71

BIS Quarterly Review June 2019 International banking and financial market developments BIS

BIS Quarterly Review

June 2019

International banking and financial market developments

BIS

BIS Quarterly Review Monetary and Economic Department

Editorial Committee:

Claudio Borio Stijn Claessens Benoît Mojon Hyun Song Shin Philip Wooldridge

General queries concerning this commentary should be addressed to Philip Wooldridge (tel +41 61 280 8006, e-mail: [email protected]), queries concerning specific parts to the authors, whose details appear at the head of each section, and queries concerning the statistics to Patrick McGuire (tel +41 61 280 8921, e-mail: [email protected]).

This publication is available on the BIS website (www.bis.org/publ/qtrpdf/r_qt1906.htm).

© Bank for International Settlements 2019. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated.

ISSN 1683-0121 (print) ISSN 1683-013X (online)

BIS Quarterly Review, June 2019 iii

BIS Quarterly Review

June 2019

The June issue focuses on BIS statistics. Analyses of financial market developments will be included in the BIS Annual Economic Report to be published on 30 June 2019. International banking and financial market developments

Concentration in cross-border banking ................................................................................... 1

Iñaki Aldasoro and Torsten Ehlers

Key takeaways ........................................................................................................................... 2

Distribution of cross-border banking relationships ................................................... 2

Box A: Analysing bilateral country links using the BIS international banking statistics ............................................................................ 4

Concentration and the fall in cross-border interbank credit .................................. 5

Conclusions ................................................................................................................................ 8

Box B: The importance of small cross-border banking links for emerging market economies ...................................................................... 9

BIS statistics: Charts ............................................................................................................... A1

Special features in the BIS Quarterly Review ..................................................... B1

List of recent BIS publications ....................................................................................... C1

Notations used in this Review

billion thousand million e estimated lhs, rhs left-hand scale, right-hand scale $ US dollar unless specified otherwise … not available . not applicable – nil or negligible Differences in totals are due to rounding. The term “country” as used in this publication also covers territorial entities that are not states as understood by international law and practice but for which data are separately and independently maintained.

iv BIS Quarterly Review, June 2019

Abbreviations

Currencies

ARS Argentine peso MAD Moroccan dirham

AUD Australian dollar MXN Mexican peso

BGN Bulgarian lev MYR Malaysian ringgit

BHD Bahraini dinar NOK Norwegian krone

BRL Brazilian real NZD New Zealand dollar

CAD Canadian dollar OTH all other currencies

CHF Swiss franc PEN Peruvian sol

CLP Chilean peso PHP Philippine peso

CNY (RMB) Chinese yuan (renminbi) PLN Polish zloty

COP Colombian peso RON Romanian leu

CZK Czech koruna RUB Russian rouble

DKK Danish krone SAR Saudi riyal

EUR euro SEK Swedish krona

GBP pound sterling SGD Singapore dollar

HKD Hong Kong dollar THB Thai baht

HUF Hungarian forint TRY Turkish lira

IDR Indonesian rupiah TWD New Taiwan dollar

ILS Israeli new shekel USD US dollar

INR Indian rupee VES bolívar soberano

JPY Japanese yen ZAR South African rand

KRW Korean won

BIS Quarterly Review, June 2019 v

Countries

AE United Arab Emirates CY Cyprus

AF Afghanistan CZ Czech Republic

AL Albania DE Germany

AM Armenia DJ Djibouti

AO Angola DK Denmark

AR Argentina DM Dominica

AT Austria DO Dominican Republic

AU Australia DZ Algeria

AZ Azerbaijan EA euro area

BA Bosnia and Herzegovina EC Ecuador

BD Bangladesh EE Estonia

BE Belgium EG Egypt

BF Burkina Faso ER Eritrea

BG Bulgaria ES Spain

BH Bahrain ET Ethiopia

BI Burundi FI Finland

BJ Benin FJ Fiji

BM Bermuda FO Faeroe Islands

BN Brunei FR France

BO Bolivia GA Gabon

BR Brazil GB United Kingdom

BS The Bahamas GD Grenada

BT Bhutan GE Georgia

BY Belarus GH Ghana

BZ Belize GN Guinea

CA Canada GQ Equatorial Guinea

CD Democratic Republic of the Congo GR Greece

CF Central African Republic GT Guatemala

CG Republic of Congo GW Guinea-Bissau

CH Switzerland GY Guyana

CI Côte d’Ivoire HN Honduras

CL Chile HK Hong Kong SAR

CM Cameroon HR Croatia

CN China HT Haiti

CO Colombia HU Hungary

CR Costa Rica ID Indonesia

CV Cape Verde IE Ireland

vi BIS Quarterly Review, June 2019

Countries (cont)

IL Israel MW Malawi

IN India MX Mexico

IQ Iraq MY Malaysia

IR Iran MZ Mozambique

IS Iceland NG Nigeria

IT Italy NL Netherlands

JE Jersey NO Norway

JM Jamaica NR Nauru

JO Jordan NZ New Zealand

JP Japan OM Oman

KE Kenya PA Panama

KG Kyrgyz Republic PE Peru

KH Cambodia PG Papua New Guinea

KR Korea PH Philippines

KW Kuwait PK Pakistan

KY Cayman Islands PL Poland

KZ Kazakhstan PT Portugal

LA Laos PY Paraguay

LB Lebanon QA Qatar

LC St Lucia RO Romania

LK Sri Lanka RS Serbia

LR Liberia RU Russia

LS Lesotho RW Rwanda

LT Lithuania SA Saudi Arabia

LU Luxembourg SC Seychelles

LV Latvia SD Sudan

LY Libya SE Sweden

MA Morocco SG Singapore

MD Moldova SK Slovakia

ME Montenegro SI Slovenia

MK Macedonia FYR SR Suriname

MM Myanmar SS South Sudan

MN Mongolia ST São Tomé and Príncipe

MO Macao SAR SV El Salvador

MR Mauritania SZ Eswatini

MT Malta TD Chad

MU Mauritius TG Togo

MV Maldives TH Thailand

BIS Quarterly Review, June 2019 vii

Countries (cont)

TJ Tajikistan UZ Uzbekistan

TL East Timor VC St Vincent and the Grenadines

TM Turkmenistan VE Venezuela

TO Tonga VG British Virgin Islands

TR Turkey VN Vietnam

TT Trinidad and Tobago XM euro area

TW Chinese Taipei ZA South Africa

UA Ukraine ZM Zambia

US United States AE advanced economy

UY Uruguay EME emerging market economy

BIS Quarterly Review, June 2019 1

Concentration in cross-border banking1

Cross-border bank credit is dominated by a small number of very sizeable links between banks in one country and borrowers in another. The largest-sized cross-border banking links are mainly between major advanced economies. Concentration increased up until the Great Financial Crisis (GFC) and has abated only slightly since. It is higher for interbank credit than for credit to the non-bank sector. Despite the substantial decline in interbank credit in the aftermath of the GFC, concentration in the interbank segment has remained high.

JEL classification: G15, F30, G21.

A structural feature of cross-border banking is its high degree of concentration, with a small number of very large bilateral links accounting for the lion’s share of total global cross-border bank credit. The largest links are almost exclusively between advanced economies, while links involving emerging market economies (EMEs) tend to be of smaller size. Concentration in cross-border bank links increased up to the Great Financial Crisis (GFC) and remained high. Overall, it is higher for cross-border interbank credit compared with bank credit to the non-bank sector. While the share of cross-border interbank credit has fallen significantly since the GFC, concentration has remained high for interbank links.

The concentration of cross-border bank linkages is highly relevant for financial spillovers, as the GFC revealed (Ehlers and McGuire (2017), Avdjiev and Takáts (2014), Herrmann and Mihaljek (2013), Borio et al (2011)). In this article, we take a closer look at the size distribution as well as the sectoral composition of cross-border banking links at the country level. Cross-border interbank credit was particularly affected during the GFC (Claessens (2017)), including the model whereby local banks tap cross-border funding from global banks (Bruno and Shin (2014)). Using the BIS locational banking statistics (LBS), we document the pattern of bilateral (country-level) cross-border bank credit (assets) of banks located in one country vis-à-vis bank and non-bank borrowers in another.2

1 The authors would like to thank Stefan Avdjiev, Claudio Borio, Stijn Claessens, Bryan Hardy, Swapan-

Kumar Pradhan, Patrick McGuire, Benoît Mojon, Hyun Song Shin, Nikola Tarashev and Philip Wooldridge for valuable comments and suggestions, as well as Deimantė Kupčiūnienė for excellent research assistance. The views expressed in this article are those of the authors and do not necessarily reflect those of the BIS.

2 Creditor banks in a given country are in most cases also cross-border borrowers. This article, however, focuses only on one direction of cross-border bank linkages. While this greatly simplifies the analysis, it misses some relevant liabilities such as cross-border deposits. Nonetheless, it covers cross-border interbank linkages, which proved to be particularly important during the GFC.

Iñaki Aldasoro

Torsten Ehlers

2 BIS Quarterly Review, June 2019

The first section of this article documents the size distribution of cross-border banking links. It then shows that concentration is mainly due to links within advanced economies. The second section looks at the sectoral composition, focusing on the persistently higher concentration in cross-border interbank links relative to links vis-à-vis the non-bank sector.

Distribution of cross-border banking relationships

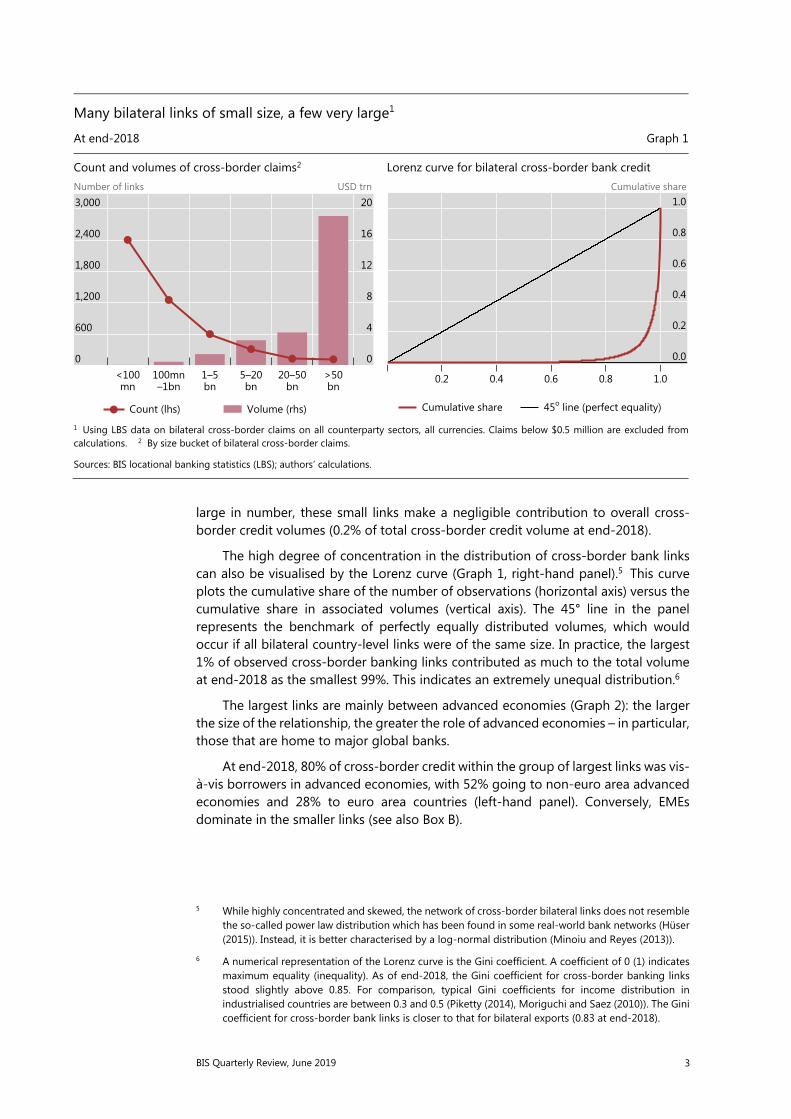

At end-2018, the outstanding stock of cross-border bank claims stood at $28.5 trillion.3 This stock consisted of the sum of 4,822 bilateral relationships between creditor banks in one country and borrowers in another (see Box A for a more detailed data description and a comparison with consolidated data). The concentration in cross-border links can be characterised along two complementary dimensions: the number of country-level links between banks and borrowers; and the size or volume of each link.4

A small number of links are exceptionally large in size and are behind the lion’s share of overall volumes (Graph 1, left-hand panel, bars). Two thirds of the $28.5 trillion in total lending as of end-2018 were accounted for by 117 bilateral relationships larger than $50 billion in size.

The flip side of the small number of very sizeable links is the high number of small-sized links (left-hand panel, line). As of end-2018, around 50% of all existing bilateral links at the country level were smaller than $100 million in volume. While

3 As our interest lies in country-to-country relationships, throughout our analysis we exclude cross-

border claims unallocated by counterparty country and vis-à-vis international organisations.

4 The precision of reporting in the LBS has improved with time. Up to Q2 2012, values were reported to the BIS in integers of millions of US dollars. Since then, values have been reported down to thousands of US dollars by most reporters. This can artificially influence the number of bilateral links. For this reason, in this article we set a threshold of $0.5 million for bilateral links to be considered, ie bilateral links smaller than that amount are set to zero.

Key takeaways

A small number of very large cross-border links dominate global cross-border bank credit. Only 2.4% of all bilateral links between banks in one country and borrowers in another were greater than $50 billion in size at end-2018, but they constituted a full two thirds of global cross-border bank credit volumes.

Concentration in cross-border bank credit is mainly due to links involving advanced economies. Just five major creditor countries – France, Germany, Japan, the United Kingdom and the United States – account for 55% of global cross-border credit and close to 70% of the volume of the largest bilateral country-level links.

