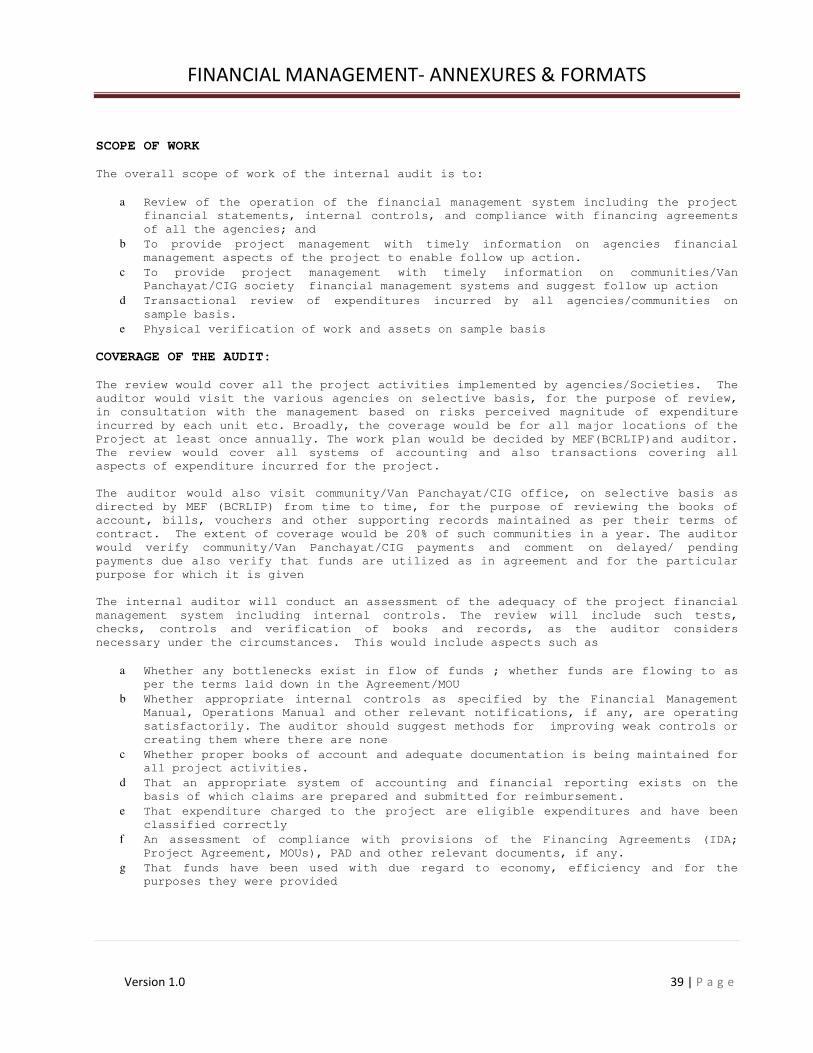

SCOPE OF WORK

The overall scope of work of the internal audit is to:

a Review of the operation of the financial management system including the project

financial statements, internal controls, and compliance with financing agreements

of all the agencies; and

b To provide project management with timely information on agencies financial

management aspects of the project to enable follow up action.

c To provide project management with timely information on communities/Van

Panchayat/CIG society financial management systems and suggest follow up action

d Transactional review of expenditures incurred by all agencies/communities on

sample basis.

e Physical verification of work and assets on sample basis

COVERAGE OF THE AUDIT:

The review would cover all the project activities implemented by agencies/Societies. The

auditor would visit the various agencies on selective basis, for the purpose of review,

in consultation with the management based on risks perceived magnitude of expenditure

incurred by each unit etc. Broadly, the coverage would be for all major locations of the

Project at least once annually. The work plan would be decided by MEF(BCRLIP)and auditor.

The review would cover all systems of accounting and also transactions covering all

aspects of expenditure incurred for the project.

