35

blinkx plc H12015 Results London, UK 11 November 2014

| Date post: | 19-May-2018 |

| Category: |

Documents |

| Upload: | trankhuong |

| View: | 214 times |

| Download: | 1 times |

blinkx plc

H12015 Results

London, UK 11 November 2014

Safeharbor Statement

2

This announcement or presentation contains (or may contain) certain forward-looking statements with respect to certain of

blinkx's plans and its current goals and expectations relating to its future financial condition and performance and which involve

a number of risks and uncertainties. blinkx cautions readers that no forward-looking statement is a guarantee of future

performance and that actual results could differ materially from those contained in the forward-looking statements. These

forward-looking statements can be identified by the fact that they do not relate only to historical or current facts. Forward-

looking statements sometimes use words such as 'aim', 'anticipate', 'target', 'expect', 'estimate', 'intend', 'plan', 'goal', 'believe', or

other words of similar meaning. Examples of forward-looking statements include, among others, statements regarding blinkx's

future financial position, income growth, impairment charges, business strategy, projected levels of growth in its markets,

projected costs, estimates of capital expenditure, and plans and objectives for future operations of blinkx and other statements

that are not historical fact.

By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances,

including, but not limited to US and UK domestic and global economic and business conditions, the effects of blogs and media

coverage, the effects of continued volatility in credit markets, market-related risks such as changes in interest rates and

exchange rates, the policies and actions of governmental and regulatory authorities, changes in legislation, the further

development of standards and interpretations under International Financial Reporting Standards ("IFRS") applicable to past,

current and future periods, evolving practices with regard to the interpretation and application of standards under IFRS, the

outcome of pending and future litigation, the success of future acquisitions and other strategic transactions and the impact of

competition - a number of which factors are beyond blinkx's control. As a result, blinkx's actual future results may differ materially

from the plans, goals, and expectations set forth in blinkx's forward-looking statements.

Any forward-looking statements made herein by or on behalf of blinkx speak only as of the date they are made. Except as

required by the FCA, AIM or applicable law, blinkx expressly disclaims any obligation or undertaking to release publicly any

updates or revisions to any forward-looking statements contained in this announcement or presentation to reflect any changes in

blinkx expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is

based. Neither the content of the Company's website (or any other website) nor the content of any website accessible from

hyperlinks on the Company's website (or any other website) is incorporated into, or forms part of, this announcement.

Agenda

Overview

Financials

Sector Trends

Vision and Growth

Appendix

3

H1 2015 Highlights

Source: eMarketer, blinkx Estimates 1. Does not include acquisition and non-recurring expense, purchase intangibles Includes, or share base compensation 2. Adjustments include acquisitions and non-recurring expenses, share based compensation and other income

• Continued robust sector growth, with an accelerating shift to mobile

• Evolving standards continue to impact demand relationships and requirements

• Increasing consolidation, particularly within the supply side of the ecosystem

• Revenue of $106M, Adjusted EBITDA of ~$1M

• 20% contribution from mobile versus 1% in H12014

• Strong, debt free balance sheet with ~$115M in cash

• 299 staff, including Technology(93), Sales (86), Operations (51), Services (21), G&A (39), Marketing (9)

• Realignment and restructuring of resources to focus on fast growing segments of the sector

• Continued Integration of acquisitions to facilitate cross-product, cross-device offerings at scale

• Products: Focus on Audience, Content, Advertiser and Platform offerings

• Technology: Common data, targeting, reporting, advertising and content management platforms

• Marketing: Brand consolidation, leadership in industry consortia and events, integrated sales support

• Disruption of $100B video advertising market as linear and digital TV converge and standards evolve

• Accelerating shift from desktop to mobile and from direct to automated (programmatic) trading

• Race to scale through consolidation across both supply and demand portions of the ecosystem

4

Outlook

Financials

Operations

Initiatives

Sector

Commercial Model

5

Consumer Advertiser

Content

Ad Units

6

Ric

h M

ed

ia

Vid

eo

Pre

roll

Vid

eo

Se

arc

h

Co

mp

ariso

n S

ho

pp

ing

Co

nte

xtu

al

Mo

bile

Vid

eo

Mo

bile

Ba

nn

er

Mo

bile

Ric

h M

ed

ia

Na

tiv

e, So

cia

l

Key Financials

7

Notes: 1. H12015 numbers in line one, H12014 Numbers in line two

2. EBITDA adjustments include acquisitions and non-recurring expenses, share based compensation and other income 3. Current employee count includes staff reduction from a calendar year peak of 343