Concentration is a structural feature of cross-border bank credit. Even amid a significant drop in cross-border interbank credit after the Great Financial Crisis (GFC), concentration in interbank links remained high. Concentration in cross-border credit to non-banks has increased since the GFC.

Small cross-border links account for an insignificant share of global bank credit but can be economically important for emerging market economies (Box B).

BIS Quarterly Review, June 2019 3

large in number, these small links make a negligible contribution to overall cross-border credit volumes (0.2% of total cross-border credit volume at end-2018).

The high degree of concentration in the distribution of cross-border bank links can also be visualised by the Lorenz curve (Graph 1, right-hand panel).5 This curve plots the cumulative share of the number of observations (horizontal axis) versus the cumulative share in associated volumes (vertical axis). The 45° line in the panel represents the benchmark of perfectly equally distributed volumes, which would occur if all bilateral country-level links were of the same size. In practice, the largest 1% of observed cross-border banking links contributed as much to the total volume at end-2018 as the smallest 99%. This indicates an extremely unequal distribution.6

The largest links are mainly between advanced economies (Graph 2): the larger the size of the relationship, the greater the role of advanced economies – in particular, those that are home to major global banks.

At end-2018, 80% of cross-border credit within the group of largest links was vis-à-vis borrowers in advanced economies, with 52% going to non-euro area advanced economies and 28% to euro area countries (left-hand panel). Conversely, EMEs dominate in the smaller links (see also Box B).

5 While highly concentrated and skewed, the network of cross-border bilateral links does not resemble

the so-called power law distribution which has been found in some real-world bank networks (Hüser (2015)). Instead, it is better characterised by a log-normal distribution (Minoiu and Reyes (2013)).

6 A numerical representation of the Lorenz curve is the Gini coefficient. A coefficient of 0 (1) indicates maximum equality (inequality). As of end-2018, the Gini coefficient for cross-border banking links stood slightly above 0.85. For comparison, typical Gini coefficients for income distribution in industrialised countries are between 0.3 and 0.5 (Piketty (2014), Moriguchi and Saez (2010)). The Gini coefficient for cross-border bank links is closer to that for bilateral exports (0.83 at end-2018).

Many bilateral links of small size, a few very large1

At end-2018 Graph 1

Count and volumes of cross-border claims2 Lorenz curve for bilateral cross-border bank credit Number of links USD trn Cumulative share

1 Using LBS data on bilateral cross-border claims on all counterparty sectors, all currencies. Claims below $0.5 million are excluded fromcalculations. 2 By size bucket of bilateral cross-border claims.

Sources: BIS locational banking statistics (LBS); authors’ calculations.

3,000

2,400

1,800

1,200

600

0

20

16

12

8

4

0

bnbnbnbn–1bnmn>5020–505–201–5100mn<100

Count (lhs) Volume (rhs)

1.0

0.8

0.6

0.4

0.2

0.0

1.00.80.60.40.2

Cumulative share 45o line (perfect equality)

4 BIS Quarterly Review, June 2019

Box A

Analysing bilateral country links using the BIS international banking statistics

The BIS international banking statistics (IBS) are collected by national authorities at the bank level but reported to the BIS at the country level; all banks in a given reporting country are aggregated together. Therefore, the IBS measure country-to-country links but do not measure the much larger number of bilateral links between individual banks and borrowers. At end-2018, the locational banking statistics (LBS) captured the positions of more than 8,000 banks, reported as 47 country aggregates. Banks reported their positions against borrowers in more than 215 countries, resulting in 5,927 country-to-country links. Many of these links are for insignificant amounts of less than $0.5 million. Excluding these small links results in 4,822 links greater than $0.5 million.

The LBS include intragroup business and measure the geographical concentration of cross-border business. For example, a US bank might route its cross-border business via a financial centre such as London, resulting in two links: from the United States to the United Kingdom, and from the United Kingdom to the country where the final borrower resides. Therefore, the LBS potentially underestimate concentration of bank creditors because the same banking group may operate in different countries at the same time. The BIS consolidated banking statistics (CBS) take a nationality perspective and consolidate the worldwide claims of a given banking group to the country where it is headquartered.

Not surprisingly, the number of links is much higher in the LBS than the CBS: 4,822 versus 3,550 at end-2018 (Graph A, left-hand panel). In part, this is due to differences in the number of reporting countries: 47 in the LBS, compared with 31 in the CBS. But the different reporting concepts of the LBS and the CBS mean that they cover different elements of international banking links. The CBS, by definition, do not contain claims between affiliates of the same banking group. The CBS, however, include credit extended locally by a foreign office of a given banking group. They distinguish between international claims (cross-border and local claims in foreign currency) and local claims in local currency. Internationally active banking groups tend to have large subsidiaries in advanced economies and in many major emerging market economies, reflected in a relatively high share of local claims in local currency.

In terms of how concentrated international banking is, the cross-border claims in the LBS and foreign claims in the CBS present a very similar picture (Graph A, right-hand panel; see also Graph 1, left-hand panel). The largest size group (>$50 billion) constitutes 3.1% of all consolidated links by number (versus 2.4% for LBS), which amount to 70% of all claims by volume (67% in the LBS). The smallest bilateral links (<$100 million) make up 49% of all consolidated links (50% for LBS) while they amount to only 0.1% of consolidated claims by volume (0.2% for LBS).

Concentration and composition of consolidated banking links At end-2018 Graph A

Volume and count by counterparty country region CBS foreign claims, count and volume2, 3 Number of links USD trn Number of links USD trn

1 BIS locational banking statistics (LBS). Claims below $0.5 million are excluded from calculations. 2 BIS consolidated banking statistics (CBS). Claims below $0.5 million are excluded from calculations. 3 By size bucket of bilateral foreign claims.

Sources: BIS consolidated banking statistics on an immediate counterparty basis; BIS locational banking statistics; authors’ calculations.

3,200

2,400

1,600

800

0

10.0

7.5

5.0

2.5

0.0OffshoreEMEsOther AEsEuro area

LBS cross-border claims1

CBS foreign claims2

Count (lhs):LBS cross-border claims1

CBS international claims2

CBS local claims inlocal currency2

Volume (rhs):

1,600

1,200

800

400

0

16

12

8

4

0

bnbnbnbn–1bnmn>5020–505–201–5100mn<100

Count (lhs) Volume (rhs)

BIS Quarterly Review, June 2019 5

Turning to the creditor country perspective, the concentration around advanced economies is even more pronounced. Across all size groups, advanced economies provide at least 50% of cross-border credit, and more than 80% within the largest size group. Close to 70% of the volume of the largest-sized links, and 55% of total global cross-border credit, is explained by creditors in only five major advanced economies: France, Germany, Japan, the United Kingdom and the United States.

Concentration and the fall in cross-border interbank credit

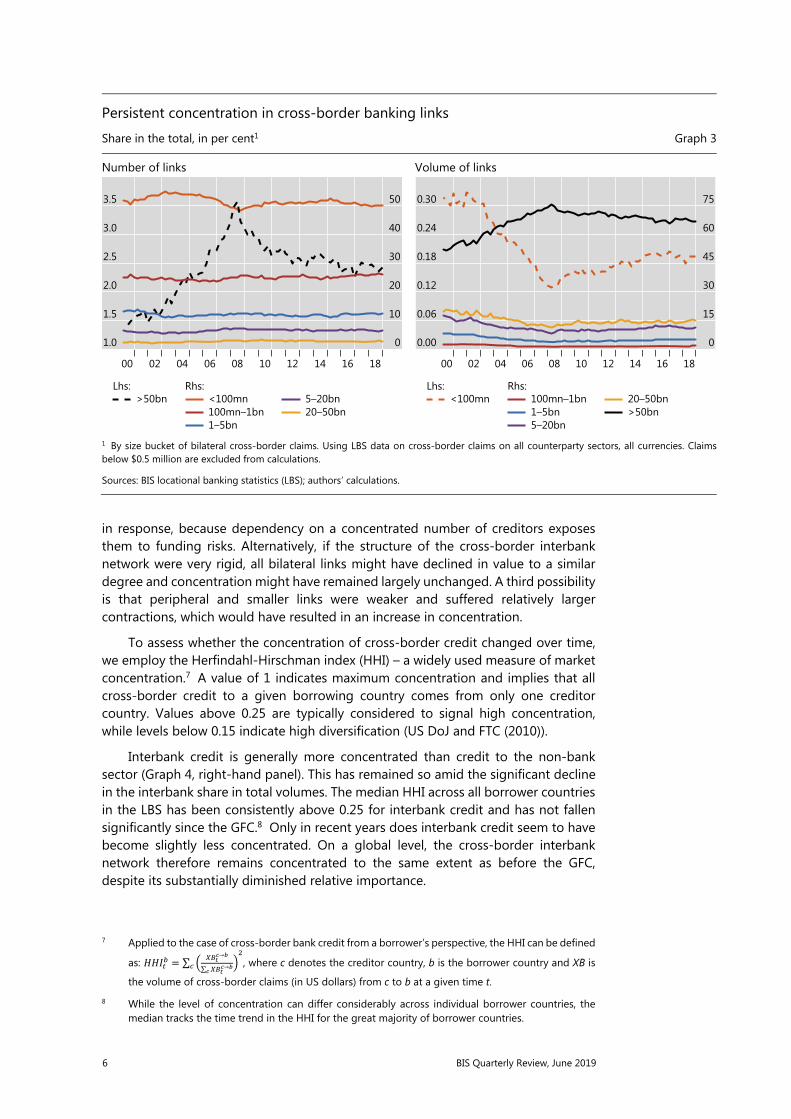

The distribution of links across the different size buckets has been very stable over time. This suggests that concentration is a structural feature of the cross-border banking network. The increase in the share of very large links (Graph 3, left-hand panel, dashed line) in the years before the GFC exacerbated the already high concentration (right-hand panel, black line). The share in total cross-border bank credit volumes of the largest links rose from around 50% to 75% in the six years up to 2008. It has declined only gradually since, to 67% at end-2018.

The structural nature of concentration is underscored by how concentration in interbank links responded to the significant fall in cross-border interbank credit in the aftermath of the GFC. While global cross-border bank credit to the non-bank sector has continued to grow since the GFC, cross-border interbank credit has been falling (Graph 4, left-hand panel). This has resulted in a significant and persistent reduction in the share of interbank credit, from around 65% at end-2008 to 53% at end-2018 (red line).

The rapid initial decline in interbank cross-border credit, and the fall in its share, could conceivably have affected concentration in several possible ways. One possibility is that interbank borrowers could have tried to diversify their creditor base

Concentration by recipient and lender country region

At end-2018, in per cent1 Graph 2

By region of borrowing country By region of creditor country

1 By size bucket of bilateral cross-border claims. Using LBS data on bilateral cross-border claims on all counterparty sectors, all currencies. Claims below $0.5 million are excluded from calculations. Regional composition is different between the two panels since only a limited number of countries within a region report LBS.

Sources: BIS locational banking statistics (LBS); authors’ calculations.

100

80

60

40

20

0

bnbnbnbn–1bnmn>5020–505–201–5100mn<100

Euro area Other AEs EMEs

100

80

60

40

20

0

bnbnbnbn–1bnmn>5020–505–201–5100mn<100

Offshore Big 5: DE, FR, GB, JP and US

6 BIS Quarterly Review, June 2019

in response, because dependency on a concentrated number of creditors exposes them to funding risks. Alternatively, if the structure of the cross-border interbank network were very rigid, all bilateral links might have declined in value to a similar degree and concentration might have remained largely unchanged. A third possibility is that peripheral and smaller links were weaker and suffered relatively larger contractions, which would have resulted in an increase in concentration.

To assess whether the concentration of cross-border credit changed over time, we employ the Herfindahl-Hirschman index (HHI) – a widely used measure of market concentration.7 A value of 1 indicates maximum concentration and implies that all cross-border credit to a given borrowing country comes from only one creditor country. Values above 0.25 are typically considered to signal high concentration, while levels below 0.15 indicate high diversification (US DoJ and FTC (2010)).

Interbank credit is generally more concentrated than credit to the non-bank sector (Graph 4, right-hand panel). This has remained so amid the significant decline in the interbank share in total volumes. The median HHI across all borrower countries in the LBS has been consistently above 0.25 for interbank credit and has not fallen significantly since the GFC.8 Only in recent years does interbank credit seem to have become slightly less concentrated. On a global level, the cross-border interbank network therefore remains concentrated to the same extent as before the GFC, despite its substantially diminished relative importance.

7 Applied to the case of cross-border bank credit from a borrower’s perspective, the HHI can be defined

as: = ∑ →∑ → , where c denotes the creditor country, b is the borrower country and XB is

the volume of cross-border claims (in US dollars) from c to b at a given time t.

8 While the level of concentration can differ considerably across individual borrower countries, the median tracks the time trend in the HHI for the great majority of borrower countries.

Persistent concentration in cross-border banking links

Share in the total, in per cent1 Graph 3

Number of links Volume of links

1 By size bucket of bilateral cross-border claims. Using LBS data on cross-border claims on all counterparty sectors, all currencies. Claims below $0.5 million are excluded from calculations.

Sources: BIS locational banking statistics (LBS); authors’ calculations.

3.5

3.0

2.5

2.0

1.5

1.0

50

40

30

20

10

0

18161412100806040200

>50bnLhs:

<100mn100mn–1bn1–5bn

Rhs:5–20bn20–50bn

0.30

0.24

0.18

0.12

0.06

0.00

75

60

45

30

15

0

18161412100806040200

<100mnLhs:

100mn–1bn1–5bn5–20bn

Rhs:20–50bn>50bn

BIS Quarterly Review, June 2019 7

The drop in the interbank share was to a significant extent driven by the well documented contraction in credit extended by European banks following the GFC and the euro area crisis (McCauley et al (2017)). Interbank lending to euro area countries and other advanced economies was particularly affected. Hence, concentration in interbank credit may have responded differently across recipient country regions.