The auditor would also visit community/Van Panchayat/CIG office, on selective basis as

directed by MEF (BCRLIP) from time to time, for the purpose of reviewing the books of

account, bills, vouchers and other supporting records maintained as per their terms of

contract. The extent of coverage would be 20% of such communities in a year. The auditor

would verify community/Van Panchayat/CIG payments and comment on delayed/ pending

payments due also verify that funds are utilized as in agreement and for the particular

purpose for which it is given

The internal auditor will conduct an assessment of the adequacy of the project financial

management system including internal controls. The review will include such tests,

checks, controls and verification of books and records, as the auditor considers

necessary under the circumstances. This would include aspects such as

a Whether any bottlenecks exist in flow of funds ; whether funds are flowing to as

per the terms laid down in the Agreement/MOU

b Whether appropriate internal controls as specified by the Financial Management

Manual, Operations Manual and other relevant notifications, if any, are operating

satisfactorily. The auditor should suggest methods for improving weak controls or

creating them where there are none

c Whether proper books of account and adequate documentation is being maintained for

all project activities.

d That an appropriate system of accounting and financial reporting exists on the

basis of which claims are prepared and submitted for reimbursement.

e That expenditure charged to the project are eligible expenditures and have been

classified correctly

f An assessment of compliance with provisions of the Financing Agreements (IDA;

Project Agreement, MOUs), PAD and other relevant documents, if any.

g That funds have been used with due regard to economy, efficiency and for the

purposes they were provided

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 40 | P a g e

h That an adequate system is in place to ensure that goods, works and services are

being procured in accordance with relevant financing agreements and the

procurement procedures prescribed in the MOU is followed.

i That yearly work plans are prepared and expenditures are incurred as per approved

plans and variances if any are monitored and analyzed.

j That adequate record is maintained for assets created under the project including

details of cost, quantity and location. Physical verification of the assets is

being conducted by the management on a periodic basis and adequate records thereof

are maintained. The auditor should carryout physical verification of assets for at

least 20% base on the value and risk perceived.

k Whether Bank reconciliation statements are being prepared on a monthly basis.

l In case of State societies confirming that the books of account and balance sheet

prepared under the societies act match with the progress report submitted to MEF

(BCRLIP) and clear linkages exist between the books of account and statements

submitted to MEF (BCRLIP).

m Verifying compliance with recommendation of the earlier audit reports and

commenting thereon.

n Verify Interim Unaudited Financial Reports (IUFR) on the basis of books of

accounts maintained by agencies.

TIMING AND REPORTING:

The internal audit would be carried out on Quarterly basis throughout the year. The

auditor will provide quarterly reports to the project management highlighting the

findings made during the quarterly internal audit of Society/community/Van Panchayat

review. This will be in the form of a Management Letter which will inter-alia include;

� Comments and observations on the Society/community/Van Panchayat/Forest

Department financial management records systems and controls that were examined

during the course of the review.

� Comments on the expenditure and works of the Society/community/Van

Panchayat/Forest Department, funds utilized with respect to the purpose for

which they have been provided, and for any mis-application / mis-utilisation.

� Deficiencies and areas of weaknesses in systems and controls of the

Society/community/Van Panchayat/Forest Department and recommendation for their

improvement

� Compliance with covenants in the financing agreement and comments, if any, on

internal and external matters affecting such compliance

� Matters that have come to attention during the review and might have a

significant impact on the implementation of the project

� Any special review procedures required of a compliance nature (for example,

compliance of the procurement procedures etc., recommended by the World Bank)

� Any other matters that the auditor considers pertinent

The reports should be submitted as follows:

• Quarterly reports should be submitted within 45 days from the end of the quarter.

• Annual Report: Consolidated annual report for the financial year shall be

submitted along with the last quarter report.