Revenue

$106.0m $111.6m

Adj. EBTIDA

$1.0m $18.2m

Adj. PBT

-$3.4.m $15.1m

Net Cash

$114.5m $69.4m

Employees

299 270

Mobile

20% 1%

H1 2015 KPIs

8

PREMIUM CONVENTIONAL TECH &

SERVICES OPPORTUNITY TOTAL

01010

11001

10110

Notes:

Premium: High Value Motion ads Direct sold Exchange traded Video, rich media, text, ads Conventional: High Volume, Static Ads, Agency representation Desktop, Mobile, Banner Ads Technology & Services: Relate to managing digital assets and advertising services that support current revenue streams Opportunity: Access to interactions blinkx.com, blinkx Syndicates and Affiliates and emerging channels, e.g. mobile, ConnectedTV

Revenue ($)

Revenue (%)

$74.9

71%

$26.4M

25%

$4.7M

4%

$106.0M

100%

eCPM ($) $8.73 $0.50

Interactions (B)

Volume (%)

9

3%

53

20%

199

77.0%

261

100%

KPI Trends

9 Note: Figures above are unaudited

0

50

100

150

200

250

300

350

H1 '12 H2 '12 H1 '13 H2 '13 H1 '14 H2 '14 H1 '15

Opportunity

Premium

Conventional

Volume Trends, (B)

$4.45 $4.78 $4.67 $4.80

$5.65

$7.92

$8.73

$0.67 $0.66 $0.82 $0.85 $0.83 $0.71 $0.50

H1 '12 H2 '12 H1 '13 H2 '13 H1 '14 H2 '14 H1 '15

Premium Conventional

Pricing Trends, ($/eCPM)

16 16 31

45 43 53 61

55

226

254

314 322 305

261

H1 '12 H2 '12 H1 '13 H2 '13 H1 '14 H2 '14 H1 '15

Monetisation

Interaction

Interaction & Monetisation Trends, (B) Interaction & Monetisation Trends, (B)

80% 80% 77% 79% 76% 76% 71%

11% 16% 18% 18% 21% 21% 25%

9% 4% 5% 3% 3% 3% 4%

H1 '12 H2 '12 H1 '13 H2 '13 H1 '14 H2 '14 H1 '15

Premium Conventional Tech & Services

Revenue Contribution, (%)

Sector Trends

10

‣ Offline Spend Continues to Move Online

‣ Growth of Video and Accelerating Shift to Mobile

‣ Rise of Automated (Programmatic) Trading

‣ Emerging and Evolving Standards

‣ Industry Consolidation

Ad Spend Continues to Migrate

11

37

43 40 40

34 33

2012 2013

Digital Broadcast Print

US Digital, Broadcast, Print ($B)

Source: eMarketer, Kleiner, Perkins, Caufield and Byers, IAB

32 32 30

27 25

11

19

28

40

49

2013 2014 2015 2016 2017

Desktop* Mobile**

US Digital Ad Spending, by Channel, 2012 - 2017 ($B)

20

23

26

28

31

10 11

12 13

15

4 6

8 10

11

3 4

5 7

9

2 2 2 2 3

2013 2014 2015 2016 2017

Search Banners and other*Video Rich mediaSponsorships

US Digital Ad Spending, 2013 - 2017 ($B)

5%

12%

38%

25%

20% 19%

10%

45%

22%

4%

Print Radio TV Internet Mobile

Time Spent Ad Spend

Media Consumption v. Ad Spend, 2014

$30B Opportunity

By The Numbers

29,000+ Websites 5,000+ Publishers 1,000+ Brands

74% Reach (US)1 73% Reach (UK)1 72% Reach (Canada)1

3,210 CPU Cores 1.7+ GB/Sec 200K+ Queries/Sec 15K+ Ads Served/Sec

Mobile Impressions2

Mobile Web — 2.1 B 1.2 Billion (Smartphone)

900 Million (Tablet)

In-App – 500 MM 350 Million (Smartphone)