Despite the sharp drop in cross-border interbank credit to euro area countries, concentration in the euro area did not abate but intensified (Graph 5, first panel). This can be explained by the relative stability of interbank links to major euro area countries, which tend to be of large size, while interbank credit to periphery countries recorded strong declines.

Other advanced economies and recipients in offshore centres did see a decline in the concentration of cross-border interbank credit (Graph 5). However, this did not occur in the immediate aftermath of the GFC. The decrease in the concentration of interbank credit for advanced economy borrowers outside of the euro area occurred in more recent years (second panel), and is largely explained by the contraction in the volume of large links coming from offshore centres. Concentration for borrowers in offshore centres (fourth panel) dropped substantially from the peak in 2010, but has not abated further with the continued decline in the interbank share. For borrowers in EMEs, interbank shares have increased slightly since the GFC, mainly driven by China. Concentration in interbank credit is much higher for EME borrowers than for borrowers in advanced economies, but shows no clear trend (third panel).

Interbank claims have been declining while their concentration has remained high1 Graph 4

Cross-border claims by counterparty sector HHI by counterparty sector3 Per cent USD trn HHI

1 Using LBS data on bilateral cross-border claims in all currencies. Claims below $0.5 million are excluded from calculations. Reporting of LBSstatistics improves over time; from end-December 2015, this includes China and Russia as reporting countries. 2 Interbank share is calculated as the ratio of claims on the bank sector over claims on all counterparty sectors. 3 Median value of Herfindahl-Hirschman index (HHI) across the counterparty countries within a sector. HHI is calculated as the sum of squared market shares, where market share is the share of claims held by a creditor in total claims on a counterparty country.

Sources: BIS locational banking statistics (LBS); authors’ calculations.

65

60

55

50

30

20

10

018161412100806040200

Interbank share2Lhs:

BankRhs:

Non-bank

0.35

0.30

0.25

0.20181614121008060402

Bank

Non-bank

8 BIS Quarterly Review, June 2019

Interbank concentration remains high despite the decline in interbank credit1 Graph 5

Euro area Other AEs EMEs Offshore centres Per cent HHI Per cent HHI Per cent HHI Per cent HHI

1 Using LBS data on bilateral cross-border claims on the bank sector in all currencies. Claims below $0.5 million are excluded fromcalculations. 2 Interbank share is calculated as the ratio of claims on the bank sector over claims on all counterparty sectors. 3 Median value of the Herfindahl-Hirschman index (HHI) across the counterparty countries within a region. HHI is calculated as the sum of squaredmarket shares, where market share is the share of claims held by a creditor in total claims on a counterparty country.

Sources: BIS locational banking statistics (LBS); authors’ calculations.

Conclusions

Cross-border interbank links are highly concentrated. A small number of very large country-level links (>$50 billion), mostly between advanced economies, dominate cross-border bank credit. Just five major creditor countries – France, Germany, Japan, the United Kingdom and the United States – account for 55% of global cross-border credit and close to 70% of the volume of the largest bilateral links. The share of the largest links increased in the run-up to the GFC and has declined only slightly since.

Concentration in cross-border credit is of a structural nature. This is corroborated by the high concentration in interbank links, which persisted amid the significant decline of cross-border interbank credit after the GFC. From a research perspective, a relevant implication of the structurally high concentration in cross-border banking links is that empirical analyses that give equal weight to all observations are likely to yield unreliable results for a number of important questions (Amiti et al (2017)). From a policy perspective, the persistently high concentration in links implies that cross-border banking remains a potentially important channel for transmitting financial shocks.

70

60

50

40

0.4

0.3

0.2

0.118130803

70

60

50

40

0.4

0.3

0.2

0.118130803

Interbank share2Lhs:

70

60

50

40

0.4

0.3

0.2

0.118130803

HHI3Rhs:

70

60

50

40

0.4

0.3

0.2

0.118130803

BIS Quarterly Review, June 2019 9

Box B

The importance of small cross-border banking links for emerging market economies

While small links – smaller than $100 million in size – account for a minor share of the total volume of cross-border credit, they account for a significant share of credit to borrowers in many emerging market economies (EMEs). For example, cross-border credit to borrowers in Gambia and Sierra Leone is entirely through small links (Graph B1). But small links are not equally important for all EMEs. For the largest, such as Brazil and China, small links are negligible.

Small links matter for small EME recipient countries1

At end-2018, percentage of GDP Graph B1

1 Using LBS data on cross-border claims on all counterparty sectors, all currencies. Claims below $0.5 million are excluded from calculations.

Sources: IMF, World Economic Outlook; BIS locational banking statistics (LBS); authors’ calculations.

Small cross-border banking links and the fall in interbank links1

By counterparty country region Graph B2

Emerging Asia Central and eastern Europe Latin America Middle East and Africa Average count USD bn Average count USD bn Average count USD bn Average count USD bn

1 Using data on bilateral cross-border claims on all counterparty sectors, in all currencies, where claims are below $100 million and above$0.5 million. For a list of countries in each region, see Table A3 on the BIS website (https://stats.bis.org/statx/srs/table/a3). 2 Average count of links is calculated as the ratio of total bilateral links with volume below $100 million to the number of creditors reporting links of any size.

Sources: BIS locational banking statistics; authors’ calculations.

12

10

8

6

4

2

0

Gam

bia Si

erra L

eone

Micr

onesia

Centra

l Afr.

Rep.

Leso

tho G

renad

a Bh

utan

Moldova H

aiti

Burki

na Fa

so Bo

tswan

a Be

nin

Turkm

enist

an Tu

nisia

Parag

uay

Niger

Boliv

ia Ta

nzan

ia G

uatem

ala Ka

zakh

stan

Bosn

ia an

d Herz

. M

orocc

o Ko

rea Br

azil

China

Small links (<$100mn) Other links (≥$100mn)

12

10

8

6

4

16

12

8

4

01814100602

6

5

4

3

2

8

6

4

2

018130803

BanksNon-banks

Count2 (lhs):

10

8

6

4

2

12

9

6

3

01814100602

BanksNon-banks

Volume (rhs):

18

15

12

9

6

20

15

10

5

01814100602

10 BIS Quarterly Review, June 2019

The volume of lending to EMEs associated with small cross-border relationships has increased steadily over the past two decades. This trend is evident for lending to both the non-bank and the bank sector (Graph B2). However, volumes disguise a fall in the average number of small bilateral links between banks and borrowers in EMEs. The only exception is non-bank borrowing in emerging Asia, which saw an increase in the average number of country-to-country links. Since 2014, the average number of interbank bilateral links has been declining for many EMEs, particularly in the Middle East and Africa and in emerging Asia. The decline in correspondent banking relationships in recent years may have contributed to the fall in the number of small bilateral links (CPMI (2019)).

BIS Quarterly Review, June 2019 A1

Annexes

BIS Statistics: Charts

The statistics published by the BIS are a unique source of information about the structure of and activity in the global financial system. BIS statistics are presented in graphical form in this annex and in tabular form in the BIS Statistical Bulletin, which is published concurrently with the BIS Quarterly Review. For introductions to the BIS statistics and a glossary of terms used in this annex, see the BIS Statistical Bulletin.

The data shown in the charts in this annex can be downloaded from the BIS Quarterly Review page on the BIS website (www.bis.org/publ/quarterly.htm). Data may have been revised or updated subsequent to the publication of this annex. For the latest data and to download additional data, see the statistics pages on the BIS website (www.bis.org/statistics/index.htm). A release calendar provides advance notice of publication dates (www.bis.org/statistics/relcal.htm).

A Locational banking statistics

A.1 Cross-border claims, by sector, currency and instrument ........................................ A4

A.2 Cross-border claims, by borrowing region..................................................................... A5

A.3 Cross-border claims, by borrowing country .................................................................. A6

A.4 Cross-border claims, by nationality of reporting bank and currency of denomination ............................................................................................................................. A7

A.5 Cross-border liabilities of reporting banks..................................................................... A8

B Consolidated banking statistics

B.1 Consolidated claims of reporting banks on advanced economies ....................... A9

B.2 Consolidated claims of reporting banks on emerging market economies ..... A10

C Debt securities statistics

C.1 Global debt securities markets .......................................................................................... A11

C.2 Total debt securities, by sector of issuer ....................................................................... A11

C.3 Net issuance of international debt securities .............................................................. A12

C.4 International debt securities issued by financial and non-financial corporations .............................................................................................................................. A12

D Derivatives statistics

D.1 Exchange-traded derivatives .............................................................................................. A13

A2 BIS Quarterly Review, June 2019

D.2 Global OTC derivatives markets ....................................................................................... A14

D.3 OTC foreign exchange derivatives ................................................................................... A14

D.4 OTC interest rate derivatives .............................................................................................. A15

D.5 OTC equity-linked derivatives ........................................................................................... A15

D.6 OTC commodity derivatives ............................................................................................... A16

D.7 Credit default swaps .............................................................................................................. A16

D.8 Concentration in global OTC derivatives markets ..................................................... A17

D.9 Growth of central clearing .................................................................................................. A17

E Global liquidity indicators

E.1 Growth of international bank credit................................................................................ A18

E.2 Global bank credit to the private non-financial sector, by residence of borrower .................................................................................................................................... A19

E.3 Global credit to the non-financial sector, by currency ............................................ A20

E.4 US dollar-denominated credit to non-banks outside the United States ......... A21

E.5 Foreign currency credit to non-banks in EMDEs ...................................................... A21

F Statistics on total credit to the non-financial sector

F.1 Total credit to the non-financial sector (core debt) ................................................. A22

F.2 Total credit to the private non-financial sector (core debt) ................................. A23

F.3 Bank credit to the private non-financial sector (core debt) .................................. A24

F.4 Total credit to households (core debt) .......................................................................... A25

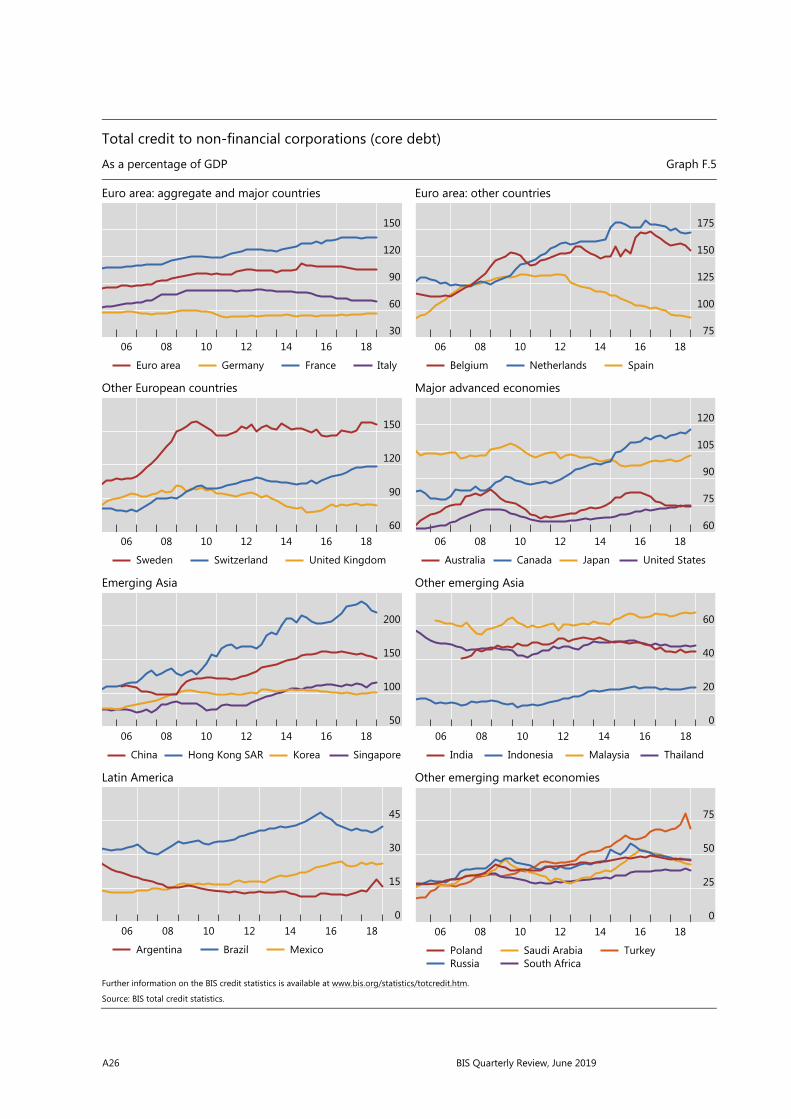

F.5 Total credit to non-financial corporations (core debt) ............................................ A26

F.6 Total credit to the government sector at market value (core debt) .................. A27