DATA SERIES AND FACILITIES TO BE PROVIDED BY THE CLIENT

The auditor would be given access to all documents, correspondence, vouchers, registers,

records, certificates, cash book, bank book, payment registers, tank expenditure

registers UCs, expenditure statements and any other information relating to the project

and deemed necessary by the Auditor. The Auditor should become familiar with and stay

updated on the project, and with the relevant policies and guidelines of the State

Government and the World Bank (including those relating to disbursements, procurement and

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 41 | P a g e

financial management and reporting). The Auditor would be provided copies of the Project

Implementation Plan; Project Appraisal Document (PAD) of the World Bank; Development

Credit Agreement, Loan Agreement and Project Agreement with IDA (including agreed minutes

of negotiations), guidelines, policies and procedures issued by project management and

implementing agencies; and relevant World Bank policies and guidelines (such as World

Bank’s Guidelines on Financial Reporting and Auditing, Financial Accounting and Reporting

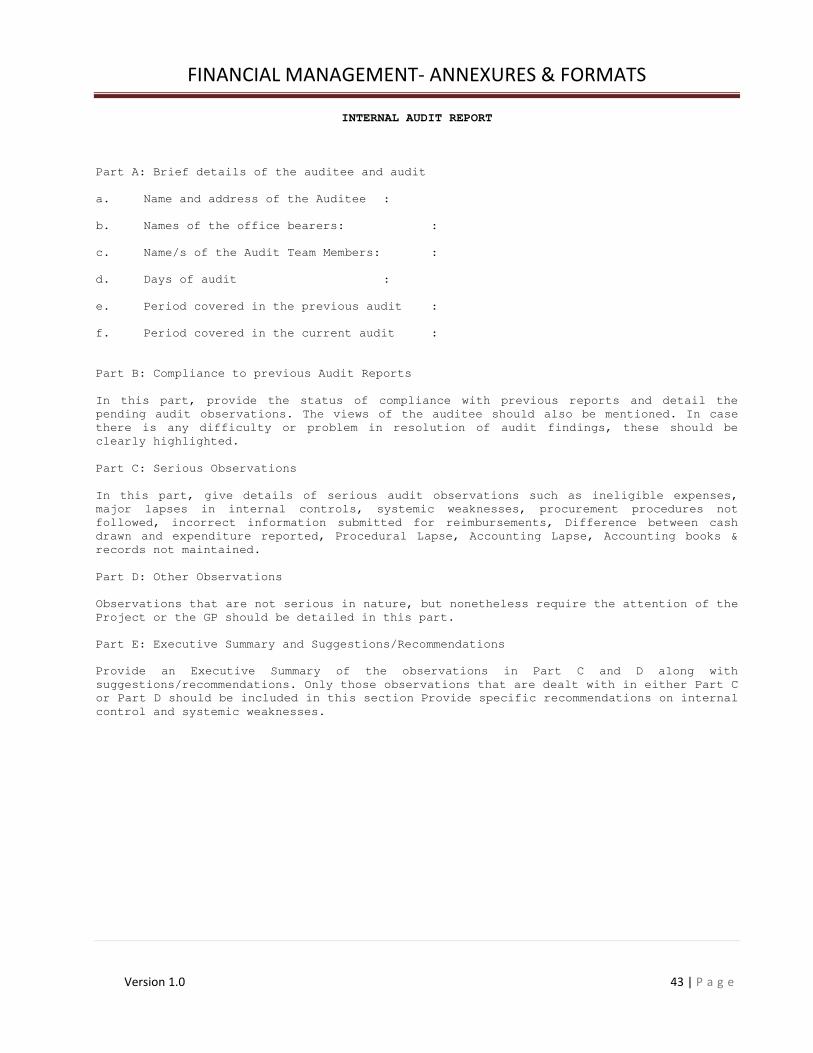

Observations that are not serious in nature, but nonetheless require the attention of the

Project or the GP should be detailed in this part.