150 Million (Tablet)

Display Impressions2

120 Billion

Video Impressions2

1 Billion

Programmatic Scale, Scope and Reach

12

1. comScore, September 2014

2. Access to Monthly Impressions, not all of which are monetized

Growth Vision

13

Connect audiences and brands through professional content

Cross Screen

14

Conclusions

15

VIDEO MOBILE PROGRAMMATIC DATA

0011010101010

0101110001010

0110101100101

0110100001001

1010010101001

0101110100100

• Sector continues to demonstrate robust growth and change

• Tech-media company with unique strengths and offerings in digital video

• Disciplined financials with profitable, revenue growth and cash management

• Unique, diverse assets in hyper growth segments of the sector

• Expanding universe of organic and inorganic growth opportunities

• Connecting digital audiences, brands through professional content at scale

Appendix

A. Sector Overview

B. Corporate Overview

C.Ecosystem, Business Model

D. Products and Services

16

A1. Mobile Shift and Video Growth

17

Avg. Time (Min/User/Day) Spent 2014 US

346 268 80 Radio

Source: eMarketer, IAB

300

600

900

1200

1500

1800

2100

2007 2008 2009 2010 2011 2012 2013 2014 2015

Mobile Internet Users Desktop Users

Mobile Internet Users vs Desktop Users, (B,WW)

4 6

8 10

11

2013 2014 2015 2016 2017

Online Video Spend ($B) Online Video Spend ($B)

11

19

28

40

2013 2014 2015 2016 2017

Online Video Spend ($B) Mobile Spend ($B)

49

A2. Growth of Programmatic Spend

18 Source: eMarketer , IDC, Magna Global

28% 34% 41% 47% 52%

25% 29%

32% 32%

31%

47% 36%

27% 21% 17%

2013 2014 2015 2016 2017

RTB Non-RTB Non-programmatic

US Display Ad Spending Share, by Type, % of Total

$110

$437

$1,051

$1,929

$2,996

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

$3,500.00

2013 2014 2015 2016 2017

RTB-based mobile sales

US Real-Time Bidding Based Mobile Sales ($B)

$6.0

$8.3

$12.1

$17.9

$23.2

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

2013 2014 2015 2016 2017

Programmatic display ad spending

Programmatic Display Ad Spending ($B)

$3.4

$4.9

$6.8

$9.0

$10.7

19% 22% 25% 28% 29%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

2013 2014 2015 2016 2017

RTB digital display ad spending

US Real-Time Bidding (RTB) Digital Display Ad Spending($B)

A3. Measurement and Consolidation

19

“Facebook To Improve Video Ads

Through LiveRail Acquisition” - Forbes

“European TV Giant RTL to Acquire

Majority Stake in Video Ad Firm

SpotXchange” – Hollywood Reporter

“Publicis to buy 20 percent of

digital advertising group Matomy”

- Reuters

“AOL Acquires Attribution

Company Convertro For $101M” – Ad Exchanger

“Viewability Standards Raise More

Questions Than They Answer” - MediaPost

“Video ad industry is in a state of

content chaos, says Yahoo CMO” – Marketing Week

“Digital Video Faces Viewability &

Measurement Hurdles” – Beet.tv

“Online Native Ads Are Held To

Higher Standards Than Those On

TV” – Tech Crunch

A4. Ecosystem Evolution

20

Definitions: NWK – Ad Network, DESK. – Trading Desk, EXCH - Exchange

CONTENT

TECHNOLOGY

CORE MKT. PLACE INFRA.

AUDIENCE

Own Represent Aggregate

ADVERTISER

Brands Agencies Platforms

NWK SSP DSP DESK SSP EXCH

Distribution

R&D

Platform

Common

Creation

TEXT VIDEO APPS

Monetization

B1. Corporate Snapshot

21

1. Adjusted for acquisitions and non-recurring expenses, share based compensation, other income

History Founded 2004

IPO 2007

Headquarters London, UK

San Francisco, CA

Locations 15 Offices

US, UK and Canada

Employees 299 Total : 299 staff, including Technology(93), Sales (86), Operations (51), Services

(21), G&A (39), Marketing (9), 15 Contractors

Technology Desktop and Mobile Video, Search, Discovery, Content Management,

Syndication, Application Distribution and Advertising Platform

Financials

(Mar 31, 2014)

$247.2M – Revenue (+36.1% YOY)

$39.6M – Adjusted EBITDA1 (+83.8% YOY)