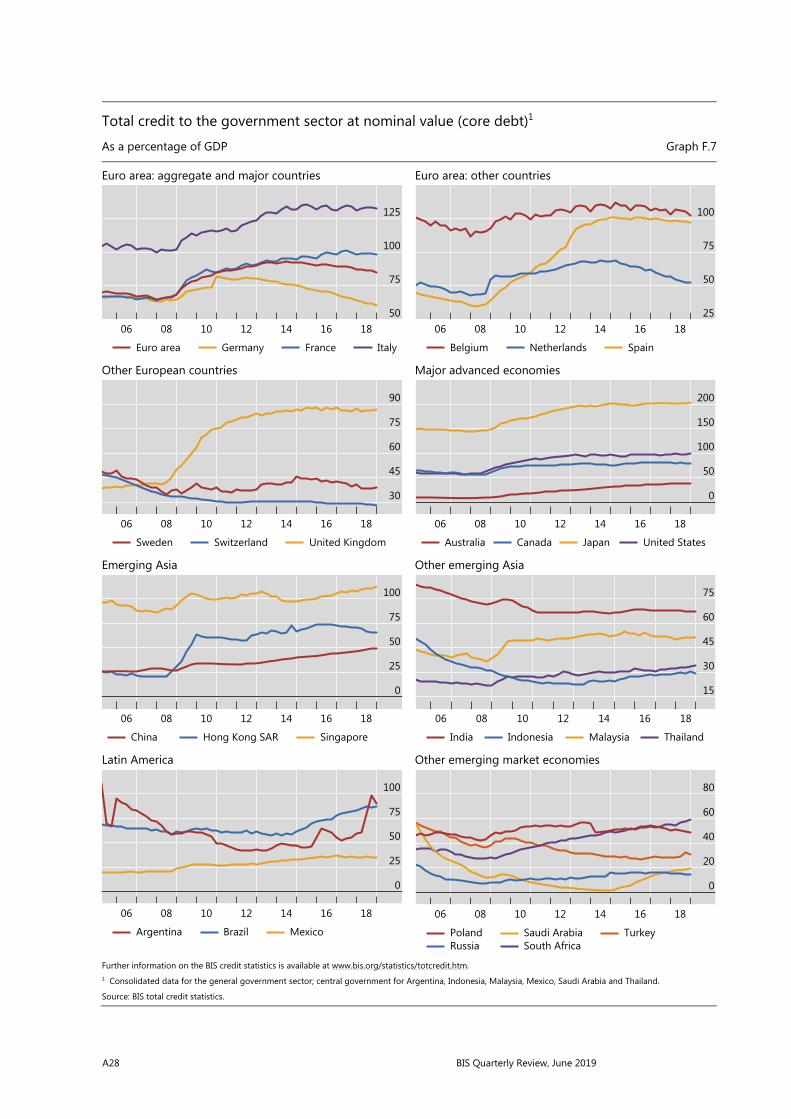

F.7 Total credit to the government sector at nominal value (core debt) ................ A28

G Debt service ratios for the private non-financial sector

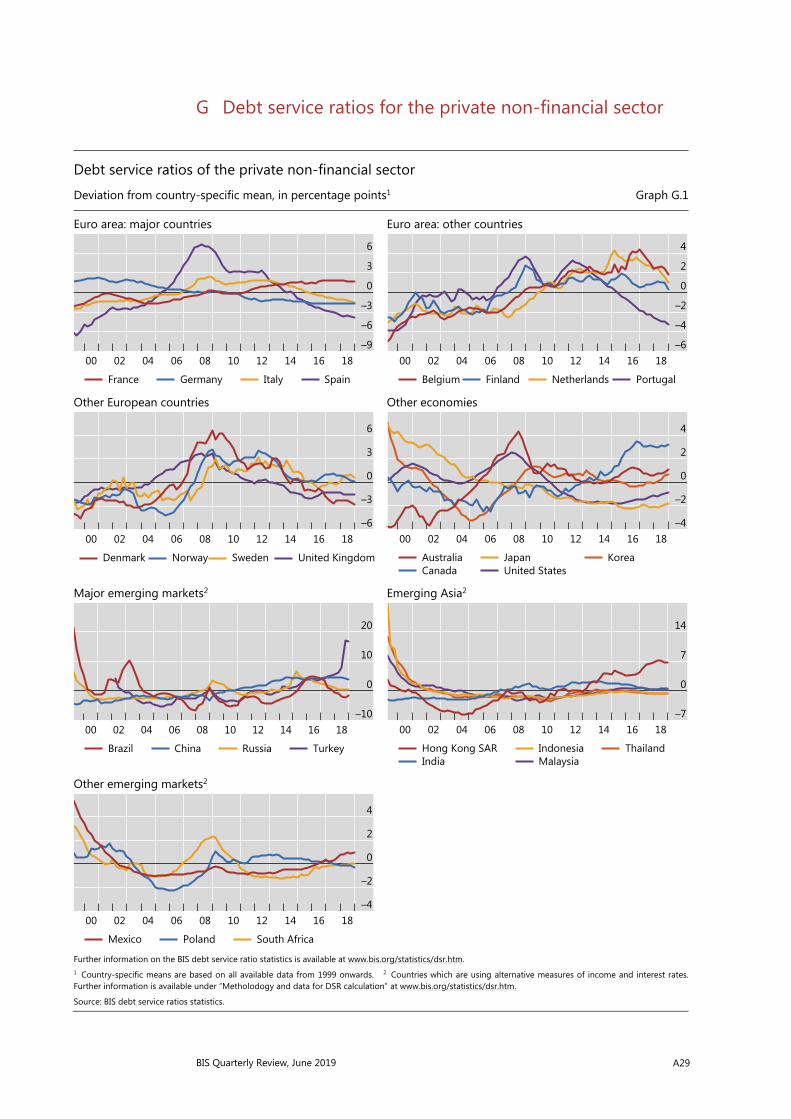

G.1 Debt service ratios of the private non-financial sector ........................................... A29

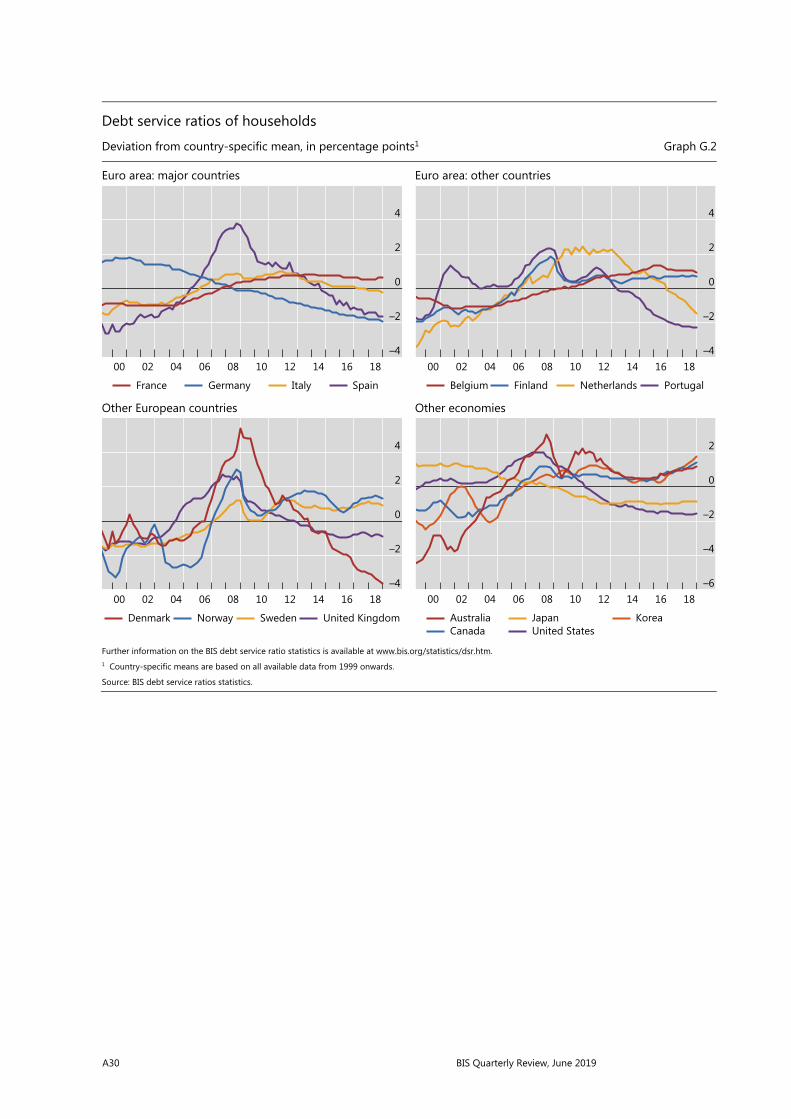

G.2 Debt service ratios of households ................................................................................... A30

G.3 Debt service ratios of non-financial corporations ..................................................... A31

BIS Quarterly Review, June 2019 A3

H Property price statistics

H.1 Real residential property prices ........................................................................................ A32

I Effective and US dollar exchange rate statistics

I.1 Real effective exchange rates ............................................................................................ A33

I.2 US dollar exchange rates ..................................................................................................... A34

J Credit-to-GDP gaps

J.1 Credit-to-GDP gaps ............................................................................................................... A35

K Consumer price indices

K.1 Consumer prices ..................................................................................................................... A36

L Central bank policy rates

L.1 Central bank policy or representative rates ................................................................. A37

A4 BIS Quarterly Review, June 2019

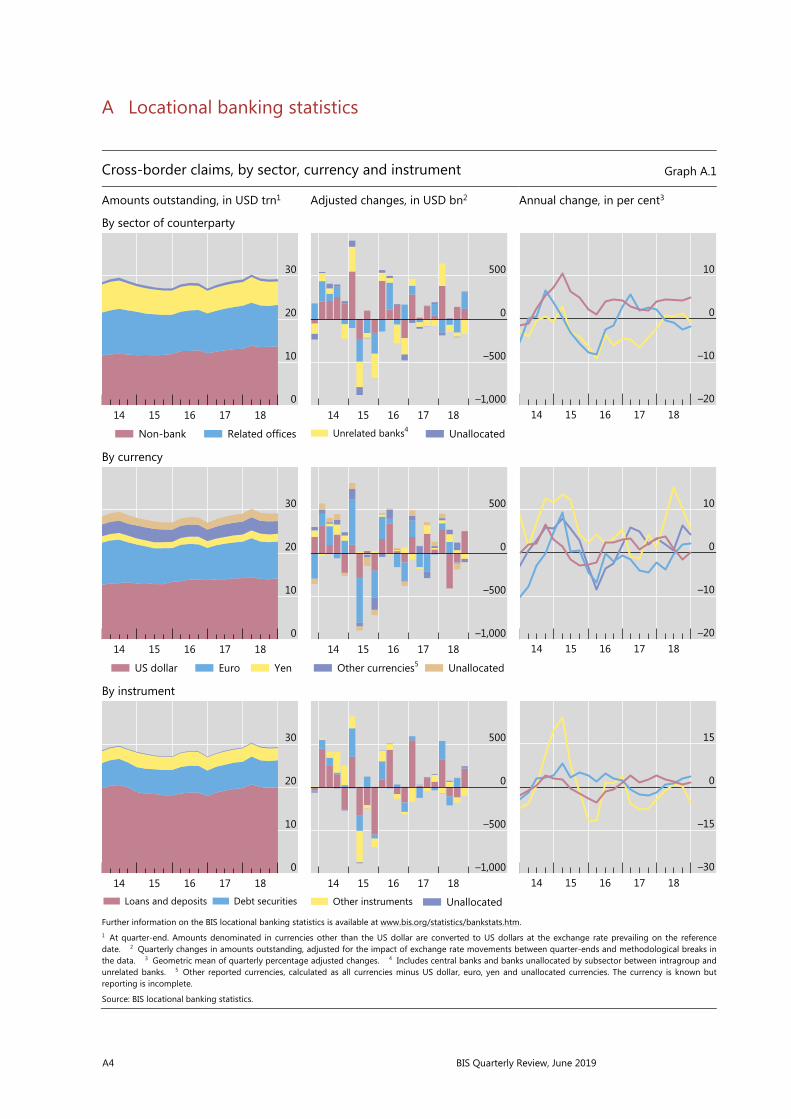

A Locational banking statistics

Cross-border claims, by sector, currency and instrument Graph A.1

Amounts outstanding, in USD trn1 Adjusted changes, in USD bn2 Annual change, in per cent3

By sector of counterparty

By currency

By instrument

Further information on the BIS locational banking statistics is available at www.bis.org/statistics/bankstats.htm. 1 At quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Quarterly changes in amounts outstanding, adjusted for the impact of exchange rate movements between quarter-ends and methodological breaks in the data. 3 Geometric mean of quarterly percentage adjusted changes. 4 Includes central banks and banks unallocated by subsector between intragroup and unrelated banks. 5 Other reported currencies, calculated as all currencies minus US dollar, euro, yen and unallocated currencies. The currency is known but reporting is incomplete.

Source: BIS locational banking statistics.

30

20

10

01817161514

Non-bank Related offices

500

0

–500

–1,0001817161514

Unrelated banks4 Unallocated

10

0

–10

–201817161514

30

20

10

01817161514

US dollar Euro Yen

500

0

–500

–1,0001817161514

Other currencies5 Unallocated

10

0

–10

–201817161514

30

20

10

01817161514

Loans and deposits Debt securities

500

0

–500

–1,0001817161514

Other instruments Unallocated

15

0

–15

–301817161514

BIS Quarterly Review, June 2019 A5

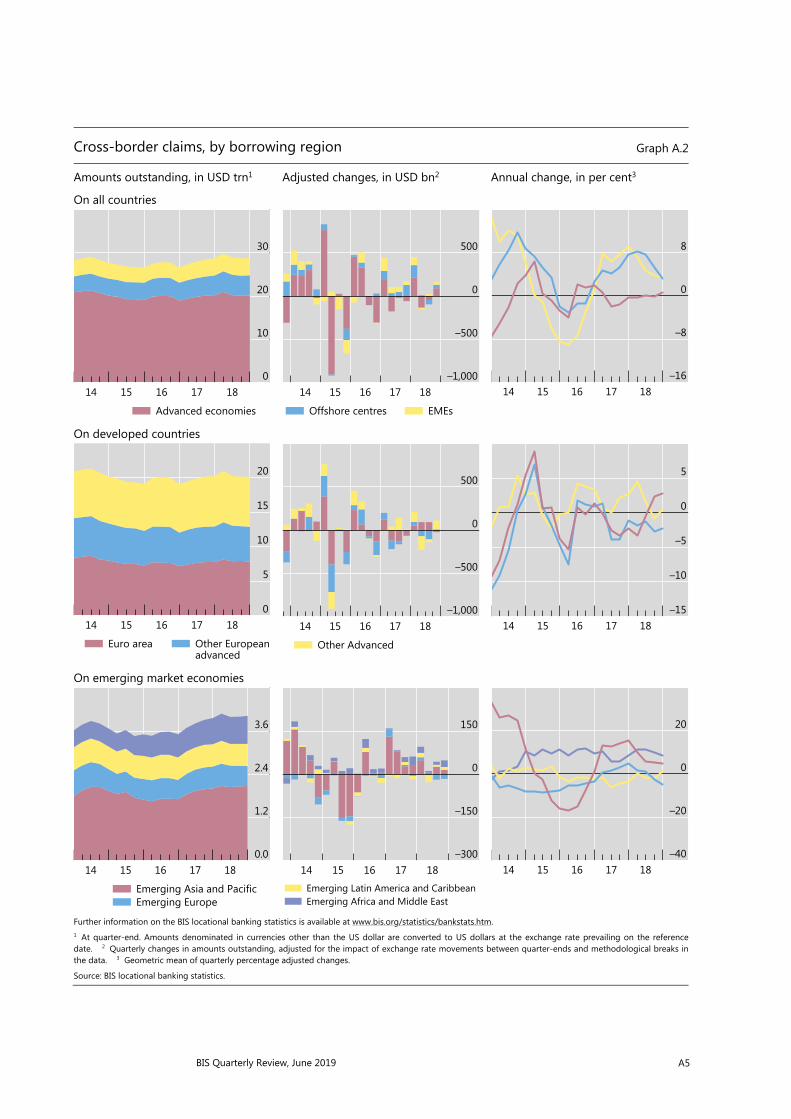

Cross-border claims, by borrowing region Graph A.2

Amounts outstanding, in USD trn1 Adjusted changes, in USD bn2 Annual change, in per cent3

On all countries

On developed countries

On emerging market economies

Further information on the BIS locational banking statistics is available at www.bis.org/statistics/bankstats.htm. 1 At quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Quarterly changes in amounts outstanding, adjusted for the impact of exchange rate movements between quarter-ends and methodological breaks in the data. 3 Geometric mean of quarterly percentage adjusted changes.