Part E: Executive Summary and Suggestions/Recommendations

Provide an Executive Summary of the observations in Part C and D along with

suggestions/recommendations. Only those observations that are dealt with in either Part C

or Part D should be included in this section Provide specific recommendations on internal

control and systemic weaknesses.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 44 | P a g e

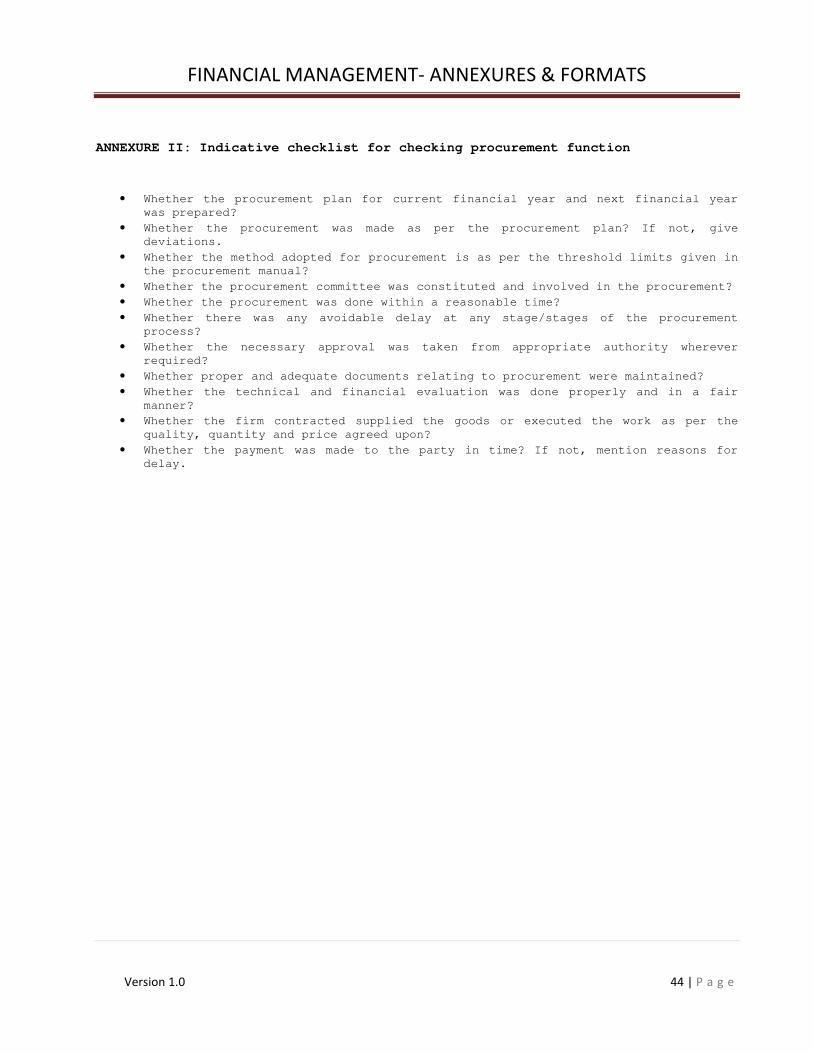

ANNEXURE II: Indicative checklist for checking procurement function

• Whether the procurement plan for current financial year and next financial year

was prepared?

• Whether the procurement was made as per the procurement plan? If not, give

deviations.

• Whether the method adopted for procurement is as per the threshold limits given in

the procurement manual?

• Whether the procurement committee was constituted and involved in the procurement?

• Whether the procurement was done within a reasonable time?

• Whether there was any avoidable delay at any stage/stages of the procurement

process?

• Whether the necessary approval was taken from appropriate authority wherever

required?

• Whether proper and adequate documents relating to procurement were maintained?

• Whether the technical and financial evaluation was done properly and in a fair

manner?

• Whether the firm contracted supplied the goods or executed the work as per the

quality, quantity and price agreed upon?