$126.9M – Net Cash

Partnerships 70+ Agencies

1,400+ Content Partners

1,000+ Brands

5,000+ Publishers

B2. History

22

premium mobile video

Apr 2009 May 2011 Nov 2011 Aug 2013 Dec 2013 May 2014

Structure Asset Purchase 1 Stock Purchase Stock Purchase Asset Purchase 2 Stock Purchase Stock Purchase

Products

App development,

licensing,

distribution and

monetization

platform

Display and rich

media advertising

network for long-tail

independent web

publishers

Self-service, auction

based performance

ad network (AdOn),

digital agency

(Prime Visibility)

Video content

syndication,

distribution and

audience extension

platform

Ultra premium,

brand focused

mobile video

technology and ad

platform

Mobile self-service

Demand Side

Platform (DSP) for

targeted

campaigns across

mobile ad units

Rationale

Expand supply of

organic, owned

and operated

audiences and

apps

Expand supply of

audiences from long

tail publishers for

new video

audience

Expand scale,

scope and reach of

audiences, new

products and

services

Accelerate video

content syndication

monetization

audience extension

Extend desktop

offerings into mobile

content,

technology,

advertising at scale

Accelerate

programmatic and

mobile offerings

including DSP and

Data Management

Platform (DMP)

1. Purchase of certain net assets from the Zango Companies from a consortium of financial institutions in a foreclosure sale 2. Purchase of certain net assets from Grab Networks Holdings Inc.