Source: BIS locational banking statistics.

30

20

10

01817161514

Advanced economies

500

0

–500

–1,0001817161514

Offshore centres EMEs

8

0

–8

–161817161514

20

15

10

5

01817161514

Euro areaadvancedOther European

500

0

–500

–1,0001817161514

Other Advanced

5

0

–5

–10

–151817161514

3.6

2.4

1.2

0.01817161514

Emerging Asia and PacificEmerging Europe

150

0

–150

–3001817161514

Emerging Latin America and CaribbeanEmerging Africa and Middle East

20

0

–20

–401817161514

A6 BIS Quarterly Review, June 2019

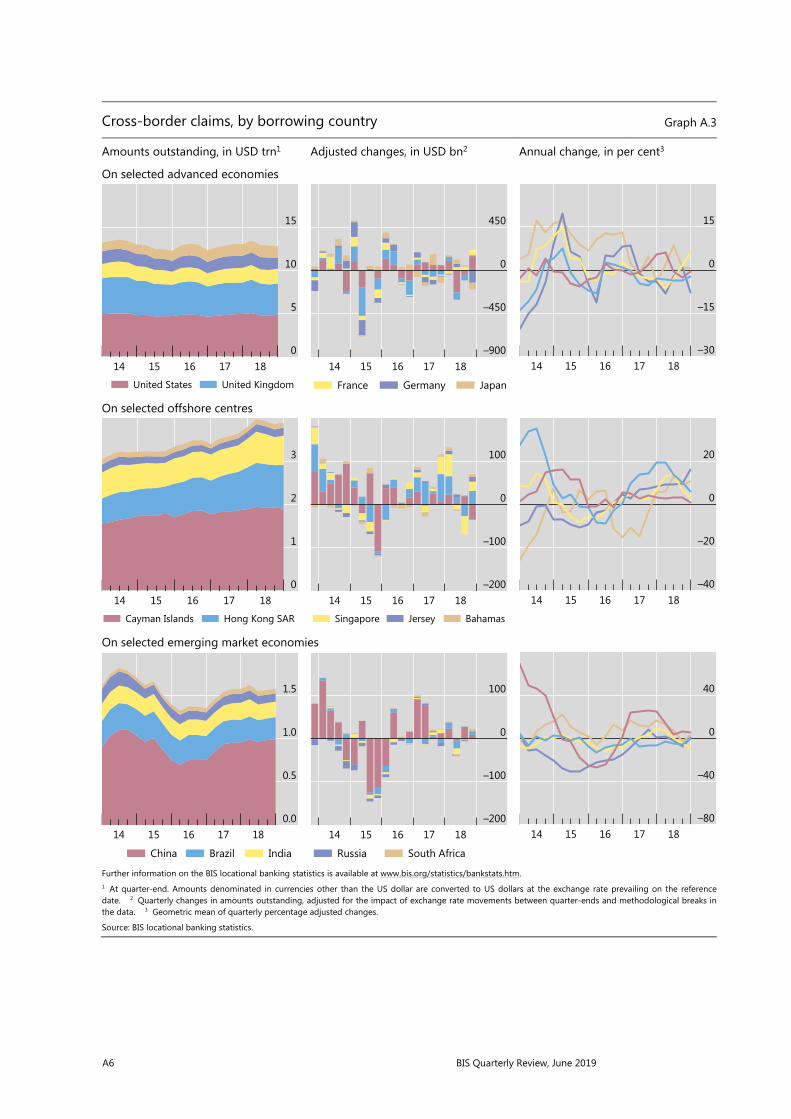

Cross-border claims, by borrowing country Graph A.3

Amounts outstanding, in USD trn1 Adjusted changes, in USD bn2 Annual change, in per cent3

On selected advanced economies

On selected offshore centres

On selected emerging market economies

Further information on the BIS locational banking statistics is available at www.bis.org/statistics/bankstats.htm. 1 At quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Quarterly changes in amounts outstanding, adjusted for the impact of exchange rate movements between quarter-ends and methodological breaks in the data. 3 Geometric mean of quarterly percentage adjusted changes.

Source: BIS locational banking statistics.

15

10

5

01817161514

United States United Kingdom

450

0

–450

–9001817161514

France Germany Japan

15

0

–15

–301817161514

3

2

1

01817161514

Cayman Islands Hong Kong SAR

100

0

–100

–2001817161514

Singapore Jersey Bahamas

20

0

–20

–401817161514

1.5

1.0

0.5

0.01817161514

China Brazil India

100

0

–100

–2001817161514

Russia South Africa

40

0

–40

–801817161514

BIS Quarterly Review, June 2019 A7

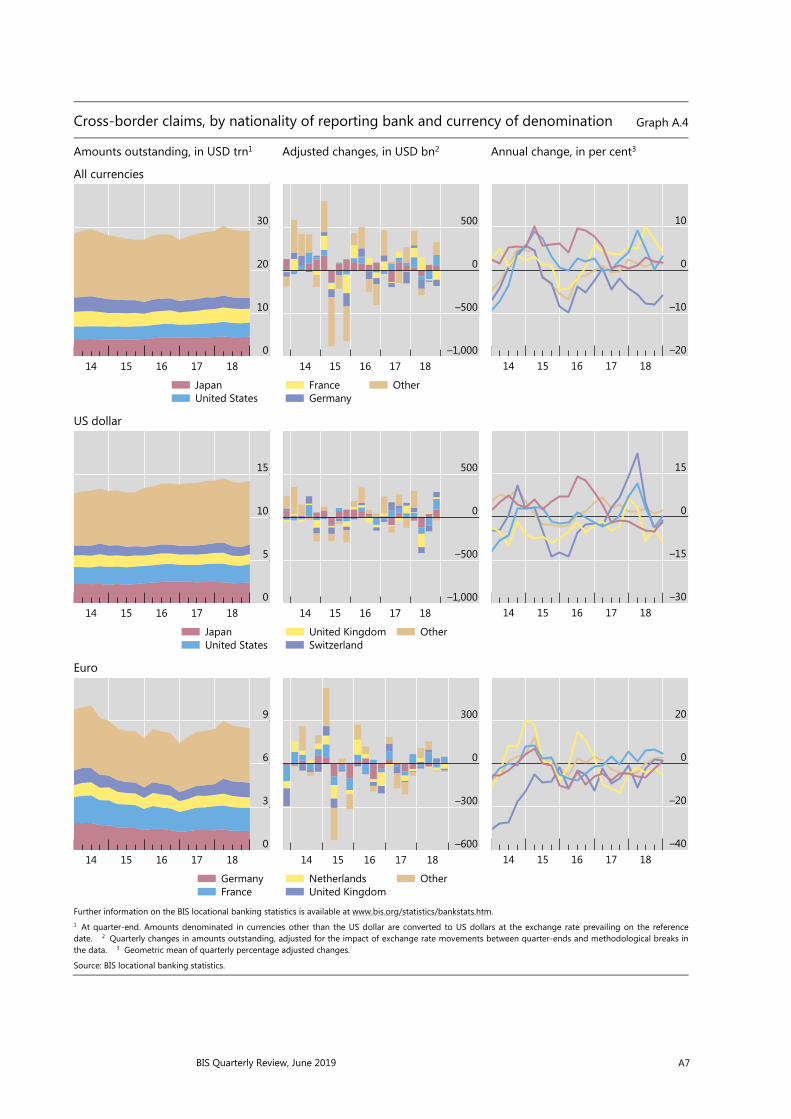

Cross-border claims, by nationality of reporting bank and currency of denomination Graph A.4

Amounts outstanding, in USD trn1 Adjusted changes, in USD bn2 Annual change, in per cent3

All currencies

US dollar

Euro

Further information on the BIS locational banking statistics is available at www.bis.org/statistics/bankstats.htm. 1 At quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Quarterly changes in amounts outstanding, adjusted for the impact of exchange rate movements between quarter-ends and methodological breaks in the data. 3 Geometric mean of quarterly percentage adjusted changes.

Source: BIS locational banking statistics.

30

20

10

01817161514

JapanUnited States

500

0

–500

–1,0001817161514

FranceGermany

Other

10

0

–10

–201817161514

15

10

5

01817161514

JapanUnited States

500

0

–500

–1,0001817161514

United KingdomSwitzerland

Other

15

0

–15

–301817161514

9

6

3

01817161514

GermanyFrance

300

0

–300

–6001817161514

NetherlandsUnited Kingdom

Other

20

0

–20

–401817161514

A8 BIS Quarterly Review, June 2019

Cross-border liabilities of reporting banks Graph A.5

Amounts outstanding, in USD trn1 Adjusted changes, in USD bn2 Annual change, in per cent3

To emerging market economies

To central banks

By currency type and location

Further information on the BIS locational banking statistics is available at www.bis.org/statistics/bankstats.htm. 1 At quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Quarterly changes in amounts outstanding, adjusted for the impact of exchange rate movements between quarter-ends and methodological breaks in the data. 3 Geometric mean of quarterly percentage adjusted changes.

Source: BIS locational banking statistics.

3

2

1

01817161514

Emerging Asia and PacificEmerging Europe

100

0

–100

–2001817161514

Emerging Latin America and CaribbeanEmerging Africa and Middle East

15

0

–15

–301817161514

1.2

0.8

0.4

0.01817161514

US dollar Euro Yen

50

0

–50

–1001817161514

Other currencies Unallocated

50

0

–50

–1001817161514

30

20

10

01817161514

Cross-border in all currenciesResident in foreign currencies

600

0

–600

–1,2001817161514

Unallocated

5

0

–5

–101817161514

BIS Quarterly Review, June 2019 A9

B Consolidated banking statistics

Consolidated claims of reporting banks on advanced economies Graph B.1

Foreign claims and local positions, in USD bn1, 2

Foreign claims of selected creditors,in USD bn1, 3

International claims, by sector and maturity, in per cent4

On the euro area

On the United States

On Japan

Further information on the BIS consolidated banking statistics is available at www.bis.org/statistics/bankstats.htm. 1 Amounts outstanding at quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Excludes domestic claims, ie claims on residents of a bank’s home country. 3 Foreign claims on an ultimate risk basis, by nationality of reporting bank. The banking systems shown are not necessarily the largest foreign bank creditors on each reference date. 4 As a percentage of international claims outstanding. 5 On an immediate counterparty basis. Includes the unconsolidated claims of banks headquartered outside but located inside CBS-reporting countries. 6 On an ultimate risk basis.

Source: BIS consolidated banking statistics (CBS).

7,500

5,000

2,500

01817161514

Foreign claims (immediate)5

Foreign claims (ultimate)6

Local claims in local currencyLocal liabilities in local currency

1,200

800

400

01817161514

FRUS

GBJP

ES

45

30

15

01817161514

BanksOfficial sectorNon-bank private sectorUp to and including 1 year

6,000

4,000

2,000

01817161514

1,500

1,000

500

01817161514

JPGB

CHFR

DE

60

40

20

01817161514

900

600

300

0

1817161514

450

300

150

0

1817161514

USFR

GBTW

AU

50

25

0

1817161514

A10 BIS Quarterly Review, June 2019

Consolidated claims of reporting banks on emerging market economies Graph B.2

Foreign claims and local positions, in USD bn1, 2

Foreign claims of selected creditors,in USD bn1, 3

International claims, by sector and maturity, in per cent4

On China

On Turkey

On Brazil

Further information on the BIS consolidated banking statistics is available at www.bis.org/statistics/bankstats.htm. 1 Amounts outstanding at quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Excludes domestic claims, ie claims on residents of a bank’s home country. 3 Foreign claims on an ultimate risk basis, by nationality of reporting bank. The banking systems shown are not necessarily the largest foreign bank creditors on each reference date. 4 As a percentage of international claims. 5 On an immediate counterparty basis. Includes the unconsolidated claims of banks headquartered outside but located inside CBS-reporting countries. 6 On an ultimate risk basis.

Source: BIS consolidated banking statistics (CBS).

1,200

800

400

0

1817161514

Foreign claims (immediate)5

Foreign claims (ultimate)6

Local claims in local currencyLocal liabilities in local currency

180

120

60

0

1817161514

GBUS

JPTW

FR

75

50

25

0

1817161514

BanksOfficial sectorNon-bank private sectorUp to and including 1 year

300

200

100

0

1817161514

75

50

25

0

1817161514

ESFR

GBUS

DE

60

40

20

0

1817161514

450

300

150

0

1817161514

180

120

60

0

1817161514

ESUS

GBJP

FR

60

40

20

0

1817161514

BIS Quarterly Review, June 2019 A11

C Debt securities statistics

Global debt securities markets1

Amounts outstanding, in trillions of US dollars2 Graph C.1

By market of issue By sector of issuer By currency of denomination3

DDS = domestic debt securities; IDS = international debt securities; TDS = total debt securities.