• Whether the payment was made to the party in time? If not, mention reasons for

delay.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 45 | P a g e

Annexure III: Illustrative Audit Checklist for communities/societies:

Name of the Community

Period covered:

Date of Visit:

Agreement No.

Sl.No. Audit Issue Yes No Remarks

1 Whether separate bank account is maintained by

community

2 Cash and bank book is kept update and is signed

by the authorized persons.

3 Cash balance in the books reconciles with

physical cash in hand (Do a cash count)

4 Whether Funds held in fixed deposit.

5 General Ledger is written up to date (give date)

6 All the vouchers are serially numbered and filed

properly

7 Bank reconciliation has been done at the end of

each month

8 Advances are classified separately and are not

included in the SOE.

Advances are adjusted on the basis of the bills

of the contractors

10 Are there advances outstanding for more than 6

months

11 Are there funds flow delays to the auditee unit.

If yes, give instances.

12 Are there any pre-signed blank cheques or large

cash withdrawals.

13 Whether all the other documents and register as

mentioned in financial management manual are

maintained or not.

14 Whether there are cases of diversion of funds or

mis utilization of funds.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 46 | P a g e

ANNEXURE IV. INTERIM UNAUDITED FINANCIAL

REPORT

** All the IUFRs would be signed by the project director and the finance officer of the

respective entities.