B3. Text v. Video Search

23

Text search engines miss the VIDEO in Video Search

blinkx actually WATCHES the video

Tesla Motors, Headquarter, Silicon

Valley, Electric

October, 2013

Tags: Tesla, Electric, Silicon Valley

http://www.aol.com/video/translogic-3-tesla-motors-part-2/517141686/

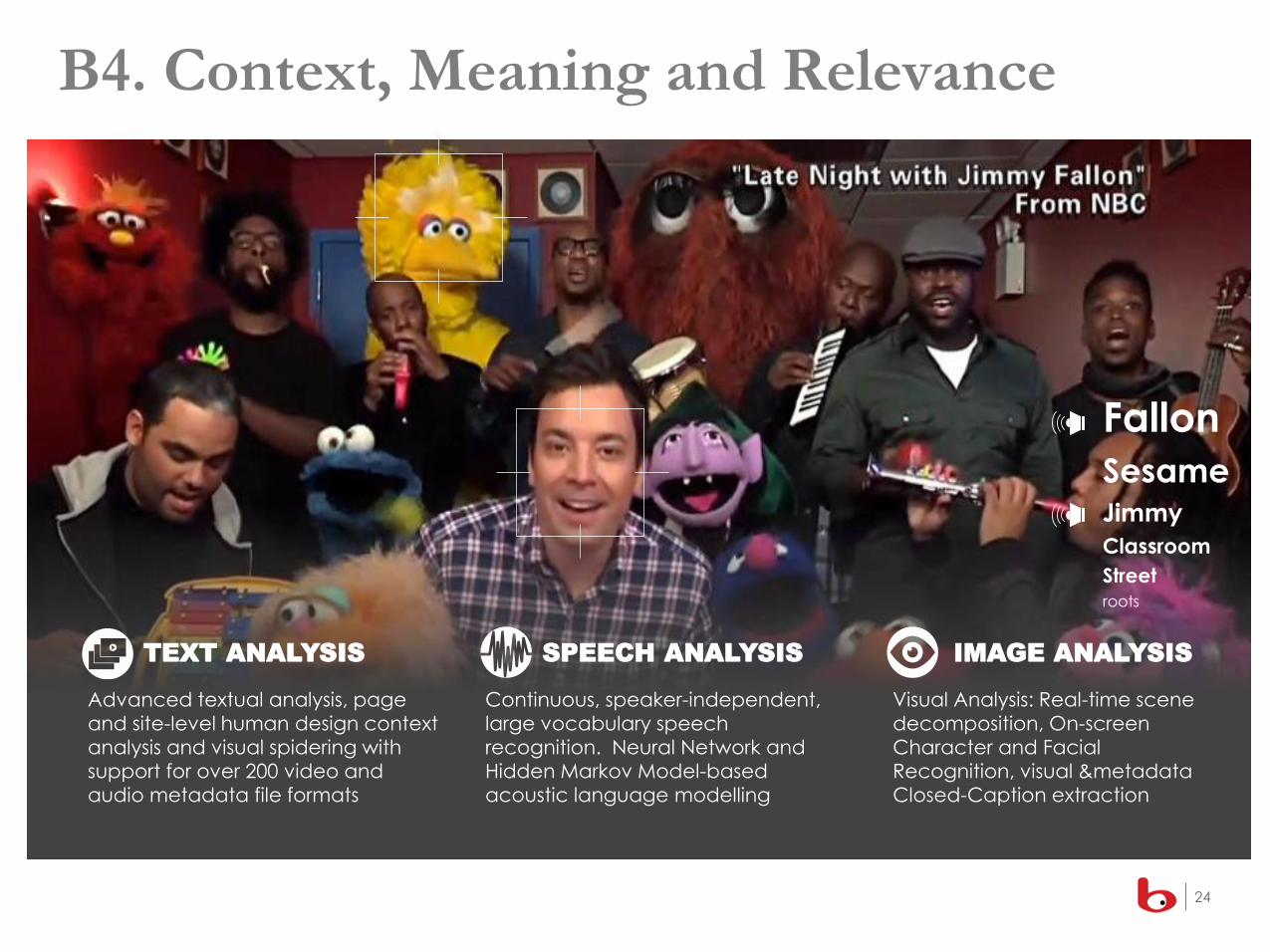

TEXT ANALYSIS

Advanced textual analysis, page

and site-level human design context

analysis and visual spidering with

support for over 200 video and

audio metadata file formats

Continuous, speaker-independent,

large vocabulary speech

recognition. Neural Network and

Hidden Markov Model-based

acoustic language modelling

Visual Analysis: Real-time scene

decomposition, On-screen

Character and Facial

Recognition, visual &metadata

Closed-Caption extraction

IMAGE ANALYSIS SPEECH ANALYSIS

Fallon

Sesame Jimmy

Classroom

Street

roots

B4. Context, Meaning and Relevance

24

B5. Competitive Map

PREMIUM CONTENT

1,400+ content partnerships ensure

ads always appear within brand-

safe, professional video content

PREMIUM ADVERTS

Serving 1,000+ brands, our patent-

pending advertising technology,

AdHoc, delivers unique targeting

for higher ROI on ad spend

AT SCALE

blinkx powers some of the largest

portals on the web. Acquisitions

increased the size of blinkx‘s overall

reach significantly to 5,000+

publishers

25

C1. Ecosystem

26

Consumer Advertiser

Website

Content

C2.Value Flow

27

Consumer Advertiser

Website

Content

$$$

$ Content

Att

en

tio

n

Co

nte

nt

Au

die

nc

e

C3. Fragmentation

28

Advertisers

Website

$$$

$ Content

Att

en

tio

n

Co

nte

nt

Au

die

nc

e

Consumers

Content Apps

C4. blinkx Engine

29

Web Publishers Agencies

AD

AD

AD

blinkx automatically matches digital audiences and brands through professionally generated content millions of times a day every day in real time.

Consumers Advertisers

Content Apps

Desktop

C5. Revenue Equation

30

Owned Controlled

Acquired

Agencies

Consumers Advertisers

Supply Demand

Mobile

Conn. TV

Dir. Sales

Exchanges

Platforms

Integrated Advertising Campaigns

Content Apps

C6. blinkx Ecosystem

31

Content

Aggregators Agencies/Platforms Audiences Advertisers

Search Discovery Syndication

Content Ads Audiences

Video Text Social Display Mobile

Applications

C7. Business Model

32

Audience

Content

Advertisers

Licensed Indexed

Platform

Traded

Search

blinkx

Syndicates

Display

Connected TV

Mobile

Monetisation

Conventional

Premium

I

Direct

Sold

II

Opportunity

D1. Integrated Advertising Model

33

Marketing Objective, Volume & Format

Conversion Metric, Price

Awareness

(Video, Display)

Interest

(Social)

Consideration

(Email)

Conversion

(Search)

Visits

$0.01/Visit

Audiences

$0.05/Profile

Signups

$0.25/Lead

Purchase

$1.00/Click

Ad Unit

Illustrative

Source: blinkx

D2. Adaptive-Screen

34

D3. Multi-Screen

35