FC = financial corporations; GG = general government; HH = households and non-profit institutions serving households; IO = international organisations; NFC = non-financial corporations.

Further information on the BIS debt securities statistics is available at www.bis.org/statistics/secstats.htm. 1 Sample of countries varies across breakdowns shown. For countries that do not report TDS, data are estimated by the BIS as DDS plus IDS. For countries that do not report either TDS or DDS, data are estimated by the BIS as IDS. 2 At quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 3 Where a currency breakdown is not available, DDS are assumed to be denominated in thelocal currency.

Sources: Dealogic; Euroclear; Thomson Reuters; Xtrakter Ltd; national data; BIS debt securities statistics; BIS calculations.

Total debt securities, by residence and sector of issuer1

Amounts outstanding for the latest available data, in trillions of US dollars2 Graph C.2

Further information on the BIS debt securities statistics is available at www.bis.org/statistics/secstats.htm. 1 For countries that do not report TDS, data are estimated by the BIS as DDS plus IDS. 2 Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date.

Sources: National data; BIS debt securities statistics.

90

60

30

0

1817161514

TDSIDS

DDS

45

30

15

0

1817161514

GGFC

NFCIO

45

30

15

0

1817161514

USDEUR

JPYOTH

40

30

20

10

0

4

3

2

1

0IEKYAUKRESNLCAITDEFRGBJPCNUS

Lhs Rhs

General governmentFinancial corporations

Non-financial corporationsHouseholds and non-profit institutions serving households

A12 BIS Quarterly Review, June 2019

Net issuance of international debt securities

By issuer sector and currency of denomination, in billions of US dollars Graph C.3

US dollars Euro Pound Sterling

Further information is available at www.bis.org/statistics/secstats.htm.

Sources: Dealogic; Euroclear; Thomson Reuters; Xtrakter Ltd; BIS debt securities statistics.

International debt securities issued by financial and non-financial corporations1

Net issuance by region, in billions of US dollars2 Graph C.4

Developed countries Developing countries Offshore centres

Further information is available at www.bis.org/statistics/secstats.htm.

1 Excluding general government. 2 For a list of countries in each region, see Table C1 (http://stats.bis.org/statx/srs/table/c1).

Sources: Dealogic; Euroclear; Thomson Reuters; Xtrakter Ltd; BIS debt securities statistics.

225

150

75

0

–75201920182017201620152014

BanksOther financial institutions

75

0

–75

–150201920182017201620152014

Non-financial corporations

40

20

0

–20

–40201920182017201620152014

General governmentInternational organizations

200

100

0

–100201920182017201620152014

90

60

30

0

–30

–60201920182017201620152014

Nationals Residents

120

90

60

30

0

–30201920182017201620152014

BIS Quarterly Review, June 2019 A13

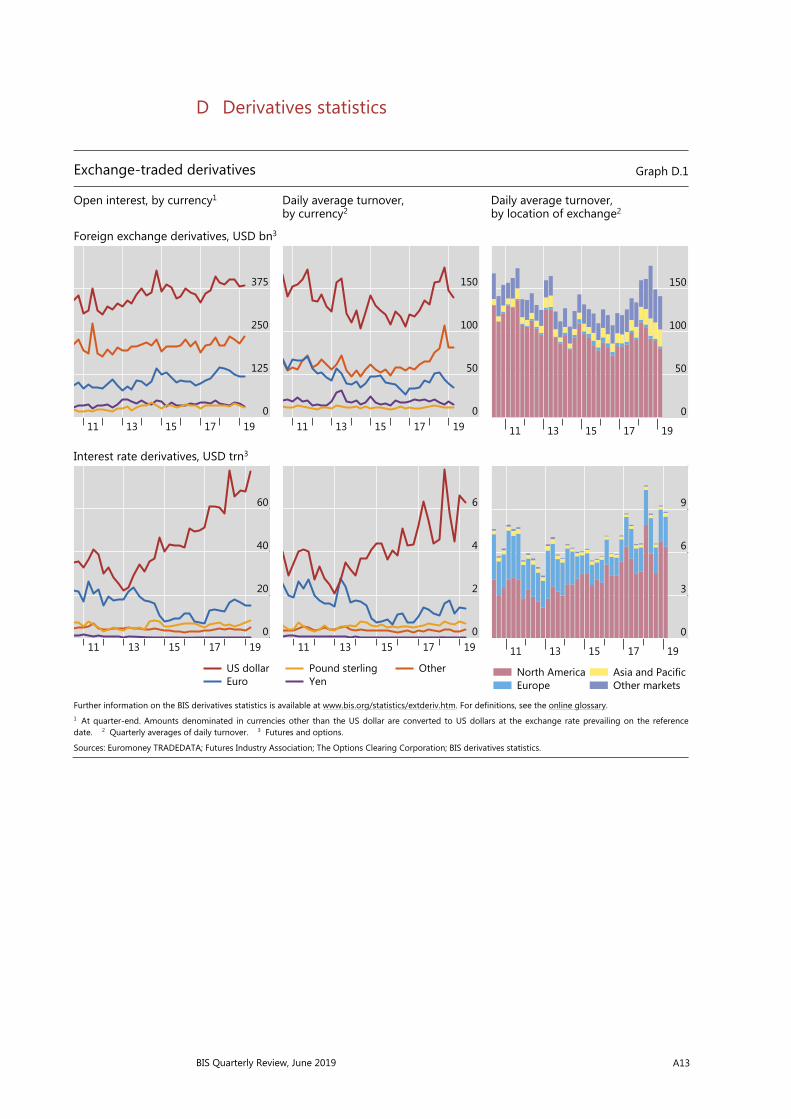

D Derivatives statistics

Exchange-traded derivatives Graph D.1

Open interest, by currency1 Daily average turnover, by currency2

Daily average turnover, by location of exchange2

Foreign exchange derivatives, USD bn3

Interest rate derivatives, USD trn3

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/extderiv.htm. For definitions, see the online glossary. 1 At quarter-end. Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date. 2 Quarterly averages of daily turnover. 3 Futures and options.

Sources: Euromoney TRADEDATA; Futures Industry Association; The Options Clearing Corporation; BIS derivatives statistics.

375

250

125

01917151311

150

100

50

01917151311

150

100

50

0

1917151311

60

40

20

01917151311

US dollarEuro

6

4

2

01917151311

Pound sterlingYen

Other

9

6

3

0

1917151311

North AmericaEurope

Asia and PacificOther markets

A14 BIS Quarterly Review, June 2019

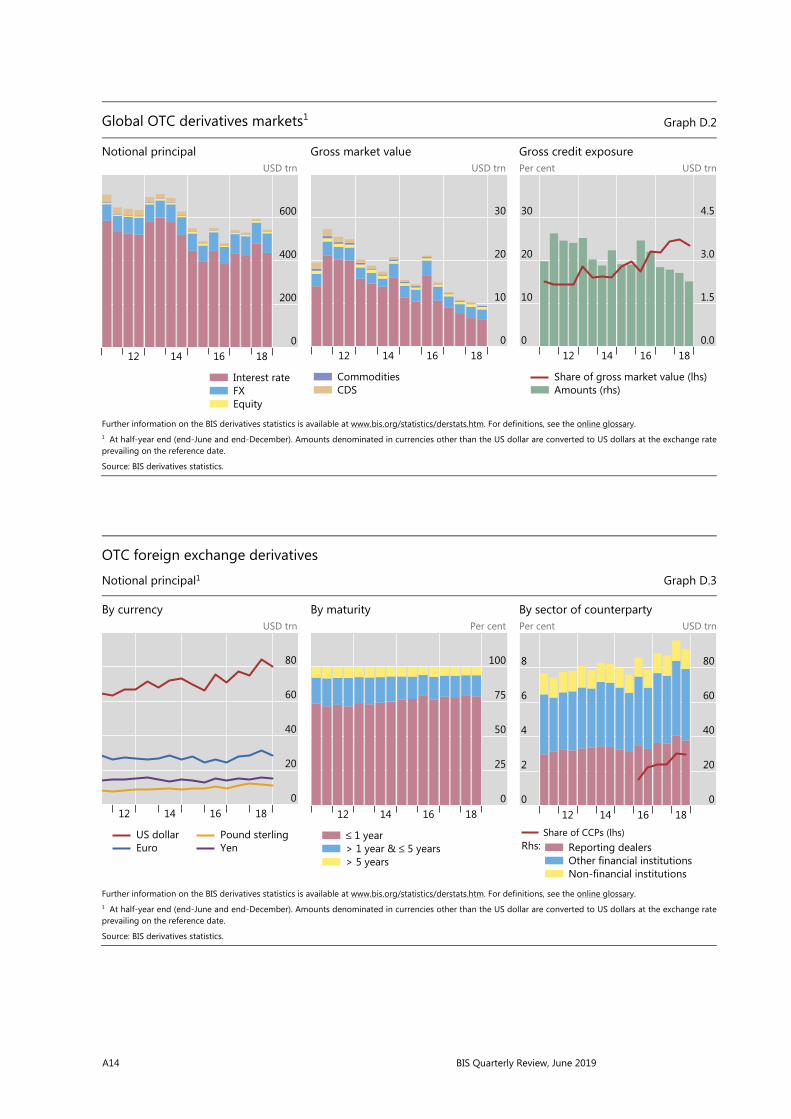

Global OTC derivatives markets1 Graph D.2

Notional principal Gross market value Gross credit exposure USD trn USD trn Per cent USD trn

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 At half-year end (end-June and end-December). Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rateprevailing on the reference date.

Source: BIS derivatives statistics.

OTC foreign exchange derivatives

Notional principal1 Graph D.3

By currency By maturity By sector of counterparty USD trn Per cent Per cent USD trn

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 At half-year end (end-June and end-December). Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date.

Source: BIS derivatives statistics.

600

400

200

018161412

Interest rateFXEquity

30

20

10

018161412

CommoditiesCDS

30

20

10

0

4.5

3.0

1.5

0.018161412

Share of gross market value (lhs)Amounts (rhs)

80

60

40

20

018161412

US dollarEuro

Pound sterlingYen

100

75

50

25

018161412

≤ 1 year> 1 year & ≤ 5 years> 5 years

8

6

4

2

0

80

60

40

20

018161412

Rhs:Share of CCPs (lhs)

Reporting dealersOther financial institutionsNon-financial institutions

BIS Quarterly Review, June 2019 A15

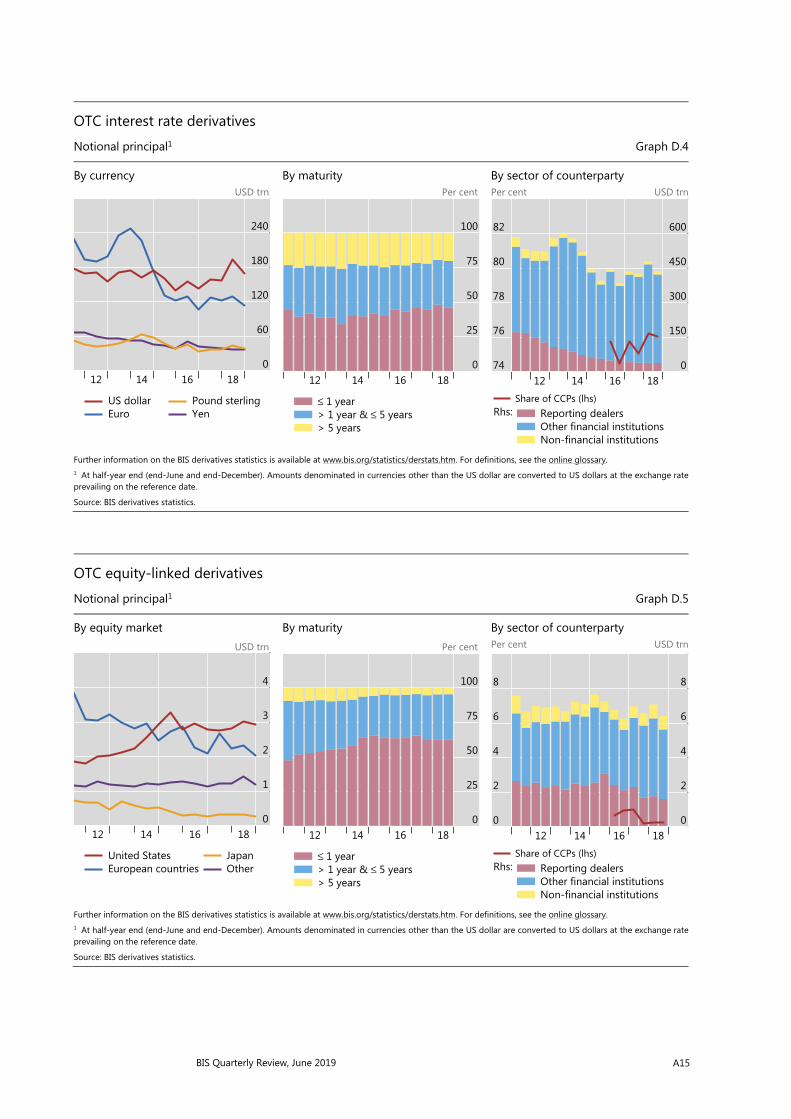

OTC interest rate derivatives

Notional principal1 Graph D.4

By currency By maturity By sector of counterparty USD trn Per cent Per cent USD trn

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 At half-year end (end-June and end-December). Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rateprevailing on the reference date.

Source: BIS derivatives statistics.

OTC equity-linked derivatives

Notional principal1 Graph D.5

By equity market By maturity By sector of counterparty USD trn Per cent Per cent USD trn

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 At half-year end (end-June and end-December). Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date.