IUFR I: CONSOLIDATED IUFR (TO BE PREPARED BY MEF) EVERY QUARTER

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 47 | P a g e

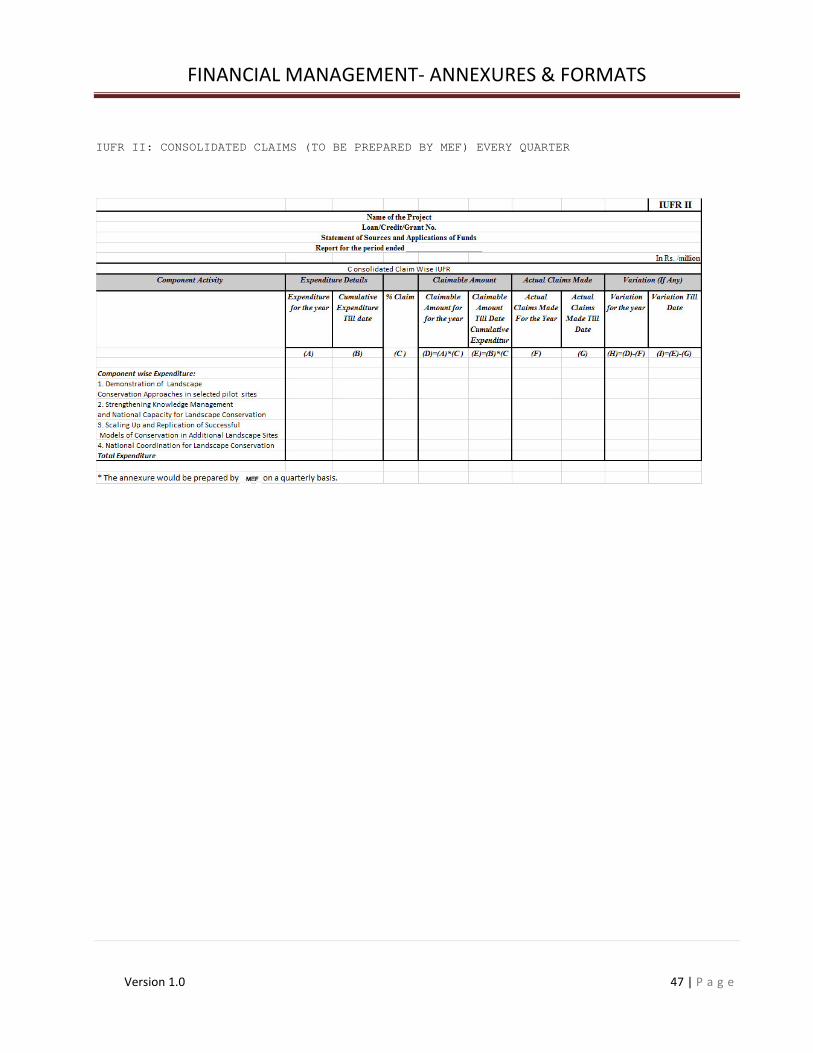

IUFR II: CONSOLIDATED CLAIMS (TO BE PREPARED BY MEF) EVERY QUARTER

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 48 | P a g e

IUFR III: CONSOLIDATED CLAIMS (TO BE PREPARED BY MEF (BCRLIP)) EVERY QUARTER

IUFR III

List of Claims submitted to World Bank

Date Of

Application Application Number Period Amount Claimed

* The annexure would be prepared by MEF (BCRLIP) on a quarterly basis.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 49 | P a g e

IUFR IV: CONSOLIDATED CLAIMS (TO BE PREPARED BY MEF) EVERY QUARTER

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 50 | P a g e

IUFR V: MEF (BCRLIP) TO BE PREPARED EVERY QUARTER

MEF (BCRLIP)

Loan/Credit/Grant No.

MEF Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

quarter

For the

Year Cumulative

1. Receipts from GOI

2. Government contribution for staff cost

Total sources

Expenditure:

A. Development of Landscape Biodiversity Cons.

Mgmt

B. Project Administration

C. Recurring Cost Excluding Government Staff Cost

D. Government staff cost

Total Expenditure

* Government Staff Cost amounts to Rs. ……………

* The annexure would be prepared by MEF (BCRLIP)on a quarterly

basis.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 51 | P a g e

IUFR VI: WII (TO BE PREPARED BY WII) EVERY QUARTER

WII

Loan/Credit/Grant No.

WII Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

quarter

For the

Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Support to Landscape Sites

B. Support to Learning Management Centres

C. Core Training Program

D. Institutional and Methodological Framework

E. Institutional Strengthening of WII

F. Project Management Cell

G. Recurring Cost Excluding Government Staff Cost

H. Staff cost

I. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

* The annexure would be prepared by WII on a quarterly basis and submitted to MEF (BCRLIP)

within 30days from the end of the quarter.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 52 | P a g e

IUFR VII: ASKOT (TO BE PREPARED BY ASKOT SOCIETY) EVERY QUARTER

Askot

Loan/Credit/Grant No.

Askot Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

quarter

For the

Year Cumulative

Opening bank balance

Add:

Receipts from GOI

Contribution for staff cost

Community contribution

Less:

Transfer To Communities

Expenditure:

A. Strengthening Biodiversity Conservation Management

B. Mainstreaming Conservation and participatory

practices

C. Support to Participation in Learning networks

D. Communications

E. Recurring Cost Excluding Government Staff Cost

F. Staff cost

G. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

* The annexure would be prepared by Askot on a quarterly basis and submitted to MEF (BCRLIP)

within 30days from the end of the quarter.

*Community contribution received in kind amounts to Rs._______

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 53 | P a g e

IUFR VIII: LRK (TO BE PREPARED BY LRK SOCIETY) EVERY QUARTER

Kutch

Loan/Credit/Grant No.

Kutch Landscape: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

quarter

For the

Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Community contribution

Less:

Expenditure:

A. Strengthening Biodiversity Conservation Management

B. Mainstreaming Conservation and participatory

practices

C. Support to Participation in Learning networks (cross

visits)

D. Communications

E. Recurring Cost Excluding Government Staff Cost

F. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

* The annexure would be prepared by Kutch on a quarterly basis and submitted to

MEF(BCRLIP)within 30days from the end of the quarter.

*Community contribution received in kind is Rs.-

_________

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 54 | P a g e

IUFR IX: GIR(TO BE PREPARED BY GIR LION SOCIETY) EVERY QUARTER

GIR

Loan/Credit/Grant No.

GIR: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

quarter

For the

Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Civil Works

B. Equipment and Vehicles

C. Teaching materials and Tools

D. Regional Planning Capacity for Gir

E. Demonstration of learning

F. Recurring Cost excluding Government Staff Cost

G. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

* The annexure would be prepared by GIR on a quarterly basis and submitted to MEF (BCRLIP)

within 30days from the end of the quarter.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 55 | P a g e

IUFR X: PERIYAR (TO BE PREPARED BY PTR SOCIETY) EVERY QUARTER

Periyar

Loan/Credit/Grant No.

Periyar: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

quarter

For the

Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Civil Works

B. Equipment and Vehicles

C. Teaching materials and Tools

D. Training for trainers and participants

E. Demonstration of learning

F. Research and Studies on Participatory

Methods

G. Documentation of Best Practices

H. Recurring Cost Excluding Government

Staff Cost

I. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 56 | P a g e

IUFR XI: KMTR (TO BE PREPARED BY KMTR SOCIETY) EVERY QUARTER

Kalakad

Loan/Credit/Grant No.

Kalakad: Statement For Receipts and Expenditure

Report for the period ended __________________

In Rs. /million

For the

quarter

For the

Year Cumulative

Opening Balance

Add:

Receipts from GOI

Contribution for staff cost

Less:

Expenditure:

A. Civil Works

B. Equipment and Vehicles

C. Teaching materials and Tools

D. Training for trainers and participants

E. Demonstration of learning

F. Research and Studies on Participatory

Methods

G. Documentation of Best Practices

H. Recurring Cost Excluding Government Staff

Cost

I. Staff cost own contribution

Total Expenditure

Closing balance

* Government Staff Cost amounts to Rs. ……………

* The annexure would be prepared by Kalakad on a quarterly basis and submitted to MEF

(BCRLIP) within 30days from the end of the quarter.

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 57 | P a g e

ANNEXURE V. MOU

MEMORANDUM OF UNDERSTANDING

BETWEEN

THE MINISTRY OF ENVIRONMENT AND FORESTS

(CONSERVATION AND SURVEY DIVISION)

C.G.O.COMPLEX, LODHI ROAD

NEW DELHI

AND STATE LEVEL LANDSCAPES SOCIETY (LRK/ASKOTE)/WII/FLC SOCIETY (GIR,KALAKAD,PERIYAR)

This Memorandum of Understanding made this …………day of …………between the Ministry of

Environment and Forests, acting through the Conservation and Survey Division C.G.O.

Complex, Lodhi Road, New Delhi-110003 (hereinafter referred to as the ‘CS&D’) of the

First Part and the State level landscape societies (LRK/ Askote/WII/ Field Learning

Centres/Societies (Gir, Kalakad, Periyar) acting through (designation and office

address), (hereinafter referred to as the Grantee), of the Second Part.

Whereas the Grantee has submitted a proposal to the Ministry of Environment and

Forests, seeking financial assistance for implementation of Biodiversity Conservation and

Rural Livelihood Improvement Project (BCRLIP) activities ……… hereinafter referred to as

the “Annual Plan of Operation”.

Biodiversity Conservation and Rural Livelihood Improvement Project (BCRLIP) aims

to enhance institutional capacity for integrating sustainable livelihoods and

biodiversity conservation objectives add the landscape level. This is to be achieved by

improving policies, tools and methodologies, knowledge and skills for developing multi-

stakeholder partnerships that support mainstreaming of biodiversity conservation

objectives, improving rural livelihoods, enhancing learning and replication of successful

participatory conservation models, and improving cost-effectiveness and sustainable

funding for conservation of biodiversity at the landscape level.

And whereas the Ministry of Environment and Forests is ready and willing to

extend financial support for the approved items of the said work, on the terms and

conditions given below for the year and thereafter.