Source: BIS derivatives statistics.

240

180

120

60

018161412

US dollarEuro

Pound sterlingYen

100

75

50

25

018161412

≤ 1 year> 1 year & ≤ 5 years> 5 years

82

80

78

76

74

600

450

300

150

018161412

Rhs:Share of CCPs (lhs)

Reporting dealersOther financial institutionsNon-financial institutions

4

3

2

1

018161412

United StatesEuropean countries

JapanOther

100

75

50

25

018161412

≤ 1 year> 1 year & ≤ 5 years> 5 years

8

6

4

2

0

8

6

4

2

018161412

Rhs:Share of CCPs (lhs)

Reporting dealersOther financial institutionsNon-financial institutions

A16 BIS Quarterly Review, June 2019

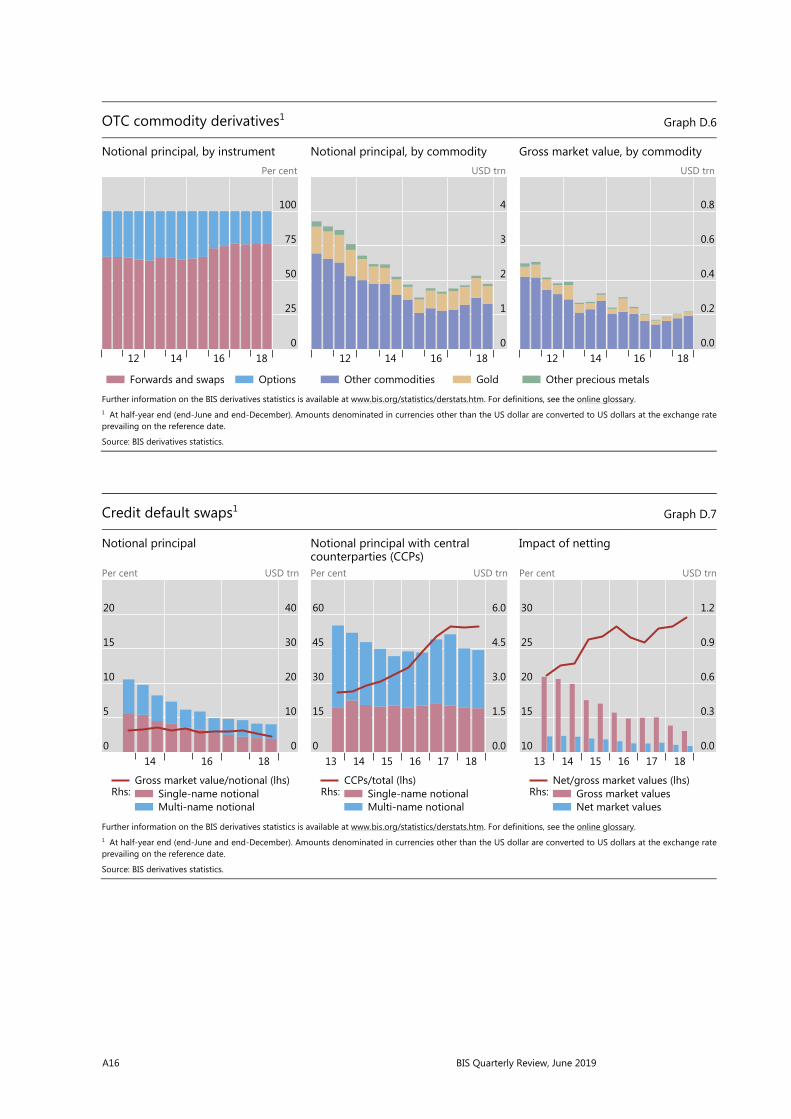

OTC commodity derivatives1 Graph D.6

Notional principal, by instrument Notional principal, by commodity Gross market value, by commodity Per cent USD trn USD trn

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 At half-year end (end-June and end-December). Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date.

Source: BIS derivatives statistics.

Credit default swaps1 Graph D.7

Notional principal Notional principal with central counterparties (CCPs)

Impact of netting

Per cent USD trn Per cent USD trn Per cent USD trn

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 At half-year end (end-June and end-December). Amounts denominated in currencies other than the US dollar are converted to US dollars at the exchange rate prevailing on the reference date.

Source: BIS derivatives statistics.

100

75

50

25

018161412

Forwards and swaps Options

4

3

2

1

018161412

Other commodities Gold

0.8

0.6

0.4

0.2

0.018161412

Other precious metals

20

15

10

5

0

40

30

20

10

0181614

Rhs:Gross market value/notional (lhs)

Single-name notionalMulti-name notional

60

45

30

15

0

6.0

4.5

3.0

1.5

0.0181716151413

Rhs:CCPs/total (lhs)

Single-name notionalMulti-name notional

30

25

20

15

10

1.2

0.9

0.6

0.3

0.0181716151413

Rhs:Net/gross market values (lhs)

Gross market valuesNet market values

BIS Quarterly Review, June 2019 A17

Growth of central clearing

Notional amounts outstanding by counterparty, in per cent Graph D.9

Interest rate derivatives Credit default swaps

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 As a percentage of notional amounts outstanding against all counterparties. 2 Including central counterparties but excluding reporting dealers. 3 For interest rate derivatives, data for CCPs prior to end-June 2016 are estimated by indexing the amounts reported at end-June 2016 to the growth since 2008 of notional amounts outstanding cleared through LCH’s SwapClear service. 4 Proportion of trades that are cleared, estimated as (CCP / 2) / (1 – (CCP / 2)), where CCP represents the share of notional amounts outstanding that dealers report against CCPs. CCPs’ share is halved to adjust for the potential double-counting of inter-dealer trades novated to CCPs.

Sources: LCH.Clearnet Group Ltd; BIS OTC derivatives statistics (Table D7 and Table D10.1); BIS calculations.

80

60

40

20

018161412100806

Reporting dealers1

Other financial institutions1, 2

80

60

40

20

018161412100806

Central counterparties1, 3

Estimated minimum clearing rate4

Concentration in global OTC derivatives markets

Herfindahl index1 Graph D.8

Foreign exchange derivatives2 Interest rate swaps Equity-linked options

Further information on the BIS derivatives statistics is available at www.bis.org/statistics/derstats.htm. For definitions, see the online glossary. 1 The index ranges from 0 to 10,000, where a lower number indicates that there are many dealers with similar market shares (as measured by notional principal)and a higher number indicates that the market is dominated by a few reporting dealers. 2 Foreign exchange forwards, foreign exchange swaps and currency swaps.

Source: BIS derivatives statistics.

1,000

800

600

40018161412

USDEUR

GBPJPY

1,400

1,000

600

20018161412

CHFCAD

SEK

6,400

4,400

2,400

40018161412

United StatesJapanEurope

Latin AmericaOther Asia

A18 BIS Quarterly Review, June 2019

E Global liquidity indicators

US dollar credit outside the United States1

Annual change, in per cent Graph E.1

Further information on the BIS global liquidity indicators is available at www.bis.org/statistics/gli.htm. 1 Annual growth of US dollar-denominated credit to non-banks outside the United States. 2 Annual growth of the US dollar nominal effective exchange rate.

Sources: Datastream; Dealogic; Euroclear; Thomson Reuters; Xtrakter Ltd; national data; BIS locational banking statistics; BIS effective exchange rate statistics; BIS calculations.

20

10

0

–10

–20201820162014201220102008200620042002

Total credit Loans Debt securities NEER2

BIS Quarterly Review, June 2019 A19

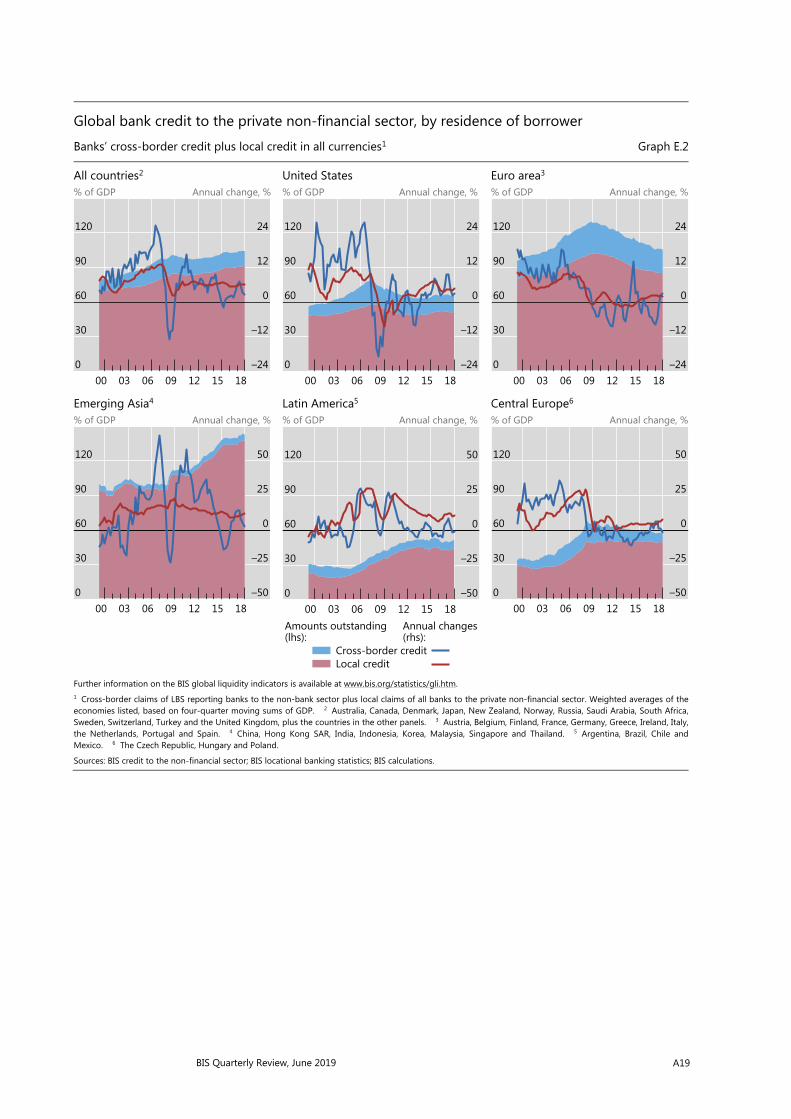

Global bank credit to the private non-financial sector, by residence of borrower

Banks’ cross-border credit plus local credit in all currencies1 Graph E.2

All countries2 United States Euro area3

% of GDP Annual change, % % of GDP Annual change, % % of GDP Annual change, %

Emerging Asia4 Latin America5 Central Europe6

% of GDP Annual change, % % of GDP Annual change, % % of GDP Annual change, %

Further information on the BIS global liquidity indicators is available at www.bis.org/statistics/gli.htm. 1 Cross-border claims of LBS reporting banks to the non-bank sector plus local claims of all banks to the private non-financial sector. Weighted averages of the economies listed, based on four-quarter moving sums of GDP. 2 Australia, Canada, Denmark, Japan, New Zealand, Norway, Russia, Saudi Arabia, South Africa,Sweden, Switzerland, Turkey and the United Kingdom, plus the countries in the other panels. 3 Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal and Spain. 4 China, Hong Kong SAR, India, Indonesia, Korea, Malaysia, Singapore and Thailand. 5 Argentina, Brazil, Chile and Mexico. 6 The Czech Republic, Hungary and Poland.

Sources: BIS credit to the non-financial sector; BIS locational banking statistics; BIS calculations.

120

90

60

30

0

24

12

0

–12

–2418151209060300

120

90

60

30

0

24

12

0

–12

–2418151209060300

120

90

60

30

0

24

12

0

–12

–2418151209060300

120

90

60

30

0

50

25

0

–25

–5018151209060300

120

90

60

30

0

50

25

0

–25

–5018151209060300

(rhs):Annual changes

(lhs):Amounts outstanding

Cross-border creditLocal credit

120

90

60

30

0

50

25

0

–25

–5018151209060300

A20 BIS Quarterly Review, June 2019

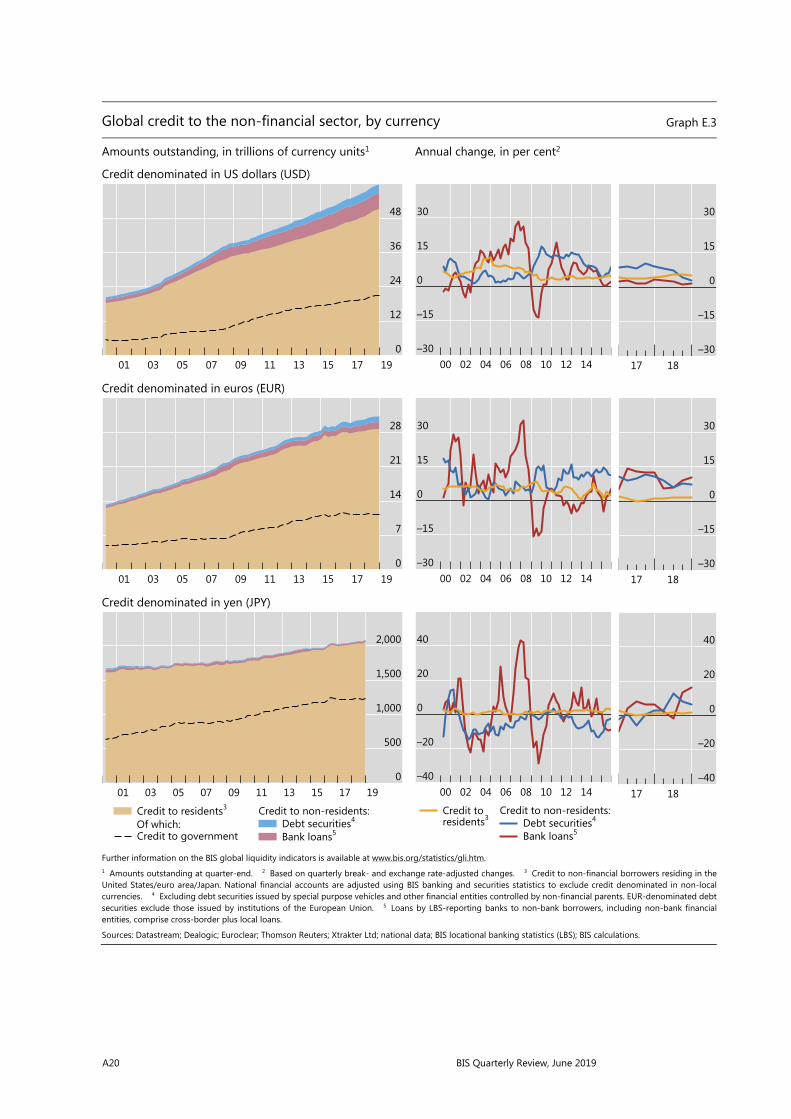

Global credit to the non-financial sector, by currency Graph E.3

Amounts outstanding, in trillions of currency units1 Annual change, in per cent2

Credit denominated in US dollars (USD)

Credit denominated in euros (EUR)

Credit denominated in yen (JPY)

Further information on the BIS global liquidity indicators is available at www.bis.org/statistics/gli.htm. 1 Amounts outstanding at quarter-end. 2 Based on quarterly break- and exchange rate-adjusted changes. 3 Credit to non-financial borrowers residing in the United States/euro area/Japan. National financial accounts are adjusted using BIS banking and securities statistics to exclude credit denominated in non-local currencies. 4 Excluding debt securities issued by special purpose vehicles and other financial entities controlled by non-financial parents. EUR-denominated debt securities exclude those issued by institutions of the European Union. 5 Loans by LBS-reporting banks to non-bank borrowers, including non-bank financial entities, comprise cross-border plus local loans.