NOW, THEREFORE, IT IS HEREBY AGREED between the Parties as follows:

ARTICLE – 1

Obligation of the Ministry of the Environment and Forests (through the CS&D). The

Ministry of the Environment and Forests has agreed and affirmed that:-

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 58 | P a g e

(1) The total approved funding for the period _______________ as per the Annual Plan

of Operation is ________________.

(2) Funding support under BCRLIP shall be made available to the ……………… in three

phases on receipt of the Annual Plan of Operation with cost estimates of work

plan of the project activities to be undertaken during a year.

a. The first installment of the funding support under the BCRLIP would be

released on approval of Annual Plan of Operations. The quantum of grant

would be 40% of the approved APO. The amount would be released within 2

weeks subject to availability of funds and the directions of the ministry of

Finance.

b. The second installment of 40% of approved APO under the BCRLIP would be

released by two weeks on receipt of UC for the 80% expenditure of the first

installment.

c. The third installment of 20% of approved APO under the BCRLIP would be

released within two weeks of receipt of first installment Utilization

Certificate. This should also indicate the 100% utilization of the 1st

installment and 80% of the second installment.

(3) To provide technical guidance on project related issues.

(4) To monitor the progress of the work as per the action plan through field visits

and through consultants as and when required.

ARTICLE-II

Obligation of Society/Wildlife Institute of India (WII)/FLC Societies that:-

The Society has agreed and affirmed that:-

(1) Annual Plan of Operation, shall be prepared for which the funding support is being

sought from Government of India as per the prescribed guidelines within a given

time. The Annual Plan of Operations must indicate the location/area of proposed

initiative/initiatives on a map, along with physical target, financial target and

unit rate, with the basis of estimation. The implementing agency has to ensure

that the Central Assistance being released will be gainfully utilized in

furtherance of the approved world programme without any time overrun under the

project/scheme. The proposed area coverage under the work programme should be

over-lapping with any other Central/State scheme. There should be no duplication

of central/external assistance in any case.

(2) A staff development plan should be prepared and submitted to the MEF for ensuring

frontline staff with the capacity to perform field work. The agreed staff

vacancies shall be filled up by the society for ensuring effective implementations

of BCRLIP activities.

(3) The society shall deposit the fund received under this project in their exclusive

and separate current account in a Nationalized Bank, which would be operated by

Chairman/Member Secretary of the society.

(4) The Society shall submit a quarterly report and an annual report to the

MEF(BCRLIP), in the form and substance as prescribed by MEF from time to time.

The progress report should invariably indicate the physical achievement (Viz….,

quantity, number area indicating location) and the objectives fulfilled on

implementation of proposed activities. A year-wise photo catalogue of physical

targets shall be maintained to facilitate verification during supervisory visits.

(5) The Society shall ensure full accountability for all funds provided by MEF/Bank.

All financial transactions should be clearly recorded with supporting details and

would be subject to audit & scrutiny of members at large. The State Level

Landscape Society will ensure that the Account of the grants released by MEF are

FINANCIAL MANAGEMENT- ANNEXURES & FORMATS

Version 1.0 59 | P a g e

audited by Statutory Auditor on an annual basis and a certificate to this affect

will be sent to MEF annually latest by 31st May each year. Proper Financial

Statement along with disclosures including clear statement of the accounting

policies would be available for any member.

(6) The money released by the MoEF through the Conservation and Survey Division shall

be made available to Community Groups (User Groups/Van Panchayts) for taking up

the works proposed in the Annual Plan of Operation (APO) immediately with due

compliance of her normative guidelines and advisories of the said Authority.

(7) The Society should consult with Panchayati Raj Institutions for providing

ecologically viable livelihood options to reduce villagers’ dependence on forest.

The Gram Sabha should be involved in restoring forest cover in the areas in order

to provide a supplementary habitat to animals moving out of that areas.