Sources: Datastream; Dealogic; Euroclear; Thomson Reuters; Xtrakter Ltd; national data; BIS locational banking statistics (LBS); BIS calculations.

48

36

24

12

019171513110907050301

30

15

0

–15

–301412100806040200

30

15

0

–15

–301817

28

21

14

7

019171513110907050301

30

15

0

–15

–301412100806040200

30

15

0

–15

–301817

2,000

1,500

1,000

500

019171513110907050301

Of which:Credit to residents3

Debt securities4

Bank loans5

Credit to non-residents:

Credit to government

40

20

0

–20

–401412100806040200

Credit toresidents3 Debt securities4

Bank loans5

Credit to non-residents:

40

20

0

–20

–401817

BIS Quarterly Review, June 2019 A21

Foreign currency credit to non-banks in EMDEs Graph E.5

US dollar-denominated credit by region Foreign currency credit to selected EMDEs1

USD trn USD bn

Further information on the BIS global liquidity indicators is available at www.bis.org/statistics/gli.htm. 1 Amounts outstanding for the latest available data.

Sources: Datastream; Dealogic; Euroclear; Thomson Reuters; Xtrakter Ltd; national data; BIS locational banking statistics (LBS); BIS calculations.

3

2

1

0181614121008060402

Emerging EuropeLatin America and Caribbean

Africa and Middle EastEmerging Asia-Pacific

450

300

150

0MYZATWCLINSAKRARBRIDRUTRMXCN

USDDenominated in: EUR JPY

US dollar-denominated credit to non-banks outside the United States1 Graph E.4

World EMDEs Per cent USD tn Per cent USD tn

Further information on the BIS global liquidity indicators is available at www.bis.org/statistics/gli.htm. 1 Non-banks comprise non-bank financial entities, non-financial corporations, governments, households and international organisations. 2 Loans by LBS-reporting banks to non-bank borrowers, including non-bank financial entities, comprise cross-border plus local loans.

Sources: Datastream; Dealogic; Euroclear; Thomson Reuters; Xtrakter Ltd; national data; BIS locational banking statistics (LBS); BIS calculations.

58

54

50

46

9

6

3

018161412100806040200

Share of bank loansLhs:

65

60

55

50

3

2

1

018161412100806040200

Bonds issued by non-banksBank loans to non-banks2

Amounts outstanding (rhs):

A22 BIS Quarterly Review, June 2019

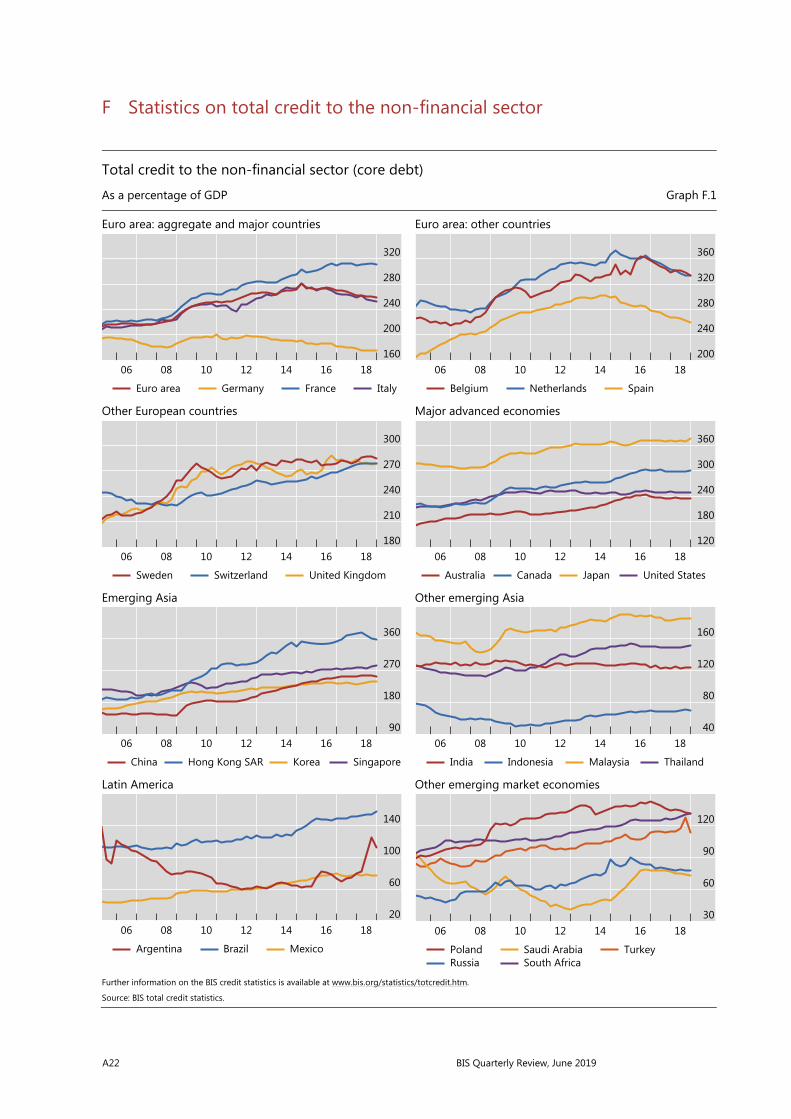

F Statistics on total credit to the non-financial sector

Total credit to the non-financial sector (core debt)

As a percentage of GDP Graph F.1

Euro area: aggregate and major countries Euro area: other countries

Other European countries Major advanced economies

Emerging Asia Other emerging Asia

Latin America Other emerging market economies

Further information on the BIS credit statistics is available at www.bis.org/statistics/totcredit.htm.

Source: BIS total credit statistics.

320

280

240

200

16018161412100806

Euro area Germany France Italy

360

320

280

240

20018161412100806

Belgium Netherlands Spain

300

270

240

210

18018161412100806

Sweden Switzerland United Kingdom

360

300

240

180

12018161412100806

Australia Canada Japan United States

360

270

180

9018161412100806

China Hong Kong SAR Korea Singapore

160

120

80

4018161412100806

India Indonesia Malaysia Thailand

140

100

60

2018161412100806

Argentina Brazil Mexico

120

90

60

3018161412100806

PolandRussia

Saudi ArabiaSouth Africa

Turkey

BIS Quarterly Review, June 2019 A23

Total credit to the private non-financial sector (core debt)

As a percentage of GDP Graph F.2

Euro area: aggregate and major countries Euro area: other countries

Other European countries Major advanced economies

Emerging Asia Other emerging Asia

Latin America Other emerging market economies

Further information on the BIS credit statistics is available at www.bis.org/statistics/totcredit.htm.

Source: BIS total credit statistics.

180

150

120

9018161412100806

Euro area Germany France Italy

275

225

175

12518161412100806

Belgium Netherlands Spain

225

200

175

15018161412100806

Sweden Switzerland United Kingdom

210

180

150

12018161412100806

Australia Canada Japan United States

280

210

140

7018161412100806

China Hong Kong SAR Korea Singapore

120

80

40

018161412100806

India Indonesia Malaysia Thailand

60

40

20

018161412100806

Argentina Brazil Mexico

80

60

40

2018161412100806

PolandRussia

Saudi ArabiaSouth Africa

Turkey

A24 BIS Quarterly Review, June 2019

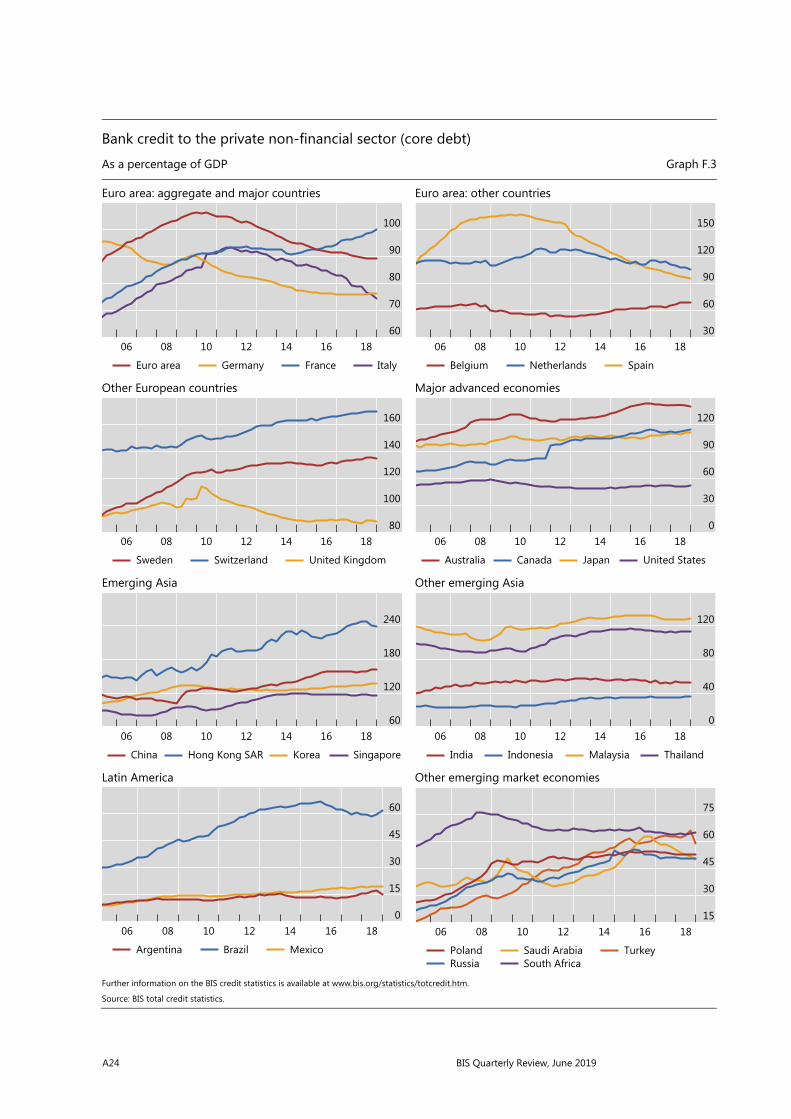

Bank credit to the private non-financial sector (core debt)

As a percentage of GDP Graph F.3

Euro area: aggregate and major countries Euro area: other countries

Other European countries Major advanced economies

Emerging Asia Other emerging Asia

Latin America Other emerging market economies

Further information on the BIS credit statistics is available at www.bis.org/statistics/totcredit.htm.

Source: BIS total credit statistics.

100

90

80

70

6018161412100806

Euro area Germany France Italy

150

120

90

60

3018161412100806

Belgium Netherlands Spain

160

140

120

100

8018161412100806

Sweden Switzerland United Kingdom

120

90

60

30

018161412100806

Australia Canada Japan United States

240

180

120

6018161412100806

China Hong Kong SAR Korea Singapore

120

80

40

018161412100806

India Indonesia Malaysia Thailand

60

45

30

15

018161412100806

Argentina Brazil Mexico

75

60

45

30

1518161412100806

PolandRussia

Saudi ArabiaSouth Africa

Turkey

BIS Quarterly Review, June 2019 A25

Total credit to households (core debt)

As a percentage of GDP Graph F.4

Euro area: aggregate and major countries Euro area: other countries

Other European countries Major advanced economies

Emerging Asia Other emerging Asia

Latin America Other emerging market economies

Further information on the BIS credit statistics is available at www.bis.org/statistics/totcredit.htm.

Source: BIS total credit statistics.

70

60

50

40

3018161412100806

Euro area Germany France Italy

120

100

80

60

4018161412100806

Belgium Netherlands Spain

120

100

80

60

4018161412100806

Sweden Switzerland United Kingdom

120

100

80

60

4018161412100806

Australia Canada Japan United States

80

60

40

20

018161412100806

China Hong Kong SAR Korea Singapore

80

60

40

20

018161412100806

India Indonesia Malaysia Thailand

28

21

14

7

018161412100806

Argentina Brazil Mexico

40

30

20

10

018161412100806

PolandRussia

Saudi ArabiaSouth Africa

Turkey

A26 BIS Quarterly Review, June 2019

Total credit to non-financial corporations (core debt)